chemicals sector future growth opportunities - africa must be part of your strategy

TRANSCRIPT

Chemicals Sector Future Growth Opportunities

Is Africa a Part of Your Strategy?

Mani James, Operations Director, Africa

Ross McLean, President, Dow Africa

Chemicals, Materials, and Food

2 July 2014

© 2014 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

2

Today’s Presenters

Mani JamesOperations Director- Africa

Frost & Sullivan, AfricaCape Town

Functional Expertise

• Over 13 years of management and strategy consulting experience, having worked for clients in North America, South East Asia, Asia Pacific and Africa.Particular expertise in:

- Market assessment and analysis

- Strategy creation and implementation

- Market entry and expansion strategies

- Customer analysis and segmentation

- Competitive strategy

- Solutions modeling and implementation

Industry Expertise

� Experience base covering a broad range of sectors, working with senior executives to develop and implement strategies across a range of geographies, with particular expertise in:

- Petrochemicals, bio-fuels, materials handling, food additives and chemicals in Africa

- Industrial automation and supply chain management

- Manufacturing

Ross McLeanPresident

Dow AfricaJohannesburg

Ross McLean, is leader for Sub-Saharan Africa and oversees Dow’s growth and expansion across the region.

Ross joined Dow in August 1997 as Finance Director of the South African agricultural chemicals division. Assuming the role of Regional Finance Director for Dow’s Africa operations in 2001, he later added the role of Country Leader and Managing Director for South Africa, to his responsibilities. During this period, Ross led several transactions to divest non-core assets in South Africa, managing successive organizational changes to realign the local team to support Dow’s ongoing business.

Relocating to Dubai in 2006, Ross assumed responsibility for various business development projects in India and the Middle East while developing Dow’s market entry strategy for Africa. Ross has over 20 years experienced in chemicals and related industries. His career spans finance, general management, mergers & acquisitions and strategic development roles in South Africa, the United Kingdom and the United Arab Emirates.

3

Focus Points

1. Occasion for the Analyst Briefing

2. Mega Trends: Then and Now

3. Case Study on DOW Chemical Company – Africa Story

4. Mega Trends: Fast Forward to 2022

4

Poll Question 1

Which group of sub-Saharan African countries are anticipated to provide future growth opportunities after South Africa, Nigeria, Kenya, and Ghana?

• Uganda, Tanzania, Ethiopia, and Rwanda

• Mozambique, Angola, Tanzania, and Zambia

• Rwanda, Uganda, Botswana, Ethiopia, and Namibia

5

Agenda

This analyst briefing:

o Mega Trends in 2010

o Success story in Africa – Dow Africa

o Mega Trends 2022

o Q & A Session

6

Urbanisation: Then and Now

Water and Wastewater Treatment

Construction & Infrastructure (Chemicals)

Urbanisation rates will continue to increase in all African regions

62%50% 51%

24%

63%

50% 52%

25%

Urbanisation as a % of Total Population: 2010 2014

Revenue Prediction in 2010 for 2013

Actual Revenues

in 2013

SouthAfrica

$916.3M $855.0M

Nigeria $241.2M $215.0M

Kenya $88.6M $82.5M

Revenue Prediction in 2010 for 2013

Actual Revenues

in 2013

SouthAfrica

$174.8M $160.0M

Kenya $73.2M $67.5M

Nigeria $160.5M $155.0M

South Africa Nigeria Ghana Kenya

Revenue Prediction in 2010 for 2013

Actual Revenues in

2013

South Africa $19.7B $19.6B

Nigeria $16.3B $16.0B

Revenue Prediction in 2010 for 2013

Actual Revenues in

2013

South Africa $4.5B $4.4B

Nigeria $273.4M $274.0M

Kenya $106.5M $105M

Ke

y D

rive

rs

for

co

ntin

ued g

row

th

Water and wastewater treatment growth to increase to achieve millennium development goals

