intercontinental journal of finance resource research review a study on the financial frauds in...

TRANSCRIPT

www.icm

rr.or

g

82

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

A STUDY ON THE FINANCIAL FRAUDS IN INDIAN BANKING SECTOR

MEGHA SINGH

Institute of Management Studies & Research, Maharishi Dayanand University, Rohtak, Haryana

ABSTRACT

EvegenyMorozov once said, “There is no doubt that the Internet brim with the spamming, scamming and

indemnity fraud. Having someone wipe out your hard drive or bank account has never been easier, and

the tools for committing electronic mischief on your enemies are cheap and widely accessible”. Very

aptly quoted, the currentstudy looks into the potential losses suffered by the Indian banking sector due to

the frauds- technology related, KYC related and advances related frauds. It highlights some interesting

facts of expanding fraud exposed condition of thin-skinned banks. This study also helps in gaining some

useful insights and becoming aware of the various potential measures that can be undertaken to reduce the

incidence of frauds.

Keywords: banking frauds, Indian banks

INTRODUCTION

Susmita, 30-year old, took Rs.30 lakh housing loan from Bank A and bought a new house. Then, with an

intention of fraud, she went to a second bank, Bank B to avail a loan against the same house which was

earlier bought out of loan. Fortunate enough, she was sanctioned the loan, second time against an already

mortgaged property. But the intentions were not fulfilled and the thingswent further. The lady went to

Bank C for getting a loan of Rs. 50 lakh against the same property. Unluckily this time, Bank C cross

checked her with the CIBIL and disclosed that the house was already mortgaged twice.

This is not the only example of banking fraud happening around. It is not merely the ignorance on part of

bank or bank staff bit also the intention of involvement in some sort of ‘cheating’. In one of his very

recent article (Patil, 2013)stated that fraud amounts due to fake usage of fake documents has risen four

times since 2010,Rs. 1202 crore to Rs. 5359 crore in 2012. Further, public sector banks have suffered a

loss of Rs. 8734 crores in the last 3 years for the reason of loan disbursements on fake document

submission by the fraudulent borrowers. For the involvement in fraud, around 6362 bank employees have

been questioned, the article stated. Is this the bank staff which has been responsible for the frauds? More

or less their involvement has always been there.

James Medisson, The Federalist Papers, in 1788, said “If men were angles, no government would be

necessary. If angels were to govern men, neither external nor internal controls on government would be

necessary”.

The existence of frauds, more particularly financial frauds has been a matter of concern for a long time. It

is usually the case that there are not new frauds, just new avenues for deception.ATM frauds, online

banking frauds, Misappropriation and criminal breach of trust, fraudulent encashment through forged

instruments like cheques, DDs, negligence and cash shortages, over valuation of property to grant higher

loans, overdrafts against forged FDRs etc are some of the incidences which are on a high rise list of

banking frauds.

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

83

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

The story comes in place, when we come across a surprising but interesting fact that “Arthashastra”, an

ancient Indian treatise authored by Kautilya and Vishnugupta, names traditionally identified with

Chanakya, written in 300 BC visualized a detailed picture of a modern word ‘fraud’. Some of the lines

describing ways of embezzlement are: “what is realised earlier is entered later on; what is realised later is

entered earlier; what ought to be realised is not realised; what is hard to realise is shown as realised; what

is collected is shown as not collected; what has not been collected is shown as collected; what is collected

in part is entered as collected in full; what is collected in full is entered as collected in part; what is

collected is of one sort, while what is entered is of another sort.”As it can be clearly interpreted that the

modus operandi of the frauds in today’s times is more or less same what “Arthashastra” has cited. This

apparently proves that what has been hitting the headlines of recent times has its roots from far ancient

times. Adding to it, even lesser seems to have changed over the centuries.

In an analysis by Ernst & Young, India Fraud Indicator 2012, it was found out that businesses are

constantly exposed to fraud risk. As recorded in the report, the losses suffered due to the fraud amounted

to Rs. 66 billion. The largest number of such fraud cases and the highest aggregate losses were witnessed

by Delhi in the year 2011-2012. The report cited that “The financial services sector, including banking,

insurance and Non-banking Financial Companies (NBFCs), was the most vulnerable to fraud and

accounted for 63% of the total number of fraudulent incidents that occurred during the year. Within the

financial sector, banks were the most common victims of fraud, followed by insurance and mutual fund

companies.”

Another report by Association of Certified Fraud Examiners’ (ACFE) 2012 titled “Report to the Nation

on Occupational Fraud and Abuse” stated that the amount involved in frauds has increased fourfold from

Rs. 2038 crores in 2009-10 to Rs.8646 crore in 2012-13. These losses obviously are due to the disastrous

scams India has witnessed in the recent years like Magnum Group fraud etc.

In its report , Ernst & Young, India Fraud Indicator 2012, it has been found out that the financial services

sector is the worst hit by frauds involving 63 % of total fraud cases reported in 2011-2012. Among the

financial services sector, banking segment id the most targeted area victimized with 83 % of the total

number of the reported fraud cases.

Studying all the statistics and data from various studies, it can be easily interpreted that the frauds in India

have grown unchecked, despite of millions infused to check this lurking evil. The ever increasing use of

technology in every sphere of business, emergence of hybrid customer based financial products,

increasing use of e-commerce applications(Nsouli&Schaechter, 2002), preference of real time

transactions, it is all inadvertently leading to more complicated and refined forms of frauds (Singh,2013).

Banking fraud hurts both banks and their customers. Banks incur substantial operating costs by refunding

customers’ monetary losses (Gates and Jacob, 2009). This, in turn, may negatively affect customer loyalty

and stimulate switching behavior (Rauyruen and Miller, 2007), thereby hurting the banks’ reputation and

impeding the attraction of new customers (Buchanan, 2010).

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

84

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

This study has been undertaken with two objectives

(i) To study the current picture of banking frauds in India

(ii) To suggest measures to check these frauds in India

LITERATURE REVIEW

According to section 25 of Indian Penal Code, “a person is said to have done a thing fraudulently if he did

that thing with intent to defraud but not otherwise.” Hence fraud can be interpreted as “an act of criminal

deception carried out singly or in collusion with others with a view to deriving gains to which one is not

legally entitled.

Reserve Bank of India has defined fraud as “All instances wherein Banks have been put to loss through

misrepresentation of books of accounts, fraudulent encashment of instruments like cheques, drafts and

bills of exchange, unauthorized handling of securities charged to banks, misfeasance, embezzlement,

theft, misappropriation of funds, conversion of property, cheating, shortages, irregularities etc.”

Frauds in retail banking entails any attempt of criminals to “achieve financial gain at the expense of

legitimate customers or financial institutions through any [..]transaction channel, such as credit cards,

debit cards, ATMs, online banking, or checks” (Sudjianto et al., 2010, p. 5).

