costar office report - mcalpine · pdf filed the costar office report ©2013 costar group,...

TRANSCRIPT

Houston Office MarketY E A R - E N D 2 0 1 2

The CoStarOffice Report

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT A

YEAR-END 2012 – HOUSTON

Table of ContentsTable of Contents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A

Methodology. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . C

Terms & Definitions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . D

Market Highlights & Overview. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

CoStar Markets & Submarkets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Inventory & Development Analysis. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5Inventory & Development AnalysisSelect Top DeliveriesSelect Top Under Construction Properties

Figures at a Glance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Figures at a Glance by Class & MarketFigures at a Glance by Class & SubmarketFigures at a Glance Grouped by CBD vs SuburbanHistorical Figures at a Glance

Leasing Activity Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Select Top Lease Transactions

Sales Activity Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Sales Activity AnalysisSelect Top Sales TransactionsAustin County Market

Analysis of Individual CoStar Submarket Clusters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22Bellaire MarketDowntown MarketE Fort Bend Co/Sugar Land MarketFM 1960 MarketGreenway Plaza MarketGulf Freeway/Pasadena MarketI-10 East MarketKaty Freeway MarketKingwood/Humble MarketNASA/Clear Lake MarketNorth Belt MarketNortheast Near MarketNorthwest MarketRichmond/Fountainview MarketSan Felipe/Voss MarketSan Jacinto County MarketSouth MarketSouth Hwy 35 MarketSouth Main/Medical Center MarketSouthwest MarketWest Loop MarketWestchase MarketWoodlands Market

Houston Office Market

B THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT C

YEAR-END 2012 – HOUSTON

Table of Contents (Continued)

Houston Office Market

B THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT C

YEAR-END 2012 – HOUSTON

Methodology

The CoStar Office Report, unless specifically stated otherwise, calculates office statistics using CoStar Group’s entire database of existing and under construction office buildings in each metropolitan area. Included are office, office condominium, office loft, office medical, all classes and all sizes, and both multi-tenant and single-tenant buildings, including owner-occupied buildings. CoStar Group's national database includes approximately 80.7 billion square feet of coverage in 3.5 million properties. All rental rates reported in the CoStar Office Report have been converted to a Full Service equivalent rental rate.

© Copyright 2013 CoStar Group, Inc. All Rights Reserved. Although CoStar makes efforts to ensure the accuracy and reliability of the information contained herein, CoStar makes no guarantee, representation or warranty regarding the quality, accuracy, timeliness or completeness of the information. The publication is provided ‘as is’ and CoStar expressly disclaims any guarantees, representations or warranties of any kind, including those of MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE.

CoStar Group, Inc.

1331 L ST NW • Washington, DC 20005• (800) 204-5960 • www.costar.com • NASDAQ: CSGP

For information on subscribing to CoStar’s other products and services, please contact us at

1-877-7COSTAR, or visit our web site at www.costar.com

Houston Office Market

D THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT E

YEAR-END 2012 – HOUSTON

Terms & DefinitionsAvailability Rate: The ratio of available space to total rentable space, calculated by dividing the total available square feet by the total rentable square feet.

Available Space: The total amount of space that is currently being marketed as available for lease in a given time period. It includes any space that is available, regardless of whether the space is vacant, occupied, available for sublease, or available at a future date.

Build-to-Suit: A term describing a particular property, developed specifically for a certain tenant to occupy, with structural features, systems, or improvement work designed specifically for the needs of that tenant. A build-to-suit can be leased or owned by the ten-ant. In a leased build-to-suit, a tenant will usually have a long term lease on the space.

Buyer: The individual, group, company, or entity that has pur-chased a commercial real estate asset.

Cap Rate: Short for capitalization rate. The Cap Rate is a calcula-tion that reflects the relationship between one year’s net operating income and the current market value of a particular property. The Cap Rate is calculated by dividing the annual net operating income by the sales price (or asking sales price).

CBD: Abbreviation for Central Business District. (See also: Central Business District)

Central Business District: The designations of Central Business District (CBD) and Suburban refer to a particular geographic area within a metropolitan statistical area (MSA) describing the level of real estate development found there. The CBD is characterized by a high density, well organized core within the largest city of a given MSA.

Class A: A classification used to describe buildings that generally qualify as extremely desirable investment-grade properties and command the highest rents or sale prices compared to other buildings in the same market. Such buildings are well located and provide efficient tenant layouts as well as high quality, and in some buildings, one-of-a-kind floor plans. They can be an archi-tectural or historical landmark designed by prominent architects. These buildings contain a modern mechanical system, and have above-average maintenance and management as well as the best quality materials and workmanship in their trim and interior fit-tings. They are generally the most attractive and eagerly sought by investors willing to pay a premium for quality.

Class B: A classification used to describe buildings that generally qualify as a more speculative investment, and as such, command lower rents or sale prices compared to Class A properties. Such buildings offer utilitarian space without special attractions, and have ordinary design, if new or fairly new; good to excellent design if an older non-landmark building. These buildings typical-ly have average to good maintenance, management and tenants. They are less appealing to tenants than Class A properties, and may be deficient in a number of respects including floor plans, condition and facilities. They lack prestige and must depend chiefly on a lower price to attract tenants and investors.

Class C: A classification used to describe buildings that gener-ally qualify as no-frills, older buildings that offer basic space and command lower rents or sale prices compared to other buildings in the same market. Such buildings typically have below-average maintenance and management, and could have mixed or low tenant prestige, inferior elevators, and/or mechanical/electrical systems. These buildings lack prestige and must depend chiefly on a lower price to attract tenants and investors.

Construction Starts: Buildings that began construction during a specific period of time. (See also: Deliveries)

Contiguous Blocks of Space: Space within a building that is, or is able to be joined together into a single contiguous space.

Deliveries: Buildings that complete construction during a specified period of time. In order for space to be considered delivered, a certificate of occupancy must have been issued for the property.

Delivery Date: The date a building completes construction and receives a certificate of occupancy.

Developer: The company, entity or individual that transforms raw land to improved property by use of labor, capital and entrepre-neurial efforts.

Direct Space: Space that is being offered for lease directly from the landlord or owner of a building, as opposed to space being offered in a building by another tenant (or broker of a tenant) trying to sublet a space that has already been leased.

Existing Inventory: The square footage of buildings that have received a certificate of occupancy and are able to be occupied by tenants. It does not include space in buildings that are either planned, under construction or under renovation.

Flex Building: A type of building designed to be versatile, which may be used in combination with office (corporate headquarters), research and development, quasi-retail sales, and including but not limited to industrial, warehouse, and distribution uses. A typi-cal flex building will be one or two stories with at least half of the rentable area being used as office space, have ceiling heights of 16 feet or less, and have some type of drive-in door, even though the door may be glassed in or sealed off.

Full Service Rental Rate: Rental rates that include all operating expenses such as utilities, electricity, janitorial services, taxes and insurance.

Gross Absorption: The total change in occupied space over a given period of time, counting space that is occupied but not space that is vacated by tenants. Gross absorption differs from leasing Activity, which is the sum of all space leased over a certain period of time. Unless otherwise noted Gross Absorption includes direct and sublease space.

Growth in Inventory: The change in size of the existing square footage in a given area over a given period of time, generally due to the construction of new buildings.

Industrial Building: A type of building adapted for such uses as the assemblage, processing, and/or manufacturing of products from raw materials or fabricated parts. Additional uses include warehousing, distribution, and maintenance facilities. The pri-mary purpose of the space is for storing, producing, assembling, or distributing product.

Landlord Rep: (Landlord Representative) In a typical lease trans-action between an owner/landlord and tenant, the broker that represents the interests of the owner/landlord is referred to as the Landlord Rep.

Leased Space: All the space that has a financial lease obligation. It includes all leased space, regardless of whether the space is currently occupied by a tenant. Leased space also includes space being offered for sublease.

Leasing Activity: The volume of square footage that is commit-ted to and signed under a lease obligation for a specific building or market in a given period of time. It includes direct leases, subleases and renewals of existing leases. It also includes any pre-leasing activity in planned, under construction, or under renovation buildings.

Market: Geographic boundaries that serve to delineate core areas that are competitive with each other and constitute a generally accepted primary competitive set of areas. Markets are building-type specific, and are non-overlapping contiguous geographic designations having a cumulative sum that matches the boundar-ies of the entire Region (See also: Region). Markets can be further subdivided into Submarkets. (See also: Submarkets)

Houston Office Market

D THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT E

YEAR-END 2012 – HOUSTON

Multi-Tenant: Buildings that house more than one tenant at a given time. Usually, multi-tenant buildings were designed and built to accommodate many different floor plans and designs for different tenant needs. (See also: Tenancy).

Net Absorption: The net change in occupied space over a given period of time. Unless otherwise noted Net Absorption includes direct and sublease space.

Net Rental Rate: A rental rate that excludes certain expenses that a tenant could incur in occupying office space. Such expenses are expected to be paid directly by the tenant and may include janitorial costs, electricity, utilities, taxes, insurance and other related costs.

New Space: Sometimes called first generation space, refers to space that has never been occupied and/or leased by a tenant.

Occupied Space: Space that is physically occupied by a tenant. It does not include leased space that is not currently occupied by a tenant.

Office Building: A type of commercial building used exclusively or primarily for office use (business), as opposed to manufactur-ing, warehousing, or other uses. Office buildings may sometimes have other associated uses within part of the building, i.e., retail sales, financial, or restaurant, usually on the ground floor.

Owner: The company, entity, or individual that holds title on a given building or property.

Planned/Proposed: The status of a building that has been announced for future development but not yet started construction.

Preleased Space: The amount of space in a building that has been leased prior to its construction completion date, or certificate of occupancy date.

Price/SF: Calculated by dividing the price of a building (either sales price or asking sales price) by the Rentable Building Area (RBA).

Property Manager: The company and/or person responsible for the day-to-day operations of a building, such as cleaning, trash removal, etc. The property manager also makes sure that the vari-ous systems within the building, such as the elevators, HVAC, and electrical systems, are functioning properly.

Quoted Rental Rate: The asking rate per square foot for a par-ticular building or unit of space by a broker or property owner. Quoted rental rates may differ from the actual rates paid by tenants following the negotiation of all terms and conditions in a specific lease.

RBA: Abbreviation for Rentable Building Area. (See also: Rentable Building Area)

Region: Core areas containing a large population nucleus, that together with adjacent communities have a high degree of eco-nomic and social integration. Regions are further divided into market areas, called Markets. (See also: Markets)

Relet Space: Sometimes called second generation or direct space, refers to existing space that has previously been occupied by another tenant.

Rentable Building Area: (RBA) The total square footage of a building that can be occupied by, or assigned to a tenant for the purpose of determining a tenant’s rental obligation. Generally RBA includes a percentage of common areas including all hall-ways, main lobbies, bathrooms, and telephone closets.

Rental Rates: The annual costs of occupancy for a particular space quoted on a per square foot basis.

Sales Price: The total dollar amount paid for a particular property at a particular point in time.

Sales Volume: The sum of sales prices for a given group of build-ings in a given time period.

Seller: The individual, group, company, or entity that sells a par-ticular commercial real estate asset.

SF: Abbreviation for Square Feet.

Single-Tenant: Buildings that are occupied, or intended to be occupied by a single tenant. (See also: Build-to-suit and Tenancy)

Sublease Space: Space that has been leased by a tenant and is being offered for lease back to the market by the tenant with the lease obligation. Sublease space is sometimes referred to as sublet space.

Submarkets: Specific geographic boundaries that serve to delin-eate a core group of buildings that are competitive with each other and constitute a generally accepted primary competitive set, or peer group. Submarkets are building type specific (office, industrial, retail, etc.), with distinct boundaries dependent on different factors relevant to each building type. Submarkets are non-overlapping, contiguous geographic designations having a cumulative sum that matches the boundaries of the Market they are located within (See also: Market).

Suburban: The Suburban and Central Business District (CBD) designations refer to a particular geographic area within a metro-politan statistical area (MSA). Suburban is defined as including all office inventory not located in the CBD. (See also: CBD)

Tenancy: A term used to indicate whether or not a building is occupied by multiple tenants (See also: Multi-tenant) or a single tenant. (See also: Single-tenant)

Tenant Rep: Tenant Rep stands for Tenant Representative. In a typical lease transaction between an owner/landlord and tenant, the broker that represents the interests of the tenant is referred to as a Tenant Rep.

Time On Market: A measure of how long a currently available space has been marketed for lease, regardless of whether it is vacant or occupied.

Under Construction: The status of a building that is in the process of being developed, assembled, built or constructed. A building is considered to be under construction after it has begun construc-tion and until it receives a certificate of occupancy.

Vacancy Rate: A measurement expressed as a percentage of the total amount of physically vacant space divided by the total amount of existing inventory. Under construction space generally is not included in vacancy calculations.

Vacant Space: Space that is not currently occupied by a tenant, regardless of any lease obligation that may be on the space. Vacant space could be space that is either available or not avail-able. For example, sublease space that is currently being paid for by a tenant but not occupied by that tenant, would be considered vacant space. Likewise, space that has been leased but not yet occupied because of finish work being done, would also be con-sidered vacant space.

Weighted Average Rental Rate: Rental rates that are calculated by factoring in, or weighting, the square footage associated with each particular rental rate. This has the effect of causing rental rates on larger spaces to affect the average more than that of smaller spaces. The weighted average rental rate is calculated by taking the ratio of the square footage associated with the rental rate on each individual available space to the square footage associated with rental rates on all available spaces, multiplying the rental rate by that ratio, and then adding together all the resulting numbers. Unless specifically specified otherwise, rental rate averages include both Direct and Sublet available spaces.

Year Built: The year in which a building completed construction and was issued a certificate of occupancy.

YTD: Abbreviation for Year-to-Date. Describes statistics that are cumulative from the beginning of a calendar year through what-ever time period is being studied.

YEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 1

OVERVIEW

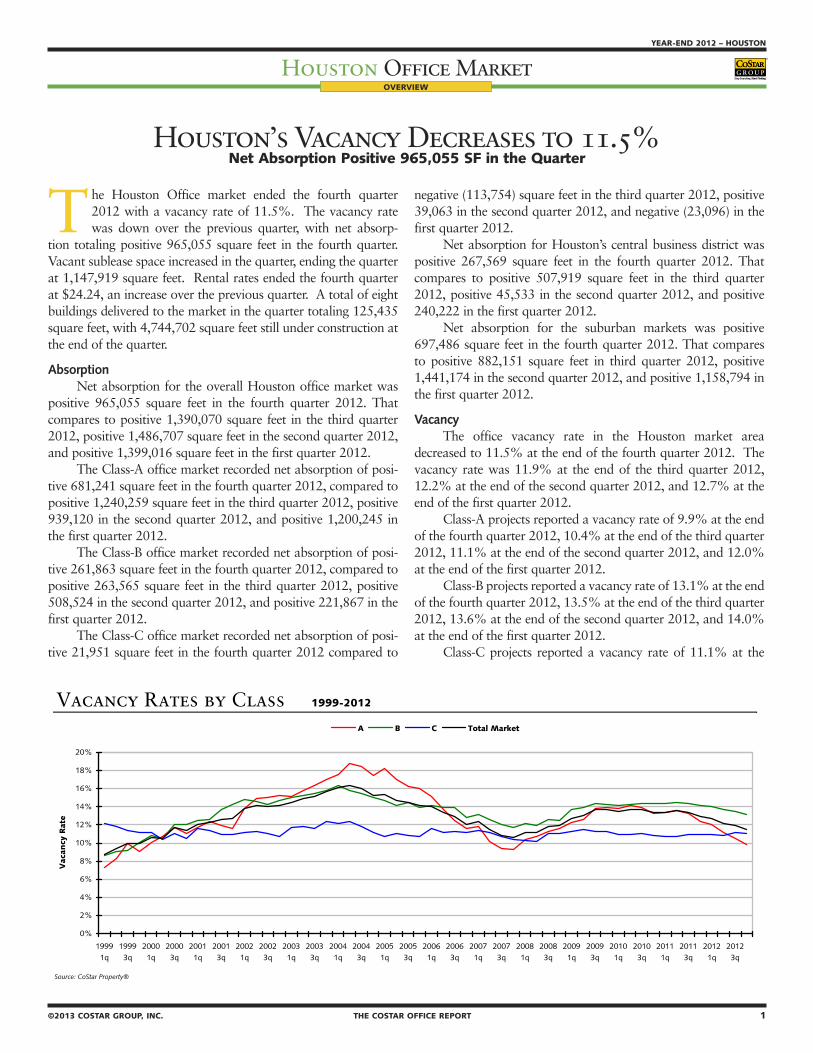

Houston’s Vacancy Decreases to 11.5% Net Absorption Positive 965,055 SF in the Quarter

The Houston Office market ended the fourth quarter 2012 with a vacancy rate of 11.5%. The vacancy rate was down over the previous quarter, with net absorp-

tion totaling positive 965,055 square feet in the fourth quarter. Vacant sublease space increased in the quarter, ending the quarter at 1,147,919 square feet. Rental rates ended the fourth quarter at $24.24, an increase over the previous quarter. A total of eight buildings delivered to the market in the quarter totaling 125,435 square feet, with 4,744,702 square feet still under construction at the end of the quarter.

AbsorptionNet absorption for the overall Houston office market was

positive 965,055 square feet in the fourth quarter 2012. That compares to positive 1,390,070 square feet in the third quarter 2012, positive 1,486,707 square feet in the second quarter 2012, and positive 1,399,016 square feet in the first quarter 2012.

The Class-A office market recorded net absorption of posi-tive 681,241 square feet in the fourth quarter 2012, compared to positive 1,240,259 square feet in the third quarter 2012, positive 939,120 in the second quarter 2012, and positive 1,200,245 in the first quarter 2012.

The Class-B office market recorded net absorption of posi-tive 261,863 square feet in the fourth quarter 2012, compared to positive 263,565 square feet in the third quarter 2012, positive 508,524 in the second quarter 2012, and positive 221,867 in the first quarter 2012.

The Class-C office market recorded net absorption of posi-tive 21,951 square feet in the fourth quarter 2012 compared to

negative (113,754) square feet in the third quarter 2012, positive 39,063 in the second quarter 2012, and negative (23,096) in the first quarter 2012.

Net absorption for Houston’s central business district was positive 267,569 square feet in the fourth quarter 2012. That compares to positive 507,919 square feet in the third quarter 2012, positive 45,533 in the second quarter 2012, and positive 240,222 in the first quarter 2012.

Net absorption for the suburban markets was positive 697,486 square feet in the fourth quarter 2012. That compares to positive 882,151 square feet in third quarter 2012, positive 1,441,174 in the second quarter 2012, and positive 1,158,794 in the first quarter 2012.

VacancyThe office vacancy rate in the Houston market area

decreased to 11.5% at the end of the fourth quarter 2012. The vacancy rate was 11.9% at the end of the third quarter 2012, 12.2% at the end of the second quarter 2012, and 12.7% at the end of the first quarter 2012.

Class-A projects reported a vacancy rate of 9.9% at the end of the fourth quarter 2012, 10.4% at the end of the third quarter 2012, 11.1% at the end of the second quarter 2012, and 12.0% at the end of the first quarter 2012.

Class-B projects reported a vacancy rate of 13.1% at the end of the fourth quarter 2012, 13.5% at the end of the third quarter 2012, 13.6% at the end of the second quarter 2012, and 14.0% at the end of the first quarter 2012.

Class-C projects reported a vacancy rate of 11.1% at the

Vacancy Rates by Class 1999-2012

Source: CoStar Property®

Absorption & Deliveries U.S. Vacancy ComparisonPast 10 Quarters Past 10 Quarters

Source: CoStar Property• Source: CoStar Property•

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

19991q

19993q

20001q

20003q

20011q

20013q

20021q

20023q

20031q

20033q

20041q

20043q

20051q

20053q

20061q

20063q

20071q

20073q

20081q

20083q

20091q

20093q

20101q

20103q

20111q

20113q

20121q

20123q

Vac

ancy

Rat

e

A B C Total Market

0.13

0.980.91

(0.29)

1.00

1.37 1.401.49

1.39

0.97

0.09

0.32

1.05

0.11

1.14

0.22

0.93

0.07

0.70

0.13

(0.4)

(0.2)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

20103q

20104q

20111q

20112q

20113q

20114q

20121q

20122q

20123q

20124q

Millio

ns

SF

Net Absorption Deliveries

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

20103q

20104q

20111q

20112q

20113q

20114q

20121q

20122q

20123q

20124q

Vac

ancy

Rat

e

Houston United States

2 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 3

OVERVIEW

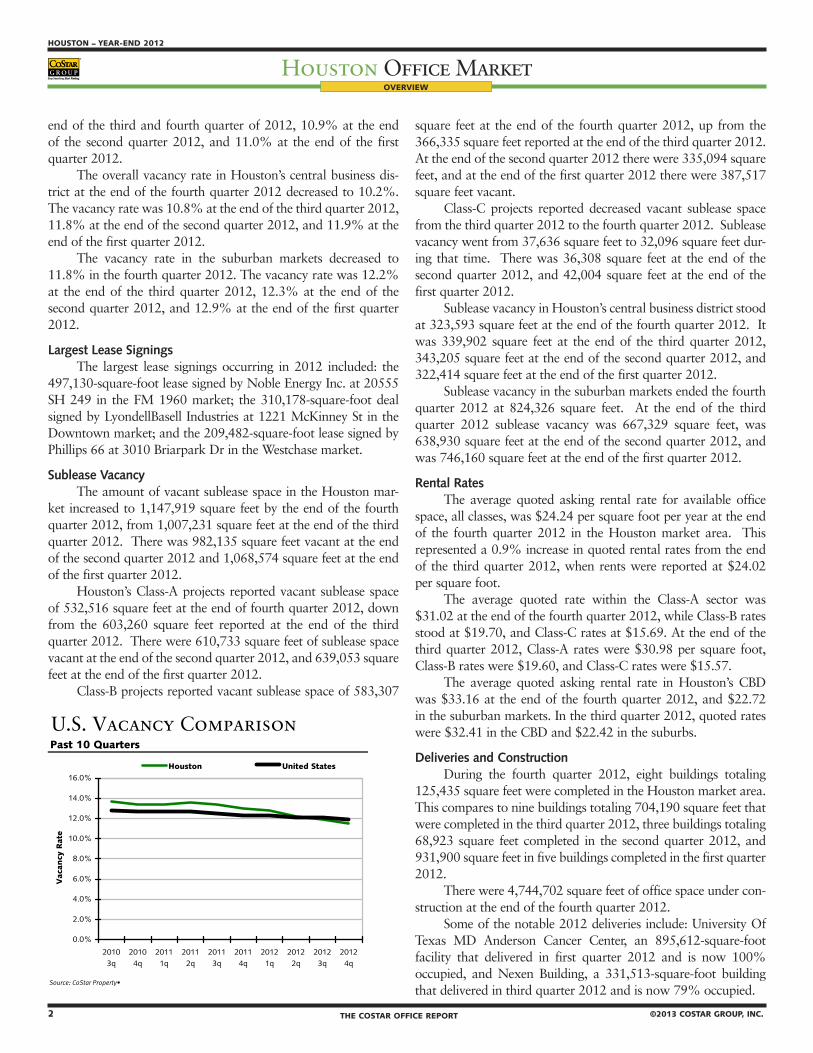

end of the third and fourth quarter of 2012, 10.9% at the end of the second quarter 2012, and 11.0% at the end of the first quarter 2012.

The overall vacancy rate in Houston’s central business dis-trict at the end of the fourth quarter 2012 decreased to 10.2%. The vacancy rate was 10.8% at the end of the third quarter 2012, 11.8% at the end of the second quarter 2012, and 11.9% at the end of the first quarter 2012.

The vacancy rate in the suburban markets decreased to 11.8% in the fourth quarter 2012. The vacancy rate was 12.2% at the end of the third quarter 2012, 12.3% at the end of the second quarter 2012, and 12.9% at the end of the first quarter 2012.

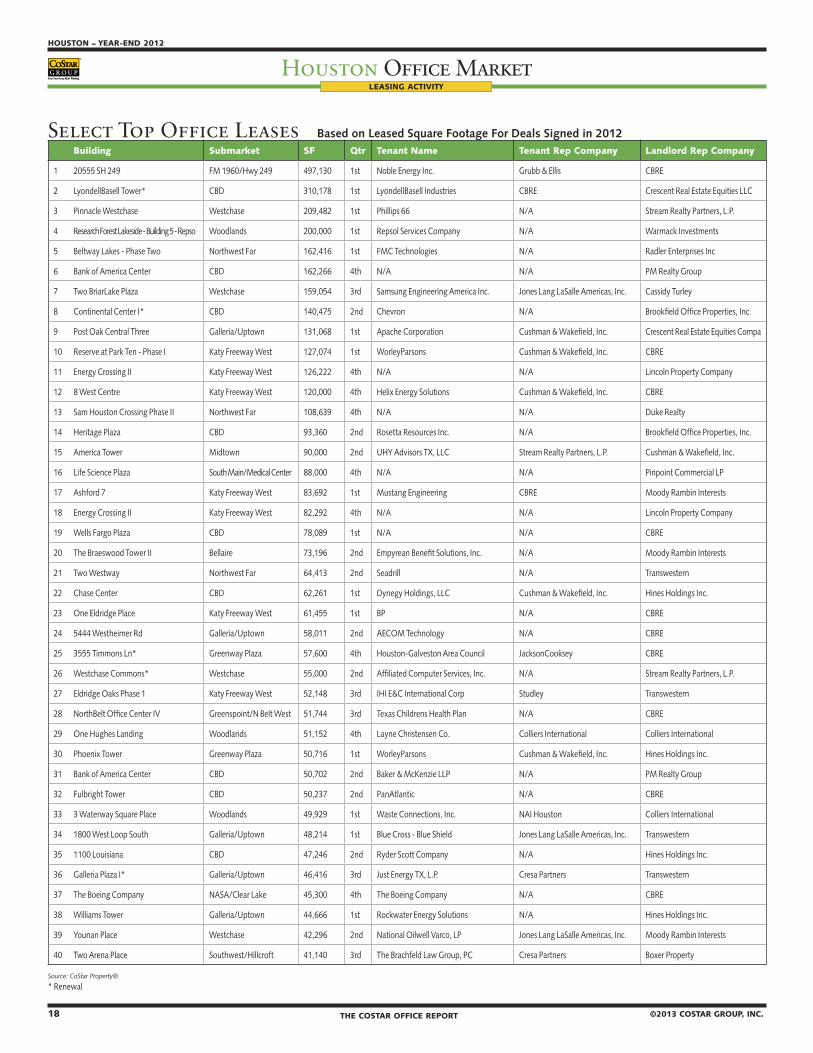

Largest Lease SigningsThe largest lease signings occurring in 2012 included: the

497,130-square-foot lease signed by Noble Energy Inc. at 20555 SH 249 in the FM 1960 market; the 310,178-square-foot deal signed by LyondellBasell Industries at 1221 McKinney St in the Downtown market; and the 209,482-square-foot lease signed by Phillips 66 at 3010 Briarpark Dr in the Westchase market.

Sublease VacancyThe amount of vacant sublease space in the Houston mar-

ket increased to 1,147,919 square feet by the end of the fourth quarter 2012, from 1,007,231 square feet at the end of the third quarter 2012. There was 982,135 square feet vacant at the end of the second quarter 2012 and 1,068,574 square feet at the end of the first quarter 2012.

Houston’s Class-A projects reported vacant sublease space of 532,516 square feet at the end of fourth quarter 2012, down from the 603,260 square feet reported at the end of the third quarter 2012. There were 610,733 square feet of sublease space vacant at the end of the second quarter 2012, and 639,053 square feet at the end of the first quarter 2012.

Class-B projects reported vacant sublease space of 583,307

square feet at the end of the fourth quarter 2012, up from the 366,335 square feet reported at the end of the third quarter 2012. At the end of the second quarter 2012 there were 335,094 square feet, and at the end of the first quarter 2012 there were 387,517 square feet vacant.

Class-C projects reported decreased vacant sublease space from the third quarter 2012 to the fourth quarter 2012. Sublease vacancy went from 37,636 square feet to 32,096 square feet dur-ing that time. There was 36,308 square feet at the end of the second quarter 2012, and 42,004 square feet at the end of the first quarter 2012.

Sublease vacancy in Houston’s central business district stood at 323,593 square feet at the end of the fourth quarter 2012. It was 339,902 square feet at the end of the third quarter 2012, 343,205 square feet at the end of the second quarter 2012, and 322,414 square feet at the end of the first quarter 2012.

Sublease vacancy in the suburban markets ended the fourth quarter 2012 at 824,326 square feet. At the end of the third quarter 2012 sublease vacancy was 667,329 square feet, was 638,930 square feet at the end of the second quarter 2012, and was 746,160 square feet at the end of the first quarter 2012.

Rental RatesThe average quoted asking rental rate for available office

space, all classes, was $24.24 per square foot per year at the end of the fourth quarter 2012 in the Houston market area. This represented a 0.9% increase in quoted rental rates from the end of the third quarter 2012, when rents were reported at $24.02 per square foot.

The average quoted rate within the Class-A sector was $31.02 at the end of the fourth quarter 2012, while Class-B rates stood at $19.70, and Class-C rates at $15.69. At the end of the third quarter 2012, Class-A rates were $30.98 per square foot, Class-B rates were $19.60, and Class-C rates were $15.57.

