cdm: a catalyst for renewable energy in developing countries? lessons from early projects veronique...

Post on 22-Dec-2015

218 views

TRANSCRIPT

CDM: A Catalyst for Renewable

Energy in Developing Countries?Lessons from Early Projects

Veronique Bishop, Franck Lecocq

World Bank, Carbon Finance Business &

Development Economics Research Group

International Energy WorkshopParis, 22-24 June 2004

The opinions expressed in this presentation are the sole responsibility of the authors. They do not necessarily represent the views of the World Bank, its executive directors or the countries they represent, nor do they

necessarily represent the views of the Carbon Finance Business or the Participants in the funds it manages.

Motivation

• About $5,000,000,000 of investment in power generation and transmission required over next 30 years to meet electricity demand in developing countries (IEA, WEO 2003)

• To do so, private capital is needed, but private investment flows have been decreasing steadily since 1997

• Can the CDM help overcome barriers to investment in clean energy, especially renewables, in developing countries?

Outline

1. Introduction

2. The CDM: Definition and activity

3. Direct cash-flow Benefits of CDM on renewable energy projects

4. Indirect benefits of CDM contracts

5. Conclusion: Replicability of early project examples

The Clean Development Mechanism (CDM)

• Flexibility mechanism of the Kyoto Protocol.

• Project-based mechanism by which…

• an entity in Annex B can participate in the financing of a project which is located in a non-Annex B country…

• and reduces emissions compared with what would have happened otherwise…

• to get emission credits (CERs) in returns.

Can the CDM contribute to renewables penetration?

• S. Mathy, J.-C. Hourcade & C. de Gouvello (2001): the CDM can leverage development because

1. It puts a value on the global environment benefits of projects which reduce GHG emissions (direct cash-flow benefits)

2. And it provides foreign capital, which is cheaper than domestic capital (indirect benefits)

• Do early CDM experience in renewables support the MHG hypothesis?

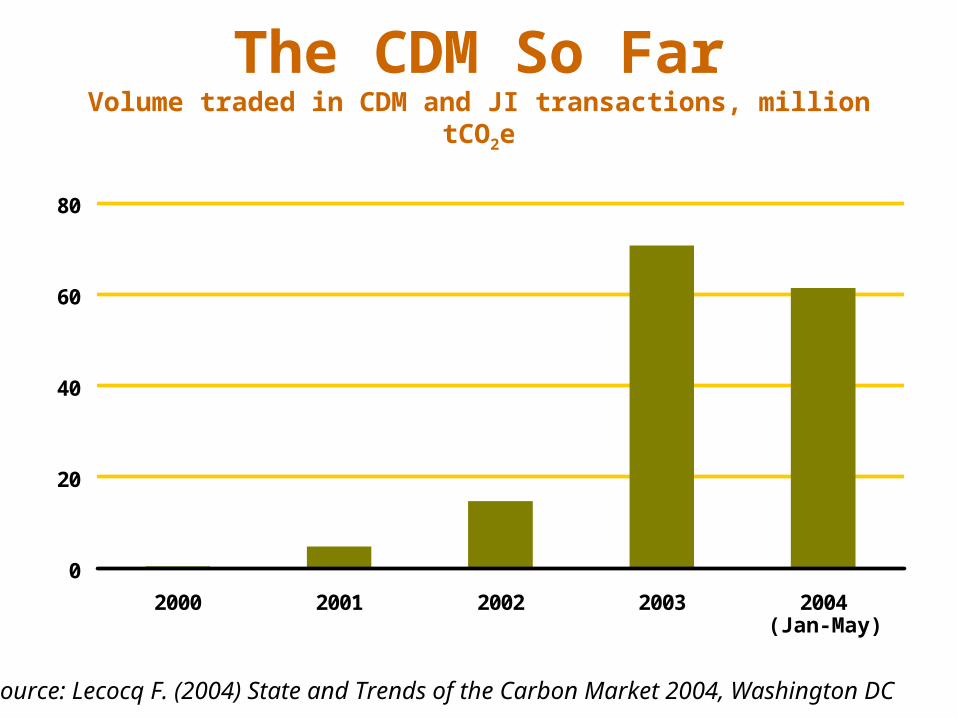

The CDM So FarVolume traded in CDM and JI transactions, million tCO2e

(Jan-May)

