do political news affect financial market returns ... · (selic over and di) which ranged from...

TRANSCRIPT

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

545

Do Political News Affect Financial Market

Returns? Evidences from Brazil

Thales Batiston Marques Economia e Relações Internacionais, Universidade Federal do Rio Grande do

Sul, Porto Alegre, Brazil

Nelson Seixas dos Santos1 Economia e Relações Internacionais, Universidade Federal do Rio Grande do

Sul, Porto Alegre, Brazil

Abstract

This paper investigates the relation between political news and market

returns. To do so we applied a Garch filter to a sample of the main Brazilian

stock market index returns (Ibovespa Index) and of short-term interest rates

(Selic Over and DI) which ranged from 01/02/2014 to 04/29/2016. Then we

looked for periods of abnormal volatility which might be associated with

political events using a parametric and a nonparametric method.

Notwithstanding there were news like important politician been arrested and

even speculation about the beginning of an impeachment process, we found

relation between abnormal volatilities and political news only in Ibovespa

returns during Presidential Elections.

Keywords: Political Events, Financial Markets, Information, GARCH.

Cite this article: Marques, T. B., & dos Santos, N. S. (2016). Do Political News Affect Financial Market Returns? Evidences from Brazil. International Journal of Management,

Accounting and Economics, 3(10), 545-571.

Introduction

The recent political events in Brazil has been grabbing the media’s attention. It is

normal to find these vehicles associating the political events with financial markets

oscillation. Nevertheless, this common sense approach to market prices runs into efficient

market hypothesis as posed by Fama (1970).

1 Corresponding author’s email: [email protected]

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

546

Actually, the impact of political events on financial markets is a widespread issue.

Smales (2015) measured the role of political uncertainty on implied volatility with

macroeconomics variables in the regression model and Australian Financial Market data.

Jovanovic & Zimmermann (2008) tested whether U.S. Federal Reserve (FED) reacts to

market’s uncertainty. They concluded that FED decreases the interest rates in periods of

abnormal volatility in the stock market and raise them in the opposite case,

notwithstanding with inflation rates. In South Africa’s Financial Markets, Naraidoo &

Raputsoane (2015) found interest rates are guided by inflation uncertainty.

In this paper, we analyzed whether fixed income and the stock market volatility

movements matches political news. To do so we used a GARCH model to filter volatility

and then we compared timing of political events and abnormal volatility to find out

correlations between them using two different approaches: a parametric and a

nonparametric method to distinguish abnormal volatilities from normal ones.

This paper is organized as follows. Section 2 is a quick introduction to Brazilian

Political Institutions and to the Financial System, which has some singularities compared

to countries like United States, France and England. The Section 0is a literature review.

The Section 4 has the Empirical Strategy, the subsections are: Data, Methods, Alternative

1 – Parametric and Alternative 2 – Non-parametric. Section 5 has the Results and

Discussion. Section 6 has Concluding Remarks and the Section 7 is the Bibliography.

Brazilian Political Institutions and Financial System

Brazil is a federative republic with a presidential system, where the legislative,

executive and judiciary branches of government are independents from each other. The

president is elected for a four-year administration and can be reelected for only one

subsequent term (Brazil, Constituição da República Federativa do Brasil: 49ª edição,

1988). The president chooses his ministers and the president of Central Bank of Brazil.

The last one needs to be approved by the senate and he can be fired at any moment, in

other words, the Central Bank is not independent

The

Table 1 shows the composition of the Brazilian Financial System.

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

547

Table 1 – Brazilian Financial System

Regulating entities Supervision Entities Operators

National

Monetary Council

(CMN)

Central Bank of

Brazil (BCB)

Financial

institutions

taking

demand

deposits

Other

financial

institutions

Other financial

intermediaries and

entities administering

financial assets of third

parties

Foreign

exchange

banks

Securities and

Exchange

Commission

(CVM)

Commodities

and futures

exchanges

Stock

exchanges

National Council

for Private

Insurance (CNSP)

Private Insurance

Superintendence

(SUSEP)

Reinsurance

Companies

Insurance

companies

Capitalization

companies

Entities

operating

private

open

pension

funds

National Council

for

Complementary

Pension (CNPC)

National

Complementary

Pension

Superintendency

(PREVIC)

Entities operating private closed pension funds

Source: Central Bank of Brazil

Financial system is built upon Law 4595/1964 (1964), which establishes National

Monetary Council (CMN) as the major normative institution of Brazilian Financial

System. (Brazil, 1964). The institution is composed by the Minister of Finance, Minister

of Planning and President of Central Bank of Brazil. The objectives of CMN are defining

monetary and exchange rate policies and establishing rules for the financial system.

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

548

The Central Bank of Brazil, according to the Constitution (1988), has the monopoly of

notes issuance, is the government’s banker and also the banker’s bank, along with this,

the Central Bank is the supervisor of the financial system, the executor of monetary and

exchange rate policies.

In June, 1999, Brazil adopted the inflation targeting regime, where de CMN defines

the inflation target and the Central Bank pursues this target using monetary policy,

although there is a tolerance level for that target. Actually, Monetary Policy Committee

(Copom) is Central Bank decision making body on monetary policy responsible for

setting the target of short-term interest rate (Selic). There is Copom’s meetings each forty-

five days and an official note is released informing the directions of the Selic rate target.

In fact, Brazil has only one stock exchange, the BM&FBovespa, which is a company

that manages the organized securities, commodities and derivatives markets. According

to the BM&FBovespa (2016) “The Bovespa Index (Ibovespa) is compiled as a weighted

average of a theoretical portfolio of stocks pursuant to criteria set forth in this

methodology”. Only shares and units listed on BM&FBovespa that are within the

inclusion criteria can compose the index.

The Clearing House for the Custody and Financial Settlement of Securities (CETIP)

is a” depositary” of mainly private fixed income, state and city public securities and some

securities representing National Treasury debts” (Central Bank of Brazil, 2016).

Political Uncertainty and Financial Markets Informational Efficiency

Fama (1970) defined market efficiency in terms of information organized three

information subsets to efficient markets: the weak form, where the information set

includes only the history of prices; the semi-strong form, where the information set is the

publicly available information; and the strong form, where the information set includes

all the information, including the private information. In the strong form the existence of

abnormal returns is not possible, because the information is repassed so rapidly to the

prices that makes impossible to achieve gains.

There is massive literature of empirical analysis of efficient markets hypothesis

(EMH). This paper focused to review the literature about these markets on emerging

countries. Kamal (2014) studied the Egyptian Exchange (EGX) before and after the 25th

January Revolution when the stock market was closed and, for both cases, rejected the

weak-form efficiency hypothesis.

Dong, Bowers, & Latham (2013) studied the relationship of the markets around the

world and if they are efficient. The authors realized that, to the market be at least efficient,

it can’t exist any global or regional leader on the market, but they founded evidences of

this existence, these conclusion violates the EMH.

Recently, in Brazil, Gabriel, Ribeiro, & de Sousa Ribeiro (2013) studied the behavior

of stock prices of companies that belong to segment of “white line” household appliances,

furniture, papers and cellulose during the period of the announcement by Brazilian

government of reduction of Industrial Products Tax (IPI) in March of 2012. Using the

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

549

event study, the results leaded to the conclusion that the market wasn’t showed the

behavior of EMH, especially the semi-strong form.

Baker, Bloom and Davis (2012), though, realized that, before 2008 crises, the stock

market usually moved in response to economic news, however this changed after the

subprime crisis, the actions of policy-makers and their statements are impacting directly

the stock market. The authors created an index to measure the policy uncertainty where

they combine three types of information:

“(…) frequency of newspaper articles that reference economic uncertainty and the

role of policy; the number of federal tax code provisions that are set to expire in coming

years; the extent of disagreement among economic forecasters about future inflation and

future government spending on goods and services” (Baker, Bloom, & Davis, 2012).

At the same time, they created another index to measure the policy uncertainty

searching for news on Google News using keywords as ‘uncertain’ or ‘uncertainty’ with

‘economic’ or ‘economy’.

According to Jovanic & Zimmermann (2008), the FED of United States reacts to

uncertainty reducing the interest rates when there is high volatility in the stock market

and raises in the opposite case, ignoring the inflation control of the last 15 years before

the study. Laakkonen (2015) studies the fixed income of United States from investors’

viewpoint and how they react to uncertainty. The author uses the volatility of Ten Years

US Treasury Note futures and concluded that investors reacts stronger when news are

associated with low uncertainty, raising the volatility and the trade volume of those future

contracts. The paper uses three types of uncertainties: the macroeconomic, discordance

between professional forecasters about the macroeconomic scenario, the financial

uncertainty, which is measure through the VIX and the political uncertainty, which is

measure by the policy uncertainty index by Baker etl al. (2012). The conclusion was that

investor react to news significantly stronger when uncertainty is low and they are more

sensitive to uncertainty in the financial market.