The average quoted asking rental rate in Houston’s CBD was $33.16 at the end of the fourth quarter 2012, and $22.72 in the suburban markets. In the third quarter 2012, quoted rates were $32.41 in the CBD and $22.42 in the suburbs.

Deliveries and ConstructionDuring the fourth quarter 2012, eight buildings totaling

125,435 square feet were completed in the Houston market area. This compares to nine buildings totaling 704,190 square feet that were completed in the third quarter 2012, three buildings totaling 68,923 square feet completed in the second quarter 2012, and 931,900 square feet in five buildings completed in the first quarter 2012.

There were 4,744,702 square feet of office space under con-struction at the end of the fourth quarter 2012.

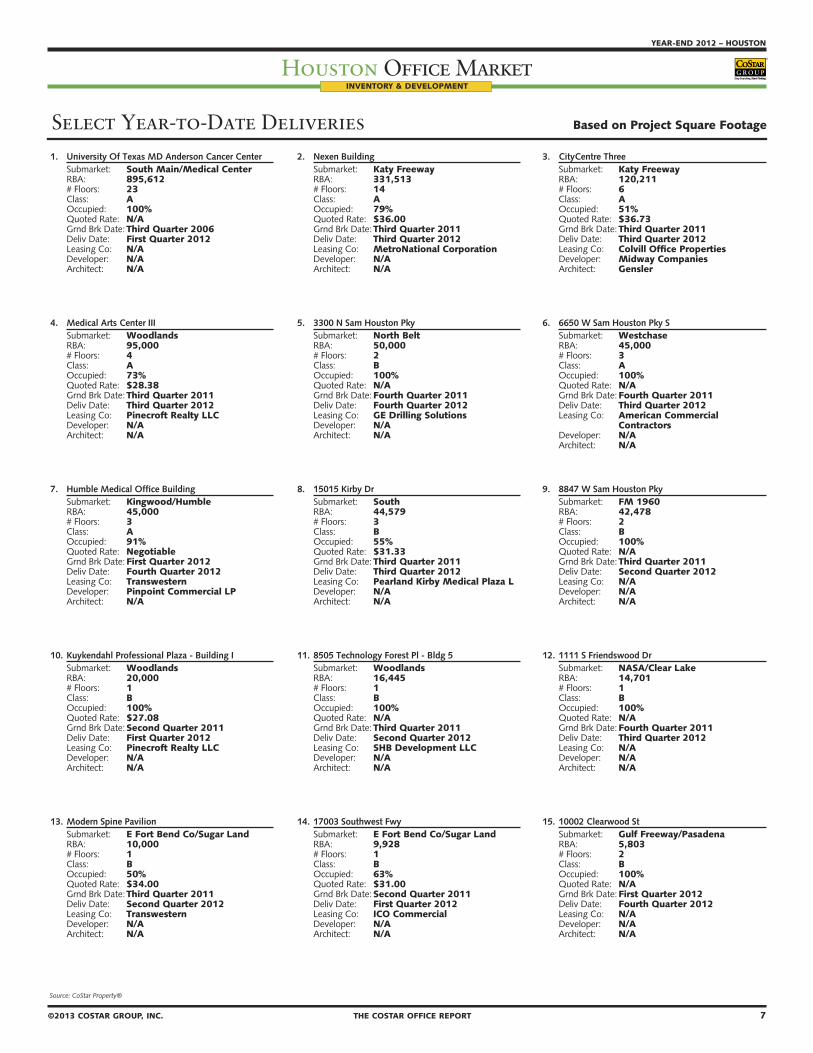

Some of the notable 2012 deliveries include: University Of Texas MD Anderson Cancer Center, an 895,612-square-foot facility that delivered in first quarter 2012 and is now 100% occupied, and Nexen Building, a 331,513-square-foot building that delivered in third quarter 2012 and is now 79% occupied.

Vacancy Rates by Class 1999-2012

Source: CoStar Property®

Absorption & Deliveries U.S. Vacancy ComparisonPast 10 Quarters Past 10 Quarters

Source: CoStar Property• Source: CoStar Property•

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

19991q

19993q

20001q

20003q

20011q

20013q

20021q

20023q

20031q

20033q

20041q

20043q

20051q

20053q

20061q

20063q

20071q

20073q

20081q

20083q

20091q

20093q

20101q

20103q

20111q

20113q

20121q

20123q

Vac

ancy

Rat

e

A B C Total Market

0.13

0.980.91

(0.29)

1.00

1.37 1.401.49

1.39

0.97

0.09

0.32

1.05

0.11

1.14

0.22

0.93

0.07

0.70

0.13

(0.4)

(0.2)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

20103q

20104q

20111q

20112q

20113q

20114q

20121q

20122q

20123q

20124q

Millio

ns

SF

Net Absorption Deliveries

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

20103q

20104q

20111q

20112q

20113q

20114q

20121q

20122q

20123q

20124q

Vac

ancy

Rat

e

Houston United States

2 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 3

OVERVIEW

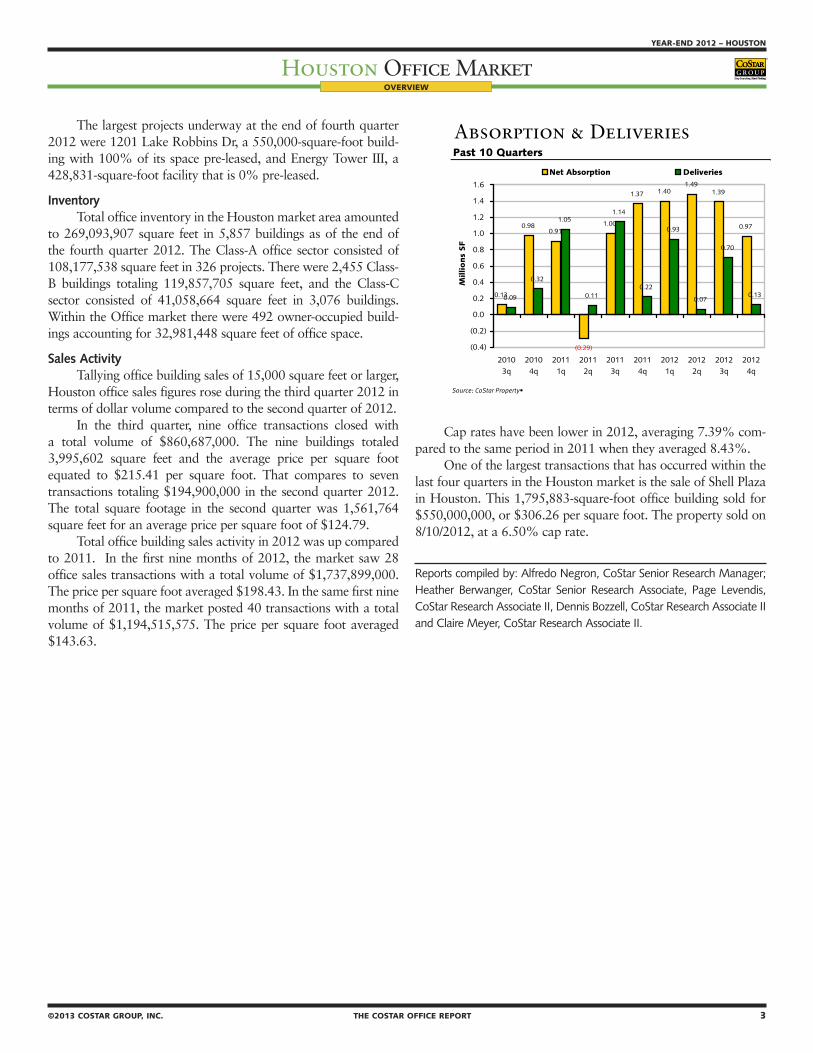

The largest projects underway at the end of fourth quarter 2012 were 1201 Lake Robbins Dr, a 550,000-square-foot build-ing with 100% of its space pre-leased, and Energy Tower III, a 428,831-square-foot facility that is 0% pre-leased.

InventoryTotal office inventory in the Houston market area amounted

to 269,093,907 square feet in 5,857 buildings as of the end of the fourth quarter 2012. The Class-A office sector consisted of 108,177,538 square feet in 326 projects. There were 2,455 Class-B buildings totaling 119,857,705 square feet, and the Class-C sector consisted of 41,058,664 square feet in 3,076 buildings. Within the Office market there were 492 owner-occupied build-ings accounting for 32,981,448 square feet of office space.

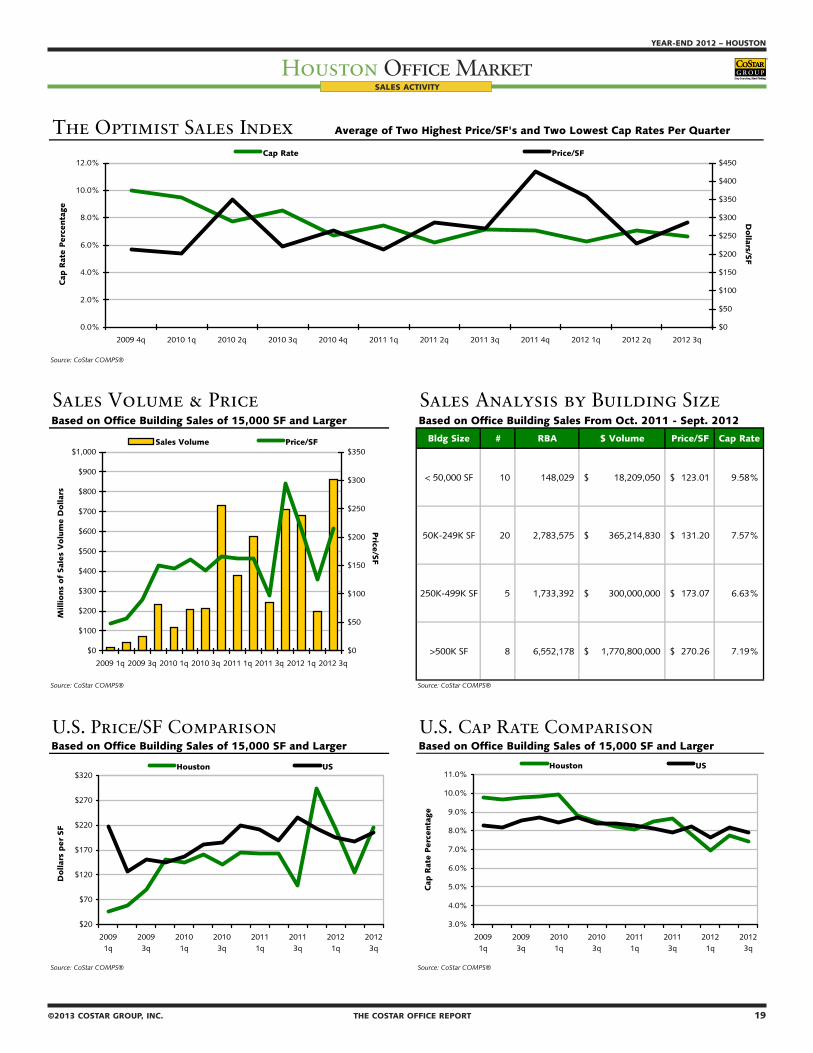

Sales ActivityTallying office building sales of 15,000 square feet or larger,

Houston office sales figures rose during the third quarter 2012 in terms of dollar volume compared to the second quarter of 2012.

In the third quarter, nine office transactions closed with a total volume of $860,687,000. The nine buildings totaled 3,995,602 square feet and the average price per square foot equated to $215.41 per square foot. That compares to seven transactions totaling $194,900,000 in the second quarter 2012. The total square footage in the second quarter was 1,561,764 square feet for an average price per square foot of $124.79.

Total office building sales activity in 2012 was up compared to 2011. In the first nine months of 2012, the market saw 28 office sales transactions with a total volume of $1,737,899,000. The price per square foot averaged $198.43. In the same first nine months of 2011, the market posted 40 transactions with a total volume of $1,194,515,575. The price per square foot averaged $143.63.

Cap rates have been lower in 2012, averaging 7.39% com-pared to the same period in 2011 when they averaged 8.43%.

One of the largest transactions that has occurred within the last four quarters in the Houston market is the sale of Shell Plaza in Houston. This 1,795,883-square-foot office building sold for $550,000,000, or $306.26 per square foot. The property sold on 8/10/2012, at a 6.50% cap rate.

Reports compiled by: Alfredo Negron, CoStar Senior Research Manager; Heather Berwanger, CoStar Senior Research Associate, Page Levendis, CoStar Research Associate II, Dennis Bozzell, CoStar Research Associate II and Claire Meyer, CoStar Research Associate II.

Vacancy Rates by Class 1999-2012

Source: CoStar Property®

Absorption & Deliveries U.S. Vacancy ComparisonPast 10 Quarters Past 10 Quarters

Source: CoStar Property• Source: CoStar Property•

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

19991q

19993q

20001q

20003q

20011q

20013q

20021q

20023q

20031q

20033q

20041q

20043q

20051q

20053q

20061q

20063q

20071q

20073q

20081q

20083q

20091q

20093q

20101q

20103q

20111q

20113q

20121q

20123q

Vac

ancy

Rat

e

A B C Total Market

0.13

0.980.91

(0.29)

1.00

1.37 1.401.49

1.39

0.97

0.09

0.32

1.05

0.11

1.14

0.22

0.93

0.07

0.70

0.13

(0.4)

(0.2)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

20103q

20104q

20111q

20112q

20113q

20114q

20121q

20122q

20123q

20124q

Millio

ns

SF

Net Absorption Deliveries

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

20103q

20104q

20111q

20112q

20113q

20114q

20121q

20122q

20123q

20124q

Vac

ancy

Rat

e

Houston United States

4 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 5

CoStar Submarket Clusters & Submarkets

In analyzing metropolitan areas, CoStar has developed geographic designations to help group properties together, called Markets, Submarket Clusters and Submarkets. Markets are the equivalent of metropolitan areas, or areas containing a large population nucleus, that together with adjacent communities have a high degree of economic and social integration. Markets are then divided into Submarket Clusters, which are core areas within a metropolitan area that are known to be competitive with each other in terms of attracting and keeping tenants. Markets are then further subdivided into smaller units called Submarkets, which serve to delineate a core group of buildings that are competitive with each other and constitute a generally accepted competitive set, or peer group.

