chapter 13 prepared by richard j. campbell copyright 2011, wiley and sons auditing human resources...

TRANSCRIPT

Chapter 13

Prepared by Richard J. Campbell

Copyright 2011, Wiley and Sons

Auditing Human ResourcesProcesses: Personnel and Payroll inService Industries

Learning Objectives1. Be familiar with the human resources

activities in a public accounting firm.

2. Learn the activities, transactions, risks, ICFR, and documents related to human resources. Recognize the impact of relevant accounting standards on the activities and transactions.

3. Understand the general structure and activities of outsourcing the payroll function to an outside service provider.

4. Understand the meaning and value of both types of service auditor (SAS 70) reports, how they may provide audit evidence, and under what circumstances more audit evidence is needed.

Chapter 13-1

Learning Objectives

5. Link the management assertions, purposes of specific controls, controls, and tests of controls for human resources.

6. Describe the purposes and execution of related substantive audit procedures for human resources accounts and disclosures, including dual purpose tests, substantive analytical procedures, and details of balances.

Chapter 13-2

Service Industries within Business Categories

Learning Objective #1Chapter 13 -3

EXHIBIT 13-1

OVERVIEW

Learning Objective #1Chapter 13 -4

Regardless of the industry, personnel functions include maintaining personnel records and performing administrative responsibilities for benefit plans.

Payroll functions involve calculating, processing, and posting employee compensation and other related expenses and liabilities

HUMAN RESOURCES ASPECTS OF PUBLIC ACCOUNTING

Chapter 13 -5 Learning Objective #1

HUMAN RESOURCES ASPECTS OF PUBLIC ACCOUNTING

Chapter 13 -6 Learning Objective #1

Hiring information is collected in the employee’s personnel file.

The information added to the payroll master file includes the employee’s name, contact information identification number, rank or staff classification, department, salary, and deduction information.

With this information the payroll processing system is able to calculate and generate a salary payment for the employee