Smales (2015) analyzed the Australian electoral cycle and the uncertainty from the

real economy and financial markets. He found the implied volatility of equity and bond

options increases with the election uncertainty, that is, there exists a relationship between

financial market uncertainty and political uncertainty

On the other side, in South Africa, which has a monetary policy institutional

framework similar to Brazil’s, Naraidoo & Raputsoane (2015) found interest rates are

guided by inflation uncertainty, output gap and financial conditions. The author defined

financial conditions with the financial condition index, which is made up by the average

price of all houses, the real stock prices, the real effective exchange rate, the credit spread,

and the future spread.

Empirical Strategy

Data

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

550

We collect a sample of Bovespa Index, DI and SELIC, because those prices are the

most used one to evaluate conditions of capital and private and public bond markets in

Brazil, respectively. T he first one was collected from the Brazil’s Central Bank Time

Series Management System (Central Bank of Brazil, 2016) at 05/11/2016 in the CSV

format. The code of Bovespa Index is 7. The series started at 01/02/2014 and ended at

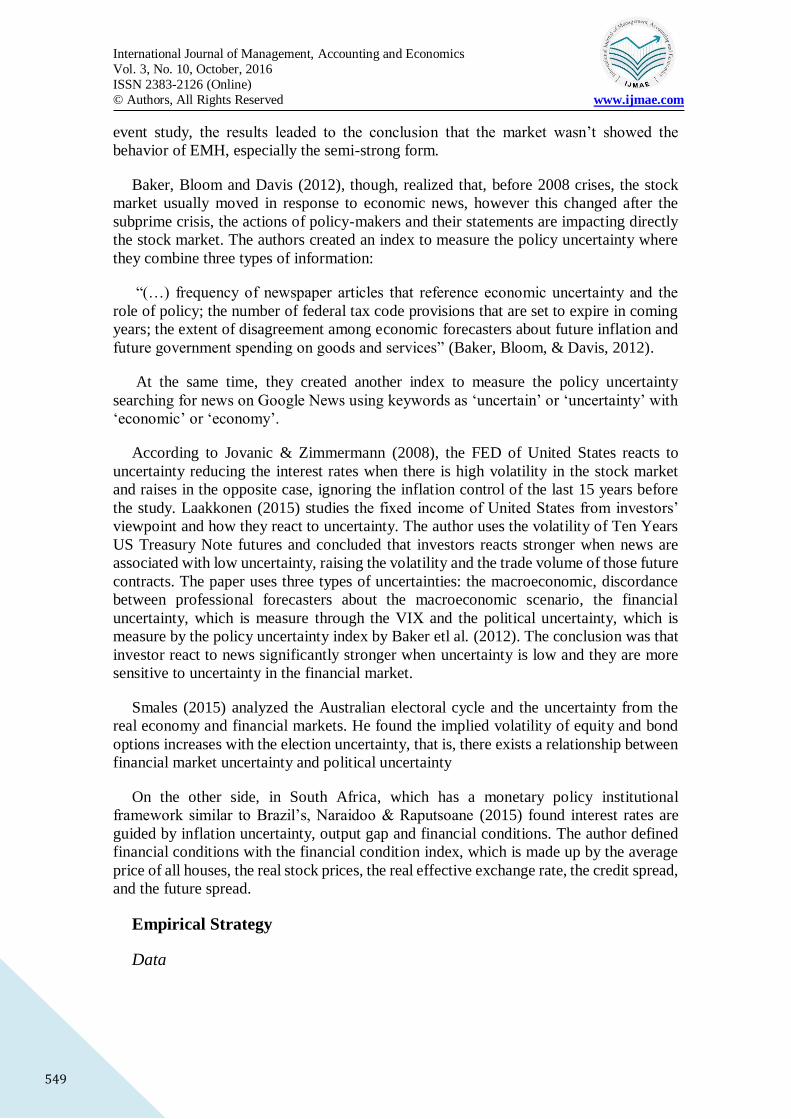

04/29/2016 and was daily separated. The Figure 1 shows the series through the time.

Figure 1 Bovespa Index 2014-2016

A crisis started to surround the Brazilian economy in 2014, which was the year of

presidential elections where Ms. Rousseff was reelected to other 4-years mandate. The

year of 2015 was marked by the explosion of the crisis, the fall of the Ms. Rousseff’s

popularity reflected on the popular manifestations demanding the impeachment of her,

the failed attempt of government to recover credibility by nominating an orthodox

economist to lead the Ministry of Finance and was also marked by the evolution of

investigations of corrupt practices with the Brazilian state-controlled oil company,

Petrobras. At last, in 2016 the president impeachment happened, where Mr. Temer, a

center-right politician and also vice-president, assumed the presidency.

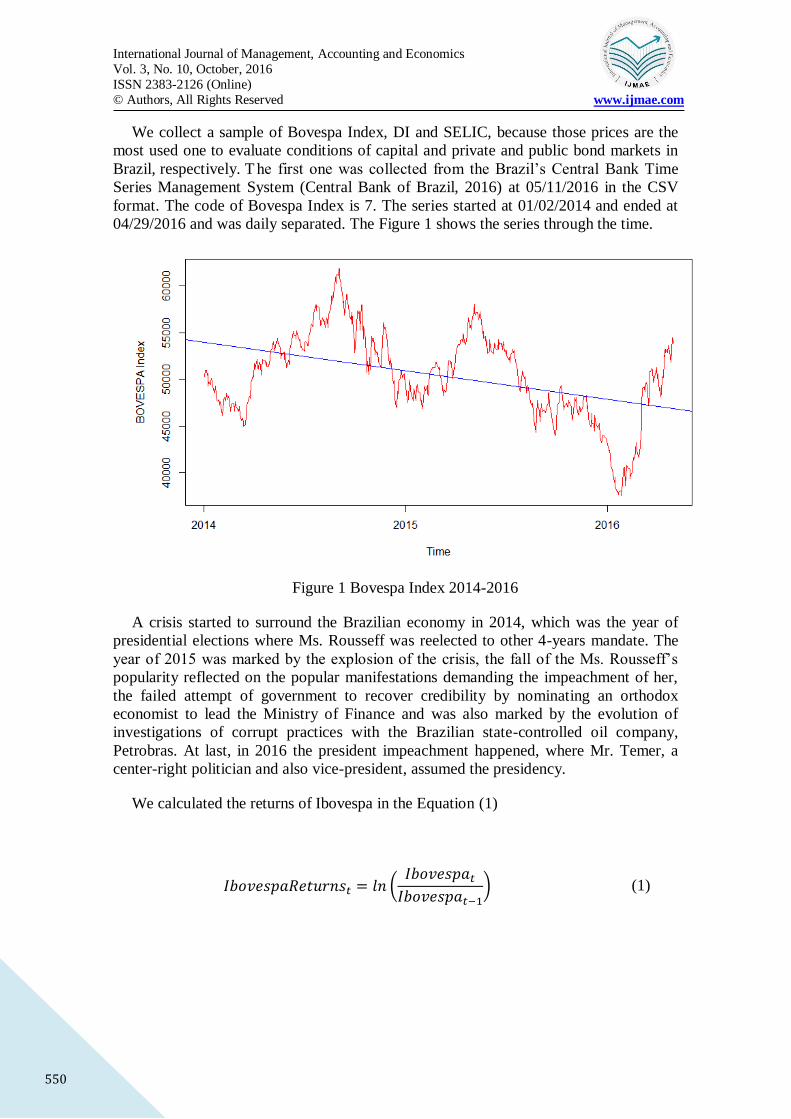

We calculated the returns of Ibovespa in the Equation (1)

𝐼𝑏𝑜𝑣𝑒𝑠𝑝𝑎𝑅𝑒𝑡𝑢𝑟𝑛𝑠𝑡 = 𝑙𝑛(𝐼𝑏𝑜𝑣𝑒𝑠𝑝𝑎𝑡𝐼𝑏𝑜𝑣𝑒𝑠𝑝𝑎𝑡−1

) (1)

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

551

Figure 2 Bovespa Index Returns 2014-2016

We tested the Ibovespa Returns (IR) to observe if the series has unit root and if the

series is stationary by using the Augmented Dickey-Fuller (ADF) test (1979) and the

Kwiatkowski–Phillips–Schmidt–Shin (KPSS) test (1992), respectively. Visually, the

Figure 2 shows a stationarity form, to confirm this hypothesis, the Table 2 and

Table 3 returns the results obtained.

Table 2 ADF Test (IR)

Estimate Std. Error t value Pr(>|t|)

z.lag.1 -0.992446 0.058360 -17.005 <2e-16 ***

z.diff.lag 0.004417 0.041436 0.107 0.915

Table 3 KPSS Test (IR)

test-statistic Significance level 5%

KPSS 0.0919 0.463

The ADF Test rejected the Null Hypothesis of unit root’s existence and the KPSS Test

accepted the Null Hypothesis of stationarity.

