colliers international covid-19 impact on retail - survey...ica introduction 2 covid-19 continues to...

TRANSCRIPT

MAY 2020

Colliers International – COVID-19

Impact On Retail - Survey

“Together through challenging times”

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

INTRODUCTION

2

Covid-19 continues to dominate global headlines, ushering in unprecedented changes to the way we

eat, live, work, shop and play- changes that just months ago were unfathomable. This survey was

conducted to anonymously gather and provide real data concerning the impact of Covid-19 on the

retail industry in the Middle East and how both landlords and retailers are coping. Thanks to all the

respondents we have been able to conduct a meaningful survey and we are confident that the data

output of this survey can subsequently provide strategic insights that can be used by landlords and

retailers for their decision-making process.

This survey covers both landlords and retailers with a split of approximately 39% and 61%

respectively. Respondents operate their business in the United Arab Emirates, Saudi Arabia, Kuwait

and Bahrain.

The respondent landlords own regional shopping centres, community centres, street retail,

standalone retail and retail below residential and/or office buildings. Respondent retailers are active

in a wide variety of retail categories such as fashion (men’s, ladies, unisex, luxury), fashion

accessories, handbags, shoes, gym, sportswear & goods, electronics, food and beverage,

supermarket/hypermarket, jewelry & watches, health & beauty, cosmetics, perfumes and

entertainment amongst others. It is fair to conclude that the majority of retail categories have been

covered in this survey. The survey did not get any participation from super regional mall landlords;

this might be due to the fact that the majority of super regional mall landlords contacted during the

course of this survey were already working on and announcing, in some cases, generous tenant

support packages and countermeasures to mitigate the impact of COVID-19.

This survey has identified six key conclusions which will be discussed throughout document,

followed by the survey conclusion.

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

SURVEY SAMPLE

3

61% 39%

Retailers Landlords

Respondents’ Country of Operation

Typology of Respondents

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

SURVEY SAMPLE (CONT’D)

4

What is the business focus of your company?

Landlords

Retailers

*Other (please specify): Strip Malls, Waterfront Retail below residential building, various retail

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

SURVEY SAMPLE (CONT’D)

5

How many people are employed in your company?

Landlords

Retailers

Colliers International – COVID-19 Retail Impact Survey, May 2020

Quarter 1 2020 impact

35% of retailers estimate the decrease in revenue to be more than 70%, in sharp contrast with

landlords’ estimations where only 9% estimate the same decline.

The fact that landlords estimate their Q1 revenue impact to be significantly lower than the

retailer’s revenue impact most probably lies in the fact that landlords generally collect quarterly

rent in advance, whilst in contrast, retailers saw an immediate drop in revenue the moment

stores were forced to close.

Quarter 2 2020 impact

Responses show an even bigger discrepancy between landlord and retailer expectations of the

pandemic’s revenue impact on their business with 59% of the retailers estimating that quarter 2

will bring a revenue decrease of more than 70% and only 9% of landlords.

The continued negative Q2 outlook from the retailers might be because the physical store

closures only happened towards the end of Q1, leaving retailers in shock and in “damage

control” mode.

For Q2 and depending on how long restrictions and countermeasures will stay in force, they

might believe the shift in consumer behavior will not have returned to levels that were seen

before COVID-19, because consumers are expected to be cautious when going outside. In

addition to this, retailers typically give landlords postdated cheques - in advance - for the yearly

rent, which in theory means landlords can collect the rent if they cash the cheque when it is due,

potentially seriously impacting the retailers cashflow position.

“Retailers physical store revenue impact is

estimated to be hit harder than landlords

retail asset revenue for Q1 and Q2 2020.”

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

ESTIMATED PANDEMIC IMPACT

7

Landlords

Retailers

How would you estimate the pandemic's revenue impact on your physical

retail store(s)? Can you give a rough percentage estimation for Q1 2020?

How would you estimate the pandemic's revenue impact on your

retail asset(s)? Can you give a rough percentage estimation for

Q1 2020?

*Increase (please specify): both online and in storeColliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

ESTIMATED PANDEMIC IMPACT

8

How would you estimate the pandemic's revenue impact on your retail

asset(s)? Can you give a rough percentage estimation for Q2 2020?

Landlords

Retailers

How would you estimate the pandemic's revenue impact on your physical

retail store(s)? Can you give a rough percentage estimation for Q2 2020

Colliers International – COVID-19 Retail Impact Survey, May 2020

Quarter 1 2020 impact on online sales

Retailers that had their e-commerce platforms up and running before the Covid-19

pandemic started have hugely benefited from a change in consumer behavior,

shifting from predominantly in store shopping to - in many cases forced - online

shopping, due to store closures. The vast majority of retailers, 59% have seen an

increase of between 20% and over 70%.

