colombia: recent economic performance and prospects · colombia: recent economic performance and...

TRANSCRIPT

COLOMBIA:

RECENT ECONOMIC PERFORMANCE AND PROSPECTS

Jose Darío Uribe E.

Governor of the Banco de la República

1. Introduction

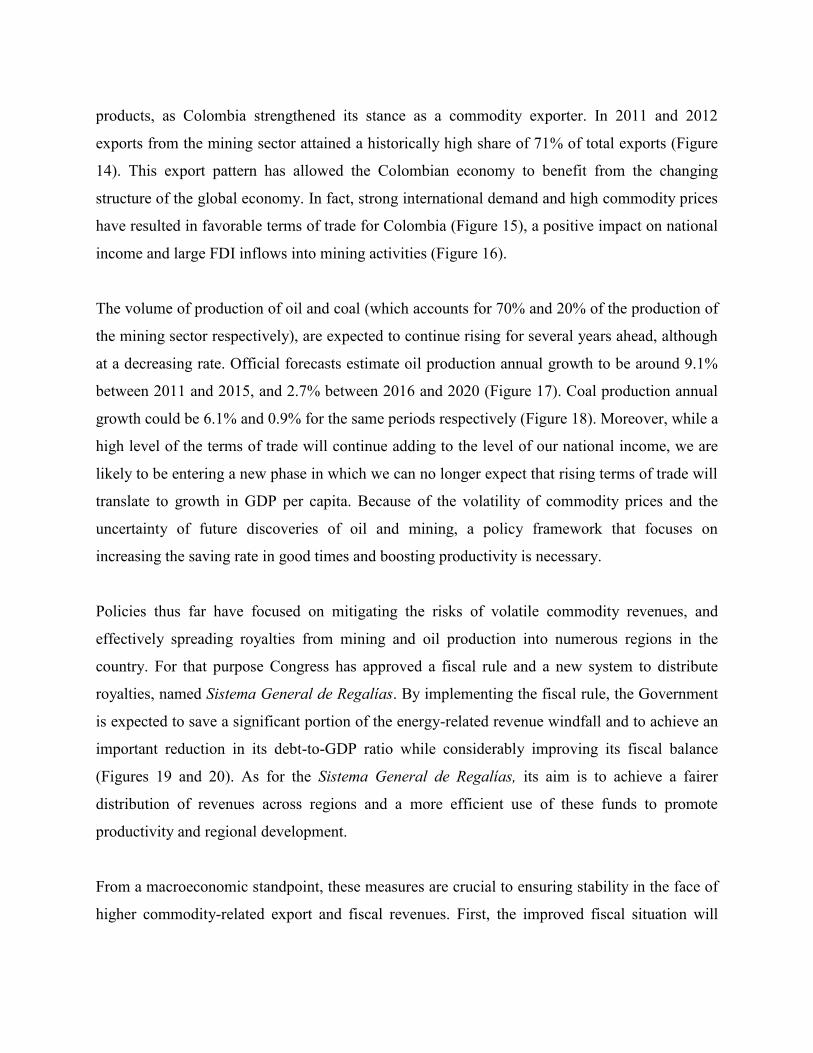

Colombia is the fourth largest economy in Latin America (Figure 1), and its mid-term growth

prospects remain strong by regional standards. After overcoming a deep economic and financial

crisis by the end of the nineties, the Colombian economy has followed a path of higher growth

based on greater export and investment rates. This process has been driven by both local and

external structural factors. At the same time, the economy has proven to be more resilient to

external shocks than in the past within a sound policy framework that has enabled both monetary

and fiscal policies to work counter-cyclically. This framework has been developed based on

lessons from past experiences, and is an essential element to higher average growth, thanks to its

contribution to the reduction of macroeconomic volatility and financial stability.

In the following presentation I will describe the evolution of the Colombian economy in recent

years and highlight the importance of the monetary policy regime. I will also discuss the

medium-term outlook with an emphasis on upcoming challenges, as well as the role of a policy

framework to deal with them.

