beneficial owner data collection flow chart

TRANSCRIPT

Beneficial Ownership Flow Chart Intellectual Property of IBA © Rev. 4/1/19

BENEFICIAL OWNER DATA COLLECTION FLOW CHART

1 FIN-2018-G001 issued 4/3/18; Question #7. 2 Five years after account closure for identifying information (i.e. name, address, DOB, identification number); five years after receipt for validation documents (e.g. driver’s license, passport, etc.); FIN-2018-G001; Question #9. 3 CD defined as having specific maturity date, cannot be withdrawn before that date without incurring penalty, no new funds added. FIN-2018-R004 issued 9/7/18. 4 May renew, modify or extend without substantively changing the terms or requiring additional underwriting. FIN-2018-R004. 5 Revolving loan (allows customer to pay down and redraw funds up to designated line amount). May change certain terms of commercial LOC/credit card (such as credit limit), without requiring additional underwriting. FIN-2018-R004. 6 Renewal of contract with minimal or no communication with customer other than payment of rental fee. FIN-2018-R004. 7 FIN-2018-G001 and FIN-2018-R004.

Legal Entity Customer (LEC)

“New” Account Opened

Legal Entity Customer (LEC)

Account Renewed/Rolled

Over

Beneficial Owner(s)

(BOs) not existing

customer(s)

Beneficial Owner(s) are

existing customer(s) (i.e.

Bank has performed CIP) -

Follow either path below

based on bank policy

Collect Name, Address,

DOB and Identification

Number and Validate

Info

If accurate and up-to-

date, have

BO/authorized

individual re-certify

its accuracy

If not accurate and

up-to-date, obtain

updated info and

validate with

acceptable ID

If CD product3, no

new money added;

OR

If qualifying loan

renewal,

modification,

extension;4 OR

Have

BO/Authorized

individual certify its

accuracy

Retain original and

re-certified info per

rule2

Retain original and

updated info per

rule2

If qualifying

commercial

LOC/credit card

renewal,

modification,

extension;5 OR

Renewal of Safe

Deposit Box

Contract6

Renewal/rollover

not meeting CD3,

loan4, LOC5, safe

deposit box6

definition

Not considered

“new account”

(i.e. No

requirement to

obtain BO

information)

Collect Name,

Address, DOB and

Identification

Number and

Validate Info

Retain original

(if applicable)

and re-

certified info

per rule2

Retain

original info

per rule2

Have

BO/authorized

individual

certify to its

accuracy

Review existing

identifying

information1

Have

BO/Authorized

individual certify

its accuracy

This tool explains the Data Collection Beneficial Ownership requirements only as permitted under the rule in 31 CFR 1010.230 and related FAQs.7 Bank should follow its policies and procedures regarding data collection, validation, certification, documentation, address discrepancies, OFAC, etc.

Reg. E Error Resolution Flow Chart

March 2, 2018

Customer reports

EFT error

The 10/45/90 day rules do not apply. However, Bank must

investigate and give credit to the customer for any unauthorized

transactions that occurred within 60 calendar days of the financial

institution's transmittal of the periodic statement on which the error

first appeared. See Reg. E Consumer Liability Guide

Was the error reported within 60

calendar days of the financial

institution's transmittal of the

periodic statement?

NO

Did an error occur?

YES

NO

Was error

reported orally?

1. Provisionally credit account within 10 business

days** of receipt of notice of error unless

exception above applies.

2. Notify the customer either orally or in writing of

the provisional credit within 2 business days of

providing unless exception above applies.

YES

FINISHED

Error resolved within 10

business days?

Bank now

has up to 45

calendar days

*** to

investigate

and resolve.

*Exception: If Bank does not receive the

written notice of error within 10 business

days, it does not have to provide

provisional credit if the investigation takes

longer than 10 days. However, it must still

investigate the error and make correction,

if applicable.

Bank must provide written explanation within 3 business days after

concluding investigation. The notification must inform the

customer that they have the right to see the bank’s documentation.

