cpc financial statements 4q16 - s3.amazonaws.coms3.amazonaws.com/inktankir2/cpg/cpc fy16...

TRANSCRIPT

KPMG Hazem Hassan Nasr Abou ElAbas-Morsion International Public Accounts & Consultant Public Accounts & Consultant AUDITORS’ REPORT To the shareholders of Cairo Poultry Company "An Egyptian joint stock Company" Report on the Financial Statements We have audited the accompanying consolidated financial statements of Cairo Poultry Company S.A.E, which comprise the consolidated balance sheet as at 31 December 2016 , and the related consolidated statements of income, changes in shareholders’ equity, and cash flow for the year then ended, and a summary of significant accounting policies and other explanatory notes. Management's Responsibility for the Financial Statements These consolidated financial statements are the responsibility of Company’s management. Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with the Egyptian Accounting Standards and in the light of the prevailing Egyptian laws, management responsibility includes, designing, implementing and maintaining internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error management responsibility also includes selecting and applying appropriate accounting policies and making accounting estimates that are reasonable in the circumstances. Auditor's Responsibility Our responsibility is to express an opinion on these consolidated financial statements based on our audit. Except as described below, We conducted our audit in accordance with the Egyptian Standards on Auditing and in the light of the prevailing Egyptian laws. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the consolidated financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion on the consolidated financial statements. Basis for Qualified Opinion As described in note no. (31) the consolidated financial statements include assets, liabilities, revenues and expenses refers to subsidiaries that were audited by other auditors amounted to L.E 700 580 972, L.E, 390 226 709 and L.E 822 281 932 and 760 376 907 with a percentage of 30%,29.6%, 29.3% and 29.9% respectively to total consolidated assets, liabilities, expenses and revenues as at 31 December 2016. Against 29.5% 29.9% 29.7% and 29.3% respectively to total consolidated assets, liabilities, expenses and consolidated revenues as at 31 December 2015, So we couldn't determine whether there is an important adjustments to be made of the value of these assets, liabilities, expenses and revenues recorded in the consolidated financial statements to be relevant in accordance with Egyptian Accounting Standards. Qualified Opinion In our opinion, except for the effects of such adjustments, if any, as might have been determined to be necessary had we audited the financial statements of such subsidiary companies referred to in paragraph above, the consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of the group as at 31 December 2016 and the results of its operations and its cash flows for the financial year then ended, in accordance with Egyptian Accounting Standards and relevant Egyptian laws and regulations that related to prepare this consolidated financial statements. Salah El Missary Nasr Abou ElAbas Capital Authority Controller Capital Authority Controller Register N0.(364) Register N0.(106) KPMG Hazem Hassan Morison International Cairo, 17 January 2016

Cairo Poultry Company (An Egyptian Joint Stock Company) Consolidated financial statements for the year ended 31 December 2016 and auditors’ report

KPMG Hazem Hassan Nasr Abou ElAbas Public Accounts & Consultant Public Accounts & Consultant

Cairo Poultry Company "An Egyptian Joint Stock Company" Contents

Pages Auditors’ report ................................................................................................................... Consolidated balance sheet ………………………………………………………………

1 Consolidated income statement ........................................................................................... 2 Consolidated statement of changes in shareholders’ equity ................................................ 3 Consolidated statement of cash flows ................................................................................ 4 Notes to the Consolidated financial statements ................................................................... 5 – 43

- 1 -

Translation From ArabicCairo Poultry Company(An Egyptian Joint Stock Company)Consolidated balance sheetAs at 31 December 2016

Note no. 31/12/2016 31/12/2015

Non-current assets L.E. L.E.Property, Plant and equipment (12) 932 744 282 912 284 878Breeders (13) 108 978 076 80 022 388Plant Wealth (14) 357 749 371 264Projects under construction (15) 29 014 380 9 807 639Other financial investments (16) 760 738 762 500Investments in associate companies (17) 130 221 767 135 887 946Available for sale investments (1-18) - 105 548 717Other non-current assets 212 704 258 104Total non-current assets 1 202 289 696 1 244 943 436

Current assetsInventories (19) 536 198 041 372 375 294Biological assets (20) 84 118 137 62 705 618Trade receivables & other debit balances (21) 306 154 728 238 952 701Due from related parties (1-32) 68 696 066 39 492 055Cash and cash equivalent (22) 137 813 237 83 397 366Non-current assets avaiable for sale - 7 467 860Total current assets 1 132 980 209 804 390 894Total assets 2 335 269 905 2 049 334 330

Shareholders' EquityIssued & paid - up capital (33) 383 201 280 348 364 800Reserves (34) 164 707 695 156 649 645Special reserve- change in value of investments available for sale (35) - 2 846 685Revaluation surplus 39 685 042 39 685 042Retained earnings 178 060 886 192 448 838Parent company's share in profits of treasury stocks sale 196 446 196 446Net profit for the year 237 431 691 270 462 518Total equity attributable to the shareholders of the parent company 1 003 283 040 1 010 653 974Minority interest (2-31) 13 518 253 13 649 240Total Shareholders' Equity 1 016 801 293 1 024 303 214

Non-current liabilitiesLong term loans (36) 62 747 615 91 134 250Deffered tax liabilities (1-26) 65 839 302 63 098 866Deffered sales tax installments 240 000 280 000Total non-current liabilities 128 826 917 154 513 116

Provisions of claims (23) 183 494 008 85 776 245Banks-credit facilities (24) 615 457 324 367 008 883Banks-overdrafts 389 644 7 194 733Tax authority creditors-income tax 79 683 910 71 606 932Trade payables & other credit balances (25) 241 411 748 261 294 098Due to related parties (2-32) 4 185 325 5 531 055Long term loans - current portion (36) 65 019 736 72 106 054Total current liabilities 1 189 641 695 870 518 000Total shareholders' equity and non-current liabilities 2 335 269 905 2 049 334 330

Notes in pages from (6) to (43) form an integral part of the consolidated financial statements.

Group Finance & Admin Director Managing Director Chairman

Acc. Ahmed Abd Elraouf Mr.Adel Al-Alfi Eng.Mohamed Tarek Zakaria

Auditors' report "Attached"

- 2 -

Translation From Arabic

The financial The financialNote no. year from year from

1/1/2016 to 1/1/2015 to 31/12/2016 31/12/2015

L.E. L.E.

Net Sales 2 653 065 777 2 265 087 581

Cost of Sales ( 2 036 777 551) ( 1 669 793 535)

Gross profit 616 288 226 595 294 046

Other operating revenues (5) 104 069 897 110 759 929Selling & Distribution expenses (174 920 065) (137 794 506)General & Administrative expenses (6) (110 010 045) (101 679 920)Other operating expenses (7) (138 790 571) (62 999 776)Board of Directors remunerations ( 144 000) ( 144 000)Operating income 296 493 442 403 435 773

Revenue from investments available for sale - 5 410 523

Revenue from the sale of investments available for sale 7 830 066 -

The group's share in the net profit of associate companies (17) 7 979 419 13 035 316

Finance income & cost (9) 30 810 972 (60 358 136)

Net profit for the year before income tax 343 113 899 361 523 476

Income tax (79 683 910) (71 606 932)Prior year tax adjustment 2 666 844 839 174Deferred tax (1-26) (2 740 436) 11 675 377Net profit after income tax 263 356 397 302 431 095

Distributed as follows:

Parent company's share in profit 260 484 431 298 739 303

Non controlling interest share in profit 2 871 966 3 691 792263 356 397 302 431 095

Notes in pages from (6) to (43) form an integral part of the consolidated financial statements.

For the financial year ended 31 December 2016

Cairo Poultry Company(An Egyptian Joint Stock Company)Consolidated income Statement

- 3 -

Translation from arabic

The financial The financial

year from year from 1/1/2016 to 1/1/2015 to 31/12/2016 31/12/2015

L.E. L.E.

Net profit for the year 263 356 397 302 431 095Other comprehensive income

Investment avaliable to sale (2 846 685) (33 179 185)Other comprehensive income for the year 260 509 712 269 251 910Distributed as followsParent Company's share in profit 257 637 746 265 560 118Minority interest 2 871 966 3 691 792

260 509 712 269 251 910Notes in pages from (6) to (43) form an integral part of the consolidated financial statements.

Cairo Poultry Company(An Egyptian Joint Stock Company)Consolidated statement of comprehensive income For the financial year ended 31 December 2016

-4-

Translation From ArabicCairo Poultry CompanyJoint Stock CompanyConsolidated statements of changes in shareholders' equityFor the year ended 31 December 2016

Parent company's share in profits

Share Re-evaluation Retained of treasury Net Profit for Minority Total

capital reserves surplus earnings stocks sale the year interest

L.E. L.E. L.E. L.E. L.E. L.E. L.E. L.E. L.E. L.E.

