deloitte touche consulting . group. - kaiser...

TRANSCRIPT

;

Deloitte &Touche Consulting. Group.

March 25, 1997·

Ms. Meg KeeblerVice President Ambulatory CareHealthPartners8100 34th Avenue South

Bloomington, Minnesota

Dear Ms. Keebler:

A division of,Deloitte& Touche UP400 One Financial Plaza120 South Sixth StreetMinneapolis, Minnesota 55402 - 1WTel: (612) 397 4000Fax: (612) 3974350

The purpose of this letter is to confirm our participation in HealthPartners' Medical GroupManagement (MGM) project. This letter documents our understanding of the services you haverequested us to provide and our professional fees.

BACKGROUND

To support rapidly changing business needs, HealthPartners is embarking on an effort to enhanceits medical group management functions. While the scope is not yet .;onfirmed, this effort willinclude operational redesign and a ne\.l(information system implementation. To date,HealthPartners has completed a substantial amount of work in the early phases of this effort,

. in.eluding identifying high-level project objectives, mapping several current processes,identifying potential first sites, and selecting an information systems vendor.

Two of HealthPartners objectives in delivering this project are to deliver results quickly an~utilize internal staff as much as feasible. You would, however, like to use consulting assistancein "jump-starting" the project. These activities would include assistance with:

• Clarifying project direction, including:

• Developing a common vision

• Clarifying the project objectives and critical success factors

• Defining project scope

• Identifying criteria for evaluating project success

• Establishing the project management infrastructure, including:

• Determining project organization and staffing needs

• Defining tools & techniques to expedite the project

• Detennining issue tracking and resolution process

• Developing the workplan

• Establishing a change management program, including:

• Setting user expectations

• Developing a communication plan

DeloittB ToucheTohmatsu

International

DYOI0073

Trade Secret

-.--'-"

2

Ms. Meg KeeblerMarch 25, 1997-2-

SERVICES TO BE PROVIDED

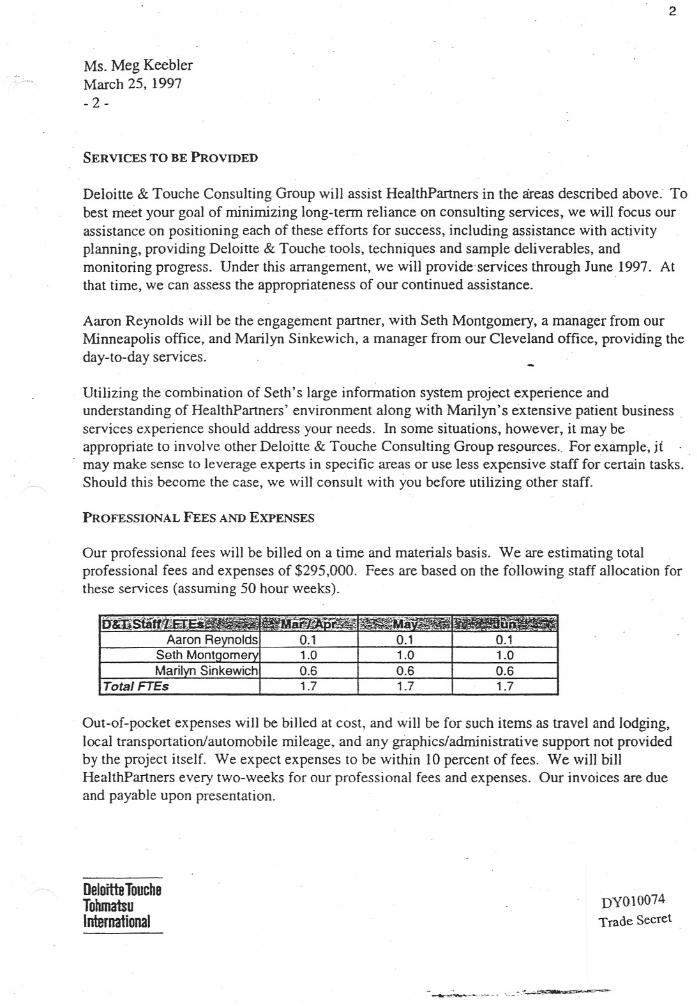

Deloitte & Touche Consulting Group will assist HealthPartners in the areas described above. Tobest meet your goal of minimizing long-term reliance on consulting services, we will focus ourassistance on positioning each of these efforts for success, including assistance with activityplanning, providing Delaitte & Touche tools, techniques and sample deliverables, andmonitoring progress. Under this arrangement, we will provide services through June1997. Atthat time, we can assess the appropriateness of our continued assistance.

