commercial mortgage commentary - cmls

TRANSCRIPT

cmls.ca | 1Copyright © 2019 CMLS Financial Ltd. All rights reserved. Any reproduction of any of this commentary without the express written consent of CMLS Financial Ltd. is strictly prohibited. The material in this commentary is provided for information purposes only on an “as is” basis without warranties or conditions of any kind either express or implied. FSCO LICENSE NO. 11749

MAY 2019

Commercial Mortgage CommentaryCMLS Mortgage Analytics Group

Customer Forward Thinking.™

Making News

IntroductionThe Commercial Mortgage Commentary aims to inform the market

on commercial real estate finance news. We focus on the fol-

lowing capital sources for commercial real estate: Conventional

Mortgages, CMHC-Insured Mortgages, Commercial Mortgage

Backed Securities (CMBS), High Yield Mortgages, First Mortgage

Bonds and Senior Unsecured debt for REITs and REOCs.

There were two headline transactions that occurred in Q1/2019:

Bentall Centre Sale

Blackstone Property Partners (BPP) and Hudson Pacific Properties

purchased the four-tower Bentall Centre from China’s Anbang

Insurance Group. While the purchase price has yet to be disclosed,

the deal is expected to be the most expensive real estate transaction

in BC year to date. Anbang originally acquired the complex in 2016

for $1.06 billion amidst allegations the deal circumvented Canadian

laws around foreign ownership of key domestic assets. BPP will act

as managing partner with an 80% stake, while Hudson Pacific will

oversee the daily operations as the operating partner with a 20%

share in the property.

BCI/RBC Partnership

RBC Asset Management announced a $7-billion agreement

with BCI and QuadReal. This newly created fund will be one of

Canada’s most diversified commercial real estate portfolios and

will include over 40 of BCI’s current Canadian real estate assets.

The fund is expected to open for investment in Q3/2019.

Economic EnvironmentThe prevailing economic environment influences rates at which

lenders are willing to provide capital. 2019 started off with a weaker

economic outlook from the Bank of Canada (BOC), resulting mainly

from the slowdown in the global economy and the fear of a recession.

The weaker prospects have resulted in a decrease in bond yields

over the first quarter of 2019. Notably, the treasury yield curve

inverted in late March for the first time since 2007, as the yield

on a three-year bill traded higher than that of a 10-year bond.

Capital Thinking.™cmls.ca | 2

Customer Forward Thinking.™

Copyright © 2019 CMLS Financial Ltd. All rights reserved. Any reproduction of any of this commentary without the express written consent of CMLS Financial Ltd. is strictly prohibited. The material in this commentary is provided for information purposes only on an “as is” basis without warranties or conditions of any kind either express or implied. FSCO LICENSE NO. 11749

