planning strategies in wake of the new 3.8% medicare “surtax” presented by: robert s. keebler,...

TRANSCRIPT

Planning Strategies in Wake of the New 3.8% Medicare “Surtax”

Presented by:

Robert S. Keebler, CPA, MST, AEP (Distinguished)Keebler & Associates, LLP

420 South Washington StreetGreen Bay, WI 54301

Circular 230 Disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication, including attachments, was not written to be used and cannot be used for the purpose of (i) avoiding tax-related penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any tax-related matters addressed herein. If you would like a written opinion upon which you can rely for the purpose of avoiding penalties, please contact us.

Personal Financial Planning Section2

• Beginning with the 2013 tax year, a new 3.8% Medicare “surtax” will apply to all taxpayers whose income exceeds a certain “threshold amount”. This new “surtax” will, in essence, raise the marginal income tax rate for affected taxpayers.

• Thus, a taxpayer in the 39.6% tax bracket (i.e. the highest marginal income tax rate in 2013) would have a marginal rate of 43.4%!

3.8% Medicare “Surtax” Overview

Personal Financial Planning Section3

Current Tax Rate

Tax Rate in 2013+

Tax Rate in 2013+

(w/surtax)10% 15% 15%15% 15% 15%25% 28% 28%28% 31% 34.8%33% 36% 39.8%35% 39.6% 43.4%

NOTE: The chart above assumes that the 3.8% Medicare surtax would not begin to apply until a person’s taxable income reaches the 31% tax bracket (based on certain net investment income and itemized deduction assumptions). However, there are times when the 3.8% could apply to a person in a lower tax bracket (i.e. 15%, 28%) or may not apply to a person in higher tax brackets (31%, 36%, 39.6%).

3.8% Medicare “Surtax” Overview

Personal Financial Planning Section4

APPLICATION TO INDIVIDUALS – The new Medicare surtax is equal to 3.8% times the lesser of the following:

1. “Net investment income”, OR

2. The excess (if any) of –

a. “Modified adjusted gross income” (“MAGI”) for such taxable year, over the

b. “Threshold amount”

3.8% Medicare “Surtax” Overview

Personal Financial Planning Section5

APPLICATION TO ESTATES AND TRUSTS – The new Medicare surtax is equal to 3.8% times the lesser of the following:

1. Undistributed “net investment income” for such taxable year, or

2. The excess (if any) of –

a. “Adjusted gross income” (as defined in section 67(e) for such taxable year, over the

b. Dollar amount at which the highest tax bracket in section 1(e) begins for such taxable year

3.8% Medicare “Surtax” Overview

Personal Financial Planning Section6

Three critical terms associated with the 3.8% Medicare surtax:

• “Net investment income”• “Threshold amount”• “Modified adjusted gross income” (“MAGI”)

3.8% Medicare “Surtax” Overview

Personal Financial Planning Section7

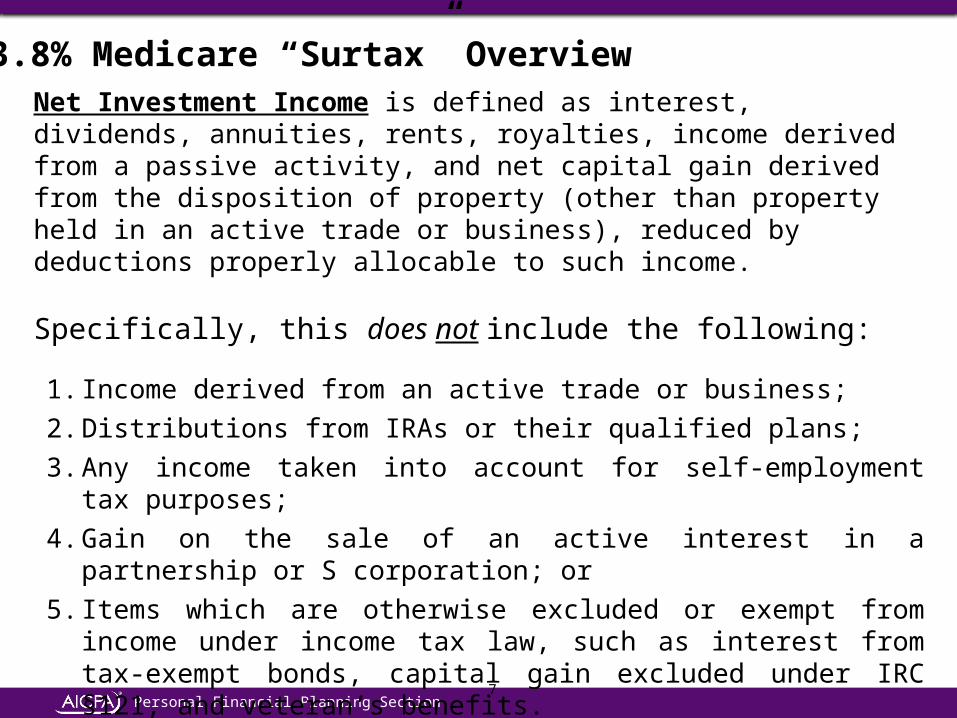

Net Investment Income is defined as interest, dividends, annuities, rents, royalties, income derived from a passive activity, and net capital gain derived from the disposition of property (other than property held in an active trade or business), reduced by deductions properly allocable to such income.

Specifically, this does not include the following:

1. Income derived from an active trade or business;

2. Distributions from IRAs or their qualified plans;

3. Any income taken into account for self-employment tax purposes;

4. Gain on the sale of an active interest in a partnership or S corporation; or

5. Items which are otherwise excluded or exempt from income under income tax law, such as interest from tax-exempt bonds, capital gain excluded under IRC §121, and veteran’s benefits.

