cover slide title placeholder - tradewinds · cidade de itajai fpso conversion lpg lng newbuildings...

TRANSCRIPT

March 18 - 20 , 2013

CMA Conference

NYSE: TK 2 www.teekay.com

This presentation contains forward-looking statements (as defined in Section 21E of the Securities Exchange Act of 1934, as

amended) which reflect management’s current views with respect to certain future events and performance, including

statements regarding: the estimated cost and timing of delivery of FPSO, shuttle tanker, LNG and LPG newbuildings, including

the Petrojarl Knarr FPSO and the two fuel-saving LNG carriers, the commencement of associated time-charter contracts and the

effect on the Company’s future operating results; the timing of completion of repairs and field re-installation for the Petrojarl Banff

FPSO; the timing, certainty and costs of Teekay Offshore’s acquisition of the HiLoad DP unit from Remora and Teekay Parent’s

investment in Remora, and the effect of these acquisitions on the Company’s future cash flows; the estimated timing of

commencement of new charter contracts upon delivery of FPSO and shuttle tanker newbuildings; the timing and certainty of

securing long-term employment for the two LNG carrier newbuildings; the timing of field installation for the Voyageur Spirit FPSO

and of the sale of the Voyageur Spirit FPSO from Sevan to Teekay Parent and then to Teekay Offshore; expected timing of

redeliveries of vessels chartered-in by Teekay Parent; the timing, certainty and effect on Teekay Parent’s balance sheet and

liquidity from distribution growth from daughter subsidiaries and proceeds from sale of warehoused assets; and the Company’s

future capital expenditure commitments and the debt financings that the Company expects to obtain for its remaining unfinanced

capital expenditure commitments. The following factors are among those that could cause actual results to differ materially from

the forward-looking statements, which involve risks and uncertainties, and that should be considered in evaluating any such

statement: changes in production of or demand for oil, petroleum products, LNG and LPG, either generally or in particular

regions; greater or less than anticipated levels of tanker newbuilding orders or greater or less than anticipated rates of tanker

scrapping; changes in trading patterns significantly affecting overall vessel tonnage requirements; changes in applicable industry

laws and regulations and the timing of implementation of new laws and regulations; changes in the typical seasonal variations in

tanker charter rates; changes in the offshore production of oil or demand for shuttle tankers, FSOs and FPSOs; decreases in oil

production by or increased operating expenses for FPSO units; trends in prevailing charter rates for shuttle tanker and FPSO

contract renewals; the potential for early termination of long-term contracts and inability of the Company to renew or replace

long-term contracts or complete existing contract negotiations; the inability to negotiate new contracts on the two LNG carrier

newbuildings or the HiLoad DP unit to be acquired from Remora; changes affecting the offshore tanker market; shipyard

production or vessel conversion delays and cost overruns; delays in commencement of operations of FPSO units at designated

fields; changes in the Company’s expenses; the Company’s future capital expenditure requirements and the inability to secure

financing for such requirements; the inability of the Company to complete vessel sale transactions to its public company

subsidiaries or to third parties; conditions in the United States capital markets; and other factors discussed in Teekay’s filings

from time to time with the SEC, including its Report on Form 20-F for the fiscal year ended December 31, 2011. The Company

expressly disclaims any obligation or undertaking to release publicly any updates or revisions to any forward-looking statements

contained herein to reflect any change in the Company’s expectations with respect thereto or any change in events, conditions

or circumstances on which any such statement is based.