CMLS INSTITUTIONAL SERVICES COMMERCIAL MORTGAGE COMMENTARY MAY 2019

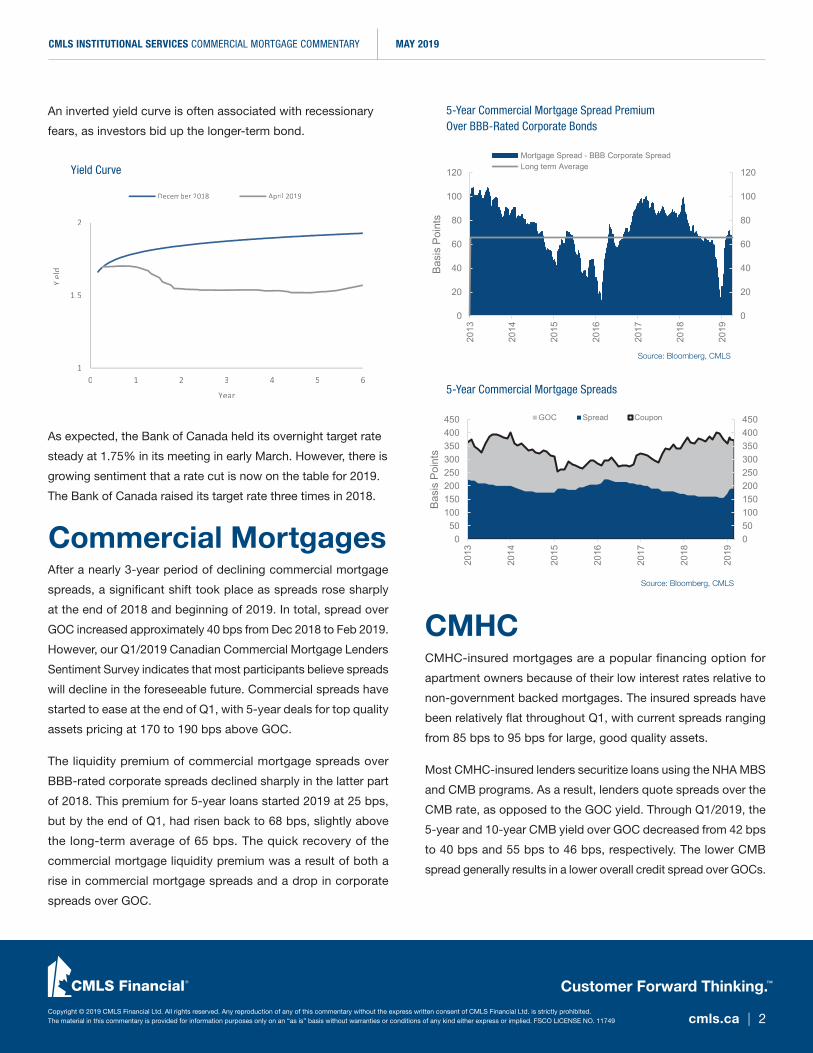

After a nearly 3-year period of declining commercial mortgage

spreads, a signifi cant shift took place as spreads rose sharply

at the end of 2018 and beginning of 2019. In total, spread over

GOC increased approximately 40 bps from Dec 2018 to Feb 2019.

However, our Q1/2019 Canadian Commercial Mortgage Lenders

Sentiment Survey indicates that most participants believe spreads

will decline in the foreseeable future. Commercial spreads have

started to ease at the end of Q1, with 5-year deals for top quality

assets pricing at 170 to 190 bps above GOC.

The liquidity premium of commercial mortgage spreads over

BBB-rated corporate spreads declined sharply in the latter part

of 2018. This premium for 5-year loans started 2019 at 25 bps,

but by the end of Q1, had risen back to 68 bps, slightly above

the long-term average of 65 bps. The quick recovery of the

commercial mortgage liquidity premium was a result of both a

rise in commercial mortgage spreads and a drop in corporate

spreads over GOC.

CMHC-insured mortgages are a popular fi nancing option for

apartment owners because of their low interest rates relative to

non-government backed mortgages. The insured spreads have

been relatively fl at throughout Q1, with current spreads ranging

from 85 bps to 95 bps for large, good quality assets.

Most CMHC-insured lenders securitize loans using the NHA MBS

and CMB programs. As a result, lenders quote spreads over the

CMB rate, as opposed to the GOC yield. Through Q1/2019, the

5-year and 10-year CMB yield over GOC decreased from 42 bps

to 40 bps and 55 bps to 46 bps, respectively. The lower CMB

spread generally results in a lower overall credit spread over GOCs.

As expected, the Bank of Canada held its overnight target rate

steady at 1.75% in its meeting in early March. However, there is

growing sentiment that a rate cut is now on the table for 2019.

The Bank of Canada raised its target rate three times in 2018.

An inverted yield curve is often associated with recessionary

fears, as investors bid up the longer-term bond.

Commercial Mortgages

CMHC

5-Year Commercial Mortgage Spreads

1

1.5

2

0 1 2 3 4 5 6

Yiel

d

Year

December 2018 April 2019

Yield Curve

Source: Bloomberg, CMLS

CMLS FINANCIAL COMMERCIAL MORTGAGE COMMENTARY

Customer Forward Thinking.™

Copyright © 2018 CMLS Financial Ltd. All rights reserved. Any reproduction of any of this commentary without the express written consent of CMLS Financial Ltd. is strictly prohibited. The material in this commentary is provided for information purposes only on an “as is” basis without warranties or conditions of any kind either express or implied. FSCO LICENSE NO. 11749 cmls.ca | 2

As expected, the Bank of Canada held its overnight target rate steady at 1.75% in its meeting in early March. However, there is growing sentiment that the possibility of a rate cut is now on the table for 2019. The Bank of Canada raised its target rate three times in 2018.

