appendix a: formula sheet

TRANSCRIPT

391© The Author(s) 2017J.Y. Abor, Entrepreneurial Finance for MSMEs, DOI 10.1007/978-3-319-34021-0

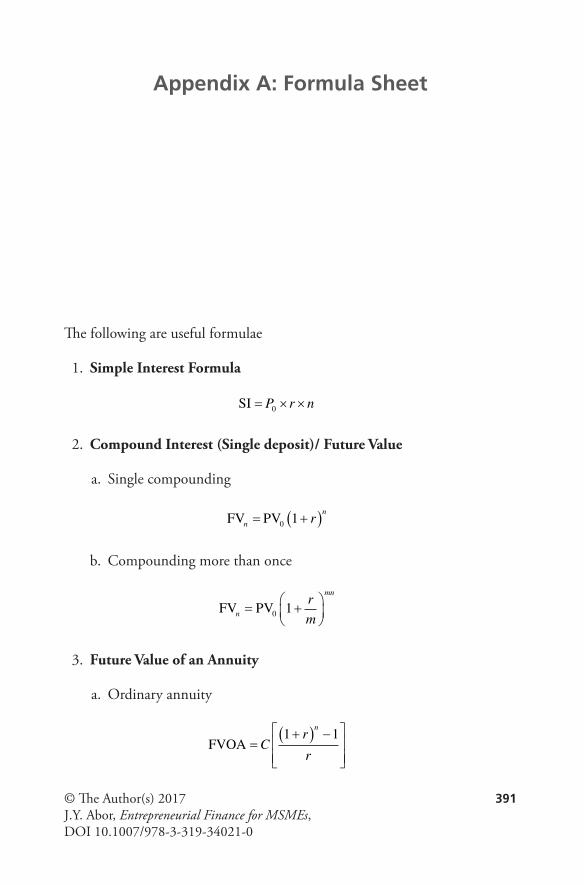

The following are useful formulae

1. Simple Interest Formula

SI = × ×P r n0

2. Compound Interest (Single deposit)/ Future Value

a. Single compounding

FV PVn

nr= +( )0 1

b. Compounding more than once

FV PVn

mnr

m= +

0 1

3. Future Value of an Annuity

a. Ordinary annuity

FVOA =+( ) −

Cr

r

n1 1

Appendix A: Formula Sheet

392 Appendix A: Formula Sheet

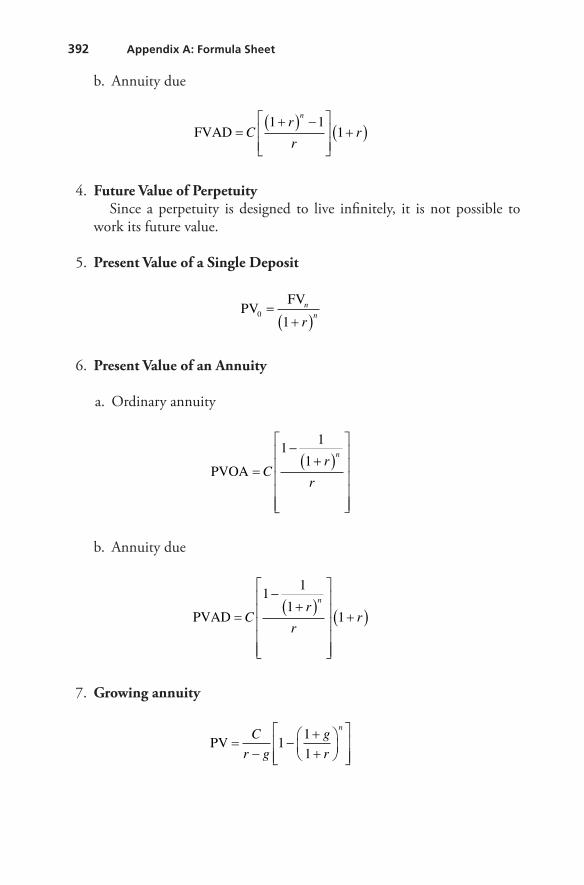

b. Annuity due

FVAD =+( ) −

+( )Cr

rr

n1 1

1

4. Future Value of PerpetuitySince a perpetuity is designed to live infinitely, it is not possible to

work its future value.

5. Present Value of a Single Deposit

PVFV

01

=+( )

nn

r

6. Present Value of an Annuity

a. Ordinary annuity

PVOA =

−+( )

Cr

r

n1

1

1

b. Annuity due

PVAD =

−+( )

+( )Cr

rr

n1

1

11

7. Growing annuity

PV =−

−++

C

r g

g

r

n

11

1

Appendix A: Formula Sheet 393

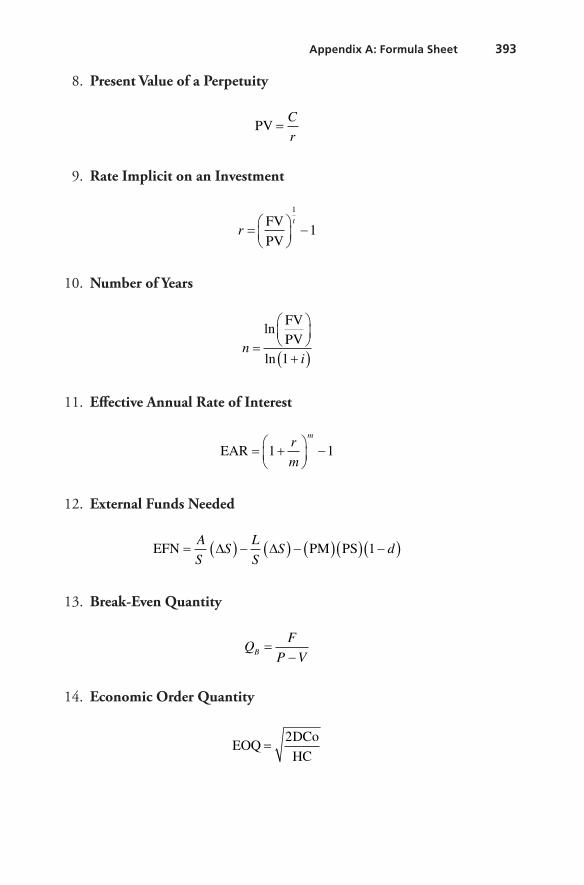

8. Present Value of a Perpetuity

PV =

C

r

9. Rate Implicit on an Investment

r

t

=

−

FV

PV

1

1

10. Number of Years

n

i=

+( )