Investigate Error

FINISHED

YES

NO

Bank must:

1. Make correction within 1

business day after determining an

error occurred.

2. Within 3 business days, notify the

customer either orally or in

writing the results of the

investigation. Inform the

customer that provisional credit is

final.

Was provisional credit given?

Bank must:

1. Notify the customer of the date and amount debited

from their account.

2. Notify the customer that the Bank will honor

transaction against the account for 5 business days

after the notification. (Bank need only pay those items

that would have been paid if it had not debited the

account. Bank also cannot charge any overdraft fees

should an OD occur.)

3. Notify the customer that he/she has the right to request

copies of the documentation used in the error

resolution.

NO

YES

Was error reported in writing?

FINISHED **If disclosed, can extend to 20 business days for new

accounts.

***If disclosed, can extend to 90 calendar days for

POS or foreign initiated transactions or new accounts.

Does Bank require written

notice of error? (Bank can

require notice in writing

within 10 business days if

requested at the time

customer reports the error.)

Intellectual Property of the IBA - All Rights Reserved.

Regulation E Consumer Liability Guide1

12 CFR 1005.6

01.27.16

Trigger If consumer notifies2 financial institution…

Then the consumer’s maximum liability is…

Loss or theft of access device3

Within 2 business days after learning of loss or theft (timely notice)

Lesser of $50 or total amount of unauthorized transfers

More than 2 business days after learning of loss or theft (timely notice NOT given)

Lesser of $500 or the sum of:

$50 or total amount of unauthorized transfers occurring before learning of the loss and during the first two business days after learning of the loss, whichever is less, plus

The amount of unauthorized transfers occurring after the two business days and before notice to the financial institution.

More than 60 calendar days after the first periodic statement is sent to the consumer detailing the first unauthorized transfer using the access device (timely notice NOT given)

For transfers occurring on the first statement where the unauthorized transaction occurred and within the 60-day period4, the lesser of $500 or the sum of:

The lesser of $50 or the amount of unauthorized transfers before learning of the loss and during the first two business days after learning of the loss, whichever is less, and

The amount of unauthorized transfers occurring after two business days during the 60-day period,

PLUS, the amount of ALL unauthorized transfers occurring after the 60-day period4 until the financial institution is notified.

Unauthorized transfer(s) appearing on the periodic statement (no use of access device)

Within 60 calendar days after sending the periodic statement on which the unauthorized transfer first appears (time notice given)

No liability

More than 60 calendar days after sending the periodic statement on which the unauthorized transfer first appears

No liability for unauthorized transactions in first 60 calendar days after statement. Unlimited liability for all unauthorized transfers occurring more than 60 calendar days after the first period statement on which unauthorized transfers occurred and before notice to the institution.

1 This guide only reflects Regulation E error resolution timeframes and liability and does not take into consideration MasterCard, VISA or NACHA liability provisions.

2 Notice is given when consumer takes reasonable steps necessary to provide financial institution with pertinent information. Customer may notify institution in person, by telephone, or

in writing. If in writing, notice is given at time customer mails the notice or transmits it to the institution. 3 Includes debit cards, personal identification numbers (PINs), telephone transfer and telephone bill payment codes, and other means that may be used by a consumer to initiate an

electronic funds transfer (EFT) to or from a consumer account. 4 The “60-day period” starts the day the first periodic statement was sent to the consumer detailing the first unauthorized transfer using the access device.

Iowa Bankers Association Intellectual Property – All Rights Reserved 8/7/17

Raffles, Lotteries, Promotional Games

Contest Definition Allowable? Requirements

Lotteries/Raffles Offer of a prize

Distribution of prize by chance – random selection

Giving something of value (“consideration”) in exchange for chance to win such as purchase ticket, opening account, obtaining a loan (legal consideration)

Not all that enter will win

No – Section 20 of the FDIA prohibits banks from conducting or participating in lotteries Bank may display items subject to raffle

Prohibited Activity:

Making, taking, buying, selling, redeeming tickets

Advertising lottery

Announcing, advertising or publicizing participant/winner

Allowing sale of tickets on premises

Determining prize winner

Promotional Games of Chance

Offer of a prize

Distribution of prize by chance

No requirement of payment or thing of value to enter (no “consideration”)

Open to customers and non-customers

Yes – allowable under Iowa code chapter 714B and Iowa Administrative Code 61-32.1(b)(1)

Clearly disclose no purchase, payment, donation, account required to win

Make entry forms available to non-customers (lobby, newspaper or online)

Ensure customers don’t have significantly better chance of winning

Advertisements include odds of winning (may be dependent on number of entries)

State prize is subject to 1099-MISC reporting if FMV of $600 or more

No limitation on value of prize as long as not given in relation to amount of any deposit or length of time a deposit remains at bank

Prizes must be delivered to winner within 30 days of drawing.

For more detail, see Iowa Banking Guide Article at

https://www.iowabankers.com/userdocs/IBAPrivate/Raffles,_Lotteries,_Promotional_Games_and_Prize_Drawings.doc

Questions: Contact primary regulator or Iowa’s Department of Inspections and Appeals, Gaming Division. 515-281-6848 or www.state.ia.us/government/dia

Reg. E Error Notices© Page 1 of 2 April 2014

Sample Notices – Reg. E Error Resolution

Notice – Provisional Credit (Must be provided to consumer within two business days after provisional crediting.)

Date

Customer Name Address City, State, ZIP

Re: Electronic Fund Transfer Investigation Account #

Dear: [Bank Name] has received your notice of possible Electronic Fund Transfer (EFT) error to your account. We have begun our investigation and have today provisionally credited your account with $--, the amount you identified as a possible error [or: the amount you identified as a possible error, less your maximum liability of $50]. This information is available for your use while we conduct our investigation.

Once our investigation is complete, we will notify you of the final resolution. In the interim you may contact [Bank or designated employee] at [phone] should you have questions.

Sincerely,

Name/title

Notice – Final Resolution – Error Occurred (Must be provided to consumer within three business days after completing investigation.)

Date

Customer Name Address City, State, ZIP

Re: Electronic Fund Transfer Investigation Account #

Dear: In response to your notice of possible Electronic Fund Transfer (EFT) error to your account, we have investigated the transaction you identified as erroneous and have determined the transaction was in fact in error.

Provisional credit in the amount of $-- was deposited to your account on [date]. Please be advised this provisional credit has been made final.

Should you have any questions about our investigation of your notice of error, please contact [Bank or designated employee] at [phone].

Sincerely,

Name, Title

Reg. E Error Notices© Page 2 of 2 April 2014

Sample Notices – Reg. E Error Resolution

Notice – No Error or Different Error Occurred (Must be provided to consumer within three business days after completing investigation.)

Date

Customer Name Address City, State, ZIP

Re: Electronic Fund Transfer Investigation Account #

Dear: In response to your notice of possible Electronic Fund Transfer (EFT) error to your account, we have investigated the transaction you identified as erroneous and have determined the transaction was not in error. Our investigation concluded [describe records obtained by bank that prove the transaction was conducted by the consumer, authorized by the consumer, or was in an amount different that as described by the consumer]. You have a right to request copies of the documents we relied upon in making our determination. If you would like copies of these documents, please contact [Bank or designated employee] at [phone].

Today, we debited (removed the funds from) your account in the amount of $--, reversing the provisional credit deposited to your account on [date]. If this reversal results in a negative/overdrawn balance, we will not charge our standard overdraft fee. We will honor all checks, drafts or similar payments to third parties and preauthorized transfers from your account to the extent of the reversal of provisional credit, for five business days from today’s date. There will be no overdraft or insufficient check charge to your account during this five business day timeframe as a result of any overdraft or insufficient funds, to the extent that the item would have been paid if the provisional credit had not been reversed.

Should you have any questions about our investigation, please contact [Bank or designated employee] at [phone].

