2004 - colorado department of education

TRANSCRIPT

BUSINESS ECONOMIC OUTLOOK

2004

T H I R T Y - N I N T H A N N U A L

Sponsored by the University of Colorado at Boulder,

Leeds School of Business, and KeyBank

BUSINESS ECONOMIC OUTLOOK

2004

T H I R T Y - N I N T H A N N U A L

Price per copy: $50.00

Additional copies may be ordered from:

Business Research Division

University of Colorado at Boulder

420 UCB

Boulder, CO 80309-0420

303-492-8227

ISBN 0-89478-204-5

Copyright 2003 by the

Business Research Division

Leeds School of Business

University of Colorado at Boulder

Boulder, CO 80309-0420

Material contained within the accompanying tables is in the public domain and, with

appropriate credit, may be reproduced without permission. Please reference,

“Business Research Division, Leeds School of Business, University of Colorado at Boulder.”

Printed on recycled paper.

Preface .................................................................................................................................................................. 2

Colorado Then and Now............................................................................................................................................ 4

United States and Colorado Economic Outlook...................................................................................................... 6

Population, Labor Force, and Personal Income .................................................................................... 10

Agriculture................................................................................................................................................ 13

Natural Resources and Mining................................................................................................................ 15

Construction ............................................................................................................................................ 19

Manufacturing.......................................................................................................................................... 22

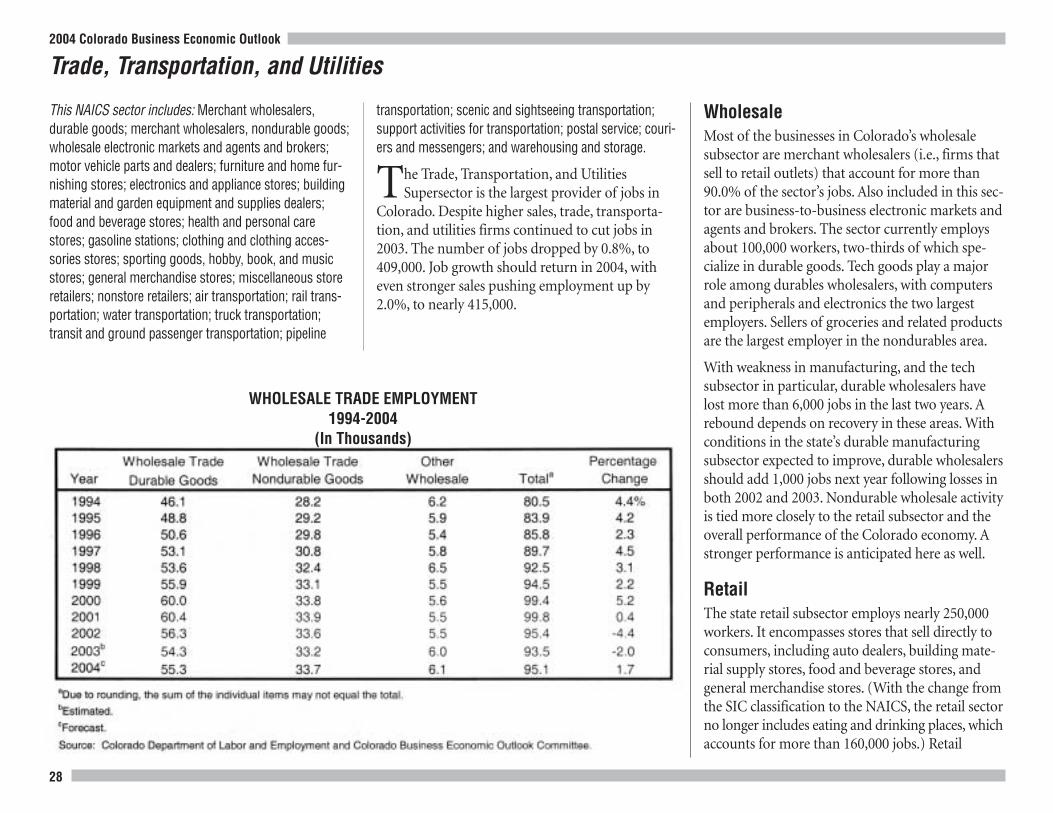

Trade, Transportation, and Utilities........................................................................................................ 28

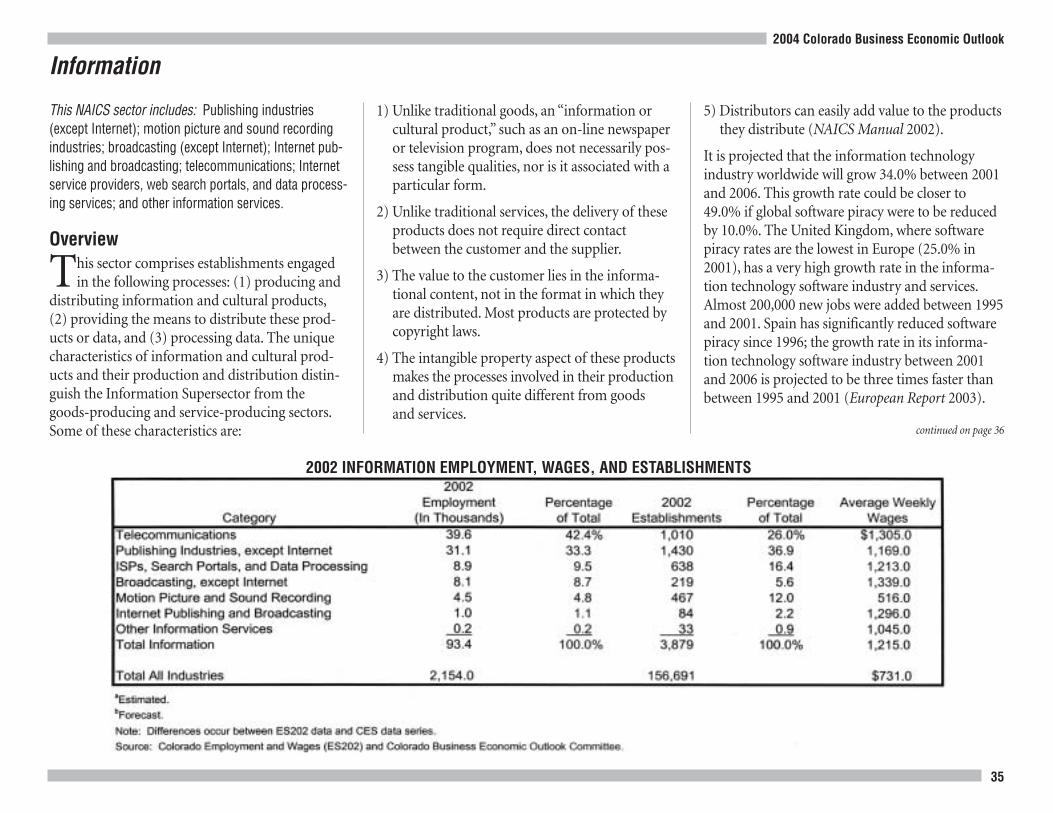

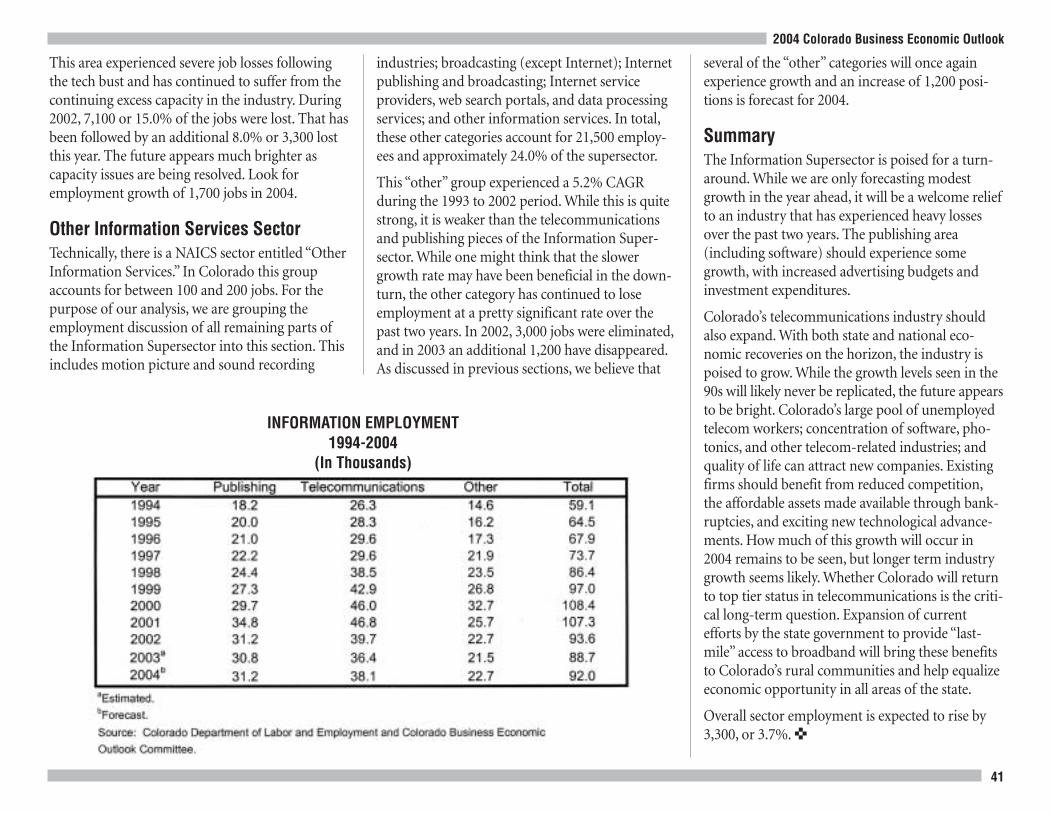

Information .............................................................................................................................................. 35

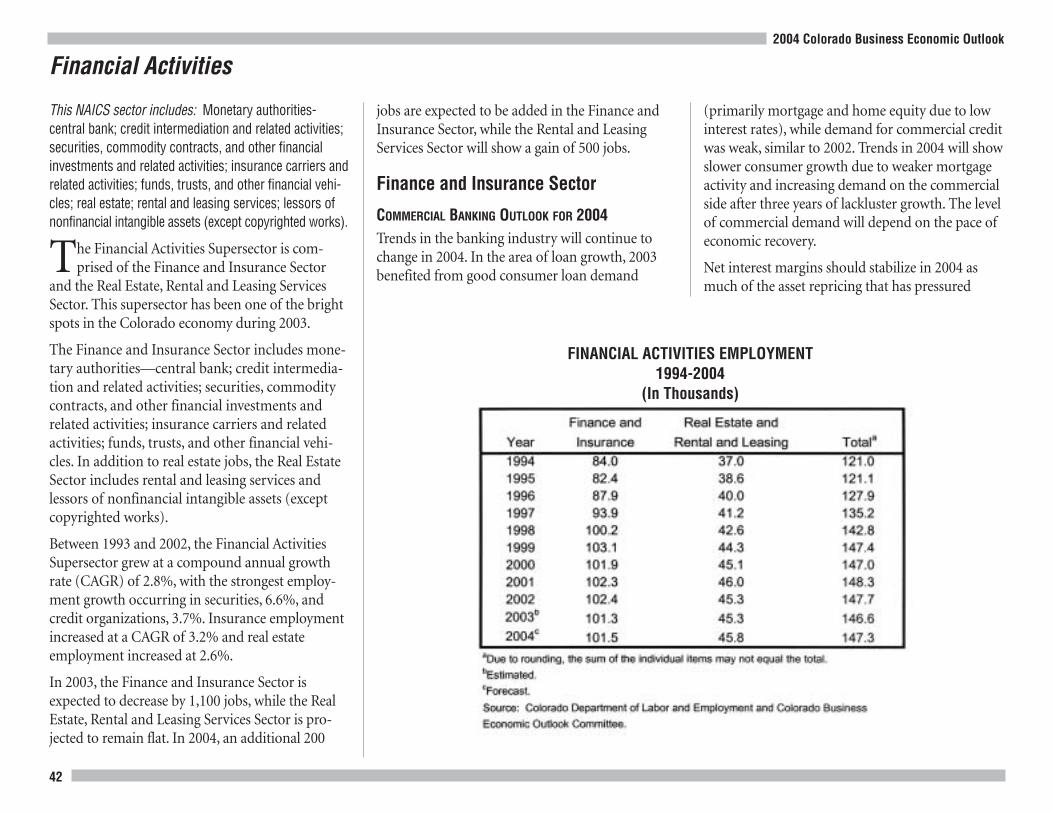

Financial Activities .................................................................................................................................. 42

