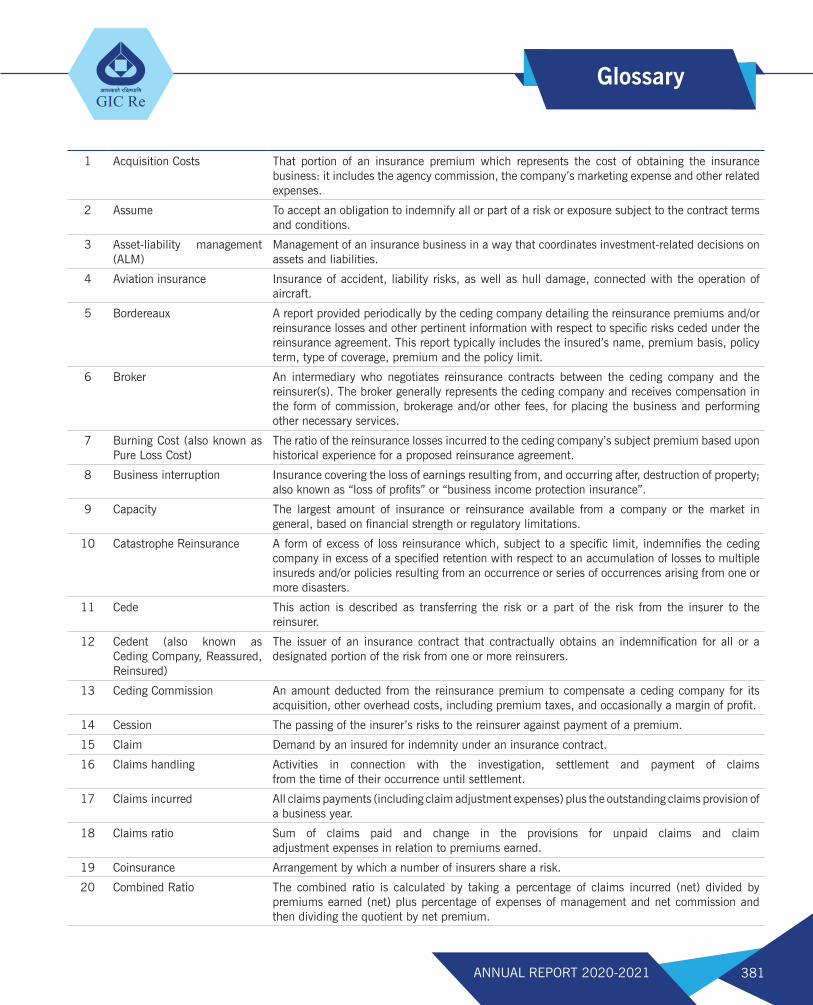

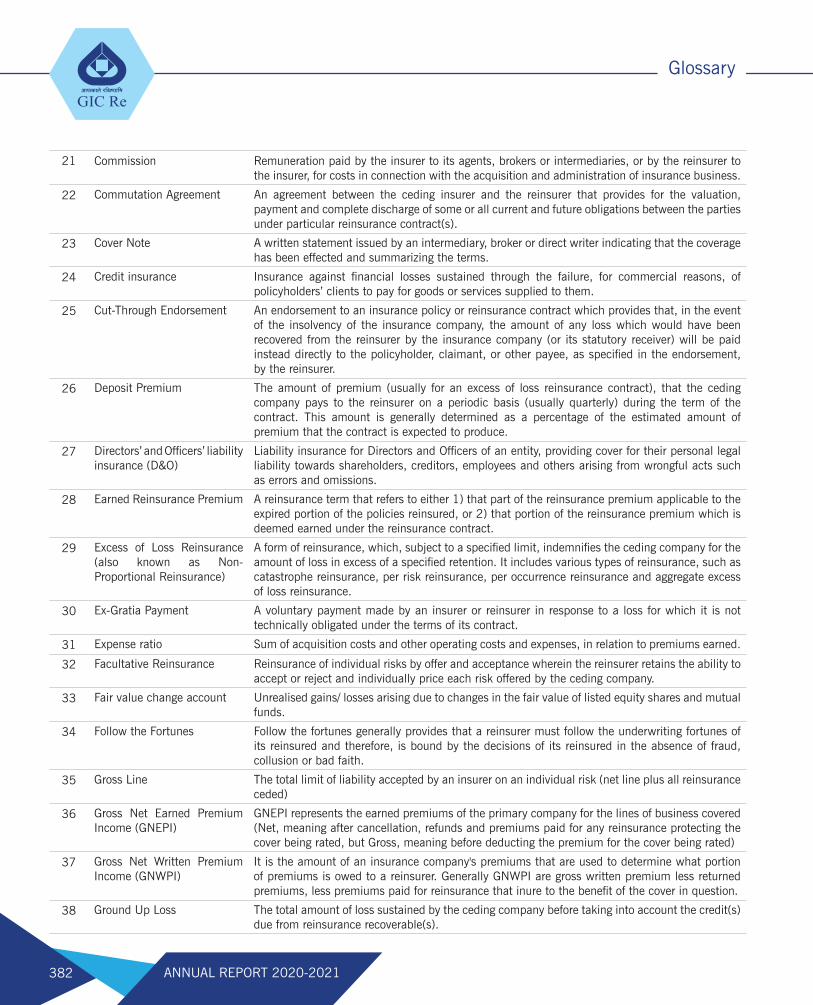

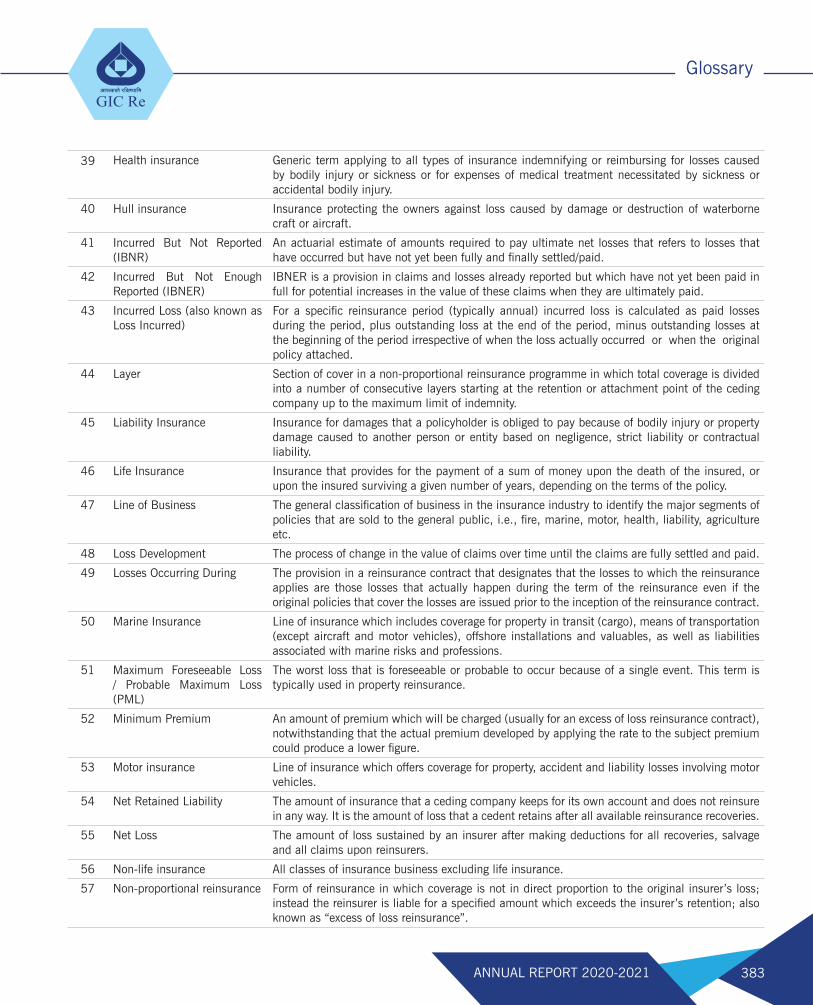

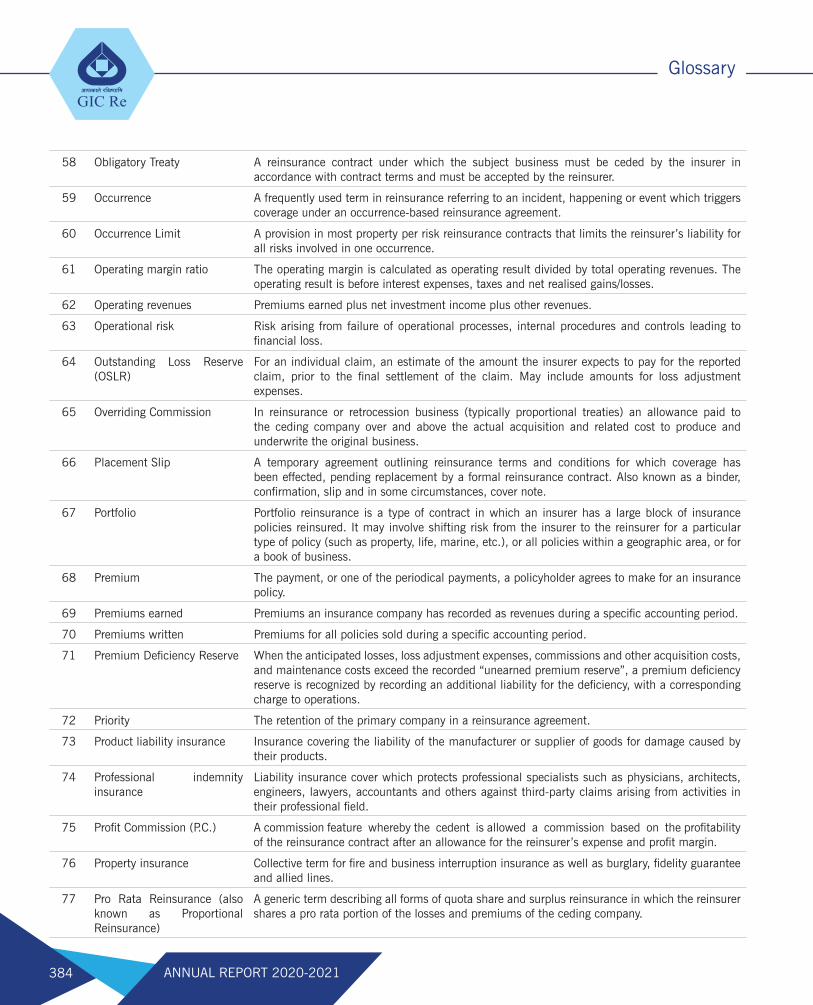

+11 4 fflwrut cfiljr pt ,q (1lffif '$"q;fr) - gic

TRANSCRIPT

Ref. No.: GIC Re/SE/AGM/20-21/3

To, The Manager Listing Department BSE Limited Phiroze Jeejeebhoy Tower Dalal Street Mumbai - 400001

Scrip Code: (BSE - 540755/ NSE - GICRE)

Dear Sir/Madam,

Date: 29th November, 2021

The Manager Listing Department The National Stock Exchange of India Ltd. Exchange Plaza, 5th Floor, Plot C/1, G Block, Bandra Kurla Complex Mumbai - 400051

Sub: SEBI (Listing Obligations and Disclosure Requirements) Regulations 2015

('Listing Regulations')

Regulation 34: Annual Report of the Corporation for Financial Year 2020-21

Pursuant to regulation 34(1) of the SEBI Listing Regulations, please find enclosed herewith copy of Annual Report of the Corporation for the Financial Year 2020-21 which interalia includes Notice of the 49th Annual General Meeting of the Corporation scheduled to be held on Tuesday, 21st December, 2021 at 3 :00 p.m. (1ST) through Video Conference/ Other Audio Visual Means. The said Annual Report is being circulated to the Members of the Corporation through electronic mode.

The Annual Report is hosted on the website of the Corporation at www.gicofindia.com and on the website of the e-voting Agency, Mis. National Securities and Depository Limited at www.evoting.nsdl.com .

You are requested to take note of the above and arrange to bring this to the notice of all concerned.

Thanking y OU

For General Insurance Corporation of India

�I \'}.o� (Satheesh Kumar) CS & Compliance Officer

Encl.: A/A

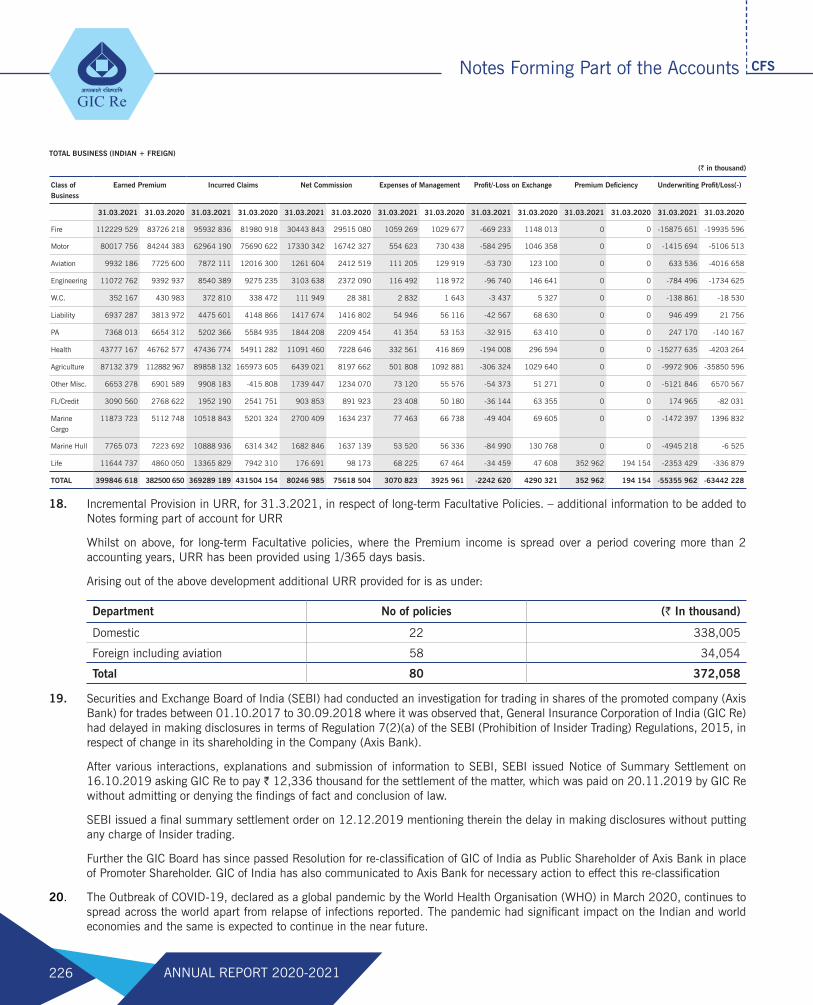

��

GICRe

'+11��4 fflWRUT cfilJr Pt�,q (1lffif��'$"q;fr)

General Insurance Corporation of India

"�m", 170. �- cTcTm. �. �-400 020. "SURAKSHA", 170, J. Tata Road, Churchgate, Mumbai - 400 020. INDIA Tel.: +91-22-2286 7000 www.gicofindia.in

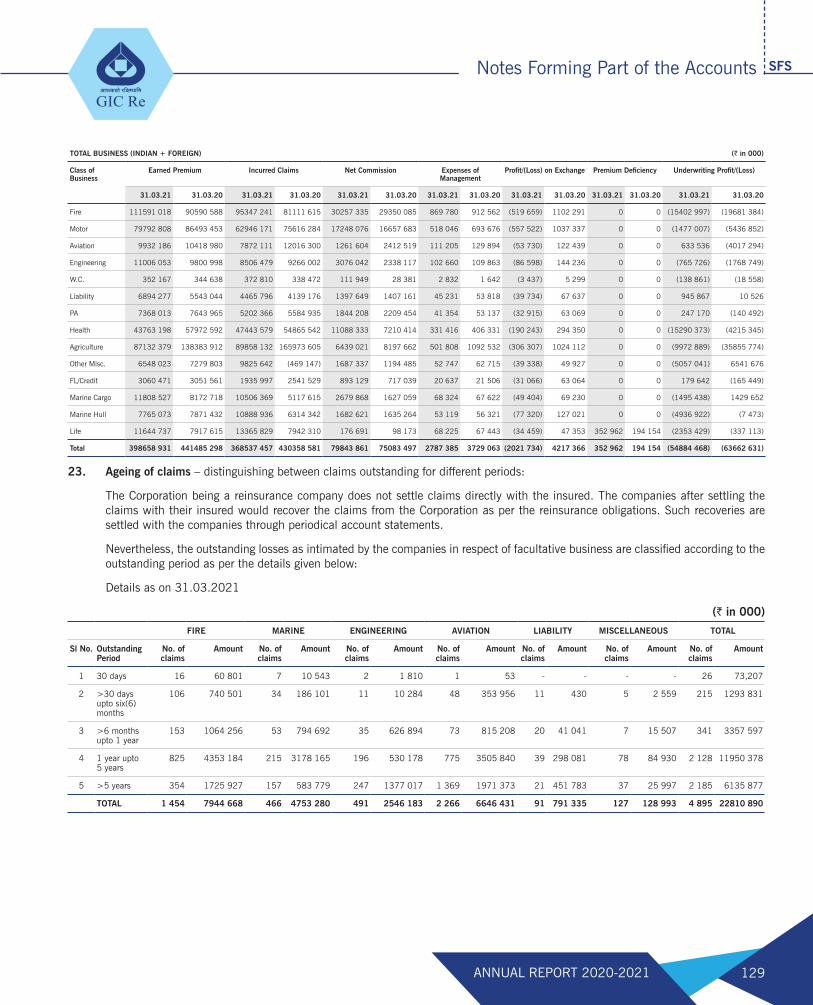

__....,.-,

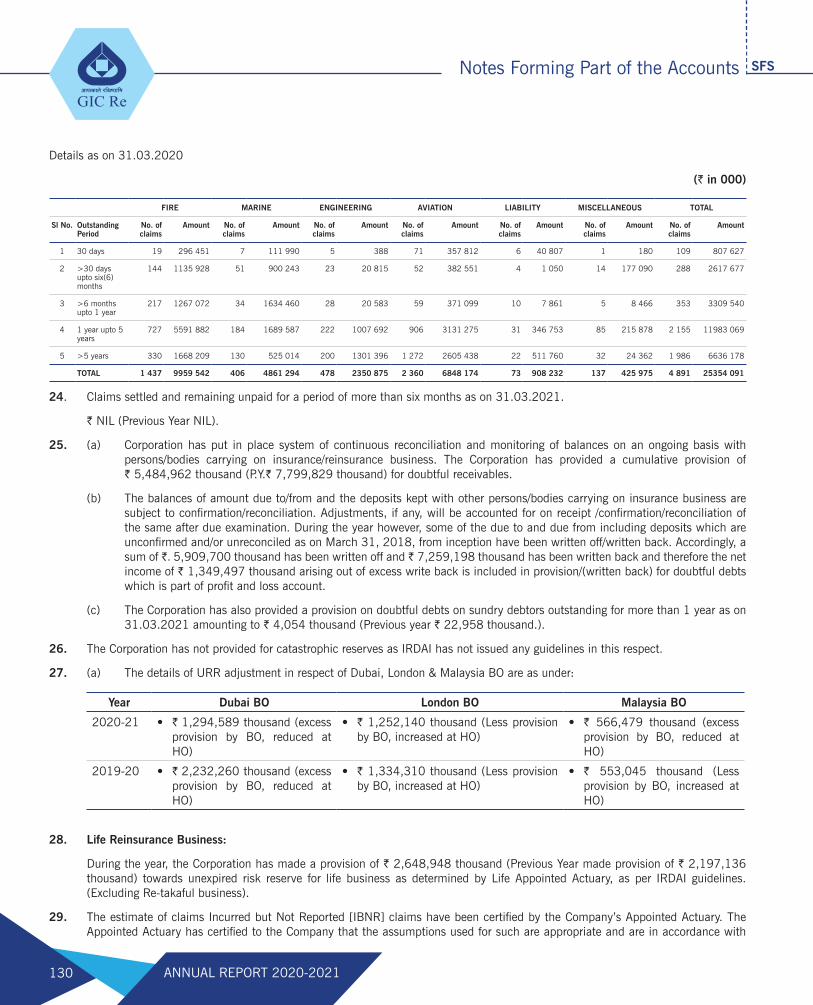

LOOKING UP. LOOKING AHEAD.

49th ANNUAL REPORT 2020-2021

LOOKING UP. LOOKING AHEAD.

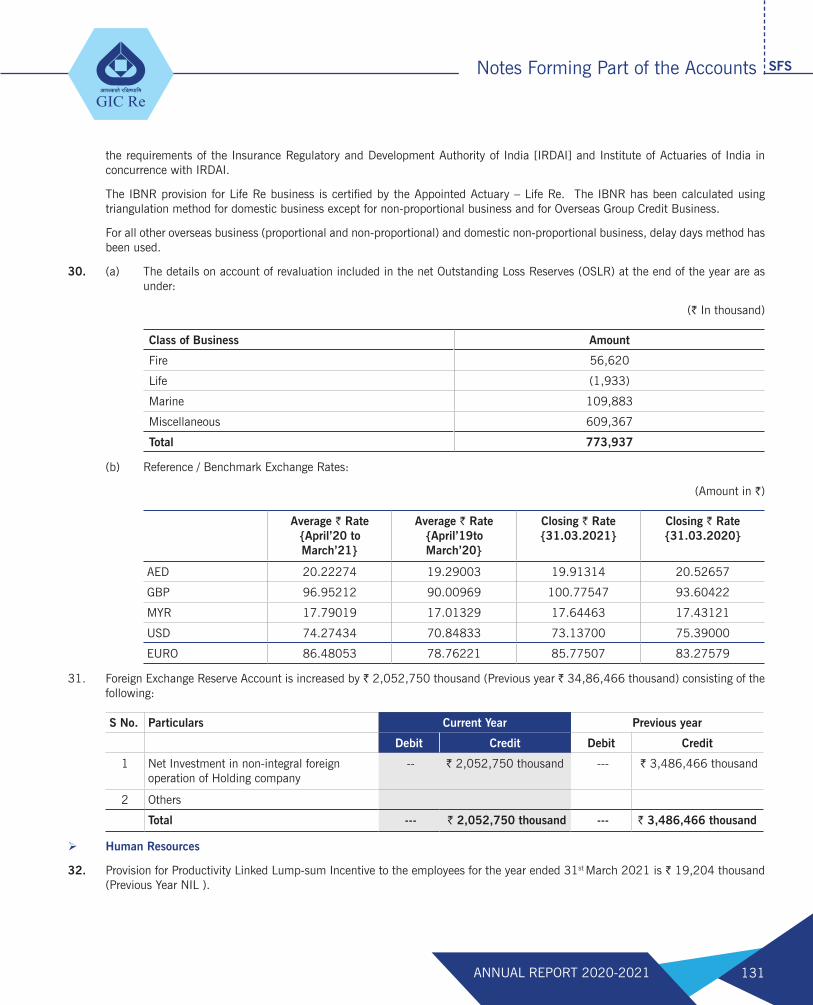

49th ANNUAL REPORT 2020-2021

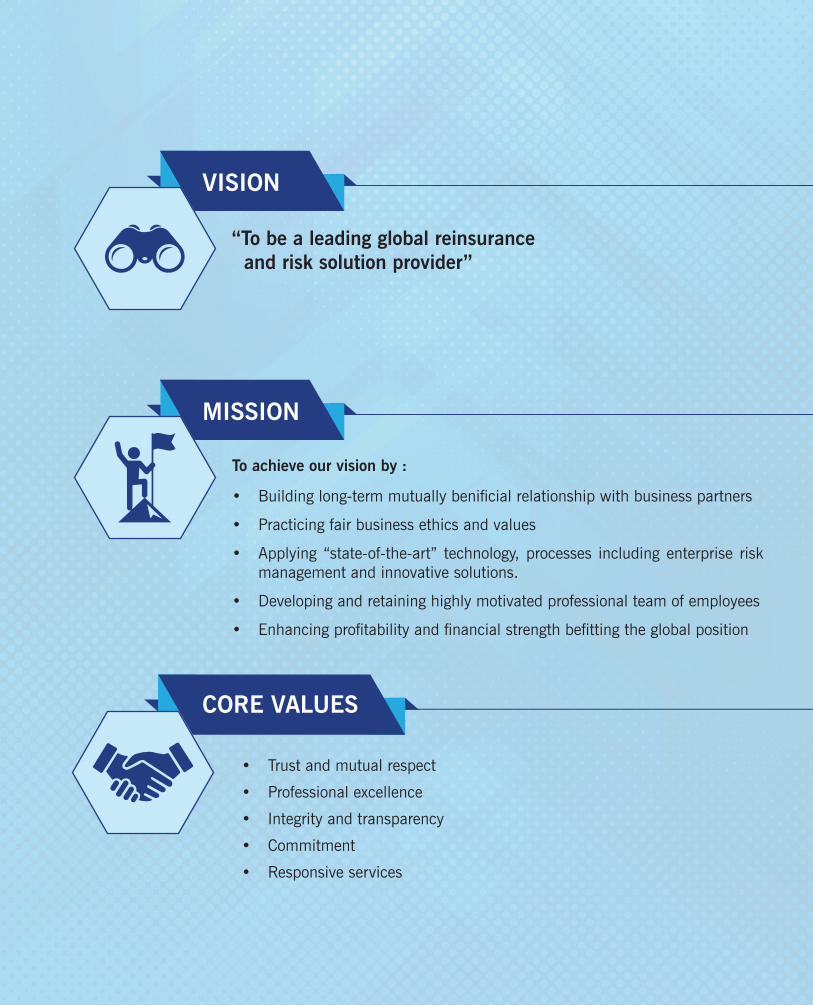

• Trust and mutual respect

• Professional excellence

• Integrity and transparency

• Commitment

• Responsive services

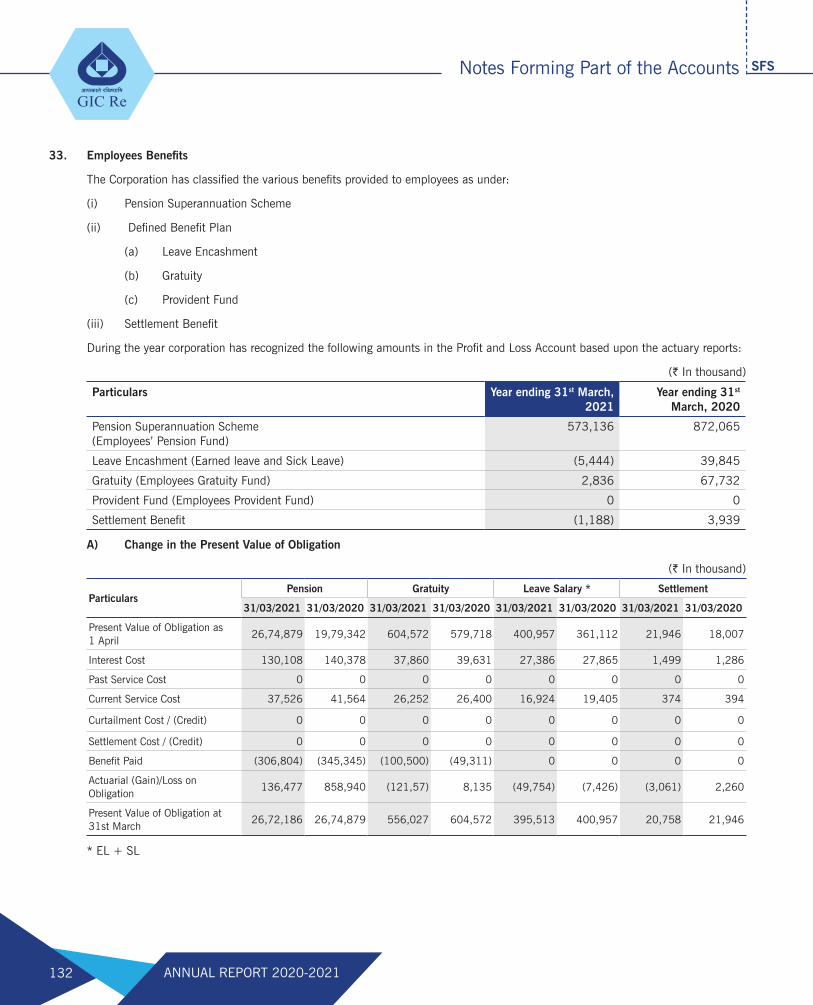

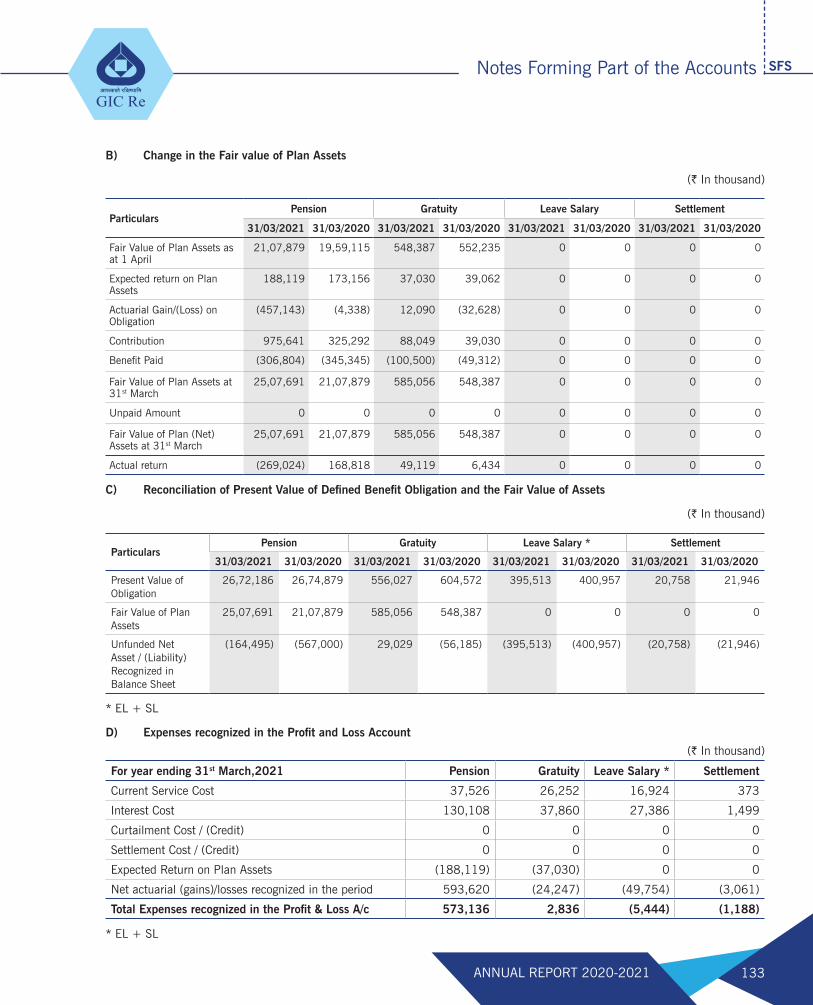

To achieve our vision by :

• Building long-term mutually benificial relationship with business partners

• Practicing fair business ethics and values

• Applying “state-of-the-art” technology, processes including enterprise risk management and innovative solutions.

