csx q4_2006

TRANSCRIPT

11

Fourth Quarter 2006Earnings Presentation

Fourth Quarter 2006Earnings Presentation

22

Forward Looking DisclosureThis presentation and other statements by the company contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act with respect to, among other items: projections and estimates of earnings, revenues, cost-savings, expenses, or other financial items; statements of management’s plans, strategies and objectives for future operation, and management’s expectations as to future performance and operations and the time by which objectives will be achieved; statements concerning proposed new products and services; and statements regarding future economic, industry or market conditions or performance. Forward-looking statements are typically identified by words or phrases such as “believe,” “expect,” “anticipate,” “project,” and similar expressions. Forward-looking statements speak only as of the date they are made, and the company undertakes no obligation to update or revise any forward-looking statement. If the company does update any forward-looking statement, no inference should be drawn that the company will make additional updates with respect to that statement or any other forward-looking statements.

Forward-looking statements are subject to a number of risks and uncertainties, and actual performance or results could differ materially from that anticipated by these forward-looking statements. Factors that may cause actual results to differ materially from those contemplated by these forward-looking statements include, among others: (i) the company’s success in implementing its financial and operational initiatives, (ii) changes in domestic or international economic or business conditions, including those affecting the rail industry (such as the impact of industry competition, conditions, performance and consolidation); (iii) legislative or regulatory changes; (iv) the inherent business risks associated with safety and security; and (v) the outcome of claims and litigation involving or affecting the company. Other important assumptions and factors that could cause actual results to differ materially from those in the forward-looking statements are specified in the company’s SEC reports, accessible on the SEC’s website at www.sec.gov and the company’s website at www.csx.com.

33

Executive Summary

Michael WardChairman, President andChief Executive Officer

44

Fourth quarter overview . . .

Surface Transportation produced record results

Yield environment remains strong

Operations building strong service momentum

Economic environment remains positive

Note: Comparable 2006 earnings per share exclude insurance recoveries, a Conrail property gain and income tax benefits

Fourth Quarter Earnings Per Share

$0.52 $0.52

$0.75

$0.57

Reported Comparable

2005 2006

55

Sales and Marketing Review

Clarence GoodenExecutive Vice PresidentSales and Marketing

66

Revenue increased 8% to $2.4 billion

Fourth QuarterRevenue in Millions

2005 2006

$2,219

$2,396

Record fourth quarter revenues, up $177 million

Overall volumes were essentially flat

Yield environment remains strong

77

Revenue per unit increased 8%

Fourth Quarter Revenue Per Unit2006 versus 2005

8%

(2%)

4%

11%

11%

Surface Transportation

Intermodal

Automotive

Coal

Merchandise

88

Price continues to drive RPU growth

Year-Over-Year Change

6.6%6.7%6.8%6.2%6.3%5.6%6.0%4.8%

8.6%9.6% 9.0%

11.0% 11.7%12.6%

11.8%

8.4%

Q12005

Q22005

Q32005

Q42005

Q12006

Q22006

Q32006

Q42006

Price Increase on 'Same Store Sales' Total Revenue per Unit

Note: Price increases on a ‘Same Store Sales’ basis excludes fuel surchargeand mix impacts

99

Merchandise revenue increased 9%

Fourth Quarter2006 versus 2005

9%

(3%)

11%

Revenue Volume RPU

19th consecutive quarter of revenue growth

Pricing environment remains strong

Volumes soft in several markets, partially offset by Agricultural growth

1010

Coal revenue increased 16%

Fourth Quarter2006 versus 2005

16%

5%

11%

Revenue Volume RPU

Strong demand continues in certain markets

Utility inventories are at target levels

Continued favorable pricing environment

1111

Automotive revenue decreased 7%

Fourth Quarter2006 versus 2005

(7%)

(10%)

4%

Revenue Volume RPU

Volume down on production declines

New Domestics continue to gain market share

Pricing opportunities continue

1212

Intermodal revenue decreased 2%

Fourth Quarter2006 versus 2005

(2%)

0%

(2%)

Revenue Volume RPU

Overall volume flat; international growth offset domestic declines

Mix impacted overall revenue-per-unit; pricing environment still favorable

Operating Income— Declined in Q4— Improved for full year— 2007 outlook positive

1313

First quarter revenue outlook positive

AutomotiveEmerging Markets

Food & Consumer

Forest Products

Agricultural Products

Chemicals

Coal, Coke & Iron Ore

Intermodal

Metals

Phosphate & Fertilizer

UnfavorableNeutralFavorable

1414

Looking forward . . .