An inverted yield curve is often associated with recessionary fears, as investors bid up the longer-term bond. Input Graph on the yield Curve (Use target data for end of Q1 yield curve)

CMHC-insured mortgages are a popular financing option for apartment owners because of their low interest rates relative to those of non-government backed mortgages. The insured spreads have been relatively flat throughout Q1, with current spreads ranging from 85 bps to 95 bps for large, good quality assets. Most CMHC-insured lenders securitize loans using the NHA MBS and CMB programs. As a result, lenders quote spreads over the CMB rate, as opposed to the GOC yield. Through Q1/2019, the 5-year and 10-year CMB yield over GOC decreased from 42 bps to 40 bps and 55 bps to 46 bps, respectively. The lower CMB spread generally results in a lower credit spread over GOCs.

CMHC

Commercial Mortgages After a nearly 3-year period of declining commercial mortgage spreads, a significant shift took place as spreads rose sharply at the end of 2018 and beginning of 2019. In total, spread over GOC increased approximately 40 bps from Dec 2018 to Feb 2019. However, our Q1/2019 Canadian Commercial Mortgage Lenders Sentiment Survey indicates that most participants saw spreads declining in the foreseeable future. GOC yields compressed at the end of Q1, just as commercial spreads were starting to ease. The liquidity premium of commercial mortgage spreads over BBB-rated corporate spreads declined sharply in the latter part of 2018. This premium for 5-year loans started 2019 at 25 bps, but by the end of Q1, had risen back to 68 bps, slightly above the long-term average of 65 bps. The quick recovery of the commercial mortgage liquidity premium was a result of both a rise in commercial mortgage spreads and a drop in corporate spreads over GOC.

0

20

40

60

80

100

120

0

20

40

60

80

100

120

2013

2014

2015

2016

2017

2018

2019

Bas

is P

oint

s

5-year Commercial Mortgage Spread Premium over BBB-rated Corporate Bonds

Mortgage Spread - BBB Corporate SpreadLong term Average

050100150200250300350400450

050

100150200250300350400450

2013

2014

2015

2016

2017

2018

2019

Bas

is P

oint

s

5-Year Commercial Mortgage Spreads

GOC Spread Coupon

1

1.5

2

0 1 2 3 4 5 6

Yiel

d

Year

Yield Curve

December 2018 April 2019

5-Year Commercial Mortgage Spread Premium Over BBB-Rated Corporate Bonds

Source: Bloomberg, CMLS

CMLS FINANCIAL COMMERCIAL MORTGAGE COMMENTARY

Customer Forward Thinking.™

Copyright © 2018 CMLS Financial Ltd. All rights reserved. Any reproduction of any of this commentary without the express written consent of CMLS Financial Ltd. is strictly prohibited. The material in this commentary is provided for information purposes only on an “as is” basis without warranties or conditions of any kind either express or implied. FSCO LICENSE NO. 11749 cmls.ca | 2

As expected, the Bank of Canada held its overnight target rate steady at 1.75% in its meeting in early March. However, there is growing sentiment that the possibility of a rate cut is now on the table for 2019. The Bank of Canada raised its target rate three times in 2018.

An inverted yield curve is often associated with recessionary fears, as investors bid up the longer-term bond. Input Graph on the yield Curve (Use target data for end of Q1 yield curve)

CMHC-insured mortgages are a popular financing option for apartment owners because of their low interest rates relative to those of non-government backed mortgages. The insured spreads have been relatively flat throughout Q1, with current spreads ranging from 85 bps to 95 bps for large, good quality assets. Most CMHC-insured lenders securitize loans using the NHA MBS and CMB programs. As a result, lenders quote spreads over the CMB rate, as opposed to the GOC yield. Through Q1/2019, the 5-year and 10-year CMB yield over GOC decreased from 42 bps to 40 bps and 55 bps to 46 bps, respectively. The lower CMB spread generally results in a lower credit spread over GOCs.