3.8% Medicare “Surtax” Overview

Personal Financial Planning Section8

Subject to Surtax Exempt from Surtax

Wages X

Taxable Interest X

Exempt Interest X

Dividends X

Annuity Income X

Passive Royalty X

Active Royalty X

Rents X

3.8% Medicare “Surtax” OverviewTypes of Income Subject to Surtax

Personal Financial Planning Section9

“Threshold amount”: is the key factor in determining the “lesser of” formula for purposes of calculating the surtax.

Threshold amounts

• Single taxpayers - $200,000

• Married taxpayers - $250,000

• Estates/trusts - $11,650 (i.e. top income tax bracket in 2012)

3.8% Medicare “Surtax” Overview

Personal Financial Planning Section10

“Modified adjusted gross income” (“MAGI”): is the amount that is compared to the “threshold amount” to determine the “net investment income” that is subject to the surtax.

MAGI equals:

• Adjusted gross income (i.e., Form 1040, Line 37) PLUS

• Net foreign earned income exclusion (i.e., gross income excluded under the foreign earned income exclusion less certain deductions or exclusions that were disallowed due to the foreign earned income exclusion)

3.8% Medicare “Surtax” Overview

Personal Financial Planning Section11

Example 1: John, a single taxpayer, has $100,000 of salary and $50,000 of net investment income for MAGI of $150,000. The 3.8% surtax would not apply because his MAGI is less than $200,000.

Example 2: Linda, a single taxpayer, has $225,000 of net investment income and no other source of income. The 3.8% surtax would apply to $25,000 of income (the lesser of investment income of $225,000 or the excess of $225,000 MAGI over $200,000 “threshold amount”).

Example 3: Terry & Tina, married filing jointly, have $300,000 of salaries and no net investment income. The tax 3.8% surtax will not apply because they have no investment income.

3.8% Medicare “Surtax” Overview

Personal Financial Planning Section12

Example 4: Peter & Paula, married filing jointly, have $400,000 of salaries and $50,000 of net investment income. They will pay the 3.8% surtax on $50,000.

Example 5: Sarah & Scott, married filing jointly, have $200,000 of salaries and $150,000 of net investment income for total MAGI of $350,000. The 3.8% surtax would apply to $100,000 of income (excess of $350,000 MAGI over $250,000 threshold amount).

Example 6: Randy, a single taxpayer, age 69, has investment income of $200,000 and is not subject to the surtax. In the following year, Randy has an RMD from his IRA of $125,000. In this case $325,000 of MAGI exceeds the $200,000 threshold and $125,000 is subject to the 3.8% surtax.

3.8% Medicare “Surtax” Overview

Personal Financial Planning Section13

Example 7: The John Smith Trust has investment income of $51,000 and has made no distributions during the current tax year. In this case, $39,800 of income ($51,000 - $11,200 top bracket amount) will be subject to the 3.8% surtax.

Example 8: David and Veronica, married filing jointly, have pension and IRA income and tax-exempt interest income. The 3.8% surtax does not apply regardless of income because they have no “net investment income”.

Example 9: In 2012, Jill, age 60 and single, has wages of $200,000 and taxable interest income from CDs of $100,000. During 2012 Jill moves half of her investments into an annuity and purchases a life insurance policy with the remaining CDs. Because of this planning, in 2013 all of her interest income is sheltered in either the annuity or the life insurance policy. Thus, Jill is not subject to the 3.8% surtax.

3.8% Medicare “Surtax” Overview

Personal Financial Planning Section14

Example 10: The Anita Jones Trust has net investment income of $100,000 and made a distribution of 100% of that income during the current tax year. In this case, the trust will not be subject to the 3.8% surtax (but the trust beneficiaries might be subject to the 3.8% surtax based on their own tax situations).

Example 11: Gary and Barb, married filing jointly, have $130,000 of pension income and $115,000 of net investment income. Further, Gary withdrew $50,000 from his Roth IRA. Given these facts, none of the investment income is subject to the 3.8% surtax because Gary and Barb’s MAGI ($245,000) was below the $250,000 threshold amount.

Example 12: Same facts as Example 11, except that Gary withdrew $50,000 from his traditional IRA. In this situation, $45,000 [($130,000 + $115,000 + $50,000) - $250,000] of net investment income would be subject to the 3.8% surtax.

3.8% Medicare “Surtax” Overview

Personal Financial Planning Section15

Planning Around the “Surtax”Strategies for Reducing “Net Investment Income”

• Municipal bonds

• Tax-deferred annuities

• Life insurance

• Rental real estate

• Oil & gas investments

• Choice of accounting year for estate/trust

• Timing of estate/trust distributions

Personal Financial Planning Section16

Planning Around the “Surtax”Strategies for Reducing “Net Investment Income”Municipal Bond Example

Jacob, a single taxpayer, on average has $180,000 of salary income, $5,000 of interest income and $15,000 of dividend income each year. Recently, Jacob inherited $1,000,000 from his uncle and has determined that he would like to invest the money either in: (a) taxable corporate bonds earning 7% or (b) tax-exempt municipal bonds earning 4.5%. Assuming that Jacob is in the 36% marginal income tax bracket for the 2013 tax year and lives in a state without an income tax, below is a summary of the after-tax yield on each investment:

Corporate bond Municipal bond 4.214% 4.5%

{7% x [1 – (36% + 3.8%)]}

Personal Financial Planning Section17

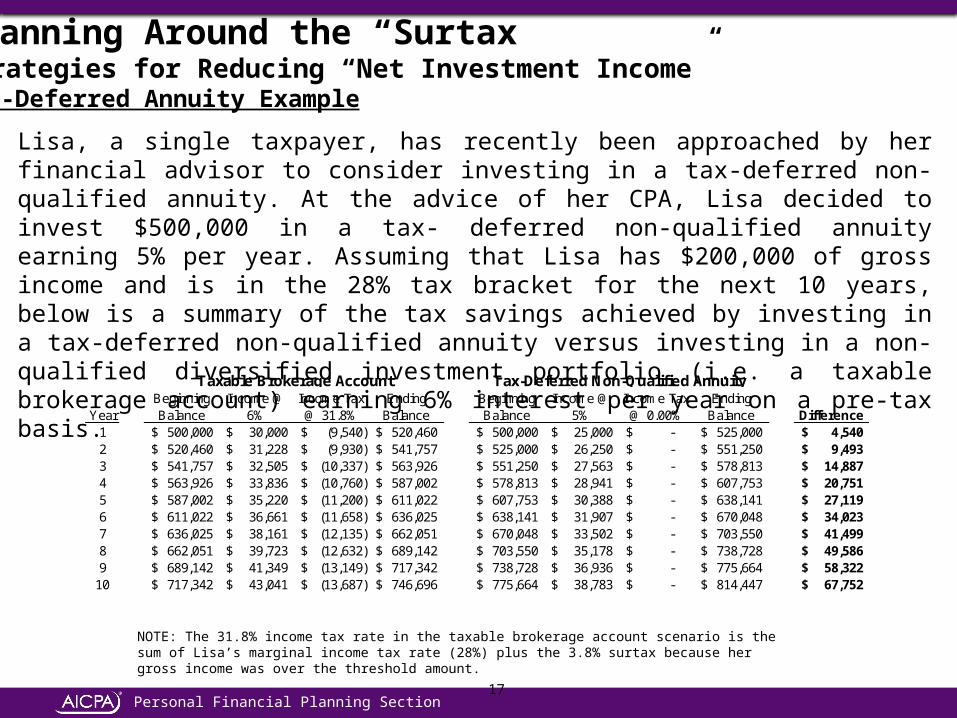

Planning Around the “Surtax”Strategies for Reducing “Net Investment Income”Tax-Deferred Annuity Example

Lisa, a single taxpayer, has recently been approached by her financial advisor to consider investing in a tax-deferred non-qualified annuity. At the advice of her CPA, Lisa decided to invest $500,000 in a tax- deferred non-qualified annuity earning 5% per year. Assuming that Lisa has $200,000 of gross income and is in the 28% tax bracket for the next 10 years, below is a summary of the tax savings achieved by investing in a tax-deferred non-qualified annuity versus investing in a non-qualified diversified investment portfolio (i.e. a taxable brokerage account) earning 6% interest per year on a pre-tax basis.

YearBeginning Balance

Income @ 6%

Income Tax @ 31.8%

Ending Balance

Beginning Balance

Income @ 5%

Income Tax @ 0.00%

Ending Balance Difference

1 500,000$ 30,000$ (9,540)$ 520,460$ 500,000$ 25,000$ -$ 525,000$ 4,540$ 2 520,460$ 31,228$ (9,930)$ 541,757$ 525,000$ 26,250$ -$ 551,250$ 9,493$ 3 541,757$ 32,505$ (10,337)$ 563,926$ 551,250$ 27,563$ -$ 578,813$ 14,887$ 4 563,926$ 33,836$ (10,760)$ 587,002$ 578,813$ 28,941$ -$ 607,753$ 20,751$ 5 587,002$ 35,220$ (11,200)$ 611,022$ 607,753$ 30,388$ -$ 638,141$ 27,119$ 6 611,022$ 36,661$ (11,658)$ 636,025$ 638,141$ 31,907$ -$ 670,048$ 34,023$ 7 636,025$ 38,161$ (12,135)$ 662,051$ 670,048$ 33,502$ -$ 703,550$ 41,499$ 8 662,051$ 39,723$ (12,632)$ 689,142$ 703,550$ 35,178$ -$ 738,728$ 49,586$ 9 689,142$ 41,349$ (13,149)$ 717,342$ 738,728$ 36,936$ -$ 775,664$ 58,322$

10 717,342$ 43,041$ (13,687)$ 746,696$ 775,664$ 38,783$ -$ 814,447$ 67,752$

Tax-Deferred Non-Qualified AnnuityTaxable Brokerage Account

NOTE: The 31.8% income tax rate in the taxable brokerage account scenario is the sum of Lisa’s marginal income tax rate (28%) plus the 3.8% surtax because her gross income was over the threshold amount.

Personal Financial Planning Section18

Planning Around the “Surtax”Strategies for Reducing “Net Investment Income”Life Insurance Example

• Tim, a married-filing-jointly taxpayer, recently paid a $250,000 single premium to purchase a $2,000,000 second-to-die whole-life life insurance policy. At the end of Year 10, Tim withdrew $50,000 from the policy’s cash value when it was worth $450,000.

• Given these facts, none of the $200,000 of earnings to-date ($450,000 current cash value - $250,000 initial premium), or any future earnings within the life insurance policy, are subject to the 3.8% surtax until Tim withdraws more than his initial single premium amount.

• Further, even if Tim withdraws earnings from the life insurance policy in a future tax year, none of the earnings will be subject to the 3.8% surtax, provided that Tim’s MAGI (which would include the earnings withdrawn from the life insurance policy) is below the “threshold amount” (i.e. $250,000 for married-filing-jointly taxpayers).