ln

ln

FVPV1

11. Effective Annual Rate of Interest

EAR = +

−1 1

r

m

m

12. External Funds Needed

EFN PM PS= ( ) − ( ) − ( )( ) −( )A

SS

L

SS d∆ ∆ 1

13. Break-Even Quantity

Q

F

P VB =−

14. Economic Order Quantity

EOQ

DCo

HC=

2

394 Appendix A: Formula Sheet

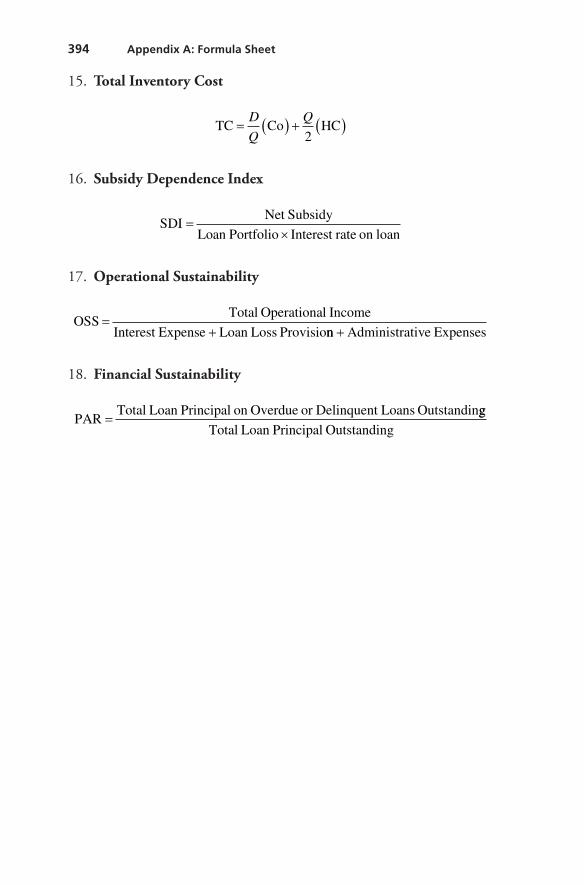

15. Total Inventory Cost

TC Co HC= ( ) + ( )D

Q

Q

2

16. Subsidy Dependence Index

SDI

Net Subsidy

Loan Portfolio Interest rate on loan=

×

17. Operational Sustainability

OSS

Total Operational Income

Interest Expense Loan Loss Provisio=

+ nn Administrative Expenses+

18. Financial Sustainability

PAR

Total Loan Principal on Overdue or Delinquent Loans Outstandin=

gg

Total Loan Principal Outstanding

Ap

pen

dix

B: F

inan

cial

Tab

les

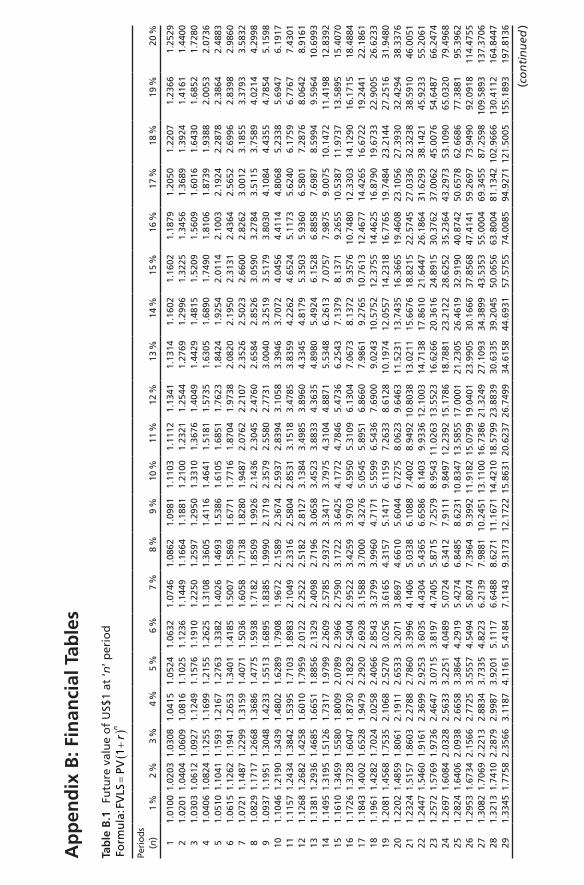

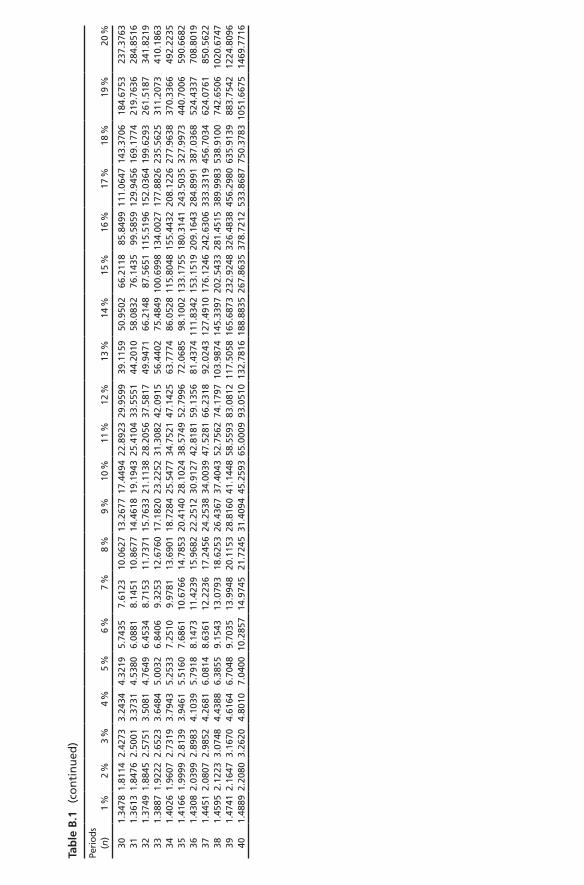

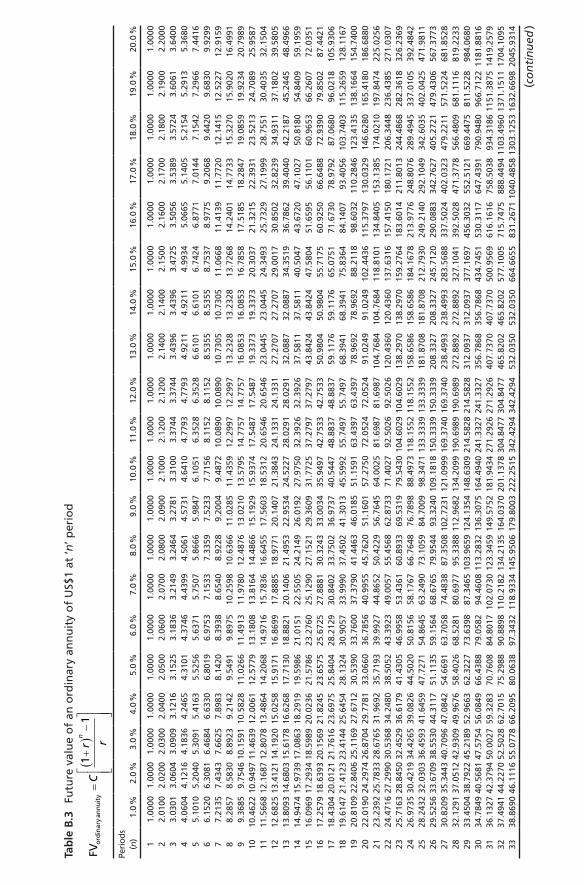

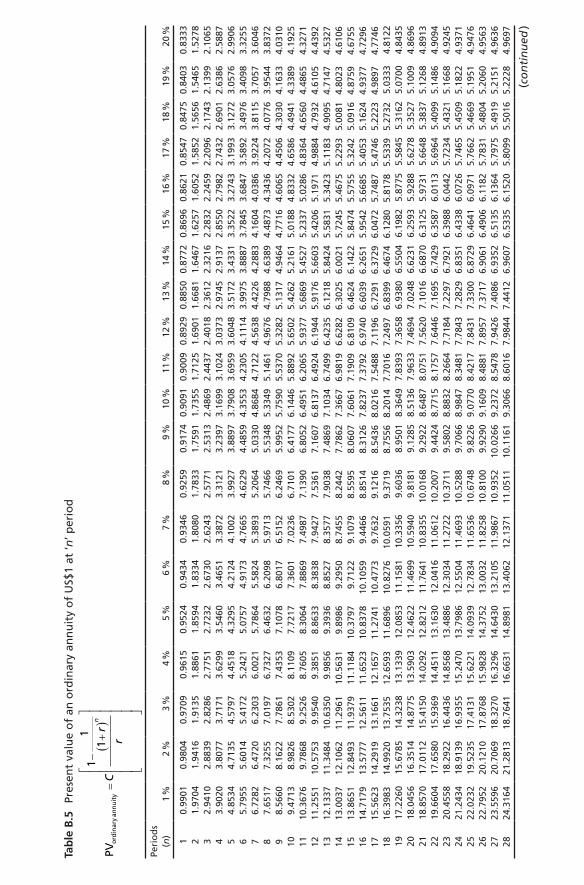

Tab

le B

.1

Futu

re v

alu

e o

f U

S$1

at ‘n

’ per

iod

Form

ula

FVLS

PV:

=+

()

1r

n

Peri

ods

(n)

1 %

2 %

3 %

4 %

5 %

6 %

7 %

8 %

9 %

10 %

11 %

12 %

13 %

14 %

15 %

16 %

17 %

18 %

19 %

20 %

11.

0100

1.02

031.

0308

1.04

151.

0524

1.06

321.

0746

1.08

621.

0981

1.11

031.

1112

1.13

411.

1314

1.16

021.

1602

1.18

791.

2050

1.22

071.

2366

1.25

292

1.02

011.

0404

1.06

091.

0816

1.10

251.

1236

1.14

491.

1664

1.18

811.

2100

1.23

211.

2544

1.27

691.

2996

1.32

251.

3456

1.36

891.

3924

1.41

611.

4400

31.

0303

1.06

121.

0927

1.12

491.

1576

1.19

101.

2250

1.25

971.

2950

1.33

101.

3676

1.40

491.

4429

1.48

151.

5209

1.56

091.

6016

1.64

301.

6852

1.72

804

1.04

061.

0824

1.12

551.

1699

1.21

551.

2625

1.31

081.

3605

1.41

161.

4641

1.51

811.

5735

1.63

051.

6890

1.74

901.

8106

1.87

391.

9388

2.00

532.

0736

51.

0510

1.10

411.

1593

1.21

671.

2763

1.33

821.

4026

1.46

931.

5386

1.61

051.

6851

1.76

231.

8424

1.92

542.

0114

2.10

032.

1924

2.28

782.

3864

2.48

836

1.06

151.

1262

1.19

411.

2653

1.34

011.

4185

1.50

071.

5869

1.67

711.

7716

1.87

041.

9738

2.08

202.

1950

2.31

312.

4364

2.56

522.

6996

2.83

982.

9860

71.

0721

1.14

871.

2299

1.31

591.

4071

1.50

361.

6058

1.71

381.

8280

1.94

872.

0762

2.21

072.

3526

2.50

232.

6600

2.82

623.

0012

3.18

553.

3793

3.58

328

1.08

291.

1717

1.26

681.

3686

1.47

751.

5938

1.71

821.

8509

1.99

262.

1436

2.30

452.

4760

2.65

842.

8526

3.05

903.

2784

3.51

153.

7589

4.02

144.

2998

91.

0937

1.19

511.

3048

1.42

331.

5513

1.68

951.

8385

1.99

902.

1719

2.35

792.

5580

2.77

313.

0040

3.25

193.

5179

3.80

304.

1084

4.43

554.

7854

5.15

9810

1.10

461.

2190

1.34

391.

4802

1.62

891.

7908

1.96

722.

1589

2.36

742.

5937

2.83

943.

1058

3.39

463.

7072

4.04

564.

4114

4.80

685.

2338

5.69

476.

1917

111.

1157

1.24

341.

3842

1.53

951.

7103

1.89

832.

1049

2.33

162.

5804

2.85

313.

1518

3.47

853.

8359

4.22

624.

6524

5.11

735.

6240

6.17

596.

7767

7.43

0112

1.12

681.