Source: Lecocq F. (2004) State and Trends of the Carbon Market 2004, Washington DC

0

20

40

60

80

2000 2001 2002 2003 2004

Technology DistributionIn percent of volume purchased from Jan. 2003 to May 2004

LFG18%

Hydro11%

Wind6%

Biomass14%

HFC31%

N2O1%

Fuel Switching

4%

EnergyEfficiency

6%

LULUCF4%

Other5%

Source: Lecocq F. (2004) State and Trends of the Carbon Market 2004, Washington DC

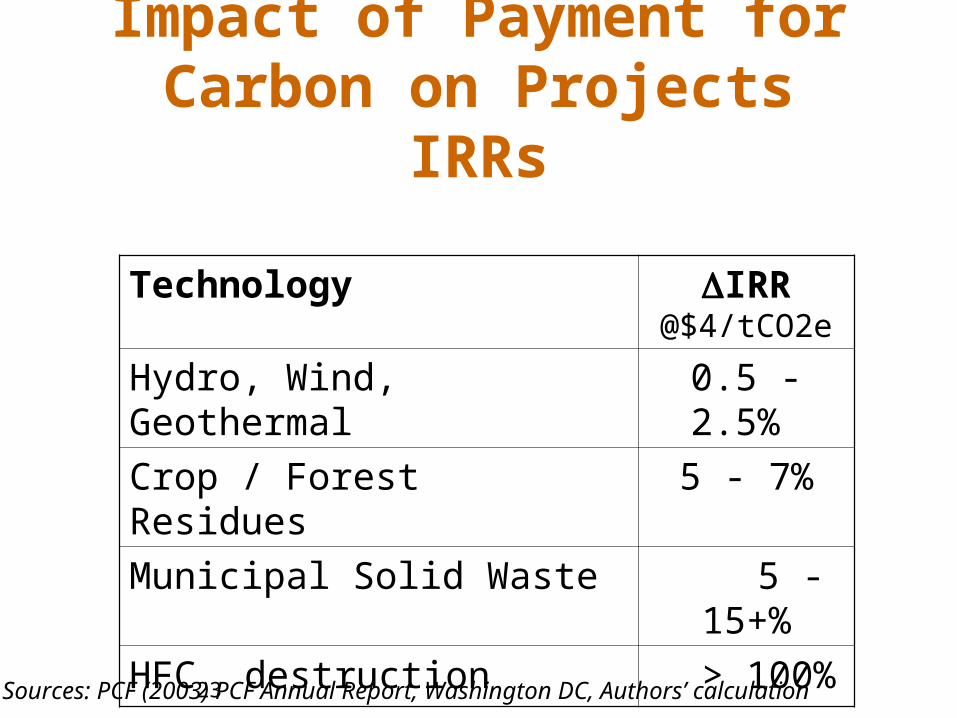

Impact of Payment for Carbon on Projects IRRs

Technology IRR @$4/tCO2e

Hydro, Wind, Geothermal 0.5 - 2.5%

Crop / Forest Residues 5 - 7%

Municipal Solid Waste 5 - 15+%

HFC23 destruction > 100%

Sources: PCF (2003) PCF Annual Report, Washington DC, Authors’ calculation

Renewables: Carbon Revenues per Unit of Output

Fuel Displaced Generic Emissions Factor

(tCO2e/MWh)