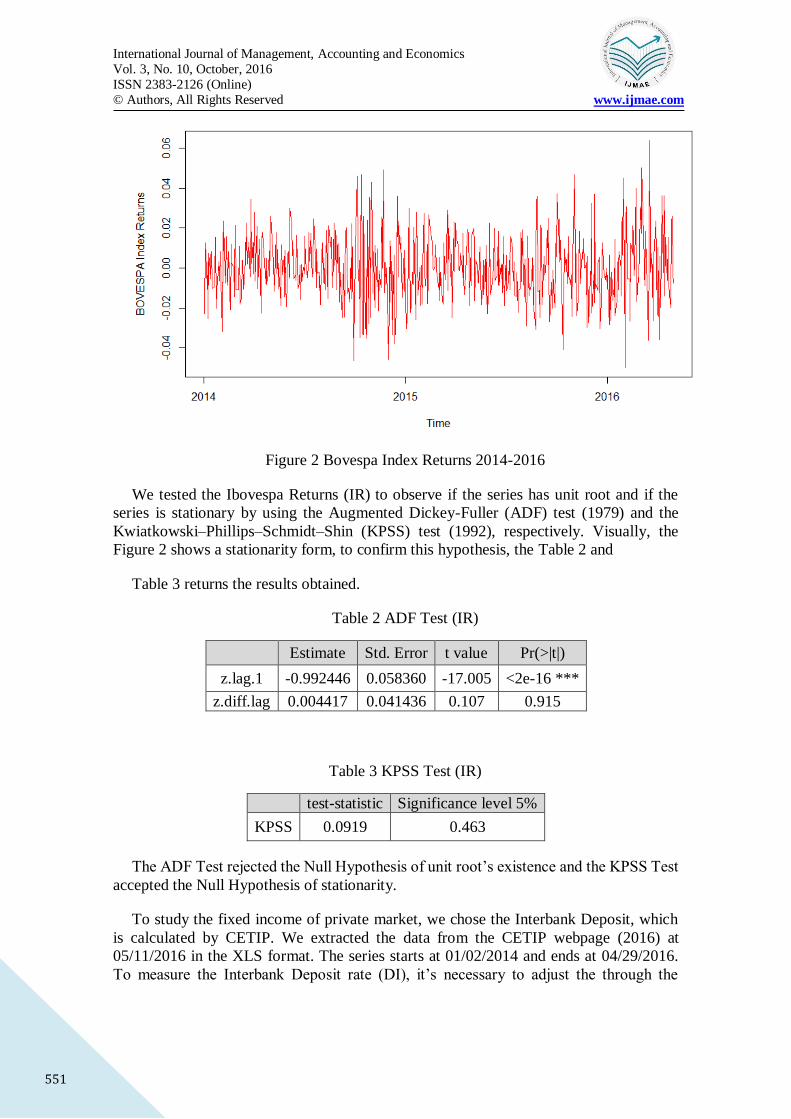

To study the fixed income of private market, we chose the Interbank Deposit, which

is calculated by CETIP. We extracted the data from the CETIP webpage (2016) at

05/11/2016 in the XLS format. The series starts at 01/02/2014 and ends at 04/29/2016.

To measure the Interbank Deposit rate (DI), it’s necessary to adjust the through the

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

552

Equation (2). The file is only available in Portuguese, daily factor is fator diário in the

XLS file.

𝑋𝑡 = 𝐹𝑎𝑡𝑜𝑟𝑑𝑖á𝑟𝑖𝑜 − 1 (2)

Figure 3 DI

The Figure 3 shows a deterministic trend. The Hypothesis of unit root of ADF Test

was accepted and the Null Hypothesis of stationarity of KPSS Test was rejected, implying

in non-stationarity. The Error! Reference source not found. and Table 5 returns the

results obtained from the tests.

Table 4 ADF Test (DI)

Estimate Std. Error t value Pr(>|t|)

(Intercept) 3.013e-06 2.154e-06 1.399 0.162

z.lag.1 -6.997e-03 5.779e-03 -1.211 0.226

Tt 1.643e-09 1.849e-09 0.888 0.375

z.diff.lag 9.374e-03 4.170e-02 0.225 0.822

Table 5 KPSS Test (DI)

test-statistic significance level 5%

KPSS 0.3567 0.146

We solved the unit root problem, as showed at Table 6 and Table 7, using the daily

variation of the DI. The Figure 4 shows the behavior of the data.

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

553

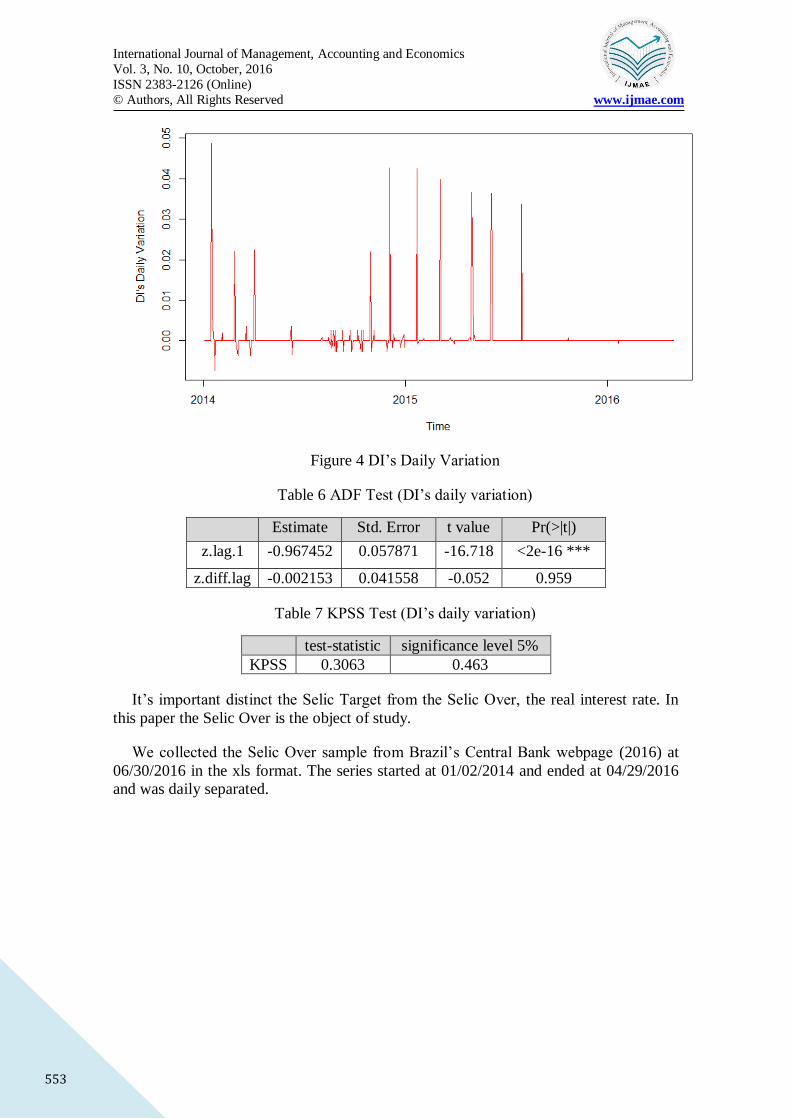

Figure 4 DI’s Daily Variation

Table 6 ADF Test (DI’s daily variation)

Estimate Std. Error t value Pr(>|t|)

z.lag.1 -0.967452 0.057871 -16.718 <2e-16 ***

z.diff.lag -0.002153 0.041558 -0.052 0.959

Table 7 KPSS Test (DI’s daily variation)

test-statistic significance level 5%

KPSS 0.3063 0.463

It’s important distinct the Selic Target from the Selic Over, the real interest rate. In

this paper the Selic Over is the object of study.

We collected the Selic Over sample from Brazil’s Central Bank webpage (2016) at

06/30/2016 in the xls format. The series started at 01/02/2014 and ended at 04/29/2016

and was daily separated.