Balance as at 1/1/2015 348 364 800 144 891 780 36 025 870 46 820 572 281 344 034 196 446 168 445 858 1 026 089 360 11 455 691 1 037 545 051Close 2014 profit in retained earnings - - - - 168 445 858 - ( 168 445 858) - - -Transferred to reserves - 8 694 107 - - ( 8 777 646) - - ( 83 539) 83 539 -Dividends for the year 2014 - - - - ( 174 182 380) - - ( 174 182 380) ( 1 152 303) ( 175 334 683)

Dividends for employee and management director for the year 2014 - - - - ( 67 967 995) - - ( 67 967 995) - ( 67 967 995)

tax on divdiends ( 6 985 571) ( 6 985 571) ( 6 985 571)Evaluation differences from investment in related parties ( 7 135 530) - ( 7 135 530) - ( 7 135 530)

Minority interest - - - - 429 479 - - 429 479 ( 429 479) -Adjustment 143 059 143 059 143 059

Other comprehensive income for the year ended 31 December 2016 - - (33 179 185) - - - 298 739 303 265 560 118 3 691 792 269 251 910

348 364 800 153 585 887 2 846 685 39 685 042 192 448 838 196 446 298 739 303 1 035 867 001 13 649 240 1 049 516 241

Periodic dividends during 2015

Transferred to reserves - 3 063 758 - - (3 063 758) - -

Dividends for employee and management director for the year 2015 - - - - (18 964 258) (18 964 258) - ( 18 964 258)

Tax on divdiends (6 248 769) (6 248 769) - ( 6 248 769)Balance as at 31/12/2015 348 364 800 156 649 645 2 846 685 39 685 042 192 448 838 196 446 270 462 518 1 010 653 974 13 649 240 1 024 303 214

Balance as at 1/1/2016 348 364 800 156 649 645 2 846 685 39 685 042 192 448 838 196 446 270 462 518 1 010 653 974 13 649 240 1 024 303 214

Close 2015 profit in retained earnings - - - - 270 462 518 - ( 270 462 518) - - -

Transferred to reserves - 6 518 192 - - ( 6 686 648) - - ( 168 456) 168 456 -

Amount held from retained earnings 34 836 480 - ( 34 836 480) - - - -

Dividends for the year 2015 - - - - ( 176 607 392) - - ( 176 607 392) ( 2 424 991) ( 179 032 383)

Dividends for employee and management director for the year 2015 - - - - ( 62 461 051) - - ( 62 461 051) - ( 62 461 051)

tax on divdiends ( 5 032 521) ( 5 032 521) ( 5 032 521)

Minority interest - - - - 747 068 - - 747 068 ( 747 068) -

Adjustment - - - - 26 554 - - 26 554 - 26 554

Other comprehensive income for the year ended 31 December 2016 - - ( 2 846 685) - - - 260 484 431 257 637 746 2 871 966 260 509 712

383 201 280 163 167 837 - 39 685 042 178 060 886 196 446 260 484 431 1 024 795 922 13 517 603 1 038 313 525

Periodic dividends during 2016

Transferred to reserves - 1 539 858 - - - - ( 1 540 508) ( 650) 650 -

Dividends for employee and management director for the year 2016 - - - - - - ( 17 024 064) ( 17 024 064) - ( 17 024 064)

Tax on dividends - - - - - - ( 4 488 168) ( 4 488 168) - ( 4 488 168)

Balance as at 31/12/2016 383 201 280 163 167 837 - 39 685 042 178 060 886 196 446 260 484 431 1 024 795 922 13 517 603 1 016 801 293Notes in pages from (6) to (43) form an integral part of the consolidated financial statements.

Total equity attributable to the

shareholders of the parent company

Special reserves evaluation

differences of available for

sale investments

- 5 -

Translation From Arabic

Financial year Financial year

From 1/1/2016 From 1/1/2015Note Till 31/12/2016 Till 31/12/2015 No. L.E. L.E.

Cash Flows from Operating Activities Net profit for the year 343 113 899 361 523 476Adjustments from operating activities:Depreciation of fixed assets (12) 72 710 017 70 334 519Capital loss( gain ) ( 2 230 671) ( 367 235)Amortization of breeders (13) 148 947 983 128 067 443 Profits from sale of breeders ( 35 875 213) (30 878 397) Impairment in breeders 7 790 692 39 243 Reverse in breeders impairment ( 2 584 517) (10 455 361) Depreciation of plant wealth 85 644 184 536Loss from sale of plant wealth 8 916 97 114 Impairment in plant wealth - 39 241Impairment in projects under costructions - 4 183 242 Reverse in plant wealth impairment ( 81 045) - Investments impairment 1 762 - Revenue from the sale of investments ( 7 830 066) - Revenue from the sale of assets avaialable for sale ( 3 532 140) - Loss in ivestment liquidation 10 000 16 077 The group's share in the net profits of associates companies ( 7 979 419) (13 035 316) Impairment in inventories - formed 990 763 636 007 Reverse the impairment in inventories ( 1 554 795) ( 212 414) Impairment in trade receivables - formed 12 478 192 10 410 086 Reverse the impairment in trade receivables ( 6 147 071) (4 263 663) Impairment in other debit balances - formed 180 609 994 805 Reverse the impairment in other debit balances ( 201 347) ( 32 438) Provision of claims - formed (23) 105 897 671 34 462 739 Provision of claims- no longer required ( 1 342 463) (23 807 384) Investments revenue - (5 410 523) Credit interests ( accured basis ) (9) ( 3 054 274) ( 346 047) Finance interests & expense ( accured basis ) (9) 100 761 506 61 050 946

720 564 633 583 230 696Changes in working capitalChange in inventories ( 163 258 715) ( 64 642 429)Change in biological assets ( 21 412 519) ( 8 971 744)Change in trade receivables & other debit balances ( 73 467 010) ( 68 832 237)Change in trade payables & other credit balances ( 169 915 121) ( 76 055 096)Change in due from related parties ( 29 204 011) 25 232 270Change in due to related parties ( 1 345 730) 3 941 769Provisions for contengencies - used ( 6 837 445) ( 1 595 858)Financial interests paid ( 97 668 747) ( 62 713 572)Net cash flows generated from operating activities 157 455 335 329 593 799 Cash Flows From Investing ActivitiesProceeds from sale of fixed assets 4 531 193 2 207 347Payments for acquisition of fixed assets & projects under construc ( 114 676 684) ( 40 507 671)Payments for purchase of Poultry breeders ( 183 109 846) ( 138 211 710)Cash flows from sister company's distribution 11 126 272Proceeds from sale of Poultry breeders 35 875 213 30 878 397Proceeds from sale of investment 110 522 098 -Collected revenue from investments - 5 410 523Proceeds from sale of assets available for sale 2 500 000 -Liquidation of investments - 45 798Collected interests (cash basis) 3 054 274 346 047Net cash flow used in investing activities (130 177 480) (139 831 269) Cash Flows From Financing ActivitiesChange in banks - credit facilities 248 448 441 85 872 505Change in loans ( 35 472 953) ( 26 831 956)Cash dividends paid for shareholders ( 179 032 383) ( 175 334 703)Net cash flows used in financing activities 33 943 105 (116 294 154) Net change in cash & cash equivalents during the year 61 220 960 73 468 396 Cash and cash equivalents at 1 January 76 202 633 2 734 237 Cash and cash equivalents at 30 September (22) 137 423 593 76 202 633

Notes in pages from (6) to (43) form an integral part of the consolidated financial statements.