MARKETS

Submarket Clusters Submarkets

Austin County Austin County

Bellaire Bellaire

Downtown CBD* Midtown

E Fort Bend Co/Sugar Land E Fort Bend Co/Sugar Land

FM 1960 FM 1960/Champions FM 1960/Hwy 249 FM 1960/I-45 North

Greenway Plaza Greenway Plaza

Gulf Freeway/Pasadena Gulf Freeway/Pasadena

I-10 East I-10 East

Katy Freeway Katy Freeway East Katy Freeway West

Kingwood/Humble Kingwood/Humble

NASA/Clear Lake NASA/Clear Lake

North Belt Greenspoint/IAH Greenspoint/N Belt West

Northeast Near Northeast Near

Northwest North Loop West Northwest Far Northwest Near

Richmond/Fountainview Richmond/Fountainview

San Felipe/Voss San Felipe/Voss

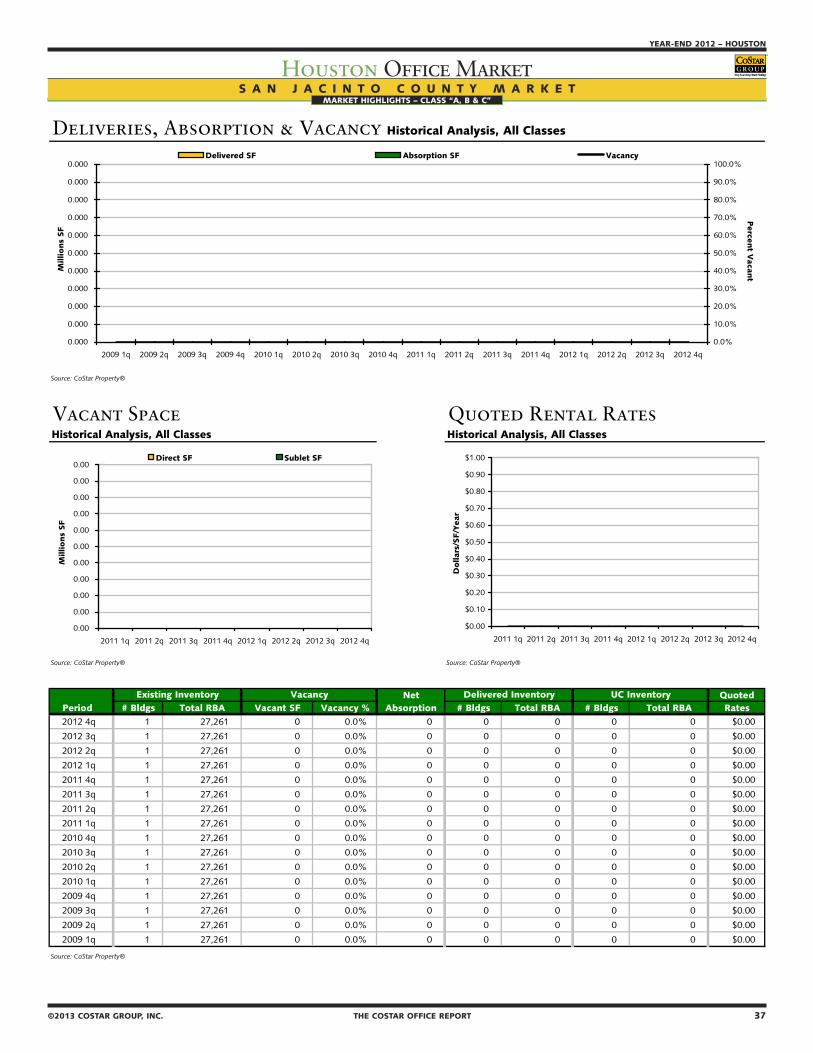

San Jacinto County San Jacinto County

South South

South Hwy 35 South Hwy 35

South Main/Medical Center South Main/Medical Center

Southwest Southwest Beltway 8 Southwest/Hillcroft

West Loop Galleria/Uptown Post Oak Park Riverway

Westchase Westchase

Woodlands Woodlands

* Submarkets comprising the CBD. For statistics reference the CBD vs Suburban Figures at a Glance Page.

4 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 5

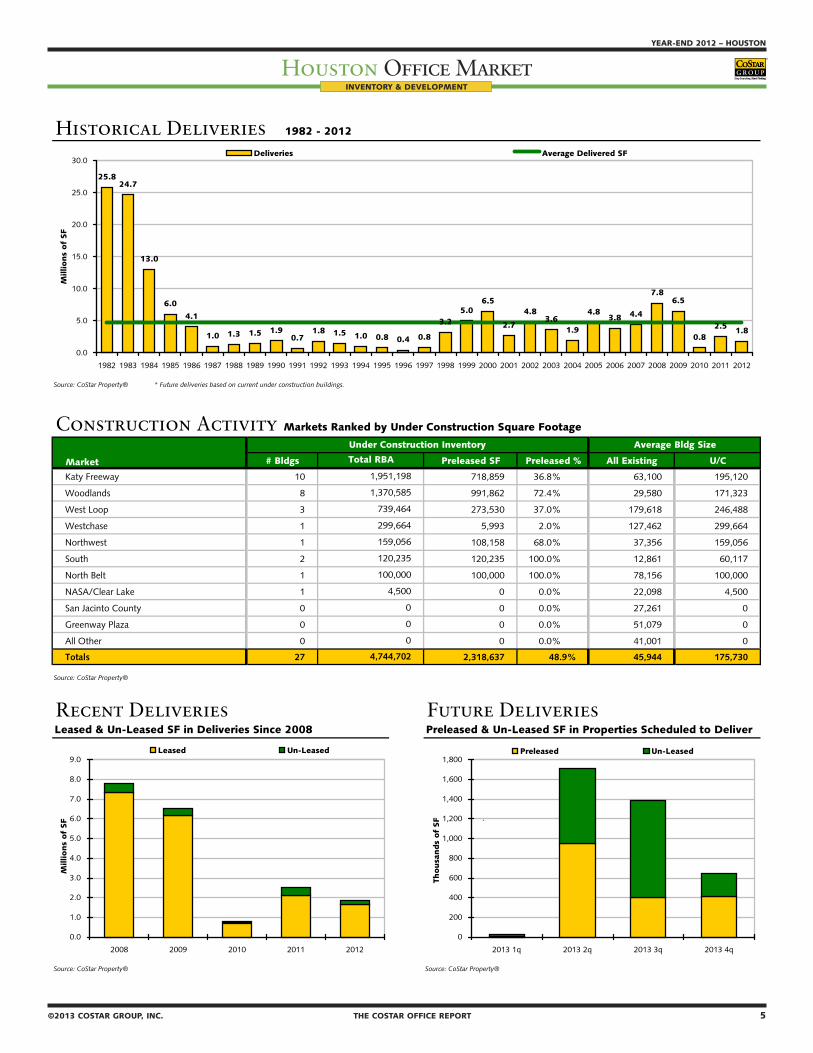

Historical Deliveries 1982 - 2012

Source: CoStar Property® * Future deliveries based on current under construction buildings.

Construction Activity Markets Ranked by Under Construction Square Footage

# Bldgs Preleased SF Preleased % All Existing U/C

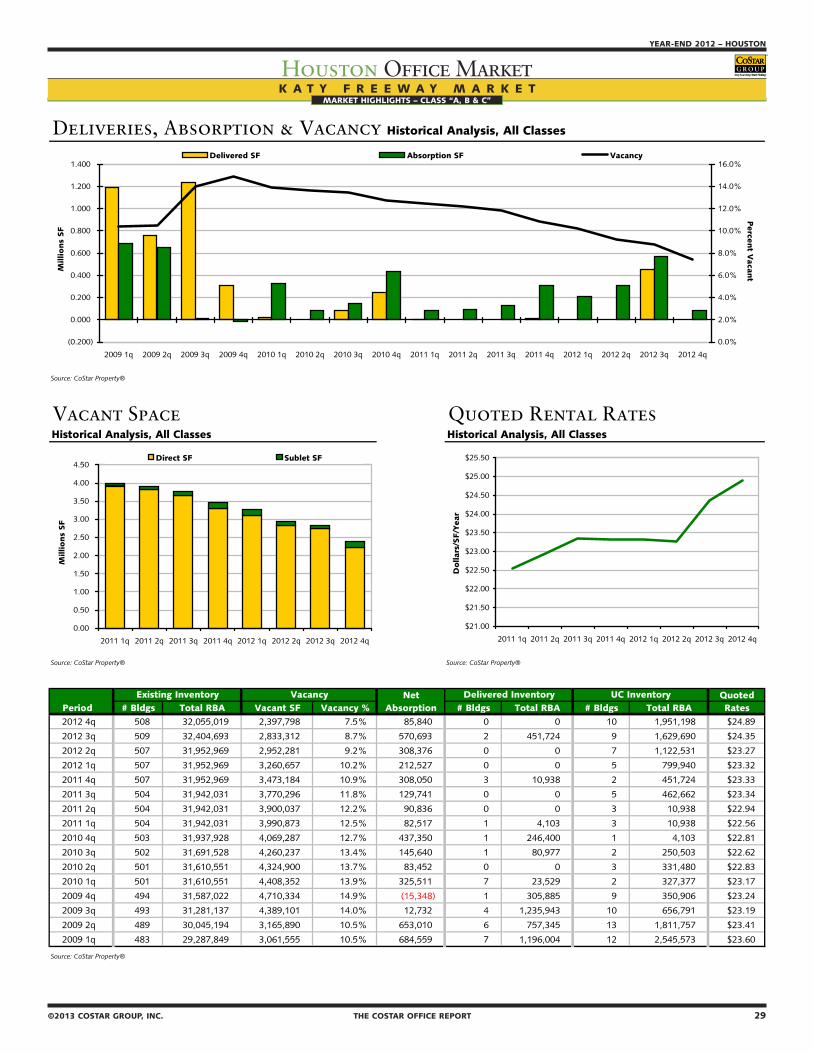

Katy Freeway 10 718,859 36.8% 63,100 195,120

Woodlands 8 991,862 72.4% 29,580 171,323

West Loop 3 273,530 37.0% 179,618 246,488

Westchase 1 5,993 2.0% 127,462 299,664

Northwest 1 108,158 68.0% 37,356 159,056

South 2 120,235 100.0% 12,861 60,117

North Belt 1 100,000 100.0% 78,156 100,000

NASA/Clear Lake 1 0 0.0% 22,098 4,500

San Jacinto County 0 0 0.0% 27,261 0

Greenway Plaza 0 0 0.0% 51,079 0

All Other 0 0 0.0% 41,001 0

Totals 27 2,318,637 48.9% 45,944 175,730

Source: CoStar Property®

Recent Deliveries Future Deliveries Leased & Un-Leased SF in Deliveries Since 2008 Preleased & Un-Leased SF in Properties Scheduled to Deliver

Source: CoStar Property® Source: CoStar Property®

4,500

0

0

Market

Under Construction Inventory Average Bldg Size

Total RBA

0

1,951,198

4,744,702

1,370,585

739,464

299,664

159,056

120,235

100,000

25.824.7

13.0

6.0

4.1

1.0 1.3 1.5 1.90.7

1.8 1.5 1.0 0.8 0.4 0.8

3.25.0

6.5

2.7

4.83.6

1.9

4.83.8 4.4

7.86.5

0.82.5 1.8

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Millio

ns

of

SF

Deliveries Average Delivered SF

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2008 2009 2010 2011 2012

Millio

ns

of

SF

Leased Un-Leased

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2013 1q 2013 2q 2013 3q 2013 4q

T

Thousa

nds

of

SF

Preleased Un-Leased

INVENTORY & DEVELOPMENT

6 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 7

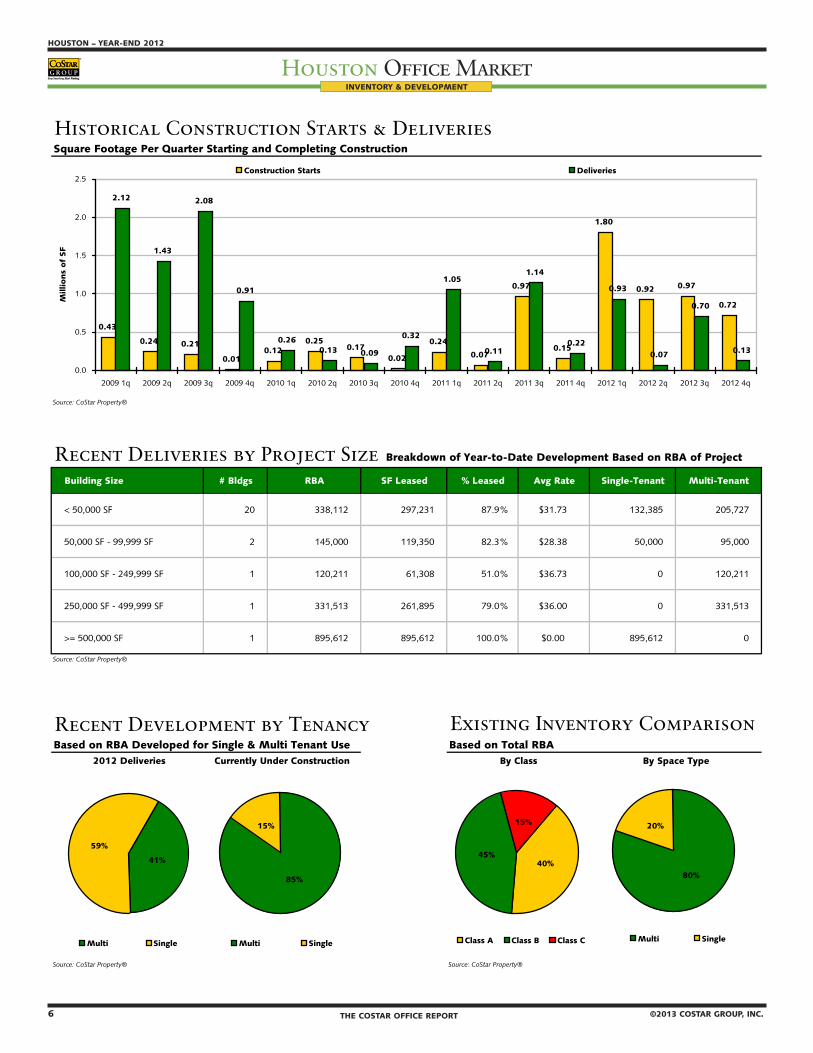

Historical Construction Starts & DeliveriesSquare Footage Per Quarter Starting and Completing Construction

Source: CoStar Property®

Recent Deliveries by Project Size Breakdown of Year-to-Date Development Based on RBA of Project

Building Size # Bldgs RBA SF Leased % Leased Avg Rate Single-Tenant Multi-Tenant

< 50,000 SF 20 338,112 297,231 87.9% $31.73 132,385 205,727

50,000 SF - 99,999 SF 2 145,000 119,350 82.3% $28.38 50,000 95,000

100,000 SF - 249,999 SF 1 120,211 61,308 51.0% $36.73 0 120,211

250,000 SF - 499,999 SF 1 331,513 261,895 79.0% $36.00 0 331,513

>= 500,000 SF 1 895,612 895,612 100.0% $0.00 895,612 0

Source: CoStar Property®

Recent Development by Tenancy Existing Inventory ComparisonBased on RBA Developed for Single & Multi Tenant Use Based on Total RBA

