an east asian monetary union: china included?

TRANSCRIPT

The Economics of China 01/09/2013

KATHOLIEKE UNIVERSITEIT LEUVEN

An East Asian Monetary Union: China Included?

Abstract:

This paper discusses the feasibility of China’s inclusion in an East Asian monetary union. A

broad-based empirical analysis is used to determine whether China satisfies the three classic

economic Optimum Currency Area (OCA) criteria. The group of countries that is selected for

analysis includes China and the ASEAN4 (Indonesia, Malaysia, the Philippines and

Thailand). The research results indicate that China is not yet ready for monetary integration

because it has underdeveloped money and capital markets, its economy is still relatively

closed for trade, its exports are not very diversified and trade intensity with the ASEAN4

countries is only limited. Nonetheless, some recent developments such as the China-ASEAN

Free Trade Agreement and China’s rapidly improving stage of economic development

indicate that China may alter its macroeconomic conditions in favor of monetary integration

with the East Asian region in the long run.

Submitted by Karel Vanhulle

On behalf of: Dr. Filip De Beule

1

1. Introduction

The dramatic consequences of the Asian financial crisis in 1997/1998 stimulated East Asian

policymakers to swiftly adopt measures that would strengthen the region’s financial resilience

in order to avoid any future crises. This led to the most advanced arrangement of financial

cooperation in the East Asian region: the Chiang Mai Initiative.

According to integration optimists, initiatives for financial cooperation in the East Asian

region after the Asian financial crisis constituted a ‘shining beacon of hope’. Initial studies on

the feasibility of monetary integration in East Asia, such as the study by Bayoumi and

Eichengreen (1999), highlighted that many East Asian economies satisfied the necessary

economic conditions for currency union membership. Therefore, there has been a proliferation

of studies that explored the feasibility of East Asian monetary integration since.

The main theory to assess the costs and benefits of monetary integration is the Optimum

Currency Area (OCA) theory. Two main research methods have been used to analyze the

OCA properties: the shock-symmetry approach and broad-based empirical studies. Most of

these studies conclude that the East Asian region as a whole does not constitute an optimum

currency area, but there are some clusters of countries that do indicate strong signs of

economic correlation. According to the shock-symmetry approach China is consistently

excluded as a potential member for East Asian monetary integration. More broad-based

empirical studies do however portray less uniform results about China’s exclusion.

Additionally, China’s rapid economic growth, its huge international reserves, adjustments in

its exchange rate regime and strongly increased intra-regional trade in the past decade may

change perspectives on China’s current position as a potential member of a currency union.

Therefore, this study discusses whether China reaches the necessary economic conditions for

monetary integration, based on an analysis of the three classic economic OCA criteria.

This paper is structured as follows: Section 2 gives an overview of the essential literature

about monetary integration, with a focus on China’s role. Section 3 describes the

methodology that is used to analyze China’s current economic position for monetary

integration. Section 4 presents the research results and section 5 concludes.

2. Literature Review

This literature review begins with the Asian financial crisis and how it led to more regional

monetary cooperation (section 2.1.). Thereafter, section 2.2. provides a review of the main

2

theory to assess the feasibility of monetary integration. Finally, the most important literature

on the feasibility of East Asian monetary integration is discussed in section 2.3.

2.1.The Asian Financial Crisis and Initiatives for Regional Monetary Cooperation

Massive currency attacks made the Thai government float its Baht in July 1997 (Katada,

2012), an event that announced the start of a severely contagious crisis. Since the crisis

proved to be regional, it quickly made the currencies of Indonesia, South Korea and other

neighboring countries also lose over 20% and more of their value (Webber, 2000). But even

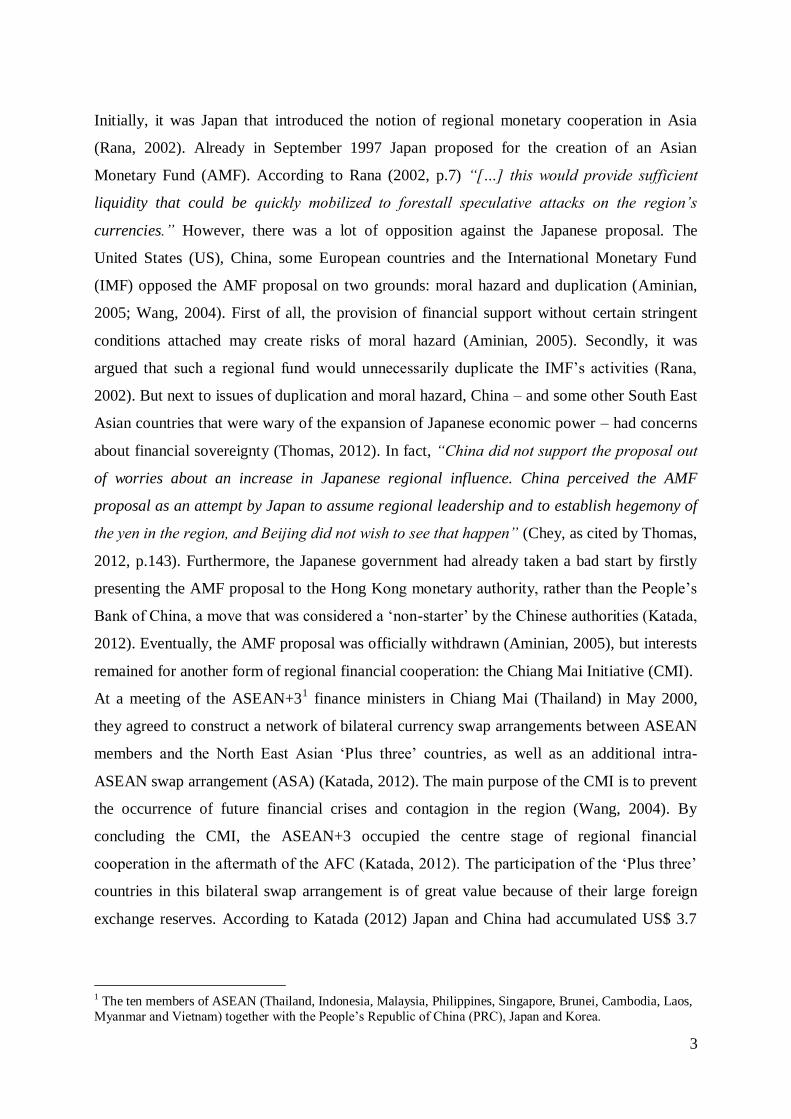

though the Asian Financial Crisis (AFC) began as a currency crisis, it had drastic effects on

the real economy of most East Asian nations (see Figure 1). One of the only countries that had

largely escaped the turmoil was China, which nonetheless did play an important role during

the event. First of all, the Chinese government rigorously defended the Hong Kong dollar

when it also came under attack (Webber, 2000). And secondly, China was able to resist the

pressure to devalue its own currency and compete with the East Asian economies whose

currencies had massively devaluated. As a result, China gained high marks with the East

Asian countries who aimed to ‘export their way out of crisis’ (Katada, 2012).

Although most East Asian economies were able to swiftly recover (see Figure 1), the crisis

did profoundly shock the region and changed opinions about obstacles for monetary

integration (Aminian, 2005). As stated by Katada (2012, p.130): “In many ways, this shock

gave immediate and unequivocal commitment to regional financial and monetary

cooperation.”

Figure 1: East Asian Growth Rates

Source: Ito, 2007

3

Initially, it was Japan that introduced the notion of regional monetary cooperation in Asia

(Rana, 2002). Already in September 1997 Japan proposed for the creation of an Asian

Monetary Fund (AMF). According to Rana (2002, p.7) “[…] this would provide sufficient

liquidity that could be quickly mobilized to forestall speculative attacks on the region’s

currencies.” However, there was a lot of opposition against the Japanese proposal. The

United States (US), China, some European countries and the International Monetary Fund

(IMF) opposed the AMF proposal on two grounds: moral hazard and duplication (Aminian,

2005; Wang, 2004). First of all, the provision of financial support without certain stringent

conditions attached may create risks of moral hazard (Aminian, 2005). Secondly, it was

argued that such a regional fund would unnecessarily duplicate the IMF’s activities (Rana,

2002). But next to issues of duplication and moral hazard, China – and some other South East

Asian countries that were wary of the expansion of Japanese economic power – had concerns

about financial sovereignty (Thomas, 2012). In fact, “China did not support the proposal out

of worries about an increase in Japanese regional influence. China perceived the AMF

proposal as an attempt by Japan to assume regional leadership and to establish hegemony of

the yen in the region, and Beijing did not wish to see that happen” (Chey, as cited by Thomas,

2012, p.143). Furthermore, the Japanese government had already taken a bad start by firstly

presenting the AMF proposal to the Hong Kong monetary authority, rather than the People’s

Bank of China, a move that was considered a ‘non-starter’ by the Chinese authorities (Katada,

2012). Eventually, the AMF proposal was officially withdrawn (Aminian, 2005), but interests

remained for another form of regional financial cooperation: the Chiang Mai Initiative (CMI).