Economic Forecast2007-2008

2.3%

3.2%

1.8%2.1%

2007 2008

GDP Industrial Production

GDP and IDP forecasted at about 2% to 3%

Continued strong pricing environment

Short-term volume weakness; long-term strength

Service and capacity improvements will support growth

1515

Operations Review

Tony IngramExecutive Vice PresidentChief Operating Officer

1616

Leadership, discipline and execution

Safety performance improving

Positive operating trends continue

Asset utilization improving

SafetySafety

ProductivityProductivity

ServiceService

LeadershipLeadership

DisciplineDiscipline

ExecutionExecution

ReliablePerformance

ReliablePerformance

1717

Safety performance remains strong

Rolling 12-month Averages

FRA Personal Injury

1.77 1.681.54 1.42 1.39

Q42005

Q12006

Q22006

Q32006

Q42006

FRA Train Accidents

4.414.01 3.86

3.52 3.35

Q42005

Q12006

Q22006

Q32006

Q42006

13 WeekAverage

1.32

13 WeekAverage

3.48

21% Year21% Year--OverOver--Year ImprovementYear Improvement 24% Year24% Year--OverOver--Year ImprovementYear Improvement

1818

On-time performance is improving

Rolling 12-month Averages

On-Time Originations

51%57%

65%71% 76%

Q42005

Q12006

Q22006

Q32006

Q42006

On-Time Arrivals

40%46%

52%57%

63%

Q42005

Q12006

Q22006

Q32006

Q42006

13 WeekAverage

76%

13 WeekAverage

66%

49% Year49% Year--OverOver--Year ImprovementYear Improvement 56% Year56% Year--OverOver--Year ImprovementYear Improvement

