10march 2021_india_daily - kotak securities

TRANSCRIPT

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES. REFER TO THE END OF THIS MATERIAL.

Contents

Daily Alerts

Change in Reco

Adani Ports and SEZ: Forays into large high-growth markets

US$1 bn worth of equity investments open large high-growth markets for

ADSEZ

Share consideration helps lower leverage, creating leeway for more

acquisitions

Increase Fair Value to Rs790, implying a 13X FY2023E EV/EBITDA multiple

Sector alerts

Automobiles & Components: Commodity pressures to persist in near term

RM headwinds to negatively impact gross margins for automotive OEMs in

coming quarters

Sharp jump in retail fuel prices further elevates cost of ownership for

consumers

Another round of price hikes may dent volume growth prospects

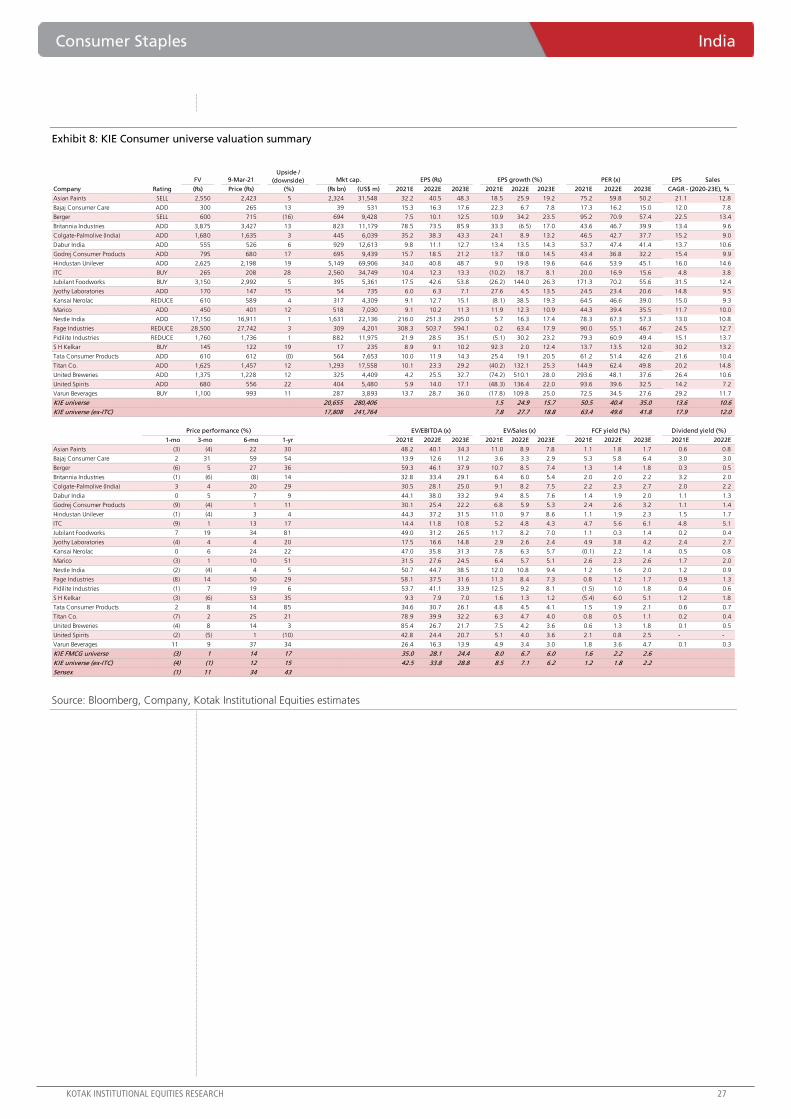

Consumer Staples: Month in review - Feb 2021

Pricing - Price hikes continue in edible oil and soaps; muted activity in other

categories

RM - Inflationary trends in oil commodities while mixed price trends in agri-

commodities

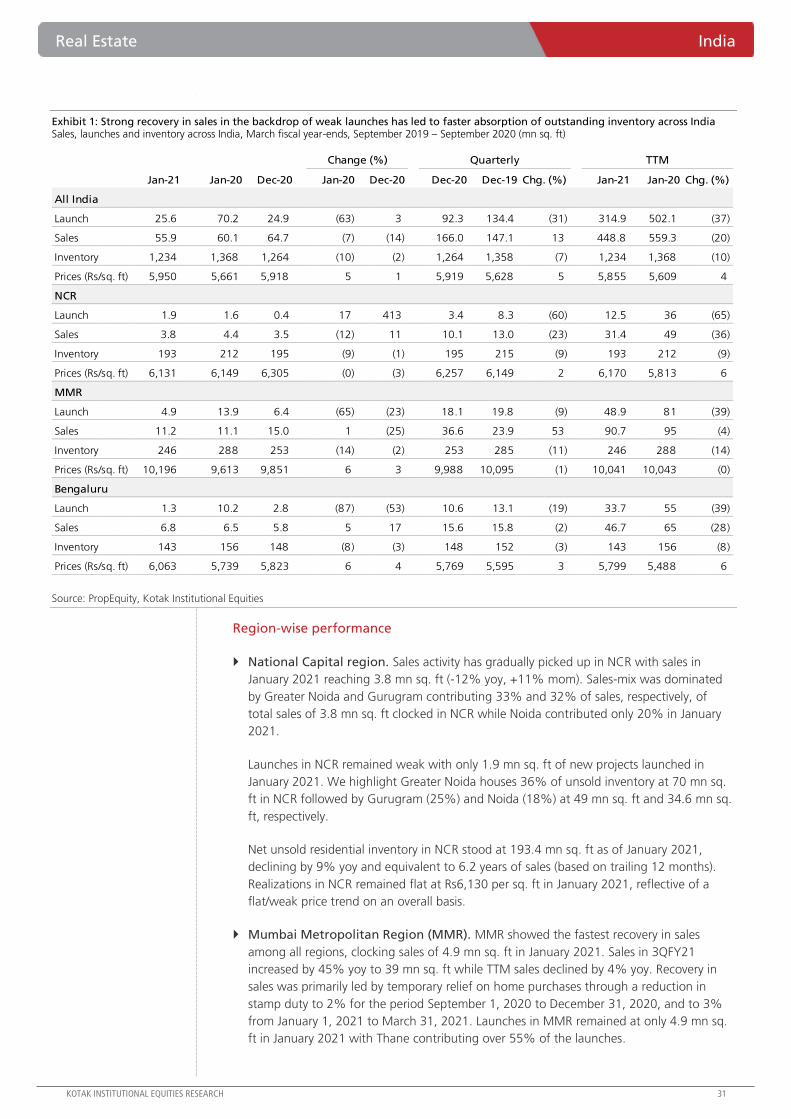

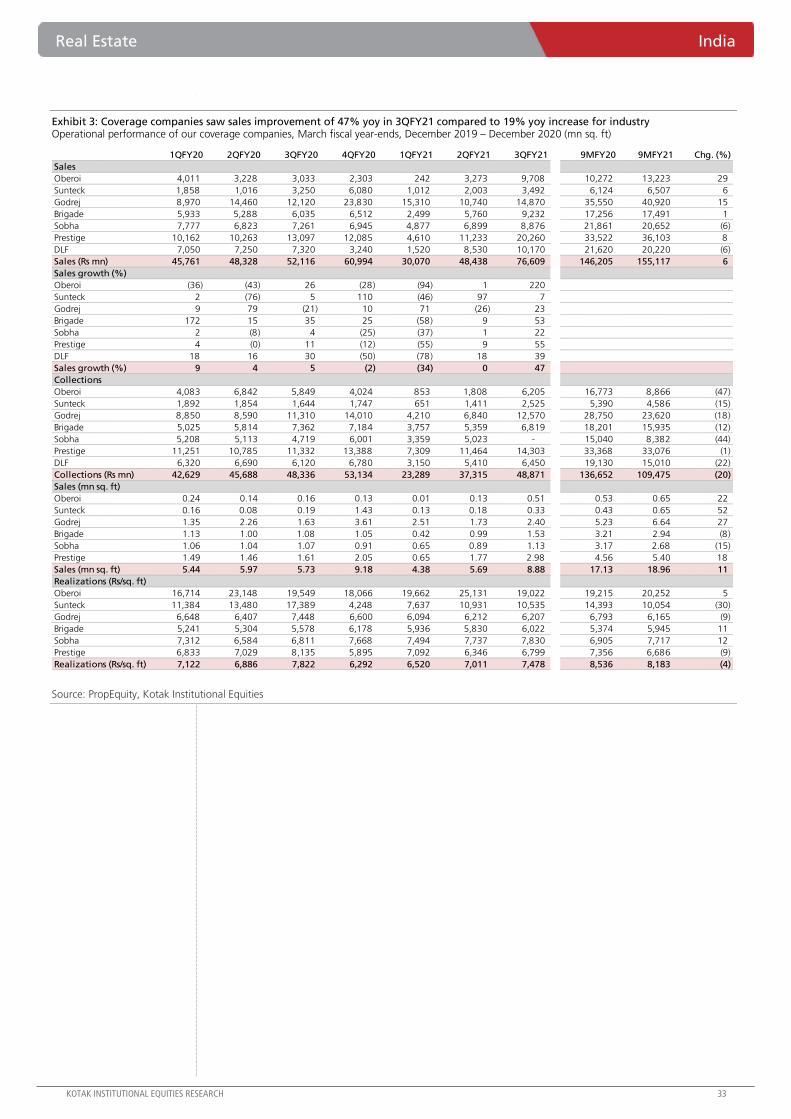

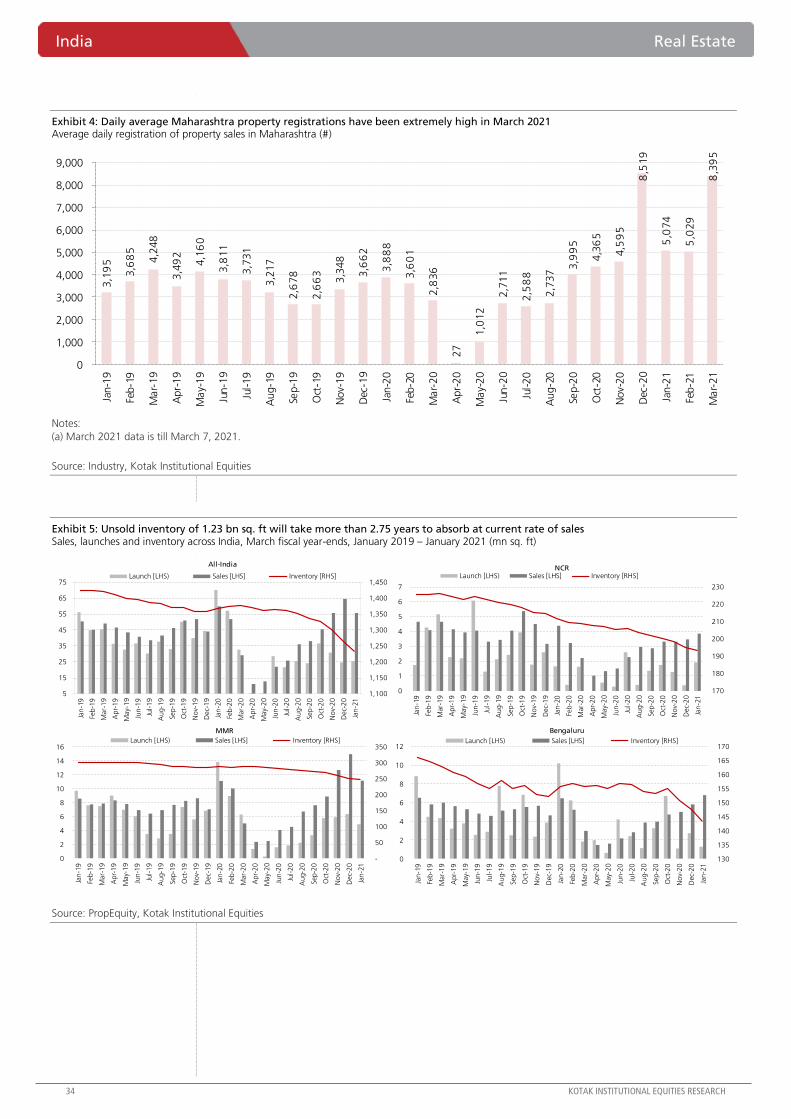

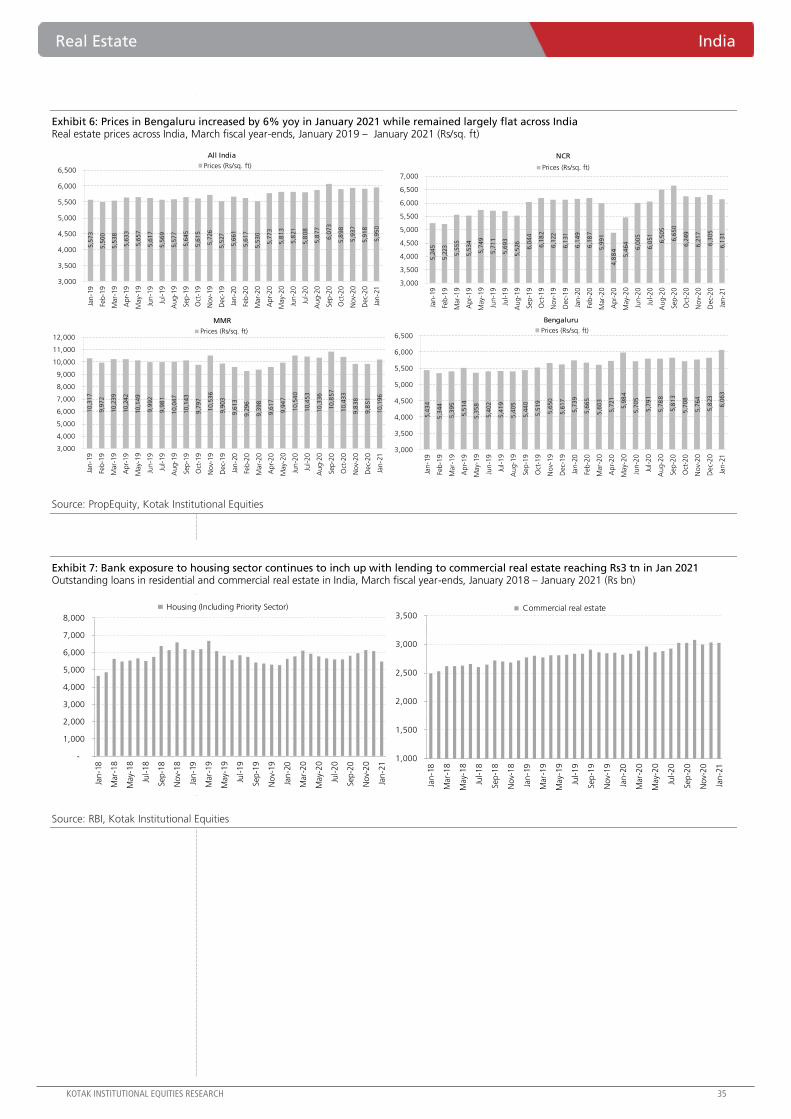

Real Estate: Real estate - state of the market

Strong sales, weak launches have led to faster absorption of outstanding

inventory

Listed players to continue to cheer; 4QFY21 likely to be exciting quarter

with planned launches

Favorable demand-supply dynamics make for a case of probable price

increases

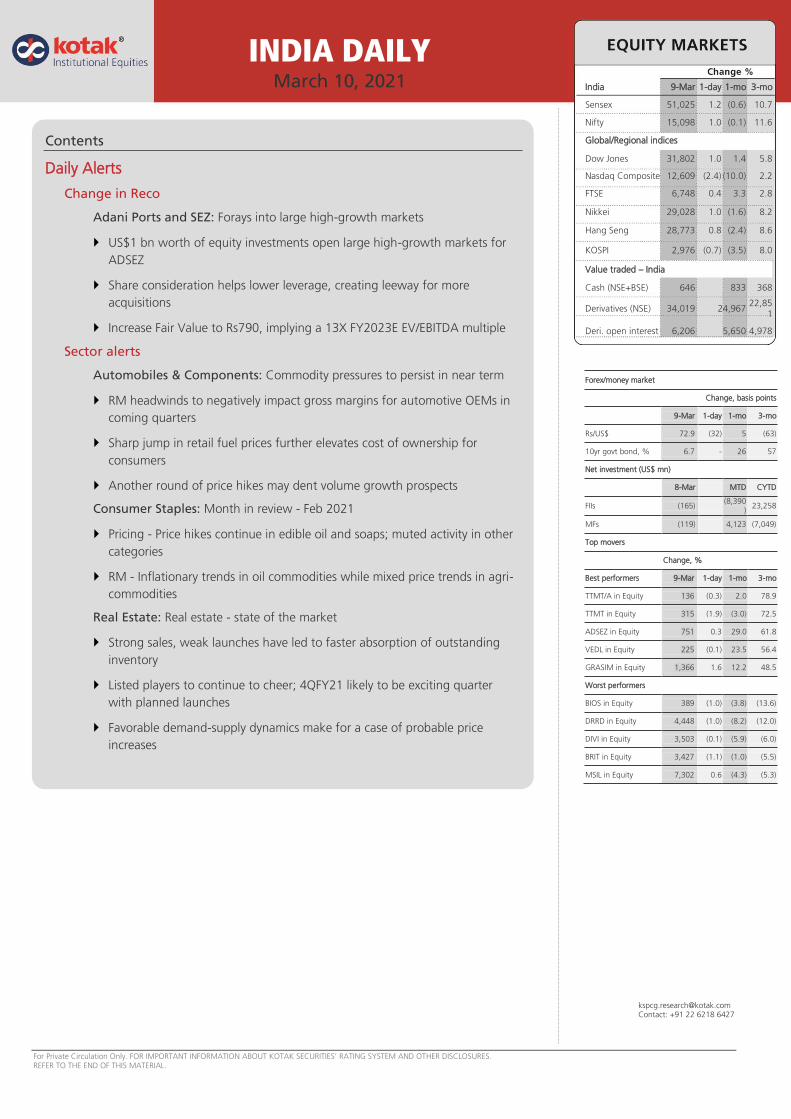

INDIA DAILY March 10, 2021 India 9-Mar 1-day 1-mo 3-mo

Sensex 51,025 1.2 (0.6) 10.7

Nifty 15,098 1.0 (0.1) 11.6

Global/Regional indices

Dow Jones 31,802 1.0 1.4 5.8

Nasdaq Composite 12,609 (2.4) (10.0) 2.2

FTSE 6,748 0.4 3.3 2.8

Nikkei 29,028 1.0 (1.6) 8.2

Hang Seng 28,773 0.8 (2.4) 8.6

KOSPI 2,976 (0.7) (3.5) 8.0

Value traded – India

Cash (NSE+BSE) 646 833 368

Derivatives (NSE) 34,019 24,967 22,85

1

Deri. open interest 6,206 5,650 4,978

Forex/money market

Change, basis points

9-Mar 1-day 1-mo 3-mo

Rs/US$ 72.9 (32) 5 (63)

10yr govt bond, % 6.7 - 26 57

Net investment (US$ mn)

8-Mar MTD CYTD

FIIs (165) (8,390

) 23,258

MFs (119) 4,123 (7,049)

Top movers

Change, %

Best performers 9-Mar 1-day 1-mo 3-mo

TTMT/A in Equity 136 (0.3) 2.0 78.9

TTMT in Equity 315 (1.9) (3.0) 72.5

ADSEZ in Equity 751 0.3 29.0 61.8

VEDL in Equity 225 (0.1) 23.5 56.4

GRASIM in Equity 1,366 1.6 12.2 48.5

Worst performers

BIOS in Equity 389 (1.0) (3.8) (13.6)

DRRD in Equity 4,448 (1.0) (8.2) (12.0)

DIVI in Equity 3,503 (0.1) (5.9) (6.0)