• Developing and retaining highly motivated professional team of employees

• Enhancing profitability and financial strength befitting the global position

MISSION

“To be a leading global reinsurance and risk solution provider”

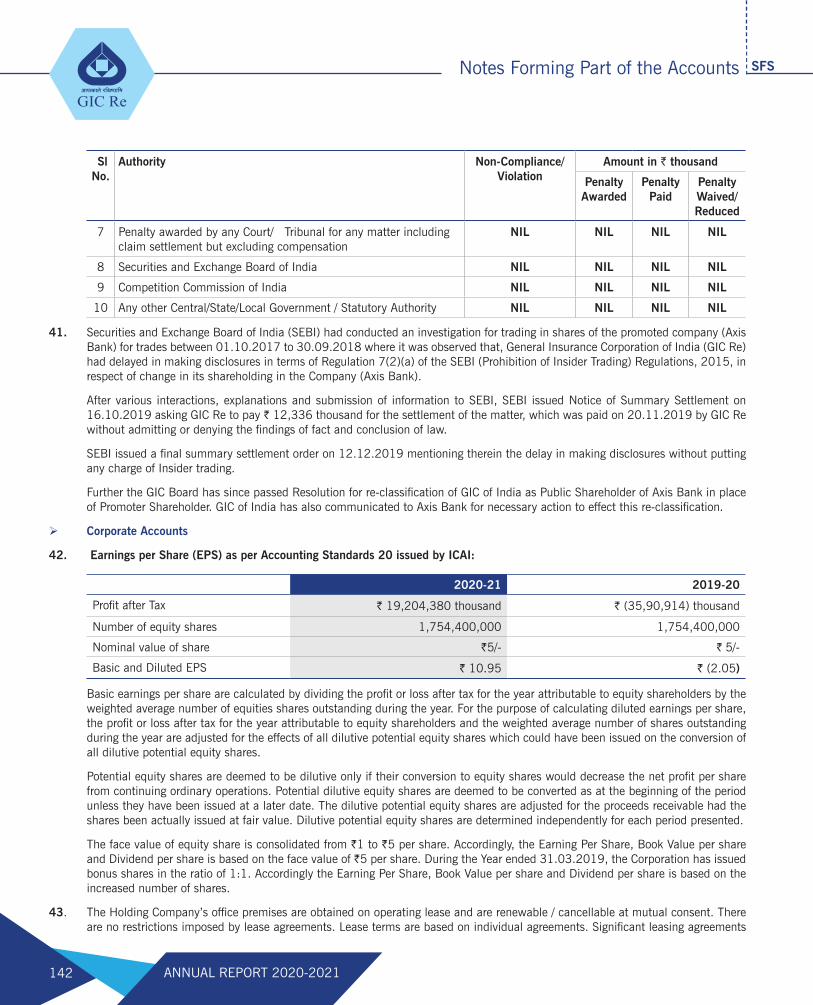

VISION

CORE VALUES

CORPORATE OVERVIEW

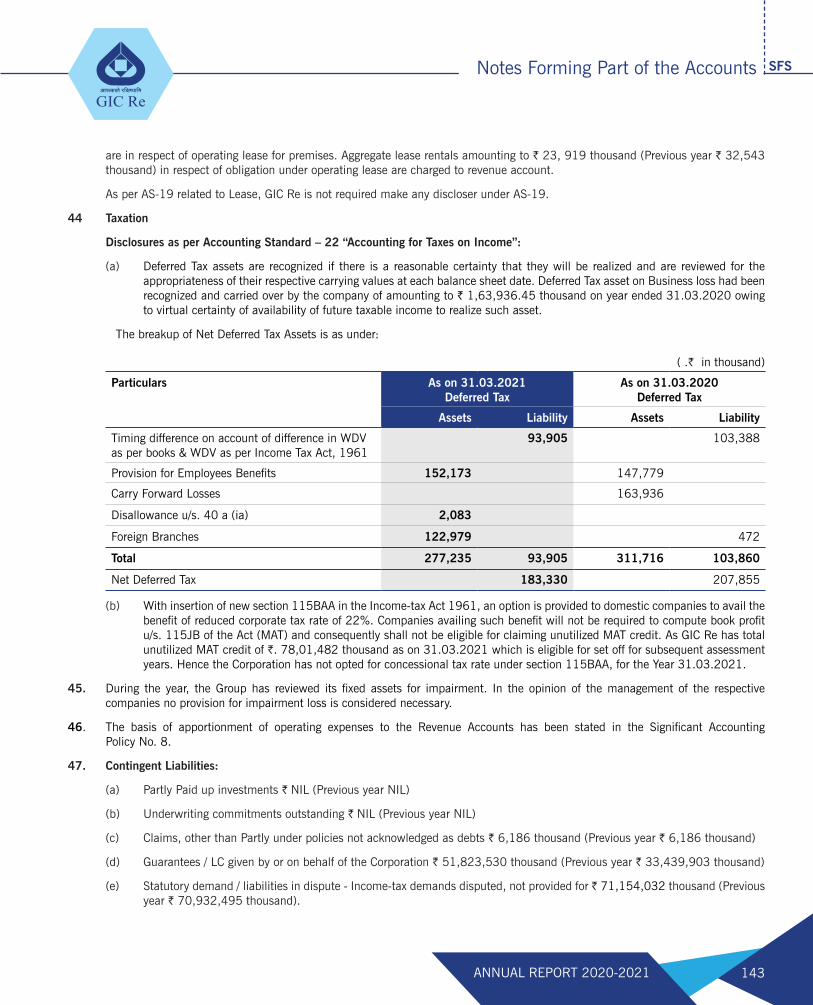

REPORTS

STANDALONE FINANCIAL STATEMENTS

CONTENTS

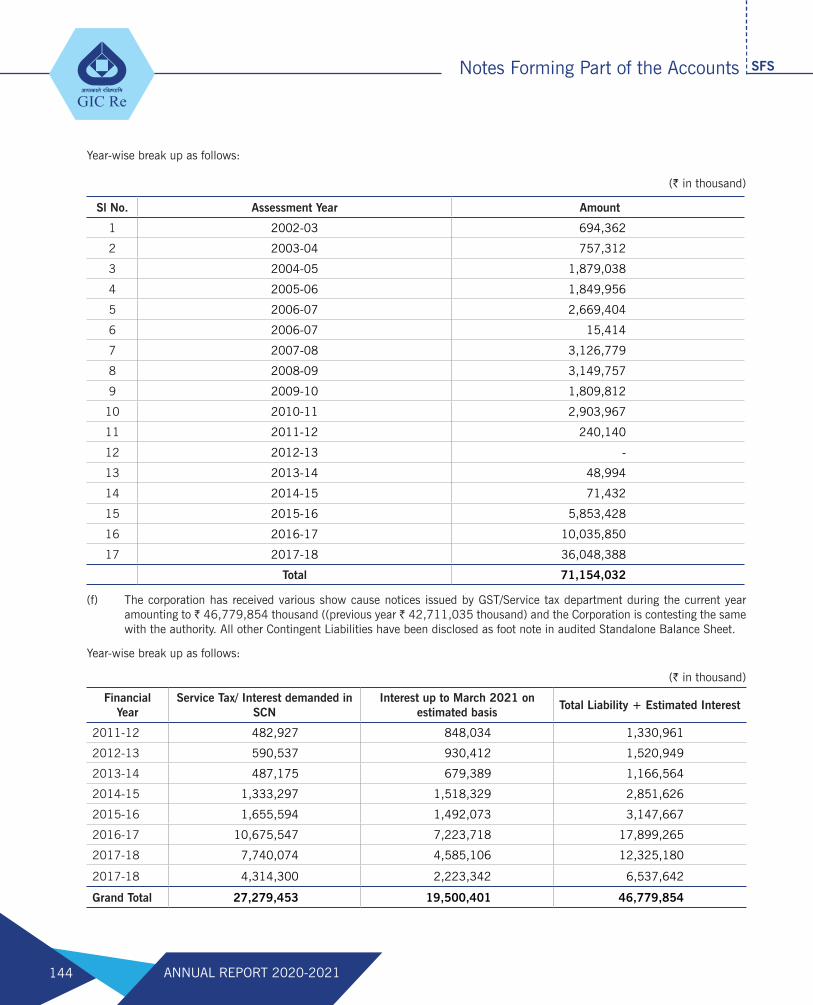

Chairman’s Message ........................................................................................................... 04

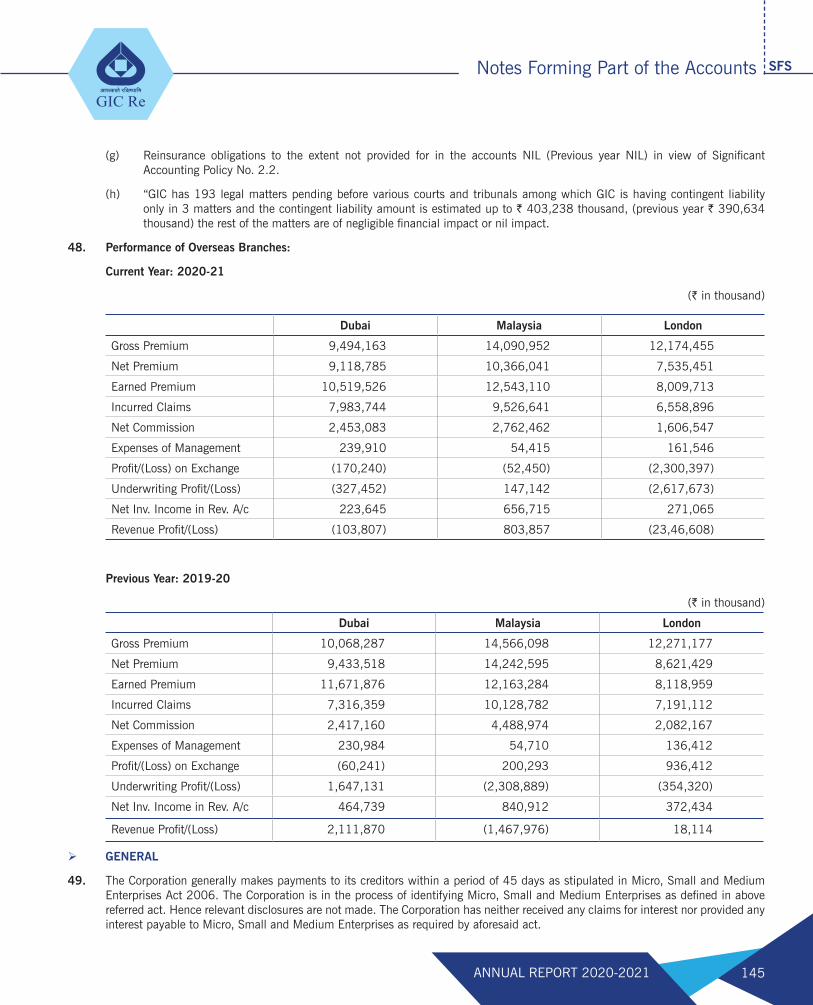

Corporate Information ......................................................................................................... 06

Corporate Chronicle ............................................................................................................. 08

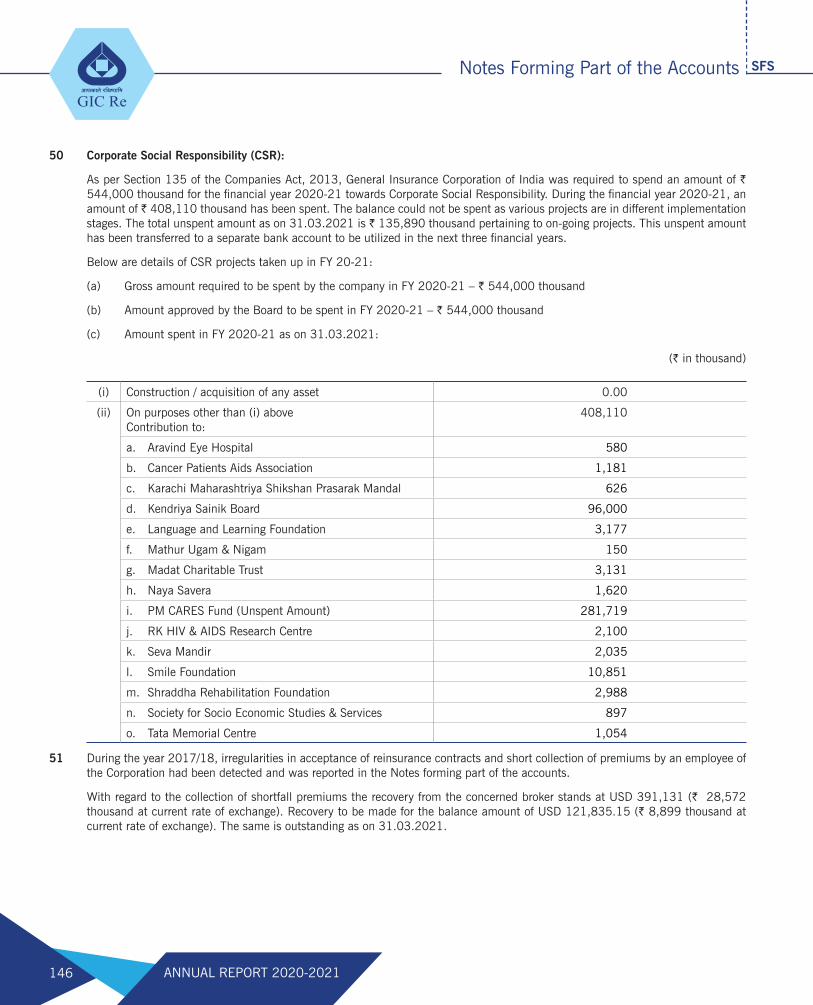

Board of Directors ............................................................................................................... 10

Management ...................................................................................................................... 13

Directors’ Report ................................................................................................................ 14

Corporate Governance Report ............................................................................................... 34

Corporate Social Responsibility Report .................................................................................. 52

Management Discussion and Analysis Report ........................................................................ 54

Management Report ............................................................................................................ 62

Business Responsibility Report ............................................................................................. 64

Independent Auditors’ Report ............................................................................................... 73

Comments of the Comptroller and Auditor General of India ..................................................... 86