2682

1.42

581.

6010

1.79

592.

0122

2.25

222.

5182

2.81

273.

1384

3.49

853.

8960

4.33

454.

8179

5.35

035.

9360

6.58

017.

2876

8.06

428.

9161

131.

1381

1.29

361.

4685

1.66

511.

8856

2.13

292.

4098

2.71

963.

0658

3.45

233.

8833

4.36

354.

8980

5.49

246.

1528

6.88

587.

6987

8.59

949.

5964

10.6

993

141.

1495

1.31

951.

5126

1.73

171.

9799

2.26

092.

5785

2.93

723.

3417

3.79

754.

3104

4.88

715.

5348

6.26

137.

0757

7.98

759.

0075

10.1

472

11.4

198

12.8

392

151.

1610

1.34

591.

5580

1.80

092.

0789

2.39

662.

7590

3.17

223.

6425

4.17

724.

7846

5.47

366.

2543

7.13

798.

1371

9.26

5510

.538

711

.973

713

.589

515

.407

016

1.17

261.

3728

1.60

471.

8730

2.18

292.

5404

2.95

223.

4259

3.97

034.

5950

5.31

096.

1304

7.06

738.

1372

9.35

7610

.748

012

.330

314

.129

016

.171

518

.488

417

1.18

431.

4002

1.65

281.

9479

2.29

202.

6928

3.15

883.

7000

4.32

765.

0545

5.89

516.

8660

7.98

619.

2765

10.7

613

12.4

677

14.4

265

16.6

722

19.2

441

22.1

861

181.

1961

1.42

821.

7024

2.02

582.

4066

2.85

433.

3799

3.99

604.

7171

5.55

996.

5436

7.69

009.

0243

10.5

752

12.3

755

14.4

625

16.8

790

19.6

733

22.9

005

26.6

233

191.

2081

1.45

681.

7535

2.10

682.

5270

3.02

563.

6165

4.31

575.

1417

6.11

597.

2633

8.61

2810

.197

412

.055

714

.231

816

.776

519

.748

423

.214

427

.251

631

.948

020

1.22

021.

4859

1.80

612.

1911

2.65

333.

2071

3.86

974.

6610

5.60

446.

7275

8.06

239.

6463

11.5

231

13.7

435

16.3

665

19.4

608

23.1

056

27.3

930

32.4

294

38.3

376

211.

2324

1.51

571.

8603

2.27

882.

7860

3.39

964.

1406

5.03

386.

1088

7.40

028.

9492

10.8

038

13.0

211

15.6

676

18.8

215

22.5

745

27.0

336

32.3

238

38.5

910

46.0

051

221.

2447

1.54

601.

9161

2.36

992.

9253

3.60

354.

4304

5.43

656.

6586

8.14

039.

9336

12.1

003

14.7

138

17.8

610

21.6

447

26.1

864

31.6

293

38.1

421

45.9

233

55.2

061

231.

2572

1.57

691.

9736

2.46

473.

0715

3.81

974.

7405

5.87

157.

2579

8.95

4311

.026

313

.552

316

.626

620

.361

624

.891

530

.376

237

.006

245

.007

654

.648

766

.247

424

1.26

971.

6084

2.03

282.

5633

3.22

514.

0489

5.07

246.

3412

7.91

119.

8497

12.2

392

15.1

786

18.7

881

23.2

122

28.6

252

35.2

364

43.2

973

53.1

090

65.0

320

79.4

968

251.

2824

1.64

062.

0938

2.66

583.

3864

4.29

195.

4274

6.84

858.

6231

10.8

347

13.5

855

17.0

001

21.2

305

26.4

619

32.9

190

40.8

742

50.6

578

62.6

686

77.3

881

95.3

962

261.

2953

1.67

342.

1566

2.77

253.

5557

4.54

945.

8074

7.39

649.

3992

11.9

182

15.0

799

19.0

401

23.9

905

30.1

666

37.8

568

47.4

141

59.2

697

73.9

490

92.0

918

114.

4755

271.

3082

1.70

692.

2213

2.88

343.

7335

4.82

236.

2139

7.98

8110

.245

113

.110

016

.738

621

.324

927

.109

334

.389

943

.535

355

.000

469

.345

587

.259

810

9.58

9313

7.37

0628

1.32

131.

7410

2.28

792.

9987

3.92

015.

1117

6.64

888.

6271

11.1

671

14.4

210

18.5

799

23.8

839

30.6

335

39.2

045

50.0

656

63.8

004

81.1

342

102.

9666

130.

4112

164.

8447

291.

3345

1.77

582.

3566

3.11

874.

1161

5.41

847.

1143

9.31

7312

.172

215

.863

120

.623

726

.749

934

.615

844

.693

157

.575

574

.008

594

.927

112

1.50

0515

5.18

9319

7.81

36

(co

nti

nu

ed )

Peri

ods

(n)

1 %

2 %

3 %

4 %

5 %

6 %

7 %

8 %

9 %

10 %

11 %

12 %

13 %

14 %

15 %

16 %

17 %

18 %

19 %

20 %

301.

3478

1.81

142.

4273

3.24

344.

3219

5.74

357.

6123

10.0

627

13.2

677

17.4

494

22.8

923

29.9

599

39.1

159

50.9

502

66.2

118

85.8

499

111.

0647

143.

3706

184.

6753

237.

3763

311.

3613

1.84

762.

5001

3.37

314.

5380

6.08

818.

1451

10.8

677

14.4

618

19.1

943

25.4

104

33.5

551

44.2

010

58.0

832

76.1

435

99.5

859

129.

9456

169.

1774

219.

7636

284.

8516

321.

3749

1.88

452.

5751

3.50

814.

7649

6.45

348.

7153

11.7

371

15.7

633

21.1

138

28.2

056

37.5

817

49.9

471

66.2

148

87.5

651

115.

5196

152.

0364

199.

6293

261.

5187

341.

8219

331.

3887

1.92

222.

6523

3.64

845.

0032

6.84

069.

3253

12.6

760

17.1

820

23.2

252

31.3

082

42.0

915

56.4

402

75.4

849

100.

6998

134.

0027

177.

8826

235.

5625

311.

2073

410.

1863

341.

4026

1.96

072.

7319

3.79

435.

2533

7.25

109.

9781

13.6

901

18.7

284

25.5

477

34.7

521

47.1

425

63.7

774

86.0

528

115.

8048

155.

4432

208.

1226

277.

9638

370.

3366

492.

2235

351.

4166

1.99

992.

8139

3.94

615.

5160

7.68

6110

.676

614

.785

320

.414

028

.102

438

.574

952

.799

672

.068

598

.100

213

3.17

5518

0.31

4124

3.50

3532

7.99

7344

0.70

0659

0.66

8236

1.43

082.

0399

2.89

834.

1039

5.79

188.

1473

11.4

239

15.9

682

22.2

512

30.9

127

42.8

181

59.1

356

81.4

374

111.

8342

153.

1519

209.

1643

284.

8991

387.

0368

524.

4337

708.

8019

371.

4451

2.08

072.

9852

4.26

816.

0814

8.63

6112

.223

617

.245

624

.253

834

.003

947

.528

166

.231

892

.024

312

7.49

1017

6.12

4624

2.63

0633

3.33

1945

6.70

3462

4.07

6185

0.56

2238

1.45

952.

1223

3.07

484.

4388

6.38

559.

1543

13.0

793

18.6

253

26.4

367

37.4

043

52.7

562

74.1

797

103.

9874

145.

3397

202.

5433

281.

4515

389.

9983

538.

9100

742.

6506

1020

.674

739

1.47

412.

1647

3.16

704.

6164

6.70

489.

7035

13.9

948

20.1

153

28.8

160

41.1

448

58.5

593

83.0

812

117.

5058

165.

6873

232.

9248

326.

4838

456.

2980

635.

9139

883.

7542

1224

.809

640

1.48

892.

2080

3.26

204.

8010

7.04

0010

.285

714

.974

521

.724

531

.409

445

.259

365

.000

993

.051

013

2.78

1618

8.88

3526

7.86

3537

8.72

1253

3.86

8775

0.37

8310

51.6

675

1469

.771

6

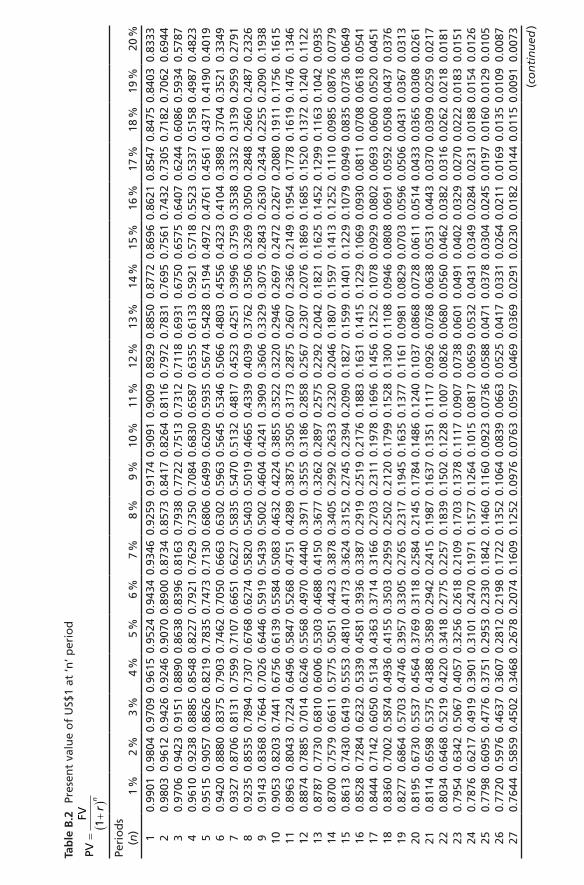

Tab

le B

.1

(co

nti

nu

ed)

Tab

le B

.2

Pres

ent

valu

e o

f U

S$1

at ‘n

’ per

iod

PVFV

=+

()

1r

n

Peri

od

s(n

)1

%2

%3

%4

%5

%6

%7

%8

%9

%10

%11

%12

%13

%14

%15

%16

%17

%18

%19

%20

%

10.

