corporate restructuring.ppt

TRANSCRIPT

Corporate Restructuring

Business Restructuring Financial Restructuring

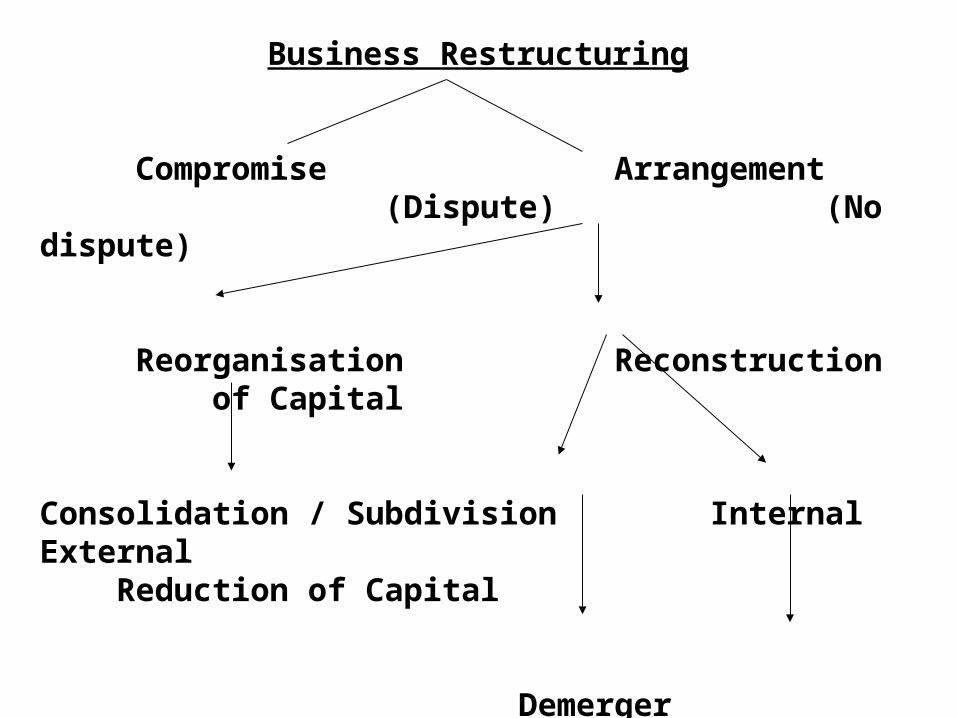

Business Restructuring

Compromise Arrangement (Dispute) (No dispute)

Reorganisation Reconstruction of Capital

Consolidation / Subdivision Internal External Reduction of Capital

Demerger Amalgamation

Compromise, Arrangement and Reconstruction

S 391-Power to compromise or make arrangements with Creditors and Members

S 392-Power of Tribunal to enforce Compromise and Arrangement

S 393-Information as to Compromise and Arrangement with Creditors and Members

S 394-Provisions for facilitating Reconstruction and Amalgamation of companies

Section 391 to Section 393 pertain to Compromise or Arrangement

Section 394 pertains to Reconstruction or Amalgamation

Section 396 pertains to Power of the Central Govt for Amalgamation of Companies in National Interest

