2020/21 ksp policy consultation report - knowledge sharing

TRANSCRIPT

Presented by the MOEF, Republic of Korea

2020/21 KSP Policy Consultation Report

2020/21 KSP Policy Consultation ReportDevelopm

ent of Microfinance through Strengthening

Legal Role and Supervisory Capacity Building in Myanm

ar

Myanmar Development of Microfinance through Strengthening Legal Role and Supervisory Capacity Building in Myanmar

Government Publications Registration Number

11-1051000-001100-01

Myanmar Development of Microfinance through Strengthening Legal Role and Supervisory Capacity Building in Myanmar

2020/21 KSP Policy Consultation Report

KSP-미얀마-final.indd 1 2021-11-29 오후 2:59:57

Government Publications Registration Number 11-1051000-001100-01ISBN 979-11-5932-642-4 979-11-5932-641-7 (set)Copyright ⓒ 2021 by Ministry of Economy and Finance, Republic of Korea

Project Title DevelopmentofMicrofinancethroughStrengtheningLegalRoleandSupervisoryCapacity

Building in Myanmar

Prepared for Republic of the Union of Myanmar

In cooperation with Ministry of Planning, Finance and Industry

Supported by Ministry of Economy and Finance (MOEF), Republic of Korea

Prepared by Korea Development Institute (KDI)

Project Directors Jungwook Kim, Executive Director, Center for International Development (CID), KDI

Sanghoon Ahn, Former Executive Director, CID, KDI

Project Manager Hokyung Bang, Director of Division of Policy Consultation, CID, KDI

ProjectOfficers Hanbit Jung, Research Associate, Division of Policy Consultation, CID, KDI

Eunjung Yang, Senior Research Associate, Division of Policy Consultation, CID, KDI

Senior Advisor Woong-Seob Zhin, Former Governor of Financial Supervisory Service, Republic of Korea

Principal Investigator Joonhyuk Song, Professor, Hankuk University of Foreign Studies

Authors Chapter1. BumyoalLee,SeniorAdvisor,FinancialSupervisoryService

Chapter 2. Joonhyuk Song, Professor, Hankuk University of Foreign Studies

Thida Tun, Independent Researcher

Chapter3. Ji-YunLee,Manager,KoreaInclusiveFinanceAgency

Sung-Min Cheon, Head of Household Support Planning & Management Division,

Korea Asset Management Corporation

UNaingMinLatt,StaffOfficer,FinancialRegulatoryDepartment,Ministryof

Planning, Finance and Industry

English Editor KoreaTranslationsCo.,Ltd.

2020/21 KSP Policy Consultation Report

KSP-미얀마-final.indd 2 2021-11-29 오후 2:59:57

2020/21 KSP Policy Consultation ReportDevelopment of Microfinance through

Strengthening Legal Role and Supervisory Capacity Building in Myanmar

KSP-미얀마-final.indd 3 2021-11-29 오후 2:59:57

PrefaceKnowledge is an essential ingredient in a country’s economic growth and social development. Of

particular importance is a government’s capacity to formulate and implement policies. The global

society is focused on implementing the Sustainable Development Goals (SDGs), which promotes

knowledge sharing between countries in order to improve their policy capacity and to tackle

development issues and enhance global prosperity.

Indeed, knowledge has taken on an ever-greater importance as the world continues to confront the

COVID-19 pandemic. During this crisis which has caused limited physical interactions, the value of

knowledge-sharing through innovation and technology has become more evident considering these

methodsofferthemostflexibleandpromptopportunitiestodevelopandsharetimelysolutions.

When it comes to Korea’s economic development, knowledge laid the foundation for Korea’s

unprecedented transformation from a poor agro-based economy into a modern industrialized nation

with an open and democratic society. Technology transfer from abroad and educational investments

helped expand the domestic knowledge stock and made this transformation possible. The Korean

government accumulated invaluable practical lessons not found in conventional textbooks through

its course of economic development.

As a result, Korea’s Ministry of Economy and Finance (MOEF) introduced the Knowledge Sharing

Program (KSP) in 2004 to share Korea’s development experience with the international community

through joint research, policy consultations, and capacity-building activities. Since its inception, the

program has played a vital role in supporting socio-economic development of partner countries

around the world.

The Korea Development Institute (KDI) has participated in implementing KSP since the program’s

launch and has been working with more than eighty foreign countries. KDI, Korea’s leading think-

tank with an extensive experience in policy research, has provided solutions to the challenges that

partner countries face in a variety of fields ranging from industrial development to public-sector

reform. In the 2020/21 KSP cycle, KDI carried out twenty-three policy consultation projects including

with two new participant countries — Albania and Uruguay.

Among the many meaningful 2020/21 KSP projects for mutual learning, one in particular worth

highlighting, was initiated by Myanmar’s Ministry of Planning, Finance and Industry (MPFI) entitled,

“DevelopmentofMicrofinancethroughStrengtheningLegalRoleandSupervisoryCapacityBuilding

in Myanmar.” Based on MPFI’s request, MOEF and KDI organized a virtual research team consisting

KSP-미얀마-final.indd 4 2021-11-29 오후 2:59:57

of Burman and Korean experts. The team conducted an in-depth analysis of internal and external

policy environments, identified Myanmar’s key development challenges, and offered policy

recommendations and action plans.

Although the COVID-19 pandemic continued to proliferate in 2020/21 and despite many restrictions

duringthistime,theprojectwasimplementedeffectivelybyutilizingvariousmethodstoimprove

interaction and mutual understanding with our partner countries. Moreover, the project was

successfully completed thanks to the cooperation and devotion from both the country and KDI

teams.

On behalf of KDI, I would like to express my deepest appreciation to the Director General, Financial

Regulatory Department (FRD), MPFI for their collaboration in the project. In particular, I would

like to extend my profound gratitude to His Excellency U Zaw Naing, Director General, Mr. U Ko Ko

Maung,DeputyDirector,andMr.UNaingMinLatt,OfficerattheFRDfortheirunwaveringsupport.

The completion of this project would not have been possible without their devotion. I also wish to

thank the KSP consultation team—Senior Advisor Woong-Seob Zhin, Principal Investigator Professor

JoonhyukSong,researchersBumyoalLee,Ji-YunLeeandSung-MinCheonandlocalconsultantsMr.

UNaingMinLattandMs.ThidaTun—forproducingthisreport.

ThisprojectbenefitedgreatlyfrommanyothersbothinsideandoutsidetheMyanmargovernment.

I would like to extend my sincere thanks to all who have made valuable contributions to a successful

completion of the project. I am also grateful to the Center for International Development of KDI, in

particular Executive Director Dr. Jungwook Kim, Former Executive Director Dr. Sanghoon Ahn, Project

ManagerDr.HokyungBang,andProjectOfficerMs.HanbitJung,fortheirhardworkanddedication

to the project.

IfirmlybelievethattheKSPwillserveasasteppingstonetofurtherelevatemutuallearningand

economic cooperation between Myanmar and Korea, and hope it will contribute to their sustainable

development.

Jang Pyo Hong

President

Korea Development Institute

KSP-미얀마-final.indd 5 2021-11-29 오후 2:59:57

Contents2020/21 KSP with Myanmar ············································································································ 015Executive Summary ·························································································································· 019

Chapter 1 Recommendations for Improving Microfinance Regulations and Supervision

Summary ·········································································································································· 0251. Introduction ·································································································································· 0282.MicrofinanceinMyanmar ············································································································ 029 2.1.MicrofinanceLandscapeandSupervisoryStructure ·························································· 029 2.2.RulesandRegulationsofMicrofinance ··············································································· 032 2.3. Financing Needs and Market Infrastructures ····································································· 0343.Korea’sExperienceinMicrofinanceSupervision ········································································ 037 3.1. Financial Supervisory System in Korea ················································································ 037 3.2. Nonbank Financial Institutions ···························································································· 038 3.3. Regulations for MSBs and Moneylenders ··········································································· 041 3.4. Examination and Enforcement Actions ··············································································· 046 3.5. Self-regulatory Organizations ······························································································ 0534.ChallengesintheMicrofinanceMarketandKorea’sSupervisoryEfforts ································· 054 4.1. Prudential Supervision and Market Impact ········································································ 054 4.2.SupervisoryEffortstoAdvancetheMicrofinanceIndustry ················································ 057 4.3.LimitationsandConcernsRelevanttotheSupervisionoftheMicrofinanceMarket ········ 0595.DiscussionsandRecommendationsforDevelopmentofMicrofinanceinMyanmar ·············· 061 5.1. ImprovementofSupervisoryEfficiency ··············································································· 061 5.2. Rationalization of Current Regulations ··············································································· 064 5.3. Responding to Changes in the Market Environment·························································· 0696. Conclusions ··································································································································· 071References ········································································································································ 073Appendices ······································································································································· 076

KSP-미얀마-final.indd 6 2021-11-29 오후 2:59:57

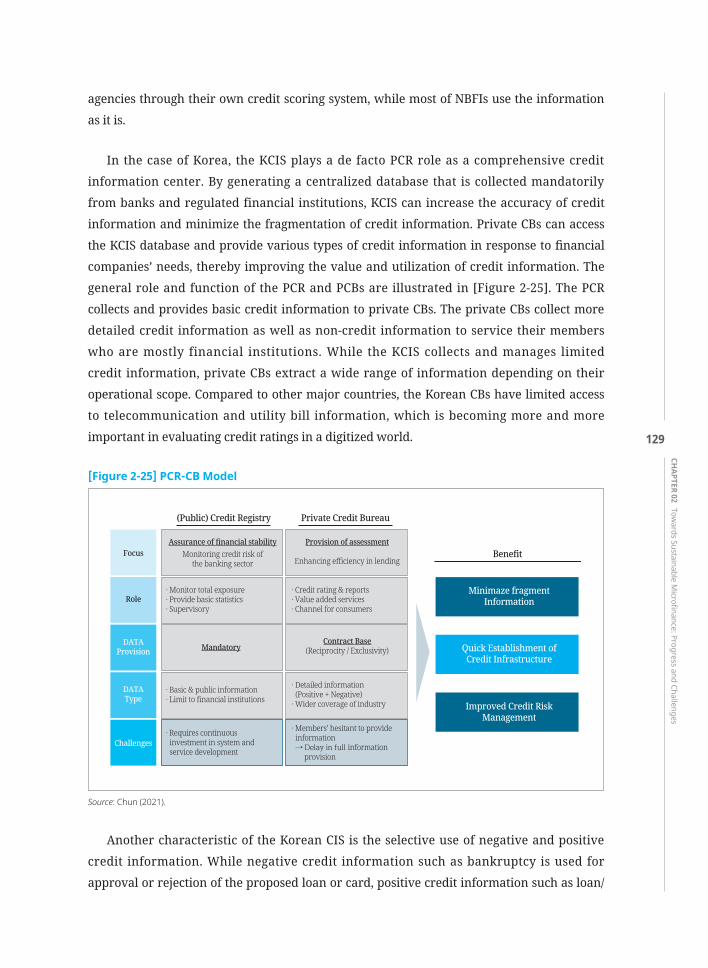

Chapter 2 Towards Sustainable Microfinance: Progress and Challenges

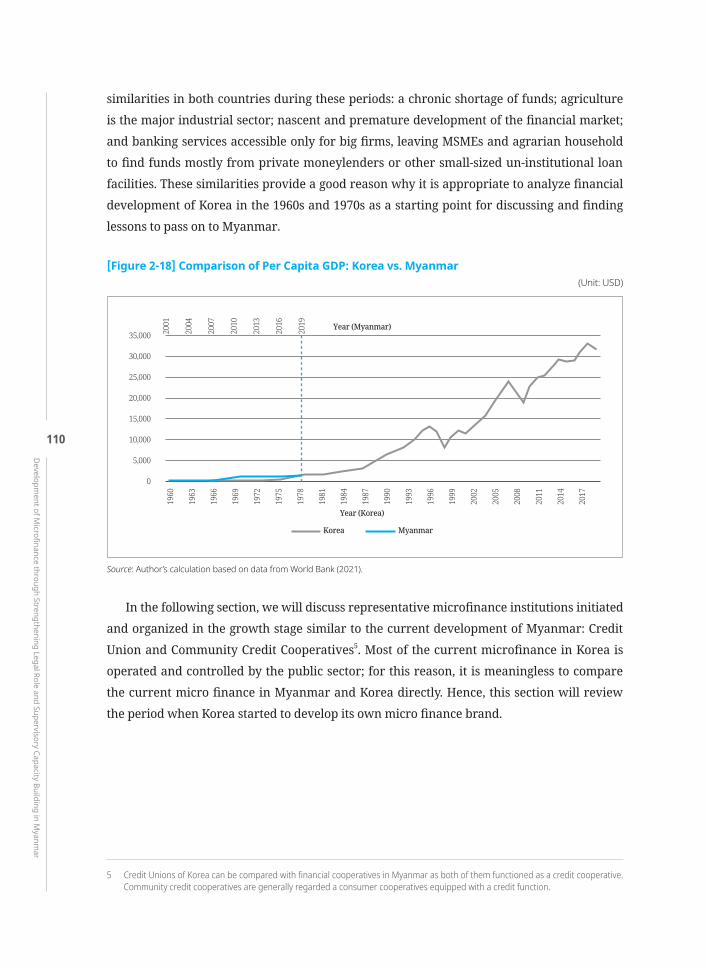

Summary ·········································································································································· 0791. Introduction ·································································································································· 0812. Recent Developments and Review of Myanmar’s Financial Markets ········································ 085 2.1.RecentDevelopmentsintheFinancialMarketandMicrofinanceIndustry ······················ 085 2.2. Global Competitiveness of the Financial Sector ·································································· 097 2.3. InitiativestoUpgradetheMicrofinanceSector ·································································· 101 2.4. IssuesandChallengesintheMyanmarMicrofinanceIndustry ········································· 1043.Korea’sExperienceinMicrofinance ····························································································· 107 3.1.MicrofinanceinRetrospective ······························································································ 107 3.2.TraditionalMicrofinance:CFIs ······························································································ 1114. Korea’s Experience with the Credit Information System (CIS) ··················································· 125 4.1. The Outline of CIS ················································································································· 125 4.2. CIS of Korea ··························································································································· 1275.PolicyRecommendationstowardsaSustainableMicrofinanceIndustryinMyanmar ············ 131 5.1. Extending the Scope and Role of the Credit Information System ····································· 131 5.2. Enhancing the Role and Responsibility of the Central Agency··········································· 1356. Conclusion ···································································································································· 137References ········································································································································ 139Appendix ··········································································································································· 141

Chapter 3 Public Microfinance and the Debt Relief System: Korean Experiences

Summary ·········································································································································· 1471. Introduction ·································································································································· 1512.TheLocalFinancialEnvironmentofMyanmar ··········································································· 152 2.1. Financial Market ···················································································································· 152 2.2. Banking Industry ·················································································································· 154 2.3.MicrofinanceSectorinMyanmar ························································································· 155 2.4. Policy Finance and Myanmar’s State-Owned Banks ··························································· 1583. Inclusive Finance in Korea ··········································································································· 160 3.1.PublicMicrofinance ·············································································································· 160

KSP-미얀마-final.indd 7 2021-11-29 오후 2:59:57

3.2. Debt Relief System in Korea ································································································· 1734. Conclusion ···································································································································· 183References ········································································································································ 190