Banking frauds can be classified in three broad categories (Chakraborty, 2013):

(i) Technology Related Frauds

Since banks have been trying to focus on providing alternative channels to the customers, other the

physical branches, as a part of ‘branchless banking’, it has left some holes providing space to fraudsters

(Bhutto &Janjua, 2011). All the fraudulent activities which are performed at/through internet banking

channel; at ATMs by stealing pins or using fake pads; cloning fake debit or credit cards; using mobile

banking services – these all form a part of technology related frauds. To cut their costs and time,

customers are adopting web as a new means of faster transactions (Berney, 2008; Dubey, 2013) This acts

as a welcoming chance to fraudsters since customers are not present physically to authenticate their

transaction (Malphurus, 2009; Gates & Jacob, 2009). Customers are victimized by criminals who steal

their identities, make usage of stolen or lost cards or gain an unauthorized access of the customers’

accounts through wrong means (Gates & Jacob, 2009; Greene, 2009). New, even more complex and

sophisticated means are employed to steal data online (Singh, 2013). A common practice used these days

is “phishing”. Under phishing, private data of the customers like user ID or password is asked through an

e-mail. This practice has become a serious threat to online security (Bergholz et al., 2010). The payment

through online banking or cards is gaining importance globally (Worthington, 2009). In India, private

sector banks has a bigger share in technology related frauds by private including online banking, ATM ,

cards and other digitized transactions ( Soni&Soni, 2013). The volume of fraudulent transactions

committed by a third party has risen (Banks, 2005).

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

85

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

(ii) KYC Related Threats

Banks which are lenient in observation (Sharma & Brahma, 2000) and fulfilling the KYC requirements

are preyed with such threats. They either do not submit proper documentation or submit stolen

documentation. A lax corporate culture with inadequate internal controls, lack of requisite risk controls

andnegligent staff filled with overconfidence shapes a perfect “Fraud- friendly environment” (Harris &

William, 2004). Improper documented accounts are basically deposit accounts to fool the customers by

sending e-mail or SMS of winning prize or lottery. In return asks to deposit some processing charges. As

soon as the money is deposited, it is withdrawn through ATMs. Using stolen identities is another

grooming practice. It is basically called identity theft. It may comprise fraudsters illicitly gainingaccess to

customer accounts (Hartmann-Wendels et al., 2009), but usually refers toopening new accounts in the

customer’s name (Malphrus, 2009). Such frauds not only have a high impact on the profitability, but also

it creates a negative impact on bank-customer relationship (Hoffman &Birnbrich, 2012), due to lost trust

& confidence (Krummeck, 2000). The customer brings the fraud in notice of bank staff, blocks and

reopens or reissues a new account or card and finally, takes the big charge of dispute to recover its

financial losses (Douglous, 2009). All these hassles lead to increased dissatisfaction because of perceived

service failure (Varela-Neira et al., 2010).

(iii) Advances Related Frauds

Frauds related to the grant of credit facilities account for the largest share in total value of frauds in Indian

banking sector. In the words of Mr J.P. Dua, Chairman and Managing Director, Allahabad Bank, “The

maximum number of frauds is pertaining to fake title deeds. It is a major area of concern for all banks”. In

his article (Patil, 2013) has reported that public sector banks, because of submission of fake documents,

have suffered a loss of Rs. 8734 crores in the last 3 years.

When the customer himself plays the game of cheating or forgery, then the damages are even bigger. In

the cases, where the amount involved is greater than 50 lakhs, the fraudster or embezzler is “opportunist’s

type”. These embezzlers take advantage of the weaknesses of the internal controls and use its deficiency

for their own benefit (Smith, 1995). An ineffective internal control (Khanna&Arora, 2009), stressed

employees and readily available computer technology adds to the opportunities of fraud (Haugen and

Selin, 1999). Hence its prevention has become a major area of concern for the banks as well as public

policy makers (Sullivan, 2010).

SOME STATISTICS

Reserve Bank of India (RBI) has majorly acted as an advisory when it comes to his role in in preventing

frauds. Although the primary responsibility lies with the bank itself, RBI regularly issue guidelines about

major fraud prone areas and also ways to protect themselves against the frauds. In order to facilitate the

process, banks report all the frauds and the action taken thereon to the RBI. Nomination of a senior

official for submission of all the related returns has been asked by the RBI. Various circulars directing

banks to submit different types of frauds on basis of amount have been issued and revised from time to

time. The system of this reporting stated back in 1970 and the scope was extended over to urban

cooperative banks and deposits taking NBFCs registered with RBI in 2005-06. The purview of reporting

was further enhanced in March 2012 to take in NBFC-ND-SIs with an asset base of Rs. 100 crore and

above.

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

86

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

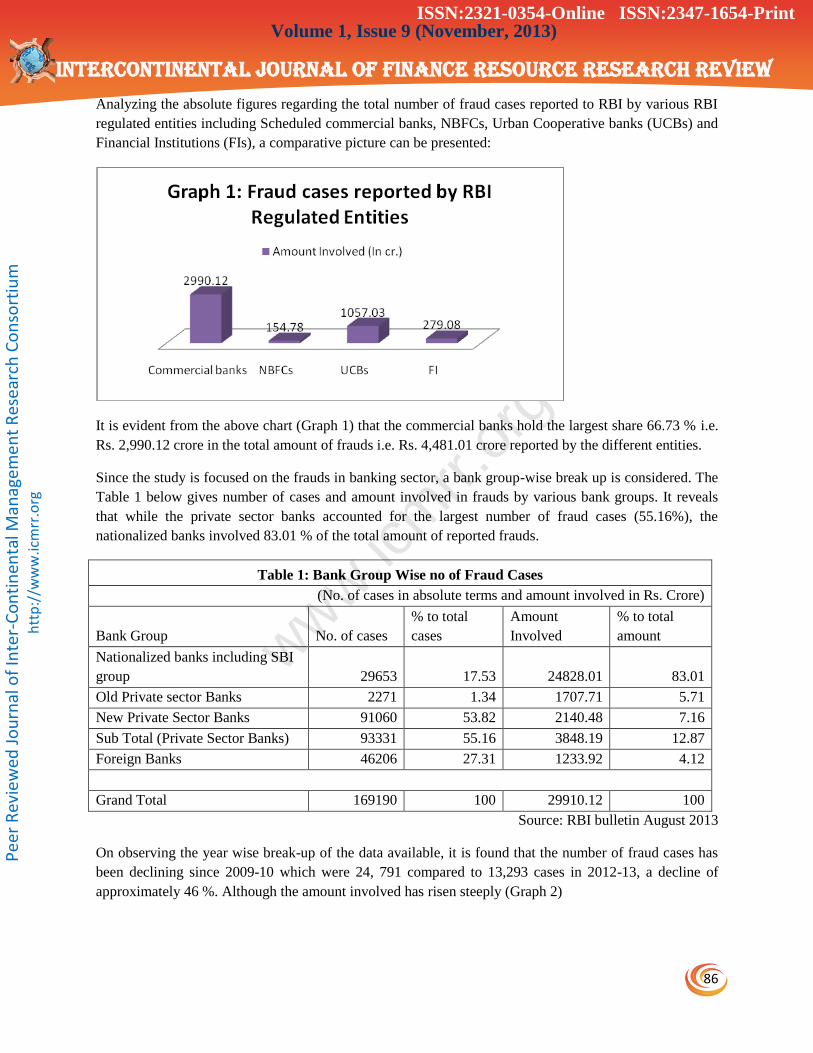

Analyzing the absolute figures regarding the total number of fraud cases reported to RBI by various RBI

regulated entities including Scheduled commercial banks, NBFCs, Urban Cooperative banks (UCBs) and