Forward Looking Statements

NYSE: TK 3 www.teekay.com

OPERATIONAL

LEADERSHIP

NYSE: TK 4 www.teekay.com

Teekay is turning 40, what a great journey it‟s been…

Founded in 1973 as regional charterer

Evolved to tanker owner

Diversified into new segments

Created an innovative financial structure to raise capital & grow in assets

Today: $11b in assets,

170 vessels & a world leader in each of our segments

>

NYSE: TK

NYSE:

TGP NYSE:

TOO

NYSE:

TNK

PRODUCT TANKER

CRUDE TANKER

FPSO

FSO

LNG CARRIER

SHUTTLE TANKER

>

<

NYSE: TK 5 www.teekay.com

MOL NYK Teekay Golar MaranGas

BWGas

K Line

32 31 27

10 5 14 12

8 1 2

11 15

2

In Service On Order

11 14

9 9 5 4

4

2 1

1

In Service On Order

Teekay is a Leader in Each of its Business Segments

Operates Third Largest Independent Fleet in the World

Source: Clarkson Research Services, Platou, Company Websites, Industry Sources. 1 Aframax and Suezmax tankers. Includes vessels under commercial management. 2 Excludes one VLCC and six MR product tankers. 3 Includes shuttle tankers.

Controls More Than 50% of the World’s Fleet

Largest Operator of Shuttle Tankers

Leading Position in LNG Carriers

Leader in Harsh Weather Operations in the North Sea

Leading Position in Leased FPSOs

Transports Approximately 10% of the World’s Seaborne Oil3

Largest Operator of Mid-Size1 Conventional Tankers

Note: Excludes state & oil company fleets.

15

Teekay KnutsenNYK

Tranpetro Viken /PJMR

Lauritzen

33

18

2

3

4

4

7

5

In Service On Order37

22

9

40

32 29

21 20 16

12 51 65 65 59

40 26 22

32 2

3 2

Owned / Chartered-InCommercially ManagedOn Order

Teekay2 Heidmar

Pools SCF AET /

MISC

OSG

Pools

Stena

Sonangol Tsakos

83

67 65 59

40 29 24

14

11 10

5 5

SBM MODEC BW

Offshore

Teekay Bluewater Bumi

Armada

NYSE: TK 6 www.teekay.com

The Teekay Competitive Advantage

Market

Insight

Operational

Excellence

Strategic

Partnerships

Customer

Relationships

Business

Development

Financial

Expertise

Corporate

Governance

Engineering Project

Management

NYSE: TK 7 www.teekay.com

Organizational Alignment

NYSE: TK 8 www.teekay.com

PROJECT

DEVELOPER

NYSE: TK 9 www.teekay.com

$3.5 billion Invested in Gas and Offshore Projects Since 2011

Shuttle Tanker

Newbuildings Voyageur Spirit FPSO,

Upgrade

Establishment of Teekay

Marine Ltd.

Hummingbird Spirit FPSO,

Commercial Integration

Piranema Spirit FPSO,

Integration

Final Angola LNG

carrier delivered

Petrojarl Knarr FPSO,

Newbuilding

Petrojarl Banff FPSO,

Repair & Upgrade

Maersk LNG Joint

Venture

Cidade de Itajai FPSO

Conversion

Exmar LPG

Joint Venture LNG Newbuildings

NYSE: TK 10 www.teekay.com

Teekay Projects in Execution

2013

SHUTTLE

& FSO

4 BG Shuttle Tankers

Remora HiLoad DP Unit

Salamander FSO Project

TANKER VLCC Newbuilding

2014 2015/16

FPSO

Voyageur Spirit

Petrojarl I Redeployment

Petrojarl Banff Re-start

Petrojarl Knarr FPSO

Cidade de Itajai

GAS

4 Exmar LPG Newbuildings

2 LNG Newbuildings

4 Exmar LPG Newbuildings

NYSE: TK 11 www.teekay.com

LNG Newbuildings

• Recently ordered two 173,400 cbm LNG Carriers, with options to order up to

three additional vessels, from Daewoo Shipbuilding and Marine Engineering

(DSME) of South Korea

• Equipped with efficient M-type, Electronically Controlled, Gas Injection (MEGI)

twin engines

• TGP intends to secure long-term employment for both vessels prior to delivery in