Aaron Reynolds will be the engagement partner, with Seth Montgomery, a manager from ourMinneapolis office, and Marilyn Sinkewich, a manager from our Cleveland office, providing theday-to-day services.

Utilizing the combination of Seth's large information system project experience andunderstanding of HealthPartners 'environment along with Marilyn's extensive patient businessservices experience should address your needs. In some situations, however, it may beappropriate to involve other Deloitte & Touche Consulting Group respurces .. For example, jtmay make sense to leverage experts in specific areas or use less expensive staff for certain tasks.Should this become the case, we wilt consult with you before utilizing other staff.

PROFESSIONAL FEES AND EXPENSES

Our professional fees will be billed on a time and materials basis. We are estimating totalprofessional fees and expenses of $295,000. Fees are based on the following staff allocation forthese services (assuming 50 hour weeks).

·-·-~---~"'.~-·~~"Iii0.1 0.11.0 1.00.6 0.61.7 1.7

Out-of-pocket expenses will be billed at cost, and will be for such items as travel and lodging,local transportation/automobile mileage, and any graphics/administrative support not providedby the project itself. We expect expenses to be within 10 percent of fees. We will billHealthPartners every two-weeks for our professional fees and expenses. Our invoices are dueand payable upon presentation.

DeloittB Touche

Tohmatsu

International

DYOI0074

Trade Secret

3

Ms. Meg KeeblerMarch 25, 1997- 3 -

Should either HealthPartners or Deloitte & Touche Consulting Group identify appropriatechanges in scope, or other matters arise that would affect the work effort, we will inform eachother as soon as possible and discuss the impact. Changes mutually agreed to will bedocumented in a revised letter of understanding. Additionally, both HealthPartners and Deloitte& Touche Consulting Group will provide 30-days notice of any changes that could affect projectstaffing or HealthPartners' completion of the project.

* * * * *

We appreciate this opportunity to work with you and HealthPartners on this importantengagement. If you have any questions regarding this letter or any other matter, please feel freeto contact Seth Montgomery (BealthPartners x5531) or Aaron Reynolds (3974396).

Please sign and return a copy of this letter to indicate your acceptance of our mutualcommitments.

Deloitte & Touche-Consulting Group by:

Aaron L. Reynolds

Deloitta ToucheTohmafsu

International DYOI0075

Trade Secret

January 7, 1999

Mr. Kirby EricksonExecutive Vice President Administration and Hea1thplanHealthPartners8100 34th Avenue South

Bloomington, MN 55425

Dear Mr. Erickson:

The purpose of this letter is to confirm our understanding ofDeloitte Consulting continuedparticipation and commitment to support HealthPartners'.Medical Group Management.(MGM)

. project through assistance with HealthPartners Medical Group (HPMG) Patient Accountingintegration efforts. This letter documents our understanding of the services we were asked toprovide and our related professional fees for the period of January 1, -1-999through March 31, 1999.

SERVICES TO BE PROVIDED

Utilizing our firm's experience with the MGM project, Region's patient accounting department, andpatient accounting integration efforts in general, Deloine Consulting will support HPMG PatientAccounting integration efforts by providing assistance in two key areas:

• Department Staff Integration Planning. We will assist with the department integrationthrough the development of a detailed staffing plan for the integration of the Regions andHealthPartners professional services patient accounting departments. Activities and deliverablesinClude identification oftransitioning staff, assessment of department skill sets, gap analysisbased on budgeted resource requirements, development of resource hiring plan, anddevelopment of a staff transition plan based on Resolute deployment on the Regions campus .

