cattle industry “situation and outlook ” tscra march, 2012

TRANSCRIPT

Cattle Industry“Situation and

Outlook ”TSCRA

March, 2012

2012 -967,000 Hd. (3%)2013F Flat

Slaughter Reductions2013 vs. 2011

•1.4 Million Non-Fed

•.8 Million Fed

•2.2 million Total

•8,500/day

•2- 4,000+/day packing plants

•1-4,000+/day and 4-1,000+/day packing plants

A Long-Term Chart…

Source: U.S. Dept of Census, various published research estimates

U.S. Dollar Index

The weak dollar has stimulated exports

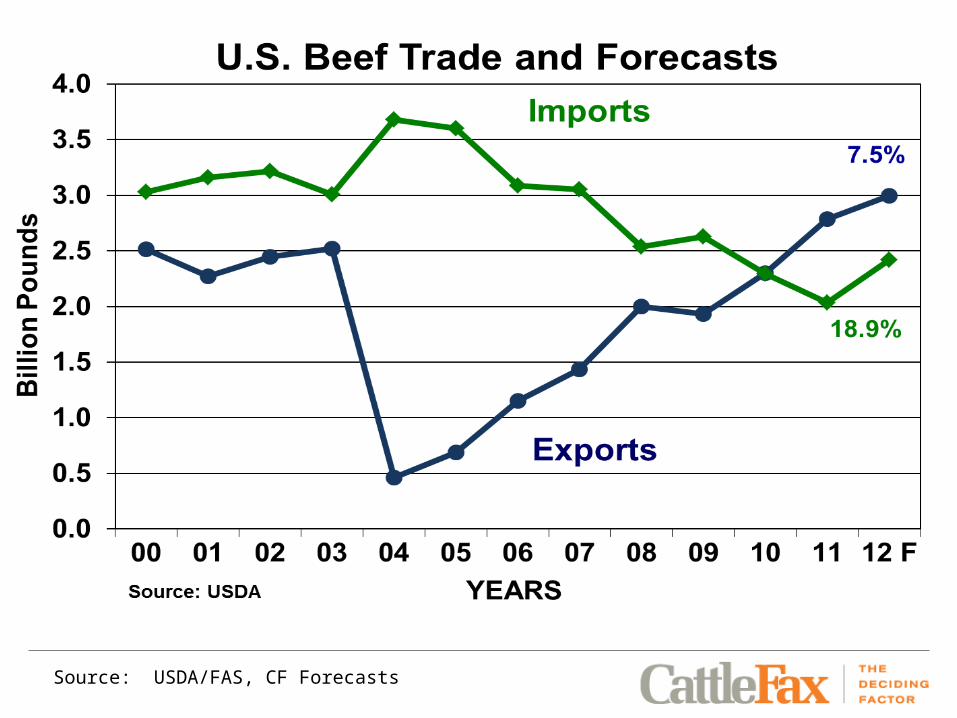

Source: USDA/FAS, CF Forecasts

The U.S. exports 18 percent of totalred meat and poultry production.

United States28%

Brazil22%EU-27

15%

Canada7%

Australia6%

Others22%

2011 Global Meat/Poultry ExportsTotal: 24 million metric tons (53.4 bil

lbs.) 15 billion pounds of U.S.beef, pork and poultrywere exported in 2011.

2.8 bil beef, 5.2 bil pork, 7 bil poultry

Demand

Retail- Higher prices will limit movement and featuring. Competition between proteins.

Food Service- Improvements noted in SSS. Fast food ,casual dinning, high end.

Exports- Slowing YOY gains, Low Dollar, Challenges with access.Imports- Increasing, High domestic prices vs. tighter Global supplies.

