commercial applications of company law: commentary

TRANSCRIPT

Commercial Applications of Company Law:

Commentary

SECURITIES AND TAKEOVERS

Media specific legend

Dashed border denotes print specific data

Wavy border denotes cd specific data

Double border denotes web specific data

Dot-Dash border denotes electronic specific data

SECURITIES AND TAKEOVERS

Page 2

SECURITIES AND TAKEOVERS

[¶2701] Introduction

This chapter gives an overview of some of New Zealand’s securities laws. This area of law is

usually called “securities regulation”. However, it is undergoing rapid and extensive change. In

the future, it will be known as “financial markets law” as a result of the changes flowing from the

Financial Markets Authority Act 2011 (FMA Act).

1 For an extended discussion of securities regulation in New Zealand, see Chapters 31–34 by S Griffiths in J Farrar (gen ed), Company and Securities Law in New Zealand (2008); G Walker, “Securities Regulation in New Zealand” in G Walker, International Securities Regulation: Pacific Rim, Vols 1–4 (New York: Oxford University Press), Release 2010-2. For a discussion of the changes flowing from the FMA Act, see: P. Maume and G. Walker, “Capital Markets Matter: A New Era in New Zealand Securities Regulation” (2011) 29 C&SLJ 184; P. Maume and G. Walker, “Goodbye to All That: A New Financial Markets Authority for New Zealand” (2011) C&SLJ 239 and P. Maume and G. Walker, “A New Financial Markets Law for New Zealand” (2011) 29 C&SLJ 455.

The laws comprising securities regulation are related to company law because they regulate the

issue of, trading in and acquisition of company securities (in cases involving changes in control of

larger companies).

Until 1978, most of the laws governing the issue of equity and debt securities in New Zealand

were contained in the Companies Act 1955. The position changed when the Securities Act 1978

was passed. Part II of that Act regulates the “ primary market ” where new equity and debt

securities are issued. The Securities Act 1978 was still in force in late 2011.

So-called “ secondary market ” regulation comprises those laws governing trading and dealings

in securities once they have been issued. As of late 2011, secondary market regulation in New

Zealand is principally contained in the the Securities Markets Act 1988 .This Act, the Securities

Act and certain other enactments, however, are expected to be repealed by the Financial Markets

Conduct Bill 2011. The resulting Act will set out a new framework for securities regulation.This

chapter deals with the following key areas:

• regulation of primary offers of securities (Pt II of the Securities Act)

• regulation of secondary trading in securities

• the Financial Markets Bill 2011

• takeovers (the Takeovers Act 1993, and the Takeovers Code 2000 made pursuant to the

Act), and

• substantial security holder disclosure.

SECURITIES OFFERS AND ISSUES

[¶2702] Overview of Recent Legislative Amendments

Key legislative changes include:

the Financial Markets Authority Act 2011

the Securities Amendment Act 2011

the Securities Amendment Regulations 2011

Key features of the Financial Markets Conduct Bill 2011 are discussed in ¶2711.

The FMA Act was discussed in Chapter 2. The passing on the FMA Act meant that some

immediate changes had to be made to the Securities Act 1978 and the Securities Markets Act

1988.

The Securities Act 1978 was amended by the Securities Amendment Act 2011 which largely

came into effect on 1 May 2011. The remaining provisions come into effect in stages and the Act

will be in full force on 1 July 2013. All of Part 1 (“Securities Commission”) and Part 3 (“General

SECURITIES AND TAKEOVERS

Page 3

Investigation and Enforcement Powers”) of the Securities Act 1978 have been repealed. They

have been replaced by Part 1 of the FMA Act (which established the FMA) and Part 3 of the FMA

Act (“General Information-gathering and Enforcement Powers”).

The Securities Markets Act 1988 was amended by the Securities Markets Amendment Act 2011

which came into full effect on 1 May 2011. The changes made by this amending legislation were

also designed to bring into effect certain changes made by the FMA Act

We provide an overview of the the Securities Amendment Regulations 2011 in ¶2705,

[¶2703] How are securities issues regulated?

This section of the chapter summarises the securities law requirements that apply where a

company is proposing to create and issue new securities. Such new securities may be shares or

debentures. In the Securities Act 1978, shares are termed “equity securities” and debentures are

termed “debt securities”. An issue of new securities is referred to as a primary offer of securities.

The different types of primary offers are described in Chapter 19.

The company law aspects of securities issues are dealt with at some length in Chapter 19 (issues

of equity securities) and Chapter 20 (issues of debt securities). In those chapters, we noted that

the securities laws impose disclosure requirements on an issuing company (“an issuer”) that

apply except in relation to certain excluded or exempt kinds of offers as described below.

Securities regulation also imposes restrictions on advertising and the conduct of securities offers

that are designed to protect the interests of the investing public. These requirements are

contained in the Securities Act.

The Securities Act intends to ensure that investors who are considering subscribing for securities

in a company have adequate and accurate information about the company and the securities to

be issued.

2 See the discussion in G Walker, “Securities Regulation, Efficient Markets and Behavioural Finance: Reclaiming the Legal Genealogy” (2006) 36 (3) HKLJ 481–517.

The special information requirements of investors in securities arise, in part, from the intangible

nature of a security (as opposed, for example, to the tangible nature of a car). Thus, we can

assess a car by inspection but the same considerations do not apply for a share certificate. More

generally, we can describe the relationship between a seller and a buyer of securities as one of

informational asymmetry — that is, the seller and the buyer do not necessarily share the same

information about the security. An asymmetry arises because the seller knows more about the

securities than the buyer. One of the aims of securities regulation is to reduce informational

asymmetry by way of disclosure. Professor James D Cox of Duke University School of Law has

described the need for these disclosure requirements in the following way:

“The securities laws exist because of the unique informational needs of investors.

Unlike cars and other tangible products, securities are not inherently valuable. Their

worth comes only from the claims they entitle their owner to make upon the assets

and earnings of the issuer, or the voting power that accompanies such claims.

Deciding whether to buy or sell a security thus requires reliable information about

such matters as the issuer’s financial condition … With this data, investors can

attempt a reasonable estimate of the present value of the bundle of rights that

ownership confers.”

3 J Cox, R Hillman and D Langevoort, Securities Regulation: Cases and Materials (5th ed, 2006), p 1.

The Securities Act also contains provisions regulating the conduct of an offer of securities in order

to ensure that potential investors are provided with the necessary information and are able to

consider and act on it free from inappropriate sales practices.

New Zealand courts consider the main purpose of the New Zealand securities regulation regime

to be investor protection: see the discussion of Re AIC Merchant Finance Ltd; National Mutual Life

Nominees Ltd v Watson, below.

SECURITIES AND TAKEOVERS

Page 4

[¶2704] Which offers are subject to the disclosure and other

requirements in the Securities Act?

We noted at ¶2602 that the Securities Act 1978 is mainly concerned with ensuring that those

who are offered company securities have sufficient information to make an informed judgement

as to whether to take up the offer and subscribe for the securities. Section 33 of the Securities

Act prohibits the offering of a security to the public in the absence of a registered prospectus or

an investment statement. The provision states as follows:

No security shall be offered to the public for subscription, by or on behalf of an issuer,

unless—

(a) the offer is made in, or accompanied by, an authorised advertisement that is an

investment statement that complies with this Act and regulations; or

(b) the offer is made in an authorised advertisement that is not an investment

statement; or

(c) the offer is made in, or accompanied by, a registered prospectus that complies

with this Act and regulations

Where s 33 applies, all of the provisions of Pt 2 of the Act apply. For s 33 to apply, there must

be:

• a security

• that is offered

• to the public.

What is a “security”?

For s 33 to apply, what is offered to the public must be a “security”.

5 The leading decision on the definition of a security is Culverden Retirement Village Ltd v Registrar of Companies (1997) 8 NZCLC 261,301 (PC).

In this way, the definition of a security is the gateway to the application of the Act. Section 2D(1)

of the Act is the principal definition section. It begins by defining a security in general terms as

“any interest or right to participate in any capital, assets, earnings, royalties or other property of

any person”. Section 2D(1) then goes on to include the following instruments as securities:

• an equity security

• a debt security

• a unit in a unit trust

• an interest in a superannuation scheme

• a life insurance policy

• any interest or right that is declared by regulation to be a security for the purposes of the

Securities Act, and

• any renewal or variation of the terms or conditions of a security.