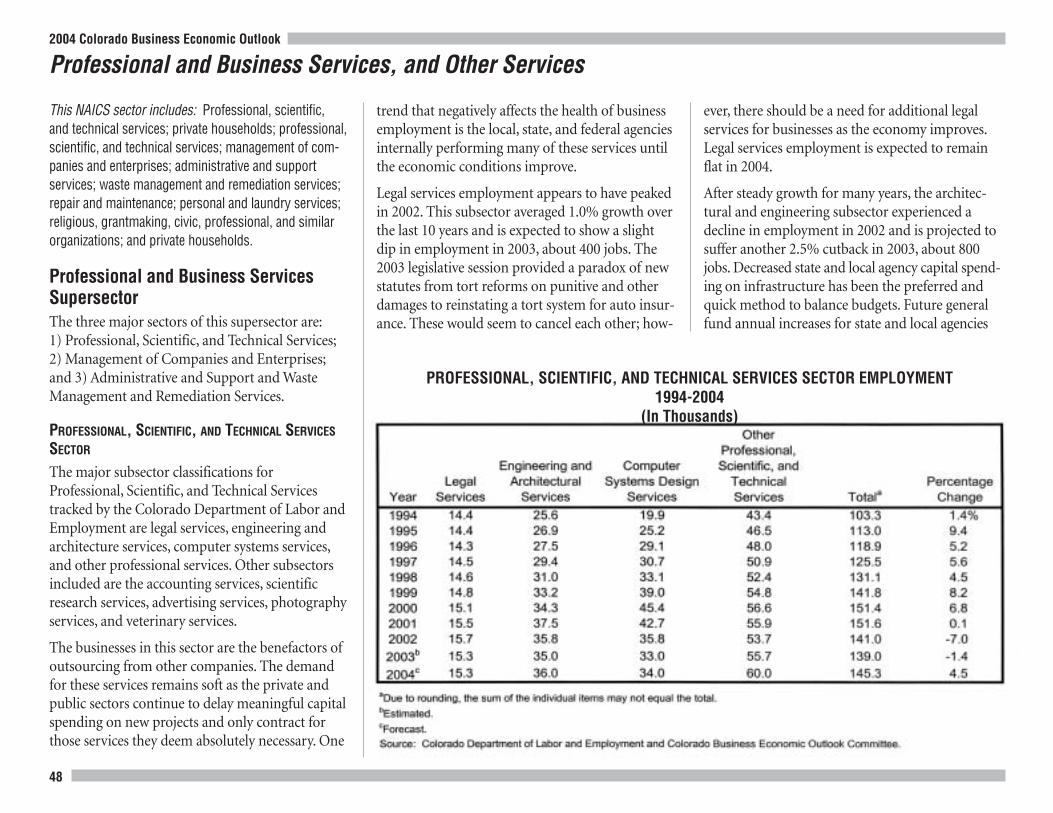

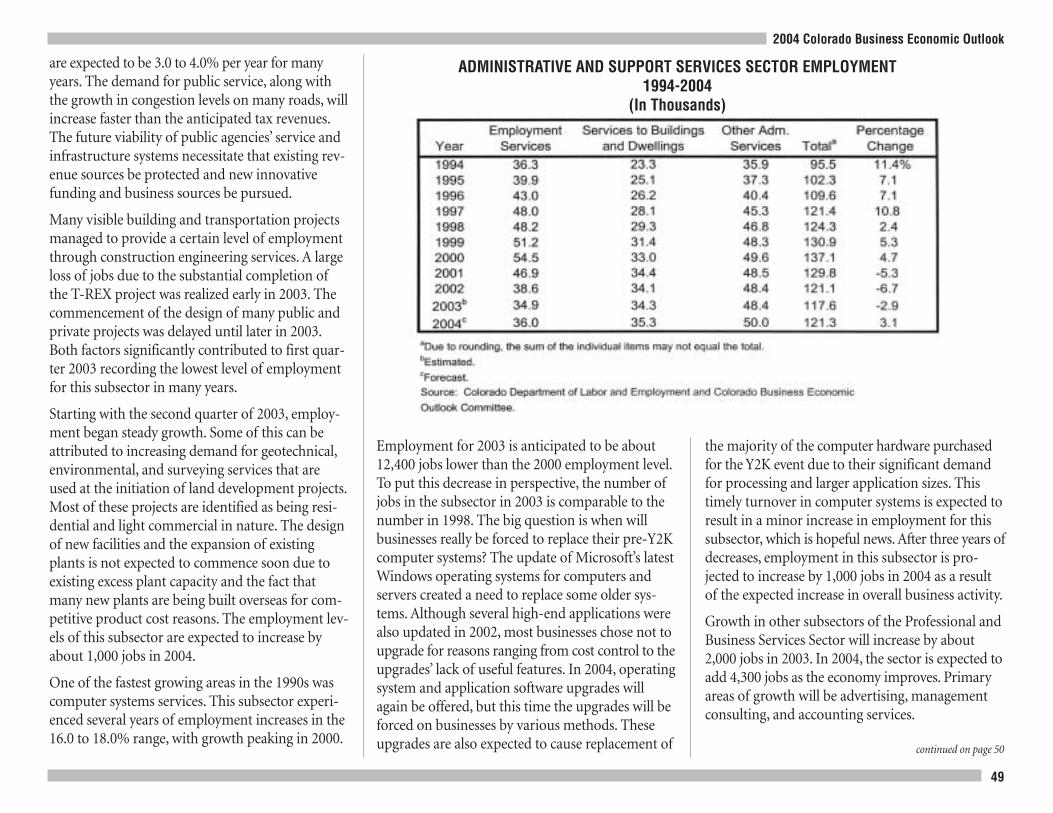

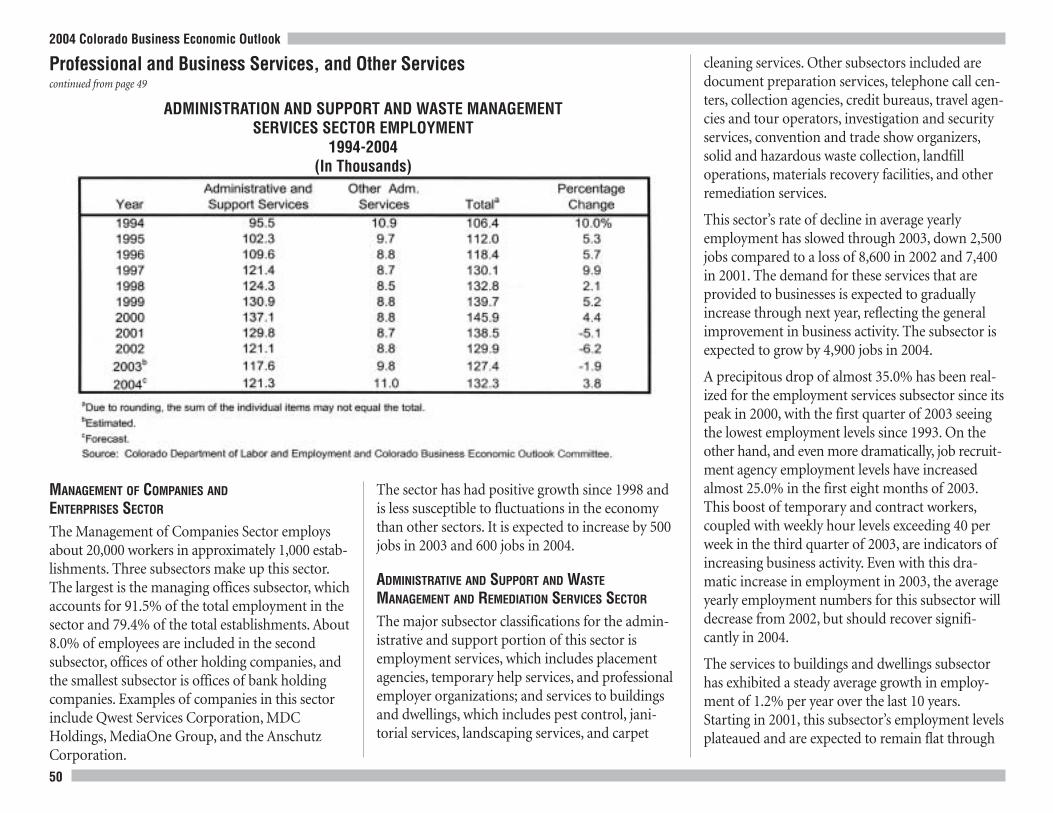

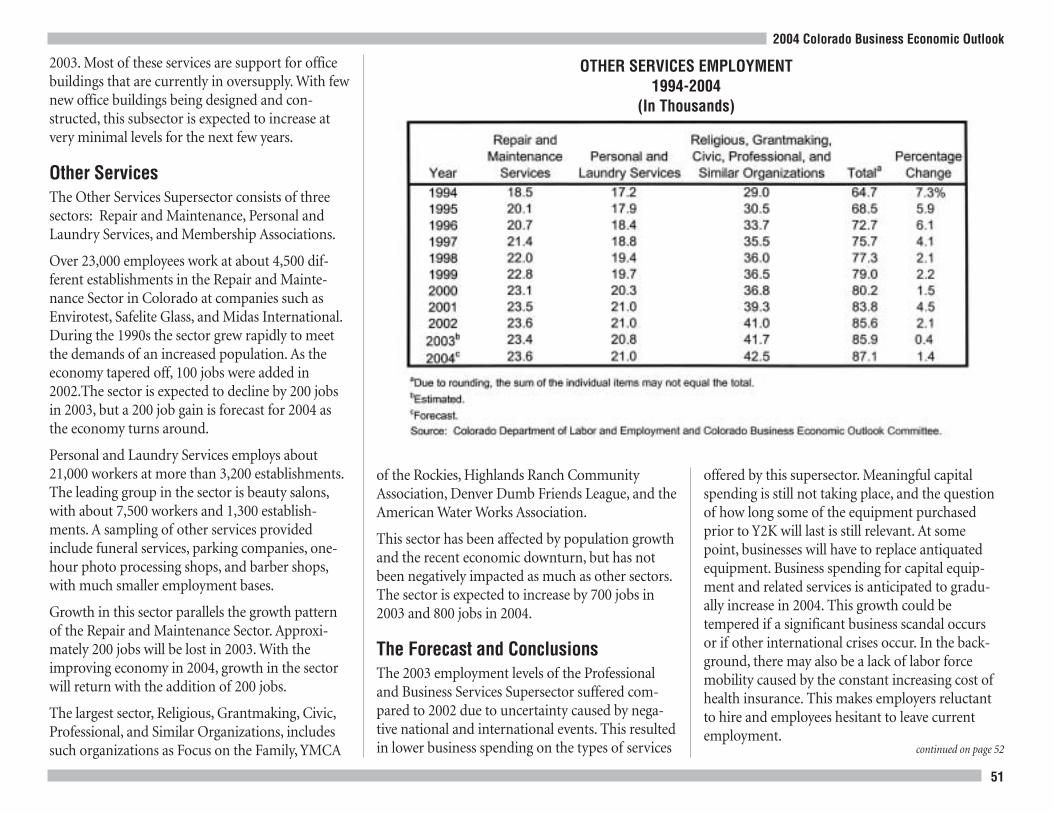

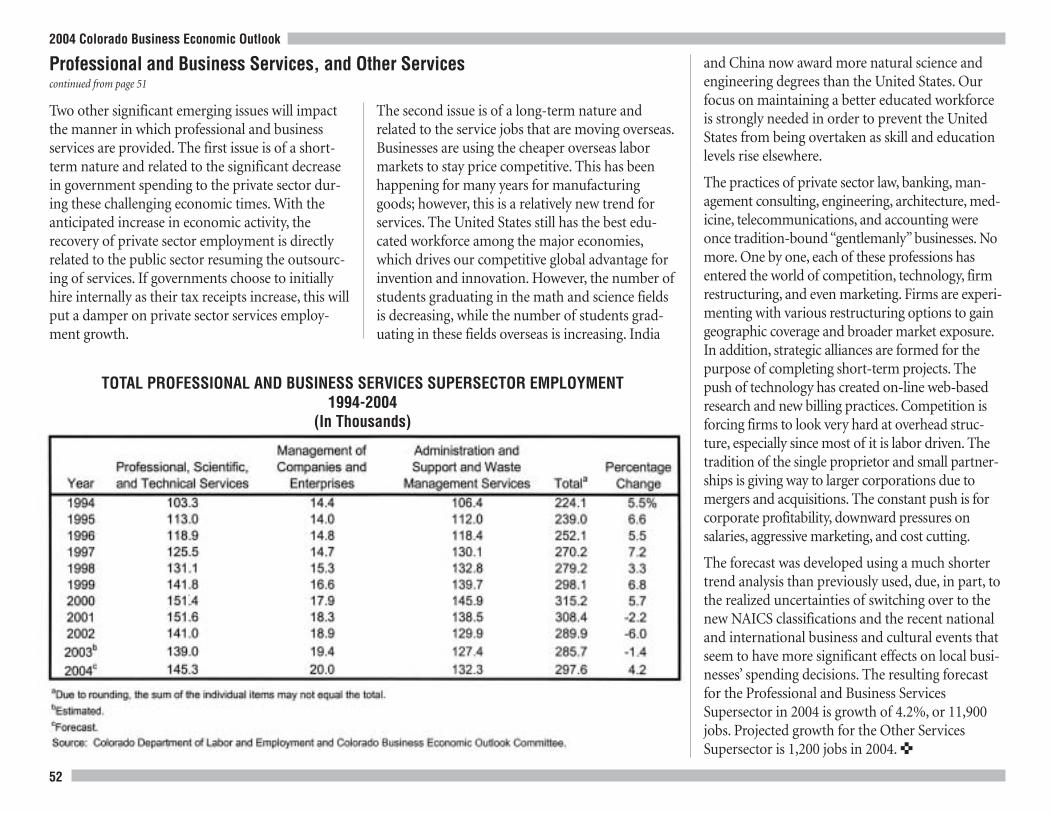

Professional and Business Services, and Other Services........................................................................ 48

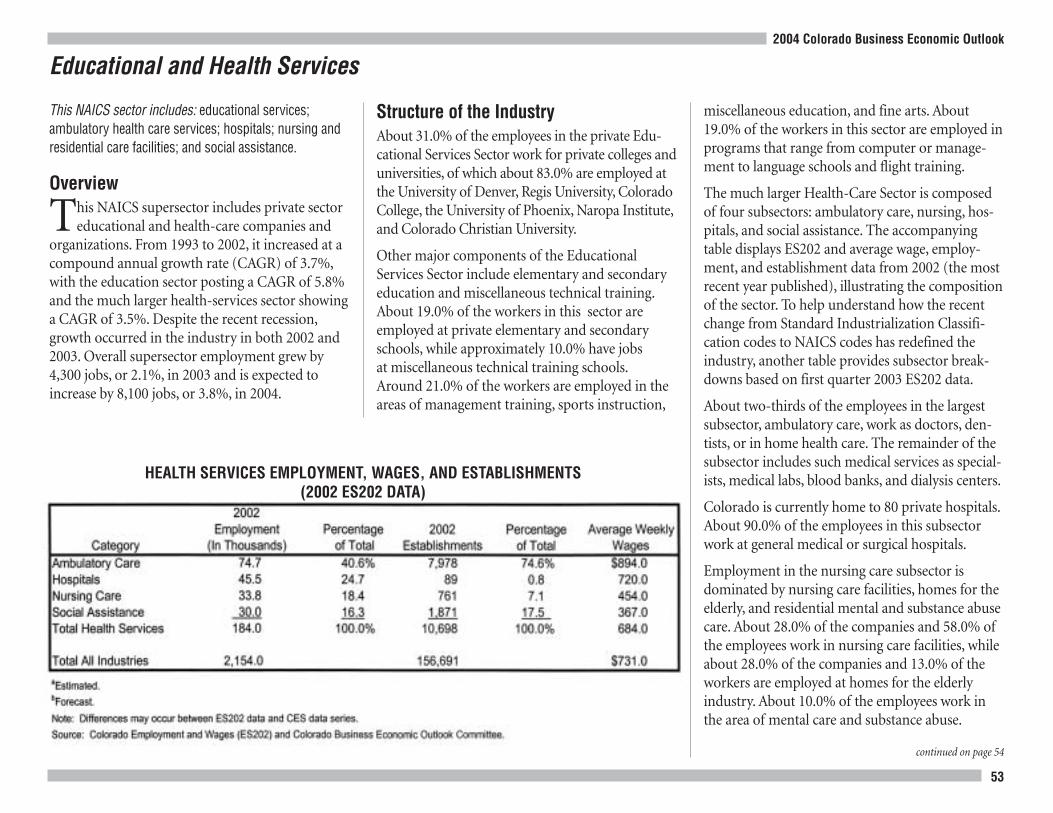

Educational and Health Services ............................................................................................................ 53

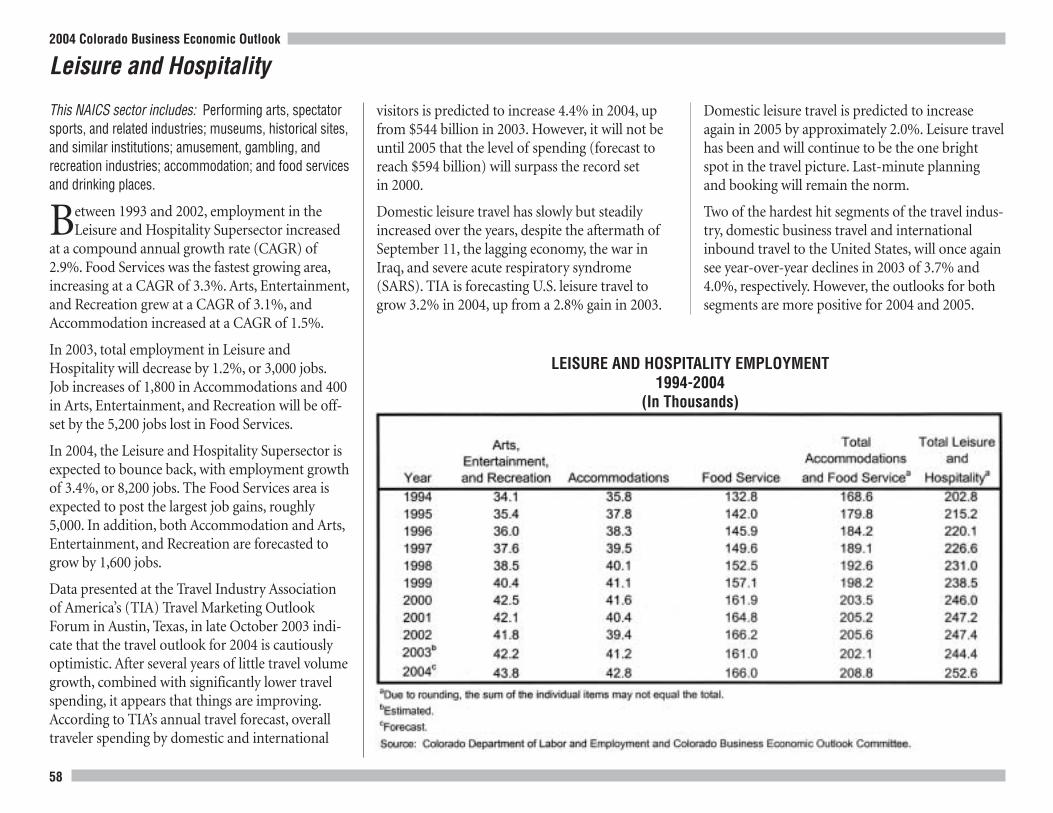

Leisure and Hospitality............................................................................................................................ 58

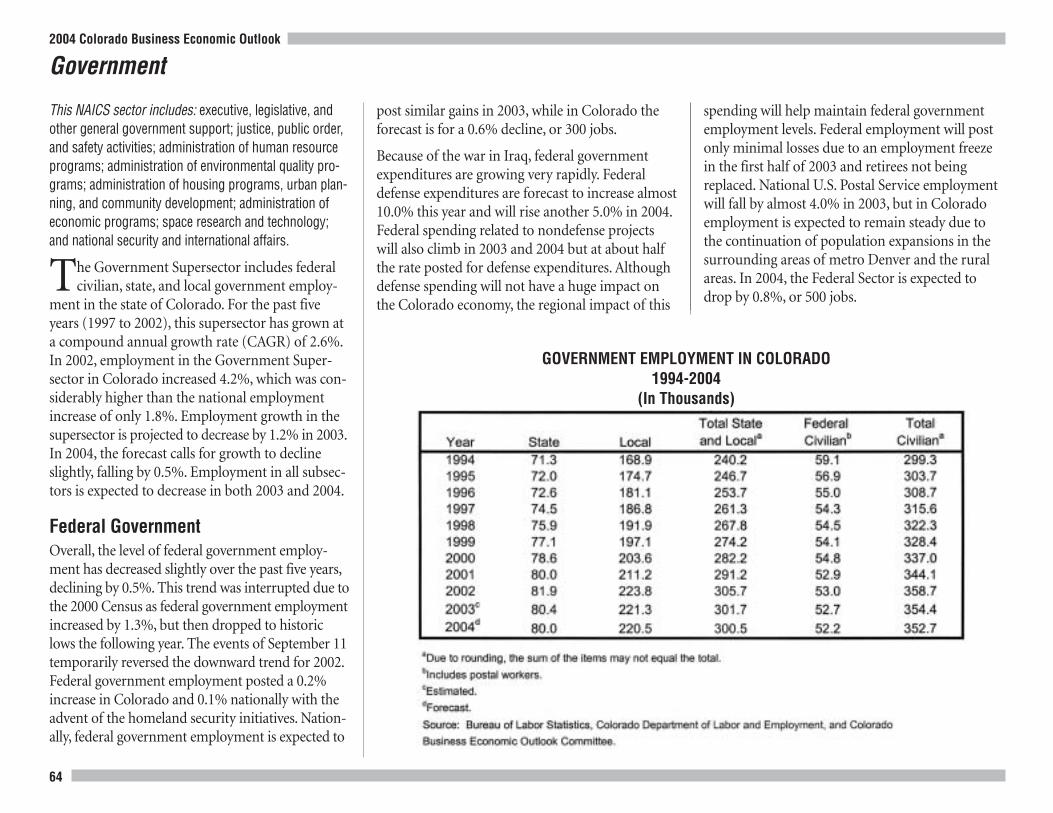

Government.............................................................................................................................................. 64

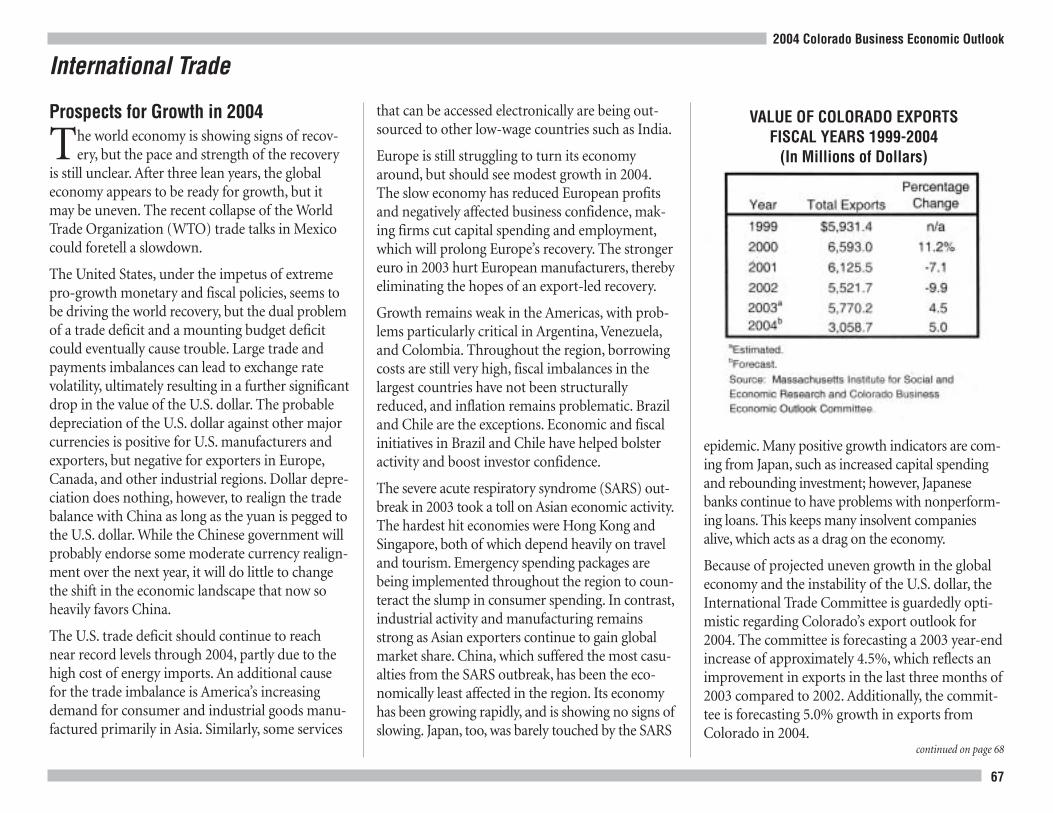

International Trade .................................................................................................................................. 67

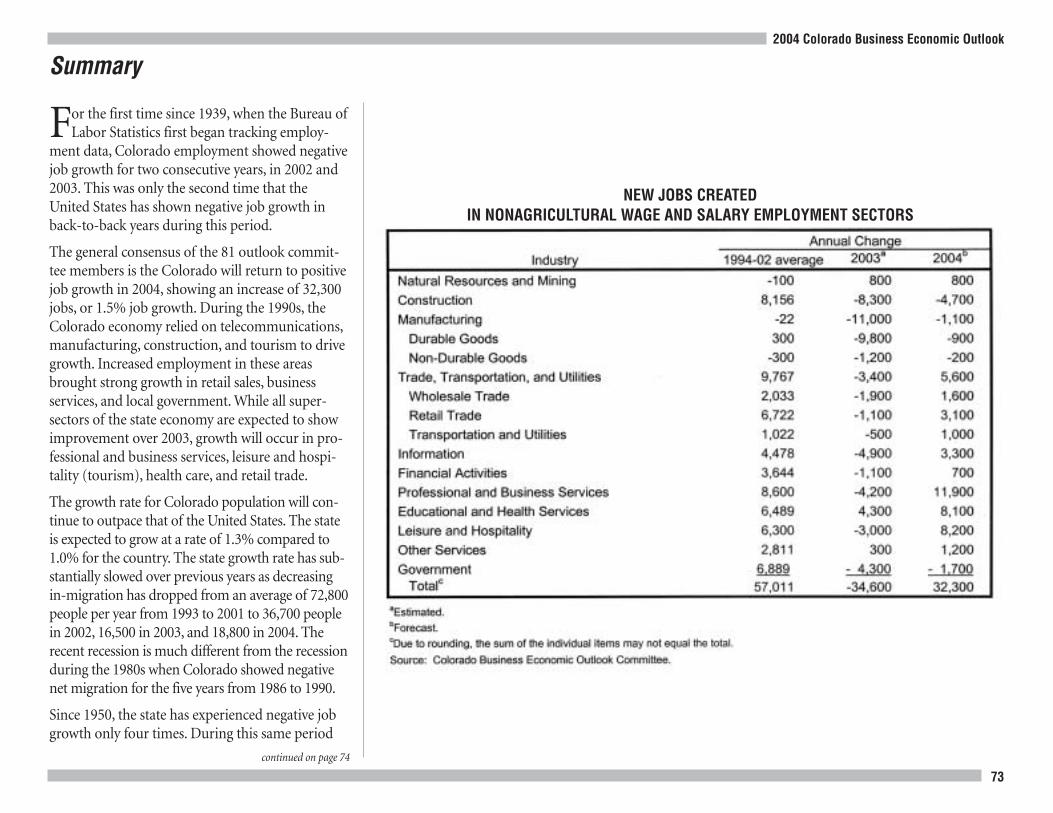

Summary .................................................................................................................................................. 73

From Around the State: La Plata County .............................................................................................. 75

From Around the State: Mesa County .................................................................................................. 76

From Around the State: Northern Colorado ........................................................................................ 77

From Around the State: Pueblo County................................................................................................ 78

From Around the State: Southern Colorado ........................................................................................ 79

Steering Committee Members .................................................................................................................................. 81

Estimating Groups ...................................................................................................................................................... 82

Business Research Division ........................................................................................................................................ 86

University of Colorado at Boulder: Services to Business and Industry ................................................................ 88

Table of Contents

2004 Colorado Business Economic Outlook

2

The annual Colorado Business EconomicOutlook focuses attention on the changing

structure of the Colorado economy, both past andpresent, and projects employment and major eco-nomic indicators for the coming year. With rele-vant, understandable information concerningColorado’s future, we hope to assist in the advance-ment of sound economic development decisionsby policymakers throughout the state. In addition,we strive to give businesses more informationabout the economic reality of the environment inwhich they operate.