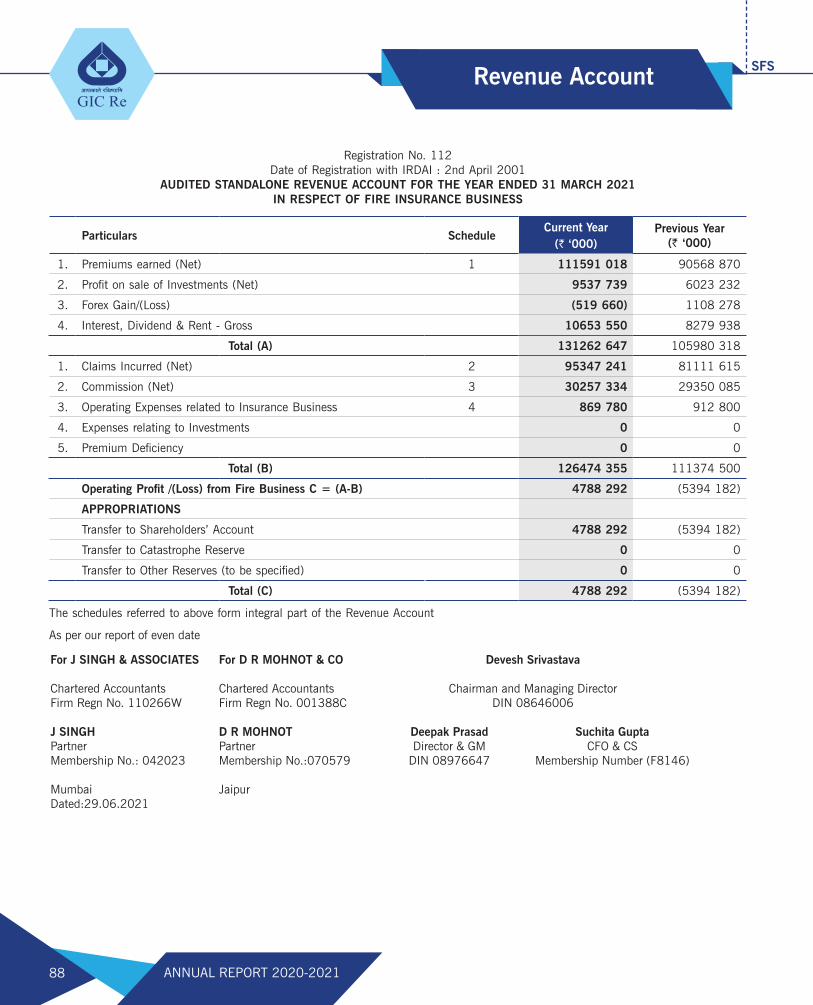

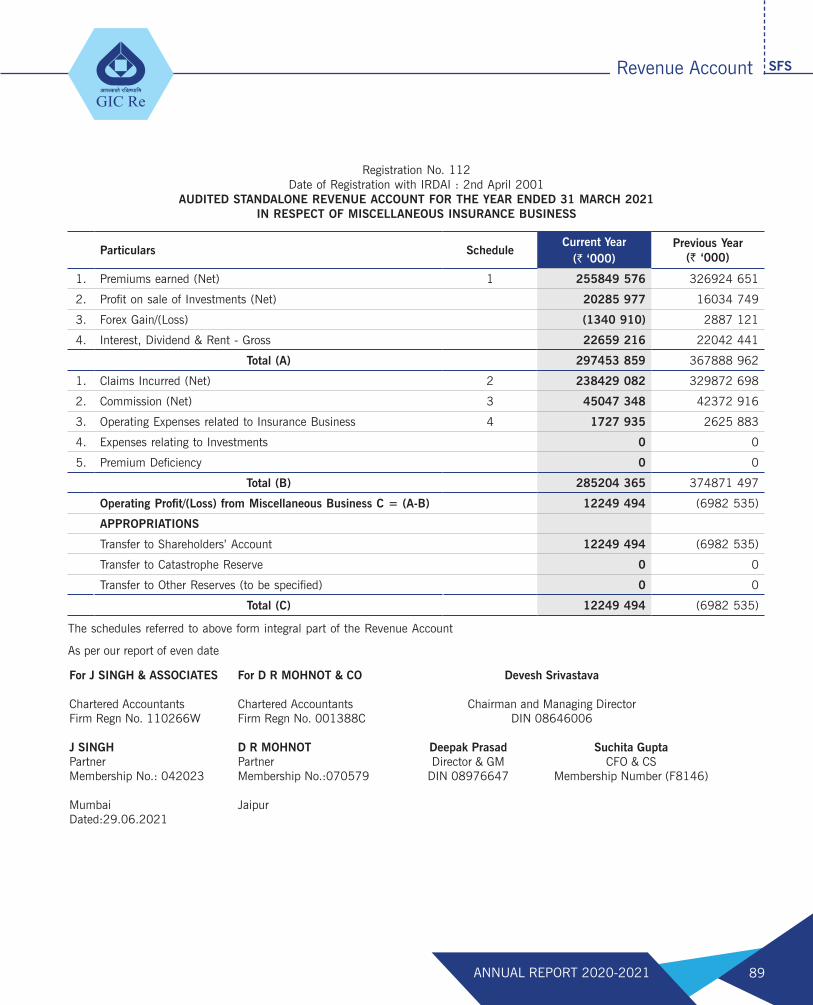

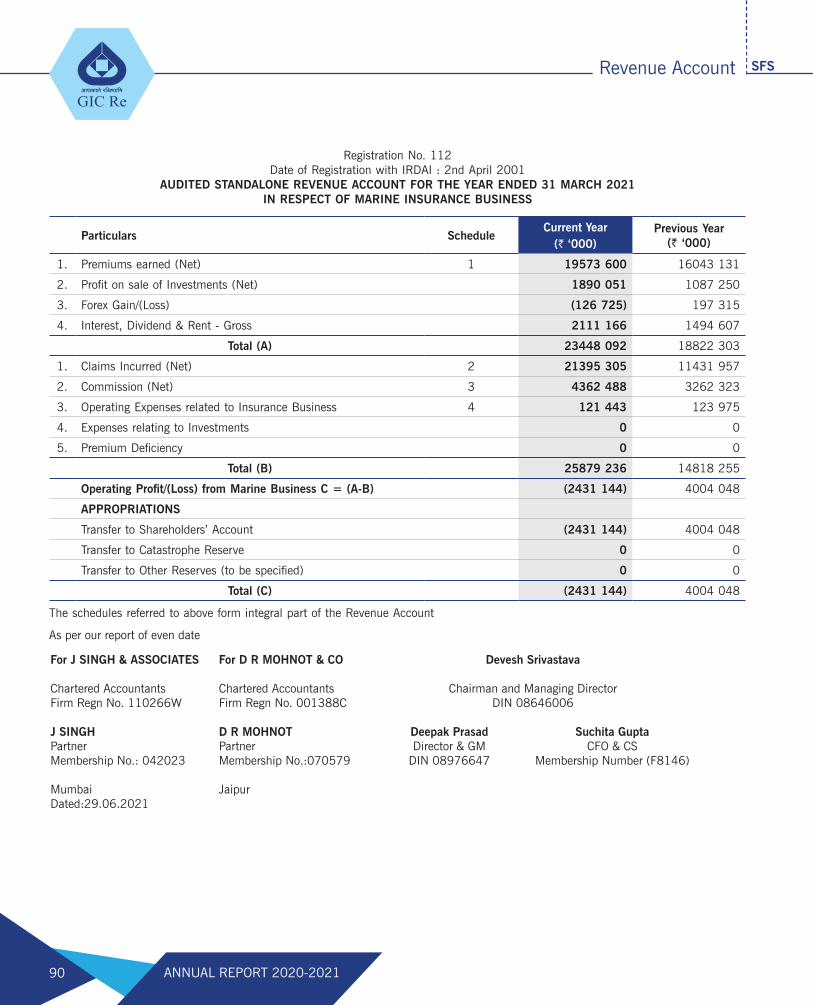

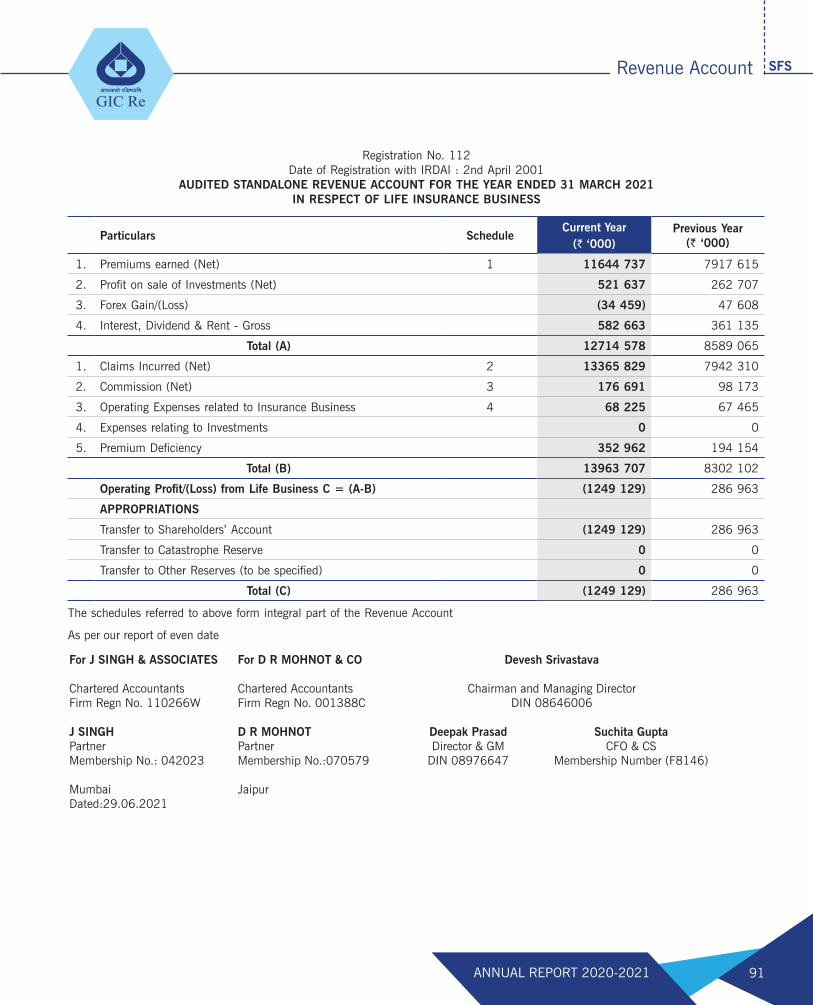

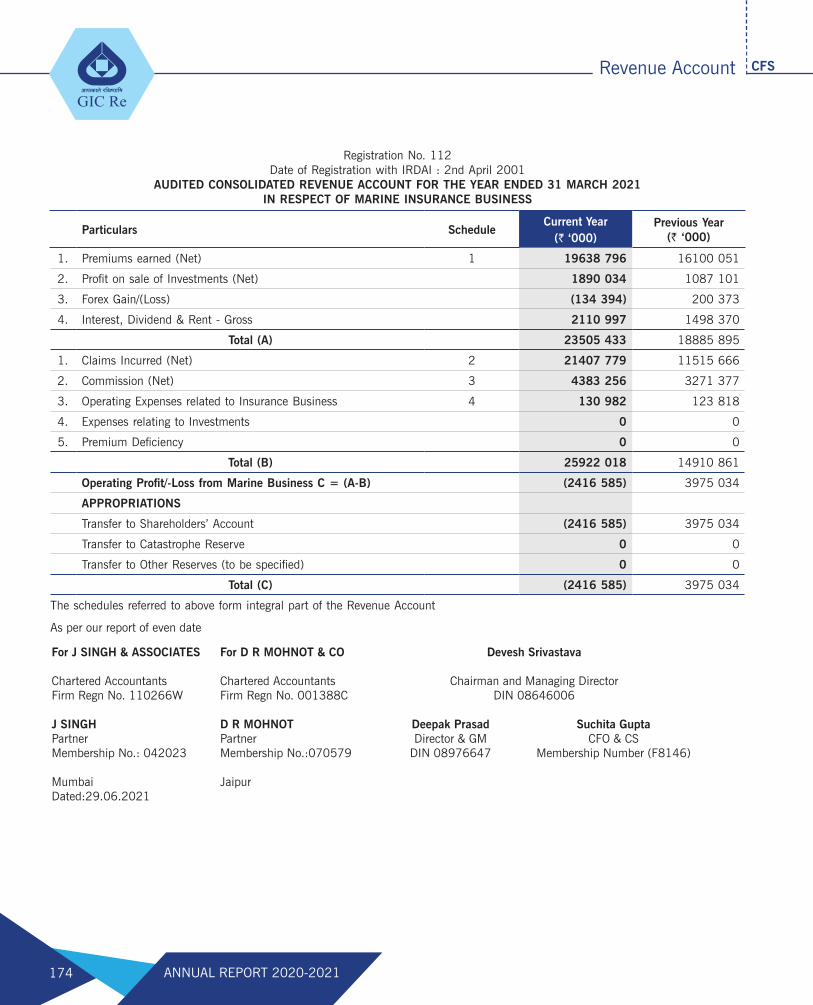

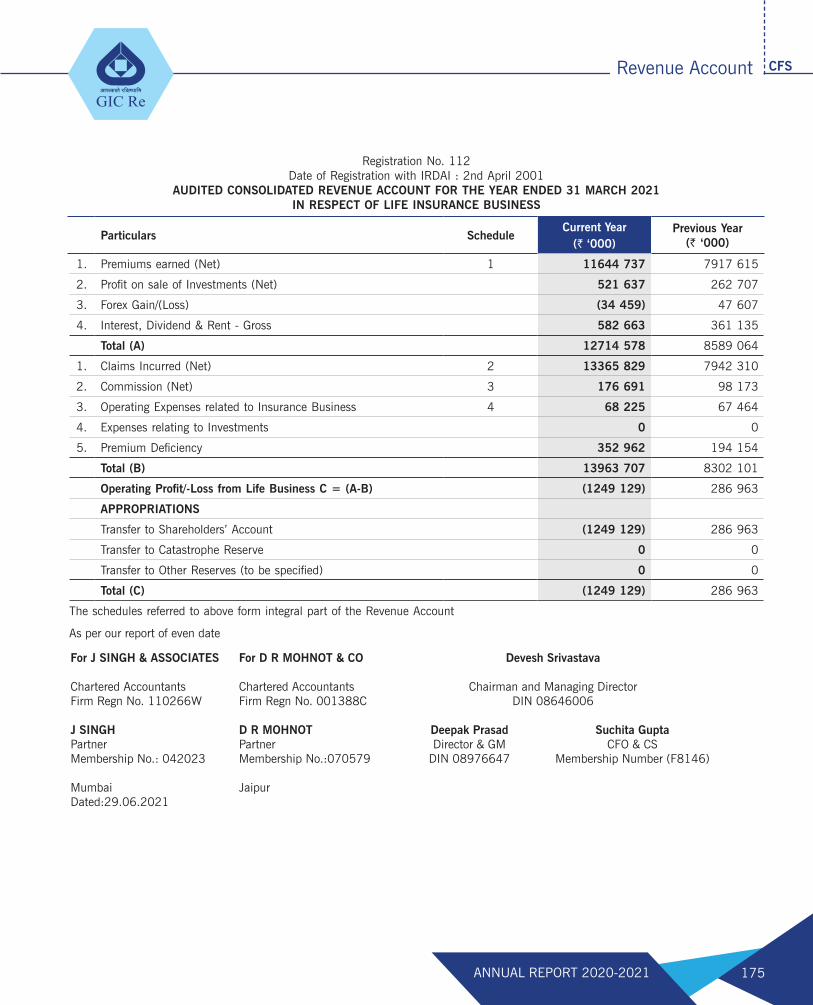

Revenue Account ............................................................................................................... 88

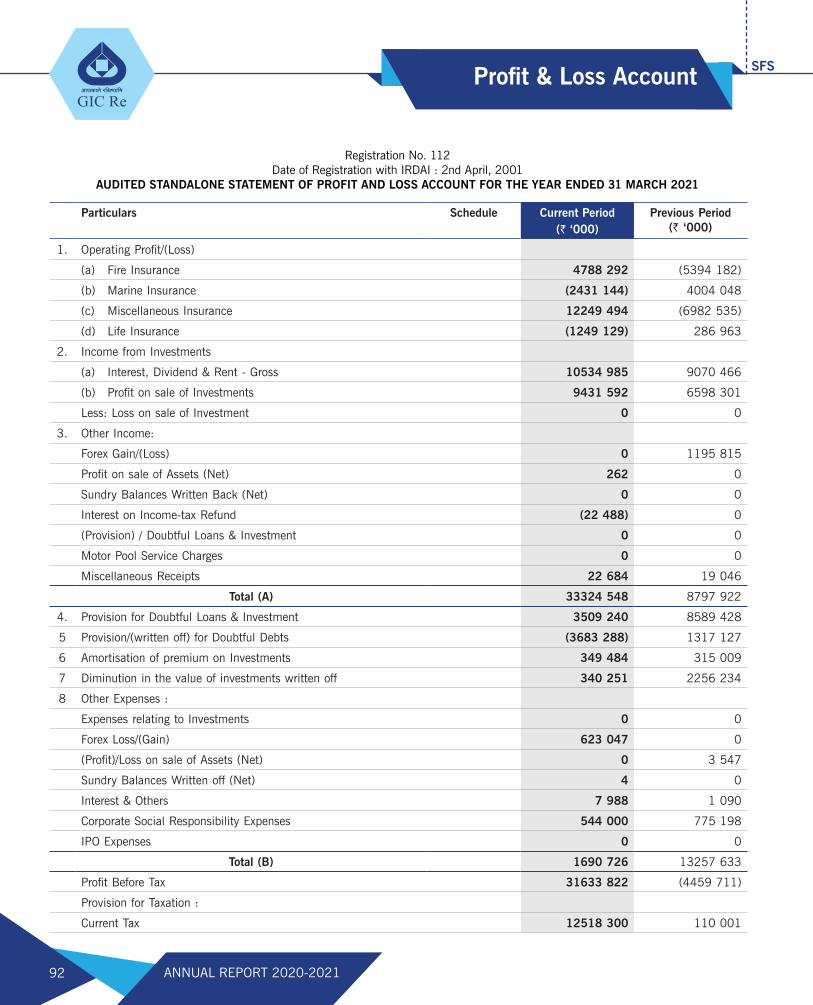

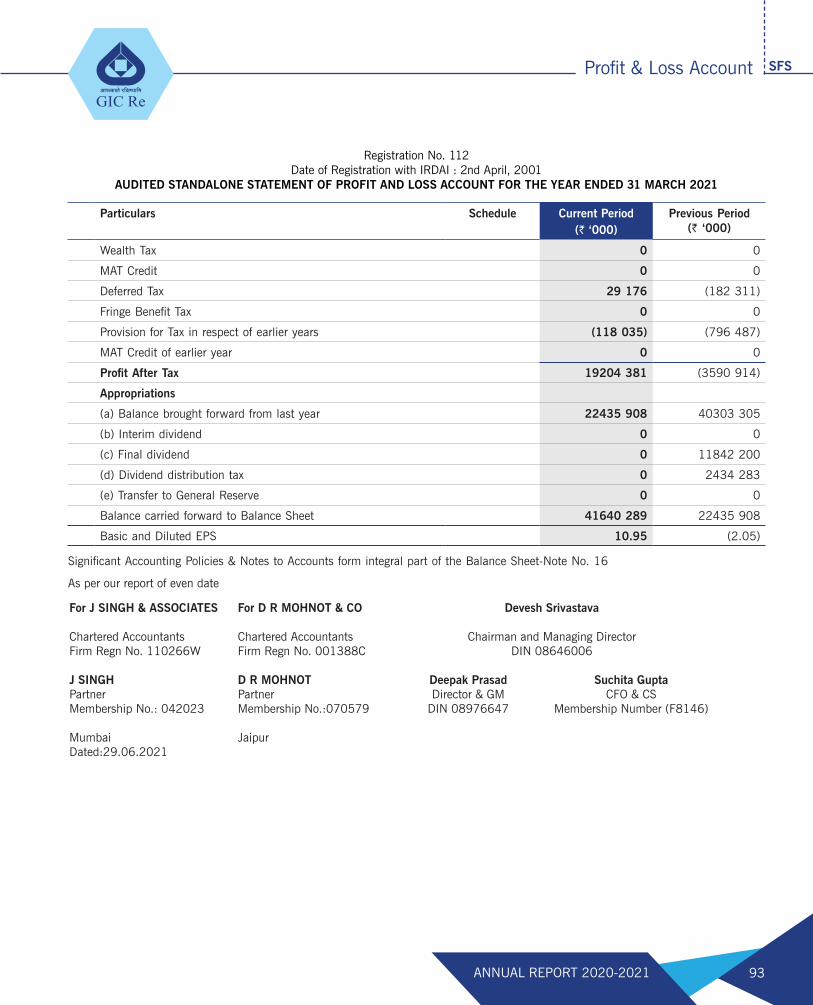

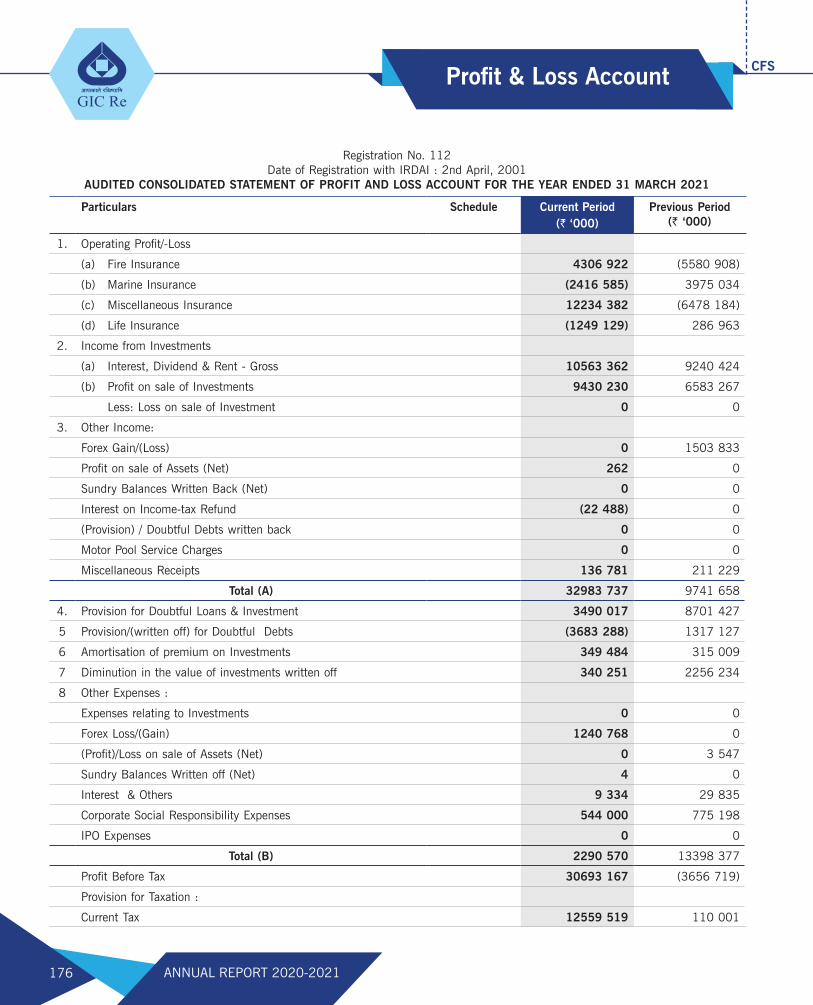

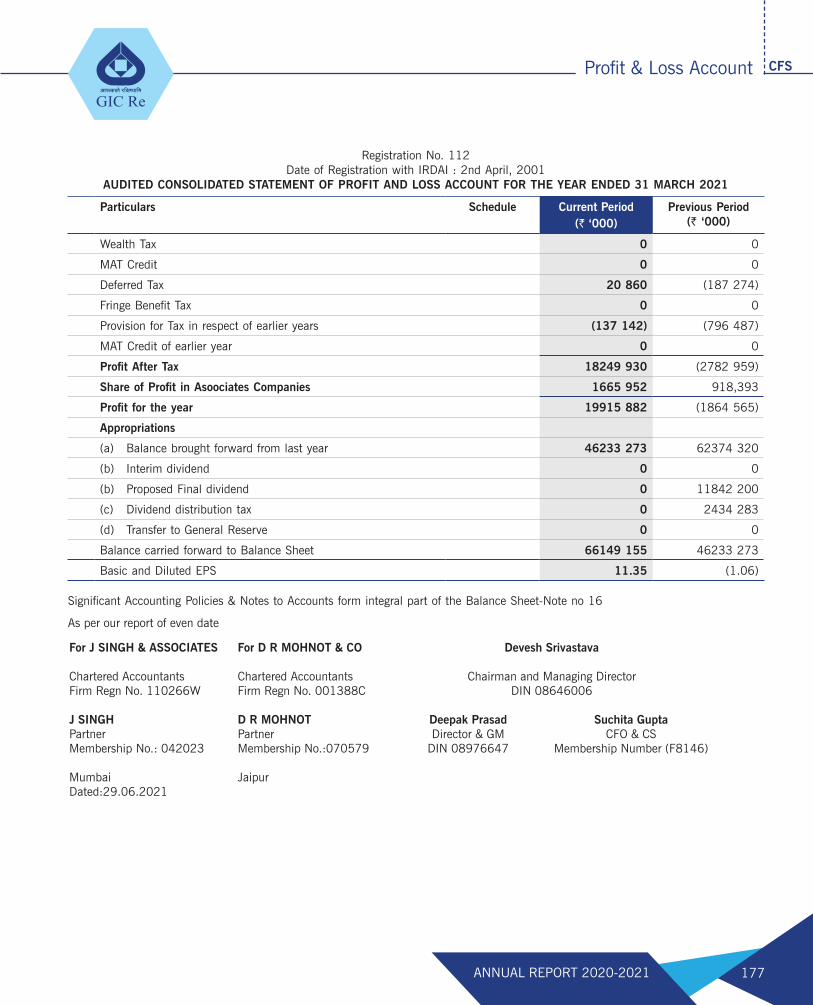

Profit & Loss Account ......................................................................................................... 92

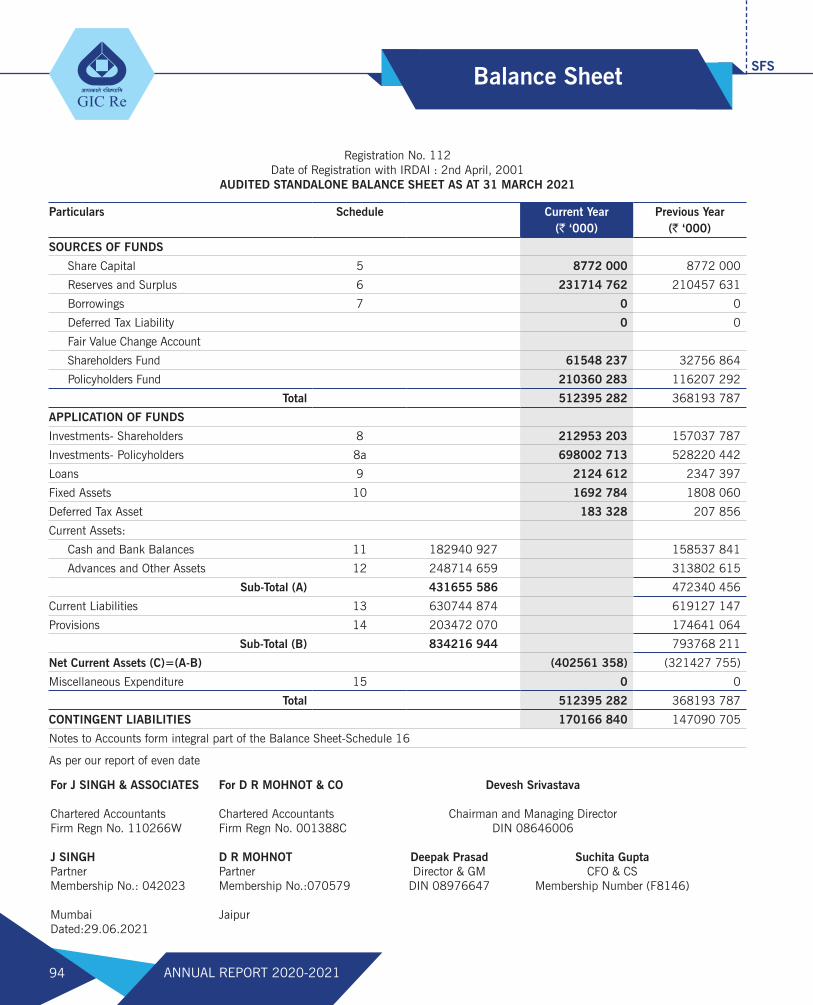

Balance Sheet ................................................................................................................... 94

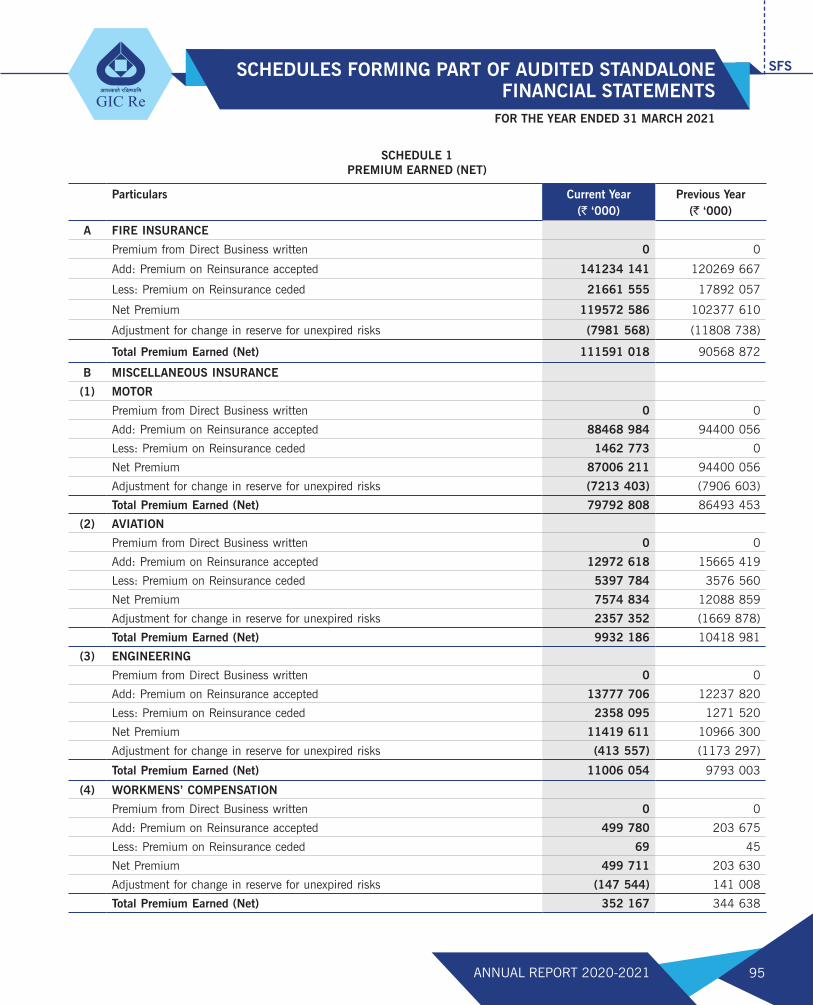

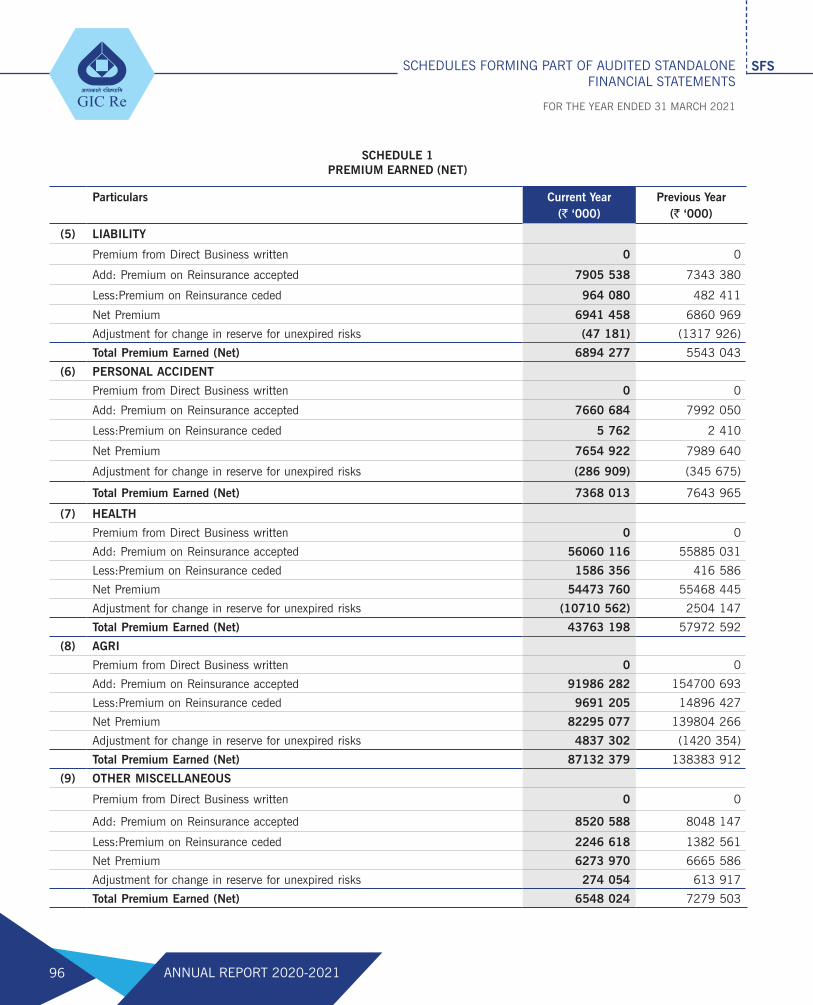

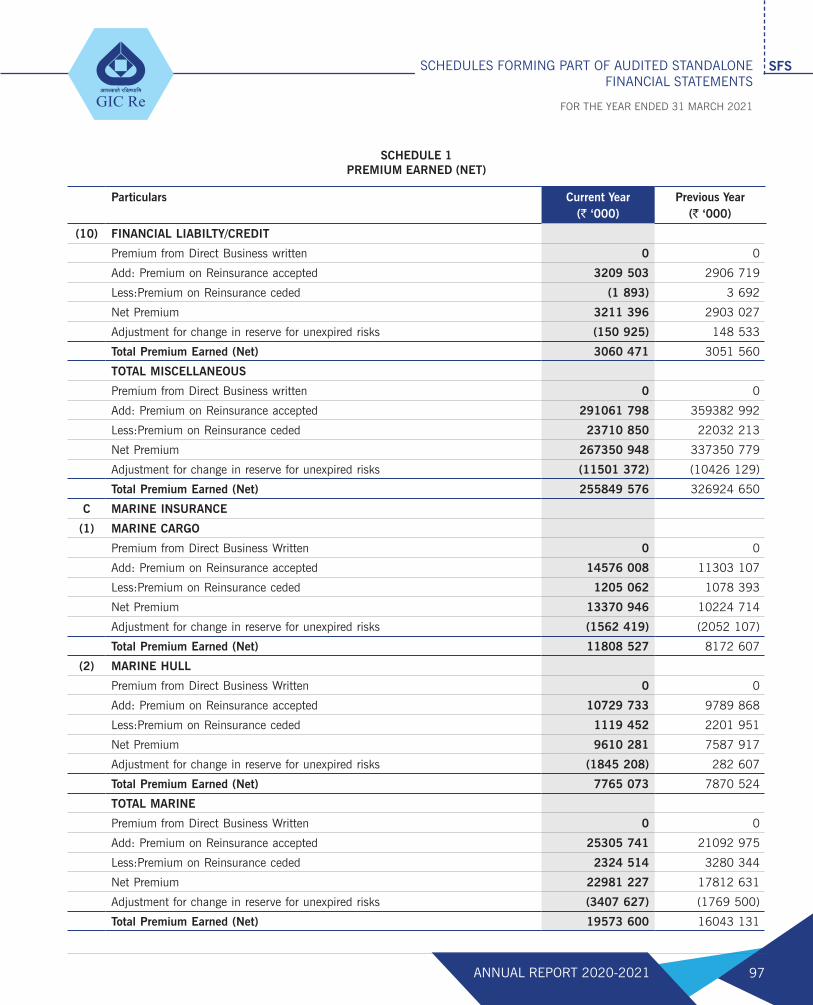

Schedules forming part of Financial Statements ..................................................................... 95

Significant Accounting Policies .............................................................................................. 120

Notes forming Part of Accounts ............................................................................................. 124

CONSOLIDATED FINANCIAL STATEMENTS

ANNUAL REPORT OF SUBSIDIARIES

Contents

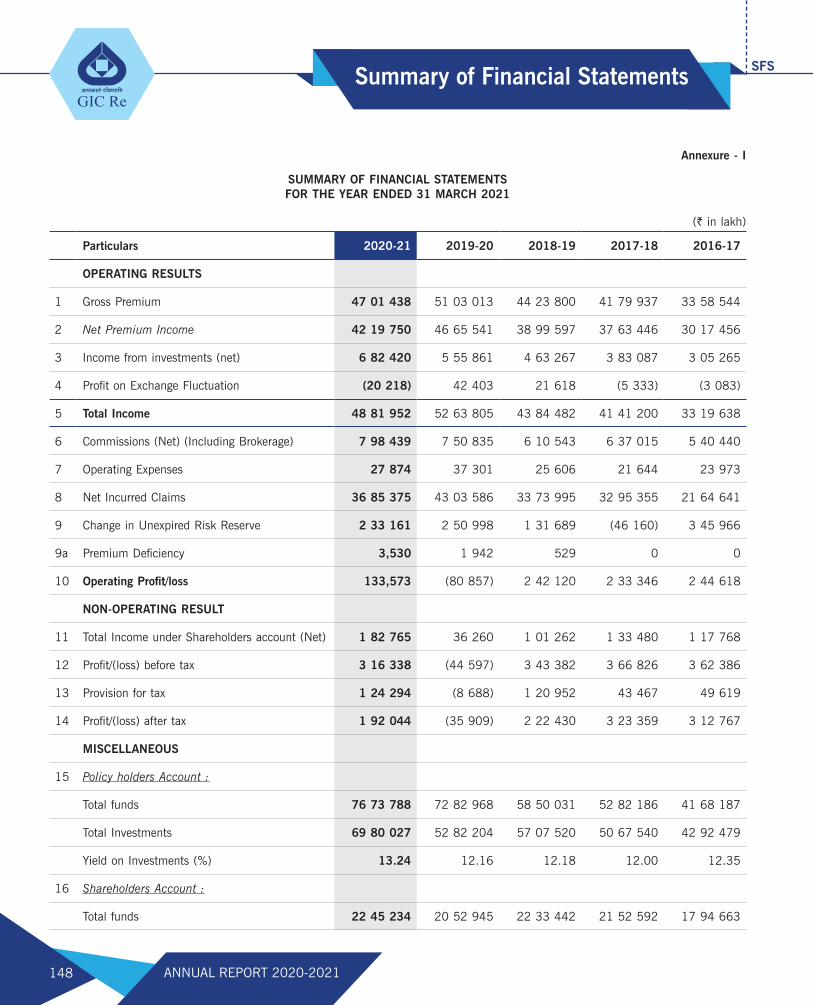

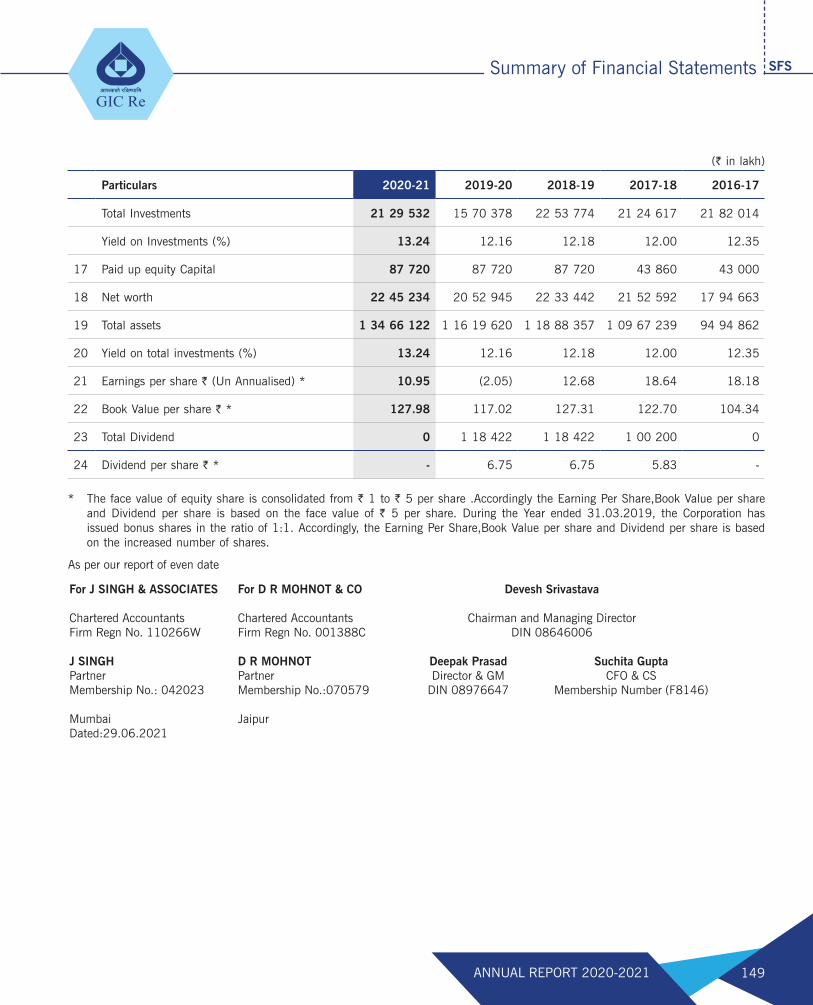

Summary of Financial Statements ......................................................................................... 148