This information is integrated with the engagement management system

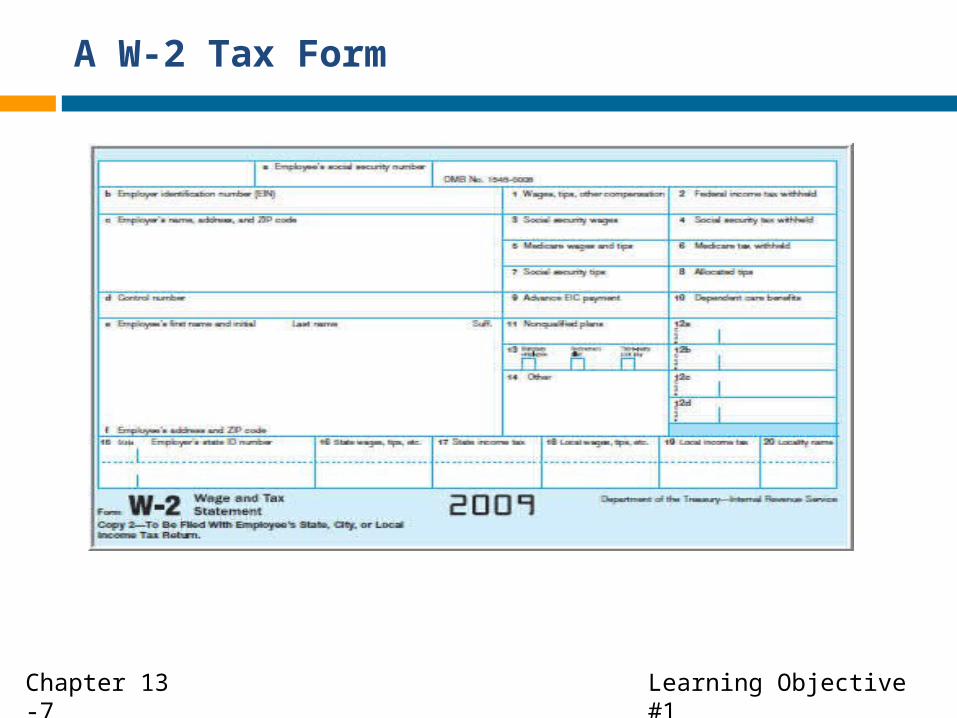

A W-2 Tax Form

Chapter 13 -7 Learning Objective #1

Public Accounting Firm Work-in-Process Record

Chapter 13 -8 Learning Objective #1

Time and Expense Report Input to PayrollProcessing

Learning Objective #1Chapter 13-9

EXHIBIT 13-2

Time and Expense Report Input toEngagement Management

Learning Objective #1Chapter 13-10

EXHIBIT 13-3

BUSINESS PROCESSES, DOCUMENTS, AND INTERNAL CONTROLS

Learning Objective #2Chapter 13-11

Management objectives related to payroll center around paying employees accurately, paying other entities for payroll-related liabilities as required, satisfying reporting obligations imposed by government, and accounting for the various transactions properly in the accounting records and financial statements.

In service industries, human resources expenses may be the largest expense incurred.

Employees document information regarding their identification and status for taxes on W-4 forms.

A W-4 Tax Form

Learning Objective #2Chapter 13-12

A Job Time Ticket

Chapter 13 -13 Learning Objective #3

A Sample Payroll Register

Chapter 13 -14 Learning Objective #2

Business Activities and Related Documents

Chapter 13 -15 Learning Objective #3

EXHIBIT 13-4

Potential Misstatements and Controls

Chapter 13 -16 Learning Objective #2

The major internal control concerns related to human resources and payroll are that payments are for valid transactions and are authorized.

To accomplish the payroll controls objectives, the company must have policies and procedures in place regarding human resources.

Check-in and check-out functions can be punching a time clock or logging in and out on a computer terminal.

USING AN OUTSIDE SERVICE PROVIDER FOR PAYROLL

Learning Objective #3Chapter 13 - 17

Many organizations use an outside service provider to perform the calculations and prepare the records associated with paying employees.

The services typically provided by external payroll processing service organizations include: Updating the payroll master file Keeping track of current and year-to-date information by

employee as well as for the company as a whole Preparing documents and forms required for tax purposes

such as W-2 forms and quarterly payroll tax returns Submitting information for general ledger entries back to

the organization

Outputs of the Service Provider

Learning Objective #3Chapter 13 - 18

The output can be provided in either electronic or hard-copy form: Updated payroll master file Payroll register or journal Deduction exception report Management summary Labor cost report

Payroll Outsourcing Activities

Learning Objective #3Chapter 13 - 19

EXHIBIT 13-5

User Company Controls

Learning Objective #3Chapter 13 - 20

Employee-Related Controls Input and Submission Controls Controls for Correcting Processing

Errors Output-Monitoring Controls

REPORTS ON THE PROCESSING OF TRANSACTIONS BYA SERVICE ORGANIZATION

Learning Objective #4Chapter 13 - 21

If the services affect any of the items in the following list, the service provider is considered a part of the entity’s IT system. Classes of transactions significant to the financial

statements Procedures of initiating, recording, processing and

reporting transactions Accounting records, supporting information and

specific accounts related to the entity’s transactions and financial statements

Method of capture of events and conditions significant to the entity’s financial statements

The financial reporting process leading to preparation of financial statements, including estimates and disclosures

