aspire 2015 - auckland€¦ · - since april 2015 - uses a small amount of blood from a finger...

TRANSCRIPT

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

1

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

The Age of DisruptionAndres Webersinke

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

2

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

What’s not the agenda?The 2014 CNBC’s Disruptor 50 List

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Electronic CigarettesDisruption in the tobacco market

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

3

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• E-cigarettes or Electronic Nicotine Delivery Systems (ENDS) have been hailed as an aid to smoking cessation and now account for 1% of the $100 billion global tobacco market

• Scientific evidence that e-cigs aid in quitting smoking is inclonusive• Many smokers become dual-users of tobacco and e-cigarettes• They are, however, gaining popularity: in the UK, e-cigs use has tripled in the two

years to 2013 from 700,000 to 2.1 million users (2.6 million users by 2014)• Many fear their popularity could re-glamorise smoking, enticing new smokers or

discouraging others from stopping

E-cigarettes

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• 7.3% of Victorian adults had used electronic cigarettes in the past 12 months in 2013

• Use more likely in younger age groups (<30 years)- 53.8% of current; 30.5% of former; and 4.8% of never-smokers

• Use of e-cigarettes nearly doubled in Australia (2014) - E-cigarette use among current and ex-tobacco users has increased from 6.7% to 11.4% in

past 12 months

• Use of e-cigarettes in New Zealand (New Zealand Health Promotion Agency)

- Adults: ever-use: 13%; current use: 1%- Adolescents: ever-use: 20%; current use: 3%

Vape – Word of the year (Oxford Dictionary 2014)Inhale or exhale the vapour produced by an electronic cigarette or similar device

Aspire 2015 - Auckland

Source: Global Drug Survey 2015

Source: Centre for Behavioural Research in Cancer, Cancer Council Victoria, Electronic Cigarette Use in Victoria 2010 to 2013 (publication pending)

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

4

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Australia: a number of laws relating to poisons, therapeutic goods and tobacco control apply- Federal Department of Health: nicotine can be imported as an unapproved therapeutic good (e.g. a

smoking cessation aid), subject to a prescription and only 3 months’ supply

• NZ: The Medicines Act and the Smoke-free Environments Act 1990 (SFEA) regulate the sale, advertising and use of e-cigs and the liquids used in e-cigs- You can import nicotine-containing e-cigs for own use (up to a 3 months' supply)

• New EU rules (mid-2016) for e-cigs aimed at harmonising quality and safety requirements - For e-cigs classified as consumer products the maximum nicotine content may not exceed

20 mg/ml

- Higher concentrations may be available under a pharmaceutical framework

Legislation

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Cotinine screening (the routine test for applicants who claim to be non-smokers) cannot identify the method of nicotine intake

• Individuals who remain addicted to nicotine are in danger of using tobacco• It is highly plausible they will revert to smoking or become dual users

Key considerations for Life insurers

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

5

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

9

1 1

12

83 2

9

8

8 9

124

9 10

0

5

10

15

20

25

Not smokedcigarettes >

12 mths

…but regular cigar only

…but 1-2 cigars p.m.

…but on NRT …but using e-cig only

S-NZ

S-AUS

NS-NZ

NS-AUS

Gen Re’s 2015 Underwriting Survey

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Most life insurers in Australasia only ask about tobacco smoking, anyone only using e-cigs does not smoke and would answer No

• At least one Australian life insurer explicitly asks about any sort of “tobacco” use incl. nicotine replacement products and e-cigarettes

How would we know someone is e-cig only user?

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

6

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

The Advice WizardDisruption in the provision of advice

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Making advice affordable- Where investments are low- Where rules-based advice suffices

• Also appropriate for protection business !?- Filling the gap between “best advice” and “general” or “no” advice business

Digital Advice or Robo-Advice

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

7

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Humans aren’t replaced completely• Primary use for now: automating initial information

gathering• Provides written recommendations• Triggered by massive wave of Fintech start-ups

and fee-for-service rules• Progression from simple to intelligent

automation (with human adviser being coachrather than back-up)

Digital Advice or Robo-Advice

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

The Diagnosed SelfLimits of diagnostics are being disrupted

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

8

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Known for the US$100 direct to consumer personal gnome test based on saliva- Results for predispositions for more than 90 traits* and conditions

• Invention of the Year 2008 (Time)• FDA: “genetic test is considered a medical device” thus requiring federal approval• Approval not granted• Tests now limited to mainly ancestry and some health-related components• Selling mainly in the US and Canada

23andMe

Aspire 2015 - Auckland

*One trait is earwax type: wet or dry

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

The Diagnosed SelfDisruption in laboratory diagnostics

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

9

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• “World’s most accurate HIV self-test” – BioSure, a UK company believing in the expansion of rapid testing in healthcare situations and for self-testing

- Order online – just £30- Since April 2015- Uses a small amount of blood from a finger prick- Result within 15 minutes - 99.7% sensitivity, 99.9% specificity

• AAZ (France) offers similar kit since September 2015 (€25)• Since 2012 OraSure (USA) offers OraQuick in-home HIV test (US$ 40)

HIV home test kit

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• One drop of blood is enough to run 30 lab tests (200 tests are offered)• Information available on your mobile app within hours• Costs a fraction of the usual lab charges

An industry revolution

Or a marketing phenomenon?