Financial Institutions (FIs), a comparative picture can be presented:

It is evident from the above chart (Graph 1) that the commercial banks hold the largest share 66.73 % i.e.

Rs. 2,990.12 crore in the total amount of frauds i.e. Rs. 4,481.01 crore reported by the different entities.

Since the study is focused on the frauds in banking sector, a bank group-wise break up is considered. The

Table 1 below gives number of cases and amount involved in frauds by various bank groups. It reveals

that while the private sector banks accounted for the largest number of fraud cases (55.16%), the

nationalized banks involved 83.01 % of the total amount of reported frauds.

Table 1: Bank Group Wise no of Fraud Cases

(No. of cases in absolute terms and amount involved in Rs. Crore)

Bank Group No. of cases

% to total

cases

Amount

Involved

% to total

amount

Nationalized banks including SBI

group 29653 17.53 24828.01 83.01

Old Private sector Banks 2271 1.34 1707.71 5.71

New Private Sector Banks 91060 53.82 2140.48 7.16

Sub Total (Private Sector Banks) 93331 55.16 3848.19 12.87

Foreign Banks 46206 27.31 1233.92 4.12

Grand Total 169190 100 29910.12 100

Source: RBI bulletin August 2013

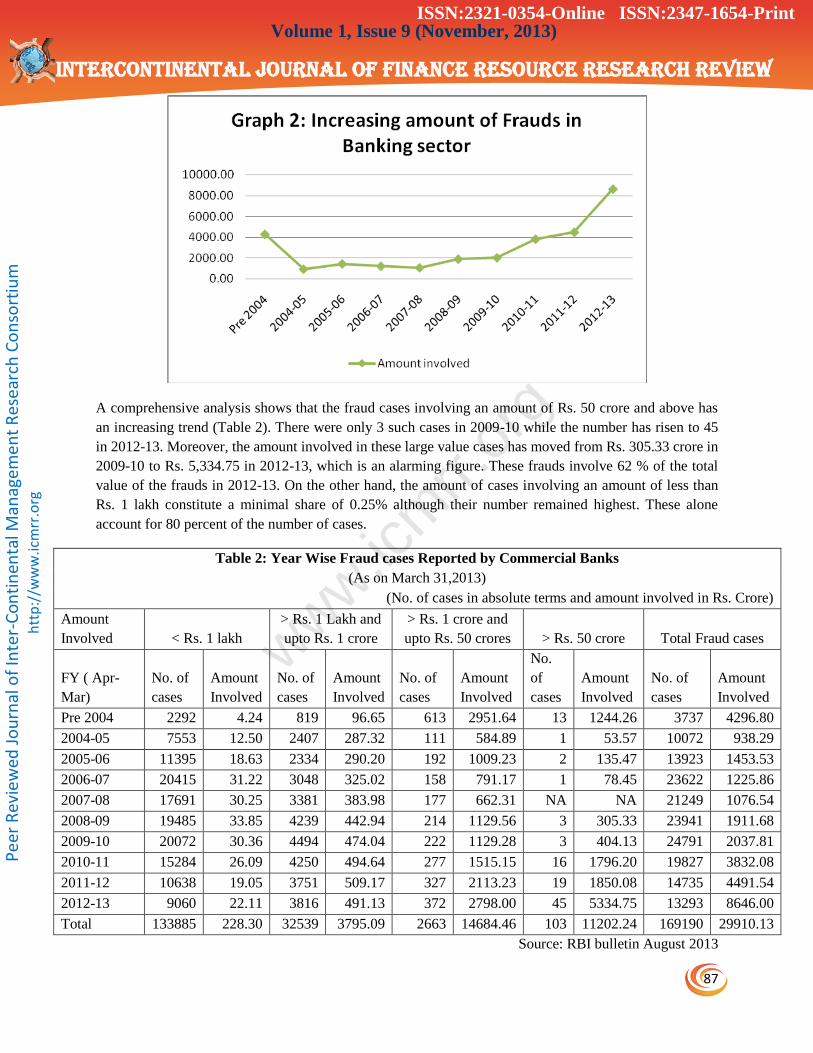

On observing the year wise break-up of the data available, it is found that the number of fraud cases has

been declining since 2009-10 which were 24, 791 compared to 13,293 cases in 2012-13, a decline of

approximately 46 %. Although the amount involved has risen steeply (Graph 2)

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

87

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

A comprehensive analysis shows that the fraud cases involving an amount of Rs. 50 crore and above has

an increasing trend (Table 2). There were only 3 such cases in 2009-10 while the number has risen to 45

in 2012-13. Moreover, the amount involved in these large value cases has moved from Rs. 305.33 crore in

2009-10 to Rs. 5,334.75 in 2012-13, which is an alarming figure. These frauds involve 62 % of the total

value of the frauds in 2012-13. On the other hand, the amount of cases involving an amount of less than

Rs. 1 lakh constitute a minimal share of 0.25% although their number remained highest. These alone

account for 80 percent of the number of cases.