9901

0.98

040.

9709

0.96

150.

9524

0.94

340.

9346

0.92

590.

9174

0.90

910.

9009

0.89

290.

8850

0.87

720.

8696

0.86

210.

8547

0.84

750.

8403

0.83

332

0.98

030.

9612

0.94

260.

9246

0.90

700.

8900

0.87

340.

8573

0.84

170.

8264

0.81

160.

7972

0.78

310.

7695

0.75

610.

7432

0.73

050.

7182

0.70

620.

6944

30.

9706

0.94

230.

9151

0.88

900.

8638

0.83

960.

8163

0.79

380.

7722

0.75

130.

7312

0.71

180.

6931

0.67

500.

6575

0.64

070.

6244

0.60

860.

5934

0.57

874

0.96

100.

9238

0.88

850.

8548

0.82

270.

7921

0.76

290.

7350

0.70

840.

6830

0.65

870.

6355

0.61

330.

5921

0.57

180.

5523

0.53

370.

5158

0.49

870.

4823

50.

9515

0.90

570.

8626

0.82

190.

7835

0.74

730.

7130

0.68

060.

6499

0.62

090.

5935

0.56

740.

5428

0.51

940.

4972

0.47

610.

4561

0.43

710.

4190

0.40

196

0.94

200.

8880

0.83

750.

7903

0.74

620.

7050

0.66

630.

6302

0.59

630.

5645

0.53

460.

5066

0.48

030.

4556

0.43

230.

4104

0.38

980.

3704

0.35

210.

3349

70.

9327

0.87

060.

8131

0.75

990.

7107

0.66

510.

6227

0.58

350.

5470

0.51

320.

4817

0.45

230.

4251

0.39

960.

3759

0.35

380.

3332

0.31

390.

2959

0.27

918

0.92

350.

8535

0.78

940.

7307

0.67

680.

6274

0.58

200.

5403

0.50

190.

4665

0.43

390.

4039

0.37

620.

3506

0.32

690.

3050

0.28

480.

2660

0.24

870.

2326

90.

9143

0.83

680.

7664

0.70

260.

6446

0.59

190.

5439

0.50

020.

4604

0.42

410.

3909

0.36

060.

3329

0.30

750.

2843

0.26

300.

2434

0.22

550.

2090

0.19

3810

0.90

530.

8203

0.74

410.

6756

0.61

390.

5584

0.50

830.

4632

0.42

240.

3855

0.35

220.

3220

0.29

460.

2697

0.24

720.

2267

0.20

800.

1911

0.17

560.

1615

110.

8963

0.80

430.

7224

0.64

960.

5847

0.52

680.

4751

0.42

890.

3875

0.35

050.

3173

0.28

750.

2607

0.23

660.

2149

0.19

540.

1778

0.16

190.

1476

0.13

4612

0.88

740.

7885

0.70

140.

6246

0.55

680.

4970

0.44

400.

3971

0.35

550.

3186

0.28

580.

2567

0.23

070.

2076

0.18

690.

1685

0.15

200.

1372

0.12

400.

1122

130.

8787

0.77

300.

6810

0.60

060.

5303

0.46

880.

4150

0.36

770.

3262

0.28

970.

2575

0.22

920.

2042

0.18

210.

1625

0.14

520.

1299

0.11

630.

1042

0.09

3514

0.87

000.

7579

0.66

110.

5775

0.50

510.

4423

0.38

780.

3405

0.29

920.

2633

0.23

200.

2046

0.18

070.

1597

0.14

130.

1252

0.11

100.

0985

0.08

760.

0779

150.

8613

0.74

300.

6419

0.55

530.

4810

0.41

730.

3624

0.31

520.

2745

0.23

940.

2090

0.18

270.

1599

0.14

010.

1229

0.10

790.

0949

0.08

350.

0736

0.06

4916

0.85

280.

7284

0.62

320.

5339

0.45

810.

3936

0.33

870.

2919

0.25

190.

2176

0.18

830.

1631

0.14

150.

1229

0.10

690.

0930

0.08

110.

0708

0.06

180.

0541

170.

8444

0.71

420.

6050

0.51

340.

4363

0.37

140.

3166

0.27

030.

2311

0.19

780.

1696

0.14

560.

1252

0.10

780.

0929

0.08

020.

0693

0.06

000.

0520

0.04

5118

0.83

600.

7002

0.58

740.

4936

0.41

550.

3503

0.29

590.

2502

0.21

200.

1799

0.15

280.

1300

0.11

080.

0946

0.08

080.

0691

0.05

920.

0508

0.04

370.

0376

190.

8277

0.68

640.

5703

0.47

460.

3957

0.33

050.

2765

0.23

170.

1945

0.16

350.

1377

0.11

610.

0981

0.08

290.

0703

0.05

960.

0506

0.04

310.

0367

0.03

1320

0.81

950.

6730

0.55

370.

4564

0.37

690.

3118

0.25

840.

2145

0.17

840.

1486

0.12

400.

1037

0.08

680.

0728

0.06

110.

0514

0.04

330.

0365

0.03

080.

0261

210.

8114

0.65

980.

5375

0.43

880.

3589

0.29

420.

2415

0.19

870.

1637

0.13

510.

1117

0.09

260.

0768

0.06

380.

0531

0.04

430.

0370

0.03

090.

0259

0.02

1722

0.80

340.

6468

0.52

190.

4220

0.34

180.

2775

0.22

570.

1839

0.15

020.

1228

0.10

070.

0826

0.06

800.

0560

0.04

620.

0382

0.03

160.

0262

0.02

180.

0181

230.

7954

0.63

420.

5067

0.40

570.

3256

0.26

180.

2109

0.17

030.

1378

0.11

170.

0907

0.07

380.

0601

0.04

910.

0402

0.03

290.

0270

0.02

220.

0183

0.01

5124

0.78

760.

6217

0.49

190.

3901

0.31

010.

2470

0.19

710.

1577

0.12

640.

1015

0.08

170.

0659

0.05

320.

0431

0.03

490.

0284

0.02

310.

0188

0.01

540.

0126

250.

7798

0.60

950.

4776

0.37

510.

2953

0.23

300.

1842

0.14

600.

1160

0.09

230.

0736

0.05

880.

0471

0.03

780.

0304

0.02

450.

0197

0.01

600.

0129

0.01

0526

0.77

200.

5976

0.46

370.

3607

0.28

120.

2198

0.17

220.

1352

0.10

640.

0839

0.06

630.

0525

0.04

170.

0331

0.02

640.

0211

0.01

690.

0135

0.01

090.

0087

270.

7644

0.58

590.

4502

0.34

680.

2678

0.20

740.

1609

0.12

520.

0976

0.07

630.

0597

0.04

690.

0369

0.02

910.

0230

0.01

820.

0144

0.01

150.

0091

0.00

73

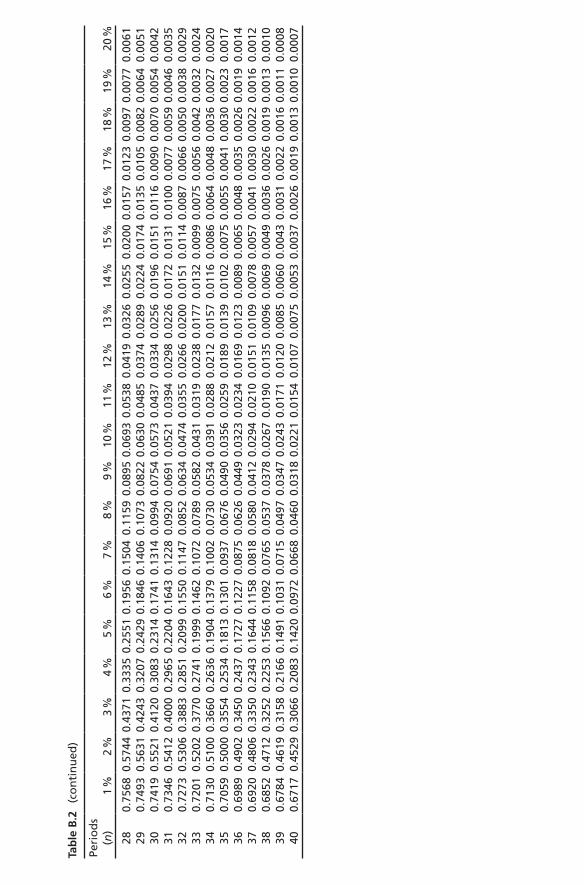

(co

nti

nu

ed )

Peri

od

s(n

)1

%2

%3

%4

%5

%6

%7

%8

%9

%10

%11

%12

%13

%14

%15

%16

%17

%18

%19

%20

%

280.

7568

0.57

440.

4371

0.33

350.

2551

0.19

560.