early-2016

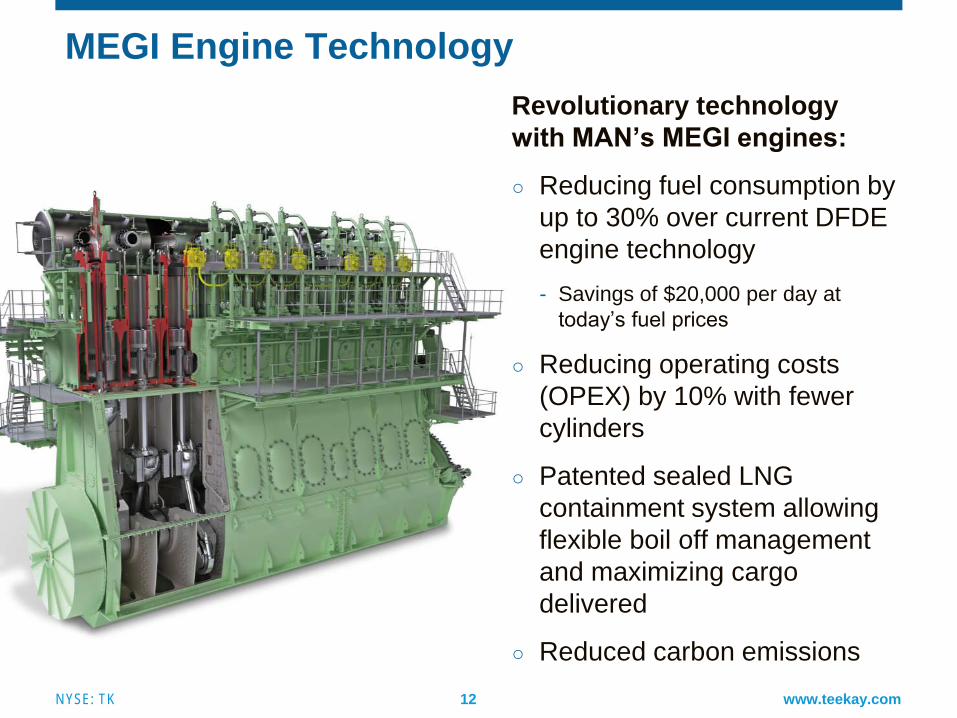

NYSE: TK 12 www.teekay.com

MEGI Engine Technology

Revolutionary technology

with MAN‟s MEGI engines:

○ Reducing fuel consumption by

up to 30% over current DFDE

engine technology

- Savings of $20,000 per day at

today’s fuel prices

○ Reducing operating costs

(OPEX) by 10% with fewer

cylinders

○ Patented sealed LNG

containment system allowing

flexible boil off management

and maximizing cargo

delivered

○ Reduced carbon emissions

NYSE: TK 13 www.teekay.com

• Complements TOO’s

market leading shuttle

tanker operations and

broadens offshore loading

service offering

• Alternative Offloading

solution, especially in long-

haul export markets with

benign sea conditions

• An additional channel for

future growth projects

○ Omnibus agreement will

provide right of first refusal

for TOO to acquire future

HiLoad DP units

Remora‟s HiLoad DP Unit Provides Strategic Benefits

NYSE: TK 14 www.teekay.com

• Charterer Petrobras

• First-Oil February, 2013

• Aframax conversion at Jurong

Shipyard, Singapore

• 50/50 Joint Venture with Brazil-

based Odebrecht

• Firm Contract Length: 9 years

• Extension Options: 6 x 1 years

• Designed Water Depth:

up to 1,000m

• Operating Depth: ~250m

• Processing Capacity: 80,000

bbls/d

• Storage Capacity: 650,000 bbls

• Tiro & Sidon fields on Block BM-

S-40, Santos Basin, offshore

Brazil

○ +150 million barrels of recoverable

oil

Petrojarl Cidade de Itajai FPSO

NYSE: TK 15 www.teekay.com

• Charterer BG Group

• Delivery Dates: ○ Hull 2037, Q2-2013

○ Hull 2038, Q2-2013

○ Hull 2039, Q3-2013

○ Hull 2040, Q4-2013

• Received commitments for long-

term financing for Hull 2037 and

Hull 2038

• Suezmax-sized DP2 shuttle

tankers

• Delivered Cost: ~$120m / vessel

• Being constructed at Samsung

Shipyard, South Korea

• Contract Length:

10 years plus 2 x 5-year options

• Will service BG’s pre-salt

requirements

Brazil Newbuildings Delivering for BG Contract in 2013

NYSE: TK 16 www.teekay.com

• Knarr FPSO is Teekay’s largest FPSO newbuilding project to date

○ Maximum design production capacity of 63,000 bbls/day

○ Currently under construction at the Samsung Heavy Industries yard in

South Korea

• Upon delivery, the Knarr FPSO will be employed on a 10-year

contract with BG on the Knarr oil and gas field in the North Sea

Knarr FPSO Project

NYSE: TK 17 www.teekay.com

Strategic Transaction with Sevan

• Teekay saw the current market need

○ Customers became increasingly accepting of

Sevan’s new technology

• Innovative technology could be applied to

multiple applications

• Teekay could offer customers both FPSO

solutions => increasing competitive position

• Teekay had immediate access to capital

required complete transaction:

○ Cash, PIPE investors and bridge-financing

• Ultimately, project execution provided value:

○ Voyageur Spirit conversion held to budget and

~$80 million liquidity uplift on sale to TOO

○ $25 million investment in Sevan up ~3x

NYSE: TK 18 www.teekay.com

ASSET

MANAGER

NYSE: TK 19 www.teekay.com

TEEKAY

OFFSHORE PARTNERS

• Execute on FPSO newbuilding projects currently warehoused by Teekay Parent

• Pursue redeployment opportunities for existing FPSOs and complete Banff FPSO repairs

• Enhance GP cash flows through dropdown of eligible FPSOs to Teekay Offshore and pursuit of

future Teekay LNG growth initiatives

• Complete implementation of previously announced cost saving initiatives

• Complete project financings and refinancings

• Continue focus on high HSEQ standards and strong operational KPIs across all fleets

2013 Priorities

TEEKAY

LNG PARTNERS

TEEKAY

TANKERS TEEKAY

TANKERS LTD.

TEEKAY CORPORATION (PARENT)

• Bid on point-to-point LNG

• Bid on FSRU projects

• Consider accretive on-the-

water asset acquisitions

• Deliver shuttle tanker

newbuildings in 2013

• Complete HiLoad DP

acquisition and capital

upgrades

• Bid on new FPSO and FSO

projects with post-2015

deliveries

• Consider investment in fuel-

efficient conventional tanker

newbuildings or acquisition of

quality on-the-water vessels.

NYSE: TK 20 www.teekay.com

Executing on Our Financial Strategy

Prudently Managing

Growth

Improving

Profitability

Accessing Multiple

Sources of Capital

• Reducing costs and adding profitable growth

• Expected to return to run-rate profitability in 2013

compared to a net loss of over $100 million in 2011

• Corporate structure provides financial flexibility

• Over $6.0 billion of debt and equity capital raised

during past 4 years

• Continuing to diversify sources of capital

• Teekay Parent on the path to being net debt free by

end-2014

• Disciplined approach to new investments

NYSE: TK 21 www.teekay.com

• On a Consolidated Basis, Teekay Corporation profitability is improving

• Expect to return to run-rate profitability in 2013, despite continued weakness

in spot tanker rates

Focus on Profitability is Achieving Results

1) Consolidated adjusted net income (loss) excludes gains and losses on vessel sales / write downs, unrealized gain / loss on derivatives and other Appendix A adjustments made from time to time. Please refer to Appendix A in Teekay

Corporation’s quarterly earnings releases for more detail.

Teekay Corporation Consolidated Adjusted Net Income (loss)1

Spot Tanker Rates 2010 2011 2012

Aframax $16,300 / day $13,000 / day $12,200 / day

Suezmax $22,500 / day $14,300 / day $17,100 / day

($140)

($120)

($100)

($80)

($60)

($40)

($20)

$0

2010 2011 2012

$ M

illi

on

s

Impact of Petrojarl Banff FPSO off-hire

NYSE: TK 22 www.teekay.com

$13.0 billion

* Pro forma for newbuildings to be delivered and the new LPG joint venture with Exmar, including newbuildings to be delivered.