Quarter 2 2020 impact on online sales

For the second quarter of 2020, 60% estimated an increase of between 20% and

more than 70%.

The short - and medium-term outlook of retailers for their e-commerce business is

optimistic, many retailers believe they have reached new customers and existing

customers have started spending more online. Many retailers therefore believe this

might result in an ongoing change of consumer behavior.

“Retailers see incredible growth in online

sales in Q1 2020 and they expect this

growth to continue in Q2 2020”

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

E-COMMERCE - RETAILERS

10

How would you estimate the pandemic's revenue impact on your e-

commerce business? Can you give a rough percentage estimation for

Q1 2020?

Retailers

Retailers

How would you estimate the pandemic's revenue impact on your e-

commerce business? Can you give a rough percentage estimation for

Q2 2020?

Other: Decrease of 70%+

Other: Decrease of 70%

Colliers International – COVID-19 Retail Impact Survey, May 2020

All the landlords offering rent free periods stated they offered 1 to 3

months. With the same % of those landlords offering rent free also

offering to extend the lease term for the same rent-free period.

92% of retailers are seeking rent free periods of between 3 to 6

months. Only 58% of retailers offered to extend the lease term for

the rent-free period.

“Landlord and retailer expectations of support

packages are not aligned.”

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

RENT-FREE PERIOD

12

Have you offered rent-free or other support packages to your tenants? What

are they?

Landlords

How long is the rent-free period that you have offered?

Landlords

*Other (please specify): rent deferment with lease extension, too early to estimate the impact

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

RENT-FREE PERIOD

13

Have you asked for any rent-free or other support packages from your

Landlord(s)? What are they?

Retailers

Retailers

Other: Rent break and Turnover rent

How long is the rent-free period that you have asked for?

Other: Depends on situation as example all malls was closed by government

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a SERVICE CHARGES DURING RENT-

FREE PERIOD

14

Did you ask the tenant to pay service charges during the rent-free period?

Retailers

Landlords

Did you offer to pay service charges during the rent-free period?

*100% of landlord respondents that have offered a rent-free period

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a EXTENDED LEASE TERMS FOR RENT-

FREE PERIOD

15

Did you offer to extend the lease term equivalent to the rent-free period?

Retailers

Landlords

Did you offer to extend the lease term equivalent to the rent-free period?

*100% of landlord respondents that have offered a extension of the lease term equivalent to the rent-free

period

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

RENT BREAK PERIOD - LANDLORD

16

How long is the rent break period (deferred rent payment period) that you

have offered?

Landlords

Landlords

Did you ask the tenant to pay service charges during the rent break period

(deferred rent payment period)?

Other: One to one approach. Deferring Q2 payment over following 3-4 months

*100% of landlord respondents that have offered a rent-break

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

RENT BREAK PERIOD - LANDLORD (CONT’D)

17

Did you ask the tenant to extend the lease term equivalent to the rent break

period (deferred rent payment period)?

Landlords

Landlords

Did you offer a step rent/balloon payment equivalent to the rent break

(deferred rent payment) at the end of the lease?

*100% of landlord respondents that have offered a rent-break

*100% of landlord respondents that have offered a rent-free period

Colliers International – COVID-19 Retail Impact Survey, May 2020

“There is a much greater alignment from

landlords and retailers on recovery

expectations, the reduction in physical space

requirements and structural lease changes.”

Retailers are more optimistic than landlords on the prospect of recovery going beyond a

year; 64% of landlords and only 35% of retailers.

Both landlords and retailers agree that they expect the long-term consequences for the

retail industry to be an increased usage of e-commerce by customers (82% landlords

and 76% retailers).

They also agree that there will be an increase of turnover based rent (64% landlords

and 71% retailers).

Divergence of opinion appears on the future of physical space with 36% of landlords

believing that retail space may be redeveloped for other uses against only 12% of

retailers.

If retailers indeed believe that consumer behavior is going to change in the longer-term,

spearheading increased spending online, it appears intuitive that landlords and retailers

both have a great belief in changes in physical demand for retail space.

The impact of turnover rent based only deals can provide a lot of flexibility to retailers.

Shorter lease terms in combination with turnover based rent only will also create a

challenge in terms of real estate financing with banks most likely seeking a fixed rent

component in order assess repayment risk.

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

RECOVERY

19

From today and for your business, how long do you think it will take to

recover from the outbreak?

Retailers

Landlords

From today and for your business, how long do you think it will take to

recover from the outbreak?

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

LONGER TERM CONSEQUENCES

20

In your opinion, what longer-term consequences can be expected for the

retail industry?

Retailers

Landlords

In your opinion, what longer-term consequences can be expected for the

retail industry?

Other: Decline in addressable market as a result of (1) potential population drop, (2) reduced discretionary

spend as people are made redundant or take salary cuts.