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

554

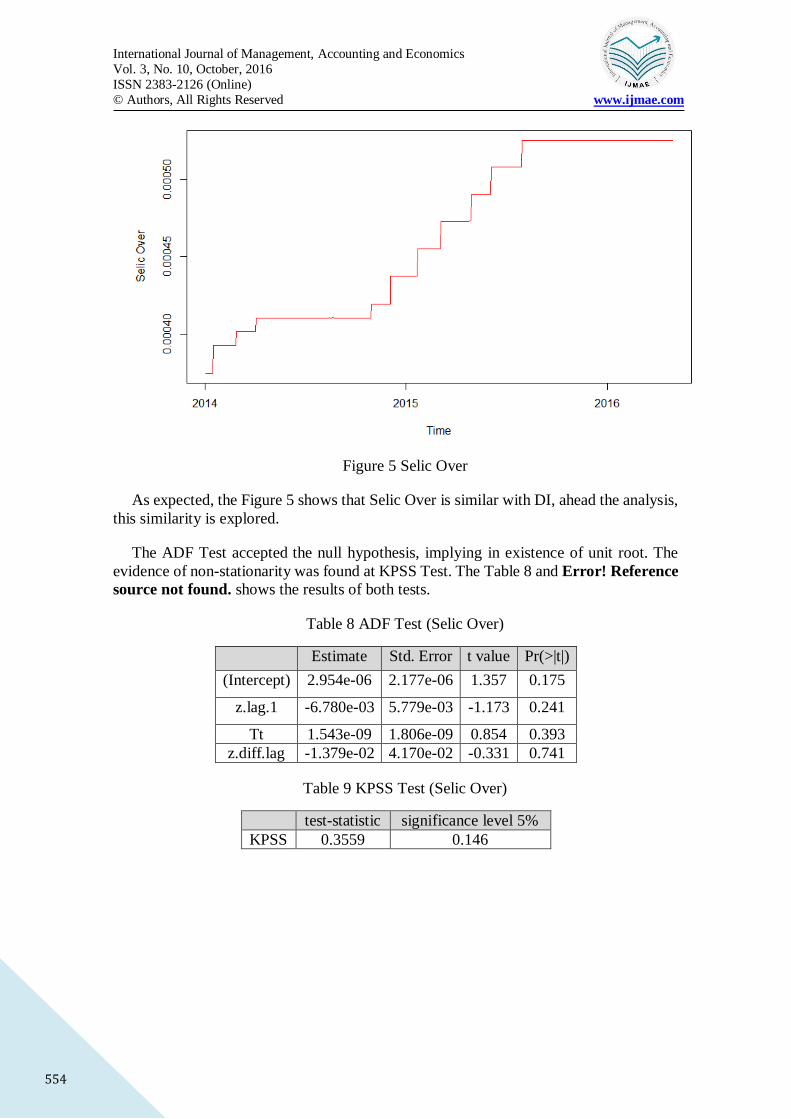

Figure 5 Selic Over

As expected, the Figure 5 shows that Selic Over is similar with DI, ahead the analysis,

this similarity is explored.

The ADF Test accepted the null hypothesis, implying in existence of unit root. The

evidence of non-stationarity was found at KPSS Test. The Table 8 and Error! Reference

source not found. shows the results of both tests.

Table 8 ADF Test (Selic Over)

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.954e-06 2.177e-06 1.357 0.175

z.lag.1 -6.780e-03 5.779e-03 -1.173 0.241

Tt 1.543e-09 1.806e-09 0.854 0.393

z.diff.lag -1.379e-02 4.170e-02 -0.331 0.741

Table 9 KPSS Test (Selic Over)

test-statistic significance level 5%

KPSS 0.3559 0.146

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

555

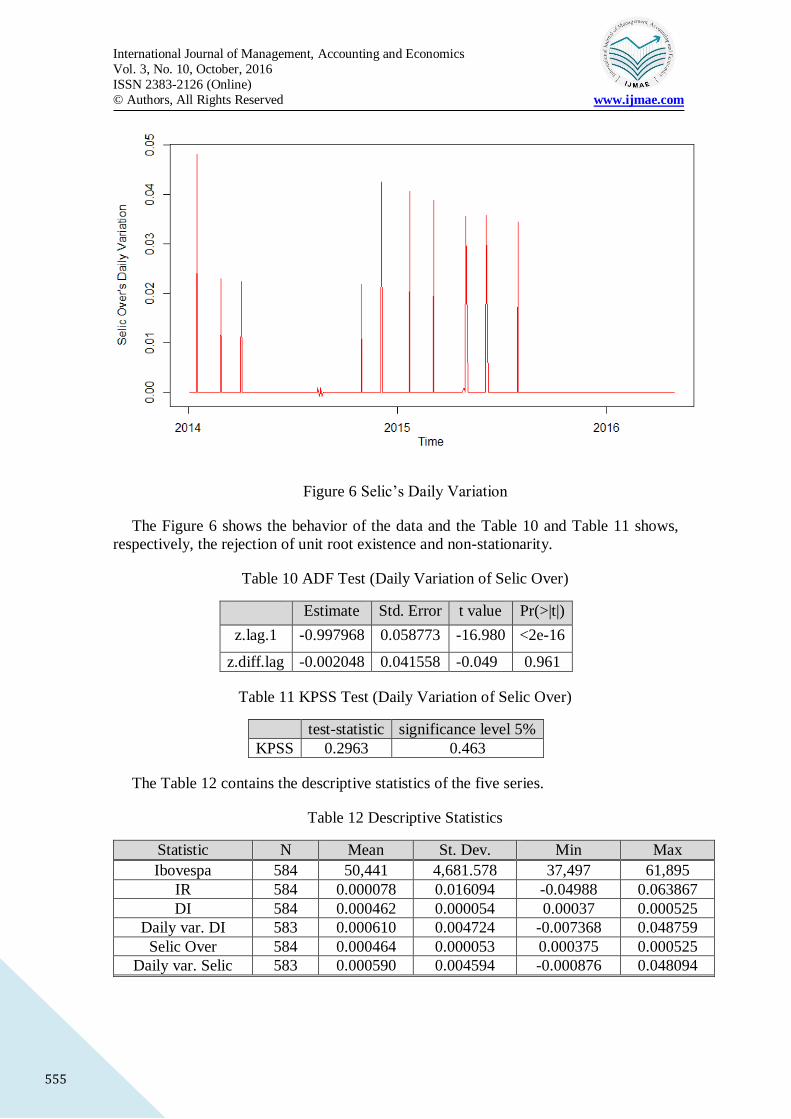

Along with the DI, we solved the Selic unit root using the daily variation of the series.

Figure 6 Selic’s Daily Variation

The Figure 6 shows the behavior of the data and the Table 10 and Table 11 shows,

respectively, the rejection of unit root existence and non-stationarity.

Table 10 ADF Test (Daily Variation of Selic Over)

Estimate Std. Error t value Pr(>|t|)

z.lag.1 -0.997968 0.058773 -16.980 <2e-16

z.diff.lag -0.002048 0.041558 -0.049 0.961

Table 11 KPSS Test (Daily Variation of Selic Over)

test-statistic significance level 5%

KPSS 0.2963 0.463

The Table 12 contains the descriptive statistics of the five series.

Table 12 Descriptive Statistics

Statistic N Mean St. Dev. Min Max

Ibovespa 584 50,441 4,681.578 37,497 61,895

IR 584 0.000078 0.016094 -0.04988 0.063867

DI 584 0.000462 0.000054 0.00037 0.000525

Daily var. DI 583 0.000610 0.004724 -0.007368 0.048759

Selic Over 584 0.000464 0.000053 0.000375 0.000525

Daily var. Selic 583 0.000590 0.004594 -0.000876 0.048094

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

556

Methods

The study, mainly, is divided in two parts: Filtering the normal and abnormal volatility

with GARCH (Bollerslev, 1986) considering everything above (under) the mean plus

(minus) two standard deviations of the Conditional Standard Deviation (CSD) series

obtained to each series as abnormal volatility. The second part is to look for political

events on the days where abnormal volatility was found.

For the parametric analysis, the authors defined abnormal volatility in the Equation (3)

and Equation (4).

𝐴𝑏𝑛𝑜𝑟𝑚𝑎𝑙𝑉𝑜𝑙𝑎𝑡𝑖𝑙𝑖𝑡𝑦 > 𝑚𝑒𝑎𝑛 + 2(𝑠𝑡𝑎𝑛𝑑𝑎𝑟𝑑𝑑𝑒𝑣𝑖𝑎𝑡𝑖𝑜𝑛) (3)

𝐴𝑏𝑛𝑜𝑟𝑚𝑎𝑙𝑉𝑜𝑙𝑎𝑡𝑖𝑙𝑖𝑡𝑦 < 𝑚𝑒𝑎𝑛 − 2(𝑠𝑡𝑎𝑛𝑑𝑎𝑟𝑑𝑑𝑒𝑣𝑖𝑎𝑡𝑖𝑜𝑛) (4)

A non-parametric alternative where, instead of using Equation (3) and Equation (4)

as the determinants of abnormal volatility, every point between the 5th and 95th percentile

was considered normal volatility.

Alternative 1 – Parametric

We applied GARCH on the returns of Ibovespa, the daily variation of DI and the daily

variation of Selic. The filter procedure occurs by analyzing the Conditional Standard

Deviation series extracted from GARCH.

To examine if the model is suitable, it’s necessary to analyze if the residuals behave

like white noise. The Ljung-Box test (Box & Pierce, 1970) and (Ljung & Box, 1978),

where the Null Hypothesis is that the data are independently distributed, was used. The

results of the three series are the acceptance of the Null Hypothesis, evidencing the

characteristics of white noise as showed at Table 13.

Table 13 Ljung-Box Test

Data P-value

IR Residuals from Garch 0.8099

DI’s Daily Variation Residuals from Garch 0.7304

Selic Over Residuals from Garch 0.6884

To test the normality of the residuals obtained from GARCH, we used the Shapiro-

Wilk test (Shapiro & Wilk, 1965). As showed at

Table 14, the Null Hypothesis of normality was reject in all series.