Contents

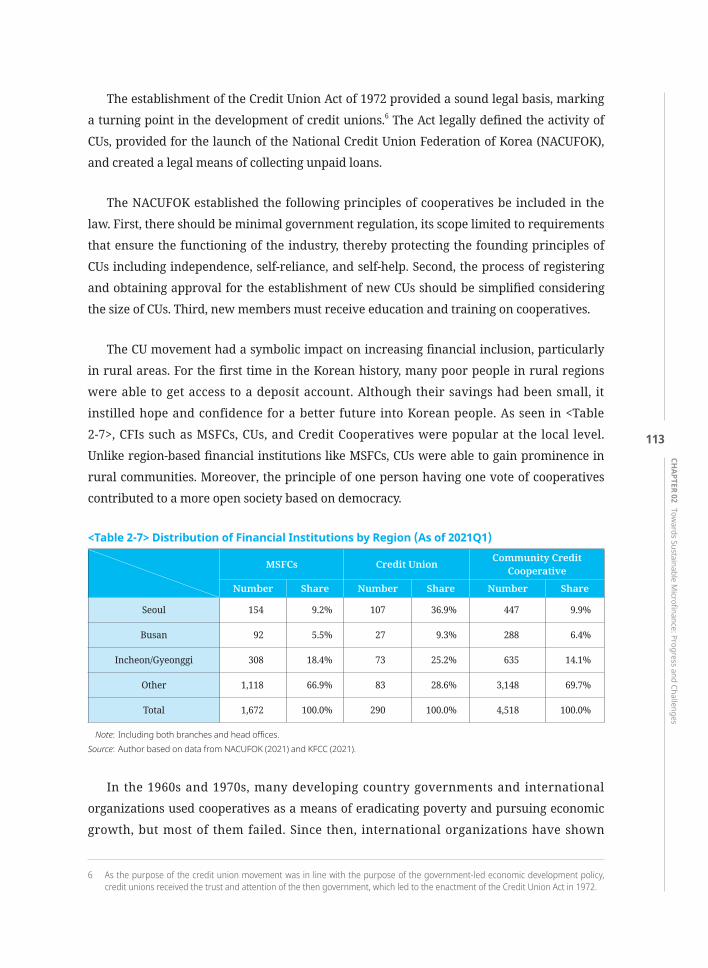

KSP-미얀마-final.indd 8 2021-11-29 오후 2:59:57

Chapter 1

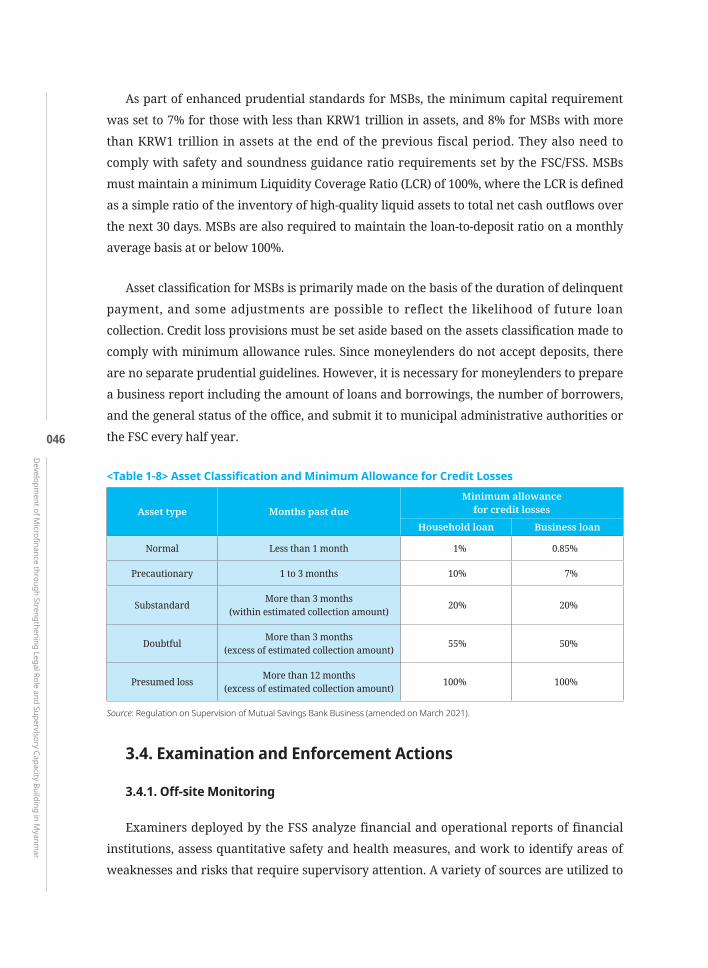

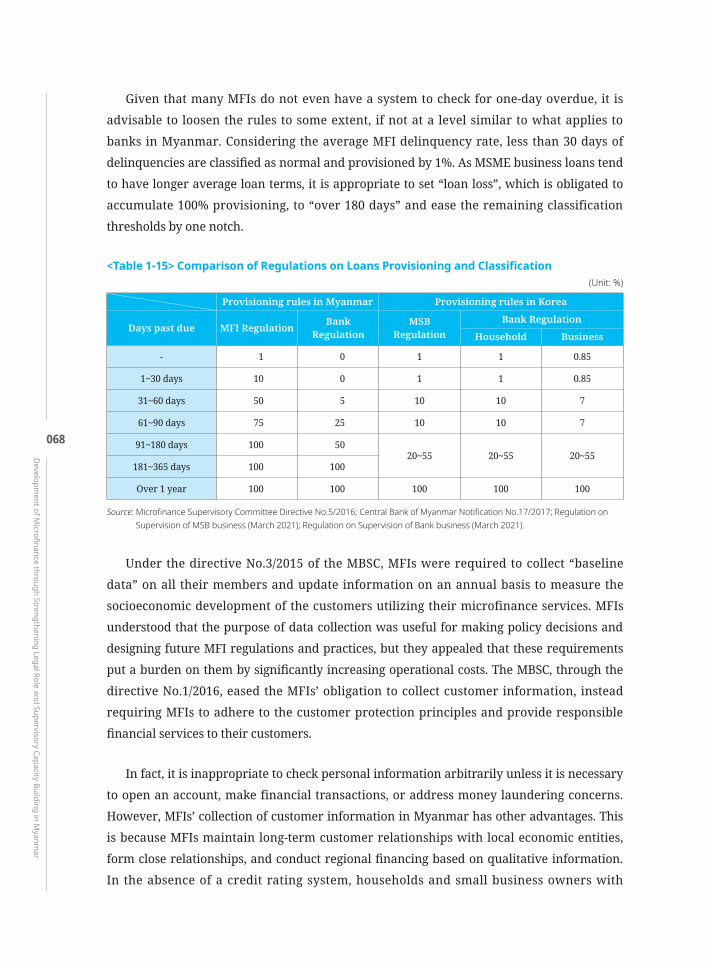

<Table1-1> MicrofinanceCoverageAreainMyanmar ····························································· 032<Table1-2> MajorRulesandRequirementsforMicrofinanceInstitutions ····························· 033<Table1-3> RegulationsonLoansProvisioningandClassification ·········································· 034<Table 1-4> Mutual Savings Banks’ Soundness Indicators ······················································· 040<Table 1-5> Number of Registered Moneylenders···································································· 041<Table1-6> Moneylenders’LoanBalanceandAverageInterestRate ····································· 041<Table 1-7> Major Rules and Requirements for MSB and Moneylenders ······························· 042<Table1-8> AssetClassificationandMinimumAllowanceforCreditLosses ·························· 046<Table 1-9> Post-examination Actions ······················································································· 049<Table 1-10> Summary of MSBs’ Business Report ······································································ 050<Table 1-11> Rating Components and Evaluation Factors ························································· 051<Table 1-12> Remedial Actions under Prompt Corrective Action ··············································· 052<Table 1-13> Key Functions of Korea Federation of Savings Banks ··········································· 053<Table1-14> KeyFunctionsoftheConsumerLoanFinanceAssociation ··································· 054<Table1-15> ComparisonofRegulationsonLoansProvisioningandClassification ················ 068

Chapter 2

<Table 2-1> Overview of SOBs ··································································································· 086<Table2-2> AssetsandNumberofBranchesof10LargestDomesticPrivateBanks (As of Fiscal Year-End 2017) ···················································································· 086<Table2-3> NumberofListedCompanies ················································································· 089<Table 2-4> Financial Status of the Top 20 MFIs ········································································ 091<Table 2-5> Code of Conduct for MFIs ······················································································· 103<Table 2-6> Foreign Assistance to Korea’s Credit Unions (As of Jan 31, 1972) ························· 112<Table 2-7> Distribution of Financial Institutions by Region (As of 2021Q1)··························· 113<Table 2-8> Distribution of Religious Population of Korea in 1984 ·········································· 116<Table 2-9> Source of Financing of Saemaul Project ································································· 117<Table2-10> LocationofFarmer’sSavingsbasedonAnnualIncomein1975 ·························· 118<Table2-11> UseofLoanfromCCs ······························································································ 118<Table 2-12> Coverage of Credit Information ············································································· 130<Table 2-13> Countries with/without PCR and CB ······································································ 131

