are you ready for asc 842: leases? - aronson llc

TRANSCRIPT

© Aronson LLC | aronsonllc.com |

Are You Ready for ASC 842:

Leases?Mark Phillips, CPA and Chris Vasquez, CPA | Nov. 17, 2021

© Aronson LLC | aronsonllc.com 2

Your Instructors and Producer

Mark Phillips, CPA

Partner, Assurance Services

Chris Vasquez, CPA

Partner, Assurance Services

Heather LeGate

People Development Specialist

Ask or chat your questions during the webinar at any time.

3© Aronson LLC | aronsonllc.com

We are using Zoom as the learning webinar

platform.

To earn CPE credits for this course, you must

respond to at least 75% of all polling

questions.

• You will receive credit if you answer

the polls, not whether you get them

correct.

How to Earn CPE Credits

© Aronson LLC | aronsonllc.com

By the end of this course, you should be able to:

• Recall key concepts from ASC Topic 842.

• Calculate ROU (right of use) asset, analyze

schedules, and differentiate journal entries for

finance and operating leases.

Learning Objectives

© Aronson LLC | aronsonllc.com

Agenda

• Overview of New Standard

• Operating Lease Accounting: Lessees

• Finance Lease Accounting: Lessees

• Lessor Accounting

• Presentation, Disclosures, and Transition

Requirements

• What Reporting Entities Should Do Now

• Conclusion and Q&A

Overview of New Standard

© Aronson LLC | aronsonllc.com 7

Why Lease Accounting Rules Are Changing

Clarification of definition of a lease

Reduced opportunities for structuring contracts to avoid balance sheet recognition

More faithful representation of lessee’s rights and obligations arising from leases