The first five of the above instruments are further defined in s 2(1) — the interpretation section

of the Securities Act. The interpretation section also contains a definition of another type of

security that is not referred to in s 2D(1). This is a participatory security , which s 2(1) defines

as any security other than one of the first five instruments listed above. This definition is

intended to cover such interests as partnership interests in racehorses or timeshares.

For the most part, the Act is concerned with the issuance of debt securities and equity securities.

The most common form of debt security is a debenture. A debenture is an interest-bearing loan

to a company. Equity securities are shares in a company that carry ownership and control

rights.

SECURITIES AND TAKEOVERS

Page 5

What interests are exempt from the operation of the Act?

Some interests are exempt or partially exempt from the operation of the Securities Act. These

are specified in s 5.

First, some interests are exempt from Part 2 of the Act. These include interests in real estate

where a separate certificate of title can be issued.

6 Section 5(1)(b), Securities Act 1978.

Secondly, some interests are exempt from some provisions of the Act. For example, the issuance

of debt securities by a registered bank does not require the use of a disclosure document such as

a prospectus.

7 Section 5(2C).

Further, s 5(2CA) permits advertisements that state that the issuer is considering making an

offer, include the broad terms of the proposed offer, and seek preliminary expressions of interest.

In the United States, this kind of activity is called “testing the waters”.

In 2004, a new category of partial exemption, one applying to “eligible persons”, was created.

8 Section 5(2CB).

Eligible persons are persons who are wealthy, experienced in investing money, or experienced in

the industry or business to which the security relates as defined.

9 Section 5(2CC).

What is an “offer”?

Section 2(1) defines an offer as including an invitation and any proposal or offer to make an

offer. In this way, the term “offer” is given a much broader meaning than the term has in

contract law: see Orr v Martin.

10 (1991) 5 NZCLC 67,383.

The reason why the term “ offer ” has an extended meaning is because the Securities Act has

investor protection goals, one of which is the regulation of the activity of fund-raising. It would

be difficult to regulate the activity of fund-raising if only contractual offers were caught by the

Act. For these reasons, case law on the term “offer” in the Securities Act has stated that the term

includes invitations to treat and making securities available by mere creation and word of mouth.

Who are the “public”?

As stated, s 33 prohibits the offering of a security to the public . Obviously, this means that

there must be some definition of the term “public”. Defining that term is not easy. Australia

avoided this problem by simply requiring a disclosure document for all offers of securities and

then providing exemptions for, among other things, small-scale personal offers, offers to

sophisticated investors and offers to professional investors. This is the solution adopted in the

Financial Markets Conduct Bill 2011.

11 In Australia, s 706 of the Corporations Act 2001 states: “An offer of securities for sale needs disclosure unless section

708 says otherwise.” Section 708 then lists the types of offers that do not need disclosure.

Section 3 of the Act attempts to define the term “public”.

Section 3(1) provides:

“Any reference in this Act to an offer of securities to the public shall be construed as

including—

(a) A reference to offering the securities to any section of the public, however

selected; and

(b) A reference to offering the securities to individual members of the public

selected at random; and

(c) A reference to offering the securities to a person if the person became known

SECURITIES AND TAKEOVERS

Page 6

to the offeror as a result of any advertisement made by or on behalf of the offeror

and that was intended or likely to result in the public seeking further information

or advice about any investment opportunity or services,—

whether or not any such offer is calculated to result in the securities becoming

available for subscription by persons other than those receiving the offer.”

While s 3(2) provides:

“None of the following offers shall constitute an offer of securities to the public:

(a) An offer of securities made to any or all of the following persons only:

(i) relatives or close business associates of the issuer:

(ii) persons whose principal business is the investment of money or who, in

the course of and for the purposes of their business, habitually invest money:

(iia) persons who are each required to pay a minimum subscription price of at

least $500,000 for the securities before the allotment of those securities:

(iib) persons who have each previously paid a minimum subscription price of

at least $500,000 for securities (the initial securities) in a single

transaction before the allotment of the initial securities, provided that—

(A) the offer of the securities is made by the issuer of the initial securities;

and

(B) the offer of the securities is made within 18 months of the date of the

first allotment of the initial securities

(iii) any other person who in all the circumstances can properly be regarded

as having been selected otherwise than as a member of the public:

12 The leading decision on s 3(2)(a)(iii) is Lawrence v Registrar of Companies (2004) 9 NZCLC

263,480 (CA).

(b) An invitation to a person to enter into a bona fide underwriting or sub-

underwriting agreement with respect to an offer of securities:”

Section 3(1) is the inclusive part of the definition, and paragraphs (a)– (c) are aimed at negating

decisions made before the passing of the Act that had the effect of narrowing the meaning of

term “the public”.

Section 3(2) is the exclusive part of the definition, and defines those offers that fall outside the

provisions of Pt II. The most useful of the exclusionary provisions from an issuer’s point of view

are those that enable an offer to be made without a prospectus to relatives, close business

associates and habitual investors. Section 3(2)(a)(iia) was inserted into the Act in 2004. It

follows s 708(8) of the Australian Corporations Act 2001, which provides that offers to

sophisticated investors (that is, those investing at least $A500,000) do not require disclosure. In

addition to these exclusions, an underwriting agreement is also outside the terms of the Act.

Section 3(2)(a)(iib) was inserted into the Act in July 2009 by the Securities Disclosure and

Financial Amendment Act 2009. It introduces a new category of exempt offers. This is an offer of

securities (“the further securities”) made only to persons who have previously paid a minimum

subscription price of at least $500,000 for securities.

Section 3(3) makes it clear that a pre-existing relationship with the offeree is not sufficient to

avoid the application of Pt II. Under this subsection, the fact that an offer is made to a person

who is a purchaser of goods from, or is an employee or client of, or the holder of securities in,

the issuer does not of itself prevent such an offer from being an offer to the public.

Under s 3(5), “proof of an offer to one member of the public selected as a member of the public

shall be prima facie evidence of an offer of securities to the public”.

Section 33 of the Act provides that securities may be offered to the public only by way of an

SECURITIES AND TAKEOVERS

Page 7

investment statement or registered prospectus.

The provision is central to the investor protection rationale of the legislation. It is designed to

enable investors to make informed decisions about the financial state of the issuing entity. The

term “public” implies that disclosure is not necessary every time a company offers securities, and

is complemented by statutory provisions exempting “non-public” offerings. In most cases,

however, the threshold question for an issuing entity is whether its securities will be offered to

“the public”. Because the term “public” is vague, there has been considerable litigation

concerning its meaning.

What did Kiwi Dairies say about s 3?

Some of the problems surrounding s 3 have been resolved by the leading Court of Appeal

decision of Securities Commission v Kiwi Co-operative Dairies Ltd.

14 (1995) 7 NZCLC 260,828; [1995] 3 NZLR 26 (CA). See also Lawrence v Registrar of Companies (2004) 9 NZCLC

263,480 (CA).

Here, Kiwi Dairies operated as a cooperative dairy company. Dairy farmers had to be members of

the cooperative in order to sell milk. Each bought one share for that purpose. There were a total

of 2,652 supplying shareholders. Kiwi Dairies solicited funds from its shareholders via a monthly

newsletter and paid interest on funds deposited. No prospectus was issued. In the High Court,

Doogue J held that the shareholders were all close business associates of Kiwi and hence the

offers did not constitute an offer to the public. In a unanimous judgment, the Court of Appeal

reversed that decision.

The Court of Appeal set out five general principles applicable to s 3 and the exceptions under s

3(2)(a). This decision has clarified a number of the problems associated with s 3:

• The first principle flowing from the Kiwi Dairies decision is that the exceptions will not

assist an offeror from being caught by s 3(1) unless all the persons to whom the offer was

made come within the exceptions in s 3(2). It is the offering of the security for subscription

which breaches s 33, not the final allotment. Consequently, in determining whether an offer

must comply with Pt II of the Act, one must consider all those who have received an offer,

even if some or all of them did not accept the offer. Where the question of whether the offer

is public or non-public is “evenly balanced”, the courts should find there is a public offer. This

means that an issuer seeking to uphold an allotment pursuant to s 3 must consider

examining all offerees. Such a result is objectionable on economic grounds since the process

is costly, time-consuming and inefficient.