TESTS OF CONTROLS FOR HUMAN RESOURCES TRANSACTIONS

Learning Objective #5Chapter 13 - 22

EXHIBIT 13-6

TESTS OF CONTROLS FOR HUMAN RESOURCES TRANSACTIONS

Learning Objective #5Chapter 13 - 23

EXHIBIT 13-6

TESTS OF CONTROLS FOR HUMAN RESOURCES TRANSACTIONS

Learning Objective #5Chapter 13 - 24

EXHIBIT 13-6

TESTS OF CONTROLS FOR HUMAN RESOURCES TRANSACTIONS

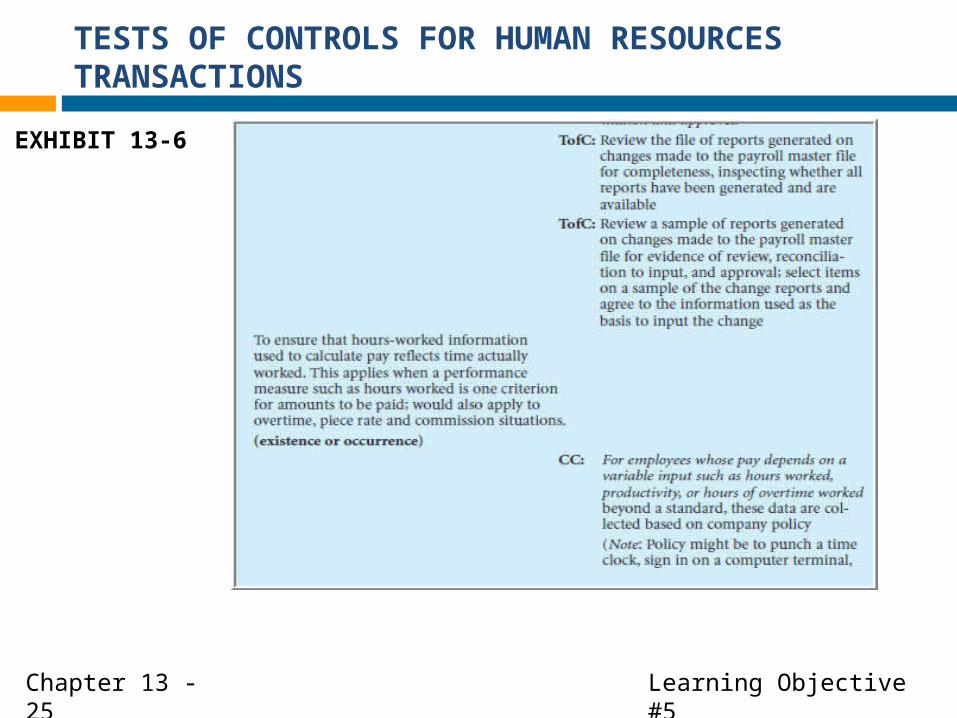

Learning Objective #5Chapter 13 - 25

EXHIBIT 13-6

TESTS OF CONTROLS FOR HUMAN RESOURCES TRANSACTIONS

Learning Objective #5Chapter 13 - 26

EXHIBIT 13-6

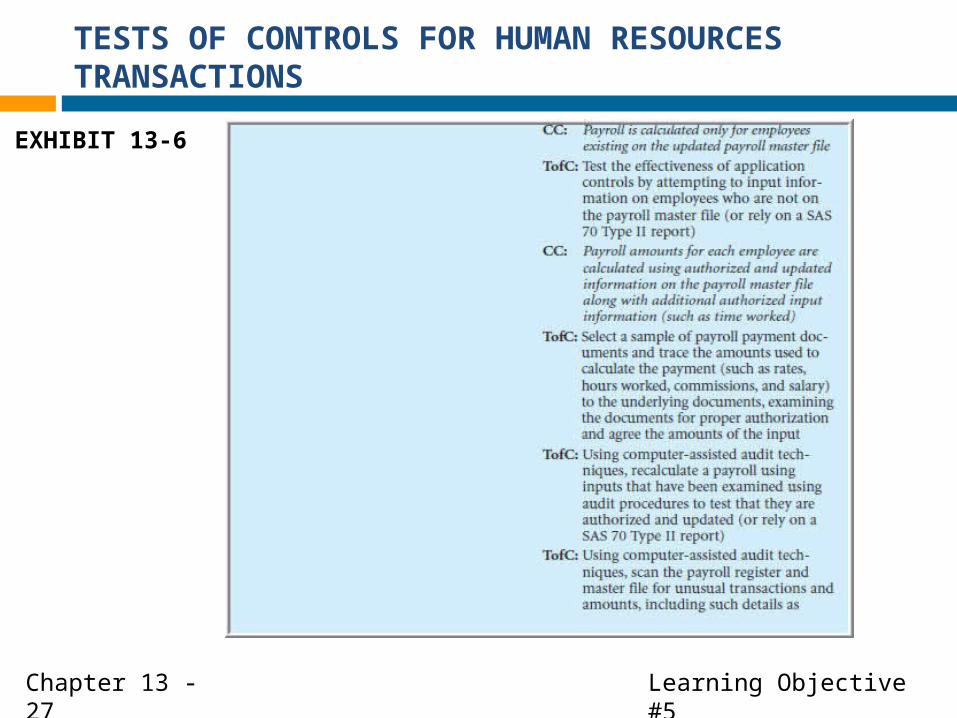

TESTS OF CONTROLS FOR HUMAN RESOURCES TRANSACTIONS

Learning Objective #5Chapter 13 - 27

EXHIBIT 13-6

TESTS OF CONTROLS FOR HUMAN RESOURCES TRANSACTIONS