1504

0.11

590.

0895

0.06

930.

0538

0.04

190.

0326

0.02

550.

0200

0.01

570.

0123

0.00

970.

0077

0.00

6129

0.74

930.

5631

0.42

430.

3207

0.24

290.

1846

0.14

060.

1073

0.08

220.

0630

0.04

850.

0374

0.02

890.

0224

0.01

740.

0135

0.01

050.

0082

0.00

640.

0051

300.

7419

0.55

210.

4120

0.30

830.

2314

0.17

410.

1314

0.09

940.

0754

0.05

730.

0437

0.03

340.

0256

0.01

960.

0151

0.01

160.

0090

0.00

700.

0054

0.00

4231

0.73

460.

5412

0.40

000.

2965

0.22

040.

1643

0.12

280.

0920

0.06

910.

0521

0.03

940.

0298

0.02

260.

0172

0.01

310.

0100

0.00

770.

0059

0.00

460.

0035

320.

7273

0.53

060.

3883

0.28

510.

2099

0.15

500.

1147

0.08

520.

0634

0.04

740.

0355

0.02

660.

0200

0.01

510.

0114

0.00

870.

0066

0.00

500.

0038

0.00

2933

0.72

010.

5202

0.37

700.

2741

0.19

990.

1462

0.10

720.

0789

0.05

820.

0431

0.03

190.

0238

0.01

770.

0132

0.00

990.

0075

0.00

560.

0042

0.00

320.

0024

340.

7130

0.51

000.

3660

0.26

360.

1904

0.13

790.

1002

0.07

300.

0534

0.03

910.

0288

0.02

120.

0157

0.01

160.

0086

0.00

640.

0048

0.00

360.

0027

0.00

2035

0.70

590.

5000

0.35

540.

2534

0.18

130.

1301

0.09

370.

0676

0.04

900.

0356

0.02

590.

0189

0.01

390.

0102

0.00

750.

0055

0.00

410.

0030

0.00

230.

0017

360.

6989

0.49

020.

3450

0.24

370.

1727

0.12

270.

0875

0.06

260.

0449

0.03

230.

0234

0.01

690.

0123

0.00

890.

0065

0.00

480.

0035

0.00

260.

0019

0.00

1437

0.69

200.

4806

0.33

500.

2343

0.16

440.

1158

0.08

180.

0580

0.04

120.

0294

0.02

100.

0151

0.01

090.

0078

0.00

570.

0041

0.00

300.

0022

0.00

160.

0012

380.

6852

0.47

120.

3252

0.22

530.

1566

0.10

920.

0765

0.05

370.

0378

0.02

670.

0190

0.01

350.

0096

0.00

690.

0049

0.00

360.

0026

0.00

190.

0013

0.00

1039

0.67

840.

4619

0.31

580.

2166

0.14

910.

1031

0.07

150.

0497

0.03

470.

0243

0.01

710.

0120

0.00

850.

0060

0.00

430.

0031

0.00

220.

0016

0.00

110.

0008

400.

6717

0.45

290.

3066

0.20

830.

1420

0.09

720.

0668

0.04

600.

0318

0.02

210.

0154

0.01

070.

0075

0.00

530.

0037

0.00

260.

0019

0.00

130.

0010

0.00

07

Tab

le B

.2

(co

nti

nu

ed)

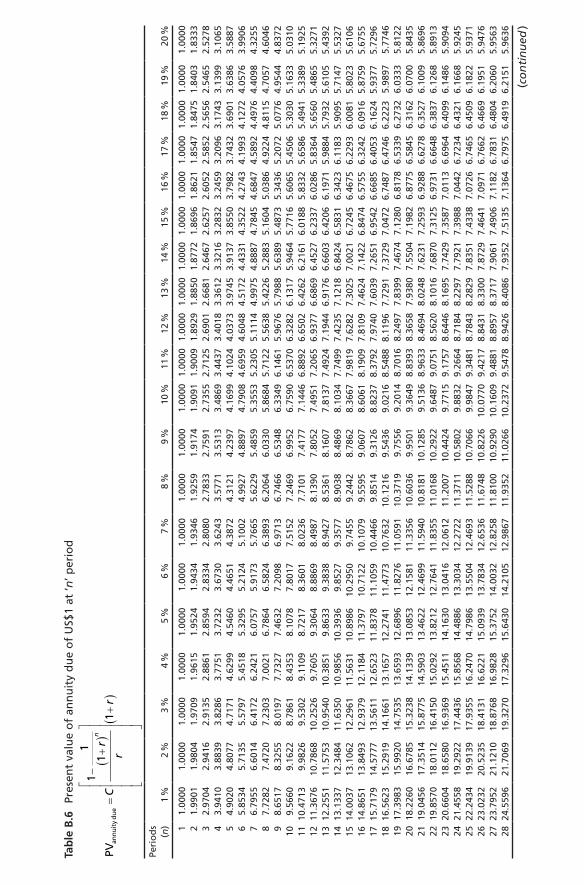

Tab

le B

.3

Futu

re v

alu

e o

f an

ord

inar

y an

nu

ity

of

US$

1 at

‘n’ p

erio

d

FVordinaryan

nuity=

+(

)−

C

r r

n1

1

Peri

ods

(n)

1.0

%2.

0 %

3.0

%4.

0 %

5.0

%6.

0 %

7.0

%8.

0 %

9.0

%10

.0 %

11.0

%12

.0 %

13.0

%14

.0 %

15.0

%16

.0 %

17.0

%18

.0 %

19.0

%20

.0 %

11.

0000

1.00

001.

0000

1.00

001.

0000

1.00

001.

0000

1.00

001.

0000

1.00

001.

0000

1.00

001.

0000

1.00

001.

0000

1.00

001.

0000

1.00

001.

0000

1.00

002

2.01

002.

0200

2.03

002.

0400

2.05

002.

0600

2.07

002.

0800

2.09

002.

1000

2.12

002.

1200

2.14

002.

1400

2.15

002.

1600

2.17

002.

1800

2.19

002.

2000

33.

0301

3.06

043.

0909

3.12

163.

1525

3.18

363.

2149

3.24

643.

2781

3.31

003.

3744

3.37

443.

4396

3.43

963.

4725

3.50

563.

5389

3.57

243.

6061

3.64

004

4.06

044.

1216

4.18

364.

2465

4.31

014.

3746

4.43

994.

5061

4.57

314.

6410

4.77

934.

7793

4.92

114.

9211

4.99

345.

0665

5.14

055.

2154

5.29

135.

3680

55.

1010

5.20

405.

3091

5.41

635.

5256

5.63

715.

7507

5.86

665.

9847

6.10

516.

3528

6.35

286.

6101

6.61

016.

7424

6.87

717.

0144

7.15

427.

2966

7.44

166

6.15

206.

3081

6.46

846.

6330

6.80

196.

9753

7.15

337.

3359

7.52

337.

7156

8.11

528.

1152

8.53

558.

5355

8.75

378.

9775

9.20

689.

4420

9.68

309.

9299

77.

2135

7.43

437.

6625

7.89

838.

1420

8.39

388.

6540

8.92

289.

2004

9.48

7210

.089

010

.089

010

.730

510

.730

511

.066

811

.413

911

.772

012

.141

512

.522

712

.915

98

8.28

578.

5830

8.89

239.

2142

9.54

919.

8975

10.2

598

10.6

366

11.0

285

11.4

359

12.2

997

12.2

997

13.2

328

13.2

328

13.7

268

14.2

401

14.7

733

15.3

270

15.9

020

16.4

991

99.

3685

9.75

4610

.159

110

.582

811

.026

611

.491

311

.978

012

.487

613

.021

013

.579

514

.775

714

.775

716

.085

316

.085

316

.785

817

.518

518

.284

719

.085

919

.923

420

.798

910

10.4

622

10.9

497

11.4

639

12.0

061

12.5

779

13.1

808

13.8

164

14.4

866

15.1

929

15.9

374

17.5

487

17.5

487

19.3

373

19.3

373

20.3

037

21.3

215

22.3

931

23.5

213

24.7

089

25.9

587

1111

.566

812

.168

712

.807

813

.486

414

.206

814

.971

615

.783

616

.645

517

.560

318

.531

220

.654

620

.654

623

.044

523

.044

524

.349

325

.732

927

.199

928

.755

130

.403

532

.150

412

12.6

825

13.4

121

14.1

920

15.0

258

15.9

171

16.8

699

17.8

885

18.9

771

20.1

407

21.3

843

24.1

331

24.1

331

27.2

707

27.2

707

29.0

017

30.8

502

32.8

239

34.9

311

37.1

802

39.5

805

1313

.809

314

.680

315

.617

816

.626

817

.713

018

.882

120

.140

621

.495

322

.953

424

.522

728

.029

128

.029

132

.088

732

.088

734

.351

936

.786

239

.404

042

.218

745

.244

548

.496

614

14.9

474

15.9

739

17.0

863

18.2

919

19.5

986

21.0

151

22.5

505

24.2

149

26.0

192

27.9

750

32.3

926

32.3

926

37.5

811

37.5

811

40.5

047

43.6

720

47.1

027

50.8

180

54.8

409

59.1

959

1516

.096

917

.293

418

.598

920

.023

621

.578

623

.276

025

.129

027

.152

129

.360

931

.772

537

.279

737

.279

743

.842

443

.842

447

.580

451

.659

556

.110

160

.965

366

.260

772

.035

116

17.2

579

18.6

393

20.1

569

21.8

245

23.6

575

25.6

725

27.8

881

30.3

243

33.0

034

35.9

497

42.7

533

42.7

533

50.9

804

50.9

804

55.7

175

60.9

250

66.6

488

72.9

390

79.8

502

87.4

421

1718

.430

420

.012

121

.761

623

.697

525

.840

428

.212

930

.840

233

.750

236

.973

740

.544

748

.883

748

.883

759

.117

659

.117

665

.075

171

.673

078

.979

287

.068

096

.021

810

5.93

0618

19.6

147

21.4

123

23.4

144

25.6

454

28.1

324

30.9

057

33.9

990

37.4

502

41.3

013

45.5

992

55.7

497

55.7

497

68.3

941

68.3

941

75.8

364

84.1

407

93.4

056

103.