2012 Retail Protein Prices

Feb.Percent Change

vs. Year AgoChoice Beef $5.05 +9.2%

All-Fresh Beef $4.61 +6.1%

Ground Beef $2.95 +10.8%

Composite Pork $3.50 +6.5%

Composite Broiler $1.83 +2.9%Fresh Whole Chicken $1.36 +7.1%Boneless Breast $3.11 -2%

Whole Frozen Turkey $1.67 +9.5%Source: USDA and BLS

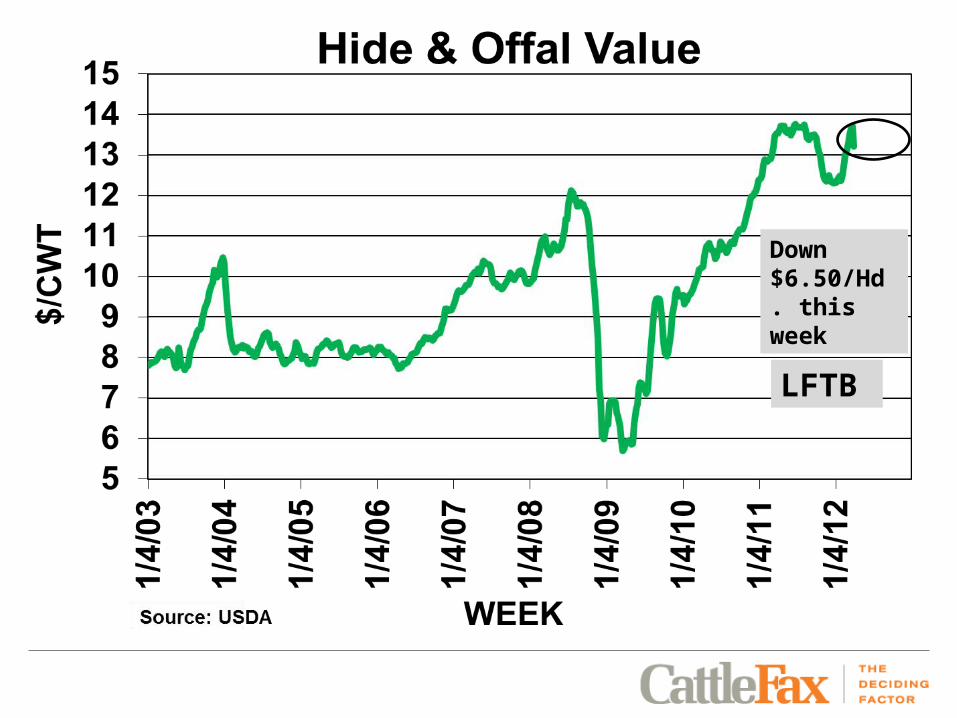

LFTB

1Q 2012 vs. 1Q 2011

2011 vs. 2010

2010 vs. 2006

90s Trimmings

+10% +18% +20%

Chuck +1% +20% +26%Round +.5% +19% +13%Rib +11% +11% +3%Loin +16% +11% -9%

Price Changes Beef

40

Down $6.50/Hd. this week

LFTB

Per Capita Net Beef Supply Demand Change vs. Prior Year

-5% -2% +0% +2% +5%58 $109.9

6$112.98 $114.99 $117.01 $120.03

57 $112.93

$115.96 $117.97 $119.99 $123.01

56 $115.91

$118.93 $120.95 $122.96 $125.99

55 $118.89

$121.91 $123.93 $125.94 $128.96

54 $121.89

$124.91 $126.93 $128.94 $131.96

53 $124.87

$127.89 $129.90 $131.92 $134.94

52 $127.82

$130.85 $132.86 $134.88 $137.90

51 $130.80

$133.83 $135.84 $137.86 $140.88

50 $133.78

$136.80 $138.82 $140.83 $143.86

2012 Fed Price projections based on Changes in Supply and Demand

Record high prices for all class’s of cattle

2012 Profitability

•Feedlot - Negative for the year. Risk management a must.

•Stocker/Backgrounder- Still Positive- But narrow margins are expected.

•Cow/Calf- Positive margins, record high calf values more than offset increasing input cost.

Markets work! The industry will expand.

More structural change on the way.

Global market access is crucial.

Production cost increases staggering, will moderate.

Record amount of volatility, risk, capital.

“Manage for a margin” don’t “guess markets”

Great time to be in Ag, but you must adapt to a global market environment.

SUMMARY

Thank You

Have a Profitable 2012