Urbanisation and growing middle income earners continue to drive demand for commodity products

Materials – Packaging

Oil & Gas – Petrochemicals

Source: IMF, Frost & Sullivan

7

2010

2010

2010

2010

Road Rail Electricity Airports Telecom

2013

2013

2013

2013

Road Rail Electricity Airports Telecom

Infrastructure Development: Then and Now

Road and rail = km per 1000 capita; Electricity = MW per 1000 capita; Airports and telecom per capita

$XXBKenya ($B) Ghana ($B) South Africa ($B)Nigeria ($B)

15%

Investment since 2010

to 2013 to $2.9B

Investment since 2010

to 2013 to $1.5B

4%

Investment since 2010

to 2013 to $6.5B

7%

Infr

astr

uctu

re

Eff

icie

ncy

Ra

nkin

g

109 Ghana

135 Nigeria

1

148

102 Kenya

66 South Africa

6.4 4.525.4

15.284.6

64.2

Planned spend 2010-2013

Actual spend 2010-2013

10.75.9

Planned spend 2010-2013

Actual spend 2010-2013

Planned spend 2010-2013

Actual spend 2010-2013

Planned spend 2010-2013

Actual spend 2010-2013

Source: IMF, World Bank, PWC, Frost & Sullivan

8

Sustainability: Then and Now

HydroFossil Fuels (includes nuclear for SARenewables

2010 2013

2010 2013

Kenya: Energy Mix Evolution

South Africa: Energy Mix Evolution

2010 2013

Ghana: Energy Mix Evolution

2010 2013

Nigeria: Energy Mix Evolution

15%

KenyaAgriculture yield

by 2030 with a

2% GDP

investment in a green economy

24%

South AfricaIncrease crop yields by 2030 –investing in ecological practices

Source: The Financial Times Limited, Frost & Sullivan

Trillion cubic feet shale gas reserves in South Africa

468

Planned or possible investment in the US by chemicals companies to use shale gas

$91B

Reduction in price since 2011 for ethane in the US produced from shale feedstock

>1/3

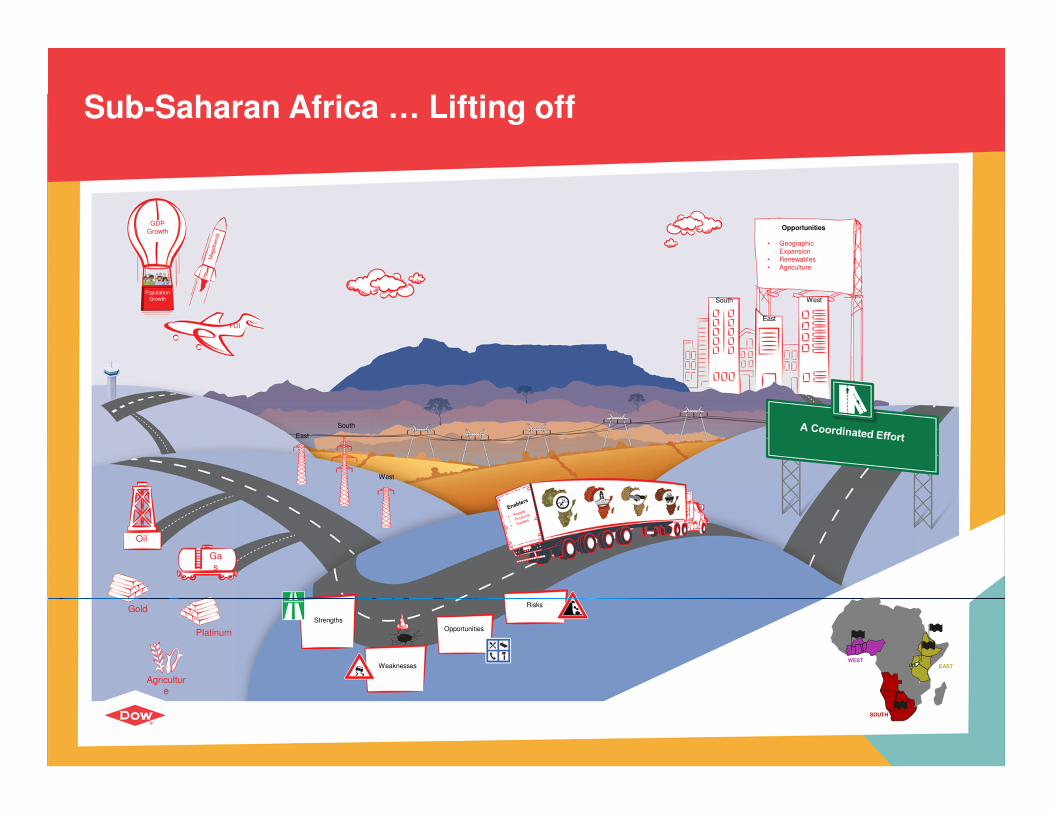

Sub-Saharan Africa … Lifting off

EAST

SOUTH

WEST

GDP Growth

Population Growth

FDI

South

West

East

Oil

Gas

Strengths

Weaknesses

Opportunities

RisksGold

Agriculture

Opportunities

• Geographic Expansion

• Renewables• Agriculture

South West

East

Platinum

10

Mega Trends: Fast Forward to 2022

