ahmedabad branch e-newsletter

TRANSCRIPT

The Institute of Chartered Accountants of India (Set up by an Act of Parliament)

PRICE :

` 10/-

AHMEDABAD BRANCH OF WIRC OF ICAI

Chairman’s Message

Photo Gallery

Editorial 2

Office Bearers 3

Sub-Committees 4 1

MEMBERS

CA. , CCMAniket Talati98255 51448

CA. , RCMHitesh Pomal98240 49402

CA. Vikash Jain, RCM93277 15892

CA. Chintan Patel, RCM90999 21163

EX. OFFICIO MEMBERS

CHAIRMANCA. Ganesh Nadar99744 77447

VICE CHAIRMANCA. Fenil Shah89050 30507

SECRETARYCA. Harit Dhariwal99789 42299

TREASURERCA. Anjali Choksi98257 73179

CHAIRMAN : CA. Rahul MaliwalCO-CHAIRMAN : CA. Hemlata R. DewnaniCONVENER : CA. Mohit Tibrewal

CA. Bishan Shah

CA. Rahul Maliwal

CA. Sunil SanghviWarm Greeting from CA. Ganesh Nadar !

th With full sense of responsibility and commitment to deliver on 26 February, 2019, I have taken over the charge as Chairman of the Ahmedabad Branch of WIRC of ICAI, the second largest branch of ICAI.

A day to remember and cherish about, Yes I am carrying a strong agenda to ensure a very simple cause – betterment of our fraternity…..a mission to see our esteem Profession reach unparallel heights !

It's a privilege to be here and I very well understand the level of commitment which have to be given by me as a Team, in ensuring every act and deeds being done in a manner which gives and makes our members to be proud to be a CA and builds brand CA in our society.

ICAI has changed guards and elected CA. Prafulla Chhajed as President and CA. Atul Gupta as Vice President of ICAI. Both these leaders are one of the best and we would be seeing many visible changes in months to come. I am fortunate to know personally CA. Prafulla Chhajed, he is a man of actions, a man who has seen working at Branch, a grass root leader and hence he will be one of the finest President we have seen. A person who knows best for our members and students, will frame polices and ensuring it gets implemented and delivered during his tenure itself.

We also now have from Ahmedabad young and dynamic leaders elected and positioning themselves in Central Council and Regional Councils. It starts with young dynamic Central Council Member CA. Aniket Talati and three energetic young Regional Council Members CA. Hitesh Pomal, CA. Vikash Jain and CA. Chintan Patel. Presently majority of our Managing Committee members have all worked together with all our Central Council Member and Regional Council Members making the whole Managing Committee a cohesive team to deliver best for our fraternity consistently for the whole tenure of 3 years.

NEWSLETTER COMMITTEE

Devam ShethKushal Bhadrikbhai Reshamwala Mahadev Prasad BirlaMahavir Prafulchandra ShahNeelo PorwalPranay MehtaSagar ChhataniTwinkle S ShahVaibhav Shah

MEMBERS

e-NewsletterVol. No. 6Issue No. 01March 2019

OFFICE BEARERS

Accounting, Auditing &Company Law Updates

GST Update

FEMA Updates

International TaxationUpdates

Direct Tax Updates

RERA

Important Due datesfor Compliance

7

8

9

10

11

13

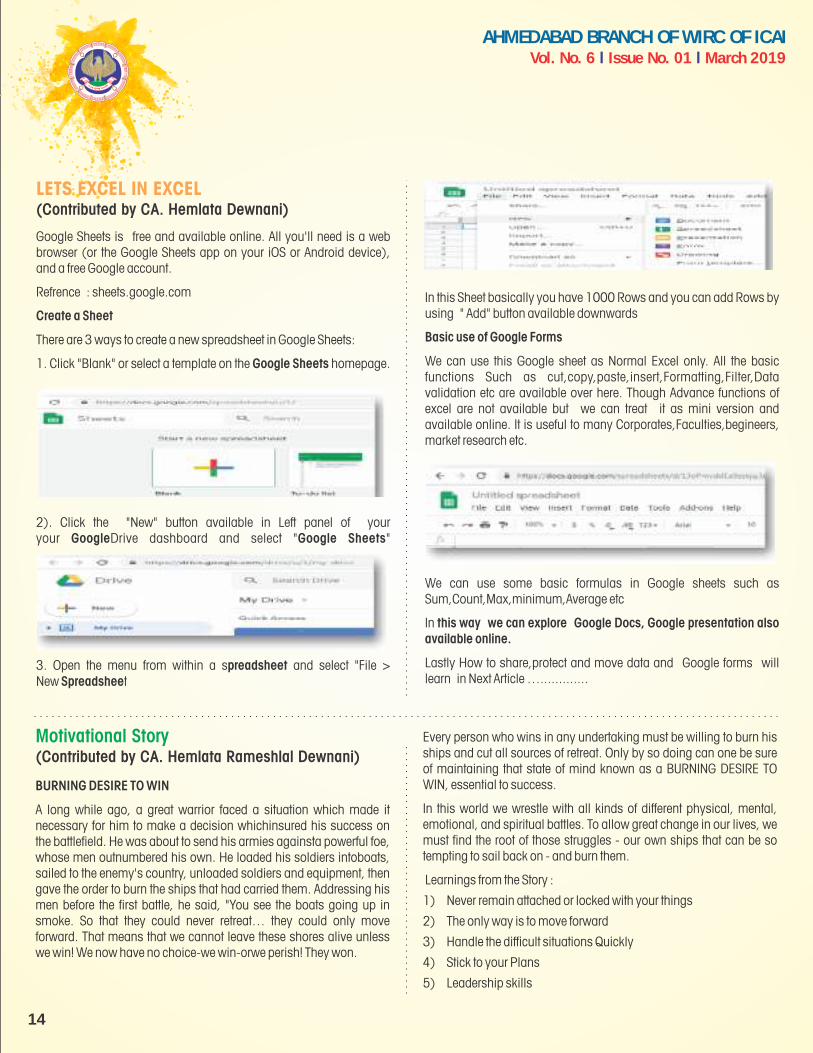

Lets Excel in Excel 14

15

16

2

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

Dear Members,

This Year chairman of the branch has blessed me with the responsibility of the Newsletter Committee. I sincerely accept the same and want to assure that entire team of committee shall dedicatedly put the efforts to ensure best knowledge to share.

This month is not just beautiful in terms of the beauty nature beholds but also has many festivals that magnify the festivity of the season. What makes India special is the diversity, along with it comes the variety of cultures and festivals of India.

Similarly it is beautiful for our profession in terms of the compliances we need to magnify in this month. This month is special because of the compliance in all diverse fields of Accounting, Direct Taxation & Indirect Taxation.

March 1: International Yoga Day- Prepare ourselves mentally and physically at the start of this month for what it takes out of ud.

March 5: Shivratri- Destroy and cure all the defects crept in during the year

March 8: International Women's day- Bring parity to genders and balance to the books of accounts

March 20 Holika Dahan: Magical Evacuation of Prahlad from the fire & Tactical preparation of financial statements from the data received

March 21 Dhuleti & Parsi New Year: Symbolizing the triumph of our efforts & Focus on the renewal (amendmends) that a new year is going to bring.