Improvements in comparability of lessee’s financial statements

8© Aronson LLC | aronsonllc.com

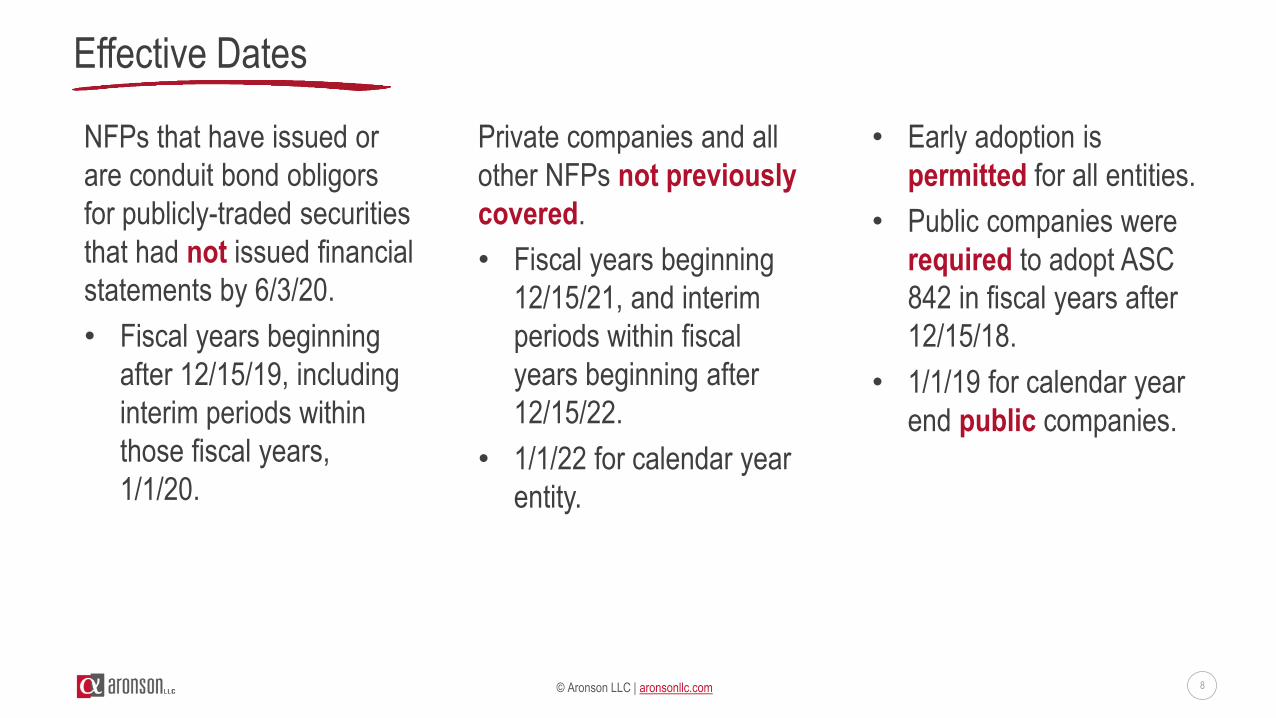

Effective Dates

NFPs that have issued or

are conduit bond obligors

for publicly-traded securities

that had not issued financial

statements by 6/3/20.

• Fiscal years beginning

after 12/15/19, including

interim periods within

those fiscal years,

1/1/20.

Private companies and all

other NFPs not previously

covered.

• Fiscal years beginning

12/15/21, and interim

periods within fiscal

years beginning after

12/15/22.

• 1/1/22 for calendar year

entity.

• Early adoption is

permitted for all entities.

• Public companies were

required to adopt ASC

842 in fiscal years after

12/15/18.

• 1/1/19 for calendar year

end public companies.

© Aronson LLC | aronsonllc.com 9

Accounting Standards Codification Topic 842: Scope

Applies to leases and subleases of identified property, plant, and equipment.

Does not apply to leases of:

• Intangible assets, like software licensing agreements for Microsoft Office

• Explore for or use nonregenerative resources such as minerals, oil, natural gas

• Biological assets

• Inventory

• Assets under construction

• Contracts for individuals

© Aronson LLC | aronsonllc.com 10

ASC 840 versus ASC 842: Accounting Standards Definition of Lease

ASC 840:

• Agreement conveying right to use PP&E for a stated period.

• Physically distinguishable portions of PP&E can be leased, for example, a floor of an office

building.

ASC 842:

• Contract is, or contains, a lease if it conveys right to control the use of an identified asset for

a period in exchange for consideration.

• Right to control use requires lessee to have both right to obtain substantially all economic

benefits from use of identified asset and right to direct use of identified asset.

• Specified time but could be output like right to use machine to produce 100,000 units.

• Identified asset which is typically, explicitly identified, but could be implied.

© Aronson LLC | aronsonllc.com 11

ASC 842: Accounting Standards Definition of Lease

Identified asset must be:

• Physically distinct like a vehicle, building, floor of a building, or last mile of a telecom

network that connects a single customer to network.

• Not physically distinct, but lessee has right to substantially all, 90%+, capacity of asset like

a capacity portion of an oil pipeline or a fiber optic cable.

• Free of substantive substitution rights held by supplier. Substantive substitution rights

exist if both of the following occur:

1. Supplier has practical ability to substitute alternative assets throughout period of use.

2. Supplier would benefit economically from exercise of its right to substitute asset.

Note: Supplier’s right or obligation to replace an asset for repairs or if technological upgrade

becomes available does not preclude customer from having right to use an identified asset.

© Aronson LLC | aronsonllc.com

Customer enters a contract with ship owner for transport of cargo from Rotterdam to Sydney on specified ship.

• Ship is explicitly specified in contract, and ship owner does not have substitution rights.

• Cargo will occupy substantially all capacity of ship.

• Contract specifies cargo to be transported on ship and dates of pickup and delivery.

Does customer have the right to direct how and for what purpose ship is used?