2012 Deliveries

Source: CoStar Property® Source: CoStar Property®

Currently Under Construction By Class By Space Type

0.43

0.24 0.21

0.010.12

0.250.17

0.02

0.24

0.07

0.97

0.15

1.80

0.92 0.97

0.72

2.12

1.43

2.08

0.91

0.260.13 0.09

0.32

1.05

0.11

1.14

0.22

0.93

0.07

0.70

0.13

0.0

0.5

1.0

1.5

2.0

2.5

2009 1q 2009 2q 2009 3q 2009 4q 2010 1q 2010 2q 2010 3q 2010 4q 2011 1q 2011 2q 2011 3q 2011 4q 2012 1q 2012 2q 2012 3q 2012 4q

Millio

ns

of

SF

Construction Starts Deliveries

85%

15%

Multi Single

59%

41%

Multi Single

15%

40%45%

Class A Class B Class C

20%

80%

Multi Single

INVENTORY & DEVELOPMENT

6 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 7

������������������������������ �������������������������������

������������������������

���� �������������������������������������������������������� ������������������������������ ����������������� ��������� ����������� ����������������� ������������������������������������������������ ������������������������������ �������������� �������������� ����

���� ������������������������� ����������������� ����������������� ��������� ����������� ���������������� ��������������������������������������������������� ������������������������������ ������������������������������������ �������������� ����

���� ��������������������������� ����������������� ����������������� �������� ����������� ���������������� ��������������������������������������������������� ������������������������������ ����������������������������������� ��������������������������� ��������

���� ���������������������������������� �������������� ���������������� �������� ����������� ���������������� ��������������������������������������������������� ������������������������������ ������������������������������� �������������� ����

���� ��������������������������������� ��������������� ���������������� �������� ����������� ����������������� ������������������������������������������������� ������������������������������� �������������������������������� �������������� ����

���� ����������������������������������� �������������� ���������������� �������� ����������� ����������������� ������������������������������������������������� ������������������������������ ��������������������

���������������������� �������������� ����

���� ���������������������������������������� �������������������� ���������������� �������� ����������� ���������������� ������������������������������������������������������� ������������������������������� ����������������������� ��������������������������������� ����

���� ������������������������� ���������� ���������������� �������� ����������� ���������������� ��������������������������������������������������� ������������������������������ ����������������������������������������� �������������� ����

���� ��������������������������������� ������������ ���������������� �������� ����������� ����������������� ������������������������������������������������ ������������������������������� �������������� �������������� ����

���������������������������������������������������������� �������������� ���������������� �������� ����������� ����������������� ���������������������������������������������������� ������������������������������ ������������������������������� �������������� ����

�������������������������������������������������� �������������� ���������������� �������� ����������� ����������������� ������������������������������������������������ ������������������������������� ������������������������������ �������������� ����

������������������������������������� �������������������� ���������������� �������� ����������� ����������������� ������������������������������������������������� ������������������������������ �������������� �������������� ����

������������������������������������� ������������������������������ ���������������� �������� ����������� ���������������� ��������������������������������������������������� ������������������������������� ����������������������� �������������� ����

����������������������������������� ������������������������������ ��������������� �������� ����������� ���������������� ���������������������������������������������������� ������������������������������ ������������������������� �������������� ����

���������������������������������� �������������������������� ��������������� �������� ����������� ����������������� ������������������������������������������������ ������������������������������� �������������� �������������� ����

INVENTORY & DEVELOPMENT

8 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 9

INVENTORY & DEVELOPMENT

���������������������������������������� �������������������������������

������������������������

���� ������������������������������� �������������� ����������������� ��������� ������������ ����������������� ������������������������������������������������ ������������������������������� �������������������

���������������������� �������������������

���������������������� ������������������������������

�����

���� ��������������������������� ����������������� ����������������� ��������� ������������ ��������������� ��������������������������������������������������� ������������������������������ ������������������������������ ������������������������������������ ������������������

���� ����������������������������� ����������������� ����������������� �������� ������������ ���������������� ���������������������������������������������������� ������������������������������ ����������������������������������� ��������������������������� �����������������������

���� ������������������������ ����������������� ����������������� ��������� ������������ ����������������� ������������������������������������������������� ������������������������������� �������������� �������������� ����

���� ����������������������������� �������������� ����������������� ��������� ������������ ���������������� ��������������������������������������������������� ������������������������������� ��������������������������������������� �������������� ����

���� ����������������������������� �������������� ����������������� ��������� ������������ ��������������� ��������������������������������������������������� ������������������������������ ��������������� �������������� ��������

���� ������������������������������������������������ �������������� ����������������� ��������� ������������ ���������������� ������������������������������������������������������� ������������������������������� ������������������������������ �������������� ����

���� ���������������������������������� �������������� ����������������� ��������� ������������ ��������������� ���������������������������������������������������� ������������������������������ ����������������������������� �������������������������������� �����

���� ���������������������������������� �������������� ����������������� ��������� ������������ ���������������� ��������������������������������������������������� ������������������������������� ��������������������������������� ��������������������������

������������������� ��������������������������

����������������������������� ����������������� ����������������� �������� ������������ ���������������� ��������������������������������������������������� ������������������������������ ��������������� �������������� ����

���������������������������������� �������������� ����������������� �������� ������������ ���������������� ���������������������������������������������������� ������������������������������ ��������������������������������� �������������� ����

������������������������������� ����������������� ����������������� �������� ������������ ��������������� ��������������������������������������������������� ������������������������������� ����������������������� �������������� ����

��������������������������������������������� �������������� ����������������� �������� ������������ ���������������� ���������������������������������������������������� ������������������������������� ���������������������� �������������� ����

���������������������������������������� ����������������� ����������������� �������� ������������ ��������������� ��������������������������������������������������� ������������������������������� ��������������������������������� �������������������������������� ����

������������������������������������� �������������� ����������������� �������� ������������ ���������������� ���������������������������������������������������� ������������������������������� ����������������������������������� �������������� ����

8 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 9

Class A Market Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

Austin County 0 0 0 0 0.0% 0 0 0 $0.00 Bellaire 7 1,190,230 222,760 227,986 19.2% (111,098) 0 0 $24.99 Downtown 37 33,702,976 2,431,498 2,748,126 8.2% 981,570 0 0 $36.57 E Fort Bend Co/Sugar Land 19 3,684,230 838,842 844,986 22.9% 104,145 0 0 $27.24 FM 1960 20 3,798,687 1,146,343 1,148,673 30.2% 202,333 0 0 $24.34 Greenway Plaza 17 6,410,983 537,173 537,173 8.4% 124,842 0 0 $29.58 Gulf Freeway/Pasadena 1 52,362 8,279 8,279 15.8% 4,819 0 0 $30.22 I-10 East 0 0 0 0 0.0% 0 0 0 $0.00 Katy Freeway 64 15,538,223 678,088 743,510 4.8% 954,126 451,724 1,736,107 $30.26 Kingwood/Humble 2 131,665 72,164 72,164 54.8% 14,660 45,000 0 $32.13 NASA/Clear Lake 12 1,755,479 189,568 189,568 10.8% 50,224 0 0 $23.57 North Belt 20 4,550,663 325,541 366,585 8.1% 708 0 100,000 $22.66 Northeast Near 0 0 0 0 0.0% 0 0 0 $0.00 Northwest 22 3,924,369 423,005 464,073 11.8% 396,489 0 159,056 $22.80 Richmond/Fountainview 0 0 0 0 0.0% 0 0 0 $0.00 San Felipe/Voss 3 1,714,930 317,929 317,929 18.5% (7,420) 0 0 $32.68 San Jacinto County 0 0 0 0 0.0% 0 0 0 $0.00 South 1 80,000 0 0 0.0% 20,702 0 0 $25.63 South Hwy 35 0 0 0 0 0.0% 0 0 0 $0.00 South Main/Medical Center 14 4,471,845 668,518 670,518 15.0% 601,507 895,612 0 $29.71 Southwest 9 2,058,852 341,502 345,167 16.8% 55,242 0 0 $16.91 West Loop 35 14,575,737 1,412,078 1,451,447 10.0% 34,407 0 739,464 $33.14 Westchase 23 6,843,460 411,939 421,559 6.2% 500,241 45,000 299,664 $34.65 Woodlands 20 3,692,847 104,873 104,873 2.8% 133,368 95,000 1,303,585 $35.49

Totals 326 108,177,538 10,130,100 10,662,616 9.9% 4,060,865 1,532,336 4,337,876 $31.02

Source: CoStar Property®

Class B Market Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

Austin County 4 30,995 0 0 0.0% 0 0 0 $0.00 Bellaire 26 2,911,702 174,202 174,202 6.0% 123,025 0 0 $20.48 Downtown 163 19,509,932 2,132,550 2,143,233 11.0% (45,815) 0 0 $24.63 E Fort Bend Co/Sugar Land 214 4,412,677 505,882 593,482 13.4% (22,433) 26,084 0 $21.55 FM 1960 337 8,245,776 1,434,960 1,508,713 18.3% 127,049 42,478 0 $16.34 Greenway Plaza 48 3,975,524 304,664 306,664 7.7% 27,105 0 0 $23.01 Gulf Freeway/Pasadena 144 3,274,007 398,996 405,269 12.4% 13,285 15,590 0 $20.07 I-10 East 22 623,689 97,674 97,674 15.7% 12,814 0 0 $15.22 Katy Freeway 248 12,673,652 1,291,634 1,396,961 11.0% 185,208 0 215,091 $20.10 Kingwood/Humble 64 1,668,188 99,833 100,833 6.0% 47,789 0 0 $20.01 NASA/Clear Lake 194 5,517,776 836,408 838,398 15.2% (189,875) 19,196 4,500 $19.46 North Belt 80 7,310,919 1,261,102 1,319,095 18.0% 131,313 50,000 0 $16.77 Northeast Near 24 645,135 93,907 93,907 14.6% 32,244 30,000 0 $21.34 Northwest 154 8,561,278 1,450,050 1,455,839 17.0% 162,744 0 0 $17.24 Richmond/Fountainview 25 941,806 258,259 258,259 27.4% 7,039 0 0 $16.18 San Felipe/Voss 36 3,452,866 263,564 274,903 8.0% 61,531 0 0 $20.75 San Jacinto County 1 27,261 0 0 0.0% 0 0 0 $0.00 South 73 1,522,069 187,683 187,683 12.3% 36,580 58,279 120,235 $24.77 South Hwy 35 29 328,704 8,017 8,017 2.4% (5,033) 0 0 $14.94 South Main/Medical Center 63 4,338,857 309,206 309,206 7.1% (10,226) 0 0 $23.16 Southwest 126 7,420,666 1,543,157 1,705,024 23.0% (77,320) 0 0 $16.17 West Loop 65 7,710,867 1,204,966 1,217,583 15.8% 95,335 0 0 $23.58 Westchase 73 8,020,632 796,596 823,219 10.3% 175,594 0 0 $18.26 Woodlands 242 6,732,727 455,005 473,458 7.0% 367,866 56,485 67,000 $23.34

Totals 2,455 119,857,705 15,108,315 15,691,622 13.1% 1,255,819 298,112 406,826 $19.70

Source: CoStar Property®

Existing Inventory Vacancy

Existing Inventory Vacancy

FIGURES AT A GLANCE

10 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 11

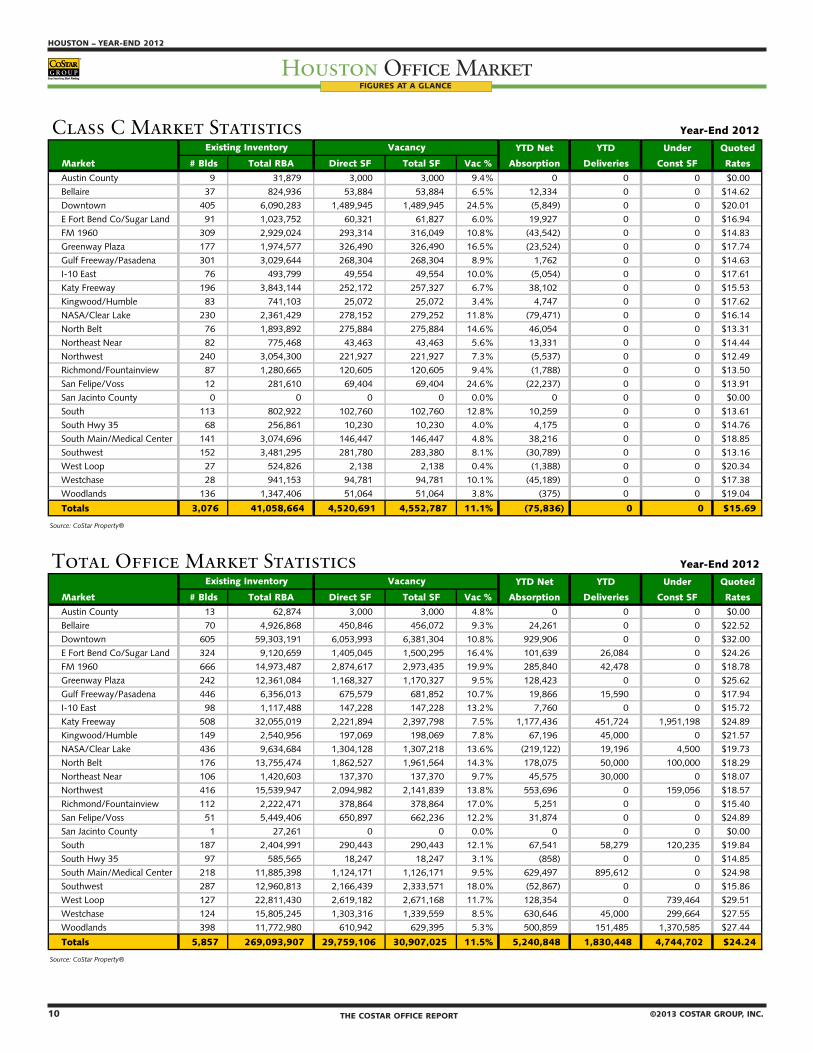

Class C Market Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

Austin County 9 31,879 3,000 3,000 9.4% 0 0 0 $0.00 Bellaire 37 824,936 53,884 53,884 6.5% 12,334 0 0 $14.62 Downtown 405 6,090,283 1,489,945 1,489,945 24.5% (5,849) 0 0 $20.01 E Fort Bend Co/Sugar Land 91 1,023,752 60,321 61,827 6.0% 19,927 0 0 $16.94 FM 1960 309 2,929,024 293,314 316,049 10.8% (43,542) 0 0 $14.83 Greenway Plaza 177 1,974,577 326,490 326,490 16.5% (23,524) 0 0 $17.74 Gulf Freeway/Pasadena 301 3,029,644 268,304 268,304 8.9% 1,762 0 0 $14.63 I-10 East 76 493,799 49,554 49,554 10.0% (5,054) 0 0 $17.61 Katy Freeway 196 3,843,144 252,172 257,327 6.7% 38,102 0 0 $15.53 Kingwood/Humble 83 741,103 25,072 25,072 3.4% 4,747 0 0 $17.62 NASA/Clear Lake 230 2,361,429 278,152 279,252 11.8% (79,471) 0 0 $16.14 North Belt 76 1,893,892 275,884 275,884 14.6% 46,054 0 0 $13.31 Northeast Near 82 775,468 43,463 43,463 5.6% 13,331 0 0 $14.44 Northwest 240 3,054,300 221,927 221,927 7.3% (5,537) 0 0 $12.49 Richmond/Fountainview 87 1,280,665 120,605 120,605 9.4% (1,788) 0 0 $13.50 San Felipe/Voss 12 281,610 69,404 69,404 24.6% (22,237) 0 0 $13.91 San Jacinto County 0 0 0 0 0.0% 0 0 0 $0.00 South 113 802,922 102,760 102,760 12.8% 10,259 0 0 $13.61 South Hwy 35 68 256,861 10,230 10,230 4.0% 4,175 0 0 $14.76 South Main/Medical Center 141 3,074,696 146,447 146,447 4.8% 38,216 0 0 $18.85 Southwest 152 3,481,295 281,780 283,380 8.1% (30,789) 0 0 $13.16 West Loop 27 524,826 2,138 2,138 0.4% (1,388) 0 0 $20.34 Westchase 28 941,153 94,781 94,781 10.1% (45,189) 0 0 $17.38 Woodlands 136 1,347,406 51,064 51,064 3.8% (375) 0 0 $19.04