Happy Holi!

CA. Rahul MaliwalChairman, Newsletter Committee

Editorial Message

At WIRC also, we now have new Chairperson CA Priti Savla, this certainly shows how we all have evolved ourselves towards women empowerment.

Warmly welcoming all the Co – Chairmen and Conveners of various Committees of our Branch, it is heartening and satisfying to see Members willing to participate in various activities.

Will always be a Team Player ! This whole year as Chairman would strive and ensure we have best Knowledge Share, better understanding of New Practise Areas & Opportunities, every act and action is Brand Building of CA in Ahmedabad, getting Connected with Young Members & Members in Industries, focus for Women CAs & their Empowerment and creating environment to ensure Fellowship & Networking.

Yes, March is a month of Bank Branch Audit and we from Branch will be bring our best program with best speakers thus ensuring our members have one of the finest program of all time.

March is month of Holi - a festival of colour and a celebration that symbolizes the victory of devotion and virtue over evils. Wishing all our Members “May all the seven colours of the rainbow come together this Holi and bless you and your family, life with happiness and joy – Have a Happy Holi”

Looking forward for happening best days ahead !

Thanks & Regards

CA. Ganesh NadarChairman

Mission to take our esteem Profession to unparallel heights !

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

Office Bearers2019-2022.

CA. Ganesh NadarChairman

CA. Bishan Shah

CA. Anjali ChoksiTreasurer

CA. Harit DhariwalSecretary

CA. Fenil ShahVice Chairman

CA. Aniket TalatiCCM

CA. Rahul Maliwal CA. Sunilkumar Sanghvi

CA. Pomal ShahRCM, WIRC

CA. Vikash JainRCM, WIRC

CA. Chintan PatelRCM, WIRC

Managing Committee Members

Ex-Officio

3

4

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

Sub-Committees for the year 2019-20

Name Designation

CA. Sunil Sanghvi Chairman

CA. Shaleen Patni Co-Chairman

CA. Vishal Mehta Convenor

CA. Ashish Sharma Member

CA. Ayush Dhariwal Member

CA. Bankim Shah Member

CA. Deep Thakkar Member

CA. Dinesh Shah Member

CA. Hardik Patwa Member

CA. Harshesh Jasvani Member

CA. Harshit Sheth Member

CA. Hemendra Shah Member

CA. Hitesh Shah Member

CA. Jainam Shah Member

CA. Jigar Shah Member

CA. Jimit Shah Member

CA. Ketan Mistry Member

CA. Marmik Shah Member

CA. Meghal Shah Member

CA. Mehul Thakker Member

CA. Mohit Balani Member

CA. Mohit Mehta Member

CA. Mohit Tibrewala Member

CA. Nilay Shah Member

CA. Pankaj Patel Member

CA. Rahul Maloo Member

CA. Rohit Maloo Member

CA. Ronakkumar Kher Member

CA. Rushi Shah Member

CA. Saumya Sheth Member

CA. Shail Shah Member

CA. Sulabh Padshah Member

CA. Vicky Jain Member

CA. Vishank Patel Member

CA. Vivek Agrawal Member

CA. Zeal Bangadiwala Member

DIRECT TAX & INTERNATIONALACCOUNTING & AUDITING

Name Designation

CA. Chairman

CA. Hardik Sutaria Co-Chairman

CA. Krishnakant Solanki Convener

CA. Anand Sharma Member

CA. Bindesh Jain Member

CA. Bonykumar Shah Member

CA. Brijesh Thakkar Member

CA. Kiransinh Chavda Member

CA. Paurav Shah Member

CA. Priyam Shah Member

CA. Rajan Shah Member

CA. Rathin Majmudar Member

CA. Samip Shah Member

CA. Utsav Hirani Member

CA. Vishank Patel Member

Hitesh Pomal

Name DesignationCA. Bishan Shah ChairmanCA. Tarang Kothari Co-ChairmanCA. Hem Chhajed ConvenerCA. Abhinav Malaviya MemberCA. Akshatkumar Vithalani MemberCA. Amish Khandhar MemberCA. Bhavesh Jhalawadia MemberCA. Brijesh Thakar MemberCA. Chintan Vasa MemberCA. Darpan Shah MemberCA. Gunjan Shah MemberCA. Hardik Modh MemberCA. Harsh Rathi MemberCA. Hirenbhai Pathak MemberCA. Janakkumar Tanna MemberCA. Jay Dalwadi MemberCA. Jaykin Shah MemberCA. Jaykishan Vidhwani MemberCA. Jenil Shah MemberCA. Jigar Shah MemberCA. Ketan Mistry MemberCA. Labdhi Shah MemberCA. Mahavir Shah MemberCA. Meet Jadawala MemberCA. Monish Shah MemberCA. Mukesh Laddha MemberCA. Niral Parikh MemberCA. Nitesh Jain MemberCA. Pankajkumar Patel MemberCA. Pooja Jajwani MemberCA. Pooja Shah MemberCA. Pravinkumar DhandhariaMemberCA. Punit Prajapati MemberCA. Rahul Patel MemberCA. Rashmin Vaja MemberCA. Surajkumar Jain MemberCA. Tapas Ruparelia MemberCA. Urvashi Jindal MemberCA. Vishrut Shah MemberCA. Yash Parikh MemberCA. Zeal Bangdiwala Member