Table 2: Year Wise Fraud cases Reported by Commercial Banks

(As on March 31,2013)

(No. of cases in absolute terms and amount involved in Rs. Crore)

Amount

Involved < Rs. 1 lakh

> Rs. 1 Lakh and

upto Rs. 1 crore

> Rs. 1 crore and

upto Rs. 50 crores > Rs. 50 crore Total Fraud cases

FY ( Apr-

Mar)

No. of

cases

Amount

Involved

No. of

cases

Amount

Involved

No. of

cases

Amount

Involved

No.

of

cases

Amount

Involved

No. of

cases

Amount

Involved

Pre 2004 2292 4.24 819 96.65 613 2951.64 13 1244.26 3737 4296.80

2004-05 7553 12.50 2407 287.32 111 584.89 1 53.57 10072 938.29

2005-06 11395 18.63 2334 290.20 192 1009.23 2 135.47 13923 1453.53

2006-07 20415 31.22 3048 325.02 158 791.17 1 78.45 23622 1225.86

2007-08 17691 30.25 3381 383.98 177 662.31 NA NA 21249 1076.54

2008-09 19485 33.85 4239 442.94 214 1129.56 3 305.33 23941 1911.68

2009-10 20072 30.36 4494 474.04 222 1129.28 3 404.13 24791 2037.81

2010-11 15284 26.09 4250 494.64 277 1515.15 16 1796.20 19827 3832.08

2011-12 10638 19.05 3751 509.17 327 2113.23 19 1850.08 14735 4491.54

2012-13 9060 22.11 3816 491.13 372 2798.00 45 5334.75 13293 8646.00

Total 133885 228.30 32539 3795.09 2663 14684.46 103 11202.24 169190 29910.13

Source: RBI bulletin August 2013

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

88

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

The figures depict the development of frauds in our economy, but the standalone figures cannot give a

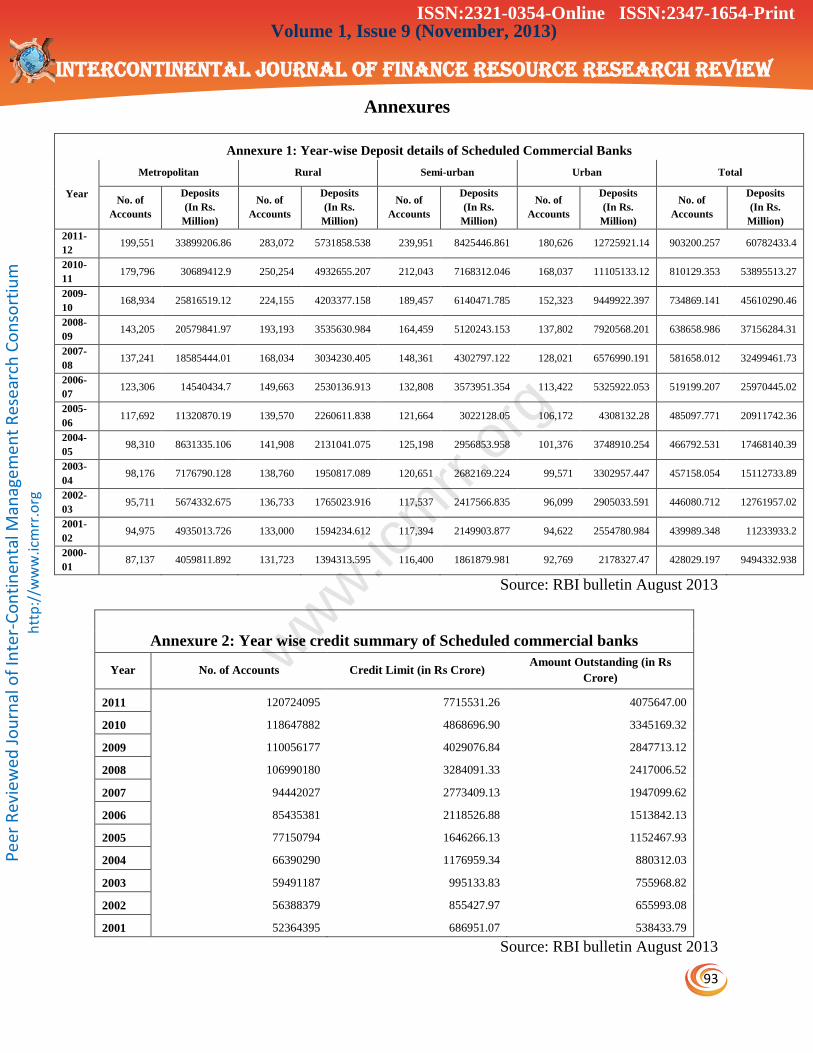

represent picture. To put things in perspective, the increasing amount of deposits in scheduled commercial

banks is quoted. The number of deposit accounts has doubled in last ten year, specifically in rural and

semi-urban areas, from 133,000 (2001-02) to 283,072 (2011-12) in rural area and 117,394 to 239,951 in

semi urban area (Annex 1).The total figures of these accounts shows that there number has gone up from

43.99 crore to 90.32 crores. Also, a similar trend in the credit facilities can be seen. The amount of credit

limit granted has expanded from Rs. 686,951 crore in 2001 to Rs. 11,76,959 crore in 2004 to Rs.

32,84,091 crore in 2008 to Rs. 77,15,531 crore by the end of year 2011 (Annex 2). Likewise, the number

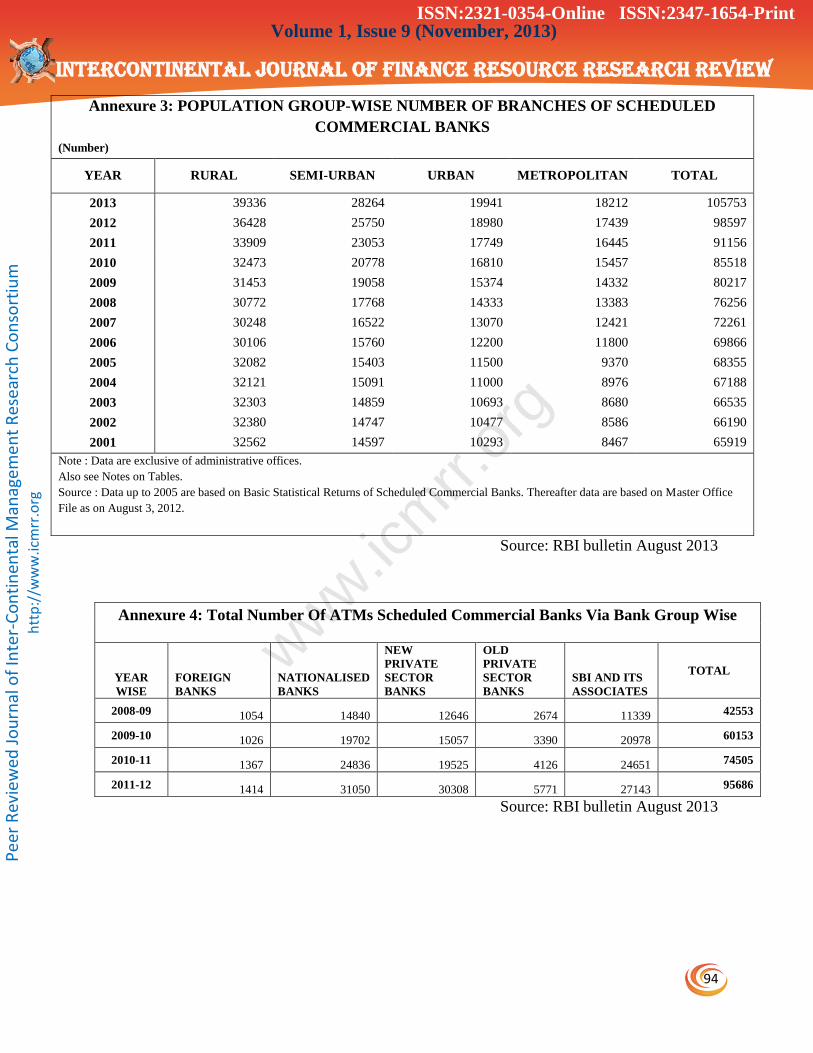

of brick and mortar branches(Annex 3), online transactions, mobile banking transactions, number of