• Yes

• No

Poll 1: Right to Direct Use

© Aronson LLC | aronsonllc.com 13

ASC 842: Identified Assets

Identified assets may be explicitly or implicitly identified in a contract.

Explicit:

• Asset location, address, or specific identifiers like serial numbers.

• Physically distinct asset, or physically distinct portions of larger assets.

• Capacity portions of an asset are not identified asset unless asset is essentially dedicated to accrue to customer.

Implicit:

• Supplier has only one asset of that particular asset type available.

Note: No identified asset if supplier has substantive substitution rights, practical and economically beneficial to supplier.

© Aronson LLC | aronsonllc.com 14

Embedded Leases

Telecommunication service providers

• Cable and satellite services

• Set top boxes and modems

Transportation vendors

• Transportation and delivery

• Trains, cars, trucks, airports

Energy suppliers

• Power purchase agreements

• Power plant, wind, solar assets

IT or software vendors

• Cloud computing

• Servers, racks, space, hubs

Advertising vendors

• Advertising agreements

• Advertising equipment like billboards

Manufacturing suppliers

• Manufacturing agreements

• Plant, machinery, equipment

© Aronson LLC | aronsonllc.com 15

Decision Tree for Identifying Lease

Step 1: Is there an identified

asset?

Step 2: Does customer have right to obtain

substantially all economic benefits from use?

Step 3: Who has right to direct how and for

what purpose asset is used?

Does the customer have the right to operate

asset, and supplier does not have right to

change operating instructions?

Did customer design asset, such that its use is

predetermined for contract term?

Contract

does not

contain a

lease

Contract

contains a

lease

Yes

Yes

Neither

No

No

No

Supplier

No

Customer

Yes

Yes

© Aronson LLC | aronsonllc.com

We presented a decision tree to help you

determine whether a contract qualifies as a leader

under ASC 842. Which of the following multi-year

contracts generally qualifies as a lease? Select all

that apply.

• Help desk

• Laptops

• Microsoft Office

• Copiers

• Vehicles

Poll 2: Decision Tree

17© Aronson LLC | aronsonllc.com

New Lease Classifications

Finance lease

Operating lease

Short-term lease:

• Policy election that treats as previous

operating lease, off-balance sheet.

• Lease terms at least commencement of

no more than one year and no option to

purchase that lessee is reasonably certain

to exercise.

© Aronson LLC | aronsonllc.com 18

Finance Lease

Very similar to previous capital lease criteria.

Elimination of bright-line tests, 75% or 90%.

Inclusion of terms such as substantially all, reasonably certain, and major part.

Additional criteria around alternative use.

© Aronson LLC | aronsonllc.com 19

Finance Lease Recognition Criteria

Lessee is required to classify lease as finance when it meets any one of recognition criteria in

FASB ASC 842-10-25-2:

1. Lease transfers ownership of underlying asset to lessee by end of lease term.

2. Lease contains purchase option that lessee is reasonably certain to exercise.

3. Lease term is for major part of remaining economic life of underlying asset.

4. Present value of lease payments and residual value guaranteed by lessee equals or

exceeds substantially all of fair value of underlying asset.

5. New: Underlying asset is specialized and expected to have no alternative use to lessor at

end of lease term.

© Aronson LLC | aronsonllc.com 20

Lease and Nonlease Components

Occurs when lessor leases more than one asset to lessee and/or provides services in addition to lease of asset, such as CAM (common area maintenance), snow removal, and machine maintenance.

• Lease arrangement can contain lease components, nonlease components, and other items –‘non-components’.

• Contract consideration needs to be allocated between lease and nonlease components, but not non-components. This is generally based on standalone selling price and is a similar concept to ASC 606.

• Nonlease components, if not combined with lease components, should be accounted for in accordance with other GAAP.

• Lessee payments of taxes and insurance are not considered a separate lease or nonleasecomponent as payments represent lessee’s reimbursement of lessor’s costs and do not represent payments for goods and services.