2. Higher Growth and Greater Resilience

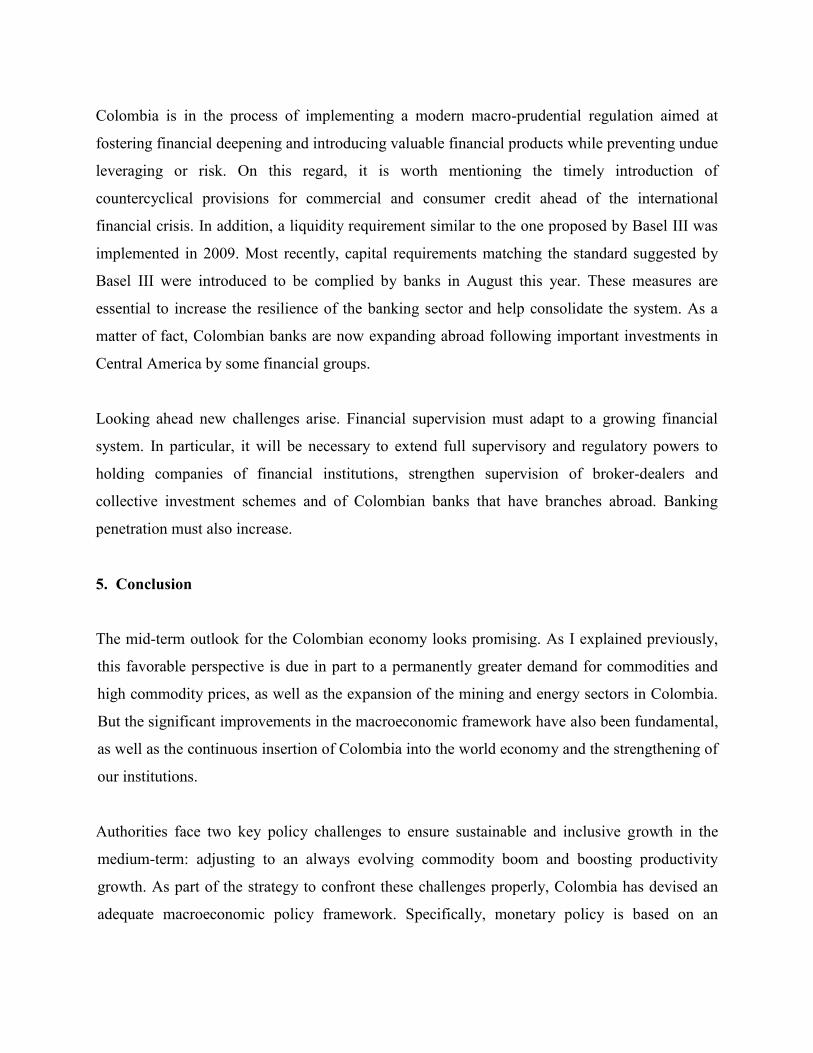

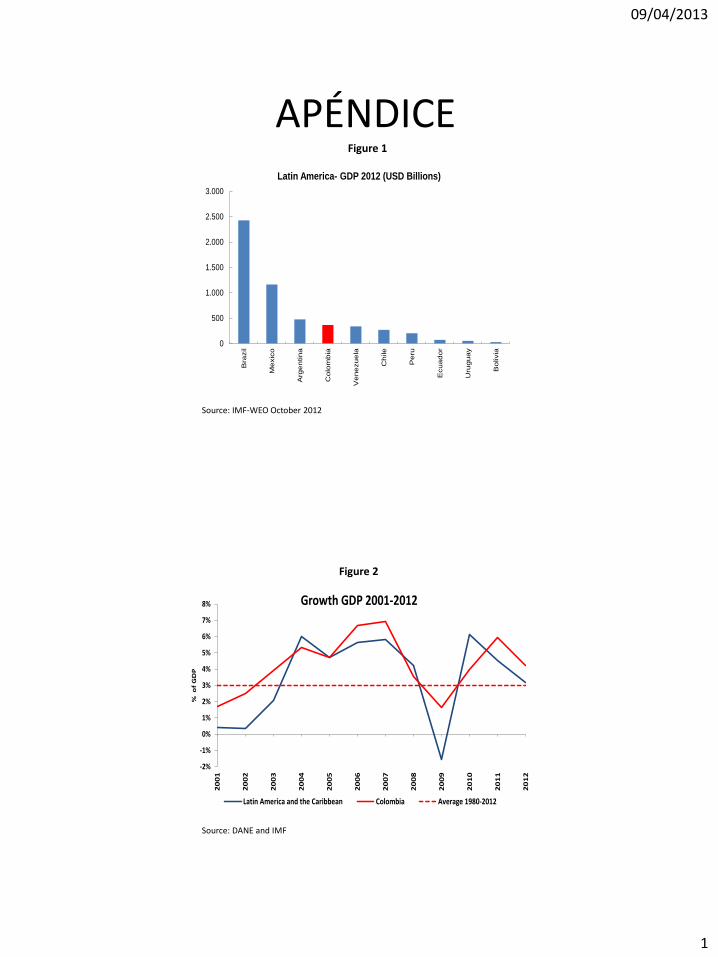

During the first decade of the XXI century economic growth in Colombia exceeded the average

growth rate for Latin America and the Caribbean, as well as its own historical growth average

(Figures 2 and 3). As a result, the Colombian economy now belongs to the group of upper-

middle income countries (Figure 4).

