brazos community bank by kathrine beakley: senior vp for portfolio management by kathrine beakley:...

TRANSCRIPT

Brazos Community Bank

By Kathrine Beakley:

•Senior VP for Portfolio Management

Brazos Community Bank• Located in Navasota, TX

• Falls under the Dallas Federal Reserve

• Established in 1901 as an Agricultural Lender

Brazos Community Bank Today

• Personal Banking

• Business Banking

• Agricultural Banking

• e-Banking

Where Our Money Comes From

Our Loan Portfolio

Loan Decision Factors

By Katie Parrish:

VP for Credit

Loan Decision Factors

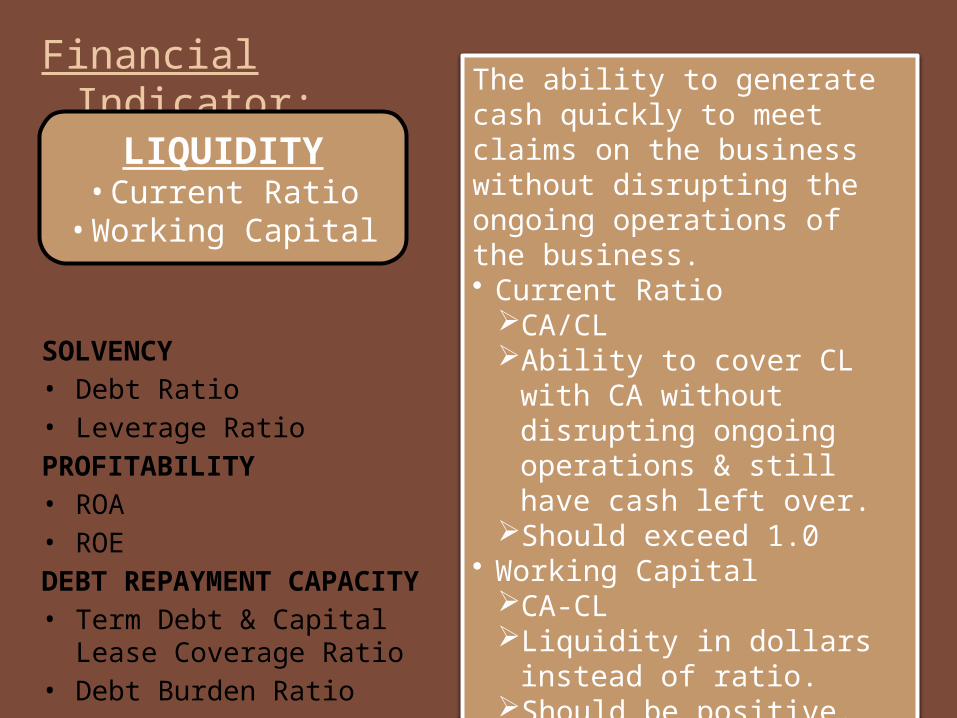

• Financial Indicators– Liquidity– Solvency– Profitability– Debt Repayment Capacity

• Credit Scoring

Financial Indicator:

SOLVENCY• Debt Ratio• Leverage RatioPROFITABILITY• ROA• ROEDEBT REPAYMENT

CAPACITY• Term Debt & Capital

Lease Coverage Ratio• Debt Burden Ratio

The ability to generate cash quickly to meet claims on the business without disrupting the ongoing operations of the business.• Current Ratio

CA/CLAbility to cover CL with

CA without disrupting ongoing operations & still have cash left over.

Should exceed 1.0• Working Capital

CA-CLLiquidity in dollars

instead of ratio.Should be positive.

LIQUIDITY• Current Ratio

• Working Capital

The ability of the firm to convert all its assets, retire all of its liabilities, and have cash left over.• Debt Ratio

Debt/AssetsAbility to liquidate

firm, cover all liabilities out of all assets, and have cash left over.