Carbon Revenue US$/MWh at US$4/tCO2e

Gas 0.50 $2.00

Coal 0.85 $3.40

Diesel 0.75-1.50 $3.00 - $6.00

Source: PCF (2003) PCF Annual Report, Washington DC

Direct Benefits of CDM on Project Finance: Summary

• At current prices ($4/tCO2e), direct cash-flow impact of CDM is significant for projects mitigating non-CO2 gases

• For renewable energy, on the other hand, the impact is positive but small

not sufficient, in general, to make project viable

• In addition, CERs paid on delivery in most contracts (commodity model) and not upfront as postulated in MHG:

The upfront financial gap persists

Indirect Benefits of CDM

• Emission Reduction Purchase Agreements (ERPA) generate high quality cash-flow

– OECD – sourced– Investment-grade payor (usually governments or

highly rated private companies)– $- or €- denominated Exchange Rate Risk can be eliminated

• In addition, financial engineering can help tap additional upfront capital through monetization of ERPA

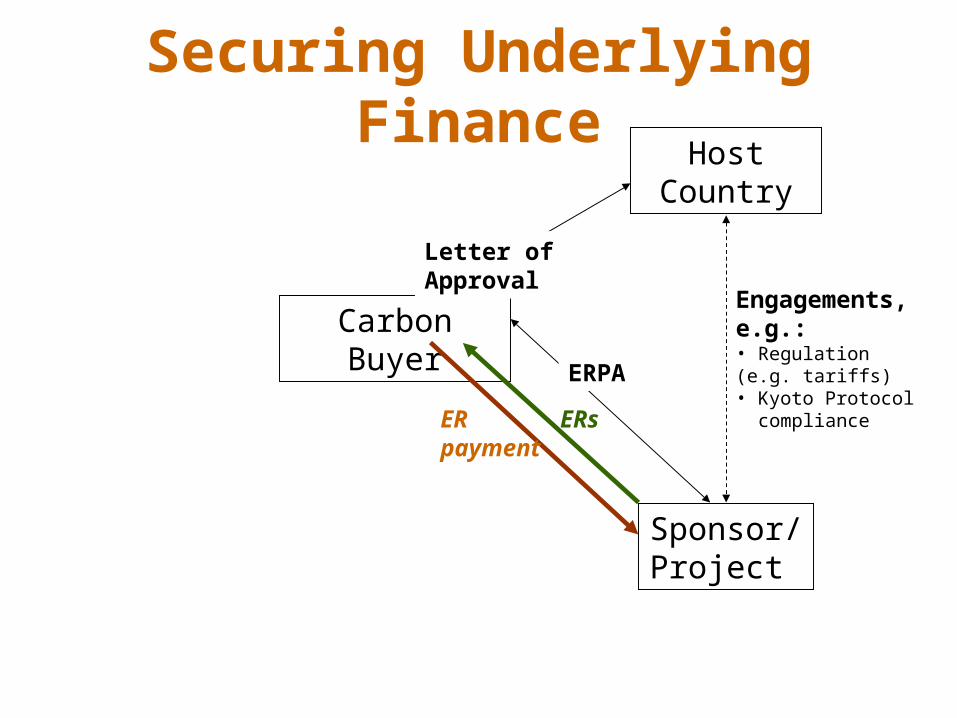

Host Country

Sponsor/ Project

Carbon Buyer

ERPA

Engagements, e.g.:• Regulation (e.g. tariffs)• Kyoto Protocol compliance

ERs

Letter of Approval

ER payment

Securing Underlying Finance

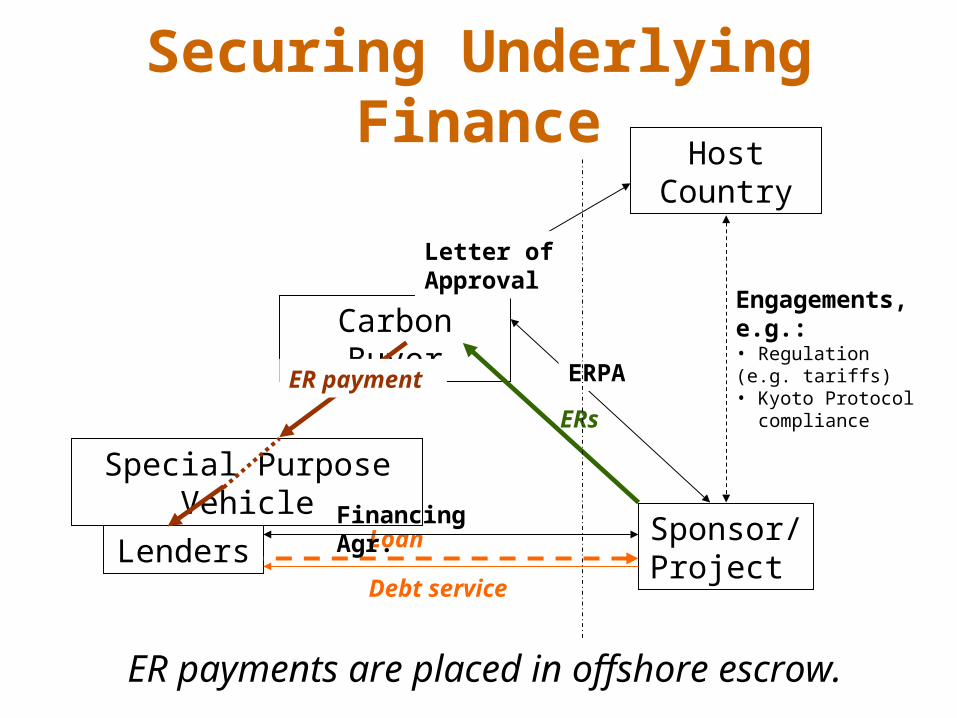

Host Country

Sponsor/ Project

Carbon Buyer

ERPA

Engagements, e.g.:• Regulation (e.g. tariffs)• Kyoto Protocol compliance

ERs

Letter of Approval

ER payment

Securing Underlying Finance

LendersDebt service?

Loan ??

Special Purpose Vehicle

Host Country

Sponsor/ Project

Carbon Buyer

ERPA

Engagements, e.g.:• Regulation (e.g. tariffs)• Kyoto Protocol compliance

ERs

Letter of Approval

Securing Underlying Finance

LendersDebt service

LoanFinancing Agr.

ER payment

ER payments are placed in offshore escrow.