At a meeting of the ASEAN+31 finance ministers in Chiang Mai (Thailand) in May 2000,

they agreed to construct a network of bilateral currency swap arrangements between ASEAN

members and the North East Asian ‘Plus three’ countries, as well as an additional intra-

ASEAN swap arrangement (ASA) (Katada, 2012). The main purpose of the CMI is to prevent

the occurrence of future financial crises and contagion in the region (Wang, 2004). By

concluding the CMI, the ASEAN+3 occupied the centre stage of regional financial

cooperation in the aftermath of the AFC (Katada, 2012). The participation of the ‘Plus three’

countries in this bilateral swap arrangement is of great value because of their large foreign

exchange reserves. According to Katada (2012) Japan and China had accumulated US$ 3.7

1 The ten members of ASEAN (Thailand, Indonesia, Malaysia, Philippines, Singapore, Brunei, Cambodia, Laos,

Myanmar and Vietnam) together with the People’s Republic of China (PRC), Japan and Korea.

4

trillion in dollar-denominated foreign exchange reserves as of September 2010, which makes

them able to provide the necessary emergency funding in dollars.

Asian policymakers however, mostly those of Japan that tried to push through the AMF

proposal, long strived to pool the CMI swap lines and create a multilateral emergency funding

institution (Katada, 2012). They achieved their goal in 2010 when the CMI was

multilateralized under the CMI Multilateralizion (CMIM) agreement, establishing a $120

billion crisis fund for the region (Rana et al., 2012). At the 15th

ASEAN+3 meeting in 2012,

the CMIM has even doubled in size to $240 billion (Ministry of Strategy and Finance, 2012).

Each member country does keep the same share of financial contributions and voting powers,

as displayed in Table 1. The table clearly indicates the valuable, financially balanced, role of

both China and Japan in East Asia’s most institutionalized and advanced construction of

financial cooperation.

Table 1: Financial Contributions to the CMIM per Country

Source: Ministry of Strategy and Finance, 2012

Additional major developments that enhance the financial resilience of the East Asian region

are two capital market initiatives that help to develop the regional bond markets (Yu et al.,

2010). According to Katada (2012) the AFC had highlighted the weakness of the region’s

financial market and thus created a need for increased facility in direct financing in the Asian

economies. First, on the funding side, the Asian Bond Fund (ABF) was launched in 2002 to

help fund and promote the development of regional and domestic bond markets (Yu et al.,

2010). Second, on the issuing side, the Asian Bond Market Initiative (ABMI) was launched in

2003 under the ASEAN+3 framework “[…] to develop efficient and liquid bond markets in

Asia” (Yu et al., 2010, p.2874).

However, according to Grimes, as cited by Katada (2012, p.132), the regional currency

arrangement is “arguably the most important component of regional financial cooperation in

East Asia that could have the most lasting long-term effects.” Although there is plenty of

discussion on the desirability of such an arrangement there has been no real progress in the

development of a regional currency arrangement so far (Katada, 2012).

5

Nonetheless, Katada (2012, p.129) states that: “[…] integration optimists argue that East

Asia’s financial cooperation provides a shining beacon of hope.” Supplementary are East

Asia’s surprisingly high levels of progress towards the Optimum Currency Area conditions

(Bayoumi and Eichengreen, 1999). Hence, these favorable conditions make some, such as

Mundell (2003), believe that Asia will eventually need a common currency. But before going

deeper into the discussion about the feasibility of such an East Asian common currency area,

the main theory to assess the costs and benefits of monetary integration will be elaborated on

in the following section.

2.2.The Theory of Optimum Currency Areas

According to Baldwin and Wyplosz (2011, p.402) the Optimum Currency Area theory

presents “a systematic way of trying to decide whether it makes sense for a group of countries

to abandon their national currencies.” It does so by employing a range of economic and

political criteria that recognize that the real economic cost of giving up the exchange rate

instrument arises in the presence of asymmetric shocks – shocks that do not affect all currency

union member countries (Baldwin and Wyplosz, 2011). Hence, the loss of the exchange rate

instrument is of little consequence when countries face similar/symmetric shocks, since it is

more likely that they would respond with similar policies (Lee and Azali, 2012).

Although the OCA theory does not really say anything about the optimality (to become part of

a currency union or not to?) it does balance out the costs and benefits of monetary integration.

Some of the main benefits of participating in a currency area include: increased usefulness of

money; savings in transaction and hedging costs; improved price stability, and; increased

trade. On the costs side countries can experience some of the following disadvantages when

becoming member of a currency union: changeover costs of switching to a new currency (on

the administrative, legal, hardware and psychological level); the loss of autonomous monetary

policy to cope with asymmetric disturbances, and; negative external effects because of

indebted member countries (Mongelli, 2002).

As mentioned, there is a range of economic and political criteria to determine the optimality

of monetary integration. Monegelli (2002) refers to these criteria as ‘OCA properties’.

According to the author, the number of properties and methods of analysis have greatly

evolved since the OCA theory has been developed 50 years ago. Nonetheless, Mongelli

(2002, p.24) states that “the basic ‘pioneering’ intuitions of the optimum currency area theory

were remarkably strong.” These pioneering intuitions include the theories of Mundell (1961),

6

McKinnon (1962) and Kenen (1969). These are also known as the ‘classic’ economic OCA

criteria. According to Mundell (1961), who was the first to suggest the concept of an

‘optimum currency area’, an essential ingredient of a common currency area is a high degree

of factor mobility. The rationale for this goes as follows: in the presence of an asymmetric

shock, country A may be struck with unemployment, while unaffected country B faces

inflationary pressure (Baldwin and Wyplosz, 2011). However, a high degree of labor mobility

can mitigate the effects of this asymmetric shock and thus have a stabilizing function. Since it

is conventionally assumed that capital is mobile (Baldwin and Wyplosz, 2011) and a common

currency would stimulate its mobility (Mundell, 1961), it is labor mobility that becomes the

real hurdle. The second ‘classic’ economic OCA property, McKinnon’s (1962) theory,

indicates that economies that are open to trade and trade heavily with one another form an

optimum currency area. First of all, exchange rate changes in a highly open economy will

mean great fluctuations in price variability, which makes the usage of national monetary

policies in open economies more costly (McKinnon, 1962). Hence, De Grauwe (2009, p.54)

concludes that “the cost of a monetary union most likely declines with the degree of openness

of a country.” Secondly, increased trade and thus more trade competition equalizes prices of

goods when expressed in the same currency (Baldwin and Wyplosz, 2011). Therefore, such

flexible prices make the loss of autonomous monetary policy less costly. Finally, according to

the theory of Kenen (1969) countries form an optimum currency area when their product

portfolio is highly diversified and when they produce similar goods. A highly diversified

product portfolio means that shocks will be smaller, whilst less diversity between countries’

structure of production makes shocks more symmetric. Furthermore, Mongelli (2002)

indicates that in the course of time additional OCA properties have been added, such as

similarity in inflation rates and fiscal and political integration. But despite the progress in the

development of the OCA theory, there is still no simple OCA-test with a clear-cut scoring

card (Mongelli, 2002). Therefore, Mongelli (2002, p.34) concludes that “[…] we are still far

away from a unified theory in this field.”