BRIT in Equity 3,427 (1.1) (1.0) (5.5)

MSIL in Equity 7,302 0.6 (4.3) (5.3)

[email protected]: +91 22 6218 6427

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

US$1 bn worth of equity investments open large high-growth markets for ADSEZ

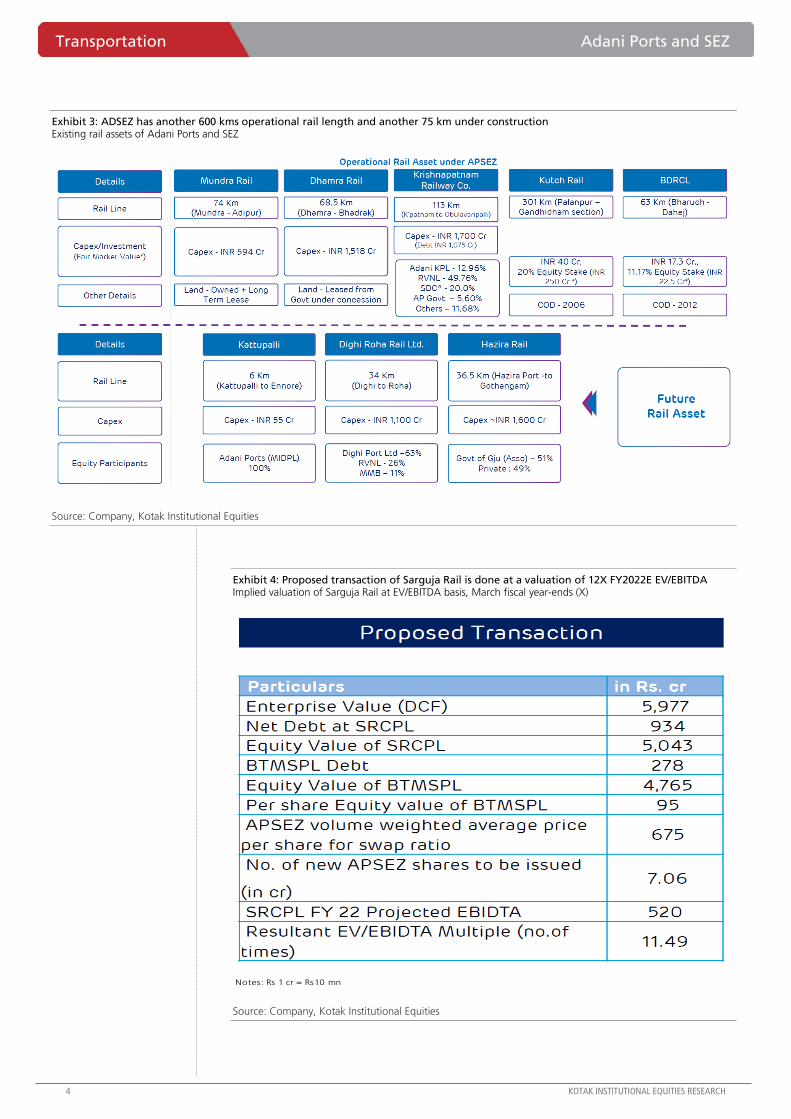

The Sarguja Rail acquisition (US$0.6 bn equity outgo) would help ADSEZ enter a 100 mn

ton market for coal transportation, 10X the current throughput of the asset. Incremental capex

for capacity expansion would be limited to setting loop lines, aiding expansion of business

returns. The Gangavaram Port acquisition (US$0.3 bn equity outgo) fortifies ADSEZ’s

positioning in the state of Andhra Pradesh. State volumes have grown at 10% CAGR over the

past three years with the port gaining share, growing volumes at 25% CAGR. The 250 mn ton

approved master plan equates to 7X of throughput of the port and 1.5X of the throughput of

the state. Dighi port acquisition (US$0.1 bn equity outgo) opens another 70 mn ton volume

market in Maharashtra beyond JNPT, ~7X of the capacity equivalent that ADSEZ paid for the asset.

Share consideration helps lower leverage, creating leeway for more acquisitions

A meaningful part of the equity outgo for the three acquisitions would get funded by equity

issuance to the promoter and Warburg Pincus (US$0.8 bn). The remaining equity commitment

would get paid back over a period of two years from the incremental cash profits. We envisage

ADSEZ’s consolidated net debt to EBITDA to move towards ~2X over FY2022/23. This creates

scope for further acquisitions – (1) acquiring promoter’s stake in Gangavaram Port (<0.4X

ADSEZ’s FY2022E EBITDA), (2) acquiring 56% stake in Concor (~1.5X ADSEZ’s FY2022E

EBITDA) and (3) acquiring stake in the west coast terminal (<0.4X ADSEZ’s FY2022E EBITDA).

On a separate note, we also note the hedge that the rail asset acquisition creates for the

thermal coal operations of ADSEZ’s port portfolio. Against the related ~100 mn ton of thermal

coal exposure, the Sarguja Rail acquisition opens a similar sized market for substitution by

domestic coal.

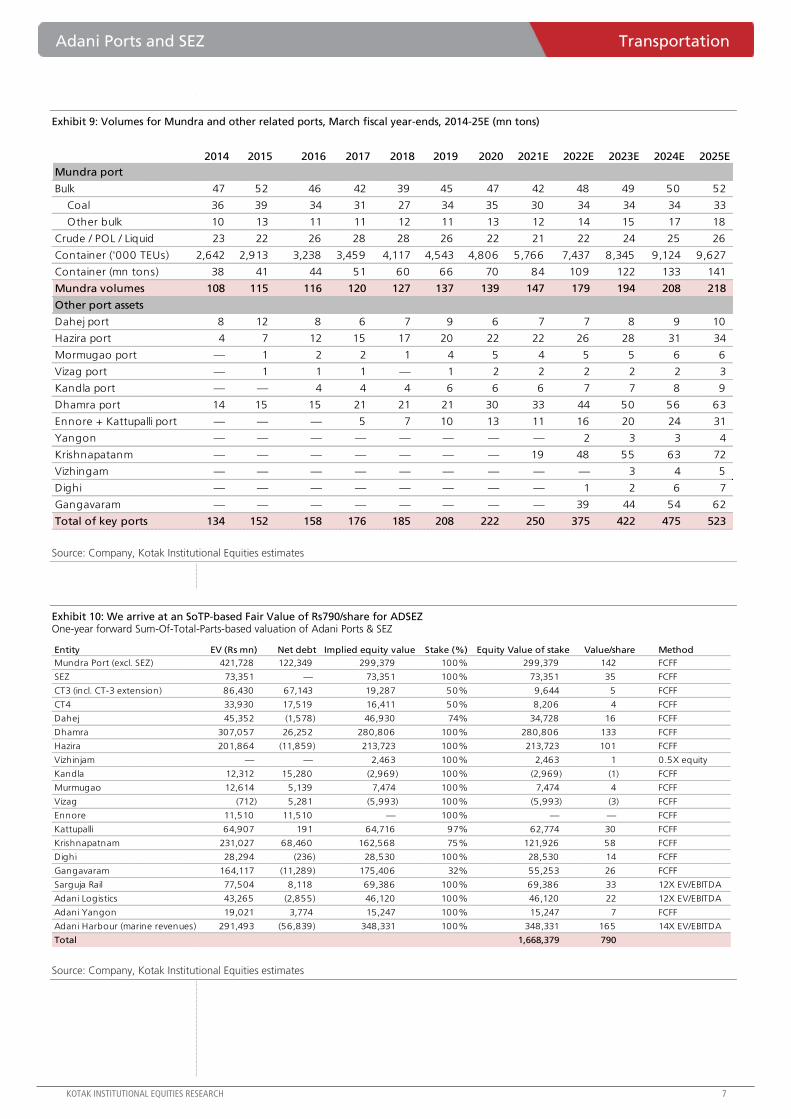

Increase Fair Value to Rs790, implying a 13X FY2023E EV/EBITDA multiple

We factor the three acquisitions into our estimates, yielding broadly unchanged EPS. We

increase our FV by ~21% on (1) latent value of the three acquisitions (7%), (2) higher medium-

term estimates for existing assets (6%), (3) lower CoE of 12.25% (4%) and (4) roll-forward to

June 2023 (3%). The implied 13X FY2023E EV/EBITDA multiple is in the middle of the 10-15X

historical one-year forward range.

https://ultraviewer.et/en/ownload.html

Adani Ports and SEZ (ADSEZ) Transportation

Forays into large high-growth markets. Recent acquisitions would open further

scope of investments in large high-growth markets, create space for ADSEZ to add

more assets over time and help lower its business risk profile. Our revised FV of Rs790

implies a 13X FY2023E EV/EBITDA multiple, factoring in the latent value of these

acquisitions, higher medium-term volume estimates for existing port assets and a lower

cost of equity. It, however, does not factor in the option value of further asset/stake

acquisitions that ADSEZ may bid for. We downgrade the stock to ADD (from BUY).

ADD

MARCH 09, 2021

CHANGE IN RECO.

Sector view: Attractive

CMP (`): 751

Fair Value (`): 790

BSE-30: 51,025

Aditya Mongia

Teena Virmani

Adani Ports and SEZ

Stock data Forecasts/valuations 2021E 2022E 2023E

CMP(Rs)/FV(Rs)/Rating 751/790/ADD EPS (Rs) 22.0 33.5 39.7

52-week range (Rs) (high-low) 768-203 EPS growth (%) (15.1) 52.3 18.7

Mcap (bn) (Rs/US$) 1,526/21 P/E (X) 34.2 22.4 18.9

ADTV-3M (mn) (Rs/US$) 6,449/88 P/B (X) 5.4 3.9 3.3

Shareholding pattern (%) EV/EBITDA (X) 21.8 14.5 12.0

Promoters 63.7 RoE (%) 16.9 20.1 18.8

FPIs/MFs/BFIs 17.7/3.9/11.7 Div. yield (%) 0.5 0.6 0.6

Price performance (%) 1M 3M 12M Sales (Rs bn) 128 181 207

Absolute 29.0 61.8 133.2 EBITDA (Rs bn) 83 122 141

Rel. to BSE-30 29.8 46.2 62.9 Net profits (Rs bn) 46 71 84

[email protected]: +91 22 6218 6427

Adani Ports and SEZ Transportation

KOTAK INSTITUTIONAL EQUITIES RESEARCH 3

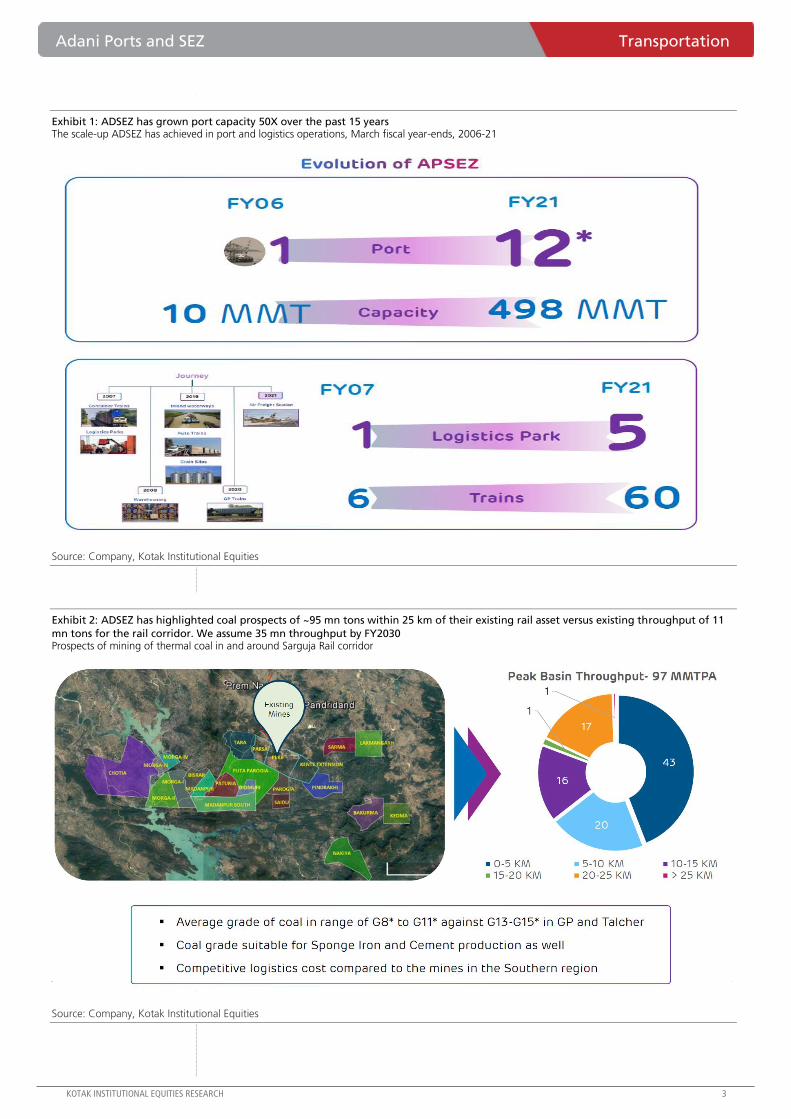

Exhibit 1: ADSEZ has grown port capacity 50X over the past 15 years The scale-up ADSEZ has achieved in port and logistics operations, March fiscal year-ends, 2006-21

Source: Company, Kotak Institutional Equities

Exhibit 2: ADSEZ has highlighted coal prospects of ~95 mn tons within 25 km of their existing rail asset versus existing throughput of 11

mn tons for the rail corridor. We assume 35 mn throughput by FY2030 Prospects of mining of thermal coal in and around Sarguja Rail corridor

Source: Company, Kotak Institutional Equities

Source: Company, Kotak Institutional Equities

Transportation Adani Ports and SEZ

4 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 3: ADSEZ has another 600 kms operational rail length and another 75 km under construction Existing rail assets of Adani Ports and SEZ

Source: Company, Kotak Institutional Equities

Exhibit 4: Proposed transaction of Sarguja Rail is done at a valuation of 12X FY2022E EV/EBITDA Implied valuation of Sarguja Rail at EV/EBITDA basis, March fiscal year-ends (X)

Source: Company, Kotak Institutional Equities

Notes: Rs 1 cr = Rs10 mn

Adani Ports and SEZ Transportation

KOTAK INSTITUTIONAL EQUITIES RESEARCH 5

Exhibit 5: Gangavaram Port outperformed AP ports with growth 2.5X of overall AP market growth

during 2017-20 Volumes from AP market and Gangavaram Port, March fiscal year-ends, 2016-25E (mn tons)

Source: Ministry of Shipping, Company, Kotak Institutional Equities

Exhibit 6: APSEZ is acquiring Gangavaram Port at attractive valuations of 9X FY2020 EV/EBITDA Implied valuation of Gangavaram Port at EV/EBITDA and P/E, March fiscal year-ends (X)

Source: Company, Kotak Institutional Equities

19 1826 30 35 32 39 44

5462

130 131

150 170 173159

184203

223245

0

5

10

15

20

25

30

0

50

100

150

200

250

300

2016 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025E

Gangavaram (mn tons) - LHS Andhra Pradesh (mn tons) - LHS

Gangavaram market share (%) - RHS

Notes: 1cr = 10 mn

Transportation Adani Ports and SEZ

6 KOTAK INSTITUTIONAL EQUITIES RESEARCH

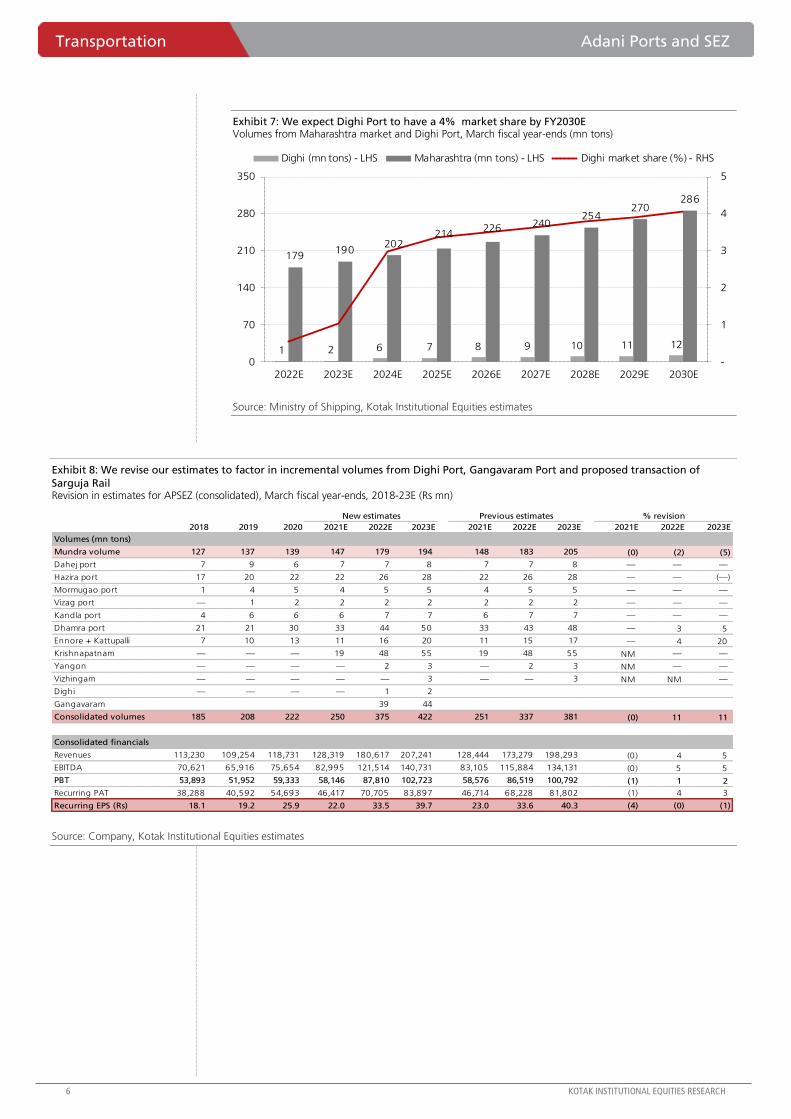

Exhibit 7: We expect Dighi Port to have a 4% market share by FY2030E Volumes from Maharashtra market and Dighi Port, March fiscal year-ends (mn tons)

Source: Ministry of Shipping, Kotak Institutional Equities estimates

Exhibit 8: We revise our estimates to factor in incremental volumes from Dighi Port, Gangavaram Port and proposed transaction of

Sarguja Rail Revision in estimates for APSEZ (consolidated), March fiscal year-ends, 2018-23E (Rs mn)

Source: Company, Kotak Institutional Equities estimates

1 2 6 7 8 9 10 11 12

179190

202214

226 240254

270286

-

1

2

3

4

5

0

70

140

210

280

350

2022E 2023E 2024E 2025E 2026E 2027E 2028E 2029E 2030E

Dighi (mn tons) - LHS Maharashtra (mn tons) - LHS Dighi market share (%) - RHS

2018 2019 2020 2021E 2022E 2023E 2021E 2022E 2023E 2021E 2022E 2023E

Volumes (mn tons)

Mundra volume 127 137 139 147 179 194 148 183 205 (0) (2) (5)

Dahej port 7 9 6 7 7 8 7 7 8 — — —

Hazira port 17 20 22 22 26 28 22 26 28 — — (—)

Mormugao port 1 4 5 4 5 5 4 5 5 — — —

Vizag port — 1 2 2 2 2 2 2 2 — — —

Kandla port 4 6 6 6 7 7 6 7 7 — — —

Dhamra port 21 21 30 33 44 50 33 43 48 — 3 5

Ennore + Kattupalli 7 10 13 11 16 20 11 15 17 — 4 20

Krishnapatnam — — — 19 48 55 19 48 55 NM — —

Yangon — — — — 2 3 — 2 3 NM — —

Vizhingam — — — — — 3 — — 3 NM NM —

Dighi — — — — 1 2

Gangavaram 39 44

Consolidated volumes 185 208 222 250 375 422 251 337 381 (0) 11 11

Consolidated financials

Revenues 113,230 109,254 118,731 128,319 180,617 207,241 128,444 173,279 198,293 (0) 4 5