7403

115.

2659

128.

1167

1920

.810

922

.840

625

.116

927

.671

230

.539

033

.760

037

.379

041

.446

346

.018

551

.159

163

.439

763

.439

778

.969

278

.969

288

.211

898

.603

211

0.28

4612

3.41

3513

8.16

6415

4.74

0020

22.0

190

24.2

974

26.8

704

29.7

781

33.0

660

36.7

856

40.9

955

45.7

620

51.1

601

57.2

750

72.0

524

72.0

524

91.0

249

91.0

249

102.

4436

115.

3797

130.

0329

146.

6280

165.

4180

186.

6880

2123

.239

225

.783

328

.676

531

.969

235

.719

339

.992

744

.865

250

.422

956

.764

564

.002

581

.698

781

.698

710

4.76

8410

4.76

8411

8.81

0113

4.84

0515

3.13

8517

4.02

1019

7.84

7422

5.02

5622

24.4

716

27.2

990

30.5

368

34.2

480

38.5

052

43.3

923

49.0

057

55.4

568

62.8

733

71.4

027

92.5

026

92.5

026

120.

4360

120.

4360

137.

6316

157.

4150

180.

1721

206.

3448

236.

4385

271.

0307

2325

.716

328

.845

032

.452

936

.617

941

.430

546

.995

853

.436

160

.893

369

.531

979

.543

010

4.60

2910

4.60

2913

8.29

7013

8.29

7015

9.27

6418

3.60

1421

1.80

1324

4.48

6828

2.36

1832

6.23

6924

26.9

735

30.4

219

34.4

265

39.0

826

44.5

020

50.8

156

58.1

767

66.7

648

76.7

898

88.4

973

118.

1552

118.

1552

158.

6586

158.

6586

184.

1678

213.

9776

248.

8076

289.

4945

337.

0105

392.

4842

2528

.243

232

.030

336

.459

341

.645

947

.727

154

.864

563

.249

073

.105

984

.700

998

.347

113

3.33

3913

3.33

3918

1.87

0818

1.87

0821

2.79

3024

9.21

4029

2.10

4934

2.60

3540

2.04

2547

1.98

1126

29.5

256

33.6

709

38.5

530

44.3

117

51.1

135

59.1

564

68.6

765

79.9

544

93.3

240

109.

1818

150.

3339

150.

3339

208.

3327

208.

3327

245.

7120

290.

0883

342.

7627

405.

2721

479.

4306

567.

3773

2730

.820

935

.344

340

.709

647

.084

254

.669

163

.705

874

.483

887

.350

810

2.72

3112

1.09

9916

9.37

4016

9.37

4023

8.49

9323

8.49

9328

3.56

8833

7.50

2440

2.03

2347

9.22

1157

1.52

2468

1.85

2828

32.1

291

37.0

512

42.9

309

49.9

676

58.4

026

68.5

281

80.6

977

95.3

388

112.

9682

134.

2099

190.

6989

190.

6989

272.

8892

272.

8892

327.

1041

392.

5028

471.

3778

566.

4809

681.

1116

819.

2233

2933

.450

438

.792

245

.218

952

.966

362

.322

773

.639

887

.346

510

3.96

5912

4.13

5414

8.63

0921

4.58

2821

4.58

2831

2.09

3731

2.09

3737

7.16

9745

6.30

3255

2.51

2166

9.44

7581

1.52

2898

4.06

8030

34.7

849

40.5

681

47.5

754

56.0

849

66.4

388

79.0

582

94.4

608

113.

2832

136.

3075

164.

4940

241.

3327

241.

3327

356.

7868

356.

7868

434.

7451

530.

3117

647.

4391

790.

9480

966.

7122

1181

.881

631

36.1

327

42.3

794

50.0

027

59.3

283

70.7

608

84.8

017

102.

0730

123.

3459

149.

5752

181.

9434

271.

2926

271.

2926

407.

7370

407.

7370

500.

9569

616.

1616

758.

5038

934.

3186

1151

.387

514

19.2

579

3237

.494

144

.227

052

.502

862

.701

575

.298

890

.889

811

0.21

8213

4.21

3516

4.03

7020

1.13

7830

4.84

7730

4.84

7746

5.82

0246

5.82

0257

7.10

0571

5.74

7588

8.44

9411

03.4

960

1371

.151

117

04.1

095

3338

.869

046

.111

655

.077

866

.209

580

.063

897

.343

211

8.93

3414

5.95

0617

9.80

0322

2.25

1534

2.42

9434

2.42

9453

2.03

5053

2.03

5066

4.66

5583

1.26

7110

40.4

858

1303

.125

316

32.6

698

2045

.931

4

(co

nti

nu

ed )

Peri

ods

(n)

1.0

%2.

0 %

3.0

%4.

0 %

5.0

%6.

0 %

7.0

%8.

0 %

9.0

%10

.0 %

11.0

%12

.0 %

13.0

%14

.0 %

15.0

%16

.0 %

17.0

%18

.0 %

19.0

%20

.0 %

3440

.257

748

.033

857

.730

269

.857

985

.067

010

4.18

3812

8.25

8815

8.62

6719

6.98

2324

5.47

6738

4.52

1038

4.52

1060

7.51

9960

7.51

9976

5.36

5496

5.26

9812

18.3

684

1538

.687

819

43.8

771

2456

.117

635

41.6

603

49.9

945

60.4

621

73.6

522

90.3

203

111.

4348

138.

2369

172.

3168

215.

7108

271.

0244

431.

6635

431.

6635

693.

5727

693.

5727

881.

1702

1120

.713

014

26.4

910

1816

.651

623

14.2

137

2948

.341

136

43.0

769

51.9

944

63.2

759

77.5

983

95.8

363

119.

1209

148.

9135

187.

1021

236.

1247

299.

1268

484.

4631

484.

4631

791.

6729

791.

6729

1014

.345

713

01.0

270

1669

.994

521

44.6

489

2754

.914

335

39.0

094

3744

.507

654

.034

366

.174

281

.702

210

1.62

8112

7.26

8116

0.33

7420

3.07

0325

8.37

5933

0.03

9554

3.59

8754

3.59

8790

3.50

7190

3.50

7111

67.4

975

1510

.191

419

54.8

936

2531

.685

732

79.3

481

4247

.811

238

45.9

527

56.1

149

69.1

594

85.9

703

107.

7095

135.

9042

172.

5610

220.

3159

282.

6298

364.

0434

609.

8305

609.

8305

1030

.998

110

30.9

981

1343

.622

217

52.8

220

2288

.225

529

88.3

891

3903

.424

250

98.3

735

3947

.412

358

.237

272

.234

290

.409

111

4.09

5014

5.05

8518

5.64

0323

8.94

1230

9.06

6540

1.44

7868

4.01

0268

4.01

0211

76.3

378

1176

.337

815

46.1

655

2034

.273

526

78.2

238

3527

.299

246

46.0

748

6119

.048

240

48.8

864

60.4

020

75.4

013

95.0

255

120.

7998

154.

7620

199.

6351

259.

0565

337.

8824

442.

5926

767.

0914

767.

0914

1342

.025

113

42.0

251

1779

.090

323

60.7

572

3134

.521

841

63.2

130

5529

.829

073

43.8

578

Tab

le B

.3

(co

nti

nu

ed)

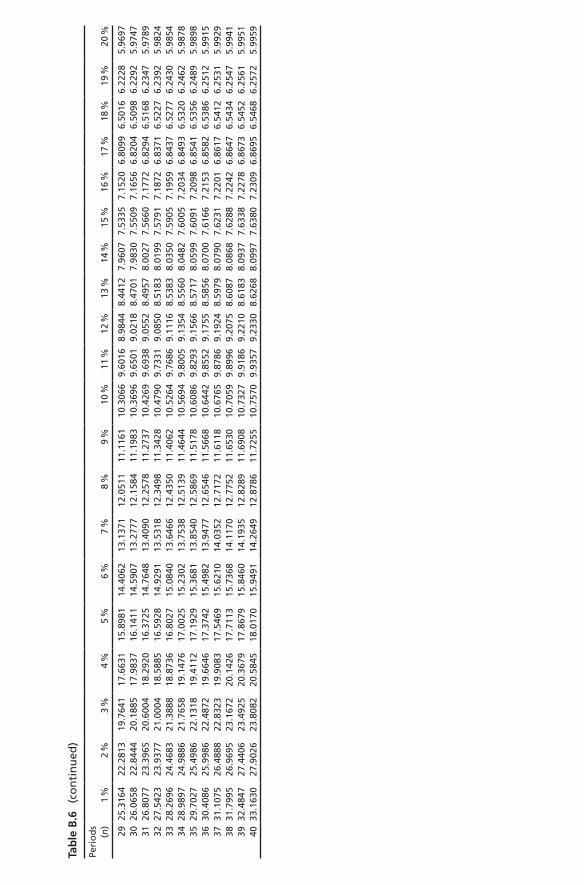

Tab

le B

.4

Futu

re v

alu

e o

f an

an

nu

ity

du

e o

f U

S$1

at ‘n

’ per

iod

FVan

nuitydue=

+(

)−

+

()

Cr r

rn

11

1

Peri

ods

(n)

1 %

2 %

3 %

4 %

5 %

6 %

7 %

8 %

9 %

10 %

11 %

12 %

13 %

14 %

15 %

16 %

17 %

18 %

19 %

20 %

11.