A final aspect inherent to single currency areas and crucial for the understanding of the OCA

theory is the rivalry between the paradigm of the ‘Krugman specialization hypothesis’ and the

paradigm of the ‘endogeneity of OCA hypothesis’. On one hand, Krugman (1993) argues that

if trade costs fall, which happens when a country becomes a member of a currency area, firms

will aim to exploit the increasing returns by relocating their business. As a result, national

specialization will lead to more inter-industry trade between countries, which consequently

causes business cycles to be more asynchronous and eventually turn currency areas less

7

optimal. On the other hand, Frankel and Rose (1998, p.22) argue that “a country is more

likely to satisfy the criteria for entry into a currency union ex post than ex ante.” According

to the authors, membership of a currency union decreases trading costs and thereby enhances

trade activity between member countries. In the case of more intra-industry trade it may result

into more synchronized business cycles, which makes the single currency area more ‘optimal’

(Frankel and Rose, 1998).

2.3.China in Studies on East Asian Optimum Currency Areas

To determine East Asia’s optimum currency area, scholars have mainly concentrated on two

approaches: analysis of the symmetry of shocks and broad-based empirical studies. First of

all, broad-based empirical studies focus on the OCA properties that were discussed in section

2.2. Because of the absence of a unifying framework, scholars have the opportunity to select

the properties which they argue that are best to determine the optimality of monetary

integration. However, because every scholar has the freedom to select the properties (s)he

likes, one can end up drawing different borders for a currency area by referring to different

OCA properties. This is called the ‘problem of inconclusiveness’ by Tavlas (1993). The

second methodology, the similarity of shocks approach, captures the interaction between

several properties, and is therefore known as a ‘catch all’ property (Mongelli, 2002).

According to this technique, countries that experience similar demand and supply shocks and

whose economy adjusts rapidly to shocks have lower value in exchange rate policy autonomy

and are better candidates for monetary integration (Lee and Koh, 2012).

Studies that have used the Structural Vector Autoregression (VAR) method to assess the

symmetry of macroeconomic disturbances (Bacha, 2008; Huang and Guo, 2006; Lee and

Koh, 2012; Sato et al., 2009) or a related method (Lee and Azali, 2012) all conclude that

China is not suitable as a member country of a monetary union in the East Asian region.

Basically it comes down to the fact that, according to the VAR approach, China displays

asymmetric shocks or insignificant correlations with the other East Asian economies. Most

studies however, provide the reader with additional information about China’s exclusion or

put forward a point of concern.

First of all, Lee and Azali (2012) indicate that the regional factor – which explains output

fluctuations – mostly increased for the worst-hit countries of the AFC. Therefore, the authors

conclude that it is possibly the contagion effect of the AFC which led to the increase in the

regional factor. Since China remained relatively intact by the AFC, it could not profit of an

8

increase in its regional factor. On the contrary, its country-specific factor in explaining output

fluctuations increased (Lee and Azali, 2012). Secondly, Huang and Guo (2012) indicate that

China shows no significant correlations with the rest of East Asia in its supply, demand and

monetary disturbances. Additionally, the authors state that China’s response to external

shocks is different from other countries, probably due to China’s fixed exchange rate

arrangement throughout the estimation period (which is limited to 2006). However, since

China has shifted to controlled appreciation from 2005 onwards (letting the nominal value of

the renminbi rise about 32 percent against the dollar (Henning, 2012)), this might have

important implications for the correlation of shocks between China and other East Asian

economies. Supplementary is the remark of Sato et al. (2009, p.2936) who state that their

“analysis may not be able to fully catch the marked development of recent regional

integration process and the growing presence of the Chinese economy in the last decade or

so, […].” Finally, Lee and Koh (2012) indicate that China’s supply shocks are not

synchronized with an ASEAN grouping. Nonetheless, the authors remark that the exclusion of

China from a monetary union raises a concern, because, being one of the fastest growing and

largest economies, it possesses huge international reserves which would enhance the stability

of a currency union.

Broad-based empirical studies that have used a variety of OCA properties (Aminian, 2005;

Quah, 2009) or a unique ‘hierarchical clustering approach’ (Quah and Crowley, 2010) to

assess the feasibility of monetary integration do not come to such a uniform conclusion as

scholars that used a symmetry of shocks approach. First of all, Quah (2009), who assesses the

feasibility of monetary integration with the US dollar as anchor currency, concludes that

China scores ‘moderately eligible’ to become part of such a dollar area. This indicates that

China obtains relatively good scores on various OCA properties for monetary integration.

Secondly, Quah and Crowley’s (2010) hierarchical clustering approach shows that China

shares strong pre-crisis OCA features with Malaysia and Thailand (which are merged at the

smallest distance). In the post-crisis period China shows strong symmetries with the

Philippines and Taiwan (Quah and Crowley, 2010). Finally, Aminian (2005) concludes that

East Asian economies may not constitute an OCA as a whole (which is confirmed by most

other studies on East Asian monetary integration), but regional clusters are possible. Aminian

(2005) indicates that there are two East Asian groupings with significantly correlated

9

economic structures: (1) Japan and Asian Newly Industrialized Economies2 (NIEs), and; (2)

ASEAN 43 plus China.

Overall, the symmetry of shocks approach consistently excludes China as a potential member

of a monetary union, whilst more broad-based empirical studies provide less uniform results.

Additionally, China’s rapid economic growth, its huge international reserves, adjustments in

its exchange rate regime and strongly increased intra-regional trade in the past decade may

shed a different light on China’s current position as a potential member of a currency union.

Therefore, this study will provide an assessment of China’s position in an East Asian

monetary union. The main goal of this study can be formulated in the following research

question:

Is China in a favorable economic position for monetary integration?

The grouping that is selected for analysis is determined according to the findings of Aminian

(2005), namely, China and the ASEAN 4. Japan and the NIE’s can logically be excluded from

an East Asian monetary union that includes China because of their highly developed

economic structures which would automatically lead to asynchronous business cycles and

thus higher costs for monetary integration.

3. Methodology

According to Mongelli (2002, p.26), studies that have analyzed the symmetry of shocks

“provide a useful benchmark of comparisons across many countries whose economic and

financial structures would be otherwise difficult to summarize.” However, the author also

refers to the fact that the results of such studies are ambiguous and often in conflict.

Because this study is limited to only five countries (China and the ASEAN4) it is feasible to

present a decent overview of the country-specific achievements to each OCA criterion. As

such, this study does not capture the interaction between several OCA properties as shock

symmetry-related methods do, but it provides the reader with better insights in each specific

OCA property. However, because there is still no OCA-test with a clear cut scoring card

(Mongelli, 2002), the OCA properties that will be analyzed can be selected according to the

preferences of the author.

2 These include: Korea, Taiwan, Singapore and Hong Kong 3 ASEAN4 refers to: Thailand, Malaysia, the Philippines and Indonesia

10

Since the basic ‘pioneering’ intuitions of the OCA theory have proven to be remarkably

strong (Mongelli, 2002), the three main classic economic OCA criteria are selected for

analysis. These include the theories of Mundell (1961), McKinnnon (1963) and Kenen (1969),

which were discussed in more detail in section 2.2. Hence, this study can be perceived as a

broad-based empirical study.

Along the analysis the cases of both East Asia and Europe are discussed. Since many

European countries have opted to proceed with monetary integration in 1999 (creating the

European Economic and Monetary Union), Europe provides an obvious metric for the Asian

economies (Bayoumi and Eichengreen, 1999).

The data sources include: UN Comtrade for data on trade, and; the World Bank website for

general macroeconomic data.

4. Research Findings

Section 4.1. discusses East Asia’s openness to trade and regional trade intensity.

Subsequently, section 4.2. discusses the similarity of East Asian economies and their export

diversification. Finally, section 4.3. examines whether capital and labor are mobile across the

East Asian grouping.

4.1.Openness to Trade and Trade Intensity

As stated by Baldwin and Wyplosz (2011, p. 422): “Openness, which may reduce the

usefulness of an independent exchange rate, is usually defined as the share of economic

activity devoted to international trade.” The ratio of the sum of exports and imports to Gross

Domestic Product (GDP) is ought to be an appropriate index to measure openness to trade. A

high index result indicates high openness to trade, and may even go beyond 100%. To

determine whether the East Asian countries of the selected grouping are open to trade (in

2012), a comparative analysis is made with the situation of the Euro area member countries in

1999. The results are shown in Figure 2.

Overall, the selected East Asian economies display similar levels of openness as the Euro area

members did when they opted for monetary integration. At the top level are Malaysia and

Thailand, which show very high levels of openness, most likely due to their export-oriented

growth strategy. The remaining East Asian economies, including China, display rather low

levels of openness, although they do reach a level that is comparable to that of leading

European powers such as Germany and France. Therefore, the European benchmark indicates

11

that one can assume that China’s level of openness – as is the case for the Philippines and

Indonesia – is not that much of an implication. Nonetheless, a higher degree of openness

remains preferable in order to decrease the costs of monetary integration.