Performance Ratio .............................................................................................................. 150

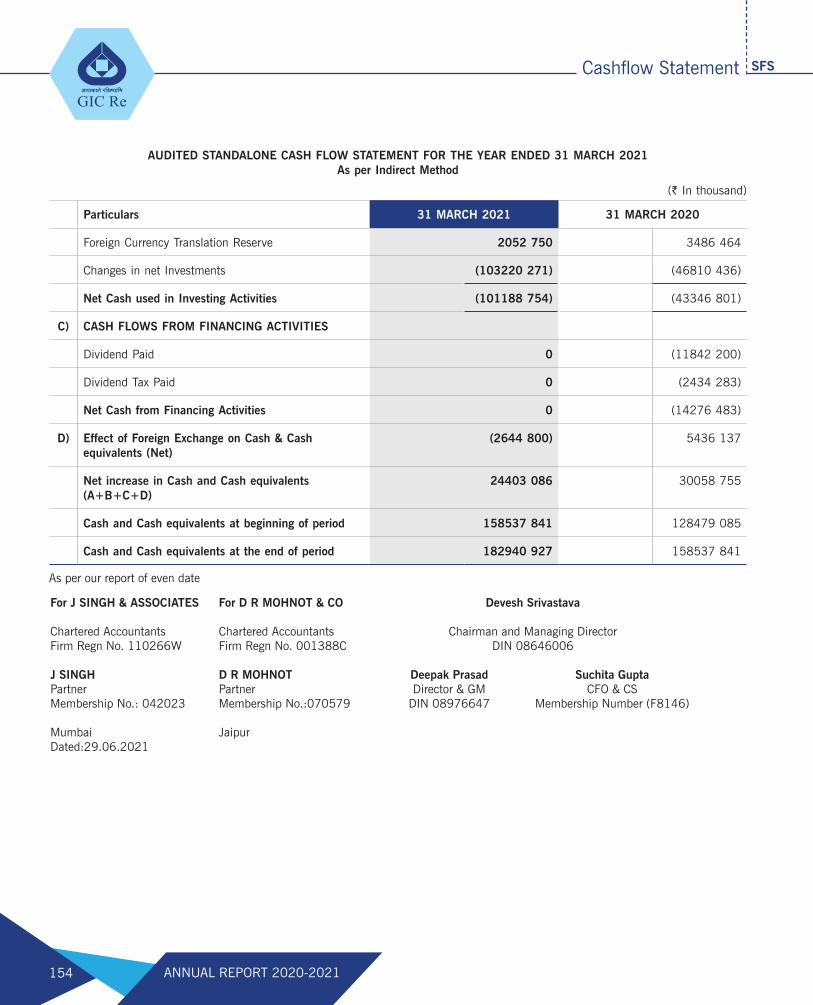

Cash Flow Statement .......................................................................................................... 153

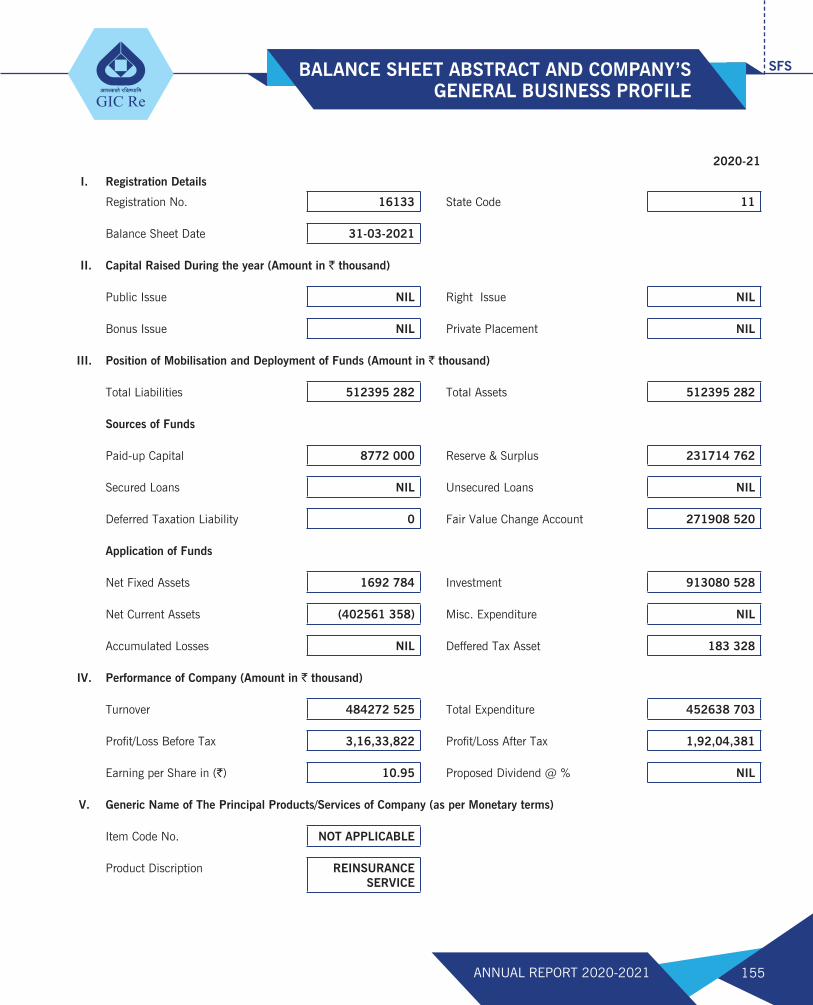

Balance Sheet Abstract and Company’s General Business Profile ............................................. 155

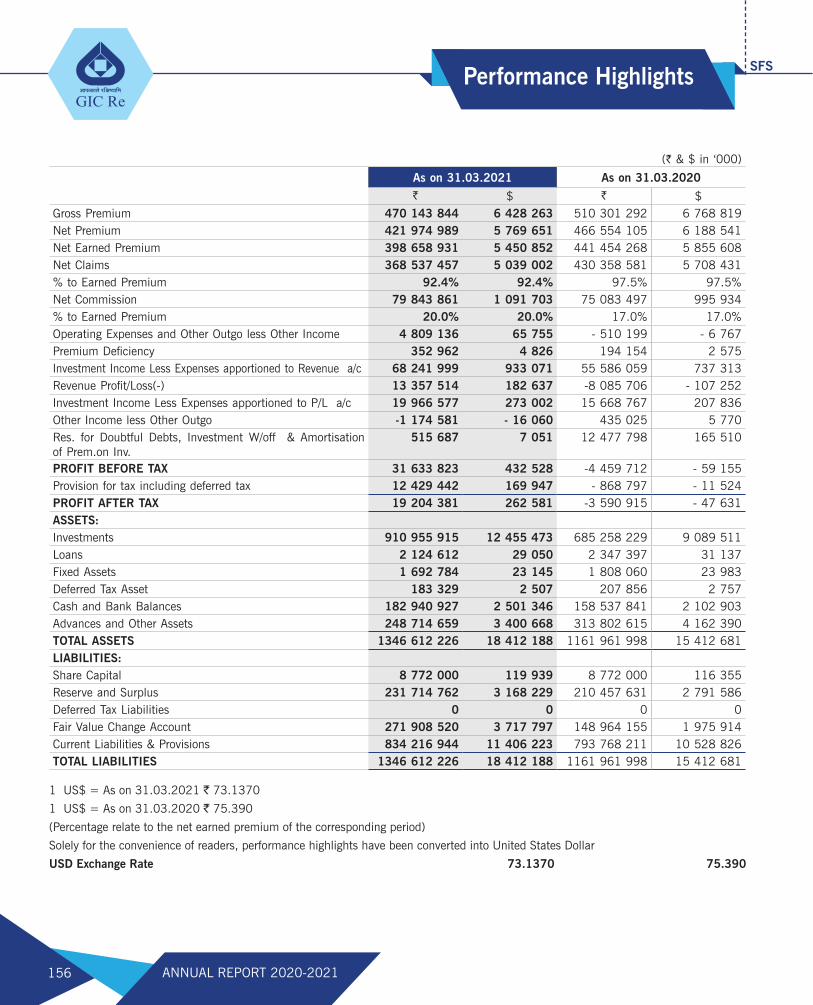

Performance Highlights ....................................................................................................... 156

Auditors’ Report ................................................................................................................. 158

Comments of the Comptroller and Auditor General of India ..................................................... 169

Revenue Account ............................................................................................................... 172

Profit & Loss Account ......................................................................................................... 176

Balance Sheet ................................................................................................................... 178

Schedules forming part of Consolidated Financial Statements .................................................. 179

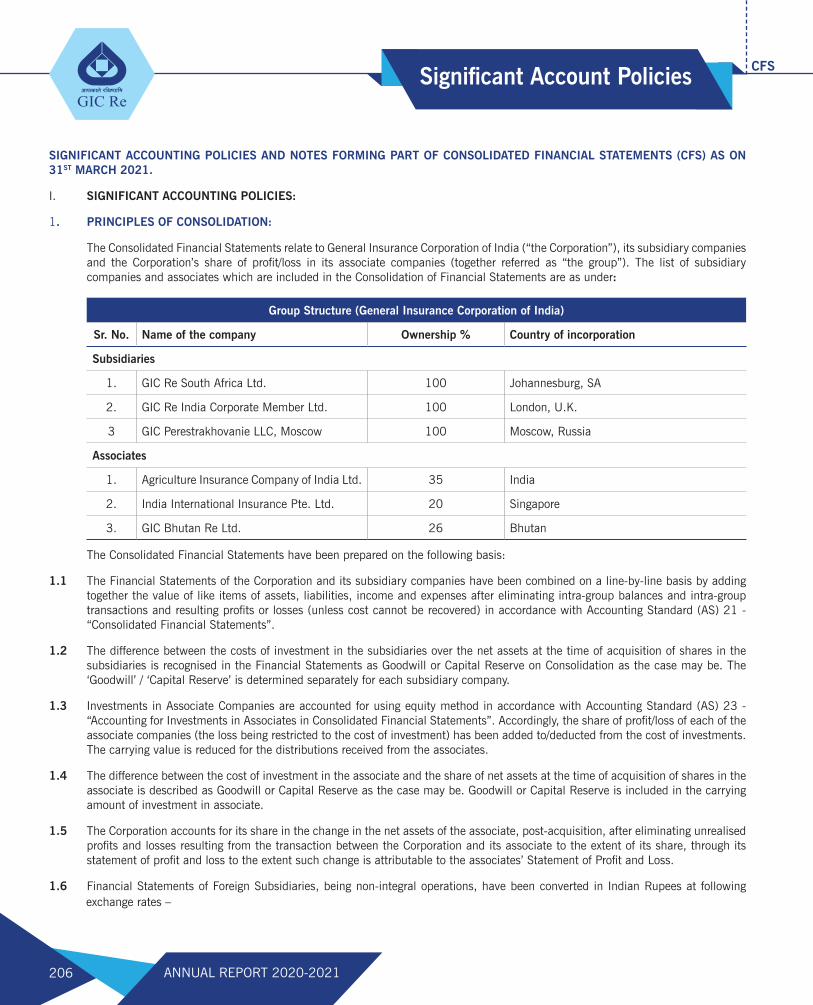

Significant Accounting Policies on Consolidated Financial Statements ....................................... 206

Notes forming Part of Consolidated Financial Statements ........................................................ 212

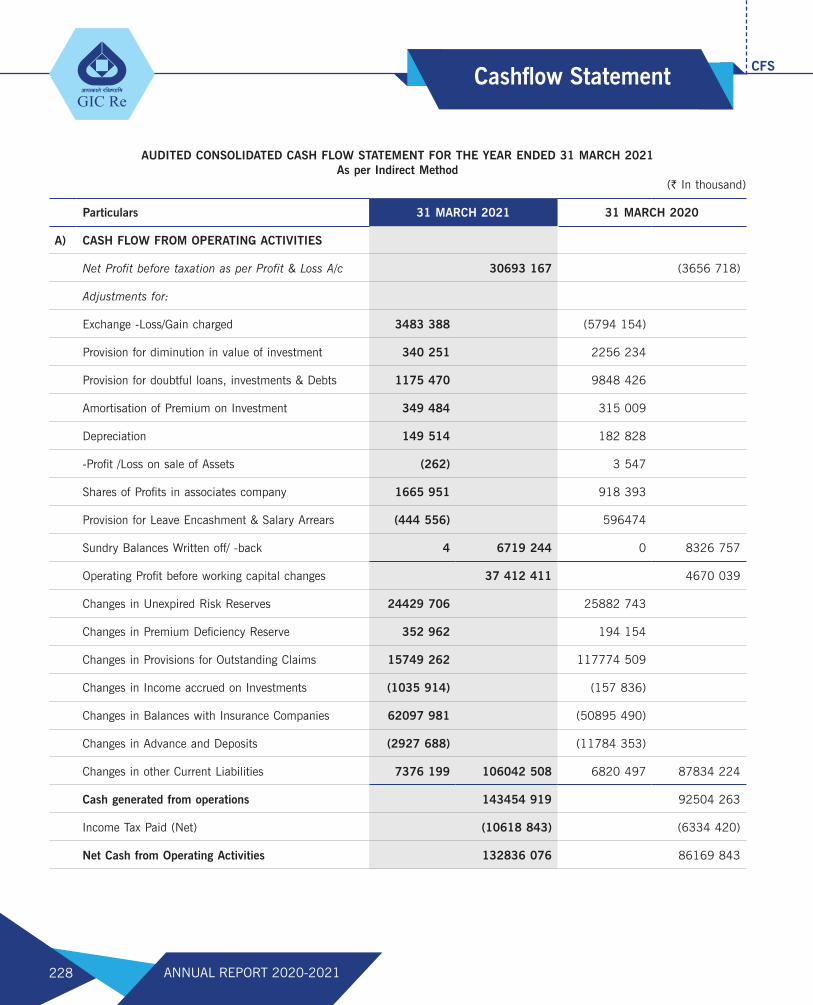

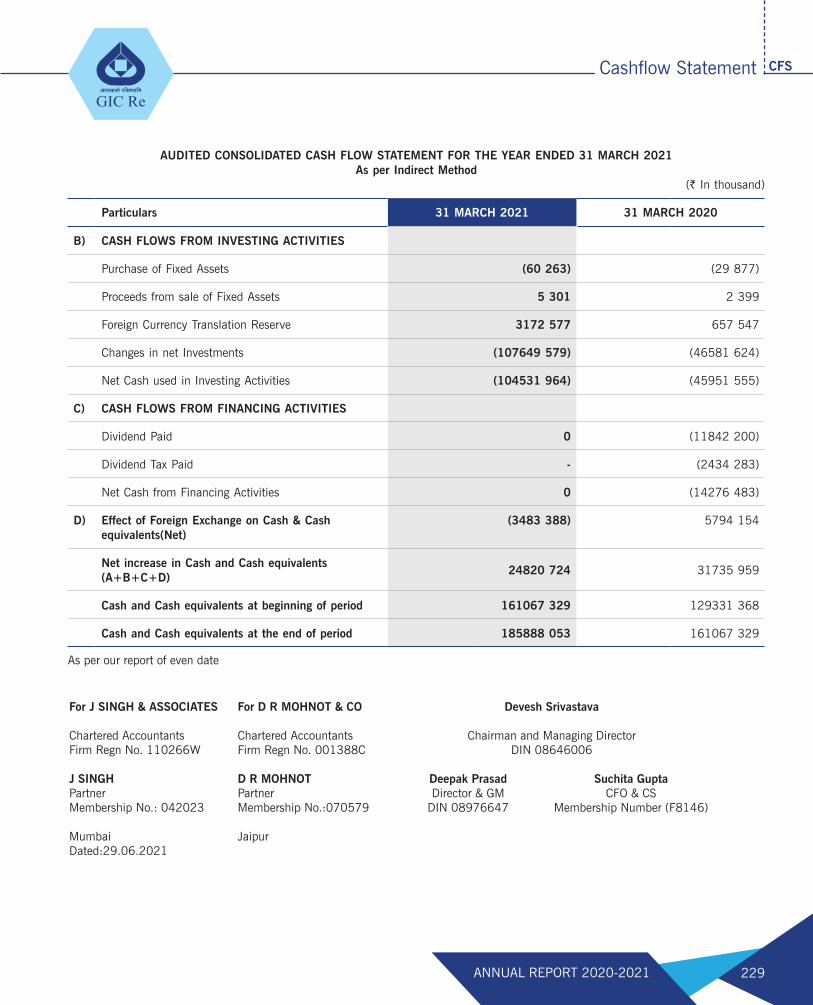

Consolidated Cash Flow Statement ...................................................................................... 228

GIC Re South Africa Ltd. ..................................................................................................... 231

GIC Re, India, Corporate Member Limited ............................................................................. 277

GIC Re Perestrakhovanie LLC ............................................................................................... 311

Notice of Annual General Meeting ........................................................................................ 371

Glossary ............................................................................................................................ 381

4 ANNUAL REPORT 2020-2021

Chairman’s Message

Dear Shareholders,

I have great pleasure in welcoming you to the 49th Annual General Meeting of your Company.

I am addressing you all at a time when the nation has valiantly emerged from the second wave of Corona virus. Having made good progress on vaccination, the general expectation is now towards very muted third wave, if at all it strikes. There is good news on the economic front in terms of recovery from the shrinkage of economic output of last year which bore the full impact of the pandemic.

Your company is now entering the golden jubilee year, half a century of its existence. This is also time when the Corporation has witnessed a full circle from being at the core of nationalization to opening up and now a reasonable balance between public and private sector market participation.

The business model, hitherto characterized by underwriting losses getting cross-subsidised by investment income is changing to underwriting profitability, will dictate goals, as the market further

matures. Indian economy will continue to be an important part of the Asian economic growth engine and its knock-on effect on insurance will be experienced by the industry. Insurance under-penetration of the Indian market will certainly provide the tailwinds.

Macro-economic and Industry overview

India’s real gross domestic product (GDP) at current prices stood at ` 135.13 lakh crore in FY 2020-21, as per the provisional estimates of annual national income for 2020-21.

Health and fire insurance segments witnessed decent growth while the motor was impacted due to the nationwide lockdown. The growth in fire segment can be attributed to upward revision in the premium rates while growing demand for health covers on the back of Covid-19 pandemic boosted the health segment.

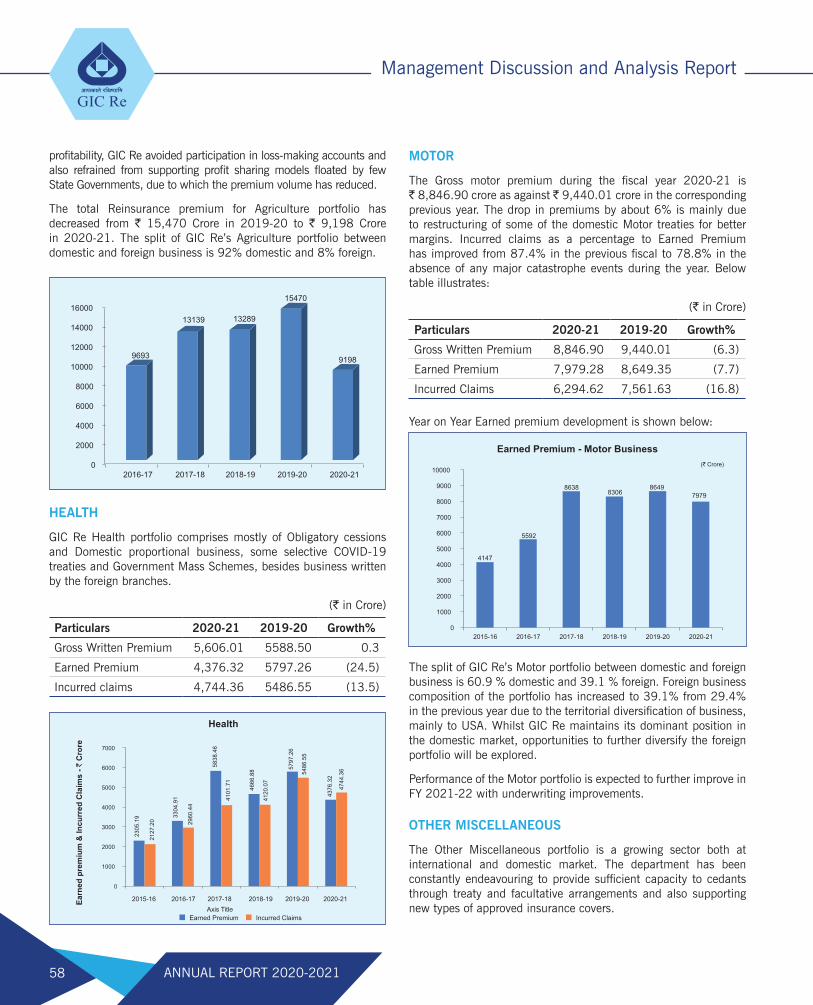

On the domestic front, GIC Re has been prudently participating in the Indian Agriculture insurance industry with implementation of the Pradhan Mantri Fasal Bima Yojana scheme (PMFBY) in 2016. PMFBY scheme is a yield index-based product and Restructured Weather Based Crop Insurance product is a weather index product. GIC Re has been cautiously underwriting both domestic and foreign business with a keen interest to increase the premium volume while simultaneously controlling the combined ratio.

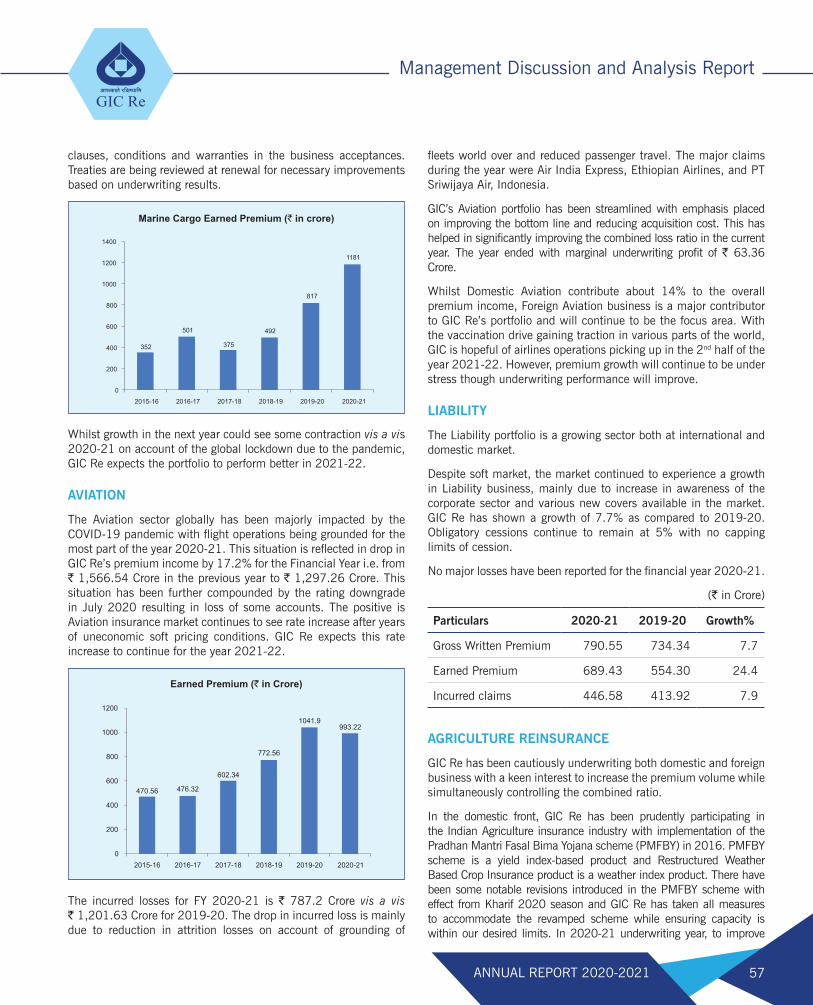

The Aviation sector globally has been majorly impacted by the COVID-19 pandemic with flight operations being grounded for the most part of the year 2020-21. This situation is reflected in drop of GIC Re’s premium income by 17.2% for the Financial Year.

The climate change is still posing a serious concern for most of the insurers. Amid the second wave of the COVID-19 pandemic, India witnessed some cyclones like Tauktae, Yaas, Amphan and Nisarga, leaving behind a trail of destruction across several Indian states.

Economy activity picked up from the fourth quarter of the financial year on the back of robust fiscal and monetary stimulus, mega vaccination drive and low inflation. During the year stock market indices reflected continuous increase from their historic low levels of March 2020 and the interest rates remained subdued.

Economic growth picked up during the year and the global GDP surpassed its pre-pandemic level mainly aided by strong policy support and ongoing vaccine deployments leading to resumption of economic activities, especially in the service sectors. As per the OECD Economic Outlook, the Organization for Economic Co-operation and Development projected that the Global GDP would grow by 5.7% in 2021 and 4.5% in 2022. The recent moderation in some countries due to the impact of delta variant and supply side constraints are expected to unwind over time and lead to faster recoveries in 2022.

Devesh SrivastavaChairman and Managing Director

5ANNUAL REPORT 2020-2021

Chairman’s Message

Financial performance

The gross direct premium underwritten by non-life insurance companies in India increased by 5.2% to ` 1.99 Lakh Crore in FY 2020-21 compared to ` 1.89 Lakh Crore in FY 2019-20.

Your company has booked Gross premium during Financial Year 2020-21 of ` 47,014.38 Crore. The underwriting loss for the Financial Year was ` 5,488.45 Crore as against ` 6,367.18 Crore in the previous year. Profit before tax for the Financial Year was ` 3,163.38 Crore (as against Loss before tax of ` 447.97). Your company reported a Profit after Tax of ` 1,920.44 Crore for the Financial Year as against Loss after Tax of ` 359.09 Crore during the previous year.