Diversified Business Model

As at December 31, 2006 As at September 30, 2012 Pro forma*

$7.7 billion

Shuttle Tanker and FSO

18%

FPSO 30%

Liquefied Gas 33%

Fixed-Rate Conventional

Tanker 10%

Spot-Rate Conventional

Tanker 9%

Total Assets:

Shuttle Tanker and

FSO 24%

FPSO 24%

Liquified Gas 19%

Fixed-Rate Conventional Tanker

13%

Spot-Rate Conventional Tanker

20%

NYSE: TK 23 www.teekay.com

Current Sources

• Commercial Bank Debt

○ Expanded banking group

○ $200 million Corporate Revolver

secured by Daughter LP Units

• Export Credit Agency (ECA) Facilities

• U.S. Corporate Bonds

• Norwegian Kroner Bonds

○ TK, TGP and TOO

• Joint Venture Partners

• Daughter Company Equity

○ Overnights, PIPEs

Other Potential Sources

• Project Bonds

• Structured debt / equity instruments

Diversifying Sources of Capital

$2,624

$2,141

$450

$681

$186

Teekay Corporation Sources of Capital

(December 31, 2008 - Present) ($ millions)

Consolidated Total: $6.1 Billion

NYSE: TK 24 www.teekay.com

TEEKAY IS A PLAY ON THE

BUILD-OUT OF GLOBAL

ENERGY INFRASTRUCTURE

NYSE: TK 25 www.teekay.com

Global Energy Demand to Grow 40% by 2030

Source: BP

NYSE: TK 26 www.teekay.com

LNG

• LNG is the key to transitioning natural

gas from a regional to a global market

• Growth in LNG liquefaction,

transportation and regasification projects

• LNG is playing an increasing role in

many countries’ energy mix

Global Infrastructure Build-Out In Progress

0

10

20

30

40

50

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

8

LNG Import / Export Countries

Exporting Countries Importing Countries

Oil

• Remaining conventional land-based

crude increasingly controlled by

National Oil Companies

• Business of Independent Oil

Companies shifting to deepwater

offshore and unconventional crude

sources (i.e. oil sands, shale, heavy oil)

0

10

20

30

40

50

60

70

US

D B

illi

on

s

Deepwater Capex Forecast

Source: Clarksons / GIIGNL / JP Morgan Source: Douglas Westwood

NYSE: TK 27 www.teekay.com

OFFSHORE

NYSE: TK 28 www.teekay.com

• Decrease in total global and North Sea offshore oil production

• Continued increase in deepwater well supply

• Historic high rates of deepwater drilling will lead to FPSO and shuttle demand

in future years

• Trend towards deeper water suits FPSO and shuttle solutions

World Becoming More Reliant On Offshore Oil

World Offshore Crude Oil Production by Type and Region

Source: IEA World Energy Outlook, 2012

NYSE: TK 29 www.teekay.com

• Production lags exploration and drilling by roughly 10 years or more on the

Norwegian Continental Shelf (NCS)