1919

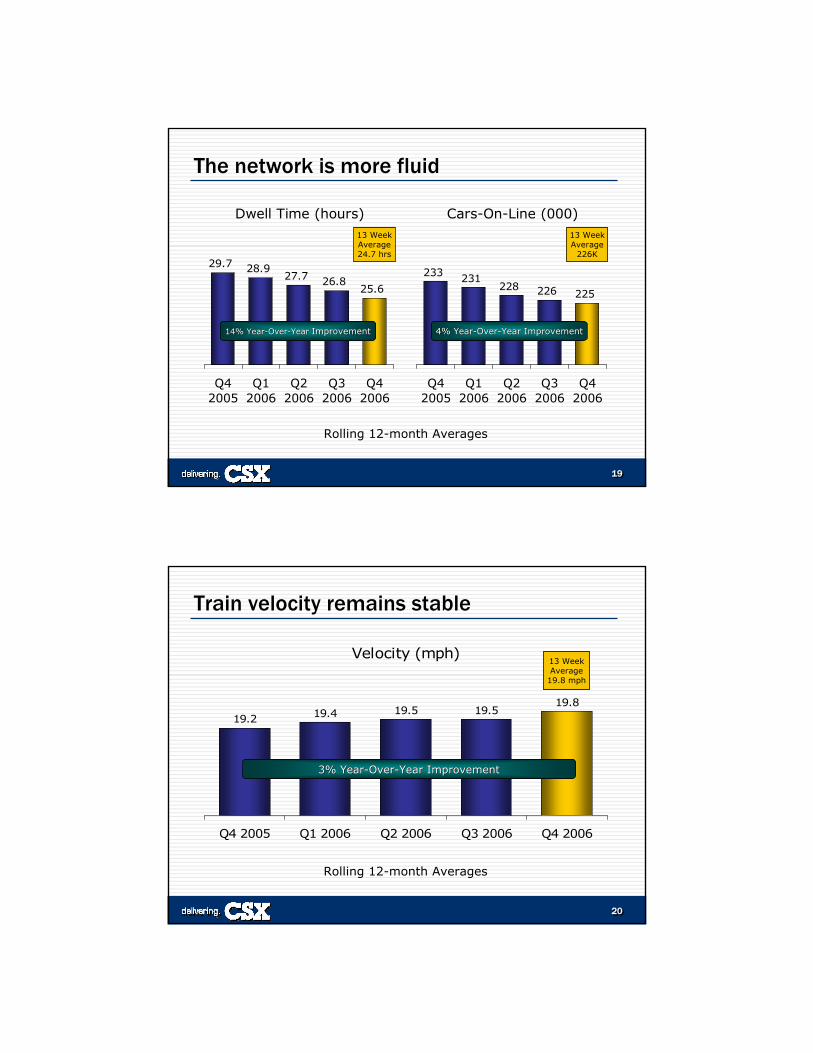

The network is more fluid

Rolling 12-month Averages

Cars-On-Line (000)

233 231228 226 225

Q42005

Q12006

Q22006

Q32006

Q42006

Dwell Time (hours)

29.7 28.927.7 26.8

25.6

Q42005

Q12006

Q22006

Q32006

Q42006

13 WeekAverage24.7 hrs

13 WeekAverage

226K

14% Year14% Year--OverOver--Year Year ImprovementImprovement 4% Year4% Year--OverOver--Year ImprovementYear Improvement

2020

Train velocity remains stable

Velocity (mph)

19.2 19.4 19.5 19.519.8

Q4 2005 Q1 2006 Q2 2006 Q3 2006 Q4 2006

13 WeekAverage

19.8 mph

3% Year3% Year--OverOver--Year ImprovementYear Improvement

Rolling 12-month Averages

2121

Looking forward . . .

Safety momentum will be sustained

Targeting consistent service improvement

Continue managing resources for growth and productivity

2222

Financial Results

Oscar MunozExecutive Vice PresidentChief Financial Officer

2323

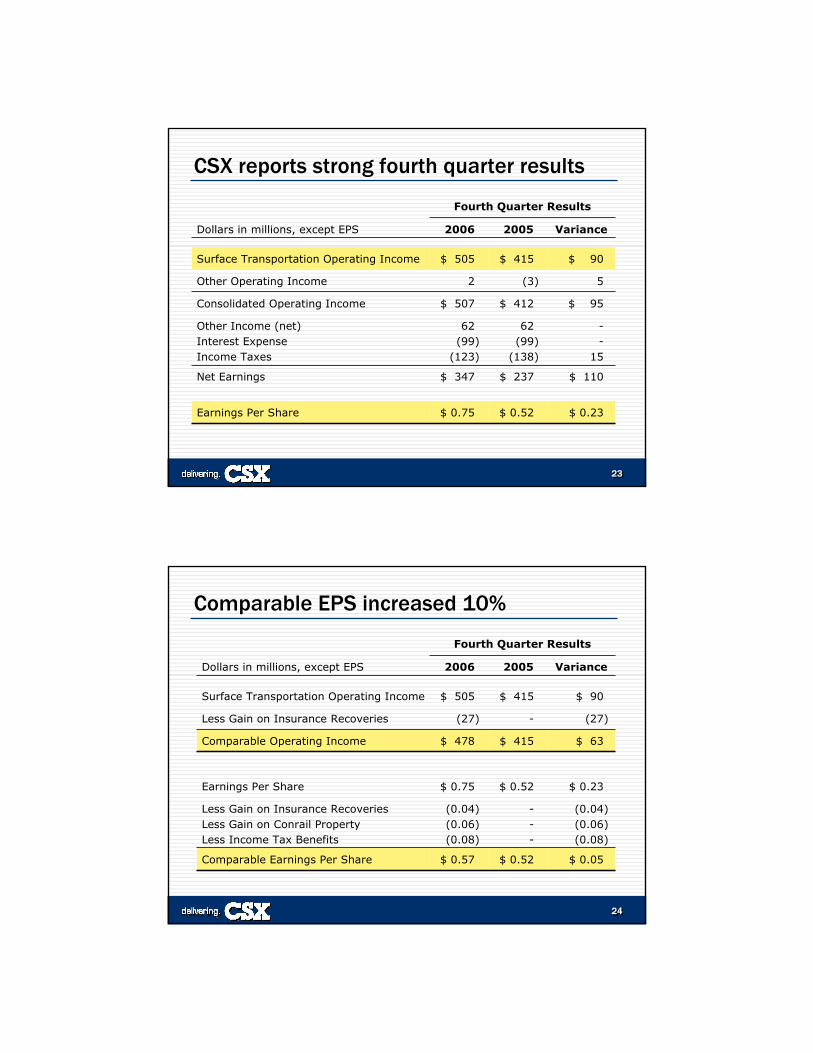

CSX reports strong fourth quarter results

$ 110$ 237$ 347Net Earnings

$ 0.23$ 0.52$ 0.75Earnings Per Share

--

15))