EBITDA 70,621 65,916 75,654 82,995 121,514 140,731 83,105 115,884 134,131 (0) 5 5

PBT 53,893 51,952 59,333 58,146 87,810 102,723 58,576 86,519 100,792 (1) 1 2

Recurring PAT 38,288 40,592 54,693 46,417 70,705 83,897 46,714 68,228 81,802 (1) 4 3

Recurring EPS (Rs) 18.1 19.2 25.9 22.0 33.5 39.7 23.0 33.6 40.3 (4) (0) (1)

% revisionNew estimates Previous estimates

Adani Ports and SEZ Transportation

KOTAK INSTITUTIONAL EQUITIES RESEARCH 7

Exhibit 9: Volumes for Mundra and other related ports, March fiscal year-ends, 2014-25E (mn tons)

Source: Company, Kotak Institutional Equities estimates

Exhibit 10: We arrive at an SoTP-based Fair Value of Rs790/share for ADSEZ One-year forward Sum-Of-Total-Parts-based valuation of Adani Ports & SEZ

Source: Company, Kotak Institutional Equities estimates

2014 2015 2016 2017 2018 2019 2020 2021E 2022E 2023E 2024E 2025E

Mundra port

Bulk 47 52 46 42 39 45 47 42 48 49 50 52

Coal 36 39 34 31 27 34 35 30 34 34 34 33

Other bulk 10 13 11 11 12 11 13 12 14 15 17 18

Crude / POL / Liquid 23 22 26 28 28 26 22 21 22 24 25 26

Container ('000 TEUs) 2,642 2,913 3,238 3,459 4,117 4,543 4,806 5,766 7,437 8,345 9,124 9,627

Container (mn tons) 38 41 44 51 60 66 70 84 109 122 133 141

Mundra volumes 108 115 116 120 127 137 139 147 179 194 208 218

Other port assets

Dahej port 8 12 8 6 7 9 6 7 7 8 9 10

Hazira port 4 7 12 15 17 20 22 22 26 28 31 34

Mormugao port — 1 2 2 1 4 5 4 5 5 6 6

Vizag port — 1 1 1 — 1 2 2 2 2 2 3

Kandla port — — 4 4 4 6 6 6 7 7 8 9

Dhamra port 14 15 15 21 21 21 30 33 44 50 56 63

Ennore + Kattupalli port — — — 5 7 10 13 11 16 20 24 31

Yangon — — — — — — — — 2 3 3 4

Krishnapatanm — — — — — — — 19 48 55 63 72

Vizhingam — — — — — — — — — 3 4 5

Dighi — — — — — — — — 1 2 6 7

Gangavaram — — — — — — — — 39 44 54 62

Total of key ports 134 152 158 176 185 208 222 250 375 422 475 523

Entity EV (Rs mn) Net debt Implied equity value Stake (%) Equity Value of stake Value/share Method

Mundra Port (excl. SEZ) 421,728 122,349 299,379 100% 299,379 142 FCFF

SEZ 73,351 — 73,351 100% 73,351 35 FCFF

CT3 (incl. CT-3 extension) 86,430 67,143 19,287 50% 9,644 5 FCFF

CT4 33,930 17,519 16,411 50% 8,206 4 FCFF

Dahej 45,352 (1,578) 46,930 74% 34,728 16 FCFF

Dhamra 307,057 26,252 280,806 100% 280,806 133 FCFF

Hazira 201,864 (11,859) 213,723 100% 213,723 101 FCFF

Vizhinjam — — 2,463 100% 2,463 1 0.5X equity

Kandla 12,312 15,280 (2,969) 100% (2,969) (1) FCFF

Murmugao 12,614 5,139 7,474 100% 7,474 4 FCFF

Vizag (712) 5,281 (5,993) 100% (5,993) (3) FCFF

Ennore 11,510 11,510 — 100% — — FCFF

Kattupalli 64,907 191 64,716 97% 62,774 30 FCFF

Krishnapatnam 231,027 68,460 162,568 75% 121,926 58 FCFF

Dighi 28,294 (236) 28,530 100% 28,530 14 FCFF

Gangavaram 164,117 (11,289) 175,406 32% 55,253 26 FCFF

Sarguja Rail 77,504 8,118 69,386 100% 69,386 33 12X EV/EBITDA

Adani Logistics 43,265 (2,855) 46,120 100% 46,120 22 12X EV/EBITDA

Adani Yangon 19,021 3,774 15,247 100% 15,247 7 FCFF

Adani Harbour (marine revenues) 291,493 (56,839) 348,331 100% 348,331 165 14X EV/EBITDA

Total 1,668,379 790

Transportation Adani Ports and SEZ

8 KOTAK INSTITUTIONAL EQUITIES RESEARCH

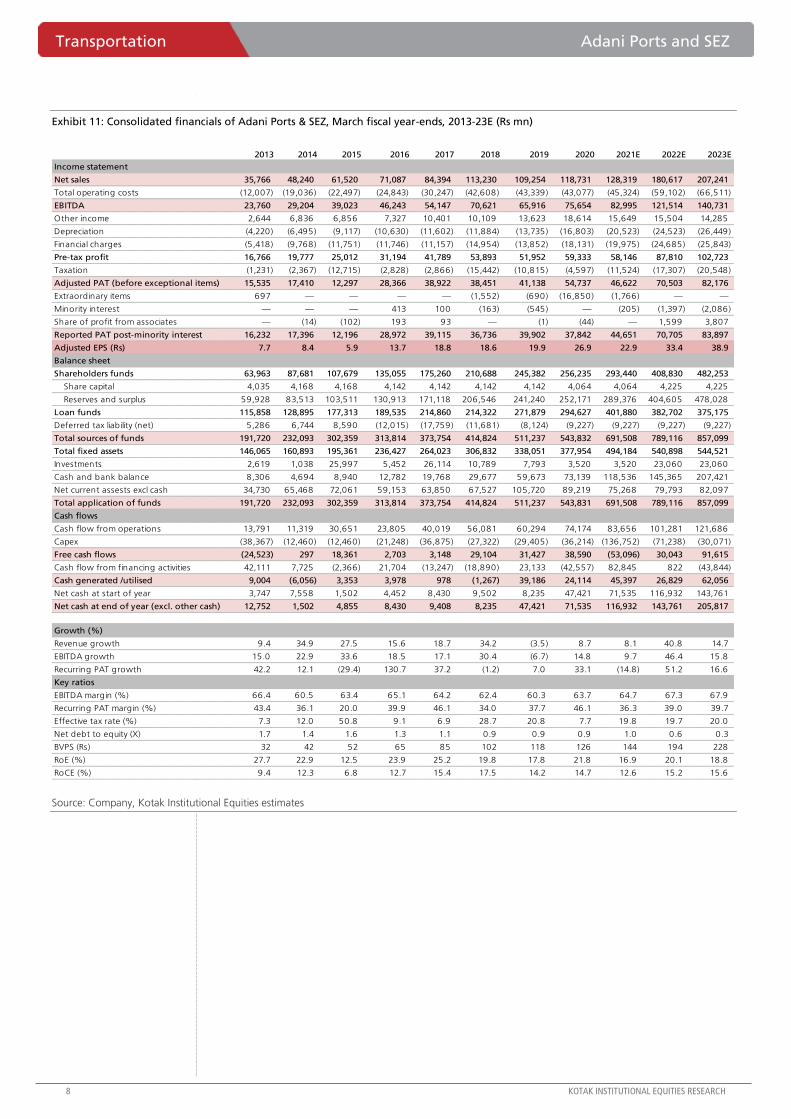

Exhibit 11: Consolidated financials of Adani Ports & SEZ, March fiscal year-ends, 2013-23E (Rs mn)

Source: Company, Kotak Institutional Equities estimates

2013 2014 2015 2016 2017 2018 2019 2020 2021E 2022E 2023E

Income statement

Net sales 35,766 48,240 61,520 71,087 84,394 113,230 109,254 118,731 128,319 180,617 207,241

Total operating costs (12,007) (19,036) (22,497) (24,843) (30,247) (42,608) (43,339) (43,077) (45,324) (59,102) (66,511)

EBITDA 23,760 29,204 39,023 46,243 54,147 70,621 65,916 75,654 82,995 121,514 140,731

Other income 2,644 6,836 6,856 7,327 10,401 10,109 13,623 18,614 15,649 15,504 14,285

Depreciation (4,220) (6,495) (9,117) (10,630) (11,602) (11,884) (13,735) (16,803) (20,523) (24,523) (26,449)

Financial charges (5,418) (9,768) (11,751) (11,746) (11,157) (14,954) (13,852) (18,131) (19,975) (24,685) (25,843)

Pre-tax profit 16,766 19,777 25,012 31,194 41,789 53,893 51,952 59,333 58,146 87,810 102,723

Taxation (1,231) (2,367) (12,715) (2,828) (2,866) (15,442) (10,815) (4,597) (11,524) (17,307) (20,548)

Adjusted PAT (before exceptional items) 15,535 17,410 12,297 28,366 38,922 38,451 41,138 54,737 46,622 70,503 82,176

Extraordinary items 697 — — — — (1,552) (690) (16,850) (1,766) — —

Minority interest — — — 413 100 (163) (545) — (205) (1,397) (2,086)

Share of profit from associates — (14) (102) 193 93 — (1) (44) — 1,599 3,807

Reported PAT post-minority interest 16,232 17,396 12,196 28,972 39,115 36,736 39,902 37,842 44,651 70,705 83,897

Adjusted EPS (Rs) 7.7 8.4 5.9 13.7 18.8 18.6 19.9 26.9 22.9 33.4 38.9

Balance sheet

Shareholders funds 63,963 87,681 107,679 135,055 175,260 210,688 245,382 256,235 293,440 408,830 482,253

Share capital 4,035 4,168 4,168 4,142 4,142 4,142 4,142 4,064 4,064 4,225 4,225

Reserves and surplus 59,928 83,513 103,511 130,913 171,118 206,546 241,240 252,171 289,376 404,605 478,028

Loan funds 115,858 128,895 177,313 189,535 214,860 214,322 271,879 294,627 401,880 382,702 375,175

Deferred tax liability (net) 5,286 6,744 8,590 (12,015) (17,759) (11,681) (8,124) (9,227) (9,227) (9,227) (9,227)

Total sources of funds 191,720 232,093 302,359 313,814 373,754 414,824 511,237 543,832 691,508 789,116 857,099

Total fixed assets 146,065 160,893 195,361 236,427 264,023 306,832 338,051 377,954 494,184 540,898 544,521

Investments 2,619 1,038 25,997 5,452 26,114 10,789 7,793 3,520 3,520 23,060 23,060

Cash and bank balance 8,306 4,694 8,940 12,782 19,768 29,677 59,673 73,139 118,536 145,365 207,421

Net current assests excl cash 34,730 65,468 72,061 59,153 63,850 67,527 105,720 89,219 75,268 79,793 82,097

Total application of funds 191,720 232,093 302,359 313,814 373,754 414,824 511,237 543,831 691,508 789,116 857,099

Cash flows

Cash flow from operations 13,791 11,319 30,651 23,805 40,019 56,081 60,294 74,174 83,656 101,281 121,686

Capex (38,367) (12,460) (12,460) (21,248) (36,875) (27,322) (29,405) (36,214) (136,752) (71,238) (30,071)

Free cash flows (24,523) 297 18,361 2,703 3,148 29,104 31,427 38,590 (53,096) 30,043 91,615

Cash flow from financing activities 42,111 7,725 (2,366) 21,704 (13,247) (18,890) 23,133 (42,557) 82,845 822 (43,844)

Cash generated /utilised 9,004 (6,056) 3,353 3,978 978 (1,267) 39,186 24,114 45,397 26,829 62,056

Net cash at start of year 3,747 7,558 1,502 4,452 8,430 9,502 8,235 47,421 71,535 116,932 143,761

Net cash at end of year (excl. other cash) 12,752 1,502 4,855 8,430 9,408 8,235 47,421 71,535 116,932 143,761 205,817

Growth (%)

Revenue growth 9.4 34.9 27.5 15.6 18.7 34.2 (3.5) 8.7 8.1 40.8 14.7

EBITDA growth 15.0 22.9 33.6 18.5 17.1 30.4 (6.7) 14.8 9.7 46.4 15.8

Recurring PAT growth 42.2 12.1 (29.4) 130.7 37.2 (1.2) 7.0 33.1 (14.8) 51.2 16.6

Key ratios

EBITDA margin (%) 66.4 60.5 63.4 65.1 64.2 62.4 60.3 63.7 64.7 67.3 67.9

Recurring PAT margin (%) 43.4 36.1 20.0 39.9 46.1 34.0 37.7 46.1 36.3 39.0 39.7

Effective tax rate (%) 7.3 12.0 50.8 9.1 6.9 28.7 20.8 7.7 19.8 19.7 20.0

Net debt to equity (X) 1.7 1.4 1.6 1.3 1.1 0.9 0.9 0.9 1.0 0.6 0.3

BVPS (Rs) 32 42 52 65 85 102 118 126 144 194 228

RoE (%) 27.7 22.9 12.5 23.9 25.2 19.8 17.8 21.8 16.9 20.1 18.8

RoCE (%) 9.4 12.3 6.8 12.7 15.4 17.5 14.2 14.7 12.6 15.2 15.6

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

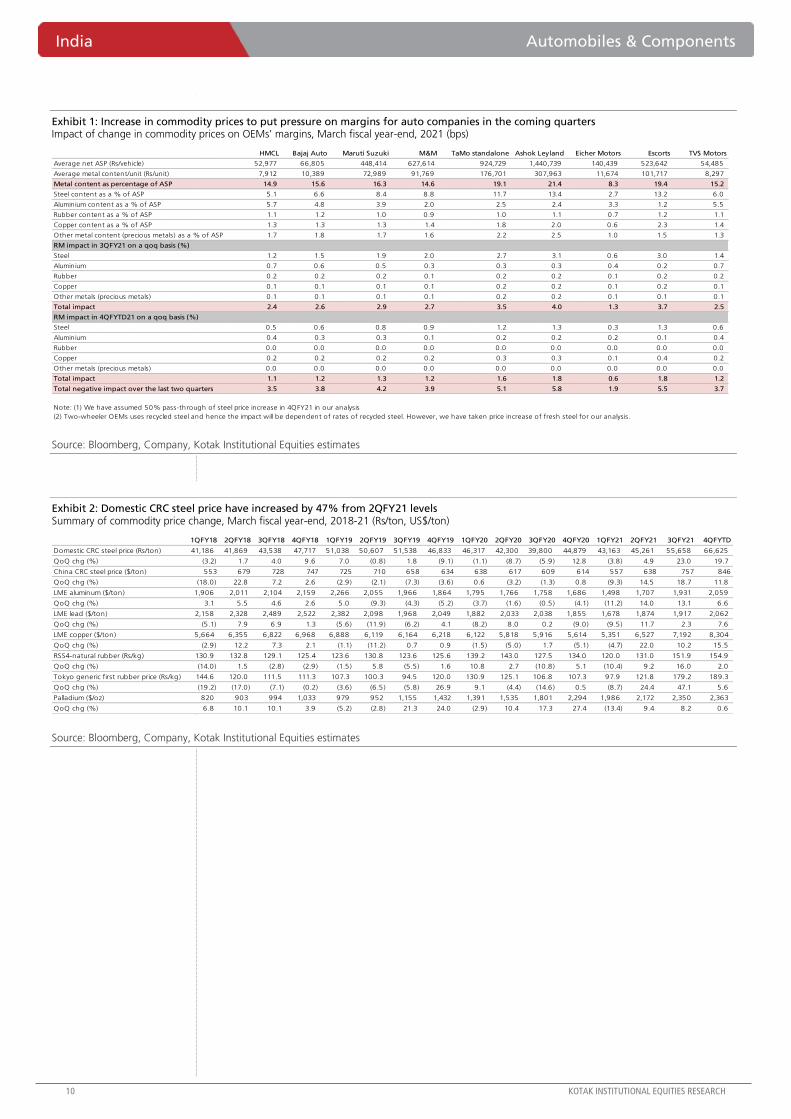

RM headwinds to negatively impact gross margins for automotive OEMs in coming quarters

As per our analysis, automotive OEMs’ RM basket prices have increased by 190-580 bps from

2QFY21 levels over the past two quarters due to the sharp jump in commodity prices (Exhibit 1).

Steel and copper prices have increased by 54-55% from 1QFY21 levels whereas aluminum and

lead prices have increased by 23-37% in the same period. Also, precious metal prices have

more than doubled from FY2019 levels given the shift towards the BS-VI regime, which has

increased the demand for these metals. International rubber prices have increased by 93% from

1QFY21 levels led by (1) strong recovery in Chinese demand (China accounts for 43% of the

global NR demand) and (2) production-related issues. As per ANRPC, global rubber production

declined by 9% yoy in CY2020 due to (1) floods in South East Asia which resulted in a fungal

disease that causes abnormal fall in leaves and (2) production in Thailand has been affected due

to Covid-related travel restrictions, which has prevented tappers from Laos and Myanmar going

to Thailand’s rubber plantations (Exhibit 2). As a result, we expect RM basket prices to go up by

190-380 bps for two-wheeler OEMs (HMCL, Bajaj Auto, Eicher Motors and TVS Motor) from

2QFY21 levels.

We expect 390-430 bps price increase in the RM basket for M&M and Maruti Suzuki (assuming

only 50% of the steel price increase will get passed through during 4QFY21). Also, we expect

Tata Motors, Ashok Leyland and Escorts RM basket prices to go up by 510-580 bps from

2QFY21 levels. In order to mitigate this impact, OEMs have taken price hikes in the range of

1.5-4% over the past two quarters (Exhibit 3). However, we believe this will not completely

offset the impact of commodity inflation and expect gross margins of automotive

OEMs (except Royal Enfield) to get negatively impacted during 4QFY21 by 50-400 bps.