Contents l List of Tables

KSP-미얀마-final.indd 9 2021-11-29 오후 2:59:57

Chapter 3

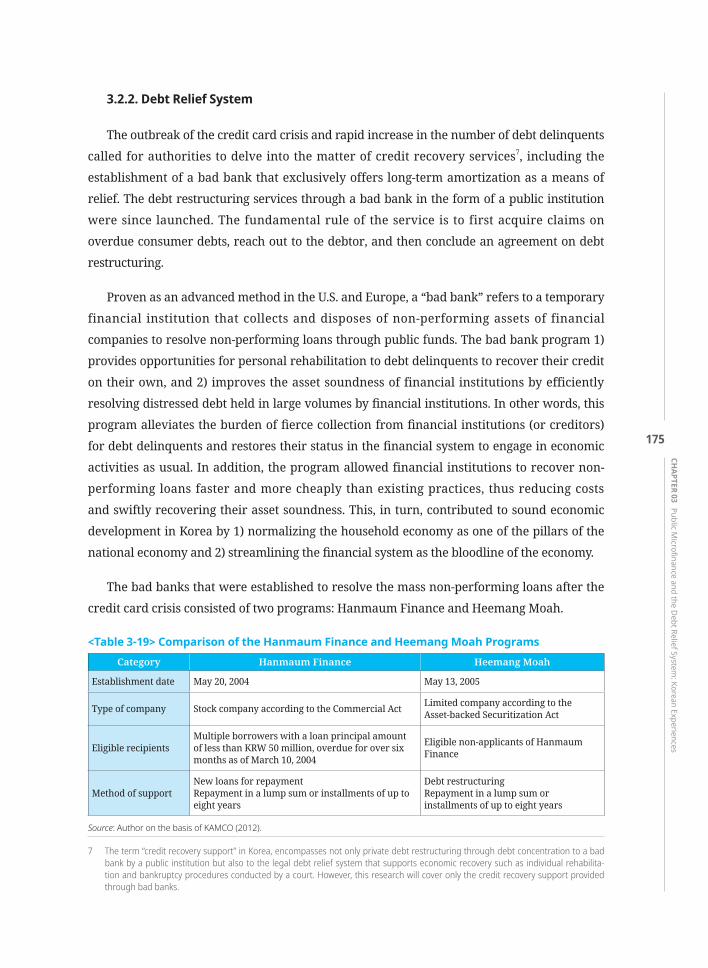

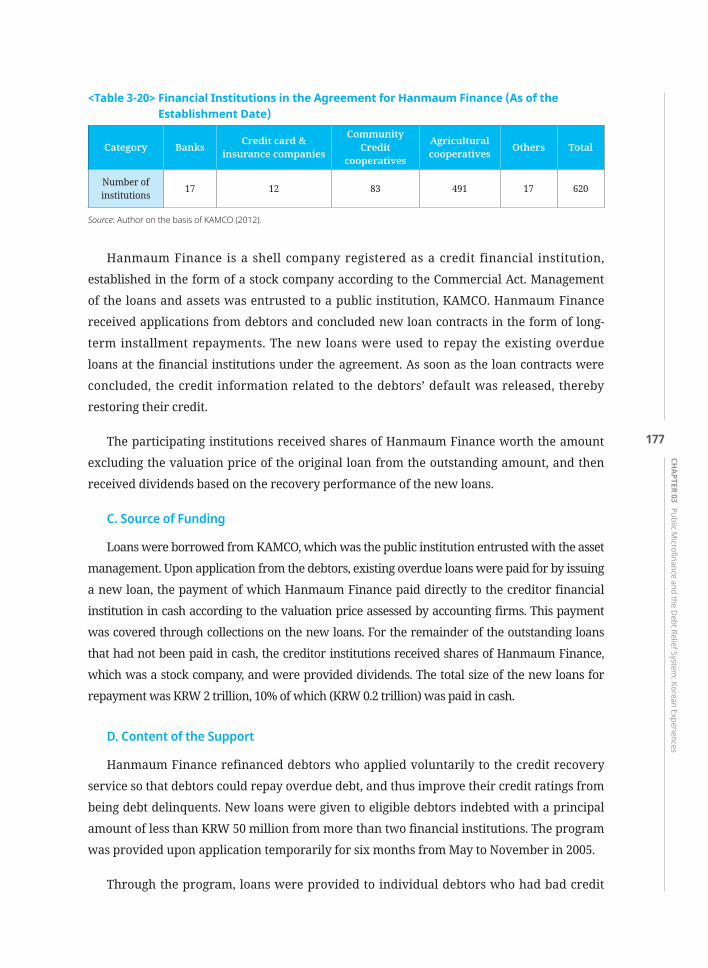

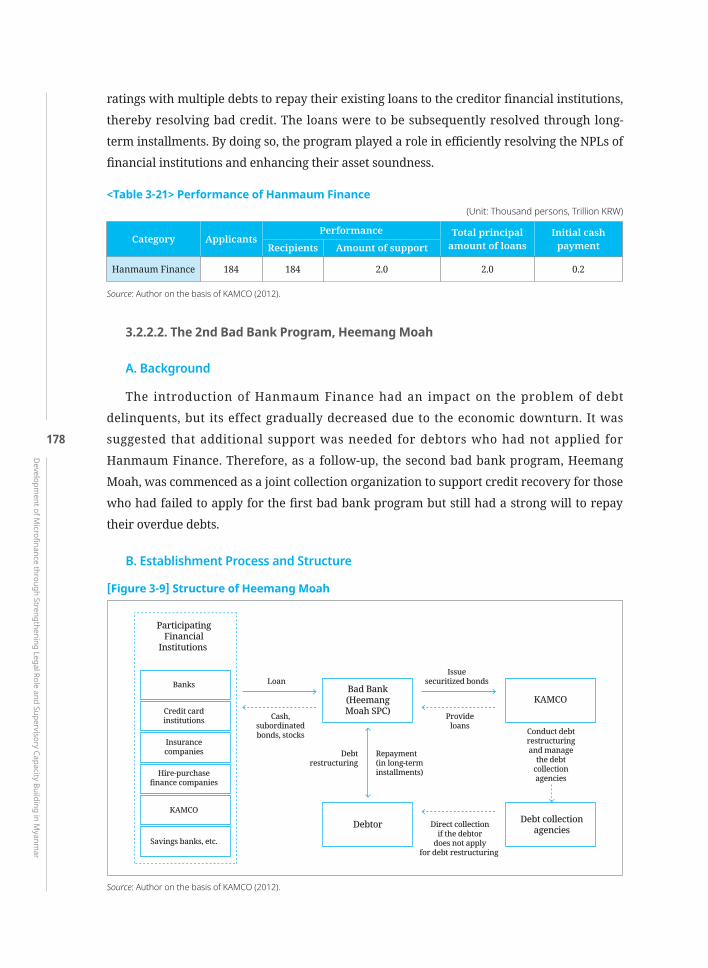

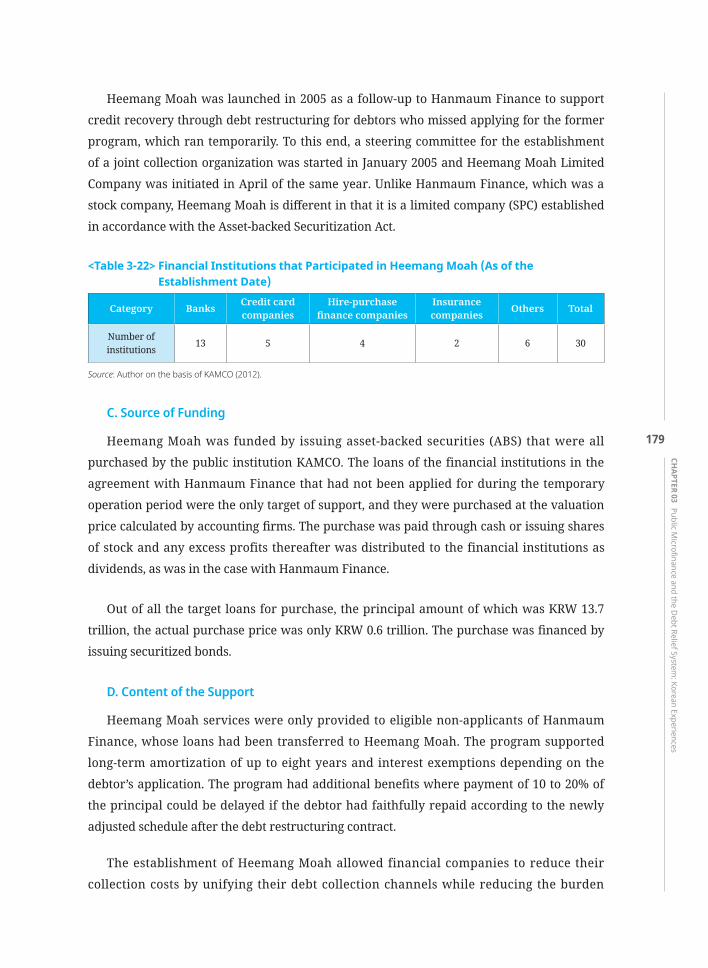

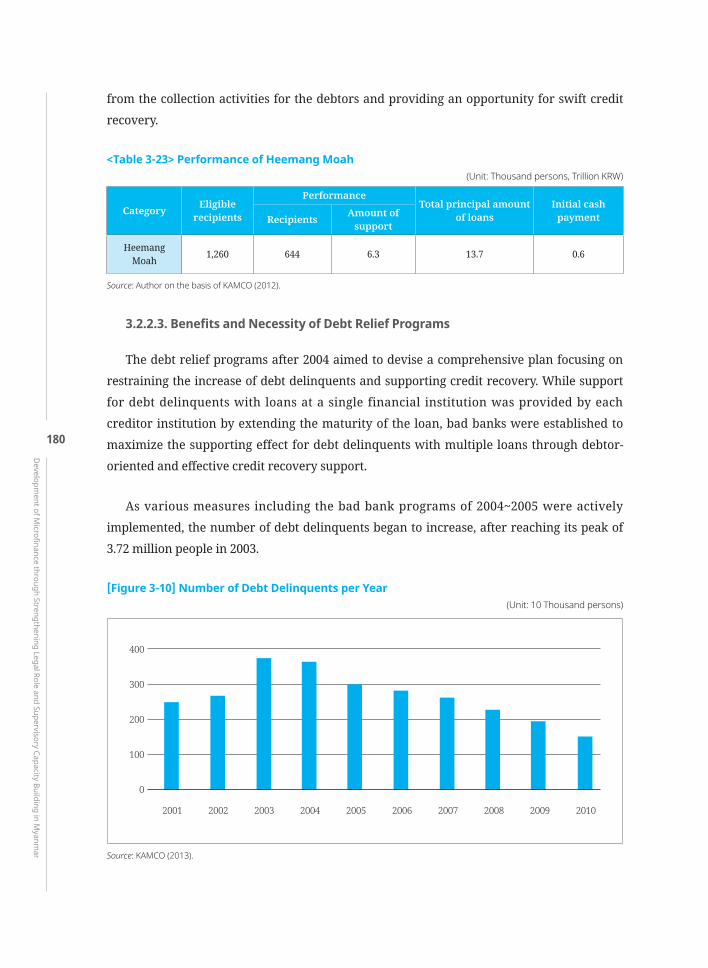

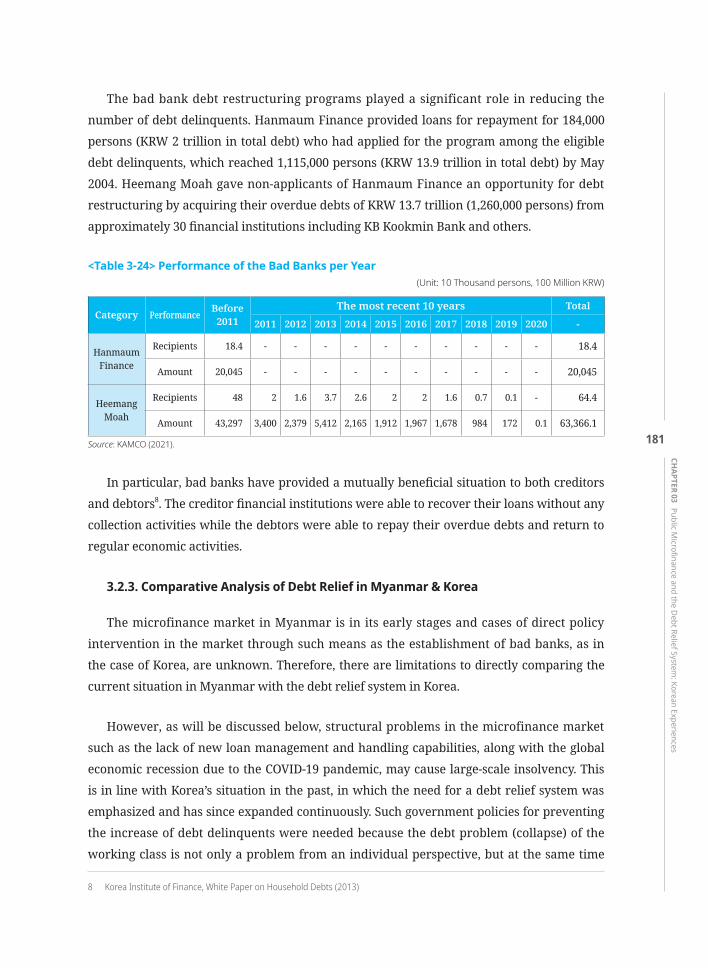

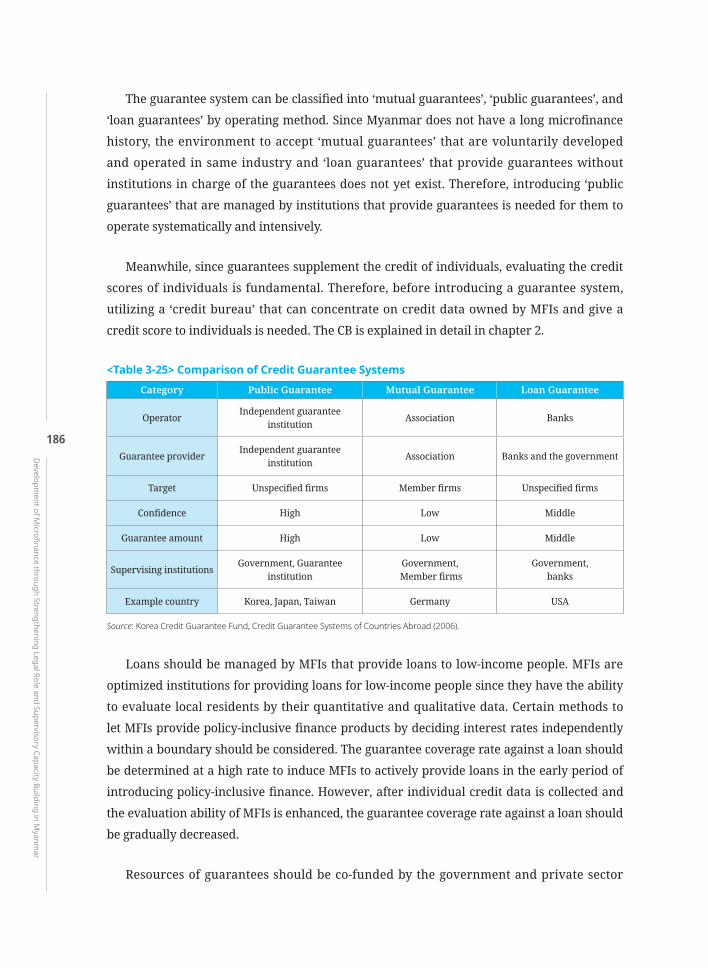

<Table3-1> InformalLendingSysteminMyanmar ·································································· 154<Table 3-2> Deposits and Credit Functions of Banks in Myanmar ··········································· 155<Table3-3> DepositsandCreditFunctionsofMicrofinanceinMyanmar ······························· 157<Table 3-4> State-Owned Banks’ Financial Products and Services and Outreach Areas ········· 158<Table3-5> MADBLoanConditions ··························································································· 160<Table3-6> MisoCreditLoanRequirementsandtheSourceofFunding ································ 164<Table3-7> SunshineLoanRequirementsandtheSourceofFunding ··································· 165<Table3-8> PublicMicrofinanceSupportPerformanceTrends(2008~2020) ·························· 166<Table3-9> LoanPerformanceofPolicy-InclusiveFinancebyGender(2008~2020) ·············· 166<Table3-10> LoanPerformanceofPolicy-InclusiveFinancebyAge(2008~2020) ···················· 167<Table3-11> LoanPerformanceofPolicy-InclusiveFinancebyIncome(2008~2020) ·············· 167<Table3-12> ComparisonoftheInterestRateonCreditLoansfromPublic MicrofinanceandFinancialCompanies(2020) ····················································· 168<Table 3-13> Financial Education System ···················································································· 168<Table 3-14> Financial Education Topics ······················································································ 169<Table 3-15> Business Type and Areas of Consulting ································································· 170<Table3-16> ComparisonofPublicMicrofinanceinMyanmarandKorea ································ 172<Table 3-17> Usage of Credit Cards ····························································································· 174<Table 3-18> Delinquency Rate of Credit Card Institutions ························································ 174<Table 3-19> Comparison of the Hanmaum Finance and Heemang Moah Programs ············· 175<Table 3-20> Financial Institutions in the Agreement for Hanmaum Finance (As of the Establishment Date) ··············································································· 177<Table 3-21> Performance of Hanmaum Finance ······································································· 178<Table 3-22> Financial Institutions that Participated in Heemang Moah (As of the Establishment Date) ··············································································· 179<Table 3-23> Performance of Heemang Moah ············································································ 180<Table 3-24> Performance of the Bad Banks per Year ································································ 181<Table 3-25> Comparison of Credit Guarantee Systems····························································· 186

Contents l List of Tables

KSP-미얀마-final.indd 10 2021-11-29 오후 2:59:57

Contents l List of Figures

Chapter 1

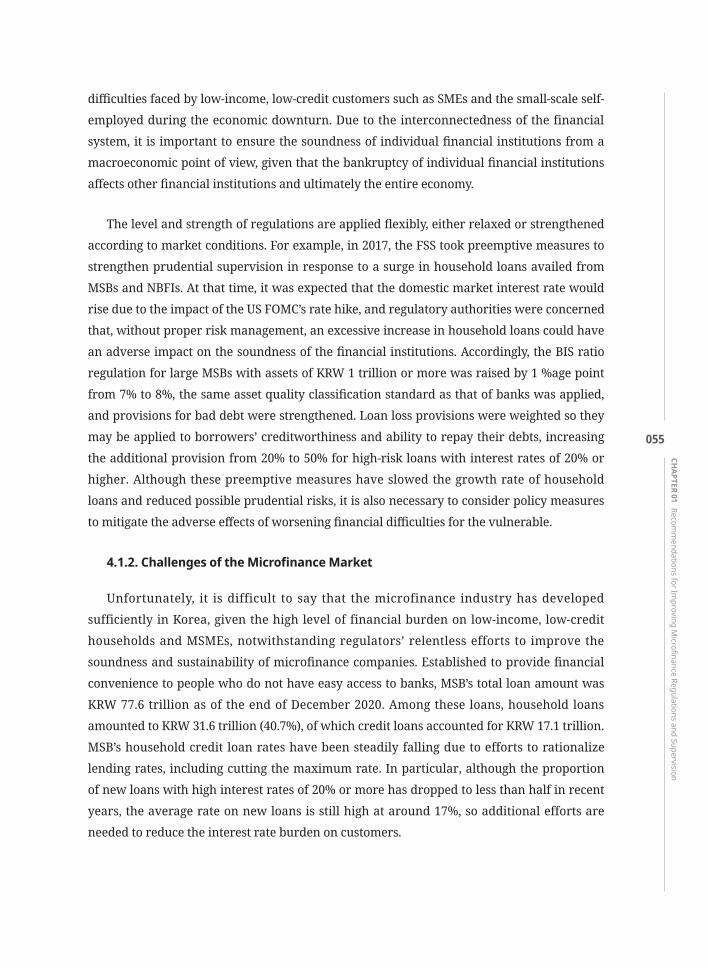

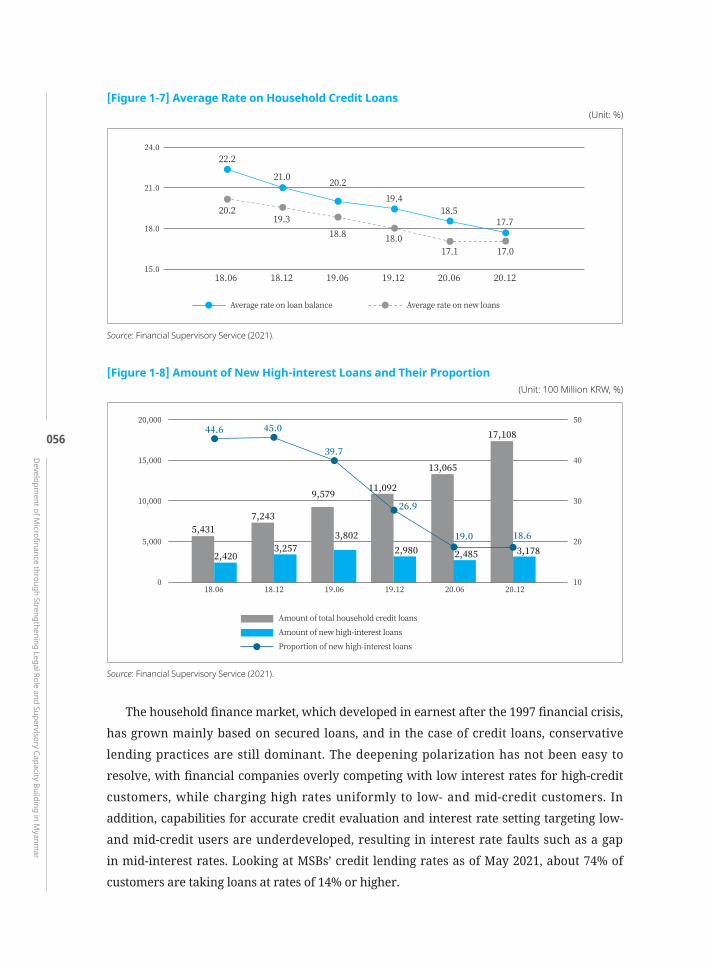

[Figure 1-1] FRD Organization Chart ·························································································· 030[Figure1-2] NumberofMFIsandOutstandingLoans ····························································· 031[Figure 1-3] Number of Operating MFIs in Types (As of January 2021) ··································· 031[Figure 1-4] Financial Supervisory System in Korea ·································································· 037[Figure 1-5] MSBs’ Capital Adequacy & Asset Soundness ························································· 039[Figure 1-6] FSS General Examination Process ·········································································· 048[Figure1-7] AverageRateonHouseholdCreditLoans ····························································· 056[Figure1-8] AmountofNewHigh-interestLoansandTheirProportion ·································· 056[Figure1-9] HouseholdCreditLoansbyInterestRates(Aggregatedby37MSBs) ················· 057