The information presented at the Thirty-NinthAnnual Outlook Forum in Denver and the otherforecast presentations throughout the state isreported with greater detail in this publication. Itpresents as complete and knowledgeable a forecastof the 2004 Colorado economy as is possible givenour publishing deadline.

We are extremely pleased to have concerned andcommitted individuals from Colorado business,education, and government organizations through-out the state join and work with us for severalmonths, estimating and projecting the data seriespresented in this statistical summary, as well asproviding significant portions of the narrative. The

efforts of these individuals aregreatly appreciated. A complete listof the contributors appears at theback of this book. If you have ques-tions about the economic sectors orstate regions, we encourage you tocontact these individuals.

I would especially like to acknowl-edge the support and hard work of the LeedsSchool of Business and University of Colorado atBoulder personnel in the preparation, presenta-tion, and promotion of this project. My sincerestthanks go to Gary Horvath, Marketing Analyst;Cindy DiPersio, Publications Coordinator; TerryRosson, Program Assistant; Lynn Reed, GraphicDesigner; Julie Arnett, Research Assistant; BrendanHickey, Erin Hickey, and Spencer Thompson,Student Research Assistants; Lori Call, Director ofCommunications; and Greg Swenson, Staff Writerwith the Office of News Services, for their help inassembling and presenting the 2004 BusinessEconomic Outlook Forum.

IntroductionThe University of Colorado atBoulder Leeds School of Businessis pleased to present our annualforecast of Colorado’s economy.Our program analyzes changesthat took place this past year andprojects activity for 2004.

Work on the forecast began in July, when datacollection and statistical updates were performed.Committees were formed in September with morethan 80 leaders in business, education, and govern-ment, as well as economists and specialists, agreeingto participate. Members were split into 13 groups,each group representing a major economic sector.

Beginning with this forecast, the economic sectorsreflect the new North American IndustryClassification System (NAICS), adopted in January2001. The system is more relevant to the moderneconomy, and will allow the United States todirectly compare its economic data with that ofother NAFTA members, Canada and Mexico.

Forecasts for each sector were prepared by extrapo-lating historical trends and then modifying theresults with

Preface

1) Information from extensive survey work con-ducted with key Colorado business and industryleaders;

2) The expert knowledge and judgment of com-mittee members; and

3) Known or expected economic changes affectingcertain industrial sectors within the state.

The unique nature of the Business EconomicOutlook forecast is its combined approach of usingdetailed statistics with extensive survey researchand expert opinion. We believe this methodologyprovides additional qualitative insight particularlyrelevant to the short-term forecasting process.

Richard L. Wobbekind, Ph.D.Associate Dean of External Relations and DirectorBusiness Research DivisionLeeds School of BusinessUniversity of Colorado at Boulder

3

2004 Colorado Business Economic Outlook

A Return to Optimism

For the first time in several years,there seems to be a glimmer of

light at the end of the tunnel—andsome promising economic news forthe United States and for Colorado.In what we all hope is the beginningof a sustained economic trend, itwas announced several weeks agothat the U.S. gross domestic product grew by 7.2%in the third quarter. Better still is what we see hap-pening in this region. The business community hasseemingly weathered the worst of the cycle, andevidence suggests that some industries are gettinghealthy once again.

Whether we’re at the peak or the bottom of thecycle, though, KeyBank has been and continues tobe strongly committed to this community, and toserving the total financial needs of Colorado. We’refocused on being more valuable to our clients andto this community by offering better ideas andfinancial solutions that are meaningful and rele-vant in today’s economic environment.

With that as a backdrop, it is KeyBank’s privilegeonce again this year to partner with the Universityof Colorado’s Leeds School of Business to sponsorthis annual event. This is the third year of our part-nership, and I cannot think of a better organization

to team with in order to provideyou with the latest in-depth knowl-edge and investment research.

Today, we will hear about currenteconomic trends, and what theexperts anticipate for the comingyear. How will an election yearnext year affect the economy? How

can this region leverage its role as a major distribu-tion hub to uncover future growth opportunities?And finally, will sectors such as technology, tele-communications, and tourism bounce back, or arethere new, emerging sectors that will lead this areaback to economic prosperity?

On behalf of KeyBank, I would like to thank youfor your continued commitment to this importantprogram, and for supporting the 2004 installmentof the Leeds School of Business annual economicforecast.

Michael B. HobbsExecutive Vice PresidentKeyBank Commercial Banking

4

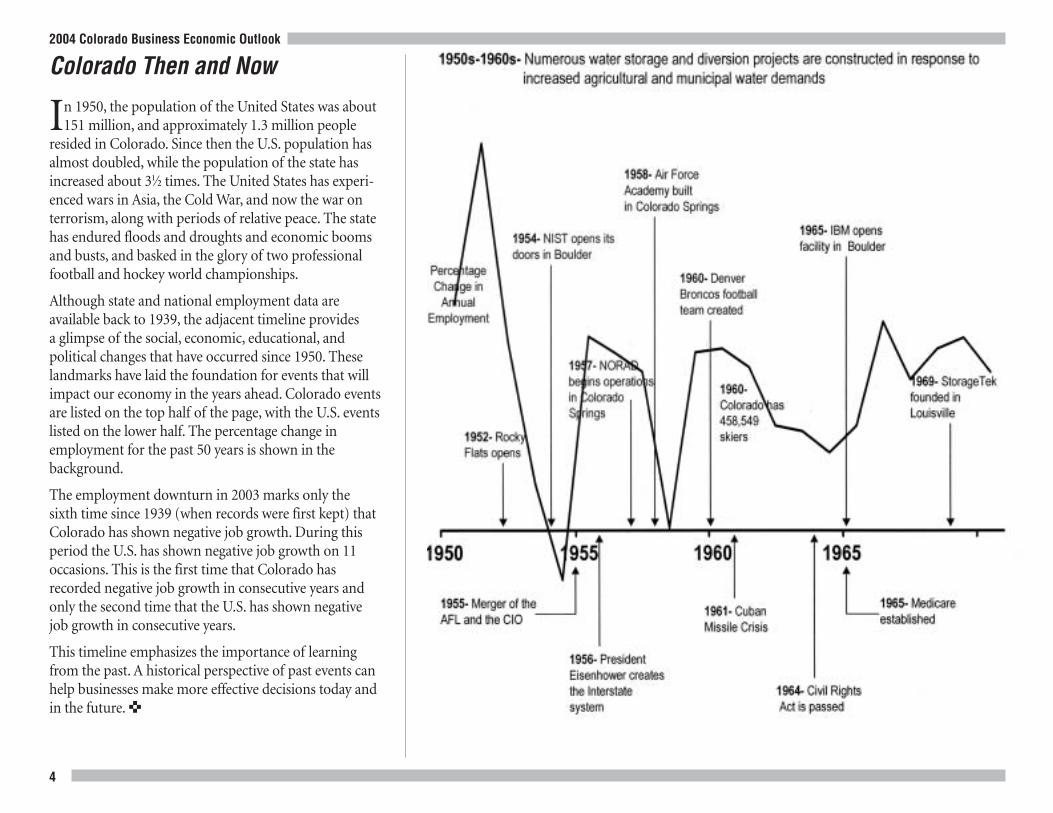

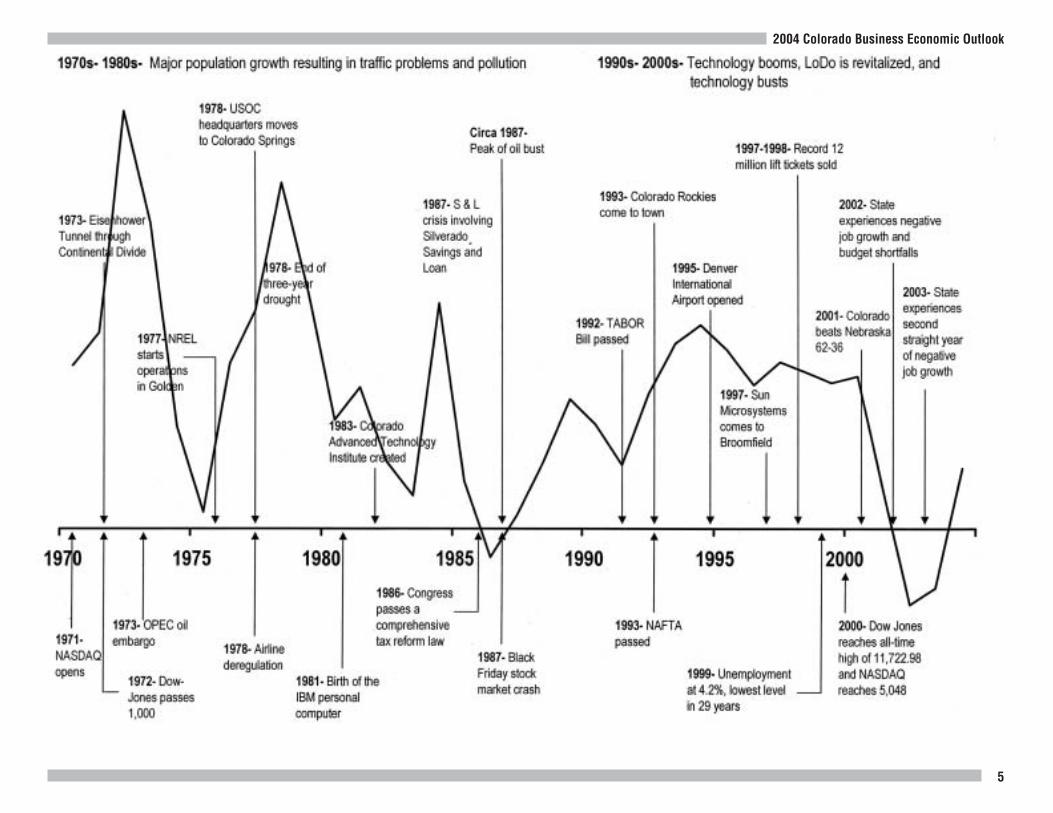

Colorado Then and Now

In 1950, the population of the United States was about151 million, and approximately 1.3 million people

resided in Colorado. Since then the U.S. population hasalmost doubled, while the population of the state hasincreased about 31⁄2 times. The United States has experi-enced wars in Asia, the Cold War, and now the war onterrorism, along with periods of relative peace. The statehas endured floods and droughts and economic boomsand busts, and basked in the glory of two professionalfootball and hockey world championships.

Although state and national employment data areavailable back to 1939, the adjacent timeline provides a glimpse of the social, economic, educational, andpolitical changes that have occurred since 1950. Theselandmarks have laid the foundation for events that willimpact our economy in the years ahead. Colorado eventsare listed on the top half of the page, with the U.S. eventslisted on the lower half. The percentage change inemployment for the past 50 years is shown in thebackground.

The employment downturn in 2003 marks only the sixth time since 1939 (when records were first kept) thatColorado has shown negative job growth. During thisperiod the U.S. has shown negative job growth on 11occasions. This is the first time that Colorado hasrecorded negative job growth in consecutive years andonly the second time that the U.S. has shown negative job growth in consecutive years.

This timeline emphasizes the importance of learningfrom the past. A historical perspective of past events canhelp businesses make more effective decisions today andin the future. ✜

2004 Colorado Business Economic Outlook

5

2004 Colorado Business Economic Outlook

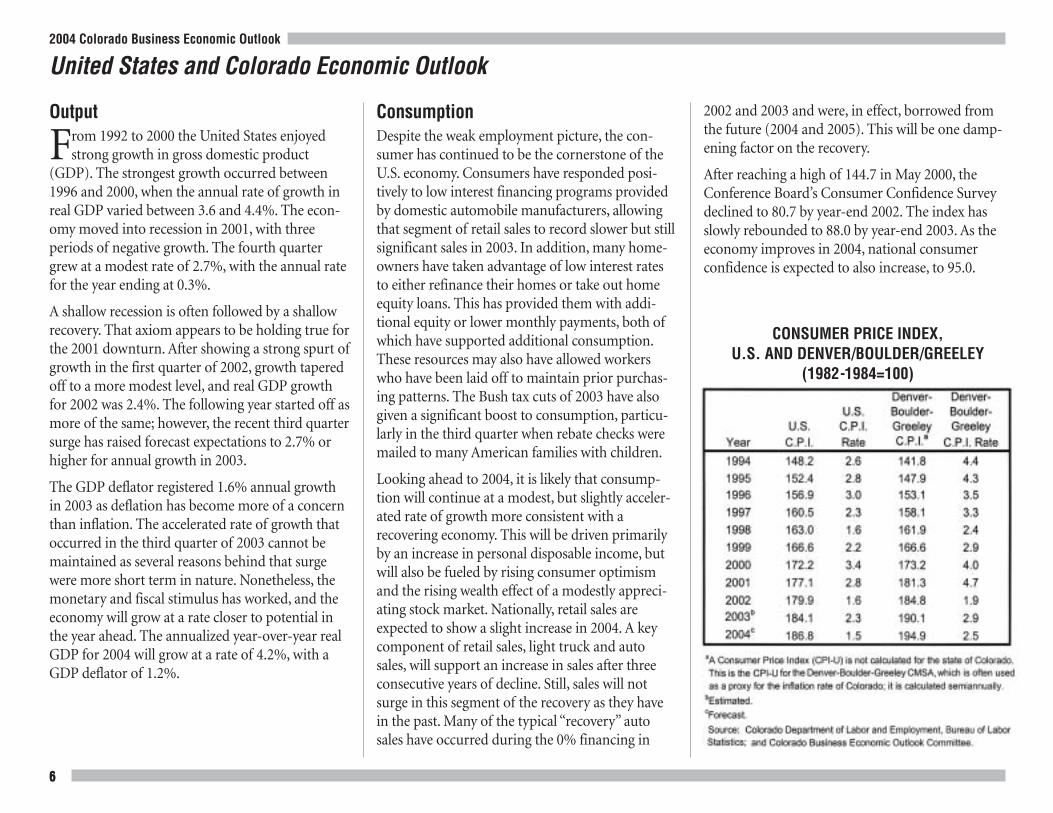

CONSUMER PRICE INDEX, U.S. AND DENVER/BOULDER/GREELEY

(1982-1984=100)

2004 Colorado Business Economic Outlook

66

Output

From 1992 to 2000 the United States enjoyedstrong growth in gross domestic product

(GDP). The strongest growth occurred between1996 and 2000, when the annual rate of growth inreal GDP varied between 3.6 and 4.4%. The econ-omy moved into recession in 2001, with threeperiods of negative growth. The fourth quartergrew at a modest rate of 2.7%, with the annual ratefor the year ending at 0.3%.

A shallow recession is often followed by a shallowrecovery. That axiom appears to be holding true forthe 2001 downturn. After showing a strong spurt ofgrowth in the first quarter of 2002, growth taperedoff to a more modest level, and real GDP growthfor 2002 was 2.4%. The following year started off asmore of the same; however, the recent third quartersurge has raised forecast expectations to 2.7% orhigher for annual growth in 2003.

The GDP deflator registered 1.6% annual growthin 2003 as deflation has become more of a concernthan inflation. The accelerated rate of growth thatoccurred in the third quarter of 2003 cannot bemaintained as several reasons behind that surgewere more short term in nature. Nonetheless, themonetary and fiscal stimulus has worked, and theeconomy will grow at a rate closer to potential inthe year ahead. The annualized year-over-year realGDP for 2004 will grow at a rate of 4.2%, with aGDP deflator of 1.2%.

United States and Colorado Economic Outlook

ConsumptionDespite the weak employment picture, the con-sumer has continued to be the cornerstone of theU.S. economy. Consumers have responded posi-tively to low interest financing programs providedby domestic automobile manufacturers, allowingthat segment of retail sales to record slower but stillsignificant sales in 2003. In addition, many home-owners have taken advantage of low interest ratesto either refinance their homes or take out homeequity loans. This has provided them with addi-tional equity or lower monthly payments, both ofwhich have supported additional consumption.These resources may also have allowed workerswho have been laid off to maintain prior purchas-ing patterns. The Bush tax cuts of 2003 have alsogiven a significant boost to consumption, particu-larly in the third quarter when rebate checks weremailed to many American families with children.

Looking ahead to 2004, it is likely that consump-tion will continue at a modest, but slightly acceler-ated rate of growth more consistent with arecovering economy. This will be driven primarilyby an increase in personal disposable income, butwill also be fueled by rising consumer optimismand the rising wealth effect of a modestly appreci-ating stock market. Nationally, retail sales areexpected to show a slight increase in 2004. A keycomponent of retail sales, light truck and autosales, will support an increase in sales after threeconsecutive years of decline. Still, sales will notsurge in this segment of the recovery as they havein the past. Many of the typical “recovery” autosales have occurred during the 0% financing in

2002 and 2003 and were, in effect, borrowed fromthe future (2004 and 2005). This will be one damp-ening factor on the recovery.

After reaching a high of 144.7 in May 2000, theConference Board’s Consumer Confidence Surveydeclined to 80.7 by year-end 2002. The index hasslowly rebounded to 88.0 by year-end 2003. As theeconomy improves in 2004, national consumerconfidence is expected to also increase, to 95.0.

2004 Colorado Business Economic Outlook

7

While there is no state indicator of consumer con-fidence, the Conference Board measures consumerconfidence for the Mountain States. Prior to 1991the Mountain index for consumer confidence wasconsistently lower than the U.S. index. In 1991 thistrend reversed itself, and consumer confidence inthe Mountain States has remained higher than inthe United States overall. On occasion, theMountain index was up to 30 points higher thanthe U.S. index during the mid-1990s, but as thedecade ended the difference dropped to a range of5 to 10 points. During the recent downturn the dif-ference between the two indexes has become muchsmaller. Although Rocky Mountain consumer con-fidence has recently surged, the year-end index forthe Mountain States is expected to be only 100.0for 2003 and 110.0 for 2004.

InvestmentAnother component to growth is investment.During both 2001 and 2002, companies showed a decrease in business investments of more than5.0% each year. This negative trend has reverseditself in 2003 as companies found that they couldno longer postpone certain business expenditures.Year-end investment should rise by 2.0%, modestby the standards set in the late 1990s, but positiveafter the aforementioned two years of decline. Aswe go forward, continued replacement investment,augmented by an increased demand for expansion-ary investment, will drive growth in this area.Business investments are expected to expand by a more robust 9.2% in 2004.

In part as a result of this increase in investment,industrial production will rise by 4.3% in 2004after experiencing a meager 0.1% gain this year.Business inventories will also grow from less than

$1 billion in 2003 to $43.7 billion in 2004. The fail-ure of businesses to expand their inventories in2003 was one of the major reasons that the macro-economic recovery was slow. Currently, inventory-to-sales ratios are at their lowest levels in history,which indicates they will need to be replenished inshort order. As orders pick up, firms will be morelikely to invest in inventory to make certain theycan fulfill demand for their product. However, it isnot clear that we will return to historic inventory-to-sales ratios even during a more robust recovery.Much of the investment in “just-in-time” produc-tion and other cost-saving devices will likely changethe long-term inventory-to-sales ratio relationship.