Table 14 Shapiro-Wilk Test

Data P-value

IR Residuals from Garc 0.0009223

DI’s Daily Variation Residuals from Garch < 2.2e-16

Selic Over Residuals from Garch < 2.2e-16

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

557

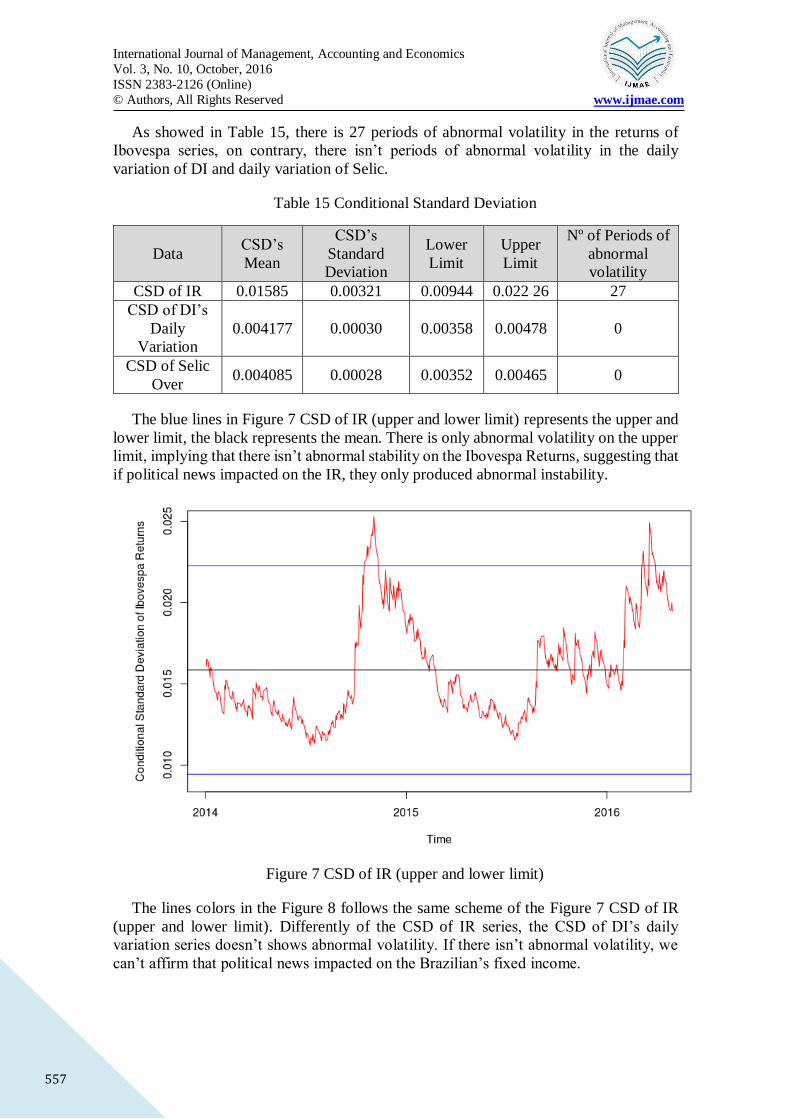

As showed in Table 15, there is 27 periods of abnormal volatility in the returns of

Ibovespa series, on contrary, there isn’t periods of abnormal volat ility in the daily

variation of DI and daily variation of Selic.

Table 15 Conditional Standard Deviation

Data CSD’s

Mean

CSD’s

Standard

Deviation

Lower

Limit

Upper

Limit

Nº of Periods of

abnormal

volatility

CSD of IR 0.01585 0.00321 0.00944 0.022 26 27

CSD of DI’s

Daily

Variation

0.004177 0.00030 0.00358 0.00478 0

CSD of Selic

Over 0.004085 0.00028 0.00352 0.00465 0

The blue lines in Figure 7 CSD of IR (upper and lower limit) represents the upper and

lower limit, the black represents the mean. There is only abnormal volatility on the upper

limit, implying that there isn’t abnormal stability on the Ibovespa Returns, suggesting that

if political news impacted on the IR, they only produced abnormal instability.

Figure 7 CSD of IR (upper and lower limit)

The lines colors in the Figure 8 follows the same scheme of the Figure 7 CSD of IR

(upper and lower limit). Differently of the CSD of IR series, the CSD of DI’s daily

variation series doesn’t shows abnormal volatility. If there isn’t abnormal volatility, we

can’t affirm that political news impacted on the Brazilian’s fixed income.

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

558

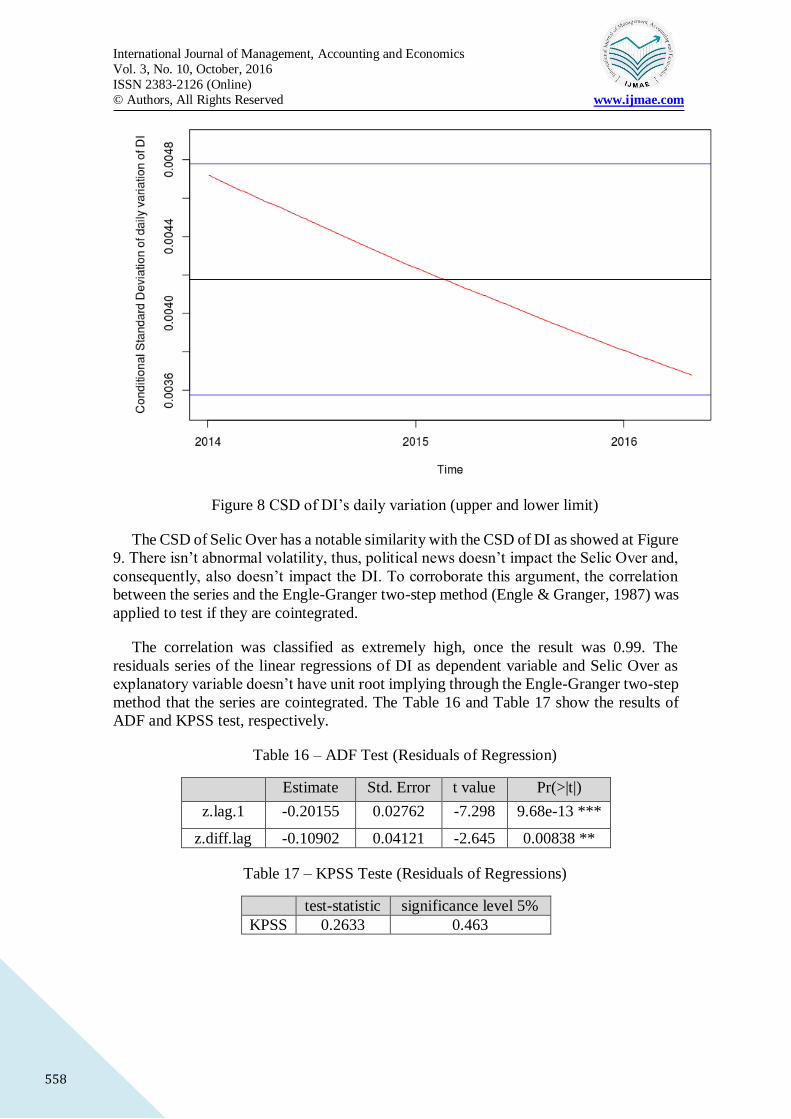

Figure 8 CSD of DI’s daily variation (upper and lower limit)

The CSD of Selic Over has a notable similarity with the CSD of DI as showed at Figure

9. There isn’t abnormal volatility, thus, political news doesn’t impact the Selic Over and,

consequently, also doesn’t impact the DI. To corroborate this argument, the correlation

between the series and the Engle-Granger two-step method (Engle & Granger, 1987) was

applied to test if they are cointegrated.

The correlation was classified as extremely high, once the result was 0.99. The

residuals series of the linear regressions of DI as dependent variable and Selic Over as

explanatory variable doesn’t have unit root implying through the Engle-Granger two-step

method that the series are cointegrated. The Table 16 and Table 17 show the results of

ADF and KPSS test, respectively.

Table 16 – ADF Test (Residuals of Regression)

Estimate Std. Error t value Pr(>|t|)

z.lag.1 -0.20155 0.02762 -7.298 9.68e-13 ***

z.diff.lag -0.10902 0.04121 -2.645 0.00838 **

Table 17 – KPSS Teste (Residuals of Regressions)

test-statistic significance level 5%

KPSS 0.2633 0.463

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

559

Figure 9 CSD of Selic’s daily variation (upper and lower limit)

Alternative 2 – Non-parametric

A non-parametric technique is to work with de critical points of the conditional

standard deviation of the series. Examining the percentiles of the series, it is possible to

points with normal and abnormal volatility. In this study, was decided to use the 5th and

the 95th percentiles of the three series to consider everything bellow the 5th percentile and

everything above the 95th percentile an abnormal volatility. The Table 18 shows the

values of the percentiles mentioned on this paragraph. The abnormal volatility of DI and

Selic happened on the same days, the Ibovespa returns have a different behavior.

Table 18 – Percentiles of Conditional Standard Deviation

Data 5% 95% Nº of periods with abnormal volatility

garch_ret_csd 0.01194074 0.02194739 60

garch_di_csd 0.003724591 0.004659724 60

garch_seli_csd 0.003662363 0.004659724 60

Differently of the Alternative 1, in this case abnormal volatility was found on the upper

and lower limits, indicating that, even though instability found previously, exists

abnormal stability on IR too. The Figure 10 shows the CSD of IR and their limits. The

black line represents the mean of the series and the blue lines represents the upper (95th

percentile) and lower (5th percentile) limits.