CMHC

Commercial Mortgages After a nearly 3-year period of declining commercial mortgage spreads, a significant shift took place as spreads rose sharply at the end of 2018 and beginning of 2019. In total, spread over GOC increased approximately 40 bps from Dec 2018 to Feb 2019. However, our Q1/2019 Canadian Commercial Mortgage Lenders Sentiment Survey indicates that most participants saw spreads declining in the foreseeable future. GOC yields compressed at the end of Q1, just as commercial spreads were starting to ease. The liquidity premium of commercial mortgage spreads over BBB-rated corporate spreads declined sharply in the latter part of 2018. This premium for 5-year loans started 2019 at 25 bps, but by the end of Q1, had risen back to 68 bps, slightly above the long-term average of 65 bps. The quick recovery of the commercial mortgage liquidity premium was a result of both a rise in commercial mortgage spreads and a drop in corporate spreads over GOC.

0

20

40

60

80

100

120

0

20

40

60

80

100

120

2013

2014

2015

2016

2017

2018

2019

Bas

is P

oint

s

5-year Commercial Mortgage Spread Premium over BBB-rated Corporate Bonds

Mortgage Spread - BBB Corporate SpreadLong term Average

050100150200250300350400450

050

100150200250300350400450

2013

2014

2015

2016

2017

2018

2019

Bas

is P

oint

s

5-Year Commercial Mortgage Spreads

GOC Spread Coupon

1

1.5

2

0 1 2 3 4 5 6

Yiel

d

Year

Yield Curve

December 2018 April 2019

Capital Thinking.™cmls.ca | 3

Customer Forward Thinking.™

Copyright © 2019 CMLS Financial Ltd. All rights reserved. Any reproduction of any of this commentary without the express written consent of CMLS Financial Ltd. is strictly prohibited. The material in this commentary is provided for information purposes only on an “as is” basis without warranties or conditions of any kind either express or implied. FSCO LICENSE NO. 11749

CMLS INSTITUTIONAL SERVICES COMMERCIAL MORTGAGE COMMENTARY MAY 2019

In early April, we saw the fi rst CMBS issuance of 2019. Real Estate

Asset Liquidity Trust issued REAL-T 2019-HBC, a $250-million

CMBS comprised of 2 loans secured by Hudson’s Bay stand-alone

department stores located in Montreal and Ottawa. REAL 2019-

HBC features a 4.229% weighted average interest rate, a 48-month

weighted average term and AAA subordination of 16.875%. The

LTC ratio is 46.7% due to the signifi cant amount of cash equity

($252 million) behind the subject loan.

CMHC-insured multi-family properties can be securitized in two

NHA MBS pools: the 965 pool, which is comprised of fi xed rate

loans that allow prepayment with penalty; and the 966 pool, which

does not allow prepayments.

The pools have increased signifi cantly year-over-year, with the

combined amount going from $1.8 billion in Q1/2018 to $2.7 billion

in Q1/2019.

CMHC (continued)

CMBS

CMHC New Issuances ($Billions)

Source: DBRS, Bloomberg

Customer Forward Thinking.™

cmls.ca | 3 Copyright © 2018 CMLS Financial Ltd. All rights reserved. Any reproduction of any of this commentary without the express written consent of CMLS Financial Ltd. is strictly prohibited. The material in this commentary is provided for information purposes only on an “as is” basis without warranties or conditions of any kind either express or implied. FSCO LICENSE NO. 11749

CMLS FINANCIAL COMMERCIAL MORTGAGE COMMENTARY

CMBS

In early April, we saw the first CMBS issuance of 2019. Real Estate Asset Liquidity Trust issued REAL-T 2019-HBC, a $250-million CMBS comprised of 2 loans secured by Hudson’s Bay stand-alone department stores located in Montreal and Ottawa. REAL 2019-HBC features a 4.229% weighted average interest rate, a 48-month weighted average term and AAA subordination of 16.875%. The LTC ratio is 46.7% due to the significant amount of cash equity ($252 million) behind the subject loan.