In 2004, housing starts are expected to decline as mortgage rates continue their slow rise from

40-year lows reached in July 2003. Still, the housingmarket is expected to be better than it was in the1999-2001 period. This optimism is fueled byincreased employment levels and continued goodmortgage rates. (Mortgage rates remain at 20-yearlows at the time of this writing, November 2003.)In Colorado, the number of housing starts will notbe as strong as at the national level, although webelieve that permits will move slightly back into thepositive range. Much of the new construction inColorado will continue to be in lower priced homes.

No appreciable improvement is anticipated in theU.S. international trade position until internationaleconomic conditions improve. Although the dollar

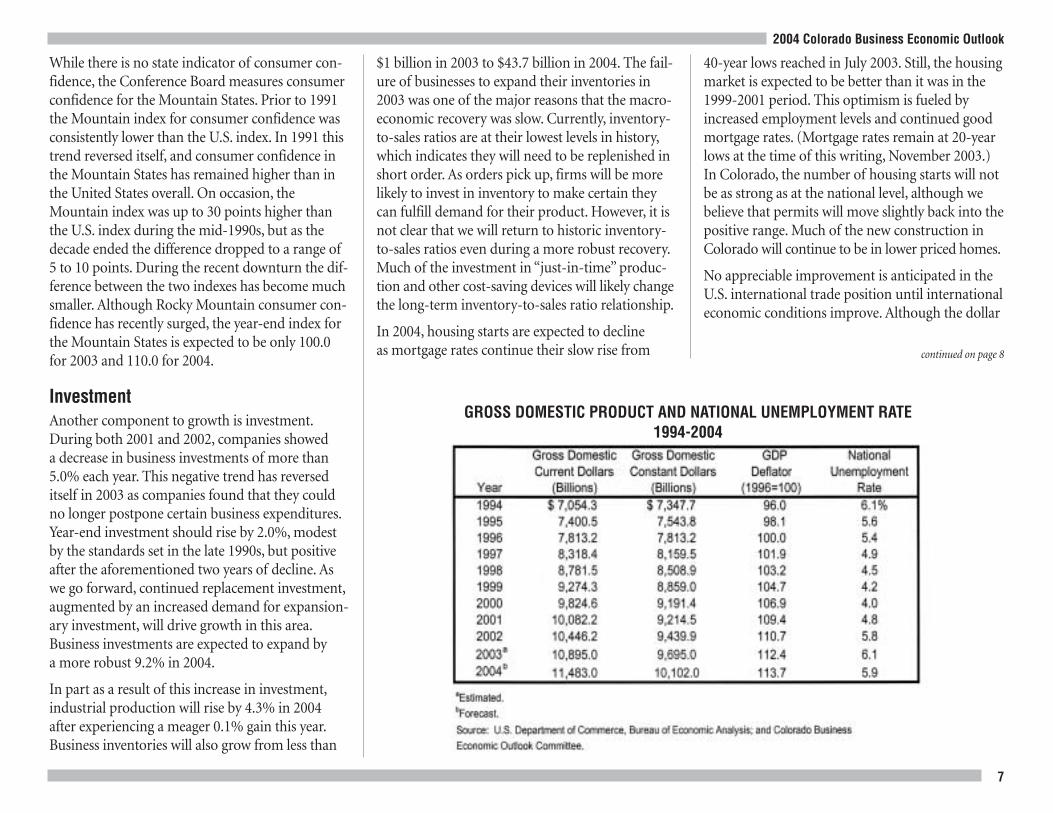

GROSS DOMESTIC PRODUCT AND NATIONAL UNEMPLOYMENT RATE1994-2004

continued on page 8

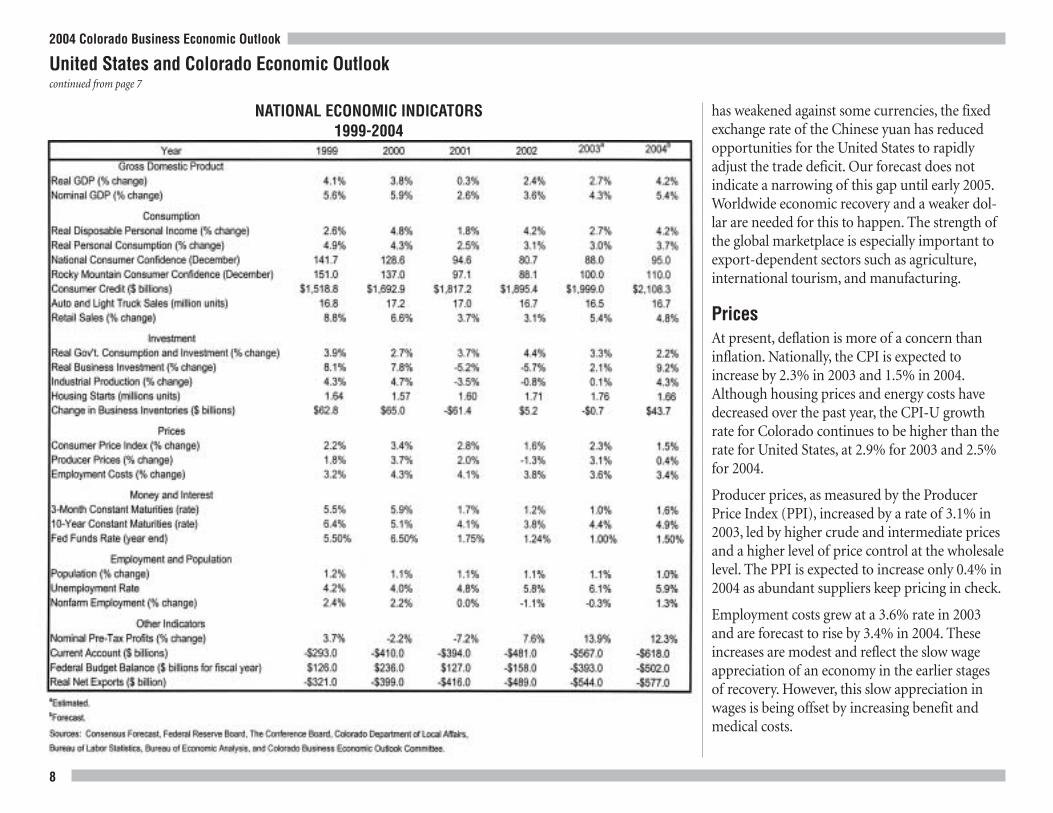

NATIONAL ECONOMIC INDICATORS1999-2004

2004 Colorado Business Economic Outlook

8

United States and Colorado Economic Outlookcontinued from page 7

has weakened against some currencies, the fixedexchange rate of the Chinese yuan has reducedopportunities for the United States to rapidlyadjust the trade deficit. Our forecast does notindicate a narrowing of this gap until early 2005.Worldwide economic recovery and a weaker dol-lar are needed for this to happen. The strength ofthe global marketplace is especially important toexport-dependent sectors such as agriculture,international tourism, and manufacturing.

PricesAt present, deflation is more of a concern thaninflation. Nationally, the CPI is expected toincrease by 2.3% in 2003 and 1.5% in 2004.Although housing prices and energy costs havedecreased over the past year, the CPI-U growthrate for Colorado continues to be higher than therate for United States, at 2.9% for 2003 and 2.5%for 2004.

Producer prices, as measured by the ProducerPrice Index (PPI), increased by a rate of 3.1% in2003, led by higher crude and intermediate pricesand a higher level of price control at the wholesalelevel. The PPI is expected to increase only 0.4% in2004 as abundant suppliers keep pricing in check.

Employment costs grew at a 3.6% rate in 2003and are forecast to rise by 3.4% in 2004. Theseincreases are modest and reflect the slow wageappreciation of an economy in the earlier stagesof recovery. However, this slow appreciation inwages is being offset by increasing benefit andmedical costs.

2004 Colorado Business Economic Outlook

9

Employment and PopulationNational unemployment increased from 4.8% in2001 to 5.8% in 2002 and 6.1% in 2003. We fore-cast a slight decline, to 5.9%, in 2004 as overalllabor conditions and hiring improve. More robusthiring plans will be partially offset by some of theworkers reentering the workforce. This increase inlabor force participation, while welcomed, willkeep the unemployment number high.

As 2004 begins, job creation at the national level isexpected to be broad based, with most sectorsexperiencing growth. Throughout the year, the

service-producing subsectors are expected to growmore rapidly, while the goods-producing sectorsare expected to lag.

The Colorado economy depends on the nationaland global economy for its growth. Unemploymentin the state is expected to again remain below thatof the United States, coming in at a rate of 5.7% in2003 and dropping to 5.6% in 2004.

Nationally, population is expected to show growthof 1.1% in 2003 and 1.0% in 2004, while the growthof the state is expected to slow to 1.2% in 2003 andincrease slightly, to 1.3%, in 2004. The biggest

factor in the slowing of the state’s growth rate fromthe rates of the 1990s has been the significantdecrease in net migration. While net migration issubstantially lower than the 1990s, it is still positiveand has helped to stabilize housing market pricesin an extremely weak employment environment.

In the sections that follow, a summary of 2003 anda forecast for 2004 is presented. These sections pro-vide insight into the key factors influencing each ofthese sectors. We trust this data and analysis willprove useful in your business and policy decision-making process. ✜

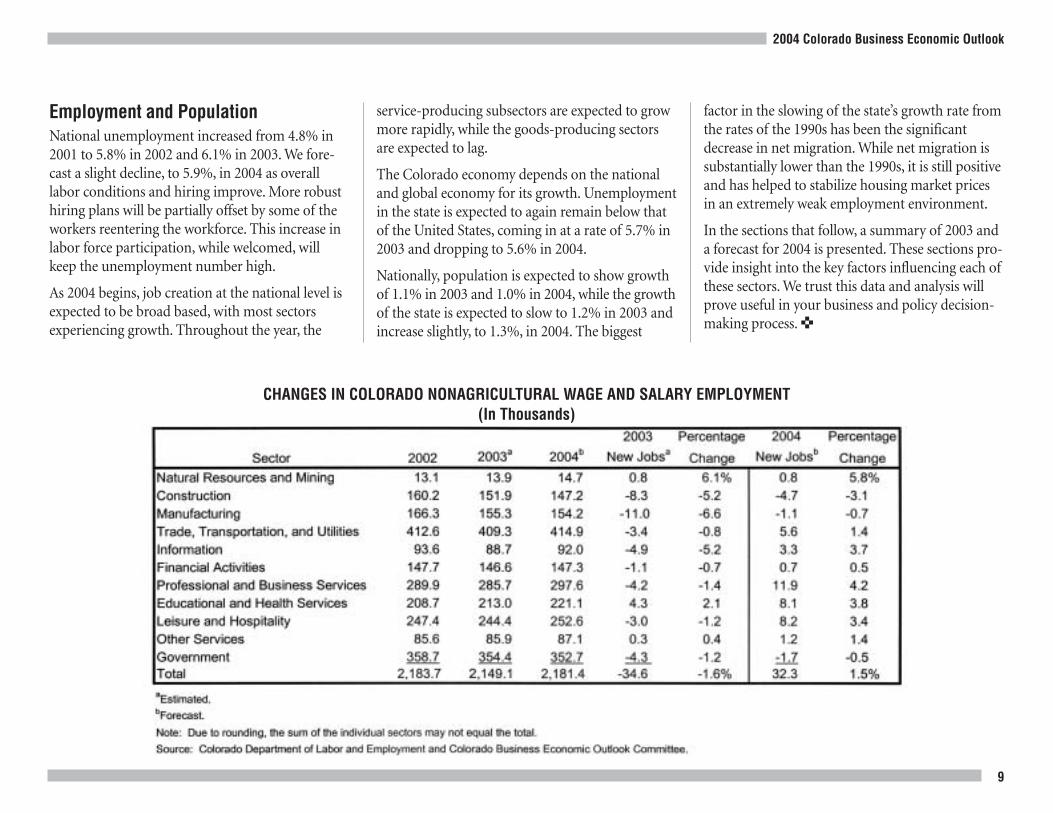

CHANGES IN COLORADO NONAGRICULTURAL WAGE AND SALARY EMPLOYMENT(In Thousands)

2004 Colorado Business Economic Outlook

10

Population, Labor Force, andPersonal Income

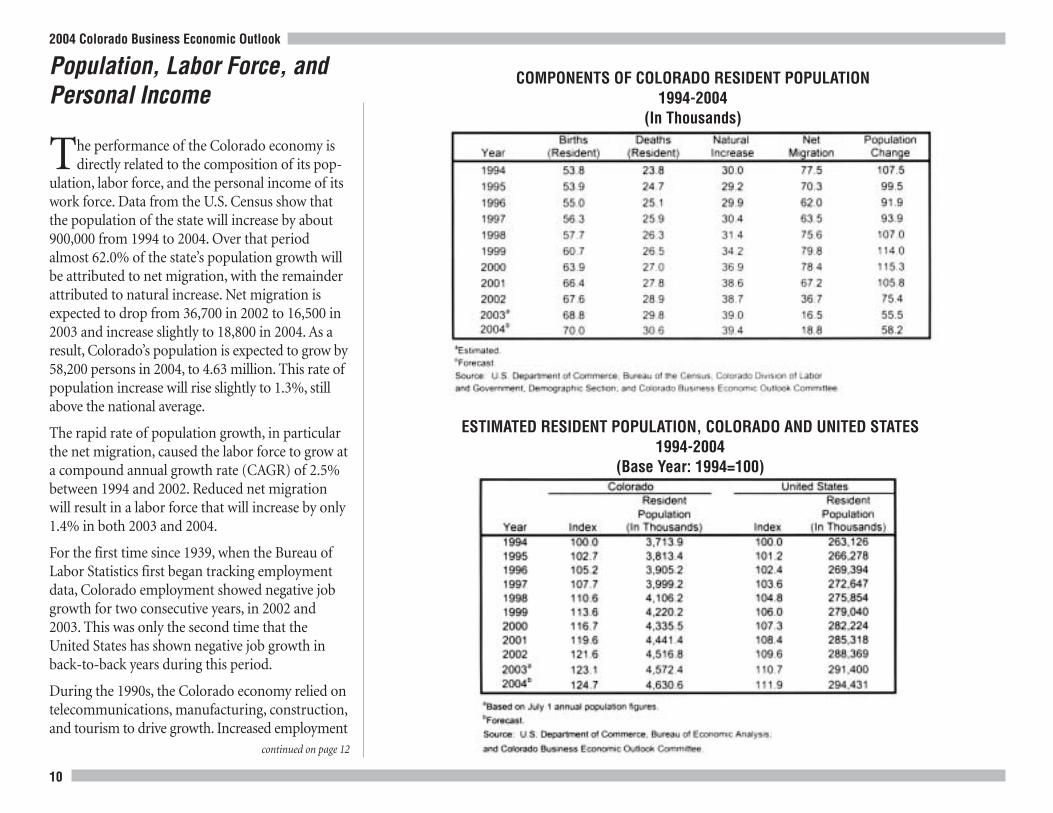

The performance of the Colorado economy isdirectly related to the composition of its pop-

ulation, labor force, and the personal income of itswork force. Data from the U.S. Census show thatthe population of the state will increase by about900,000 from 1994 to 2004. Over that periodalmost 62.0% of the state’s population growth willbe attributed to net migration, with the remainderattributed to natural increase. Net migration isexpected to drop from 36,700 in 2002 to 16,500 in2003 and increase slightly to 18,800 in 2004. As aresult, Colorado’s population is expected to grow by58,200 persons in 2004, to 4.63 million. This rate ofpopulation increase will rise slightly to 1.3%, stillabove the national average.

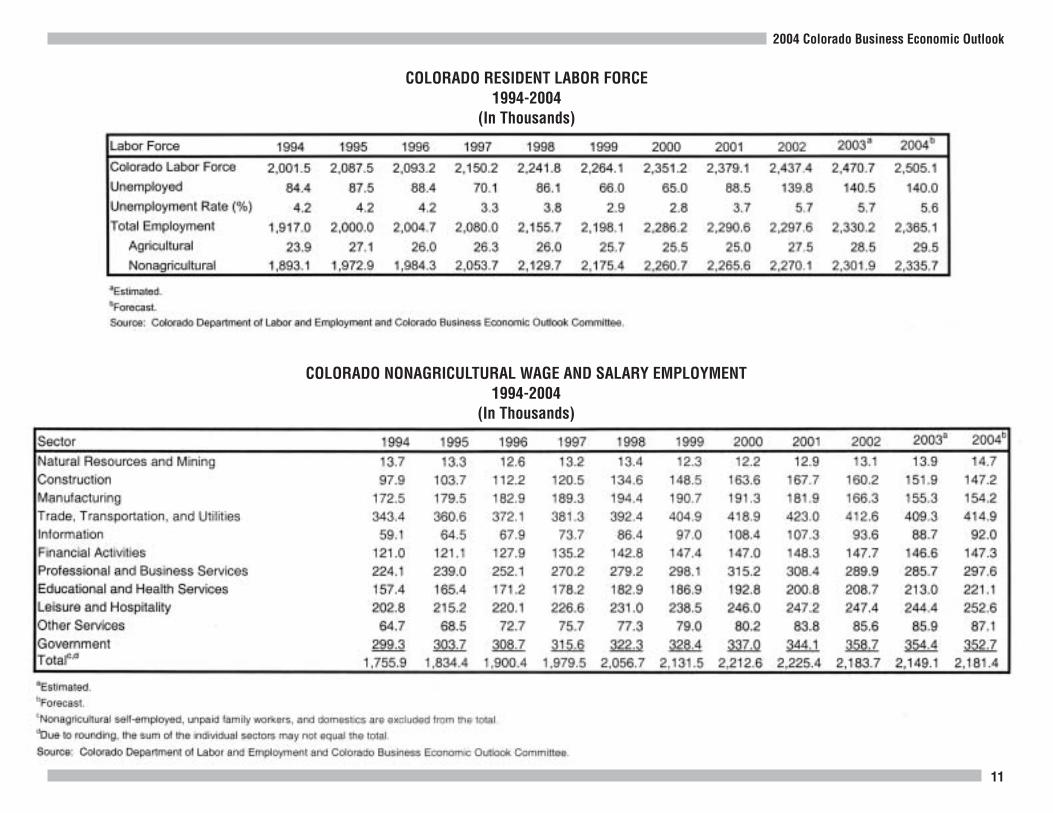

The rapid rate of population growth, in particularthe net migration, caused the labor force to grow ata compound annual growth rate (CAGR) of 2.5%between 1994 and 2002. Reduced net migrationwill result in a labor force that will increase by only1.4% in both 2003 and 2004.

For the first time since 1939, when the Bureau ofLabor Statistics first began tracking employmentdata, Colorado employment showed negative jobgrowth for two consecutive years, in 2002 and2003. This was only the second time that theUnited States has shown negative job growth inback-to-back years during this period.

During the 1990s, the Colorado economy relied ontelecommunications, manufacturing, construction,and tourism to drive growth. Increased employment

COMPONENTS OF COLORADO RESIDENT POPULATION1994-2004

(In Thousands)

ESTIMATED RESIDENT POPULATION, COLORADO AND UNITED STATES1994-2004

(Base Year: 1994=100)

continued on page 12

2004 Colorado Business Economic Outlook

11

COLORADO RESIDENT LABOR FORCE1994-2004

(In Thousands)

COLORADO NONAGRICULTURAL WAGE AND SALARY EMPLOYMENT1994-2004

(In Thousands)

2004 Colorado Business Economic Outlook

12

Population, Labor Force, and Personal Incomecontinued from page 10

in these areas fostered strong growth in retail sales,business services, and local government. In 2004 allsupersectors of the state economy are expected toshow improvement over 2003; however, not all sec-tors will add jobs. Strong growth will be seen inprofessional and business services, leisure and hos-pitality (tourism), health care, and retail trade. In2004 Colorado will return to positive job growth,showing an increase of 32,300 jobs, or a 1.5% gain.

In 2002 the state’s level of unemployment jumpedabove the natural rate of unemployment, 4.5 to5.0%, for the first time since 1993. The unemploy-ment rate increased to average 5.7%, where it isexpected to remain for 2003. Despite an increase inemployment of 32,300 jobs, Colorado unemploy-ment will not drop significantly as labor force par-ticipation rates are likely to increase. Unemploy-ment is expected to be 5.6% in 2004.