62(99

(138))

62(99

(123

Other Income (net)Interest ExpenseIncome Taxes

$ 95$ 412$ 507Consolidated Operating Income

5)(32Other Operating Income

$ 90$ 415$ 505Surface Transportation Operating Income

Variance20052006Dollars in millions, except EPS

Fourth Quarter Results

2424

Comparable EPS increased 10%

)))

(0.04(0.06(0.08

---

)))

(0.04(0.06(0.08

Less Gain on Insurance RecoveriesLess Gain on Conrail PropertyLess Income Tax Benefits

$ 0.05$ 0.52$ 0.57Comparable Earnings Per Share

$ 0.23$ 0.52$ 0.75Earnings Per Share

$ 63$ 415$ 478Comparable Operating Income

)(27-)(27Less Gain on Insurance Recoveries

$ 90$ 415$ 505Surface Transportation Operating Income

Variance20052006Dollars in millions, except EPS

Fourth Quarter Results

2525

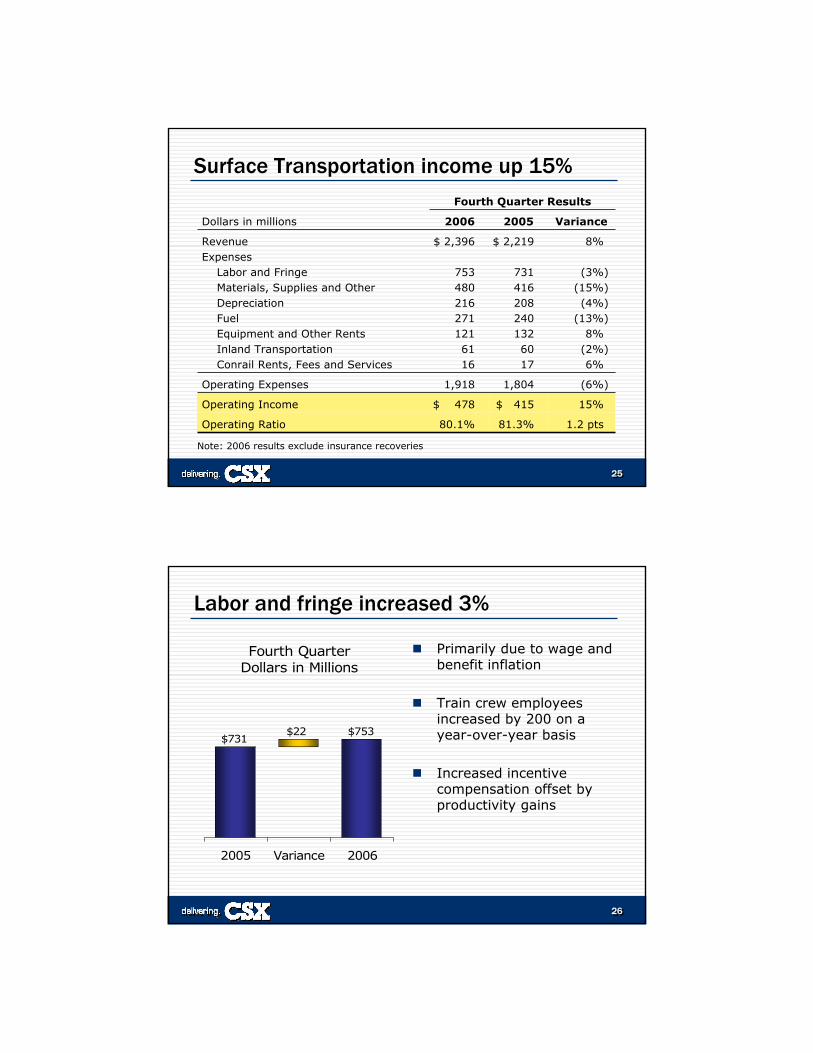

Surface Transportation income up 15%

15%$ 415 $ 478Operating Income

1.2 pts81.3%80.1%Operating Ratio

)(6%1,8041,918Operating Expenses

))))