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

560

Figure 10 CSD of IR (5th and 9th percentile limit)

The CSD of DI’s Daily Variation, using the percentile method, returns periods of high

and low volatility. The Figure 11 shows this behavior.

Figure 11 CSD of DI’s Daily Variation (5th and 9th percentile limit)

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

561

The periods of abnormal volatility of the Selic series using the percentile method are

the same of the DI. The Figure 12 evidences this similarity.

Figure 12 CSD of Selic’s Daily Variation (5th and 9th percentile limit)

The Figure 13 shows the histogram of CSD of IR

Figure 13 Histogram of CSD of IR

The Figure 14 shows the histogram of CSD of DI’s Daily Variation

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

562

Figure 14 Histogram of CSD of DI’s Daily Variation

The Figure 15 shows the histogram of CSD of Selic’s daily variation.

Figure 15 Histogram of CSD of Selic’s Daily Variation

Results and Discussion

The results obtained using the parametric approach leaded to similar conclusions of

Smales (2015), that is, when agents don’t know who is going to win the elections, the

market volatility increases. The political events we founded were crossed with the 27

periods of abnormal volatility. As we can see in Table 19, results showed evidences the

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

563

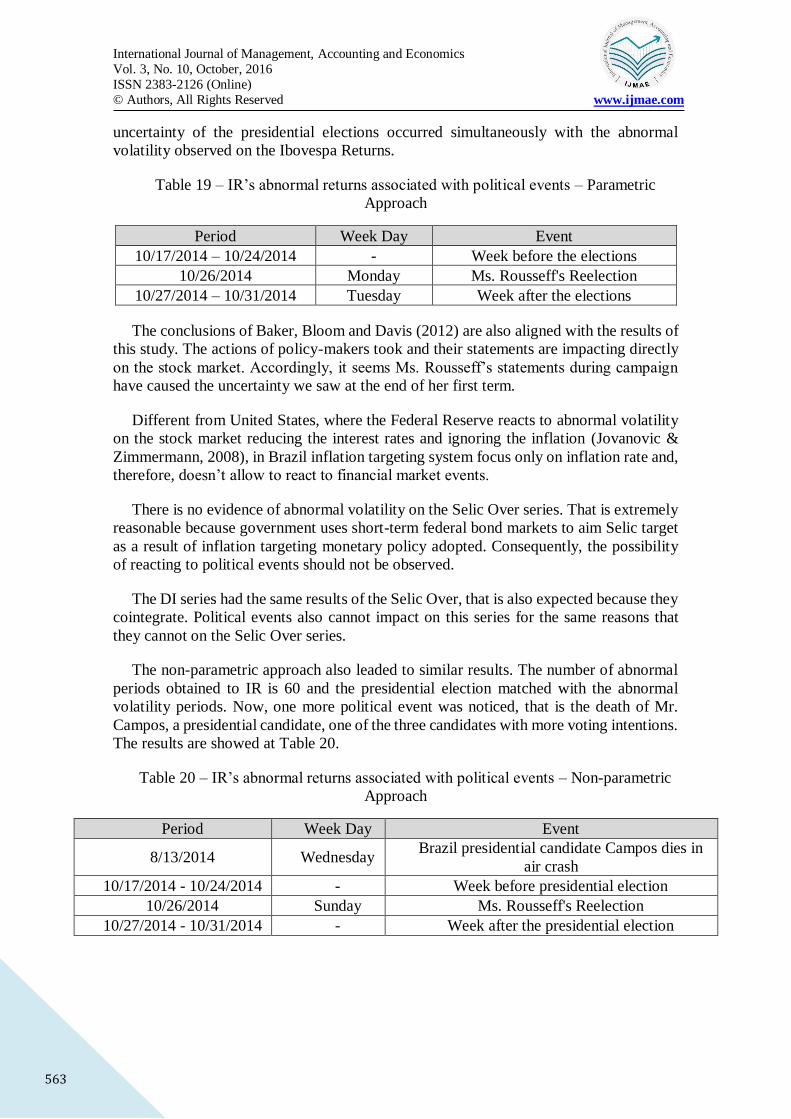

uncertainty of the presidential elections occurred simultaneously with the abnormal

volatility observed on the Ibovespa Returns.

Table 19 – IR’s abnormal returns associated with political events – Parametric

Approach

Period Week Day Event

10/17/2014 – 10/24/2014 - Week before the elections

10/26/2014 Monday Ms. Rousseff's Reelection

10/27/2014 – 10/31/2014 Tuesday Week after the elections

The conclusions of Baker, Bloom and Davis (2012) are also aligned with the results of

this study. The actions of policy-makers took and their statements are impacting directly

on the stock market. Accordingly, it seems Ms. Rousseff’s statements during campaign

have caused the uncertainty we saw at the end of her first term.

Different from United States, where the Federal Reserve reacts to abnormal volatility

on the stock market reducing the interest rates and ignoring the inflation (Jovanovic &

Zimmermann, 2008), in Brazil inflation targeting system focus only on inflation rate and,

therefore, doesn’t allow to react to financial market events.

There is no evidence of abnormal volatility on the Selic Over series. That is extremely

reasonable because government uses short-term federal bond markets to aim Selic target

as a result of inflation targeting monetary policy adopted. Consequently, the possibility

of reacting to political events should not be observed.

The DI series had the same results of the Selic Over, that is also expected because they

cointegrate. Political events also cannot impact on this series for the same reasons that

they cannot on the Selic Over series.

The non-parametric approach also leaded to similar results. The number of abnormal

periods obtained to IR is 60 and the presidential election matched with the abnormal

volatility periods. Now, one more political event was noticed, that is the death of Mr.

Campos, a presidential candidate, one of the three candidates with more voting intentions.

The results are showed at Table 20.

Table 20 – IR’s abnormal returns associated with political events – Non-parametric

Approach

Period Week Day Event

8/13/2014 Wednesday Brazil presidential candidate Campos dies in

air crash

10/17/2014 - 10/24/2014 - Week before presidential election

10/26/2014 Sunday Ms. Rousseff's Reelection

10/27/2014 - 10/31/2014 - Week after the presidential election

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

564

Since as we had already noticed Selic wasn’t managed taking into account political

events, it is expected to see the abnormal points obtained from the non-parametric

approach on the extremes of our sample doesn’t mean anything at all.

As showed at Table 19 and Table 20, the parametric and non-parametric methods,

respectively, returned periods which only can be associated with the presidential

elections, bringing conclusions that only an event with this proportion can cause abnormal

stress on the market. Events like politicians being arrested, corruptions scandals and

things like that, although it might seem important, don’t actually impact on the returns.

Therefore, our results point to the acceptance of the semi-strong efficient market

hypothesis.

Concluding Remarks

This paper has the objective of associate the political events to the financial market

through the Ibovespa Returns, the DI rate and the Selic Over Rate. Two methods are used:

the parametric, which uses Garch to extract the volatility of the series, identifying the

abnormal periods using the Equation (3) and the Equation (4). After this, the abnormal

volatility was associated with political events that happened at the same days of stress.

The non-parametric approach also used Garch to extract the volatility of the series, but

used the 5th and 95th percentile to determine what is abnormal. Everything below the 5th

and everything above the 95th was considered abnormal. After this selection, the political

events were associated with the same rational of the parametric approach.

Both approaches concluded that only the events related with the presidential elections

were relevant and could cause stress to the Ibovespa Returns. The Selic Over and DI were

not impacted with political events, that could be explained with the caution of the Central

Bank of Brazil in preserving the control of inflation.

Anyway, to be more confident about the result we presented we intend to make further

studies collecting an wider sample of political news using web scraping technique and

measuring the impact of the political news associated with abnormal volatilities through

the Event Studies approach.

References

Abdullah D. F., &. S. (2012). The Relationship between Intellectual Capital and

Corporate Performance. Social and Behavioral Sciences, 40, 537-541.

Akers, M. D., Giacomino, D. E., & Bellovary, J. L. (2014, January 14). Earnings

Management and Its Implications: Educating the Accounting Profession. The CPA

Journal.

Amat, O., Elvira, O., & Platikanova, P. (2008). Earnings Management and Audit

Adjustments: An Empirical Study of IBEX 35 Constituents. Working papers, Department

of Economics and Business, Universitat Pompeu Fabra ; 1129 .

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

565

Arslan, M. &. (2015). Intellectual Capital and Its Impact on Financial Performance: A

Study of Oil and Gas Sector of Pakistan. International Letters of Social and Humanistic

Sciences, 2(2), 125-140.

Attar, P. H., & Adibi, A. (2015). People Supervision on Sovereignty from the

Perspective of Islam and Iranian Laws. International Journal of Management, Accounting

and Economics, 2(2), 156-166.

Aziz, S., Ghani, U., & Niazi, A. (2013). Impact of Celebrity Credibility on Advertising

Effectiveness. Pakistan Journal of Commerce & Social Sciences, 7(1), 107-127.