For the financial year ended 31 December 2016

Cairo Poultry company

(An Egyptian Joint Stock Company)

Consolidated Statement of cash flows

-22-

Cairo Pultry Company (SAE) Translation From ArabicNotes to consolidated financial statements for the year ended 31 December 2016

12- Property, plant and equipment Machinery & Vehicles Tools and Furniture &

Lands Buildings equipments equipments office supplies TotalL.E L.E L.E L.E L.E L.E L.E

Cost as at 1 January 2015 98 950 217 642 302 830 695 888 060 104 082 179 31 075 744 20 050 390 1 592 349 420Additions of the year - 17 692 122 24 515 834 10 566 453 2 309 719 3 595 244 58 679 372Disposals of the year - ( 1 499 097) ( 3 920 606) ( 3 814 723) ( 443 923) ( 230 510) ( 9 908 859)

cost as at 31 December 2015 98 950 217 658 495 855 716 483 288 110 833 909 32 941 540 23 415 124 1 641 119 933

Cost as at 1 January 2016 98 950 217 658 495 855 716 483 288 110 833 909 32 941 540 23 415 124 1 641 119 933Additions of the year 10 000 000 34 336 453 35 413 122 10 134 652 3 224 528 2 361 188 95 469 943Disposals of the year - ( 2 327 210) ( 12 030 445) ( 6 468 222) ( 1 601 523) ( 368 439) ( 22 795 839)Cost as at 31 December 2016 108 950 217 690 505 098 739 865 965 114 500 339 34 564 545 25 407 873 1 713 794 037

Accumulated depreciation as at 1/1/2015 - 159 506 922 384 507 431 85 308 420 24 357 099 12 986 523 666 666 395Depreciation of the year - 20 947 237 37 017 108 7 960 129 2 056 801 2 353 244 70 334 519Disposals accumulated depreciation - ( 711 602) ( 3 085 951) ( 3 778 679) ( 403 648) ( 185 979) ( 8 165 859)Accumulated depreciation as at 31/12/2015 - 179 742 557 418 438 588 89 489 870 26 010 252 - 15 153 788 728 835 055

Accumulated depreciation as at 1/1/2016 - 179 742 557 418 438 588 89 489 870 26 010 252 15 153 788 728 835 055Depreciation of the year - 22 449 178 37 590 520 7 878 509 2 008 761 2 783 049 72 710 017Disposals accumulated depreciation - ( 1 271 485) ( 11 087 534) ( 6 255 381) ( 1 571 651) ( 309 266) ( 20 495 317)Accumulated depreciation as at 31/12/2016 - 200 920 250 444 941 574 91 112 998 26 447 362 17 627 571 781 049 755Net book value as at 31/12/2016 108 950 217 489 584 848 294 924 391 23 387 341 8 117 183 7 780 302 932 744 282Net book value as at 31/12/2015 98 950 217 478 753 298 298 044 700 21 344 039 6 931 288 8 261 336 912 284 878

-25-

Cairo Poultry Company (S.A.E.) Translation From ArabicNotes to the Consolidated financial statements for the year ended 31 December 201616- Other financial investments

investee Percentage Investment investmentCountry Number Participation Nominal nominal paid value value

of of purchased percentage value value as at up till as at as at establishment shares per share 31/12/2016 31/12/2016 31/12/2016 31/12/2015

% L.E. L.E. % L.E. L.E.

A - Investments of Cairo poultry Company (The parent company)

* Cairo Feed Ingredients Trading Egypt 42 000 84 100 4 200 000 25 1 050 000 1 050 000

** Cairo Reyer Breeding Company Egypt 6 000 60 100 600 000 100 600 000 600 000

Less:

Impairment in investment value - (1 200 000) (1 200 000)

Total 4 800 000 450 000 450 000

B - Investments of Cairo Misr poultry grand parent( subsidiary)

* Cairo Feed Ingredients Trading Egypt 500 5 100 50 000 25 12 500 12 500

Wadi Al -Natron for Agricultural Development Egypt 50 1 100 5 000 25 1 250 1 250

Wadi Al - Natron for land reclamation Egypt 50 1 100 5 000 25 1 250 1 250

Cairo company for land reclamation Egypt 50 1 100 5 000 25 1 250 1 250

Cairo Company for Agricultural Development Egypt 50 1 100 5 000 25 1 250 1 250

Al - Frafra for Agricultural development Egypt 50 1 100 5 000 25 1 250 1 250

Less:

Impairment in investment value - ( 13 381) ( 12 500)

Total 75 000 5 369 6 250

C- Investments of New Cairo Poultry company (Subsidiary)

** Cairo Reyer Breeding Company Egypt 2 000 20 100 200 000 100 200 000 200 000

Wadi Al - Natron for land reclamation Egypt 50 1 100 5 000 25 1 250 1 250

Wadi Al -Natron for Agricultural Development Egypt 50 1 100 5 000 25 1 250 1 250

Cairo company for land reclamation Egypt 50 1 100 5 000 25 1 250 1 250

Cairo Company for Agricultural Development Egypt 50 1 100 5 000 25 1 250 1 250

Al - Frafra for Agricultural development Egypt 50 1 100 5 000 25 1 250 1 250

Less:

Impairment in investment value - ( 50 881) ( 50 000)

Total 225 000 155 369 156 250

D- Investments of Cairo Poultry processing (subsidiary)

Cairo Trading & Importing Company Egypt 5 100 51 100 510 000 25 127 500 127 500

Less:

Impairment in investment value - ( 127 500) ( 127 500)

Total 510 000 - -

E- Investments of Cairo Broilers Company (subsidiary)

** Cairo Reyer Breeding Company Egypt 2000 20 100 200 000 100 200 000 200 000

Less:

Impairment in investment value ( 50 000) ( 50 000)

Total 200 000 150 000 150 000

G- Investments of Wadi Al Natron for Parent Company(subsidiary)

Cairo Feed Ingredients Trading Egypt 7450 14.9 100 745 000 25 186 250 186 250

Less:

Impairment in investment value ( 186 250) ( 186 250)

Total 745 000 - -

Balance as at 31/12/2016 760 738 762 500

*

** Cairo Reyer Breeding Company has been under liquidation according to the general assembly on 23 January 2010

Cairo Feed Ingredients Trading company is temperorly inactive according to board of director desicion dated 21 February 2007.

-26-

Cairo Poultry Company (S.A.E.) Translation From ArabicNotes to the consolidated financial statements for the year ended 31 December 2016

17- Investements in associates

investee Percentage Description Country Number Participation Nominal nominal paid

of of purchased percentage value value as at up till as at as at establishment shares per share 31/12/2016 31/12/2016 31/12/2015

% L.E. L.E. % L.E. L.E.Egyptation Company for Starch & Glucose industry Egypt 14 501 321 28.91 8.3 120 360 964 100 130 221 767 135 887 946Total value of investment in associates at 31 December 2016 130 221 767 135 887 946

17-1 A brief of financial statements of Egyptation Company for Starch Group share

Participation Gain for in associatepercentage Non current Current Total Current Long term Total consolidated companies'

% assets assets assets liabilities liabilities liabilities Revenues Expenses year net profit

Direct participation (27.27%),Indirect participation (1.64%) 28.91 548 260 339 264 076 089 812 336 428 275 846 349 536 490 079 812 336 428 655 294 496 ( 627 694 286) 27 600 210 7 979 419

The value of investement according to equity method

-27-

Cairo Poultry Company (S.A.E.) Translation From ArabicNotes to the consolidated financial statements for the year ended 31 December 2016

18 Other investments

18-1 Available-for-sale investments 31/12/2016 31/12/2015L.E. L.E.

First: quoted investments (with active market)

Abou Dhabi Islamic Bank - 479 797

*Egyptian Kuwaiti Holding - 103 939 920

Second: unquoted investments (with inactive market)

The cooperative Productive society for the owners of fodder factoroies in Kalyoubia

- 10 000

Middle east for Nile Transportation - 1 119 000

- 105 548 717

*

*

*

**

Investment in Egyptian Kuwaiti Holding is sold according to the ordinary general assembly decision to sell the shares on February 27,2016 & 25 528 028 shares are sold by 0.48 dollar per share with net realizable value 12 253 453 dollar equal to 108 809 441 L.E

Investments in Middle east for Nile transportation 187 500 shares is sold by 0.8175 dollar per share with net realizable value 153 281 dollar equal to 1 361 122 L.E

Investments in Abu Dhabi Islamic Bank 95 768 shares is sold by 3.67 L.E per share with net realizable value 351 469 L.E

This investment is liquidated in 31 march 2016

-37-

32 Related parties transaction

Name of the Company Nature of transactions Volume of transactions Balance as at

31/12/2016Balance as at

31/12/2015

L.E. L.E. L.E.

32-1 Due from Related Parties

Americana Kuwait Meet sector Frozen chicken sales 37 961 445 14 292 378 6 078 244

Americana Egypt for Stores & Cool Stores Materials Purchases 4 679 41 094 18 183

Security service 203 047Cairo feed ingredients trading Payment of expenses on

behalf of the company - 523 274 722 914

Egyptian Company for touristic projects Chicken sales 299 959 714 31 533 219 33 285 737Purchases & services 927 190

Security service 2 167 506Americana group for food and beverages Security service 272 061 82 265 24 006Beafy Chicken sales 2 847 320 510 020 82 890International For Food Industries Current -payment of exprnses - - 2 995

Egyptian International For Food Industries Chicken sales 413 194 37 299 -

Egyptation Company for Starch & Gluco Egyptation Com Materials Purchases 36 248 525 22 199 791 -Security service 294 527 Chicken sales 53 029

Less: Impairment of Cairo feed ingredients trading balance ( 523 274) ( 722 914) 68 696 066 39 492 055

Nature of transactions Volume of transactions

during the yearBalance as at

31/12/2016Balance as at

31/12/2015

32-2 Due to Related Parties L.E. L.E. L.E.