Urbanisation and Infrastructure Development

Energy Demand and Resource

Drain

Water and Food Scarcity

Supply Chain Efficiencies

Emerging African Economies

11

Emerging African Economies

• x

South Africa

Nigeria

Kenya

Ghana

IndicatorAngola Tanzania

2014 GDP ($ billion) 129.79 36.61

GDP Growth Rate (2015-2019)

5.6% 7.0%

Manufacturing Size($ million in 2012)

7,220.4 2,609.2

Ease of Doing Business (2014) 179/189 145/189

Indicator Zambia Mozambique

2014 GDP ($ billion) 24.85 17.35

GDP Growth Rate (2015-2019)

6.6% 7.8%

Manufacturing Size($ million in 2012)

1,723.6 *1,573.9

Ease of Doing Business (2014) 83/189 139/189

Source: IMF, World Bank, Frost & Sullivan* 2011 data

Rw

anda

MATZ and

RUBEN

INTRODUCING...

12

Poll Question 2

Have you identified the right distribution partners for your African Growth Strategy?

• Yes

• Not sure, time will tell

• No, we are searching for alternatives

13

Supply Chain Efficiencies—Major Trends

Source: Frost & Sullivan

Improve Integrate InvestKey Strategies:

14

Supply Chain Efficiencies—Logistics Performance Index

Source: World Bank, Frost & Sullivan

Logistics Performance Index, Global, 2010 and 2014

Year Rank Score

Angola2014 112 2.54

2010 142 2.25

Tanzania2014 138 2.33

2010 95 2.60

Zambia2014 123 2.46

2010 138 2.28

Mozambique2014 147 2.23

2010 136 2.29

Uganda2014 - -

2010 66 2.82

Ethiopia2014 104 2.59

2010 123 2.41

Namibia2014 93 2.66

2010 152 2.02

Botswana2014 120 2.49

2010 134 2.32

Rwanda2014 80 2.76

2010 151 2.04

Growth of African Cities% increase, 2010- 2025 forecast

0 50 100

Cape Town

Johannesburg

Durban

Cairo

Casablanca

Algiers

Alexandria

Douala

Accra

Ibadan

Lagos

Dakar

Abidjan

Addis Ababa

Luanda

Kinshasa

Nairobi

Dar es Salaam

15

Urbanisation and Infrastructure Development—$28 billion will be invested in transport corridor development

Road

Rail

Ports

$9.2 billion

$14.8 billion

$3.5 billion

Roads in good condition

Western 72%

Central 49%

Eastern 82%

Southern 100%

Container dwell times (International standard: 7 days)