I am pleased to inform that the investment performance of your company during Financial Year 2020-21 has been very strong with the book value of Investments growing by 17% to ` 68,798.54 Crore while the Fair Value of Investments Assets increasing by 30% to ` 95,989.39 Crore over the previous year. Income from investment (including Profit on Sale of investments) during the year was ` 8,820.86 Crore registering a growth of 23.8% over the previous year. The yield on average level of investments improved from 12.16% in the last financial year to 13.24% in 2020-21.

The company has been working towards underwriting profitability and has taken major steps in this regard for some segments in the domestic property class through adoption of Insurance Information Bureau published burn costs. Alongside, we did major rebalancing of our risk portfolio by streamlining our Agri book. We are also upgrading our risk assessment processes towards this goal of underwriting profitability.

GIC Re continued to maintain its leadership in the domestic market which contributed 64% of the premium income for Financial Year 2020-21. Your company has a Net worth (including fair value of investments) of 49,643.19 Crore and total assets 134,661.22 Crore, while the Solvency ratio increased to 1.74 as at 31.03.2021 from 1.53 as at 31.03.2020.

A.M. Best in their August 2021 report has maintained its “stable” outlook for the global reinsurance on the back of positive pricing momentum along with market discipline. However, there remains risks associated with property catastrophe events, uncertainty around coronavirus-related losses, low interest rates and shrinking reserve release. The market hardening is likely to continue in the foreseeable future and take care of the lower investment income on the back of falling reinvestment rates.

Future Outlook

The Indian Insurance industry is expected to achieve high single digit growth despite hiccups due to the ongoing Covid-19 pandemic which has affected consumer sentiment. With the second Covid

wave behind us and economic recovery back on track, insurance industry can be expected to recover in tandem.

The market will continue to be led by Health, Motor and Agri classes of business. Owing to greater awareness and risk aversion together with significant medical costs, health segment, particularly retail segment can be expected to grow well in the medium term.

The life and health insurance have grown significantly during Corona pandemic and brings about a major shift in the perception among consumers and in the delivery modes by insurance providers. Technology has also driven shift on the back of ongoing pandemic, with innovative product offerings and rise in demand for standardized product will aid future growth of the industry.

GIC Re, having had phenomenal growth during last few years, is in a consolidation mode as reflected in rebalancing the risk portfolio for agriculture insurance. The continued and enhanced focus on the bottom line is expected to bear fruit after a lag, given the very nature of the reinsurance operations.

Last few years have put stress on underwriting performance of the reinsurance industry owing to record level of catastrophe activities and Covid-19 pandemic and current hardening of rates can be expected to continue in the near term.

In India, the equity market made a sharp V-shaped recovery. India remained a preferred investment destination in FY 2021-22 with foreign investments pouring into equity markets and augured well for quicker recovery in emerging economies.

As the market conditions gradually improve, reinsurers with financial strength and reputation can leverage their market position to take advantage of growing markets.

The future of the Indian Insurance Industry is bright. Demographic factors such as young insurable population, growing middle class, and growing awareness of the need for protection and retirement planning will support the growth of insurance sector in India.

I assure you that your company has been fully geared up to support the Indian and World insurance industry and would continue to focus on achieving underwriting surplus in the nearest future. Profitable diversified growth will be our focus in the coming years.

I take this opportunity to thank all stakeholders, Board members, customers, intermediaries and colleagues for their continued support and co-operation during the year.

Devesh SrivastavaChairman and Managing Director

6 ANNUAL REPORT 2020-2021

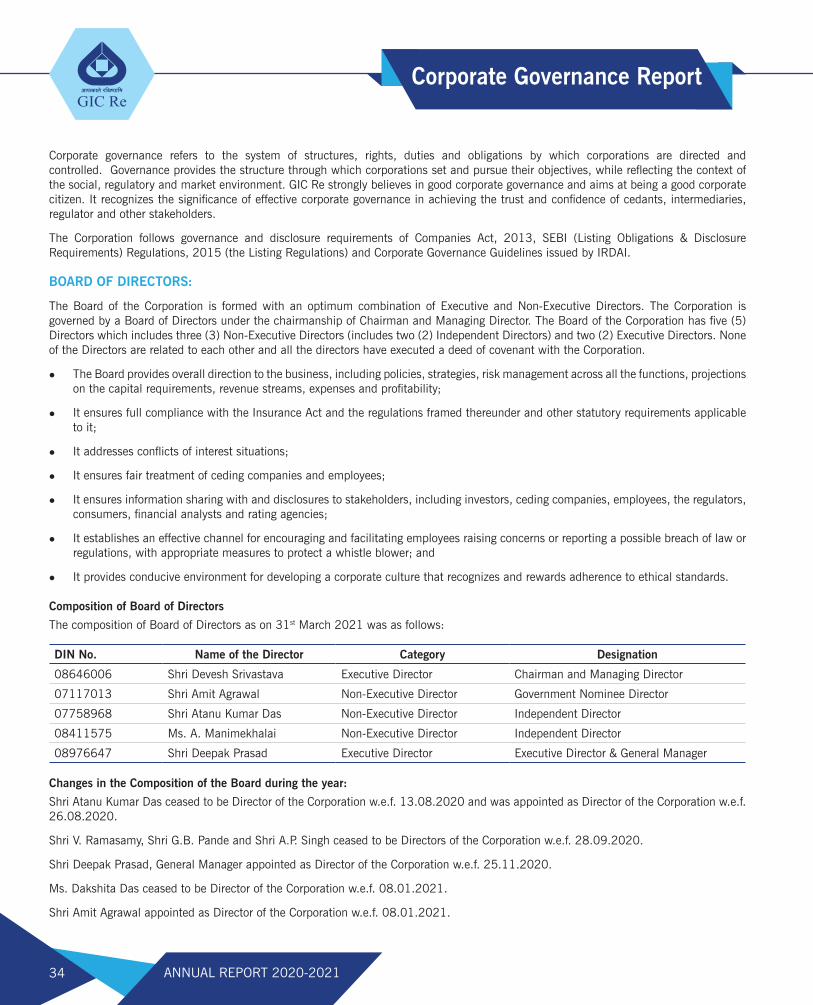

Corporate Information

DIRECTORS Shri Devesh Srivastava Chairman and Managing Director Shri Amit Agrawal W.e.f. 08.01.2021 Ms. Dakshita Das Upto 08.01.2021 Shri Atanu Kumar Das Ms. A. Manimekhalai Shri V. Ramasamy Upto 28.09.2020 Shri Amarendra Pratap Singh Upto 28.09.2020 Shri G. B. Pande Upto 28.09.2020 Shri Deepak Prasad W.e.f. 25.11.2020 and upto 31.07.2021

MANAGEMENTChairman and Managing Director Shri Devesh Srivastava

Director & General Manager Shri Deepak Prasad W.e.f. 25.11.2020 and upto 31.07.2021

General Managers Smt. Reena Bhatnagar Upto 30.06.2020 Shri Deepak Prasad Appointed as Director w.e.f. 25.11.2020 Smt. Madhulika Bhaskar Shri Deepak Godbole Upto 07.07.2019 (Deputation to Insurance Institute of India) Shri S. N. More Upto 31.12.2020 Smt. Suchita Gupta Upto 02.08.2021 (Transferred to National Insurance Co. Ltd.) Shri Satyajit Tripathy Upto 06.08.2021 (Transferred to New India Assurance Co. Ltd.) Shri Ramaswamy Narayanan (Proforma promotion) (Deputation to London) Smt. Girija Subramanian W.e.f. 27.07.2020 Smt. Jayashree Ranade W.e.f. 28.06.2021 Shri Hitesh Joshi W.e.f. 28.06.2021

Chief Vigilance Officer Shri B. Padhi W.e.f. 28.06.2019

Appointed Actuary (Non-Life) Shri Sateesh Bhat

Appointed Actuary (Life) Shri Vikash Kumar Sharma W.e.f. 24.07.2020

Deputy General Managers Shri Charles G. Ashirvatham Upto 31.05.2020 Ms. Blessy Sequeira Upto 31.07.2021 Shri Uttam Kumar Sharma Upto 30.06.2021 Shri Rajesh Pawar Shri Paul Lobo Shri Rajesh Khadatare Shri Balaji Thiagrajan Shri G. Radhakrishna Smt. Sarita Kunder Shri S. K. Rath Shri Savio Fernandes Shri Nago Bhima Sonawane W.e.f. 24.08.2020 Smt. Jayashri Balkrishna W.e.f. 24.08.2020 Smt. Chandra Iyer W.e.f. 24.08.2020 Shri V. Balkrishna W.e.f. 24.08.2020 Shri Sachindra Salvi W.e.f. 12.07.2021 Smt Modha Poojary W.e.f. 12.07.2021 Shri Sandip Karmarkar W.e.f. 12.07.2021

7ANNUAL REPORT 2020-2021

Corporate Information

Company Secretary Shri Satheesh Kumar W.e.f. 01.07.2021 Smt. Suchita Gupta Upto 01.07.2021

Statutory Auditors M/s. J. Singh & Associates M/s. D. R Mohnot & Co. Chartered Accountants Chartered Accountants 505/506/507 Hubtown, Head Office: C-35A, Nakshtra Pride, Viva Shankar wadi, Lajpat Marg, C-Scheme, Jaipur Western Express Highway Branch Office: 606, Janki Centre, Between Andheri & Jogeshwari (E) Shah Industrial Estate, Off Veera Desai Road, Mumbai – 400 060 Andheri (W), Mumbai - 400 053

Secretarial Auditor M/s. S. N. Ananthasubramanian & Co. Company Secretaries 10/26, Brindaban Thane - 400 601

Registrar & Transfer Agent KFin Technologies Pvt. Ltd. ‘Karvy Selenium’, Tower B, Plot No 31 & 32, Financial District, Nanakramguda, Gachibowli, Hyderabad - 500 032 Tel. No.: (040) 6716 2222/3321 1000 E-mail: [email protected] Website: www.kfintech.com

Stock Exchanges BSE Ltd. National Stock Exchange of India Ltd. P. J. Towers, Dalal Street Exchange Plaza, C-1, Block G, Mumbai - 400 001 Bandra Kurla Complex, Bandra (E), Mumbai - 400 051Banker Bank of India Ground Floor, Eros Theatre Building, Jamshedji Tata Road, Churchgate, Mumbai - 400 020

Registered Office ‘‘Suraksha’’, 170, J. T. Road, Churchgate, Mumbai - 400 020 (India) Tel.: +91 22 2286 7000 Email : [email protected] Website: www.gicofindia.com

CIN L67200MH1972GOI016133

IRDAI Registration No. 112

8 ANNUAL REPORT 2020-2021

Corporate Chronicle

Sr.No. Date and Year Event

1 22nd November 1972 General Insurance Corporation of India was formed in the pursuance of section 9(1) of GIBNA Act and also under the Companies Act, 1956 as Private Company limited by Shares

2 1st January 1973 The general insurance business in India was nationalized, 107 general insurance companies was merged and GIC of India was formed as the holding Company with four subsidiaries viz, The New India Assurance Co. Ltd., National Insurance Co. Ltd., Oriental Insurance Co. Ltd. and United India Insurance Co. Ltd.

3 1st January 1978 Loss Prevention Association of India was formed by GIC of India and its 4 subsidiaries

4 6th December 1978 Kenindia Assurance Company Ltd. was incorporated by merging branch operations of subsidiaries of GIC and LIC operating in Kenya

5 1st January 1988 India International Insurance Pte. Ltd. was set up as a locally incorporated wholly owned subsidiary Company of GIC and four Public Sector Insurance Companies in Singapore

6 12th December 1989 GIC Housing Finance Co. Ltd was set up by GIC of India and the four Public Sector Insurance Companies

7 25th May 1993 GIC Asset Management Co. Ltd was set up by GIC of India and the four Public Sector Insurance Companies

8 19th April 2000 Insurance Regulatory & Development Authority (IRDA) was formed

9 3rd November 2000 GIC notified as “Indian Reinsurer”

10 June 2001 London representative office set up

11 April 2002 Moscow representative office set up

12 20th December 2002 Agricultural Insurance Company of India was set up by GIC Re, the 4 PSU Companies and NABARD

13 April 2003 Life Reinsurance started its Underwriting activities

14 1st April 2002 GIC Re appointed as managers to the Terrorism Insurance Pool

15 7th August 2002 GIBNA Act Amended

16 21st March 2003 GIC Re ceased to be holding Company

17 April 2005 Dubai representative office set up

18 February 2006 SAP went live

19 27th April 2006 Loss Prevention Association of India was amalgamated with GIC Re

20 1st January 2007 Dubai representative office was upgraded to a Branch office

21 1st April 2007 GIC Re was appointed as managers to Motor Third Party Pool

22 1st January 2008 London representative office was upgraded to branch office and commenced its operations

9ANNUAL REPORT 2020-2021

Corporate Chronicle

Sr.No. Date and Year Event

23 19th June 2008 Signing of Co-operation Agreement with Hannover Re for Life Re Business

24 10th October 2008 Retakaful Reinsurance

25 16th October 2008 GIC Re mandated to form Nat Cat Pool for Afro Asian Region

26 16th January 2009 GIC Re registered as Eventual Reinsurer in Brazil

27 11th November 2010 GIC Re Malaysia Branch start functioning

28 20th September 2011 Launch of e-Thru platform by Mr. J. Harinarayan, Chairman, IRDA

29 19th October 2011 GIC Re won the Marine Insurance Award at Seatrade Middle East and Indian Subcontinent Awards 2011

30 5th July 2012 GIC Re entered into a joint venture agreement for setting up the 1st Reinsurance Company in Bhutan

31 26th November 2012 GIC Re won the Marine Insurance Award second time in a row, at Seatrade Middle East and Indian Subcontinent Awards 2012

32 5th September 2013 The joint venture Reinsurance Company in Bhutan-GIC Bhutan Re Ltd. became operational

33 19th September 2013 GIC Re appointed as Managers of FAIR NATCAT Reinsurance Pool at Beijing, China

34 11th August 2014 GIC Re South Africa Ltd., the Wholly owned subsidiary of GIC Re in South Africa established

35 12th June 2015 India Nuclear Insurance Pool launched

36 29th January 2016 GIC Re, India, Corporate Member Limited, the Wholly owned subsidiary of GIC Re in UK established

37 4th February 2016 GIC Re converted into ‘Public Limited Company’

38 21st April 2017 GIC Re opened IFSC Insurance office in GIFT City

39 25th October 2017 GIC Re got listed on BSE Limited and National Stock Exchange of India Limited

40 1st April 2018 GIC Syndicate 1947

41 30th January 2020 GIC Perestrakhovanie LLC (GIC Re’s 100% subsidiary) received its reinsurance operations license from Central Bank of Russia

10 ANNUAL REPORT 2020-2021

Shri Devesh Srivastava

Shri Amit Agrawal

Chairman and Managing Director (DIN: 08646006)

Additional Secretary, Department of Financial Services, Ministry of Finance (DIN: 07117013)

Shri Devesh Srivastava has been involved in the insurance sector since 1987 following his joining the industry as a direct recruit. He has experience in both direct insurance and reinsurance. He has gained international exposure through postings to the company’s London branch where he was overseeing operations in UK, Europe, Caribbean countries of Brazil, Argentina, and Mexico territories. He was a key player in the setting up of GIC Re’s Lloyds Syndicate 1947 in London. He is presently employed on a full-time basis by the Company in the capacity of Chairman and Managing Director.

Shri Devesh Srivastava holds a B.Sc (Hons) and a Master of Science degree from St Stephen’s College, Delhi. He subsequently obtained a post-graduate degree in Management, majoring in Marketing with a Gold Medal from the Management Development Institute (MDI) Gurgaon.

Shri Srivastava is presently on the Boards of GIC Re South Africa Ltd.- Johannesburg, GIC Perestrakhovanie LLC - Russia, Export & Credit Guarantee Corporation, Indian Register of Shipping, Kenindia Assurance Co. Ltd. - Nairobi, Agriculture Insurance Corporation of India, Health TPA Ltd., Asian Reinsurance Corporation, GIC Housing Finance Ltd. and GIC Re Corporate Member, London.

Shri Amit Agrawal is a member of the Indian Administrative Service since 1993. Since 2016, he has served in the Ministry of Finance, Department of Financial Services, currently as Additional Secretary to the Government of India and earlier as Joint Secretary. He is also serving as Director on the Boards of Bank of Baroda, General Insurance Corporation of India and United India Insurance Company Limited, and as Part-time Member on the Insurance Regulatory and Development Authority of India and Member on the Council of the Institute of Actuaries of India.

An alumnus of Indian Institute of Technology Kanpur, he has previously served in top positions in the Government of India and the State Governments of Chhattisgarh and Madhya Pradesh, broadly in the areas of finance, technology and technical education.

His earlier charges include that of Director in the Prime Minister’s Office; Adviser and Director in the Office of Prime Minister’s Economic Advisory Council; Officer on Special Duty with the Chairman of the National Innovation Council; Head of various State Government departments and agencies; and head of district administration and local government institutions. He has earlier served on the Boards of 16 companies, including Indian Bank and ICICI Bank.

Board of Directors

11ANNUAL REPORT 2020-2021

Shri Atanu Kumar Das

Ms. A. Manimekhalai

Managing Director & CEO, Bank of India (DIN: 07758968)

Executive Director, Canara Bank (DIN: 08411575)

Atanu Kumar Das is an Independent Director of our Corporation. He holds a Master’s degree of Arts in Analytical and Applied Economics from Utkal University. He has been part of several important training programs/workshops conducted at premier institutions like IIM (Kozhikode), IIM (Ahmedabad), ASCI (Hyderabad), NIBM, BTC, Frankfurt School of Business Management and IDRBT – Certification Programme in IT and Cyber Security for Board Members – Hyderabad. He has experience of working in public sector banks. Previously, he has worked at Vijaya Bank. He has taken charge as Managing Director & CEO of Bank of India w.e.f. 20.01.2020.

Ms. A. Manimekhalai is a seasoned banker having more than 3 decades of Banking Experience.

She holds Masters Degree in Business Administration (Marketing) from Bangalore University and is a Certified Associate of Indian Institute of Bankers (CAIIB).

She started her banking career in e-Vijaya Bank as an Officer in 1988 and scaled up as Branch Head, Regional Head and functional head of various Departments at Corporate Office. She was instrumental in devising & implementation of strategic policies covering core areas like strategic planning, setting organizational goals, growth strategies, action plans, compliance, internal control and various other functions.

As an Executive Director of Canara Bank, she has been overseeing various important portfolios viz., Strategic Planning, Credit & related matters, Inspection, State Level Lead Bank responsibilities and overseeing the functioning of Regional Rural Banks (4 RRBs). She played a pivotal role in the amalgamation of Canara Bank and Syndicate Bank.

Presently, she is overseeing entire Credit portfolio of the Bank, Marketing and Financial Inclusion. On a regular basis through Webinars, madam is providing required guidance for the staff members and also customers on various banking subjects viz., Webinars on Resolution Framework for MSMEs which has helped the most.

Apart from the above, she is also a member of the following committees:

l The Expert Committee constituted by NABARD to suggest the future road map of RRBs

l Working Group on Financial Inclusion & Related issues constituted by DFS, Govt. of India, Ministry of Finance

In addition to above, presently she is holding Directorships in 5 companies and providing value added inputs, necessary guidance and directions which has helped in the growth of these companies.

Board of Directors

13ANNUAL REPORT 2020-2021

Management

Shri Devesh SrivastavaChairman and Managing Director

Shri Deepak GodboleGeneral Manager

Smt Jayashree RanadeGeneral Manager

Shri Sateesh BhatAppointed Actuary (Non-Life)

Smt. Madhulika BhaskarGeneral Manager

Smt Girija SubramanianGeneral Manager

Shri B PadhiChief Vigilance Officer

Shri Ramaswamy NarayananGeneral Manager

Shri Hitesh JoshiGeneral Manager

Shri Vikash Kumar SharmaAppointed Actuary (Life)

14 ANNUAL REPORT 2020-2021

To the Members,

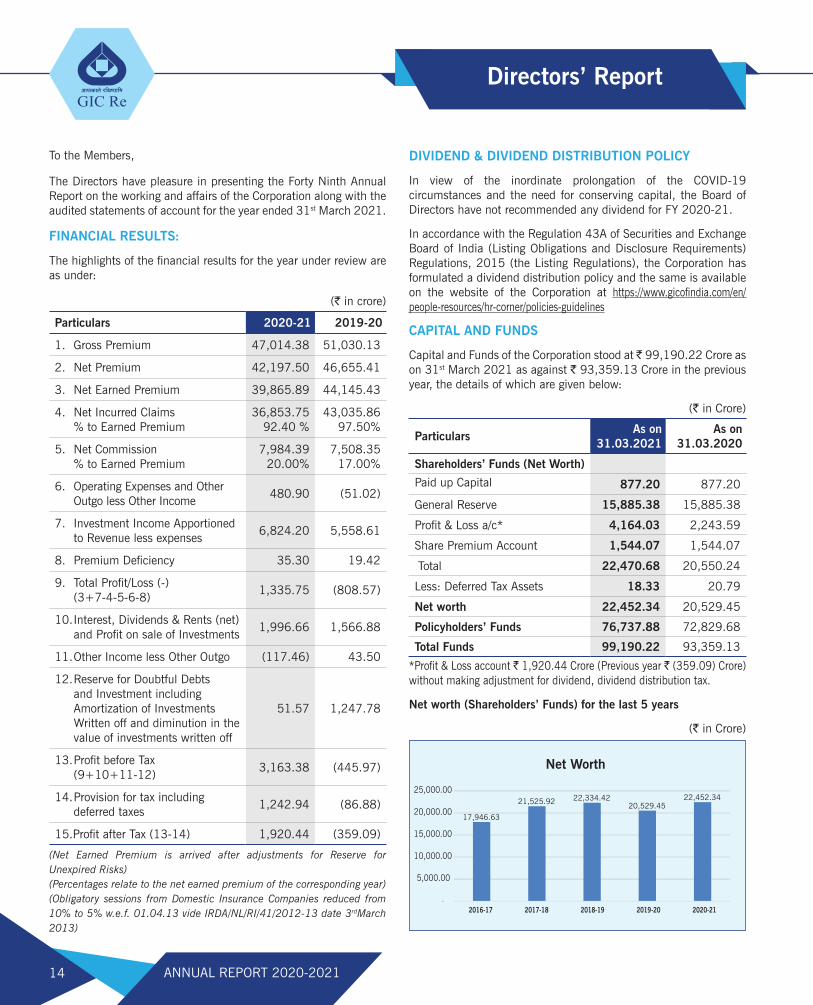

The Directors have pleasure in presenting the Forty Ninth Annual Report on the working and affairs of the Corporation along with the audited statements of account for the year ended 31st March 2021.

FINANCIAL RESULTS:

The highlights of the financial results for the year under review are as under:

(` in crore)

Particulars 2020-21 2019-20

1. Gross Premium 47,014.38 51,030.13

2. Net Premium 42,197.50 46,655.41

3. Net Earned Premium 39,865.89 44,145.43

4. Net Incurred Claims % to Earned Premium

36,853.7592.40 %

43,035.8697.50%

5. Net Commission % to Earned Premium

7,984.3920.00%

7,508.3517.00%

6. Operating Expenses and Other Outgo less Other Income

480.90 (51.02)

7. Investment Income Apportioned to Revenue less expenses

6,824.20 5,558.61

8. Premium Deficiency 35.30 19.42

9. Total Profit/Loss (-) (3+7-4-5-6-8)

1,335.75 (808.57)

10. Interest, Dividends & Rents (net) and Profit on sale of Investments

1,996.66 1,566.88

11. Other Income less Other Outgo (117.46) 43.50

12. Reserve for Doubtful Debts and Investment including Amortization of Investments Written off and diminution in the value of investments written off

51.57 1,247.78

13. Profit before Tax (9+10+11-12)

3,163.38 (445.97)

14. Provision for tax including deferred taxes

1,242.94 (86.88)

15.Profit after Tax (13-14) 1,920.44 (359.09)

(Net Earned Premium is arrived after adjustments for Reserve for Unexpired Risks)(Percentages relate to the net earned premium of the corresponding year)(Obligatory sessions from Domestic Insurance Companies reduced from 10% to 5% w.e.f. 01.04.13 vide IRDA/NL/RI/41/2012-13 date 3rdMarch 2013)

DIVIDEND & DIVIDEND DISTRIBUTION POLICY

In view of the inordinate prolongation of the COVID-19 circumstances and the need for conserving capital, the Board of Directors have not recommended any dividend for FY 2020-21.

In accordance with the Regulation 43A of Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 (the Listing Regulations), the Corporation has formulated a dividend distribution policy and the same is available on the website of the Corporation at https://www.gicofindia.com/en/people-resources/hr-corner/policies-guidelines

CAPITAL AND FUNDS

Capital and Funds of the Corporation stood at 99,190.22 Crore as on 31st March 2021 as against ` 93,359.13 Crore in the previous year, the details of which are given below:

(` in Crore)

ParticularsAs on

31.03.2021As on

31.03.2020

Shareholders’ Funds (Net Worth)

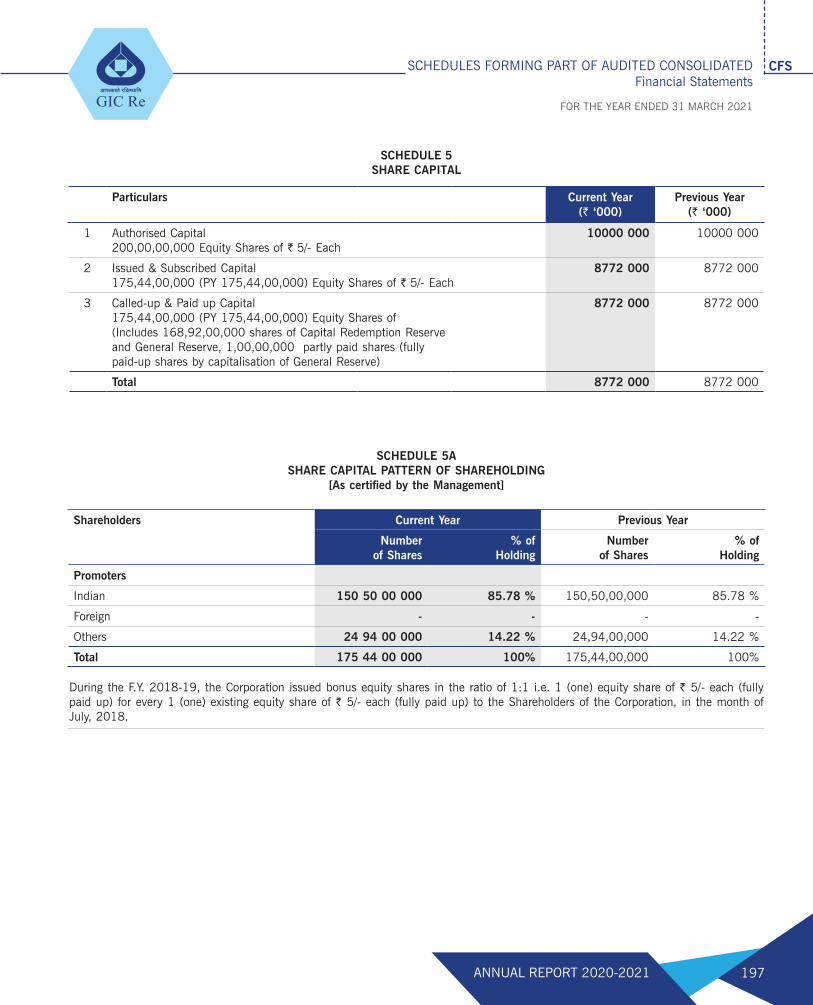

Paid up Capital 877.20 877.20

General Reserve 15,885.38 15,885.38

Profit & Loss a/c* 4,164.03 2,243.59

Share Premium Account 1,544.07 1,544.07

Total 22,470.68 20,550.24

Less: Deferred Tax Assets 18.33 20.79

Net worth 22,452.34 20,529.45

Policyholders’ Funds 76,737.88 72,829.68

Total Funds 99,190.22 93,359.13

*Profit & Loss account ` 1,920.44 Crore (Previous year ` (359.09) Crore) without making adjustment for dividend, dividend distribution tax.