• Integrated Business Operational Preparation. We will assist in preparations for department

integration by performing an assessment to identify ~as for operational design to support thecombined RegionsIHP professional patient account management: Activities include

.documenting Regions and HP operational processes to identify gaps between existing andneeded processes to support HPMG account management.

In addition, Amy will provide Continued Resolute Implementation Evaluation, Analysis andSupport for Patient Accounting. She will assist with patient accounting's Resolute implementationthrough continued: evaluation of system functionality and usage. Areas to be evaluated include cashapplications, billing follow-up and collections. We will also continue to provide issue analysis andresolution support as they relate to Regions activities.

P 009332

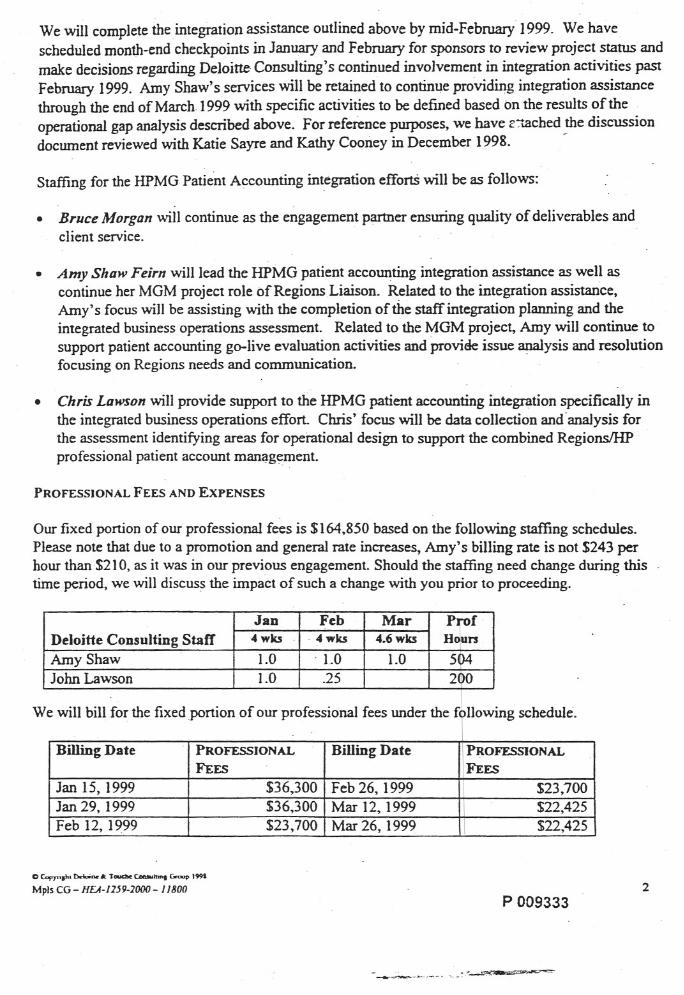

We will complete the integration assistance outlined above by mid-February 1999. We havescheduled month-end checkpoints in January and February for sponsors to review project starus andmake decisions regarding Deloitte Consulting's continued involvement in integration activities pastFebruary 1999. Amy Shaw'sservices will be retained to continue providing integration assistancethrough the end of March 1999 with specific activities to be defined based on the results of theoperational gap analysis described above. For reference purposes, we have r~ched the discussiondocument reviewed with Katie Sayre and Kathy COmley in December 1998. ~

Staffing for the HPMG Patient Accounting integration effortS will be as follows:

• Bruce Morgan will continue as the engagement partner ensuring quality of deliverables andclient service.

• Amy Shaw Feirn will lead the HPMO patient accounting integration assistance as well ascontinue her MOM project role of Regions Liaison. Related to the integration assistance,Amy's focus will be assisting with the completion of the staff integration planning and theintegrated business operations assessment. Related to the MOM project, Amy will continue tosupport patient accounting go-live evaluation activities and provide issue analysis and resolutionfocusing on Regions needs and communication.

• Chris Lawson will provide support to the HPMG patient accounting integration specifically inthe integrated business operations effort. Chris' focus will be data collection and "analysis forthe assessment identifying areas for operational design to support the combined RegionsIHP "professional patient account man<lg~ment.