• Admin or other fees charged by lessor to set up or service lease, or other charges that do not result in transfer of a good or service to lessee, are not components.

21© Aronson LLC | aronsonllc.com

Separate Lease Components

Right to use underlying asset is separate lease component if bothconditions are met:

1. Lessee can benefitfrom ROU either on its own or together with other resources that are readily available to lessee.

2. ROU is neither highly dependent on nor highly interrelated with other rights to use underlying assets in contract.

Generally, lessee needs to

account for lease of land

separately from other

leased assets:

• Lessee that leases an

entire building, is

inherently leasing land

underneath building.

Lessee may elect to

account for separate lease

components as a single

component, a portfolio

approach, if:

• Leases start and finish

on same dates.

• Doing so does not result

in a materially different

accounting treatment.

22© Aronson LLC | aronsonllc.com

Practical Expedient for Lease and Nonlease Components

Lessee may elect to apply the practical expedient to not separate lease and nonlease components.

Accounting policy election must be applied by class of underlying asset.

• Each separate lease component and associated nonlease component(s) are accounted for a single lease component.

This practical expedient does not permit lessees to treat multiple lease components as a single lease component but may not use portfolio approach.

Lessors may also make this practical expedient, if nonlease components would otherwise be accounted for under ASC 606.

In addition, for lessor to use alternative, bothof the following must be met:

1. Timing and pattern of revenue recognition are same for nonleasecomponent(s) and related lease component.

2. Combined single lease component, if accounted for separately, would be classified as an operating lease.

© Aronson LLC | aronsonllc.com 23

Lease Term

Non-cancelable periods.

Options that lessee is reasonably

certain to exercise.

Options controlled by lessor.

© Aronson LLC | aronsonllc.com 24

Lease Modifications

Previous standard was very complex.

Guidance simplified in new lease standard.

Lessee must determine whether modification results in new contract or change to existing lease.

Operating Lease Accounting: Lessees

© Aronson LLC | aronsonllc.com 26

Initial Measurement of Lease Liability

At lease inception, record lease liability equal to present value of all remaining lease payments, discounted using discount rate of lease.

Lessees should use discount rate implicit in lease whenever that rate is readily determinable. Usually, only lessors know this rate.

If rate implicit in lease is not readily determinable, lessee should use its incremental borrowing rate which is the rate of interest lessee would have to pay to borrow on collateralized basis over similar term.

Lessee that is not a public business entity may, as an accounting policy election applied to all leases, elect to use risk-free discount rate for lease. Risk-free discount rate should be period comparable to that of lease term.

© Aronson LLC | aronsonllc.com 27

Initial Measurement of ROU Assets for Operating Leases

Lessee initially measures ROU asset at cost, which consists of:

• Amount of initial measurement of lease liability, recorded at present value.

• Any lease payments made to lessor at or before commencement date, less any incentives

received.

• Any initial direct costs incurred by lessee.

Inputs needed to initially calculate ROU asset:

Lease

liability

Lease

prepayments

Initial

direct

costs

Lease

incentives

received

ROU

Asset

Subtract deferred rent

to eliminate existing lease

28© Aronson LLC | aronsonllc.com

Subsequent Measurement

Lease liability is subsequently adjusted to

agree to present value of remaining lease

payments at each balance sheet date.

• That is, increase lease liability for interest

on liability, and subtract any lease

payments made in period.

Lease expense under ASC 842 is calculated

in same way as under ASC 840.

Straight line of total net cash outflows under

lease, unless another systematic basis is

more appropriate.

Cash payments reduce lease liability when

made.

Lease expense does not include interest on

lease liability.

ROU asset is subsequently adjusted to be

the plug to offset movements in lease liability,

lease expense, and cash payments.

If ROU asset is partly or fully impaired, then it

is written down.

29© Aronson LLC | aronsonllc.com

Operating Lease Example: Key Facts

• Lease commenced on January 1, 2022.