Should not exceed 0.5• Leverage Ratio

Debt/EquityOften used in loan

decisionsShould not exceed 1.0

Financial Indicator:LIQUIDITY• Current Ratio• Working Capital

PROFITABILITY• ROA• ROEDEBT REPAYMENT CAPACITY• Term Debt & Capital

Lease Coverage Ratio• Debt Burden Ratio

SOLVENCY• Debt Ratio• Leverage

Ratio

Financial Indicator:LIQUIDITY• Current Ratio• Working CapitalSOLVENCY• Debt Ratio• Leverage Ratio

DEBT REPAYMENT CAPACITY• Term Debt & Capital

Lease Coverage Ratio• Debt Burden Ratio

The ability of a firm to generate a level of revenue that exceeds its total costs of production• Return on Assets

NI/TAHow efficient

management is at using assets to generate earnings

Should be positive & high• Return on Equity

NI/EHow much profit company

makes with money from shareholders

Should be positive & high

PROFITABILITY• ROA• ROE

Financial Indicator:LIQUIDITY• Current Ratio• Working CapitalSOLVENCY• Debt Ratio• Leverage RatioPROFITABILITY• ROA• ROE

The ability of the firm to meet its scheduled term debt and capital lease payments and have cash left over.• Term Debt & Capital Lease

Coverage Ratio (EBIT-Taxes)/Term Debt

& Capital Lease Payments

Ability to cover term debt & capital lease payments due

Non-farm income often included

Should exceed 1.0• Debt Burden Ratio

Debt/NINumber of years to

retire debt based on net cash income

Should be low & falling

DEBT REPAYMENT CAPACITY

• Term Debt & Capital Lease

Coverage Ratio• Debt Burden Ratio

Financial Indicator Minimum General Desired Trend

LIQUIDITY•Current Ratio•Working Capital

•1.0•Positive

Increasing

SOLVENCY•Debt Ratio•Leverage Ratio

•<0.5•<1.0

Decreasing

PROFITABILITY•ROA•ROE

•Positive, high•Positive, high

Increasing

DEBT REPAYMENT CAPACITY•Term Debt & Capital Lease Coverage Ratio•Debt Burden Ratio

•>1.0•Low, Falling

Increasing

Credit Scoring•A number that shows us the risk we would be

taking by lending to potential borrower

•Shows histprical ability to repay loan

•Fast, objective way to justify loans

•Use FICO (Fair Isaac Company) scores

FICO Sources:Experian

TransUnionEquifax

Components of Credit Score

National Scores

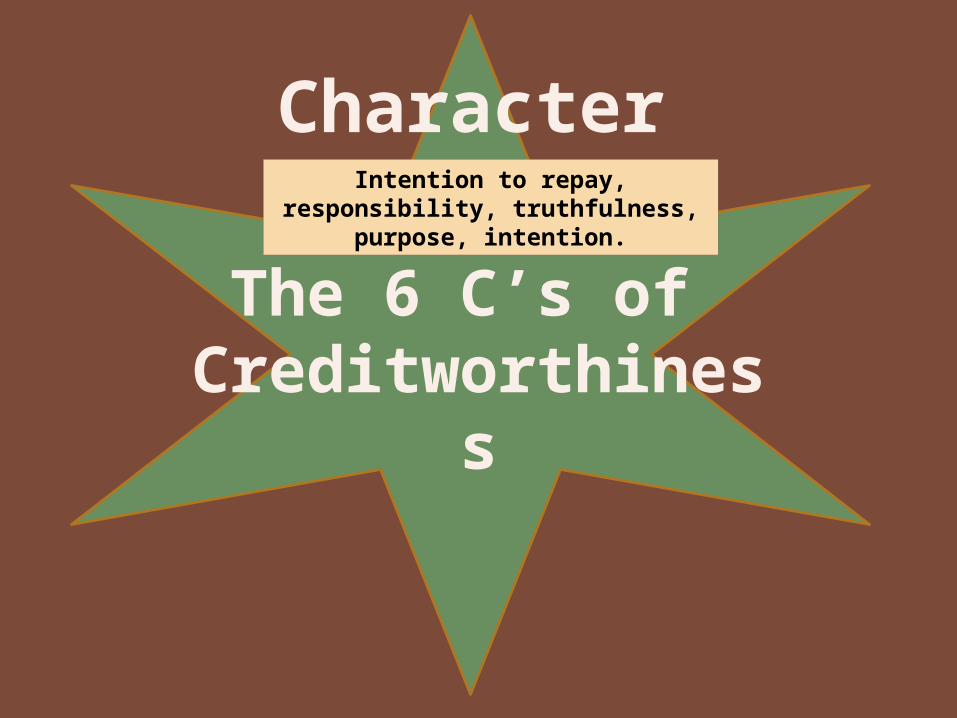

Character

The 6 C’s of Creditworthines

s

Intention to repay, responsibility, truthfulness,

purpose, intention.