INDIRECT TAX COMMITTEE

Name Designation

CA. Rahul Maliwal Chairman

CA. Hemlata Dewnani Co-Chairman

CA. Mohit Tibrewal Convener

CA. Devam Sheth Member

CA. Harsh Kapadia

CA. Kushal Reshamwala

CA. Mahadev Prasad Birla

CA. Mahavir Shah

CA. Neelo Porwal

CA. Pranay Mehta

CA. Sagar Chhatani

CA. Twinkle Logar

CA. Vaibhav Shah

Member

Member

Member

Member

Member

Member

Member

Member

Member

WEBSITE & NEWSLETTER

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

Name Designation

CA. Anjali Choksi Chairperson

CA. Durgesh Pandey Co-Chairman

CA. Rushabh Shah Convener

CA. Abhishek Jain Member

CA. Aditya Shah Member

CA. Anand Sharma Member

CA. Ankur Khakhar Member

CA. Charmi Doshi Member

CA. Gopal Baldi Member

CA. Jay Parekh Member

CA. Jaykishan Vidhwani Member

CA. Kaushal Trivedi Member

CA. Ketan Mistry Member

CA. Manishkumar Dubey Member

CA. Monil Shah Member

CA. Mukesh Dholakiya Member

CA. Nisarg Shah Member

CA. Riken Patel Member

CA. Sachin Soni Member

CA. Sarthak Bhansali Member

CA. Shivang Chokshi Member

CA. Silva Shah Member

CA. Sulabh Patel Member

CA. Vedant Parikh Member

CA. Vishal Langalia Member

CA. Vishank Patel Member

CA. Zalak Parikh Member

INFORMATION TECHNOLOGY MEMBERS IN INDUSTRIES

Name Designation

CA. Chairman

CA. Ravi Jain Co-Chairman

CA. Sunit Shah Convener

CA. Darshit Khetani Convener

CA. Arpit Bhahmbhatt Member

CA. Chetan Jagetiya Member

CA. Dipen Shah Member

CA. Hashmat Aswani Member

CA. Homesh Mulchandani Member

CA. Kalpeet Doshi Member

CA. Mahavir Shah Member

CA. Mayank Patel Member

CA. Neerav Shah Member

CA. Nikhar Agarwal Member

CA. Nimesh Bhavsar Member

CA. Ninad Parikh Member

CA. Sambhav Golecha Member

CA. Shivam Soni Member

CA. Vipul Ranka Member

Vikash Jain

Name Designation

CA. Chintan Patel Chairman

CA. Jaykin Shah Co-Chairman

CA. Divyang Shah Convener

CA. Ashish Shah Member

CA. Deep Thakkar Member

CA. Drashti Sanghvi Member

CA. Gaurav Kanudawala Member

CA. Gaurav Mehta Member

CA. Harshit Dalal Member

CA. Silva Shah Member

POST QUALIFICATION COURSE

Name Designation

CA. Chairman

CA. Mayurkumar Modha Co-Chairman

CA. Bhavesh Rathod Convener

CA. Ami Bodar Member

CA. Ashish Shah

CA. Chintan Lakhani

CA. Chintan Thakkar

CA. Chintankumar Shah

CA. Dhaval Limbani

CA. Disha Shah

CA. Hemang Shah

CA. Hiteshkumar Shah

CA. Jigar Limbachiya

CA. Jigneshkumar Thumar

CA. Kumar Manish

CA. Kunal Shah

CA. Malav Desai

CA. Manan Shah

CA. Manojbhai Chaudhary

CA. Mukeshkumar Dharade

CA. Nirav Shah

CA. Rahil Shah

CA. Rahul Shah

CA. Rajiv Tanna

CA. Rikinkumar Patel

CA. Rinal Jhaveri

CA. Ronak Shah

CA. Siddharth Modi

CA. Silva Shah

CA. Tushar Shah

CA. Utkarsh Desai

CA. Vibha Pandey

Bishan Shah

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

Member

PROFESSIONAL DEVELOPMENT

5

Name DesignationCA. Chairman

MentorMentor

Agrawal Nikita Vice ChairmanMehta Devanshi Kumarbhai Jt. SecretaryBhanushali Vishal H Jt. SecretaryPatel Trupil Kirankumar TreasurerAgarwal Ravi Shrichand MemberNagor Rahul Ishvarbhai Member

Bishan Shah

WICASA

6

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

Name Designation

CA. Chairperson

CA. Kaumudi Parikh Co-Chairperson

CA. Silva Shah Convener

CA. Hetal Kotak Convener

CA. Akta Patel Member

CA. Ami Desai Member

CA. Charmi Doshi Member

CA. Dipti Shah Member

CA. Disha Shah Member

CA. Hema Shah Member

CA. Hiral Gajera Member

CA. Jinal Shah Member

CA. Krishna Khandwala Member

CA. Mansi Thakkar Member

CA. Niti Ajmera Member

CA. Pooja Shah Member

CA. Pranali Thakore Member

CA. Praneeta Shukla Member

CA. Purvi Shah Member

CA. Reshma Bellani Member

CA. Shilpa Makadia Member

CA. Shruti Gandhi Member

CA. Silva Shah Member

CA. Vidhi Desai Member

CA. Vibha Pandey Member

CA. Zalak Parikh Member

Anjali Choksi

WOMEN MEMBERS EMPOWERMENT YOUNG MEMBERS SKILLS AND INNOVATION DEVELOPMENT

Name DesignationCA. Fenil Shah ChairmanCA. Palak Pavagadhi Co-ChairmanCA. Rinkesh Shah ConvenerCA. Harshid Patel ConvenerCA. Nilay Shah ConvenerCA. Abhishek Goyal MemberCA. Amita Shah MemberCA. Anand Sharma MemberCA. Aneri Sheth MemberCA. Deep Shah MemberCA. Devang Sanghvi MemberCA. Divyang Shah MemberCA. Dharmik Vora MemberCA. Harshad Maloo MemberCA. Hem Chhajed MemberCA. Himanshi Agarwal MemberCA. Hitixa Raja MemberCA. Jainam Shah MemberCA. Janak Tanna MemberCA. Jaykin Shah MemberCA. Jaykishan Vidhwani MemberCA. Jeetesh Chopra MemberCA. Jigar Shah MemberCA. Kaival Shah MemberCA. Kapil Rana MemberCA. Kaushal Trivedi MemberCA. Maulin Shah MemberCA. Mayur Vekareeya MemberCA. Milind Shah MemberCA. Mohit Balani MemberCA. Moxi Shah MemberCA. Mulen Shah MemberCA. Nikhil Makhija MemberCA. Nikhil Shah MemberCA. Nimesh Hariya MemberCA. Nimit Agarwal MemberCA. Pankaj Patel MemberCA. Parag Prajapati MemberCA. Paurav Shah MemberCA. Poorav Doshi MemberCA. Pratibha Sisodia MemberCA. Rachit Gohil Member

CA. Raj Shah MemberCA. Rohan Thakkar MemberCA. Ronak Jain MemberCA. Rushabh Sharedalal MemberCA. Sahil Gala MemberCA. Siddharth Panchal MemberCA. Siddharth Shah MemberCA. Vedant Parikh MemberCA. Vipul Ranka MemberCA. Vivek Vithlani Member

Name Designation

CA. Chairman

CA. Harshid Patel Co-Chairman

CA. Nidhiben Shah Convener

CA. Kaival Shah Member

CA. Nilaykumar Shah Member

Fenil Shah

LIBRARY & STUDENTS

Name DesignationCA. ChairmanCA. Neerav Agrawal Co-ChairmanCA. Vikas Asawa ConvenorCA. Abhishek Chopra MemberCA. Anil Choudhary MemberCA. Ankitkumar Thakkar MemberCA. Arpan Bhavsar MemberCA. Bhavik Somani MemberCA. Chetan Jagetiya MemberCA. Chintan Thakkar MemberCA. Chirag Jain MemberCA. Dheeraj Bangar MemberCA. Dilip Chechani MemberCA. Girish Gore MemberCA. Hiral Gajera MemberCA. Hiren Pathak MemberCA. Manish Dubey MemberCA. Mitt Patel MemberCA. Mohil Ramniwash MemberCA. Narayan Kela MemberCA. Parag Jagetiya MemberCA. Prignesh Mandowara MemberCA. Priyam Bhatt MemberCA. Rathin Majmudar MemberCA. Rounak Mandowara MemberCA. Sachin Dharwal MemberCA. Sahil Gala MemberCA. Utkarsh Desai MemberCA. Vaibhav Dixit MemberCA. Yogesh Shah Member