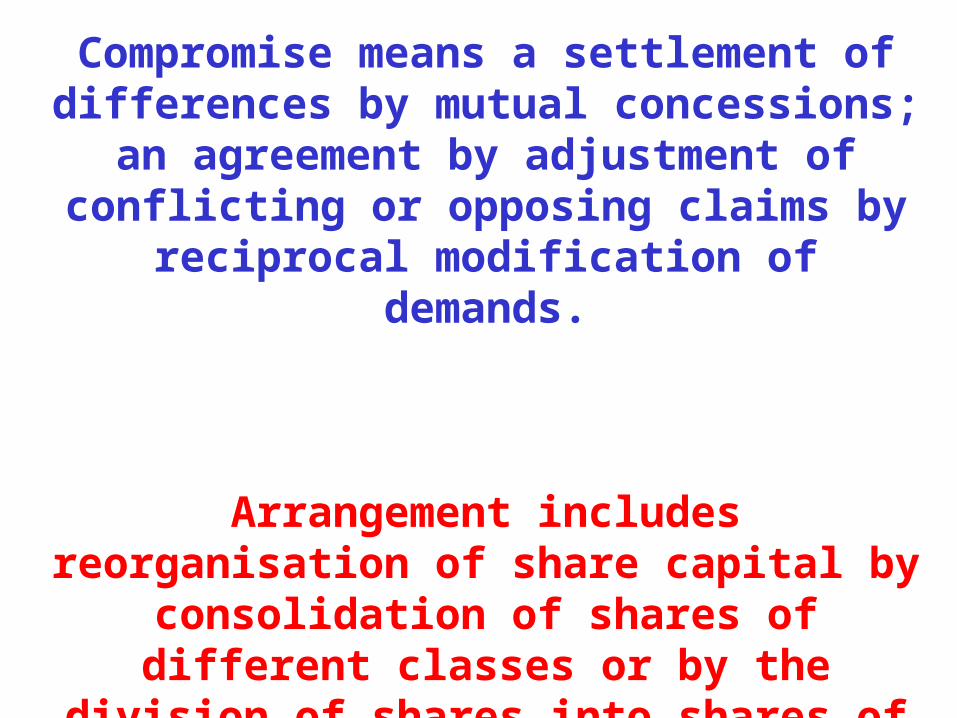

Compromise means a settlement of differences by mutual concessions; an agreement by

adjustment of conflicting or opposing claims by reciprocal modification of demands.

Arrangement includes reorganisation of share capital by consolidation of shares of different

classes or by the division of shares into shares of different classes or by both these methods.

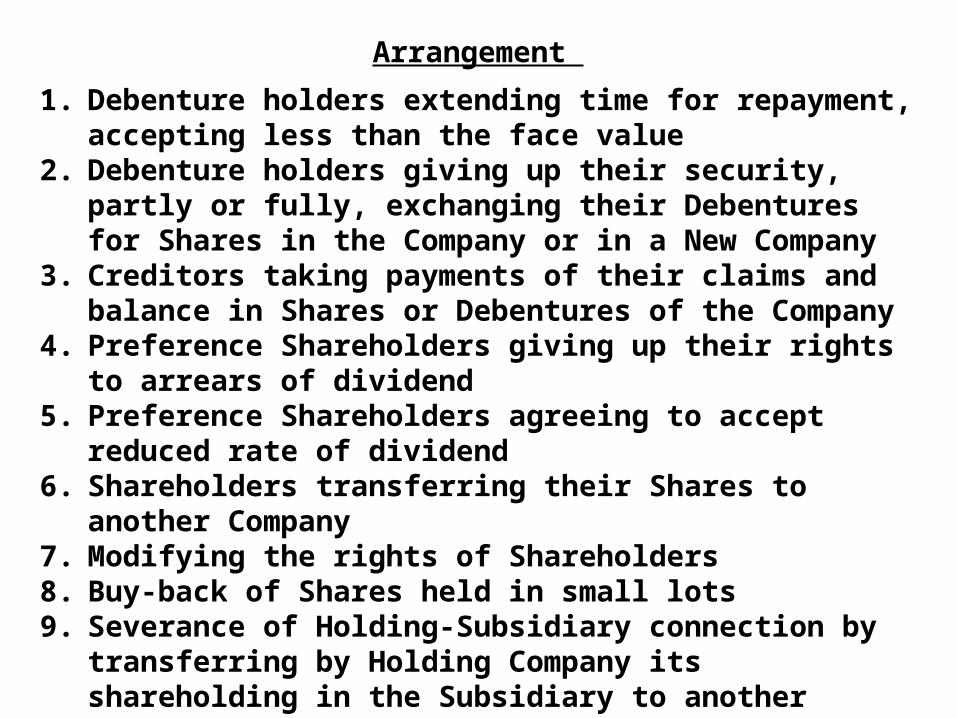

Arrangement

1. Debenture holders extending time for repayment, accepting less than the face value

2. Debenture holders giving up their security, partly or fully, exchanging their Debentures for Shares in the Company or in a New Company