Learning Objective #5Chapter 13 - 28

EXHIBIT 13-6

TESTS OF CONTROLS FOR HUMAN RESOURCES TRANSACTIONS

Learning Objective #5Chapter 13 - 29

EXHIBIT 13-6

TESTS OF CONTROLS FOR HUMAN RESOURCES TRANSACTIONS

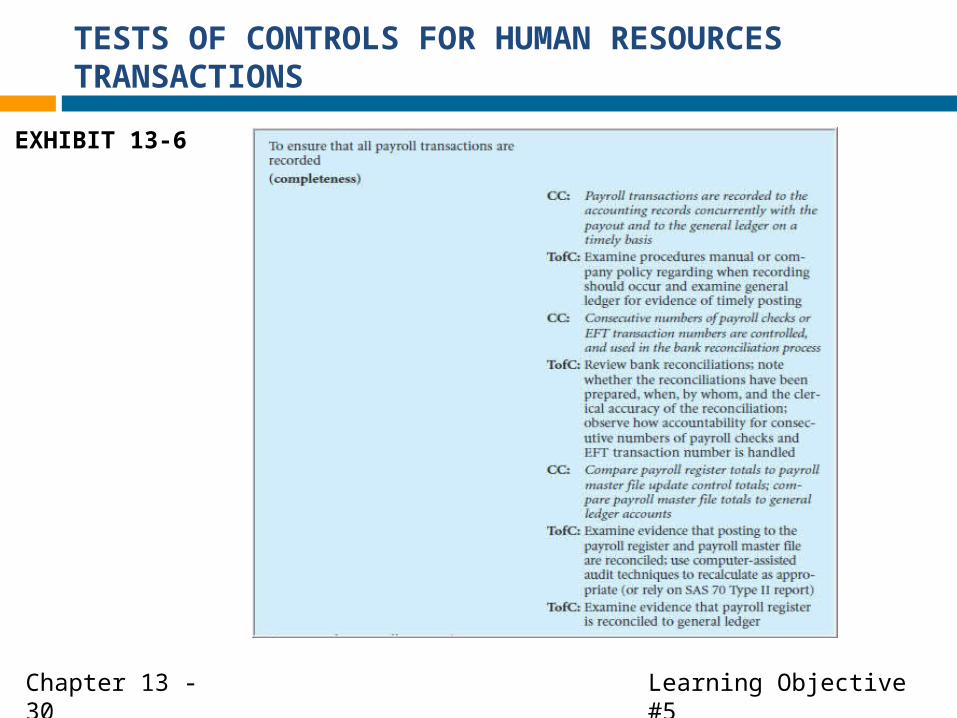

Learning Objective #5Chapter 13 - 30

EXHIBIT 13-6

TESTS OF CONTROLS FOR HUMAN RESOURCES TRANSACTIONS

Learning Objective #5Chapter 13 - 31

EXHIBIT 13-6

TESTS OF CONTROLS FOR HUMAN RESOURCES TRANSACTIONS

Learning Objective #5Chapter 13 - 32

EXHIBIT 13-6

DUAL PURPOSE TESTS

Learning Objective #6Chapter 13 - 33

EXHIBIT 13-7

DUAL PURPOSE TESTS

Learning Objective #6Chapter 13 - 34

EXHIBIT 13-7

DUAL PURPOSE TESTS

Learning Objective #6Chapter 13 - 35

EXHIBIT 13-7