Rahul Maliwal

CPE

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

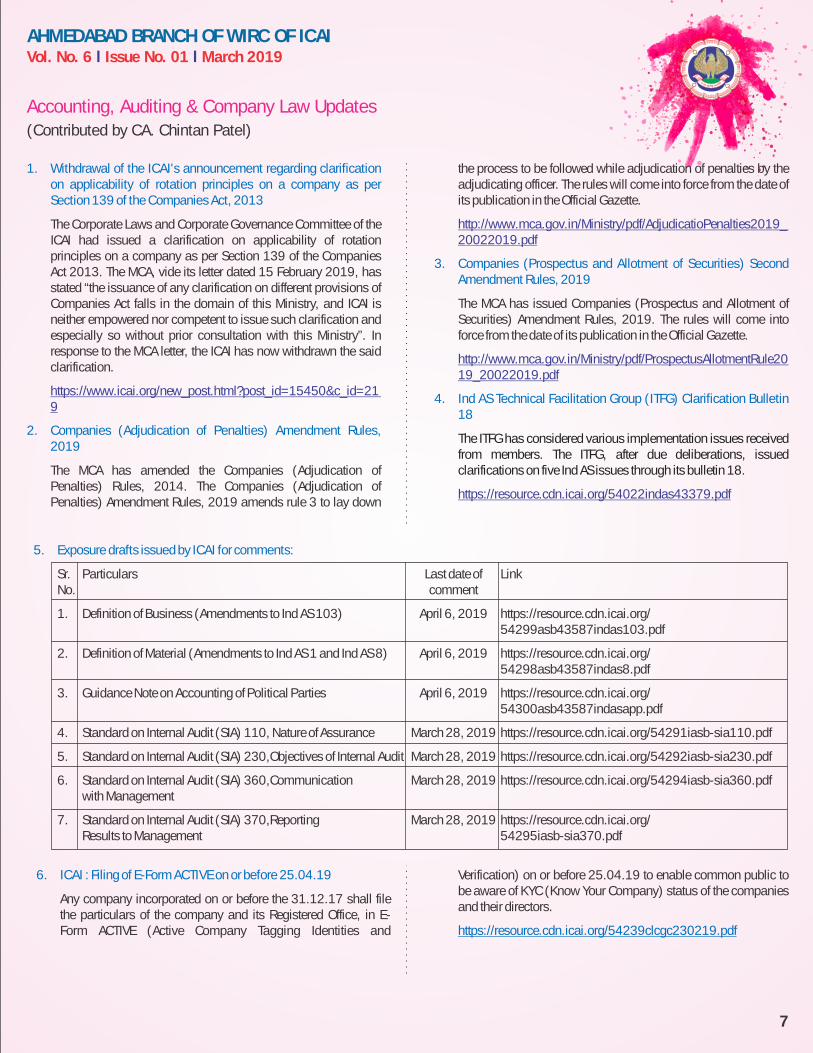

1. Withdrawal of the ICAI's announcement regarding clarification on applicability of rotation principles on a company as per Section 139 of the Companies Act, 2013

2. Companies (Adjudication of Penalties) Amendment Rules, 2019

The Corporate Laws and Corporate Governance Committee of the ICAI had issued a clarification on applicability of rotation principles on a company as per Section 139 of the Companies Act 2013. The MCA, vide its letter dated 15 February 2019, has stated “the issuance of any clarification on different provisions of Companies Act falls in the domain of this Ministry, and ICAI is neither empowered nor competent to issue such clarification and especially so without prior consultation with this Ministry”. In response to the MCA letter, the ICAI has now withdrawn the said clarification.

The MCA has amended the Companies (Adjudication of Penalties) Rules, 2014. The Companies (Adjudication of Penalties) Amendment Rules, 2019 amends rule 3 to lay down

https://www.icai.org/new_post.html?post_id=15450&c_id=219

the process to be followed while adjudication of penalties by the adjudicating officer. The rules will come into force from the date of its publication in the Official Gazette.

The MCA has issued Companies (Prospectus and Allotment of Securities) Amendment Rules, 2019. The rules will come into force from the date of its publication in the Official Gazette.

http://www.mca.gov.in/Ministry/pdf/AdjudicatioPenalties2019_20022019.pdf

http://www.mca.gov.in/Ministry/pdf/ProspectusAllotmentRule2019_20022019.pdf

https://resource.cdn.icai.org/54022indas43379.pdf

3. Companies (Prospectus and Allotment of Securities) Second Amendment Rules, 2019

4. Ind AS Technical Facilitation Group (ITFG) Clarification Bulletin 18

The ITFG has considered various implementation issues received from members. The ITFG, after due deliberations, issued clarifications on five Ind AS issues through its bulletin 18.

Accounting, Auditing & Company Law Updates(Contributed by CA. Chintan Patel)

5. Exposure drafts issued by ICAI for comments:

Sr. Particulars Last date of LinkNo. comment

1. Definition of Business (Amendments to Ind AS 103) April 6, 2019 https://resource.cdn.icai.org/54299asb43587indas103.pdf

2. Definition of Material (Amendments to Ind AS 1 and Ind AS 8) April 6, 2019 https://resource.cdn.icai.org/54298asb43587indas8.pdf

3. Guidance Note on Accounting of Political Parties April 6, 2019 https://resource.cdn.icai.org/54300asb43587indasapp.pdf

4. Standard on Internal Audit (SIA) 110, Nature of Assurance March 28, 2019 https://resource.cdn.icai.org/54291iasb-sia110.pdf

5. Standard on Internal Audit (SIA) 230,Objectives of Internal Audit March 28, 2019 https://resource.cdn.icai.org/54292iasb-sia230.pdf

6. Standard on Internal Audit (SIA) 360,Communication March 28, 2019 https://resource.cdn.icai.org/54294iasb-sia360.pdfwith Management

7. Standard on Internal Audit (SIA) 370,Reporting March 28, 2019 https://resource.cdn.icai.org/Results to Management 54295iasb-sia370.pdf

6. ICAI : Filing of E-Form ACTIVE on or before 25.04.19

Any company incorporated on or before the 31.12.17 shall file the particulars of the company and its Registered Office, in E-Form ACTIVE (Active Company Tagging Identities and

Verification) on or before 25.04.19 to enable common public to be aware of KYC (Know Your Company) status of the companies and their directors.

https://resource.cdn.icai.org/54239clcgc230219.pdf

7

8

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

SPECIAL GST COMPOSITION SCHEME LAUNCHED

CBIC on 07.03.2019 issued notification No. 2/2019-Central Tax (Rate) and Notification No. 2/2019- Union Territory Tax (Rate) prescribing a Special Composition Scheme with effect from 01.04.2019. This scheme is prescribed in form of a conditional exemption of tax in excess of 6% for those registered persons who were otherwise not eligible for opting composition scheme u/s 10 of CGST Act, 2017.

As per this scheme an eligible registered person shall have to pay tax only @ 6% on their FIRST supplies of goods or services or both up to an aggregate turnover of fifty lakh rupees made on or after the 1st day of April in any financial year.