3. Creditors taking payments of their claims and balance in Shares or Debentures of the Company

4. Preference Shareholders giving up their rights to arrears of dividend

5. Preference Shareholders agreeing to accept reduced rate of dividend

6. Shareholders transferring their Shares to another Company7. Modifying the rights of Shareholders8. Buy-back of Shares held in small lots 9. Severance of Holding-Subsidiary connection by transferring by

Holding Company its shareholding in the Subsidiary to another Company and allotment of Shares by it to the Shareholders of the Holding Company

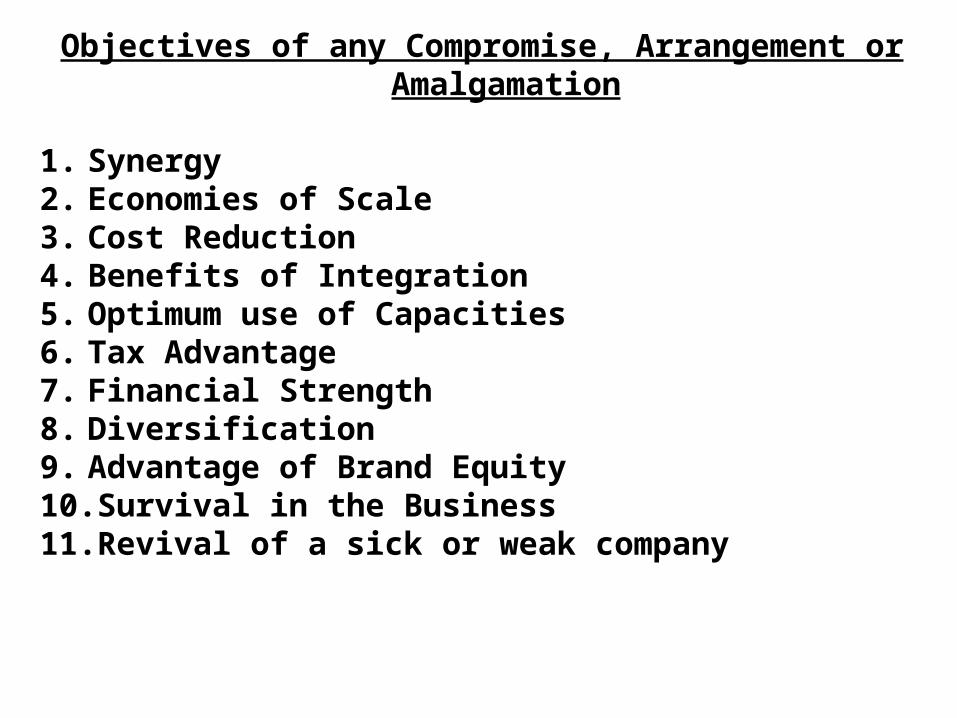

Objectives of any Compromise, Arrangement or Amalgamation

1. Synergy2. Economies of Scale3. Cost Reduction4. Benefits of Integration5. Optimum use of Capacities6. Tax Advantage7. Financial Strength8. Diversification9. Advantage of Brand Equity10. Survival in the Business11. Revival of a sick or weak company