ATMs (Annex 4), number of point-of sale transactions expanded two-fold in some and even more in

others. A granular analysis explains that, on an average, approximately 10 crore transactions are

happening on daily basis and 0.4 frauds per million, which is comparatively not very high. Although, the

increasing number and amount involved in frauds in comparison to the rising magnitude of banking

transactions is not alarming, yet they cannot be neglected.

Every person using e-mail, must have received one mail congratulating the user on winning lakhs and

crores via online lottery, which even the user cannot recall. But, in most of such cases, the winner is prey

of cyber-crime. With the expanding use of mobile phones and internet technology, the number victims

keep rising. According to National Crime Records Bureau, 2,876 cyber cases were registered under IT

Act in 2012 as against 1,791 cases (2011) posting a 60.6% year –on-year increase. IT solutions company

Unisys says mobile frauds are an area of concern for companies as well as 20-30% of financial

transactions are done via mobile devices and this is expected and this is expected to grow to 50% by

2015. A latest victim who fell prey to the fraudsters is Harsh Goenka whose promoted RPG group’s

current account was hacked and Rs. 2.34 crore were siphoned off using RTGS. Banks, unfortunately, has

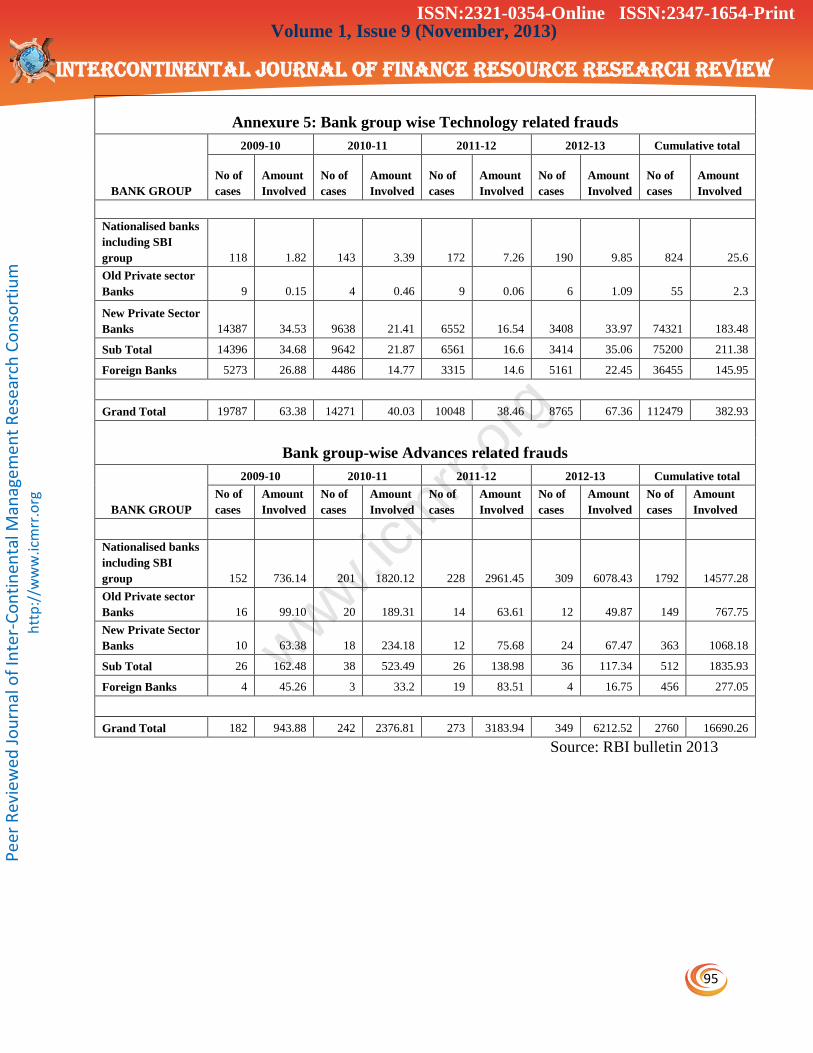

not played a proactive role in curbing this menace. As compared to 2011-12, the distressing figures come

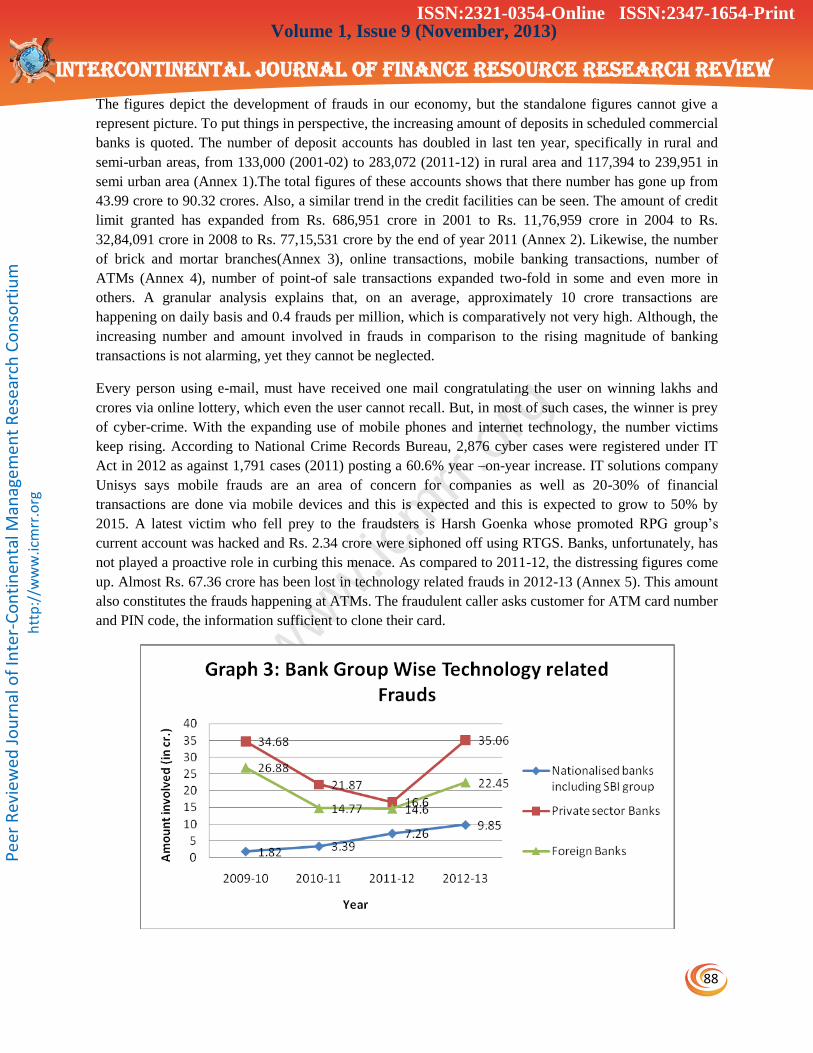

up. Almost Rs. 67.36 crore has been lost in technology related frauds in 2012-13 (Annex 5). This amount