• The second principle we can extract from Kiwi Dairies is that, while the section does not

provide any numerical limits, the larger the number of offerees the greater the possibility of s

3(2) not applying. Here, s 3(5) (proof of an offer to one member of the public is prima facie

proof of an offer to the public) is also relevant.

• The third principle is that the burden of proof is on the issuer that wishes to rely on the

exemptions in s 3(2). This approach, coupled with the requirement to show that each offeree

comes within appropriate exemption, places a substantial weight on an offeror. An error of

judgment in offering to one non-exempt offeree leaves the offeror (and its officers) liable for

the repayment of all the funds received under s 37(6).

• The fourth principle is that the determination of whether a person falls within a s 3(2)

exception is made on an objective basis.

• The fifth general principle goes to the purpose of the Act as interpreted by the courts. In

Re AIC Merchant Finance Ltd (in rec); National Mutual Life Nominees Ltd v Watson,

Richardson J stated:

“The pattern of the Securities Act and the sanctions it imposes make it plain that

the broad statutory goal is to facilitate the raising of capital by securing the

timely disclosure of relevant information to prospective subscribers for securities.

In that way the Act is aimed at protection of investors. That aim is achieved by

regulating the conduct of issuers of securities and by providing sanctions for

infringement by those issuers and their officers.”

SECURITIES AND TAKEOVERS

Page 8

15 (1990) 5 NZCLC 66,153 at pp 66,158–66,159; [1990] 2 NZLR 385 (CA) at p 391.

Richardson J further commented:

“It is perhaps true to say that the premise underlying the Securities Act, as with much

commercial law, is that the best protection of the public lies in full disclosure of the

company’s affairs and of the security it is offering. That then allows the investor to

make an informed investment decision, which in turn facilitates the functioning of

financial markets.”

16 Ibid at NZCLC p 66,159; NZLR p 392.

The Court of Appeal in Kiwi Dairies cited these comments of Richardson J with approval.

[¶2705] What must be disclosed?

If an offer by a company to issue securities does not come within:

• the exclusionary provisions of s 3(2), or

• the exemptions within s 5 of the Securities Act 1978,

the disclosure obligations contained in s 33 of the Act apply. In that event, the issuing

company will be required to prepare:

• an authorised advertisement that is an investment statement, or

• an authorised advertisement that is not an investment statement, or

• a registered prospectus.

In practice, the two most important forms of disclosure document are the investment

statement and the prospectus .

It is important to understand that, in order to comply with s 33, an issuer must prepare (i) a

prospectus, or (ii) an investment statement and a prospectus. This is because:

• s 37(1) requires that securities offered to the public may not be allotted unless at the time

of subscription there was a registered prospectus in existence, and

• s 54B(3) requires that an issuer must send a copy of a registered prospectus to a

prospective investor “on request”.

The introduction of the investment statement

In 1996, changes to the law relating to the offering of securities were made in New Zealand.

These changes came into effect on 1 October 1997. An important change to the Securities Act

was the optional requirement for an investment statement to accompany an offer of securities.

The introduction of investment statements changed the logistics of public offerings in New

Zealand. Some background explanation is necessary.

New Zealand traditionally regulated the primary securities market under the Securities Act by

requiring the registration of a disclosure document called a “prospectus” when securities were

offered to the public.

17 For a full discussion, see P Fitzsimons, “Public Offerings of Securities in New Zealand”, in G Walker (gen ed), Securities Regulation in Australia and New Zealand (2nd ed, 1998), p 352.

Each investor was required to receive a prospectus before subscribing for securities. A prospectus

had to contain extensive information (including financial information). Sometimes, the end result

was a complex and lengthy document often criticised for increasing regulatory costs without

assisting the average New Zealander to determine whether or not to invest in a particular

security or allow him or her to compare the merits of competing investment products. The

solution was to introduce a shorter, more “user friendly” disclosure document called an

“investment statement”.

What must be included in an investment statement?

SECURITIES AND TAKEOVERS

Page 9

Section 38D states that the purpose of the investment statement is to provide certain key

information that is likely to assist a “prudent but non-expert person” to decide whether or not to

subscribe for securities, and also to bring the attention of such a person to the fact that other

important information can be obtained from other documents.

Investment statements seek to achieve two policy goals. The first is to better inform investors . The second is to reduce the compliance burden placed on issuers by lowering costs. From the

outset, it was unclear whether the second goal could be achieved in practice, since issuers would

always have to prepare two documents — the investment statement and the prospectus —

which, without more, would increase compliance costs. A prospectus still has to be prepared

because of the need to comply with s 37(1), which states that a security cannot be allotted

unless a registered prospectus is in existence, and with s 54B(3), the “request disclosure”

provision. On the other hand, by using an investment statement, print runs of the prospectus

might be lowered by (say) 50%. There are, however, serious doubts as to whether the

investment statement regime is working as intended. In April 2000, one practitioner noted that

investment statements were often more complicated than the prospectuses they were supposed

to replace and expressed serious reservations about the new regime.

The form and content of the investment statement is set out in s 38E of the Securities Act.

Section 38E provides that every statement shall be in writing, and state the date at which the

statement is prepared.

In addition to indicating that it is an investment statement, an investment statement is required

to set out certain information at the beginning of the investment statement as well as statements

advising investors to choose their investment adviser carefully. Schedule 13 of the Securities

Regulations 2009 specifies the matters requiring disclosure in an investment statement.

The questions, which have to be answered in the investment statement (in plain English), are:

• What sort of investment is this?

• Who is involved in providing it for me?

• How much do I pay?

• What are the charges?

• What returns will I get?

• What are my risks?

• Can the investment be altered?

• How do I cash in my investment?

• Whom do I contact with inquiries about my investment?

• Is there anyone to whom I can complain if I have problems with the investment?

• What other information can I obtain about this investment?\

The Securities Regulations 2009 have been amended by Securities Amendment Regulations

2011. These amendments include changes to Schedule 13. The key changes include:

requiring disclosure of information on the FMA and the new financial advisers’ regime

telling investors to check the type of adviser they are dealing with, the services the

adviser can provide and the products the adviser can advise on

if the securities being offered are equity securities or life insurance policies, the

investment statement must include the names and addresses of the issuer and the

directors of the issuers as at the date of the investment statement

informing investors about the opportunity to search for information about registered

financial providers at http://www.fspr.govt.nz

SECURITIES AND TAKEOVERS

Page 10

provide information about the relevant dispute resolution scheme, and

inform investors that they can also complain to the FMA if they have concerns about the

behaviour of a financial adviser.

21 Regulation 14 of the Securities Amendment Regulations 2011.

There are a number of essential characteristics of investment statements. These include the

following:

• An investment statement is the principal selling document of an offer. A prospectus is

required to be provided only on request.

20 Section 54B(3).

• Investment statements are not required for all securities offerings. Call debt securities, call

building society shares and bonus bonds do not require an investment statement.

• One important feature of the Regulations surrounding investment statements is that they

allow a significant degree of flexibility in the presentation and use of an investment

statement. The Regulations do not limit the information, statements or matters that can be

contained in the investment statement.

22 Section 38E(3).

This enables an investment statement to be included in other documents or be provided with

additional information over and above that specified. An investment statement may also

relate to one or more kinds of securities or one or more offers of subscriptions for securities

of a particular kind.

23 Section 38E(2).

• NZX listing rules require that draft offering documents be submitted for scrutiny.

24 NZX Listing Rule 5.2.2.

What must be included in a prospectus?

As a preliminary matter, s 37(1) states that securities offered to the public cannot be allotted

unless at the time of the subscription there was a registered prospectus in existence (subject to

the relief regime appearing in s 37AA and following). This means that all offers of securities to

the public require a registered prospectus. Section 39 states that every prospectus and registered

prospectus must:

• be in writing

• be dated

• specify any documents to be endorsed on or attached to the prospectus or registered

prospectus for registration purposes, and

• contain all the information, statements, certificates and other matters that it is required to

contain by the Regulations.

What is a ”simplified disclosure prospectus”?