PROFESSIONAL FEES AND EXPENSES

Our fixed portion of our professional fees is $164,850 based on the following staffing schedules.Please note that due to a promotion and general rate increases, Amy's billing rate is not $243 perhour than $210, as it was in our previous engagement. Should the staffing need change during thistime period, we will discuss the impact of such a change with you prior to proceeding.

JaDFebMarPrfDeJoitte ConsuJtiDg Staff

4wks" 4wks4.6 wksH~ursAmy Shaw

1.0" 1.01.0504John Lawson

1.0.25 200

We will bill for the fixed f fi Ifi hedul ""££ ...,

BilliDg Date

PROFESSIONALBilling Date\PROFESSIONALFEES

FEES

Jan 15,1999$36,300Feb 26,1999I$23,700

Jan 29,1999$36,300Mar 12, 1999I$22,425

Feb 12, 1999$23,700Mar 26, 1999I

$22,425

c c..pyn••••r>.Ionw ok ToudM: c- ••••••~ ._

Mpls CG - HEA-J 159-1()()() - J 1800P 009333

2

TOTAL I $164.850 I

As with our previous arrangement, the services of Bruce Morgan will be billed based on actual time

spent on the project. We estimate the professional fees for his services, based on an average of 8hours per week, will be $29,232. We will billJor their services based on actual time spent

Therefore, the total estimated professional fees are estimated to be $164,850 + $29,232. In additionto professional fees, actual out of pocket expenses wi1I be billed at cost Out of pocket expensesinclude travel, lodging, meals, transportation, graphics support, etc.

Should either HealthPartners or Deloitte Consulting identify appropriate changes in scope, or othermatters arise that would affect the work effort, we will inform each other as soon as possible and

discuss the impact before proceeding. If this letter does not accurately reflect your understanding,please advise us immediately.

STANDARD BUSINESS PRACTICES

Our General Business Terms for consulting engagements are attached as Exhibit A and areincorporated into this letter by this reference .

• • • • •

We appreciate the opportunity to continue to work with you and HealthPartnerson this importantengagement. If yc:>uhave any questio~ regarding this letter or any other matter, please contactBruce Morgan at 397-4401.

Deloitte Consulting by:

ACKNOWLEDGED AND ACCEPTED BY HEALTHP ARTNERS:

Date

Kirby Erickson, Executive Vice President Administration and Healthplan

o COfryriaht Ddoiao • T cUch<C""""""w Gn..p I_

MplsCG-HEA-/159-1000- //800P 009334

3

May 10, 1999

Ms. Katie Sayre

HealthPartners

81QO 34th Avenue SouthBloomington, MN 55425

Dear Ms. Sayre

The purpose ofthis letter is to confirm our understanding of Deloitte Consulting's continuedparticipation and committnent to support HealthPartners' Medical Group Management (MOM)

project and HealthPartners Medical Group (HPMO) Patient Accounting;ntegration efforts. Thisletter documents our understanding of the services we have been asked to provide and our relatedprofessional fees for the period of May 17, 1999 Llu-oughJuly 3D, 1999, based on discussioils duringour meeting on May 6, 1999.

SERVICES TO BE PROVIDED

Utilizing our firm's experience and knowledge with the MOM project, Regions Hospital patientaccounting department, and patient accounting integration efforts in general, Deloine Consultingwill support HPMG Patient Accounting integration efforts by providing assistance in the followingareas:

• Assistance related to Phase I, Stage IV of the MGM project. Continue in role ofMGMbusiness team leader through May 31, 1999 assisting with issue management regardingResolute Stage IV go-live. Assist as MGM technical advisor on Stage IV issues through golive .

• Assistance related to patient accounting operations. Continue to assist in preparing fordepartrrient integration by performing operational design necessary to support the combinedRegionsIHP professional patient account management as discussed with you and MorrieAnderson on May 6, 1999 (see attached matrix). Assistance will be solidified through furtherdiscussions with departtnent management and supervisors.

We will complete the assistance outlined above by July 3D, 1999 and will continue to schedulemonth-end checkpoints for sponsors and patient accounting leadership to review project status.Staffing for the outlined effort will be as follows:

P 009559

• Bruce Morgan will continue as the engagement pannerensuring quality of deliverables.appropriate resource allocation and overall client service.