also constitutes the frauds happening at ATMs. The fraudulent caller asks customer for ATM card number

and PIN code, the information sufficient to clone their card.

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

89

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

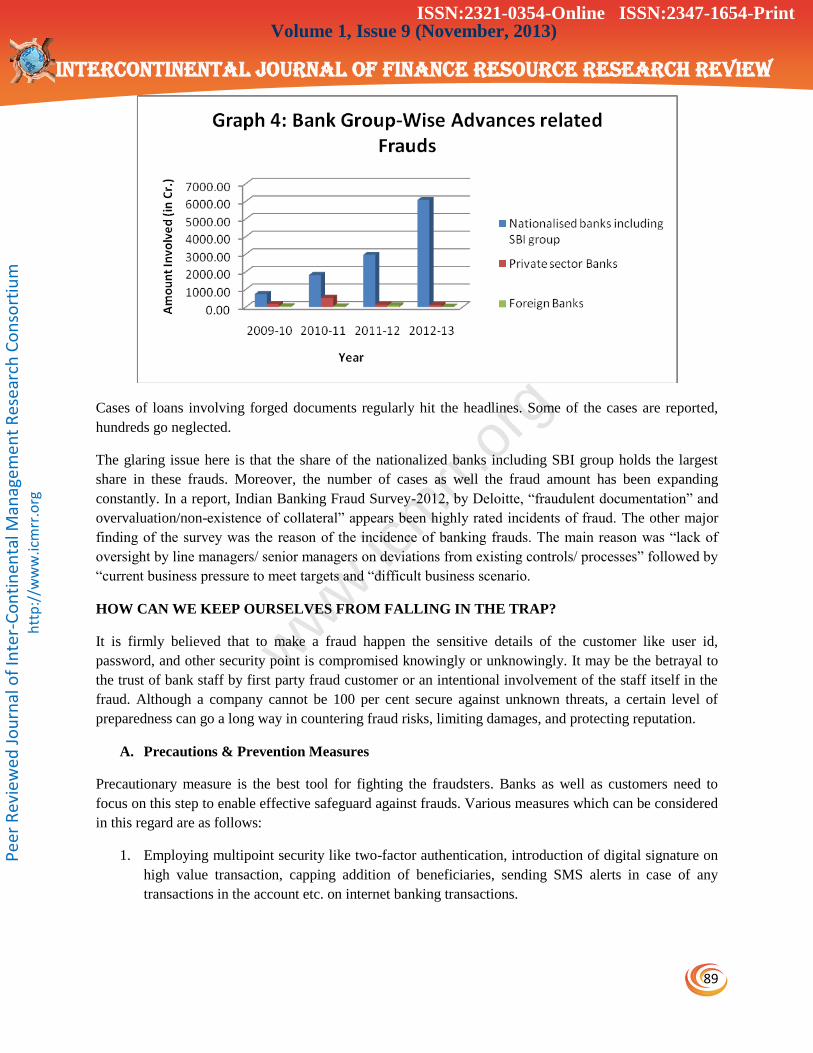

Cases of loans involving forged documents regularly hit the headlines. Some of the cases are reported,

hundreds go neglected.

The glaring issue here is that the share of the nationalized banks including SBI group holds the largest

share in these frauds. Moreover, the number of cases as well the fraud amount has been expanding

constantly. In a report, Indian Banking Fraud Survey-2012, by Deloitte, “fraudulent documentation” and

overvaluation/non-existence of collateral” appears been highly rated incidents of fraud. The other major

finding of the survey was the reason of the incidence of banking frauds. The main reason was “lack of

oversight by line managers/ senior managers on deviations from existing controls/ processes” followed by

“current business pressure to meet targets and “difficult business scenario.

HOW CAN WE KEEP OURSELVES FROM FALLING IN THE TRAP?

It is firmly believed that to make a fraud happen the sensitive details of the customer like user id,

password, and other security point is compromised knowingly or unknowingly. It may be the betrayal to

the trust of bank staff by first party fraud customer or an intentional involvement of the staff itself in the

fraud. Although a company cannot be 100 per cent secure against unknown threats, a certain level of

preparedness can go a long way in countering fraud risks, limiting damages, and protecting reputation.

A. Precautions & Prevention Measures

Precautionary measure is the best tool for fighting the fraudsters. Banks as well as customers need to

focus on this step to enable effective safeguard against frauds. Various measures which can be considered

in this regard are as follows:

1. Employing multipoint security like two-factor authentication, introduction of digital signature on

high value transaction, capping addition of beneficiaries, sending SMS alerts in case of any

transactions in the account etc. on internet banking transactions.

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

90

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

2. Adopting upgraded technology solutions like converting all strip based cards to chip based cards,

velocity checks on number of transactions effected per day/per beneficiary, capturing internet

protocol check as an additional validation check for any transaction, etc.

3. Moreover, the unrestricted use of social media websites at the office exposes a company to higher

fraud risk. A little IT expert , with even little time and effort, can easily gather sufficient

information about a company, its employees, vendors, suppliers, buyers and other related parties.

This captured information can be used in a negative manner. Hence, companies should try to keep

a check of the usage of these websites on official systems

4. Banks should constantly educate the general public about the types of embezzlement happening

around them. It needs to constantly seek awareness through print media, electronic media and

emails, cautioning customers not to fall prey to the false promising statements.

5. Adhering to the reporting guidelines issued by the RBI. To put a check, RBI has asked all the

banks to report cases involving an amount of Rs. 1 lakh and above to the police. The public sector

lenders to report any case of Rs. 1 crore and above to the Central bureau of Investigation. A

considerable delay has been noticed in declaring the fraud cases. It has to kept in mind that longer

the delay, larger the time in given to fraudsters to defraud its mischief and time to erase the trail

of its wrong doing.