Totals 3,076 41,058,664 4,520,691 4,552,787 11.1% (75,836) 0 0 $15.69

Source: CoStar Property®

Total Office Market Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

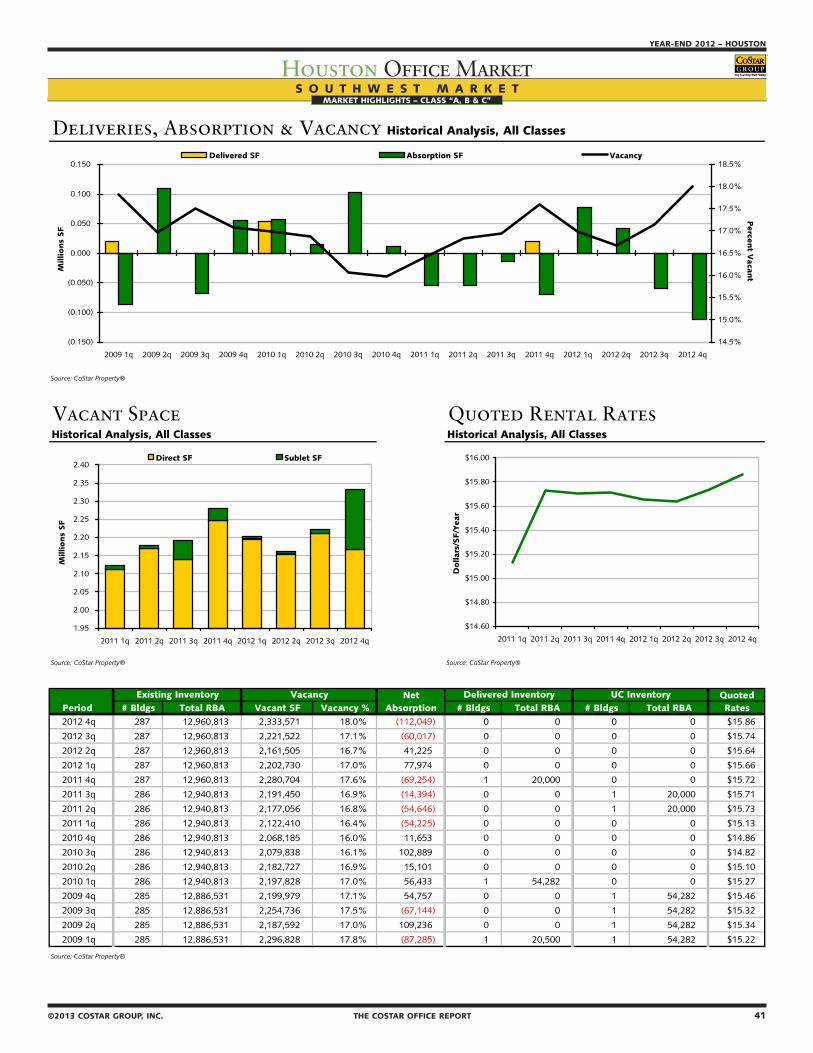

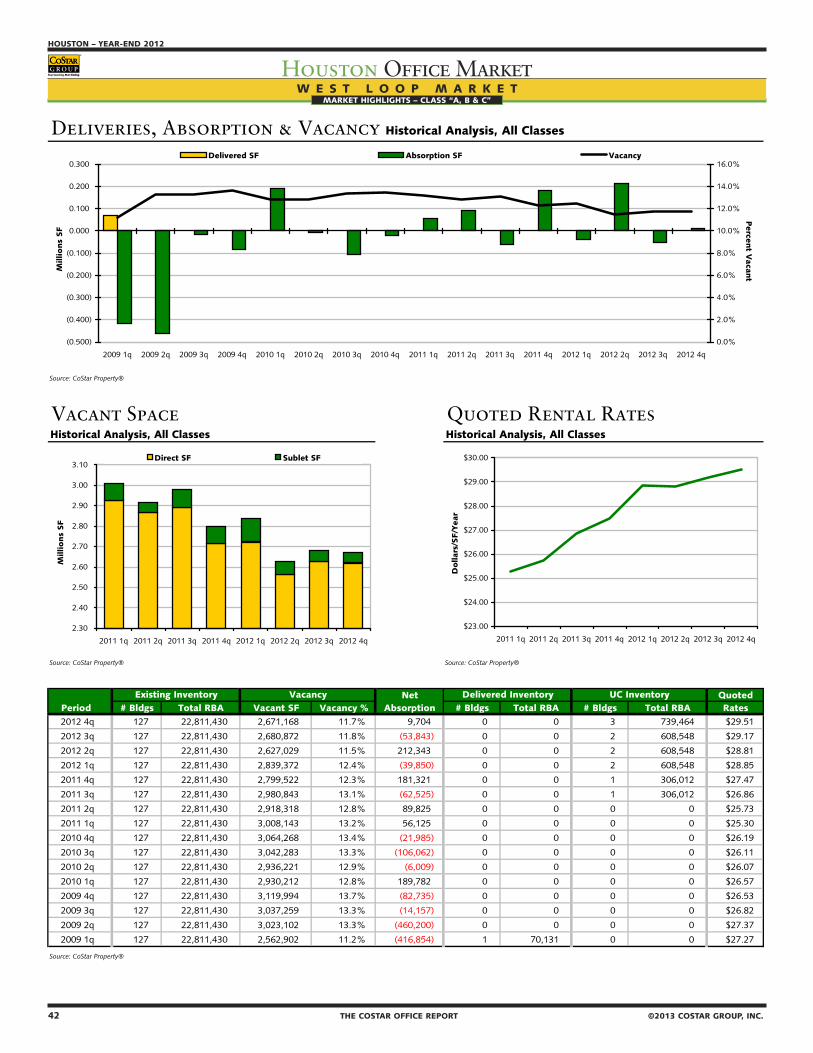

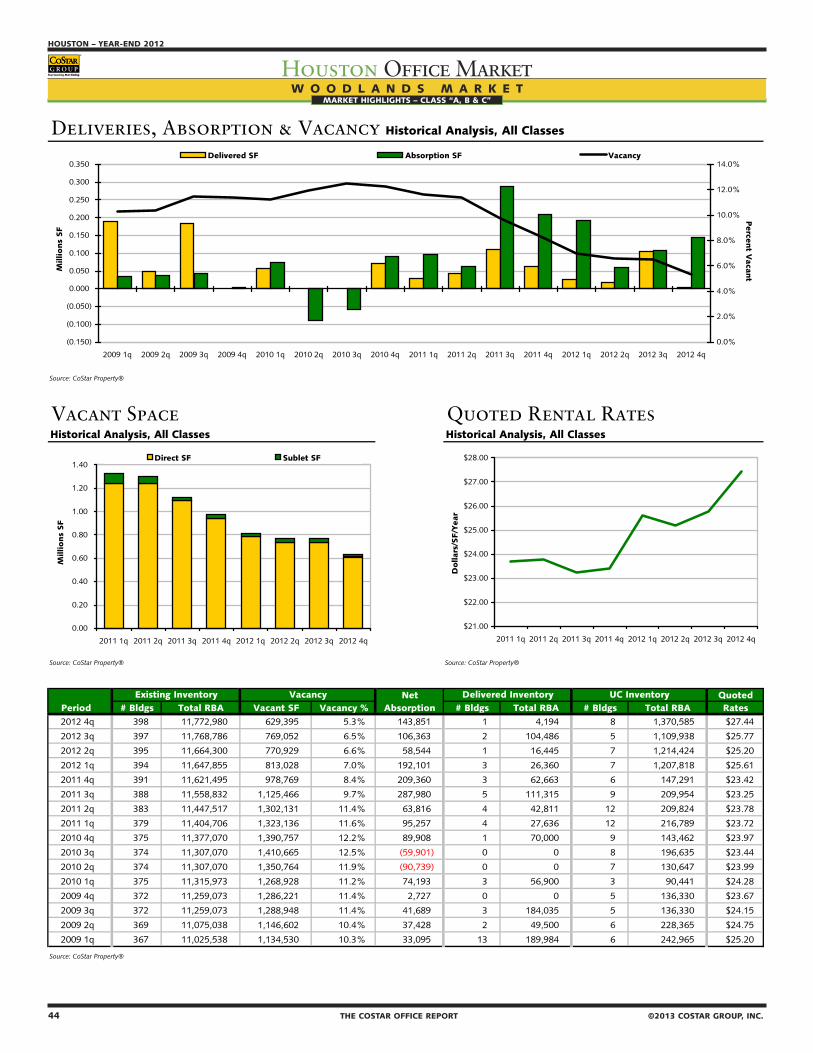

Austin County 13 62,874 3,000 3,000 4.8% 0 0 0 $0.00 Bellaire 70 4,926,868 450,846 456,072 9.3% 24,261 0 0 $22.52 Downtown 605 59,303,191 6,053,993 6,381,304 10.8% 929,906 0 0 $32.00 E Fort Bend Co/Sugar Land 324 9,120,659 1,405,045 1,500,295 16.4% 101,639 26,084 0 $24.26 FM 1960 666 14,973,487 2,874,617 2,973,435 19.9% 285,840 42,478 0 $18.78 Greenway Plaza 242 12,361,084 1,168,327 1,170,327 9.5% 128,423 0 0 $25.62 Gulf Freeway/Pasadena 446 6,356,013 675,579 681,852 10.7% 19,866 15,590 0 $17.94 I-10 East 98 1,117,488 147,228 147,228 13.2% 7,760 0 0 $15.72 Katy Freeway 508 32,055,019 2,221,894 2,397,798 7.5% 1,177,436 451,724 1,951,198 $24.89 Kingwood/Humble 149 2,540,956 197,069 198,069 7.8% 67,196 45,000 0 $21.57 NASA/Clear Lake 436 9,634,684 1,304,128 1,307,218 13.6% (219,122) 19,196 4,500 $19.73 North Belt 176 13,755,474 1,862,527 1,961,564 14.3% 178,075 50,000 100,000 $18.29 Northeast Near 106 1,420,603 137,370 137,370 9.7% 45,575 30,000 0 $18.07 Northwest 416 15,539,947 2,094,982 2,141,839 13.8% 553,696 0 159,056 $18.57 Richmond/Fountainview 112 2,222,471 378,864 378,864 17.0% 5,251 0 0 $15.40 San Felipe/Voss 51 5,449,406 650,897 662,236 12.2% 31,874 0 0 $24.89 San Jacinto County 1 27,261 0 0 0.0% 0 0 0 $0.00 South 187 2,404,991 290,443 290,443 12.1% 67,541 58,279 120,235 $19.84 South Hwy 35 97 585,565 18,247 18,247 3.1% (858) 0 0 $14.85 South Main/Medical Center 218 11,885,398 1,124,171 1,126,171 9.5% 629,497 895,612 0 $24.98 Southwest 287 12,960,813 2,166,439 2,333,571 18.0% (52,867) 0 0 $15.86 West Loop 127 22,811,430 2,619,182 2,671,168 11.7% 128,354 0 739,464 $29.51 Westchase 124 15,805,245 1,303,316 1,339,559 8.5% 630,646 45,000 299,664 $27.55 Woodlands 398 11,772,980 610,942 629,395 5.3% 500,859 151,485 1,370,585 $27.44

Totals 5,857 269,093,907 29,759,106 30,907,025 11.5% 5,240,848 1,830,448 4,744,702 $24.24