Figure 2: Openness to Trade

Note: The index is the ratio of the sum of exports and imports to GDP. The data for the East Asian economies is from

2012 and the data for the Euro area members is from 1999.

Source: Author's calculations (Data from World Bank database and UN Comtrade)

Secondly, increased trade stimulates international competitiveness between companies, which

equalizes prizes and thus makes a common monetary policy less costly. To analyze trade

interdependency in greater depth, the bilateral trade linkages between China and the ASEAN4

countries are measured according to the ‘trade intensity index’, as used by Goto (2002). The

trade intensity index between country i and country j is defined as follows:

Ii,j = (Ti,j/Ti)/(Tw,j/Tw)

where Ti,j = trade volume of county i with country j,

Ti = total trade volume of country i,

Tw,j = trade volume of the world with country j,

and Tw = total trade volume of the world.

In order to eliminate the effect of the mere size of the country concerned, the index is

normalized by dividing by the relative share of the country in total world trade. If the degree

of trade interaction between country i and country j is equal to that between the world and

12

country j, then the index is equal to unity. The higher the index, the more closely the two

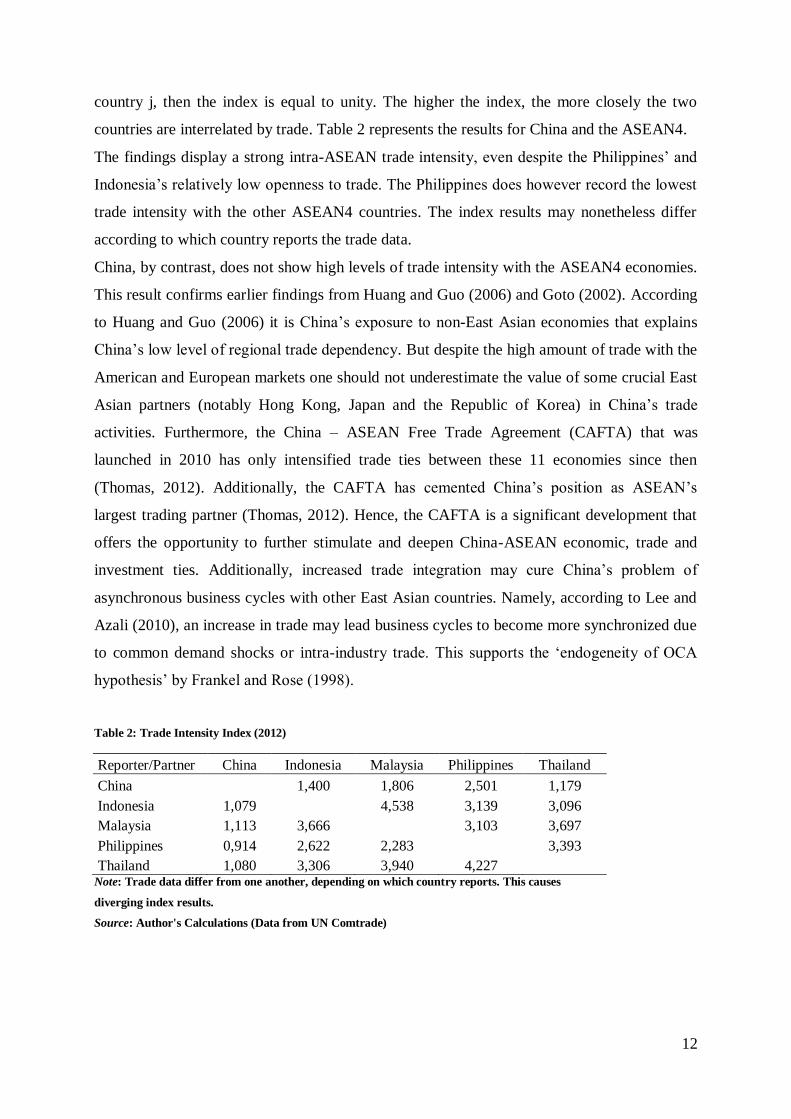

countries are interrelated by trade. Table 2 represents the results for China and the ASEAN4.

The findings display a strong intra-ASEAN trade intensity, even despite the Philippines’ and

Indonesia’s relatively low openness to trade. The Philippines does however record the lowest

trade intensity with the other ASEAN4 countries. The index results may nonetheless differ

according to which country reports the trade data.

China, by contrast, does not show high levels of trade intensity with the ASEAN4 economies.

This result confirms earlier findings from Huang and Guo (2006) and Goto (2002). According

to Huang and Guo (2006) it is China’s exposure to non-East Asian economies that explains

China’s low level of regional trade dependency. But despite the high amount of trade with the

American and European markets one should not underestimate the value of some crucial East

Asian partners (notably Hong Kong, Japan and the Republic of Korea) in China’s trade

activities. Furthermore, the China – ASEAN Free Trade Agreement (CAFTA) that was

launched in 2010 has only intensified trade ties between these 11 economies since then

(Thomas, 2012). Additionally, the CAFTA has cemented China’s position as ASEAN’s

largest trading partner (Thomas, 2012). Hence, the CAFTA is a significant development that

offers the opportunity to further stimulate and deepen China-ASEAN economic, trade and

investment ties. Additionally, increased trade integration may cure China’s problem of

asynchronous business cycles with other East Asian countries. Namely, according to Lee and

Azali (2010), an increase in trade may lead business cycles to become more synchronized due

to common demand shocks or intra-industry trade. This supports the ‘endogeneity of OCA

hypothesis’ by Frankel and Rose (1998).

Table 2: Trade Intensity Index (2012)

Reporter/Partner China Indonesia Malaysia Philippines Thailand

China

1,400 1,806 2,501 1,179

Indonesia 1,079

4,538 3,139 3,096

Malaysia 1,113 3,666

3,103 3,697

Philippines 0,914 2,622 2,283

3,393

Thailand 1,080 3,306 3,940 4,227 Note: Trade data differ from one another, depending on which country reports. This causes

diverging index results.

Source: Author's Calculations (Data from UN Comtrade)

13

4.2.Economic Similarity and Export Diversification

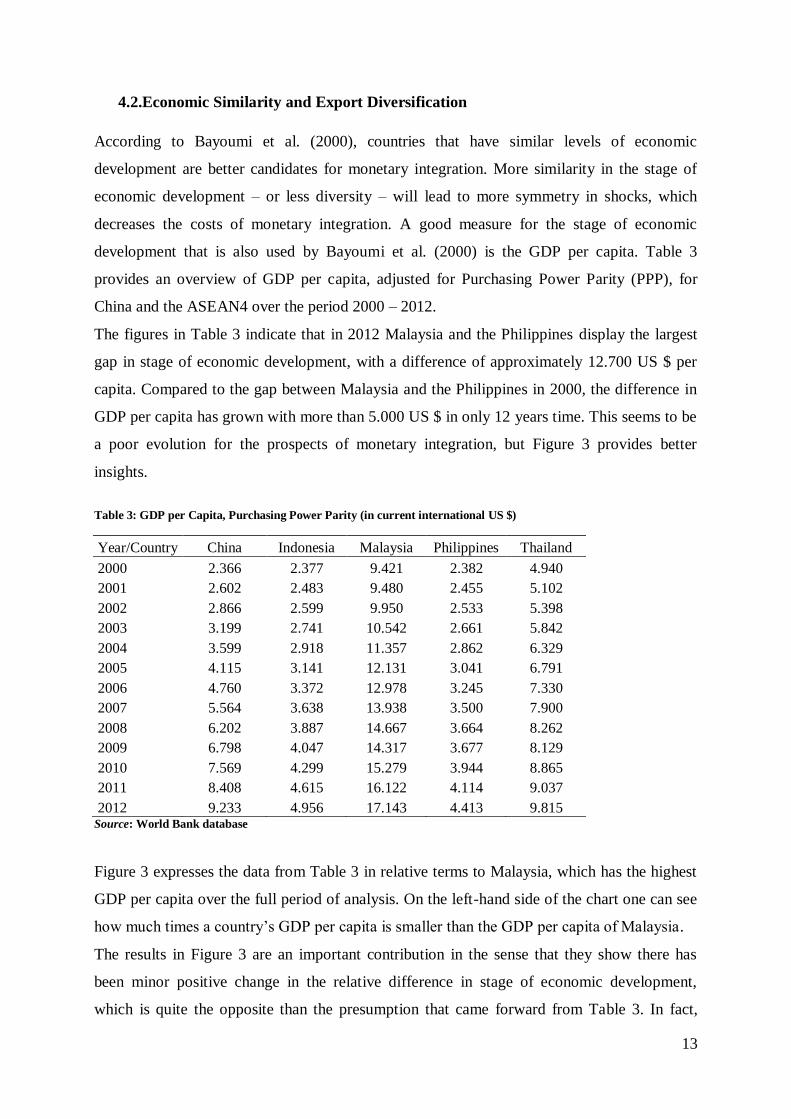

According to Bayoumi et al. (2000), countries that have similar levels of economic

development are better candidates for monetary integration. More similarity in the stage of

economic development – or less diversity – will lead to more symmetry in shocks, which

decreases the costs of monetary integration. A good measure for the stage of economic

development that is also used by Bayoumi et al. (2000) is the GDP per capita. Table 3

provides an overview of GDP per capita, adjusted for Purchasing Power Parity (PPP), for