• Monthly payments of $10,000 for five years, paid in advance.

• $5,000 initial direct costs.

• Lessor provides $12,000 cash incentive.

• Lessor pays for $6,000 of lessee moving costs.

• Discount rate of 10%

• Total lease expense is $587,000 or $117,400 per year.

• Lessor’s reimbursement of moving costs reduces rent expense, not moving expense.

© Aronson LLC | aronsonllc.com 30

Present Value of Future Payments: Lease Liability

LEASE LIABILITY PAYMENTS

Day 1: Before up-front

payment

$474,576

Day 1: After up-front

payment

$464,576

End of Year 1 $394,282

End of Year 2 $309,912

© Aronson LLC | aronsonllc.com 31

Day 1 Journal Entries

Journal Entry

DR: ROU asset $461,576

CR: Cash $10,000 Upfront payment

DR: A/P or cash $6,000 Moving expenses

DR: Cash $12,000 Cash incentive

CR: Cash $5,000 Initial direct costs

CR: Lease liability $464,576

© Aronson LLC | aronsonllc.com 32

End of Year 1

Lease liability $394,282

ROU asset $383,882 DR: Lease liability $70,294

Lease expense $117,400 DR: Lease expense $117,400

Cash paid $110,000 CR: Cash paid $110,000

CR: ROU asset $77,694

© Aronson LLC | aronsonllc.com 33

End of Year 2

Lease liability $309,912

ROU asset $302,112 DR: Lease

liability

$84,370

Lease expense $117,400 DR: Lease

expense

$117,400

Cash paid $120,000 CR: Cash paid $120,000

CR: ROU asset $81,770

Finance Accounting: Lessees

© Aronson LLC | aronsonllc.com 35

Initial Measurement

The balances initially recorded for a finance lease are the same as for an operating lease.

Lease liability is the present value of all remaining lease payments, discounted using the

discount rate of the lease.

ROU asset is equal to the lease liability adjusted for the following:

• Add any lease payments made to the lessor at or before the lease commencement.

• Add any initial direct costs incurred by the lessee.

• Deduct any lease incentives received from the lessor.

© Aronson LLC | aronsonllc.com

What input do you subtract when calculating ROU

assets?

• Lease prepayments

• Lease incentives received

• Initial direct costs

Poll 3: ROU Asset

37© Aronson LLC | aronsonllc.com

Deferred Rent Liabilities

Upon adoption of ASC 842, most finance

leases will previously have been classified as

capital leases, and so we do not expect to

see existing deferred rent liabilities under

ASC 840 netted against the new ASC 842

ROU assets for finance leases.

© Aronson LLC | aronsonllc.com 38

Subsequent Measurement

Lease liability is subsequently adjusted to present value of remaining lease payments at each

balance sheet date, same as operating lease. That is, increase lease liability for interest on

liability, and subtract any lease payments made in period.

Interest expense does arise under finance lease, unlike an operating lease, and is a

component of total lease expense. Interest expense is calculated using effective interest method

to produce constant period interest rate on lease liability.

ROU asset is subsequently amortized on straight-line basis over earlier of lease term or useful

economic life of ROU asset, unless another systematic basis is more appropriate, not the same

as operating lease.

39© Aronson LLC | aronsonllc.com

Finance Lease Components

As a result, lease expense will be front-

loaded.

• Higher in early years, and lower in later

years.

• Unlike operating lease expense which is

typically straight line.

Finance lease expense has at least two components:

• Interest component is equal to interest accruing on the finance lease liability.

• Amortization component is equal to amortization of ROU asset.

40© Aronson LLC | aronsonllc.com

Other Possible Components

Other possible components to a finance

lease or operating lease expense include:

• Variable lease payments that are not

included in lease liability, for example,

variable lease payments that do not

depend on an index or rate.

• Changes to variable lease payments that

depend on an index or rate.