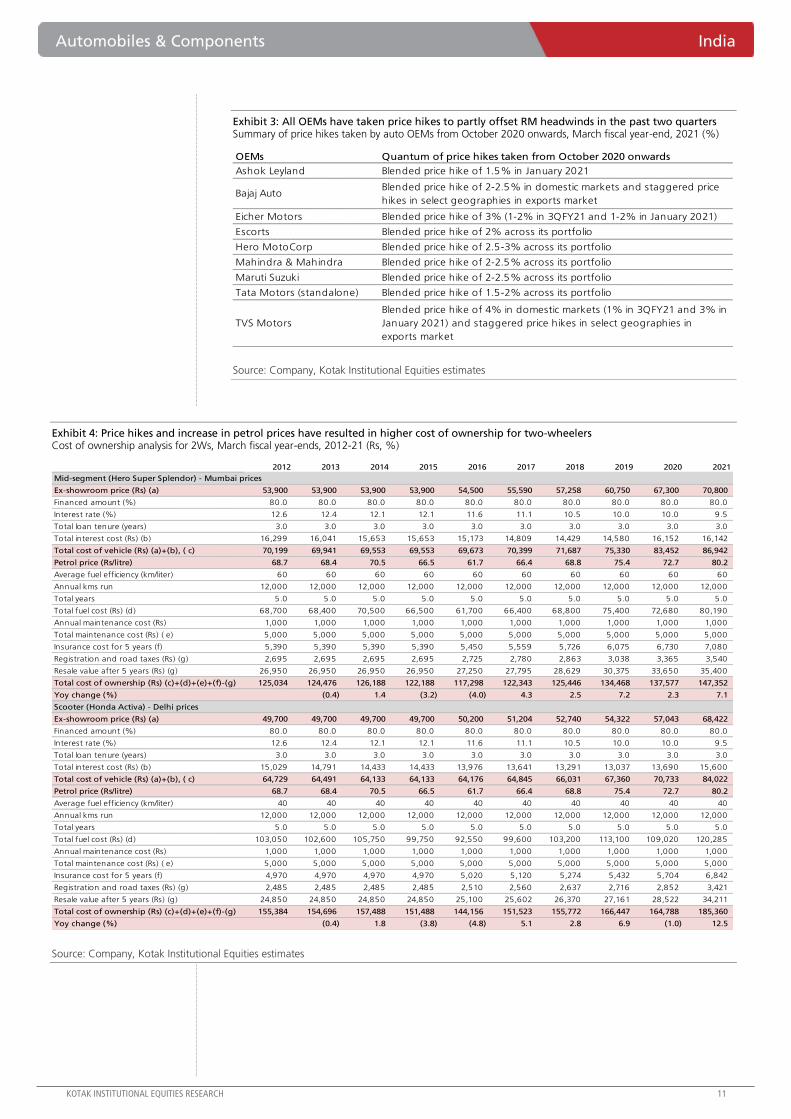

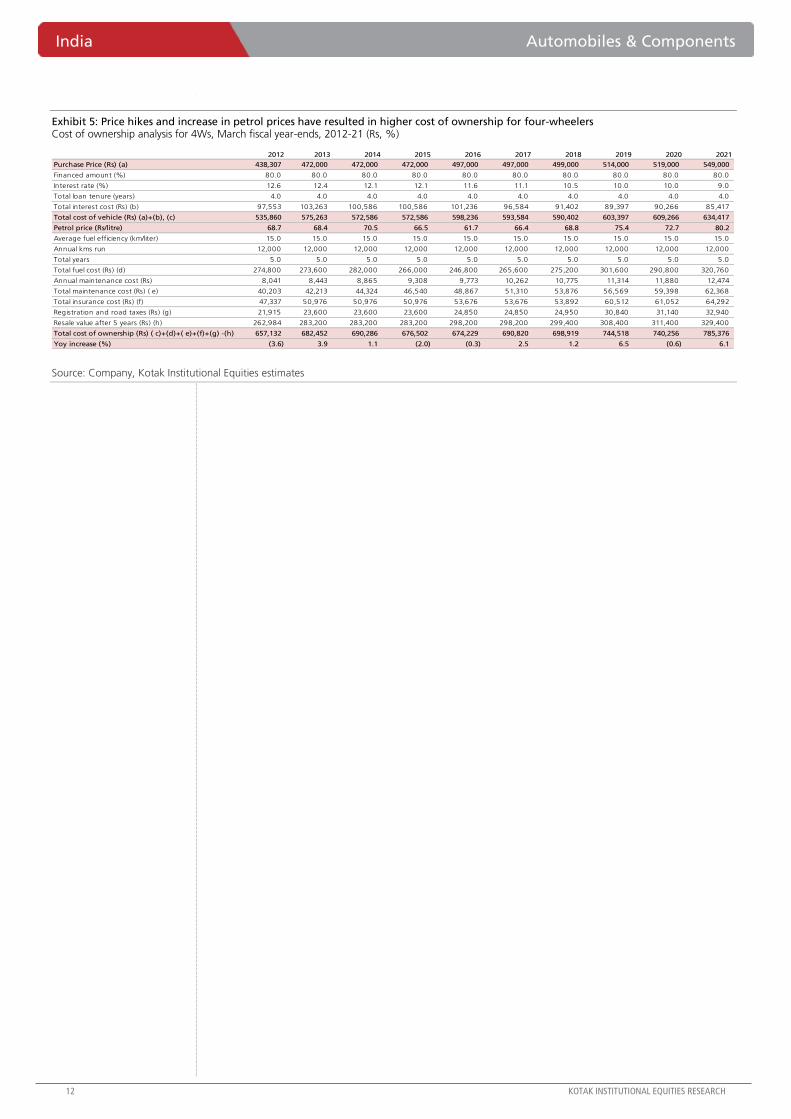

Sharp jump in retail fuel prices further elevates cost of ownership for consumers

The cost of ownership for consumers has sharply increased over the past two years led by (1) 8-

15% price increase due to the BS-VI transition, (2) price hikes taken by OEMs to offset RM

headwinds during FY2021E and (3) the recent surge in retail fuel prices. As a result, total cost of

ownership for two-wheeler consumers has increased by 7-13% on a yoy basis whereas total

cost of ownership for PV consumers has increased by 6% on a yoy basis in FY2021 (Exhibits 4-

5) assuming average petrol price of Rs80.2/liter in FY2021. If we assume current retail price of

petrol at around ~Rs90-91/liter, total cost of ownership for two-wheeler consumers will increase

by 14-21% yoy whereas total cost of ownership for PV consumers will increase by 11% yoy.

Another round of price hikes may dent volume growth prospects

Overall, we expect automotive OEMs’ (except Royal Enfield) gross margins to decline by 50-400

bps on a qoq basis in 4QFY21 mainly due to increase in commodity prices, partly offset by price

hikes taken by the OEMs. OEMs will have to take further price increase to completely offset RM

headwinds. However, we are already witnessing signs of slowdown in domestic 2W demand

due to sharp increase in cost of ownership.

Automobiles & Components India

Commodity pressures to persist in near term. We expect gross margins of

automotive OEMs to remain under pressure in the coming quarters given sharp increase

in commodity prices. Automotive OEMs have taken price hikes to partly offset the

impact of RM headwinds. We except gross margins of TVS Motor and Royal Enfield to

get least impacted sequentially whereas gross margins of CV players (Tata Motors and

Ashok Leyland) and Escorts may decline by 300-400 bps on a qoq basis in 4QFY21.

CAUTIOUS

MARCH 09, 2021

UPDATE

BSE-30: 51,025

Hitesh Goel

Rishi Vora

[email protected]: +91 22 6218 6427

India Automobiles & Components

10 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 1: Increase in commodity prices to put pressure on margins for auto companies in the coming quarters Impact of change in commodity prices on OEMs’ margins, March fiscal year-end, 2021 (bps)

Source: Bloomberg, Company, Kotak Institutional Equities estimates

Exhibit 2: Domestic CRC steel price have increased by 47% from 2QFY21 levels Summary of commodity price change, March fiscal year-end, 2018-21 (Rs/ton, US$/ton)

Source: Bloomberg, Company, Kotak Institutional Equities estimates

HMCL Bajaj Auto Maruti Suzuki M&M TaMo standalone Ashok Leyland Eicher Motors Escorts TVS Motors

Average net ASP (Rs/vehicle) 52,977 66,805 448,414 627,614 924,729 1,440,739 140,439 523,642 54,485

Average metal content/unit (Rs/unit) 7,912 10,389 72,989 91,769 176,701 307,963 11,674 101,717 8,297

Metal content as percentage of ASP 14.9 15.6 16.3 14.6 19.1 21.4 8.3 19.4 15.2

Steel content as a % of ASP 5.1 6.6 8.4 8.8 11.7 13.4 2.7 13.2 6.0

Aluminium content as a % of ASP 5.7 4.8 3.9 2.0 2.5 2.4 3.3 1.2 5.5

Rubber content as a % of ASP 1.1 1.2 1.0 0.9 1.0 1.1 0.7 1.2 1.1

Copper content as a % of ASP 1.3 1.3 1.3 1.4 1.8 2.0 0.6 2.3 1.4

Other metal content (precious metals) as a % of ASP 1.7 1.8 1.7 1.6 2.2 2.5 1.0 1.5 1.3

RM impact in 3QFY21 on a qoq basis (%)

Steel 1.2 1.5 1.9 2.0 2.7 3.1 0.6 3.0 1.4

Aluminium 0.7 0.6 0.5 0.3 0.3 0.3 0.4 0.2 0.7

Rubber 0.2 0.2 0.2 0.1 0.2 0.2 0.1 0.2 0.2

Copper 0.1 0.1 0.1 0.1 0.2 0.2 0.1 0.2 0.1

Other metals (precious metals) 0.1 0.1 0.1 0.1 0.2 0.2 0.1 0.1 0.1

Total impact 2.4 2.6 2.9 2.7 3.5 4.0 1.3 3.7 2.5

RM impact in 4QFYTD21 on a qoq basis (%)

Steel 0.5 0.6 0.8 0.9 1.2 1.3 0.3 1.3 0.6

Aluminium 0.4 0.3 0.3 0.1 0.2 0.2 0.2 0.1 0.4

Rubber 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Copper 0.2 0.2 0.2 0.2 0.3 0.3 0.1 0.4 0.2

Other metals (precious metals) 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Total impact 1.1 1.2 1.3 1.2 1.6 1.8 0.6 1.8 1.2

Total negative impact over the last two quarters 3.5 3.8 4.2 3.9 5.1 5.8 1.9 5.5 3.7

Note: (1) We have assumed 50% pass-through of steel price increase in 4QFY21 in our analysis

(2) Two-wheeler OEMs uses recycled steel and hence the impact will be dependent of rates of recycled steel. However, we have taken price increase of fresh steel for our analysis.

1QFY18 2QFY18 3QFY18 4QFY18 1QFY19 2QFY19 3QFY19 4QFY19 1QFY20 2QFY20 3QFY20 4QFY20 1QFY21 2QFY21 3QFY21 4QFYTD

Domestic CRC steel price (Rs/ton) 41,186 41,869 43,538 47,717 51,038 50,607 51,538 46,833 46,317 42,300 39,800 44,879 43,163 45,261 55,658 66,625

QoQ chg (%) (3.2) 1.7 4.0 9.6 7.0 (0.8) 1.8 (9.1) (1.1) (8.7) (5.9) 12.8 (3.8) 4.9 23.0 19.7

China CRC steel price ($/ton) 553 679 728 747 725 710 658 634 638 617 609 614 557 638 757 846

QoQ chg (%) (18.0) 22.8 7.2 2.6 (2.9) (2.1) (7.3) (3.6) 0.6 (3.2) (1.3) 0.8 (9.3) 14.5 18.7 11.8

LME aluminum ($/ton) 1,906 2,011 2,104 2,159 2,266 2,055 1,966 1,864 1,795 1,766 1,758 1,686 1,498 1,707 1,931 2,059

QoQ chg (%) 3.1 5.5 4.6 2.6 5.0 (9.3) (4.3) (5.2) (3.7) (1.6) (0.5) (4.1) (11.2) 14.0 13.1 6.6

LME lead ($/ton) 2,158 2,328 2,489 2,522 2,382 2,098 1,968 2,049 1,882 2,033 2,038 1,855 1,678 1,874 1,917 2,062

QoQ chg (%) (5.1) 7.9 6.9 1.3 (5.6) (11.9) (6.2) 4.1 (8.2) 8.0 0.2 (9.0) (9.5) 11.7 2.3 7.6

LME copper ($/ton) 5,664 6,355 6,822 6,968 6,888 6,119 6,164 6,218 6,122 5,818 5,916 5,614 5,351 6,527 7,192 8,304

QoQ chg (%) (2.9) 12.2 7.3 2.1 (1.1) (11.2) 0.7 0.9 (1.5) (5.0) 1.7 (5.1) (4.7) 22.0 10.2 15.5

RSS4-natural rubber (Rs/kg) 130.9 132.8 129.1 125.4 123.6 130.8 123.6 125.6 139.2 143.0 127.5 134.0 120.0 131.0 151.9 154.9

QoQ chg (%) (14.0) 1.5 (2.8) (2.9) (1.5) 5.8 (5.5) 1.6 10.8 2.7 (10.8) 5.1 (10.4) 9.2 16.0 2.0

Tokyo generic first rubber price (Rs/kg) 144.6 120.0 111.5 111.3 107.3 100.3 94.5 120.0 130.9 125.1 106.8 107.3 97.9 121.8 179.2 189.3

QoQ chg (%) (19.2) (17.0) (7.1) (0.2) (3.6) (6.5) (5.8) 26.9 9.1 (4.4) (14.6) 0.5 (8.7) 24.4 47.1 5.6

Palladium ($/oz) 820 903 994 1,033 979 952 1,155 1,432 1,391 1,535 1,801 2,294 1,986 2,172 2,350 2,363

QoQ chg (%) 6.8 10.1 10.1 3.9 (5.2) (2.8) 21.3 24.0 (2.9) 10.4 17.3 27.4 (13.4) 9.4 8.2 0.6

Automobiles & Components India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 11

Exhibit 3: All OEMs have taken price hikes to partly offset RM headwinds in the past two quarters Summary of price hikes taken by auto OEMs from October 2020 onwards, March fiscal year-end, 2021 (%)

Source: Company, Kotak Institutional Equities estimates

Exhibit 4: Price hikes and increase in petrol prices have resulted in higher cost of ownership for two-wheelers Cost of ownership analysis for 2Ws, March fiscal year-ends, 2012-21 (Rs, %)

Source: Company, Kotak Institutional Equities estimates

OEMs Quantum of price hikes taken from October 2020 onwards

Ashok Leyland Blended price hike of 1.5% in January 2021

Bajaj AutoBlended price hike of 2-2.5% in domestic markets and staggered price

hikes in select geographies in exports market

Eicher Motors Blended price hike of 3% (1-2% in 3QFY21 and 1-2% in January 2021)

Escorts Blended price hike of 2% across its portfolio

Hero MotoCorp Blended price hike of 2.5-3% across its portfolio

Mahindra & Mahindra Blended price hike of 2-2.5% across its portfolio

Maruti Suzuki Blended price hike of 2-2.5% across its portfolio

Tata Motors (standalone) Blended price hike of 1.5-2% across its portfolio

TVS Motors

Blended price hike of 4% in domestic markets (1% in 3QFY21 and 3% in

January 2021) and staggered price hikes in select geographies in

exports market

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Mid-segment (Hero Super Splendor) - Mumbai prices

Ex-showroom price (Rs) (a) 53,900 53,900 53,900 53,900 54,500 55,590 57,258 60,750 67,300 70,800

Financed amount (%) 80.0 80.0 80.0 80.0 80.0 80.0 80.0 80.0 80.0 80.0

Interest rate (%) 12.6 12.4 12.1 12.1 11.6 11.1 10.5 10.0 10.0 9.5

Total loan tenure (years) 3.0 3.0 3.0 3.0 3.0 3.0 3.0 3.0 3.0 3.0

Total interest cost (Rs) (b) 16,299 16,041 15,653 15,653 15,173 14,809 14,429 14,580 16,152 16,142

Total cost of vehicle (Rs) (a)+(b), ( c) 70,199 69,941 69,553 69,553 69,673 70,399 71,687 75,330 83,452 86,942

Petrol price (Rs/litre) 68.7 68.4 70.5 66.5 61.7 66.4 68.8 75.4 72.7 80.2

Average fuel efficiency (km/liter) 60 60 60 60 60 60 60 60 60 60

Annual kms run 12,000 12,000 12,000 12,000 12,000 12,000 12,000 12,000 12,000 12,000

Total years 5.0 5.0 5.0 5.0 5.0 5.0 5.0 5.0 5.0 5.0

Total fuel cost (Rs) (d) 68,700 68,400 70,500 66,500 61,700 66,400 68,800 75,400 72,680 80,190

Annual maintenance cost (Rs) 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000

Total maintenance cost (Rs) ( e) 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000

Insurance cost for 5 years (f) 5,390 5,390 5,390 5,390 5,450 5,559 5,726 6,075 6,730 7,080

Registration and road taxes (Rs) (g) 2,695 2,695 2,695 2,695 2,725 2,780 2,863 3,038 3,365 3,540

Resale value after 5 years (Rs) (g) 26,950 26,950 26,950 26,950 27,250 27,795 28,629 30,375 33,650 35,400

Total cost of ownership (Rs) (c)+(d)+(e)+(f)-(g) 125,034 124,476 126,188 122,188 117,298 122,343 125,446 134,468 137,577 147,352

Yoy change (%) (0.4) 1.4 (3.2) (4.0) 4.3 2.5 7.2 2.3 7.1

Scooter (Honda Activa) - Delhi prices

Ex-showroom price (Rs) (a) 49,700 49,700 49,700 49,700 50,200 51,204 52,740 54,322 57,043 68,422

Financed amount (%) 80.0 80.0 80.0 80.0 80.0 80.0 80.0 80.0 80.0 80.0

Interest rate (%) 12.6 12.4 12.1 12.1 11.6 11.1 10.5 10.0 10.0 9.5

Total loan tenure (years) 3.0 3.0 3.0 3.0 3.0 3.0 3.0 3.0 3.0 3.0

Total interest cost (Rs) (b) 15,029 14,791 14,433 14,433 13,976 13,641 13,291 13,037 13,690 15,600

Total cost of vehicle (Rs) (a)+(b), ( c) 64,729 64,491 64,133 64,133 64,176 64,845 66,031 67,360 70,733 84,022

Petrol price (Rs/litre) 68.7 68.4 70.5 66.5 61.7 66.4 68.8 75.4 72.7 80.2

Average fuel efficiency (km/liter) 40 40 40 40 40 40 40 40 40 40

Annual kms run 12,000 12,000 12,000 12,000 12,000 12,000 12,000 12,000 12,000 12,000

Total years 5.0 5.0 5.0 5.0 5.0 5.0 5.0 5.0 5.0 5.0

Total fuel cost (Rs) (d) 103,050 102,600 105,750 99,750 92,550 99,600 103,200 113,100 109,020 120,285

Annual maintenance cost (Rs) 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000

Total maintenance cost (Rs) ( e) 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000

Insurance cost for 5 years (f) 4,970 4,970 4,970 4,970 5,020 5,120 5,274 5,432 5,704 6,842

Registration and road taxes (Rs) (g) 2,485 2,485 2,485 2,485 2,510 2,560 2,637 2,716 2,852 3,421

Resale value after 5 years (Rs) (g) 24,850 24,850 24,850 24,850 25,100 25,602 26,370 27,161 28,522 34,211

Total cost of ownership (Rs) (c)+(d)+(e)+(f)-(g) 155,384 154,696 157,488 151,488 144,156 151,523 155,772 166,447 164,788 185,360

Yoy change (%) (0.4) 1.8 (3.8) (4.8) 5.1 2.8 6.9 (1.0) 12.5

India Automobiles & Components

12 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 5: Price hikes and increase in petrol prices have resulted in higher cost of ownership for four-wheelers Cost of ownership analysis for 4Ws, March fiscal year-ends, 2012-21 (Rs, %)

Source: Company, Kotak Institutional Equities estimates

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Purchase Price (Rs) (a) 438,307 472,000 472,000 472,000 497,000 497,000 499,000 514,000 519,000 549,000

Financed amount (%) 80.0 80.0 80.0 80.0 80.0 80.0 80.0 80.0 80.0 80.0

Interest rate (%) 12.6 12.4 12.1 12.1 11.6 11.1 10.5 10.0 10.0 9.0

Total loan tenure (years) 4.0 4.0 4.0 4.0 4.0 4.0 4.0 4.0 4.0 4.0

Total interest cost (Rs) (b) 97,553 103,263 100,586 100,586 101,236 96,584 91,402 89,397 90,266 85,417

Total cost of vehicle (Rs) (a)+(b), (c) 535,860 575,263 572,586 572,586 598,236 593,584 590,402 603,397 609,266 634,417

Petrol price (Rs/litre) 68.7 68.4 70.5 66.5 61.7 66.4 68.8 75.4 72.7 80.2

Average fuel efficiency (km/liter) 15.0 15.0 15.0 15.0 15.0 15.0 15.0 15.0 15.0 15.0

Annual kms run 12,000 12,000 12,000 12,000 12,000 12,000 12,000 12,000 12,000 12,000

Total years 5.0 5.0 5.0 5.0 5.0 5.0 5.0 5.0 5.0 5.0

Total fuel cost (Rs) (d) 274,800 273,600 282,000 266,000 246,800 265,600 275,200 301,600 290,800 320,760

Annual maintenance cost (Rs) 8,041 8,443 8,865 9,308 9,773 10,262 10,775 11,314 11,880 12,474

Total maintenance cost (Rs) ( e) 40,203 42,213 44,324 46,540 48,867 51,310 53,876 56,569 59,398 62,368

Total insurance cost (Rs) (f) 47,337 50,976 50,976 50,976 53,676 53,676 53,892 60,512 61,052 64,292

Registration and road taxes (Rs) (g) 21,915 23,600 23,600 23,600 24,850 24,850 24,950 30,840 31,140 32,940

Resale value after 5 years (Rs) (h) 262,984 283,200 283,200 283,200 298,200 298,200 299,400 308,400 311,400 329,400

Total cost of ownership (Rs) ( c)+(d)+( e)+(f)+(g) -(h) 657,132 682,452 690,286 676,502 674,229 690,820 698,919 744,518 740,256 785,376

Yoy increase (%) (3.6) 3.9 1.1 (2.0) (0.3) 2.5 1.2 6.5 (0.6) 6.1

For Private Circulation Only. FOR IMPORTANT INFORMATION ABOUT KOTAK SECURITIES’ RATING SYSTEM AND OTHER DISCLOSURES, REFER TO THE END OF THIS MATERIAL.