Summary of recent CMBS DealsOriginal Size(million CAD)

A1 A2 A1

2019 REAL-T 2019-HBC $250 2 2 1.76x

REAL-T 2018-1 $352 63 72 1.40x

CCMOT4 2018-4 $550 53 53 1.33x 110 160 5.0 9.3

2017 REAL-T 2017 $407 71 111 1.36x 125 175 3.5 7.1

IMSCI 2016-7 $352 38 60 1.47x 163 200 5.5 9.0

REAL-T 2016-2 $421 47 72 1.38x 125 165 3.5 7.0

REAL-T 2016-1 $401 55 91 1.30x 150 195 5.8 10.0

CCMOT 2015-3 $570 42 59 1.41x 155 n/a 3.9 n/a

REAL-T 2015-1 $335 46 46 1.50x 112 145 5.8 10.0

IMSCI 2015-6 $325 47 64 1.44x 115 150 5.5 10.0

2014 MCIC 2014-1 $224 32 32 1.36x 110 n/a 3.8 n/a

CMLSI 2014-1 $284 37 37 1.47x 115 145 5.5 10.0

REAL-T 2014-1 $281 34 46 1.59x 110 n/a 5.5 n/a

IMSCI 2014-5 $312 41 55 1.44x 78 95 2.8 5.8

Weighted Average Life

Deal

2016

2015

# of Loans # of PropertiesWeighted Avg.

DBRS Term DSCR

AAA Spreads (bps)

2018

0.910.93 1.02 0.98

1.19

0.901.23 1.17

1.521.47

0.8

1.3

1.8

2.3

2.8

Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019

CMHC New Issuances ($Billions)

965 966CMHC-insured multi-family properties can be securitized in either of two NHA MBS pools: the 965 pool, which is comprised of fixed rate loans that allow pre-payment with penalty; and the 966 pool, which does not allow prepayments. The pools have increased significantly year-over-year, with the combined amount going from $1.8 billion in Q1/2018 to $2.7 billion in Q1/2019.

Summary of recent CMBS deals

Source: DBRS, RBC

Year Deal Original Size ($Millions, CAD) # of Loans # of Properties Weighted Average

DBRS Term DSCR

2019 REAL-T 2019-HBC $250 2 2 1.76x

2018REAL-T 2018-1 $352 63 72 1.40x

CCMOT4 2018-4 $550 53 53 1.33x

2017 REAL-T 2017 $407 71 111 1.36x

2016

IMSCI 2016-7 $352 38 60 1.47x

REAL-T 2016-2 $421 47 72 1.38x

REAL-T 2016-1 $401 55 91 1.30x

2015

CCMOT 2015-3 $570 42 59 1.41x

REAL-T 2015-1 $335 46 46 1.50x

IMSCI 2015-6 $325 47 64 1.44x

2014

MCIC 2014-1 $224 32 32 1.36x

CMLSI 2014-1 $284 37 37 1.47x

REAL-T 2014-1 $281 34 46 1.59x

IMSCI 2014-5 $312 41 55 1.44x

CMLS INSTITUTIONAL SERVICES COMMERCIAL MORTGAGE COMMENTARY MAY 2019

cmls.ca | 4

Customer Forward Thinking.™

Copyright © 2019 CMLS Financial Ltd. All rights reserved. Any reproduction of any of this commentary without the express written consent of CMLS Financial Ltd. is strictly prohibited. The material in this commentary is provided for information purposes only on an “as is” basis without warranties or conditions of any kind either express or implied. FSCO LICENSE NO. 11749

ABOUT CMLS MORTGAGE ANALYTICS GROUP

The CMLS Mortgage Analytics Group is a division of CMLS Financial Ltd., and is one of the only independent, dedicated providers of mortgage valuation

services and software for the commercial real estate fi nance industry in Canada. The CMLS Mortgage Analytics Group provides solutions to some of

Canada’s most prominent fi nancial institutions, investment managers, pension funds and consultants. With investors, regulatory bodies and governing

committees requiring increased reporting, independence and third-party advice, the CMLS Mortgage Analytics Group offers a host of risk rating, valuation,

and portfolio analysis tools to better manage risk/reward profi les in commercial mortgage portfolios. Clients engage our services to provide independent

support for mortgage purchases, fair value accounting, ongoing fund valuation, interest rate appraisals and more.