• Increasing amount of drilling on the NCS suggests project pipeline for

FPSOs & FSOs should be strong in the long-term

Innovation and Increasing Oil Production

Source: Norwegian Petroleum Directorate, The Shelf in 2012

Mobile Drill Rigs on Norwegian Continental Shelf to 2017

NYSE: TK 30 www.teekay.com

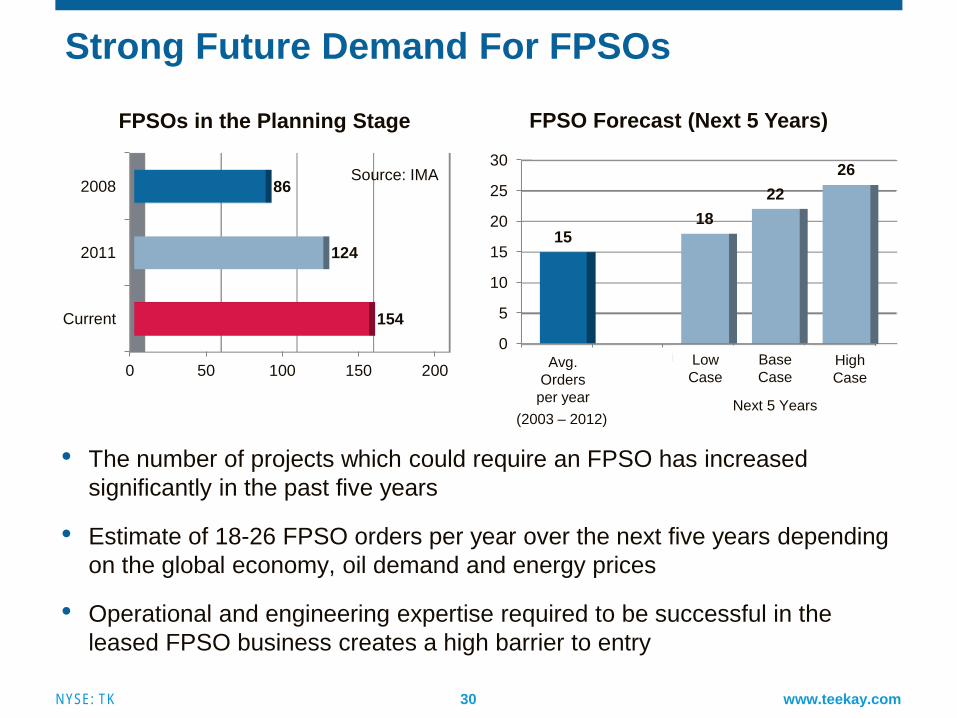

• The number of projects which could require an FPSO has increased

significantly in the past five years

• Estimate of 18-26 FPSO orders per year over the next five years depending

on the global economy, oil demand and energy prices

• Operational and engineering expertise required to be successful in the

leased FPSO business creates a high barrier to entry

Strong Future Demand For FPSOs

0 50 100 150 200

Current

2011

2008

154

124

86

FPSOs in the Planning Stage

0

5

10

15

20

25

30

Avg.Orders per

year

Low Case Base Case High Case

15 18

22

26

FPSO Forecast (Next 5 Years)

Avg.

Orders

per year

Low

Case

Base

Case High

Case

Source: IMA

(2003 – 2012) Next 5 Years

NYSE: TK 31 www.teekay.com

GAS

NYSE: TK 32 www.teekay.com

• LNG supply expected to grow by 4.5% p.a. to 2030, more than twice

as fast as underlying global gas production (2.1% p.a.)

• Demand growth driven by the power generation sector with gas

displacing coal

• Non-OECD, led by China, accounts for the majority of demand

growth

• Worldwide build-out of a global LNG market requires significant

investment in infrastructure and logistics chain

LNG Shipping In The “Golden Age of Gas”

Upstream

Liquefaction

Plant

Floating

LNG

LNG

Carrier

FSRU

Regasification

Plant

End User

NYSE: TK 33 www.teekay.com

• LNG is a cornerstone of China’s energy mix

• Chinese LNG imports expected to double to ~25-30 million tonnes

(MT) by 2015

• Domestic gas shortfall prompting India to turn to LNG imports

• India planning to double regasification capacity by end-2015

LNG Demand Growth Primarily Driven By China and India

0

2

4

6

8

10

12

14

16

18

Current Secured by2016

MOU

Mil

lio

n T

on

ne

s

Chinese LNG Purchase Agreements

Australia

Qatar

Indonesia

Malaysia

PNG

Portfolio

0

5

10

15

20

25

30

35

40

2012 2013 2014 2015 2016

Mil

lio

n T

on

nes

Pe

r A

nn

um

Indian Regasification Capacity

Source: Thomson Reuters Source: Ambit Capital

NYSE: TK 34 www.teekay.com

• Australia expected to add ~80 MTPA of LNG supply by 2020

• Requirement for additional newbuildings to move new LNG volumes

Strong LNG Supply Growth Post-2015

Source: Internal Estimates / Clarksons

200

250

300

350

400

450

500

2012 2013 2014 2015 2016 2017 2018 2019 2020

Mil

lio

n T

on

ne

s P

er

An

nu

m (

MT

PA

)