China and the ASEAN4 over the period 2000 – 2012.

The figures in Table 3 indicate that in 2012 Malaysia and the Philippines display the largest

gap in stage of economic development, with a difference of approximately 12.700 US $ per

capita. Compared to the gap between Malaysia and the Philippines in 2000, the difference in

GDP per capita has grown with more than 5.000 US $ in only 12 years time. This seems to be

a poor evolution for the prospects of monetary integration, but Figure 3 provides better

insights.

Table 3: GDP per Capita, Purchasing Power Parity (in current international US $)

Year/Country China Indonesia Malaysia Philippines Thailand

2000 2.366 2.377 9.421 2.382 4.940

2001 2.602 2.483 9.480 2.455 5.102

2002 2.866 2.599 9.950 2.533 5.398

2003 3.199 2.741 10.542 2.661 5.842

2004 3.599 2.918 11.357 2.862 6.329

2005 4.115 3.141 12.131 3.041 6.791

2006 4.760 3.372 12.978 3.245 7.330

2007 5.564 3.638 13.938 3.500 7.900

2008 6.202 3.887 14.667 3.664 8.262

2009 6.798 4.047 14.317 3.677 8.129

2010 7.569 4.299 15.279 3.944 8.865

2011 8.408 4.615 16.122 4.114 9.037

2012 9.233 4.956 17.143 4.413 9.815 Source: World Bank database

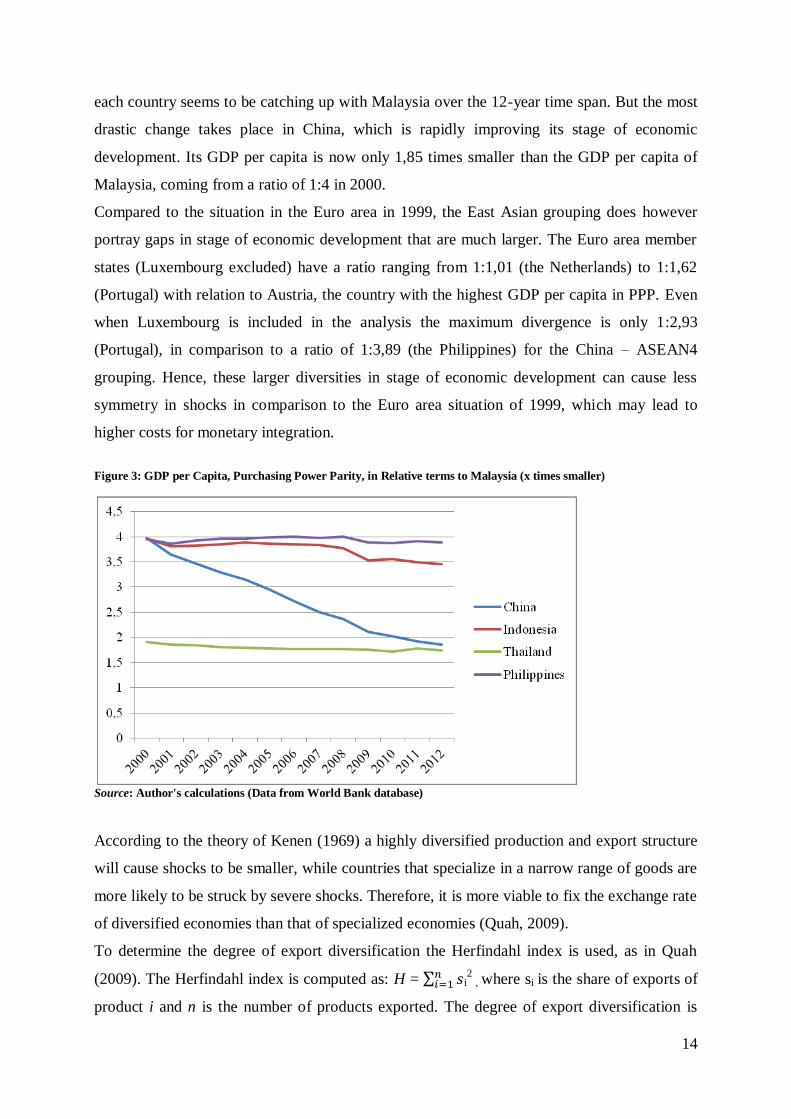

Figure 3 expresses the data from Table 3 in relative terms to Malaysia, which has the highest

GDP per capita over the full period of analysis. On the left-hand side of the chart one can see

how much times a country’s GDP per capita is smaller than the GDP per capita of Malaysia.

The results in Figure 3 are an important contribution in the sense that they show there has

been minor positive change in the relative difference in stage of economic development,

which is quite the opposite than the presumption that came forward from Table 3. In fact,

14

each country seems to be catching up with Malaysia over the 12-year time span. But the most

drastic change takes place in China, which is rapidly improving its stage of economic

development. Its GDP per capita is now only 1,85 times smaller than the GDP per capita of

Malaysia, coming from a ratio of 1:4 in 2000.

Compared to the situation in the Euro area in 1999, the East Asian grouping does however

portray gaps in stage of economic development that are much larger. The Euro area member

states (Luxembourg excluded) have a ratio ranging from 1:1,01 (the Netherlands) to 1:1,62

(Portugal) with relation to Austria, the country with the highest GDP per capita in PPP. Even

when Luxembourg is included in the analysis the maximum divergence is only 1:2,93

(Portugal), in comparison to a ratio of 1:3,89 (the Philippines) for the China – ASEAN4

grouping. Hence, these larger diversities in stage of economic development can cause less

symmetry in shocks in comparison to the Euro area situation of 1999, which may lead to

higher costs for monetary integration.

Figure 3: GDP per Capita, Purchasing Power Parity, in Relative terms to Malaysia (x times smaller)

Source: Author's calculations (Data from World Bank database)

According to the theory of Kenen (1969) a highly diversified production and export structure

will cause shocks to be smaller, while countries that specialize in a narrow range of goods are

more likely to be struck by severe shocks. Therefore, it is more viable to fix the exchange rate

of diversified economies than that of specialized economies (Quah, 2009).