6. Other than engaging closely with their technology vendors, banks need to build rapport with other

banks, NBFCs, security and investigative agencies and regulators so as to keep themselves

updated and ensure prompt response, whenever required.

7. Bank need to employ well scrutinized employee. A background check is must to ascertain if the

prospective employee has any criminal record or dubious background. Apart from keeping an eye

on the new hiring, a job rotation of existing ones is required. Keeping too long at one place gives

him/her confidence and experience to perpetuate the fraud unnoticed.

B. Detection& Investigation Measures

1. Internal checks i.e. operational controls like different enterer and verifier etc. can be built in the

routine banking system help in detection of fraud at a much earlier stage. Any minor alteration or

forgery may be neglected by one hand, but may not pass by two. Atleast, the clerical errors can be

easily avoided. Or, may be a transaction, different from its routine conduct can be checked.

2. Surprise audits can be done, to avoid the embezzlement by the internal employee. Checking of

cashiers, reconciliation and balancing of accounts at different branches, stock-taking of security

stationery, checking of different registers etc. are the various measures aimed at fraud detection.

3. A proper internal control audit may be devised on a half yearly or annually basis which goes

through each and every detail of the activities of the branch.

C. Solution

This is the last thing one can think of. After ‘all the evil’ had happened, everyone has to react very wisely.

1. On the part of the bank, it should be ready to face the wrath of the victim generously and try to

calm him down with all its support. Obviously, what, why, when, how- such questions be solved

as soon as possible. Most importantly, it needs to keep the customer updated with its progress on

an active basis. Along with this, banks need to update police, if required and other regulators

immediately so that the fraudster may not get out unnoticed.

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

91

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

2. As a customer, it is his duty to bring all aspects of the case in notice of the concerned authorities

immediately. He needs to behave wisely and look forward toward a prudent solution to the fraud,

specifically the monetary losses.

A good corporate governance system serves as base for mitigating the fraudulent activities. RBI has

clearly indicated that fraud risk management, fraud monitoring and fraud investigation function must

be owned by the bank’s CEO, Audit Committee of the Board and, in respect of large value frauds, the

Special Committee of the Board. The role of the other top level management cannot be overlooked.

There has to be a constant exchange of information among various parties on a lower and higher

level. In the current economic climate, banks needs to seek ways to gain maximum positive advantage

of new technology. They need to scrutinize all the prospective vulnerable areas, put in red marks and

plug loopholes quickly and effectively.

REFERENCES

1. Berney, L. (2008). For online merchants, fraud prevention can be a balancing act”. Cards &

Payments, 21(2), 22-29.

2. Bergholz, A., Beer, J. de, Glahn, S., Moens, M.-F., Paab G. and Strobel, S. (2010). New

filtering approaches for phishing email. Journal of Computer Security, 18, 35-42.

3. Buchanan, R. (2010). Banks on Guard. Latin Trade, 18(5), 58-60.

4. Douglass, D.B. (2009). An examination of the fraud liability shift in consumer card-based

payment systems. Economic Perspectives, 33(1), 43-52.

5. Dubey, N. (2013). India: banking Frauds- Prevent or Lament. Retrieved from

http://www.mondaq.com/india/x/250030/Financial+Services/Banking+Frauds+Prevent+Or+

Lament on 13/11/2013.

6. Gates, T. and Jacob, K. (2009). Payments fraud: perception versus reality – a conference

Summary. Economic Perspectives, 33(1), 7-15.

7. Greene, M.N. (2009). Divided we fall: fighting payments fraud together. Economic

Perspectives, 33(1), 37-42.

8. Hartmann-Wendels, T., Ma¨hlmann, T. and Versen, T. (2009). Determinants of banks’ risk

exposure to new account fraud – evidence from Germany. Journal of Banking & Finance,

33(2), 347-57.

9. Haugen, S. and Selin J.R.(1999). Identifying and controlling computer crime and employee

fraud. Industrial Management & Data Systems, 99(8), 340-344.

10. Hoffman, A.O.I &Birnbrich, C. (2012). The impact of fraud prevention on bank customer

relationships – An empirical investigation in retail banking. International Journal of Bank

Marketing, 30(5), 390-407.

11. Krummeck, S. (2000). The role of ethics in fraud prevention: a practitioner’s perspective.

Business Ethics: A European Review, 9(4), 268-72.

12. Khanna, A. &Arora, B. (2009). A study to investigate the reasons for bank frauds and

implementation of preventive security controls in Indian Banking Industry. International

Journal of Business Science & Applied Management, 4(3), 1-21.

13. Malphrus, S. (2009). Perspectives on retail payments fraud. Economic Perspectives, 33(1),

31-36.

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

92

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

14. Nsouli, S.M. &Schaechter, A. (2002). Challenges of the “E-banking Revolution”. Finance &

Development. 39(3). Retrieved from http://www.ieo-imf.org/external/pubs/ft/fandd/2002/09/

nsouli.htm .

15. Patil, G. (2013, October 9). Fake bank loan documents result in Rs. 8,734 crore fraud.

Retrieved fromhttp://www.dnaindia.com/india/report-fake-bank-loan-documents-result-in-

rs8734-crore-fraud-1900713 on 12/11/2013 .

16. Rauyruen, P. and Miller, K. (2007). Relationship quality as a predictor of B2B customer

loyalty. Journal of Business Research, 60(1), 21-31.

17. Sharma, S. and Brahma (2000). A Role of Insider in banking Fraud. Retrieved from

http://www.manuputra.com .

18. Singh, A. (2013). Changing face of fraud in India. Ernst &Yound, India. Retrieved from

http://www.ey.com/IN/en/Newsroom/News-releases/Published-editorial---Changing-face-of-

fraud-in-India on 13/11/2013.

19. Smith, E. R.(1995). A positive approach to dealing with embezzlement. The White Paper,

August/September, 17-18.

20. Smith, M. (2011). Effect of fraud on economic development- A case study of Nigerian bank

sector.

21. Sullivan, R.J. (2010). The changing nature of U.S. card payment fraud: industry and public

policy option. Economic Review, 95(2), 101-133.

22. Varela-Neira, C., Va´zquezCasielles, R. and Iglesias, V. (2010). Lack of preferential

treatment:

23. effects on dissatisfaction after a service failure. Journal of Service Management, 21(1), 45-

68.

24. Worthington, S. (2009). Debit cards and fraud. International Journal of Bank Marketing,

27(5), 400-402.

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

93

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

Annexures

Annexure 1: Year-wise Deposit details of Scheduled Commercial Banks

Year

Metropolitan Rural Semi-urban Urban Total

No. of

Accounts

Deposits

(In Rs.

Million)

No. of

Accounts

Deposits

(In Rs.

Million)

No. of

Accounts

Deposits

(In Rs.