Net worth (Shareholders’ Funds) for the last 5 years

(` in Crore)

17,946.63

21,525.92 22,334.42 20,529.45

22,452.34

-

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

2016-17 2017-18 2018-19 2019-20 2020-21

Net Worth

Directors’ Report

15ANNUAL REPORT 2020-2021

ASSETS

Total assets of the Corporation were ` 1,34,661.22 Crore as on 31st March 2021 as compared to ` 1,16,196.20 Crore as on 31st March 2020.

CONSOLIDATED FINANCIAL STATEMENT

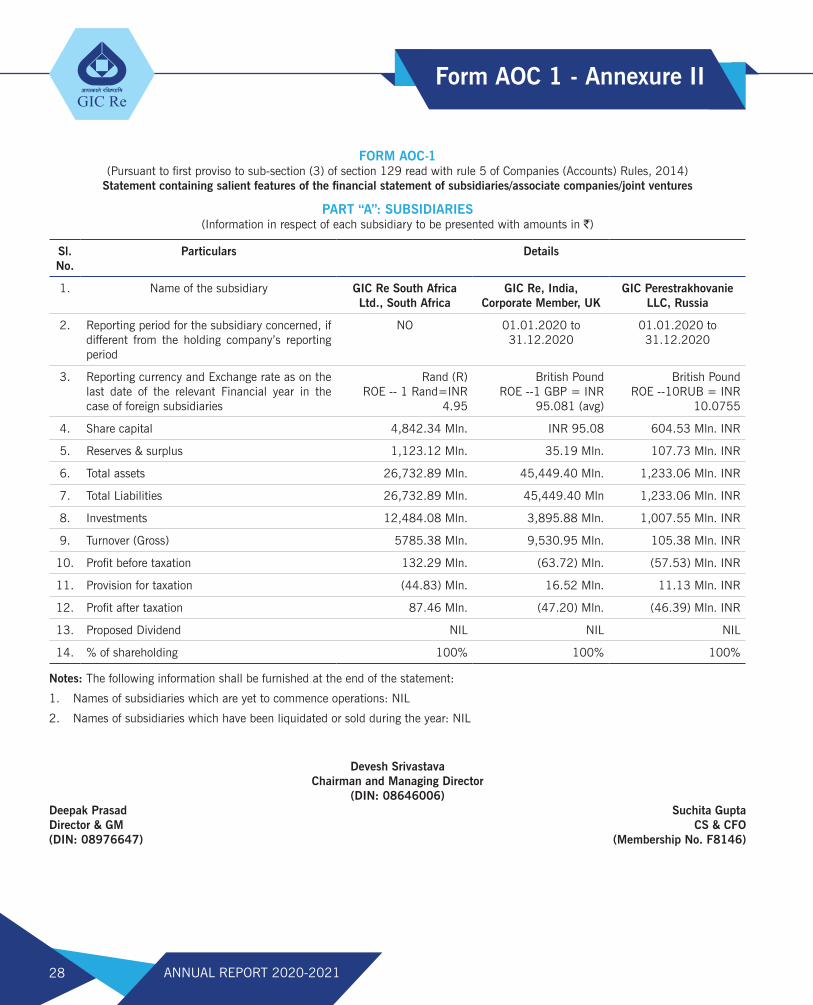

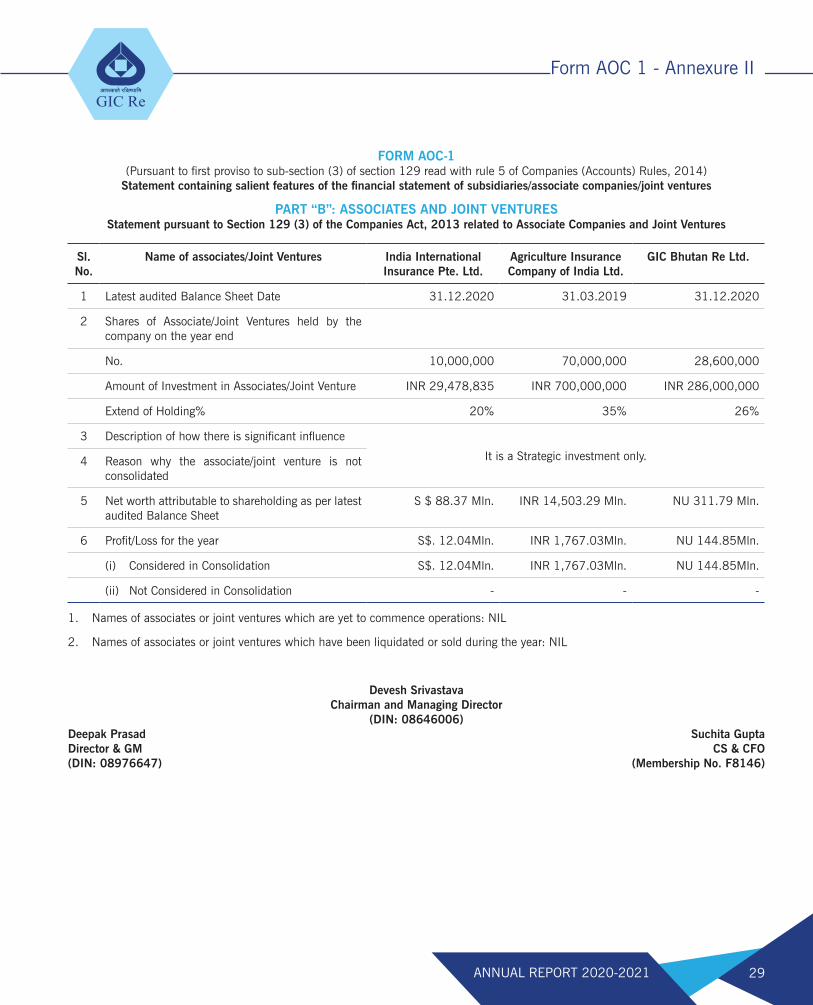

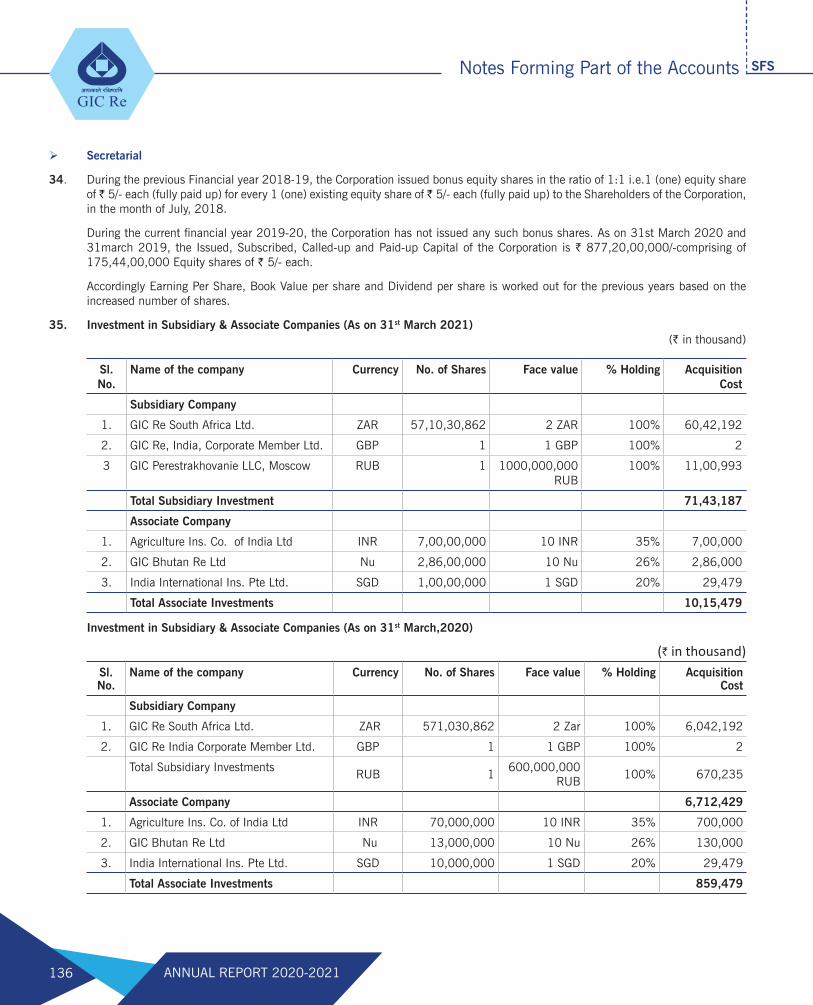

As per the provision of Section 129 (2) of the Companies Act, 2013, at every Annual General Meeting of a company, the Board of Directors of the company shall lay before such meeting financial statements for the financial year. Section 129 (3) of the Companies Act, 2013 provides that where a company has one or more subsidiaries, it shall, in addition to financial statements provided under sub-section (2) of Section 129, prepare a consolidated financial statements of the company and of all the subsidiaries in the same form and manner as that of its own which shall also be laid before the Annual General Meeting of the company along with the laying of its financial statements under sub-section (2) of Section 129.

Explanation:

The Corporation is preparing Consolidated Financial Statements as it has three subsidiaries namely GIC Re South Africa Limited, GIC Re, India, Corporate Member Limited, UK and GIC Perestrakhovanie LLC, Moscow apart from three Associate Companies namely, Agriculture Insurance Company of India Ltd. (AICIL), India International Insurance Pte. Ltd., Singapore and GIC Bhutan Re Ltd.

FINANCIAL RATING AND RANKING

Global rating agency A M Best revised the Financial Strength Rating (FSR) to B++ (Good) from A- (Excellent) and the Long-Term Issuer Credit Rating (Long-Term ICR) to “bbb+” from “a-” of the Corporation in July 2020. The outlook of the FSR has been revised to stable from negative whilst the Long-Term ICR outlook is negative. These Credit Ratings (ratings) reflect the Corporation’s balance sheet strength, which AM Best categorizes as strong, as well as its adequate operating performance, favourable business profile and appropriate enterprise risk management (ERM).

CARE Ratings Limited has issued ‘AAA (Is)’ Issuer Rating for the Corporation in December 2020 with a stable outlook. The rating reflects the Corporation’s strategic importance as the dominant Indian reinsurer with comfortable liquidity position and moderation in asset quality. Ownership by Government of India, experienced management and diversified business profile are key rating sensitivities.

During the year 2020, the Corporation was ranked 11th by Standard & Poor’s in the Top 40 Global Reinsurance Groups Ranked by Net Reinsurance Premiums Written in year 2019.

A M Best also ranked the Corporation as 12th in the Top 50 World’s Largest Reinsurance Groups based on Gross Written Premium in year 2019.

SOLVENCY RATIO

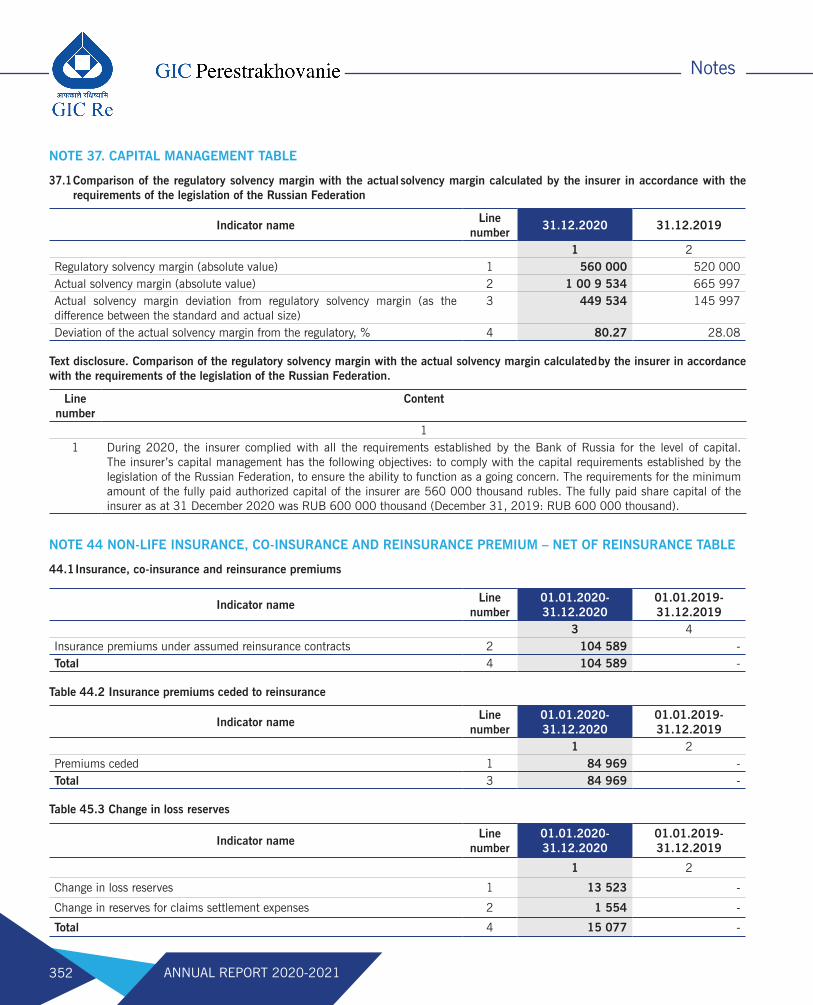

The Solvency Margin of the Corporation as on 31st March 2021 stood at 1.74 as against 1.53 in the previous year.

INVESTMENTS

The book value of the investment of the Corporation in India (representing investment, loans & deposits) amount to 68,798.54 Crore as on 31st March 2021 as against ` 58,756.58 Crore in the previous year. The Investment Income of ` 8,443.55 Crore were apportioned to Policyholders & Shareholders as under:

(` in Crore)

Particulars 2020-21 2019-20

Apportioned to Policyholders (PH) 6,531.93 5,294.62

Apportioned to Shareholders (SH) 1,911.62 1,492.48

*Ratio of PH/SH – 77.36/22.64

The mean yield on funds with profit on sale of investments stood at 13.24% (Previous year 12.16%). The percentage of net NPA (Non-Performing Assets) to Gross loan assets (including Government Securities) was NIL (Previous year 0.63%).

INSURANCE REGULATORY AND DEVELOPMENT AUTHORITY OF INDIA (IRDAI)

The Corporation being a Reinsurance Company, its working and functions, are governed by the Insurance Regulatory and Development Authority of India (IRDAI). The Corporation’s existing paid-up equity capital of ` 877.20 Crore conforms to the specifications of the IRDAI. The Accounts of the Corporation are drawn up according to the stipulations prescribed in the IRDAI (Preparation of Financial Statements and Auditor’s Report) Regulations, 2002.

IRDAI has identified the Corporation as a Domestic Systemically Important Insurer (D-SII) in July 2020 as per the framework put in place for identification & monitoring of the operations of Domestic Systemically Important Insurers.

ALTERNATE RISK TRANSFER (ART)/STRUCTURED SOLUTIONS (RETRO PROGRAMME)

IRDAI vide letter dated 25th February 2019 approved the continuation of the existing Structured Solutions Contract. Following IRDAI approval, two lines of business made cessions to the contract i.e. Aviation from 1st April 2019 on XOL basis attached to the 2018-2019 contract year and cessions in respect of Non-Marine Domestic on XOL basis from 1st June 2019 were ceded to the 2019-2020 year of contract. Thereafter no cessions were

Directors’ Report

16 ANNUAL REPORT 2020-2021

made from any class of business. The contract continues to be live in respect of certain run-off business. The Corporation and the reinsurers will maintain all contractual rights and obligations arising out of the contract and towards statutory dues, till the final closure at a mutually agreed date after both parties agree to the net balance quantum.

PARTICULARS OF LOANS, GUARANTEES OR INVESTMENTS

The provisions of Section 186(4) of the Companies Act, 2013 (the Act) requiring disclosure in the financial statements of the full particulars of the loans given, investment made or guarantee given or security provided and the purpose for which the loan or guarantee or security are proposed to be utilised by the recipient of the loan or guarantee or security are not applicable to the Corporation.

SIGNIFICANT AND MATERIAL ORDERS PASSED BY THE REGULATORS OR COURTS OR TRIBUNALS IMPACTING THE GOING CONCERN STATUS OF THE COMPANY AND ITS FUTURE OPERATIONS

There are no significant and/or material orders passed by the Regulators or Courts or Tribunals impacting the going concern status of future operations of the Corporation.

ENTERPRISE RISK MANAGEMENT (ERM)

The Corporation has in place a robust ERM policy. The policy defines a Governance structure as well as the roles and responsibilities at each level. The ERM department is headed by the Chief Risk Officer (CRO) who reports to the Board Risk Management Committee through the Chairman and Managing Director (CMD) and Management-level ERM committee.

ERM department conducts risk assessment with the assistance of the Risk and Mitigation Plan Owners (RMOs), primarily Scale V level officers, where new risks are brought for discussion and thereafter the entire risk universe is re-calibrated with the objective of prioritization for mitigation. During the exercise, RMOs also propose controls/ mitigation plans, which post deliberations are implemented. The ERM department conducts periodic review of the risk universe and checks the control effectiveness. ERM Department informs these developments and deviations to the Management and Board Risk Management Committees.

As part of its allied activities, the ERM department reviews the Business Continuity Plan (BCP) and Business Impact Assessment (BIA) which aims at providing continuity of services at a defined minimum acceptable level of critical functions, to safeguard the financial, competitive and reputational position in the short and medium term.

During the year under review, a neutral Third-Party Consultant was appointed for carrying out the Stress Test Exercise of GIC Re. The annual Stress Test Exercise was carried out for the financial Year 2020-21 based on financial data as on 31st March of 2020.

The Stress Test Exercise evaluated scenarios of significant adverse threats to the future financial condition and found it to be adequately resilient. The Stress Test Report was presented to the Board and subsequently shared with IRDAI.

The Standard Operating Procedures (SOP) is already in place for two key functions of the Corporation viz: Reinsurance and Investment and their related accounting activities and the same are modified on need basis, as per user department requests with the approval of the Corporation’s Enterprise Risk Management Committee.

An Anti-Fraud Policy framed by the Corporation which covers prevention, identification, investigation and reporting of frauds is reviewed every year. Corporation has declared ‘Zero Tolerance’ to any non-compliance to the terms and conditions of the Anti-Fraud Policy. ERM department as part of compliance files the Fraud Monitoring Returns with the Regulator.

This year was exceptional and the Corporation had to face many challenges due to outbreak of COVID-19 pandemic. By invoking Business Continuity Plan (BCP) in lockdown period, critical users along with other users were able to work from home. This led to smooth functioning of the core activities of the Corporation.

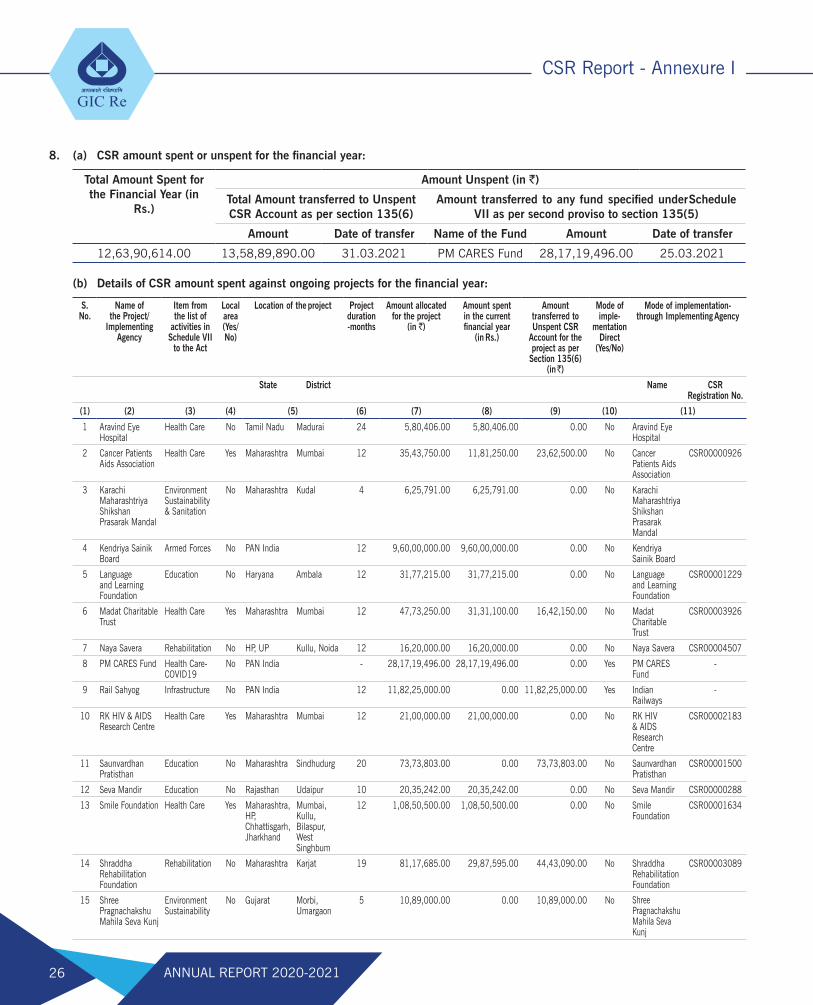

CORPORATE SOCIAL RESPONSIBILITY (CSR) REPORTING

The Corporation is having a Corporate Social Responsibility Policy (CSR Policy) indicating the activities to be undertaken by the Corporation, which has been approved by the Board.

The CSR Policy may be accessed on the Corporation’s website at the link: https://www.gicofindia.com/en/people-resources/hr-corner/policies-guidelines

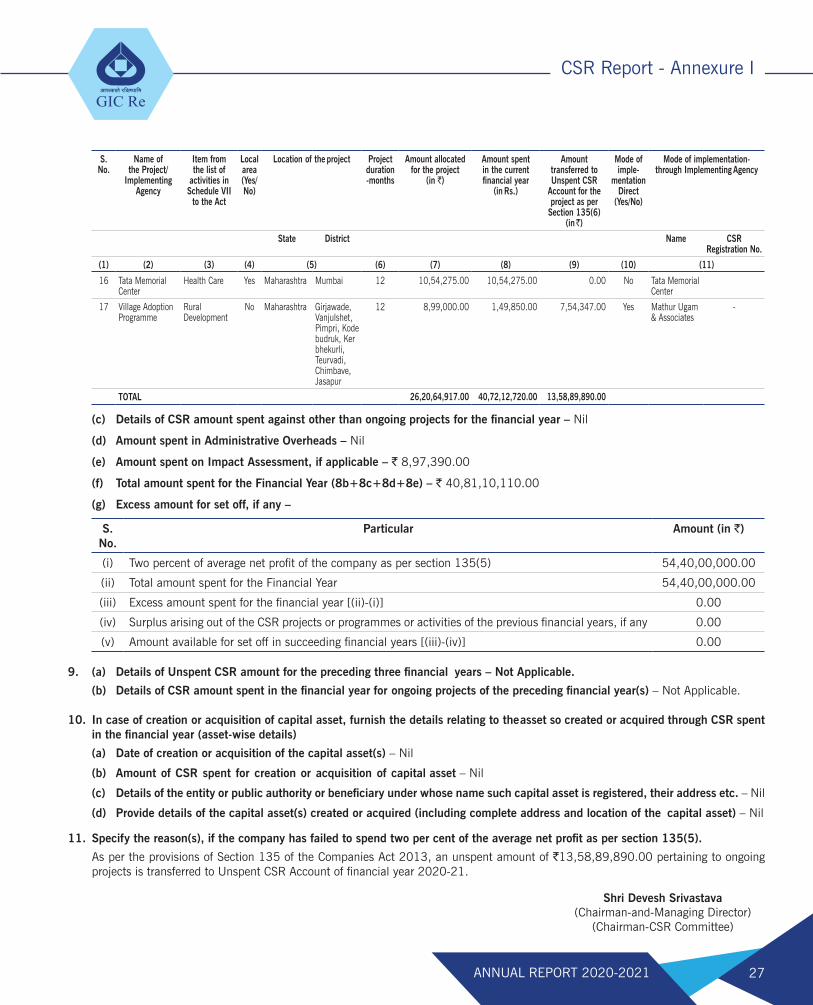

The CSR Reporting as per Section 135 of the Companies Act, 2013 given in Annexure I.

PERFORMANCE AND FINANCIAL POSITION OF SUBSIDIARIES, JOINT VENTURES AND ASSOCIATES

Pursuant to Section 129(3) of the Companies Act, 2013 read with Rule 5 of the Companies (Accounts) Rules, 2014, a separate statement containing salient features of the Financial Statements of Subsidiary, Associate and Joint Venture Companies in Form AOC-1 forms part of the Directors’ Report for the financial year 2020-21 as Annexure-II and the details on their performance & financial position are given in Management Discussion & Analysis Report.

Further, in terms of proviso to Section 136(1) of the Companies Act, 2013 and Regulation 46 of the Listing Regulations, 2015, the Corporation will place separate audited Financial Statements in respect of each of its Subsidiary Company on its website and also provide a copy to any Shareholder of the Corporation who seeks the same. The Financial Statements of the Subsidiary Companies will also be kept open for inspection at the registered offices of the Corporation/ the respective Subsidiary Companies.

Directors’ Report

17ANNUAL REPORT 2020-2021

AUDITORS AND AUDIT REPORT

STATUTORY AUDITORS

M/s. J. Singh & Associates, Chartered Accountants and M/s D. R. Mohnot & Co., Chartered Accountants were appointed as Joint Statutory Auditors to audit the accounts of the Corporation for the financial year 2020-21 by the Comptroller & Auditor General of India under Section 139 and Section 143 of the Companies Act, 2013.

The Auditors Report does not contain any qualification, reservation or adverse remark.

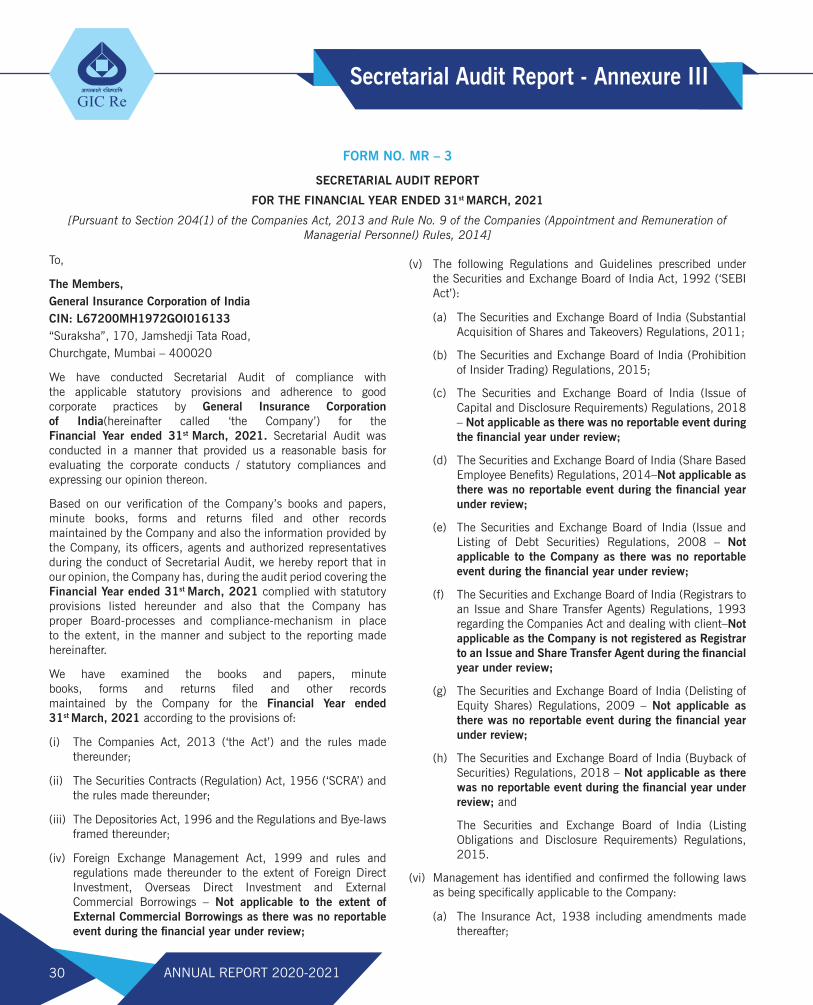

SECRETARIAL AUDIT

The Board has reappointed M/s. S. N. Ananthasubramanian & Co., Company Secretaries to conduct Secretarial Audit for the financial year 2020-21.