To determine the degree of export diversification the Herfindahl index is used, as in Quah

(2009). The Herfindahl index is computed as: H = i

2 , where si is the share of exports of

product i and n is the number of products exported. The degree of export diversification is

15

measured by the inverse of the Herfindahl index, which is a popular indicator of the degree of

specialization (Quah, 2009). Since export data of individual products are unavailable, export

data according to the first-digit sub-industries of the United Nation’s Standard International

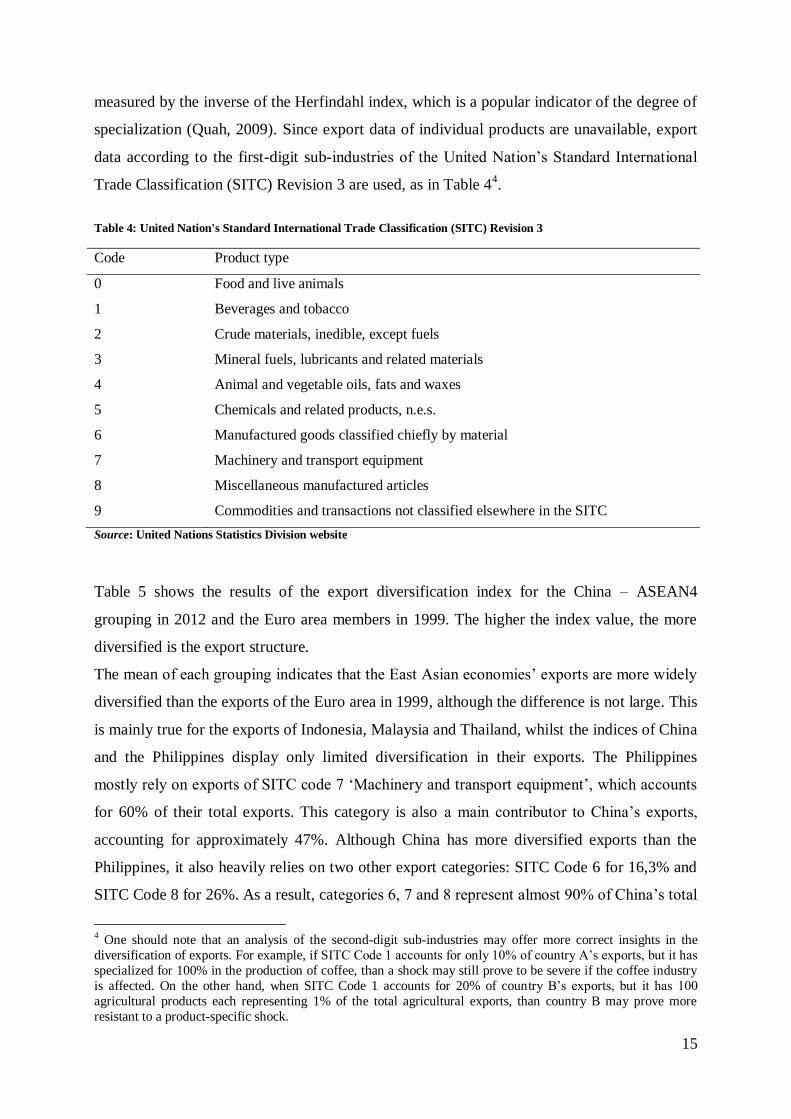

Trade Classification (SITC) Revision 3 are used, as in Table 44.

Table 4: United Nation's Standard International Trade Classification (SITC) Revision 3

Code Product type

0 Food and live animals

1 Beverages and tobacco

2 Crude materials, inedible, except fuels

3 Mineral fuels, lubricants and related materials

4 Animal and vegetable oils, fats and waxes

5 Chemicals and related products, n.e.s.

6 Manufactured goods classified chiefly by material

7 Machinery and transport equipment

8 Miscellaneous manufactured articles

9 Commodities and transactions not classified elsewhere in the SITC

Source: United Nations Statistics Division website

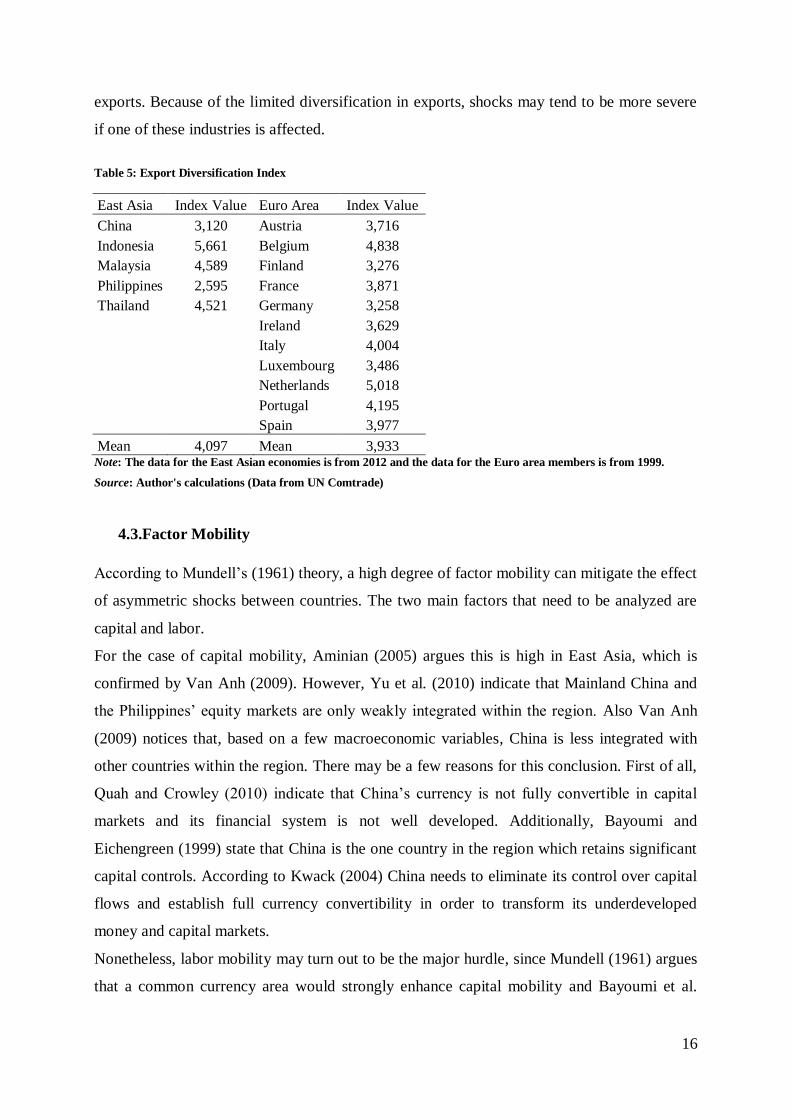

Table 5 shows the results of the export diversification index for the China – ASEAN4

grouping in 2012 and the Euro area members in 1999. The higher the index value, the more

diversified is the export structure.

The mean of each grouping indicates that the East Asian economies’ exports are more widely

diversified than the exports of the Euro area in 1999, although the difference is not large. This

is mainly true for the exports of Indonesia, Malaysia and Thailand, whilst the indices of China

and the Philippines display only limited diversification in their exports. The Philippines

mostly rely on exports of SITC code 7 ‘Machinery and transport equipment’, which accounts

for 60% of their total exports. This category is also a main contributor to China’s exports,

accounting for approximately 47%. Although China has more diversified exports than the

Philippines, it also heavily relies on two other export categories: SITC Code 6 for 16,3% and

SITC Code 8 for 26%. As a result, categories 6, 7 and 8 represent almost 90% of China’s total

4 One should note that an analysis of the second-digit sub-industries may offer more correct insights in the

diversification of exports. For example, if SITC Code 1 accounts for only 10% of country A’s exports, but it has

specialized for 100% in the production of coffee, than a shock may still prove to be severe if the coffee industry

is affected. On the other hand, when SITC Code 1 accounts for 20% of country B’s exports, but it has 100

agricultural products each representing 1% of the total agricultural exports, than country B may prove more

resistant to a product-specific shock.

16

exports. Because of the limited diversification in exports, shocks may tend to be more severe

if one of these industries is affected.

Table 5: Export Diversification Index

East Asia Index Value Euro Area Index Value

China 3,120 Austria 3,716

Indonesia 5,661 Belgium 4,838

Malaysia 4,589 Finland 3,276

Philippines 2,595 France 3,871

Thailand 4,521 Germany 3,258

Ireland 3,629

Italy 4,004

Luxembourg 3,486

Netherlands 5,018

Portugal 4,195

Spain 3,977

Mean 4,097 Mean 3,933 Note: The data for the East Asian economies is from 2012 and the data for the Euro area members is from 1999.

Source: Author's calculations (Data from UN Comtrade)

4.3.Factor Mobility

According to Mundell’s (1961) theory, a high degree of factor mobility can mitigate the effect

of asymmetric shocks between countries. The two main factors that need to be analyzed are

capital and labor.

For the case of capital mobility, Aminian (2005) argues this is high in East Asia, which is

confirmed by Van Anh (2009). However, Yu et al. (2010) indicate that Mainland China and

the Philippines’ equity markets are only weakly integrated within the region. Also Van Anh

(2009) notices that, based on a few macroeconomic variables, China is less integrated with

other countries within the region. There may be a few reasons for this conclusion. First of all,

Quah and Crowley (2010) indicate that China’s currency is not fully convertible in capital

markets and its financial system is not well developed. Additionally, Bayoumi and

Eichengreen (1999) state that China is the one country in the region which retains significant

capital controls. According to Kwack (2004) China needs to eliminate its control over capital

flows and establish full currency convertibility in order to transform its underdeveloped

money and capital markets.