Personal Financial Planning Section19

Jerry & Mary, married-filing-jointly taxpayers, have $50,000 of net royalty income annually from a gas well in Wyoming. In addition, Jerry has $100,000 in wages, Mary has $75,000 in wages and the both of them have $30,000 in dividend income each year.

At the end of 2012, Jerry & Mary invested $275,000 into a residential real estate property. Based on past results, on average the property value increases by about 3.5% per year and the rental brings in about $5,000 of net income before depreciation. Assuming that the property is depreciated over a 27½-year life, the $275,000 investment will produce a $10,000 annual depreciation expense, resulting in a net rental loss of $5,000. This resulting net rental loss can then be used to offset Jerry & Mary’s net royalty income. Assuming that Jerry and Mary are in the 31% income tax bracket in 2013, below is a summary of the return on investment earned by Jerry & Mary’s from their rental real estate property.

Property appreciation $9,625 ($275,000 x 3.5%)Net cash flow from rental 5,000Income tax savings from rental loss 1,550 ($5,000 x 31%)Surtax savings from rental loss 190 ($5,000 x 3.8%)Total return on investment $16,365

Total return on investment (%) 5.95% ($16,365/$275,000)

Planning Around the “Surtax”Strategies for Reducing “Net Investment Income”Rental Real Estate Example

Personal Financial Planning Section20

• George, a single taxpayer, recently invested $100,000 in a working interest in an oil well. According to the oil well driller’s accountants, 80% of the initial investment can be deducted in the first year as an “intangible drilling cost” (“IDC”). Assuming that George has $80,000 of net investment income subject to the 3.8% surtax and is in the 36% marginal income tax bracket, below is a summary of the total tax savings from the oil well investment.

Income tax savings from IDC deduction $28,800 [($100,000 x 80%) x 36%]Surtax savings from IDC deduction 3,040 [($100,000 x 80%) x 3.8%]Total tax savings $31,840

Planning Around the “Surtax”Strategies for Reducing “Net Investment Income”Oil & Gas Investment Example

Personal Financial Planning Section21

On February 10, 2012, Patricia passed away. During the course of the 2012 tax year, Patricia’s estate had $50,000 of net investment income, $600 of miscellaneous non-investment income and no deductible expenses. In January 2013, the executor of Mary’s estate was trying to determine whether the estate should elect a calendar year-end (i.e. December 31, 2012) or a fiscal year-end (i.e. January 31, 2013).

Assuming a top marginal tax bracket amount of $12,000 in 2013, if the executor were to choose a calendar year-end of December 31, 2012, the estate would save $1,440 [($50,000 - $12,000) x 3.8%] in surtax.

Planning Around the “Surtax”Strategies for Reducing “Net Investment Income”Choice of Accounting Year Example

Personal Financial Planning Section22

During the 2013 tax year, the Smith Family Trust had $100,000 of net investment income and $19,900 of deductible expenses. The trustee is now trying to decide if a distribution of trust accounting income should be made to the trust beneficiaries. Assuming that each of the trust beneficiaries is currently in the 28% tax bracket and each has gross income below the Medicare surtax “threshold amount”, below is a summary of the tax savings that would occur if an $80,000 distribution was made:

No Distribution

$80K Distribution

Gross Income 100,000$ 100,000$ Less: Deductible Expenses (19,900) (19,900) Adjusted Total Income 80,100$ 80,100$ Less: Income Distribution Deduction - (80,000) Less: Exemption (100) (100) Taxable Income 80,000$ -$

Income Tax @ Trust Level 30,407$ -$ Income Tax @ Beneficiary Level - 12,000 Total Income Tax 30,407$ 12,000$

Medicare Surtax @ Trust Level 2,614$ -$ Medicare Surtax @ Beneficiary Level - - Total Medicare Surtax 2,614$ -$

Total Taxes 33,021$ 12,000$

SAVINGS 21,021$

Planning Around the “Surtax”Strategies for Reducing “Net Investment Income”Trust/Estate Distribution Example

Personal Financial Planning Section23

Planning Around the “Surtax”Strategies for Reducing “MAGI”

• Roth IRA conversions

• Charitable remainder trusts (CRTs)

• Non-grantor charitable lead trusts (CLTs)

• Installment sales

Personal Financial Planning Section24

Roth IRA benefits

• Lowers overall taxable income long-term

• Tax-free compounding

• No RMDs at age 70½

• Tax-free withdrawals for beneficiaries

• More effective funding of the “bypass trust”

PURPOSE OF STRATEGY (as it relates to the 3.8% surtax): To lower MAGI below the “threshold amount” over the long-term.

Planning Around the “Surtax”Strategies for Reducing “MAGI”Roth IRA Conversions

Personal Financial Planning Section25

In simplest terms, a traditional IRA will produce the same after-tax result as a Roth IRA provided that:• The annual growth rates are the same

• The tax rate in the conversion year is the same as the tax rate during the withdrawal years (i.e. A x B x C = D; A x C x B = D)