Sincerely,

Name, Title

Reg. E Error Resolution Worksheet © Revised 10/2019

Regulation E – Error Resolution Worksheet

** Attach copies of all supporting documentation to this form and retain for 2 years.

Customer Name: Account #: Date customer notified bank of error: If notification was provided orally, date of written notification (if applicable): Date of error: / / Description of error: Provisional credit provided? Y N If yes, date account is credited: Date customer notified of provisional credit: Method of notification: (Consumer must be notified of the credit within two days of the provision) Date of final resolution: Description of resolution: (If it has been determined that an error occurred, it must be corrected within one business day after determination and the results of the investigation reported to the consumer within three business days. The consumer must be informed whether or not any provisional credit is final) Date customer notified of resolution: Method of notification: Oral___ Written___ Other _____________________________________ (Notification required no matter the outcome of investigation. If it has been determined that an error did not occur, written explanation of the bank’s findings is required.) If no error was discovered, date provisional credit was debited: (The bank may debit the account and send a letter to the consumer advising of the date and amount of the debit and must honor overdrafts for five business days after the date of debit. Only those items that would have cleared had the account not been debited need to be honored. Conversely, the bank may send a letter notifying the consumer that the account will be debited five days from the date of the mailing. If this option is used, the letter must tell the consumer the actual date the debit will occur.)

Employee: _________________________________________________ Date: _______________

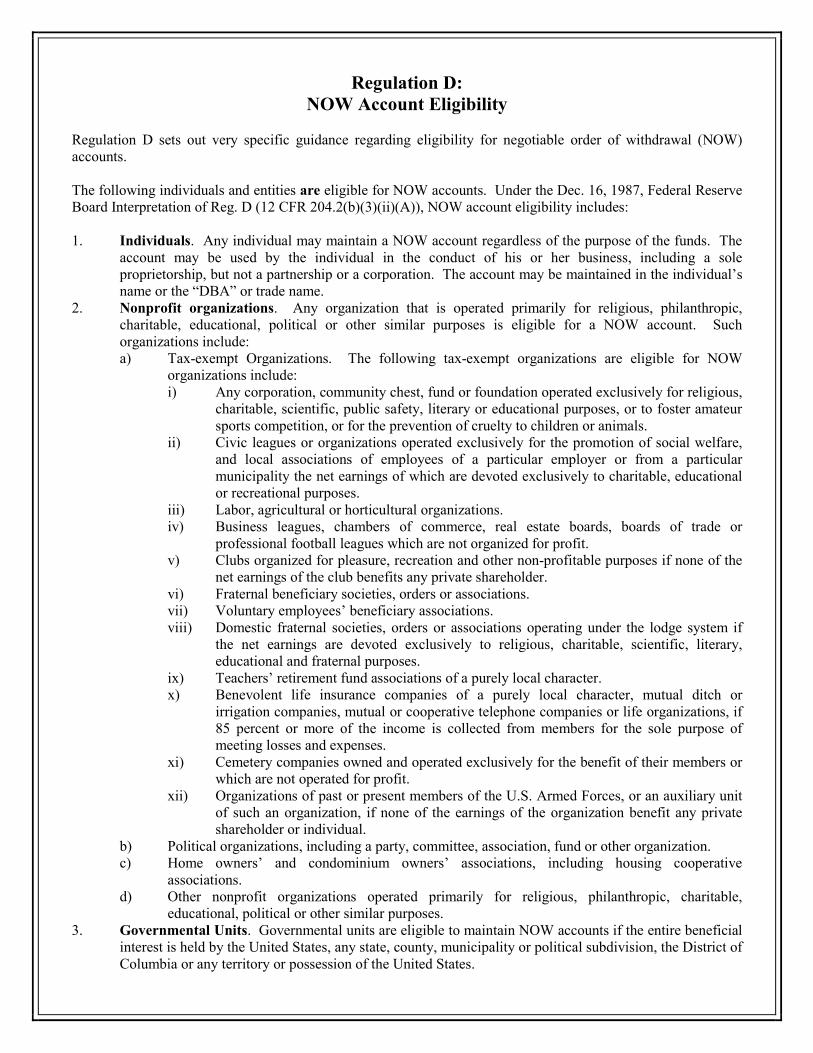

Regulation D: NOW Account Eligibility

Regulation D sets out very specific guidance regarding eligibility for negotiable order of withdrawal (NOW) accounts. The following individuals and entities are eligible for NOW accounts. Under the Dec. 16, 1987, Federal Reserve Board Interpretation of Reg. D (12 CFR 204.2(b)(3)(ii)(A)), NOW account eligibility includes: 1. Individuals. Any individual may maintain a NOW account regardless of the purpose of the funds. The