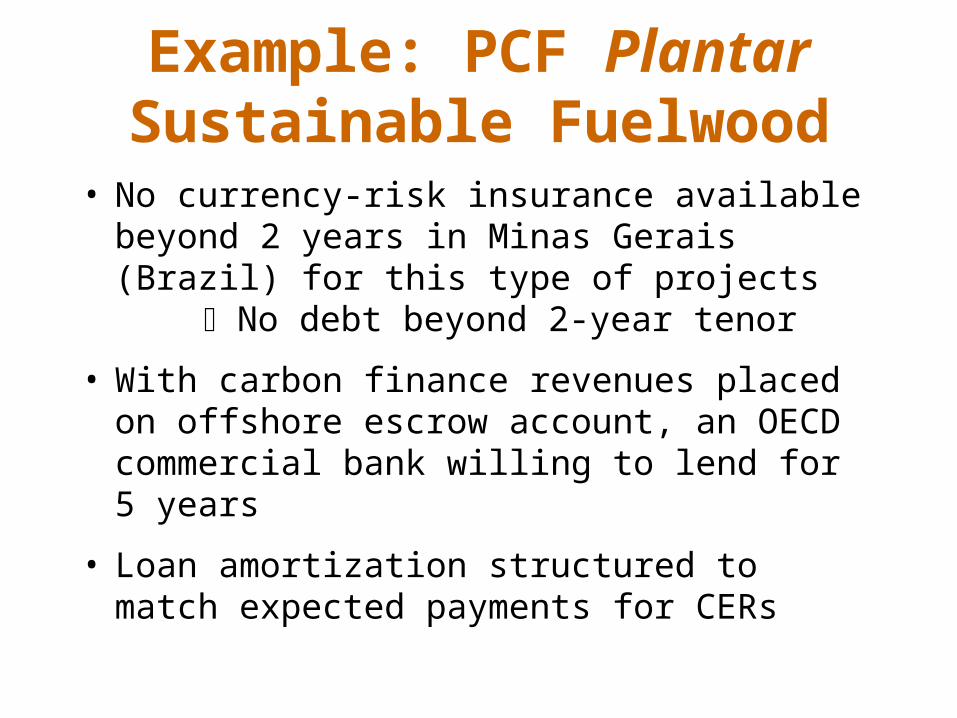

Example: PCF Plantar Sustainable Fuelwood

• No currency-risk insurance available beyond 2 years in Minas Gerais (Brazil) for this type of projects

No debt beyond 2-year tenor

• With carbon finance revenues placed on offshore escrow account, an OECD commercial bank willing to lend for 5 years

• Loan amortization structured to match expected payments for CERs

Example: PCF Plantar Sustainable Fuelwood

-4000

-2000

0

2000

4000

6000

1 2 3 4 5 6 7

Year

Cash

Flo

ws (

$000)

LoanDisbursementPCF Payments

LoanAmortization

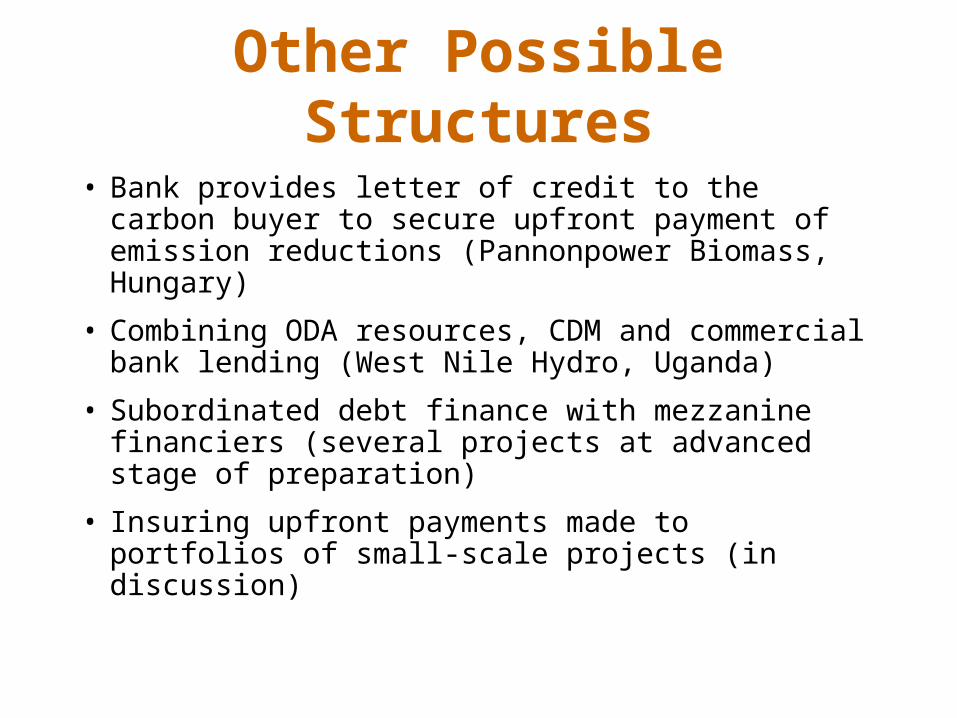

Other Possible Structures

• Bank provides letter of credit to the carbon buyer to secure upfront payment of emission reductions (Pannonpower Biomass, Hungary)