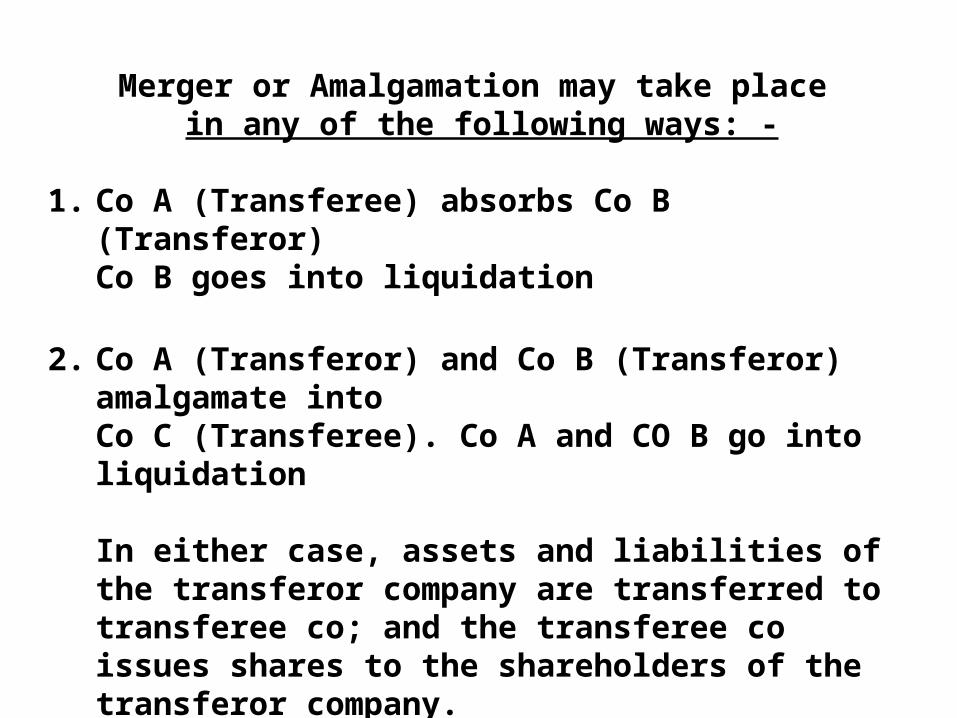

Merger or Amalgamation may take place in any of the following ways: -

1. Co A (Transferee) absorbs Co B (Transferor)Co B goes into liquidation

2. Co A (Transferor) and Co B (Transferor) amalgamate into Co C (Transferee). Co A and CO B go into liquidation

In either case, assets and liabilities of the transferor company are transferred to transferee co; and the transferee co issues shares to the shareholders of the transferor company.