LNG Capacity Additions By Region vs. LNG Carrier Orderbook

Others Russia Africa North America Australia Existing

170 MTPA by 2020 =

170 incremental LNG carriers

NYSE: TK 35 www.teekay.com

• 200+ MTPA of North American LNG export projects in the planning stage

○ Cheniere’s 18 MTPA Sabine Pass terminal the only project fully approved

• Every 10 MTPA moving USG to Asia creates demand for ~18-20 LNGCs

○ Versus ~7-8 LNGCs to move 10 MTPA from Australia to Asia

North American Exports Provide Upside

0 50 100 150 200 250 300 350 400 450

Proposed Projects

Under Construction

Existing Global LNG Capacity

Million Tonnes per Annum

Global LNG Production Capacity

North America Australia Qatar Rest of World

NYSE: TK 36 www.teekay.com

Looking to Take Advantage of Regional Pricing

Current Spot Natural Gas Prices

US Henry Hub

$3.19 / MMBtu

UK NBP

$10.36 / MMBtu

N.E. Asia LNG

$19.00 / MMBtu

$3-4 / MMBtu Henry Hub means US LNG can

be delivered into Asia for ~$7-10 / MMBtu

NYSE: TK 37 www.teekay.com

LNG Fleet Utilization Improves Post - 2015

• 78 LNG carriers due to deliver by end-2015

○ Little new LNG supply growth during this time; fleet utilization expected to fall

• New LNG supply post-2015 expected to create significant demand for

new vessels over and above the current orderbook

-80

-60

-40

-20

0

20

40

60

80

2012 2013 2014 2015 2016 2017

Nu

mb

er

of

Vessels

Source: Clarksons / Internal Estimates

Tonnage Supply / Demand Balance

Vessels on Order Vessel Demand Surplus / Deficit Total Surplus / Deficit

VESSEL SURPLUS

VESSEL DEFICIT

NYSE: TK 38 www.teekay.com

TANKERS

NYSE: TK 39 www.teekay.com

• Spot tanker rates have been below the long-term average since 2009

○ Aframax 2009-13 average of $14,300 / day vs. $23,500 / day long-term average

○ Suezmax 2009-13 average of $21,700 / day vs. $31,000 / day long-term average

Currently In 5th Year of Tanker Market Downturn

0

10

20

30

40

50

60

70

80

90

„00

0 U

SD

/ D

ay

Source: Clarksons

Aframax Spot Rates Suezmax Spot Rates VLCC Spot Rates

NYSE: TK 40 www.teekay.com

• 2012 / 13 projected to be the trough in terms of tanker fleet utilization / rates

• Improvement in rates from late 2013 / 2014 due to slowing fleet growth (sub-3% p.a.)

coupled with economic recovery, improved oil demand

• Pace of ordering is low and must remain low

• Aframax supply / demand outlook more balanced than other tanker segments

Gradual Recovery Starting Late 2013 / 2014

0%

1%

2%

3%

4%

5%

6%

7%

8%

76%

78%

80%

82%

84%

86%

88%

90%

92%Fleet Utilization Tanker Demand Growth Tanker Supply Growth

Note: Tanker Supply Growth for 2015 and 2016 are based on forecasted assumptions versus actual orders.

NYSE: TK 41 www.teekay.com

Shift in Global Refining Driving Long Haul LR2 Product

Tanker Demand

-0.6 mb/d

+2.9 mb/d

-0.4 mb/d

+1.9 mb/d

-0.3 mb/d

N. American refining capacity

remains flat as US East Coast /

Caribs closures are balanced by

expansion projects in US Gulf

Refinery capacity expansion

Refinery capacity contraction

Refinery Capacity Additions / Reductions 2012-17

+0.9 mb/d To Asia / Pacific

NYSE: TK 42 www.teekay.com