Pricing – Price hikes continue in edible oil and soaps; muted activity in other categories

Home and personal care: We witness further price increase in soaps with the rise in palm

oil/PFAD prices. HUL has raised the price of select SKUs of Lux and Lifebuoy soap by 9%

while GCPL has raised price of select SKUs of Cinthol Original soap by 2%. In detergent

powders, HUL has raised price of 1 Kg SKU of Rin Advance by 4%. In HI, Jyothy Labs has

raised price of Maxo LV refill by about 3%. In shampoos, Patanjali has raised the price of

select SKUs of Kesh Kanti shampoo by 7%. P&G has increased the price of Olay Total Effects

face cleanser by 11%.

Foods and beverages: We have seen minimal pricing actions in foods/beverages with the

exception of edible oils. Marico has raised the price of multiple SKUs of Saffola edible oils

with 3% price increase in Saffola Tasty Blend, Gold and Active variants. ITC has raised the

price of 150 gm pack of Sunfeast Bourbon biscuit by 7%. Lactalis (Prabhat brand) has hiked

milk procurement price by Re1 to Rs30 per liter in Maharashtra. Nestle India has raised the

price of 400 gm pouch pack of Nestea Iced tea by 9%. Mondelez has lowered the effective

price of Cadbury 5 Star chocolate by 7% through grammage increase.

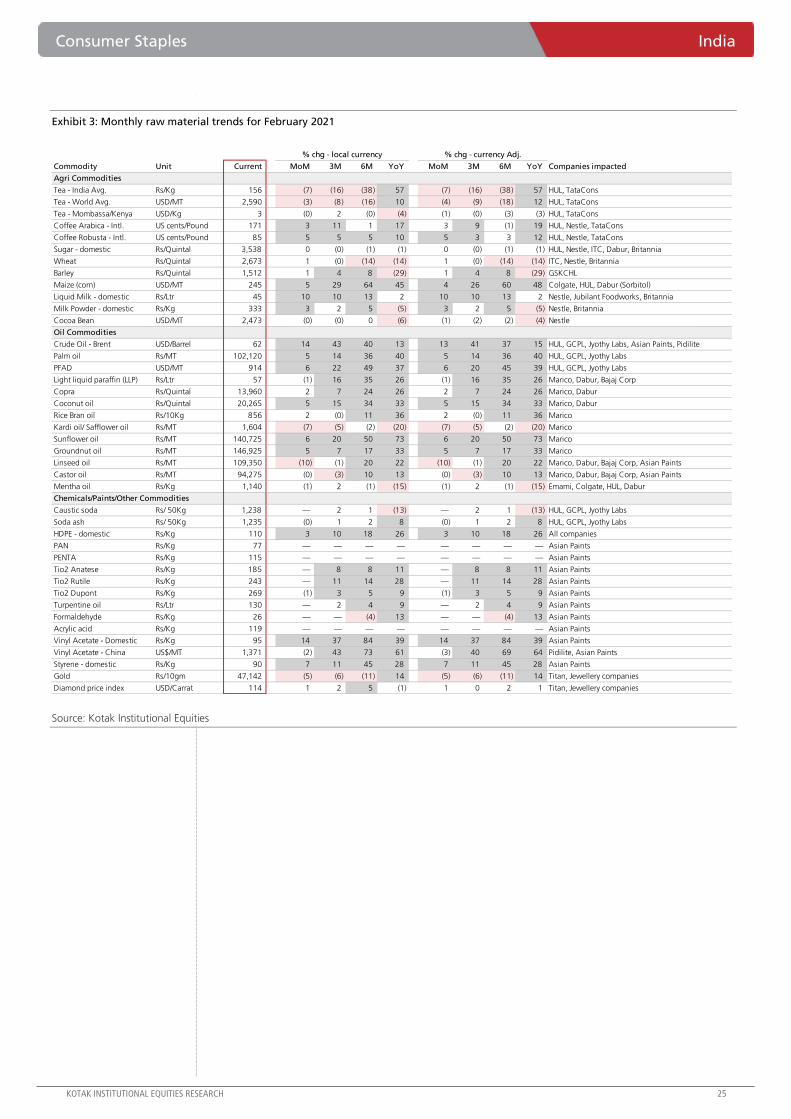

RM– Inflationary trends in oil commodities while mixed price trends in agri-commodities

See Exhibit 3 for detailed RM inflation impact.

Agri-inputs. Agri-commodities showed mixed trends in February. Domestic tea prices

continued to moderate in February (down 7% mom). Tea prices are down 40% from its

recent peak (August 2020) but is still up 57% on yoy basis. International coffee prices saw

some inflationary pressure (up 3-5% mom). Milk prices rose sharply (up 10% mom). The

price increase is due to (1) higher freight costs and (2) increase in the price of animal feed.

Prices are expected to remain firm in the near term; we note that milk prices have seen a

steady increase post the Covid-led slump in April. SMP prices were up 3% mom. Wheat,

sugar and barley prices were broadly stable. Maize continued to see inflationary pressure (up

5% mom).

Oil commodities basket. Crude prices were up 14% mom for the month; on a yoy basis

crude is up 13%. Most of the agri-oils continued to see inflationary pressure for the month.

Palm oil and PFAD prices continued to rise (up 5-6% mom) and are now up 37-40% on a

yoy basis. Copra and coconut oil saw 2-5% mom rise. Marico’s management expects copra

prices to start easing from 1Q on the back of a healthy crop outlook. Sunflower and

groundnut oil also saw a sharp increase of 5-6% mom. Sunflower oil is up 73% on a yoy

basis due to lower production in some of the international markets. Mentha and LLP were

stable for the month while rice bran oil saw moderate inflation of 2% mom.

Other commodities. Sharp inflationary pressure was seen for select commodities. VAM

(China) prices continued to remain hard – hovering close to US$1,400/MT level in February

(post the sharp increase in December). Styrene monomer too saw a sharp price increase of

7% mom. Gold prices continued to ease (down 5% mom); it is down 11% mom in the past

six months.

Consumer Staples India

Month in review – Feb 2021. The KIE consumer universe was down 3% over the past

one month, underperforming the broader markets by 200 bps. On the in-market activity

front, further price increases were seen in soaps and select edible oils. On RM front, we

witnessed (1) a sharp price increase in milk, (2) further increase in prices of most oil

commodities, and (3) further inflationary pressure in VAM and monomers. Broad-based

inflation would weigh on gross margins of most consumer companies in the near term.

ATTRACTIVE

MARCH 10, 2021

UPDATE

BSE-30: 51,025

Jaykumar Doshi

Aniket Sethi

Sushruta Mishra

[email protected]: +91 22 6218 6427

India Consumer Staples

14 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Who benefits? (1) Easing tea prices should provide some relief to HUVR and TATACONS,

(2) continued benign intensity for wheat benefits ITC, NEST and BRIT.

Who gets impacted? (1) Higher prices for monomers and VAM are negative for paint

companies and PIDI. (2) PFAD inflation to hurt HUVR, GCPL and JYL. (3) Inflation in

Copra, and LLP would weigh on edible oil and hair oil categories (Marico). (4) Increase in

milk prices hurts NEST and BRIT.

Sector (KIE consumer universe) underperformed the broader markets

Our overall consumer coverage universe underperformed the broader markets over the past

month, down 3% (down 4% ex-ITC) while the broader market was down 1%.

Key stocks that outperformed were – VBL (+11% mom), JUBI (+7% mom), CLGT (+3%

mom) and TATACONS (+2% mom). Key under-performers were GCPL (-9% mom), PAG (-

8% mom), TTAN (-7% mom) and BRGR (-6% mom).

On a 12-month basis, the sector is now underperforming the broader markets posting 17%

absolute gain (15% ex-ITC). Our preferred picks – HUVR, TATACONS, DABUR, ITC, JUBI,

TTAN, NEST, MRCO, GCPL and VBL.

New launches and re-launches

Marico has forayed into the instant noodles category with the launch of ‘Saffola Oodles’

brand. The product, based on multi-grain oats and vegetables, is positioned as a healthy

ready-to-eat snack alternative. Saffola Oodles is available in two SKUs – single pack of 46

gm for Rs20 and pack-of-four of 184 gm for Rs80.

HUL has forayed into the machine dishwash segment with the launch of Vim Matic range

of products. Vim Matic machine dishwash range consists of Detergent Powder, Rinse Aid

(Rs375 for 500ml), Dishwash Salt (Rs200 for 1kg) and an All-In-One Tablet. Vim Matic All-

In-One tablets are priced at Rs1,200 for 30 tablets.

ITC has expanded its instant noodles portfolio under the Sunfeast YiPPee! brand with the

launch of a new Saucy Masala variant. The product is available in two SKUs – 65 gm

single pack for Rs15 and a four-in-one pack of 260 gm for Rs58.

Kikkoman (leading Japanese sauce brand) has entered the Indian market and has set up

a wholly-owned subsidiary for import and distribution of products. The brand, well

known globally for its ‘Honjozo’ soy sauce aims to be the market leader in Asian sauces

category in India.

Mars Petcare has launched its dog food brand Chappi in India. Chappi offers

Chicken/Milk for puppies and Chicken/Rice for adult dogs, along with necessary nutrients

and fibers. The product is available in 3kg/8kg SKUs for puppies and 3/8/20kg SKUs for

adult dogs.

Haldiram has forayed into health foods space through a distribution tie-up with Africa’s

Futurelife to introduce its nutritional foods range in India. Futurelife will sell its products

under Smart Foods brand which includes steel cut oats, packaged granola, and a range of

high-protein offerings.

Tata Consumer has strengthened its wellness portfolio with the launch of two new

variants of Tata Tea (Tata Tulsi Green Tea and Tata Tea Gold Care). Tata Tea Gold Care is

priced at Rs140 (for 250gm) and Rs265 (for 500gm) while Tata Tulsi Green tea is available

at Rs174 for 100gm pack.

Consumer Staples India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 15

Emami has expanded its health and wellness portfolio with the launch of a new variant

of Zandu Chyavanprash with the added-benefits of natural jaggery. The product has no-

added refined sugar and is claimed to have 2X immunity.

Heritage Foods has forayed into cheese and fresh cream category with the launch of

mozzarella cheese, processed cheese, and fresh cream. The cheese variants are available

in 500 gm for mozzarella and 200/400/1000 gm SKUs for processed cheese. Heritage

fresh cream is available in 200gm Tetra packs.

Heritage Foods has also expanded its milk-based drinks portfolio with the launch of Cool

Café – an on-the-go coffee drink available in 180 ml packs.

Amway has expanded its home care portfolio with the launch of fruit and veggie wash.

The product is priced at Rs249 for a 500 ml pack and is sold through direct sellers and

online channel. Amway has recently stepped up investments in the homecare space and

expects to register Rs2.5 bn revenue by 2025.

Del Monte has launched Olive oil priced at Rs250 for 1litre pouch pack – at a significant

discount (~60-70%) to alternative brands available in the market. The product is available

in e-commerce channels and offline outlets in select markets.

Chai Point has launched instant chai taking into account increased consumer preference

for in-home food consumption. The product is available on e-commerce channel in three

variants (masala, ginger, and cardamom) in sachet format priced at Rs180 (for pack of

10).

William Lawson has forayed into premium Scotch whisky with the launch of William

Lawson’s 13 in Telangana. The product is available in premium retail and on-trade

outlets. With this launch, William Lawson now has 13 variants in the whisky segment in

India.

Consumer Sector Newsflow

Indian FMCG industry grew 7.3% yoy in Dec-2020 quarter on the back of robust 14.2%

yoy growth in rural sales, per Nielsen. The growth was led by recovery in consumption

and continued rural growth post the festive period.

FMCG companies dial-up rural distribution expansion. With strong rural demand,

FMCG companies have accelerated distributor addition in rural markets. As per Bizom, a

sales automation firm that transacts with 7.5 mn retail stores, the number of distributors

in Indian FMCG industry increased by 42% yoy to 12,192 as of Jan-2021. The increase

was driven entirely by rural markets while distributor count shrank in cities.

Mondelez has move court against Parle Products claiming trademark infringement with

‘deceptively similar’ design of Parle’s Fabio Biscuits compared to Oreo Biscuits. Parle

launched Fabio biscuits in Jan-2020.

Grupo Bimbo has acquired Modern Foods from Everstone PE. With a topline of ~Rs4

bn, Modern Foods has ~35-40% market share in the Indian bread market. Grupo Bimbo

is the largest baking company globally, operating in 33 countries with a portfolio of 100+

brands. The company currently operates bakery brand Harvest Gold in India.

Hindustan Unilever plans to be plastic-neutral in CY2021, and will collect and

process more plastic than it uses. The company plans to enable processing of 0.1 mn

tonnes of plastic waste during the year. Among other FMCG companies, Nestle India has

achieved plastic neutrality while Dabur is expected to by March-2022.

India Consumer Staples

16 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Emami is planning for acquisition of digital-first brands in India and International

markets, to tap into opportunities arising out of Covid-19 pandemic. The company plans

to increase e-commerce salience to 6-7% in the next two years from 2.5-3% currently.

Coca-Cola’s key strategic focus areas – Addressing at Cola-Cola’s first all-India bottling

partners meet, Mr Sanket Ray highlighted deeper distribution in smaller markets,

increased focus on profitability, and investments in healthier beverages are key strategies

that the company will focus on this year.

Cosmo Films is foraying into consumer-facing businesses such as laundry sanitizers,

household accessories, and pet care products, leveraging synergies on packaging. The

company currently makes specialty films for packaging and lamination.

Leading jewelry retailers have stepped up gold jewelry hallmarking, which is

expected to become mandatory from 1st Jun-2021, for gold jewelry of 14, 18 and 22

carat. Per guidelines, failure to comply can attract penalty of up to five times the cost of

jewelry and one year imprisonment.

Rising online trade in jewelry space. Indian gems and jewelry exporters are increasing

e-commerce presence, targeting 35-40% export shipments through this channel in

FY2022. Gem and Jewelry Export Promotion Council (GJEPC) has entered into an MoU

with eBay group company (ES Online Service) to export products to the U.S market.