• Amy Feirn will manage the effort on a part-time-basis splitting her time between MOM projectissues and patient accounting operational issues.

• A consultant/analyst, managed by Amy Feim and Bruce Morgan, will conduct data collectionand analysis for the assistance related to patient accounting operations.

PROFESSIONALFEESANDEXPENSES

The fixed portion of our professional fees for the period May 17, 1999 through July 30, 1999 is$140,360 based on the following staffing schedule, assuming one FTE works 45 hours per week.The need for continued assistance from Ddoine Consulting's analyst resource for the month of Julywill be assessed and decided by the project sponsors at the end of June.

DELOITIE CONSULTING MAYJUNEJULYPROF

REsOURCES2WKS5WKS4WKSHOURS

Amy Feim

0.40.40.4198

Consultant/analyst

1.01.01.0495Total

1.41.4104693

We will bill for the fixed portion of ourprofessional fees under the following schedule.

SERVICEDATES PROFESSIONALFEES

May 17, 1999 - May 29, 1999$25,520

May 30, 1999 - June 12, 1999$25,520

June 13, 1999 - June 26, 1999$25,520

June 27, 1999 - July 10, 1999$25,520

July 11, 1999 - July 24, 1999$25.520

July 25, 1999 - July 30, 1999-$12,760

As with our previous arrangements, the services of Bruce Morgan will be billed based on actualtime spent on the project. We estimate the professional fees for his services will be minimal andaverage no more than 2 hours per week.

In addition to professional fees, actual out of pocket expenses will be billed at cost. Out of pocketexpenses include travel, lodging, meals, transportation, graphics support, etc.

Should either HealthPartners or Deloitte Consulting identify appropriate changes in scope, or othermatters arise that would affect the work effort, we will inform each other as soon as possible anddiscuss the impact before proceeding. If this letter does not accurately reflect your understanding,please advise us immediately.

() Copyri8l>1Ddoi~ I< 1_ C~lb.8 Group1

Mpls CG HeQ/lhP~rs·/18J7

P 009560

2

STANDARD BUSINESS PRACTICES

Our General Business Terms for consulting engagements are attached as Exhibit A and areincorporated into this letter by this reference.

We appreciate the opportunity to continue to work with you and HealthPartners on this important

engagement. lfyou have any questions regarding this letter or any other matter. please contactBruce Morgan at 397-4401.

Deloitte Consulting by:

Bruce A. Morgan

ACKNOWLEDGED AND ACCEPTED BY HEALTHP ARTNERS:

Date

Katie Sayre. _

o Copyrisfn Ddoi ••••. Tou<M c ••••••lti.s Group 1991

Mpls CG HeQllhPQnne~-12847

P 009561

3

Deloitte &

Touche8-CONFIDENTIAL

. Decemba 6, 1999

Delottte & Touche UPHuman Capital Advisory Servi:es400 One FtnanciaI Plaza120 South Sixth Street

:Mi'lneapoIis. Mimes0t8 554(U- 1B44

Telephone: (612) 3974000Facsimile: (612) 3974450www.us.deIoine.com

Mr. Kirby J. EricksonExecutive Vice President, Administration and HealthHealthPartners.8100 34m Avenue SouthP.O. Box 1309

Minneapolis, MN 55440-1309

Re: Kq Employa Shar~ OptionProgram DI (KEYSOP"")

Dear Kirby:

Thank you for your interest in·o~ KEYSOP idea. 1bis letter describes our se:rvices in assistingHealthPartners in the design and implementation of the Key Employee Share Option Program nt(the KEYSOP), a program devc:loped by Deloine & Touche UP. It sets forth a summary of theKEYSOP, our proposed services, and the project's timing and fees.

THEKEYSOP

Under the KEYSOP, Hea1thPartnerswill allow certain executives and physicians to exchangecompensation for discounted options granted in mumal funds. As we discussed, the mutual fundon which the option is granted is likely to be immediately purchased by Hea1tbPartners and heldin a "rabbi" trust. The appreciation between the exercise price and the fair market value "at dateof exercise is taxed when the executive or physician actually cxc:rcisesthe option.