Million)

No. of

Accounts

Deposits

(In Rs.

Million)

No. of

Accounts

Deposits

(In Rs.

Million)

2011-

12 199,551 33899206.86 283,072 5731858.538 239,951 8425446.861 180,626 12725921.14 903200.257 60782433.4

2010-

11 179,796 30689412.9 250,254 4932655.207 212,043 7168312.046 168,037 11105133.12 810129.353 53895513.27

2009-

10 168,934 25816519.12 224,155 4203377.158 189,457 6140471.785 152,323 9449922.397 734869.141 45610290.46

2008-

09 143,205 20579841.97 193,193 3535630.984 164,459 5120243.153 137,802 7920568.201 638658.986 37156284.31

2007-

08 137,241 18585444.01 168,034 3034230.405 148,361 4302797.122 128,021 6576990.191 581658.012 32499461.73

2006-

07 123,306 14540434.7 149,663 2530136.913 132,808 3573951.354 113,422 5325922.053 519199.207 25970445.02

2005-

06 117,692 11320870.19 139,570 2260611.838 121,664 3022128.05 106,172 4308132.28 485097.771 20911742.36

2004-

05 98,310 8631335.106 141,908 2131041.075 125,198 2956853.958 101,376 3748910.254 466792.531 17468140.39

2003-

04 98,176 7176790.128 138,760 1950817.089 120,651 2682169.224 99,571 3302957.447 457158.054 15112733.89

2002-

03 95,711 5674332.675 136,733 1765023.916 117,537 2417566.835 96,099 2905033.591 446080.712 12761957.02

2001-

02 94,975 4935013.726 133,000 1594234.612 117,394 2149903.877 94,622 2554780.984 439989.348 11233933.2

2000-

01 87,137 4059811.892 131,723 1394313.595 116,400 1861879.981 92,769 2178327.47 428029.197 9494332.938

Source: RBI bulletin August 2013

Annexure 2: Year wise credit summary of Scheduled commercial banks

Year No. of Accounts Credit Limit (in Rs Crore) Amount Outstanding (in Rs

Crore)

2011 120724095 7715531.26 4075647.00

2010 118647882 4868696.90 3345169.32

2009 110056177 4029076.84 2847713.12

2008 106990180 3284091.33 2417006.52

2007 94442027 2773409.13 1947099.62

2006 85435381 2118526.88 1513842.13

2005 77150794 1646266.13 1152467.93

2004 66390290 1176959.34 880312.03

2003 59491187 995133.83 755968.82

2002 56388379 855427.97 655993.08

2001 52364395 686951.07 538433.79

Source: RBI bulletin August 2013

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

94

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

Annexure 3: POPULATION GROUP-WISE NUMBER OF BRANCHES OF SCHEDULED

COMMERCIAL BANKS

(Number)

YEAR RURAL SEMI-URBAN URBAN METROPOLITAN TOTAL

2013 39336 28264 19941 18212 105753

2012 36428 25750 18980 17439 98597

2011 33909 23053 17749 16445 91156

2010 32473 20778 16810 15457 85518

2009 31453 19058 15374 14332 80217

2008 30772 17768 14333 13383 76256

2007 30248 16522 13070 12421 72261

2006 30106 15760 12200 11800 69866

2005 32082 15403 11500 9370 68355

2004 32121 15091 11000 8976 67188

2003 32303 14859 10693 8680 66535

2002 32380 14747 10477 8586 66190

2001 32562 14597 10293 8467 65919

Note : Data are exclusive of administrative offices.

Also see Notes on Tables.

Source : Data up to 2005 are based on Basic Statistical Returns of Scheduled Commercial Banks. Thereafter data are based on Master Office

File as on August 3, 2012.

Source: RBI bulletin August 2013

Annexure 4: Total Number Of ATMs Scheduled Commercial Banks Via Bank Group Wise

YEAR

WISE

FOREIGN

BANKS

NATIONALISED

BANKS

NEW

PRIVATE

SECTOR

BANKS

OLD

PRIVATE

SECTOR

BANKS

SBI AND ITS

ASSOCIATES

TOTAL

2008-09 1054 14840 12646 2674 11339 42553

2009-10 1026 19702 15057 3390 20978 60153

2010-11 1367 24836 19525 4126 24651 74505

2011-12 1414 31050 30308 5771 27143 95686

Source: RBI bulletin August 2013

ISSN:2321-0354-Online ISSN:2347-1654-Print

www.icm

rr.or

g

95

Volume 1, Issue 9 (November, 2013)

INTERCONTINENTAL JOURNAL OF FINANCE RESOURCE RESEARCH REVIEW

Pee

r R

evie

wed

Jo

urn

al o

f In

ter-

Co

nti

nen

tal M

anag

emen

t R

esea

rch

Co

nso

rtiu

m

htt

p:/

/ww

w.ic

mrr

.org

Annexure 5: Bank group wise Technology related frauds

BANK GROUP

2009-10 2010-11 2011-12 2012-13 Cumulative total

No of

cases

Amount

Involved

No of

cases

Amount

Involved

No of

cases

Amount

Involved

No of

cases

Amount

Involved

No of

cases

Amount

Involved

Nationalised banks

including SBI

group 118 1.82 143 3.39 172 7.26 190 9.85 824 25.6

Old Private sector

Banks 9 0.15 4 0.46 9 0.06 6 1.09 55 2.3

New Private Sector

Banks 14387 34.53 9638 21.41 6552 16.54 3408 33.97 74321 183.48

Sub Total 14396 34.68 9642 21.87 6561 16.6 3414 35.06 75200 211.38

Foreign Banks 5273 26.88 4486 14.77 3315 14.6 5161 22.45 36455 145.95

Grand Total 19787 63.38 14271 40.03 10048 38.46 8765 67.36 112479 382.93

Bank group-wise Advances related frauds

BANK GROUP

2009-10 2010-11 2011-12 2012-13 Cumulative total

No of

cases

Amount

Involved

No of

cases

Amount

Involved

No of

cases

Amount

Involved

No of

cases

Amount

Involved

No of

cases

Amount

Involved

Nationalised banks

including SBI

group 152 736.14 201 1820.12 228 2961.45 309 6078.43 1792 14577.28

Old Private sector

Banks 16 99.10 20 189.31 14 63.61 12 49.87 149 767.75

New Private Sector

Banks 10 63.38 18 234.18 12 75.68 24 67.47 363 1068.18

Sub Total 26 162.48 38 523.49 26 138.98 36 117.34 512 1835.93

Foreign Banks 4 45.26 3 33.2 19 83.51 4 16.75 456 277.05

Grand Total 182 943.88 242 2376.81 273 3183.94 349 6212.52 2760 16690.26

Source: RBI bulletin 2013

ISSN:2321-0354-Online ISSN:2347-1654-Print