Source: CoStar Property®

Existing Inventory Vacancy

Existing Inventory Vacancy

FIGURES AT A GLANCE

10 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 11

FIGURES AT A GLANCE

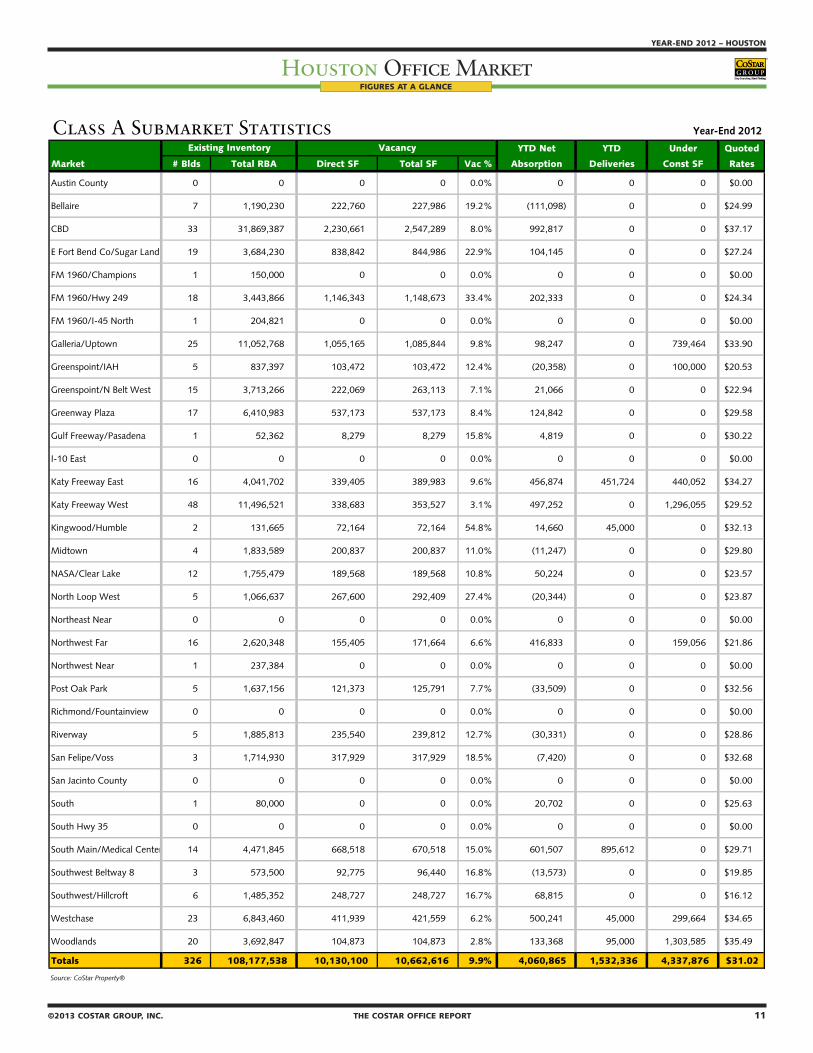

Class A Submarket Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

Austin County 0 0 0 0 0.0% 0 0 0 $0.00

Bellaire 7 1,190,230 222,760 227,986 19.2% (111,098) 0 0 $24.99

CBD 33 31,869,387 2,230,661 2,547,289 8.0% 992,817 0 0 $37.17

E Fort Bend Co/Sugar Land 19 3,684,230 838,842 844,986 22.9% 104,145 0 0 $27.24

FM 1960/Champions 1 150,000 0 0 0.0% 0 0 0 $0.00

FM 1960/Hwy 249 18 3,443,866 1,146,343 1,148,673 33.4% 202,333 0 0 $24.34

FM 1960/I-45 North 1 204,821 0 0 0.0% 0 0 0 $0.00

Galleria/Uptown 25 11,052,768 1,055,165 1,085,844 9.8% 98,247 0 739,464 $33.90

Greenspoint/IAH 5 837,397 103,472 103,472 12.4% (20,358) 0 100,000 $20.53

Greenspoint/N Belt West 15 3,713,266 222,069 263,113 7.1% 21,066 0 0 $22.94

Greenway Plaza 17 6,410,983 537,173 537,173 8.4% 124,842 0 0 $29.58

Gulf Freeway/Pasadena 1 52,362 8,279 8,279 15.8% 4,819 0 0 $30.22

I-10 East 0 0 0 0 0.0% 0 0 0 $0.00

Katy Freeway East 16 4,041,702 339,405 389,983 9.6% 456,874 451,724 440,052 $34.27

Katy Freeway West 48 11,496,521 338,683 353,527 3.1% 497,252 0 1,296,055 $29.52

Kingwood/Humble 2 131,665 72,164 72,164 54.8% 14,660 45,000 0 $32.13

Midtown 4 1,833,589 200,837 200,837 11.0% (11,247) 0 0 $29.80

NASA/Clear Lake 12 1,755,479 189,568 189,568 10.8% 50,224 0 0 $23.57

North Loop West 5 1,066,637 267,600 292,409 27.4% (20,344) 0 0 $23.87

Northeast Near 0 0 0 0 0.0% 0 0 0 $0.00

Northwest Far 16 2,620,348 155,405 171,664 6.6% 416,833 0 159,056 $21.86

Northwest Near 1 237,384 0 0 0.0% 0 0 0 $0.00

Post Oak Park 5 1,637,156 121,373 125,791 7.7% (33,509) 0 0 $32.56

Richmond/Fountainview 0 0 0 0 0.0% 0 0 0 $0.00

Riverway 5 1,885,813 235,540 239,812 12.7% (30,331) 0 0 $28.86

San Felipe/Voss 3 1,714,930 317,929 317,929 18.5% (7,420) 0 0 $32.68

San Jacinto County 0 0 0 0 0.0% 0 0 0 $0.00

South 1 80,000 0 0 0.0% 20,702 0 0 $25.63

South Hwy 35 0 0 0 0 0.0% 0 0 0 $0.00

South Main/Medical Center 14 4,471,845 668,518 670,518 15.0% 601,507 895,612 0 $29.71

Southwest Beltway 8 3 573,500 92,775 96,440 16.8% (13,573) 0 0 $19.85

Southwest/Hillcroft 6 1,485,352 248,727 248,727 16.7% 68,815 0 0 $16.12

Westchase 23 6,843,460 411,939 421,559 6.2% 500,241 45,000 299,664 $34.65

Woodlands 20 3,692,847 104,873 104,873 2.8% 133,368 95,000 1,303,585 $35.49

Totals 326 108,177,538 10,130,100 10,662,616 9.9% 4,060,865 1,532,336 4,337,876 $31.02

Source: CoStar Property®

Existing Inventory Vacancy

12 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 13

FIGURES AT A GLANCE

Class B Submarket Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

Austin County 4 30,995 0 0 0.0% 0 0 0 $0.00

Bellaire 26 2,911,702 174,202 174,202 6.0% 123,025 0 0 $20.48

CBD 62 15,211,257 1,712,130 1,719,095 11.3% 58,782 0 0 $25.00

E Fort Bend Co/Sugar Land 214 4,412,677 505,882 593,482 13.4% (22,433) 26,084 0 $21.55

FM 1960/Champions 94 2,712,660 778,488 778,488 28.7% (18,611) 0 0 $13.13

FM 1960/Hwy 249 179 3,628,510 416,345 484,576 13.4% (6,616) 42,478 0 $19.97

FM 1960/I-45 North 64 1,904,606 240,127 245,649 12.9% 152,276 0 0 $17.29

Galleria/Uptown 27 4,018,349 418,360 424,742 10.6% 339,568 0 0 $24.03

Greenspoint/IAH 29 2,013,994 281,487 285,374 14.2% 76,410 50,000 0 $17.26

Greenspoint/N Belt West 51 5,296,925 979,615 1,033,721 19.5% 54,903 0 0 $16.65

Greenway Plaza 48 3,975,524 304,664 306,664 7.7% 27,105 0 0 $23.01

Gulf Freeway/Pasadena 144 3,274,007 398,996 405,269 12.4% 13,285 15,590 0 $20.07

I-10 East 22 623,689 97,674 97,674 15.7% 12,814 0 0 $15.22

Katy Freeway East 67 3,169,093 383,407 386,407 12.2% (18,359) 0 210,000 $21.37

Katy Freeway West 181 9,504,559 908,227 1,010,554 10.6% 203,567 0 5,091 $19.48

Kingwood/Humble 64 1,668,188 99,833 100,833 6.0% 47,789 0 0 $20.01

Midtown 101 4,298,675 420,420 424,138 9.9% (104,597) 0 0 $23.36

NASA/Clear Lake 194 5,517,776 836,408 838,398 15.2% (189,875) 19,196 4,500 $19.46

North Loop West 63 3,466,741 776,940 776,940 22.4% 156,673 0 0 $17.18

Northeast Near 24 645,135 93,907 93,907 14.6% 32,244 30,000 0 $21.34

Northwest Far 68 4,107,928 551,724 557,513 13.6% (7) 0 0 $17.65

Northwest Near 23 986,609 121,386 121,386 12.3% 6,078 0 0 $15.15

Post Oak Park 24 2,653,156 643,445 648,177 24.4% (263,800) 0 0 $23.56

Richmond/Fountainview 25 941,806 258,259 258,259 27.4% 7,039 0 0 $16.18

Riverway 14 1,039,362 143,161 144,664 13.9% 19,567 0 0 $22.25

San Felipe/Voss 36 3,452,866 263,564 274,903 8.0% 61,531 0 0 $20.75

San Jacinto County 1 27,261 0 0 0.0% 0 0 0 $0.00

South 73 1,522,069 187,683 187,683 12.3% 36,580 58,279 120,235 $24.77

South Hwy 35 29 328,704 8,017 8,017 2.4% (5,033) 0 0 $14.94

South Main/Medical Center 63 4,338,857 309,206 309,206 7.1% (10,226) 0 0 $23.16

Southwest Beltway 8 98 5,621,482 1,162,752 1,324,619 23.6% (100,228) 0 0 $16.51

Southwest/Hillcroft 28 1,799,184 380,405 380,405 21.1% 22,908 0 0 $14.61

Westchase 73 8,020,632 796,596 823,219 10.3% 175,594 0 0 $18.26

Woodlands 242 6,732,727 455,005 473,458 7.0% 367,866 56,485 67,000 $23.34

Totals 2,455 119,857,705 15,108,315 15,691,622 13.1% 1,255,819 298,112 406,826 $19.70

Source: CoStar Property®

Existing Inventory Vacancy

12 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 13

FIGURES AT A GLANCE

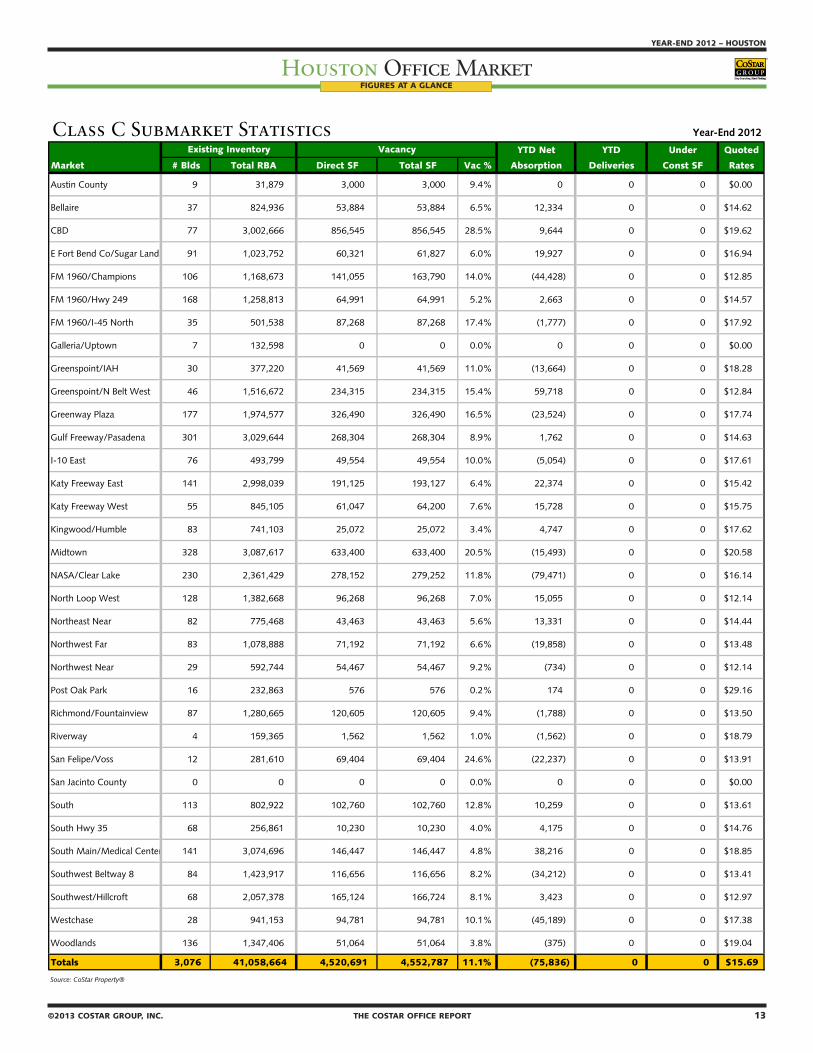

Class C Submarket Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

Austin County 9 31,879 3,000 3,000 9.4% 0 0 0 $0.00

Bellaire 37 824,936 53,884 53,884 6.5% 12,334 0 0 $14.62

CBD 77 3,002,666 856,545 856,545 28.5% 9,644 0 0 $19.62

E Fort Bend Co/Sugar Land 91 1,023,752 60,321 61,827 6.0% 19,927 0 0 $16.94

FM 1960/Champions 106 1,168,673 141,055 163,790 14.0% (44,428) 0 0 $12.85

FM 1960/Hwy 249 168 1,258,813 64,991 64,991 5.2% 2,663 0 0 $14.57

FM 1960/I-45 North 35 501,538 87,268 87,268 17.4% (1,777) 0 0 $17.92

Galleria/Uptown 7 132,598 0 0 0.0% 0 0 0 $0.00

Greenspoint/IAH 30 377,220 41,569 41,569 11.0% (13,664) 0 0 $18.28

Greenspoint/N Belt West 46 1,516,672 234,315 234,315 15.4% 59,718 0 0 $12.84

Greenway Plaza 177 1,974,577 326,490 326,490 16.5% (23,524) 0 0 $17.74

Gulf Freeway/Pasadena 301 3,029,644 268,304 268,304 8.9% 1,762 0 0 $14.63

I-10 East 76 493,799 49,554 49,554 10.0% (5,054) 0 0 $17.61

Katy Freeway East 141 2,998,039 191,125 193,127 6.4% 22,374 0 0 $15.42

Katy Freeway West 55 845,105 61,047 64,200 7.6% 15,728 0 0 $15.75

Kingwood/Humble 83 741,103 25,072 25,072 3.4% 4,747 0 0 $17.62

Midtown 328 3,087,617 633,400 633,400 20.5% (15,493) 0 0 $20.58

NASA/Clear Lake 230 2,361,429 278,152 279,252 11.8% (79,471) 0 0 $16.14

North Loop West 128 1,382,668 96,268 96,268 7.0% 15,055 0 0 $12.14

Northeast Near 82 775,468 43,463 43,463 5.6% 13,331 0 0 $14.44

Northwest Far 83 1,078,888 71,192 71,192 6.6% (19,858) 0 0 $13.48

Northwest Near 29 592,744 54,467 54,467 9.2% (734) 0 0 $12.14

Post Oak Park 16 232,863 576 576 0.2% 174 0 0 $29.16

Richmond/Fountainview 87 1,280,665 120,605 120,605 9.4% (1,788) 0 0 $13.50

Riverway 4 159,365 1,562 1,562 1.0% (1,562) 0 0 $18.79

San Felipe/Voss 12 281,610 69,404 69,404 24.6% (22,237) 0 0 $13.91

San Jacinto County 0 0 0 0 0.0% 0 0 0 $0.00

South 113 802,922 102,760 102,760 12.8% 10,259 0 0 $13.61

South Hwy 35 68 256,861 10,230 10,230 4.0% 4,175 0 0 $14.76

South Main/Medical Center 141 3,074,696 146,447 146,447 4.8% 38,216 0 0 $18.85

Southwest Beltway 8 84 1,423,917 116,656 116,656 8.2% (34,212) 0 0 $13.41

Southwest/Hillcroft 68 2,057,378 165,124 166,724 8.1% 3,423 0 0 $12.97

Westchase 28 941,153 94,781 94,781 10.1% (45,189) 0 0 $17.38

Woodlands 136 1,347,406 51,064 51,064 3.8% (375) 0 0 $19.04

Totals 3,076 41,058,664 4,520,691 4,552,787 11.1% (75,836) 0 0 $15.69

Source: CoStar Property®

Existing Inventory Vacancy

14 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 15

FIGURES AT A GLANCE

Total Office Submarket Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

Austin County 13 62,874 3,000 3,000 4.8% 0 0 0 $0.00

Bellaire 70 4,926,868 450,846 456,072 9.3% 24,261 0 0 $22.52

CBD 172 50,083,310 4,799,336 5,122,929 10.2% 1,061,243 0 0 $33.16

E Fort Bend Co/Sugar Land 324 9,120,659 1,405,045 1,500,295 16.4% 101,639 26,084 0 $24.26