An offer of securities to the public made on behalf of an issuer may be accompanied by a

simplified disclosure prospectus: s 2 of the Securities Act. A simplified disclosure prospectus is a

registered prospectus that may be used only if the regulations provide for the use of such a

prospectus. The Securities Regulations 2009, as amended by the Securities Amendment

Regulations 2011, impose limits on the types of securities that may be offered by means of a

simplified disclosure prospectus. Simplified disclosure prospectuses may be used by already listed

issuers when offering:

equity securities

SECURITIES AND TAKEOVERS

Page 11

debt securities, or

units in a unit trust.

How is a prospectus registered?

The role of the Registrar of Companies in registering prospectuses has been redefined by the

Securities Amendment Act 2011. While the Registrar of Companies will still be in charge of the

formal registration process, the FMA will have to consider whether prospectuses are misleading

or false, and contain all required information (s 43A of the Securities Act).The Registrar will have

to notify the FMA of any registration or trust deed (s 43C). The FMA has five days (or longer

when giving written notice) to assess the prospectus and, if required, issue a stop order. Some

continuous offers as prescribed by the FMA will be exempt from this regime (s 43D(2)).

A prospectus is registered by delivering it to the Registrar of Companies in Auckland. Section 41

of the Securities Act requires that every prospectus delivered to the Registrar for registration

must have endorsed on it:

• any necessary consents to its issue from an expert, and

• all documents, information, certificates and other matters which the Regulations require.

In addition, the prospectus must be signed by:

• the issuer of the prospectus if the issuer is an individual

• every person who is a director of the issuer, and

• every promoter of the securities to which the prospectus relates.

Under s 42 of the Act, the Registrar may refuse to register a prospectus if, for example, it does

not comply with the Act. Further, the FMA may suspend or cancel the registration of a prospectus

if, for example, it considers that the registered prospectus is false or misleading as to a material

particular or omits any particular. The nature and extent of consideration that the FMA gives to a

prospectus is at the FMA’s discretion. If the FMA is of the opinion that the prospectus does not

comply with the Securities Act 1978 it may prohibit the allotment of securities and cancel the

registration of prospectuses at any time (s 43G). In addition, the FMA will, at any time, be able to

prohibit the distribution of investment statements that are considered misleading, unclear or

incoherent with the registered prospectus (s 43F).

29 See s 43C.

What is the register of securities offers?

Section 43N of the Securities Act establishes a “register of securities offers” (which may be in

electronic form) at the Registrar of Companies’ office. The idea underlying this register is that

any interested person should be able to gain information contained in prospectuses or other

documents that might be relevant to investors (s 43O). The register will contain all relevant

information including names of issuers and copies of all relevant documents.

What if the information changes during the offer period?

Sometimes the information contained in a prospectus becomes out of date during the period

between delivery and expiry, or new developments occur that should be disclosed. In this case,

the issuer must deliver a memorandum of amendments to the Registrar and have that

memorandum registered: s 43 Securities Act. The memorandum of amendments must correct

the defect in the original prospectus. No registered prospectus can be distributed after

amendment unless all the amendments have been incorporated in the prospectus or attached by

way of an instrument to every copy of the prospectus that is distributed.

30 Section 34.

SECURITIES AND TAKEOVERS

Page 12

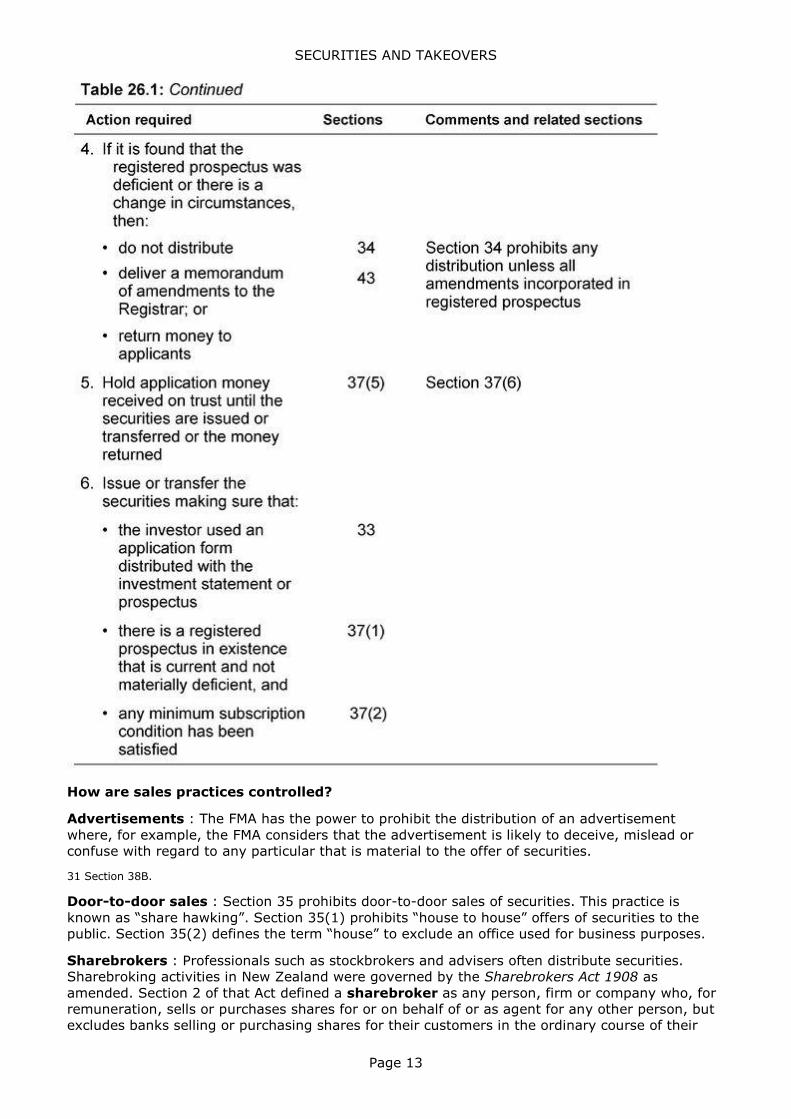

[¶2705] What procedure must be followed for an offer?

An offer that requires disclosure to investors must be conducted in accordance with Pt 2 of the

Securities Act 1978. The procedure for an offer of equity securities to the public is summarised in

Table 26.1.

SECURITIES AND TAKEOVERS

Page 13

How are sales practices controlled?

Advertisements : The FMA has the power to prohibit the distribution of an advertisement

where, for example, the FMA considers that the advertisement is likely to deceive, mislead or

confuse with regard to any particular that is material to the offer of securities.

31 Section 38B.

Door-to-door sales : Section 35 prohibits door-to-door sales of securities. This practice is

known as “share hawking”. Section 35(1) prohibits “house to house” offers of securities to the

public. Section 35(2) defines the term “house” to exclude an office used for business purposes.

Sharebrokers : Professionals such as stockbrokers and advisers often distribute securities.

Sharebroking activities in New Zealand were governed by the Sharebrokers Act 1908 as

amended. Section 2 of that Act defined a sharebroker as any person, firm or company who, for

remuneration, sells or purchases shares for or on behalf of or as agent for any other person, but

excludes banks selling or purchasing shares for their customers in the ordinary course of their

SECURITIES AND TAKEOVERS

Page 14

business and members of an authorised futures exchange where such members sell or purchase

share options. Section 165 of the Financial Advisers Act 2008 repealed the Sharebrokers Act. The

Financial Advisers Act provides a new regime for authorised financial advisers such as

sharebrokers: see Chapter 26.

[¶2706] What if the disclosure document is wrong or incomplete?

We saw at ¶2705 that defects in a disclosure document can be cured by the issuer delivering an

instrument of amendments under s 43 of the Securities Act 1978. But what happens when the

issuer fails to do this, and a person subscribes for securities on the basis of a defective disclosure

document? In these circumstances, a number of consequences may follow.

First, s 34 of the Securities Act prohibits the distribution of a security if at the time of the

distribution the registered prospectus false or misleading in a material particular.

Secondly, if the FMA is of the opinion that a registered prospectus is false or misleading as to a

material particular or does not comply with the Act, it may suspend or cancel the prospectus.

Thirdly, the liability and offence provisions contained in s 55– 65 may apply.

Anybody who subscribes for securities on the basis of a defective disclosure document may have

remedies against the issuer and others involved in the preparation of the document.