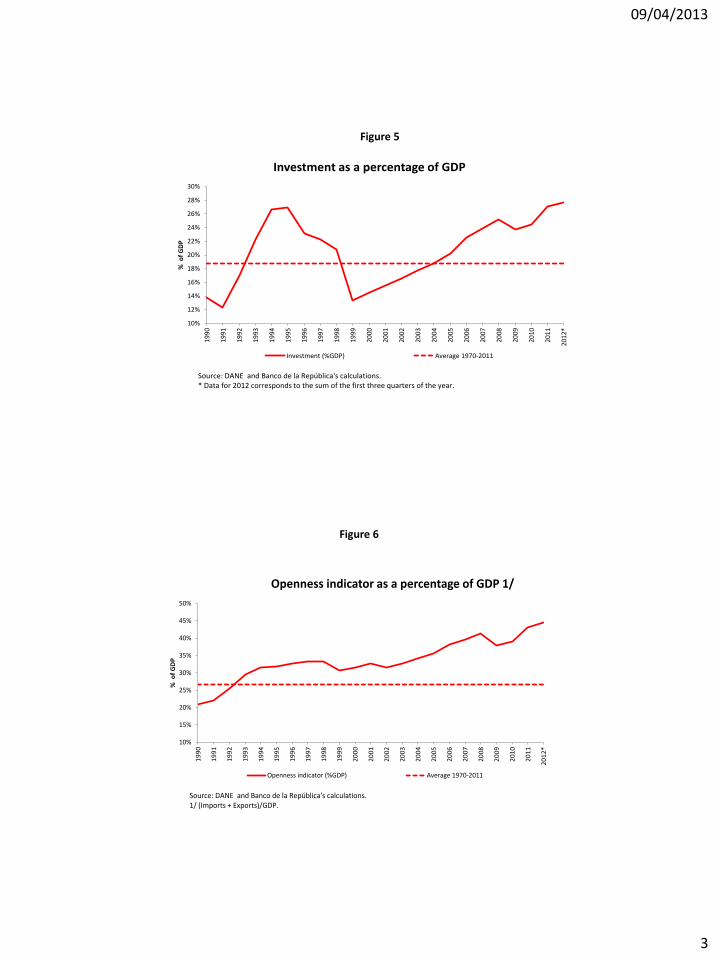

Two factors were instrumental for this accomplishment: first, an upward trend in the share of

investment with respect to output (Figure 5); and second, the continuous insertion of Colombia

into the world economy, both through international trade (exports and imports) and investment

inflows (Figure 6). Behind these achievements lie local factors such as significant improvements

in matters of security and fiscal management, as well as the attainment of a low, stable inflation.

The improved fiscal situation reinforced the market’s perception that the public debt is

sustainable and significantly decreased the uncertainty of future taxation and financing costs.

Low, stable inflation implied lower long-term real interest rates (due to nominal stability and a

smaller inflation risk), better resource allocation and productivity, and increased safety for

investors.

External factors have also been important for the new phase of growth in Colombia. Structural

changes in the world economy, such as the rapid industrialization and urbanization process in

China and India together with the growing income of several emerging market economies, meant

a greater demand for commodities and a rise in their prices. This stimulated investment in

resource-rich countries, raised their terms of trade and national incomes and diminished their

perceived riskiness. In the case of Colombia, findings of oil and mineral reserves increased the

positive impact of these events, since the combination of higher production volumes and prices

enhanced expectations of future export and fiscal revenues.

Besides increasing its potential growth through the 2000s, the Colombian economy has exhibited

a remarkable resilience to the difficult external conditions of the last few years. This has been

possible thanks to the enhancing ability to perform monetary and fiscal countercyclical policies,

coupled with favorable macroeconomic conditions such as low inflation, sustainable public debt,

and a stable financial system in the context of a flexible exchange rate regime. This increasing

resilience was evident in the reaction of the Colombian economy to the collapse of Lehman

Brothers and the ensuing global financial crisis. In contrast to its dismal response to the Asian

and Russian crises of the late nineties, the Colombian economy kept growing in 2008-2009 and

recovered rapidly in 2010-2011 (Figure 7). As a result, growth volatility has been substantially

subdued and is now lower than the average for Latin America (Figure 8).

Overall, improvements in the Colombian macroeconomic policy framework were central to

driving the economy along a higher growth path as well as to increasing its resilience in the face

of adverse shocks. Most importantly, stability strengthens the incentives to undertake long-term

productive investment projects. As I will explain next, the Central Bank’s strategy for

implementing its monetary policy has played a key role in achieving these results.