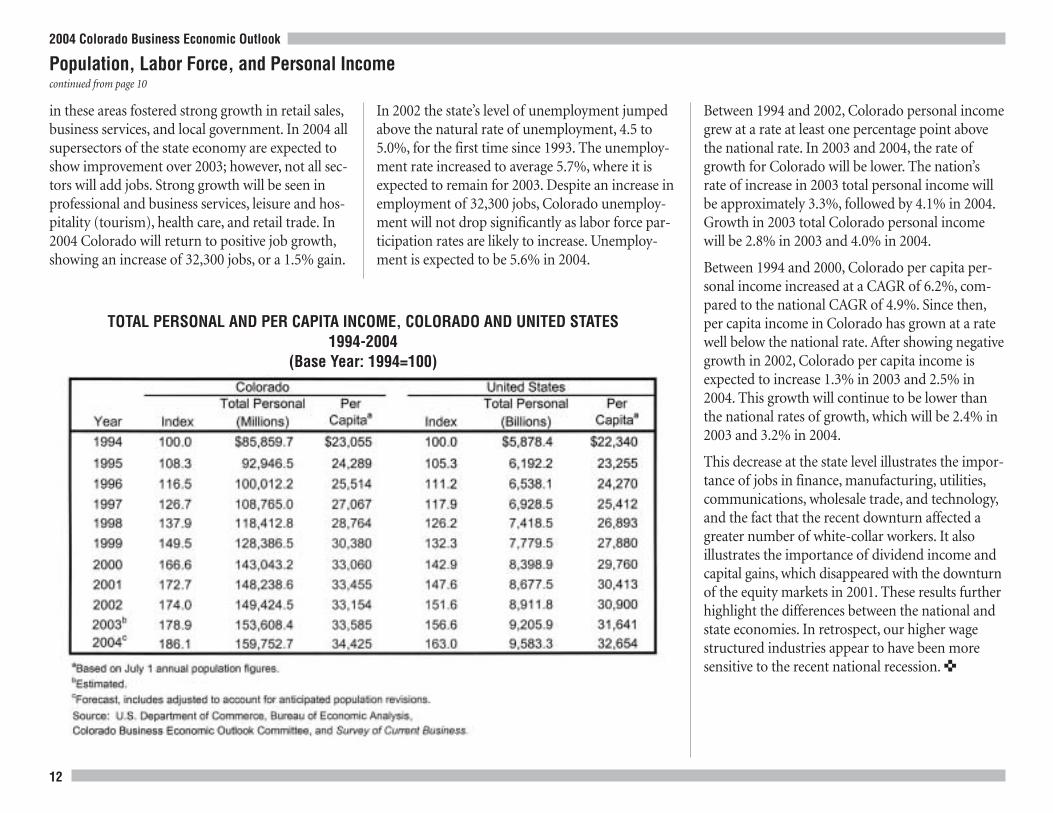

Between 1994 and 2002, Colorado personal incomegrew at a rate at least one percentage point abovethe national rate. In 2003 and 2004, the rate ofgrowth for Colorado will be lower. The nation’srate of increase in 2003 total personal income willbe approximately 3.3%, followed by 4.1% in 2004.Growth in 2003 total Colorado personal incomewill be 2.8% in 2003 and 4.0% in 2004.

Between 1994 and 2000, Colorado per capita per-sonal income increased at a CAGR of 6.2%, com-pared to the national CAGR of 4.9%. Since then,per capita income in Colorado has grown at a ratewell below the national rate. After showing negativegrowth in 2002, Colorado per capita income isexpected to increase 1.3% in 2003 and 2.5% in2004. This growth will continue to be lower thanthe national rates of growth, which will be 2.4% in2003 and 3.2% in 2004.

This decrease at the state level illustrates the impor-tance of jobs in finance, manufacturing, utilities,communications, wholesale trade, and technology,and the fact that the recent downturn affected agreater number of white-collar workers. It alsoillustrates the importance of dividend income andcapital gains, which disappeared with the downturnof the equity markets in 2001. These results furtherhighlight the differences between the national andstate economies. In retrospect, our higher wagestructured industries appear to have been moresensitive to the recent national recession. ✜

TOTAL PERSONAL AND PER CAPITA INCOME, COLORADO AND UNITED STATES1994-2004

(Base Year: 1994=100)

Agriculture2004 Colorado Business Economic Outlook

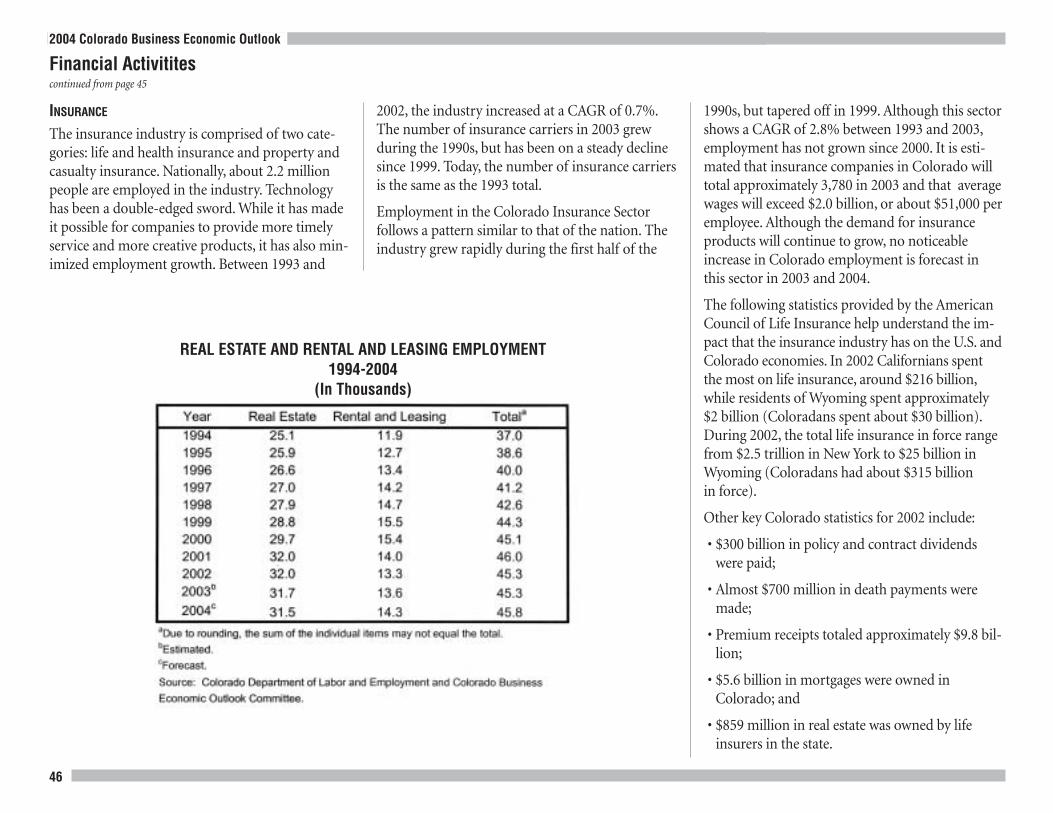

13

If 2002 will long be remembered as the year ofthe drought, 2003 will be remembered as the

year cattle prices rose to levels never before experi-enced. Although many of these same factors are inplace for 2004, it is unlikely that we can maintainthe record prices posted in late 2003. Still, 2004should be another good year for cattle prices.Crops in general will show a modest increase in2004, assuming that precipitation is normal andreservoirs are again filled to allow for irrigation.

In 2003, four important factors simultaneouslyimpacted the cattle industry. First, fewer cattle atlower weights (due to the cattle cycle) and thedrought significantly reduced the amount of beefgoing to market. Second, bovine spongiformencephalopathy, or mad cow disease, was discov-ered in Canada, stopping all beef and cattle ship-ments into the United States and further reducingdomestic supplies. The third factor is that Canadawas unable to export their beef to other countries,which opened up additional markets to U.S. sup-pliers. The final contributing factor is that con-sumer demand for beef, fueled by interest in lowcarbohydrate diets, continued the rebound thatbegan a few years ago.

As we look to 2004, many of these factors are stillin place. It is likely, however, that as protocols areestablished for Canadian cattle and beef to againenter the United States, the pressure on domesticsupplies will ease (i.e., Canada supplies about 9.0%of the beef and cattle in the United States). Canada’sreentry into other international markets will alsoaffect U.S. exports. It is expected that beef will faceincreased competition from poultry and other

protein sources, cutting into the demand for beef.The result of these changes will be that the averageprice for fed cattle will likely drop 5.0 to 6.0%, toaround $84 per hundredweight (cwt.). By historicalstandards this is still a very strong price and shouldkeep feeders profitable at least into early 2004.Feeder cattle prices are very high, however, andfeeding margins will be tight. The cattle cycle willcontinue to produce fewer cattle, so total Coloradofed cattle marketed in 2004 will be down to 2.2million, the lowest level in many years.

Because numbers of cattle remain low, most cow-calf operations should be profitable in 2004.Average calf prices are forecast to be about$1.05/lb., a record price. The one discouraging noteis that due to the drought a number of cattlemen

liquidated their herds and missed out on perhapsthe best cattle market of their lifetime. It will alsobe difficult for many of these producers to restocktheir herds at this time because the cost of breedingstock has increased significantly. Overall, due tofewer fed cattle and slightly lower fed cattle prices,total cash receipts from cattle will be down about10.0% in 2004, to $2.55 billion.

The dairy industry has experienced extremely poorprices this past year. Low milk prices have resultedin some dairies being forced out of business due tofinancial stress. Herd numbers in Colorado coulddrop as much as 10.0%. Moreover, average milkprices in 2004 should increase to the range of $13to $14/cwt., a gain of 20.0%. Total dairy products

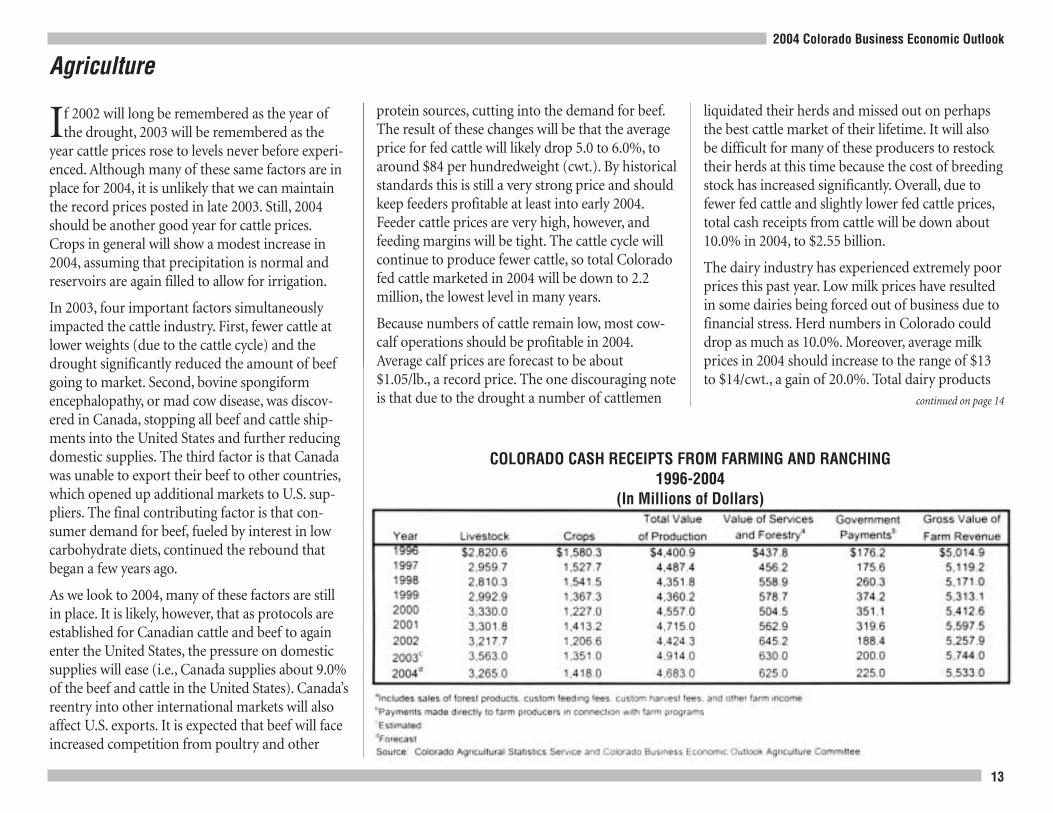

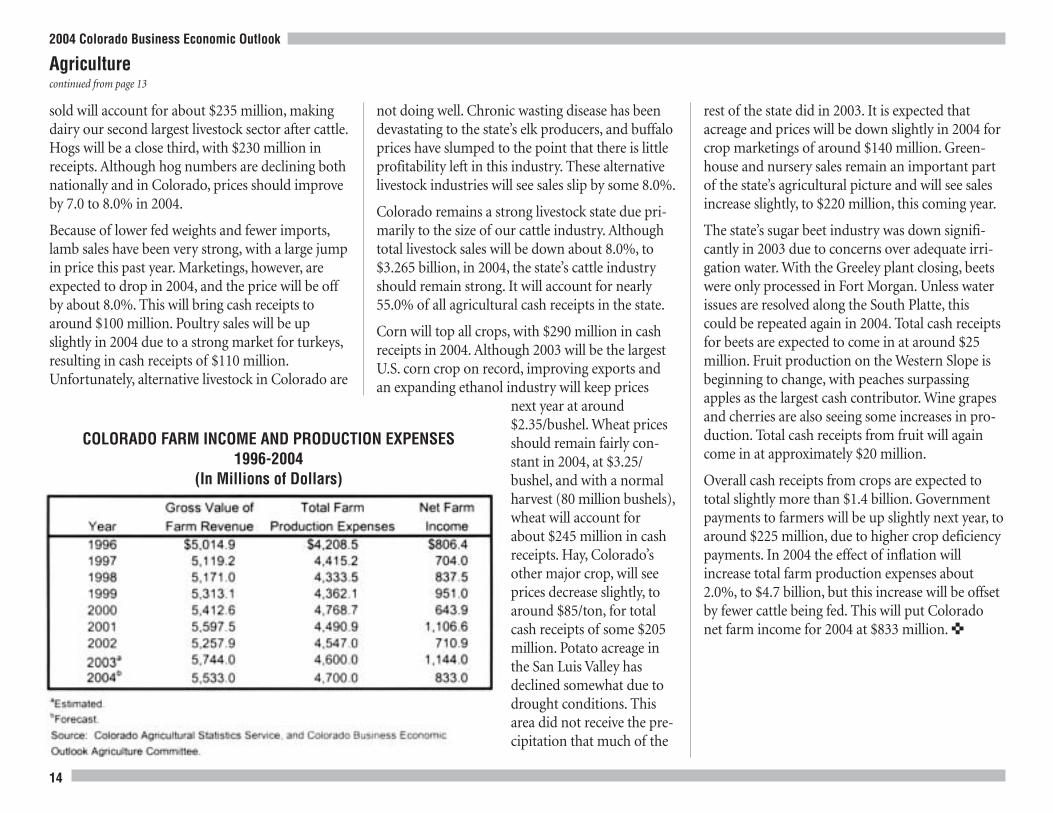

COLORADO CASH RECEIPTS FROM FARMING AND RANCHING1996-2004

(In Millions of Dollars)

continued on page 14

2004 Colorado Business Economic Outlook

14

rest of the state did in 2003. It is expected thatacreage and prices will be down slightly in 2004 forcrop marketings of around $140 million. Green-house and nursery sales remain an important partof the state’s agricultural picture and will see salesincrease slightly, to $220 million, this coming year.

The state’s sugar beet industry was down signifi-cantly in 2003 due to concerns over adequate irri-gation water. With the Greeley plant closing, beetswere only processed in Fort Morgan. Unless waterissues are resolved along the South Platte, thiscould be repeated again in 2004. Total cash receiptsfor beets are expected to come in at around $25million. Fruit production on the Western Slope isbeginning to change, with peaches surpassingapples as the largest cash contributor. Wine grapesand cherries are also seeing some increases in pro-duction. Total cash receipts from fruit will againcome in at approximately $20 million.

Overall cash receipts from crops are expected tototal slightly more than $1.4 billion. Governmentpayments to farmers will be up slightly next year, toaround $225 million, due to higher crop deficiencypayments. In 2004 the effect of inflation willincrease total farm production expenses about2.0%, to $4.7 billion, but this increase will be offsetby fewer cattle being fed. This will put Coloradonet farm income for 2004 at $833 million. ✜

sold will account for about $235 million, makingdairy our second largest livestock sector after cattle.Hogs will be a close third, with $230 million inreceipts. Although hog numbers are declining bothnationally and in Colorado, prices should improveby 7.0 to 8.0% in 2004.

Because of lower fed weights and fewer imports,lamb sales have been very strong, with a large jumpin price this past year. Marketings, however, areexpected to drop in 2004, and the price will be offby about 8.0%. This will bring cash receipts toaround $100 million. Poultry sales will be upslightly in 2004 due to a strong market for turkeys,resulting in cash receipts of $110 million.Unfortunately, alternative livestock in Colorado are

not doing well. Chronic wasting disease has beendevastating to the state’s elk producers, and buffaloprices have slumped to the point that there is littleprofitability left in this industry. These alternativelivestock industries will see sales slip by some 8.0%.

Colorado remains a strong livestock state due pri-marily to the size of our cattle industry. Althoughtotal livestock sales will be down about 8.0%, to$3.265 billion, in 2004, the state’s cattle industryshould remain strong. It will account for nearly55.0% of all agricultural cash receipts in the state.

Corn will top all crops, with $290 million in cashreceipts in 2004. Although 2003 will be the largestU.S. corn crop on record, improving exports andan expanding ethanol industry will keep prices

next year at around$2.35/bushel. Wheat pricesshould remain fairly con-stant in 2004, at $3.25/bushel, and with a normalharvest (80 million bushels),wheat will account forabout $245 million in cashreceipts. Hay, Colorado’sother major crop, will seeprices decrease slightly, toaround $85/ton, for totalcash receipts of some $205million. Potato acreage inthe San Luis Valley hasdeclined somewhat due todrought conditions. Thisarea did not receive the pre-cipitation that much of the

Agriculturecontinued from page 13

COLORADO FARM INCOME AND PRODUCTION EXPENSES1996-2004

(In Millions of Dollars)

2004 Colorado Business Economic Outlook

15

Natural Resources and Mining

This NAICS sector includes: Forestry and logging; oiland gas extraction, mining; and support activities formining.

LoggingThe logging industry has historically been anextremely small part of the Colorado economy,employing between 100 and 200 people. The recentwildfires have raised a number of issues relating tothe management of our forests; however, this is notexpected to impact employment in this sector in2003 and 2004.