Planning Around the “Surtax”Strategies for Reducing “MAGI”Roth IRA Conversions

Personal Financial Planning Section26

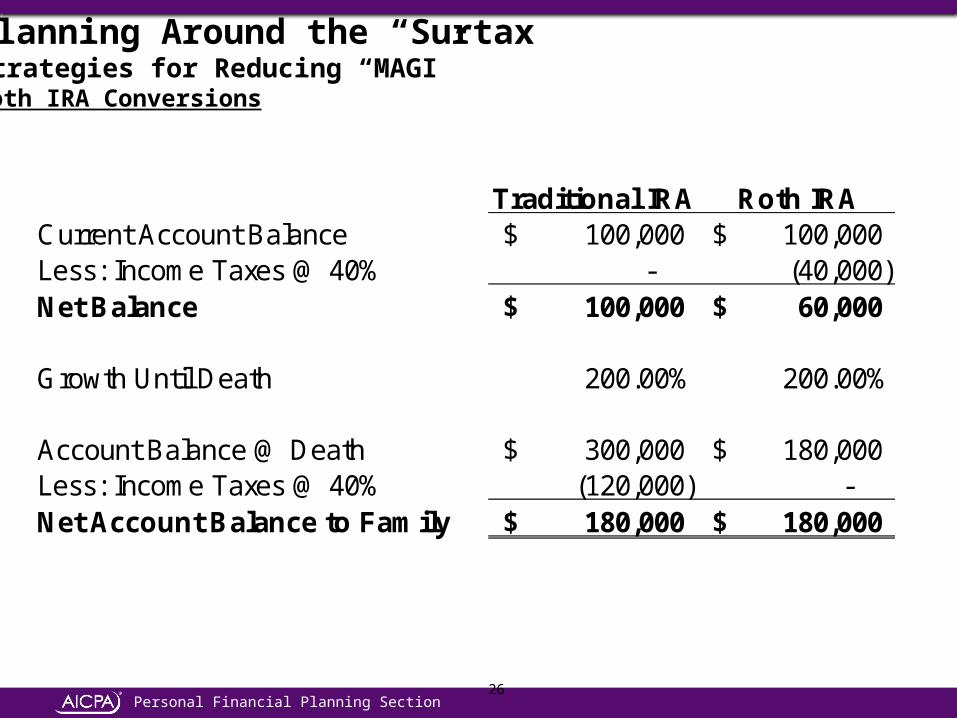

Planning Around the “Surtax”Strategies for Reducing “MAGI”Roth IRA Conversions

Traditional IRA Roth IRACurrent Account Balance 100,000$ 100,000$ Less: Income Taxes @ 40% - (40,000) Net Balance 100,000$ 60,000$

Growth Until Death 200.00% 200.00%

Account Balance @ Death 300,000$ 180,000$ Less: Income Taxes @ 40% (120,000) - Net Account Balance to Family 180,000$ 180,000$

Personal Financial Planning Section27

Planning Around the “Surtax”Strategies for Reducing “MAGI”Roth IRA Conversions

Critical decision factors• Tax rate differential (year of conversion vs. withdrawal

years)

• Use of “outside funds” to pay the income tax liability

• Need for IRA funds to meet annual living expenses

• Time horizon

Personal Financial Planning Section28

The key to successful Roth IRA conversions is to keep as much of the conversion income as possible in the current marginal tax bracket

• However, there are times when it may make sense to convert more and go into higher tax brackets

Planning Around the “Surtax”Strategies for Reducing “MAGI”Roth IRA Conversions

Personal Financial Planning Section29

10% tax bracket

15% tax bracket

25% tax bracket

28% tax bracket

33% tax bracket

35% tax bracket

Current taxable income

Target Roth IRA conversion amount

“Optimum” Roth IRA conversion amount

Planning Around the “Surtax”Strategies for Reducing “MAGI”Roth IRA Conversions

Personal Financial Planning Section30

$2,053,290

$2,946,623

$4,232,738

$2,053,290

$2,946,623

$4,232,738

$2,158,925

$3,172,169

$4,660,957

10 15 20

Year

After-Tax Investment Balance(Tax Rates Remain the Same)

Traditional IRA

Roth IRA Conversion (Pay Tax w/Roth IRA)

Roth IRA Conversion (Pay Tax w/Outside Account)

Planning Around the “Surtax”Strategies for Reducing “MAGI”Roth IRA Conversions – Chart #1 (50-Year-Old)

Personal Financial Planning Section31

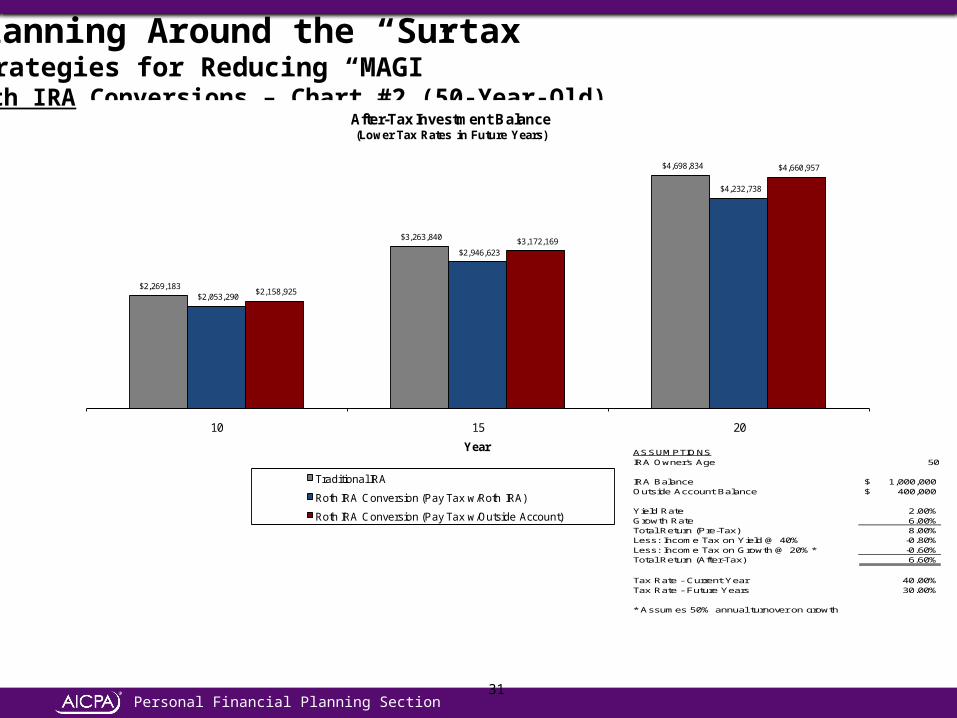

$2,269,183

$3,263,840

$4,698,834

$2,053,290

$2,946,623

$4,232,738

$2,158,925

$3,172,169

$4,660,957

10 15 20

Year

After-Tax Investment Balance(Lower Tax Rates in Future Years)