In R v Steigrad

39 [2001] NZCA 304

the court considered directors’ liability for statements in offering documents that become untrue

owing to a change in circumstances after the prospectus or advertisements initially became

available to the public. The court held that promoters and directors of finance companies have a

duty to monitor the ongoing accuracy and truthfulness of statements made in offering

documents. Accurate disclosure is important throughout the life of a prospectus or duration of

advertising campaign. The existence of an untrue statement in a prospectus must be determined

at the time the prospectus is distribution. The court rejected Mr Steigard’s argument that it is

unfair and difficult for directors to monitor the continuing accuracy of statements made in

prospectuses and advertisements. Finance companies voluntarily enter the business of offering

securities to investors in order to make money, and have a duty to ensure the timely disclosure

of relevant information to prospective subscribers for securities.

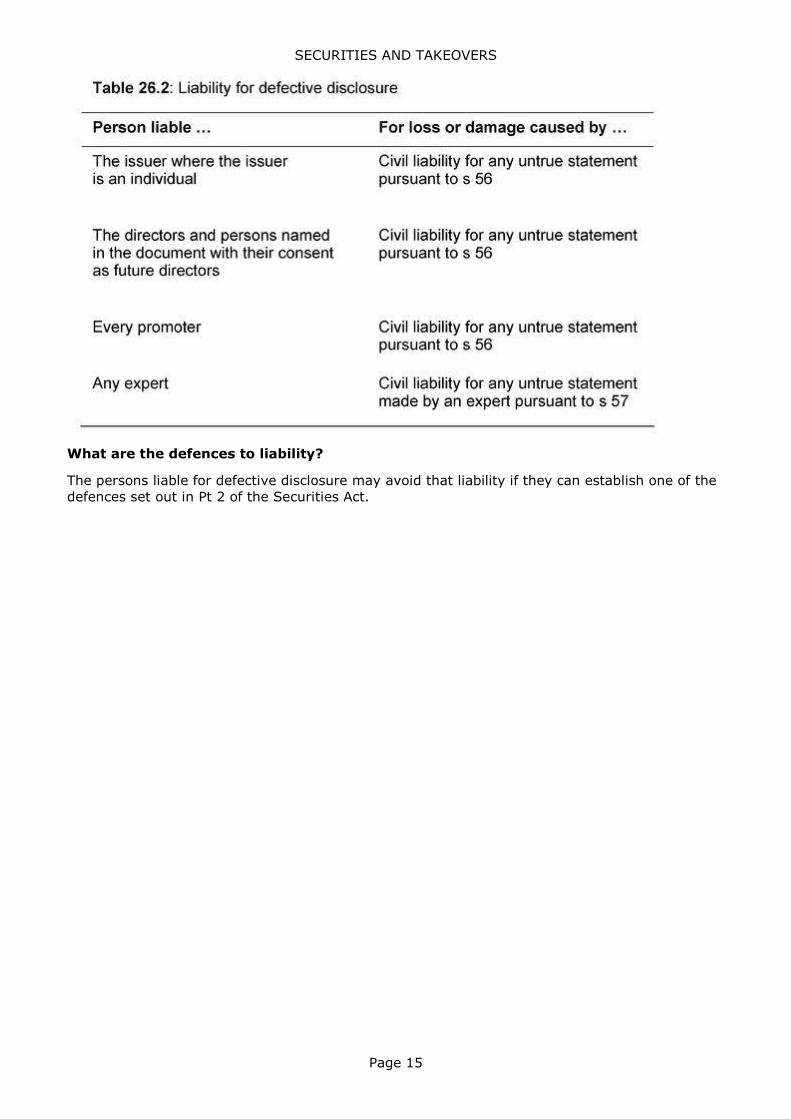

What remedies does a person have for defective disclosure?

The main remedies available to a person who suffers loss or damage because of defective

disclosure are set out in Table 26.2.

SECURITIES AND TAKEOVERS

Page 15

What are the defences to liability?

The persons liable for defective disclosure may avoid that liability if they can establish one of the

defences set out in Pt 2 of the Securities Act.

SECURITIES AND TAKEOVERS

Page 16

Finally, note that s 13 of the Securities Markets Act 1988 (which prohibits misleading or

deceptive conduct in relation to dealings in listed and non-listed securities) has a wide application

and applies to all dealings in securities, not only trading: see section 13(2). This means that s 13

can catch primary market activities. Violation of s 13 attracts the civil remedies provided for in Pt

5, subpart 3.

TRADING IN SECURITIES

[¶2707] What is “secondary trading” in securities?

Company securities include equity securities and debt securities. Secondary trading in company

securities is the buying and selling of company securities that have previously been issued by the

company.

What is an example of a secondary trade? Assume Michelle was issued 1,000 XYZ Ltd shares

when XYZ Ltd floated on the NZSX in 2005. She likes the look of the current market price and

decides to sell them. So she sells them — through a stockbroker — to Brian. This sale to Brian is

a secondary trade in XYZ Ltd shares.

[¶2708] What laws govern trading in already-issued securities?

The laws that regulate trading in already-issued securities fall into three broad groups:

SECURITIES AND TAKEOVERS

Page 17

• laws and other rules regulating securities market intermediaries, such as stockbrokers

• laws that regulate the offer for sale of already-issued securities in some situations, and

• laws prohibiting certain market practices, and misleading or deceptive conduct in

connection with any dealing in securities.

How are securities market intermediaries regulated?

Securities market intermediaries include stockbrokers, investment advisers and futures traders.

Financial Advisers Act 2008 : Sharebrokers in New Zealand were licensed under the

Sharebrokers Act 1908. Section 2 of that Act defined” sharebroker” as “any person … who, for

remuneration, sells or purchases shares for or on behalf of or as agent for any other person”.

Hence, all persons acting as brokers in a sharebroking company must be licensed. As stated

earlier, however, this legislation was repealed by s 165 of the Financial Advisers Act 2008. The

key provisions of the Financial Advisers Act are discussed in Chapter 26.

NZX regulations : The Securities Markets Act 1988 requires that the “market rules” of a

“registered market” be approved by the FMA. The market rules of NZX Limited principally

comprise the Listed Issuer Rules (the “Listing Rules”) and the Participant Rules. The Listed Issuer

Rules were last amended with effect from 6 August 2010. These may be viewed on the NZX

website. The key documents are:

• Listed Issuer Rules, and

• NZX Participant Rules.

Common law : The common law also plays a role in the regulation of securities market

intermediaries. For example, common law imposes duties and obligations arising under the law of

contract and under fiduciary principles.

When are offers for already-issued securities regulated?

A number of cases under Pt 2 of the Securities Act 1978 have involved offers of shares that have

been previously allotted to a person and are then onsold.

Section 6 provides two ways in which such offers may be brought within Pt 2. The first deals with

recently issued securities. Section 6(1) provides that, subject to the other provisions in that

section, nothing in sections 33, 34, 37-38A, 38C-43B and 44B-59 of Pt 2 applies to securities that

have been previously allotted.

Section 6(2) provides that all the provisions of the Act apply to previously allotted securities

(whether those securities were allotted in New Zealand or elsewhere) if the security was

originally allotted with a view to being offered for sale to the public in New Zealand, and the

security had not been offered for sale to the public in New Zealand or to the public outside New

Zealand under an application regime under Pt 5 of the Act.

Section 6(5) provides a presumption that securities were allotted with a view for sale to the

public if the securities were offered to the public within six months of the allotment,

33 Section 6(5)(a).

or if the securities had not been fully paid for at the time the offer was made.

34 Section 6(5)(b).

In Dodge v Snow,

35 (1999) 8 NZCLC 261,803.

Master Venning held (in the context of a summary judgment application) that the defendant

director had an arguable case that the shares in question were previously allotted securities

because the initial issue of shares occurred more than six months before the sale in question.

The second way is under s 6(3), which further extends the application of Pt II to offers of

previously allotted equity securities or securities convertible in equity. This subsection provides:

SECURITIES AND TAKEOVERS

Page 18

“All the provisions of this Act shall apply in respect of an equity security or a security

convertible into an equity security if the holder or offeror, not being the original

allotter, offers the security for sale to the public in New Zealand and the original

allotter advises, encourages, or knowingly assists the holder or offeror in connection

with the offer of sale of the security.” (Emphasis added.)