Major highlights of this scheme are as follows:

This scheme has been prescribed for a registered person:

- Whose aggregate turnover in the preceding financial year was fifty lakh rupees or below.

- Who was otherwise not eligible to pay tax under composition Scheme u/s 10 of CGST Act, 2017.

This scheme is NOT applicable for a registered person, who is:

- Not engaged in making any supply which is not leviable to tax under the GST Acts.

- A casual taxable person.

- A non-resident taxable person.

Restrictions:

- No inter-State outward supply allowed.

- Not allowed to make any supply through an electronic commerce operator who is required to collect TCS under section 52

- Not allowed to make supply of following goods: o Ice cream and other edible ice, whether or not containing cocoa (HSN 2105 00 00), o Pan Masala (HSN 2106 90 20), All goods, i.e. Tobacco

GST Update(Contributed by CA. Monish S. Shah)

and manufactured tobacco substitutes (HSN 24).

Other Features of this scheme are as follows:

- Same scheme to be followed, by all registered persons having the same PAN.

- Not eligible to collect any tax from the recipient on supplies

- Liable to pay tax even on exempted supplies.

- Liable to pay RCM u/s 9(3) and 9(4) of CGST Act, 2017.

- Not entitled to any credit of input tax.

- Issue a bill of supply instead of tax invoice.

- Mention 'taxable person paying tax in terms of notification No. 2/2019-Central Tax (Rate) dated 07.03.2019, not eligible to collect tax on supplies' at the TOP of the bill of supply.

Some Important points:

- For the purposes of determining eligibility of a person to pay tax under this scheme, the expression “first supplies of goods or services or both” shall, include the supplies from the first day of April of a financial year to the date from which he becomes liable for registration under the said Act

- For the purpose of determination of tax payable under this notification shall not include the supplies from the first day of April of a financial year to the date from which he becomes liable for registration under the Act.

- In computing aggregate turnover, value of supply of exempt services by way of extending deposits, loans or advances in so far as the consideration is represented by way of interest or discount, shall not be taken into account.

Summary of Circular No. 92/11/2019-GST dated 7th March 2018 providing Clarification on various doubts related to treatment of sales promotion schemes under GST:

There are a lot of confusion and uncertainty on tax treatment on various type of discounts and scheme prevalent in industry. Circular No. 92/11/2019-GST dated 7th March 2018 has provided answers to many unanswered questions.

Following is the summary of said circular:

Details of Transaction Impact on Valuation Impact on ITC

Free Sample and Gifts No Supply in absence of consideration except No ITC will be available under section 17(5)(h).in situations covered in Schedule I However, ITC will be available in case

transaction covered in Schedule I.

Buy One get one free offer Either will be composite or Mixed Supply Itc will be available

Discounts including 'Buy more, save Such discounts will be excluded from valuation ITC will be available on the valuation as per more' offers: Referred as Volume subject to satisfaction of parameters of Section 15(3) Section 15.

Secondary discounts shall not be excluded while determining the value of supply

Financial/commercial Credit Notes can be raised as

credit note u/s 34 cannot be issued in these situations.

Secondary discounts shall not be excluded while

determining the value of supply

ITC will be available on full value i.e no

impact of Financial/commercial Credit

Notes on ITC

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

(A) Establishment of Branch Office (BO) / Liaison Office (LO) / Project Office (PO) or any other place of business in India by

1foreign NGOs and Non-Profit organisations

RBI has issued a A.P. (DIR Series) Circular No. 20 dated 27 February 2019clarifying that all Non-Government Organisation, Non-Profit Organization, Body/Agency/Department of a foreign Government which are undertaking activities covered under Foreign Contribution (Regulation) Act, 2010 (FCRA), shall obtain registration under said Act and not seek permission under FEMA 22(R) for opening branch office or a liaison office or a project office in India.

Similarly amendments have been made in Form FNC to specify that foreign entities would not undertake any activities covered under FCRA. Accordingly, following declaration will need to be given by all foreign entities:

“We will not undertake either partly or fully, any activity that is covered under Foreign Contribution Regulation Act, 2010 (FCRA) and we understand that any misrepresentation made or false information furnished by us in this behalf would render the approval granted under the Foreign Exchange Management (Establishment in India of a branch office or liaison office or a project office or anyother place of business) Regulations, 2016, automatically as void ab initio and such approval by the Reserve Bank shall stand withdrawn without any further notice”.

(B) ECB Facility for companies under Corporate Insolvency 2Resolution Process

RBI has relaxed the end-use restrictions for resolution applicants under the Corporate Insolvency Resolution Process (CIRP) and allowed them to raise ECBs from the recognised lenders, except the branches/ overseas subsidiaries of Indian banks, for repayment of Rupee term loans of the target company under the approval route.

Accordingly the resolution applicants, who are otherwise eligible borrowers, can forward such proposals to raise ECBs, through their AD bank, to Foreign Exchange Department, Central Office, Mumbai of the Reserve Bank for approval.

3© FAQs on ODI Updated as on 28 February 2019

RBI has updated FAQs relating to Overseas Direct Investments being made by Indian entities and has clarified on applicability of filing of Form APR based on unaudited financial statements of overseas entity.

RBI has clarified that exemption from filing the APR based on unaudited balance sheet will not be available in respect of JV/WOS in a country/jurisdiction which is either under the observation of the Financial Action Task Force (FATF) or in respect of which enhanced due diligence is recommended by FATF or any other country/jurisdiction as prescribed by Reserve Bank of India.

FEMA Updates(Contributed by CA. Saumya Sheth)

1 https://www.rbi.org.in/scripts/FS_Notification.aspx?Id=11486&fn=5&Mode=02 https://www.rbi.org.in/scripts/FS_Notification.aspx?Id=11472&fn=5&Mode=03 https://www.rbi.org.in/scripts/FS_FAQs.aspx?Id=32&fn=5

- The Assessing Officer did not concur with Hempel Singapore and he estimated profits of the PE at an ad-hoc rate of 25% of the sales and the commission paid to Hempel India was allowed as an expenditure and the net income was determined as assessed income to be taxed in the hands of Hempel Singapore in India.

- Relying on the decision of Supreme Court in case of Morgan Stanley & Co and Bombay High Court in case of SET Satellite Singapore Pte Ltd., Hempel Singapore contended that Hempel India has been compensated by Hempel Singapore on account of commission payment at arm's length price, therefore no further income or profits could be said to be attributable to Hempel Singapore in India on account of agency PE. Hempel Singapore further contended that for the very instant assessment year, during assessment of Hempel India, the Transfer Pricing Officer had accepted that thesaid commission income received by Hempel India fromHempel Singapore is at arm's length.

Judicial Pronouncements

1. Hempel Singapore Pte Ltd [ITA No. 7296/MUM/2017] [TS-74-ITAT-2019(Mum)]

- Hempel Singapore a tax resident in Singapore hadappointed its wholly owned Indian subsidiary, Hempel India as a sales agentin India and it compensated Hempel India at cost plus 8.17% mark-up as commission on sales effected through the Indian subsidiary in India.