Consumer Staples India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 17

Exhibit 1: Snapshot of new product launches

Source: Company, Kotak Institutional Equities

India Consumer Staples

18 KOTAK INSTITUTIONAL EQUITIES RESEARCH

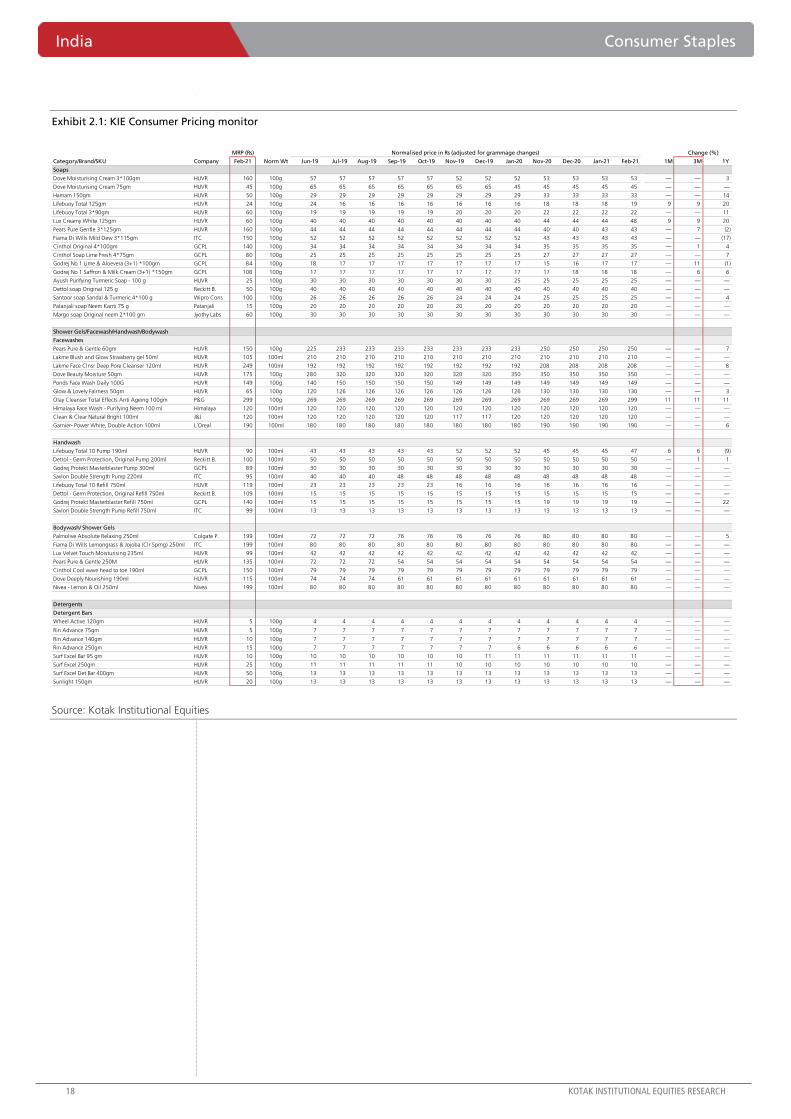

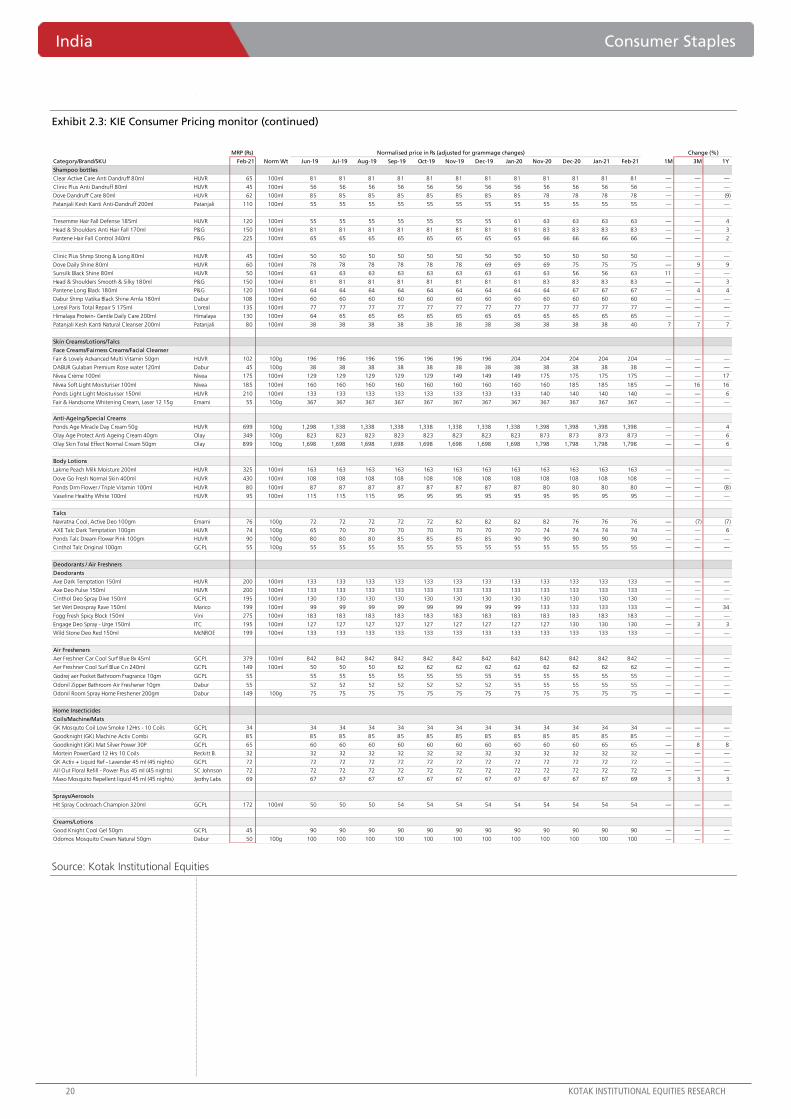

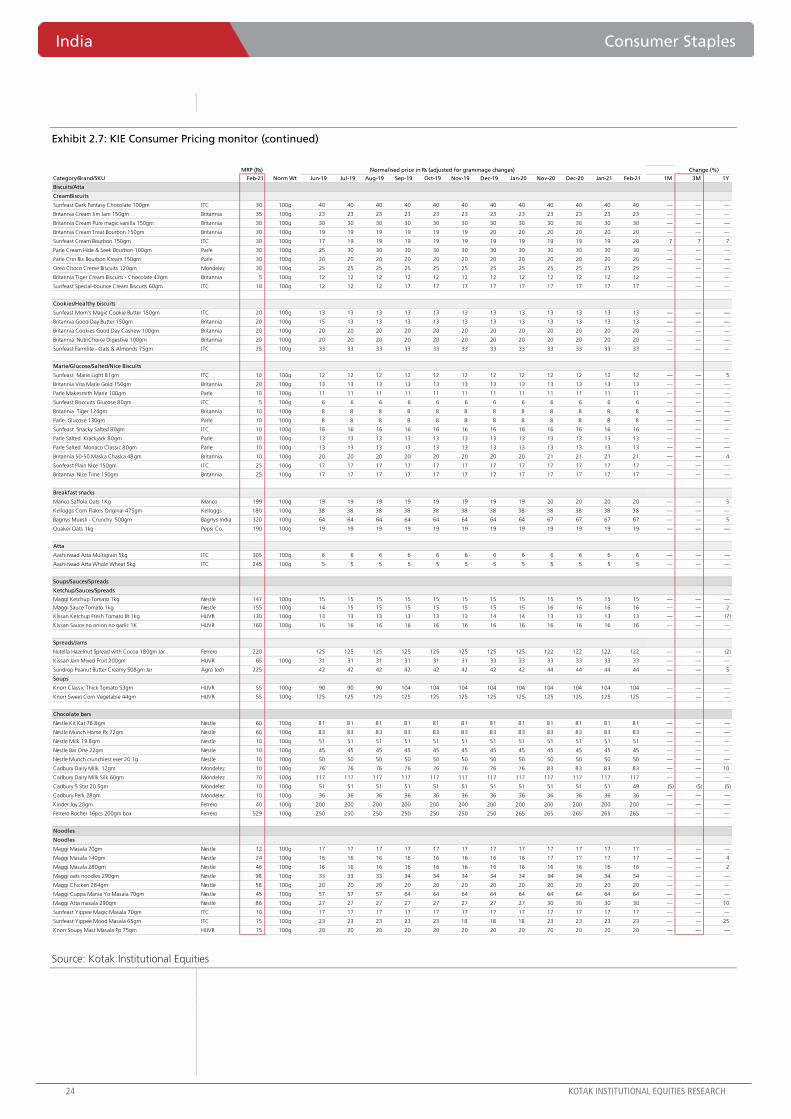

Exhibit 2.1: KIE Consumer Pricing monitor

Source: Kotak Institutional Equities

MRP (Rs)

Category/Brand/SKU Company Feb-21 Norm Wt Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Nov-20 Dec-20 Jan-21 Feb-21 1M 3M 1Y

Soaps

Dove Moisturising Cream 3*100gm HUVR 160 100g 57 57 57 57 57 52 52 52 53 53 53 53 — — 3

Dove Moisturising Cream 75gm HUVR 45 100g 65 65 65 65 65 65 65 45 45 45 45 45 — — —

Hamam 150gm HUVR 50 100g 29 29 29 29 29 29 29 29 33 33 33 33 — — 14

Lifebuoy Total 125gm HUVR 24 100g 24 16 16 16 16 16 16 16 18 18 18 19 9 9 20

Lifebuoy Total 3*90gm HUVR 60 100g 19 19 19 19 19 20 20 20 22 22 22 22 — — 11

Lux Creamy White 125gm HUVR 60 100g 40 40 40 40 40 40 40 40 44 44 44 48 9 9 20

Pears Pure Gentle 3*125gm HUVR 160 100g 44 44 44 44 44 44 44 44 40 40 43 43 — 7 (2)

Fiama Di Wills Mild Dew 3*115gm ITC 150 100g 52 52 52 52 52 52 52 52 43 43 43 43 — — (17)

Cinthol Original 4*100gm GCPL 140 100g 34 34 34 34 34 34 34 34 35 35 35 35 — 1 4

Cinthol Soap Lime Fresh 4*75gm GCPL 80 100g 25 25 25 25 25 25 25 25 27 27 27 27 — — 7

Godrej No 1 Lime & Aloevera (3+1) *100gm GCPL 84 100g 18 17 17 17 17 17 17 17 15 16 17 17 — 11 (1)

Godrej No 1 Saffron & Milk Cream (3+1) *150gm GCPL 108 100g 17 17 17 17 17 17 17 17 17 18 18 18 — 6 6

Ayush Purifying Turmeric Soap - 100 g HUVR 25 100g 30 30 30 30 30 30 30 25 25 25 25 25 — — —

Dettol soap Original 125 g Reckitt B. 50 100g 40 40 40 40 40 40 40 40 40 40 40 40 — — —

Santoor soap Sandal & Turmeric 4*100 g Wipro Cons 100 100g 26 26 26 26 26 24 24 24 25 25 25 25 — — 4

Patanjali soap Neem Kanti 75 g Patanjali 15 100g 20 20 20 20 20 20 20 20 20 20 20 20 — — —

Margo soap Original neem 2*100 gm Jyothy Labs 60 100g 30 30 30 30 30 30 30 30 30 30 30 30 — — —

Shower Gels/Facewash/Handwash/Bodywash

Facewashes

Pears Pure & Gentle 60gm HUVR 150 100g 225 233 233 233 233 233 233 233 250 250 250 250 — — 7

Lakme Blush and Glow Strawberry gel 50ml HUVR 105 100ml 210 210 210 210 210 210 210 210 210 210 210 210 — — —

Lakme Face Clnsr Deep Pore Cleanser 120ml HUVR 249 100ml 192 192 192 192 192 192 192 192 208 208 208 208 — — 8

Dove Beauty Moisture 50gm HUVR 175 100g 280 320 320 320 320 320 320 350 350 350 350 350 — — —

Ponds Face Wash Daily 100G HUVR 149 100g 140 150 150 150 150 149 149 149 149 149 149 149 — — —

Glow & Lovely Fairness 50gm HUVR 65 100g 120 126 126 126 126 126 126 126 130 130 130 130 — — 3

Olay Cleanser Total Effects Anti Ageing 100gm P&G 299 100g 269 269 269 269 269 269 269 269 269 269 269 299 11 11 11

Himalaya Face Wash - Purifying Neem 100 ml Himalaya 120 100ml 120 120 120 120 120 120 120 120 120 120 120 120 — — —

Clean & Clear Natural Bright 100ml J&J 120 100ml 120 120 120 120 120 117 117 120 120 120 120 120 — — —

Garnier- Power White, Double Action 100ml L'Oreal 190 100ml 180 180 180 180 180 180 180 180 190 190 190 190 — — 6

Handwash

Lifebuoy Total 10 Pump 190ml HUVR 90 100ml 43 43 43 43 43 52 52 52 45 45 45 47 6 6 (9)

Dettol - Germ Protection, Original Pump 200ml Reckitt B. 100 100ml 50 50 50 50 50 50 50 50 50 50 50 50 — 1 1

Godrej Protekt Masterblaster Pump 300ml GCPL 89 100ml 30 30 30 30 30 30 30 30 30 30 30 30 — — —

Savlon Double Strength Pump 220ml ITC 95 100ml 40 40 40 48 48 48 48 48 48 48 48 48 — — —

Lifebuoy Total 10 Refill 750ml HUVR 119 100ml 23 23 23 23 23 16 16 16 16 16 16 16 — — —

Dettol - Germ Protection, Original Refill 750ml Reckitt B. 109 100ml 15 15 15 15 15 15 15 15 15 15 15 15 — — —

Godrej Protekt Masterblaster Refill 750ml GCPL 140 100ml 15 15 15 15 15 15 15 15 19 19 19 19 — — 22

Savlon Double Strength Pump Refill 750ml ITC 99 100ml 13 13 13 13 13 13 13 13 13 13 13 13 — — —

Bodywash/ Shower Gels

Palmolive Absolute Relaxing 250ml Colgate P. 199 100ml 72 72 72 76 76 76 76 76 80 80 80 80 — — 5

Fiama Di Wills Lemongrass & Jojoba (Clr Sprng) 250ml ITC 199 100ml 80 80 80 80 80 80 80 80 80 80 80 80 — — —

Lux Velvet Touch Moisturising 235ml HUVR 99 100ml 42 42 42 42 42 42 42 42 42 42 42 42 — — —

Pears Pure & Gentle 250M HUVR 135 100ml 72 72 72 54 54 54 54 54 54 54 54 54 — — —

Cinthol Cool wave head to toe 190ml GCPL 150 100ml 79 79 79 79 79 79 79 79 79 79 79 79 — — —

Dove Deeply Nourishing 190ml HUVR 115 100ml 74 74 74 61 61 61 61 61 61 61 61 61 — — —

Nivea - Lemon & Oil 250ml Nivea 199 100ml 80 80 80 80 80 80 80 80 80 80 80 80 — — —

Detergents

Detergent Bars

Wheel Active 120gm HUVR 5 100g 4 4 4 4 4 4 4 4 4 4 4 4 — — —

Rin Advance 75gm HUVR 5 100g 7 7 7 7 7 7 7 7 7 7 7 7 — — —

Rin Advance 140gm HUVR 10 100g 7 7 7 7 7 7 7 7 7 7 7 7 — — —

Rin Advance 250gm HUVR 15 100g 7 7 7 7 7 7 7 6 6 6 6 6 — — —

Surf Excel Bar 95 gm HUVR 10 100g 10 10 10 10 10 10 11 11 11 11 11 11 — — —

Surf Excel 250gm HUVR 25 100g 11 11 11 11 11 10 10 10 10 10 10 10 — — —

Surf Excel Det Bar 400gm HUVR 50 100g 13 13 13 13 13 13 13 13 13 13 13 13 — — —

Sunlight 150gm HUVR 20 100g 13 13 13 13 13 13 13 13 13 13 13 13 — — —

Change (%)Normalised price in Rs (adjusted for grammage changes)

Consumer Staples India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 19

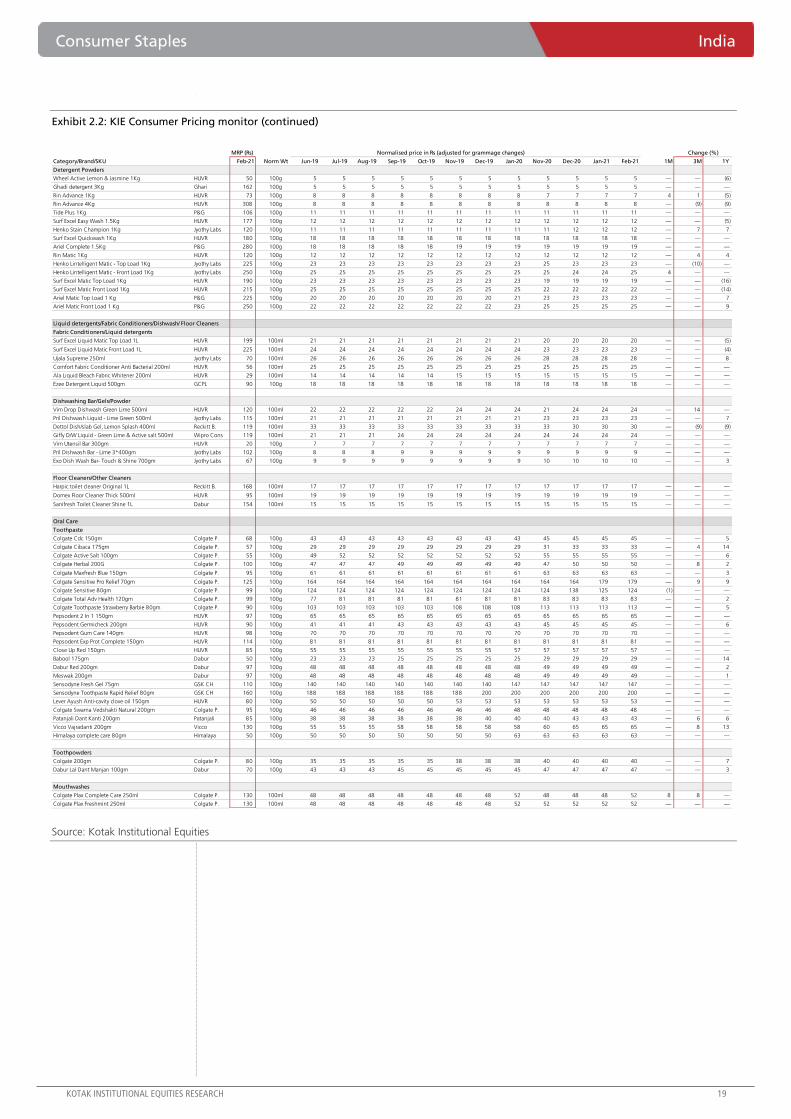

Exhibit 2.2: KIE Consumer Pricing monitor (continued)

Source: Kotak Institutional Equities

MRP (Rs)

Category/Brand/SKU Feb-21 Norm Wt Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Nov-20 Dec-20 Jan-21 Feb-21 1M 3M 1Y

Detergent Powders

Wheel Active Lemon & Jasmine 1Kg HUVR 50 100g 5 5 5 5 5 5 5 5 5 5 5 5 — — (6)

Ghadi detergent 3Kg Ghari 162 100g 5 5 5 5 5 5 5 5 5 5 5 5 — — —

Rin Advance 1Kg HUVR 73 100g 8 8 8 8 8 8 8 8 7 7 7 7 4 1 (5)

Rin Advance 4Kg HUVR 308 100g 8 8 8 8 8 8 8 8 8 8 8 8 — (9) (9)

Tide Plus 1Kg P&G 106 100g 11 11 11 11 11 11 11 11 11 11 11 11 — — —

Surf Excel Easy Wash 1.5Kg HUVR 177 100g 12 12 12 12 12 12 12 12 12 12 12 12 — — (5)

Henko Stain Champion 1Kg Jyothy Labs 120 100g 11 11 11 11 11 11 11 11 11 12 12 12 — 7 7

Surf Excel Quickwash 1Kg HUVR 180 100g 18 18 18 18 18 18 18 18 18 18 18 18 — — —

Ariel Complete 1.5Kg P&G 280 100g 18 18 18 18 18 19 19 19 19 19 19 19 — — —

Rin Matic 1Kg HUVR 120 100g 12 12 12 12 12 12 12 12 12 12 12 12 — 4 4

Henko Lintelligent Matic - Top Load 1Kg Jyothy Labs 225 100g 23 23 23 23 23 23 23 23 25 23 23 23 — (10) —

Henko Lintelligent Matic - Front Load 1Kg Jyothy Labs 250 100g 25 25 25 25 25 25 25 25 25 24 24 25 4 — —

Surf Excel Matic Top Load 1Kg HUVR 190 100g 23 23 23 23 23 23 23 23 19 19 19 19 — — (16)

Surf Excel Matic Front Load 1Kg HUVR 215 100g 25 25 25 25 25 25 25 25 22 22 22 22 — — (14)

Ariel Matic Top Load 1 Kg P&G 225 100g 20 20 20 20 20 20 20 21 23 23 23 23 — — 7

Ariel Matic Front Load 1 Kg P&G 250 100g 22 22 22 22 22 22 22 23 25 25 25 25 — — 9

Liquid detergents/Fabric Conditioners/Dishwash/ Floor Cleaners

Fabric Conditioners/Liquid detergents

Surf Excel Liquid Matic Top Load 1L HUVR 199 100ml 21 21 21 21 21 21 21 21 20 20 20 20 — — (5)

Surf Excel Liquid Matic Front Load 1L HUVR 225 100ml 24 24 24 24 24 24 24 24 23 23 23 23 — — (4)

Ujala Supreme 250ml Jyothy Labs 70 100ml 26 26 26 26 26 26 26 26 28 28 28 28 — — 8

Comfort Fabric Conditioner Anti Bacterial 200ml HUVR 56 100ml 25 25 25 25 25 25 25 25 25 25 25 25 — — —

Ala Liquid Bleach Fabric Whitener 200ml HUVR 29 100ml 14 14 14 14 14 15 15 15 15 15 15 15 — — —

Ezee Detergent Liquid 500gm GCPL 90 100g 18 18 18 18 18 18 18 18 18 18 18 18 — — —

Dishwashing Bar/Gels/Powder

Vim Drop Dishwash Green Lime 500ml HUVR 120 100ml 22 22 22 22 22 24 24 24 21 24 24 24 — 14 —

Pril Dishwash Liquid - Lime Green 500ml Jyothy Labs 115 100ml 21 21 21 21 21 21 21 21 23 23 23 23 — — 7

Dettol Dish/slab Gel, Lemon Splash 400ml Reckitt B. 119 100ml 33 33 33 33 33 33 33 33 33 30 30 30 — (9) (9)

Giffy D/W Liquid - Green Lime & Active salt 500ml Wipro Cons 119 100ml 21 21 21 24 24 24 24 24 24 24 24 24 — — —

Vim Utensil Bar 300gm HUVR 20 100g 7 7 7 7 7 7 7 7 7 7 7 7 — — —

Pril Dishwash Bar - Lime 3*400gm Jyothy Labs 102 100g 8 8 8 9 9 9 9 9 9 9 9 9 — — —

Exo Dish Wash Bar- Touch & Shine 700gm Jyothy Labs 67 100g 9 9 9 9 9 9 9 9 10 10 10 10 — — 3

Floor Cleaners/Other Cleaners

Harpic toilet cleaner Original 1L Reckitt B. 168 100ml 17 17 17 17 17 17 17 17 17 17 17 17 — — —

Domex Floor Cleaner Thick 500ml HUVR 95 100ml 19 19 19 19 19 19 19 19 19 19 19 19 — — —

Sanifresh Toilet Cleaner Shine 1L Dabur 154 100ml 15 15 15 15 15 15 15 15 15 15 15 15 — — —

Oral Care

Toothpaste

Colgate Cdc 150gm Colgate P. 68 100g 43 43 43 43 43 43 43 43 45 45 45 45 — — 5

Colgate Cibaca 175gm Colgate P. 57 100g 29 29 29 29 29 29 29 29 31 33 33 33 — 4 14

Colgate Active Salt 100gm Colgate P. 55 100g 49 52 52 52 52 52 52 52 55 55 55 55 — — 6

Colgate Herbal 200G Colgate P. 100 100g 47 47 47 49 49 49 49 49 47 50 50 50 — 8 2

Colgate Maxfresh Blue 150gm Colgate P. 95 100g 61 61 61 61 61 61 61 61 63 63 63 63 — — 3