Cairo Reyer Breeding Company Current account - 740 906 740 906

The Egyptian Company for Starch & Glucose Materials Purchases - - 2 997 721

Security service Chicken sales

New Cairo Trading & Importing Company Current -payment of exprnses - 366 366

Green Land Purchases 647 555 74 425 44 092

Security Services 398 697

Kuwaiti Company for Food-kuwaiti Current account - 1 888 653 519 180

Kuwaiti Company for Food-emirates Current account - 5 881 -

Chicken sales 260 792 1 474 427 1 124 115

Security Services 635 899 - -

Purchases 8 750 294 - -

Arab Company for cold stores & transporting rent 858 650 - 200

International for agriculture manufacturing purchases 169 572 - 104 475

Security Services 1 672 254 - -

International for food industries Current account - 667 -

4 185 325 5 531 055

The related parties are represented in the shareholders of the Company and the Companies in which they directly own shares on it, which gives them a significant influences or great control over these companies.

The following presents a brief summary of important transactions made between the Company and its related parties during the year:

Cairo Poultry Company (S. A.E.)Notes to the consolidated financial statement for the year ended December 31, 2016

Farm Frites Company

-20-

Cairo Poultry Company (S. A.E.)Notes to the consolidated financial statements for the year ended 31 December 201611- Segmentation reports

The segmentation reports was prepared on activity segments basis, the primary report for the activity segments was prepared in accordance with organizational and managerial chart of the company and its subsidiaries.Activities segmentations results include a direct participation unit in each sector activity.The primary report for activity segmentations:11-1 Segmentation reports for the year ended 31 December 2016

Fodder Fatting Incubation Processing Grands Security Agriculture

Sector Sector Sector Sector Sector Sector Sector Total

L.E L.E L.E L.E L.E L.E L.E L.E L.E L.E31/12/2016 31/12/2016 31/12/2016 31/12/2016 31/12/2016 31/12/2016 31/12/2016 31/12/2016 31/12/2016 31/12/2016

Sales 1 543 257 757 958 004 529 719 800 358 1 566 336 174 137 644 604 28 825 835 5 105 000 - ( 2 305 908 480) 2 653 065 777Sales between segments 640 374 826 696 005 742 552 599 208 366 318 483 38 584 371 12 025 850 - - ( 2 305 908 480) -

Net sales 902 882 931 261 998 787 167 201 150 1 200 017 691 99 060 233 16 799 985 5 105 000 - - 2 653 065 777

Segments' gross profit 323 513 132 52 304 935 68 338 535 133 901 957 31 004 219 4 530 399 2 695 049 - - 616 288 226Other revenues 4 718 287 5 074 323 42 476 921 21 666 408 17 607 620 72 615 207 467 12 246 256 - 104 069 897Distribution & sales expenses ( 46 521 325) ( 180 115) - ( 121 611 055) ( 6 607 570) - - - - ( 174 920 065)General & administrative expenses ( 21 773 832) ( 12 484 002) ( 2 865 882) ( 27 496 104) ( 2 872 240) ( 2 432 292) ( 5 555) ( 40 080 138) - ( 110 010 045)Other expenses ( 57 919 001) ( 5 903 226) ( 15 783 031) ( 30 491 327) ( 8 975 679) ( 350 000) - ( 19 368 307) - ( 138 790 571)Board of Directors remunerations - - - - - - - ( 144 000) - ( 144 000)

Profits results from operation 202 017 261 38 811 915 92 166 543 ( 24 030 121) 30 156 350 1 820 722 2 896 961 ( 47 346 189) - 296 493 442

Revenue From the sale of investment available for sa - - - - - - - 7 830 066 - 7 830 066

The group's share in the net profit of associate compani - - - - - - - 7 979 419 - 7 979 419

Finance expenses & interests 8 988 763 ( 10 747 919) ( 6 425 435) ( 2 630 451) ( 2 847 633) 76 965 ( 93 666) 44 490 348 - 30 810 972

Net profit for the year before income tax 211 006 024 28 063 996 85 741 108 ( 26 660 572) 27 308 717 1 897 687 2 803 295 12 953 644 - 343 113 899Income tax ( 29 567 955) ( 7 563 000) ( 10 260 093) ( 389 982) ( 6 593 176) ( 525 242) ( 629 081) ( 24 155 381) - ( 79 683 910)Difference tax 1 828 263 87 926 39 438 383 913 82 374 - 9 731 235 199 - 2 666 844Deffered tax ( 2 414 082) ( 547 173) 89 952 1 333 380 ( 885 305) 3 792 ( 971) ( 320 029) - ( 2 740 436)Net profit for the year after income tax 180 852 250 20 041 749 75 610 405 ( 25 333 261) 19 912 610 1 376 237 2 182 974 ( 11 286 567) - 263 356 397

Other Informations

Depreciation 12 575 103 13 043 753 14 330 145 29 305 557 3 124 455 186 313 144 691 - - 72 710 017Assets 809 908 962 439 212 538 371 136 337 588 932 381 109 710 398 7 020 883 9 348 406 - - 2 335 269 905Liabilities 680 819 345 203 799 264 346 284 726 32 650 137 47 629 299 3 848 985 3 436 856 - - 1 318 468 612

Activity Segments

Undistributable items

Elemenation of Consolidated transactions

-19-

Cairo Poultry Company (S. A.E.)Notes to the consolidated financial statements for the year ended 31 December 2015

11- Segmentation reports

The segmentation reports was prepared on activity segments basis, the primary report for the activity segments was prepared in accordance with organizational and managerial chart of the company and its subsidiaries.Activities segmentations results include a direct participation unit in each sector activity.The primary report for activity segmentations:

11-2 Segmentation reports for the period ended 31 December 2015

Fodder Fatting Incubation Processing Grands Security Agriculture

Sector Sector Sector Sector Sector Sector Sector Total

L.E L.E L.E L.E L.E L.E L.E L.E L.E L.E31/12/2015 31/12/2015 31/12/2015 31/12/2015 31/12/2015 31/12/2015 31/12/2015 31/12/2015 31/12/2015 31/12/2015

Sales 1 182 671 934 819 183 695 617 734 595 1 430 612 857 117 184 869 26 504 164 3 375 372 - ( 1 932 179 905) 2 265 087 581

Sales between segments 500 315 568 610 128 199 454 609 154 318 515 999 37 609 490 11 001 495 - - ( 1 932 179 905) -

Net sales 682 356 366 209 055 496 163 125 441 1 112 096 858 79 575 379 15 502 669 3 375 372 - - 2 265 087 581

Segments' gross profit 250 254 316 82 959 130 67 268 649 163 077 177 27 737 317 3 903 856 93 601 - 595 294 046

Other operating revenues 25 688 470 9 004 218 45 115 710 7 663 898 10 019 186 41 832 131 499 13 095 116 - 110 759 929

Distribution & sales expenses ( 25 323 948) ( 120 000) - ( 107 550 422) ( 4 800 136) - - - - ( 137 794 506)

General & administrative expense ( 19 961 866) ( 11 117 454) ( 2 134 466) ( 24 019 148) ( 2 467 869) ( 2 228 157) - ( 39 750 960) - ( 101 679 920)

Other operating expenses ( 7 179 934) ( 19 910 430) ( 12 987 956) ( 12 689 220) ( 6 885 986) ( 300 000) ( 134 958) ( 2 911 292) - ( 62 999 776)

Board of Directors remunerations - - - - - - ( 144 000) - ( 144 000)

Profits results from operation 223 477 038 60 815 464 97 261 937 26 482 285 23 602 512 1 417 531 90 142 ( 29 711 136) - 403 435 773

Revenue of available for sale investments - - - - - - - 5 410 523 - 5 410 523

The group's share in the net profit of associate companies - - - - - - - 13 035 316 - 13 035 316

Finance expenses & interests ( 19 557 767) ( 9 280 324) ( 6 926 505) ( 14 400 642) ( 3 405 521) 69 861 ( 86 794) ( 6 770 444) - ( 60 358 136)

Net profit for the period before income tax 203 919 271 51 535 140 90 335 432 12 081 643 20 196 991 1 487 392 3 348 ( 18 035 741) - 361 523 476

Income tax provision ( 32 609 408) ( 13 669 875) ( 11 196 963) ( 5 184 841) ( 3 560 012) ( 472 244) ( 244 547) ( 4 669 042) - ( 71 606 932)

Difference tax 592 690 - - 246 484 - - - - - 839 174

Deferred tax 1 354 890 1 935 726 4 251 154 4 438 513 ( 778 236) 18 777 23 400 431 153 - 11 675 377

