acc308 lecture 4 bentley 2

TRANSCRIPT

Curtin University is a trademark of Curtin University of TechnologyCRICOS Provider Code 00301J

School of Accounting

Accounting Theory and Analysis 308

TOPIC 3: Business Decision Making Related to Measurement and Disclosure and the Role of Accounting Theories – Part BChapter 5

Materials prepared by Lisa Cullen, selected slides from • Godfrey, J., A. Hodgson, A. Tarca, J.

Hamilton, and S. Holmes, 2010. Accounting Theory. Wiley

• Rankin, M. 2012. Contemporary Issues in Accounting, Wiley ©2012 John Wiley & Sons Australia Ltd

• Deegan, C. 2009, Financial Accounting Theory, McGrawHill

Chapter 5Theories in Accounting

What Value Does Theory Offer?

• Theories guide many activities• Accounting theories help us understand– Decisions of financial report prepares

– Actions of financial report users– Influences of organisational environment

– Potentially better measurement and reporting

• Accounting is a human activity

Types Of Theories• Normative Theories

– Recommend what should happen– Prescribe action to achieve specific objectives

– E.g. The Conceptual Framework• Positive Theories

– Describes, explains or predicts activities

– Help us understand what happens in the world

– E.g. Agency theory

Positive Accounting Theory• Used to explain and predict accounting practice.• It examines a range of relationships between the entity and – suppliers of equity capital (owners), – managerial labour (management)– debt capital (lenders or debt holders)

• based on the ‘rational economic person’ assumption– assumes investors and financial accounting users and preparers are rational utility maximisers

– Also described as self-interested wealth maximisers• In order to prescribe an appropriate accounting policy, it is necessary to know how the world actually operates. We can then normatively prescribe accounting practice

Contracting Theory• Suggests that the organisation is characterised as a legal ‘nexus of contracts’.

• With contracting parties having rights and responsibilities under these contracts.

• Positive accounting theory focuses on– managerial contracts, and – debt contracts,

• These are agency contracts used to manage relationships where there is a separation between management and capital providers. (information asymmetry)

Agency Theory• Used to understand relationships whereby a principal employs the services of, and delegates the decision making authority to, an agent.

• Creates a moral hazard.• Leads to 3 ‘costs’

– Monitoring costs – audit– Bonding costs – salaries, bonus, restrict accounting policy choices

– Residual loss – cant remove all opportunistic costs.

How do owners restrict managers as agents opportunistic or self-interest behaviour?

Owner–Manager Agency Relationships

• Agency theory identifies a number of problems that can exist between managers and owners.

• Contracts and accounting information can be used to ‘bond’ the interests of owners and managers.

• Addresses 3 specific problems– Horizon problem– Risk aversion– Dividend retention.

Manager–Lender Agency Relationships

• When a lender agrees to provide funds to an entity there is the risk that the lending party may not repay those funds.– Excessive dividend payments (fewer assets to pay debt)– Underinvestment or over investment in high risk projects – Asset substitution (lower value)– Claim dilution (taking on more debt)

• Debt holders charge interest in line with risk - To avoid higher interest costs managers have incentives to show they are acting in a way that is not detrimental to lenders.

• Note: Research has found Managers have manipulated accounting accruals in the years before and the year after violation of a debt agreement.

• Auditors need to be vigilant

Australian debt contracts

• In relation to Australian debt contracts, Cotter (1998) found– leverage covenants frequently used in bank loan contracts

– leverage most frequently measured as the ratio of total liabilities to total tangible assets

– prior charges covenants typically included in term loan agreements of larger firms

– prior charges covenants defined as a percentage of total tangible assets

– debt to assets, interest coverage and current ratio clauses frequently in use

– interest coverage required to be between 1½ and 4 times

– current ratio clauses required current assets be between 1 and 2 times the size of current liabilities

10

Role of Accounting Information in Reducing Agency Problems

• Accounting information forms one of the major components of both manager remuneration and lending contracts.

• For managers accounting information plays two roles in the contracting process: 1. To write the terms of managerial contracts.2. To determine performance against the terms of the

contracts and consequently the amount of bonus and other pay components managers will receive.

• Lenders look to regular financial updates to ensure companies are maintaining the terms of their covenants.

Information Asymmetry• Results from managers having more information about the current and future prospects of the entity than outsiders.

• Managers can choose when and how to disseminate this information.

• Under positive accounting theory there are incentives to disclose most news, good or bad, to the market.