• Impairment of ROU asset.

© Aronson LLC | aronsonllc.com 41

Finance Lease Example

End of Year 1 End of Year 2

DR: Lease liability $70,294 DR: Lease liability $84,370

DR: Lease expense $132,021 DR: Lease expense $127,945

CR: Cash paid $110,000 CR: Cash paid $120,000

CR: ROU asset $92,315 CR: ROU asset $92,315

Lessor Accounting

43© Aronson LLC | aronsonllc.com

Lease Classification

No significant changes to lessor accounting

model under ASC 842 versus ASC 840.

Existing lease classifications retained:

• Sales-type

• Directing financing

• Operating

Additional requirements to:

• Assess collectability to support

classification as direct financing lease

• In order to derecognize asset and record

revenue under sales-type lease, collection

of payments due must be probable.

Similar income statement and balance sheet

protection.

Presentation, Disclosures, and Transition Requirements

© Aronson LLC | aronsonllc.com 45

Balance Sheet for Lessee

Present separately or disclose finance and operating lease right-of-use assets and liabilities from other assets and liabilities, respectively.

If disclosed, need to call out which items lease assets and liabilities are included with.

Entity is prohibited from presenting operating financing ROU assets within same line item.

Same applies to liability side.

© Aronson LLC | aronsonllc.com 46

Balance Sheet for Lessor

No changes from previous lease requirements.

Present lease assets separately from other assets, subject to current versus noncurrent classification.

© Aronson LLC | aronsonllc.com

Finance leases:

• Amortization of right-of-use asset and interest

on lease liability consistent with other assets

and other interest expense.

Operating leases:

• Present as single lease expense consistent

with previous lease standard.

Income Statement for Lessee

© Aronson LLC | aronsonllc.com

Which of the following multi-year contracts do we

generally classify as an operating lease?

• Laptops

• Specialized equipment

• Office space

Poll 4: Operating Lease

49© Aronson LLC | aronsonllc.com

Income Statement from Lessor

• Option to present lease income separately or disclose within notes which items include lease income.

All leases:

50© Aronson LLC | aronsonllc.com

Statement of Cash Flows for Lessee

Operating Operating lease payments, variable

lease payments, interest component

of finance leases, and short-term

lease payments.

Investing Payments to bring another asset to

condition necessary for intended

use.

Financing Repayment of principal portion of

lease liability.

51© Aronson LLC | aronsonllc.com

Statement of Cash Flows for Lessor

All cash receipts from lease should be

classified as operating activities.

52© Aronson LLC | aronsonllc.com

Disclosures for Lessee and Lessor

Information about nature

of entity’s leases.

Existence of options to extend or terminate.

Significant assumptions

and judgments.

Lease transactions with related

parties.

53© Aronson LLC | aronsonllc.com

Disclosures for Lessee Only

• Residual value guarantees.

• Restrictions or covenants imposed by

leases.

• Discount rate determination.

• Lease maturity analysis.

Quantitative disclosures include lease cost

and sublease income.

Additional quantitative disclosures,

segregated by type of lease, for cash paid,

supplemental non-cash transaction

information, and weighted average remaining

lease term and discount rate.

© Aronson LLC | aronsonllc.com 54

Transition Requirements

Two modified retrospective methods permitted:

1. Entity records ROU asset and lease liability, with cumulative-effect adjustment at beginning

of earliest comparative period presented or lease commencement date, if later. For

example, 1/1/20 if one comparative year shown and adopt 1/1/21.

2. Entity records ROU asset and lease liability, with cumulative-effect adjustment at beginning

of year of adoption. For example, apply ASC 840 in FY2020 and apply ASC 842 from

1/1/21 onwards.

Full retrospective transition is prohibited.

• Practical expedients available.

© Aronson LLC | aronsonllc.com

Lease includes initial non-cancellable term of five years:

• During fourth year of lease, lessor has unilateral ability to extend lease for another two years at conclusion of initial five-year term.