Net profit for the period after income tax 173 257 443 39 800 991 83 389 623 11 581 799 15 858 743 1 033 925 ( 217 799) ( 22 273 630) - 302 431 095

Other Informations

Depreciation 12 557 641 27 997 795 13 713 642 2 378 173 13 279 850 248,675 158,743 - - 70 334 519

Assets 638 171 117 591 905 778 331 279 531 73 437 604 399 803 585 5 988 504 8 748 211 - - 2 049 334 330

Liabilities 417 328 908 308 428 867 98 386 023 43 711 928 150 555 879 3 641 314 2 978 197 - - 1 025 031 116

Activity Segments

Undistributed items

Elimination of Consolidated transactions

- 6 -

Cairo Poultry Company (An Egyptian Joint Stock Company) Notes to the consolidated financial statements for the year ended 31 December 2016

1. Company’s and subsidiaries’ background

Cairo Poultry Company – An Egyptian Joint Stock Company – was established in year 1977 - Company location: 32(B) Murad st – Giza – Egypt. Chairman of the board Prof. Dr. / Mamdouh Abdel Wahab Sharf EL Dien, according to the provisions of Investment Law No. 230 of 1989.which was replaced by the Investment Incentives and Guarantees Law No. 8 of 1997 The Company was registered under the commercial register on 26/7/1977 under No. 42444, The Company’s life was extended to be 25 Years starting from 19/7/2002. The Company is a subsidiary to the Kuwait Company for the food (Kuwait joint stock Company).

The Company’s purpose The Company’s objective is represented in: - Production and breeding and fattening chickens and produce animal feed and mix

preliminary ingredients and production of hatching eggs from parent. - Production of hatching eggs produced by parent. - Production of chicks from hatching eggs. - Production of broilers (breeding chicks). - Establishment of cooling rooms to serve the purposes of the Company - Production of eggs from breeding chicken egg. - The establishment and operation of feed mills to produce all kinds of feeds and its

concentrates of the animal, poultry, fish and non-conventional feed. - Establishment of automated slaughterhouse for poultry. - Manufacturing residues of slaughterhouse. - Conduct export of the Company's products. - Conduct import for Company’s purposes. - Open branches and granting agencies for selling the Company's products in all over the

Arab Republic of Egypt. - Trade in all products and requirements of the Company's production. - Participating in similar projects domestically and overseas. Registration in the Stock Exchange The Company is listed in the Egyptian Stock Exchanges.

2. Basis of preparation 2-1 Statement of compliance

The consolidated financial statements have been prepared in accordance with Egyptian Accounting Standards (“EAS”), and incompliance with applicable Egyptian laws and regulations. The consolidated financial statements were approved by the Company’s Board of Directors in its meeting held on 22/1/2017 for issuance.

2-2 Basis of measurement

The consolidated financial statements have been prepared on the historical cost basis except for the following items of assets & liabilities which are stated by its fair value: • financial instruments at fair value through profit or loss are measured at fair value • Semi-Finished production ( Chicks at the fatten station) • Semi-Finished production (eggs in incubation labs) • Other financial investment • Forward exchange contracts The methods used to measure fair values are discussed further in( note 4).

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

7

2-3 Functional and presentation currency

These consolidated financial statements are presented in Egyptian pound, which is the Company’s and its subsidiaries functional currency.

2-4 Use of estimates and judgments

The preparation of financial statements in conformity with Egyptian Accounting Standards requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the year in which the estimate is revised and in any future periods affected. Information about critical judgments in applying accounting policies that have the most significant effect on the amounts recognised in the financial statements is included in the following notes: Note (3-1) : Business combination Note (3-6) : Breeding wealth Note (3-17): lease classification Information about uncertainties assumptions and estimation that have a significant risk of resulting in a material adjustment within the next financial year are included in the following: • Note (12) : Property, plant and equipment. • Note (19) : Inventory impairment. • Note (21-1): Trade receivables and other debit balances impairment. • Note (23،29): Provisions and Contingent liabilities. • Note (26-1): Deferred tax.

3. Significant accounting policies The accounting policies set out below have been applied consistently to all periods presented in these consolidated financial statements.

3-1 Basis of consolidation

Subsidiary companies Subsidiaries are those enterprises controlled by the Company. Control exists when the Company has the power, to govern the financial and operating policies of an enterprise so as to obtain benefits from its activities. And when evaluating this power we have to take in consideration the present and possible voting rights in the consolidated financial statements’ date. And the subsidiaries’ financial statements will be consolidated in the consolidated financial statements from the acquisition date till the holding company loses its power. Associates Associates are those entities in which the Group has significant influence, but not control, over the financial and operating policies. Associates are accounted for using the equity method. The consolidated financial statements include the Group’s share of the income and expenses of equity accounted investees, after adjustments to align the accounting policies with those of the Group, from the date that significant influence or joint control commences until the date that significant influence or joint control ceases. When the Group’s share of losses exceeds its interest in an equity accounted investee, the carrying amount of that interest (including any long-term investments) is reduced to nil and the recognition of further losses is discontinued except to the extent that the Group has an obligation or has made payments on behalf of the investee.

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

8

Transactions eliminated on consolidation Intra-group balances, and any unrealized income and expenses arising from intra-group transactions, are eliminated in preparing the consolidated financial statements. Unrealized gains arising from transactions with equity accounted investees are eliminated against the investment to the extent of the Group’s interest in the investee. Unrealized losses are eliminated in the same way as unrealized gains, but only to the extent that there is no evidence of impairment.

3-2 Foreign currency Foreign currency transactions Transactions in foreign currencies (other than functional and presentation currency the Egyptian Pound) are translated to the functional currency at exchange rates at the dates of the transactions. Monetary assets and liabilities denominated in foreign currencies at the reporting date are retranslated to the functional currency at the exchange rate at that date. Non-monetary assets and liabilities denominated in foreign currencies that are measured at fair value are retranslated to the functional currency at the exchange rate at the date that the fair value was determined. Foreign currency differences arising on retranslation are recognised in profit or loss except for differences resulted from translation of available for sale investments which is to be recognized directly in shareholders’ equity. Non-monetary items in a foreign currency that are measured in terms of historical cost are translated using the exchange rate at the date of the transaction.

3-3 Financial instruments Non-derivative financial assets The Company initially recognises loans and receivables and deposits on the date that they are originated. All other financial assets (including assets designated at fair value through profit or loss) are recognised initially on the trade date, which is date that the Company becomes a party to the contractual provisions of the instrument.

The Company derecognises a financial asset when the contractual rights to the cash flows from the asset expire, or it transfers the rights to receive the contractual cash flows on the financial asset in a transaction in which substantially all the risks and rewards of ownership of the financial asset are transferred. Any interest in transferred financial assets that is created or retained by the Company is recognised as a separate asset or liability. Financial assets and liabilities are offset and the net amount presented in the balance sheet when, and only when, the Company has a legal right to offset the amounts and intends either to settle on a net basis or to realise the asset and settle the liability simultaneously. The Company classifies non – derivative financial assets into the following categories: financial assets at fair value through profit or loss, held-to-maturity financial assets, loans and receivables and available-for sale financial assets.

Other non-trade financial instruments When derivative financial instrument are not classified in ineligible hedging then all changes in its fair value stated through profit and loss

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

9

Financial assets at fair value through profit or loss A financial asset is classified at fair value through profit or loss if it is classified as held for trading or is designated as such upon initial recognition. Financial assets are designated at fair value through profit or loss if the Company manages such investments and makes purchase and sale decisions based on their fair value in accordance with the Company’s documented risk management or investment strategy. Attributable transaction costs are recognized in profit or loss as incurred. Financial assets at fair value through profit or loss are measured at fair value, and changes therein are recognized in profit or loss. Financial assets designated at fair value through profit or loss comprise equity securities that have been classified as available for sale.

Receivables Receivables are financial assets with fixed or determinable payments that are not quoted in an active market. Such assets are recognised initially at fair value plus any directly attributable transaction costs. Subsequent to initial recognition. Generally, trade and other receivables are stated at their nominal value less an allowance for any doubtful debts. Receivables comprise cash and cash equivalents, and trade and other receivables.

Cash and cash equivalents Cash and cash equivalents comprise cash balances and call deposits of three months or less from the acquisition date that are subject to an insignificant risk of changes in their fair value, and are used by the Company in the management of its short-term commitments.