Nonetheless, labor mobility may turn out to be the major hurdle, since Mundell (1961) argues

that a common currency area would strongly enhance capital mobility and Bayoumi et al.

17

(2000) argue that it would facilitate the harmonization of the various financial systems in East

Asia.

With regards to East Asian labor mobility there are contrasting opinions amongst scholars. On

one hand, Bayoumi and Eichengreen (1999) argue that labor mobility is relatively high in

Asia. This statement is mostly supported because of the fast adjustment to asymmetric shocks

in the East Asian region. But, Lee and Koh (2012) indicate that this high labor mobility is

mainly the case for the ASEAN region, thus China excluded.

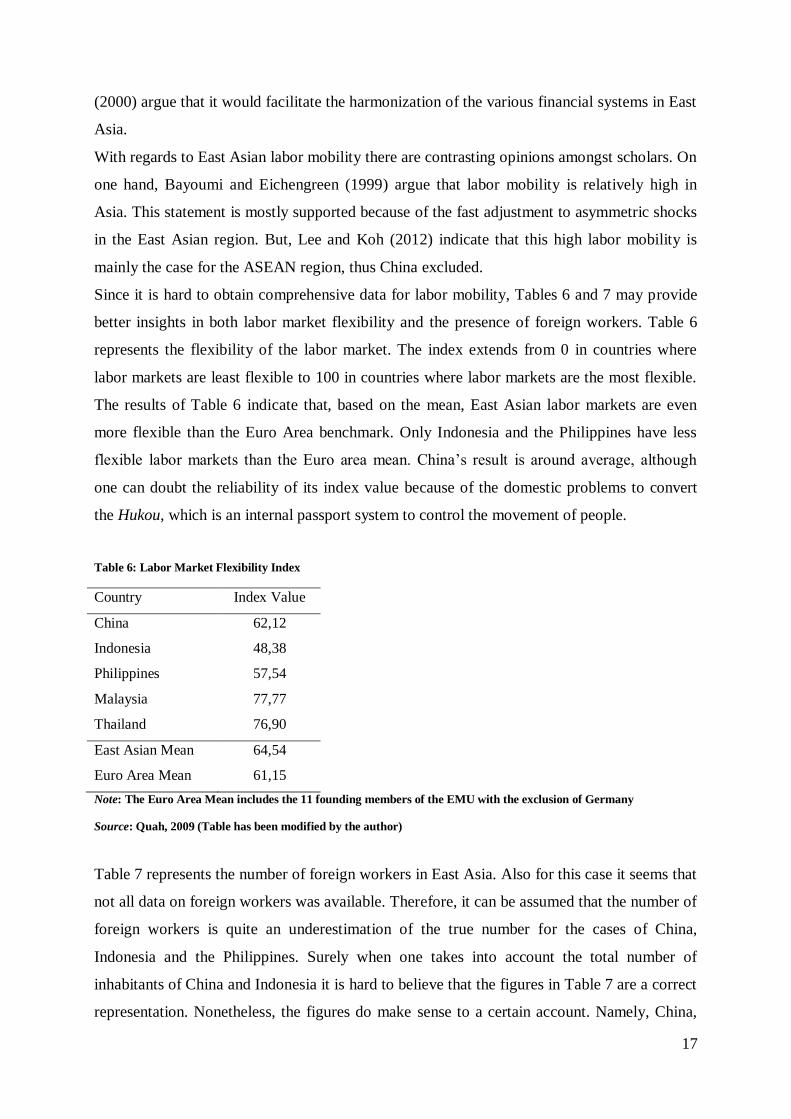

Since it is hard to obtain comprehensive data for labor mobility, Tables 6 and 7 may provide

better insights in both labor market flexibility and the presence of foreign workers. Table 6

represents the flexibility of the labor market. The index extends from 0 in countries where

labor markets are least flexible to 100 in countries where labor markets are the most flexible.

The results of Table 6 indicate that, based on the mean, East Asian labor markets are even

more flexible than the Euro Area benchmark. Only Indonesia and the Philippines have less

flexible labor markets than the Euro area mean. China’s result is around average, although

one can doubt the reliability of its index value because of the domestic problems to convert

the Hukou, which is an internal passport system to control the movement of people.

Table 6: Labor Market Flexibility Index

Country Index Value

China 62,12

Indonesia 48,38

Philippines 57,54

Malaysia 77,77

Thailand 76,90

East Asian Mean 64,54

Euro Area Mean 61,15

Note: The Euro Area Mean includes the 11 founding members of the EMU with the exclusion of Germany

Source: Quah, 2009 (Table has been modified by the author)

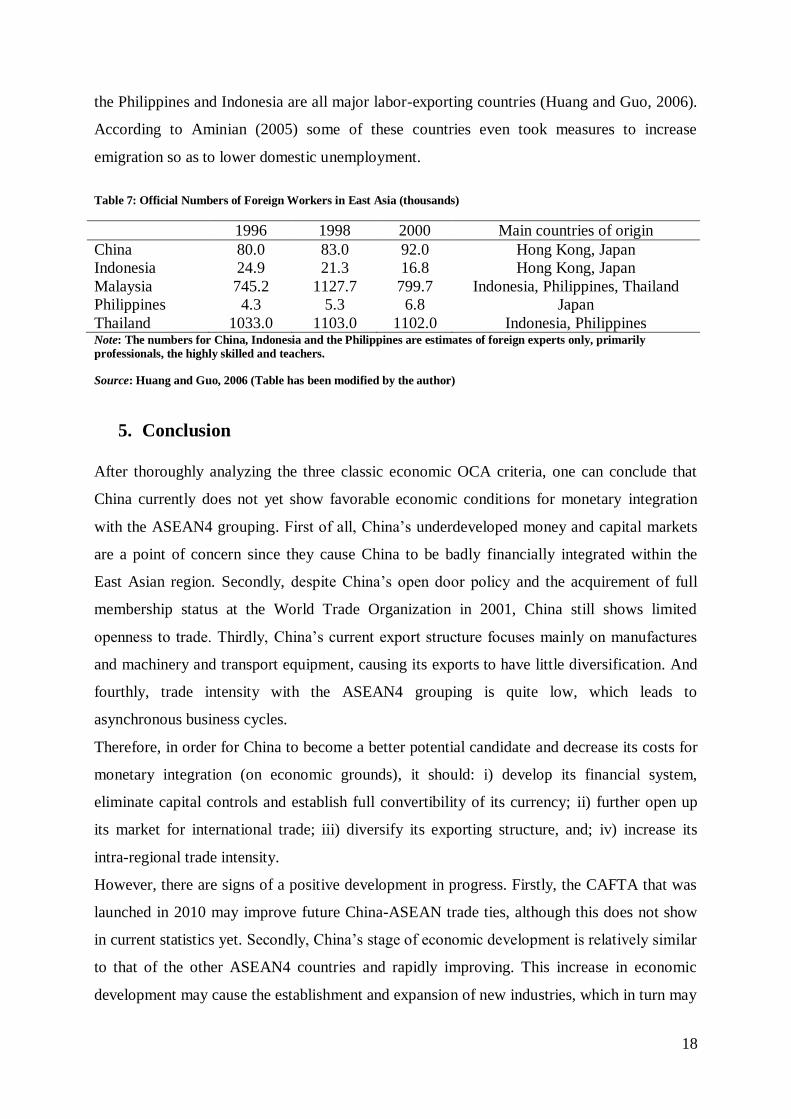

Table 7 represents the number of foreign workers in East Asia. Also for this case it seems that

not all data on foreign workers was available. Therefore, it can be assumed that the number of

foreign workers is quite an underestimation of the true number for the cases of China,

Indonesia and the Philippines. Surely when one takes into account the total number of

inhabitants of China and Indonesia it is hard to believe that the figures in Table 7 are a correct

representation. Nonetheless, the figures do make sense to a certain account. Namely, China,

18

the Philippines and Indonesia are all major labor-exporting countries (Huang and Guo, 2006).

According to Aminian (2005) some of these countries even took measures to increase

emigration so as to lower domestic unemployment.