The Secretarial Audit Report does not contain any qualification, reservation or adverse remark except that the Board of Directors of the Corporation comprised of five Directors as against the requirement of atleast six Directors under Regulation 17 (1) (c) of the Listing Regulations and since the Chairman of the Corporation is an Executive Director, atleast half of the Board strength needs to be Independent Directors, as against the present position of two Independent Directors out of five Directors as required under Regulation 17 (1) (b) of the Listing Regulations and IRDAI (Corporate Governance) Guidelines 2016.

In this regard the Corporation being a Government Company, is under the administrative control of Ministry of Finance(“MoF”) and the Directors are appointed by President of India, acting through MoF. The Corporation has been constantly pursuing the matter with MoF for ensuring compliance with composition of Board of Directors.

Pursuant to Section 204 of the Companies Act, 2013, the Secretarial Audit Report of the Corporation is given in Annexure III.

ANNUAL RETURN

Pursuant to Section 92(3) read with Section 134(3)(a) of the Companies Act, 2013, a copy of the Annual Return for the year ended 31st March 2021, with the information available up to the date of this report, is placed on the website of the Corporation at https://www.gicofindia.com/en/investors-public-disclosures/investors-en and shall be further updated as soon as possible but no later than sixty days from the date of the Annual General Meeting.

COMPLIANCE CERTIFICATE ON CORPORATE GOVERNANCE

The Corporation has annexed to this report Annexure IV, a certificate obtained from the Practicing Company Secretary regarding compliance of conditions of Corporate Governance as stipulated in SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015.

MANAGEMENT DISCUSSION & ANALYSIS REPORT

The operations and future prospects of the Corporation are dealt in the Management Discussion and Analysis Report which forms part of the Directors’ Report.

FOREIGN EXCHANGE EARNINGS & OUTGO AND OTHER INFORMATION

The particulars of Foreign Exchange earnings/outgo as required by the Companies (Accounts) Rules, 2014 is given below:

i) Earnings ` 5,164.71 Crore ii) Outgo ` 5,249.69 Crore

The earnings included all receipts denominated in foreign currencies in respect of premium, recovery of claims, outward commission and investment earnings.

The outgo comprised all payments in foreign currency in respect of outward premium, claims on reinsurance accepted, commission and expenses of management (bank charges).

Expenses on (a) Entertainment (b) Foreign Tours and (c) Publicity and Advertisement amounted to ` 11,791/-, ` 18,23,021/- and ` 2,82,34,704/- respectively for the year under review.

CONSERVATION OF ENERGY AND TECHNOLOGY ABSORPTION

The Corporation is not engaged in any manufacturing activity and as such there are no particulars to disclose under the Companies (Accounts) Rules, 2014 as regards Conservation of Energy or Technology Absorption.

PERSONNEL AND INDUSTRIAL RELATIONS

I. Staff position as on 31st March 2021

Class I - Officers 464

Class III - Clerical Employees 58

TOTAL - 522

II. Composition of Scheduled Castes and Scheduled Tribes in the Employee Strength

CadreTotal Employee

StrengthComposition

SC % ST %

Officers 464 77 16.60 27 5.82

Clerical Staff

58 11 18.97 9 15.52

Sub-Staff 0 0 0.00 0 0.00

Total 522 88 16.86 36 6.90

Directors’ Report

18 ANNUAL REPORT 2020-2021

III. Welfare of SC/ST/OBC:

The Corporation has framed rules as per the National Policy on Reservations for SC/ST & OBC, which allows reservations, concessions/relaxations to SC/ST & OBC, in recruitment and promotions wherever applicable. Special in-house training classes are conducted for employees who are in promotion zone, in order to enable them to acquire knowledge and perform better in the pre-promotional written examination. The Corporation also organizes On-line training for SC/ST candidates who apply for the Recruitment Examination on All India Basis.

DISCLOSURE UNDER THE SEXUAL HARASSEMENT OF WOMEN AT WORKPLACE (PREVENTION, PROHIBITION AND REDRESSAL) ACT, 2013

The Corporation has been employing women employees in various cadres in all offices within India and abroad. The Corporation has in place a policy against Sexual Harassment, in line with the requirement of The Sexual Harassment of Women At Work Place (Prevention, Prohibition and Redressal) Act, 2013. All employees are covered under the policy. There has been no complaint from any employee during the financial year 2020-21 and hence no complaint is outstanding for redressal as at 31st March 2021.

IMPLEMENTATION OF OFFICIAL LANGUAGE POLICY OF THE CENTRAL GOVERNMENT

In spite of trying times due to pandemic, during the year under review, the Corporation improved its performance in implementation of Official Language Policy of the Government of India and complied with all the guidelines issued by the Ministry from time to time.

As mandated by the Official Language Policy of the Government, inspections of Departments situated in head office, Mumbai and online inspections of liaison offices at Delhi and Chennai were carried out by the officials of Official Language Department.

One In-house workshop was organized and four meetings of Official Language Implementation Committee were conducted during the year. Apart from the regular translation work, translation of Financial Standing Order (FSO), Procurement Guidelines, SOP of OSD Department, Request for Proposal (RFP) of Actuarial Department and Annual Report of 2019-20 etc. were carried out.

In-house quarterly journal KSHITIJ was published regularly in digital form. It was also made available on Corporation’s website. During Hindi fortnight, various competitions were organized. To avoid the gathering, based on the instructions given by the Ministry, cultural programme on the Hindi Day was not organised and the cash prizes were transferred through NEFT after the announcement of the prize winner’s name of the competitions by the mail.

Almost all Officers and Employees are having working knowledge of Official Language.

Hindi typing facility through UNICODE is available on computers,

to enable the Officers and Employees to do their day-to-day work in Hindi.

Officials of GIC have attended online all Town Official Language Implementation Committee (TOLIC) meetings and participation was also assured in various programmes organized under the aegis of the Town Official Language Implementation Committee (TOLIC).

Official Language Department of GIC was awarded a prize for Hindi In-house magazine KSHITIJ by TOLIC.

VIGILANCE

The Vigilance Department of the Corporation is headed by a Chief Vigilance Officer (CVO) in the rank of General Manager. The emphasis of the Vigilance Department is on preventive vigilance. The department also focuses on various systems improvement initiatives.

The focus of the Corporation, in concurrence with CVC guidelines, is to take proactive steps to avoid a vigilance-like situation. Audit reports are studied, and remarks made by Auditors are analyzed. Surprise inspections are conducted periodically, and lapses studied from a vigilance angle. Based on this, suggestions are made for improvement of systems and procedures of the Corporation. The purpose is to focus and accept vigilance as an organizational objective and create an atmosphere conducive to “Zero corruption” functioning, with role clarity and clear sense of direction. To improve vigilance administration, CVO and other officers also participate in the vigilance training programs/workshops conducted by reputed organizations.

Periodical discussions are held with the officials of various departments/companies to ensure financial and office discipline and imbibe a culture of value and ethics in the Corporation.

INTERNAL AUDIT DEPARTMENT

The main objective of the Internal Audit is to keep strict control over all the activities of any organization with a view to facilitate management assurance of the authenticity of the financial records, efficiency of operations of the firm and to strengthen the overall governance mechanism. The Corporation has its systems and controls in place covering all major areas of operations such as Underwriting, Investment, Finance and IT system.

To accomplish its objectives in a systematic and disciplined manner, Internal Audit Department (IAD) has utilized the services of professional audit firms. During the Financial Year 2020-21, M/s Kailash Chand Jain & Co., Chartered Accountants, were re-appointed as Internal Auditors for Reinsurance Operations and Business Accounts and M/s Gokhale & Sathe, Chartered Accountants, were re-appointed as Internal Auditors for Investment Operations and other departments.

The IAD also appointed Internal Auditors for foreign branches of the Corporation in London, Dubai and Malaysia as also conducted

Directors’ Report

19ANNUAL REPORT 2020-2021

the audit of International Financial Service Centre Insurance Offices (IIO) at GIFT City.

Besides the above, the following special audits were also arranged by the IAD:

1. Secretarial Audit 4. Audit of Indian Nuclear Insurance Pool

2. RTI Audit 5. Audit of Indian Market Terrorism Risk Insurance Pool

3. Audit of FAIR Nat CAT Pool 6. IRMSP Audit (Investment Risk Management Systems & Processes)

IAD liaised with Comptroller & Auditor General of India (CAG) and various departments for matters relating to CAG audit. The status of Draft Paras (DPs) and Inspection Reports (IRs), issued by Comptroller & Auditor General of India (CAG), was placed before the Board and the Audit Committee of the Board from time to time.

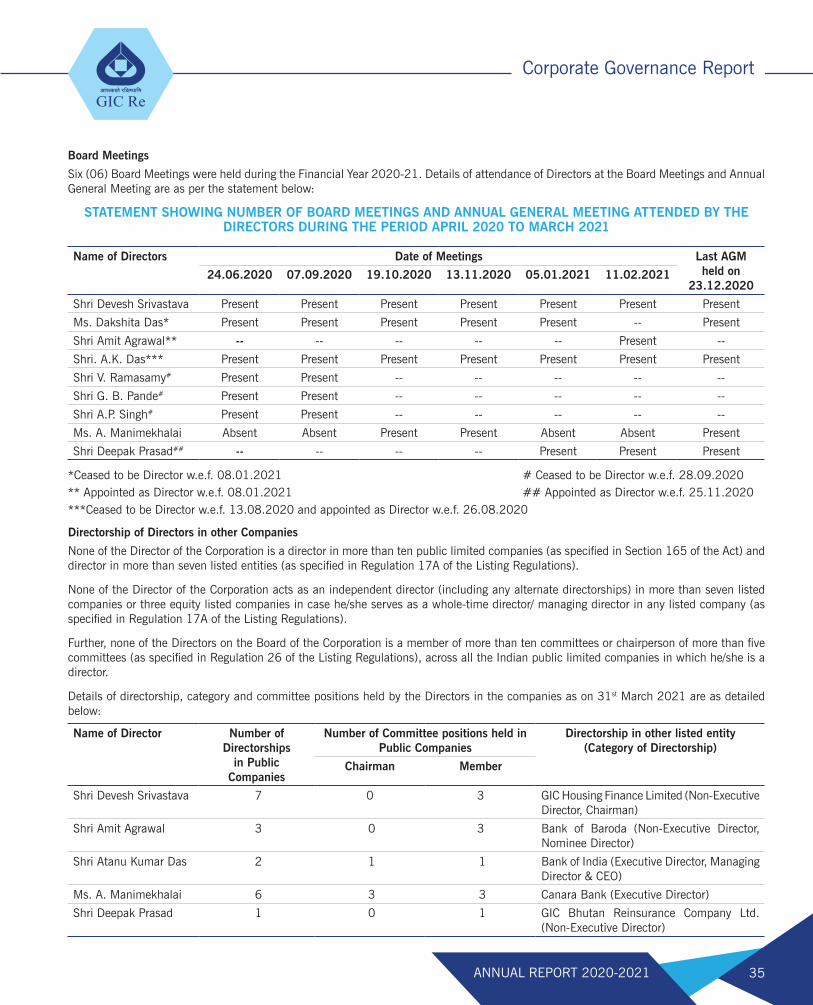

The IAD functions independently under the supervision of the Audit Committee of the Board. The Audit Reports of GIC Re, Head Office and Foreign branches are placed before the Audit Committee of the Board for their consideration and directions. Six (6) meetings of the Audit Committee of the Board were held during the year 2020-21. Action Taken Reports were presented to the Audit Committee to update them on the status of progress on the implementation of the directions of the Committee.

During the year, the guidelines and scope of audit for appointment of Internal Auditors of GIC Re, for Reinsurance was reviewed keeping in view the evolving role of auditors in a scenario where Corporate Governance, regulatory compliance, management reporting systems, transparency and prevention of fraud has gained increasing importance. Like every year emphasis was laid on core business activities and audit of Reinsurance underwriting operations, settlement of outstanding accounts & reconciliations of broker balances, Treaty acceptances, Cash Call settlements and Settlement of Accounts were audited on concurrent basis. Other departments like Human Resources, IT, Communication, General Accounts, Office Services etc. were also covered during the year.

Besides major expenditures incurred, both Revenue and Capital, having financial implications were also subjected to audit. Audit of Investment Operations was conducted on concurrent basis. This covered the primary and secondary market transactions. In line with RBI directions, Subsidiary Government Ledger (SGL) for Central and State Government Securities were subjected to concurrent audit and confirmation of correctness of balances and its reconciliation at the end of each month were sent to RBI. The same were also placed before the Audit Committee at its meetings.

The major contributions of the auditors during the year include appraising the management of the scope of improvement in

cash call servicing, broker-wise and cedant-wise receivable management, reduction in unappropriated amounts and streamlining of outstanding loss reserves. With the detailed increase in scope of audit of Investment Department, Human Resources, IT, Communication, General Accounts, Office Services etc. auditors were able to recommend better internal control, reporting and monitoring environment.

The Audit function of the Corporation has brought about improvement in data quality, acceleration in claim processing and streamlining of process of accounts receivable management in the Reinsurance Operations. By critically appraising the Management of the efficacy of the various systems and processes, the IAD facilitated to strengthen the overall governance mechanism.

The Annual Budget of the Corporation/Mid-Year budget review exercise based on Budget Estimates of individual Departments, placed before the Board were approved and implemented by Internal Audit Department.

RTI ACT, 2005

The Corporation has in place the stipulated structure to implement the RTI Act 2005, in the Organization. The Setup is headed by a General Manager designated as the Transparency & Nodal Officer. A General Manager functions as the Appellate Authority, an Assistant General Manager is the Central Public Information Officer, a Senior Manager discharges the duties of Assistant Public Information Officer under the provisions of the Act. An Assistant Manager has been nominated as Nodal Officer, MIS.

The Corporate website www.gicofindia.com also hosts information as relevant to the Corporation, under the Act. It has separate Right to Information link developed and continuously updated by the RTI Cell (https://www.gicofindia.com/en/rti) containing information and complying with the provisions under the RTI Act, 2005 and other Ministerial and CIC circulars.

The Corporation in the FY 2020-21 complied with the guidelines issued by Ministry of Personnel regarding Implementation of suomotu disclosure u/s 4 of the RTI Act, 2005 and its Audit thereof.

During the period under review, the Corporation received One Hundred Sixty-Seven (167) Applications and Seven (7) First Appeals under the RTI Act, 2005. All the Applications were duly replied, and appeals were disposed of well within the stipulated time. Three (3) Second Appeals has been filed against the Corporation before Central Information Commission and the final orders were passed in favour of the Corporation during the period under review.

INFORMATION TECHNOLOGY MANAGEMENT GROUP (ITMG)

The Information Technology Management Group of the Corporation has adopted the vision of being responsible for generating value through the use of technology. It plays the role of an enabler for business strategies and change management by the use of latest

Directors’ Report

20 ANNUAL REPORT 2020-2021

technology in hardware, software and networking to match global benchmarks.

The year under review has seen the Business Continuity Plan (BCP) for IT operations being tested under completely unforeseen conditions. The pandemic restricted mobility and access to office premises for an extended period of time. Timely investments over the years had ensured putting in place latest technologies in all aspects of the IT infrastructure. This enabled the organization could smoothly roll out work from home capability for our employees. Their safety and well being was ensured while there was no stoppage of work. Employees too rose to the challenge by adopting all the available capabilities like remote access, collaboration tools and holding virtual meetings internally and with customers.

Skill development, training and building awareness of the IT team is a continuous process and ITMG has taken the initiative to provide professional level certification on SAP modules for some of its employees. This will help develop in-house expertise on the ERP system.

The department has also initiated new projects in the areas of Limit Management for better control in the areas of Investment operations, building monitoring dashboards for Claims servicing, evaluating solvency and capital management tools.

TRAINING/HRD

Training is defined as a planned and systematic process to modify or develop attitude, knowledge or skills through learning experiences, to achieve effective performance at workplace. There is need to train and retrain the employees on continuous basis. It is a systematic and planned process which has its organisational purpose to impart and provide learning experiences that will bring about improvement in an employee and thus enabling him to make his contribution in greater measure in meeting the goals and objectives of an organisation.

We take great efforts to infuse our employees with the confidence and charisma that directs them to be good leaders. And while not everyone is required to have the ability to lead an entire team, we help them feel empowered enough to lead themselves. We ensure that employees develop a certain degree of autonomy and control in their day-to-day activities. A key principle of employee empowerment is providing employees the means for making important decisions and helping ensure those decisions are correct.

In the year 2020-21, training was imparted to all levels of employees. Training programmes were conducted for the employees through various institutes. Though the year was badly affected by the pandemic, we rose to the occasion and conducted the programmes in online mode. Both technical and behavioral programmes were conducted throughout the year.

A summary of various training programmes organized by the Training Department is given below:

OrganisationNo. of

programmesNo of

employees

National Insurance Academy 21 85

Insurance Institute of India 7 33

Indian School of Business 1 24

Other Reputed Institutes 32 123

In House 7 95

1. A high-end skill-based programme for specialist (underwriters) was conducted through Indian School of Business. The certification-based program on Art of Negotiation and Influencing Skills was conducted in mid-January 2021. 26 specialists (underwriters) were trained. It was more of a role play based virtual programme.

2. A webinar on “Parenting a Successful Child” through IIM Ahmedabad in December 2020. The programme received tremendous response from our employees (young parents). The programme was very appreciated by the nominated participants.

3. Organising a customised training programme on computation of the CSR budget which benefitted the niche group of employees in CSR department.

4. A workshop on Reinsurance Regulations for officers from all Class of Business was conducted in January 2021. This was conducted through National Insurance Academy. Approximately it helped around 35 officers get better understanding of the revised reinsurance regulations pertaining to the CBRs.

5. A specialised workshop on Mental Health and related lifestyle diseases was conducted in December 2020. The program received tremendous response and around 32 officers attended the same. The focus was entirely on equipping the officers to have a positive and proactive attitude in this current pandemic and lockdown situation.

6. Special workshop on leadership conducted on Women’s day on 8th March 2021. The programme was facilitated by Ms. Subira Merchant on Women’s day i.e. 8th March 2021. Approximately 18 female employees could avail benefits of the said workshop.

7. A customised program was organised for women employees in GIC on eve of Women’s day. An in-house program concepted and designed for the female employees of the Corporation through Prajna Self-care workshop on 9th March 2021. Approx. 20 female employees attended the workshop.

Directors’ Report

21ANNUAL REPORT 2020-2021

8. The Training Department also conducted the Pre-Promotional training programme for all eligible employees in 3 batches this year to familiarize them about the important examination topics like Reinsurance, RI Claims, Accounts etc. The faculties for this programme were in-house.

9. A one-day program on “Basics of Reinsurance” was conducted for Scale I and II officers. Approximately 50 employees gained the benefit from this programme. The programme was conducted in coordination with NIA.

10. “Workshop on Delegation” was organised to bring in an attitudinal change in Scale III & IV officers. The workshop was conducted through M/s Strategic HR & Training.

11. Certification based SAP training modules on HCM, BASIS and ABAP for about 7 officers was conducted. Officers from HR and ITMG were enrolled for these programs.

Training Department has tried to ensure most of the employees could avail of some of the training during the year 2020-21.

OVERSEAS EXPANSION

Overseas expansion of operations, through branch offices, subsidiaries and joint ventures is an integral part of the business growth strategy so as to expand the reach of the operations into multiple countries throughout the world. The Corporation targets expansion into new markets by efficiently using the potential and creating additional sustainable income opportunities, both in developed countries, where there is larger demand and in developing countries where there is increasing demand.

Expansion plans are drawn based on study of market opportunities, supported by understanding of the business, working environment and regulations in prospective markets. The Corporation has also been striking strategic partnership with reinsurers abroad to take advantage of the expertise and experience of both parties and leverage on economies of scale.

GIC Moscow Representative office was upgraded into a wholly owned subsidiary named as GIC Perestrakhovanie LLC. The subsidiary after obtaining license from the Insurance Regulator of Russian Federation has now commenced its operations from August 2020.

In accordance with the Ordinance published in official gazette dated 1st April 2020 by Brazilian insurance regulator, Superintendence of Private Insurance (SUSEP), the status of GIC Re’s Representative Office in Brazil is upgraded from ‘Eventual Reinsurer’ to ‘Admitted Reinsurer’.

INVESTMENT IN INSURANCE COMPANIES

DOMESTIC OPERATIONS

• AGRICULTURE INSURANCE COMPANY OF INDIA LTD. (AICIL)

The Corporation holds 35% equity of AICIL and NABARD holds 30% while the balance is held equally to the extent of 8.75% by the four public sector non-life insurance companies.

OVERSEAS OPERATIONS

The Corporation has 3 overseas offices viz. Branch Offices in London, Dubai and Malaysia.

Apart from this, the Corporation has three wholly owned subsidiaries viz. GIC Re South Africa Ltd., Johannesburg; GIC Re, India, Corporate Member Limited, London and GIC Perestrakhovanie LLC., Moscow. The Corporation also has invested in the share capitals of Kenindia Assurance Company Ltd., Kenya, India International Insurance Pte Ltd., Singapore, Asian Reinsurance Corporation, Bangkok, East Africa Reinsurance Company Ltd., Kenya, and GIC Bhutan Re Ltd., Bhutan.

• LONDON BRANCH (UK)

During the current financial year 2020-21, the Gross Premium written by the Branch is GBP 125.57 million compared to GBP 136.33 million last year and incurred a loss of GBP 10.43 million as against a profit of GBP 5.20 million last year.

• DUBAI BRANCH (UAE)

During the current financial year 2020-21, the Gross Premium written by the Branch is AED 469.48 million compared to AED 521.94 million last year and incurred a loss of AED 65.13 million as against a profit of AED 248.61 million last year.

• MALAYSIA BRANCH

During the current financial year 2020-21, the Gross Premium written by the Branch was RM 792.06 million compared to RM 856.16 million and earned a profit of RM 59.42 million as against a loss of RM 53.58 million last year.

• KENINDIA ASSURANCE CO. LTD., KENYA

The Corporation holds 9.19% shares in Kenindia which has a paid-up share capital of Kshs 1000 million. The total shares held by the Corporation is 9,18,752 shares of Kshs 100 each as on 31st December 2020. The Company reported a net profit after tax of Kshs 221.63 million as against net loss of 387.58 million last year. The Board of the Company recommended a dividend of Kshs 5 per share for the year ended 31st December 2020.

• INDIA INTERNATIONAL INSURANCE PTE. LTD., SINGAPORE

The Corporation holds 20% shares in India International Insurance Pte. Ltd., which has a share capital of S$ 50 million. The total shareholding of the Corporation in the Company is 10 mn shares each of S$ 1.

The Company has made a profit of S$ 12.04 million as against a profit of S$ 9.94 million last year.

Directors’ Report

22 ANNUAL REPORT 2020-2021

The Directors have considered it appropriate to recommend a first and final dividend of 7.5% on the paid-up capital of S$50.00 million for the year 2020.

• ASIAN REINSURANCE CORPORATION, BANGKOK

The Corporation is holding 6.16% of the share capital as Associate Member of Asian Re in addition to holding 0.97% of the share capital as its Regular Member on behalf of the Government of India. Asian Re has made a loss of USD 3,288,825 in 2020 as against a profit of USD 1,856,812 in 2019.

• EAST AFRICA REINSURANCE COMPANY LTD., KENYA

The Corporation has 14.7521% stake in the share capital of East Africa Reinsurance Company Ltd., an existing profit-making reinsurance company in Kenya. The total shareholding of the Corporation is 221,281 shares of 1000 Kshs as on 31st December 2020.

The Company has made a profit of Kshs. 410 million as against a profit of Kshs. 589 million last year.

Board has recommended a total dividend of Kshs. 100 million equivalent to 24.37% of PAT to registered shareholders as at 31st December 2020.

• GIC BHUTAN RE LTD.

The reinsurance company of Bhutan is a Joint Venture between the Corporation and local Bhutanese promoters. The venture began its operations in the name ‘GIC Bhutan Re Ltd’ in December 2013.

The Corporation has a 26% stake in the Joint Venture and held 28,600,000 shares of value Nu. 10 each as of 31st December 2020.

The rest of the shareholding is divided between two Local Bhutanese promoters with 17% stake each and 40% shares are held by the public.

The Company has made a profit of Nu. 144.85 million (PAT) in 2020 as against a profit of Nu. 46.96 million (PAT) in 2019.

The Company has not declared any dividend for the year ended 31st December 2020, as per RMA regulations.

• GIC RE SOUTH AFRICA LTD.

GIC Re South Africa Ltd. is the Corporation’s first 100% owned subsidiary (Wholly owned subsidiary) operational since October 2014. The company when acquired was in the run-off for both Life as well as Non-life business. GIC started writing new non-life business since January 2015.

The Corporation held 571,030,862 on par value ordinary shares with a value of ZAR 1,142,061,724 constituting 100% of GIC Re South Africa Ltd’s equity as of 31st March 2021.

It is confirmed that there was no dividend paid or declared in the period ending 31st March 2021.

• GIC RE, INDIA, CORPORATE MEMBER LIMITED

With the objective of becoming a reputed global reinsurer, GIC Re expanded into Lloyd’s of London by offering reinsurance capacity to Lloyd’s syndicates through quota share capital gearing treaties since 2011. Since as a capacity provider, GIC Re was required to have its own Corporate Membership at Lloyd’s, GIC Re acquired I-CAT CCM TEN Ltd., an existing corporate Member company, in November 2013 and renamed it as GIC Re, India, Corporate Member Ltd. which is registered as a private limited company in the UK. The Company commenced reinsurance operations in 2014.