Available -for - sale investments Available-for-sale financial assets are non-derivative financial assets that are designated as available-for-sale or are not classified in any of the above categories of financial assets. Available –for-sale financial assets are recognized initially at fair value plus any directly attributable transaction costs. Subsequent to initial recognition, they are measured at fair value and changes therein, other than impairment losses presented in fair value reserve in equity. When an investment is derecognised, the gain or loss accumulated in equity is reclassified to profit or loss. Available-for-sale financial assets comprise equity securities and debt securities. Non-derivative financial liabilities The company initially recognizes debt securities issued and subordinated liabilities on the date that they are originated. All other financial liabilities ( including liabilities designated at fair value through profit and loss) are recognized initially on the trade date, which is the date that the Company becomes a party to the contractual provisions of the instrument. The Company derecognises a financial liability when its contractual obligations are discharged, cancelled or expire. Financial assets and liabilities are offset and the net amount presented in the balance sheet when , and only when, the Company has a legal right to offset the amounts and intends either to settle on a net basis or to realize the asset and settle the liabilities simultaneously. The Company classifies non – derivative financial liabilities into the other financial liabilities category. Such financial liabilities are recognised initially at the fair value plus any directly attributable transaction costs. Subsequent to initial recognition, these financial liabilities are measured at amortised cost using the effective interest method.

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

10

Other financial liabilities comprise loans and borrowings , bank overdrafts, and trade and other payables. Bank overdrafts that are repayable on demand and form an integral part of the Company’s cash management are included as a component of cash and cash equivalents for the statement of cash flows. Capital Authorized capital The Company’s authorized capital amounts to L.E one Billion.

Issued and paid up capital The holding Company’s issued and paid up capital amounts to L.E 383 201 280 divided into 383 201 280 shares at par value L.E 1 each. Repurchase, disposal and reissue of share capital (treasury shares) When share capital recognised as equity is repurchased, the amount of the consideration paid, which includes directly attributable costs, net of any tax effects, is recognised as a deduction from equity. Repurchased shares are classified as treasury shares and are presented in the reserve for own shares. When treasury shares are sold or reissued subsequently, the amount received is recognised as an increase in equity, and the resulting surplus or deficit on the transaction is presented in share premium. Any profit or loss from selling or purchasing or issuing these equity instruments should not be recognaised in profit or loss.

3-4 Property, plant and equipment A- Recognition and measurement

Items of property, plant and equipment are measured at cost less accumulated depreciation and accumulated impairment losses (note: 12).

Cost includes expenditures that are directly attributable to the acquisition of the asset. The cost of self-constructed assets includes the cost of materials and direct labor, any other costs directly attributable to bringing the asset to a working condition for their intended use, and the costs of dismantling and removing the items and restoring the site on which they are located. and capitalised borrowing costs.

Purchased software that is integral to the functionality of the related equipment is capitalized as part of that equipment . the cost of borrowing for the acquisition, construction or production of assets included in the income statement when incurred When parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate items.

The gain and loss on disposal of an item of property, plant and equipment is determined by comparing the proceeds from disposal with the carrying amount of property, plant and equipment, and is recognized net within other income/other expenses in profit or loss.

B- Subsequent costs

The cost of replacing part of an item of property, plant and equipment is recognised in the carrying amount of the item if it is probable that the future economic benefits embodied within the part will flow to the Company and its cost can be measured reliably. The carrying amount of the replaced part is derecognized. The costs of the day-to-day servicing of property, plant and equipment are recognized in profit or loss as incurred.

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

11

C- Depreciation

Depreciation is recognized in profit or loss on a straight-line basis over the estimated useful lives of each part of an item of property, plant and equipment. Land is not depreciated. The estimated useful lives for the current and comparative periods are as follows:

Description Estimated useful Lives (Years) Buildings & Constructions 10 - 40 Machinery and equipments 7 - 14 Motor Vehicles & Transportation means 5 Tools & Equipments 5 Furniture and office equipment 3-8

Depreciation commences when the fixed asset is completed and made available for use. Depreciation methods, useful lives and residual values are reviewed at each reporting date and adjusted if appropriate.

3-5 Grants Granted assets gained by group companies from grantee are recorded after deduction the cost of purchasing till reaches the book value for the assets, the grants are recorded as revenue at consolidated income statement during the estimated life time for the asset with reducing the annual depreciation burden.

3-6 Breeders The grand Parent and parents Poultry are recorded at cost after deducting accumulated amortization for every station which consists of the cost of purchasing chicks (parent chicks) aged one day in addition to all expenses during the breeding of parents and grand parents before parents and grand parents started producing hatching eggs for each station of grand parents and parents breeding expenses for each station is calculated based on estimated production period for grand parents and parents at the station and the expected production (hatching egg production). The disposal of parents and grand parents is recognized at the liquidation of the herd.

3-7 Projects under construction

Expenditures incurred on purchasing and constructing fixed assts are initially recorded in projects under construction until the asset is completed and becomes ready for use. Upon the completion of the assets, all related costs are transferred to fixed assets. Projects under construction are measured at cost less accumulated impairment losses (note: 15). No depreciation is charged until the project is completed and transferred to fixed assets.

3-8 Plant life stock All the expenditures of planting olive trees that have been capitalized as fixed assets in the balance sheet under the plant life stock item after reaching the marginal production, and to be depreciated on 50 years according to its nature taking the value of accumulated impairment losses into consideration.

3-9 Goodwill Goodwill is initially measured at its cost , being the excess of the cost of the business combination over the Group’s interest in the net fair value of identifiable assets, liabilities and contingent liabilities. After initial recognition, the group measures acquired goodwill at cost less impairment losses. Recognized goodwill impairment losses are not subsequently reversed.

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

12

3-10 Leases

Leases are classified as operating leases. The costs in respect of operating leases are charged on a straight-line basis over the lease term (after deducting any discounts and rent-free periods effect). The accrued value from lease incentive received to take on an operating lease is recognised as income.

3-11 Inventories Inventories of raw materials, packing materials and spare parts are measured at the lower of cost or net realizable value.Net realizable value is the estimated selling price, in the ordinary course of business, less the estimated costs of completion and selling expenses. The cost includes any other costs directly attributable to bringing the inventory to a working condition for their intended use. The cost of inventory determined as follows: Raw materials and packing materials is determined at cost according to first in First out method. Spare parts and supplies are determined at cost according to weighted average method. The work in progress (Chicks in batteries) at fair value determined by career's specialists after deducting estimated cost of sales, the increase or decrease in fair value are recorded to income statement – on selling price basis after taking to account the current value at the date of the financial statements. Finished goods of (Fodders and frozen breeders) are measured at the lower of manufacturing cost or net realizable value. The manufacturing cost comprises raw materials, direct labor, and cost includes an appropriate share of overheads based on normal operating capacity.

3-12 Impairment Non - derivative financial assets A financial asset not classified as at fair value through profit or loss, including an interest in an equity-accounted investee, is assessed at each reporting date to determine whether there is objective evidence that it is impaired. A financial asset is impaired if there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the asset, and that the loss event (s) had an impact on the estimated future cash flows of that asset that can be estimated reliably.

Financial assets measured at amortised cost The Company considers evidence of impairment for financial assets measured at amortised cost (loans and receivables and held –to-maturity investment securities) at both a specific asset and collective level. All individually significant assets are assessed for specific impairment. Those found not to be specifically impaired are then collectively assessed for any impairment that has been incurred but not identified. Assets that are not individually significant are collectively assessed for impairment by grouping together assets with similar risk characteristics. In assessing collective impairment, the Company uses historical trends of the probability of default, the timing of recoveries and the amount of loss incurred, adjusted for management’s judgement as to whether current economic and credit conditions are such that the actual losses are likely to be greater or less than suggested by historical trends.

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

13

An impairment loss in respect of a financial asset measured at amortised cost is calculated as the difference between its carrying amount and the present value of the estimated future cash flows discounted at the asset’s original effective interest rate. Losses are recognised in profit or loss and reflected in an allowance account against loans and receivables or held – to – maturity investment securities. Interest on the impaired asset continues to be recognised. When an event occurring after the impairment was recognized causes the amount of impairment loss to decrease, the decrease in impairment loss is reversed through profit or loss. Available – for – sale financial assets Impairment losses on available-for-sale financial assets are recognised by reclassifying the loss accumulated in the fair value reserve in equity, to profit or loss. The cumulative loss that is reclassified from equity to profit or loss is the difference between the acquisition cost, net of any principal repayment and amortization, and the current fair value, less any impairment loss previously recognized in profit or loss. Changes in impairment provisions attributable to time application of the effective interest method are reflected as a component of interest income.

If, in a subsequent period, the fair value of an impaired available-for-sale debt security increases and the increase can be related objectively to an event occurring after the impairment loss was recognized in profit or loss, then the impairment loss is reversed, with the amount of the reversal recognized in profit or loss. However, any subsequent recovery in the fair value of an impaired available-for-sale equity security is recognized in equity.