Theranos – convenient, faster, cheaperUS-based company founded in 2003

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

10

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Theranos “Wellness Centers” are located inside some Arizona and CaliforniaWalgreens outlets (largest drug retailing chain in the US)

• 6/15: Partnership with Carlos Slim Foundation (Mexico)

• Effective July 2015: Arizona has a law that gives consumers the explicit rights to order any lab test without having to go through a doctor

Theranos

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Based on microfluidics – engineered manipulation of fluids at the submillimetrescale with the potential for improving diagnostics and biology research

• But research into microfluidics would still suggest that running 30 tests from a drop of blood is an impressive feat

• One patent is for a finger warmer – to ensure blood is collected without cellular damage

• Technology used has not been disclosed to scientific journals• No published results to compare with conventional technologies

Theranos in the test roomTherapy and Diagnosis: diagnose early to make therapy effective

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

11

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• So far, no life insurer has signed up with Theranos• Existing labs and scientists are critical (after all Theranos is the disruptor)• Customer-friendly alternative?• Potential for lower NML?• $9 Herpes simplex virus test approved by the FDA in July 2015• Theranos has stopped collecting tiny vials of blood drawn from finger pricks (on

FDA’s behest): The Wall Street Journal, 18 October 2015

Theranos and Life insurance

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Private Data for DiscountsLifestyle underwriting or“Something for Something”

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

12

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• More than 70 million wearable electronic fitness devices were sold in 2014 (source: Gartner)

• 130 million units will be shipped in 2018 (source: Juniper Research)

Wearable technology - market

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

What is measured?

Aspire 2015 - Auckland

Movement Blood Pressure

HR Variability

Glucose

Heart RateBlood Oxygen

TemperatureSleep

Calmness

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

13

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• The advancement of sensors effectively allow for the miniaturization of medical equipment that formerly only a centralized institution could afford

• Digital health to see major uptake in the coming years• Sufficient clinical data exist to support adoption• Stakeholders are starting to accept ways digital technologies can evolve care• Large healthcare firms are starting to adopt digital technologies

“Digital Revolution” – it starts in healthcareGoldman Sachs research (29 June 2015): The Digital Revolution comes to US Healthcare

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Tattoos- Temporary tattoo paper measures lactate level in sweat

• Other devices read blood glucose levels (using tear fluid), BP, HR, sleep, gait analysis, single-lead ECG etc.- Continuously measured providing more valuable information

Sweat and cry for health indicatorsBiosensor tattoos / Wearable biosensors / Healthpatch

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

14

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Health insurers- Targeting insured lives at high risk

(e.g. diabetics)- Actively managing a portfolio

Opportunities

Aspire 2015 - Auckland

• Life insurers - suggestions- Programmes with evidenced activity for

rewards- To attract fit and healthy lives- To encourage healthy behaviour from sub-

standard risks- Together with employers for e’er/e’ee schemes

- Eligibility for discounts depending on take-up rate

- Appealing to Generation X and Millennials(gaming, instant information)

- RTW support

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Think holistically- Better risks (new and in-force)- Greater loyalty- Marketing advantage- Know your customers

Offering

Aspire 2015 - Auckland

• Monetary incentive- Immediate discounts and- Maintained discounts (maintaining

status, moving up or down)

• App• Interaction with consumer• Non-insurance related incentives

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

15

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Cost• Accuracy of devices• Reliability of information (device outcome (step count) for common wearables is accurate

(Source: Case et al. Accuracy of Smartphone Applications and Wearable Devices for Tracking Physical Activity Data. JAMA 2015. Vol 313 (6))

• Take-up rate- Who uses wearables? And for how long?

• Change in technology- Throughout life of policy- Apps

• Behaviours and data privacy

Considerations / Issues

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Investment into API • Protection insurance experience MAY

improve – majority of offerings are too new to consider effectiveness (Vitality data biased?)