The KEYSOP will be subject Ul' the roles imposed under Section 83 of the Internal RevenueCode of 1986, as amended. Deloine & Touche's research and position is that a properlydesigned program should be treated as a nonstatutory stock option plan-it should, not be

considered a deferred compensation plan even if the options are granted in excl1:mge for areduction in salmy or deferral of a bonus. As part of our engagement, Deloine & Touche willissue a tax opinion letter in support of this program ..

Deloit1e Twche

Tollnatsu p 009592

Mr. Kirby 1. EricksonDecembe:r 6, 1999

Page2

,SERVICES

Our recommended approaCh in implementing the KEYSOP includes the following phases.

Phase 1:Scope Review

Impact on HumimResource (HR) Strcitegies

Phase 2:PUm and Trust Designand Exercise PriuMethodology

Phase3:Sample DocumentDrafting .-

During our ~ meeting, we will ensure a complete and accurateunderstanding of the scope of the engagement and theresponsibilities of all parties involved in the implementation. Wewill establish a timetable for project completion enabling us tpidentify and mmU'lgethe timely completion of all necessary tasks..This will include manng ammgements to obtain the'necessarybackground information, individual data for executives andphysicians to be included in the program, and any.other relevantinformation that will assist us in the development of yourKEYSOP.

We Win also meet with app.l opriate members of management toreview current HR strategies and existing comperisation plans. Wewill be determinine the impact the KEYSOP would have on .HealthPartners' human resource. strategy. Any resultant directionfrom management in this regard will be taken into account as weproceed with subsequent phases of the project.

We will assist you in e}mminine choices in plan design andfunding,. and outline the advantages and disadvantages of varioustypes of plan provisions and funding a1tematives. 1bis includes adetermination of the methodology for the establishment of theexercise price (i.e., the discounting offair market Value at date ofgrant or date of exercise).

During this phase, we will dra:ft, for review by you and your legalcounsel, the sample documents necr"5~ry to implement andadminister the KEYSOP. These sample documents include theplan and trust documenis, agreement form, beneficiary and

. assignment forms, executive snmmaries of plan provisions, mid

Board resolutions; however, they will not include SEe <fu:710sure_documents. We will assist in the language for documents relatingto the forfeiture of existing deferred compensation arrangementsand the use of salary reduction agreements as appropriate .. -

123436P 009593

DeIiritte &

Touche

I..

Mr. Kirby J. EricksonDecember 6, 1999

Page 3

Sample DocumentDraftlng (continued)

Phase 4:

Tax Opinion, AccountingOpinion, and Tax andFinancial Reporting

Phase 5:

Participant GroupMutings

The provisions included in these sample doc;uments will reflect ourknowledge and expertise in plan design, extensive analysis of thecase law, experience with similar clic:nts,Practical application ofadministrative practices 3n4 adherence to previously mentionedlegal requireIDents. However. within that framework we willincorporate plan features that arc intended to meet your objectivesdiscussed in Phase 1.

After reviow by you and your legal co~ we will meet with youto obtain your input and discuss any comments and modifications

prior to fina1i7ing the sampleKEYSO~ documents.

Based upon the contromng authorities examined, Deloitte &Touche will ~ a tax opinion in support of this arrangement

.We will also provide a report on the appropriate application ofgenCralIy accepted accounting principles to the ICEYSOPtrnnsactions in accordance with the Statement on AuditingStandards 50 {"SAS 50") established by the American Institute ofCertified Public Accountants;

One of the most imponant aspects to consider in implementing theKEYSOP is how wen it is'communicated to, and understood by.eligible physicians and executives. This understanding isnecessary not only when an eligible participant decides whether toparticipate in the plan, but also on an ongoing basis forTTl~1rinJtimportant decisions regarding the exercise of options.

We will prepare a program summary and meet with the participantgroup to explain the program and answer questions. Our proposalanticipates up to four meetings with potential particiPants.