Baker, S. R., Bloom, N., & Davis, S. J. (2012, #Feb#). Policy uncertainty: a new

indicator. CentrePiece - The Magazine for Economic Performance, Centre for Economic

Performance, LSE. Retrieved from https://ideas.repec.org/p/cep/cepcnp/362.html

Beattie, V., Brown, S., Ewers, D., John, B., Manson, S., D., T., & Turner, M. (2002).

Extraordinary Items and Income Smoothing: A Positive Accounting Approach. Journal

of Business Finance and Accounting, 21(6), 791-811.

Beneish, M. D. (1997). Detecting GAAP violation: Implications for assessing earnings

management among firms with extreme financial performance. Journal of Accounting

and Public Policy, 16(3), 271-309.

Beneish, M. D. (1999). Incentives and Penalties Related to Earnings Overstatements

that Violate GAAP. The Accounting Review(4), 425-457.

Beneish, M. D., Vargus, M. E., & Press, E. G. (2012). Insider Trading and Earnings

Management in Distressed Firms. Contemporary Accounting Research, 191-220.

Bhatt, N., Jayswal, R. M., & Patel, J. D. (2013). Impact of Celebrity Endorser's Source

Credibility on Attitude Towards Advertisements and Brands. South Asian Journal of

Management, 20(4), 74-95.

BM&FBovespa. (2016, June 12). Bovespa Index (Ibovespa). Retrieved from

BM&FBovespa: http://www.bmfbovespa.com.br/en_us/products/indices/broad-indices/

bovespa-index-ibovespa-1.htm

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity.

Journal of econometrics, 31(3), 307-327.

Bontis, N. (1998). Intellectual Capital: An Exploratory Study That Develops Measures

and Models. Management Decision, 3(1), 63-76.

Bontis, N. (2001). Assessing knowledge assets: A review of the models used to measure

intellectual capital. International Journal of Management Review, 3(1), 41-60.

Bower, A. B. (2001). Highly Attractive Models in Advertising and the Women Who

Loathe Them: The Implications of Negative Affect for Spokesperson Effectiveness.

Journal of Advertising, 30(3), 51-63.

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

566

Box, G. E., & Pierce, D. A. (1970). Distribution of residual autocorrelations in

autoregressive-integrated moving average time series models. Journal of the American

statistical Association, 65(332), 1509-1526.

Brazil. (1964, December 31). Lei 4595/1964. Law. Brazil: Diário Oficial da União.

doi:4595/1964

Brazil. (1964, Dezembro). Lei No. 4595 de 31 de Dezembro de 1964. Di\'ario Oficial

da Uni\~ao, 5425.

Brazil. (1988). Constituição da República Federativa do Brasil: 49ª edição. Edições

Câmara, 2016. Retrieved from https://books.google.com.br/books?id=jeEhCQAAQBAJ

Brazil, C. B. (2016). Dados Diários. {Dados Diários}.

Brooking, A. (1996). In Intellectual capital, core asset for the third Millennium

enterprise (p. 21). London: International Thomson Business Press.

Burroughs, J. W., & Feinberg, R. A. (1987). Using Response Latency to Assess

Spokesperson Effectiveness. Journal of Consumer Research, 14(2), 295-299.

Central Bank of Brazil. (2015). Frequently Asked Questions. Retrieved from Central

Bank of Brazil: http://www4.bcb.gov.br/pec/gci/ingl/focus/FAQ%

Central Bank of Brazil. (2016). CETIP S.A. - Mercados Organizados. Retrieved from

Central Bank of Brazil: http://www.bcb.gov.br/Pom/Spb/Ing/SecuritiesDerivatives

Foreign/CetipIngles.asp?idpai=FMISYSTEMS

Central Bank of Brazil. (2016, 06 30). Dados Diários. Retrieved from Banco Central

do Brasil: http://www.bcb.gov.br/htms/selic/selicdiarios.asp

Central Bank of Brazil. (2016, June 12). Time Series Management System - v2.1.

Retrieved from Banco Central do Brasil: https://www3.bcb.gov.br/sgspub/localizarseries/

localizarSeries.do?method=prepararTelaLocalizarSeries

CETIP. (12 de June de 2016). Estatísticas. Fonte: CETIP:

http://estatisticas.cetip.com.br/astec/series_v05/paginas/web_v05_template_informacoe

s_di.asp?str_Modulo=completo&int_Idioma=1&int_Titulo=6&int_NivelBD=2

Chang, S. L. (2007). In Valuing intellectual capital and firms’ performance: Modifying

value added intellectual coefficient in Taiwan IT industry (Ph. D. Dissertation). Ageno

School of Business, University of Golden Gate, USA. (p. 96).

Chen Goh, P. (2005). Intellectual capital performance of commercial banks in

Malaysia. Journal of Intellectual Capital, 6(3), 385-396.

Dechow, P. M., & Skinner, D. J. (2000). Earnings Management: Reconciling the

Views of Accounting Academics, Practitioners, and Regulators. Accounting Horizons,

14(2), 235-250.

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

567

Dechow, P., Sloan, R., & Sweeney, A. (1996). Causes and Consequences of Earnings

Manipulation: An Analysis of Firms Subject to Enforcement Actions by the SEC.

Contemporary Accounting Research, 13(2), 1-47.

Defond, M., & Jiambalvo, J. (1994). Debt Covenant Violation and Manipulation of

Accruals. Journal of Accounting and Economics, 17, 145-176.

Dickey, D. A., & Fuller, W. A. (1979). Distribution of the estimators for autoregressive

time series with a unit root. Journal of the American statistical association, 74(366a),

427-431.

Dong, H., Bowers, H., & Latham, W. R. (2013). Evidence on the Efficient Market

Hypothesis from 44 Global Financial Market Indexes. Working Papers, University of

Delaware, Department of Economics. Retrieved from https://ideas.repec.org/p/dlw/

wpaper/13-07..html

Edvinsson, L., & Malone, M.S. (1997). Developing a model of managing intellectual

capital. European management journal, 4(3), 356-364.

Eilifsen, A., Knivsfla IV, K. H., & Saettem, F. (1999). Earnings manipulation: cost of

capital versus tax. European Accounting Review, 8(3), 481-491.

Engle, R. F., & Granger, C. W. (1987). Co-integration and error correction:

representation, estimation, and testing. Econometrica: journal of the Econometric

Society, 251-276.

Erfgen, C., Zenker, S., & Sattler, H. (2015). The vampire effect: When do celebrity

endorsers harm brand recall? International Journal of Research in Marketing, 32(2), 155-

163. doi:10.1016/j.ijresmar.2014.12.002

Fama, E. F. (1970). Efficient capital markets: A review of theory and empirical work.

The journal of Finance, 25(2), 383-417.

Financial reports of banks. (2015). Retrieved July 27, 2015, from Comprehensive

system to inform publishers ”Codal”: http://www.codal.ir/

Financial reports of banks. (2015). Retrieved July 27, 2015, from Tehran Stock

Exchange: http://new.tse.ir/en/

Financial reports of banks. (2015). Retrieved July 27, 2015, from The Securities and

Exchange (Research, development and Islamic Studies): http://rdis.ir/CompaniesReports

.asp

Freiden, J. B. (1982). An Evaluation of Spokesperson and Vehicle Source Effects in

Advertising. Journal of Advertising Research, 5(1), 77-87.

Freiden, J. B. (1984). Advertising Spokesperson Effects: An Examination of Endorser

Type and Gender on Two Audiences. Journal of Advertising Research, 24(5), 33-41.

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

568

Friebel, G., & Guriev, S. (2005). Earnings Manipulation and Incentives in Firms.

Centre for Economic Policy Research, Discussion Paper:DP4861.

Gabriel, F. S., Ribeiro, R. B., & de Sousa Ribeiro, K. C. (2013). Hip\'oteses de mercado

eficiente: um estudo de eventos a partir da redu\cc\~ao do IPI. Revista de Gest{\~a}o,

Finan{\c{c}}as e Contabilidade, 3(1), 36.

Hair, Ringle, & Sarstedt. (2011). PLS-SEM: Indeed a Silver Bullet. Journal of

Marketing Theory and Practice, 139-151.

Hair, Sarstedt, Ringle, & Mena. (2012). An assessment of the use of partial least

squares structural equation modeling in marketing research. J. of the Acad. Mark. Sci.,

414-433.

Healy, P. M. (1985). The Effect of Bonus Schemes on Accounting Decisions. Journal

of Accounting and Economics, 7, 85-107.

Healy, P., & Wahlen, J. (1999). A Review of the Earnings Management Literature and

its Implications for Standard Setting. Accounting Horizons, 13(4), 365-383.

Henseler, J. R. (2014). A new criterion for assessing discriminant validity in variance-

based structural equation modeling. J. of the Acad. Mark. Sci., 115-135.

Hsu, P.-F. (2009). Evaluation of Advertising Spokespersons via the ANP-GRA

Selection Model. Journal of Grey System, 21(1), 35-48.

ISA, T. (2011). Impacts and Losses Caused By the Fraudulent and Manipulated

Financial Information on Economic Decisions. Review of International Comparative

Management, 12(5), 929.