Non-financial assets The carrying amounts of the Company’s non-financial assets, other than biological assets, investment property, inventories and deferred tax assets, are reviewed at each reporting date to determine whether there is any indication of impairment. If any such indication exists, then the asset’s recoverable amount is estimated. For intangible assets that have indefinite useful lives or that are not yet available for use, the recoverable amount is estimated each year at the same time. An impairment loss is recognized if the carrying amount of an asset or its related cash –generating unit (CGU) exceeds its estimated recoverable amount. The recoverable amount of an asset or CGU is the greater of its value in use and its fair value less costs to sell. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset or CGU. For the purpose of impairment testing, assets that cannot be tested individually are grouped together into the smallest group of assets that generates cash inflows from continuing use that are largely independent of the cash inflows of other assets or CGU. The Company’s corporate assets do not generate separate cash inflows and are utilized by more than one CGU. Corporate assets are allocated to CGUs on a reasonable and consistent basis and tested for impairment as part of the testing of the CGU to which the corporate asset is allocated. Impairment losses are recognised in profit or loss. An impairment loss in respect of other assets, that recognised in prior periods are assessed at each reporting date for any indications that the loss has decreased or no longer exists. An impairment loss is reversed if there has been a change in the estimates used to determine the recoverable amount. An impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortisation, if no impairment loss had been recognised.

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

14

3-13 Defined contribution plans

The Company contributes to the government social insurance system for the benefits of its employees according to the social insurance Law No. 79 of 1975 and its amendments, the Company’s contributions are recognized in income statement using the accrual basis of accounting. The company’s obligation in respect of employees’ pensions is confined to the amount of aforementioned contributions.

3-14 Private Insurance Fund

The company pays contributions to fund system services to employees for the benefit of employees of the company (the fund has an independent legal personality) and are included in the income statement in accrual basis and the company has no other obligations other than the value of the contributions mentioned above.

3-15 Provisions A provision is recognised if, as a result of a past event, the Company has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the liability.

3-16 Revenue recognition Goods sold Revenue from the sale of goods is measured at the fair value of the consideration received or receivable, and are stated net of returns, less trade discounts and quantity discount allowed by the company. Revenue is recognised when the significant risks and rewards of ownership have been transferred to the buyer. recovery of the consideration is probable, the associated costs and possible return of goods can be estimated reliably, there is no continuing management involvement with the goods, and the amount of revenue can be measured reliably. The timing of the transfers of risks and rewards varies depending on the individual terms of the contract of sale. In usually times transfer occurs when the product is received at the customer’s warehouse. No revenue is recognised in case of uncertainty to collect the receivables or its related cost or sales return or continuing management involvement with the goods.

3-17 Rental Income

Rental income from other property is recognized as other income.

3-18 Finance income and expenses Finance income comprises interest income on invested funds, dividend income, gains on the disposal of available-for-sale financial assets, fair value gains on financial assets at fair value through profit or loss.Interest income is recognised as it accrues in profit or loss, using the effective interest method. Dividend income received from investments is recognised in profit or loss when company right to this dividends arises in the financial period in which dividends are approved by the investees General assemblies . Finance cost comprise interest expense on borrowings, fair value losses on financial assets at fair value through profit or loss, impairment losses recognised on financial assets. Borrowing costs that are not directly attributable to the acquisition, construction or production of a qualifying asset are recognised in profit or loss using the effective interest method. Foreign currency gains and losses are reported on a net basis as either finance income.

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

15

3-19 Income tax Income tax on profit or loss for the year comprises current and deferred tax. Income tax is recognized in the income statement except to the extent that it relates to items recognized directly on equity, in which case it is recognized in equity. Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted or substantially enacted at the balance sheet date, and any adjustment to tax payable in respect of previous years.

3-20 Deferred tax Deferred tax providing for temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. The amount of deferred tax provided is based on the expected manner of realization or settlement of the carrying amount of assets and liabilities, using tax rates enacted or substantively enacted at the consolidated balance sheet date. A deferred tax asset is recognized only to the extent that it is probable that future taxable profits will be available against which the asset can be utilized. Deferred tax assets are reduced to the extent that it is no longer probable that the related tax benefit will be realized through incoming years.

3-21 Segmentation reports Each sector of the companies' activity segments considers as a unit that contributes in providing variant products different that the other activities (Activity segments) and each unit have risks and utilities different than the other unit exist on the company according to its activity.

4. Determination of fair value

A number of the Company’s accounting policies and disclosures require the determination of fair value, for both financial and non- financial assets and liabilities. Fair values have been determined for measurement and/or disclosure purposes based on the following methods. Where applicable, further information about the assumptions made in determining fair values is disclosed in the notes concerning that asset or liability.

4-1 Semi finished - production (Chicks in batteries)

Determined by fair value based on the opinion of the specialists in the activity, taking in consideration the change in its present value.

4-2 Semi finished - production (eggs in incubation labs) Determined by fair value based on the opinion of the specialists in the activity, taking in consideration the change in its present value.

4-3 Available for sale investments

Available for sale investments in active market is determined by fair value.

4-4 Financial instruments at fair value through profit or loss Financial instruments at fair value through profit or loss are measured at fair value and recognise the change in faire value through profit & loss.

4-5 Forward exchange contracts

The fair values of forward exchange contracts is based on fair price.

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

16

5. Other operating revenues The financial year The financial year from1/1/2016 from1/1/2015

To 31/12/2016 To 31/12/2015 L.E L.E

Export support revenue 916 400 1 1 646 484 Profit from selling Grand’s/Parents 213 875 35 30 878 397 Capital gain 864 884 3 1 800 498 Gain from sale of assets available for sale 140 532 3 - *Recovery of service duties 631 206 3 - Starch management fees 322 979 2 4 508 693 Other revenues 532 006 30 321 916 24 Dividends Macquarie company 352 904 8 238 276 General Union of Poultry Producers 689 368 10 - Provision no longer required 463 342 1 23 807 384 Reversed impairments in breeding wealth 517 584 2 10 455 361 Reversed impairments in inventory 795 554 1 212 414 Reversed impairments in plant wealth 045 81 - Reversed impairments in receivable 347 201 32 438 Reversed impairments in trade receivable 071 147 6 4 263 663

897 069 104 929 759 110

6. General and administrative expenses The financial

year The financial

year from1/1/2016 from1/1/2015 To 31/12/2016 To 31/12/2015

L.E L.E

Salaries 889 774 85 74 693 712 Depreciations 524 842 2 2 712 271 Other expenses 632 392 21 937 273 24

045 010 110 101 679 920

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

17

7. Other operating expenses

The financial year

The financial year

from1/1/2016 from1/1/2015 To 31/21/2016 To 31/12/2015 L.E L.E

Impairment in Projects under construction - 4 183 241 Impairment in breeding wealth 692 790 7 39 243 Impairment in inventory 763 990 636 007 Impairment in Trade receivables 192 478 12 10 410 086 Impairment in debtors 609 180 994 805 Capital losses 193 654 1 1 433 263 Impairment in related parties - 277 487 *End of service cost 097 739 9 - Provision for claims 671 897 105 34 462 739 Social insurance differences - 6 500 000 Loss from Investment Liquidation 000 10 16 077 Others 354 49 4 046 828

571 790 138 62 999 776 *The end of services cost for some workers that company management finalized their services during

2016, the board of directors of the holding company agreed on this decision at 22 January 2017.

** The provision for claims include amount L.E 51 480 870 for the provision of end of services for workers and that according to the decision of the board of directors forof the holding company on 22 january 2017.