123436

P 009594

Deloitle &Touche

~

Mr. Kirby J. EricksonDecember 6,1999

Page 4

PROJEcrFEES

Our fee for the above-described Core Services' in Phases 1 through 5 is estimAt~ to be S95,OOO

to SI05,OOOO. In addition, reasonable expenses for out-of-pocket costs will be billed according ,to our standard office policy. One-third o{the fee will be billed at project commencement andthe balance periodically throughout the project This project is subject to the attached businesstenns and conditions.

PROJEcr TIMING

Weare begjrmine to work on the project immediately in order to meet your timing needs.Assnmine that the necessary meetings can be cOnducted on a timely basis,meetings with planparticipants to describe the program could take place in Febmary, 2000.

OPTIONAL SERVICES

In addition to the comprehensive service package descn1>edabove, we can also provideindependent services relating to the selection and monitoring of investment mid admini~veservices. Fees for these or other additional services will be separately esrimRt~.dand billed.

Ilfl'estment Policy,AssaManag~men1, andAdministrativ~ Services

.ro'

We can also assist you in the development of an investment policyfor the KEYSOP offering, inc1udUigthe number offtmds;md therisk reward characteriStics of each,ftmd within an appropriate anayof funds. We would expect to focus on no-load mutual funds asthe primary source of asset management Within that context, wewould identify, evaluate, and assist you in the selection of fundalternatives. We would also lead a procesS to identify and selectan arlministrative service provider and a trustee. Our fee for thisoptional service is esrim~tffl to be S15,000 to $20,000.

123436 P 009595Deloitb! &

TooGb!

Mr. Kirby J. EricksonDecembcr6, 1999

Page 5

We appreciate the opportunity to present our serviCes and look forward to wolking with YOlL If. you have any questions or comments regarding any. of the temlS of this letter, please contact Dick

Berens at (612) 397-4028 or Tom Mayer at (612) 397-4145.

Sincerely,

DELOITTE & TOUCHE 1.LP

Enclosure

If the terms of this letter are acceptable, please send a faxed copy to (612) 69~-7~ 19 or return asigned copy of it by mail to DELOITTE & TOUCHE UP•.

Approved for HeaJthPartnen

By:

Title:

Date:

cc: JeffRadunz

. Tom Mayer

l23436. P 009596

DeJliitte &

Touche

January 19, 1998

Mr. David Dziuk, Controll~//HealthPartners .8100 34th Avenue SouthPO Box 1309

11ll1neapolis,~ 55440-1309

Dear Dave:

This letter is to confirm and specify the terms of our income tax compliance engagement withHealthPartners for certain taxable entities for the year ended December 31, 1997 and to clarifythe nature and extent of the services we will provide.

We will review the following 1997 federal and Minnesota income tax returns:

HealthPartners Administrators. Inc.

Consolidated Federal Income Tax Return (including MedCenters Managed Care, Inc. andMidwest Assurance COIDJpany)

Minnesota Franchise Tax Return

MedCenters Managed Care. Inc.

Minnesota Franchise Tax Return

Midwest Assurance CompanyI

Minnesota Insurance Franchise Tax Return

HealthPartners Ventures

Federal Income Tax ReturnMinnesota Franchise Tax Return

Deloitte & Touche LLP professionals of 'lOurMinneapolis office will work closely with you andyour staff in the review of these returns. We anticipate that your client service team will includeTom Mayer, Partner at 397-4145; Brian Falk, Director at 397-4016; and Beth Blumhoefer,

Senior at 397-4268. They will use othe~ members of the staff, as required, to perform the abovedescribed services.

P 009107

r

We will make no audit or other verification of the tax data you provide us, although we may need to ask you for clarification of some of the information. Our work in connection with the reviewof your tax returns does not include any procedures designed to discover errors or otherirregularities in the information underlying the returns prepared by you, should any exist.

We expect to deliver the returns on or about March 12, 1998. In oruer to meet this deadline, we

expect to receive the pro forma tax returns and workpapers for the entities by February 20, 1998.lbis deadline should provide sufficient time for us to review your workpapers and makedeterminations regarding additional information we require in order to complete the review of your tax returns. We appreciate the assistance of your staff in providing the information werequest.