Chapter 2

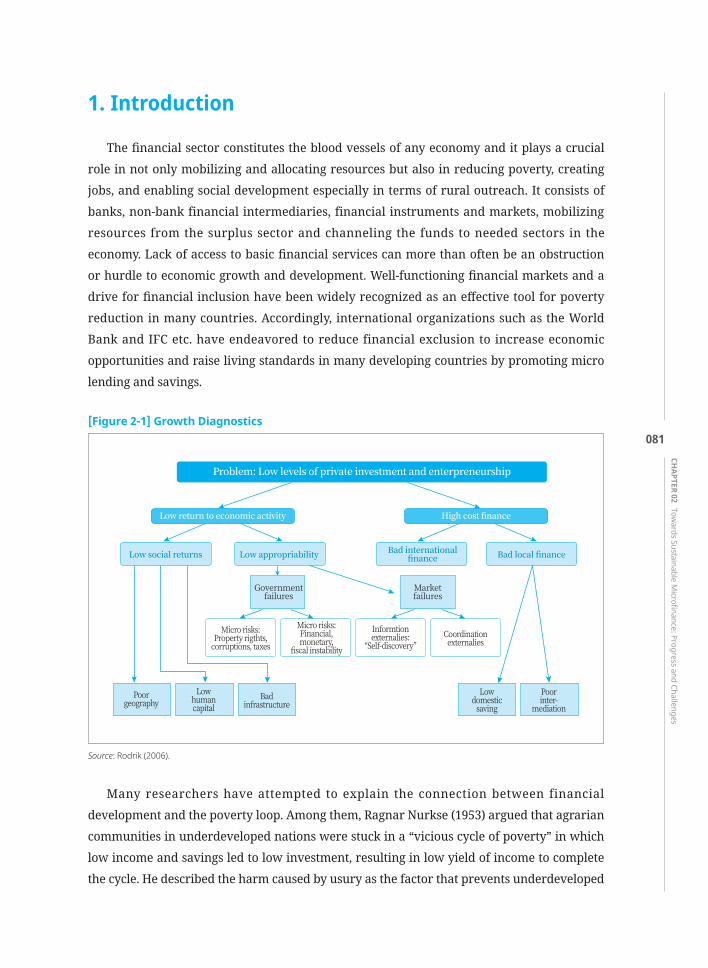

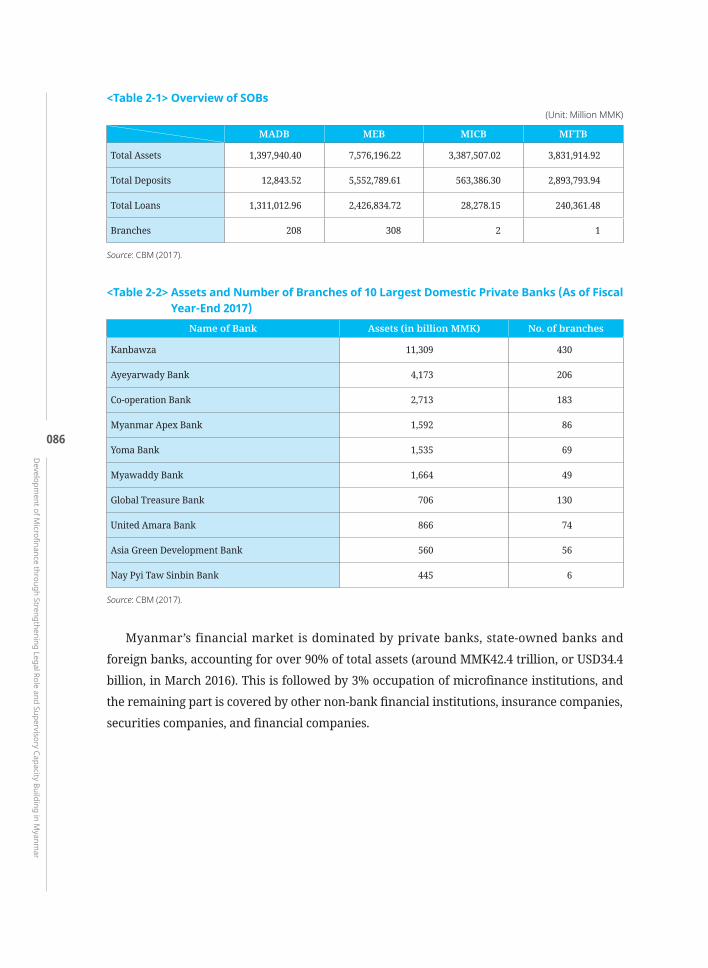

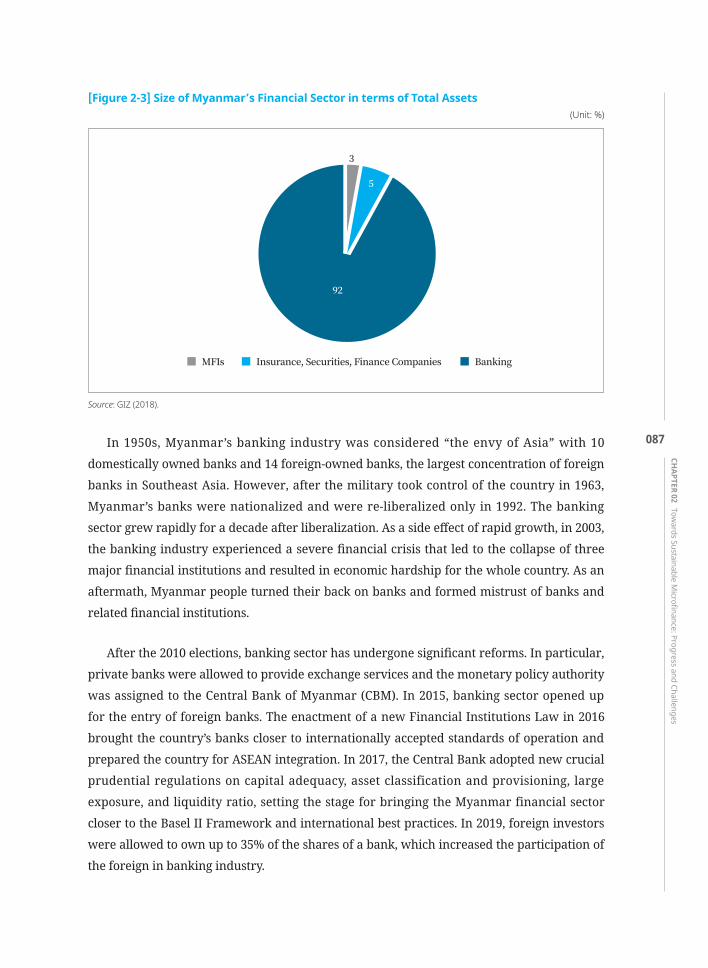

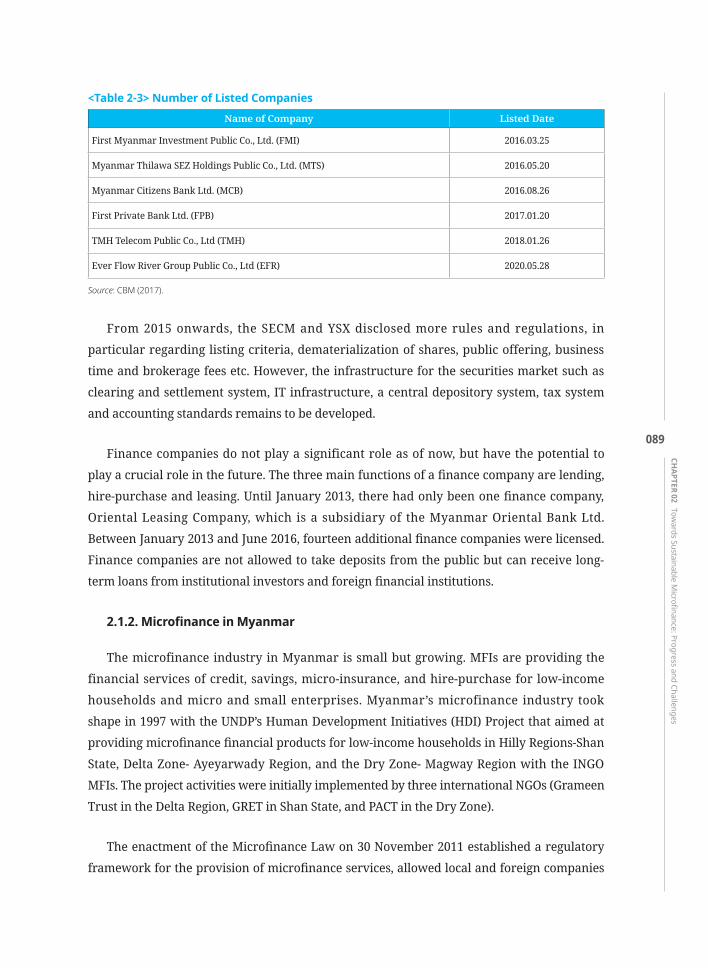

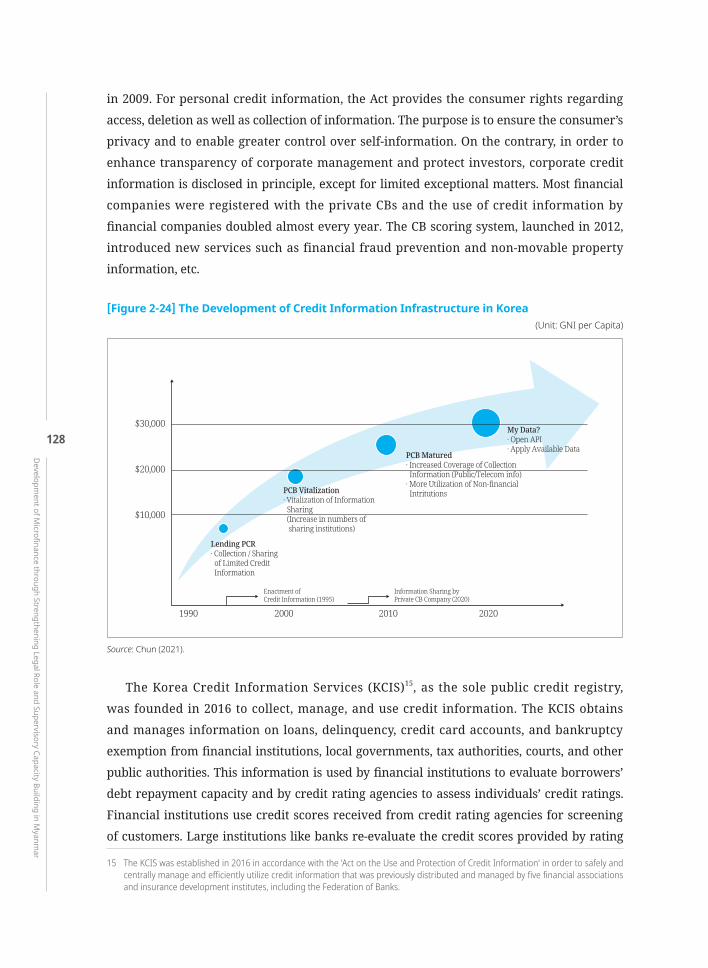

[Figure 2-1] Growth Diagnostics ································································································· 081[Figure 2-2] Banking Structure in Myanmar ·············································································· 085[Figure 2-3] Size of Myanmar’s Financial Sector in terms of Total Assets ································ 087[Figure2-4] BankingIndustryDevelopment:AnOverview ······················································ 088[Figure 2-5] Number of MFIs ······································································································ 090[Figure2-6] OutstandingLoansandSavings ············································································· 092[Figure 2-7] Financial Intermediation ························································································ 092[Figure 2-8] Numbers of Active Clients and Borrowers ····························································· 093[Figure 2-9] Financial Access in Urban and Rural Areas between 2013 and 2018 ··················· 094[Figure 2-10] Financial Access for Men and Women in Myanmar between 2013 and 2018 ····· 094[Figure 2-11] Financial Access in Myanmar between 2013 and 2018 ········································· 095[Figure 2-12] Access to a Financial Account, 2005 ······································································· 097[Figure 2-13] Access to a Financial Account, 2014 ······································································· 098[Figure 2-14] Regional Competitiveness of the Myanmar Financial Market ······························ 099[Figure 2-15] Domestic Credit Relative to GDP ············································································ 099[Figure 2-16] Domestic Credit in Myanmar ·················································································· 100[Figure2-17] LoantoDepositRatios ···························································································· 100[Figure2-18] ComparisonofPerCapitaGDP:Koreavs.Myanmar ············································ 110[Figure 2-19] Timeline of Credit Events and Institutions ····························································· 111[Figure 2-20] Number of CC Branches ·························································································· 120[Figure 2-21] Mission of KFCC ······································································································· 123

KSP-미얀마-final.indd 11 2021-11-29 오후 2:59:57

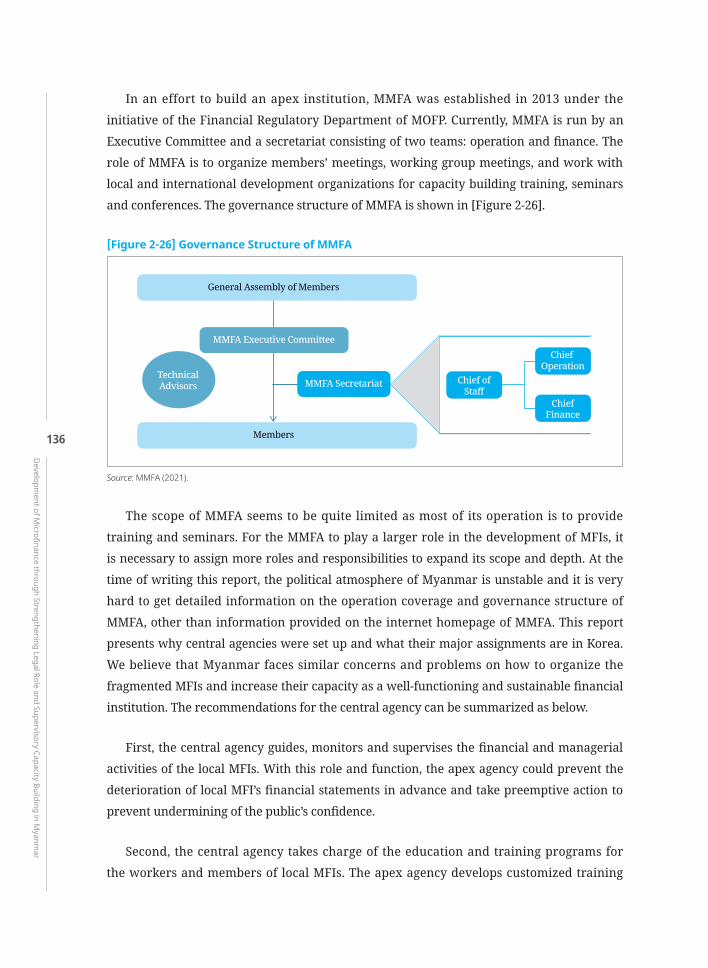

[Figure 2-22] Major Works of KFCC ······························································································· 123[Figure 2-23] Credit Information System of Korea ······································································ 127[Figure 2-24] The Development of Credit Information Infrastructure in Korea ························ 128[Figure 2-25] PCR-CB Model ·········································································································· 129[Figure 2-26] Governance Structure of MMFA ············································································· 136