Key Hypotheses• Three key hypotheses frequently used in PAT literature to explain and predict support or opposition to an accounting method– bonus plan hypothesis (bonus attached to profits)

– debt hypothesis (debt covenants) – political cost hypothesis (large firms may seek to choose methods to reduce reported profits)

• Research assumes managers will act opportunistically when selecting methods

13

Incentives to manipulate accounting numbers

• Rewarding managers on the basis of accounting profits may induce them to manipulate accounting numbers (the opportunistic perspective)– will affect their rewards

• Bonuses based on profits cause short-term rather than long-term focus– may affect investment in positive NPV projects if returns not expected to be consistent

– Evidence shown in studies by Healy (1985) & Lewllen et al (1987)

14

Market-based bonus schemes

• May be more appropriate to remunerate managers in terms of market value where accounting earnings fluctuate greatly– e.g. mining, or high technology R&D firms

• Methods include– cash bonus based on share price increases– shares– options to shares

• Managers have incentives to increase the value of the firm• Problems include

– share price also affected by factors beyond the control of managers (e.g. general market movements)

– only senior managers likely to have a significant impact on share value

15

Institutional Theory• Comes from management literature.• It considers how rules, norms and routines become established as authoritative guidelines, and considers how these elements are created, adopted and adapted over time.

• Practices within organisations can be predicted from perceptions of legitimate behaviour derived from cultural values, industry tradition, entity value etc

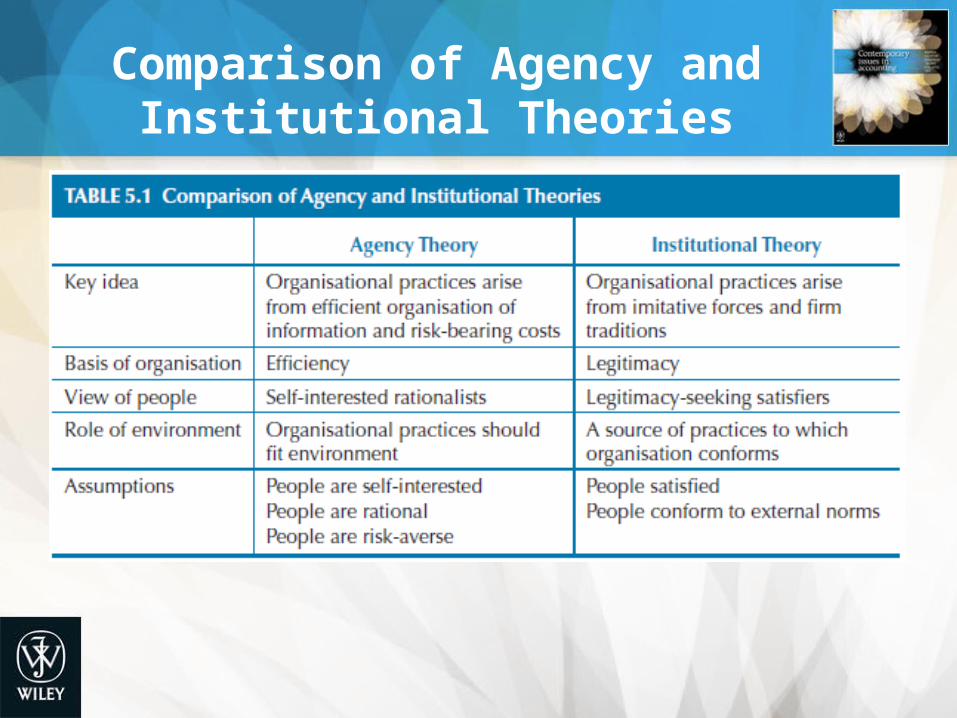

Comparison of Agency and Institutional Theories

Legitimacy Theory• Based on the idea of a social contract

– Relates to the explicit and implicit expectations society has about how businesses should act to ensure they survive into the future.

– The values and norm evident in the social contract have changed over time.

– Organisations need to show they are operating in accordance with the expectations in the social contract.

– In the past legitimacy was considered only in terms of economic performance.

– Now businesses are now expected to consider a range of issues, including the environmental and social consequences of their activities.Implications of not meeting the social

contract?• Legal restrictions• Limited resources provided• Reduced demand or products banned

Accounting Disclosures and Legitimation

• Lindblom identifies four ways an organisation can obtain or maintain legitimacy:1. Seek to educate and inform society about actual

changes in the organisation’s performance and activities

2. Seek to change the perceptions of society, but not actually change behaviour

3. Seek to manipulate perception by deflecting attention from the issue of concern to other related issues

4. Seek to change expectations of its performance.

Accounting Disclosures and Legitimation

• Disclosure of information about an organisation’s effect on, or relationship with society can be used in each of the strategies.– An entity might provide information to offset negative news which may be publicly available.