3. Monetary Policy: Low and Stable Inflation and Smoothing Output Fluctuations

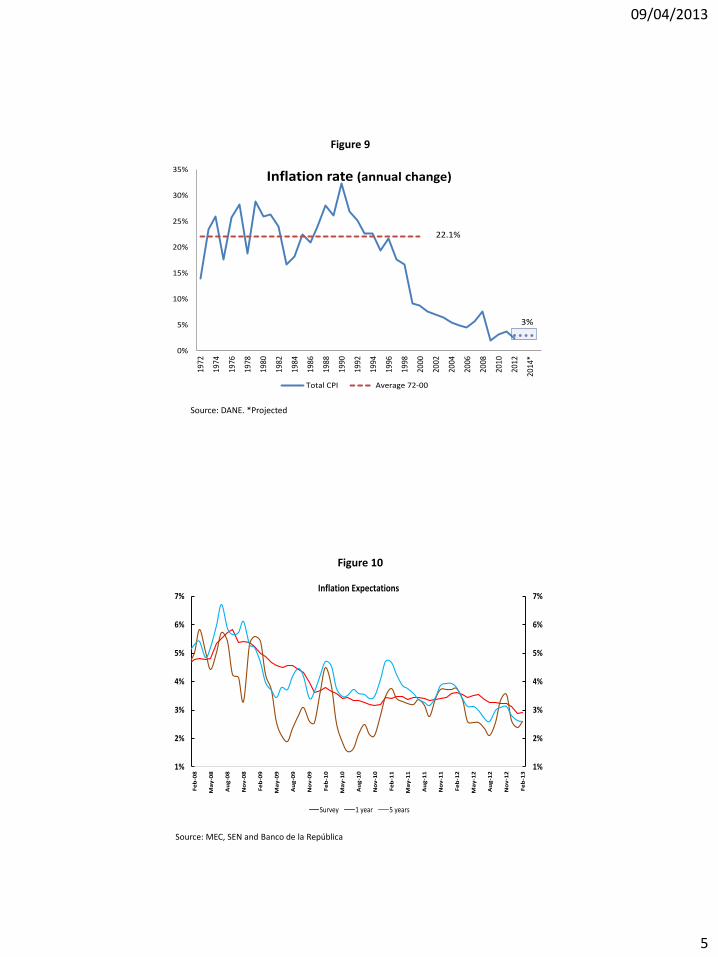

Since 1999, Banco de la República has used a flexible inflation-targeting regime. The objectives

of this strategy are to maintain a low and stable inflation and to smooth output fluctuations

around a sustainable growth path. Inflation has been gradually reduced from two-digit levels to

the official long-term target of 3%, with a control range of 1 +/- one percentage point, and it is

currently hovering at around 2%, reflecting the absence of inflationary pressures (Figure 9).

The possibility of simultaneously maintaining inflation on-target and smoothing output

fluctuations depends on the Central Bank’s capacity to anchor inflation expectations (Figure 10).

If public expectations deviate significantly from the inflation target, monetary policy loses its

ability to dampen the business cycles. Thus, the Bank’s credibility is crucial for the success of

monetary policy. Credibility comes from developing the proper policy framework and building a

track record of success in achieving and maintaining a low and stable inflation.

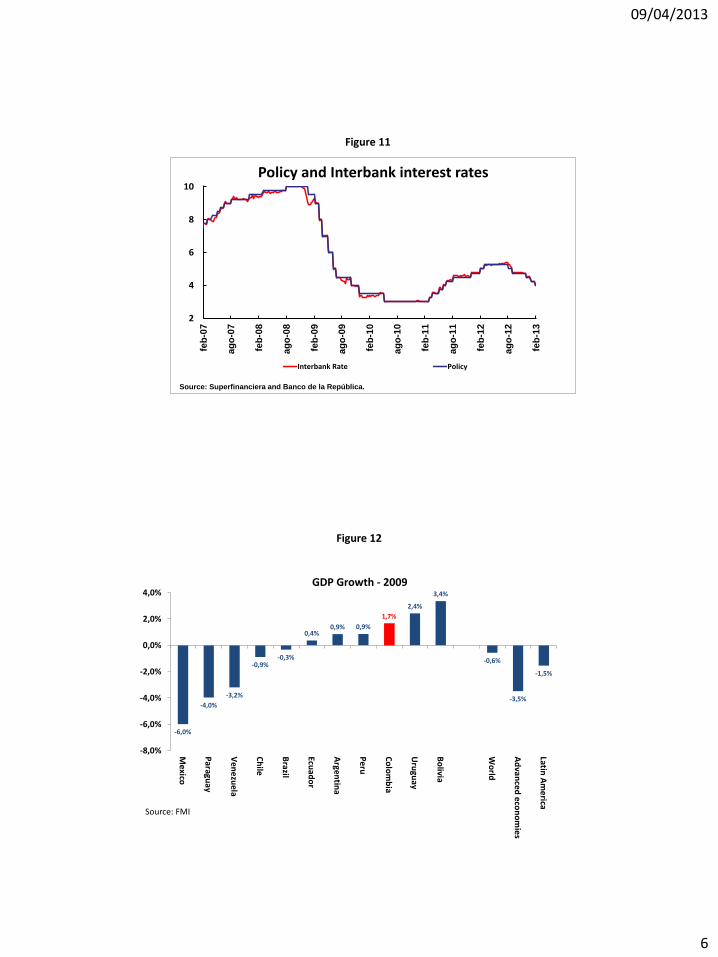

The Bank’s main instrument for monetary policy is the short-term interest rate. When aggregate

demand falls below its sustainable level and the economy faces lower inflation, the appropriate

policy reaction is to lower interest rates. For instance, after the collapse of Lehman Brothers and

the subsequent shock in September 2008, the Board of Directors of the Central Bank reduced the

policy rate from 10% to 3% (Figure 11). The combination of this extraordinary monetary

stimulus and a financial sector that continued to provide credit to households and businesses, as

well as a moderate fiscal expansion resulted in a growth rate of 1.7% in 2009, the highest among

large Latin American countries in that year (Figure 12). In contrast, once the economy recovered

its growth pace and faced a strong increase in consumer credit, the Central Bank moved off its

exceptional policy and increased interest rates from 3% in January 2011 to the “more normal”

level of 5.25% in February of 2012.