FM 1960/Champions 201 4,031,333 919,543 942,278 23.4% (63,039) 0 0 $13.08

FM 1960/Hwy 249 365 8,331,189 1,627,679 1,698,240 20.4% 198,380 42,478 0 $22.29

FM 1960/I-45 North 100 2,610,965 327,395 332,917 12.8% 150,499 0 0 $17.41

Galleria/Uptown 59 15,203,715 1,473,525 1,510,586 9.9% 437,815 0 739,464 $31.61

Greenspoint/IAH 64 3,228,611 426,528 430,415 13.3% 42,388 50,000 100,000 $18.07

Greenspoint/N Belt West 112 10,526,863 1,435,999 1,531,149 14.5% 135,687 0 0 $18.33

Greenway Plaza 242 12,361,084 1,168,327 1,170,327 9.5% 128,423 0 0 $25.62

Gulf Freeway/Pasadena 446 6,356,013 675,579 681,852 10.7% 19,866 15,590 0 $17.94

I-10 East 98 1,117,488 147,228 147,228 13.2% 7,760 0 0 $15.72

Katy Freeway East 224 10,208,834 913,937 969,517 9.5% 460,889 451,724 650,052 $24.15

Katy Freeway West 284 21,846,185 1,307,957 1,428,281 6.5% 716,547 0 1,301,146 $25.15

Kingwood/Humble 149 2,540,956 197,069 198,069 7.8% 67,196 45,000 0 $21.57

Midtown 433 9,219,881 1,254,657 1,258,375 13.6% (131,337) 0 0 $25.17

NASA/Clear Lake 436 9,634,684 1,304,128 1,307,218 13.6% (219,122) 19,196 4,500 $19.73

North Loop West 196 5,916,046 1,140,808 1,165,617 19.7% 151,384 0 0 $18.82

Northeast Near 106 1,420,603 137,370 137,370 9.7% 45,575 30,000 0 $18.07

Northwest Far 167 7,807,164 778,321 800,369 10.3% 396,968 0 159,056 $18.98

Northwest Near 53 1,816,737 175,853 175,853 9.7% 5,344 0 0 $14.09

Post Oak Park 45 4,523,175 765,394 774,544 17.1% (297,135) 0 0 $25.99

Richmond/Fountainview 112 2,222,471 378,864 378,864 17.0% 5,251 0 0 $15.40

Riverway 23 3,084,540 380,263 386,038 12.5% (12,326) 0 0 $26.33

San Felipe/Voss 51 5,449,406 650,897 662,236 12.2% 31,874 0 0 $24.89

San Jacinto County 1 27,261 0 0 0.0% 0 0 0 $0.00

South 187 2,404,991 290,443 290,443 12.1% 67,541 58,279 120,235 $19.84

South Hwy 35 97 585,565 18,247 18,247 3.1% (858) 0 0 $14.85

South Main/Medical Center 218 11,885,398 1,124,171 1,126,171 9.5% 629,497 895,612 0 $24.98

Southwest Beltway 8 185 7,618,899 1,372,183 1,537,715 20.2% (148,013) 0 0 $16.39

Southwest/Hillcroft 102 5,341,914 794,256 795,856 14.9% 95,146 0 0 $14.79

Westchase 124 15,805,245 1,303,316 1,339,559 8.5% 630,646 45,000 299,664 $27.55

Woodlands 398 11,772,980 610,942 629,395 5.3% 500,859 151,485 1,370,585 $27.44

Totals 5,857 269,093,907 29,759,106 30,907,025 11.5% 5,240,848 1,830,448 4,744,702 $24.24

Source: CoStar Property®

Existing Inventory Vacancy

14 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 15

FIGURES AT A GLANCE

Class A Market Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

CBD 33 31,869,387 2,230,661 2,547,289 8.0% 992,817 0 0 $37.17

Suburban 293 76,308,151 7,899,439 8,115,327 10.6% 3,068,048 1,532,336 4,337,876 $29.17

Totals 326 108,177,538 10,130,100 10,662,616 9.9% 4,060,865 1,532,336 4,337,876 $31.02

Source: CoStar Property®

Class B Market Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

CBD 62 15,211,257 1,712,130 1,719,095 11.3% 58,782 0 0 $25.00

Suburban 2,393 104,646,448 13,396,185 13,972,527 13.4% 1,197,037 298,112 406,826 $19.23

Totals 2,455 119,857,705 15,108,315 15,691,622 13.1% 1,255,819 298,112 406,826 $19.70

Source: CoStar Property®

Class C Market Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

CBD 77 3,002,666 856,545 856,545 28.5% 9,644 0 0 $19.62

Suburban 2,999 38,055,998 3,664,146 3,696,242 9.7% (85,480) 0 0 $15.40

Totals 3,076 41,058,664 4,520,691 4,552,787 11.1% (75,836) 0 0 $15.69

Source: CoStar Property®

Class A & B Market Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

CBD 95 47,080,644 3,942,791 4,266,384 9.1% 1,051,599 0 0 $33.81

Suburban 2,686 180,954,599 21,295,624 22,087,854 12.2% 4,265,085 1,830,448 4,744,702 $23.57

Totals 2,781 228,035,243 25,238,415 26,354,238 11.6% 5,316,684 1,830,448 4,744,702 $25.14

Source: CoStar Property®

Total Office Market Statistics Year-End 2012

YTD Net YTD Under Quoted

Market # Blds Total RBA Direct SF Total SF Vac % Absorption Deliveries Const SF Rates

CBD 172 50,083,310 4,799,336 5,122,929 10.2% 1,061,243 0 0 $33.16

Suburban 5,685 219,010,597 24,959,770 25,784,096 11.8% 4,179,605 1,830,448 4,744,702 $22.72

Totals 5,857 269,093,907 29,759,106 30,907,025 11.5% 5,240,848 1,830,448 4,744,702 $24.24

Source: CoStar Property®

Existing Inventory Vacancy

Existing Inventory Vacancy

Existing Inventory Vacancy

Existing Inventory Vacancy

Existing Inventory Vacancy

16 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012

Houston Office MarketYEAR-END 2012 – HOUSTON

Houston Office Market

©2013 COSTAR GROUP, INC. THE COSTAR OFFICE REPORT 17

FIGURES AT A GLANCE

Class A Market Statistics Year-End 2012

Net Quoted

Period # Blds Total RBA Direct SF Total SF Vac % Absorption # Blds Total RBA # Blds Total RBA Rates

2012 4q 326 108,177,538 10,130,100 10,662,616 9.9% 681,241 1 45,000 18 4,337,876 $31.02 2012 3q 325 108,132,538 10,695,597 11,298,857 10.4% 1,240,259 4 591,724 16 3,732,611 $30.98 2012 2q 321 107,540,814 11,336,659 11,947,392 11.1% 939,120 0 0 16 3,365,452 $30.91 2012 1q 321 107,540,814 12,247,459 12,886,512 12.0% 1,200,245 1 895,612 12 2,563,681 $30.41 2011 4q 320 106,645,202 12,537,551 13,191,145 12.4% 998,126 1 102,000 7 1,893,348 $29.73 2011 3q 319 106,543,202 13,401,779 14,087,271 13.2% 851,120 2 1,000,763 7 1,950,348 $29.20 2011 2q 318 105,961,926 13,706,990 14,357,115 13.5% (136,802) 0 0 5 2,098,375 $28.76 2011 1q 318 105,961,926 13,616,912 14,220,313 13.4% 720,162 1 972,474 5 2,098,375 $28.74

2010 317 104,989,452 13,347,732 13,968,001 13.3% 947,791 2 327,377 5 2,968,849 $28.99 2009 315 104,662,075 13,550,468 14,588,415 13.9% 1,899,063 21 4,943,600 5 3,040,226 $29.86 2008 294 99,718,475 10,695,964 11,543,878 11.6% 2,628,046 26 5,384,996 24 7,736,849 $29.32 2007 268 94,333,479 8,006,146 8,786,928 9.3% 4,203,158 14 2,321,336 34 8,452,882 $27.24 2006 254 92,012,143 9,518,357 10,668,750 11.6% 4,959,985 6 1,015,556 20 4,830,413 $23.69 2005 248 90,996,587 13,094,598 14,613,179 16.1% 2,635,230 12 1,668,345 8 1,614,689 $20.62 2004 236 89,328,242 13,832,672 15,580,064 17.4% (53,899) 3 413,955 13 2,210,198 $20.77 2003 233 88,914,287 12,980,438 15,112,210 17.0% 188,781 7 2,118,892 8 1,358,362 $20.50

Source: CoStar Property®

Class B Market Statistics Year-End 2012

Net Quoted

Period # Blds Total RBA Direct SF Total SF Vac % Absorption # Blds Total RBA # Blds Total RBA Rates

2012 4q 2,455 119,857,705 15,108,315 15,691,622 13.1% 261,863 7 80,435 9 406,826 $19.70 2012 3q 2,449 120,126,944 15,856,389 16,222,724 13.5% 263,565 5 112,466 13 420,261 $19.60 2012 2q 2,444 120,014,478 16,038,729 16,373,823 13.6% 508,524 3 68,923 16 522,071 $19.38 2012 1q 2,441 119,945,555 16,425,907 16,813,424 14.0% 221,867 4 36,288 16 468,168 $19.54 2011 4q 2,438 119,919,256 16,538,896 17,008,992 14.2% 339,555 9 118,668 13 267,677 $19.06 2011 3q 2,429 119,800,588 16,781,424 17,229,879 14.4% 259,240 8 143,210 18 277,944 $19.22 2011 2q 2,421 119,657,378 16,830,467 17,345,909 14.5% (130,488) 6 114,370 22 307,652 $19.08 2011 1q 2,415 119,543,008 16,555,102 17,101,051 14.3% 139,457 11 80,140 22 356,248 $18.95

2010 2,404 119,462,868 16,579,141 17,160,368 14.4% 205,976 37 468,550 21 299,420 $18.99 2009 2,368 119,003,221 16,062,340 16,906,697 14.2% (637,460) 93 1,576,732 35 466,085 $19.31 2008 2,275 117,426,489 13,897,464 14,692,505 12.5% 1,118,263 128 2,338,428 79 1,401,813 $19.98 2007 2,148 115,152,334 12,936,058 13,536,613 11.8% 2,695,149 123 2,032,879 116 2,338,669 $19.32 2006 2,029 113,525,959 14,017,818 14,605,387 12.9% 3,263,365 91 2,505,377 110 1,921,929 $17.26 2005 1,940 111,087,257 14,481,568 15,430,050 13.9% 3,698,126 105 2,885,661 83 2,691,165 $16.24 2004 1,835 108,201,596 14,943,821 16,242,515 15.0% 1,925,438 73 1,336,467 99 3,304,241 $15.89 2003 1,763 106,961,845 15,249,315 16,928,202 15.8% 10,670 67 1,409,184 64 2,229,791 $15.67

Source: CoStar Property®

Total Office Market Statistics Year-End 2012

Net Quoted

Period # Blds Total RBA Direct SF Total SF Vac % Absorption # Blds Total RBA # Blds Total RBA Rates

2012 4q 5,857 269,093,907 29,759,106 30,907,025 11.5% 965,055 8 125,435 27 4,744,702 $24.24 2012 3q 5,850 269,318,146 31,089,088 32,096,319 11.9% 1,390,070 9 704,190 29 4,152,872 $24.02 2012 2q 5,841 268,613,956 31,800,064 32,782,199 12.2% 1,486,707 3 68,923 32 3,887,523 $23.74 2012 1q 5,838 268,545,033 33,131,409 34,199,983 12.7% 1,399,016 5 931,900 28 3,031,849 $23.60 2011 4q 5,834 267,623,122 33,494,347 34,677,088 13.0% 1,365,267 10 220,668 20 2,161,025 $22.94 2011 3q 5,824 267,402,454 34,606,403 35,821,687 13.4% 1,001,792 10 1,143,973 25 2,228,292 $22.71 2011 2q 5,816 266,699,968 34,926,109 36,120,993 13.5% (291,052) 6 114,370 27 2,406,027 $22.48 2011 1q 5,811 266,588,007 34,544,521 35,717,980 13.4% 908,037 12 1,052,614 27 2,454,623 $22.54

2010 5,799 265,535,393 34,350,974 35,573,403 13.4% 1,347,344 39 795,927 26 3,268,269 $22.76 2009 5,761 264,748,369 34,234,130 36,133,723 13.6% 1,187,750 118 6,531,901 40 3,506,311 $23.60 2008 5,643 258,216,468 29,131,316 30,789,572 11.9% 3,399,027 163 7,772,873 105 9,143,312 $23.70 2007 5,484 250,652,052 25,196,059 26,624,183 10.6% 7,149,302 147 4,407,080 156 10,831,556 $22.29 2006 5,343 246,729,694 28,078,433 29,851,127 12.1% 8,170,550 113 3,848,603 140 6,805,207 $19.73 2005 5,236 243,171,816 31,969,103 34,463,799 14.2% 6,565,813 140 4,761,707 106 4,632,274 $18.02 2004 5,099 238,542,745 33,314,479 36,400,541 15.3% 2,456,720 117 1,911,112 130 5,898,996 $17.82 2003 4,986 236,793,679 33,241,000 37,108,195 15.7% (636,933) 86 3,634,001 107 3,734,675 $17.63

Source: CoStar Property®

Existing Inventory Vacancy Deliveries UC Inventory

Existing Inventory Vacancy Deliveries UC Inventory

Existing Inventory Vacancy Deliveries UC Inventory

16 THE COSTAR OFFICE REPORT ©2013 COSTAR GROUP, INC.

HOUSTON – YEAR-END 2012