Chapter 3

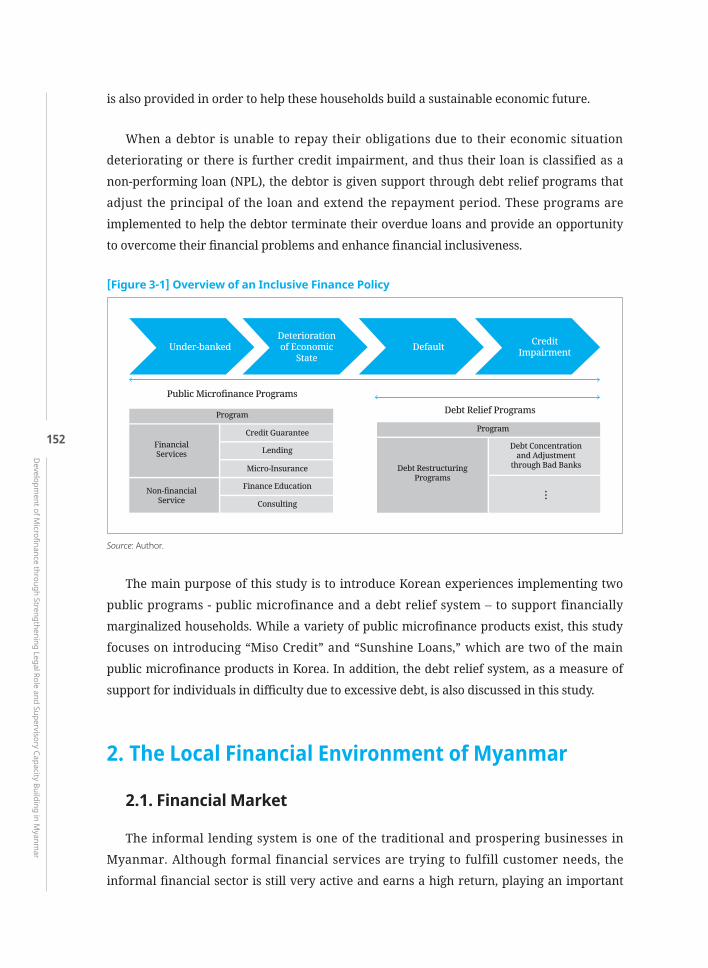

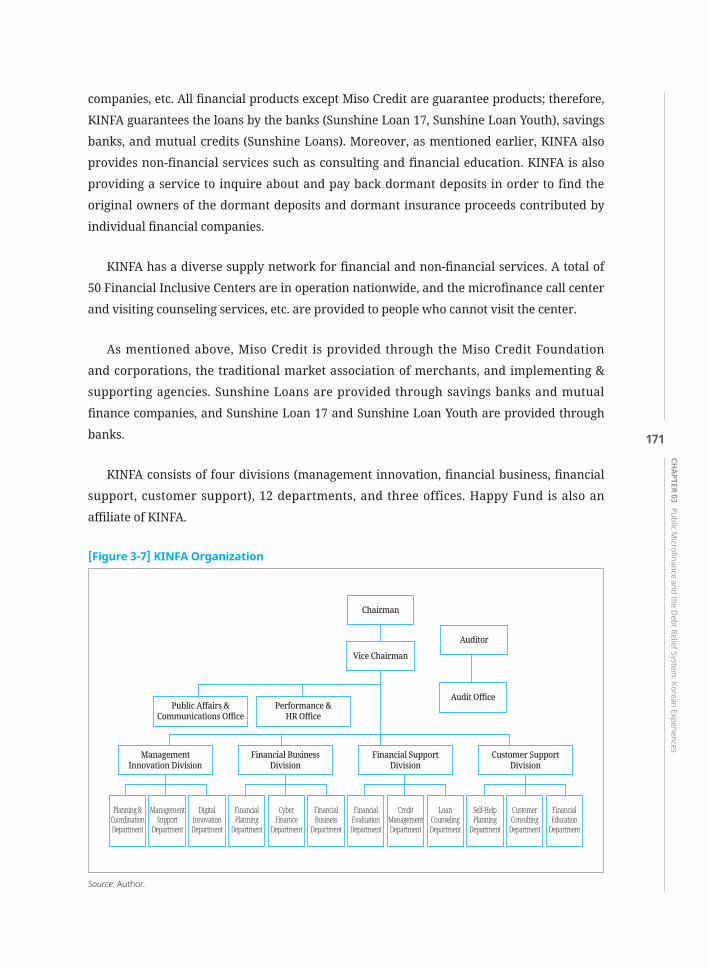

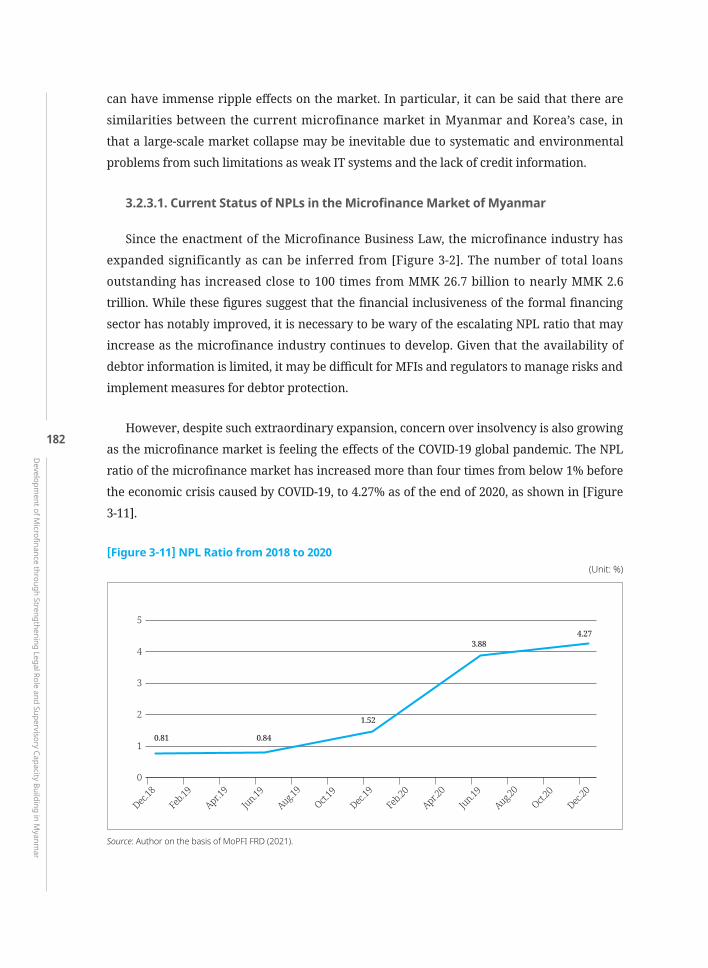

[Figure 3-1] Overview of an Inclusive Finance Policy ································································ 152[Figure3-2] HousingLoansbyStateandPrivateBanks ··························································· 155[Figure3-3] MFI’sDataforTotalLoansOutstandingandSavings ··········································· 157[Figure3-4] PurposesofLoanfromMADB ················································································ 159[Figure3-5] TrendofCreditUnionLoans ··················································································· 161[Figure3-6] TrendoftheUseoftheRegulatedMoneyLenders ··············································· 162[Figure 3-7] KINFA Organization ································································································· 171[Figure 3-8] Structure of Hanmaum Finance ············································································· 176[Figure 3-9] Structure of Heemang Moah ·················································································· 178[Figure 3-10] Number of Debt Delinquents per Year ·································································· 180[Figure3-11] NPLRatiofrom2018to2020 ·················································································· 182

Contents l List of Figures

KSP-미얀마-final.indd 12 2021-11-29 오후 2:59:57

KSP-미얀마-final.indd 13 2021-11-29 오후 2:59:57

2020/21 KSP with MyanmarHanbit Jung (Korea Development Institute)

KSP-미얀마-final.indd 14 2021-11-29 오후 2:59:57

015

2020/21 KSP with M

yanmar

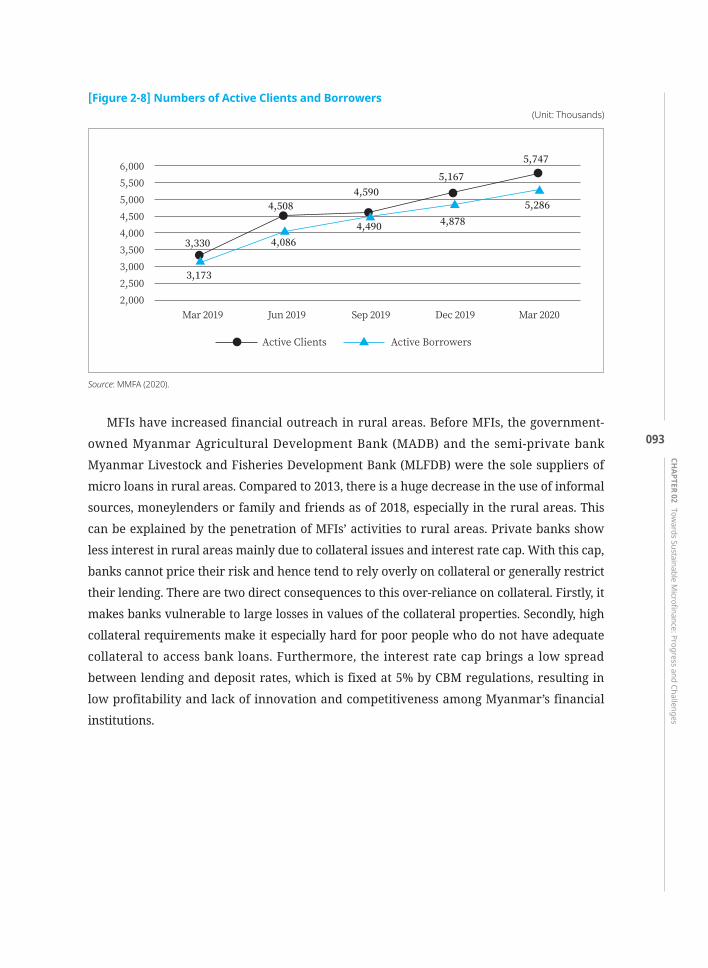

Myanmar’s government established the “12-Point Economic Policy (2016)” and “Myanmar Sustainable Development Plan (2018), while emphasizing the need to reform finance and improve access to financial services for SMEs and low-income families through the “Presidential 11 Reform Agenda (2018)”. However, only 26% of Myanmar’s population over the age of 14 had bank accounts in 2017 due to low reliability and a lack of bank access to state and private banks, which is lower than neighboring countries such as Indonesia (49%) and Vietnam (31%). Following the enactment of the Microfinance Business Law in 2011, 175 microfinance institutions are currently providing related services, and the Ministry of Planning and Finance, a local ministry, requested policy advice on revising related laws and preparing supervision measures.

The Financial Regulatory Department (FRD) under the Ministry of Planning, Finance and Industry submitted a KSP proposal for 2020/21 with three different topics for expanding financial support for low-income and SMEs by improving the microfinance laws and systems, establishing a financial reporting system, and supporting sustainable economic growth in Myanmar by improving access to financial services. Regarding Myanmar’s demand, Korea’s microfinance status would be shared in terms of market finance, public finance, and a system to enhance access to financial services through the revitalization of private financial services and fiscal policies.

Accordingly, the 2020/21 KSP with Myanmar was designed to support the establishment of policies for sustainable microfinance development and measures to improve the supervision and management of financial supervision. More specifically, there are plans to introduce not only microfinance regulation but also Korea’s experiences and its microfinance following the Preliminary Dialogue held in September 2020. As a consequence, the deliberations identified three subtopics to be studied in the follow-up project. The policy consultation team provided recommendations to Myanmar based on ample feedback from the local stakeholders

2020/21 KSP with MyanmarHanbit Jung (Korea Development Institute)

KSP-미얀마-final.indd 15 2021-11-29 오후 2:59:57

Development of M

icrofinance through Strengthening Legal Role and Supervisory Capacity Building in Myanm

ar

016

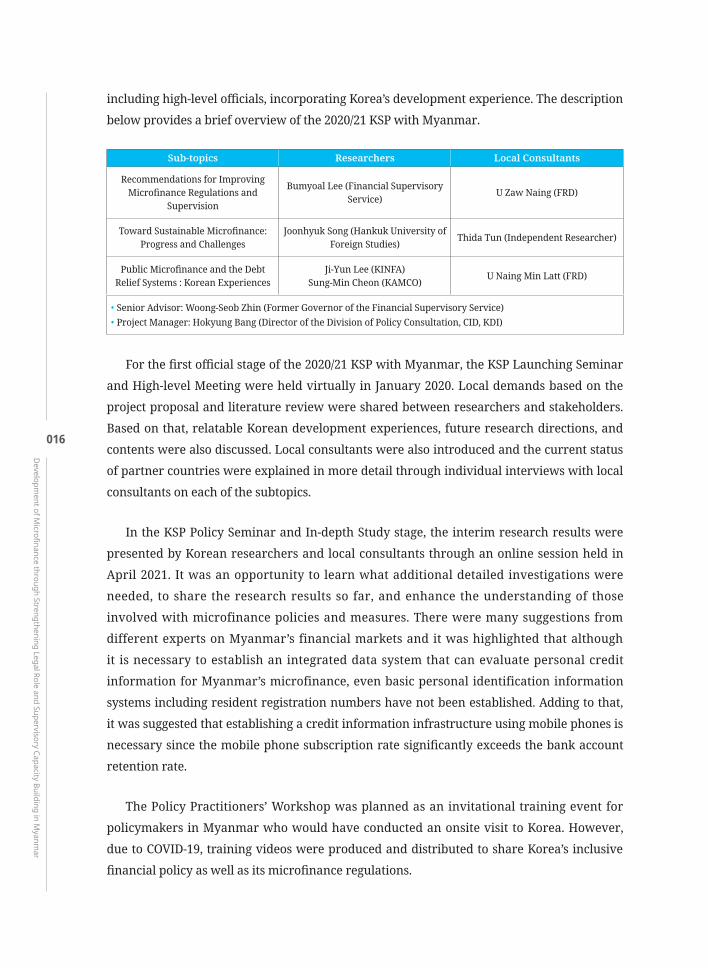

including high-level officials, incorporating Korea’s development experience. The description below provides a brief overview of the 2020/21 KSP with Myanmar.

Sub-topics Researchers Local Consultants

Recommendations for Improving Microfinance Regulations and

Supervision

Bumyoal Lee (Financial Supervisory Service) U Zaw Naing (FRD)

Toward Sustainable Microfinance: Progress and Challenges

Joonhyuk Song (Hankuk University of Foreign Studies) Thida Tun (Independent Researcher)

Public Microfinance and the Debt Relief Systems : Korean Experiences

Ji-Yun Lee (KINFA)Sung-Min Cheon (KAMCO) U Naing Min Latt (FRD)

• Senior Advisor: Woong-Seob Zhin (Former Governor of the Financial Supervisory Service) • Project Manager: Hokyung Bang (Director of the Division of Policy Consultation, CID, KDI)

For the first official stage of the 2020/21 KSP with Myanmar, the KSP Launching Seminar and High-level Meeting were held virtually in January 2020. Local demands based on the project proposal and literature review were shared between researchers and stakeholders. Based on that, relatable Korean development experiences, future research directions, and contents were also discussed. Local consultants were also introduced and the current status of partner countries were explained in more detail through individual interviews with local consultants on each of the subtopics.

In the KSP Policy Seminar and In-depth Study stage, the interim research results were presented by Korean researchers and local consultants through an online session held in April 2021. It was an opportunity to learn what additional detailed investigations were needed, to share the research results so far, and enhance the understanding of those involved with microfinance policies and measures. There were many suggestions from different experts on Myanmar’s financial markets and it was highlighted that although it is necessary to establish an integrated data system that can evaluate personal credit information for Myanmar’s microfinance, even basic personal identification information systems including resident registration numbers have not been established. Adding to that, it was suggested that establishing a credit information infrastructure using mobile phones is necessary since the mobile phone subscription rate significantly exceeds the bank account retention rate.

The Policy Practitioners’ Workshop was planned as an invitational training event for policymakers in Myanmar who would have conducted an onsite visit to Korea. However, due to COVID-19, training videos were produced and distributed to share Korea’s inclusive financial policy as well as its microfinance regulations.

KSP-미얀마-final.indd 16 2021-11-29 오후 2:59:57

017

In conclusion, KDI and the FDR collaboratively held the Final Reporting Workshop in July 2021. During this meeting, the stakeholders and researchers were able to review opportunities to increase the effectiveness of the policy proposals derived from this project. The final report on subtopic 1 analyzed Myanmar’s microfinance institutions, savings banks, and money lenders and compared them with Korea’s. It also drew implications for related laws and supervisory systems. For subtopic 2, it presented measures to strengthen legal and financial infrastructure to promote financial inclusion, focusing on cases where inclusive financial services were successfully provided through Korea’s financial policy and debt adjustment system. Subtopic 3 presented problems and solutions from Korea’s experience and operation processes related to the introduction of microfinance, and included regulatory and supervisory, accounting, and financial consumer protection systems as the main contents. A summary of the report was produced in a video and distributed for a better understanding of the final research results.

It was not an easy task to carry out this project and conduct research in the midst of COVID-19. Nevertheless, this project successfully provided multi-layered policy recommendations that are applicable to Myanmar’s current situation. For that, we would like to thank the Myanmar team, whose tremendous efforts will lead to a better system and benefit Myanmar. It was a great chance to strengthen cooperation between the two countries and we look forward to many more collaborations.

2020/21 KSP with M

yanmar

KSP-미얀마-final.indd 17 2021-11-29 오후 2:59:57

Executive SummaryJoonhyuk Song (Hankuk University of Foreign Studies)

KSP-미얀마-final.indd 18 2021-11-29 오후 2:59:57

019

Myanmar has a lower-middle income economy with a GDP per capita of 1,299 USD in 2017 and it is endeavoring to extend the provision of financial services to low-income families in a bid to promote inclusive finance to discontinue the vicious cycle of poverty. Even though Myanmar’s financial sector has been expanding in recent years, Myanmar still lacks financial competitiveness, especially in terms of the availability and accessibility of financial services compared to competing countries in the region. The government of Myanmar published the Financial Inclusion Roadmap 2019-2013 as part of the Making Access Possible (MAP) program in 2018 and rolled out the plan to overhaul its financial markets. Based on the program, the Myanmar financial regulatory authority is seeking to develop the country’s microfinance business by strengthening legal and financial reporting systems and improving client protection.