The additional test to determine whether an offer of previously allotted equity securities must

comply with the Act is therefore whether there is advice, encouragement or knowing assistance

by the original allotter. These terms are not defined in the Act.

Section 6(3) is narrowed to a certain extent by s 6(4), which provides safe harbours. The safe

harbours are:

• offers that are required to be made under the terms of the articles of association or the

constitution

• offers where the holder of the shares receives $200,000, or less, in the space of 12

months, and

• offers to not more than six members of the public (to determine whether or not there has

been an offer to more than six members of the public, s 6(6) deems an offer to have been

made to more than six members of the public where more than six persons “acquire an

interest, whether direct or indirect, in securities of the same class offered to the public”).

Which market practices are prohibited?

Laws dealing with undesirable market conduct appear in the NZX Listing Rules, the common law

and the Securities Markets Act.

NZX Listing Rules : The relationship between the NZX and the listed issuer is contractual.

Pursuant to such contract, the NZX has the discretionary power to cancel or suspend a listing.

36 Listing Rule 5.4.2.

This power may be exercised where a false market in the issuer’s securities exists.

37 Listing Rule 5.4.3(a).

Further, pursuant to NZX Listing Rule 10 (Disclosure and Information), issuers are obliged to

release relevant information to the NZX to the extent necessary to prevent the development or

subsistence of a market for their securities which is materially influenced by false or misleading

statements emanating from the issuer or other persons in circumstances in each case which

would give such information credibility.

38 Listing Rule 10.1.1(c).

Breach of this rule might invite the sanctions contained in Listing Rule 5.4.2.

Common law remedies : New Zealand is a common law country. Section 65 of the Securities

Act provides that nothing in the Act shall limit or diminish, inter alia, any liability that any person

may incur under any rule of law. Hence, common law remedies remain unaffected by the Act.

The most important common law remedies are actions for rescission of contract, deceit, negligent

misrepresentation and breach of contract.

The Securities Markets Act : On 29 February 2008 a regime dealing with “Dealing Misconduct”

was introduced in a new Pt 1 of the Securities Markets Act. This new Pt 1 prohibits several forms

of undesirable market conduct.

Misleading or deceptive conduct : Section 13 of the Securities Markets Act says that a person

must not engage in conduct, in relation to any dealings in securities, that is misleading or

deceptive or likely to mislead or deceive. Violation of s 13 attracts the civil remedies provided for

in Pt 5, subpart 3. For guidance on how this new section will be interpreted by the courts in New

Zealand, see the case law on the Australian cognate s 1041H of the Corporations Act 2001.

39 For analysis, see R Baxt, A Black and P Hanrahan, Securities and Financial Services Law, (7th ed 2008), p 282 ff.

There are also separate bans on specific kinds of misleading conduct (two of which are

SECURITIES AND TAKEOVERS

Page 19

summarised below) and on insider conduct (which is discussed at ¶2709 below).

Market manipulation : Under section 11, it is not permissible to make a statement or

disseminate information if that statement or information is false or materially misleading and is

likely to (inter alia) induce a person to trade in the securities of a public issuer or have the effect

of affecting the price for trading in those securities. Criminal liability attaches to a violation of this

section.

40 Section 11A.

A civil remedy can also be sought.

41 Section 42S.

The cognate provision in the Australian legislation is s 1041A of the Corporations Act.

42 For analysis, see ibid at p 655 ff.

False trading : Under s 11B a person must not do or omit to do anything that is likely to create

a false or misleading appearance of (i) active trading in the securities of a public issuer, or (ii) the

supply, demand, price or value of those securities where the person knows or ought to know that

their act or omission will or is likely to have that effect. Criminal liability attaches to violation of

this section.

43 Section 11D. The cognate provision in the Australian legislation is s 1041B of the Corporations Act.

For analysis, see ibid at p 661 ff.

[¶2709] What is “insider trading”?

A major overhaul of the insider trading legislation in the Securities Markets Act 1988 came into

force in February 2008. The reforms were based on the Australian model.

44 See K Kendall and G Walker, “Insider Trading in Australia and New Zealand: Information that is generally available”

(2006) 24 C&SLJ 343; J Butler, “Are we there yet? The Journey of the Insider Trading Provisions” (2008) 26 C&SLJ 460. For an overview of the Australian law on insider trading, see Austin and Ramsay, Ford’s Principles of Corporations Law, (LexisNexis Butterworths, 13th ed, 2007), para 9.600 et seq; Baxt, Black and Hanrahan, Securities and Financial Services Law, (7th ed, 2008), Chapter 18; Hanrahan, Ramsay and Stapledon, Commercial Applications of Company Law, (12th ed, 2011), Chapter 20 [check]; Ashley Black, “Insider trading and market misconduct” (2011) 29 C&SLJ 313.

In New Zealand, there exist three principal avenues to the control of insider trading. At common

law, a shareholder could recover from a director of a company where the director purchased

shares off the shareholder.

45 Coleman v. Myers [1977] 2 NZLR 225.

However, to succeed with such an action the courts held that it is necessary to establish a

fiduciary relationship between the parties,

46 Woodhouse J stated that some of these factors included a “dependence upon information and advice, the existence of a relationship of confidence, the significance of some particular transaction for the parties, and of course the extent of any positive action taken by or on behalf of the directors to promote it”. Ibid, p 325.

which would normally be only available in private companies.

47 In Cottom v GUS Properties Ltd (1995) 7 NZCLC 260,821 the Court of Appeal confirmed the applicability of the

Coleman v Myers decision and discussed that decision in the context of a non-listed company which had 200 shareholders. The court was prepared to find that directors “intending to participate as purchasers in the share exchange, owed a duty to shareholders to ensure they were fully informed of relevant matters known to the directors before making a decision to sell”. Ibid, p 260,827. McKay J thought that the company was, apart from having 200 shareholders, like a private company. Ibid.

The Companies Act 1993 has provisions dealing with insider trading. Section 145 prohibits a

director from disclosing company information to any person, or using the information without the

consent of the board. Similarly, s 148 requires a director to disclose share dealings in the

company shares to the board. Section 149 goes further and restricts a director who possesses

company information “which is information material to an assessment of the value of shares”

from acquiring or disposing of these shares unless the consideration given or received “is not less

than the fair value of these shares or security”.

SECURITIES AND TAKEOVERS

Page 20

48 Section 149(1). Section 149(2) provides that “the fair value of shares or securities is to be determined on the basis of all information known to the director or publicly available at the time”.

Under s 149(4), the director is liable to the person from whom the shares were purchased or to

whom they were sold for the difference between the sale price and the fair value of the shares.

However, s 149 does not apply in relation to a company to which Pt 1 of the Securities Markets

Act applies.

49 Section 149(6).

The third and principal means of dealing with insider trading in listed companies has been —

since 1998 — the provisions of the Securities Markets Act. In broad overview, the insider trading

regime in effect between December 1998 and 29 February 2008 was ineffective. And while it may

be that case law under the 1998–2008 will be of assistance in interpreting the new post-February

2008 regime, the better view is that scrutiny of the Australian law — upon which the New

Zealand post-February 2008 insider trading regime is modelled — will be of more utility.

What are the prohibitions on insider conduct?

The former NZSC published a guide on this topic. entitled, NZSC, New Securities Law for

Investment Advisers and Market Participants 2008: A guide to new requirements under the

Securities Markets Act 1988 (2008).

What are the three criminal offences for insider conduct?

Part 1 of the Securities Markets Act creates three criminal offences for insider conduct in relation

to securities: These are:

• the trading offence appearing in s 8C

• the disclosing (“tipping”) offence contained in s 8D, and

• the advising or encouraging offence contained in s 8E.

In addition, pursuant to s 11E, the same three offences apply to insider conduct in relation to

futures contract(s). As we shall see, civil liability also attaches such that a person (called an

“aggrieved person” in the Securities Markets Act) may seek to recover loss or damage.

What are the ingredients of the insider trading offences?

(1) Territorial connection : The relevant insider conduct must occur within New Zealand.

There is no provision in the Securities Markets Act that captures conduct outside New

Zealand as is the case in relation to the general dealing misconduct prohibition: see s 18(b).