Traditional IRA

Roth IRA Conversion (Pay Tax w/Roth IRA)

Roth IRA Conversion (Pay Tax w/Outside Account)

Planning Around the “Surtax”Strategies for Reducing “MAGI”Roth IRA Conversions – Chart #2 (50-Year-Old)

ASSUMPTIONSIRA Owner's Age 50

IRA Balance 1,000,000$ Outside Account Balance 400,000$

Yield Rate 2.00%Growth Rate 6.00%Total Return (Pre-Tax) 8.00%Less: Income Tax on Yield @ 40% -0.80%Less: Income Tax on Growth @ 20%* -0.60%Total Return (After-Tax) 6.60%

Tax Rate - Current Year 40.00%Tax Rate - Future Years 30.00%

* Assumes 50% annual turnover on growth

Personal Financial Planning Section 32

$2,053,290

$2,946,623

$4,232,738

$2,269,183

$3,263,840

$4,698,834

$2,348,409

$3,432,999

$5,019,998

10 15 20

Year

After-Tax Investment Balance(Higher Tax Rates in Future Years)

Traditional IRA

Roth IRA Conversion (Pay Tax w/Roth IRA)

Roth IRA Conversion (Pay Tax w/Outside Account)

ASSUMPTIONSIRA Owner's Age 50

IRA Balance 1,000,000$ Outside Account Balance 400,000$

Yield Rate 2.00%Growth Rate 6.00%Total Return (Pre-Tax) 8.00%Less: Income Tax on Yield @ 40% -0.80%Less: Income Tax on Growth @ 20%* -0.60%Total Return (After-Tax) 6.60%

Tax Rate - Current Year 30.00%Tax Rate - Future Years 40.00%

* Assumes 50% annual turnover on growth

Planning Around the “Surtax”Strategies for Reducing “MAGI”Roth IRA Conversions – Chart #3 (50-Year-Old)

Personal Financial Planning Section

33

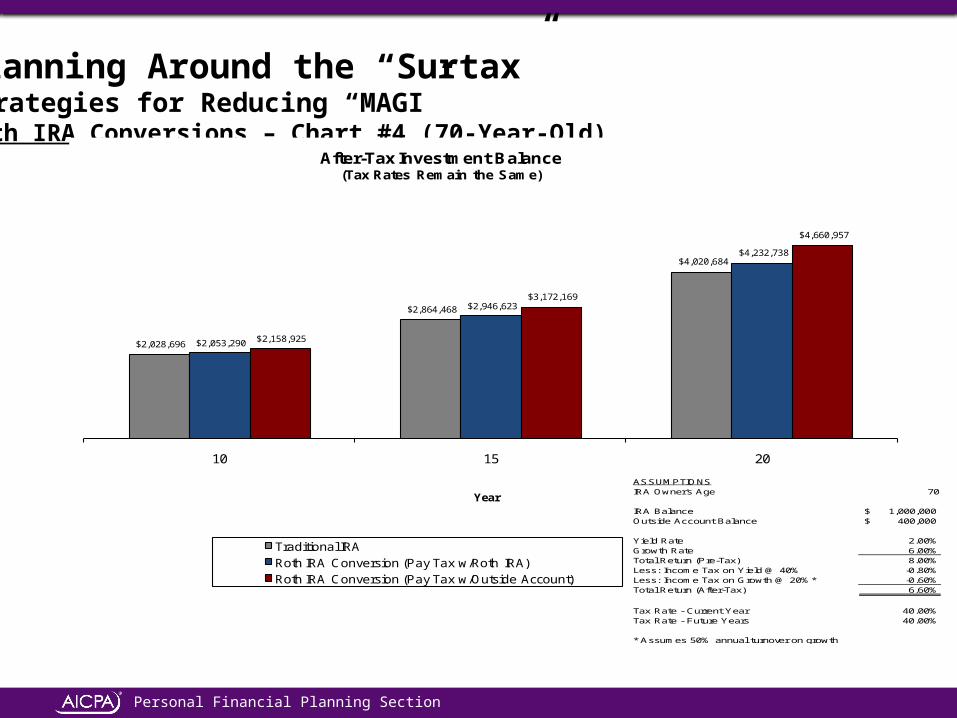

$2,028,696

$2,864,468

$4,020,684

$2,053,290

$2,946,623

$4,232,738

$2,158,925

$3,172,169

$4,660,957

10 15 20

Year

After-Tax Investment Balance(Tax Rates Remain the Same)

Traditional IRARoth IRA Conversion (Pay Tax w/Roth IRA)Roth IRA Conversion (Pay Tax w/Outside Account)

Planning Around the “Surtax”Strategies for Reducing “MAGI”Roth IRA Conversions – Chart #4 (70-Year-Old)

ASSUMPTIONSIRA Owner's Age 70

IRA Balance 1,000,000$ Outside Account Balance 400,000$

Yield Rate 2.00%Growth Rate 6.00%Total Return (Pre-Tax) 8.00%Less: Income Tax on Yield @ 40% -0.80%Less: Income Tax on Growth @ 20%* -0.60%Total Return (After-Tax) 6.60%