Microfinance is a fast-growing part of the financial industry in many developing countries and Myanmar is not an exception. Microcredit offers a chance to create jobs and reduce poverty and raise the socio-economic status of low-income families. After the enactment of the Microfinance Business Law in 2011, local and foreign companies are allowed to establish private MFIs to enlarge their source of funds. MFIs are permitted to undertake credit, saving, borrowing money from local and abroad, and hire-purchase and mobile payment. In order to draw attention from international investors to the local microfinance industry, Myanmar needs to improve its legal and financial reporting systems in accordance with international standards. Given that only 23% of the population over 15 years of age have deposit accounts and do not have sufficient collateral to qualify for a loan from a formal financial institution, MFIs can become a pivotal channel for helping the poor gain access to financial services. Myanmar’s government that took office in 2016 outlined 12 economic policies, one of which is to provide sustainable, market-driven finance for MSMEs and low-income households. Myanmar has many similarities to Korea when it was in the early stages of its financial development in the 1960s and 1970s even though the two

Executive SummaryJoonhyuk Song (Hankuk University of Foreign Studies)

Executive Summ

ary

KSP-미얀마-final.indd 19 2021-11-29 오후 2:59:57

Development of M

icrofinance through Strengthening Legal Role and Supervisory Capacity Building in Myanm

ar

020

countries differ in the size of their economies today.

After assessing the proposed research topics, the KSP mission team consulted with its Myanmar counterparts and selected three topics to help make Myanmar’s microfinance industry more transparent and robust. It is difficult to determine the adequacy of the recommendations due to the lack of information and communications caused by both the COVID-19 pandemic and the political situation in Myanmar during the research period. Despite the limitations and obstacles, the Korean mission team did its best to draw out valuable lessons in order to promote financial inclusion in Myanmar along with the progress of microfinance industry. A summary of the policy recommendations suggested for each topic is included below.

1. Recommendations for Improving Microfinance Regulations and Supervision

We examined the current state and regulatory structure of Myanmar’s microfinance industry and aimed to find factors limiting development and provide suggestions for improvement, based on Korea’s experiences in terms of relevant regulations and supervision. The scope of the research is limited to MSBs and moneylenders in Korea for direct comparison with MFIs in Myanmar.

MFIs in Myanmar have played a role in reducing poverty and improving the social and economic conditions of low-income families and MSMEs by meeting their financial needs. Despite the growth in the number of licensed MFIs in recent years, they are currently able to cover only about 30% of the demand, and MFI accessibility is much lower in rural areas than in large cities. The need for the development of the microfinance industry is emerging as an urgent and important issue in Myanmar. The development of the financial industry requires building a well-organized regulatory framework and making regulations transparent and predictable. Policy recommendations for improving the microfinance industry in Myanmar can be summarized into three areas: improving supervisory efficiency, rationalizing current regulations, and responding to changes in the market environment.

First, in a structure where the financial supervisory system is divided into the Central Bank, the FRD, and the Department of Cooperatives, cooperation and collaboration between supervisory authorities is important and should be strengthened. It is also advisable to incorporate oversight over the nonbank financial institutions and non-deposit-taking MFIs to avoid regulatory arbitrage.

KSP-미얀마-final.indd 20 2021-11-29 오후 2:59:57

021

Second, there is a need to improve the current MFI regulations. It is recommended to allow some collateral acquisition and adjust the maximum loan amounts so that the MFIs can more fully perform their role in providing financial services to low-income families and MSMEs. The current strict rules for asset classification and provisions should also be relaxed.

Lastly, financial supervision should be conducted in response to changes in the market environment. In order to solve the chronic excess demand for funds, Myanmar’s government should allow MFIs to merge in order to achieve the benefits of both economies of scale and scope. It is relatively easy for large-scale MFIs to strengthen their institutional capacities through technology, accounting systems, and human resource development, as well as complement their ability to provide collateral and funding within the group through affiliations. As a result, they can efficiently solve funding problems and provide quality microfinance services to consumers.

2. Towards Sustainable Microfinance: Progress and Challenges

The development of a financial system has long been associated with economic growth and development. Empirical studies have shown that financial deepening is strongly correlated with economic growth and development and it is vital to make the financial system sustainable. Korea has established a modern and advanced financial system, consisting of a diverse range of financial institutions. Over the last 60+ years, Korea has experienced rapid economic growth, converting an economy that was once largely poor and agrarian into an industrialized country in less than half a century. Understanding Korea’s financial development is a good starting point for establishing sustainable microfinance in Myanmar.

In order to draw out practical policy lessons, we chose periods with similar stages of development in Myanmar and Korea in terms of per capita GDP. We examined the introduction and development processes of cooperative financial institutions (CFIs) in Korea represented by Credit Unions and Community Credit Cooperatives as well as the roles and functions of the central agencies of each institution as a centralized window for dialogue with government, a facilitator to plan and perform development strategies for the industry, and a lender of the last resort to protect depositors’ savings. We discussed Korea’s experiences establishing and implementing a credit information system (CIS). The Korean CIS is an effort to achieve both a speedy establishment by delegating the role of collecting and managing data to a public entity known as KCIS as well as efficiency and innovation by promoting competition among private credit bureaus for the use of data. Based on Korea’s

Executive Summ

ary

KSP-미얀마-final.indd 21 2021-11-29 오후 2:59:57

Development of M

icrofinance through Strengthening Legal Role and Supervisory Capacity Building in Myanm

ar

022

experiences, we suggest the following two recommendations.

First, Myanmar needs to extend the scope of the role of its central information system. We propose a PCR-CR hybrid as the introduction of the CIS in Myanmar has been delayed. The adoption of this proposed system is suggested to facilitate the prompt activation of the CIS and ensure the transparency and reliability of the collected data. So far, the MCB has been launched as the first credit bureau, but its scope and coverage are limited to the banking sector, hence it needs to include data from NBFIs to extend credit-based lending practices to poor families without proper collateral.

Second, it is necessary to establish a well-functioning governance structure to monitor and supervise risk and improve managerial efficiency in the microfinance industry. After giving the proper authority to a central agency, the central agency should take a leading role in guiding and supervising the local MFIs, provide education and training, relay the inter-lending among MFIs, and set up a provisional fund to ensure the safety of depositors’ savings.

3. Public Microfinance and the Debt Relief Systems : Korean Experiences

In order to achieve inclusiveness and sustainability for Myanmar’s microfinance, it is necessary to establish a public microfinance and debt restructuring system for non-performing loans along with market microfinance in the mid to long run. Although the market-based microfinance industry is growing, MFIs are allowed to make non-collateralized loans, resulting in mostly group loans where personal sureties replace physical collateral. For urban workers or those who cannot obtain joint personal guarantees, they cannot currently access microfinance, limiting the scope of inclusive finance outlined in the Myanmar Sustainable Development Plan in 2018. In order to expand financial outreach, Myanmar’s government should consider introducing public microfinance to supplement the current microfinance industry and prevent usurious illegal moneylending. The government should also take up an initiative to expand opportunities for credit recovery for those who cannot make payments for their loans.

It seems that public microfinance and debt restructuring systems do not currently exist in Myanmar. However, it will be necessary to understand the role of these institutions and introduce them in order to strengthen financial accessibility and stabilize financial markets in cases of unexpected stress. Even with the development of financial markets, there will always be marginalized people who should be protected and supported by the government.

KSP-미얀마-final.indd 22 2021-11-29 오후 2:59:57

023

Based on Korea’s experiences, we propose three recommendations.

First, it is necessary to initiate government-led financial education to enhance the financial literacy of the poor and allow them to make rational financial choices. Improving perceptions of the danger of over-indebtedness and multiple loans will reduce both personal and social costs stemming from personal defaults and financial exclusion.

Second, Myanmar’s government should develop guarantee products to overcome funding problems by utilizing the credit multiple effect of these products. These guarantees should be co-funded by the government and the private sector to provide policy-inclusive finance. Introducing special guarantee products is also recommended in the case of banks and conglomerates funding resources.

Lastly, it is necessary to preemptively prepare a debt restructuring system that can comprehensively manage multiple debts that can lead to large-scale non-performing loans in Myanmar’s microfinance market. In addition, when a large-scale non-performing loan problem involving multiple MFIs and financial sectors arises, the government needs to take the initiative to prepare countermeasures. A bad bank established and operated to handle the financial distress created by non-performing card loans in 2003 was proven effective in Korea and, hence, is recommended to prepare for the introduction of a debt restructuring system.

Executive Summ

ary

KSP-미얀마-final.indd 23 2021-11-29 오후 2:59:57

Recommendations for Improving Microfinance Regulations and SupervisionBumyoalLee(FinancialSupervisoryService)

1. Introduction2.MicrofinanceinMyanmar3.Korea’sExperienceinMicrofinanceSupervision4.ChallengesintheMicrofinanceMarketandKorea’sSupervisoryEfforts5.DiscussionsandRecommendationsforDevelopmentofMicrofinanceinMyanmar6. Conclusions

C H A P T E R

01

KeywordsMicrofinanceinMyanmar,RevisionofMicrofinanceBusinessLaw,KnowledgeSharing,EfficientSupervision,RationalRegulation

KSP-미얀마-final.indd 24 2021-11-29 오후 2:59:58

025

CHAPTER

01Recom

mendations for Im

proving Microfinance Regulations and Supervision

Summary1

This study examines the current state and regulatory structure of Myanmar’s microfinance industry and aims to find factors limiting development and provide suggestions for improvement, based on Korea’s experience of promoting inclusive finance in terms of relevant regulations and supervision. As this study analyzes Microfinance Institutions (MFIs) regulated by the Financial Regulatory Department (FRD), the partner of this project, the scope of the report is limited to Mutual Savings Banks (MSBs) and moneylenders in Korea for direct comparison with MFIs in Myanmar.

Unlike banks that primarily provide credit to public institutions and large corporations in Myanmar, MFI has played a role in reducing poverty and improving the social and economic conditions of low-income families and Micro, Small and Medium-sized Enterprises (MSMEs) by meeting their financial needs. MFIs are not allowed to acquire collateral, and are subject to restrictions on loan and deposit rates and loan size. Compared to banks, MFI entry regulations are less stringent in terms of paid-in capital; however, MFIs are required to meet prudential standards such as solvency and liquidity ratios. The loan maturity is generally less than one year, so the provision for bad debts is also stipulated accordingly. As of the end of 2020, there were 188 MFIs in operation, including 21 deposit-taking and 167 non-deposit-taking MFIs. Cumulatively, they provide loans to 5.9 million customers. Despite the growth in the number of licensed MFIs over a short period of time, they are currently able to cover only about 30% of the demand, and accessibility is much lower in rural areas than in large cities. In the end, the need for development of the microfinance industry is emerging as an urgent and important issue in Myanmar.

1 ThecontentsofthispaperdonotreflecttheviewsoftheFinancialSupervisoryServiceofKorea.Anydiscussionofregulationsorpolicydirectionsinthispapershouldbeseensolelyastheauthor’sopinion.

Recommendations for Improving Microfinance Regulations and SupervisionBumyoalLee(FinancialSupervisoryService)1

KSP-미얀마-final.indd 25 2021-11-29 오후 2:59:58

Development of M

icrofinance through Strengthening Legal Role and Supervisory Capacity Building in Myanm

ar

026

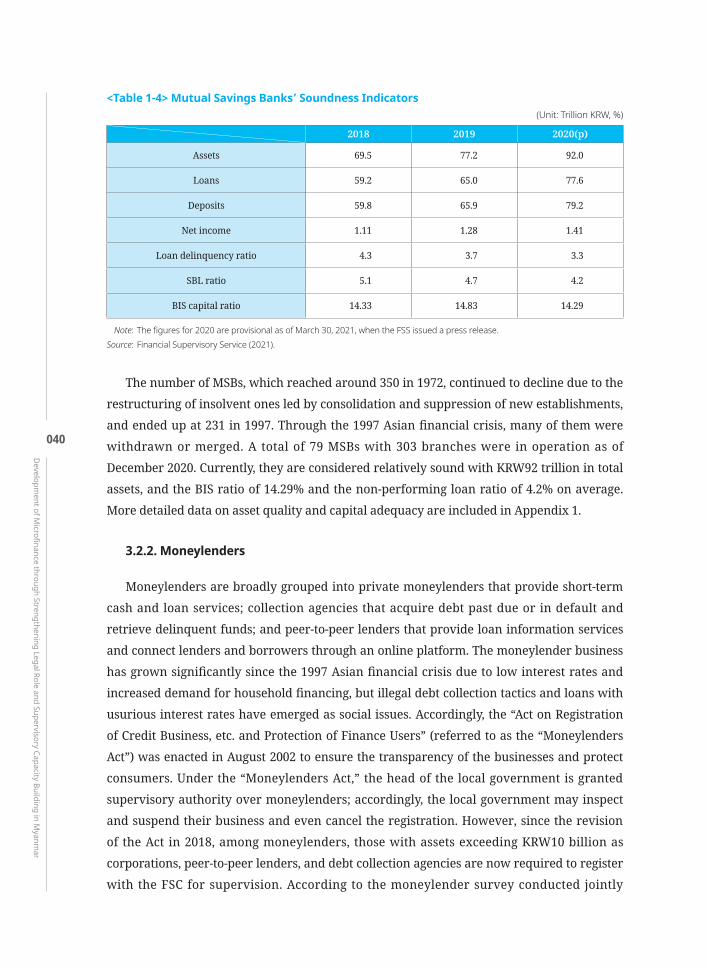

In Korea, the non-banking sector mainly provides finances to low-credit, low-income families and small businesses. MSBs were created in 1972 to remodel the private lending market into a more structured financial setting, and currently a total of 79 MSBs with 303 branches are in operation. Private moneylenders are not officially classified as financial institutions, but they are obligated to register with financial regulatory authorities or municipalities depending on the size. As of the end of 2020, there were 1,077 moneylenders registered with the Financial Services Commission and 7,424 with local governments, for a total of 8,501. MSBs are deposit-taking institutions and provide commercial banking on a limited scale; they are regulated by paid-in capital, loan rates, and business areas. In particular, they are subject to a strict credit extension limit since they can be controlled by a single large shareholder. On the other hand, there are generally few restrictions that apply to entry requirements, business areas, or financing terms for moneylenders; where there are restrictions, they are of a loose nature. MSBs are businesses that require regulatory approval not only for entry, but also for business dissolution, merger, closure, and transfer or capital reduction. They must also comply with prudential standards including rules for capital adequacy, asset classification and minimum allowances for credit losses as well as other guidelines. Unlike MSBs, there are no specific prudential guidelines for moneylenders since they do not accept deposits. However, in order to protect consumers, various obligations are imposed for advertising loans, executing loan agreements, and collecting debt.

As Korea’s integrated supervisory authority, the Financial Supervisory Service (FSS) is responsible for the safety and soundness of all financial institutions. The FSS performs its supervision responsibilities primarily by conducting off-site surveillance and on-site examination, assessing business operations and financial health of institutions, and taking actions to address any heightened stress or risk of failure. Although the purpose of supervision is not to detect and penalize violations of laws and regulations, it is natural for financial companies to feel burdened under the supervision and examination. Therefore, checks and balances have been introduced to ensure that all processes are performed transparently and objectively, and financial companies and individuals can exercise the right to appeal the decision if they are subjected to sanctions. The regulatory authorities have an additional role to play in the microfinance market because the customer base in this case comes with a high level of credit risk and is vulnerable to economic downturn. It is important not only to ensure the soundness of financial institutions, but also to prevent the exclusion of vulnerable classes from the market. To this end, the FSS is applying regulations in a flexible manner, relaxing or strengthening the level according to market conditions. In practice, designing microfinance policy is a difficult process that inevitably requires a fine balancing of both these opposing roles.