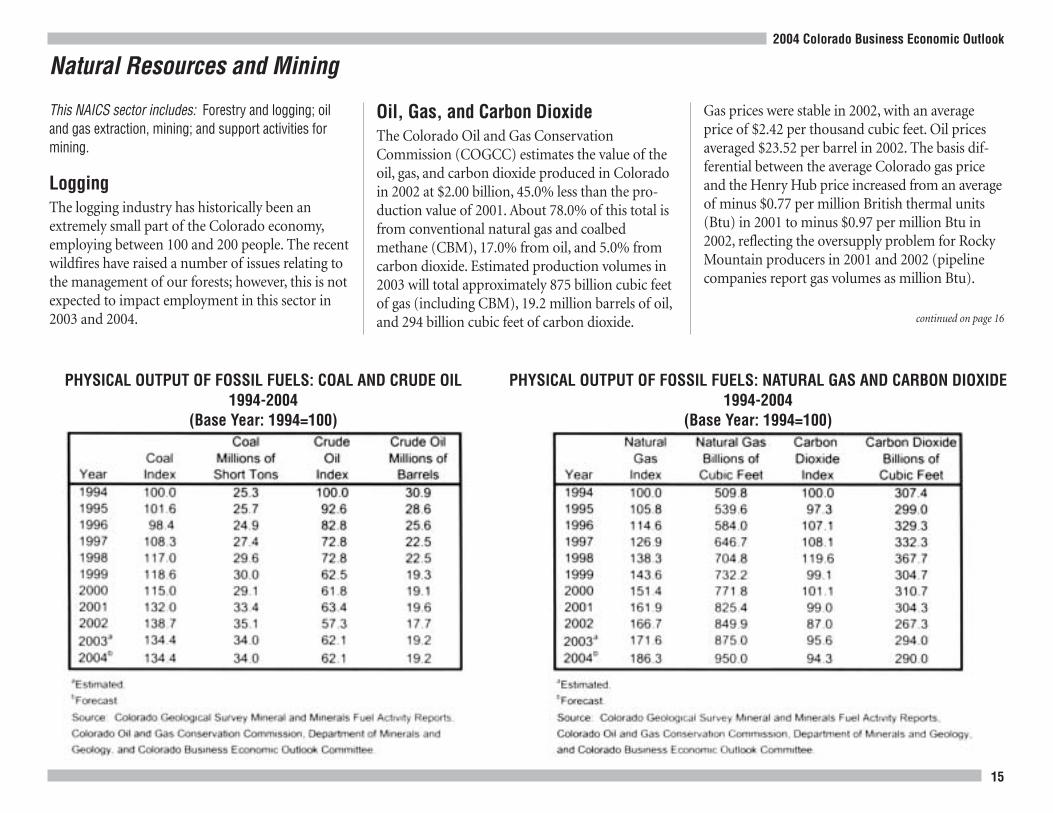

Oil, Gas, and Carbon DioxideThe Colorado Oil and Gas ConservationCommission (COGCC) estimates the value of theoil, gas, and carbon dioxide produced in Coloradoin 2002 at $2.00 billion, 45.0% less than the pro-duction value of 2001. About 78.0% of this total isfrom conventional natural gas and coalbedmethane (CBM), 17.0% from oil, and 5.0% fromcarbon dioxide. Estimated production volumes in2003 will total approximately 875 billion cubic feetof gas (including CBM), 19.2 million barrels of oil,and 294 billion cubic feet of carbon dioxide.

Gas prices were stable in 2002, with an averageprice of $2.42 per thousand cubic feet. Oil pricesaveraged $23.52 per barrel in 2002. The basis dif-ferential between the average Colorado gas priceand the Henry Hub price increased from an averageof minus $0.77 per million British thermal units(Btu) in 2001 to minus $0.97 per million Btu in2002, reflecting the oversupply problem for RockyMountain producers in 2001 and 2002 (pipelinecompanies report gas volumes as million Btu).

PHYSICAL OUTPUT OF FOSSIL FUELS: COAL AND CRUDE OIL1994-2004

(Base Year: 1994=100)

continued on page 16

PHYSICAL OUTPUT OF FOSSIL FUELS: NATURAL GAS AND CARBON DIOXIDE1994-2004

(Base Year: 1994=100)

2004 Colorado Business Economic Outlook

16

Natural Resources and Miningcontinued from page 15

COGCC estimates that the production value of oil,gas, and carbon dioxide will surpass $3 billion in2003—a 50.0% increase from 2002. Natural gasshould account for about 83.0% of this value.Average natural gas prices are forecasted to be$4.33 per million Btu in 2003—an 89.0% increaseover the 2002 average of $2.29 per million Btu—with the basis differential increasing to $1.27 permillion Btu. Daily average oil production is pre-dicted to remain flat, at 19.2 million barrels, butthe average oil price will rise to $28.80 per barrel in2003—an increase of 22.0% from the average 2002price of $23.52.

The Energy Information Administration (EIA)predicts an increase in oil and natural gas demand(and prices) in the United States for 2003 and 2004as the economy begins to recover, with a projected2.9% growth rate. This expansion is expected toresult in a 3.7% increase in natural gas demand in2003 and a continued rise in 2004. Natural gas pro-duction is expected to increase by only 1.2% in2003. The Rocky Mountain region is expected torespond to this supply deficit by increasing naturalgas production from existing fields and expandinginto new areas. The expansion of the Kern Riverpipeline, which will take an additional 900 millioncubic feet per day out of the Rocky Mountain mar-ket, has dramatically reduced the basis differentialfor gas. As a result, COGCC forecasts an averagenatural gas price in Colorado of $4.61 per thou-sand cubic feet for 2003-2004, the highest averagesince 2000-2001.

EIA reports that crude oil prices have been risingbecause of instability in the Middle East, lowinventories, continued cold weather, and a slowrecovery in Venezuelan exports. World oil pricesare expected to remain near $30 per barrel throughthe winter of 2003-2004, declining to about $27 perbarrel by late 2004.

The petroleum industry in Colorado, particularlythe natural gas segment, may be poised for anotherboom. High natural gas prices and soaring oil andgas revenues are expected to drive a resurgence innatural gas-directed activity in 2003-2004 follow-ing the downturn in 2002. Employment shouldincrease in response to higher prices and the addedpipeline capacity for delivery of natural gas tomore markets. Natural gas production is forecastedto total 875 billion cubic feet in 2003 and 950 bil-lion cubic feet in 2004. This is expected to result inan employment level for the oil and gas subsectorof 8,000 in 2003 and 8,800 in 2004. Generally,employment in this subsector is directly correlatedto energy prices. The implication for the consumeris that all energy prices will be relatively high.Gasoline is likely to be in the range of $1.50 to$2.00 per gallon in 2004. This level of gasolineprice may have a negative impact on tourism andagriculture in Colorado.

The Independent Petroleum Association ofMountain States has identified four interrelatedissues that are now challenging competitiveness inColorado and the Rocky Mountain region:

1) Financial Constraints—Drilling wells and build-ing new pipelines requires capital (cash flow andcredit).

2) Price Volatility—Uncertainty over future pricesresults in cautious investing. The cyclical natureof gas prices makes timing critical.

3) Infrastructure Deficiencies—To compete withother regions, new pipelines must be built in theRockies.

4) Regulatory Uncertainty—Delays limit a com-pany’s ability to respond to supply and demandimbalances.

CoalColorado’s coal industry set new records for pro-duction and efficiency in 2002. In that year, thestate’s 12 coal mines produced a record 35.2 mil-lion short tons of coal. This is the first time that the35-million-tons mark was surpassed, and is morethan double the coal produced in 1989. Most of theproduced coal (97.0%) is sold as steam coal forelectrical generating plants. More than half of thecoal is exported to markets in Kentucky, Indiana,Tennessee, and Mississippi. Coal sales set a recordhigh in 2002, and are only 4.0% lower throughOctober 2003. The Colorado Geological Surveyestimates that coal production for 2003 will beabout 34 million short tons.

The petroleum industry in Colorado,particularly the natural gas segment, may be poised for another boom.

Coal industry employment has also increased inrecent years. According to the Colorado Depart-ment of Labor, 1,853 coal miners were employed asof December 2002, a 3.0% increase over the previ-ous year. These miners work and live primarily inrural parts of northwest Colorado. The coal minesprovide good, stable employment to areas that mayotherwise have low employment opportunities.More than 2,400 people are currently employed inthe industry. According to a 2002 survey of coalproducers by the Colorado Mining Association, theaverage miner earns more than $80,000 annually inpay and benefits. Coal miners are the highest paidindustrial workers in Colorado and have the fourthhighest average salary for mining states.

Twelve mines currently operate in nine WesternSlope counties. The three highest coal producingcounties last year were Gunnison, Routt, andMoffat. Seven underground and five surface minessupply coal via truck and rail to power plants inColorado, Utah, and the Midwest. Oxbow Miningclosed its Sanborn Creek Mine in February 2003after opening the new adjacent Elk Creek Mine. ElkCreek will provide safer mining conditions as thecoal is only 750 feet deep, much shallower than the2,400-foot depth reached in the Sanborn CreekMine. This mine had substantial methane gas androck burst conditions.

Colorado ranks eighth in coal production nation-ally. Of the top 10 coal producing states, onlyColorado and Wyoming had increases in coal pro-duction over the previous year. This remarkableoutput in regional coal production reflects thedemand for clean western coal. Power plants in theMidwest use low-sulfur and low-mercury westernU.S. coal to blend with their higher sulfur coal in

2004 Colorado Business Economic Outlook

17

order to comply with air quality requirements.Approximately 82.0% of the electric generationoutput in Colorado is supplied by coal, giving thecitizens of Colorado the third lowest electricityrates in the nation.

According to EIA data, the average mine price forColorado coal dropped from $24.65/ton in 1985 to$17.72/ton in 2002. Prices fell during the first quar-ter of 2002 and are in the $16 to $18/ton range asof October 2003. The estimated value of Coloradocoal produced in 2002 was more than $600 million.

In the future, Colorado coal production willdepend highly on environmental regulations. Coalproduction could be constrained by national regu-latory and legislative action, including mandatorygreenhouse gas emission standards for coal-firedpower plants and regional haze regulations. Thedemand for Colorado coal is projected to fluctuatebetween 29 and 40 million short tons annuallythrough 2014. Hill & Associates, a managementconsulting firm, forecasts the demand for Coloradocoal could drop as low as 25 million tons by 2014under current air quality regulations if all powerplants attain compliance. The demand forColorado coal could fall to as low as 11 milliontons annually if stringent carbon dioxide emissionsare adopted. Under current regulations, prices areexpected to decline to the $12/ton range (2002constant dollars) by 2014 as more power plantsdevelop air pollution controls.

Nonfuel MineralsNonfuel mineral production includes metals,industrial minerals, and construction aggregates.Nonfuel mineral production and employment isforecast to remain stable in Colorado in 2004.Colorado will continue to be an important U.S.producer of molybdenum, gold, soda ash, sodiumbicarbonate, construction aggregate, gypsum, andcement. In 2002 (the most recent annual data avail-able), the U.S. Geological Survey estimated a totalvalue of nonfuel mineral production in Coloradoof $614 million. This was a gain of 6.4% over the2001 production value. The production value ofnonfuel minerals is expected to be substantiallyhigher in 2003 and 2004, due principally toincreases in the prices of gold and molybdenum.

According to U.S. Department of Labor’s Bureau of Labor Statistics, annual employment in themetal mining industry in 2002 was 1,141 workers.Nonmetallic, nonfuel mineral mining employed2,101 people in 2002. The Colorado GeologicalSurvey estimates 3,500 employees in the nonfuelmining subsector for 2003 and 2004.

Gold prices increased significantly in 2003 com-pared to the depressed prices during the previousfour years. As of early October 2003, the spot goldprice was around $380 per ounce, while the averagegold price in 2002 was $310 per ounce. This is goodnews for Colorado’s only operating gold mine, theCripple Creek & Victor Mine (CC&V) in TellerCounty. This world-class mine employs about 300people and produced 224,000 ounces of gold in2002. In late 2002, CC&V completed its two-year,$168.5 million expansion and capital improvementprogram. With the expanded production capacity,

According to EIA data, the average mineprice for Colorado coal dropped from$24.65/ton in 1985 to $17.72/ton in 2002.

continued on page 18

2004 Colorado Business Economic Outlook

18

the mine is expected to produce 300,000 to 400,000ounces of gold per year in 2003 and beyond. Thecurrent reserve base is sufficient to support goldproduction until 2012 at the expanded produc-tion rate.

Denver-based Newmont is the world’s largest goldmining company. Although it does not have anyactive mining operations in Colorado, the companyemploys several hundred people. Several smallermining and mineral exploration companies alsoare headquartered in the Denver area and provideemployment for geologists, mining and metallurgi-cal engineers, and financial specialists.

The Henderson Mine in Clear Creek County con-tinues to be North America’s largest primary pro-ducer of molybdenum. The underground mine isowned by Climax Molybdenum Company, a sub-sidiary of Phelps Dodge Corp., and employsapproximately 300 people. In 2002, the mine pro-duced 20.5 million pounds of molybdenum metal,an increase of 9.0% over the 18.8 million poundsproduced in 2001. Molybdenum prices have risensignificantly in the past two years. As of October2003, the price for molybdic oxide was more than$6.00 per pound compared to an average price of$3.75 per pound in 2002 and $2.36 per pound in2001. The Henderson Mine hopes to increase pro-duction by 5.0% over the next year and an addi-tional 5.0% the following year, according to a Julyarticle in the Clear Creek Courant.

The continued sluggish economy has resulted in aslower pace of residential and commercial con-struction in 2003, which, in turn, has led to a

decline in demand for and production of construc-tion aggregates (sand, gravel, and crushed stone).This trend is expected to stabilize or reverse in 2004as the overall economy improves. In 2002 (themost recent year for production statistics), aggre-gate mines in Colorado produced approximately62.5 million tons of construction material, for atotal estimated value of $319 million.

Several other important nonfuel mineral com-modities are produced in Colorado. Soda ash andsodium bicarbonate continue to be produced bysolution mining techniques in Rio Blanco County,

northwest of Parachute. Solvay America, Inc. pur-chased American Soda LLP from Williams inSeptember 2003 for an undisclosed price. CentexConstruction Product’s American Gypsum opera-tion produces gypsum from its mine in EagleCounty. The gypsum is manufactured into wall-board and other products at the plant in EagleCounty. Holcim (US), Inc. operates a large port-land cement manufacturing plant near Florence,Colorado. It recently upgraded the plant to a pro-duction capacity of 1.9 million tons per year. GCCRio Grande, Inc. has been planning and permittinga major new cement plant near Pueblo during thepast several years. The $200 million plant isprojected to produce 1 million tons of cement per year. When operational, the plant and mine is expected to directly employ approximately 100 people.

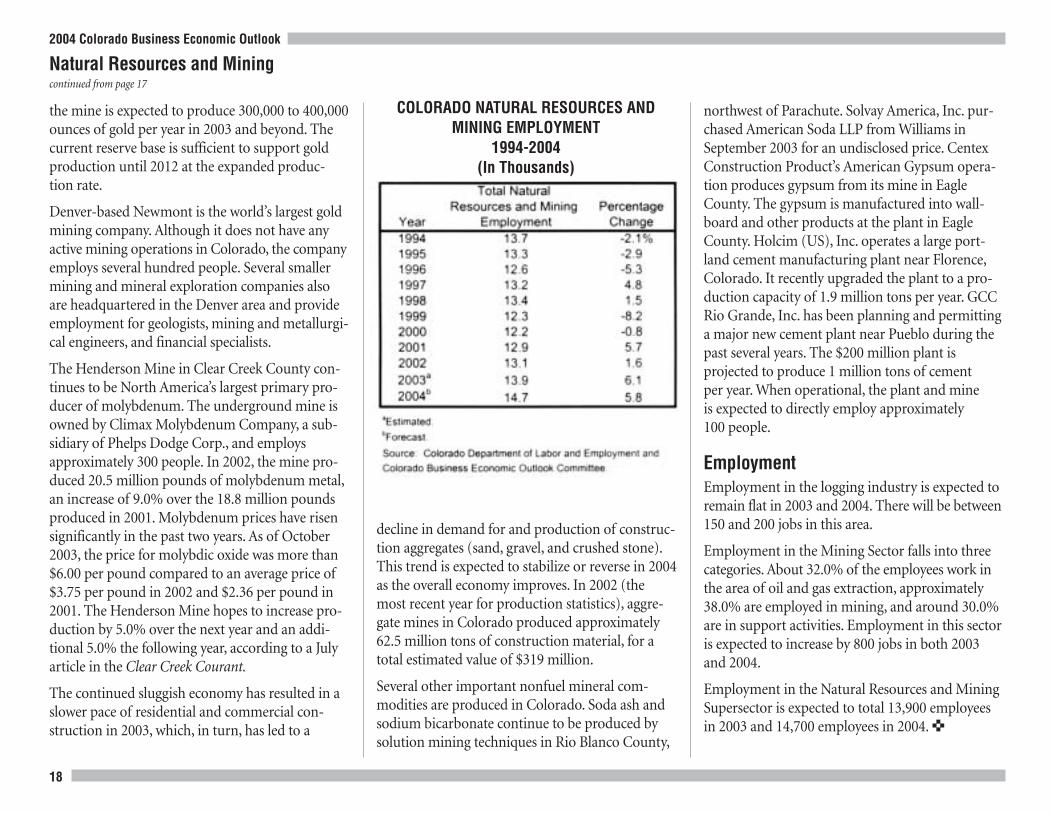

EmploymentEmployment in the logging industry is expected toremain flat in 2003 and 2004. There will be between150 and 200 jobs in this area.

Employment in the Mining Sector falls into threecategories. About 32.0% of the employees work inthe area of oil and gas extraction, approximately38.0% are employed in mining, and around 30.0%are in support activities. Employment in this sectoris expected to increase by 800 jobs in both 2003 and 2004.

Employment in the Natural Resources and MiningSupersector is expected to total 13,900 employeesin 2003 and 14,700 employees in 2004. ✜

COLORADO NATURAL RESOURCES AND MINING EMPLOYMENT

1994-2004(In Thousands)

Natural Resources and Miningcontinued from page 17

2004 Colorado Business Economic Outlook

19

This NAICS sector includes: Construction of build-ings, heavy and civil engineering construction, andspecialty trade contractors.

The effects of the slowing Colorado economycaught up with the Construction Supersector

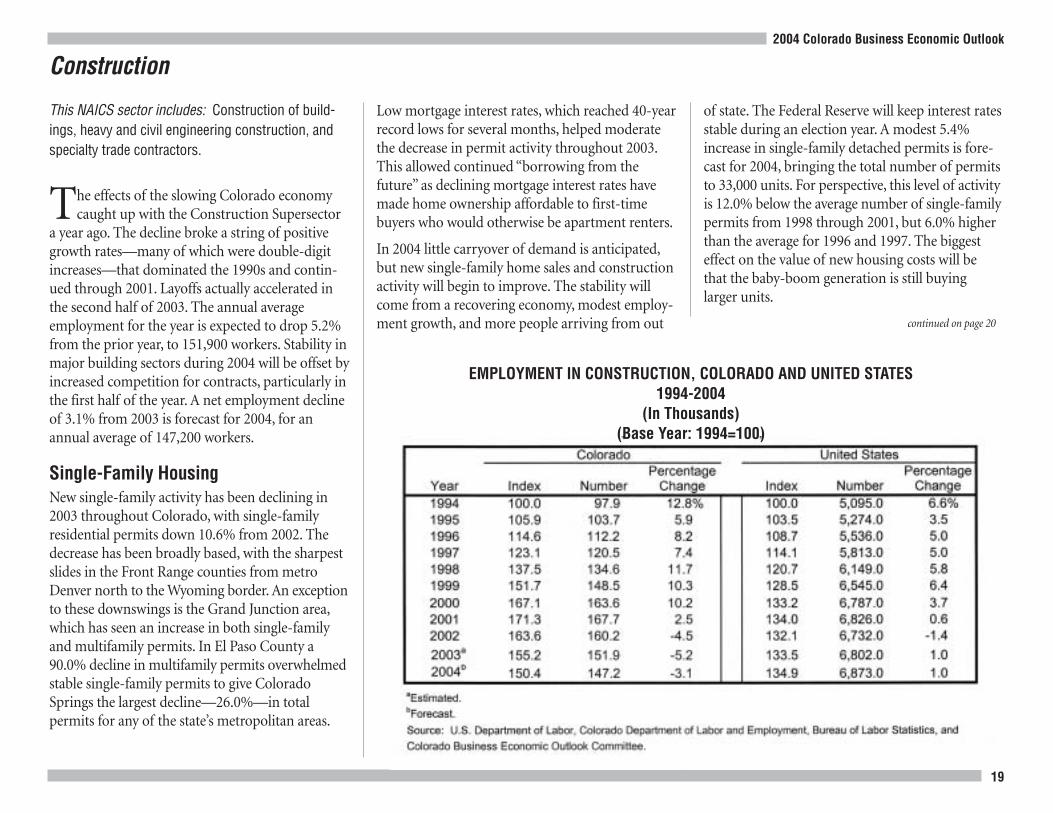

a year ago. The decline broke a string of positivegrowth rates—many of which were double-digitincreases—that dominated the 1990s and contin-ued through 2001. Layoffs actually accelerated inthe second half of 2003. The annual averageemployment for the year is expected to drop 5.2%from the prior year, to 151,900 workers. Stability inmajor building sectors during 2004 will be offset byincreased competition for contracts, particularly inthe first half of the year. A net employment declineof 3.1% from 2003 is forecast for 2004, for anannual average of 147,200 workers.