(2) Securities of a public issuer : The relevant insider conduct must be in relation to

securities. Section 2 defines the term, “security”. Note here the particular definitions

contained in paragraphs (b) and (c) of the definition which apply to Pt 1, subpart 1. The key

part of the definition of a security appearing in paragraph (b) is that the security must have

been allotted and listed on a registered exchange’s market. Paragraph (d) extends the

meaning of a security further to catch that which we might describe as relevant interests in

securities. The term, “public issuer” is also defined in s 2. It means a person who is a party

to a listing agreement with a registered exchange or a person who was previously a party to

a listing agreement with a registered exchange, in respect of any action or event or

circumstance to which the Act applied while the person was a party to a listing agreement

with a registered exchange.

(3) Information insider : There must be an “information insider”. This term is defined in s

8A. A person is an information insider of a public issuer if that person:

(a) has material information relating to the public issuer that is not generally available to

the market, and

(b) knows or ought reasonably to know that the information is material information, and

(c) knows or ought reasonably to know that the information is not generally available to

the market.

SECURITIES AND TAKEOVERS

Page 21

A public issuer may be an information insider of itself: see s 8A(2). Further, the relevant

“inside information” means the information in respect of which a person is an information

insider of the public issuer in question: s 8B.

(4) Material information relating to a public issuer : An information insider must have

material information. Although the term, “information” is not specifically defined in the Act,

note that s 4 (definition of information generally available to the market) provides some

guidance. Section 3 defines material information in relation to a public issuer as information

that:

(a) a reasonable person would expect, if it were generally available to the market, to

have a material effect on the price of listed securities of the public issuer, and

(b) relates to particular securities, a particular public issuer, or particular public issuers,

rather than to securities generally or public issuers generally.

(5) Information not generally available : Pursuant to s 4, information is generally

available to the market:

(a) if it is information that

(i) has been made known in a manner that would, or would be likely to, bring it to

the attention of persons who commonly invest in relevant securities, and

(ii) since it was made known, a reasonable period for it to be disseminated among

those persons has expired, or

(b) if it is likely that persons who commonly invest in relevant securities can readily

obtain the information — whether by observation, use of expertise, purchased from

other persons, or any other means — or

(c) if it is information that consists of deductions, conclusions, or inferences made or

drawn from either or both of the kinds of information referred to in paragraphs (a) and

(b).

(6) Materiality : The prohibition against insider conduct applies only where a reasonable

person would expect that the material information, if it were generally available to the

market, would have a material effect on the price of listed securities of the public issuer. This

is an objective test.

(7) Knowledge : Pursuant to s 8A, it must be proved that the information insider knows or

ought reasonably to know that the information is material information, and knows or ought

reasonably to know that the information is not generally available to the market.

The Three Offences

(1) The Trading Offence : Where the ingredients described above are present, an

information insider of a public issuer must not trade securities of the public issuer: s 8B.

(2) The Disclosing Offence : Where the ingredients described above are present, an

information insider (A) of a public issuer must not directly or indirectly disclose inside

information to another person (B) if A knows or ought reasonably to know or believe that B

will, or is likely to trade securities of the public issuer or if B is already a holder of those

securities, continue to hold them or advise or encourage another person (C) to trade or hold

them.

(3) The Advising or Encouraging Offence : Where the ingredients described above are

present, an information insider (A) of a public issuer must not (a) advise or encourage

another person (B) to trade or hold securities of the public issuer, or (b) advise or encourage

(B) to advise or encourage another person (C) to trade or hold those securities.

Contravention of s 8C to 8E is a criminal offence: see s 8F.

What are the exceptions to the prohibition?

SECURITIES AND TAKEOVERS

Page 22

There are eight exceptions to the prohibition on the insider conduct. These are described in s 9–

9G.

What are the affirmative defences?

There are five affirmative defences. They are:

• absence of knowledge of trading: s 10

• inside information obtained by independent research and analysis: s 10A

• equal information: s 10B

• options and trading plans: s 10C, and

• Chinese wall defence: s 10D.

What are the criminal penalties?

Section 43 provides for a criminal penalty for the criminal liability established in s 8F. For an

individual, the maximum penalty is imprisonment for a term not exceeding five years or a fine

not exceeding $300,000 or both. For a company, the maximum penalty is a fine not exceeding

$1m.

What are the civil remedies?

Civil remedies are also available for breach of the insider conduct prohibition: see s 42W. First,

the FMA may seek a pecuniary penalty and declaration of contravention: s 10D. The maximum

amount of a pecuniary penalty for a contravention of an insider conduct prohibition, market

manipulation prohibition or unsolicited offer prohibition is the greater of:

(a) the consideration for the transaction that constituted the contravention (if any), or

(b) three times the amount of the gain made, or the loss avoided, by the person in carrying

out the conduct, or

(c) $1m: s 42W.

Second, under s 42ZA, an “aggrieved person” who has suffered loss or who is likely to suffer loss,

may apply for a compensatory order. Alternatively, the FMA may apply for such an order.

[¶2710] The Financial Markets Conduct Bill

The Financial Markets Conduct Bill 2011 (FMC Bill) was introduced into Parliament on 12

October 2011.The Bill represents a comprehensive review of New Zealand's securities and

financial markets law and is intended to facilitate the development of fair, efficient and

transparent financial markets: s 3 of the FMC Bill. The purpose of the Bill is to consolidate

existing securities and financial markets legislation and provide a new, and more coherent,

financial market conduct regulatory regime. The amendments are expected to result in:

enhanced information for investors

reduced capital raising costs

the removal of unnecessary processes for director certification of advertisements

the introduction of more robust safeguards for investors when others invest money on

their behalf, such as via managed investment schemes and discretionary investment

management services, and

more opportunities for securities exchanges to develop suitable markets for smaller

companies.

50 See the Explanatory Memorandum to the FMC Bill.

SECURITIES AND TAKEOVERS

Page 23

The Bill is divided into 9 Parts:

Part 1: specifies the purposes and objectives of the bill.

Part 2: This part is entitled “Misleading or deceptive conduct or false or misleading

representations.” It prohibits misleading and deceptive conduct in connection with

financial products and financial services.

Part 3: This part deals with the “disclosure of offers of financial products.” Part 3 provides

for the disclosure to investors in relation to certain offers of financial products. Schedule 1

of the Bill contains the relevant disclosure requirements. Part 3 also deals with the

advertisements for those offers and ongoing disclosure to investors.

Part 4 provides for the governance of debt securities, the registration of managed

investment schemes and the powers of intervention to enable the supervision of debt

securities. This part also specifies the duties of issuers of all regulated products as well as

the duties of persons associated with regulated products to make protected disclosures.

Part 5 prohibits insider trading and market manipulation. It also deals with the

continuous disclosure by listed issuers.

Part 6 regulates certain financial markets services, including the licensing of certain

financial market service providers.

Part 7 provides the FMA and the High Court with certain powers to avoid, remedy or

mitigate any actual or likely adverse effects of contraventions of the legislation and

regulation.

Part 8 provides for regulations and exemptions, including powers to prescribe matters

relating to the form and content of product disclosure statements, and powers for the FMA

to designate financial products and offers, and to grant exemptions, where this is

necessary or desirable

Part 9 repeals the Securities Act 1978, the Securities Markets Act 1988, and certain other

enactments.

As stated, the FMC Bill represents a major overhaul of NZ securities laws. While the Bill in some

respects largely restates and consolidates New Zealand’s current primary and secondary markets

laws, it represents a significant shift towards Australian legislation consistent with the aims of the

MOU on Business Law Co-ordination between Australia and New Zealand. The Bill is modelled

closely on Australian equivalent legislation. It contains direct references to Australian legislation.