Colliers International – COVID-19 Retail Impact Survey, May 2020

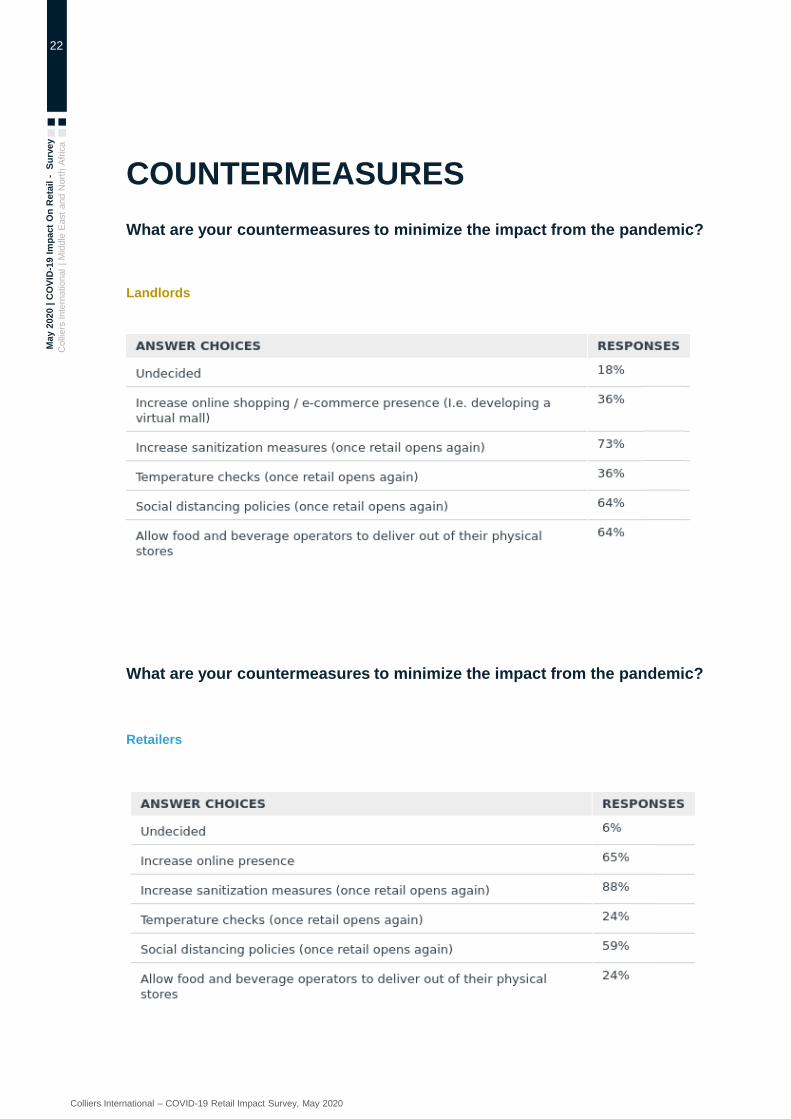

“Both retailers and landlords look at the same

counter measures to minimize the impact of

the pandemic to their business, including

increasing their online presence, increasing

sanitization measures, temperature checks,

social distancing policies and food and

beverage delivery from physical restaurants”

36% of landlords are looking at increasing their online presence (I.e. virtual malls) whilst

65% of retailers intend to do the same.

64% of landlords will allow food and beverage operators to deliver out of their physical

restaurant whilst only 24% of the retailers intend to do this.

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

COUNTERMEASURES

22

What are your countermeasures to minimize the impact from the pandemic?

Retailers

Landlords

What are your countermeasures to minimize the impact from the pandemic?

Colliers International – COVID-19 Retail Impact Survey, May 2020

“There appears to be an opportunity gap for

landlords to recover a possible decline in

retail physical space demand by providing

other support spaces”

76% of retailers stated that they already have an e-commerce platform and 77% of them indicated that they

will invest more in them conversely. 9% of landlords indicated they will invest in this, 45% won’t and 45%

are undecided.

41% of retailers indicate that they already have a fulfillment or mini fulfillment centre and 57% of them

indicate that they intend to invest more in them. Landlords on the other hand indicated that 55% of them

won’t invest in them and 45% are undecided.

29% of retailers indicate that they will invest in a collect, try and return store and 9% of the landlords

indicated that they would invest in this.

18% of retailers indicated that they would invest in cloud kitchens and 64% of landlords indicated they

won’t invest in cloud kitchens.

Increased spending online drives the need for logistics, warehouses, fulfillment centres, cloud kitchens,

collect try and return stores and data storage facilities; providing investment opportunities for investors.

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

INVESTING IN DIGITALIZATION

24

Are you looking to invest in digitalizing your physical retail portfolio

(examples: Virtual Mall)?