Tax Rate - Current Year 40.00%Tax Rate - Future Years 40.00%

* Assumes 50% annual turnover on growth

Personal Financial Planning Section 34

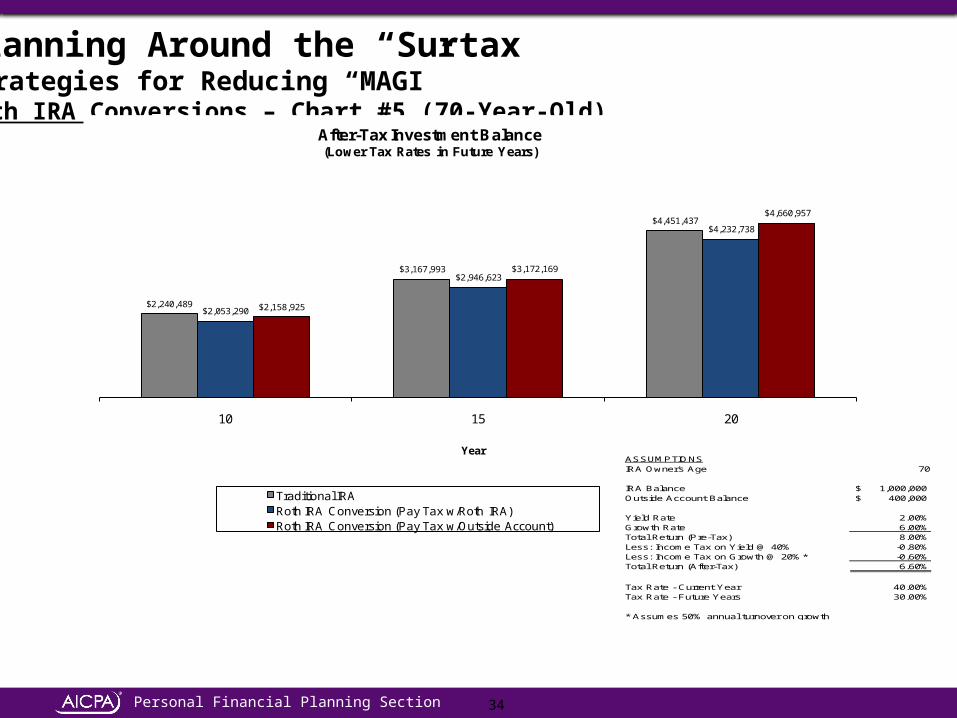

$2,240,489

$3,167,993

$4,451,437

$2,053,290

$2,946,623

$4,232,738

$2,158,925

$3,172,169

$4,660,957

10 15 20

Year

After-Tax Investment Balance(Lower Tax Rates in Future Years)

Traditional IRARoth IRA Conversion (Pay Tax w/Roth IRA)Roth IRA Conversion (Pay Tax w/Outside Account)

Planning Around the “Surtax”Strategies for Reducing “MAGI”Roth IRA Conversions – Chart #5 (70-Year-Old)

ASSUMPTIONSIRA Owner's Age 70

IRA Balance 1,000,000$ Outside Account Balance 400,000$

Yield Rate 2.00%Growth Rate 6.00%Total Return (Pre-Tax) 8.00%Less: Income Tax on Yield @ 40% -0.80%Less: Income Tax on Growth @ 20%* -0.60%Total Return (After-Tax) 6.60%

Tax Rate - Current Year 40.00%Tax Rate - Future Years 30.00%

* Assumes 50% annual turnover on growth

Personal Financial Planning Section 35

Planning Around the “Surtax”Strategies for Reducing “MAGI”Roth IRA Conversions – Chart #6 (70-Year-Old)

$2,028,696

$2,864,468

$4,020,684

$2,269,183

$3,263,840

$4,698,834

$2,348,409

$3,432,999

$5,019,998

10 15 20

Year

After-Tax Investment Balance(Higher Tax Rates in Future Years)

Traditional IRARoth IRA Conversion (Pay Tax w/Roth IRA)Roth IRA Conversion (Pay Tax w/Outside Account)

ASSUMPTIONSIRA Owner's Age 70

IRA Balance 1,000,000$ Outside Account Balance 400,000$

Yield Rate 2.00%Growth Rate 6.00%Total Return (Pre-Tax) 8.00%Less: Income Tax on Yield @ 40% -0.80%Less: Income Tax on Growth @ 20%* -0.60%Total Return (After-Tax) 6.60%

Tax Rate - Current Year 30.00%Tax Rate - Future Years 40.00%

* Assumes 50% annual turnover on growth

Personal Financial Planning Section36

Planning Around the “Surtax”Strategies for Reducing “MAGI”Charitable Remainder Trust (CRT)

A Charitable Remainder Trust (CRT) is a split interest trust consisting of an income interest and a remainder interest. During the term of the trust, the income interest is usually paid out to the donor (or some other named beneficiary). At the end of the trust term, the remainder (whatever is left in the trust) is paid to the charity or charities that have

been designated in the trust document.

PURPOSE OF STRATEGY (as it relates to the 3.8% surtax): To harbor “net investment income” in a tax-exempt environment while at the same time leveling income over a longer period of time to keep MAGI below the “threshold amount”.