)

8%

(3%(15%(4%

(13%8%

(2%6%

$ 2,219

7314162082401326017

$ 2,396

7534802162711216116

RevenueExpenses

Labor and FringeMaterials, Supplies and OtherDepreciationFuelEquipment and Other RentsInland TransportationConrail Rents, Fees and Services

Variance20052006Dollars in millions

Fourth Quarter Results

Note: 2006 results exclude insurance recoveries

2626

Labor and fringe increased 3%

Primarily due to wage and benefit inflation

Train crew employees increased by 200 on a year-over-year basis

Increased incentive compensation offset by productivity gains

Fourth QuarterDollars in Millions

$753$731

$22

2005 Variance 2006

2727

MS&O increased 15%

Consistent with third quarter 2006 expense

Cycling prior year favorability in casualty and other reserves

Driven by higher than historical inflation levels

Fourth QuarterDollars in Millions

$480

$416

$64

2005 Variance 2006

2828

Fuel increased 13%

Fourth QuarterDollars in Millions

$271$240

$31

2005 Variance 2006

Consumed 150 million gallons at average gross price of $1.81

Comparison impacted by $58 million in lower hedge

2929

Rents decreased 8%

Fourth QuarterDollars in Millions

$121$132 ($11)

2005 Variance 2006

Lower Automotive and Merchandise volumes

Asset utilization driven by improved operations

3030

All other expenses increased 3%

Fourth QuarterDollars in Millions

$208 $216

$60 $61

$8

2005 Variance 2006

$285 $293

Depreciation Inland Transportation Conrail Fees

$17 $16

3131

Comparable full year EPS increased 31%

))))

(0.22(0.06(0.16(0.27

)

--

(0.160.27

)))

(0.22 (0.06(0.32

-

Less Gain on Insurance RecoveriesLess Gain on Conrail PropertyLess Income Tax BenefitsPlus Debt Repurchase Expense

$ 0.52$ 1.70$ 2.22Comparable Earnings Per Share

$ 1.23$ 1.59$ 2.82Earnings Per Share

$ 409$ 1,549$ 1,958Comparable Operating Income

)(168-)(168Less Gain on Insurance Recoveries

$ 577$ 1,549$ 2,126Surface Transportation Operating Income

Variance20052006Dollars in millions, except EPS

Full Year Results

3232

Record 2006 Surface Transportation results

Comparable Surface Transportation Operating Income in Millions

$902$1,064

$1,549

$1,958

2003 2004 2005 2006Note: Results for 2003, 2004 and 2006 exclude provisions for casualty claims,

restructuring charges and insurance recoveries

3333

Building momentum to the mid-70’s

Comparable Surface TransportationOperating Ratio

87.9%86.8%

82.0%

79.5%

2003 2004 2005 2006Note: Results for 2003, 2004 and 2006 exclude provisions for casualty claims,

restructuring charges and insurance recoveries

3434

Growing cash supports steady investment

Free Cash FlowDollars in Millions

$281

$500

$361

2006 2007

12%

12%

58%

18%

2007 Capital Spending$1.4 Billion

Infrastructure New Capacity

Locomotive Cars & OtherInsurance Recoveries

Note: Insurance recoveries reflect current estimate

3535

Financial wrap-up . . .

Record results for Surface Transportation

Strong momentum in operating ratio

Improving 2007 cash flows with steady investment in the business

Reaffirm 2010 long-range financial targets

3636

Concluding Remarks

Michael WardChairman, President andChief Executive Officer

3737

Looking forward . . .

Producing strong results for shareholders

Industry positioned to continue its renaissance

Leveraging better service for profitable growth

Targeting greatest success in our 180th year

Demand forDemand forTransportationTransportationRemains HighRemains High

SupplySupplyChains areChains areExtendingExtending

TruckingTruckingRemainsRemains

ChallengedChallenged

3838

Fourth Quarter 2006Earnings Presentation

Fourth Quarter 2006Earnings Presentation