account may be used by the individual in the conduct of his or her business, including a sole proprietorship, but not a partnership or a corporation. The account may be maintained in the individual’s name or the “DBA” or trade name.

2. Nonprofit organizations. Any organization that is operated primarily for religious, philanthropic, charitable, educational, political or other similar purposes is eligible for a NOW account. Such organizations include: a) Tax-exempt Organizations. The following tax-exempt organizations are eligible for NOW

organizations include: i) Any corporation, community chest, fund or foundation operated exclusively for religious,

charitable, scientific, public safety, literary or educational purposes, or to foster amateur sports competition, or for the prevention of cruelty to children or animals.

ii) Civic leagues or organizations operated exclusively for the promotion of social welfare, and local associations of employees of a particular employer or from a particular municipality the net earnings of which are devoted exclusively to charitable, educational or recreational purposes.

iii) Labor, agricultural or horticultural organizations. iv) Business leagues, chambers of commerce, real estate boards, boards of trade or

professional football leagues which are not organized for profit. v) Clubs organized for pleasure, recreation and other non-profitable purposes if none of the

net earnings of the club benefits any private shareholder. vi) Fraternal beneficiary societies, orders or associations. vii) Voluntary employees’ beneficiary associations. viii) Domestic fraternal societies, orders or associations operating under the lodge system if

the net earnings are devoted exclusively to religious, charitable, scientific, literary, educational and fraternal purposes.

ix) Teachers’ retirement fund associations of a purely local character. x) Benevolent life insurance companies of a purely local character, mutual ditch or

irrigation companies, mutual or cooperative telephone companies or life organizations, if 85 percent or more of the income is collected from members for the sole purpose of meeting losses and expenses.

xi) Cemetery companies owned and operated exclusively for the benefit of their members or which are not operated for profit.

xii) Organizations of past or present members of the U.S. Armed Forces, or an auxiliary unit of such an organization, if none of the earnings of the organization benefit any private shareholder or individual.

b) Political organizations, including a party, committee, association, fund or other organization. c) Home owners’ and condominium owners’ associations, including housing cooperative

associations. d) Other nonprofit organizations operated primarily for religious, philanthropic, charitable,

educational, political or other similar purposes. 3. Governmental Units. Governmental units are eligible to maintain NOW accounts if the entire beneficial

interest is held by the United States, any state, county, municipality or political subdivision, the District of Columbia or any territory or possession of the United States.

4. Pension Funds, etc. Pension funds, escrow accounts, security deposits and other funds may be classified as NOW accounts if the entire beneficial interest is held by individuals or other entities eligible to maintain NOW accounts directly.

5. Fiduciaries. Funds held in a fiduciary capacity (either by an individual fiduciary or by a corporate fiduciary such as a bank trust department or a trustee in bankruptcy) may be held in NOW accounts if all the beneficiaries are otherwise eligible to maintain NOW accounts.

6. Grandfather Provision. NOW accounts established on or before Aug. 31, 1981, that represent funds of an ineligible entity that previously was eligible to maintain a NOW account may continue to maintain such NOW account.