• Entity is provided with two, three-year options to extend lease.

• At commencement date, entity is not sure whether to extend lease.

What is the lease term under ASC 842?

• 3 years

• 5 years

• 7 years

Poll 5: Lease Specialized Equipment

What Reporting Entities Should Do Now

© Aronson LLC | aronsonllc.com 57

Start to Think About Effects and Adoption Considerations

Effect Adoption Considerations

Balance

sheet

Lease liability is calculated as present value of sum of:

1. Remaining minimum rental payments, as defined under ASC 840.

2. Any amounts probable of being owed by lessee under residual value guarantee.

Right of use asset is equal to lease liability adjusted for the following:

1. Prepaid or accrued rent.

2. Remaining balance of any lease incentives.

3. Unamortized initial direct costs that would have qualified for capitalization under ASC 842.

4. Impairment.

5. Carry amount of any lease exit or disposal cost liabilities.

Income

statement

Finance leases:

• Amortization of right-of-use asset and interest on lease liability consistent with other assets and other

interest expenses.

Operating leases:

• Present as a single lease expense consistent with previous lease standard.

58© Aronson LLC | aronsonllc.com

Practical Expedients

The following transition practical expedients

are available and must be elected as a

package:

• No reassessment of whether any expired

or existing contracts are or contain

leases.

• No reassessment of lease classification

for any expired or existing leases.

• No reassessment of initial direct costs for

any existing leases.

• Transition guidance is not applied to short

term lease if election is made to not

recognize these under ASC 842.

Post transition policy elections should be

considered at transition date:

• Option to not separate nonlease

components from associated lease

components, by class of asset.

• Option to not apply recognition and

measurement principles of ASC 842 to

short term leases.

© Aronson LLC | aronsonllc.com

Some clients elect practical expedient in order not

to separate lease and nonlease components in

contracts for accounting purposes. Which

statement is correct about this election?

• It allows the lessee to separate one lease

component from another.

• It allows the lessee to separate non-

components from lease components.

• It allows the lessee to account for the lease

and nonlease components as a single unit of

account.

Poll 6: Practical Expedient

© Aronson LLC | aronsonllc.com

Financial ratios may change under ASC 842,

including those used by banks, investors, board of

directors, and management.

Covenants most likely affected:

• Current ratio

• Quick ratio, known as acid test

• Working capital

• Debt to equity

• Debt service coverage ratios

• Covenants using EBITDA (earnings before

interest taxes depreciation and amortization.

Impact on Loan Covenants

© Aronson LLC | aronsonllc.com 61

Evolve Your Thinking About Leases

Borrowers may try to reduce the impact of new lease accounting rules by negotiating lease

terms that present less indebtedness on balance sheet.

• Choose shorter terms with options for renewal, or even terms that are less than a year to

qualify for off-balance-sheet treatment.

• Negotiate for leases where smaller amount of fixed rent will be carried as indebtedness on

balance sheet, with lessee paying pro-rata share of ongoing expenses, like taxes or

insurance, that are captured on off-balance-sheet.

• Freezing GAAP for operating leases. Add a clause to existing debt agreements for debt-to-

equity ratio calculation to be based upon rules in force at time of original agreement instead

of new rules.

Work with a CPA to provide clarity, guidance, or classification relevant to your specific

circumstances.

© Aronson LLC | aronsonllc.com 62

Timeline

Understand

Educate

Evaluate impact

Formulate project plan

Decide on key adoption decisions

63© Aronson LLC | aronsonllc.com

Step 1: Evaluate and Decide Methods and Transitions

• Appoint ownership

• Review new standard

and evaluate impact and

applicability

• Understand adoption

date, transition methods,

and practical expedients

• Financial statement

presentation

Evaluate impact to:

• Business operations

• Financial statement

comparability and

presentation.