Examples of Tests of Controls for Payroll Transactions

Learning Objective #6Chapter 13 - 36

EXHIBIT 13-8

Examples of Tests of Controls for Payroll Transactions

Learning Objective #6Chapter 13 - 37

EXHIBIT 13-8

Examples of Tests of Controls for Payroll Transactions

Learning Objective #6Chapter 13 - 38

EXHIBIT 13-8

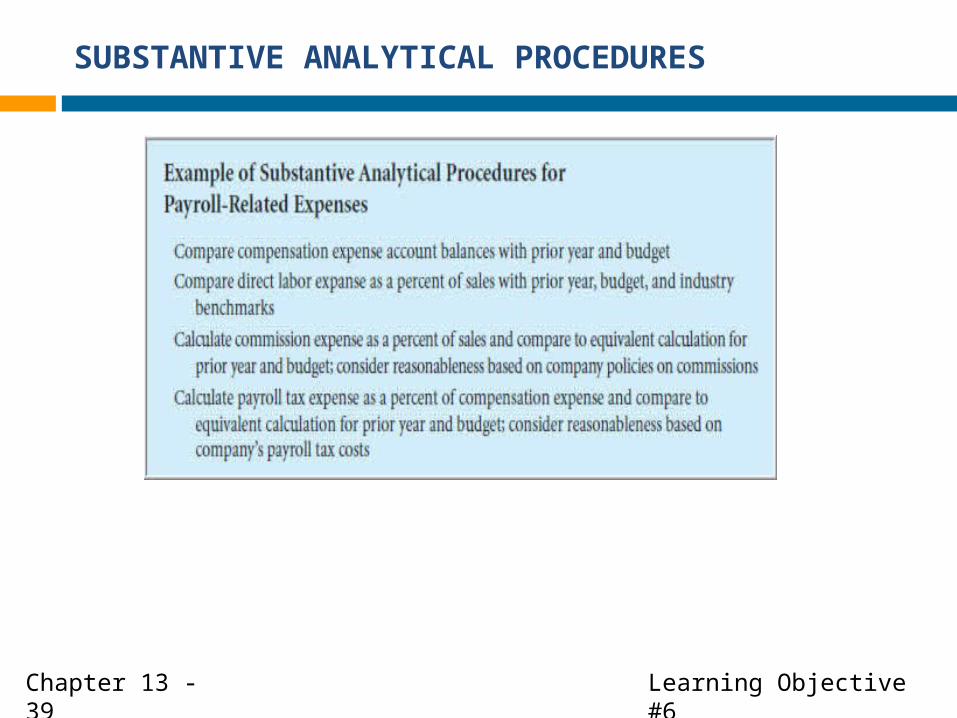

SUBSTANTIVE ANALYTICAL PROCEDURES

Learning Objective #6Chapter 13 - 39

SUBSTANTIVE ANALYTICAL PROCEDURES

Learning Objective #6Chapter 13 - 40

EXHIBIT 13-9

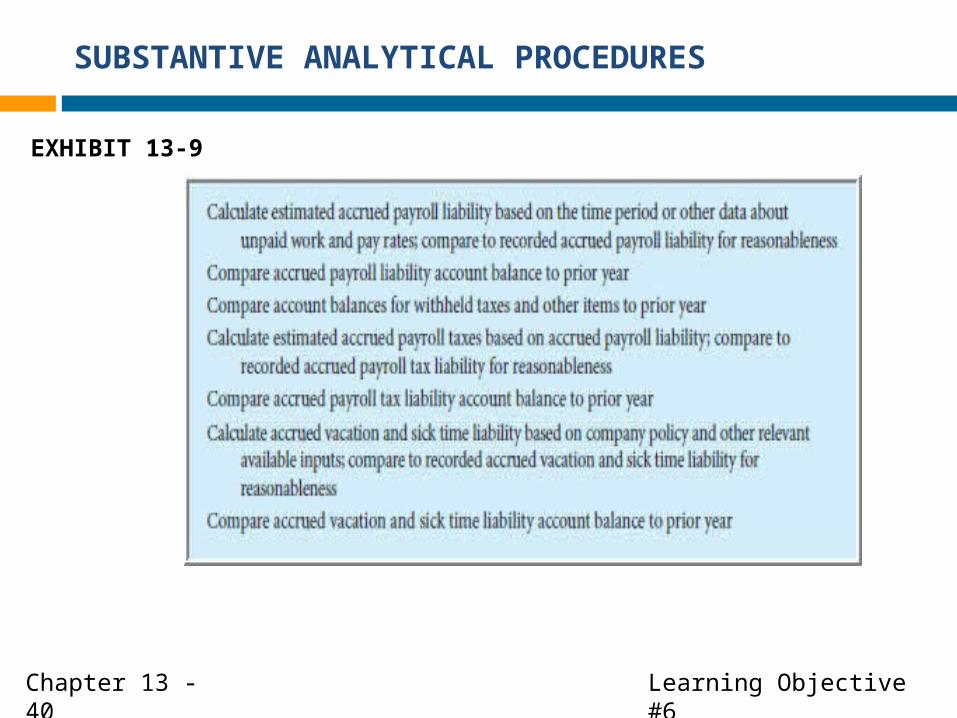

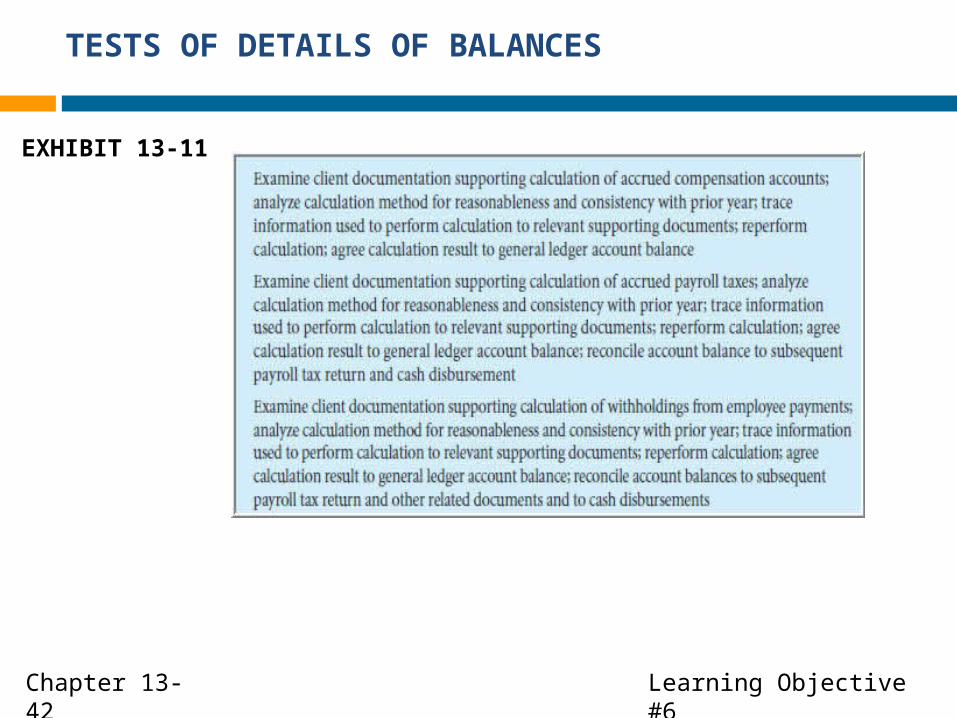

TESTS OF DETAILS OF BALANCES

Learning Objective #6Chapter 13-41

EXHIBIT 13-10

TESTS OF DETAILS OF BALANCES

Learning Objective #6Chapter 13-42

EXHIBIT 13-11

Review Question

Chapter 13-43

In which type of organization would anauditor expend more audit effort addressingwhether payroll costs were posted to the properaccount?(a) Not-for-profit(b) Service(c) Retail(d) Manufacturing

Review Question

Chapter 13-44

Which department should control theinformation on employees’ checking accountswhen the employees have provided authorizationto the employer to pay them by direct deposit?(a) Personnel(b) Treasurer or cashier(c) Accounting and payroll(d) Line department for each employee

Review Question

Chapter 13-45

Which of the following is not a serviceindustry?(a) Banking(b) Health care(c) Textbook publishing(d) Public accounting

Copyright

“Copyright © 2011 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.”