Recently, a variety of shocks of different nature and duration have affected prices and

production. Positive agricultural supply shocks, a strong peso, reductions in the value added tax,

and a weaker aggregate demand have led to a significant reduction in the inflation rate and

inflation forecasts, currently placing them below the long term target of 3%. Meanwhile, an

unexpected contraction in gross capital formation, particularly in civil works and construction,

associated with regulatory and administrative factors, led to a negative output gap at the close of

2012. For the same reason, projections for GDP growth in 2013 fall below the full potential of

the economy. These factors prompted the Bank to lower the interest rate from 5.25% in June

2012 to 3.75% last February, which will provide a necessary stimulus in the current

circumstances without putting the inflation target at risk.

The floating exchange rate is also an integral part of the Bank’s strategy for implementing

monetary policy (Figure 13). In a commodity-exporting, small, open economy with price and

wage rigidities like Colombia, most shocks are better absorbed by the exchange rate. For

example, in the second semester of 2008 the policy response to the Lehman shock prompted the

exchange rate to respond endogenously - it fell sharply, by more than 40% - which was an

expansionary impulse for the economy. Moreover, exchange rate flexibility facilitates the

adoption of a countercyclical monetary policy and makes the private sector more prudent in its

decisions of foreign indebtedness.

4. Medium-Term Outlook for the Colombian Economy: Opportunities and Challenges

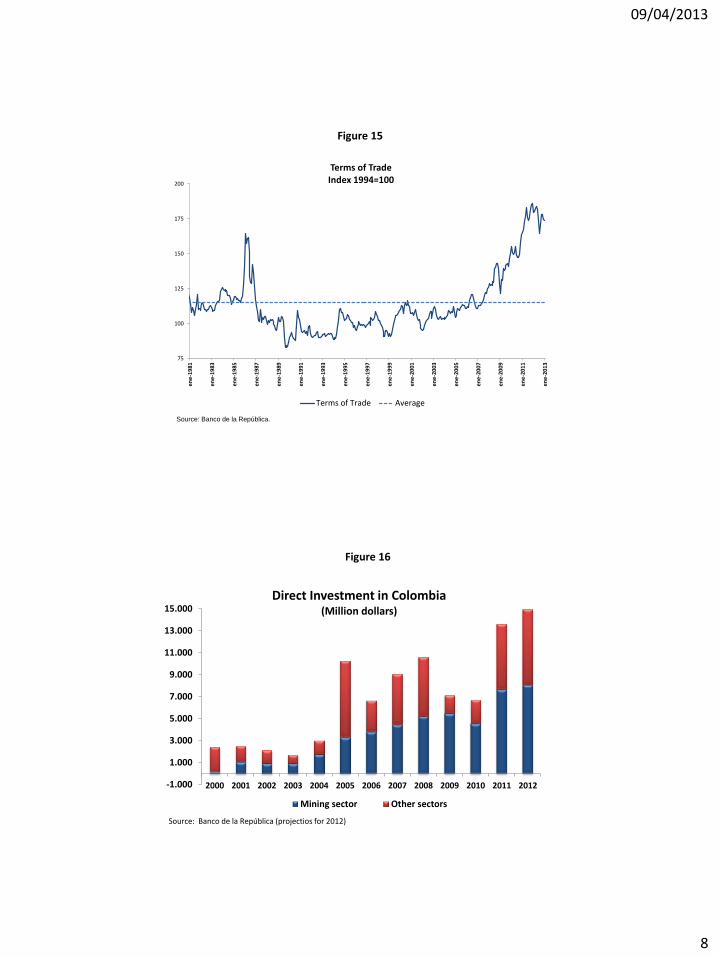

The last decade witnessed an increase in production and exports of oil, coal and other mining

products, as Colombia strengthened its stance as a commodity exporter. In 2011 and 2012

exports from the mining sector attained a historically high share of 71% of total exports (Figure

14). This export pattern has allowed the Colombian economy to benefit from the changing

structure of the global economy. In fact, strong international demand and high commodity prices

have resulted in favorable terms of trade for Colombia (Figure 15), a positive impact on national

income and large FDI inflows into mining activities (Figure 16).

The volume of production of oil and coal (which accounts for 70% and 20% of the production of

the mining sector respectively), are expected to continue rising for several years ahead, although

at a decreasing rate. Official forecasts estimate oil production annual growth to be around 9.1%

between 2011 and 2015, and 2.7% between 2016 and 2020 (Figure 17). Coal production annual

growth could be 6.1% and 0.9% for the same periods respectively (Figure 18). Moreover, while a

high level of the terms of trade will continue adding to the level of our national income, we are

likely to be entering a new phase in which we can no longer expect that rising terms of trade will

translate to growth in GDP per capita. Because of the volatility of commodity prices and the

uncertainty of future discoveries of oil and mining, a policy framework that focuses on

increasing the saving rate in good times and boosting productivity is necessary.