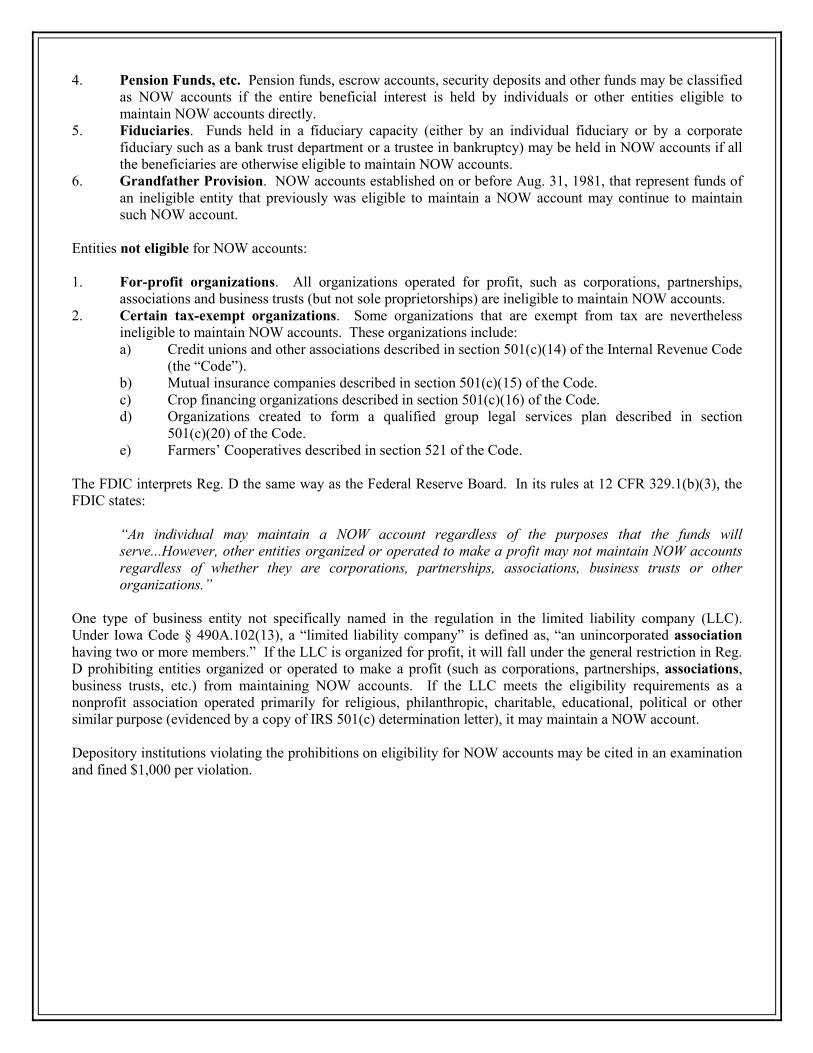

Entities not eligible for NOW accounts: 1. For-profit organizations. All organizations operated for profit, such as corporations, partnerships,

associations and business trusts (but not sole proprietorships) are ineligible to maintain NOW accounts. 2. Certain tax-exempt organizations. Some organizations that are exempt from tax are nevertheless

ineligible to maintain NOW accounts. These organizations include: a) Credit unions and other associations described in section 501(c)(14) of the Internal Revenue Code

(the “Code”). b) Mutual insurance companies described in section 501(c)(15) of the Code. c) Crop financing organizations described in section 501(c)(16) of the Code. d) Organizations created to form a qualified group legal services plan described in section

501(c)(20) of the Code. e) Farmers’ Cooperatives described in section 521 of the Code.

The FDIC interprets Reg. D the same way as the Federal Reserve Board. In its rules at 12 CFR 329.1(b)(3), the FDIC states:

“An individual may maintain a NOW account regardless of the purposes that the funds will serve...However, other entities organized or operated to make a profit may not maintain NOW accounts regardless of whether they are corporations, partnerships, associations, business trusts or other organizations.”

One type of business entity not specifically named in the regulation in the limited liability company (LLC). Under Iowa Code § 490A.102(13), a “limited liability company” is defined as, “an unincorporated association having two or more members.” If the LLC is organized for profit, it will fall under the general restriction in Reg. D prohibiting entities organized or operated to make a profit (such as corporations, partnerships, associations, business trusts, etc.) from maintaining NOW accounts. If the LLC meets the eligibility requirements as a nonprofit association operated primarily for religious, philanthropic, charitable, educational, political or other similar purpose (evidenced by a copy of IRS 501(c) determination letter), it may maintain a NOW account. Depository institutions violating the prohibitions on eligibility for NOW accounts may be cited in an examination and fined $1,000 per violation.