Single-Family HousingNew single-family activity has been declining in2003 throughout Colorado, with single-familyresidential permits down 10.6% from 2002. Thedecrease has been broadly based, with the sharpestslides in the Front Range counties from metroDenver north to the Wyoming border. An exceptionto these downswings is the Grand Junction area,which has seen an increase in both single-familyand multifamily permits. In El Paso County a90.0% decline in multifamily permits overwhelmedstable single-family permits to give ColoradoSprings the largest decline—26.0%—in totalpermits for any of the state’s metropolitan areas.

Construction

Low mortgage interest rates, which reached 40-yearrecord lows for several months, helped moderatethe decrease in permit activity throughout 2003.This allowed continued “borrowing from thefuture” as declining mortgage interest rates havemade home ownership affordable to first-timebuyers who would otherwise be apartment renters.

In 2004 little carryover of demand is anticipated,but new single-family home sales and constructionactivity will begin to improve. The stability willcome from a recovering economy, modest employ-ment growth, and more people arriving from out

of state. The Federal Reserve will keep interest ratesstable during an election year. A modest 5.4%increase in single-family detached permits is fore-cast for 2004, bringing the total number of permitsto 33,000 units. For perspective, this level of activityis 12.0% below the average number of single-familypermits from 1998 through 2001, but 6.0% higherthan the average for 1996 and 1997. The biggesteffect on the value of new housing costs will be that the baby-boom generation is still buying larger units.

EMPLOYMENT IN CONSTRUCTION, COLORADO AND UNITED STATES1994-2004

(In Thousands)(Base Year: 1994=100)

continued on page 20

2004 Colorado Business Economic Outlook

20

Constructioncontinued from page 19

Vacancies in office building throughout the FrontRange have stabilized in 2003. Construction ofnew space totaled only 185,000 square feet. Thecorporate and speculative market will likely haveexcess capacity until approximately 2008. The paceof construction in the industrial and retail sectorswill remain slow in 2004. Even a rapid recovery inthe high-tech and telecommunications industrieswould not absorb unused offices quickly, especiallyin northwest metropolitan Denver where vacancyrates declined further in 2003, to 29.5%.

Voters considered requests by school boards for$900 million in new K-12 bond issues; historically,we have seen about two-thirds of these requestspass. These moneys are not likely to be expendeduntil 2005, but a large percentage of bond issuesapproved in 2002 will continue to make this sub-sector one of the robust spots in 2004. The remain-der of government construction is mixed. The newDenver convention center hotel is on a fast scheduleand will contribute to next year’s volume, but stategovernment will be forced to restrain spending. Nosignificant capital development is expected duringthis forecast horizon.

Nonbuilding ConstructionThis segment of the construction market is drivenby large projects, such as those sponsored by theColorado Department of Transportation (CDOT),the T-REX project, water and pipeline projects, andmunicipal public works.

In 2003 the sector experienced a small decline asgovernmental budgets have remained weak andmargins on jobs bid in the public arena have

Multifamily HousingThere was a surge in production of multifamilyunits until 2003, when the economy weakened andlow interest rates made home ownership affordableto many renters. These factors combined to batterapartment and rental markets. Vacancy rates are up,rent concessions are widespread, average rents aredropping in some areas, and new product is beingabsorbed at the expense of old. The softest marketsare along the Front Range, but even the historicallytight mountain areas have not been immune.

The proportion of attached, for-sale units in totalmultifamily production continues to increase.Although this sector has benefited from low mort-gage interest rates, the low rates have been a two-edged sword. Many first-time home buyers, whotypically would be looking for an affordableattached home, have been able to qualify for ahigher priced, single-family home, pulling someattached home sellers’ best clients out of this mar-ket. As of fall 2003, the number of condominiumslisted for sale in the Denver area totaled 7,000units, a number that may dampen builders’ enthu-siasm in the short run.

After a recent construction peak of more than18,500 new units in 2001, multifamily productionwas scaled back to fewer than 13,000 units in 2002.This cutback accelerated in 2003, and we expect thetotal for this year to fall to 6,700 units. Although theDenver metro area experienced a major correctionin 2003, it still accounts for the lion’s share of multi-family construction in the state. Much of the re-mainder of Colorado has seen multifamily

production come to a virtual halt. Multifamilystarts in the nonmetropolitan areas of the state(including resort counties) will not likely exceed500 units for the year.

Another decline in multifamily starts in 2004seems unavoidable. A recovery in the apartmentmarket appears to be three to four years away inmajor Front Range markets, leaving the attachedhome sales market shouldering the burden for themultifamily sector in the next few years. Look for adrop to 5,000 multifamily permits in 2004, withmost of these intended for sale.

Nonresidential BuildingThe value of construction during 2003 in the com-mercial, retail, and institutional building subsectorswill drop 3.0% from its 2002 total. The weakness inthis sector will continue into 2004, with only asmall 4.0% gain. A larger increase from 2003 mightbe realized if nonresidential construction continuesto follow new housing starts and if the fourplanned +$100 million prisons are started in 2004in southern Colorado.

Medical buildings will again be the major exceptionto the downturn in nonresidential building. Thissector has historically accounted for less than 10.0%of nonresidential building, but it has grown to agreater proportion of that total. A surge of this typeof work will start in 2004 as the new Children’sHospital and the next phase of higher educationdevelopment at Fitzsimons begin construction.Medical office buildings, senior living, ambulatorysurgery centers, and imaging centers are expectedto remain strong into the first half of 2004.

2004 Colorado Business Economic Outlook

21

Nonbuilding work will experience an overalldecrease of about 15.0% in 2004. The highway por-tion of T-REX will decline in 2004, to $114 million,but southeast corridor contractors will continue tobuild the light-rail segment at a pace of about $150million. The 2004 CDOT highways budget (notincluding T-REX) will be down modestly, to $460million, excluding design and right of way.

A sharp decline in airport work is forecast for 2004.Denver International Airport’s sixth runway, whichis the longest at the facility, has been completed.More airport work will focus on security measures,

and spending will shift to the machinery andbuildings to support new those new facilities.

Like 2003, strength will continue in utility work forpipelines, water treatment plants, and dams andother water-related projects. Contractors report20.0 to 25.0% increases on minireservoir storage,pipelines, dam repairs, and water treatment plants.The Denver Water Board plans to accelerate theMoffat Collection System and expand the recycledwater distribution system. Utility work for develop-ers will see a similar increase in 2004 as the single-family market recovers to a small degree. ✜

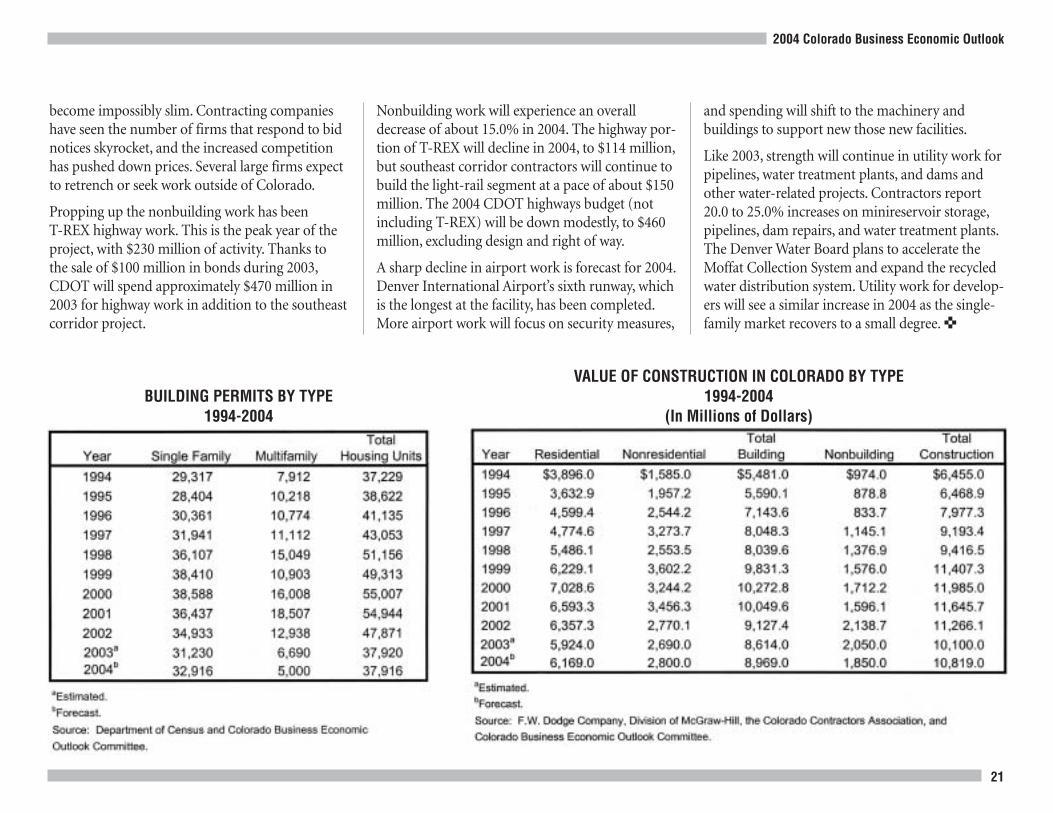

VALUE OF CONSTRUCTION IN COLORADO BY TYPE1994-2004

(In Millions of Dollars)BUILDING PERMITS BY TYPE

1994-2004

become impossibly slim. Contracting companieshave seen the number of firms that respond to bidnotices skyrocket, and the increased competitionhas pushed down prices. Several large firms expectto retrench or seek work outside of Colorado.

Propping up the nonbuilding work has been T-REX highway work. This is the peak year of theproject, with $230 million of activity. Thanks to the sale of $100 million in bonds during 2003,CDOT will spend approximately $470 million in2003 for highway work in addition to the southeastcorridor project.

2004 Colorado Business Economic Outlook

22

Manufacturing

This NAICS sector includes: Food manufacturing; bever-age and tobacco product manufacturing; textile mills;textile product mills; apparel manufacturing; leather andallied product manufacturing; wood product manufactur-ing; paper manufacturing; printing and related supportactivities; petroleum and coal products manufacturing;chemical manufacturing; plastics and rubber productsmanufacturing; nonmetallic mineral product manufactur-ing; primary metal manufacturing; fabricated metal prod-uct manufacturing; machinery manufacturing; computerand electronic product manufacturing; electrical equip-ment, appliance, and component manufacturing; trans-portation equipment manufacturing; furniture andrelated product manufacturing; and miscellaneousmanufacturing.

The state and national economic downturncontinues to be especially brutal to the manu-

facturing industry, with continual job losses postedsince 1998. While economic performance in themanufacturing industry did improve in 2003, theindustry still sustained heavy job losses. Based onthe new North American Industry ClassificationSystem (NAICS) industry definition, the manufac-turing industry lost a record 15,600 jobs in 2002.Job losses in 2003 are not expected to be quite assevere, but a further contraction of the industry, by11,000 positions, is forecasted. While the picturebrightens in 2004, it is expected that the industrywill lose another 1,100 jobs. Indeed, manufacturingjobs now account for only about 7.0% of the state’stotal employment base, down from 9.5% in 1998.

Two main themes emerged in the examination ofthe manufacturing industry this year. First, thenumber of off-shore manufacturing operations has

increased, with most industry experts expectingthat these jobs are lost to the U.S. economy forever.Second, enhanced production processes and tech-nological changes have advanced global productiv-ity at an astonishing rate. Between 1995 and 2002,global industrial production was up 30.0% even asmanufacturing employment fell 11.0%. Thismeans that manufacturers all over the world areable to do more with fewer employees due to theseproductivity increases. While there are advantagesto both off-shore operations and productivitygains, they each have their downside, namely thatdespite improving economic conditions, manufac-turing employment in the United States andColorado is still expected to decline in 2004.

Survey ResultsFor the 13th year in a row, the manufacturing com-mittee conducted a survey of Colorado manufac-turing businesses to determine their outlook on theindustry and discover their needs and concerns.Companies responding to the survey representedabout 3,700 employees or approximately 2.5% of themanufacturing employment base. Although this isa small sample size, it does give some perspectiveon the manufacturing outlook for Colorado.

Company representatives were asked whether theircompany’s performance over the past year was bet-ter than expected, worse than expected, or asexpected. Companies had expected a more positiveyear in 2003, but that did not happen. About 38.0%of the firms surveyed stated that their performancewas worse than expected, similar to last year’sresults of 37.0%. On the positive side, 33.0% noted

that their company performed better than expectedthis year compared to 30.0% last year. Twenty-ninepercent of the company representatives said per-formance was on target this year.

Companies remain cautious as we enter 2004 asevidenced by facility expansion plans for the nextthree years. More than 56.0% of the respondentssaid they have no facility expansion plans com-pared to last year when 60.0% had no such plans.On the positive side, 32.0% expect to expand theirfacilities in Colorado; this percentage was 28.0%last year. Furthermore, only 5.0% expect to down-size, the same as last year.

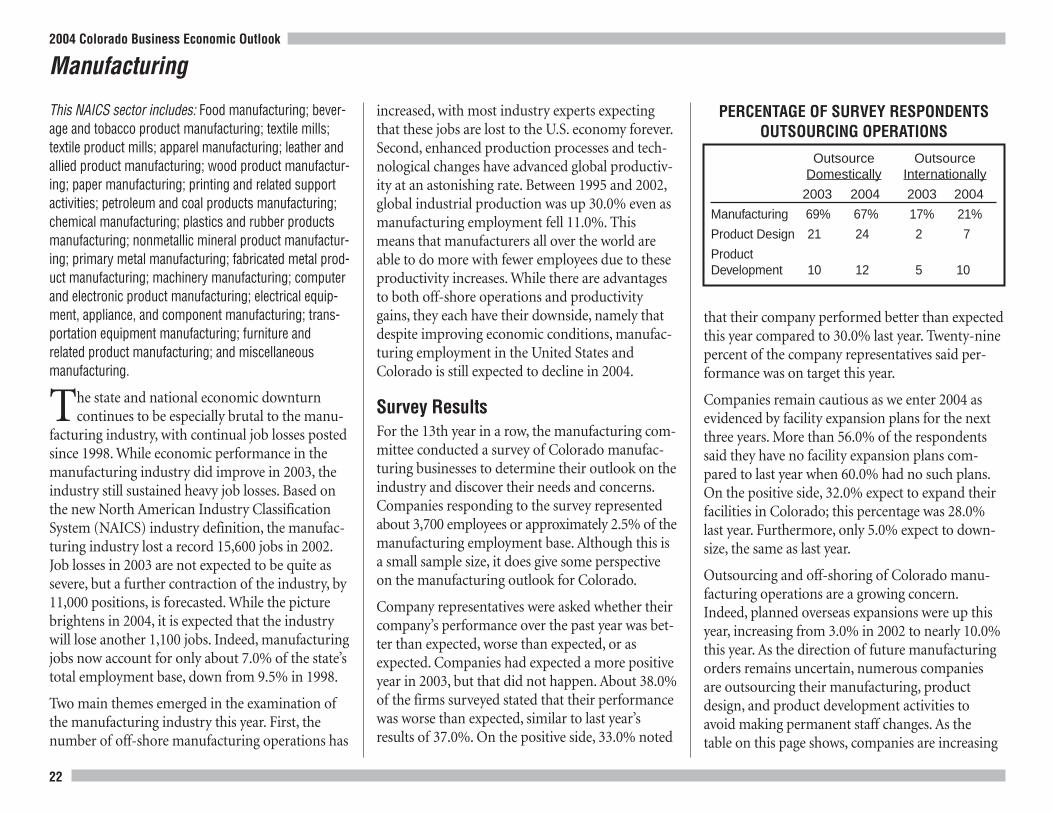

Outsourcing and off-shoring of Colorado manu-facturing operations are a growing concern.Indeed, planned overseas expansions were up thisyear, increasing from 3.0% in 2002 to nearly 10.0%this year. As the direction of future manufacturingorders remains uncertain, numerous companiesare outsourcing their manufacturing, productdesign, and product development activities toavoid making permanent staff changes. As the table on this page shows, companies are increasing

PERCENTAGE OF SURVEY RESPONDENTSOUTSOURCING OPERATIONS

Outsource OutsourceDomestically Internationally

2003 2004 2003 2004

Manufacturing 69% 67% 17% 21%

Product Design 21 24 2 7

Product Development 10 12 5 10

2004 Colorado Business Economic Outlook

23

continued on page 24

their outsourcing operations, both domesticallyand overseas.

Some level of outsourcing of manufacturing, prod-uct design, and product development is necessaryto remain cost competitive, provide productionflexibility, tap new sources of innovation, and cre-ate a presence in emerging markets. However, ifcompanies outsource excessively, they begin to losetheir sources of tacit knowledge generation andintellectual property. Without continuous productinnovation, companies can quickly lose their newproduct development capabilities. Within one ortwo product lifecycles these companies can relin-quish control of their processes, technologies, andproducts and end up as marketing shells. Manufac-turing firms should use caution in their outsourc-ing operations, making sure that they are notsubstituting short-term financial results for long-term strategic competitive advantage.

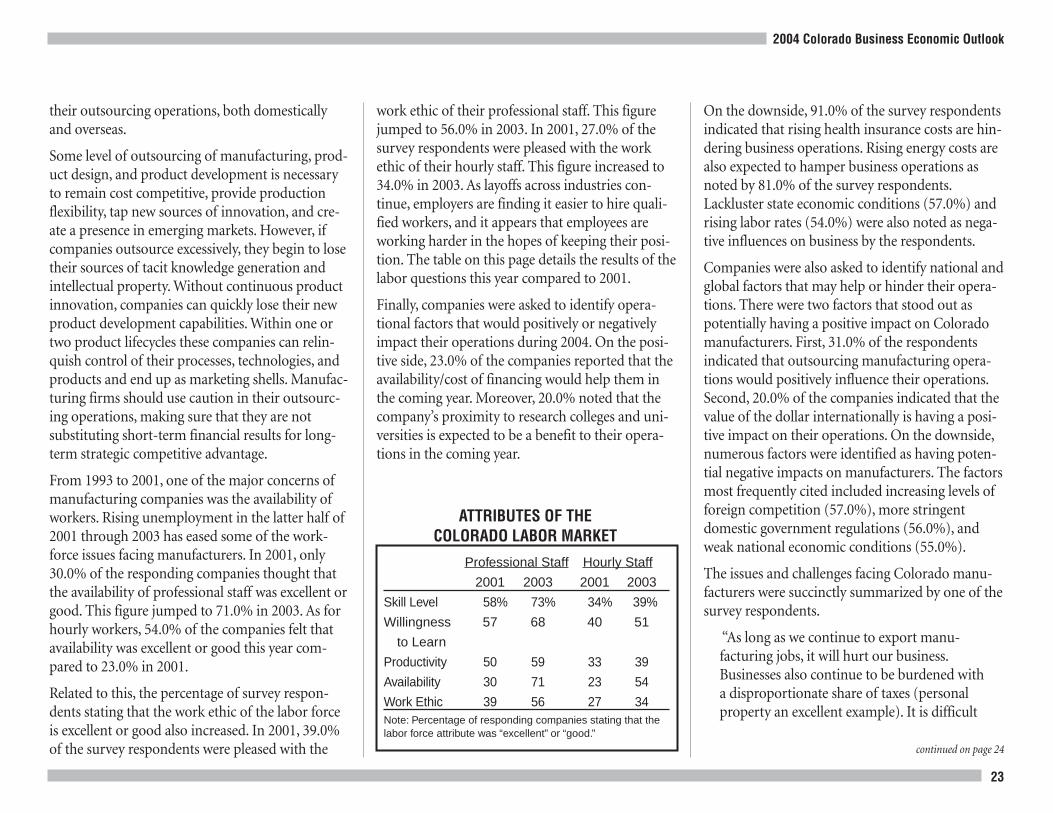

From 1993 to 2001, one of the major concerns ofmanufacturing companies was the availability ofworkers. Rising unemployment in the latter half of2001 through 2003 has eased some of the work-force issues facing manufacturers. In 2001, only30.0% of the responding companies thought thatthe availability of professional staff was excellent orgood. This figure jumped to 71.0% in 2003. As forhourly workers, 54.0% of the companies felt thatavailability was excellent or good this year com-pared to 23.0% in 2001.