Transferor Company ceases to exist

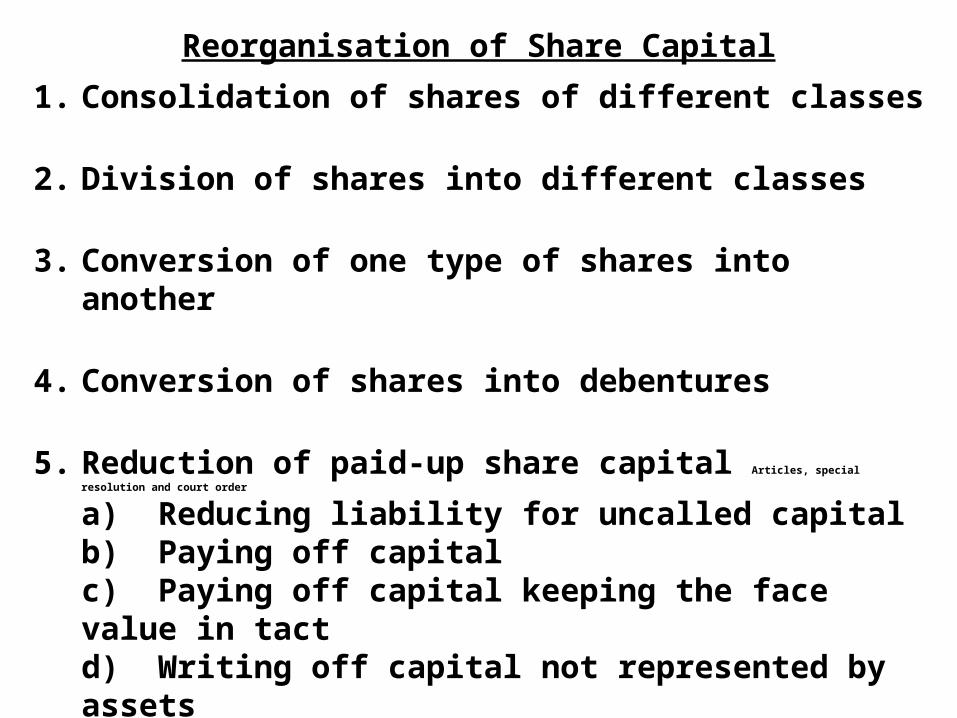

Reorganisation of Share Capital

1. Consolidation of shares of different classes

2. Division of shares into different classes

3. Conversion of one type of shares into another

4. Conversion of shares into debentures

5. Reduction of paid-up share capital Articles, special resolution and court order

a) Reducing liability for uncalled capitalb) Paying off capitalc) Paying off capital keeping the face value in tactd) Writing off capital not represented by assets

Section 391(complete Code for Single window clearance Refer Slide 12)

1. Application for Compromise or Arrangement can be made either by the Company or by any Creditor or any Member or any Class of them or by the Liquidator of a Company which is being wound up. Refer Slide 14

2. Application has to be made to the Company Law Tribunal

3. CLT may call a meeting of the Creditors or Members to be called, held and conducted in a manner as the CLT may direct. Refer Slide 26

4. Majority in number representing three-fourth in value of the Creditors or Members or any Class of them, present and voting, either in person or by proxy, must agree to such Compromise or Arrangement. (Subsequent approval by individual affidavit allowed as was held in SM Holdings

Finance Ltd Vs Mysore Machinery manufactureres Ltd.)

Section 391 (continued)

4. If CLT sanctions the scheme, it is binding on all creditors, members, company, liquidator and the contributories

5. Before the CLT issues any order, it has to satisfy that the applicants have submitted to it all material facts relating to the Company such as latest Financial Position, latest Auditor’s Report and the pendency of any Investigation of the company under Sections 235 to 251 of the Act. Court rejected the petition

since authenticated financial statements were not placed before the meeting – Bharat Synthetics Ltd Vs bank of India (1995)

6. Order of the CLT is effective only after a certified copy of the order is filed with the Registrar.

7. Copy of every such order has to be affixed to every copy of Memorandum of the company.

8. CLT may stay the continuation or commencement of any suit or proceedings against the company, if it thinks fit.

Companies eligible to enter into a scheme of Compromise and Arrangement

As per Section 390, any company liable to wound up under the act can enter into a scheme of Compromise and Arrangement.

Therefore it does not debar amalgamation of financially sound companies.

There is no bar to a company amalgamating with a fifteen-day old company having no assets and business

It is not necessary that the companies must be carrying on similar businesses in order to be eligible for amalgamation.