The 6 C’s of Creditworthines

s

Character

CapacityLegal authority to sign contract.

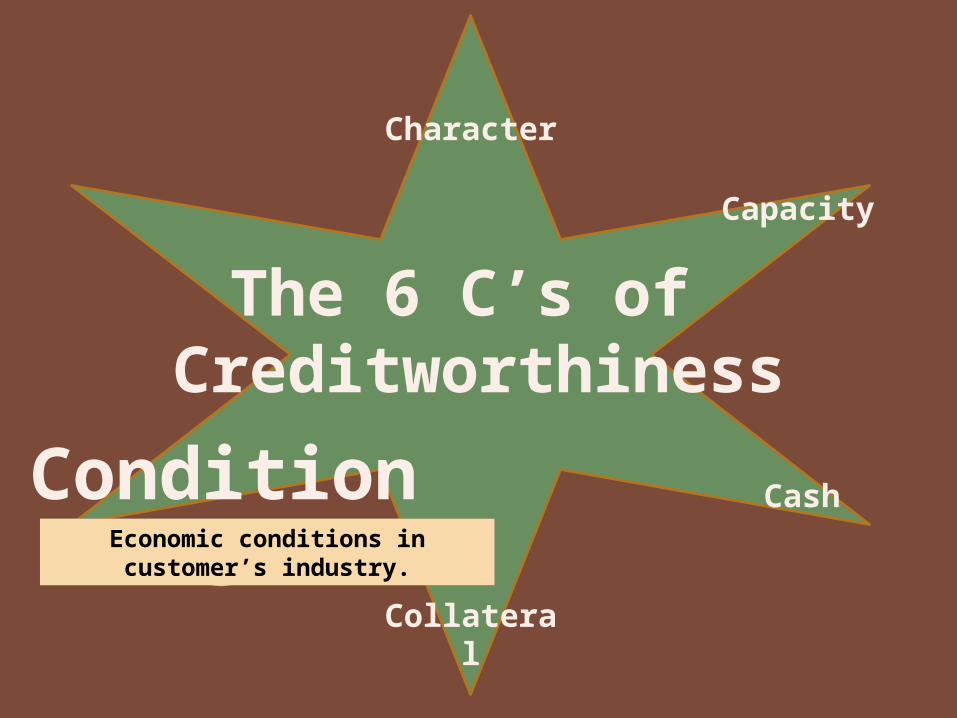

The 6 C’s of Creditworthiness

Character

Capacity

CashAbility to generate cash to

repay loan.

The 6 C’s of Creditworthiness

Character

Capacity

Cash

Collateral

Adequate net worth/assets to provide support for loan.

The 6 C’s of Creditworthiness

Character

Capacity

Cash

Collateral

ConditionsEconomic conditions in

customer’s industry.

The 6 C’s of Creditworthines

s

Character

Capacity

Cash

Collateral

Conditions

ControlWhether changes in the law would adversely affect the

customer.

Weight of Importance

•Since this is a large loan, we will consider credit score but place more emphasis on the financial indicators.

•Assuming satisfactory (above 725) credit score for Brad Roberson.

Market Analysis

By Ryan Allen:

VP for Operations & Marketing

Brazos County

• 84,000 head of cattle

• 52,000 beef cows

• Beef Cattle production is the top income producing agriculture

enterprise in county

Cattle Market

Cattle Market

• Main inputs are feed for cattle

• Pasture grazing, hay, and feed

derived from grains are most

common ways of feeding cattle

• Cattlemen are heavily dependent on

inputs

Feed Prices

• Corn is the most common grain feed used for cattle

• Range cubes used for cattle and creep pellets for calves

• Both of these are made partly of feed grains

• U.S. biofuel production has driven cost of corn up

• Corn prices expected to continue to rise unless the government intervenes

Corn Prices

Grazing and Hay

• Pasture grazing and hay usage heavily dependent on local rain fall

• Brazos county averages 39 inches of rainfall per year

• Limited pasture grazing in winter, must rely more on hay and grain feeds

Drought

• A drought causes major problems for cattle producers

• No grass for cattle in pasture grazing

• Due to a drought, hay becomes scarce and price goes up

• Hay may even have to be trucked in from out of state

Other Inputs

• Vaccinations and medication for cattle

• Fertilizer costs

• Fuel costs

• Labor

Overview of Risk

• Cattle prices dropping due to volatility of market

• Input costs increasing

• Animal health

• Weather related problems

Competition

Overview of Market Analysis

• Market is volatile, buy in winter

• Input costs are most likely to increase

• Having to compete with pork and chicken for smaller market share

• Buy Low Sell High

Costs and Returns

• Estimate bred heifer costs to be between $180,000 and $228,000 for

200 units

• Estimate bull costs to be between $6800 and $7400 for 5 2000 lbs bulls

• Estimate returns per calf cycle if calves raised to 500 lbs and no deaths

to be between $85,000 to $111,100

Evaluating Sleepy B Ranch

By Amanda Fort:

Member of the Board of Directors

Borrower Information:Sleepy B Ranch

President/CEO/Owner:Brad Roberson

Sleepy B Ranch

Background Information:• Location: Brazos County

• Operation: Cow-Calf• Total Acreage Currently Owned: 1,000

acres• Has been in operation for 5 years

• Cattle contracted from stocker operation in Amarillo, Texas

About the Requested Loan

• Type: Small Business Loan•Amount Requested: $135, 520

•Use: Wants to buy 5 bulls & 200 bred heifers

Financial & Shock Analysis

By Bradley Schmidt & Courtney Buerger:

Co-VPs for Research & Credit Analysis

Baseline-Liquidity

0.001.002.003.004.005.006.007.00

2008 2009 2010 2011 2012

Current Ratio

Baseline

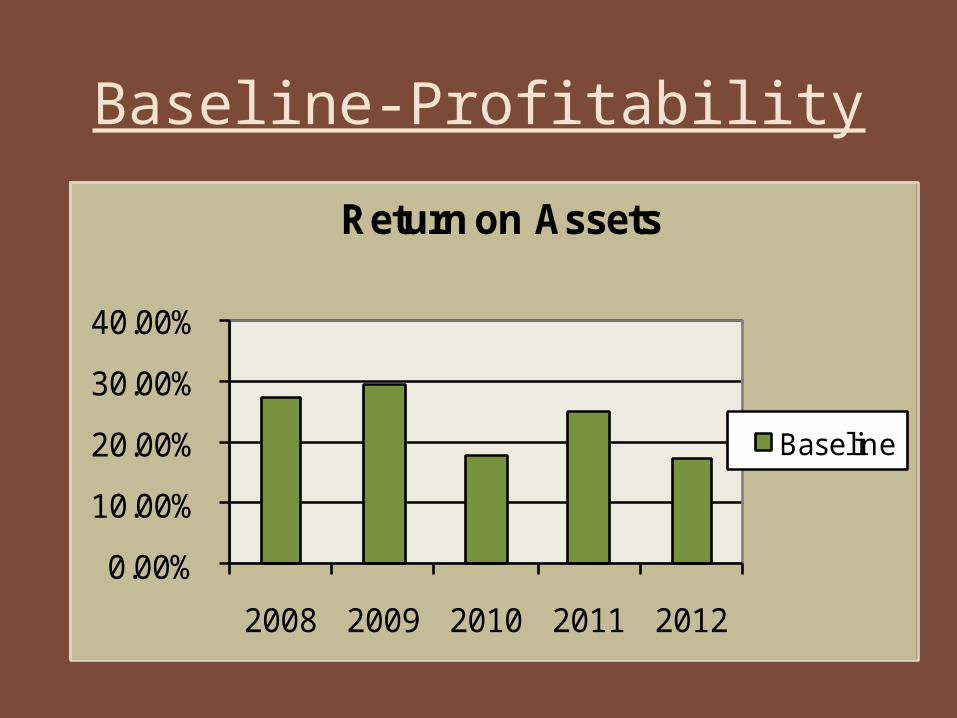

Baseline-Profitability

0.00%

10.00%

20.00%

30.00%

40.00%

2008 2009 2010 2011 2012

Return on Assets

Baseline

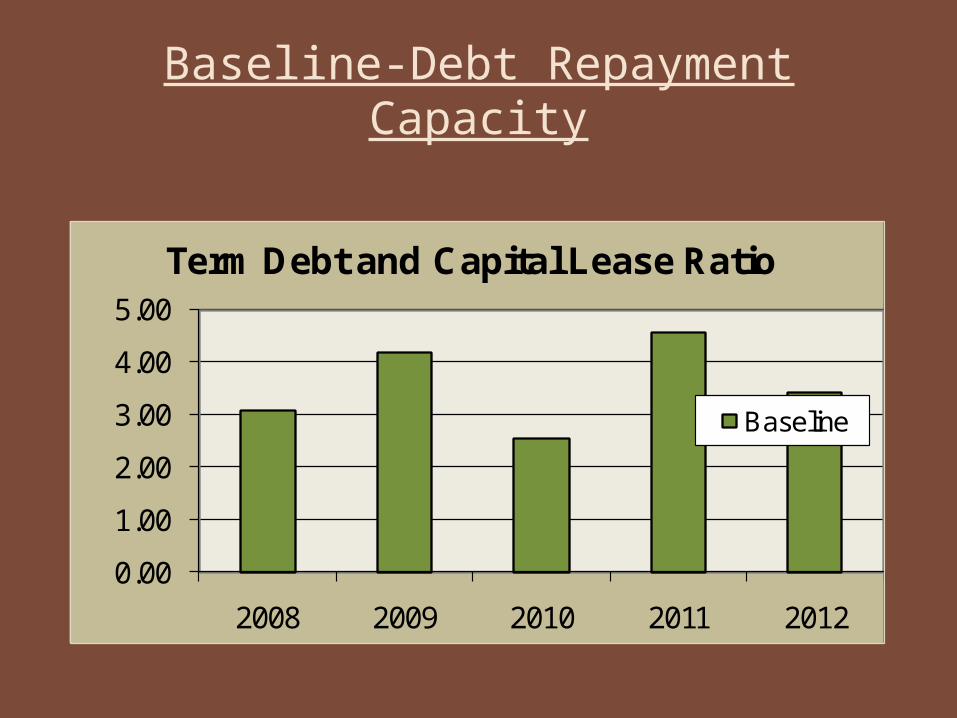

Baseline-Debt Repayment Capacity

0.00

1.00

2.00

3.00

4.00

5.00

2008 2009 2010 2011 2012

Term Debt and Capital Lease Ratio

Baseline

Baseline-Efficiency

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

2008 2009 2010 2011 2012

Variable Expense Ratio

Baseline

---------Baseline Scenario----------2008 2009 2010 2011 2012

2.57% 2.57% 2.57% 2.57% 2.57%5.00% 5.00% 5.00% 5.00% 5.00%1.50% 1.50% 1.50% 1.50% 1.50%9.07% 9.07% 9.07% 9.07% 9.07%

0.91684 0.84060 0.77070 0.70661 0.64785

$48,070 $72,042 $41,664 $83,890 $63,086$4,967 $4,967 $4,967 $4,967 $4,967

$53,036 $77,008 $46,631 $88,856 $68,053

$130,800

$48,626 $64,733 $35,938 $62,787 $128,827

$169,400

$171,511

Required rate of return:1. Risk free rate of return2. Business risk premium3. Financial risk premium4. Required rate of return

5. Present value interest factor:

Expected net cash flow:1. Net income2. Depreciation3. Total net cash flow Terminal value