• Lapse experience may be better• Improves industry image• A way to get something back from

insurance• Converts a dull industry into a

dynamic and valued industry

• Great deal of excitement around wearables

• Mass market success far from guaranteed

• Abandonment rates continue to be high

• Lack sustained benefit for the mass market

• Any insurance offering must be based on more than just wearables

Considerations

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

16

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Rent the device for € 6.99 p.m.• First assessment after 25 hours

driving and valid for remaining part of first policy year

• Up to 30% discount• Online data• Monthly calculation thereafter

• So far: low take-up rates internationally

• The biggest take-away: building R&D units

• Forming partnerships with tech firms• Learning from pitfalls• Firms that can adapt quickly,

collaborate and innovate will be able to harness the benefits of technological change

Telematics – any learnings?Example VHV Versicherung (Germany)

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Summary

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

17

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Disruption is everywhere, irreversible, rapid and progressive• Sometimes we just need to change an underwriting question (e-cigs)• Sometimes it offers opportunities for continuous or lifestyle underwriting and to

manage a portfolio overall better - For sub-standard risks and others- The way we communicate with policyholders (gamyfication; lapse behaviour, etc.)- New technology (such as microfluidics) will reduce invasiveness and offers opportunity for

lower NML

• Customers have something to offer! And we have the means to analyse it: Data- Take it or leave it

• Pace of change is increasing (and that is the true challenge for insurers)

Summary

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

The App-solute storyMatthew Ramjan

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

18

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Agenda

• The Beginning • Statistics – Growth of the App• Apps and Smartphones Statistics• Apps and Psychology – sort of• Are there benefits to business• Apps, devices and Insurance• Pros and Cons• Medical Apps• The Future and General Thoughts

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Statistics

• July 2008 – app store- opened with 500 apps

- Total current apps available for download – 1,848,845

- Total downloads to June 2015 – 100 billion- http://www.pocketgamer.biz/metrics/app-store/

• October 2008 – Google Play opened- March 2009 2,300 apps available

- 2015 – 1,660,965 apps available

- Over 50 billion apps downloaded globally- http://www.statista.com/statistics/263794/number-of-downloads-from-the-apple-app-store/

• Rough total – 3.5 mill apps available for download currently

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

19

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.Aspire 2015 - Auckland

http://www.pocketgamer.biz/metrics/app-store/

App Store Apps by Download

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Average Smartphone User

Aspire 2015 - Auckland

http://www.statista.com/chart/1435/top-10-countries-by-app-usage/

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

20

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

The Psychology of the Phone

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.Aspire 2015 - Auckland

• 70% of US smartphone users would rather give up alcohol than lose their phone…

• 62% of android users have never paid more than $1 for an app

• 34% of Iphone users check their phones at the dinner table

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

21

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Insurance Apps

Aspire 2015 - Auckland

http://www.zurich.com.au/content/zurich_au/media/media_releases/2015/zurich-launches-first-consumer-facing-life-insurance-app.html

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.Aspire 2015 - Auckland

https://play.google.com/store/apps/details?id=com.hdfcclife.activities&hl=en

Insurance Apps

HDFC Life Insurance App

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

22

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.Aspire 2015 - Auckland

https://itunes.apple.com/us/app/life-insurance-sales-application/id473664239?mt=8

Insurance Apps

Life Insurance Application

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.Aspire 2015 - Auckland

Insurance Apps

• Holloway Friendly – UK

• Lump sum to 100k Pound

• Two questions only

• Only available via app

• Supported by Gen Re

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

23

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Health Apps

• Oct 2014 – American Medical Association counted more than 97,000 health apps on the US market

• Range - lifestyle apps for fitness/wellness/nutrition, to medical apps for monitoring patients

• E.g. BP, heart rate, ECG, temperature, BSL, etc all measured with a smart phone app - Info then transmitted to personal app or GP

• Sept 2015 – UK Govt announced within 1 year, patients will be able to access full records on a Smartphone, update evidence from a wearable device and transmit direct to an app

• Apple moved into the market with the IOS 8 update- Forced everyone to take their health apps, with the upgrade- Now competing in the Health app market

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Pros and Cons with Apps

• Quality of health apps - current lack of standards for apps• Uncertainty of accuracy and clients using these as monitoring rather than seeing GP

- Potential - lead to major health issues (i.e. lack of proper monitoring of BP in a hypertensive patient)

• Big seller – Instant Blood Pressure Pro – for entertainment only BUT people using it to monitor their hypertension

• If apps accurate, possibility of medical conditions being recognised earlier in future• Could lead to increased health insurance costs but could lead to lower diagnostic

costs due to self-monitoring• Earlier diagnosis could also lead to lower longer term costs, including to insurance

companies

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

24

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Bigger risks: - anti selection - clients self-diagnose without a doctor (or Dr’s notes to record)- fraud with using wearable and app incorrectly –walk the dog!- Privacy and security – wearable information to app - portal for hackers- Apps in home devices (e.g. fridges, security system) have this potential flaw

• Legal framework issues – who is responsible for an accurate (or inaccurate) app medical assessment? What minimum standards are being applied?