For example, clause 27 of the FMC Bill states as follows: “an offer of financial products for issue

requires disclosure to an investor under this Part unless an exclusion under Part 1 of Schedule 1

applies. Compare Corporations Act 2011 s 706 (Aust).” The clause, therefore, directs the reader

to the Australian legislation. Section 706 of the Corporations Act deals with offers of securities for

issue that require disclosure to investors and, like clause 27, defines these by reference to other

provisions in the Act. Similar references to the Australian Corporations Act can be found in the

following clauses:

Clause 28 dealing with sale offers that need disclosure

Clause 31 dealing with options over financial products

Clause 35 dealing with the preparation of product disclosure statements

Clause 43 defining the meaning of “material information”

Clause 44 dealing with the consent of experts and persons who make endorsements in a

product disclosure statement

Clause 45 dealing with the presentation and wording of product disclosure statements

Clause 49 specifying the waiting periods after lodgement of product disclosure statements

Clause 55 detailing when supplementary documents or replacement product disclosure

statement may be lodged

Clauses 56 and 57 dealing with supplementary documents and replacement product

disclosure statements respectively

SECURITIES AND TAKEOVERS

Page 24

Clause 65 dealing with misleading and deceptive statements contained in product

disclosure statements

Clause 75 dealing with the distribution of product disclosure statements or registered

documents

Clause 76 dealing with permissible advertising and publicity before the product disclosure

statement is lodged

Clause 90 specifying the contents of a trust deed for debt securities

Clause 130 dealing with general duties applying in the exercise of a manager’s functions

Clause 132 specifying the duties of directors and senior managers of a manager of a

registered scheme

Clause 158 defining the term “related party benefit”

Clause 159 containing a general prohibition on transactions that result in the giving o

“related party benefits”

Clause 160 that permits certain related party benefits

Clause 210 containing a restriction on the use of information in registers

Clause 307 defining the meaning of a “financial market product” and Clause 38 specifying

what is meant by a “financial product market license”

Clause 309 containing prohibitions on holding out

Clause 333 imposing an obligation on overseas-regulated markets to give notices of

market rules and rule changes to FMA

Clause 432 dealing with duties of directors and senior managers of “DIMS licensees”, and

Clause 440 dealing with moneys paid by, or on account of, investors.

These clauses are a striking example of the effect of the MOU of Business Law Co-ordination

between Australia and New Zealand.

TAKEOVERS

[¶2711] What is a “takeover”?

A takeover involves someone acquiring enough shares in a company to give the shareholder

control of the company.

50 The best topical treatment is D Cooper, “Takeovers”, in J Farrar (gen ed), Company and Securities Law in New Zealand

(2008), Chapter 35.

Often a takeover is a full takeover, where 100% of the shares are acquired. A full takeover is

sometimes called a “merger”. But a partial takeover is also possible. Here, the takeover bidder

acquires a shareholding of less than 100% but one large enough to give control.

The Takeovers Code made pursuant to the Takeovers Act 1993 came into force on 1 July 2001.

The Takeovers Code effectively deems a shareholding of 20% or larger to be a controlling

shareholding. This reflects the fact that in many companies listed on the NZSX:

• there is a very large number of shareholders, many of whom hold only a small parcel of

shares (that is, many companies are “widely held”), and

• many shareholders do not exercise their voting rights.

In a “widely held” company, a 20% or larger shareholding will commonly provide “effective” or

“practical” control of the general meeting. That is, motions put to the shareholders in general

meeting — in relation to matters like the election of directors — will normally be passed or

rejected according to how the 20%+ shareholder votes.

[¶2712] Why do takeovers occur?

Companies are taken over for many reasons. Some of the reasons that may underlie a takeover

are summarised below.

51 For more detail, see: R Romano, “A Guide to Takeovers: Theory, Evidence, and Regulation” (1992) 9 Yale Journal on

Regulation 119; R Romano, Foundations of Corporate Law (1993), p 221 ff.

SECURITIES AND TAKEOVERS

Page 25

Synergy gains : A takeover of Company A by Company B will lead to synergy gains if the value

of the combined firm is greater than the value of A and B as independent entities. Operating

efficiencies or financial (accounting) factors, or both, may explain these synergies.

Replacing inefficient management : Takeovers — in particular “hostile” takeovers — play a

role in corporate governance. A hostile takeover bid is one that the target company’s board

discourages shareholders from accepting. The possibility of a hostile takeover bid being made for

Company A acts as an incentive to Company A’s chief executive officer (CEO) and senior

management team to work hard and maximise the value of A for its shareholders. If they do not

do that, Company B may make a takeover bid for A. If the bid succeeds, B will probably sack A’s

CEO and senior executives, and replace them with a new management team.

Expropriation : A takeover may also be motivated by the possibility of the bidder extracting

(“expropriating”) value from:

• taxpayers: interest on debt is tax-deductible, so some highly leveraged takeover bids may

be partly motivated by taxation benefits

• employees: a successful hostile bidder may fire not only the senior management team of

the target company, but also a significant proportion of its workforce — a smaller wage bill

may mean greater profits for the new owner (the successful bidder)

• consumers: if the bidder and the target operate in the same industry — and are

competitors — the takeover may result in a significant increase in the market power of the

bidder (it may be able to behave in a monopolistic fashion, and charge higher prices to

consumers of its products).

Empire building : Another possible reason for a takeover is that the CEO and senior

management of the bidder may simply be interested in running a very big firm — and one way to

grow quickly is through taking over other companies.

[¶2713] How common are takeovers in New Zealand?

Data on takeover activity in New Zealand up until 1993 may be found in John Farrar (ed),

Takeovers (1993). Today, data on takeover activity may be found in “Code Word”, the newsletter

of the Takeovers Panel, or on the website of the Takeovers Panel.

52 www.takeovers.govt.nz.

For example, “Code Word” for December 2001 reported that eight takeover notices under the

code had been received since the code came into force on 1 July 2001.

53 A discussion of the takeover battle between Lion Nathan and British liquor giant, Allied Domecq, for control of New

Zealand’s largest winemaker, Montana, can be found in G Shapira and J Johnston, “Takeovers” (2001) 19 Companies and Securities Law Journal 458.

[¶2714] What are the purposes of New Zealand’s takeover laws?

The purposes of the takeover provisions in the Takeovers Code are set out in the Takeovers Act

1993. The Takeovers Act created a Takeovers Panel. The Takeovers Panel had two main

functions. The first was to prepare a takeovers code that complied with the objectives set out in

the Act. In December 2002, this function was removed from the Panel and now rests with the

Minister who is responsible for formulating recommendations for the Takeovers Code. The second

function was to enforce the resultant code. Thus, the principal purposes of the Takeovers Code

appear in s 20, 21 and 24 of the Act.

Section 20(1) states that, in formulating a takeovers code, the Minister shall consider the

following objectives:

“(a) Encouraging the efficient allocation of resources:

(b) Encouraging competition for the control of specified companies:

(c) Assisting in ensuring that holders of securities in a takeover are treated fairly:

SECURITIES AND TAKEOVERS

Page 26

(d) Promoting the international competitiveness of New Zealand’s capital

markets:

(e) Recognising that the holders of securities must ultimately decide for

themselves the merits of a takeover offer:

(f) Maintaining a proper relation between the costs of compliance with the code

and the benefits resulting from it.”

Section 21 specifies certain matters to be considered by the Minister in formulating a code, such

as whether advance notice and publicity should be given.

Section 24 states that when formulating recommendations concerning a takeovers code, the

Minister must have regard, as far as is practicable, to any principles applying to the coordination

of business law between Australia and New Zealand as contained in the Memorandum of

Understanding between the Governments of Australia and New Zealand on the Coordination of

Business Law.

[¶2715] Overview of the Takeovers Code

There is a general prohibition contained in r 6 of the Takeovers Code on acquiring control of more

than 20% of the voting rights in a code company except as set out in the code.

Exceptions to the “fundamental rule” contained in r 6 are contained in r 7. Rule 7 states that a

person may increase a holding of voting rights beyond the 20% threshold in one of the following

ways:

• acquisition under a full offer

• acquisition under a partial offer

• acquisition approved by a resolution of the shareholders of the target company

• acquisitions of less than 5% per year by a holder of between 50% and 90% of the voting

rights, or

• acquisitions by a person holding at least 90% of voting rights in a code company.

Section 45 of the Takeovers Act 1993 also permits the Takeovers Panel to grant exemptions from

the requirements of the code.

[¶2716] What is the general prohibition?

The general prohibition or “fundamental rule” is contained in r 6 of the Takeovers Code. This rule

prohibits a person from holding or controlling more than 20% of the voting rights in a code

company except as prescribed in the code.

To whom does the general prohibition apply?

The general prohibition contained in r 6 applies to companies that:

• are party to a listing agreement with a registered exchange

• were a party to a listing agreement in the 12 months before any event referred to in the

code, or

• has 50 or more shareholders.