Jones, J. (1991). Earning Management during Import Relief Investigation. Journal of

Accounting Research, 29, 193-228.

Jovanovic, M., & Zimmermann, T. (2008, #Nov#). Stock Market Uncertainty and

Monetary Policy Reaction Functions of the Federal Reserve Bank. Ruhr Economic

Papers, Rheinisch-Westfälisches Institut für Wirtschaftsforschung, Ruhr-Universität

Bochum, Universität Dortmund, Universität Duisburg-Essen. Retrieved from

https://ideas.repec.org/p/rwi/repape/0077.html

Kamal, M. (2014, #Mar#). Studying the Validity of the Efficient Market Hypothesis

(EMH) in the Egyptian Exchange (EGX) after the 25th of January Revolution. MPRA

Paper, University Library of Munich, Germany. Retrieved from

https://ideas.repec.org/p/pra/mprapa/54708.html

Kamins, M. A. (1989). Celebrity and Noncelebrity Advertising in a Two-Sided

Context. Journal of Advertising Research, 29(3), 34-42.

Kamins, M. A., & Gupta, K. (1994). Congruence between Spokesperson and Product

type: A Matchup Hypothesis Perspective. Psychology & Marketing, 11(6), 569-586.

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

569

Kang, M., & Goodman, R. J. (2010). Effects Of Spokesperson And Message Type On

Cosmetic Surgery Advertising Among Korean Women. American Academy of

Advertising Conference Proceedings, (p. 59).

Kellogg, I., & B., K. L. (1991). Fraud, Window Dressing, and Negligence in Financial

Statements. Commercial Law Series, McGraw-Hill.

Kramer, J., & Chen, J. (2010). Title of the Article. Journal Name, 110-313.

Kuvita, T., & Karlíček, M. (2014). The risk of vampire effect in advertisements using

celebrity endorsement. Central European Business Review, 3(3), 16-22.

Kwiatkowski, D., Phillips, P. C., Schmidt, P., & Shin, Y. (1992). Testing the null

hypothesis of stationarity against the alternative of a unit root: How sure are we that

economic time series have a unit root? Journal of econometrics, 54(1-3), 159-178.

Laakkonen, H. (2015, #Mar#). Relevance of uncertainty on the volatility and trading

volume in the US Treasury bond futures market. Research Discussion Papers, Bank of

Finland. Retrieved from https://ideas.repec.org/p/hhs/bofrdp/2015_004.html

Lev, B. (1989). On the Usefulness of earnings and Earnings Research: Lessons and

Directions from Two Decades of Empirical Research. Journal of Accounting Research,

27 Supplement, 153-201.

Ljung, G. M., & Box, G. E. (1978). On a measure of lack of fit in time series models.

Biometrika, 65(2), 297-303.

Machlup. (1962). In The production and distribution of knowledge in the United

States. Prienceton, NJ: Prienceton University (p. 436).

Marr, B. G. (2003). Why do firm measure their intellectual capital. Journal of

Intellectual Capital, 4, 441-464.

Mitchel Williams, S. (2000). Is Company’s Intellectual Capital Performance and

Intellectual Capital Disclosure Practices Related Evidence from Publicly Listed

Companies from the FTSE 1000. Working Paper (Presented at McMasters Intellectual

Capital Conference, Hamilton Ontario).

Mulford, C. W., & Comiskey, E. E. (2002). 'The Financial Numbers Game' Detecting

Creative Accounting Practices. JOHN WILEY & SONS, INC.

Nabsiah, A. W., & Methaq, A. (2011). The Effect of Attitude toward Advertisement

on Yemeni Female Consumers' Attitude toward Brand and Purchase Intention. Global

Business & Management Research, 3(1), 21-29.

Naraidoo, R., & Raputsoane, L. (2015, August). Financial markets and the response of

monetary policy to uncertainty in South Africa. Empirical Economics, 49(1), 255-278.

Retrieved from https://ideas.repec.org/a/spr/empeco/v49y2015i1p255-278.html

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

570

Narayan, P. K., Liu, R., & Westerlund, J. (2016). A GARCH model for testing market

efficiency. Journal of International Financial Markets, Institutions and Money, 41(C),

121-138. Retrieved from https://ideas.repec.org/a/eee/intfin/v41y2016icp121-138.html

Nelson, M. E. (2002). Evidence from Auditors about Managers' and Auditors' Earnings

Management Decisions. Accounting Review, 77, 175-202.

Ohanian, R. (1991). The Impact of Celebrity Spokespersons’ Perceived Image on

Consumers’ Intention to Purchase. Journal of Advertising Research, 31(1), 46-54.

Oprean, C. (2012, Decembre). Testing the financial market informational efficiency in

emerging states. Review of Applied Socio-Economic Research, 4(2), 181-190. Retrieved

from https://ideas.repec.org/a/rse/wpaper/v4y2012i2p181-190.html

Pablos, P. (2004). Measuring and reporting structural capital, journal of intellectual

capital, 5(4), 629-647.

Pai, F.-Y. (2013). Ceos and spokesperson-product fit. Review of Global Management

and Services Science, 3, 1-6.

Payne, J., & Robb., S. (1997). Earnings Management: The Effect of Ex-ante Earnings

Expectations. Working Paper, University of Oklahoma, Norman.

Petter, Straub, & Rai. (2007). Specifying Formative Constructs in Information

Systems Research . MIS Quarterly, 623-656.

Priester, J. R., & Petty, R. E. (2003). The Influence of Spokesperson Trustworthiness

on Message Elaboration, Attitude Strength, and Advertising Effectiveness. Journal of

Consumer Psychology, 13(4), 408-421.

Pulic, A. (2000). In MVA and VAICTM Analysis of Randomly Selected Companies

from FTSE 250, Graz-London: Austrian Intellectual Capital Research Center (p. 26).

Rangan, S. (1998). Earnings management and the performance of seasoned equity

offerings. Journal of Financial Economics, 50, 101-122.

Richardson, S. A., Tuna, A. I., & Wu, M. (2002). Predicting Earnings Management:

The Case of Earnings Restatements. Social Science Research Network, working paper

series, October.

Ringle, Wende, & Becker. (2014).

Rossiter, J. R., & Smidts, A. (2012). Print advertising: Celebrity presenters. Journal of

Business Research, 65(6), 874-879.

Rostami, A. (2005). In Assessment and evaluation of the relationship between

intellectual capital and intellectual capital Tehran Stock Exchange market value of

company stock, accounting investigations and audits (Vol. 39, p. 50).

International Journal of Management, Accounting and Economics

Vol. 3, No. 10, October, 2016

ISSN 2383-2126 (Online)

© Authors, All Rights Reserved www.ijmae.com

571

Schipper, K. (1989). Commentary on Earnings Management. Accounting Horizons,

91–102.

Shapiro, S. S., & Wilk, M. B. (1965). An analysis of variance test for normality

(complete samples). Biometrika, 52(3/4), 591-611.

Smales, L. A. (2015). Better the devil you know: The influence of political

incumbency on Australian financial market uncertainty. Research in International

Business and Finance, 33(C), 59-74. Retrieved from

https://ideas.repec.org/a/eee/riibaf/v33y2015icp59-74.html

Stafford, M. R., Stafford, T. F., & Day, E. (2002). A Contingency Approach: The

Effects of Spokesperson Type and Service Type on Service Advertising Perceptions.

Journal of Advertising, 31(2), 17-35.

Stephens, N., & Faranda, W. T. (1993). Using Employees as Advertising

Spokespersons. Journal of Services Marketing, 7(2), 26-46.

Stewart, T. (1997). In Intellectual Capital: The Wealth of Organizations, Currency

Doubleday, . New York.

Sweeny, A. (1994). Debt Covenant Violations and Managers' Accounting Responses.

Journal of Accounting and Economics, 17, 281-308.

Tan, H. P. (2002). Intellectual capital and financial returns of companies. Journal of

Intellectual Capital, 8(1), 251-267.

Tayles, M. a. (2001). Dealing with the Management of Intellectual Capital: The

Potential Role of Strategic Management Accounting. Accounting, Auditing &

Accountability Journal, 15(2), 251-267.

Teoh, S. H., Welch, I., & Wong, T. J. (1998). Earnings management and the

underperformance of seasoned equity offerings. Journal of Financial Economics, 50, 63-

99.

Thompson, G. W. (1992). Consumer PR Techniques in the High Tech Arena. Public

Relations Quarterly, 37(4), 21-23.

Watson, J., Taylor, A., Haffman, T., Jorge, A., Sulivan, B., Chung, D., & Mahmood,

A. (2009). Title of the Book. New York: Publisher.

Zeghal, D. &. (2010). Analyzing value added as an indicator of intellectual capital and

its consequences on company performance. Journal of Intellectual Capital, 11(1), 39-60.

Zia, A., & Shahzad, F. (2015). Role of Advertising on Sale’s Performance: a Case

Study of Bata & Service Shoes (Okara). International Journal of Management,

Accounting and Economics, 2(1), 37-45.