- Hempel Singapore contended that commission paid to Hempel India is at arm's length. Hempel Singapore's stand before the tax authorities was that it was computing income attributable to its agency PE in India by applying transfer pricing provisions and commission paid to Hempel India, its agent, was equal to the income attributable to the agency PE, and hence the resultant taxable income in India was Nil.

(Contributed by CA. Twinkle S. Shah)International Taxation Updates

9

10

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

services rendered while carrying on the business, it was liable to be visited with TP-adjustment on account of interest income short charged/uncharged. High Court had upheld the opinion of Tribunal that charging of interest on delayed receipt of receivables was a separate international transaction which required to be benchmarked independently

3. Hydrosult Inc [TS-43-ITAT-2019(Ahd)]

- For rendering technical consultancy services under the irrigation contract, Hydrosult Inc. had hired various independent foreign professionals from the Netherlands, Australia, UK etc.

- Hydrosult Inc. contended that the services received from these individuals are in the nature of independent personal services governed by Article 14 'Independent Personal Services' (IPS) of the respective treaties. Since none of the consultants had a fixed base available to them in India for the purposes of performing their respective activities and since none of them had stayed in India for a period exceeding 183 days, hence no income was chargeable to tax in India and no tax at source was deducted.

- The Assessing Officer observed that services rendered were in the nature of technical and consultancy services and would thus fall in the Fee for Technical Services (FTS) article in contrast to the IPS article. The Assessing Officer further observed that services rendered by the professionals are not independent in character and hence the article on FTS of the relevant DTAA is squarely applicable and tax at source shall be deducted at source by Hydrosult Inc.

- Referring to a specimen agreement entered into between Hydrosult Inc and one of the consultants based in the Netherlands, Tribunal observes that the obligations arising from the contract cannot be assigned to some other persons unlike in the case of an employer; Holds that, “In view of risk fastened with the non-residents for their services, it is clear that the services are of independent nature.” Accordingly, Ahmedabad Tribunal rules that consultancy fees payment to foreign consultants in relation to irrigation development project awarded by Govt. of India, falls under the ambit of Article 14 of respective DTAAs on IPS

- Mumbai Tribunal accepts the contention of Hempel Singapore that commission payment to Hempel Indiaby Hempel Singapore is on arm's length basis, which has indeed been affirmed by the income-tax authorities in the case of Indian subsidiary for the instant assessment year, therefore, no further income could be attributable to its agency PE again.

2. McKinsey Knowledge Centre India Pvt Ltd vs. Pr CIT[SLP No.(s) 1785/2019]

- The Supreme Court (SC) dismissed the SLP filed by Mckinsey against the order of High Court in its own case and stated that it is not inclined to entertain theSLPunder Article 136 of the Constitution of India”.

Nature of Services – BPO vs. KPO

- The High Court characterised the research and information services provided by McKinsey to its Associated Enterprises as high-end knowledge process outsourcing services (KPO) provider as against Mckinsey's characterisation of its functions as a routine business process outsourcing services (BPO).

- The High Court had held that services rendered by McKinsey are specialized and require specific skill-based analysis and research that is beyond the more rudimentary nature of services rendered by a BPO. Therefore, the services provided by McKinsey are more akin to a KPO and accordingly the mark-up earned by them should be compared to other KPO companies rather than BPO.

- The crux of the issue lies in the fact that the tax authorities contend that there are differentiating features between the BPO and KPO activities based on their functions, assets and risks and hence require different bench marking and mark-up percentages. Even the Safe Harbour Rules in India (applicable to cases with value of transactions below specified thresholds) provides for 17-18% operating margin from a BPO as compared to 18 – 24% from a KPO.

Interest on Delayed Receivables

- Before High Court Mckinsey had contended that early or late realization of sale/ service proceeds was incidental to the transaction of sale/ service objecting separate benchmarking of interest. High Court had rejected this contention holding that if there was any delay in the realization of a trading debt arising from the sale of goods or

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

1. Circular No. 5/2019dated 05.02.2019 - Monetary limits for

filing/withdrawal of Wealth Tax appeals by the Department

before ITAT, HCs and SLPs/appeals before SC through

extending the scope of Circular 3 of 2018 -Measures for

reducing litigation.

Reference is invited to Board's Circular No. 3 of 2018 dated

11.07.2018 (hereinafter, referred to as "the Circular") vide

which monetary limits for filing of income tax appeals by the

Department before Income Tax Appellate Tribunal, High Courts

and SLPs/ appeals before Supreme Court were specified. Para

11 of the Circular states that the monetary limits specified in para

3 shall not apply to writ matters and Direct tax matters other than

Income tax and filing of appeals in such cases shall continue to

be governed by relevant provisions of statute and rules.

There is no charge under Wealth Tax Act, 1957 w.e.f 1st April,

2016. Therefore, as a step towards litigation management, it

has been decided by the Board that monetary limits for filing of

appeals in Income tax cases as prescribed in Para 3 of the

Circular shall also apply to Wealth Tax appeals through

extension of the Circular to Wealth tax matters in a mutatis

mutandis manner

2. CORRIGENDUM TO CIRCULAR NO.1 OF 2019 DATED 01 .01

.2019 issued on 08.02.2019 - Income-Tax Deduction from

Salaries during the Financial Year 2018-19 under Section 192

of the Income-tax Act, 1961-regarding.

The correct position of the admissibility of deduction under

section 80TTB is provided as under: - "Section 80TTB introduced

by Finance Act, 2018, w.e.f 01 .04.2019, allows deduction to a

senior citizen from his gross total income in respect of income by

way of interest on deposits with- (a) a banking company to

which the Banking Regulation Act, 1949 (10 of 1949), applies

(including any bank or banking institution referred to in section

51 of that Act); (b) a co-operative society engaged in carrying

on the business of banking (including a co-operative land

mortgage bank or a co-operative land development bank); or

(c) a Post Office as defined in clause (k) of section 2 of the

Indian Post Office Act, 1898 (6 of 1898), The amount of

https://www.incometaxindia.gov.in/communications/circular/c

ircular_5_2019.pdf

Direct Tax Updates(Contributed by CA. Mohit Tibrewal)

deduction in respect of above interest on deposit is as under: - (i)

in a case where the amount of such income does not exceed in

the aggregate fifty thousand rupees, the whole of such amount;

and (ii) in any other case, fifty thousand rupees.

However, no deduction is allowed under section 80TTB to any

partner of the firm or any member of the association or any

individual of the body if said interest is derived from any deposit

held by, or on behalf of, a firm, an association of persons or a

body of individuals.

For this purpose, "senior citizen" means an individual resident in

India who is of the age of sixty years or more at any time during

the relevant previous year. However, taxpayers claiming

deduction under section BOTTB shall not be eligible for

deduction under section 80TTA".

3. Press Release dated 01.02.2019 – Direct tax highlights of the

Interim budget 2019-20.

https://www.incometaxindia.gov.in/communications/circular/r

evised_corrigendum_80ttb_11_2_19.pdf

- Income upto Rs. 5 lakh exempted from Income Tax.