Policies thus far have focused on mitigating the risks of volatile commodity revenues, and

effectively spreading royalties from mining and oil production into numerous regions in the

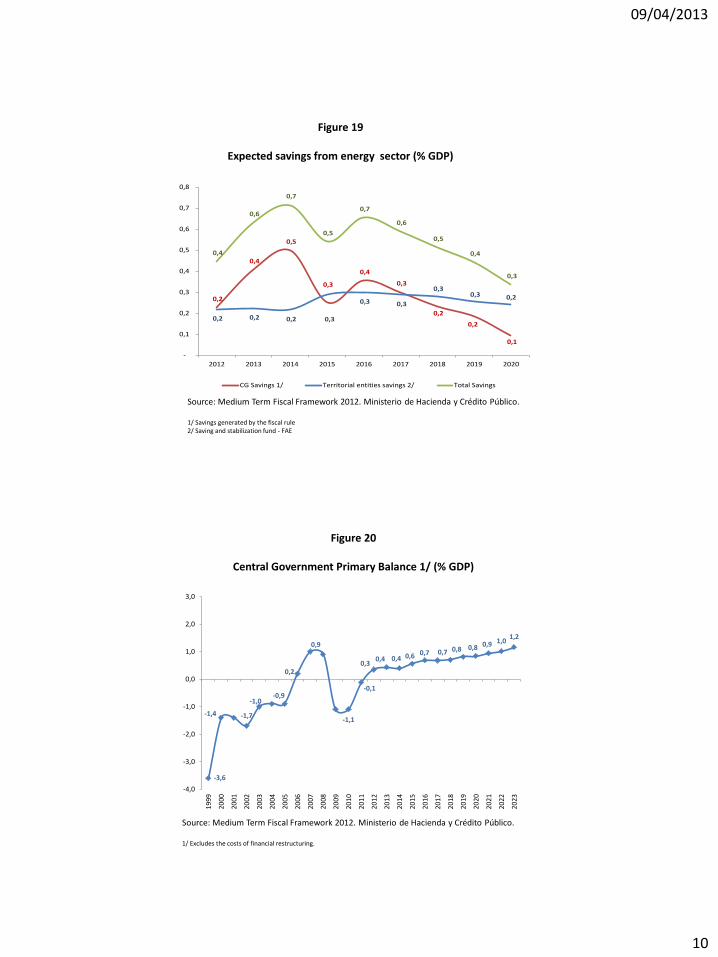

country. For that purpose Congress has approved a fiscal rule and a new system to distribute

royalties, named Sistema General de Regalías. By implementing the fiscal rule, the Government

is expected to save a significant portion of the energy-related revenue windfall and to achieve an

important reduction in its debt-to-GDP ratio while considerably improving its fiscal balance

(Figures 19 and 20). As for the Sistema General de Regalías, its aim is to achieve a fairer

distribution of revenues across regions and a more efficient use of these funds to promote

productivity and regional development.

From a macroeconomic standpoint, these measures are crucial to ensuring stability in the face of

higher commodity-related export and fiscal revenues. First, the improved fiscal situation will

reduce the vulnerability of the economy to adverse shocks and will enhance the credibility of the

inflation target. Second, the savings generated by both the fiscal rule and the system for

distributing royalties will mitigate the real appreciation of the currency that naturally follows

from a commodity boom, hence alleviating concerns of the Dutch disease. And third, the fiscal

rule will contribute to the adoption of countercyclical fiscal policies and support the role that

monetary policy plays in this respect.

The country is also likely to attract large capital inflows due to an improved risk perception.

Authorities face the challenge of maximizing the return on large, potentially volatile capital

flows, and on this regard structural policies aimed at boosting productivity will be helpful. For its

part, the Banco de la República will maintain a flexible exchange rate but accelerate the

accumulation of international reserves to counter a higher probability of misalignment of the

exchange rate, help curb the risks of the recent slowdown of the global economy, and aid the

current Colombian expansionary monetary policy.

Recent free trade agreements (FTA) with the United States, Colombia’s largest trading partner

with 38% of exports, and South Korea, are welcome measures to strengthen competitiveness in

tradable sectors other than mining and oil. The FTA with South Korea will deepen the insertion

of Colombia into the Asian market, which could promote a positive correlation between

commodity prices and demand for Colombian agriculture and manufacturing exports, and in turn

would help reduce the negative consequences of fluctuations in commodity prices on tradable

sectors different from energy-mining. In addition, Colombia has signed free trade agreements

with other countries in the Americas and a FTA with the European Union is close to ratification.

While the unemployment rate has declined in Colombia, it remains high for Latin American

standards, and a high proportion of the Colombian work force lies in informal, often low-

productivity jobs. The Ministry of Finance proposed a tax reform that was approved by Congress

in December of 2012, which seeks to increase revenue while decreasing the effective cost of

hiring labor, and to allow for a more efficient and progressive system.