Table 7: Official Numbers of Foreign Workers in East Asia (thousands)

1996 1998 2000 Main countries of origin

China 80.0 83.0 92.0 Hong Kong, Japan

Indonesia 24.9 21.3 16.8 Hong Kong, Japan

Malaysia 745.2 1127.7 799.7 Indonesia, Philippines, Thailand

Philippines 4.3 5.3 6.8 Japan

Thailand 1033.0 1103.0 1102.0 Indonesia, Philippines Note: The numbers for China, Indonesia and the Philippines are estimates of foreign experts only, primarily

professionals, the highly skilled and teachers.

Source: Huang and Guo, 2006 (Table has been modified by the author)

5. Conclusion

After thoroughly analyzing the three classic economic OCA criteria, one can conclude that

China currently does not yet show favorable economic conditions for monetary integration

with the ASEAN4 grouping. First of all, China’s underdeveloped money and capital markets

are a point of concern since they cause China to be badly financially integrated within the

East Asian region. Secondly, despite China’s open door policy and the acquirement of full

membership status at the World Trade Organization in 2001, China still shows limited

openness to trade. Thirdly, China’s current export structure focuses mainly on manufactures

and machinery and transport equipment, causing its exports to have little diversification. And

fourthly, trade intensity with the ASEAN4 grouping is quite low, which leads to

asynchronous business cycles.

Therefore, in order for China to become a better potential candidate and decrease its costs for

monetary integration (on economic grounds), it should: i) develop its financial system,

eliminate capital controls and establish full convertibility of its currency; ii) further open up

its market for international trade; iii) diversify its exporting structure, and; iv) increase its

intra-regional trade intensity.

However, there are signs of a positive development in progress. Firstly, the CAFTA that was

launched in 2010 may improve future China-ASEAN trade ties, although this does not show

in current statistics yet. Secondly, China’s stage of economic development is relatively similar

to that of the other ASEAN4 countries and rapidly improving. This increase in economic

development may cause the establishment and expansion of new industries, which in turn may

19

lead to more diversified exports. Thirdly, as stated by Mundell (1961) and Bayoumi and

Eichengreen (2000), the establishment of a common currency area may automatically lead to

more capital mobility and the harmonization of diverging financial systems. Therefore,

China’s underdeveloped financial system may not be that much of an issue for now.

This leads to the conclusion that China should not be put off as a potential member for Asian

monetary integration yet. Because of China’s economic size, its huge international currency

reserves and the potential for rapid improvements in China’s macroeconomic conditions for

monetary integration, the feasibility of an East Asian common currency union with China

included can still be a long-run objective.

A few limitations to this paper need to be mentioned. Firstly, this study only focuses on a

limited range of OCA properties, while a discussion of additional properties could give better

insights about China’s potential as an East Asian common currency area member. Secondly,

Mongelli (2002) indicates that in the case of successful currency unions, the political criteria

have often dominated the economic. Therefore, an additional assessment of the political

prerequisites for monetary integration would also be a valuable research contribution. Mainly

the Sino-Japanese rivalry for regional dominance may turn out to play a crucial role for

regional monetary integration.

References

Aminian, N. (2005) Economic integration and prospects for regional monetary cooperation in East Asia.

Structural Change and Economic Dynamics, 16: 91-110.

Bacha, O. I. (2008) A common currency area for ASEAN? Issues and feasibility. Applied Economics, 40: 515-

529.

Baldwin, R. and Wyplosz, C. (2011) The Economics of European Integration (4th ed.) Berkshire, McGraw-Hill

Education.

Bayoumi, T. and Eichengreen, B. (1999) Is Asia an optimum currency area? Can it Become one? Regional,

global and historical perspectives on Asian monetary relations, in “Exchange Rate Policies in Emerging

Asian Countries” (S. Collignon, J. Pisani-Ferry, and Y. Chul Park, Eds.), 347-367. Routledge, London.

Bayoumi, T., Eichengreen, B. and Mauro, P. (2000) On Regional Monetary Arrangements for ASEAN. Journal

of the Japanese and International Economies, 14: 121-148.

De Grauwe, P. (2009) Economics of monetary union (8th ed.) Oxford University Press.

20

Frankell, J.A. and Rose, A.K. (1998) The Endogeneity of the Optimum Currency Area Criteria. Economic

Journal, 108 (441): 1009-1025.

Goto, J. (2002) Economic Preconditions for Monetary Cooperation and Surveillance in East Asia. In Institute for

International Monetary Affairs, Japan Ministry of Finance. Strengthening Financial Cooperation and

Surveillance, 1- 26. Institute for International Monetary Affairs, Tokyo.

Henning, C.R. (2012) Choice and Coercion in East Asian Exchange Rate Regimes. Working paper, Peterson

Institute for International Economics.

Huang, Y. and Guo, F. (2006) Is currency union a feasible option in East Asia? A multivariate VAR approach.

Research in International Business and Finance, 20: 77-94.

Ito, T. (2007) Asian Currency Crisis and the International Monetary Fund, 10 Years Later: Overview. Asian

Economic Policy Review, 2: 16-49.

Katada, S.N. (2012) Regional Financial Cooperation, in “Routledge Handbook of Asian Regionalism” (Beeson,

M. and Stubbs, R., Eds.), 129-137. Routledge, London.

Kenen, P. (1969) The theory of optimum currency areas, in R. Mundell and A. Swoboda, eds., Monetary

Problems of the International Economy, Chicago University Press, Chicago.

Krugman, P. (1993) Lessons of Massachusetts for EMU, in F. Giavazzi and F. Torres, eds., The Transition to

Economic and Monetary Union in Europe, Cambdrige University Press, New York, 241-261.

Lee, G.H.Y. and Azali, M. (2010) The Endogeneity of the Optimum Currency Area Criteria in East Asia.

Economic Modelling, 77(1): 165-170.

Lee, G.H.Y. and Azali, M. (2012) Is East Asia an optimum currency area? Economic Modelling, 29: 87-95.

Lee, G.H.Y. and Koh, S.G.M. (2012) The prospects of a monetary union in East Asia. Economic Modelling, 29:

96-102.

McKinnon, R. (1962) Optimum Currency Areas. American Economic Review, 53: 717-725.

Ministry of Strategy and Finance (2012) ASEAN+3 finance ministers and central bank governors’ meeting

successfully concludes. Press Release, May 3.

Mongelli, F.P. (2002) “New” Views on the Optimum Currency Area Theory: What is EMU telling US?

Preliminary Draft, European Central Bank.

Mundell, R. (1961) A Theory of Optimum Currency Areas. American Economic Review, 51 (4): 657-665.

Mundell, R. (2003) Prospects for an Asian currency area. Journal of Asian Economic, 14: 1-10.

21

Quah, C-H. (2009) The Feasibility of East Asian Monetary Union as an Optimum Currency Area. International

Journal of Asia Pacific Studies, 5 (2): 65-88.

Quah, C-H. and Crowley, P.M. (2010) Monetary Integration in East Asia: A Hierarchical Clustering Approach.

International Finance, 13 (2): 283-309.

Rana, P.B., Chia, W-M. and Jinjarak, Y. (2012) Monetary integration in ASEAN+3: A perception survey of

opinion leaders. Journal of Asian Economics, 23: 1-12.

Sato, K., Zhang, Z. and Allen, D. (2009) The suitability of a monetary union in East Asia: What does the

cointegration approach tell? Mathematics and Computers in Simulation, 79: 2927-2937.

Tavlas, G.S. (1993) The ‘New’ Theory of Optimum Currency Areas. The World Economy, 16 (6): 663-685.

Thomas, N. (2012) China – ASEAN relations. The core of Asian regionalism, in “Routledge Handbook of Asian

Regionalism” (Beeson, M. and Stubbs, R., Eds.), 138-152. Routledge, London.

Van Anh, T.T. (2009) Financial integration in the Asia Pacific region. The economic studies, 26: 57-72.

Wang, Y. (2004) Financial cooperation and integration in East Asia. Journal of Asian Economics, 15: 939-955.

Webber, M. (2001) Finance and the real economy: theoretical implications of the financial crisis in Asia.

Geoforum, 32: 1-13.

Yu, I.W., Fung, K.P. and Tam, C.S. (2010) Assessing financial market integration in Asia – Equity markets.

Journal of Banking & Finance, 34: 2874-2885.