Present value of net cash flows

Total capital purchased

Net present value

Baseline – NPV

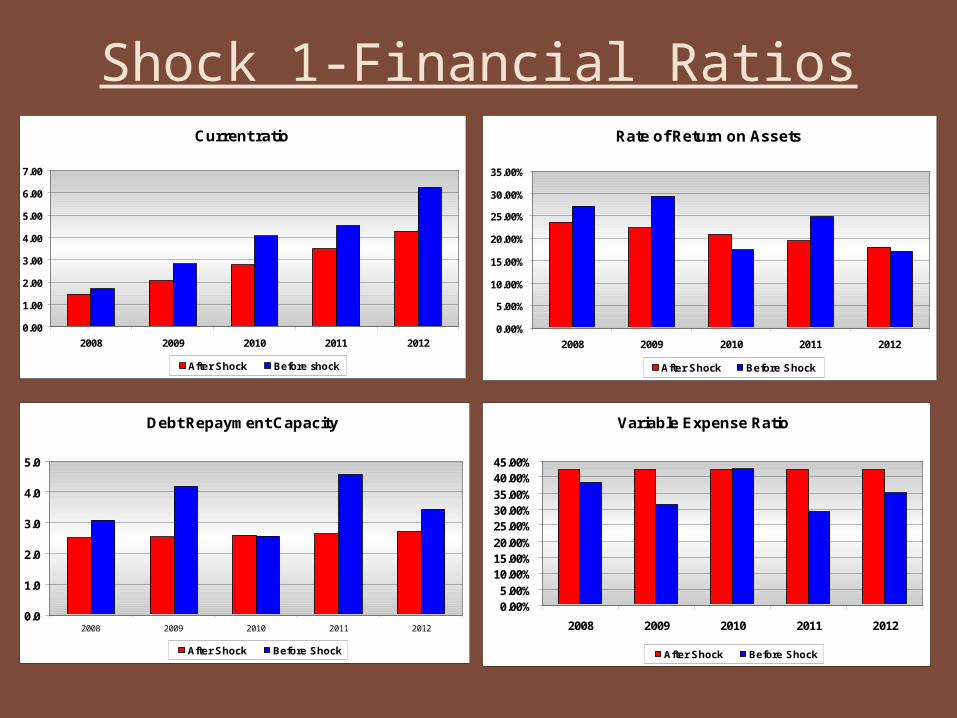

Shock 1-Expected

Lowered 1st year price by $9 per cwt

Increased sales prices by 3% per year

Lowered expected calf crop from 90% to 85%

Increased direct materials expense by 3% per year

Shock 1-Financial RatiosCurrent ratio

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

2008 2009 2010 2011 2012

After Shock Before shock

Rate of Return on Assets

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

2008 2009 2010 2011 2012

After Shock Before Shock

Debt Repayment Capacity

0.0

1.0

2.0

3.0

4.0

5.0

2008 2009 2010 2011 2012

After Shock Before Shock

Variable Expense Ratio

0.00%5.00%

10.00%15.00%20.00%

25.00%30.00%35.00%

40.00%45.00%

2008 2009 2010 2011 2012

After Shock Before Shock

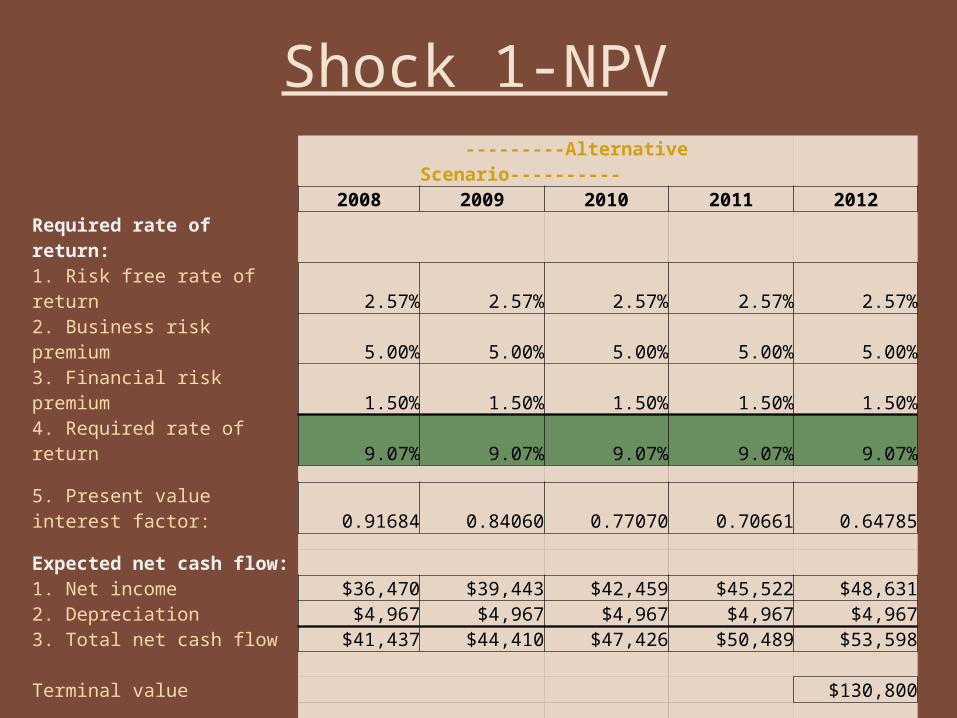

---------Alternative Scenario----------2008 2009 2010 2011 2012