Colombia is in the process of implementing a modern macro-prudential regulation aimed at

fostering financial deepening and introducing valuable financial products while preventing undue

leveraging or risk. On this regard, it is worth mentioning the timely introduction of

countercyclical provisions for commercial and consumer credit ahead of the international

financial crisis. In addition, a liquidity requirement similar to the one proposed by Basel III was

implemented in 2009. Most recently, capital requirements matching the standard suggested by

Basel III were introduced to be complied by banks in August this year. These measures are

essential to increase the resilience of the banking sector and help consolidate the system. As a

matter of fact, Colombian banks are now expanding abroad following important investments in

Central America by some financial groups.

Looking ahead new challenges arise. Financial supervision must adapt to a growing financial

system. In particular, it will be necessary to extend full supervisory and regulatory powers to

holding companies of financial institutions, strengthen supervision of broker-dealers and

collective investment schemes and of Colombian banks that have branches abroad. Banking

penetration must also increase.

5. Conclusion

The mid-term outlook for the Colombian economy looks promising. As I explained previously,

this favorable perspective is due in part to a permanently greater demand for commodities and

high commodity prices, as well as the expansion of the mining and energy sectors in Colombia.

But the significant improvements in the macroeconomic framework have also been fundamental,

as well as the continuous insertion of Colombia into the world economy and the strengthening of

our institutions.

Authorities face two key policy challenges to ensure sustainable and inclusive growth in the

medium-term: adjusting to an always evolving commodity boom and boosting productivity

growth. As part of the strategy to confront these challenges properly, Colombia has devised an

adequate macroeconomic policy framework. Specifically, monetary policy is based on an

inflation-targeting regime, which anchors inflation expectations and helps smooth the economic

cycle. This is coupled with a floating exchange rate policy that also plays a stabilizing role for

the economy and a sound banking sector.

The adoption of a fiscal rule contribute to the exercise of a countercyclical macroeconomic

policy, while the royalty distribution law help save a portion of oil revenues and ensure a fairer

and more efficient distribution system. This will reduce the impact of rising oil revenue on

domestic demand as well as on inflation and on the exchange rate.

09/04/2013

1

0

500

1.000

1.500

2.000

2.500

3.000

Bra

zil

Mexic

o

Arg

entina

Co

lom

bia

Venezuela

Chile

Peru

Ecuador

Uru

guay

Bolivia

Latin America- GDP 2012 (USD Billions)

Figure 1

Source: IMF-WEO October 2012

APÉNDICE

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

% o

f G

DP

Growth GDP 2001-2012

Latin America and the Caribbean Colombia Average 1980-2012

Figure 2

Source: DANE and IMF

09/04/2013

2

3,5%

2,7%

4,2%

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

4,5%

1980-1990 1991-2000 2001-2012*

ColombiaGDP Average Growth

Figure 3

Source: DANE and Banco de la República (IV quarter of 2012* estimated)

0

1000

2000

3000

4000

5000

6000

7000

1960 1963 1966 1969 1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011

GNI per capita, Atlas method (current US$)

Source: World Bank

Low Income

Lower middle Income

Upper middle Income

Figure 4

09/04/2013

3

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

*

% o

f G

DP

Investment as a percentage of GDP

Investment (%GDP) Average 1970-2011

Source: DANE and Banco de la República's calculations.* Data for 2012 corresponds to the sum of the first three quarters of the year.

Figure 5

Figure 6

10%

15%

20%

25%

30%

35%

40%

45%

50%

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

*

% o

f G

DP

Openness indicator as a percentage of GDP 1/

Openness indicator (%GDP) Average 1970-2011

Source: DANE and Banco de la República's calculations.1/ (Imports + Exports)/GDP.

09/04/2013

4

5,9%

2,6%

4,5%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

2004-2007 2008-2009 2010-2012

ColombiaGDP Average Growth

Figure 7

Source: DANE and Banco de la República (projections for IV quarter of 2012)

0,000

0,005

0,010

0,015

0,020

0,025

0,030

0,035

0,040

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Sta

nd

ard

De

via

tio

n(1

0-y

ea

r ro

llin

g w

ind

ow

)

GDP Volatility

Colombia Latin America and the Caribbean

Figure 8

Source: Banco de la República and IMF

09/04/2013

5

0%

5%

10%

15%

20%

25%

30%

35%

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

*

Inflation rate (annual change)

Total CPI Average 72-00

22.1%

3%

Figure 9

Source: DANE. *Projected

1%

2%

3%

4%

5%

6%

7%

1%

2%

3%

4%

5%

6%

7%

Fe

b-0

8

Ma

y-0

8

Au

g-0

8

No

v-0

8

Fe

b-0

9

Ma

y-0

9

Au

g-0

9

No

v-0

9

Fe

b-1

0

Ma

y-1

0

Au

g-1

0

No

v-1

0

Fe

b-1

1

Ma

y-1

1

Au

g-1

1

No

v-1

1

Fe

b-1

2

Ma

y-1

2

Au

g-1

2

No

v-1

2

Fe

b-1

3

Inflation Expectations

Survey 1 year 5 years

Figure 10

Source: MEC, SEN and Banco de la República

09/04/2013

6

2

4

6

8

10

feb

-07

ag

o-0

7

feb

-08

ag

o-0

8

feb

-09

ag

o-0

9

feb

-10

ag

o-1

0

feb

-11

ag

o-1

1

feb

-12

ag

o-1

2

feb

-13

Policy and Interbank interest rates

Interbank Rate Policy

Source: Superfinanciera and Banco de la República.