8. Personnel expenses The financial year The financial year

from1/1/2016 from1/1/2015 To 31/12/2016 To 31/12/2015 L.E L.E

Wages and salaries 360 418 701 306 470 974 Compulsory social security contributions 26 356 919 25 474 380 Contributions to defined contribution plans 4 179 204 4 004 265

390 954 824 335 949 619

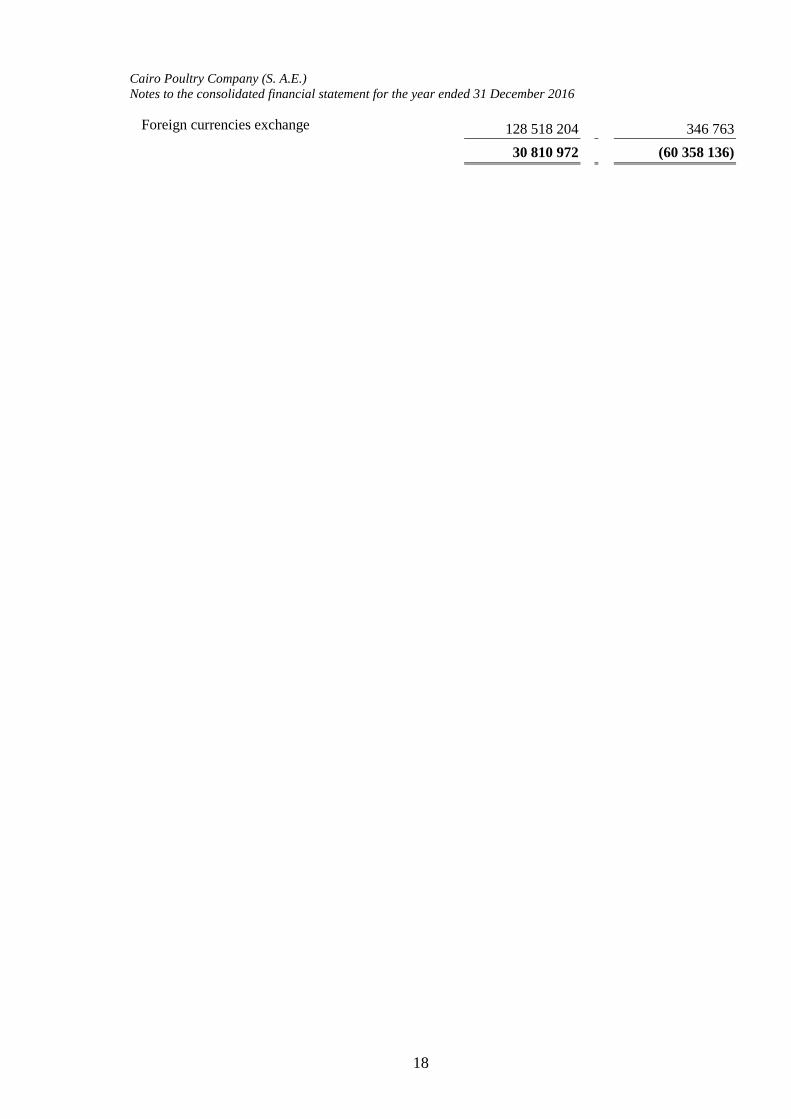

9. Finance Income & Finance Costs The financial year The financial year

from1/1/2016 from1/1/2015 To 31/12/2016 To 31/12/2015 L.E L.E

Credit interest 274 054 3 346 047 Debit interest )506 761 100 ( (61 050 946)

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

18

Foreign currencies exchange 204 518 128 346 763 972 810 30 (60 358 136)

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

19

10. Tax status 10-1 Cairo Poultry Company(Holding) 10-1-1 Corporate tax

The Company’s profits shall be subjected to corporate tax according to the provisions of Tax Law No. 187/1993 that was amended, and superseded by Law No. 91/2005. Years from 1977 till 2002 The company made final tax reconciliation with Tax Authority regarding the corporate tax and settled the due tax differences thereon. During 2013, the Tax Authority notified the company for a claim concerning adjustment of previous years from 1977 till 2002, that has been objected and the dispute has been solved and paid L.E 6.9 million the full tax differences. Years 2003/2004 Tax inspection was made& waiting for the inspection results. Years 2009/2012 Tax inspection is under proceeding for these periods Years 2013/2015 Tax inspection has not been made until this date, & the tax returns are being delivered on dates.

10-1-2 Salary tax

Years from 1988 till 2010 Tax inspection was made for the company and the tax amounts due were settlement and paid to the Tax Authority Years 2011/2015 Tax inspection has not been made until this date, & the tax returns are being delivered on dates.

10-1-3 Stamp tax

Years from 1998 till 31/12/2012 Tax inspection was made for the company and the tax amounts due were paid to the Tax Authority.

10-1-4 Value added tax The company’s activity is exempted from value added tax according to Law No. (67) for the year 2016.

10-2 Subsidiaries companies First: Companies that are subject to corporate tax. Subsidiaries Tax status New Cairo Poultry Company

Year 2007 A tax claim on the company received form no(19) income tax based on estimation inspection on taxable project for the year 2007 with amount 47 155 521. The company has appealed the assessment and dispute had been transferred to the appealed committee for this tax dispute. Incubation lab / Noubarya project/ Salehya

Inspected till 31/12/2004

Years 2009 & 2010 Tax inspection is under proceeding for these

years .

Years 2009 till 2010 A tax claim on the company receives from no.

(19) income tax based on estimation inspection on taxable projects& tax inspection will be finalized for this years.

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

20

Cairo Poultry Processing Years from 2013 to 2015

The company was inspected by the tax authority and was informed about tax claim and the company objected in legal date were referred the dipute to the internal committee, it was a solution to the dispute interior committee with a total tax liabilities of L.E 593 936.

Misr Grand Parents Co. Inspected till 31/12/2008& tax amounts due were paid Years 2009&2010 was inspected and under settlement.

Cairo Grand Parents Co Inspected till 31/12/1998& inspection in process for years 1999 to 2004.

Madina Poultry Company Inspection in process for years 2006 to 2010.

Cairo Poultry company for Broilers Inspection in process for years 2008 to 2010.

Cairo Feed Company Inspection in process for years 2010 to 2012.

Cairo Broilers Company Inspection in process for years 2009 to 2012.

Cairo Leasing Company

Not inspected yet

Cairo Misr Grand parents Company Inspection in process for years 2009 to 2013

Almadena for Poultry production Inspection in process for years 2006 to 2010

Second: Companies that are exempted from the corporate tax

Subsidiaries Date ends tax exemption New Cairo Poultry Company(Sina 2000/2 for

fatten chicks Hasbo project

2020

2020

Wadi Al Natron for Parents

Wadi Al Natron for Broilers Company(Alkadsia)

31/12/2017 22/10/2021

Fifth: Withdraws & deposits under tax account

All the Companies apply the withholding tax and pay in the due dates.

Third: Companies that are not exempted from the corporate tax Corporation Guard Services: The company has been inspected till 31/12/2009 and the tax amounts due were paid and inspection in process for years 2010&2012.

El Delta Trading & Importing: The company has not been inspected yet. Fourth: Companies have not commenced its activities (under liquidation)

Cairo Reyer Breeding Company.

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

21

11. Segmentation reports

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

22

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

23

12. Property, Plant and Equipment

Cairo Poultry Company (S. A.E.) Notes to the consolidated financial statement for the year ended 31 December 2016

24

12-1 The following represents the fixed assets items which were purchased through the group companies based on initial selling contracts at 31 December 2016 , the necessary regulatory procedures for registering and transferring its possession under the company's name are currently under progress :-

L.E. Land 76 868 566 Building& Construction 3 906 583

80 775 144 12-2 The machinery and equipment balance includes L.E. 10 934 739, representing in the cost for

acquiring a treatment line for solid wastes purposes (Cairo processing company), this amount was partially financed by the Ministry of Environment (The project of controlling the industrial pollution- financed by the World Bank-). The amount of L.E. 1 108 279 equal to 20% of total finance represents a non-refundable grant. Based on the accounting policy no. (3-5), the value of this grant was deducted from cost value of the said treatment line.

12-3 The building caption includes the amount of L.E 11 196 260 represents total finance cost

capitalized to this caption during the period of its construction in the previous years. 12-4 The machinery and equipment caption includes the amount of L.E 11 280 471 represents total

finance cost capitalized to this caption in the previous years. 12-5 The fixed assets owned by the group was insurance in the amount of L.E 3.6 Billion . 12-6 The fully depreciated assets and still used in operations amounted L.E. 045 242 297 as at 31

December 2016. (L.E. 283 856 192 as at 31 December 2015). 12-7 As at 31 December 2016, No inoperative assets are exists.

13. Breeding wealth

31/12/2016 31/12/2015 L.E. L.E. Cost Beginning of the year 53 955 746 54 344 359 Additions of the year 73 264 926 49 234 662 Disposals of the year (49 371 625) (49 623 275) Cost at the year end 77 849 047 53 955 746 Accumulated amortization Beginning of the year 16 392 046 22 290 031 Amortization of the year 49 842 750 40 768 744 Disposals accumulated amortization (47 423 798) (46 666 729) Accumulated amortization at the year end 18 810 998 16 392 046 Net breeding wealth at the year end 59 038 049 37 563 700 Breeding expenses Beginning of the year 56 480 630 51 884 978 Breeding additions of the year 111 792 747 91 894 351 *Amortization of the year (99 105 233) (87 298 699) End of the year 69 168 144 56 480 630 Total breeding wealth 128 206 193 94 044 330 *Deduct impairment (19 228 117) (14 021 942) 108 978 076 80 022 388

* The company’s management formed an impairment of the year represents the impairment in the value of Breeding wealth(Breeders) according to the study of the Company’s technical based on the expected exhausted standards of Breeding .