KSP-미얀마-final.indd 26 2021-11-29 오후 2:59:58

027

CHAPTER

01Recom

mendations for Im

proving Microfinance Regulations and Supervision

Although it is difficult to determine the adequacy of the FRD’s examination process and post-examination actions due to the lack of information, the policy recommendations for improving the microfinance industry in Myanmar are drawn based on Korea’s experience and summarized in three aspects: improving supervisory efficiency, rationalizing current regulations, and responding to changes in the market environment. First, in an administrative structure where the financial supervisory system is divided into the Central Bank, the FRD and the Department of Cooperatives, cooperation and collaboration between these supervisory authorities is important and should be strengthened. If possible, it is advisable to incorporate oversight over the nonbank financial institutions and non-deposit taking MFIs to avoid regulatory arbitrage. At the same time, in order that supervision and examination are conducted consistently without being influenced by the individual examiner’s judgment, it is necessary to strengthen supervisory competence. To compensate for insufficient supervisory resources, it is desirable to enhance the role of the self-regulatory organization representing the MFI. Second, there is a need to improve the current MFI regulations. To name a few, it seems reasonable to allow some collateral acquisition and adjust the maximum loan amount so that the MFI can expand its role in providing financial services to low income families and small business owners. While introducing overdue interest, the rules for asset classification and provisions need to be relaxed. On the other hand, liberalization of interest rates and expansion of MFI business areas must be pursued with caution. Given the difficulty of pre-assessing the market impact of deregulations, it should be designed with due consideration of potential side effects on the market in the future.

Lastly, as market competition intensifies, financial institutions are striving to strengthen efficiency, cost management and sustainability, and creating a more integrated institution is an increasingly popular strategy to achieve all of these goals. As MFIs in Myanmar are struggling to collect loan repayments from borrowers affected by COVID-19, the soundness of MFI has deteriorated, and eventually restructuring of insolvent MFI will be inevitable. It would be relatively easy for large-scale MFIs to strengthen institutional capacities including technology, accounting system, and human resource development as well as complement the ability to provide collateral and funding within the group through affiliation. As a result, they can solve the funding problem and provide quality microfinance services to consumers in an efficient manner. The branding of large MFIs will also be of great help in overcoming the general negative perceptions on financial companies that have gained strength through the past financial crisis. However, bigger MFIs are not always better. If the MFI market is polarized into large and small, and regulations on loan rates and collateral are eased, then the market is likely to develop in a very different form. Large MFIs will likely focus on loans with collateral for high credit borrowers just like banks, whereas small MFIs will charge the maximum rates on credit loans regardless of the funding rate. Regulatory authorities should

KSP-미얀마-final.indd 27 2021-11-29 오후 2:59:58

Development of M

icrofinance through Strengthening Legal Role and Supervisory Capacity Building in Myanm

ar

028

pay attention to the possibility that MFIs may, in this process, overlook their original purpose of improving the quality of life for low income households and providing financial options for MSMEs.

Korea and Myanmar differ in the size of their economy and the stage of market development, but the same principles should be applied to financial supervision and regulation. The development of the financial industry requires building a well-organized regulatory framework and making the regulations transparent and predictable. The regulations themselves also need to be changed as the environment changes, so it is important to check regularly whether the current regulations are effective. To do this, financial regulatory authorities must constantly communicate with the industry and streamline regulations in a timely manner. The growth of Myanmar’s MFI during its second decade should not simply be a continuation of its first. Through continuous technological innovation, development of client-centered products and services, and ongoing efforts for reinforcement of supervisory capabilities, it is hoped that the microfinance industry can serve as a cornerstone of improving the quality of life for people in Myanmar.

1. Introduction

In Myanmar, cooperative forms of mutual aid have been around since the early 20th century, but microfinance started its journey in earnest in 1997 under the United Nations Development Program (UNDP) of Human Development Initiative. After enactment of the Microfinance Business Law (MBL) in November 2011, regulated formal microfinance institutions have come into action. The industry itself is growing rapidly through the institutionalization of a number of local cooperatives and private financial institutions, and the participation of domestic and foreign financial institutions and NGOs has expanded steadily. However, despite the growth in the number of licensed Microfinance Institutions (MFIs), they are able to cover only about 30% of the demand, which is markedly insufficient to meet the financial needs of the low-income families and Micro, Small and Medium Enterprises (MSMEs). Accordingly, the government is seeking ways to further develop the microfinance industry, starting with the revision of the MBL.

This study examines the current state and regulatory structure of Myanmar’s microfinance industry. In particular, it aims to find factors limiting development and provide suggestions for improvement, based on Korea’s experience of promoting inclusive finance in terms of relevant regulations and supervision. As this study analyzes MFIs regulated by the Financial Regulatory Department (FRD) under the Ministry of Planning and Finance (MOPF)

KSP-미얀마-final.indd 28 2021-11-29 오후 2:59:58

029

CHAPTER

01Recom

mendations for Im

proving Microfinance Regulations and Supervision

which is the partner of this project, it is to be noted that the scope of this report is limited to Mutual Savings Banks (MSBs) and moneylenders in Korea that can be compared directly with MFIs in Myanmar.2

The remainder of the report is organized as follows. Section 2 reviews Myanmar’s microfinance industry including MFI regulations, current state, business environment and related infrastructures. Session 3 describes Korea’s financial supervisory experiences with regard to low-credit, low-income households and MSMEs, focusing on MSBs and moneylenders. The regulatory and supervisory systems including procedures for examination and sanction are also presented. Section 4 explains the current state of the Korean microfinance market and the challenges facing the regulatory authorities, Lastly, Section 5 provides policy recommendations for developing the microfinance industry in Myanmar, and concerns and hopes for the future are briefly described in Section 6.

2. Microfinance in Myanmar

2.1. Microfinance Landscape and Supervisory Structure

The financial industry in Myanmar is dominated by banks and MFIs, while Non-Bank Financial Institutions (NBFIs), insurance and securities industries are in the early stages of development.3 Unlike banks that are supervised by the Central Bank of Myanmar (CBM) and primarily provide credit to public institutions and large corporations, the objectives of the MFIs are to reduce poverty and improve social, health and economic conditions for low income people as clearly stated in the MBL. It defines the role of microfinance as issuing micro-credit, taking deposits, supporting remittances, providing insurance and carrying out other financial services.4

Regarding oversight of the MFI, the MOPF develops laws and regulations for the microfinance industry through the Microfinance Business Supervisory Committee (MBSC),

2 Creditunionsandagricultural,fisheriesandforestrycooperativesinKoreaarealsoanimportantpartofthefinancialservicesforlow-credit,low-incomehouseholdsandMSMEs,buttheycanbeconsideredsimilartothecooperativesthataresupervisedbytheDepartmentofCooperativeundertheMinistryofAgricultureLivestockandIrrigation(MOALI)inMyanmar.AnoverviewofKorea'smutualcreditcooperativesandpolicyfinancecanbefoundintheprecedingstudy,“Korea’sExperienceofMicrofinanceandSMEFinancingthroughCreditUnionsandCooperatives,”2016/17KnowledgeSharingProgramwithGuatemala,pp.196-210.

3 IntheFinancialInstitutionsLaw(FIL)enactedin1990,theterm"financialcompany"wasusedseparatelyfrom“bank”tocollectivelyrefertofinancialinstitutionsthatperformsecuredandunsecuredloans,installmentfinancingandleasingbusiness.However,therevisedFILin2016newlyintroducedtheconceptoftheNBFIandclassifiedit intofinancialcompaniesandleasingandfactoringbusinessaccordingtothebusinesstype.Currently29companiesareoperatingwiththeapprovaloftheCentralBankofMyanmar(CBM).

4 ThebiggestdifferencebetweenabankandanMFIiswhethercollateral isreceived.Forbanks,onlysecuredloansareaccepted,whereasMFIsonlyhandlecreditloans.

KSP-미얀마-final.indd 29 2021-11-29 오후 2:59:58

Development of M

icrofinance through Strengthening Legal Role and Supervisory Capacity Building in Myanm

ar

030

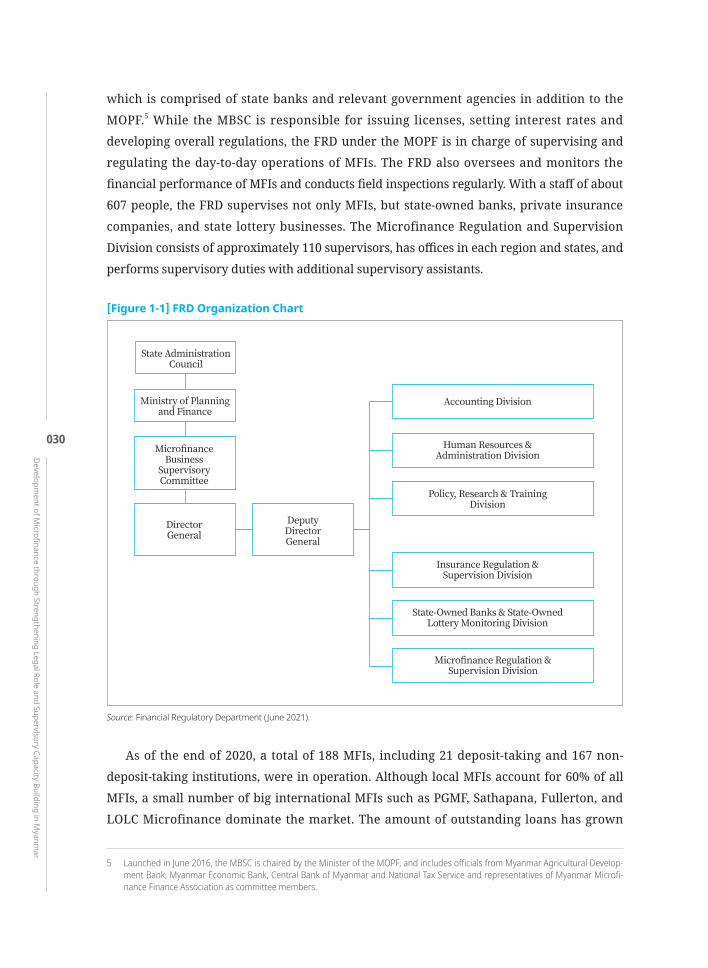

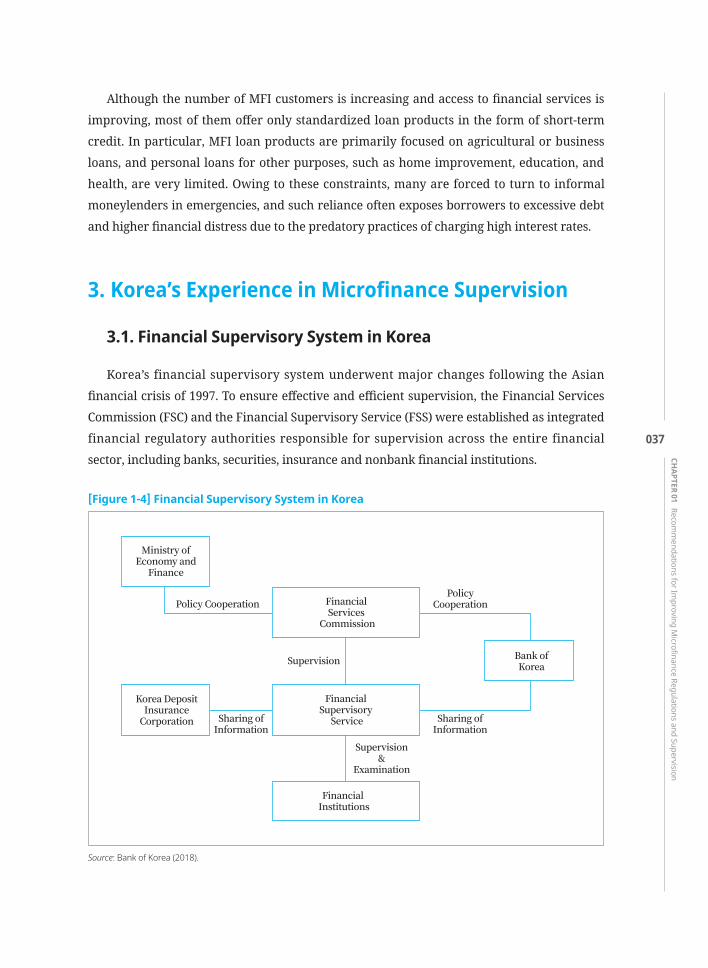

which is comprised of state banks and relevant government agencies in addition to the MOPF.5 While the MBSC is responsible for issuing licenses, setting interest rates and developing overall regulations, the FRD under the MOPF is in charge of supervising and regulating the day-to-day operations of MFIs. The FRD also oversees and monitors the financial performance of MFIs and conducts field inspections regularly. With a staff of about 607 people, the FRD supervises not only MFIs, but state-owned banks, private insurance companies, and state lottery businesses. The Microfinance Regulation and Supervision Division consists of approximately 110 supervisors, has offices in each region and states, and performs supervisory duties with additional supervisory assistants.

[Figure 1-1] FRD Organization Chart

State AdministrationCouncil

Ministry of Planningand Finance

MicrofinanceBusiness

SupervisoryCommittee

DirectorGeneral

DeputyDirectorGeneral

Microfinance Regulation &Supervision Division

State-Owned Banks & State-OwnedLottery Monitoring Division

Insurance Regulation &Supervision Division

Policy, Research & TrainingDivision

Human Resources &Administration Division

Accounting Division

Source: Financial Regulatory Department (June 2021).

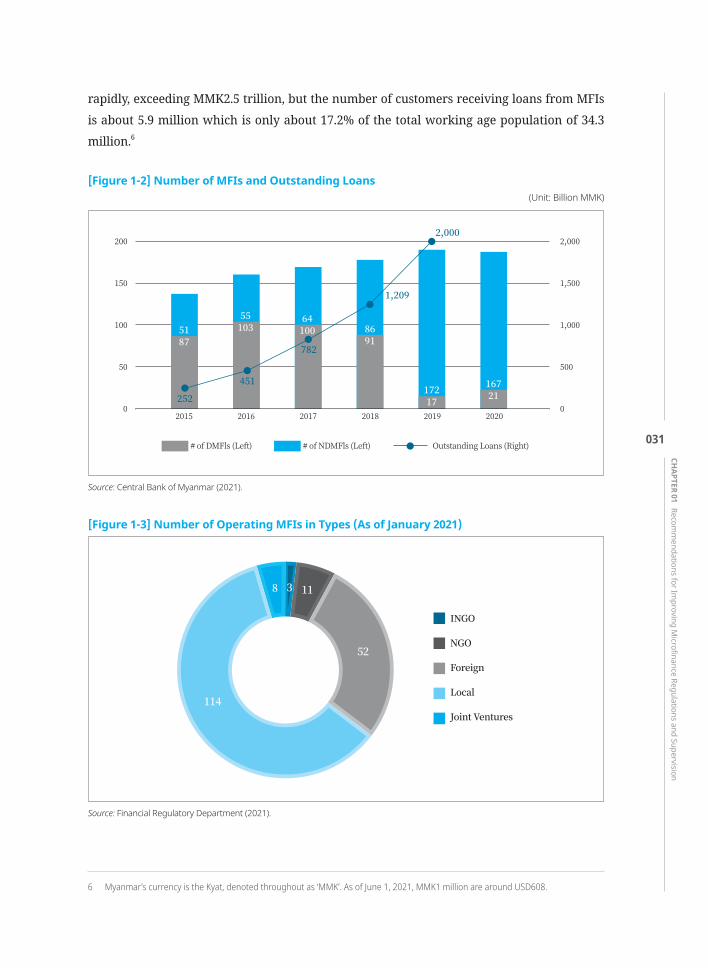

As of the end of 2020, a total of 188 MFIs, including 21 deposit-taking and 167 non-deposit-taking institutions, were in operation. Although local MFIs account for 60% of all MFIs, a small number of big international MFIs such as PGMF, Sathapana, Fullerton, and LOLC Microfinance dominate the market. The amount of outstanding loans has grown

5 LaunchedinJune2016,theMBSCischairedbytheMinisteroftheMOPF,andincludesofficialsfromMyanmarAgriculturalDevelop-mentBank,MyanmarEconomicBank,CentralBankofMyanmarandNationalTaxServiceandrepresentativesofMyanmarMicrofi-nanceFinanceAssociationascommitteemembers.

KSP-미얀마-final.indd 30 2021-11-29 오후 2:59:58

031

CHAPTER

01Recom

mendations for Im

proving Microfinance Regulations and Supervision

rapidly, exceeding MMK2.5 trillion, but the number of customers receiving loans from MFIs is about 5.9 million which is only about 17.2% of the total working age population of 34.3 million.6

[Figure 1-2] Number of MFIs and Outstanding Loans (Unit: Billion MMK)

�

��

����

# of DMFls (Left)

���� ���� ���� ���� ����

���

���

���

�

���

�,���

�,���

�,���

# of NDMFls (Left) Outstanding Loans (Right)

����

���

���

���

�,���

�,���

�����

�����

����

����� ��

���

Source: Central Bank of Myanmar (2021).