Colgate Sensitive Pro Relief 70gm Colgate P. 125 100g 164 164 164 164 164 164 164 164 164 164 179 179 — 9 9

Colgate Sensitive 80gm Colgate P. 99 100g 124 124 124 124 124 124 124 124 124 138 125 124 (1) — —

Colgate Total Adv Health 120gm Colgate P. 99 100g 77 81 81 81 81 81 81 81 83 83 83 83 — — 2

Colgate Toothpaste Strawberry Barbie 80gm Colgate P. 90 100g 103 103 103 103 103 108 108 108 113 113 113 113 — — 5

Pepsodent 2 In 1 150gm HUVR 97 100g 65 65 65 65 65 65 65 65 65 65 65 65 — — —

Pepsodent Germicheck 200gm HUVR 90 100g 41 41 41 43 43 43 43 43 45 45 45 45 — — 6

Pepsodent Gum Care 140gm HUVR 98 100g 70 70 70 70 70 70 70 70 70 70 70 70 — — —

Pepsodent Exp Prot Complete 150gm HUVR 114 100g 81 81 81 81 81 81 81 81 81 81 81 81 — — —

Close Up Red 150gm HUVR 85 100g 55 55 55 55 55 55 55 57 57 57 57 57 — — —

Babool 175gm Dabur 50 100g 23 23 23 25 25 25 25 25 29 29 29 29 — — 14

Dabur Red 200gm Dabur 97 100g 48 48 48 48 48 48 48 48 49 49 49 49 — — 2

Meswak 200gm Dabur 97 100g 48 48 48 48 48 48 48 48 49 49 49 49 — — 1

Sensodyne Fresh Gel 75gm GSK CH 110 100g 140 140 140 140 140 140 140 147 147 147 147 147 — — —

Sensodyne Toothpaste Rapid Relief 80gm GSK CH 160 100g 188 188 188 188 188 188 200 200 200 200 200 200 — — —

Lever Ayush Anti-cavity clove oil 150gm HUVR 80 100g 50 50 50 50 50 53 53 53 53 53 53 53 — — —

Colgate Swarna Vedshakti Natural 200gm Colgate P. 95 100g 46 46 46 46 46 46 46 48 48 48 48 48 — — —

Patanjali Dant Kanti 200gm Patanjali 85 100g 38 38 38 38 38 38 40 40 40 43 43 43 — 6 6

Vicco Vajradanti 200gm Vicco 130 100g 55 55 55 58 58 58 58 58 60 65 65 65 — 8 13

Himalaya complete care 80gm Himalaya 50 100g 50 50 50 50 50 50 50 63 63 63 63 63 — — —

Toothpowders

Colgate 200gm Colgate P. 80 100g 35 35 35 35 35 38 38 38 40 40 40 40 — — 7

Dabur Lal Dant Manjan 100gm Dabur 70 100g 43 43 43 45 45 45 45 45 47 47 47 47 — — 3

Mouthwashes

Colgate Plax Complete Care 250ml Colgate P. 130 100ml 48 48 48 48 48 48 48 52 48 48 48 52 8 8 —

Colgate Plax Freshmint 250ml Colgate P. 130 100ml 48 48 48 48 48 48 48 52 52 52 52 52 — — —

Change (%)Normalised price in Rs (adjusted for grammage changes)

India Consumer Staples

20 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 2.3: KIE Consumer Pricing monitor (continued)

Source: Kotak Institutional Equities

MRP (Rs)

Category/Brand/SKU Feb-21 Norm Wt Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Nov-20 Dec-20 Jan-21 Feb-21 1M 3M 1Y

Shampoo bottles

Clear Active Care Anti Dandruff 80ml HUVR 65 100ml 81 81 81 81 81 81 81 81 81 81 81 81 — — —

Clinic Plus Anti Dandruff 80ml HUVR 45 100ml 56 56 56 56 56 56 56 56 56 56 56 56 — — —

Dove Dandruff Care 80ml HUVR 62 100ml 85 85 85 85 85 85 85 85 78 78 78 78 — — (9)

Patanjali Kesh Kanti Anti-Dandruff 200ml Patanjali 110 100ml 55 55 55 55 55 55 55 55 55 55 55 55 — — —

Tresemme Hair Fall Defense 185ml HUVR 120 100ml 55 55 55 55 55 55 55 61 63 63 63 63 — — 4

Head & Shoulders Anti Hair Fall 170ml P&G 150 100ml 81 81 81 81 81 81 81 81 83 83 83 83 — — 3

Pantene Hair Fall Control 340ml P&G 225 100ml 65 65 65 65 65 65 65 65 66 66 66 66 — — 2

Clinic Plus Shmp Strong & Long 80ml HUVR 45 100ml 50 50 50 50 50 50 50 50 50 50 50 50 — — —

Dove Daily Shine 80ml HUVR 60 100ml 78 78 78 78 78 78 69 69 69 75 75 75 — 9 9

Sunsilk Black Shine 80ml HUVR 50 100ml 63 63 63 63 63 63 63 63 63 56 56 63 11 — —

Head & Shoulders Smooth & Silky 180ml P&G 150 100ml 81 81 81 81 81 81 81 81 83 83 83 83 — — 3

Pantene Long Black 180ml P&G 120 100ml 64 64 64 64 64 64 64 64 64 67 67 67 — 4 4

Dabur Shmp Vatika Black Shine Amla 180ml Dabur 108 100ml 60 60 60 60 60 60 60 60 60 60 60 60 — — —

Loreal Paris Total Repair 5 175ml L'oreal 135 100ml 77 77 77 77 77 77 77 77 77 77 77 77 — — —

Himalaya Protein- Gentle Daily Care 200ml Himalaya 130 100ml 64 65 65 65 65 65 65 65 65 65 65 65 — — —

Patanjali Kesh Kanti Natural Cleanser 200ml Patanjali 80 100ml 38 38 38 38 38 38 38 38 38 38 38 40 7 7 7

Skin Creams/Lotions/Talcs

Face Creams/Fairness Creams/Facial Cleanser

Fair & Lovely Advanced Multi Vitamin 50gm HUVR 102 100g 196 196 196 196 196 196 196 204 204 204 204 204 — — —

DABUR Gulabari Premium Rose water 120ml Dabur 45 100g 38 38 38 38 38 38 38 38 38 38 38 38 — — —

Nivea Crème 100ml Nivea 175 100ml 129 129 129 129 129 149 149 149 175 175 175 175 — — 17

Nivea Soft Light Moisturiser 100ml Nivea 185 100ml 160 160 160 160 160 160 160 160 160 185 185 185 — 16 16

Ponds Light Light Moisturiser 150ml HUVR 210 100ml 133 133 133 133 133 133 133 133 140 140 140 140 — — 6

Fair & Handsome Whitening Cream, Laser 12 15g Emami 55 100g 367 367 367 367 367 367 367 367 367 367 367 367 — — —

Anti-Ageing/Special Creams

Ponds Age Miracle Day Cream 50g HUVR 699 100g 1,298 1,338 1,338 1,338 1,338 1,338 1,338 1,338 1,398 1,398 1,398 1,398 — — 4

Olay Age Protect Anti Ageing Cream 40gm Olay 349 100g 823 823 823 823 823 823 823 823 873 873 873 873 — — 6

Olay Skin Total Effect Normal Cream 50gm Olay 899 100g 1,698 1,698 1,698 1,698 1,698 1,698 1,698 1,698 1,798 1,798 1,798 1,798 — — 6

Body Lotions

Lakme Peach Milk Moisture 200ml HUVR 325 100ml 163 163 163 163 163 163 163 163 163 163 163 163 — — —

Dove Go Fresh Normal Skin 400ml HUVR 430 100ml 108 108 108 108 108 108 108 108 108 108 108 108 — — —

Ponds Drm Flower / Triple Vitamin 100ml HUVR 80 100ml 87 87 87 87 87 87 87 87 80 80 80 80 — — (8)

Vaseline Healthy White 100ml HUVR 95 100ml 115 115 115 95 95 95 95 95 95 95 95 95 — — —

Talcs

Navratna Cool, Active Deo 100gm Emami 76 100g 72 72 72 72 72 82 82 82 82 76 76 76 — (7) (7)

AXE Talc Dark Temptation 100gm HUVR 74 100g 65 70 70 70 70 70 70 70 74 74 74 74 — — 6

Ponds Talc Dream Flower Pink 100gm HUVR 90 100g 80 80 80 85 85 85 85 90 90 90 90 90 — — —

Cinthol Talc Original 100gm GCPL 55 100g 55 55 55 55 55 55 55 55 55 55 55 55 — — —

Deodorants / Air Freshners

Deodorants

Axe Dark Temptation 150ml HUVR 200 100ml 133 133 133 133 133 133 133 133 133 133 133 133 — — —

Axe Deo Pulse 150ml HUVR 200 100ml 133 133 133 133 133 133 133 133 133 133 133 133 — — —

Cinthol Deo Spray Dive 150ml GCPL 195 100ml 130 130 130 130 130 130 130 130 130 130 130 130 — — —

Set Wet Deospray Rave 150ml Marico 199 100ml 99 99 99 99 99 99 99 99 133 133 133 133 — — 34

Fogg Fresh Spicy Block 150ml Vini 275 100ml 183 183 183 183 183 183 183 183 183 183 183 183 — — —

Engage Deo Spray - Urge 150ml ITC 195 100ml 127 127 127 127 127 127 127 127 127 130 130 130 — 3 3

Wild Stone Deo Red 150ml McNROE 199 100ml 133 133 133 133 133 133 133 133 133 133 133 133 — — —

Air Fresheners

Aer Freshner Car Cool Surf Blue Bx 45ml GCPL 379 100ml 842 842 842 842 842 842 842 842 842 842 842 842 — — —

Aer Freshner Cool Surf Blue Cn 240ml GCPL 149 100ml 50 50 50 62 62 62 62 62 62 62 62 62 — — —

Godrej aer Pocket Bathroom Fragrance 10gm GCPL 55 55 55 55 55 55 55 55 55 55 55 55 55 — — —

Odonil Zipper Bathroom Air Freshener 10gm Dabur 55 52 52 52 52 52 52 52 55 55 55 55 55 — — —

Odonil Room Spray Home Freshener 200gm Dabur 149 100g 75 75 75 75 75 75 75 75 75 75 75 75 — — —

Home Insecticides

Coils/Machine/Mats

GK Mosquto Coil Low Smoke 12Hrs - 10 Coils GCPL 34 34 34 34 34 34 34 34 34 34 34 34 34 — — —

Goodknight (GK) Machine Activ Combi GCPL 85 85 85 85 85 85 85 85 85 85 85 85 85 — — —

Goodknight (GK) Mat Silver Power 30P GCPL 65 60 60 60 60 60 60 60 60 60 60 65 65 — 8 8

Mortein PowerGard 12 Hrs 10 Coils Reckitt B. 32 32 32 32 32 32 32 32 32 32 32 32 32 — — —

GK Activ + Liquid Ref - Lavender 45 ml (45 nights) GCPL 72 72 72 72 72 72 72 72 72 72 72 72 72 — — —

All Out Floral Refill - Power Plus 45 ml (45 nights) SC Johnson 72 72 72 72 72 72 72 72 72 72 72 72 72 — — —

Maxo Mosquito Repellent liquid 45 ml (45 nights) Jyothy Labs 69 67 67 67 67 67 67 67 67 67 67 67 69 3 3 3

Sprays/Aerosols

Hit Spray Cockroach Champion 320ml GCPL 172 100ml 50 50 50 54 54 54 54 54 54 54 54 54 — — —

Creams/Lotions

Good Knight Cool Gel 50gm GCPL 45 90 90 90 90 90 90 90 90 90 90 90 90 — — —

Odomos Mosquito Cream Natural 50gm Dabur 50 100g 100 100 100 100 100 100 100 100 100 100 100 100 — — —

Change (%)Normalised price in Rs (adjusted for grammage changes)

Consumer Staples India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 21

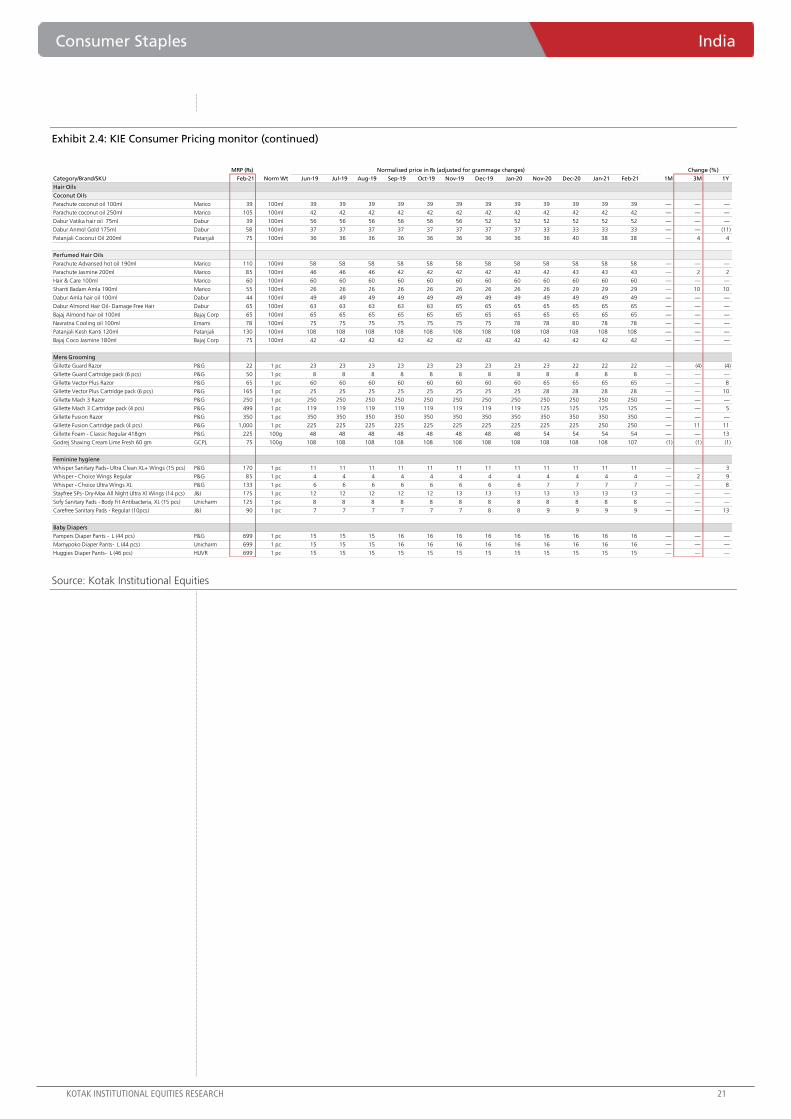

Exhibit 2.4: KIE Consumer Pricing monitor (continued)

Source: Kotak Institutional Equities

MRP (Rs)

Category/Brand/SKU Feb-21 Norm Wt Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Nov-20 Dec-20 Jan-21 Feb-21 1M 3M 1Y

Hair Oils

Coconut Oils

Parachute coconut oil 100ml Marico 39 100ml 39 39 39 39 39 39 39 39 39 39 39 39 — — —

Parachute coconut oil 250ml Marico 105 100ml 42 42 42 42 42 42 42 42 42 42 42 42 — — —

Dabur Vatika hair oil 75ml Dabur 39 100ml 56 56 56 56 56 56 52 52 52 52 52 52 — — —

Dabur Anmol Gold 175ml Dabur 58 100ml 37 37 37 37 37 37 37 37 33 33 33 33 — — (11)

Patanjali Coconut Oil 200ml Patanjali 75 100ml 36 36 36 36 36 36 36 36 36 40 38 38 — 4 4

Perfumed Hair Oils

Parachute Advansed hot oil 190ml Marico 110 100ml 58 58 58 58 58 58 58 58 58 58 58 58 — — —

Parachute Jasmine 200ml Marico 85 100ml 46 46 46 42 42 42 42 42 42 43 43 43 — 2 2

Hair & Care 100ml Marico 60 100ml 60 60 60 60 60 60 60 60 60 60 60 60 — — —

Shanti Badam Amla 190ml Marico 55 100ml 26 26 26 26 26 26 26 26 26 29 29 29 — 10 10

Dabur Amla hair oil 100ml Dabur 44 100ml 49 49 49 49 49 49 49 49 49 49 49 49 — — —

Dabur Almond Hair Oil- Damage Free Hair Dabur 65 100ml 63 63 63 63 63 65 65 65 65 65 65 65 — — —

Bajaj Almond hair oil 100ml Bajaj Corp 65 100ml 65 65 65 65 65 65 65 65 65 65 65 65 — — —

Navratna Cooling oil 100ml Emami 78 100ml 75 75 75 75 75 75 75 78 78 80 78 78 — — —

Patanjali Kesh Kanti 120ml Patanjali 130 100ml 108 108 108 108 108 108 108 108 108 108 108 108 — — —

Bajaj Coco Jasmine 180ml Bajaj Corp 75 100ml 42 42 42 42 42 42 42 42 42 42 42 42 — — —

Mens Grooming

Gillette Guard Razor P&G 22 1 pc 23 23 23 23 23 23 23 23 23 22 22 22 — (4) (4)

Gillette Guard Cartridge pack (6 pcs) P&G 50 1 pc 8 8 8 8 8 8 8 8 8 8 8 8 — — —

Gillette Vector Plus Razor P&G 65 1 pc 60 60 60 60 60 60 60 60 65 65 65 65 — — 8

Gillette Vector Plus Cartridge pack (6 pcs) P&G 165 1 pc 25 25 25 25 25 25 25 25 28 28 28 28 — — 10

Gillette Mach 3 Razor P&G 250 1 pc 250 250 250 250 250 250 250 250 250 250 250 250 — — —

Gillette Mach 3 Cartridge pack (4 pcs) P&G 499 1 pc 119 119 119 119 119 119 119 119 125 125 125 125 — — 5

Gillette Fusion Razor P&G 350 1 pc 350 350 350 350 350 350 350 350 350 350 350 350 — — —

Gillette Fusion Cartridge pack (4 pcs) P&G 1,000 1 pc 225 225 225 225 225 225 225 225 225 225 250 250 — 11 11

Gillette Foam - Classic Regular 418gm P&G 225 100g 48 48 48 48 48 48 48 48 54 54 54 54 — — 13

Godrej Shaving Cream Lime Fresh 60 gm GCPL 75 100g 108 108 108 108 108 108 108 108 108 108 108 107 (1) (1) (1)

Feminine hygiene

Whisper Sanitary Pads- Ultra Clean XL+ Wings (15 pcs) P&G 170 1 pc 11 11 11 11 11 11 11 11 11 11 11 11 — — 3

Whisper - Choice Wings Regular P&G 85 1 pc 4 4 4 4 4 4 4 4 4 4 4 4 — 2 9

Whisper - Choice Ultra Wings XL P&G 133 1 pc 6 6 6 6 6 6 6 6 7 7 7 7 — — 8

Stayfree SPs- Dry-Max All Night Ultra Xl Wings (14 pcs) J&J 175 1 pc 12 12 12 12 12 13 13 13 13 13 13 13 — — —

Sofy Sanitary Pads - Body Fit Antibacteria, XL (15 pcs) Unicharm 125 1 pc 8 8 8 8 8 8 8 8 8 8 8 8 — — —

Carefree Sanitary Pads - Regular (10pcs) J&J 90 1 pc 7 7 7 7 7 7 8 8 9 9 9 9 — — 13

Baby Diapers

Pampers Diaper Pants - L (44 pcs) P&G 699 1 pc 15 15 15 16 16 16 16 16 16 16 16 16 — — —

Mamypoko Diaper Pants- L (44 pcs) Unicharm 699 1 pc 15 15 15 16 16 16 16 16 16 16 16 16 — — —

Huggies Diaper Pants- L (46 pcs) HUVR 699 1 pc 15 15 15 15 15 15 15 15 15 15 15 15 — — —