0100

1.02

001.

0300

1.04

001.

0500

1.06

001.

0700

1.08

001.

0900

1.10

001.

1100

1.12

001.

1300

1.14

001.

1500

1.16

001.

1700

1.18

001.

1900

1.20

002

2.03

012.

0604

2.09

092.

1216

2.15

252.

1836

2.21

492.

2464

2.27

812.

3100

2.34

212.

3744

2.40

692.

4396

2.47

252.

5056

2.53

892.

5724

2.60

612.

6400

33.

0604

3.12

163.

1836

3.24

653.

3101

3.37

463.

4399

3.50

613.

5731

3.64

103.

7097

3.77

933.

8498

3.92

113.

9934

4.06

654.

1405

4.21

544.

2913

4.36

804

4.10

104.

2040

4.30

914.

4163

4.52

564.

6371

4.75

074.

8666

4.98

475.

1051

5.22

785.

3528

5.48

035.

6101

5.74

245.

8771

6.01

446.

1542

6.29

666.

4416

55.

1520

5.30

815.

4684

5.63

305.

8019

5.97

536.

1533

6.33

596.

5233

6.71

566.

9129

7.11

527.

3227

7.53

557.

7537

7.97

758.

2068

8.44

208.

6830

8.92

996

6.21

356.

4343

6.66

256.

8983

7.14

207.

3938

7.65

407.

9228

8.20

048.

4872

8.78

339.

0890

9.40

479.

7305

10.0

668

10.4

139

10.7

720

11.1

415

11.5

227

11.9

159

77.

2857

7.58

307.

8923

8.21

428.

5491

8.89

759.

2598

9.63

6610

.028

510

.435

910

.859

411

.299

711

.757

312

.232

812

.726

813

.240

113

.773

314

.327

014

.902

015

.499

18

8.36

858.

7546

9.15

919.

5828

10.0

266

10.4

913

10.9

780

11.4

876

12.0

210

12.5

795

13.1

640

13.7

757

14.4

157

15.0

853

15.7

858

16.5

185

17.2

847

18.0

859

18.9

234

19.7

989

99.

4622

9.94

9710

.463

911

.006

111

.577

912

.180

812

.816

413

.486

614

.192

914

.937

415

.722

016

.548

717

.419

718

.337

319

.303

720

.321

521

.393

122

.521

323

.708

924

.958

710

10.5

668

11.1

687

11.8

078

12.4

864

13.2

068

13.9

716

14.7

836

15.6

455

16.5

603

17.5

312

18.5

614

19.6

546

20.8

143

22.0

445

23.3

493

24.7

329

26.1

999

27.7

551

29.4

035

31.1

504

1111

.682

512

.412

113

.192

014

.025

814

.917

115

.869

916

.888

517

.977

119

.140

720

.384

321

.713

223

.133

124

.650

226

.270

728

.001

729

.850

231

.823

933

.931

136

.180

238

.580

512

12.8

093

13.6

803

14.6

178

15.6

268

16.7

130

17.8

821

19.1

406

20.4

953

21.9

534

23.5

227

25.2

116

27.0

291

28.9

847

31.0

887

33.3

519

35.7

862

38.4

040

41.2

187

44.2

445

47.4

966

1313

.947

414

.973

916

.086

317

.291

918

.598

620

.015

121

.550

523

.214

925

.019

226

.975

029

.094

931

.392

633

.882

736

.581

139

.504

742

.672

046

.102

749

.818

053

.840

958

.195

914

15.0

969

16.2

934

17.5

989

19.0

236

20.5

786

22.2

760

24.1

290

26.1

521

28.3

609

30.7

725

33.4

054

36.2

797

39.4

175

42.8

424

46.5

804

50.6

595

55.1

101

59.9

653

65.2

607

71.0

351

1516

.257

917

.639

319

.156

920

.824

522

.657

524

.672

526

.888

129

.324

332

.003

434

.949

738

.189

941

.753

345

.671

749

.980

454

.717

559

.925

065

.648

871

.939

078

.850

286

.442

116

17.4

304

19.0

121

20.7

616

22.6

975

24.8

404

27.2

129

29.8

402

32.7

502

35.9

737

39.5

447

43.5

008

47.8

837

52.7

391

58.1

176

64.0

751

70.6

730

77.9

792

86.0

680

95.0

218

104.

9306

1718

.614

720

.412

322

.414

424

.645

427

.132

429

.905

732

.999

036

.450

240

.301

344

.599

249

.395

954

.749

760

.725

167

.394

174

.836

483

.140

792

.405

610

2.74

0311

4.26

5912

7.11

6718

19.8

109

21.8

406

24.1

169

26.6

712

29.5

390

32.7

600

36.3

790

40.4

463

45.0

185

50.1

591

55.9

395

62.4

397

69.7

494

77.9

692

87.2

118

97.6

032

109.

2846

122.

4135

137.

1664

153.

7400

1921

.019

023

.297

425

.870

428

.778

132

.066

035

.785

639

.995

544

.762

050

.160

156

.275

063

.202

871

.052

479

.946

890

.024

910

1.44

3611

4.37

9712

9.03

2914

5.62

8016

4.41

8018

5.68

8020

22.2

392

24.7

833

27.6

765

30.9

692

34.7

193

38.9

927

43.8

652

49.4

229

55.7

645

63.0

025

71.2

651

80.6

987

91.4

699

103.

7684

117.

8101

133.

8405

152.

1385

173.

0210

196.

8474

224.

0256

2123

.471

626

.299

029

.536

833

.248

037

.505

242

.392

348

.005

754

.456

861

.873

370

.402

780

.214

391

.502

610

4.49

1011

9.43

6013

6.63

1615

6.41

5017

9.17

2120

5.34

4823

5.43

8527

0.03

0722

24.7

163

27.8

450

31.4

529

35.6

179

40.4

305

45.9

958

52.4

361

59.8

933

68.5

319

78.5

430

90.1

479

103.

6029

119.

2048

137.

2970

158.

2764

182.

6014

210.

8013

243.

4868

281.

3618

325.

2369

2325

.973

529

.421

933

.426

538

.082

643

.502

049

.815

657

.176

765

.764

875

.789

887

.497

310

1.17

4211

7.15

5213

5.83

1515

7.65

8618

3.16

7821

2.97

7624

7.80

7628

8.49

4533

6.01

0539

1.48

4224

27.2

432

31.0

303

35.4

593

40.6

459

46.7

271

53.8

645

62.2

490

72.1

059

83.7

009

97.3

471

113.

4133

132.

3339

154.

6196

180.

8708

211.

7930

248.

2140

291.

1049

341.

6035

401.

0425

470.

9811

2528

.525

632

.670

937

.553

043

.311

750

.113

558

.156

467

.676

578

.954

492

.324

010

8.18

1812

6.99

8814

9.33

3917

5.85

0120

7.33

2724

4.71

2028

9.08

8334

1.76

2740

4.27

2147

8.43

0656

6.37

7326

29.8

209

34.3

443

39.7

096

46.0

842

53.6

691

62.7

058

73.4

838

86.3

508

101.

7231

120.

0999

142.

0786

168.

3740

199.

8406

237.

4993

282.

5688

336.

5024

401.

0323

478.

2211

570.

5224

680.

8528

2731

.129

136

.051

241

.930

948

.967

657

.402

667

.528

179

.697

794

.338

811

1.96

8213

3.20

9915

8.81

7318

9.69

8922

6.94

9927

1.88

9232

6.10

4139

1.50

2847

0.37

7856

5.48

0968

0.11

1681

8.22

3328

32.4

504

37.7

922

44.2

189

51.9

663

61.3

227

72.6

398

86.3

465

102.

9659

123.

1354

147.

6309

177.

3972

213.

5828

257.

5834

311.

0937

376.

1697

455.

3032

551.

5121

668.

4475

810.

5228

983.

0680

2933

.784

939

.568

146

.575

455

.084

965

.438

878

.058

293

.460

811

2.28

3213

5.30

7516

3.49

4019

8.02

0924

0.33

2729

2.19

9235

5.78

6843

3.74

5152

9.31

1764

6.43

9178

9.94

8096

5.71

2211

80.8

816

3035

.132

741

.379

449

.002

758

.328

369

.760

883

.801

710

1.07

3012

2.34

5914

8.57

5218

0.94

3422

0.91

3227

0.29

2633

1.31

5140

6.73

7049

9.95

6961

5.16

1675

7.50

3893

3.31

8611

50.3

875

1418

.257

931

36.4

941

43.2

270

51.5

028

61.7

015

74.2

988

89.8

898

109.

2182

133.

2135

163.

0370

200.

1378

246.

3236

303.

8477

375.

5161

464.

8202

576.

1005

714.

7475

887.