– An organisation may draw attention to strengths.• Public reporting through the annual report or the entity website can be a powerful tool in showing an organisation is meeting the expectations of society.

• Accounting numbers can also be manipulated to show lower profits for example if a particular industry is under scrutiny for making too high profits (thereby addressing part of the perceived social contract)

Legitimacy Theory - Empirical Studies

• Patten (1992)• examined the change in the extent of environmental disclosures of US oil firms around the Exxon Valdez oil spill in Alaska

• legitimacy theory suggested that they would increase disclosure in the annual report after the spill

• found the increase in disclosure occurred across the industry

• Deegan and Rankin (1996)• used Legitimacy Theory to explain changes in annual report environmental disclosure policies around proven environmental prosecutions

• prosecuted firms disclosed significantly more environmental information in the year of prosecution than any other year

• prosecuted firms disclosed more information than non-prosecuted firms

• Legitimacy Theory is different to, but is aligned with the Political Cost Hypothesis (PCH) of positive accounting theory

• PCH- Highly visible firms are likely to adopt accounting methods to reduce profits to lower political scrutiny

Stakeholder Theory• Considers the relationships that exist between the organisation and its various stakeholders.

• Stakeholders are ‘any group or individual who can affect or is affected by the achievements of an organisation’s objectives’

• There are two versions of stakeholder theory– a normative theory, known as the ‘ethical branch’,

– an empirical theory of management, which is a positive theory

Normative Branch of Stakeholder Theory

• Argues that organisations should treat all their stakeholders fairly.

• An organisation should be managed for the benefit of all its’ stakeholders.

• Stakeholders are identified, and should be considered in organisational decisions because of their interest in the activities of the organisation.

Managerial Branch of Stakeholder Theory

• Seeks to explain how stakeholders influence organisational actions.

• The extent to which an organisation will consider its stakeholders is related to the power or influence of those stakeholders.– A stakeholders’ power is related to the degree of control they have over resources required by the organisation.

Role of Accounting Information in Stakeholder Theory

• One important way of meeting stakeholders’ needs and expectations is providing information about organisational activities and performance. (Annual Report)

• Stakeholder theory has been used to examine disclosure of voluntary information to stakeholders, most commonly relating to social and environmental performance.

Contingency Theory• Proposes that organisations are all affected by a range of factors that differ across organisations.

• Organisations need to adapt their structure to take into account a range of factors such as – External environment.– Organisational size.– Business strategy.

Contingency Theory• Contingency frameworks have been used to evaluate management accounting information and internal control systems.

• They conclude that– There is no universally appropriate accounting system that can be applied to all organisations.

– Features of appropriate accounting systems are contingent upon the specific circumstances the organisation faces.

Using Theories To Understand Accounting

Decisions• Accountants use judgement to make a range of accounting decisions on a daily basis.

• Examples include:– Whether to expense or capitalise costs.– What accounting estimates to use.– What, where and how to disclose information.

• Theories offer some assistance in explaining managers’ and accountants’ decisions.

Expensing and Capitalising Costs

• Agency theory would hold that – Managers on compensation contracts which have bonuses tied to a current measure of entity performance

– Entities with lending agreements with a leverage covenant,

• would prefer to capitalise costs.• Institutional theory would explain the influence of external norms on managerial compensation policy.

Accounting Estimates• Agency contracts can explain managerial decisions in this regard. – Managers and accountants, acting in self interest, are likely to ensure their own bonuses are maximised and the entity is not at risk of breaching debt contracts.

• Legitimacy and stakeholder theory suggest there are times entities, for political reasons, will actively reduce their reported profits.

Disclosure Policy• Disclosure policy relates to additional disclosure within the annual report or media releases.

• Stakeholder theory would explain these disclosures in terms of providing relevant information to maintain relationships with powerful stakeholders.

• Legitimacy theory sees voluntary disclosure as a way of maintaining or regaining legitimacy by demonstrating how the entity is meeting societal expectations.

Next Week • Chapter 6 –Products of the financial reporting process

• Chapter 10 - Fair value – what is it, how is it calculated and does it result in a measure that will result in better business decisions?