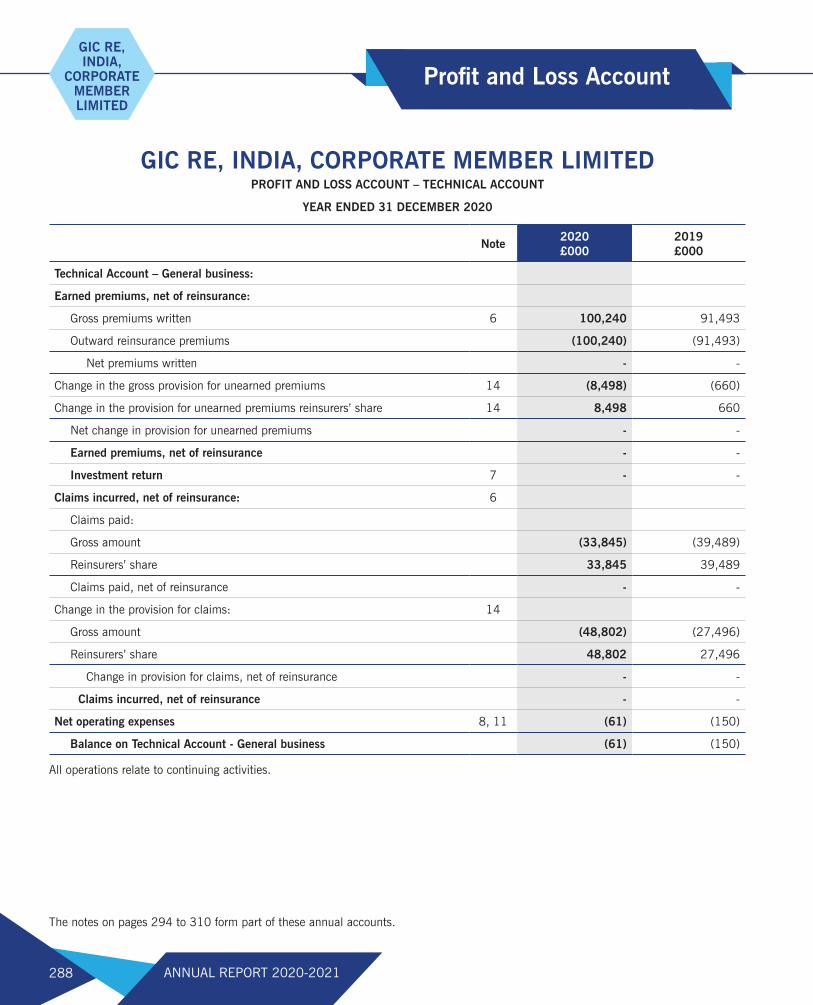

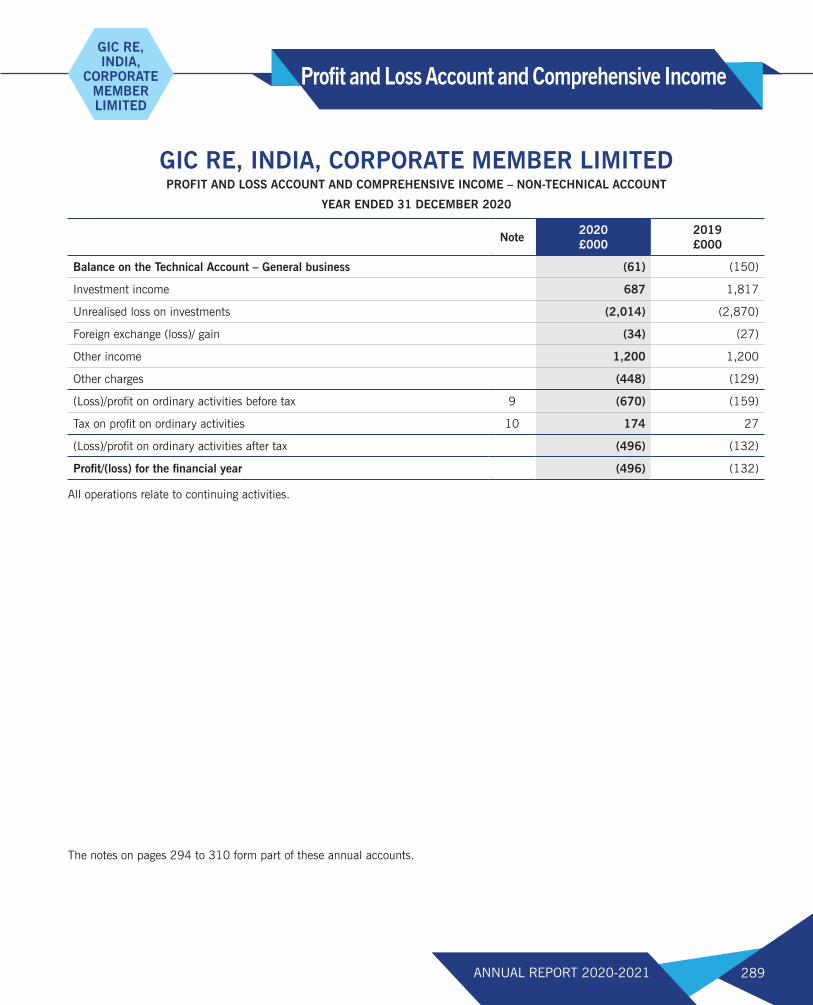

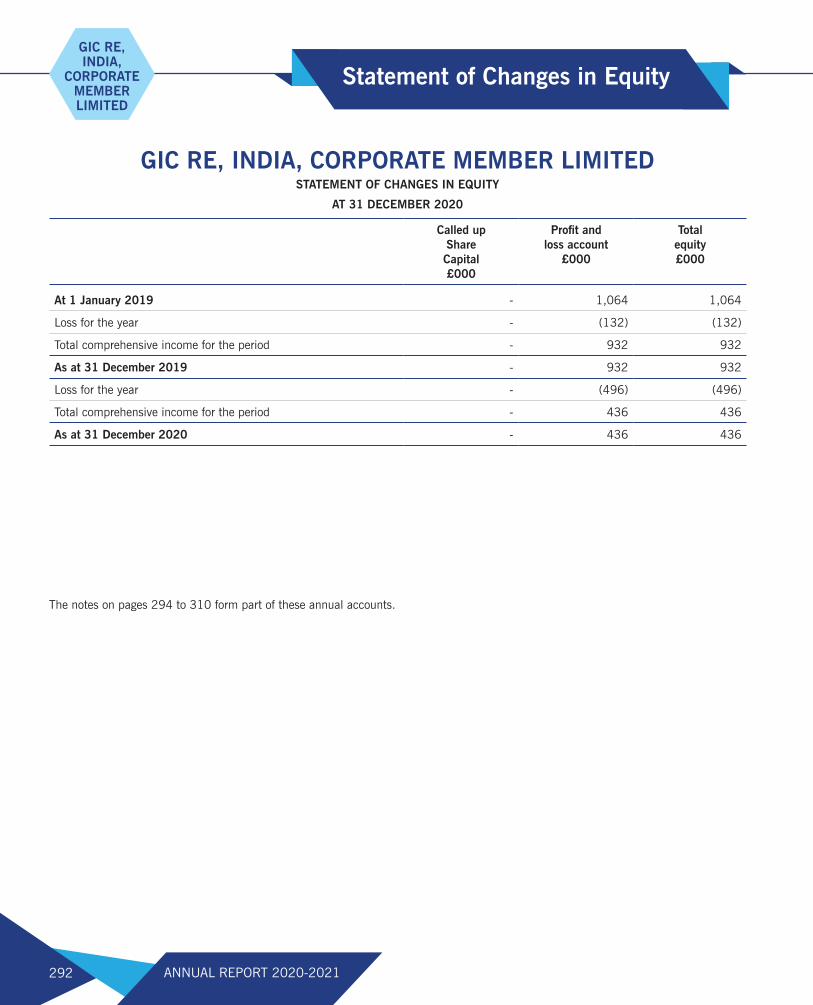

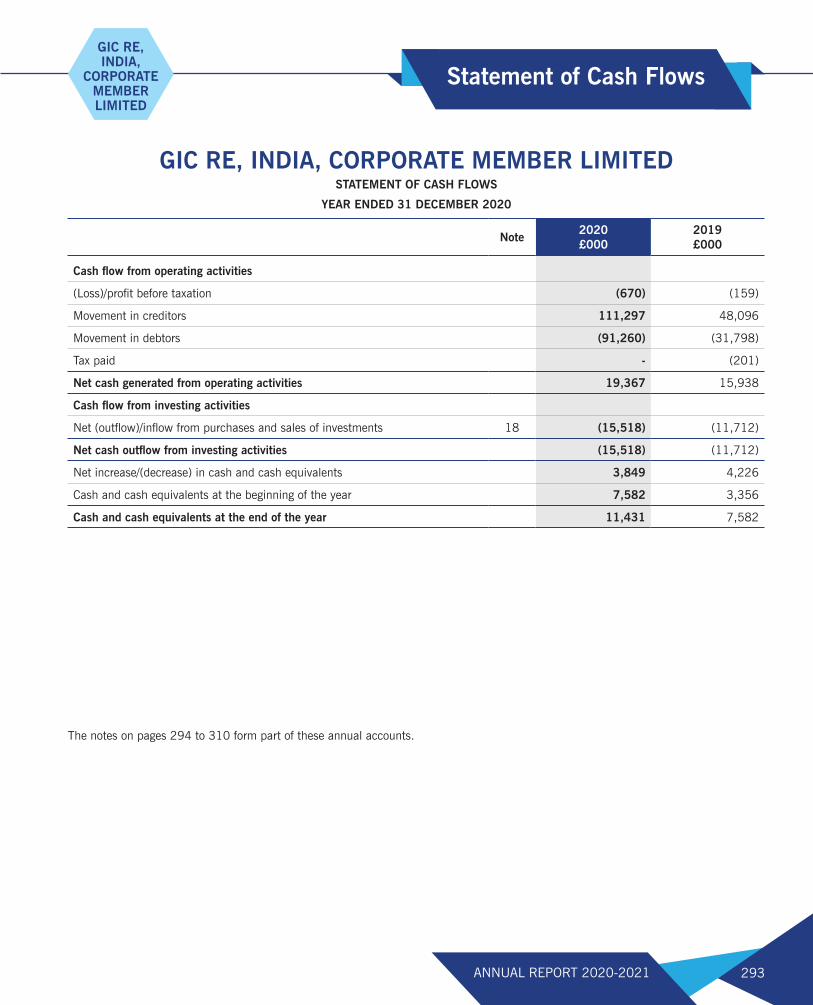

Loss for the year ended 31st December 2020 was £ 496,000 as against £ 132,000. The business underwritten by the Company is fully reinsured with GIC Re.

The company has not declared payment of any dividend for the year.

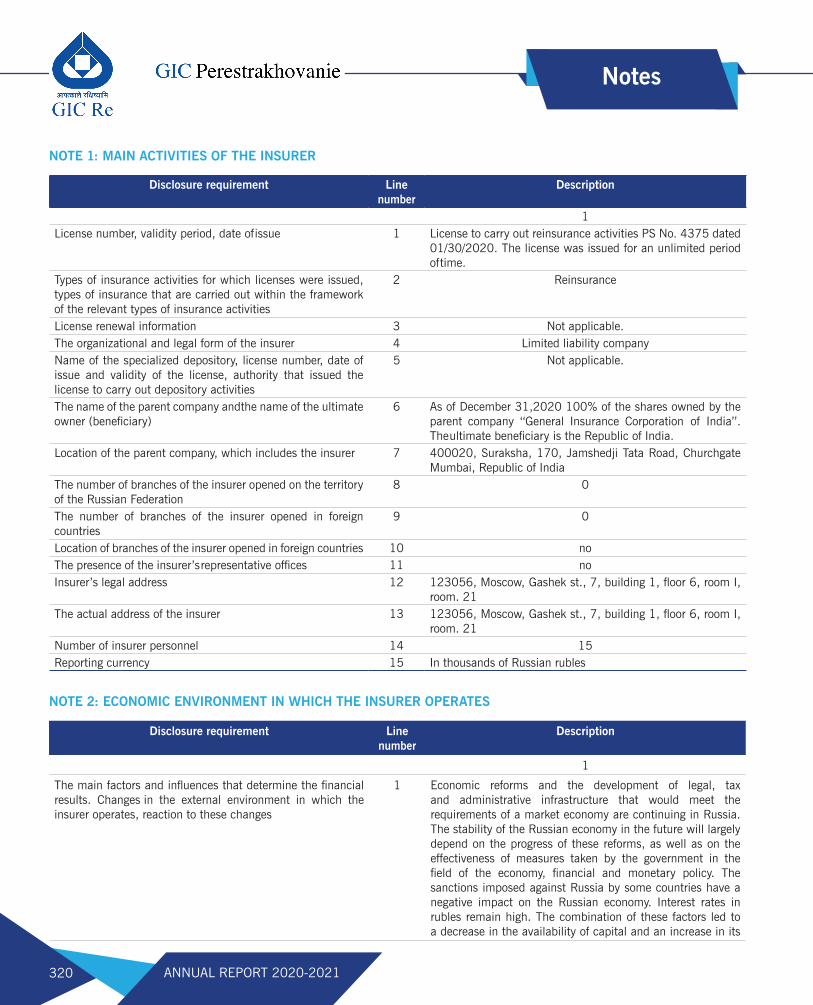

• GIC PERESTRAKHOVANIE LLC

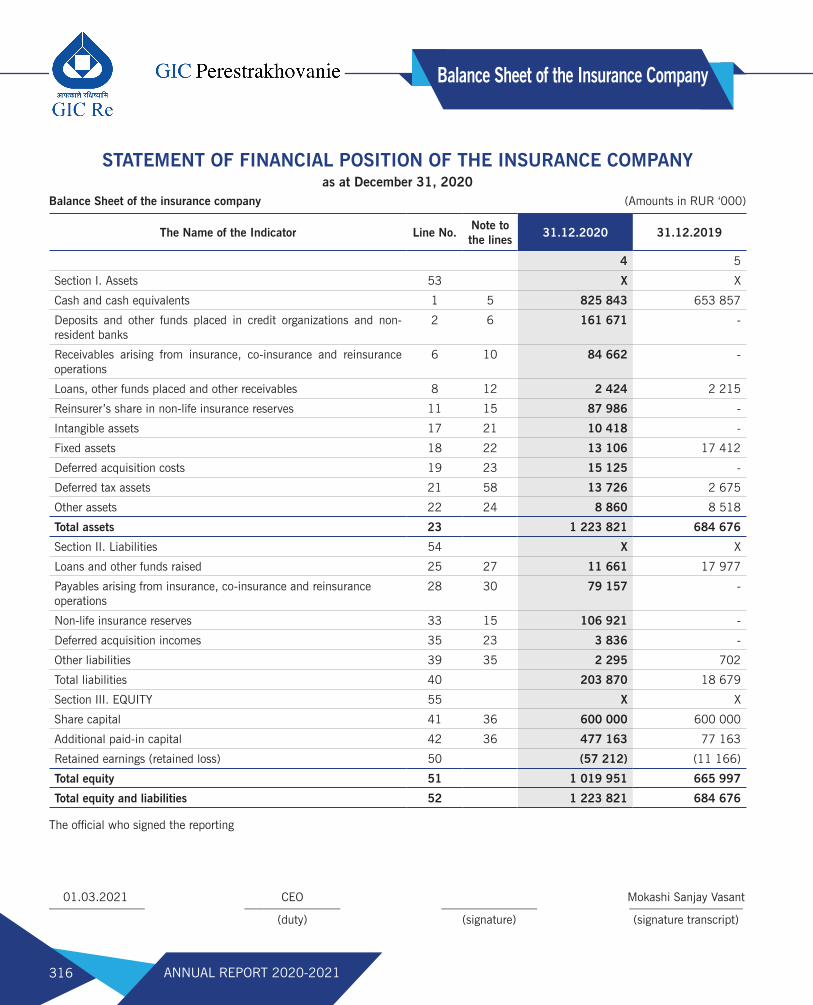

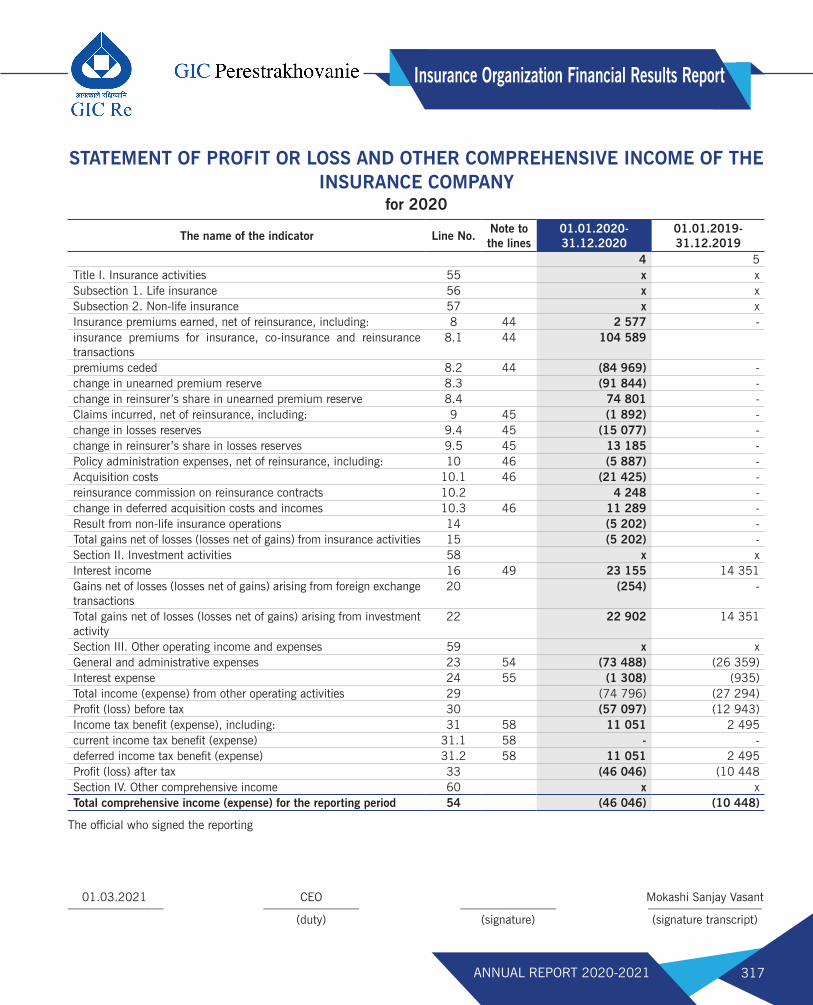

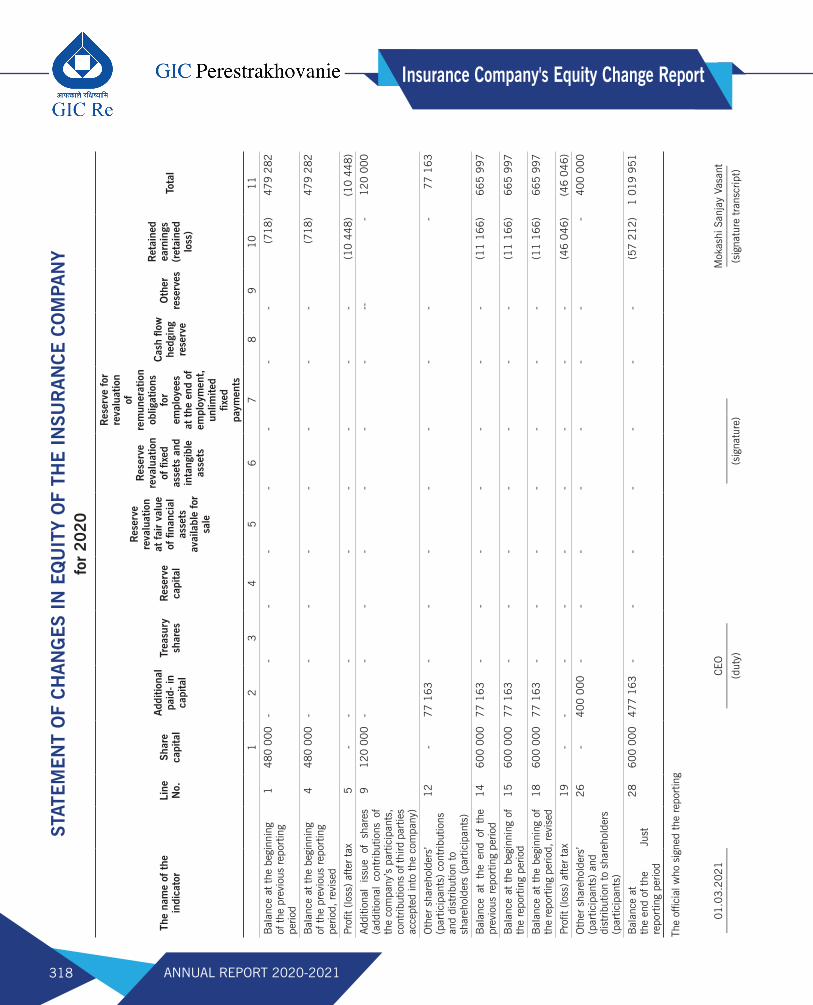

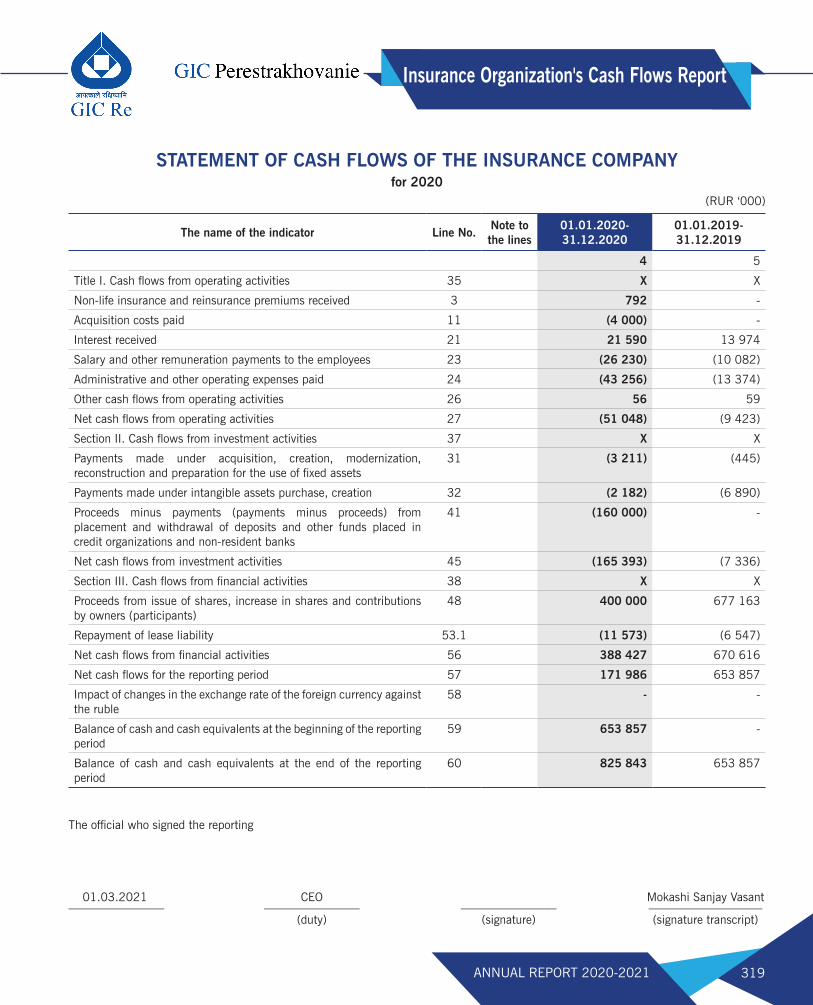

“GIC Perestrakhovanie LLC” commenced its operations during August 2020. It now writes reinsurance business emanating from the Russia Federation and former Soviet Union countries, namely, Armenia, Moldova, Azerbaijan, Kyrgyzstan, Kazakhstan, Turkmenistan Uzbekistan, Tajikistan, Belarus and Georgia. As per the plan, GIC Re’s existing portfolio would be renewed by the subsidiary at the respective renewal dates and use the locational advantage to grow the business further. During the year, the subsidiary was rated B++ with Stable outlook by A.M Best.

The subsidiary could close its financial year ended on 31st December 2020 with a written premium of 104.59 million Rubles. The net incurred claim to earned premium ratio was 73.45%. As the subsidiary could transact its business only for a brief period during 2020, the financial statements for the year ended 31st December 2020 are not reflective of subsidiary’s projected business figures.

LISTING OF EQUITY SHARES

The shares of the Corporation are listed on National Stock Exchange of India Limited (NSE) and BSE Limited (BSE).

PUBLIC DEPOSITS

The Corporation has not accepted any deposits under Section 73 of the Companies Act, 2013.

DIRECTORS AND OTHER KEY MANAGERIAL PERSONNEL

The Board of Directors of the Corporation as on 31st March 2021 consisted of five (5) Directors, comprising of two (2) Independent Directors, one (1) Government Nominee Director and two (2) Whole Time Directors including the Chairman and Managing Director.

Directors’ Report

23ANNUAL REPORT 2020-2021

None of the Directors are related to any other Director or employee of the Corporation.

The details pertaining to composition and change in Board, committees and details of meetings is provided under Corporate Governance Report.

DECLARATION BY INDEPENDENT DIRECTORS

All the Independent directors have given a declaration that they meet the criteria of independence as laid down under Section 149(6) of the Companies Act, 2013 and the Listing Regulations. The Independent directors have confirmed that they have registered with the database maintained by the Indian Institute of Corporate Affairs (IICA).

The Corporation, being a Government Company, is under the administrative control of Ministry of Finance (MoF), the power to appoint Directors (including Independent Directors) vests with the Government of India. The appointment of Directors is done by MoF after due processes involving screening, review and compliances. In the opinion of the Board, the Independent Directors possess integrity and the requisite expertise and experience. As regards the proficiency, as on date, the Independent Directors have yet to undergo the online proficiency self-assessment test conducted by IICA.

POLICY FOR SELECTION AND APPOINTMENT OF DIRECTORS AND THEIR REMUNERATION

The Corporation being a Government Company, is exempted to furnish information under Section 134(3)(e) of the Companies Act, 2013 vide MCA Notification dated 5thJune 2015.

POLICY FOR REMUNERATION OF KEY MANAGERIAL PERSON AND OTHER EMPLOYEES

The Corporation, being a Government Company, the remuneration payable to Key Managerial Persons and other employees are as per the Government of India norms.

CODE OF CONDUCT UNDER SECURITIES AND EXCHANGE BOARD OF INDIA (PROHIBITION OF INSIDER TRADING) REGULATIONS, 2015

The Corporation has in place a Code of Conduct to regulate, monitor and report trades in securities by Directors, Employees & Connected Persons which is in conformity with the Securities and Exchange Board of India (Prohibition of Insider Trading) Regulations, 2015. The Code is applicable to the Employees of the Corporation, Designated Persons, and their Immediate Relatives and Connected Persons, to the extent applicable. The objective of the Code is to prohibit insider trading in any manner by the Designated Persons and to maintain confidentiality of unpublished price sensitive information and access to information on a ‘need to know’ basis.

VIGIL MECHANISM/ WHISTLE BLOWER POLICY

The Corporation, being a Government Company is subjected to the CVC Guidelines and the Corporation has a separate Vigilance Department administering the Vigilance matters.

The Corporation has a Whistle Blower Policy/Vigil Mechanism Policy approved by the Board and the same is placed on the website of the Corporation.

CORPORATE GOVERNANCE

The Corporation continues to adopt the best practices of Corporate Governance to ensure transparency, integrity and accountability in its functioning. The Corporate Governance Report has been incorporated as a separate section, forming part of this Annual Report.

BUSINESS RESPONSIBILITY REPORTING

Business Responsibility Report as stipulated under Regulation 34 of the Listing Regulations forms part of the Annual Report and has been hosted on the website of the Corporation and can be viewed at www.gicofindia.com.

CEO / CFO CERTIFICATION

In terms of the Listing Regulations, the certification by the Managing Director & CEO and Chief Financial Officer of the Corporation on the financial statements and internal controls relating to financial reporting has been obtained.

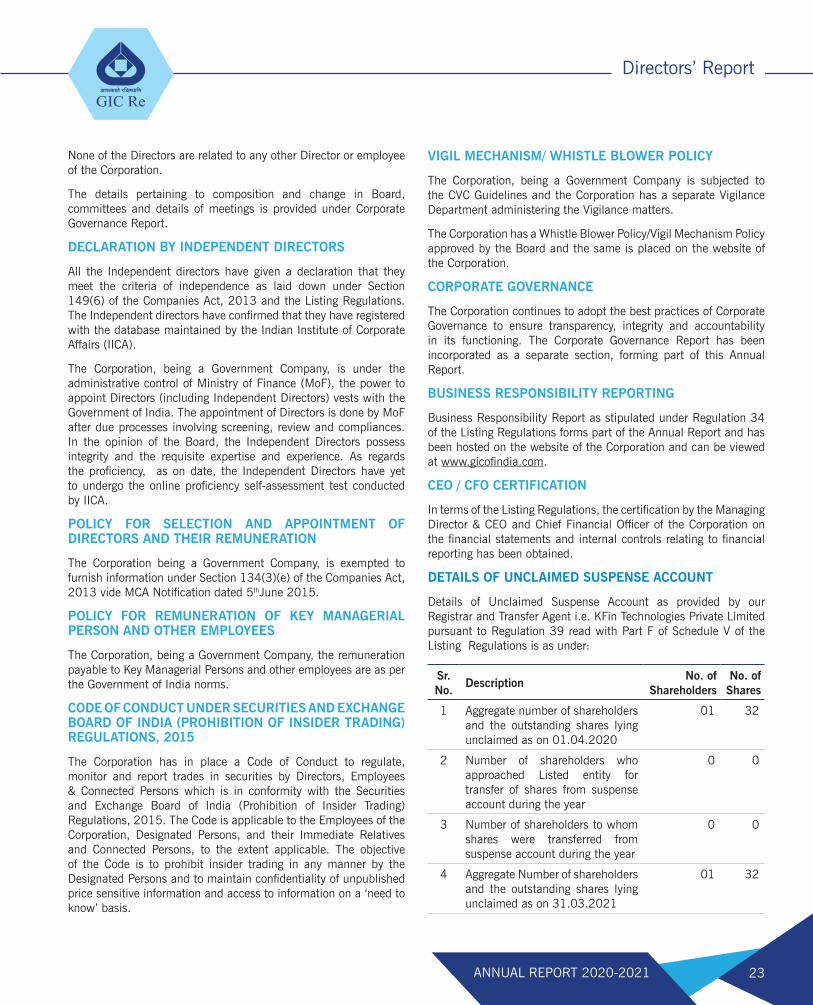

DETAILS OF UNCLAIMED SUSPENSE ACCOUNT

Details of Unclaimed Suspense Account as provided by our Registrar and Transfer Agent i.e. KFin Technologies Private Limited pursuant to Regulation 39 read with Part F of Schedule V of the Listing Regulations is as under:

Sr. No.

DescriptionNo. of

ShareholdersNo. of Shares

1 Aggregate number of shareholders and the outstanding shares lying unclaimed as on 01.04.2020

01 32

2 Number of shareholders who approached Listed entity for transfer of shares from suspense account during the year

0 0