Required rate of return:1. Risk free rate of return 2.57% 2.57% 2.57% 2.57% 2.57%2. Business risk premium 5.00% 5.00% 5.00% 5.00% 5.00%3. Financial risk premium 1.50% 1.50% 1.50% 1.50% 1.50%4. Required rate of return 9.07% 9.07% 9.07% 9.07% 9.07%

5. Present value interest factor: 0.91684 0.84060 0.77070 0.70661 0.64785

Expected net cash flow:1. Net income $36,470 $39,443 $42,459 $45,522 $48,6312. Depreciation $4,967 $4,967 $4,967 $4,967 $4,9673. Total net cash flow $41,437 $44,410 $47,426 $50,489 $53,598 Terminal value $130,800

Present value of net cash flows $37,991 $37,331 $36,551 $35,676 $119,462

Total capital purchased $169,400

Net present value $97,611

Shock 1-NPV

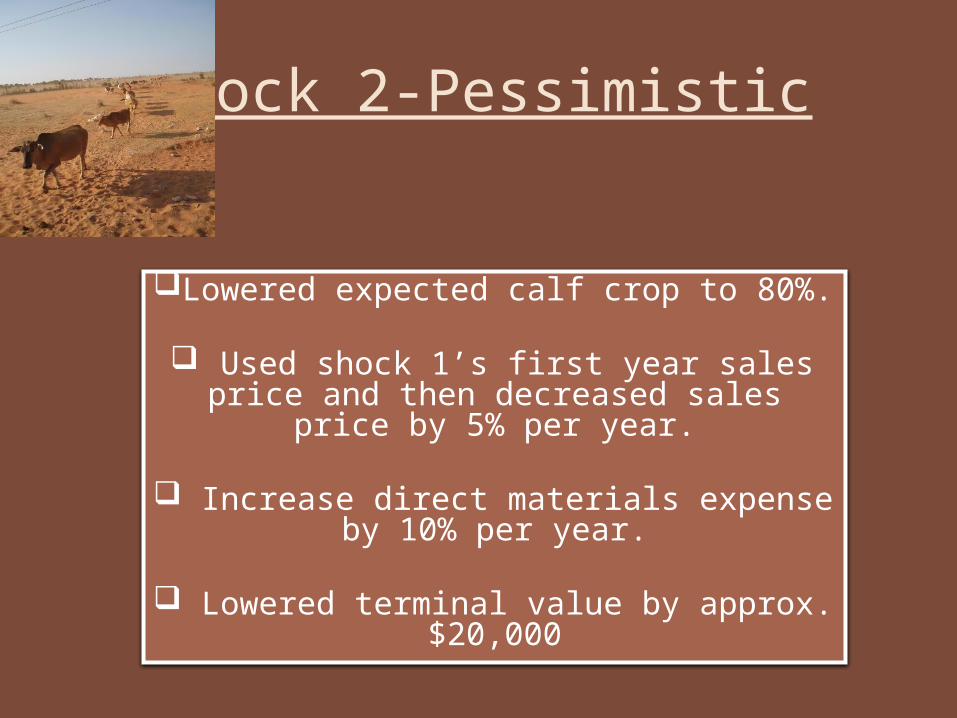

Shock 2-Pessimistic

Lowered expected calf crop to 80%.

Used shock 1’s first year sales price and then decreased sales price by 5% per year.

Increase direct materials expense by 10% per year.