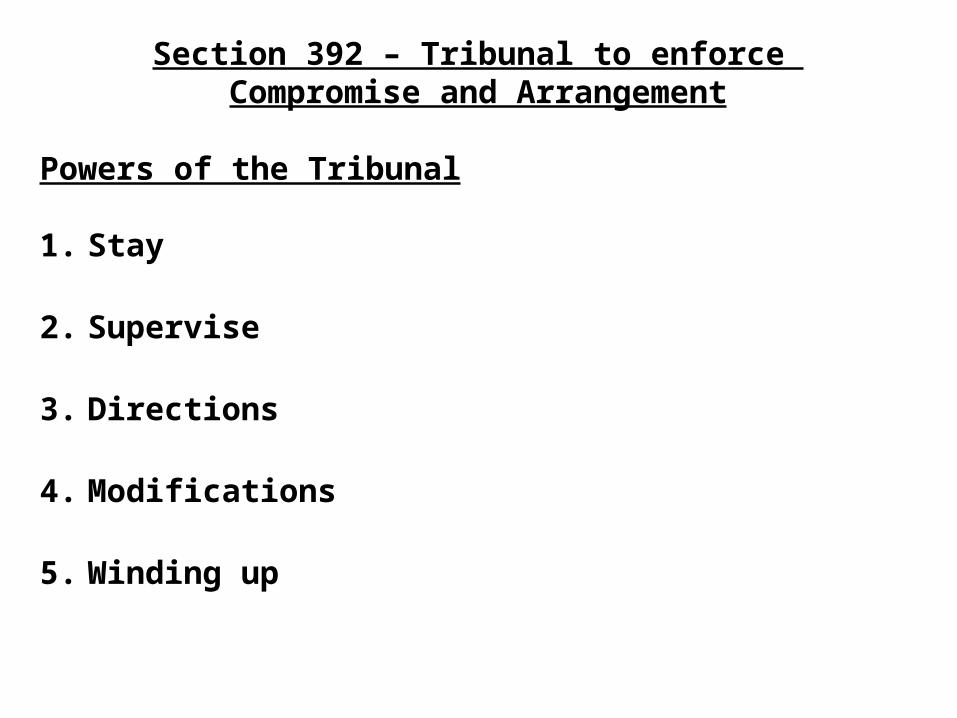

Section 392 – Tribunal to enforce Compromise and Arrangement

Powers of the Tribunal

1. Stay

2. Supervise

3. Directions

4. Modifications

5. Winding up

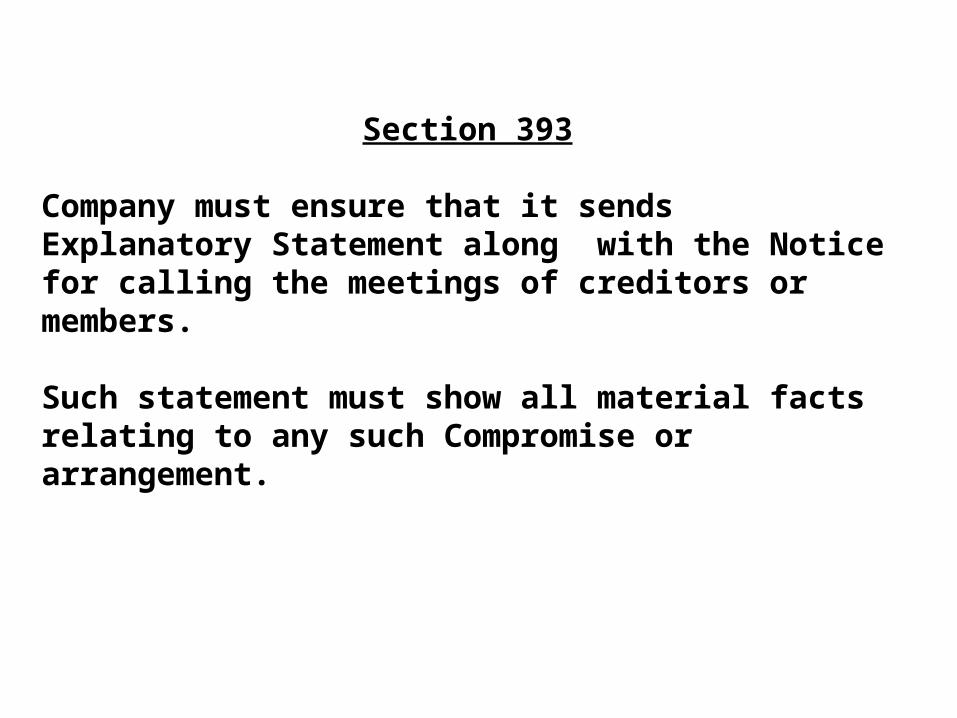

Section 393

Company must ensure that it sends Explanatory Statement along with the Notice for calling the meetings of creditors or members.

Such statement must show all material facts relating to any such Compromise or arrangement.