• Combining ODA resources, CDM and commercial bank lending (West Nile Hydro, Uganda)

• Subordinated debt finance with mezzanine financiers (several projects at advanced stage of preparation)

• Insuring upfront payments made to portfolios of small-scale projects (in discussion)

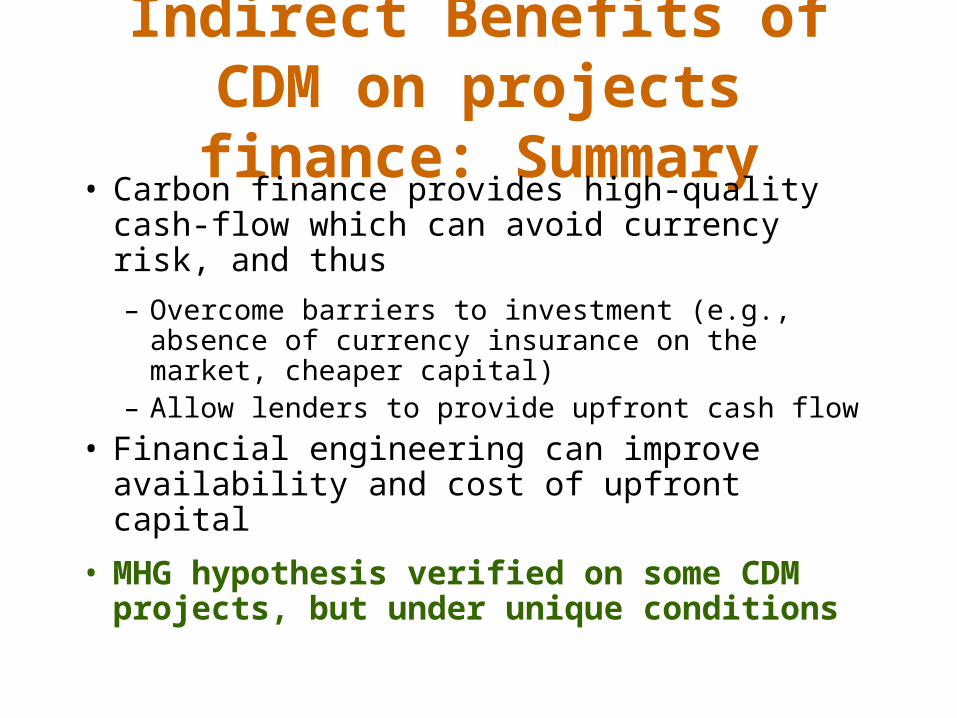

Indirect Benefits of CDM on projects finance: Summary

• Carbon finance provides high-quality cash-flow which can avoid currency risk, and thus

– Overcome barriers to investment (e.g., absence of currency insurance on the market, cheaper capital)

– Allow lenders to provide upfront cash flow

• Financial engineering can improve availability and cost of upfront capital

• MHG hypothesis verified on some CDM projects, but under unique conditions

Is this Replicable for Renewable Energy?

Hardly! There are still considerable barriers:

• Cash flow generated by CDM remains small

• CDM process still too complex

– High transaction costs; Policy risks (host country approval, non-registration) cannot be mitigated by the private sector

• Additionality paradox: The best projects are also the most vulnerable to registration risk

• Market too thin (< $600m) for financial institutions to invest human / financial capital