• Need for technology

• Identify external partners

to fill skill set gaps and

accelerate compliance,

like auditors or

technology partners

Decide on key adoption

dates and transition

methods:

• Design timeline of

compliance and work

backwards from

compliance deadline

• Create project plan

© Aronson LLC | aronsonllc.com 64

Step 2: Create Inventory of Leases

Detailed lease commitment schedule by lease type that agrees to financial statement discloses and all contracts related to those material leases, including amendments.

Historical accounting analysis for all material lease contracts.

Reconciliation of income statement and balance sheet amounts like rent expenses, prepaid rent, and deferred rent, to detailed analysis noted above.

65© Aronson LLC | aronsonllc.com

Step 2: Gather Available Historical Information

Other places to look:

• Listing of leased assets from all entities,

departments, and locations.

• Listing of recurring payments from

accounts payable.

• Copies of all contracts from all entities,

departments, and locations.

Evaluate all contracts to determine scope.

• Are there any embedded leases?

66© Aronson LLC | aronsonllc.com

Step 3: Data Extraction from Steps 1 and 2 and Input Lease Data

Consideration of lease solutions and

technology.

Relevant historical financial information data:

• Cumulative prepaid rent or deferred rent

• Remaining lease incentives

• Unamortized initial direct costs

Relevant data from lease agreements:

• Lease term, lease commencement, and lease expiration dates

• Security deposits

• Purchase, renewal, and termination options

• Lease payments and escalations

• Rent abatement and holidays

• Incentives

• Nonlease components

67© Aronson LLC | aronsonllc.com

Step 4: Calculation and Reporting

Calculation, resulting lease amortization schedules, transition adjustments and financial reporting:

• Determine interest rates at transition date.

• Amortization schedules.

• Generate or calculate transition entries.

• Update lease accounting policies, practical expedients.

• Create financial statements and draft disclosures at transition.

• Reconcile outputs, financial statements, and disclosures to GL and lease accounting solution.

Create financial statements and draft

disclosures on an ongoing basis.

Qualitative disclosures:

• Nature of leases

• Sublease information

• Leases that have not yet commenced

• Significant assumptions and judgment

with discount rate and lease versus

nonlease components

• Policy elections like short-term leases

exemption and lease and nonlease

component combination

© Aronson LLC | aronsonllc.com

A supplier and customer enter into a contract for

customer to use piece of equipment for five years.

Supplier only requires that customer not damage

equipment. Is this considered a lease?

• Yes

• No

• Possibly

• Need more information

Poll 7: Contracts

Conclusion and Q&A

© Aronson LLC | aronsonllc.com 70

How Aronson Can Help

Calculating lease liabilities, ROU assets, and related expenses

Developing lease discount rate

Drafting policy notes and disclosures

Identifying population of leases

Identifying whether contract is or contains a lease

Allocation of lease contract consideration between lease and nonlease components

Training team members how to calculate ROU assets and lease liabilities

Assisting with process notes documentation and key internal controls

© Aronson LLC | aronsonllc.com 71

Additional Resources

Aronson

• Lease Accounting Hub

Our team of experts are here to help you think strategically through the process. Contact our

team to get started today.

• Chris Vasquez, CPA, Partner in Construction and Real Estate Services Group

• Mark Phillips, CPA, Partner in Diversified Commercial Services Group

• Mark Robins, CPA, Partner in Nonprofit Services Group

• Will Donahue, CPA, Senior Manager in Nonprofit Services Group

Any Questions?Thank you for your time.

73© Aronson LLC | aronsonllc.com

Your CPE Certificate and Course Evaluation

Upon successful completion of this course, Prolaera automatically sends your CPE certificate to your email used to register for this session on Zoom. Please disregard any links for evaluations in that email.

Students, instructors, and producers, we want your feedback!

• The producer has emailed you with a link to the course evaluation. Please take it now.

• We will close the survey COB Nov. 17, 2021.