[Figure 1-3] Number of Operating MFIs in Types (As of January 2021)

INGO

NGO

Foreign

Local

Joint Ventures���

� � ��

��

Source: Financial Regulatory Department (2021).

6 Myanmar’scurrencyistheKyat,denotedthroughoutas‘MMK’.AsofJune1,2021,MMK1millionarearoundUSD608.

KSP-미얀마-final.indd 31 2021-11-29 오후 2:59:58

Development of M

icrofinance through Strengthening Legal Role and Supervisory Capacity Building in Myanm

ar

032

Looking at the current coverage area, microfinance services are available in 259 townships, which constitute about 78% of the total 330 townships in Myanmar corresponding to Cities in Korea. However, access to the MFIs becomes more difficult going further down to remote areas such as Wards, Tract Villages, and Villages that are comparable to Gu, Gun or smaller in Korea; thus, it may be said that only 42% of villages are able to receive MFI services.

<Table 1-1> Microfinance Coverage Area in MyanmarTarget Area Number of Areas Implemented Areas %

Townships 330 259 78.48

Wards 3,441 2,276 66.14

Tract Villages 13,969 7,905 56.59

Villages 63,854 27,194 42.59

Source: Financial Regulatory Department (2021).

2.2. Rules and Regulations of Microfinance

Compared to banks, entry regulations for MFI are less stringent, requiring paid-in capital of only MMK300 million and MMK100 million for deposit-taking MFI (DMFI) and non-deposit-taking MFI (NDMFI) respectively. A one-year temporary license needs a full conversion following addition regulatory review, but it does not seem like a heavy burden given the continued increase in participation. MFI business regulations were relaxed significantly in 2016, but DMFI licensing regulations have been tightened, requiring a minimum of three years of operating experience and two consecutive years of recording profits. In addition, the DMFI must have an appropriate operational management information system and strong internal controls to accommodate customer deposits. These requirements apply not only to newly established MFIs, but also to MFIs that are already in operation. As a result, some of the smaller DMFIs that were unable to meet these requirements returned their licenses or have switched to NDMFIs. As can be seen in [Figure 1-2] above, the number of DMFIs in 2019 decreased by more than 80% compared to 2018.

The most important business rule after the establishment of the MFI is the regulation on interest rates and loan size. MFI lending rate is capped at 28% per annum or 2.33% per month while unofficial private lenders typically charge at 10 to 20% per month. There are also strict restrictions on compulsory and voluntary deposits required of MFI customers. Compulsory deposits may not exceed 5% of the loan amount, and are constrained by the interest rate floor of 14%. As long as the MFI meets the 12% solvency ratio, voluntary

KSP-미얀마-final.indd 32 2021-11-29 오후 2:59:58

033

CHAPTER

01Recom

mendations for Im

proving Microfinance Regulations and Supervision

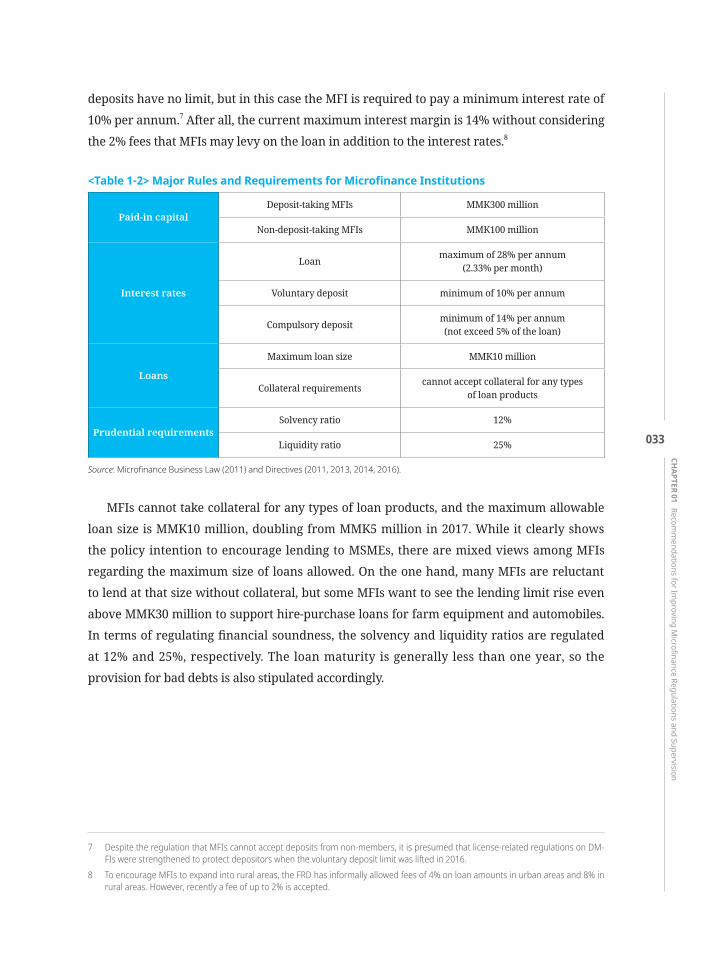

deposits have no limit, but in this case the MFI is required to pay a minimum interest rate of 10% per annum.7 After all, the current maximum interest margin is 14% without considering the 2% fees that MFIs may levy on the loan in addition to the interest rates.8

<Table 1-2> Major Rules and Requirements for Microfinance Institutions

Paid-in capitalDeposit-taking MFIs MMK300 million

Non-deposit-taking MFIs MMK100 million

Interest rates

Loan maximum of 28% per annum(2.33% per month)

Voluntary deposit minimum of 10% per annum

Compulsory deposit minimum of 14% per annum(not exceed 5% of the loan)

Loans

Maximum loan size MMK10 million

Collateral requirements cannot accept collateral for any types of loan products

Prudential requirementsSolvency ratio 12%

Liquidity ratio 25%

Source: Microfinance Business Law (2011) and Directives (2011, 2013, 2014, 2016).

MFIs cannot take collateral for any types of loan products, and the maximum allowable loan size is MMK10 million, doubling from MMK5 million in 2017. While it clearly shows the policy intention to encourage lending to MSMEs, there are mixed views among MFIs regarding the maximum size of loans allowed. On the one hand, many MFIs are reluctant to lend at that size without collateral, but some MFIs want to see the lending limit rise even above MMK30 million to support hire-purchase loans for farm equipment and automobiles. In terms of regulating financial soundness, the solvency and liquidity ratios are regulated at 12% and 25%, respectively. The loan maturity is generally less than one year, so the provision for bad debts is also stipulated accordingly.

7 DespitetheregulationthatMFIscannotacceptdepositsfromnon-members,itispresumedthatlicense-relatedregulationsonDM-FIswerestrengthenedtoprotectdepositorswhenthevoluntarydepositlimitwasliftedin2016.

8 ToencourageMFIstoexpandintoruralareas,theFRDhasinformallyallowedfeesof4%onloanamountsinurbanareasand8%inruralareas.However,recentlyafeeofupto2%isaccepted.

KSP-미얀마-final.indd 33 2021-11-29 오후 2:59:58

Development of M

icrofinance through Strengthening Legal Role and Supervisory Capacity Building in Myanm

ar

034

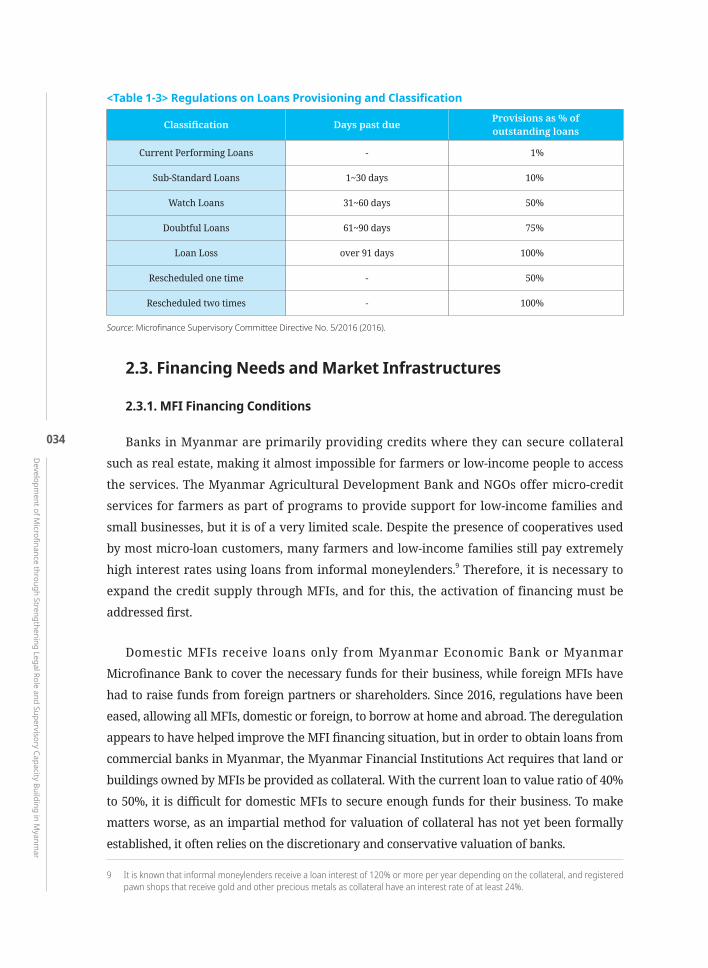

<Table 1-3> Regulations on Loans Provisioning and Classification

Classification Days past due Provisions as % ofoutstanding loans

Current Performing Loans - 1%

Sub-Standard Loans 1~30 days 10%

Watch Loans 31~60 days 50%

Doubtful Loans 61~90 days 75%

Loan Loss over 91 days 100%

Rescheduled one time - 50%

Rescheduled two times - 100%

Source: Microfinance Supervisory Committee Directive No. 5/2016 (2016).

2.3. Financing Needs and Market Infrastructures

2.3.1. MFI Financing Conditions

Banks in Myanmar are primarily providing credits where they can secure collateral such as real estate, making it almost impossible for farmers or low-income people to access the services. The Myanmar Agricultural Development Bank and NGOs offer micro-credit services for farmers as part of programs to provide support for low-income families and small businesses, but it is of a very limited scale. Despite the presence of cooperatives used by most micro-loan customers, many farmers and low-income families still pay extremely high interest rates using loans from informal moneylenders.9 Therefore, it is necessary to expand the credit supply through MFIs, and for this, the activation of financing must be addressed first.

Domestic MFIs receive loans only from Myanmar Economic Bank or Myanmar Microfinance Bank to cover the necessary funds for their business, while foreign MFIs have had to raise funds from foreign partners or shareholders. Since 2016, regulations have been eased, allowing all MFIs, domestic or foreign, to borrow at home and abroad. The deregulation appears to have helped improve the MFI financing situation, but in order to obtain loans from commercial banks in Myanmar, the Myanmar Financial Institutions Act requires that land or buildings owned by MFIs be provided as collateral. With the current loan to value ratio of 40% to 50%, it is difficult for domestic MFIs to secure enough funds for their business. To make matters worse, as an impartial method for valuation of collateral has not yet been formally established, it often relies on the discretionary and conservative valuation of banks.

9 Itisknownthatinformalmoneylendersreceivealoaninterestof120%ormoreperyeardependingonthecollateral,andregisteredpawnshopsthatreceivegoldandotherpreciousmetalsascollateralhaveaninterestrateofatleast24%.

KSP-미얀마-final.indd 34 2021-11-29 오후 2:59:58

035

CHAPTER

01Recom

mendations for Im

proving Microfinance Regulations and Supervision

Most foreign MFIs, which are large in size and capable of strengthening credit from foreign partners, have been financed through equity capital, loans from headquarters and affiliates, and borrowing from offshore banks, but prefer to borrow from local banks in Myanmar owing to the currency risk caused by the high volatility of MMK. Foreign MFIs are unable to provide real estate as collateral which makes it difficult to finance locally, as domestic banks in Myanmar have doubts about the MFI business model itself. Given the much lower cost of financing through the international capital markets, it is necessary to develop adequate hedging measures against foreign exchange risk for all foreign and domestic MFIs.10

2.3.2. Excess Demand and Insufficient Market infrastructure

There are still many restrictions on the MFI financing, but the demand for credit, especially for MSMEs, continues to grow rapidly. Like other ASEAN countries, MSMEs play an important role in Myanmar’s economic well-being. As the main driving force for future national economic development, more than 90% of all enterprises are classified as SMEs, accounting for 50% to 95% of employment and 30% to 53% of GDP. Currently two main channels are available for financing of MSME: policy loan through state-owned banks and loans through commercial banks and MFIs.

Policy loans with interest rates far below the market rate are always in short supply compared to demand. It is difficult for MSMEs to access even loans through commercial banks, which are less competitive than policy loans, because they are unable to provide sufficient collateral for them. After all, self-employed and small business owners with little or no collateral have no option other than to get a loan through MFI. However, most of them do not have the financial documents they need to borrow, and even the basic concepts of finance and debt management are not understood well, making it difficult for them to borrow the necessary amount.

Another important issue is the lack of market infrastructure for MFIs. The lack of an established credit information system has led to structural issues owing to which it costs more to maintain and expand than to enter the market. This in turn is hindering the profitability of MFIs and impeding vitalization of business. For many years, the Myanmar government and banks have been working with international organizations to establish a credit rating system. As a result, Myanmar Credit Bureau (MCB), a joint venture between the Myanmar Banking Association (MBA) and Singapore’s Asian Credit Bureau Holdings, was

10 Giventhatthereisnosecondarybondortreasurybillsmarket,theAMROadvisedtheCentralBankofMyanmartoconsiderintro-ducingitsownversionofDomesticNon-DeliverableForwardasatoolformanagingliquidityandhedgingagainstexchangeraterisk(ASEAN+3MacroeconomicResearchOffice(AMRO),2019).

KSP-미얀마-final.indd 35 2021-11-29 오후 2:59:58

Development of M

icrofinance through Strengthening Legal Role and Supervisory Capacity Building in Myanm

ar

036

launched as the first credit rating agency with approval from the CBM in April of last year. The MCB will take at least several years to play a full-fledged role by accumulating sufficient data necessary for credit evaluation, but its launch serves as the first step toward the official operation of a credit rating system in Myanmar. Along with the launch of the MCB, the Myanmar Microfinance Association (MMFA) also built a platform for collecting and sharing credit information, but this platform has not received the FRD’s official approval yet. It is expected that the upcoming revised MBL and subsequent directives will establish a legal basis for collecting and sharing customer information, which could lead to a more extensive and advanced system for collection and evaluation of credit information with the functions of analyzing customer credit and repayment capabilities.

2.3.3. Other Operational Challenges

While previous studies have not raised concerns or significant implications with regard to over- indebtedness, recent reports from local MFIs indicate that multiple borrowing is increasingly prevalent. According to a survey conducted by M-CRIL in June 2018, about 31% of MFI clients in Myanmar had three or more loans, and the rate of receiving such multiple loans was the highest in Yangon. The multiple-debt problem has an adverse impact on the soundness of financial companies, impedes the smooth supply of microfinance and, if escalates, will act as a risk factor for the entire economy. Although it is clear that problems arise due to the weakening ability of the vulnerable to repay debts when macroeconomic conditions deteriorate, borrowers prefer to take out loans at every opportunity in the presence of excess demand for financing. Local MFI managers also point out that borrowers have limited understanding of the risks associated with borrowing and insufficient knowledge of appropriate accounting practices, budget management and investment. While the aforementioned credit bureaus will play an important role in reducing risk for financial institutions, training in financial literacy is essential to ensure safe and efficient retail lending to low-income people.

Another challenge arises from the fact that Myanmar is a largely cash-driven economy, so MFIs’ loan operations are mainly based on face-to-face transactions. Loan officers typically spend long hours collecting, counting and disbursing cash to new customers, especially in rural areas. Currently, most MFIs are located in urban areas such as Yangon and Mandalay, due to which people living in other areas have limited access to financial services. This is due to the high cost of operating MFIs in rural areas. In order to offset this, MFIs may consider providing incentives such as differentiating the fees and charges levied while processing loans, or financing low-interest policy loans.

KSP-미얀마-final.indd 36 2021-11-29 오후 2:59:58

037