Retailers

Landlords

Are you looking to invest in an e-commerce platform to create an omni-

channel customer experience?

*77% of retailers that already have an e-commerce platform indicate they will invest more in it

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

CLOUD KITCHENS

25

Are you looking at introducing “cloud kitchens” in your physical retail

portfolio (cloud kitchens are shared kitchen spaces not accessible for

customers and made for restaurant delivery only)?

Retailers

Landlords

Are you looking at investing in “cloud kitchens” (cloud kitchens are shared

kitchen spaces not accessible for customers and made for restaurant delivery

only)?

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

FULFILLMENT CENTRES

26

Are you looking at introducing “fulfillment or mini fulfillment centers” in your

physical retail portfolio (fulfillment centers are physical locations not

accessible to customers where e-commerce customer goods are fulfilled.)?

Retailers

Landlords

Are you looking at investing in “fulfillment or mini fulfillment centers” to

better service your e-commerce customers (fulfillment centers are physical

locations not accessible to customers where e-commerce customer goods

are fulfilled.) ?

*57% of retailers that already have a fulfillment centre or mini fulfillment center indicate they will invest more in it

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a COLLECT, TRY AND RETURN STORES

27

Are you looking at introducing "Collect, Try and Return" stores in your physical

retail portfolio (Collect, Try and Return stores are physical locations where e-

commerce customers can collect, try and return their orders.)?

Retailers

Landlords

Are you looking at investing in a "collect, try and return store" to better

service your e-commerce customers (collect, try and return stores are

physical locations where e-commerce customers can collect, try and

return their orders.)?

Other: No objection and will promote this

Other: 3 times - not applicable to our business

Colliers International – COVID-19 Retail Impact Survey, May 2020

May 2

020 |

CO

VID

-19 I

mp

act

On

Reta

il -

Su

rvey

Colli

ers

Inte

rnational

| M

iddle

East

and N

ort

h A

fric

a

CONCLUSION

28

It has become apparent from the survey results that the COVID-19 pandemic has caused

unprecedented - largely negative - short term consequences for the retail industry in the

Middle East, at the same time it provides various opportunities for both landlords and

retailers alike. The identified discrepancy between landlords and retailers in Q1 and Q2

revenue signifies the lagging effect of when exactly both parties feel the impact of reduced

income flow. Physical store retailers were affected quicker and harder due to forced

physical store closures; contrasting to the almost instant increase in e-commerce business.

As consumers were forced to move from mostly buying their products in brick and mortar

stores to e-commerce platforms this has created new online customers for retailers,

accelerated an already growing base and is expected to further drive the shift in the retail

landscape and customer behavior.

Conversely to retailers, landlords initial revenue impact has been delayed as rents are paid

in advance, but they are likely to see a greater long-term impact with potential store

closures and the reduced demand for physical space as retailer's online presence grows.

The relationship between landlord and retailer is expected to shift further with a greater

emphasis from retailers on flexible arrangements such as shorter lease terms and greater

reliance on turnover rent-based payments. The inevitable consequence is a move towards

a deeper partnership approach as the shared risk and mutually beneficial outcome begins

to overtake the current transactional relationship model.

In the immediacy of the COVID-19 impact, retailers are mitigating their short-term revenue

shortfalls by asking for support packages from landlords. From the survey results it

becomes clear that landlord and retailer expectations of support packages are not aligned.

Tenants seek uncompromising rent-free periods of 3 to 6 months with no obligation to pay

service charges with landlords responding with 1 to 3 months of rent-free. Retailers and

landlords are aligned over two key issues. Firstly, both are expecting a slow recovery of

their business with the majority of them believing it will take most likely 7 to 12 months or

more than one year to recover. Secondly the implementation of COVID-19 related

precautionary measures.

Whilst the current format of the physical retail store may be under threat cooperation can

exist and future investments opportunities exist in; in e-commerce platforms, cloud kitchens,

fulfillment centers, logistics and collect try and return stores.

Colliers outlook is that the pandemic has potentially triggered a paradigm shift in consumer

behavior, which will subsequently effect retailers and landlords, not only when it comes to

revenue impact but also when it comes down to their future (contractual) relationships,

omni-channel retailing, customer experience and innovation. It becomes increasingly

apparent that dialogue and a mutual open-minded attitude towards the future of landlord

and tenant relationships are crucial to overcome the Covid-19 impact on both their

businesses and to address the future of the retail business.

Colliers International – COVID-19 Retail Impact Survey, May 2020

FOR MORE INFORMATION

Pedro Santos

Associate Director

Retail Advisory

Middle East and North Africa

+971 52 645 21 66

Ricardo Bergsma

Director

Retail Advisory & Retail Leasing

Middle East and North Africa

+971 55 743 37 37