4494

1102

.496

013

70.1

511

1703

.109

532

37.8

690

45.1

116

54.0

778

65.2

095

79.0

638

96.3

432

117.

9334

144.

9506

178.

8003

221.

2515

274.

5292

341.

4294

425.

4632

531.

0350

663.

6655

830.

2671

1039

.485

813

02.1

253

1631

.669

820

44.9

314

3339

.257

747

.033

856

.730

268

.857

984

.067

010

3.18

3812

7.25

8815

7.62

6719

5.98

2324

4.47

6730

5.83

7438

3.52

1048

1.90

3460

6.51

9976

4.36

5496

4.26

9812

17.3

684

1537

.687

819

42.8

771

2455

.117

634

40.6

603

48.9

945

59.4

621

72.6

522

89.3

203

110.

4348

137.

2369

171.

3168

214.

7108

270.

0244

340.

5896

430.

6635

545.

6808

692.

5727

880.

1702

1119

.713

014

25.4

910

1815

.651

623

13.2

137

2947

.341

1

(co

nti

nu

ed )

Peri

ods

(n)

1 %

2 %

3 %

4 %

5 %

6 %

7 %

8 %

9 %

10 %

11 %

12 %

13 %

14 %

15 %

16 %

17 %

18 %

19 %

20 %

3542

.076

950

.994

462

.275

976

.598

394

.836

311

8.12

0914

7.91

3518

6.10

2123

5.12

4729

8.12

6837

9.16

4448

3.46

3161

7.74

9379

0.67

2910

13.3

457

1300

.027

016

68.9

945

2143

.648

927

53.9

143

3538

.009

436

43.5

076

53.0

343

65.1

742

80.7

022

100.

6281

126.

2681

159.

3374

202.

0703

257.

3759

329.

0395

421.

9825

542.

5987

699.

1867

902.

5071

1166

.497

515

09.1

914

1953

.893

625

30.6

857

3278

.348

142

46.8

112

3744

.952

755

.114

968

.159

484

.970

310

6.70

9513

4.90

4217

1.56

1021

9.31

5928

1.62

9836

3.04

3446

9.51

0660

8.83

0579

1.21

1010

29.9

981

1342

.622

217

51.8

220

2287

.225

529

87.3

891

3902

.424

250

97.3

735

3846

.412

357

.237

271

.234

289

.409

111

3.09

5014

4.05

8518

4.64

0323

7.94

1230

8.06

6540

0.44

7852

2.26

6768

3.01

0289

5.19

8411

75.3

378

1545

.165

520

33.2

735

2677

.223

835

26.2

992

4645

.074

861

18.0

482

3947

.886

459

.402

074

.401

394

.025

511

9.79

9815

3.76

2019

8.63

5125

8.05

6533

6.88

2444

1.59

2658

0.82

6176

6.09

1410

12.7

042

1341

.025

117

78.0

903

2359

.757

231

33.5

218

4162

.213

055

28.8

290

7342

.857

840

49.3

752

61.6

100

77.6

633

98.8

265

126.

8398

164.

0477

213.

6096

279.

7810

368.

2919

486.

8518

645.

8269

859.

1424

1145

.485

815

29.9

086

2045

.953

927

38.4

784

3667

.390

649

12.5

914

6580

.496

588

12.6

294

Tab

le B

.4

(co

nti

nu

ed)

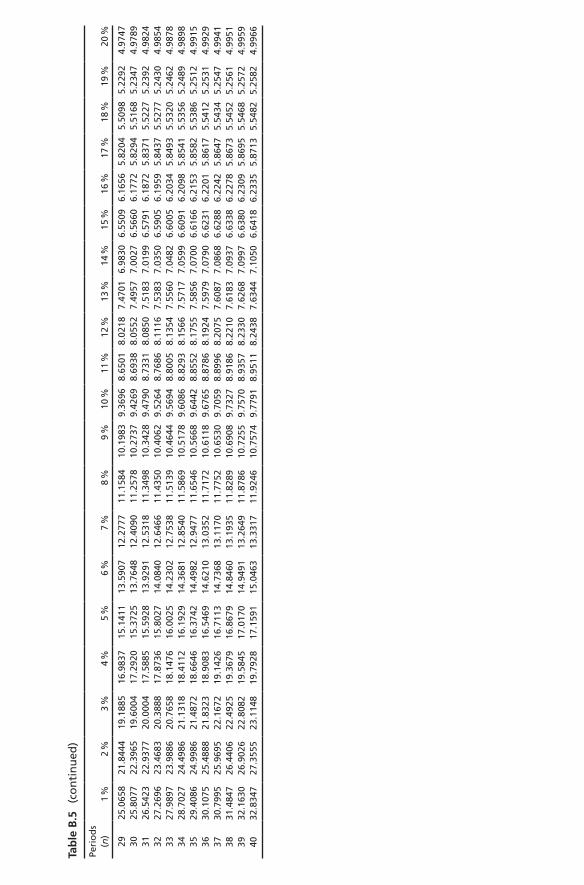

Tab

le B

.5

Pres

ent

valu

e o

f an

ord

inar

y an

nu

ity

of

US$

1 at

‘n’ p

erio

d

PVordinaryan

nuity=

−+

()

Cr

r

n1

1

1

Peri

od

s(n

)1

%2

%3

%4

%5

%6

%7

%8

%9

%10

%11

%12

%13

%14

%15

%16

%17

%18

%19

%20

%

10.

9901

0.98

040.

9709

0.96

150.

9524

0.94

340.

9346

0.92

590.

9174

0.90

910.

9009

0.89

290.

8850

0.87

720.

8696

0.86

210.

8547

0.84

750.

8403

0.83

332

1.97

041.

9416

1.91

351.

8861

1.85

941.

8334

1.80

801.

7833

1.75

911.

7355

1.71

251.

6901

1.66

811.

6467

1.62

571.

6052

1.58

521.

5656

1.54

651.

5278

32.

9410

2.88

392.

8286

2.77

512.

7232

2.67

302.

6243

2.57

712.

5313

2.48

692.

4437

2.40

182.

3612

2.32

162.

2832

2.24

592.

2096

2.17

432.

1399

2.10

654

3.90

203.

8077

3.71

713.

6299

3.54

603.

4651

3.38

723.

3121

3.23

973.

1699

3.10

243.

0373

2.97

452.

9137

2.85

502.

7982

2.74

322.

6901

2.63

862.

5887

54.

8534

4.71

354.

5797

4.45

184.

3295

4.21

244.

1002

3.99

273.

8897

3.79

083.

6959

3.60

483.

5172

3.43

313.

3522

3.27

433.

1993

3.12

723.

0576

2.99

066

5.79

555.

6014

5.41

725.

2421

5.07

574.

9173

4.76

654.

6229

4.48

594.

3553

4.23

054.

1114

3.99

753.

8887

3.78

453.

6847

3.58

923.

4976

3.40

983.

3255

76.

7282

6.47

206.

2303

6.00

215.

7864

5.58

245.

3893

5.20

645.

0330

4.86

844.

7122

4.56

384.

4226

4.28

834.

1604

4.03

863.

9224

3.81

153.

7057

3.60

468

7.65

177.

3255

7.01

976.

7327

6.46

326.

2098

5.97

135.

7466

5.53

485.

3349

5.14

614.

9676

4.79

884.

6389

4.48

734.

3436

4.20

724.

0776

3.95

443.

8372

98.

5660

8.16

227.

7861

7.43

537.

1078

6.80

176.

5152

6.24

695.

9952

5.75

905.

5370

5.32

825.

1317

4.94

644.

7716

4.60

654.

4506

4.30

304.

1633

4.03

1010

9.47

138.

9826

8.53

028.

1109

7.72

177.

3601

7.02

366.

7101

6.41

776.

1446

5.88

925.

6502

5.42

625.

2161

5.01

884.

8332

4.65

864.

4941

4.33

894.

1925

1110

.367

69.

7868

9.25

268.

7605

8.30

647.

8869

7.49

877.

1390

6.80

526.

4951

6.20

655.

9377

5.68

695.

4527

5.23

375.

0286

4.83

644.

6560

4.48

654.

3271

1211

.255

110

.575

39.

9540

9.38

518.

8633

8.38

387.

9427

7.53

617.

1607

6.81

376.

4924

6.19

445.

9176

5.66

035.

4206

5.19

714.

9884

4.79

324.

6105

4.43

9213

12.1

337

11.3

484

10.6

350

9.98

569.

3936

8.85

278.

3577

7.90

387.

4869

7.10

346.

7499

6.42

356.

1218

5.84

245.

5831

5.34

235.

1183

4.90

954.

7147

4.53

2714

13.0

037

12.1

062

11.2

961

10.5

631

9.89

869.

2950

8.74

558.

2442

7.78

627.

3667

6.98

196.

6282

6.30

256.

0021

5.72

455.

4675

5.22

935.

0081

4.80

234.

6106

1513

.865

112

.849

311

.937

911

.118

410

.379

79.

7122

9.10

798.

5595

8.06

077.

6061

7.19

096.

8109

6.46

246.

1422

5.84

745.

5755

5.32

425.

0916

4.87

594.

6755

1614

.717

913

.577

712

.561

111

.652

310

.837

810

.105

99.

4466

8.85

148.

3126

7.82

377.

3792

6.97

406.

6039

6.26

515.

9542

5.66

855.

4053

5.16

244.

9377

4.72

9617

15.5

623

14.2

919

13.1

661

12.1

657

11.2

741

10.4

773

9.76

329.

1216

8.54

368.

0216