You have engaged us to provide a review of income tax returns prepared by you. The scope ofour review is limited by you as to the_time we can expend and, therefore, the review steps we caD.perform are limited.

We cannot warrant to you that our review steps will enable us to id£ntify every potentialissue, election, filing, or notice requirement in your returns.

-By executing and returning this letter, you are representing to us that all information which youfurnish us for the purpose of the income tax return review will be true, complete and accurate,

and, in addition, you retained all necessary written support and documentation for thatinformation should it be required by an IRS or state examination at a later date.

We understand that you will prepare and file all estimated tax payments necessary to avoid anyunderpayment of estimated tax payment penalties. We would be pleased to assist you inreviewing your estimated tax calculations, at your request, at our standard hourly rates.

Your returns may be selected for review by the taxing authorities. Any proposed adjustments bythe examining agent are subject to certain rights of appeal. In the event of such tax examination,we will be available to represent you and will render an additional fee statement for the time andexpenSes incurred.

The tax law provides for a penalty to be imposed where a taxpayer makes a substantialunderstatement of tax liability. If you would like information on the amount or circumstances ofthis penalty, please let us know.

Management is responsible for the proper recording of transactions in the books of accounts, forthe safeguarding of assets, and for the substantial accuracy of the financial records. You have thefinal responsibility for the income tax returns and, therefore; should review them carefully b",foreyou sign and file them.

We anticipate that our fee for these services will be $12,250, including out-of-pocket expenses.Fee statements will be submitted on the following time schedule and are payable uponpresentation:

P 009708

-.~.

February 15, 1998March 15, 1998

$ 6,250$ 6,000

In the course of reviewing your tax returns, we may identify issues not contemplated at the timewe began our services that must be resolved in order to allow us to complete our review of yourtax returns. In cases where fees beyond our initial estimate may be required, we will discusssuch circumstances with you in advance whenever possible. Our fee estimates also assume thatthe information we are to review will be submitted in an organized, systematic, way. If not sosubmitted, additional time and fees may be required.

The maximum liability "ofDeloitte & Touche LLP and its personnel ("D&T') relating to servicesrendered under this letter (regardless of form or claim whether in contract, statute or tortincluding without limitation, negligence or otherwise) shall be limited to the fees paid to D&Tfor the portion ofD&T's services or work giving rise to the "liability. In no event shall D&T beliable for lost profits or for any consequential; special, incidental, indirect, or punitive damages.

Any controversy or claim arising out of or relating to this Jetter or the breach thereof shall besubmitted :first to voluntary mediation, and if mediation is not successful !Vithinninety days afterthe beginning of the mediation process, then to binding arbitration. If in arbitration, the arbitratormay not award non-monetary damages nor equitable relief. The arbitrator shall have no power toaward punitive damages nor any other damages not measured by the prevailing party's actualdamages. The mediator will be selected by agreement of the parties. Ifnecessary, an arbitrationshall be conducted before a panel of three arbitrators to be selected as provided in the AAA rules.Each party will bear its own costs in the mediation. The fees and expenses of the mediator willbe shared equally by the parties. Costs of arbitration shall be shared equally by the parties,subject to final apportionment by the arbitrators.

This agreement and all issues arising under or relating to this agreement shall be interpreted, /1governed and construed"in accordance with the laws of the State of New York (without givingeffect to its choice of laws principles).

Our policy is to dispose of our copies of tax returns and workpapers, and other tax information,that is more than six years old. Accordingly, we will dispose of such information in our filespertaining to you without further notice, provided that we do not hear from you to the contrary.Your responsibility for retention of your own tax records varies, depending upon the type ofreturn or other information involved. We suggest that you maintain indefinitely copies of taxreturns, workpapers, and tax records to support y()ur cost or basis in your assets, contributionsthat you may make, and other tax needs.

If the foregoing fairly sets forth your understanding, please sign the enclosed copy of this letter atthe space inqicated and return it to our office in the enclosed envelope.

P 009709

We want to express our appreciation for this opportunity to work with-you. Please call me at(612)-397-4016 if you have any questions regarding this engagement. _

Very truly yours,

Brian~alkTax Director

Enclosure

APPROVED:

By:

Date:

90485/kh

P 009710