- Standard Deduction to be raised to Rs. 50,000 from Rs.

40,000 for salaried employees.

- TDS threshold to be raised from Rs. 10,000 to Rs. 40,000

on interest earned on bank/post office deposits.

- Existing rates of income tax to continue.

- Tax exempted on notional rent on a second self-occupied

house.

- Housing and real estate sector to get boost-

o TDS threshold for deduction of tax on rent to be

increased from Rs. 1,80,000 to Rs. 2,40,000.

o Benefit of rollover of capital gains increased from

investment in one residential house to two residential

houses for capital gains up to Rs. 2 crore.

11

12

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

o Tax benefits for affordable housing extended till 31st

March, 2020 under Section 80-IBA of Income Tax Act.

- Tax exemption period on notional rent, on unsold

inventories, extended from one year to two years.

The level of income-tax compliance has continuously increased

over the last three Financial Years, which is reflected in the

number of Income-Tax Returns filed over this period, as given

hereunder: -

S.No. Financial Year Total Number of Percentage increaseIncome Tax over previousRefund filed Financial Year

1 2015-16 4.63 Crore 14.6%

2 2016-17 5.57 Crore 20.3%

3 2017-18 6.86 Crore 23.2%

The total amount of refunds made to the assesses during the

period under reference is as under:

Financial Year Refund (Rs. Crore)

2015-16 122271

2016-17 162661

2017-18 151602

nd 2018-19 (up to 2 February 2019) 143117

thAs on 15 January 2019, 3,07,485 returns including 36,616

cases of refunds are pending for scrutiny. The scrutiny of these

cases is to be completed by 31.12.2019. A total of 16,21,848

claims of refund (including non-scrutiny cases) are pending for

issue as on 31st January, 2019.

http://www.pib.nic.in/PressReleseDetail.aspx?PRID=1562187

4. Press Release dated 12.02.2019 – Income Tax Refunds

Since only about 0.5% of the returns is selected for scrutiny,

refunds are issued expeditiously at the time of processing itself

for the bulk of the taxpayers. With regard to the pending scrutiny

cases, the Assessing Officers have already been advised in the

Central Action Plan for 2018-19 to expedite assessment in such

cases, especially cases selected for “limited scrutiny”, so that

resultant refunds, if any, can be issued at the earliest.

.

The head of a prominent organisation allegedly indulging in

anti-national activities alongwith his associates were covered in

a sensitive search action by the Income Tax Department today.

Search action has been conducted at 4 premises in the Valley

and 3 in the national capital. The search action has yielded

credible evidence of large scale undisclosed financial

transactions carried out in the business of quarrying, hotels etc.

During the search, clinching evidence was also unearthed of

huge unaccounted expenditure having been incurred in cash on

the reconstruction and remodelling of the residential premises

presently being used by the tax evader's family. Despite carrying

out large scale financial transactions, neither the main

protagonist nor any member of his family has ever filed any

income tax return. The evidence found in search action is robust

enough to show a deliberate and wilful attempt to evade tax.

In the search action, 3 hard discs have also been seized. The

analysis of the information contained in the discs is likely to yield

even more substantial evidence against the tax evader and his

associates. This action is part of a concerted drive to trace illegal

sources of funding that have financed the separatist elements

and their activities in the Valley.

5. Press Release dated 26.02.2019 - Income Tax Department

hits at terror financing activities in J&K Region

http://www.pib.nic.in/PressReleseDetail.aspx?PRID=1564079

http://www.pib.nic.in/PressReleseDetail.aspx?PRID=1566579

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

allottee as it defined the same as a group/collective of allottee by

whatever name called, registered under any law for the time being in

force.

The said lacuna has been filled up in Rule 9(1) of GujRERA Rule,

which talk about the execution of agreement for sale shall be in the

form as per “Annexure A “given in Rule and as per clause 9 of the

model form of agreement, allottees of apartment in building shall join

in forming and registering the society or Association or a Limited

Company to be known by such name as the promoter may decide and

for this purpose also from time to time sign and execute the

application for registration and/or membership and the other papers

and documents necessary for the formation and registration of the

society or Association or Limited Company and for becoming a

member including the bye-laws of the proposed Society and duly fill

in, sign and return to the promoter within seven days of the same

being forwarded by the Promoter to the Allottee, so as to enable the

promoter to register the common organisation of allottee.

Explanation:-The above clause of model agreement for sale give

better clarity the it is the joint duty of allottees and promoter to form the

association of allottee.

Further to this, the above clause give the clarity on formation of

association also which clearly says that association can be formed in

any way i.e. Society/Association or Limited Company.

Gujarat Real Estate Regulatory Authority (GujRERA Authority) has

issued one order i.e. GujRERA Order No. 13 dated 09.07.2018 where

it has directed that association of allottee cannot be formed by way of

Company, LLP or Society but it has to be under the Gujarat Co-

Operative Society Act, 1961.

While issuing this order GujRERA Authority has considered the

provision of Section 4 along with the section 7 of Gujarat Co-Operative

Society Act, 1961.

However the GujRERA Authority has issued another order i.e. GujRERA

Order No-18 dated 18.12.2018 where it has clarified that association

can be formed by way of Society under Gujarat Co-Operative Society

Act, 1961 or as a company under Section 8 of the Companies

Act,2013.

Real Estate (Regulation and Development) Act, 2016

Provisions and rules related to “Association of allottee” and

formation of association of allottee:-

Real Estate (Regulation and Development Act), 2016 (RERA) does

not defined the terminology “association of allottee” while the same is

defined in Gujarat Real Estate (Regulation and Development)

(General) Rule 2017 (GujRERA Rule).

As per GujRERA Rule 2(1)(c) “association of allottees” means a

collective of the allottees of a real estate project, by whatever name

called, registered under any law for the time being in force, acting as

group to serve the cause of its members, and shall include the

authorised representative of the allottees.

Section 11 of RERA describe the function and duties of the promoter

and Section 11(4)(e) of the act said that, Promoter shall enable the

formation of society or co-operative society or federation of allottee

under the laws applicable.

Further proviso to this section says that in absence of local law, the

association of allottee shall be formed within 3 months of the majority

of allotment is done in real estate project.

Explanation:- it is important to note that word used in section

11(4)(e) is that the promoter has to “enable” the formation of

association and it does not bind the promoter to form the association.

Further to this, proviso of the section says that the association “shall

be form” but who (promoter or allottees) will form the association is

not clear in the Act.

Apart from the above point, that who shall form the association one

another point is not cleared in RERA i.e. related to status/nature/form

of association of allottee.

Section 11(4) (e) talk about the formation of society/co-operative

society/federation of society under the law applicable while proviso

says that association may be form by whatever name called, if there is

no local law.