Figure 11

-6,0%

-4,0%

-3,2%

-0,9% -0,3%

0,4% 0,9% 0,9%

1,7%

2,4%

3,4%

-0,6%

-3,5%

-1,5%

-8,0%

-6,0%

-4,0%

-2,0%

0,0%

2,0%

4,0%

Me

xico

Pa

raguay

Ve

ne

zuela

Ch

ile

Brazil

Ecuad

or

Argen

tina

Pe

ru

Co

lom

bia

Uru

guay

Bo

livia

Wo

rld

Ad

vanced

econ

om

ies

Latin A

me

rica

GDP Growth - 2009

Source: FMI

Figure 12

09/04/2013

7

1600

1800

2000

2200

2400

2600

2800

feb

-07

ago

-07

feb

-08

ago

-08

feb

-09

ago

-09

feb

-10

ago

-10

feb

-11

ago

-11

feb

-12

ago

-12

feb

-13

COP/USD Colombian exchange rate

Source: Banco de la República.

Figure 13

55% 62% 61% 56%56%

55% 56% 57% 49%

45% 36% 30% 28%

45% 38% 39% 44%

44%

45%

44%

43%

51%

55%

64%

70% 72%

0

10.000

20.000

30.000

40.000

50.000

60.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012(Jan-Nov)

To

tal

Ex

po

rts

(US

$ m

illi

on

s)

Composition of Colombian Exports

Others Mining goods

Figure 14

Source: DANE - DIAN

09/04/2013

8

75

100

125

150

175

200e

ne

-19

81

en

e-1

98

3

en

e-1

98

5

en

e-1

98

7

en

e-1

98

9

en

e-1

99

1

en

e-1

99

3

en

e-1

99

5

en

e-1

99

7

en

e-1

99

9

en

e-2

00

1

en

e-2

00

3

en

e-2

00

5

en

e-2

00

7

en

e-2

00

9

en

e-2

01

1

en

e-2

01

3

Terms of Trade Index 1994=100

Terms of Trade Average

Source: Banco de la República.

Figure 15

Figure 16

-1.000

1.000

3.000

5.000

7.000

9.000

11.000

13.000

15.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Direct Investment in Colombia(Million dollars)

Mining sector Other sectors

Source: Banco de la República (projectios for 2012)

09/04/2013

9

2015:1228 mbd

2018:1313 mbd

-15%

-10%

-5%

0%

5%

10%

15%

20%

0

200

400

600

800

1.000

1.200

1.400

1.600

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Ye

ar -o

n-ye

ar p

erce

nta

ge ch

an

ge

tho

usa

nd

ba

rre

ls p

er

da

y

Production Annual change

Figure 17

Oil Production in Colombia

Source: Medium Term Fiscal Framework 2012. Ministerio de Hacienda y Crédito Público.

2015: 99 mill-ton

2020:103 mill-ton

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0

20

40

60

80

100

120

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Ye

ar -o

n-y

ea

r pe

rcen

tag

e ch

an

ge

M

illi

on

s o

f t

on

s

Production Annual change

Figure 18

Coal Production in Colombia

Source: Medium Term Fiscal Framework 2012. Ministerio de Hacienda y Crédito Público.

09/04/2013

10

0,2

0,4

0,5

0,3

0,4

0,3

0,2

0,2

0,1

0,2 0,2 0,2 0,3

0,3 0,3

0,3 0,3 0,2

0,4

0,6

0,7

0,5

0,7

0,6

0,5

0,4

0,3

-

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

2012 2013 2014 2015 2016 2017 2018 2019 2020

CG Savings 1/ Territorial entities savings 2/ Total Savings

Figure 19

Expected savings from energy sector (% GDP)

Source: Medium Term Fiscal Framework 2012. Ministerio de Hacienda y Crédito Público. 1/ Savings generated by the fiscal rule 2/ Saving and stabilization fund - FAE

-3,6

-1,4 -1,7

-1,0-0,9

0,2

0,9

-1,1

-0,1

0,30,4 0,4 0,6 0,7 0,7 0,8 0,8 0,9 1,0

1,2

-4,0

-3,0

-2,0

-1,0

0,0

1,0

2,0

3,0

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

Figure 20

Central Government Primary Balance 1/ (% GDP)

Source: Medium Term Fiscal Framework 2012. Ministerio de Hacienda y Crédito Público. 1/ Excludes the costs of financial restructuring.