REG. CC HOLD FLOW CHART – Most Restrictive Order

Intellectual Property of IBA 9.11.2018

New Account §229.13(a)

•Must include this option in Funds Availability Policy to use.•Does Account Qualify for "New Account Hold? (First checking account - consumer or business -

open for 30 calendar days or less).• If account qualifies, place NEW ACCOUNT hold for reasonsable time period (typically 9 business

days) on full deposit for non-official checks. ($200 rule does not appy)• If account qualifiies and Official Check is deposited, place NEW ACCOUNT hold for 9 business days on

all but first $5,000 of deposited checks.• If account does not qualify for New Account hold, continue to next step.

Redeposit§229.13(c)

•Does the deposit include a previously returned deposit item (returned for reason other than for endorsement or post date)?

•If previously returned item is deposited, place EXCEPTION HOLD for REDEPOSITED Check for 7 business days on full amount of deposited checks. ($200 rule does not apply)

•If transaction does not include a redeposited check, continue to next step.

Repeat Overdrafts§229.13(d)

•Has the account been repeatedly overdrawn or would have been repeatedly overdrawn had the checks been paid (6 banking days or more in previous six months or 2 banking days or more in previous six months in amount of $5,000 or more)

• If account has repeat overdrafts, place EXCEPTION HOLD for REPEAT OVERDRAFT for 7 business days on full amount of deposited checks. ($200 rule does not apply)

• If customer is not a repeat overdrafter, continue to next step.

Reasonable Cause

§229.13(e)

•Is there reason to doubt collectibility of deposit item (paying bank indicates it won't pay, check is altered, stale dated more than six months, post dated)?

•Cannot place hold just because type of check (credit card advance, insurance check, etc.)• If reason to doubt collectibility exists, place EXCEPTION HOLD for REASON TO DOUBT

COLLECTIBILITY for 7 business days on full amount of deposited checks. ($200 rule does not apply)•Document reason bank doubts collectibility on internal forms.• If check is paid, refund any NSF/OD fees assocaited with hold.• If no reason to doubt collectibility, continue to next step.

Emergency Conditions§229.13(f)

•Is the bank unable to make funds available due to emergency conditions (computer malfunction, natural disaster, war, etc.)?

• If emergency exists, place EXCEPTION HOLD for EMERGENCY CONDITIONS for 7 business days on full amount of deposited checks (or a reasonable period after emergency has ceased if longer than 7 business days after date of deposit). ($200 rule does not apply)

• If not, continue to next step.

Large Deposit§229.13(b)

•Does the deposit include checks totaling more than $5,000?•If yes, place LARGE DEPOSIT HOLD on amount EXCEEDING $5,000 of deposited checks for 7 business

days•NOTE: Case-by-case hold may be placed for $4,800 for two business days on first $5,000. The first

$200 must be made available the next business day.• If no, continue to next step.

Case-by-Case

§229.10(c)

•Must include this option in Funds Availability Policy to use.•May be used for any reason (hold amount under $5,000 for large deposit hold, want to verify funds,

unable to use any of the reasons above)•Must make first $200 of checks deposited available next business day ($200 total - not per check)•Place CASE-BY-CASE HOLD for all but $200 of checks deposited for 2 business days.

REMINDER

NEXT Day Items - first $5,000 not subject to New Account hold: • U.S Treasury

Checks • Teller Checks • U.S. Postal

Service Money Orders

• Federal Reserve Bank Checks

• Federal Home Loan Checks

• Cashier’s Checks Certified Checks

REMINDER

Not Subject to Exception/Case-by-Case Holds:

• Electronic Payments (Wires , ACH)

• Cash • On-Us Checks