ERIC CLARK, CFA Managing Director604.488.3897 [email protected]

SUKHMAN GREWAL, CFA Associate Director604.235.5110 [email protected]

COLIN LEE, CFA Senior Market [email protected]

RESEARCH TEAM:Meeran AmirJoanne ZhaoMax Schriber

Senior Unsecured debt for REITs and REOCs is often an attractive

substitute for conventional commercial mortgage fi nancing.

In Q1/2019, senior unsecured debt issuance reached $1.175

billion, up from $1 billion in Q4/18. Brookfi eld Property issued a

$350-million, 5-year debenture at a spread of 280.4 bps, which

was 50 bps higher than their equal term issuance in Q3/2018.

Senior Unsecured Debt

2019 Issuer NameIssue Size ($Millions)

Issuance Rating Term (yrs) Spread (bps)

Q1

SmartCentres REIT 350 BBB 2.25 111.9

Artis REIT 250 BBBL 2 190

Brookfi eld Property Finance ULC 350 BBB 5.05 247.7

Morguard Corp 225 BBBL 5 280.4

Total/Average Q1 1,175 3.58

Senior Unsecured Debt Issuances

The First Mortgage bond market saw its fi rst activity since Q1/2018

with an aggregate $660-million bond on the Bay Wellington Tower

in Toronto. The tower features 47-storeys and 1.4 million square

feet, with a LEED Gold certifi cation.

Issued by Brookfi eld Offi ce Properties, the bond is comprised of

$270 million Series A: 7-year, 3.299% coupon and $390 million

Series B: 10-year, 3.464% coupon. Both series feature a 5-year

interest only period and a 30-year amortization.

First Mortgage Bonds First Mortgage Bond Issuances and Maturities

Source: Bloomberg, CMLS

Senior Unsecured debt for REITs and REOCs is often an attractive substitute for conventional commercial mortgage financing. In Q1/2019, senior unsecured debt issuance reached $1.175 billion, up from $1 billion in Q4/18. BrookfieldProperty issued a $350-million, 5-year debenture at a spread of 280.4 bps, which was 50bps higher than their equal termissuance in Q3/2018.

About CMLS Mortgage Analytics Group

The CMLS Mortgage Analytics Group is a division of CMLS Financial Ltd., and is one of the only independent, dedicated providersof mortgage valuation services and software for the commercial real estate finance industry in Canada. The CMLS MortgageAnalytics Group provides solutions to some of Canada’s most prominent financial institutions, investment managers, pension fundsand consultants. With investors, regulatory bodies and governing committees requiring increased reporting, independence and third-party advice, the CMLS Mortgage Analytics Group offers a host of risk rating, valuation, and portfolio analysis tools to better managerisk/reward in commercial mortgage portfolios. Clients engage our services to provide independent support for mortgage purchases,fair value accounting, ongoing fund valuation, interest rate appraisals and more.

Eric Clark, CFAManaging [email protected]

Sukhman Grewal, CFAAssociate [email protected]

Research TeamMeeran AmirJoanne ZhaoMax Schriber

Senior Unsecured Debt

First Mortgage BondsThe First Mortgage bond market saw its firstactivity since Q1/2018 with an aggregate$660-million bond on the Bay Wellington Tower in Toronto. The tower features 47-storeys and 1.4 million square feet, with LEED Gold certifications.

Issued by Brookfield Office Properties, thebond is comprised of Series A: 7-year, 3.299%coupon and Series B: 10-year, 3.464%coupon. Both series feature a 5-year interest-only period and a 30-year amortization.

Colin Lee, CFASenior Market [email protected]

2019 Issuer Name Issue Size Millions ($) Issuance Rating Term (yrs) Spread (bps)

SmartCentres REIT 350 BBB 2.25 111.9

Artis REIT 250 BBBL 2 190

Brookfield Property Finance ULC 350 BBB 5.05 247.7

Morguard Corp 225 BBBL 5 280.4

Total/Average 1175 3.58

Q1

1.3

1.8

2.5

1.3

0.5

-0.1

0.9

0.6

0.56

1.16

0.71 0.45

1.02 0.79

0.59

1.5

1.0

0.5

0.0

0.5

1.0

1.5

2.0

2.5

1.5

1.0

0.5

0.0

0.5

1.0

1.5

2.0

2.520

11

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

First Mortgage Bond Issuances and Maturities ($Billions)

Issuances Maturities