Related to this, the percentage of survey respon-dents stating that the work ethic of the labor forceis excellent or good also increased. In 2001, 39.0%of the survey respondents were pleased with the

work ethic of their professional staff. This figurejumped to 56.0% in 2003. In 2001, 27.0% of thesurvey respondents were pleased with the workethic of their hourly staff. This figure increased to34.0% in 2003. As layoffs across industries con-tinue, employers are finding it easier to hire quali-fied workers, and it appears that employees areworking harder in the hopes of keeping their posi-tion. The table on this page details the results of thelabor questions this year compared to 2001.

Finally, companies were asked to identify opera-tional factors that would positively or negativelyimpact their operations during 2004. On the posi-tive side, 23.0% of the companies reported that theavailability/cost of financing would help them inthe coming year. Moreover, 20.0% noted that thecompany’s proximity to research colleges and uni-versities is expected to be a benefit to their opera-tions in the coming year.

On the downside, 91.0% of the survey respondentsindicated that rising health insurance costs are hin-dering business operations. Rising energy costs arealso expected to hamper business operations asnoted by 81.0% of the survey respondents.Lackluster state economic conditions (57.0%) andrising labor rates (54.0%) were also noted as nega-tive influences on business by the respondents.

Companies were also asked to identify national andglobal factors that may help or hinder their opera-tions. There were two factors that stood out aspotentially having a positive impact on Coloradomanufacturers. First, 31.0% of the respondentsindicated that outsourcing manufacturing opera-tions would positively influence their operations.Second, 20.0% of the companies indicated that thevalue of the dollar internationally is having a posi-tive impact on their operations. On the downside,numerous factors were identified as having poten-tial negative impacts on manufacturers. The factorsmost frequently cited included increasing levels offoreign competition (57.0%), more stringentdomestic government regulations (56.0%), andweak national economic conditions (55.0%).

The issues and challenges facing Colorado manu-facturers were succinctly summarized by one of thesurvey respondents.

“As long as we continue to export manu-facturing jobs, it will hurt our business.Businesses also continue to be burdened witha disproportionate share of taxes (personalproperty an excellent example). It is difficult

ATTRIBUTES OF THECOLORADO LABOR MARKET

Professional Staff Hourly Staff

2001 2003 2001 2003

Skill Level 58% 73% 34% 39%

Willingness 57 68 40 51

to Learn

Productivity 50 59 33 39

Availability 30 71 23 54

Work Ethic 39 56 27 34Note: Percentage of responding companies stating that thelabor force attribute was “excellent” or “good.”

2004 Colorado Business Economic Outlook

24

enough competing with foreign labor rates,escalating health costs (that many foreigncountries do not have), unfavorable currencyvaluations, etc. without having our own local,state, and federal governments add to theproblem.”

Employment Forecast Colorado manufacturers took another beating in2003 after sustaining a record loss of 15,600 jobs in2002. The industry contracted by an additional11,000 positions in 2003, a 6.6% decline. While thepicture is brighter for 2004 as national and inter-national economies improve, employment is stillexpected to drop by 0.7%.

NONDURABLE GOODS

Under the newly implemented NAICS, the largestnondurable goods subsector in Colorado is foodmanufacturing. The value of food product ship-ments throughout the United States continues toincrease, with shipments increasing 4.3% fromAugust 2002 to 2003. Total inventories are holdingsteady, while the ratio of inventories to shipmentshas declined since the beginning of the year, indi-cating some industry strength. Employment in thefood products industry nationally shows a positivetrend, with stronger growth since the beginning of2003. In Colorado, employment in this subsector isexpected to remain at 19,500 positions in 2003, the

same level as 2002. The industry is forecasted toexpand by 100 positions in 2004.

The beverage manufacturing subsector in Coloradohas remained relatively stable since 1999. Totalemployment in 2002 stood at 5,900 positions, andis expected to increase by 100 positions in both2003 and 2004. Colorado is a leading producer ofbeer and micro-brews, and also has significantwine, water, and soda production operations.

The printing and related support activities subsec-tor includes newspaper production, commercialprinting, periodicals, books, greeting cards, andother miscellaneous publishing. Computerizationand the economic downturn have contributed to

Manufacturingcontinued from page 23

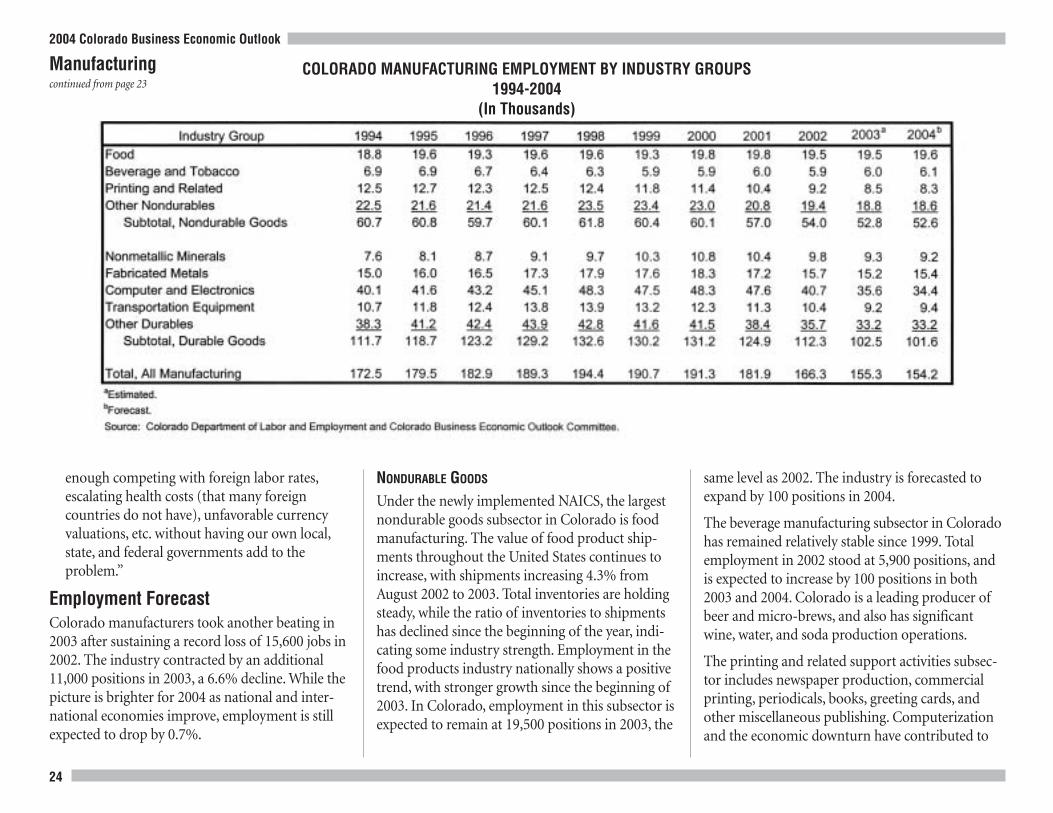

COLORADO MANUFACTURING EMPLOYMENT BY INDUSTRY GROUPS1994-2004

(In Thousands)

2004 Colorado Business Economic Outlook

25

continual declines in the subsector since 1998, bothnationally and in Colorado. Computer hardwareand software has increased the ability of all compa-nies to produce and distribute reports and publica-tions electronically rather than in printed format.Furthermore, the economic downturn decreaseddemand for printed media by businesses. The totalvalue of shipments in the United States in theprinting subsector is down 5.6% from August 2002to August 2003. This decline began in 2000 whenshipments throughout the United States peaked at

a little over $9 billion. Colorado employment in theprinting and related support activities subsectorcontinues to decline, with a loss of 700 positionsexpected in 2003 followed by an additional loss of200 jobs in 2004.

The other nondurable goods subsectors includetextiles, apparel and leather goods, paper manufac-turing, petroleum and coal products, chemicals,and plastics and rubber products. With the excep-tion of the latter two categories, these subsectors

have a small, yet stable, presence in Colorado. Thetextiles and apparel and leather goods subsectorsemploy about 3,200 people, but continue to facestiff overseas competition. Roughly 2,600 peopleare employed in paper manufacturing in the state,including cardboard containers, packaging, andpaper products. Another 700 people work in thepetroleum and coal products subsector, mainlywithin petroleum refining operations. Flat toslightly declining employment is expected withinall of these subsectors in 2003 and 2004.

The chemical manufacturing subsector includespetrochemical manufacturing, industrial gases,biotechnology, pharmaceuticals, household chemi-cals, and related industries. This is a very volatilesubsector, with wide swings in individual companyemployment resulting from the success or failure of medical clinical trials and changes in the price of oil. Biotechnology is an important emergingsubsector for the Colorado economy and has beentargeted in state economic development efforts.The continued development of the Bioscience ParkCenter at the former Fitzsimons Army MedicalCenter and the transformation of this site to aneducational medical complex present long-termopportunities for the industry, though employ-ment is expected to grow by only 100 jobs in both2003 and 2004. Chemical manufacturing employsapproximately 7,100 Colorado workers.

The plastics and rubber products subsectorincludes companies producing plastic film, plasticfoam products, and other miscellaneous products.Rubber firms have a limited presence in Colorado,

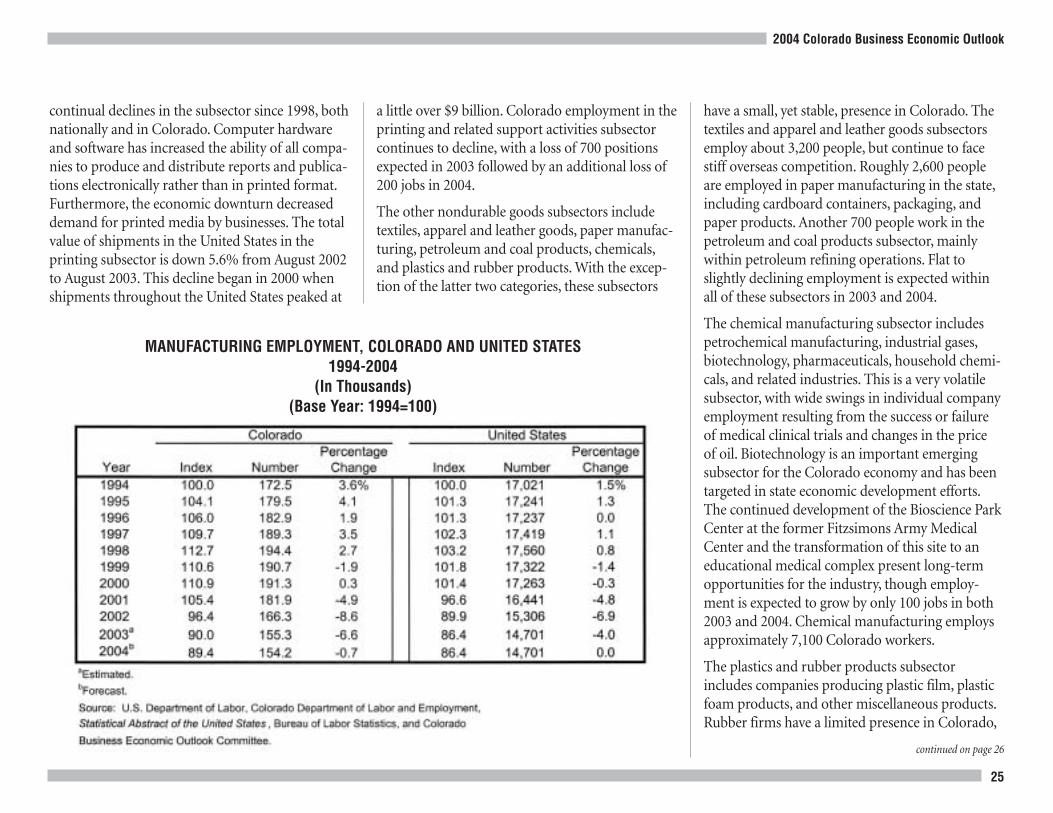

MANUFACTURING EMPLOYMENT, COLORADO AND UNITED STATES1994-2004

(In Thousands)(Base Year: 1994=100)

continued on page 26

2004 Colorado Business Economic Outlook

26

Manufacturingcontinued from page 25

while the plastics industry continues to grow. Thissubsector includes injection-molding companies,which are closely tied to the biotech and electronicsindustries. The recent slowdown in those industriesmeans that employment in the rubber and plasticssubsector will decline by 200 workers in both 2003and 2004, down from the 2002 employment baseof 5,400 workers.

The other nondurable goods subsectors areexpected to decline by 600 positions in 2003

and 200 positions in 2004. This brings the totalNondurable Goods Sector employment forecast to52,800 positions in 2003, down from 54,000 jobs in2002. Employment will continue to fall slightly in2004, declining by 200 positions. Nondurablegoods employment continues to represent aboutone-third of Colorado’s total manufacturingemployment base.

DURABLE GOODS

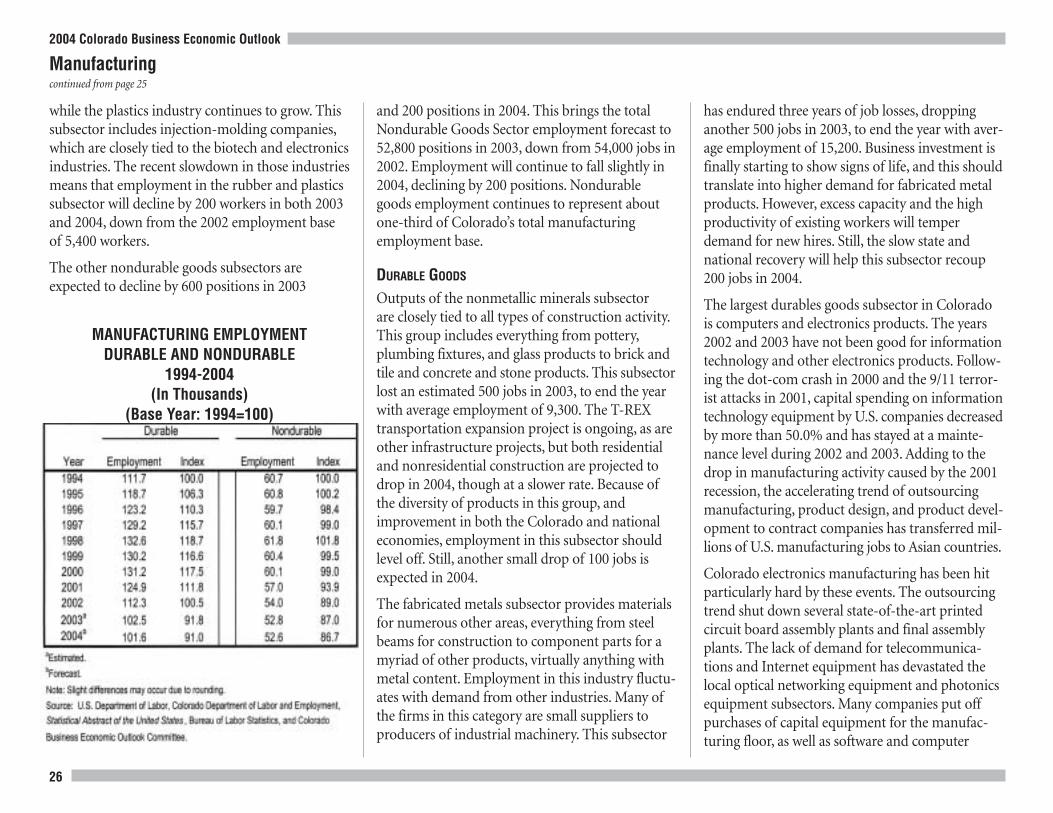

Outputs of the nonmetallic minerals subsector are closely tied to all types of construction activity.This group includes everything from pottery,plumbing fixtures, and glass products to brick andtile and concrete and stone products. This subsectorlost an estimated 500 jobs in 2003, to end the yearwith average employment of 9,300. The T-REXtransportation expansion project is ongoing, as areother infrastructure projects, but both residentialand nonresidential construction are projected todrop in 2004, though at a slower rate. Because ofthe diversity of products in this group, andimprovement in both the Colorado and nationaleconomies, employment in this subsector shouldlevel off. Still, another small drop of 100 jobs isexpected in 2004.

The fabricated metals subsector provides materialsfor numerous other areas, everything from steelbeams for construction to component parts for amyriad of other products, virtually anything withmetal content. Employment in this industry fluctu-ates with demand from other industries. Many ofthe firms in this category are small suppliers toproducers of industrial machinery. This subsector

has endured three years of job losses, droppinganother 500 jobs in 2003, to end the year with aver-age employment of 15,200. Business investment isfinally starting to show signs of life, and this shouldtranslate into higher demand for fabricated metalproducts. However, excess capacity and the highproductivity of existing workers will temperdemand for new hires. Still, the slow state andnational recovery will help this subsector recoup200 jobs in 2004.

The largest durables goods subsector in Coloradois computers and electronics products. The years2002 and 2003 have not been good for informationtechnology and other electronics products. Follow-ing the dot-com crash in 2000 and the 9/11 terror-ist attacks in 2001, capital spending on informationtechnology equipment by U.S. companies decreasedby more than 50.0% and has stayed at a mainte-nance level during 2002 and 2003. Adding to thedrop in manufacturing activity caused by the 2001recession, the accelerating trend of outsourcingmanufacturing, product design, and product devel-opment to contract companies has transferred mil-lions of U.S. manufacturing jobs to Asian countries.

Colorado electronics manufacturing has been hitparticularly hard by these events. The outsourcingtrend shut down several state-of-the-art printedcircuit board assembly plants and final assemblyplants. The lack of demand for telecommunica-tions and Internet equipment has devastated thelocal optical networking equipment and photonicsequipment subsectors. Many companies put offpurchases of capital equipment for the manufac-turing floor, as well as software and computer

MANUFACTURING EMPLOYMENTDURABLE AND NONDURABLE

1994-2004(In Thousands)

(Base Year: 1994=100)

2004 Colorado Business Economic Outlook

27

systems for the front office, during the recession.However, older equipment and IT systems willneed to be replaced in the near future, and thisshould bring about new orders in those subsectors.While these new orders will eventually lead to theneed for more workers, employment conditionswill remain bleak in the short-term as companiesmake use of excess capacity and productive, exist-ing employees. Colorado employment in this sub-sector will be down by about 5,100 jobs in 2003,and decline by another 1,200 positions in 2004.

Lockheed Martin dominates the transportationequipment subsector. Increased defense and secu-rity spending in 2003 has provided LockheedMartin and Ball Aerospace with several newdefense and security-related contracts. However,other contracts have been completed and somemanufacturing activities have been transferred outof Colorado. On balance, transportation equip-ment subsector employment is expected todecrease by about 1,200 jobs in 2003 but willrebound with the addition of 200 jobs in 2004.

The other Durable Goods Sectors include woodproducts, primary metals, machinery, electricalequipment and appliances, furniture, and miscella-neous manufacturing. Employment in this diversegroup of subsectors is expected to stay flat during2003 and 2004. However, slight improvements inmany of these subsectors over the last severalmonths bode well for late 2004 into 2005.

Employment in the wood products and furnituresubsectors fell by about 900 positions between2002 and 2003 due to overall recessionary condi-tions. With decreased home construction but

improving consumer demand, the net impact isexpected to be a loss of just 100 positions in 2004.

Roughly 2,000 people are employed in the primarymetals subsector, which includes steel and alu-minum refining, as well as the manufacture ofmetal alloys and superalloys. Output from the pri-mary metals subsector provides materials for manyother subsectors, especially fabricated metals. Dueto the overall sluggishness of the manufacturingindustry, the primary metals subsector is alsoexpected to remain flat in 2003 and 2004.

Demand is strengthening for a wide variety ofgoods, with companies starting to see increases inorders for machinery, and electrical equipment and appliances. Still, with excess capacity in mostindustries, business investment has not picked upas expected. Employment within these two subsec-tors fell from 11,900 workers in 2002 to 10,700 in2003. With new orders coming in, employmentshould stabilize at about 10,600 workers in 2004.

While the shift to NAICS improved the definitionof most manufacturing sectors, the miscellaneousmanufacturing subsector became even broader.Indeed, about 4,500 Colorado workers had beenclassified in miscellaneous manufacturing under