Western 11-30 days

Eastern 5-28 days

Southern 4-8 days

Freight transport by rail

Western 11%

Central 2%

Eastern 2%

Southern 85%

Existing road networks will be rehabilitated and expanded to create nine Trans-African Highways

Rail networks will be extended and upgraded to complement the Trans-African highways

Capacity building at ports will decrease bottlenecks and support growth in trade and industry

Ten transport corridors are being developed across the region to improve road and rail networks and increase port capacity

Current State of Transport Infrastructure:

*based on active projects in 2013 Source: World Bank; Frost & Sullivan

16

Energy Demand and Resource Drain—African Trade Corridors: What is driving their development and why?

C

B Bauxite

UraniumGold

Copper

Diamonds Oil

Gas Timber

KEY:

Iron Ore

Coal

C

CC

CC

C

C

BB

B

Is the Green Economy relevant to Africa? Source: EIA; Frost & Sullivan

Angola:

• Second-largest oil producer in SSA with 1.8 million barrels per day in 2013

• Second-largest volume of proved natural gas reserves in SSA in 2014 (9.71 trillion cubic feet)

• First LNG plant opened in 2013 in Soyo

Mozambique:

• Contains 4.5 trillion cubic feet of proved natural gas reserves

• First commercial crude oil production to take place in Inhassoro in 2014

Tanzania:

• Produces small volumes (32.8 billion cubic feet in 2012) of natural gas for own use

• Future export opportunities with offshore natural gas discoveries

17

Water and Food Scarcity

2012 Global Hunger Index

Level of Severity

Angola 24.1 Alarming

Tanzania 19.3 Serious

Zambia 23.3 Alarming

Mozambique 23.3 Alarming

Uganda 16.1 Serious

Ethiopia 28.7 Alarming

Namibia 13.2 Serious

Botswana 13.7 Serious

Rwanda 19.7 Serious

Source: IFPRI, Frost & Sullivan

Increase in net food imports at constant prices in sub-Saharan Africa since 2000 (FAO).>60%

Cereal yield (kg per hectare) vs. rate of developed countries

Sub-Saharan African share of the global crop protection market

5%

Fertilizers used per hectare (aim is 50kg) compared to 80kg, the world average.

Soil degradation. Annual mineral nutrient loss ranges from 30kg to 60kg per hectare (Henao & Baanante).

75%

27%

9kg

In Africa:

Income from crop production

Annual value of grain is lost postharvest

70%

15%

Ageing infrastructure, water leakages

Dam rehabilitation

Treatment plants need to keep pace with urbanisation

1

34

5

2

Severity

18

Key Take-Aways – Success factors in Africa

Key Cash cow products in the broad range

Strengthen e-commerce platforms

Affordable product pricing

Strong local Distributor partnerships

Country and city specific strategy

Regulatory and incentive policies by country

Trusted brand & loyalty -Strong local presence

Key

Success Factors

Aggressive product promotion

“Do not judge me by my successes, judge me by how many times I fell down and got back up again” Nelson Mandela

19

Next Steps

Develop Your Visionary and Innovative SkillsGrowth Partnership Service Share your growth thought leadership and ideas or

join our GIL Global Community

Join our GIL Community NewsletterKeep abreast of innovative growth opportunities

20

Your Feedback is Important to Us

Growth Forecasts?

Competitive Structure?

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

What would you like to see from Frost & Sullivan?

21

https://twitter.com/frostsullivansa

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

22

For Additional Information

Samantha James

Corporate Communications

African Operations

+27 21 680 3574

Mani James

Operations Director

African Operations

+27 21 680 3208

Avril Harvey

Team leader

Chemicals, Materials and Food

+27 21 680 3283

Danielle Kruger

Strategic Account Manager

Chemicals , Materials and Food

+27 21 680 3262