Even in definition of association given in GujRERA Rule 2(1)(c) does

not specify that what will be the status/nature/form of association of

(Contributed by CA. Mahadev Birla)RERA

13

14

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

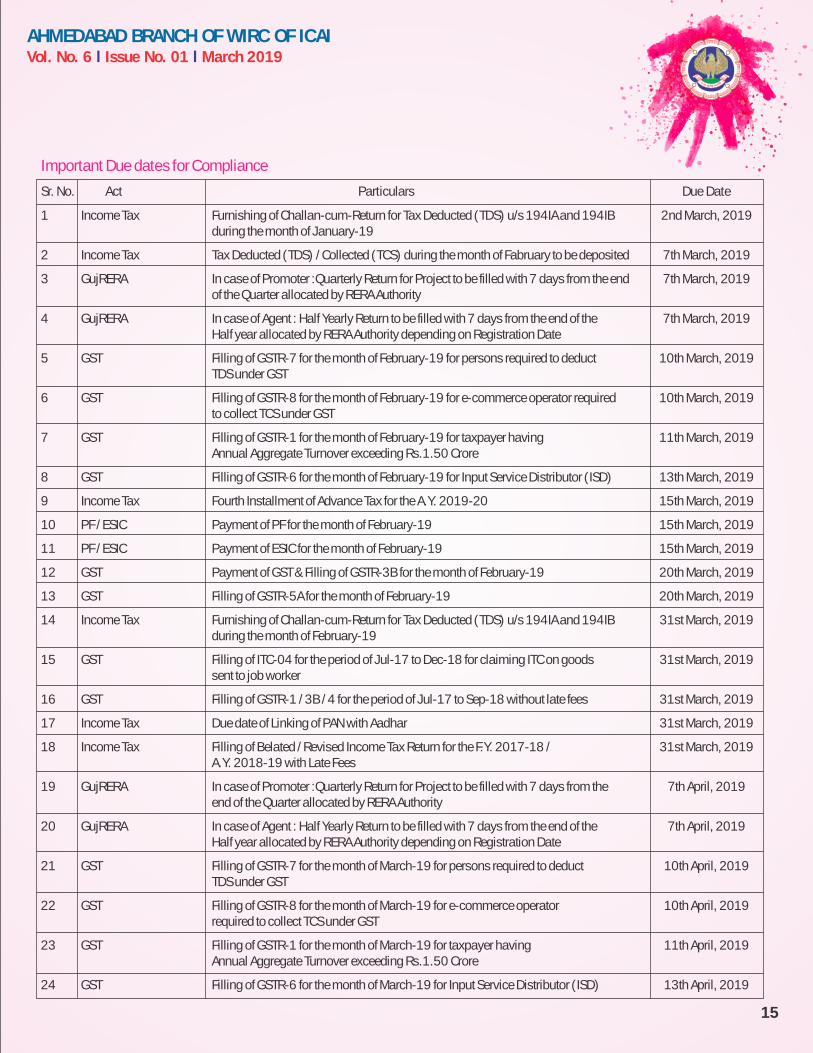

Important Due dates for Compliance

Sr. No. Act Particulars Due Date

1 Income Tax Furnishing of Challan-cum-Return for Tax Deducted (TDS) u/s 194IA and 194IB 2nd March, 2019during the month of January-19

2 Income Tax Tax Deducted (TDS) / Collected (TCS) during the month of Fabruary to be deposited 7th March, 2019

3 GujRERA In case of Promoter :Quarterly Return for Project to be filled with 7 days from the end 7th March, 2019of the Quarter allocated by RERA Authority

4 GujRERA In case of Agent : Half Yearly Return to be filled with 7 days from the end of the 7th March, 2019Half year allocated by RERA Authority depending on Registration Date

5 GST Filling of GSTR-7 for the month of February-19 for persons required to deduct 10th March, 2019TDS under GST

6 GST Filling of GSTR-8 for the month of February-19 for e-commerce operator required 10th March, 2019to collect TCS under GST

7 GST Filling of GSTR-1 for the month of February-19 for taxpayer having 11th March, 2019Annual Aggregate Turnover exceeding Rs.1.50 Crore

8 GST Filling of GSTR-6 for the month of February-19 for Input Service Distributor (ISD) 13th March, 2019

9 Income Tax Fourth Installment of Advance Tax for the A.Y. 2019-20 15th March, 2019

10 PF / ESIC Payment of PF for the month of February-19 15th March, 2019

11 PF / ESIC Payment of ESIC for the month of February-19 15th March, 2019

12 GST Payment of GST & Filling of GSTR-3B for the month of February-19 20th March, 2019

13 GST Filling of GSTR-5A for the month of February-19 20th March, 2019

14 Income Tax Furnishing of Challan-cum-Return for Tax Deducted (TDS) u/s 194IA and 194IB 31st March, 2019during the month of February-19

15 GST Filling of ITC-04 for the period of Jul-17 to Dec-18 for claiming ITC on goods 31st March, 2019sent to job worker

16 GST Filling of GSTR-1 / 3B / 4 for the period of Jul-17 to Sep-18 without late fees 31st March, 2019

17 Income Tax Due date of Linking of PAN with Aadhar 31st March, 2019

18 Income Tax Filling of Belated / Revised Income Tax Return for the F.Y. 2017-18 / 31st March, 2019A.Y. 2018-19 with Late Fees

19 GujRERA In case of Promoter :Quarterly Return for Project to be filled with 7 days from the 7th April, 2019end of the Quarter allocated by RERA Authority

20 GujRERA In case of Agent : Half Yearly Return to be filled with 7 days from the end of the 7th April, 2019Half year allocated by RERA Authority depending on Registration Date

21 GST Filling of GSTR-7 for the month of March-19 for persons required to deduct 10th April, 2019TDS under GST

22 GST Filling of GSTR-8 for the month of March-19 for e-commerce operator 10th April, 2019required to collect TCS under GST

23 GST Filling of GSTR-1 for the month of March-19 for taxpayer having 11th April, 2019Annual Aggregate Turnover exceeding Rs.1.50 Crore

24 GST Filling of GSTR-6 for the month of March-19 for Input Service Distributor (ISD) 13th April, 2019

15

16

AHMEDABAD BRANCH OF WIRC OF ICAIVol. No. 6 Issue No. 01 March 2019l l

Disclaimer : The Ahmedabad Branch of WIRC of ICAI is not in any way responsible for the result of any action taken on the basis of the advertisement published in the Newsletter.The members, however, may bear in mind the provision of the Code of Ethics while responding to the advertisements.

AHMEDABAD BRANCH OF WIRC OF ICAIICAI Bhawan, 123, Sardar Patel Colony, Near Usmanpura Under Bridge, Naranpura, Ahmedabad - 380 014

Phone : 079-3989 3989, 2768 0946, 2768 0537 Email : [email protected] Web : www.icaiahmedabad.org

All Gujarat Income Tax Open House on 20.02.2019 Lecture Meeting on Interim Budget 2019 on 07.02.2019

ICAI Convocation on 2019 on 01.02.2019

Live Screening of Union Budget 2019 on 01.02.2019 Seminar on UDIN - An Easy Way to Secure Certificates on 06.02.2019

Lecture Meeting on SME Listing and It’s Benefits on 22.02.2019 Post Qualification Course on ISA PT from 16.02.2019