Lowered terminal value by approx. $20,000

Shock 2 – Financial RatiosCurrent ratio

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

2008 2009 2010 2011 2012

After Shock Before shock

Rate of Return on Assets

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

2008 2009 2010 2011 2012

After Shock Before Shock

Debt Repayment Capacity

0.0

1.0

2.0

3.0

4.0

5.0

2008 2009 2010 2011 2012

After Shock Before Shock

Variable Expense Ratio

0.00%10.00%

20.00%30.00%40.00%

50.00%60.00%70.00%

80.00%90.00%

2008 2009 2010 2011 2012

After Shock Before Shock

Shock 2 – NPV ---------Alternative Scenario----------

2008 2009 2010 2011 2012

Required rate of return:1. Risk free rate of return 2.57% 2.57% 2.57% 2.57% 2.57%2. Business risk premium 5.00% 5.00% 5.00% 5.00% 5.00%3. Financial risk premium 1.50% 1.50% 1.50% 1.50% 1.50%4. Required rate of return 9.07% 9.07% 9.07% 9.07% 9.07%

5. Present value interest factor: 0.91684 0.84060 0.77070 0.70661 0.64785

Expected net cash flow:1. Net income $33,643 $27,479 $21,161 $14,645 $7,8822. Depreciation $4,967 $4,967 $4,967 $4,967 $4,9673. Total net cash flow $38,610 $32,446 $26,128 $19,612 $12,848 Terminal value $111,100

Present value of net cash flows $35,399 $27,274 $20,136 $13,858 $80,300

Total capital purchased $169,400

Net present value $7,567

Shock 3 – Very Pessimistic

Lowered expected calf crop to 80%.

Used shock 1’s first year sales price and then decreased sales price by 10% per year.

Increase direct materials expense by 10% per year.

Lowered terminal value by approx. $20,000

Shock 3 – Financial RatiosCurrent ratio

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

2008 2009 2010 2011 2012

After Shock Before shock

Rate of Return on Assets

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

2008 2009 2010 2011 2012

After Shock Before Shock

Debt Repayment Capacity

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

2008 2009 2010 2011 2012

After Shock Before Shock

Variable Expense Ratio

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

2008 2009 2010 2011 2012

After Shock Before Shock

Shock 3 - NPV ---------Alternative Scenario----------

2008 2009 2010 2011 2012

Required rate of return:1. Risk free rate of return 2.57% 2.57% 2.57% 2.57% 2.57%2. Business risk premium 5.00% 5.00% 5.00% 5.00% 5.00%3. Financial risk premium 1.50% 1.50% 1.50% 1.50% 1.50%4. Required rate of return 9.07% 9.07% 9.07% 9.07% 9.07%

5. Present value interest factor: 0.91684 0.84060 0.77070 0.70661 0.64785

Expected net cash flow:1. Net income $33,643 $23,383 $13,585 $4,131 -$6,7892. Depreciation $4,967 $4,967 $4,967 $4,967 $4,9673. Total net cash flow $38,610 $28,350 $18,552 $9,097 -$1,822 Terminal value $111,100

Present value of net cash flows $35,399 $23,831 $14,298 $6,428 $70,796

Total capital purchased $169,400

Net present value -$18,648

Conclusion & Decision

By Courtney Buerger:

Co-VP for Research & Credit Analysis

Financial Indicator Our Credit Standard

Ratios

Baseline AverageRatios

Expected Averaged

Ratios

LIQUIDITY•Current Ratio•Working Capital

•1.25•Positive

•3.88•$119,066

•2.82•$63,326

SOLVENCY•Debt Ratio•Leverage Ratio

•<0.5•<1.0

•.40•.84

•.45•1.04 but decreasing

PROFITABILITY•ROA•ROE

•Positive, high•Positive, high

•23.24%•37.59%

•20.88%•34.72%

DEBT REPAYMENT CAPACITY•Term Debt & Capital Lease Coverage Ratio•Debt Burden Ratio

•>1.25•Low, Falling

•3.57•2.03

•2.6•2.67

YearBeginning Principal

Principal Payment

Interest Payment

Total Payment

Ending Principal

1 $135,520 $22,198 $13,552 $35,750 $113,322

2 $113,322 $24,418 $11,332 $35,750 $88,905

3 $88,905 $26,859 $8,890 $35,750 $62,045

4 $62,045 $29,545 $6,205 $35,750 $32,500

5 $32,500 $32,500 $3,250 $35,750 $0

nominal totals $135,520 $43,229 $178,749

Amortization Table

Conclusion

•Borrower’s original baseline numbers are on the optimistic side and

fluctuate greatly, but the adjusted numbers are strong enough to justify

the loan

•Cattle markets are volatile, cyclical, and have high input risks

•Outside income of $60,000 will compensate for risks

•We have decided to grant the $135,520 loan for 5 years at a 10%

fixed interest rate

•Land will be used as collateral