Personal Financial Planning Section37

Donor(Income Beneficiary)

Public Charity

(Remainder Beneficiary)

Transfer of highly-appreciated assets

Donor receives an immediate income tax deduction for present

value of the remainder interest (must be at least 10% of the value of the

assets originally contributed)

At the donor’s death (or at the end of the trust term), the charity receives the residual assets held in the trust

Annual (or more frequent) payments for life (or a term of

years)

CRT

Planning Around the “Surtax”Strategies for Reducing “MAGI”Charitable Remainder Trust (CRT)

Personal Financial Planning Section38

Charitable Remainder Annuity Trust (CRAT) – the beneficiaries receive a stated amount of the initial trust assets each year.• The amount received is established at the beginning of the trust and will not

change during the term of the trust regardless of investment performance (unless inadequate investment performance causes the trust to run out of assets)

Charitable Remainder Unitrust (CRUT) – the income beneficiaries receive a stated percentage of the trust’s assets each year.• The distribution will vary from year to year depending on the investment

performance of the trust assets and the amount withdrawn

Two Main Types of CRTs

Planning Around the “Surtax”Strategies for Reducing “MAGI”Charitable Remainder Trust (CRT)

Personal Financial Planning Section39

• Annual payout can neither be less than 5% nor more than 50%.

• The present value of the remainder interest must be at least 10% of the value of the assets contributed to the trust.

• The trust term cannot be more than 20 years (if a term interest is used)

Special Considerations

Planning Around the “Surtax”Strategies for Reducing “MAGI”Charitable Remainder Trust (CRT)

Personal Financial Planning Section40

A Charitable Lead Trust (CLT) is a split interest trust consisting of an income interest and a remainder interest. During the term of the trust, the income interest is paid out to a named charity. At the end of the trust term, the remainder (whatever is left in the trust) is paid to non-charitable beneficiaries (e.g. children of the donor) that have been designated in the trust document.

PURPOSE OF STRATEGY (as it relates to the 3.8% surtax): To offset “net investment income” against charitable deductions dollar-for-dollar in a tax-efficient manner.

Planning Around the “Surtax”Strategies for Reducing “MAGI”Charitable Lead Trust (CLT)

Personal Financial Planning Section

41

Donor(Income Beneficiary)

PublicCharity

(Income Beneficiary)

Transfer of cash, stock and/or other assets

At the donor’s death (or at the end of the trust term),

the remainder beneficiaries receive the residual assets

held in the trust

Annual (or more frequent) payments for life (or a term of years)

CLT

Donor’s Children(Remainder Beneficiary)

Planning Around the “Surtax”Strategies for Reducing “MAGI”Charitable Lead Trust (CLT)

Personal Financial Planning Section42

Charitable Lead Annuity Trust (CLAT) – The charitable beneficiary receives a stated amount of the initial trust assets each year.• The amount received is established at the beginning of the trust and will

not change during the term of the trust regardless of investment performance (unless inadequate investment performance causes the trust to run out of assets)

Charitable Lead Unitrust (CLUT) – The charitable beneficiary receives a stated percentage of the trust’s assets each year.• The distribution will vary from year to year depending on the investment

performance of the trust assets and the amount withdrawn

Two Main Types of CLTs

Planning Around the “Surtax”Strategies for Reducing “MAGI”Charitable Lead Trust (CLT)

Personal Financial Planning Section43

An installment sale is a type of sale in which the seller sells an asset to another person in exchange for a promissory note paid over a period of time. If executed correctly, the taxable gain recognized by the seller will be deferred until payments are made on the principal of the note.

PURPOSE OF STRATEGY (as it relates to the 3.8% surtax): To level “net investment income” over a longer period of time so as to keep MAGI below the “threshold amount”.

Planning Around the “Surtax”Strategies for Reducing “MAGI”Installment Sale

Personal Financial Planning Section44

Seller BuyerSale of highly-appreciated asset

Promissory note paid over a period of years

Taxable gain is deferred until payments on principal are made

Planning Around the “Surtax”Strategies for Reducing “MAGI”Installment Sale

Personal Financial Planning Section 45

To be added to our newsletter, please email

or

visit our website at

www.keeblerandassociates.com

Personal Financial Planning Section 46

PFP Section Resources (aicpa.org/PFP)

Series: Proactive Planning in Preparation for 2013• Access the seminar recording and slide decks from the following

2 web seminars at aicpa.org/PFP/webseminars- Proactive Planning in Preparation for 2013 (5/7)- Investment Strategies in Preparation for 2013 (5/29)

• Upcoming web seminars in Proactive Planning in Preparation for 2013 series:- Estate Planning Strategies In-Depth (date TBD)- Post Election: What Now?

Visit aicpa.org/PFP/proactiveplanning for more resources

Personal Financial Planning Section 47

New Keebler Chart on Gain Harvesting

Available to PFP/PFS members

Personal Financial Planning Section 48

New Toolkit from Bob Keebler!

Preparing Your Client for the 2013 Tax Increases: Tools, Tips and Tactics

Get up to speed quickly and educate your clients on the forces shaping the individual tax landscape right now. The information and resources on this multimedia toolkit will enable you to help your individual clients make good decisions and implement practices that will yield benefits in 2013.

PFP/PFS members pay $59 for this toolkit (a savings of more than 50% off of the regular price)

Available on www.CPA2Biz.com

Personal Financial Planning Section

Circular 230 DisclosurePursuant to the rules of professional conduct set forth in Circular 230, as promulgated by the United States Department of the Treasury, nothing contained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service, and it cannot be used by any taxpayer for such purpose. No one, without our express prior written permission, may use or refer to any tax advice in this communication in promoting, marketing, or recommending a partnership or other entity, investment plan or arrangement to any other party.

For discussion purposes only. This work is intended to provide general information about the tax and other laws applicable to retirement benefits. The author, his firm or anyone forwarding or reproducing this work shall have neither liability nor responsibility to any person or entity with respect to any loss or damage caused, or alleged to be caused, directly or indirectly by the information contained in this work. This work does not represent tax, accounting, or legal advice. The individual taxpayer is advised to and should rely on their own advisors.

49