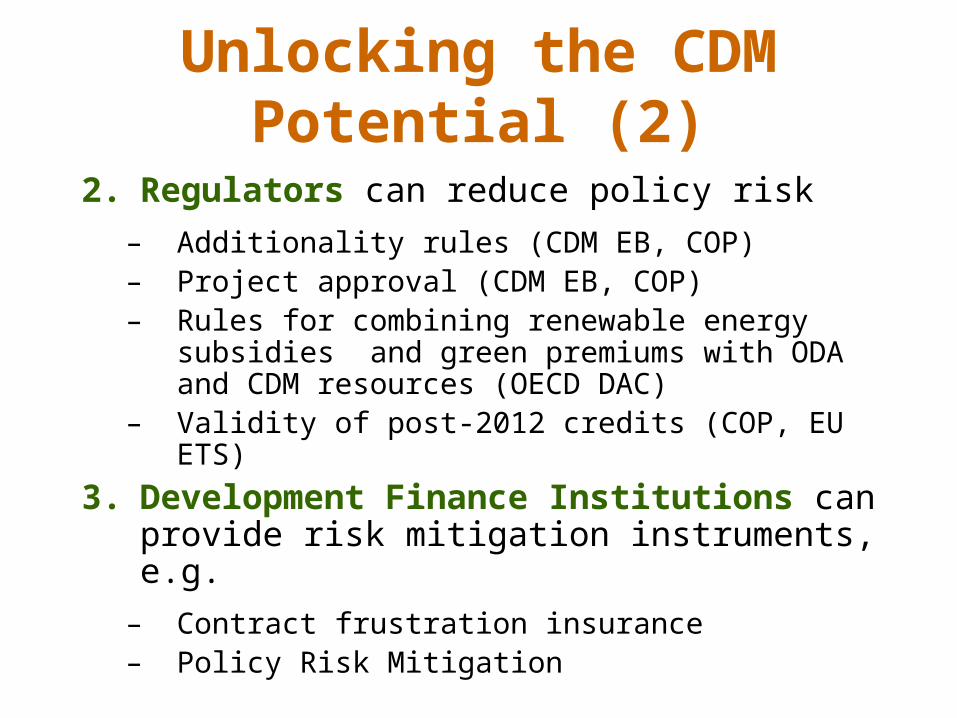

Unlocking the CDM Potential

To attract commercial financial institutions, we need

– Evidence of sizeable, profitable market– Acceptable Host Country investment climate– Adequate risk mitigation

Therefore, specific measures can increase leverage of carbon finance

1. Host Countries can improve investment climate for renewables

Unlocking the CDM Potential (2)

2. Regulators can reduce policy risk

– Additionality rules (CDM EB, COP)– Project approval (CDM EB, COP)– Rules for combining renewable energy subsidies

and green premiums with ODA and CDM resources (OECD DAC)

– Validity of post-2012 credits (COP, EU ETS)

3. Development Finance Institutions can provide risk mitigation instruments, e.g.

– Contract frustration insurance– Policy Risk Mitigation

To Sum Up

• CDM has benefits beyond the simple cash-flow associated with purchase of CERs

• For non-CO2 projects, cash-Flow + Additional benefits already make a huge difference

• For renewables, CDM is no silver bullet

– Cash-flow benefits are too thin at current prices– Indirect benefits can help some projects go

through, but under rather unique conditions

• But policy measures can unlock the potential of the CDM to foster clean power generation

www.carbonfinance.org

ANNEXES

Barriers to Power Generation Investment

• High upfront cost long payback period

• Long lead times high development costs

• Country risk (political unrest, etc.)

• Exchange rate risk

• Policy and regulatory risk

– Notably inadequate electricity tariffs & enforcement of tariff policy

• Individual buyers with poor credit ratings

• Poor revenue collection

Additional Barriers for Renewables

• Resource risk (intermittency)

• Technology efficacy risk (limited data)

• Small projects high transaction costs

• Less experienced sponsors with low credit rating scarce, expensive capital

high margin insurance short tenors

• Policy and regulatory risk

• Trend towards long-term PPAs

SPV

Host Country

Sponsor/ Project

Carbon Buyer

ERPA

Engagements, e.g.:• Regulation (e.g. tariffs)• Kyoto Protocol compliance

ERs

Letter of Approval

Other Structure: Subordinated Debt Finance

Senior Lenders Debt service (1st)

Loan

ER payment

Subordinated Lender(2nd)

(1st)

Debt service (2nd)Loan