Section 394

Where application under Section 394 covers amalgamation of two or more companies i.e. transfer of assets and liabilities from the Transferor Company to the Transferee Company, the CLT order may cover the following: -

1. Transfer of the Undertaking, Assets and Liabilities from the Transferor Company to the Transferee company

2. Allotment of shares, debentures etc by the Transferee Company to those who are entitle to as per the scheme

3. Continuation of any legal proceedings by or against the Transferor Company or vice versa

4. Dissolution, without Winding Up, of the Transferor Company5. Protect the interests of those who dissent from such scheme.6. CLT to obtain from Registrar and Liquidator a report that the

affairs of the company are not being conducted in a manner prejudicial to the interests of members or public interest.

7. Certified copy of the CLT order must be filed with the Registrar within 30 days

Section 394 A

CLT must give Notice to the Central Govt of every application made under S. 391 and S. 394.

CLT shall take into account any representation made by the Central Govt before passing any order

Applicability of Section 77 of the Companies Act

Section 77 provides that a company limited by shares cannot buy its own shares

Exception is provided in Section 77 A for Buy back of its own shares

But take the following examples -------------

1. A Ltd (Holding Company) and B Ltd (Subsidiary Company)A merges with B or vice versa

2. A Ltd holds the shares in B Ltd or vice versa(No holding – subsidiary relationship)A merges with B or vice versa

In either case, the transferee company would end up holding its own shares.

This would mean contravention of Section 77 of the Companies Act.

Solution would be -------

Transfer the shares so held to a third party before the scheme of amalgamation is put into process.

In the case of Himachal Telematics Ltd Vs Himachal Futuristic Communication Ltd.(1996), Delhi High Court has held that non-compliance with the provisions of Section 42 and 77 of the Act would not be bar to sanctioning a scheme of amalgamation.

Similar judgment was followed by Karnataka High Court in the case of Consolidated Coffee Ltd. (1999)

Should the Objects Clause of the Amalgamating Companies include the “the power to amalgamate” ?

In the case of Sir Mathuradas Vissanji Foundation (1996) case, the Bombay High Court has held that it is not necessary to have such a power in the objects clause. Section 391 to Section 394 of the Companies Act confer wide powers to the High Court to sanction amalgamation.

Similar views have been expressed by the High Court in Rangakala Investments Ltd.(1995), Aimco Pesticides Ltd. (1999) and Feedback Reach Consultancy Ltd. (2003)

It has also been held that there need not be union or identity between the objects of the Transferor company and the Transferee Company.

It has been held in the case of PMP Auto Indus Ltd. (1994) that Companies carrying entirely dissimilar businesses can amalgamate.

Valuation of Shares and Share Exchange ratio

Amalgamation involves allotment of shares by the Transferee Company to the shareholders of the Transferor Company.

Valuation Experts usually work out the valuation and exchange ratio based on number of factors such as ----

1. Stock Exchange prices and past history2. Dividends paid in the past3. Relative growth prospects of the companies4. Pay out Ratio of the Companies5. Relative Gearing of the Companies6. Value of the Net Assets of the companies

Supreme Court has held in the case of Hindustan Lever Employees’ Union Vs HLL (1995), that the share exchange ratio worked out by the valuation experts would be accepted unless fraud or mala fides is proved.

Book Value method has been described as “more of a talking point than a matter of substance”

Supreme Court has held in the case of Hindustan Lever Employees’ Union Vs HLL (1995), that the share exchange ratio worked out by the valuation

experts would be accepted unless fraud or mala fides is proved.

Valuer considered the “Yield Value”, the “Asset Value” and the “Market Value” with appropriate weightage for working out exchange ratio.

Valuation of shares is a technical matter which requires considerable skill and expertise. There are bound to be differences of opinion as to the correct value of shares. The court’s approach would be that of “non-interference” as long as the shareholders of both the companies accept the valuation.

Similar view has been taken by the High Court in the case of Coimbatore Cotton Mills.

In the case of Piramal Spinning and Weaving Mills Ltd (1980), the High Court held that unless the person who challenged the valuation satisfied the court that the valuation arrived at is grossly unfair, the court would not disturb the scheme of amalgamation approved by the shareholders of the two companies.