Change (%)Normalised price in Rs (adjusted for grammage changes)

India Consumer Staples

22 KOTAK INSTITUTIONAL EQUITIES RESEARCH

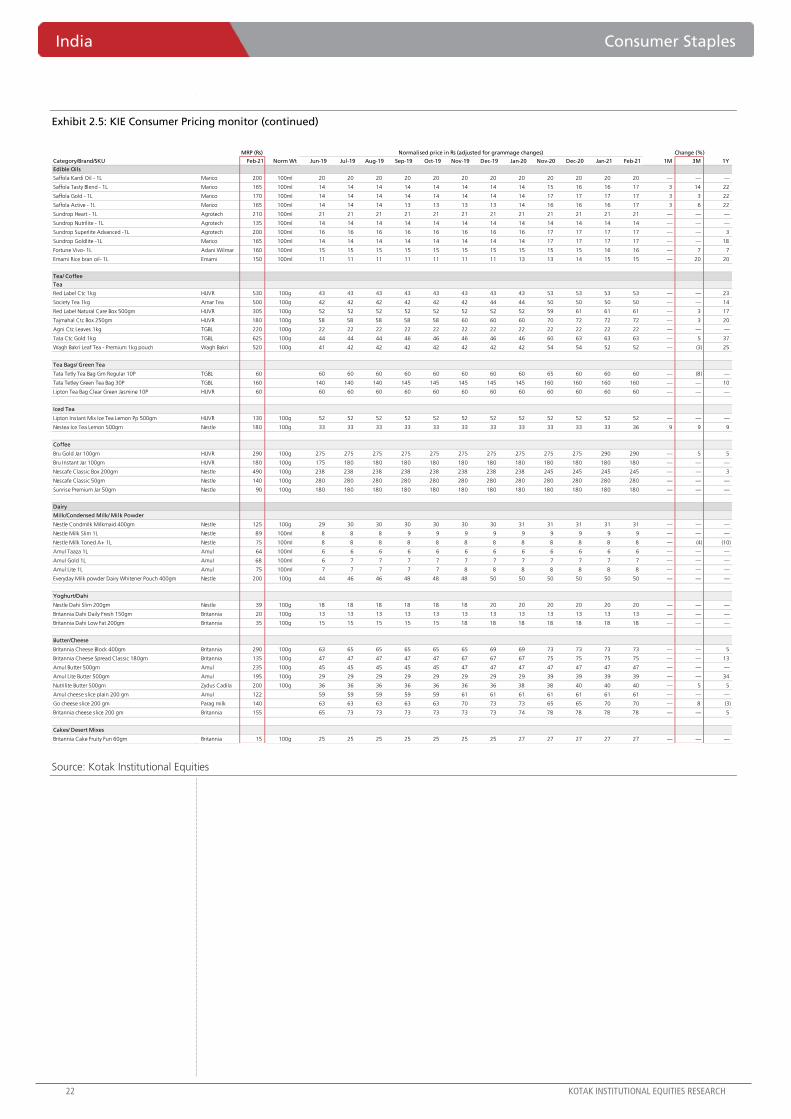

Exhibit 2.5: KIE Consumer Pricing monitor (continued)

Source: Kotak Institutional Equities

MRP (Rs)

Category/Brand/SKU Feb-21 Norm Wt Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Nov-20 Dec-20 Jan-21 Feb-21 1M 3M 1Y

Edible Oils

Saffola Kardi Oil - 1L Marico 200 100ml 20 20 20 20 20 20 20 20 20 20 20 20 — — —

Saffola Tasty Blend - 1L Marico 165 100ml 14 14 14 14 14 14 14 14 15 16 16 17 3 14 22

Saffola Gold - 1L Marico 170 100ml 14 14 14 14 14 14 14 14 17 17 17 17 3 3 22

Saffola Active - 1L Marico 165 100ml 14 14 14 13 13 13 13 14 16 16 16 17 3 6 22

Sundrop Heart - 1L Agrotech 210 100ml 21 21 21 21 21 21 21 21 21 21 21 21 — — —

Sundrop Nutrilite - 1L Agrotech 135 100ml 14 14 14 14 14 14 14 14 14 14 14 14 — — —

Sundrop Superlite Advanced -1L Agrotech 200 100ml 16 16 16 16 16 16 16 16 17 17 17 17 — — 3

Sundrop Goldlite -1L Marico 165 100ml 14 14 14 14 14 14 14 14 17 17 17 17 — — 18

Fortune Vivo- 1L Adani Wilmar 160 100ml 15 15 15 15 15 15 15 15 15 15 16 16 — 7 7

Emami Rice bran oil- 1L Emami 150 100ml 11 11 11 11 11 11 11 13 13 14 15 15 — 20 20

Tea/ Coffee

Tea

Red Label Ctc 1kg HUVR 530 100g 43 43 43 43 43 43 43 43 53 53 53 53 — — 23

Society Tea 1kg Amar Tea 500 100g 42 42 42 42 42 42 44 44 50 50 50 50 — — 14

Red Label Natural Care Box 500gm HUVR 305 100g 52 52 52 52 52 52 52 52 59 61 61 61 — 3 17

Tajmahal Ctc Box 250gm HUVR 180 100g 58 58 58 58 58 60 60 60 70 72 72 72 — 3 20

Agni Ctc Leaves 1kg TGBL 220 100g 22 22 22 22 22 22 22 22 22 22 22 22 — — —

Tata Ctc Gold 1kg TGBL 625 100g 44 44 44 46 46 46 46 46 60 63 63 63 — 5 37

Wagh Bakri Leaf Tea - Premium 1kg pouch Wagh Bakri 520 100g 41 42 42 42 42 42 42 42 54 54 52 52 — (3) 25

Tea Bags/ Green Tea

Tata Tetly Tea Bag Grn Regular 10P TGBL 60 60 60 60 60 60 60 60 60 65 60 60 60 — (8) —

Tata Tetley Green Tea Bag 30P TGBL 160 140 140 140 145 145 145 145 145 160 160 160 160 — — 10

Lipton Tea Bag Clear Green Jasmine 10P HUVR 60 60 60 60 60 60 60 60 60 60 60 60 60 — — —

Iced Tea

Lipton Instant Mix Ice Tea Lemon Pp 500gm HUVR 130 100g 52 52 52 52 52 52 52 52 52 52 52 52 — — —

Nestea Ice Tea Lemon 500gm Nestle 180 100g 33 33 33 33 33 33 33 33 33 33 33 36 9 9 9

Coffee

Bru Gold Jar 100gm HUVR 290 100g 275 275 275 275 275 275 275 275 275 275 290 290 — 5 5

Bru Instant Jar 100gm HUVR 180 100g 175 180 180 180 180 180 180 180 180 180 180 180 — — —

Nescafe Classic Box 200gm Nestle 490 100g 238 238 238 238 238 238 238 238 245 245 245 245 — — 3

Nescafe Classic 50gm Nestle 140 100g 280 280 280 280 280 280 280 280 280 280 280 280 — — —

Sunrise Premium Jar 50gm Nestle 90 100g 180 180 180 180 180 180 180 180 180 180 180 180 — — —

Dairy

Milk/Condensed Milk/ Milk Powder

Nestle Condmilk Milkmaid 400gm Nestle 125 100g 29 30 30 30 30 30 30 31 31 31 31 31 — — —

Nestle Milk Slim 1L Nestle 89 100ml 8 8 8 9 9 9 9 9 9 9 9 9 — — —

Nestle Milk Toned A+ 1L Nestle 75 100ml 8 8 8 8 8 8 8 8 8 8 8 8 — (4) (10)

Amul Taaza 1L Amul 64 100ml 6 6 6 6 6 6 6 6 6 6 6 6 — — —

Amul Gold 1L Amul 68 100ml 6 7 7 7 7 7 7 7 7 7 7 7 — — —

Amul Lite 1L Amul 75 100ml 7 7 7 7 7 8 8 8 8 8 8 8 — — —

Everyday Milk powder Dairy Whitener Pouch 400gm Nestle 200 100g 44 46 46 48 48 48 50 50 50 50 50 50 — — —

Yoghurt/Dahi

Nestle Dahi Slim 200gm Nestle 39 100g 18 18 18 18 18 18 20 20 20 20 20 20 — — —

Britannia Dahi Daily Fresh 150gm Britannia 20 100g 13 13 13 13 13 13 13 13 13 13 13 13 — — —

Britannia Dahi Low Fat 200gm Britannia 35 100g 15 15 15 15 15 18 18 18 18 18 18 18 — — —

Butter/Cheese

Britannia Cheese Block 400gm Britannia 290 100g 63 65 65 65 65 65 69 69 73 73 73 73 — — 5

Britannia Cheese Spread Classic 180gm Britannia 135 100g 47 47 47 47 47 67 67 67 75 75 75 75 — — 13

Amul Butter 500gm Amul 235 100g 45 45 45 45 45 47 47 47 47 47 47 47 — — —

Amul Lite Butter 500gm Amul 195 100g 29 29 29 29 29 29 29 29 39 39 39 39 — — 34

Nutrilite Butter 500gm Zydus Cadila 200 100g 36 36 36 36 36 36 36 38 38 40 40 40 — 5 5

Amul cheese slice plain 200 gm Amul 122 59 59 59 59 59 61 61 61 61 61 61 61 — — —

Go cheese slice 200 gm Parag milk 140 63 63 63 63 63 70 73 73 65 65 70 70 — 8 (3)

Britannia cheese slice 200 gm Britannia 155 65 73 73 73 73 73 73 74 78 78 78 78 — — 5

Cakes/ Desert Mixes

Britannia Cake Fruity Fun 60gm Britannia 15 100g 25 25 25 25 25 25 25 27 27 27 27 27 — — —

Change (%)Normalised price in Rs (adjusted for grammage changes)

Consumer Staples India

KOTAK INSTITUTIONAL EQUITIES RESEARCH 23

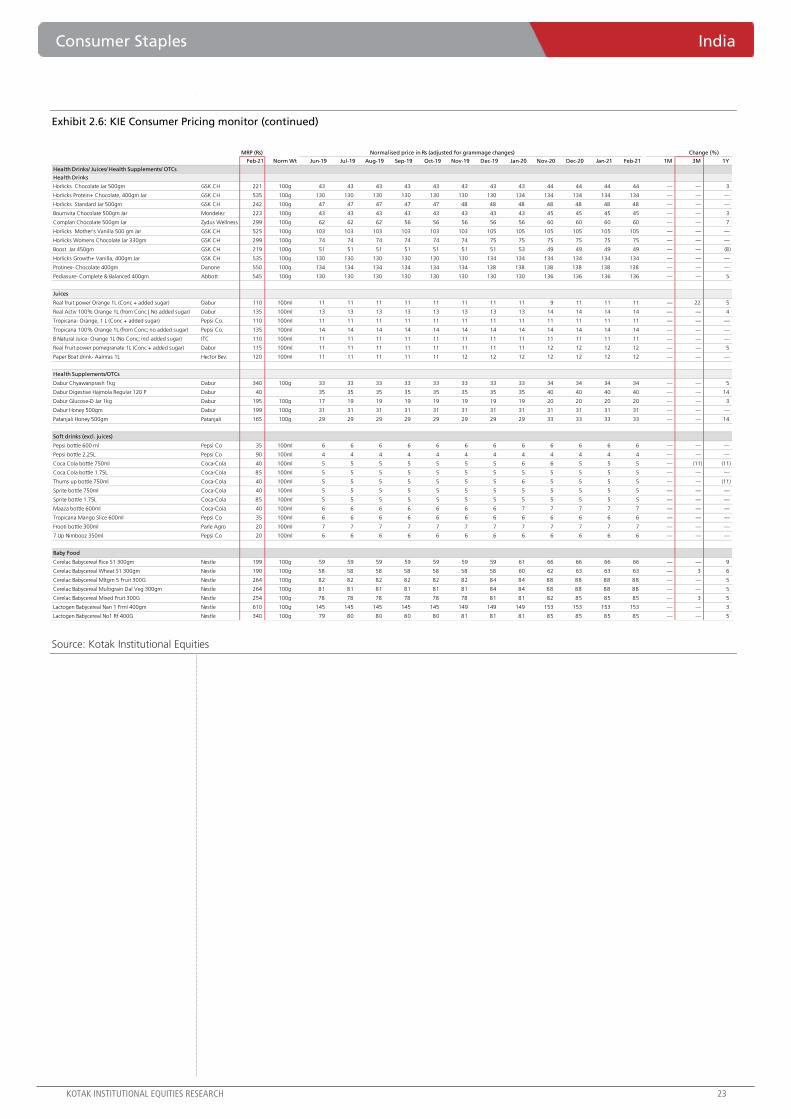

Exhibit 2.6: KIE Consumer Pricing monitor (continued)

Source: Kotak Institutional Equities

MRP (Rs)

Feb-21 Norm Wt Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Nov-20 Dec-20 Jan-21 Feb-21 1M 3M 1Y

Health Drinks/ Juices/ Health Supplements/ OTCs

Health Drinks

Horlicks Chocolate Jar 500gm GSK CH 221 100g 43 43 43 43 43 43 43 43 44 44 44 44 — — 3

Horlicks Protein+ Chocolate, 400gm Jar GSK CH 535 100g 130 130 130 130 130 130 130 134 134 134 134 134 — — —

Horlicks Standard Jar 500gm GSK CH 242 100g 47 47 47 47 47 48 48 48 48 48 48 48 — — —

Bournvita Chocolate 500gm Jar Mondelez 223 100g 43 43 43 43 43 43 43 43 45 45 45 45 — — 3

Complan Chocolate 500gm Jar Zydus Wellness 299 100g 62 62 62 56 56 56 56 56 60 60 60 60 — — 7

Horlicks Mother's Vanilla 500 gm Jar GSK CH 525 100g 103 103 103 103 103 103 105 105 105 105 105 105 — — —

Horlicks Womens Chocolate Jar 330gm GSK CH 299 100g 74 74 74 74 74 74 75 75 75 75 75 75 — — —

Boost Jar 450gm GSK CH 219 100g 51 51 51 51 51 51 51 53 49 49 49 49 — — (8)

Horlicks Growth+ Vanilla, 400gm Jar GSK CH 535 100g 130 130 130 130 130 130 134 134 134 134 134 134 — — —

Protinex- Chocolate 400gm Danone 550 100g 134 134 134 134 134 134 138 138 138 138 138 138 — — —

Pediasure- Complete & Balanced 400gm Abbott 545 100g 130 130 130 130 130 130 130 130 136 136 136 136 — — 5

Juices

Real fruit power Orange 1L (Conc + added sugar) Dabur 110 100ml 11 11 11 11 11 11 11 11 9 11 11 11 — 22 5

Real Activ 100% Orange 1L (from Conc | No added sugar) Dabur 135 100ml 13 13 13 13 13 13 13 13 14 14 14 14 — — 4

Tropicana- Orange, 1 L (Conc + added sugar) Pepsi Co. 110 100ml 11 11 11 11 11 11 11 11 11 11 11 11 — — —

Tropicana 100% Orange 1L (from Conc; no added sugar) Pepsi Co. 135 100ml 14 14 14 14 14 14 14 14 14 14 14 14 — — —

B Natural Juice- Orange 1L (No Conc; incl added sugar) ITC 110 100ml 11 11 11 11 11 11 11 11 11 11 11 11 — — —

Real Fruit power pomegranate 1L (Conc + added sugar) Dabur 115 100ml 11 11 11 11 11 11 11 11 12 12 12 12 — — 5

Paper Boat drink- Aamras 1L Hector Bev. 120 100ml 11 11 11 11 11 12 12 12 12 12 12 12 — — —

Health Supplements/OTCs

Dabur Chyawanprash 1kg Dabur 340 100g 33 33 33 33 33 33 33 33 34 34 34 34 — — 5

Dabur Digestive Hajmola Regular 120 P Dabur 40 35 35 35 35 35 35 35 35 40 40 40 40 — — 14

Dabur Glucose-D Jar 1kg Dabur 195 100g 17 19 19 19 19 19 19 19 20 20 20 20 — — 3

Dabur Honey 500gm Dabur 199 100g 31 31 31 31 31 31 31 31 31 31 31 31 — — —

Patanjali Honey 500gm Patanjali 165 100g 29 29 29 29 29 29 29 29 33 33 33 33 — — 14

Soft drinks (excl. juices)

Pepsi bottle 600 ml Pepsi Co 35 100ml 6 6 6 6 6 6 6 6 6 6 6 6 — — —

Pepsi bottle 2.25L Pepsi Co 90 100ml 4 4 4 4 4 4 4 4 4 4 4 4 — — —

Coca Cola bottle 750ml Coca-Cola 40 100ml 5 5 5 5 5 5 5 6 6 5 5 5 — (11) (11)

Coca Cola bottle 1.75L Coca-Cola 85 100ml 5 5 5 5 5 5 5 5 5 5 5 5 — — —

Thums up bottle 750ml Coca-Cola 40 100ml 5 5 5 5 5 5 5 6 5 5 5 5 — — (11)

Sprite bottle 750ml Coca-Cola 40 100ml 5 5 5 5 5 5 5 5 5 5 5 5 — — —

Sprite bottle 1.75L Coca-Cola 85 100ml 5 5 5 5 5 5 5 5 5 5 5 5 — — —

Maaza bottle 600ml Coca-Cola 40 100ml 6 6 6 6 6 6 6 7 7 7 7 7 — — —

Tropicana Mango Slice 600ml Pepsi Co 35 100ml 6 6 6 6 6 6 6 6 6 6 6 6 — — —

Frooti bottle 300ml Parle Agro 20 100ml 7 7 7 7 7 7 7 7 7 7 7 7 — — —

7 Up Nimbooz 350ml Pepsi Co 20 100ml 6 6 6 6 6 6 6 6 6 6 6 6 — — —

Baby Food

Cerelac Babycereal Rice S1 300gm Nestle 199 100g 59 59 59 59 59 59 59 61 66 66 66 66 — — 9

Cerelac Babycereal Wheat S1 300gm Nestle 190 100g 58 58 58 58 58 58 58 60 62 63 63 63 — 3 6

Cerelac Babycereal Mltgrn 5 Fruit 300G Nestle 264 100g 82 82 82 82 82 82 84 84 88 88 88 88 — — 5

Cerelac Babycereal Multigrain Dal Veg 300gm Nestle 264 100g 81 81 81 81 81 81 84 84 88 88 88 88 — — 5

Cerelac Babycereal Mixed Fruit 300G Nestle 254 100g 78 78 78 78 78 78 81 81 82 85 85 85 — 3 5

Lactogen Babycereal Nan 1 Frml 400gm Nestle 610 100g 145 145 145 145 145 149 149 149 153 153 153 153 — — 3

Lactogen Babycereal No1 Rf 400G Nestle 340 100g 79 80 80 80 80 81 81 81 85 85 85 85 — — 5

Change (%)Normalised price in Rs (adjusted for grammage changes)

India Consumer Staples

24 KOTAK INSTITUTIONAL EQUITIES RESEARCH

Exhibit 2.7: KIE Consumer Pricing monitor (continued)

Source: Kotak Institutional Equities

MRP (Rs)

Category/Brand/SKU Feb-21 Norm Wt Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Nov-20 Dec-20 Jan-21 Feb-21 1M 3M 1Y

Biscuits/Atta

CreamBiscuits

Sunfeast Dark Fantasy Chocolate 100gm ITC 30 100g 40 40 40 40 40 40 40 40 40 40 40 40 — — —

Britannia Cream Jim Jam 150gm Britannia 35 100g 23 23 23 23 23 23 23 23 23 23 23 23 — — —

Britannia Cream Pure magic vanilla 150gm Britannia 30 100g 30 30 30 30 30 30 30 30 30 30 30 30 — — —

Britannia Cream Treat Bourbon 150gm Britannia 30 100g 19 19 19 19 19 19 20 20 20 20 20 20 — — —