Aspire 2015 - Auckland

Pros and Cons with Apps

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Blood Pressure Monitor Examples

Aspire 2015 - Auckland

http://www.imedicalapps.com/2014/07/iphone-health-app-patient-harm/

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

25

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Benefits and Issues to Insurance Industry

• Currently, health and wellness tracking

• Rewards for achieving and maintaining healthy living

• Benefit to insurance company with anticipated lower claims and healthcare costs

• Risks – inaccuracy of data obtained

- Device recording inaccurately (one study found device 25% out with results)

- Client controlling the information

• Companies allowing a Bring Your Own Device (BYOD) to work

• Issues with apps – security and privacy issues

• Malware

• Transferring security issues to main system

• Currently more beneficial for existing clients to maintain health, or for claims monitoring and wellness encouragement

• Very limited current capability for underwriting

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Mobile Phone Apps – potentials for Insurance Coys.

Aspire 2015 - Auckland

• Reminders

- Pay premiums

- Complete new business process (car inspected etc)

- Submit claim information

• Updates about claims

- Etc.

• Policy information requests

• Generate leads

• Sell Insurance

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

26

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Thoughts on Apps and Insurance Companies

• Can Apps increase business? Will people really download insurance coy apps in order to buy?

• Is there another way insurance companies can use apps to a more beneficial affect?

• Using apps as link into existing clients

• When client signs up, obtain email address as well

• Once policy in force, welcome letter AND email welcome letter and include a link to the app

• Also send SMS with link to app

- Encourage to download app.

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Potential as a portal into the company:- to check own policy information

- also a portal out to advise client of benefits, discounts on policy, etc

• Can also use this for health benefits such as providing the wearable and logging it into the app. Company can track benefits and client can also log in and see score card, etc

• From underwriting point of view:

- Potential – provide wearables and link to apps for the substandard client as an encouragement towards healthier behaviours

- Healthier client should equate to lower risk of claim

Aspire 2015 - Auckland

Thoughts on Apps and Insurance Companies

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

27

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

The Future

• Google labs working on contact lens for diabetics• Contains sensors to analyse tears and send information to patients smartphone• Potential -this then monitors/controls insulin pump to ensure very good control

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Work on Smart glasses

• Smart wig- GPS wig

- PowerPoint wig

- Sensing wig

• Google also working on cancer and heart attack detecting pill- Information then fed back to a wearable device containing monitoring app that correlates the information

• Google developing a wearable sensor for cardiac and activity tracking to measure pulse, skin temperature, ECG, activity levels, to then feed back to app for doctors to monitor

• Apps to measure fluids (i.e. saliva, blood, mucous)

Aspire 2015 - Auckland

http://mobihealthnews.com/44622/google-x-is-developing-a-wearable-for-clinical-research/

http://mobihealthnews.com/40031/google-biogen-will-use-wearable-sensors-to-study-multiple-sclerosis/

The Future

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

28

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Is this the future - One day…

Aspire 2015 - Auckland

• Mike has his MobileLife app installed on his iPhone

• In the morning it tracks his morning run

- Has recently started running and because he has kept it up regularly, this triggers a premium discount on his life insurance

- CURRENTLY EXISTS (S.A.)

• Mike drives to work

- His MobileLife app notes that he rarely accelerates wildly and he avoids the peak rush hours and this earns him discounts on his life and motor cover

- CURRENTLY EXISTS (S.A.)

• He is also tracked after work as he cycles on a mountain bike trail. If he keeps that up further discounts are in store for him.

• Mike can also share his mountain bike stats with Fred. They have a competition going on who can cycle the most km during August.

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.Aspire 2015 - Auckland

• Mike gets onto his wifi scales and measures his weight

- The results are submitted to the insurer and his own app

- Potential for rewards for weight loss/maintaining healthy weight

• Mike is feeling unwell so he uses his app to communicate with his doctor and arrange a prescription without even leaving home

- CURRENTLY EXISTS (USA)

• On Friday evening Mike is tracked at the international departure lounge. MyLife App offers him travel insurance and notifies him as to emergency procedures and numbers to dial in case he needs to claim for health insurance.

- At the same time his home policy is updated with this information

- His security service is notified to keep an extra eye on his house

• During his trip Mike is tracked at a quad biking course

- Is notified his policy doesn’t cover quad biking and offered an extra premium to go ahead.

Or are we there?

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

29

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Underwriting Common Practices SurveyMatthew RamjanJames Louw

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Background

• Common underwriting practices- Belief is unchanged for many years

- Are they accurate and keeping up?

- Are they costing the industry money?

• Survey questions looked at the following common topics:- Smoker rates and what constitutes a smoker

- Common blood test requirements

- Involvement in football (Soccer/AFL/NRL/ARU/C3PO)

- Involvement in aviation

- Loadings and the practice of waiving minimal loadings

• Invitations - 25 invites, 21 responses – 84% response rate (12 NZ, 9 Aus)

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

30

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

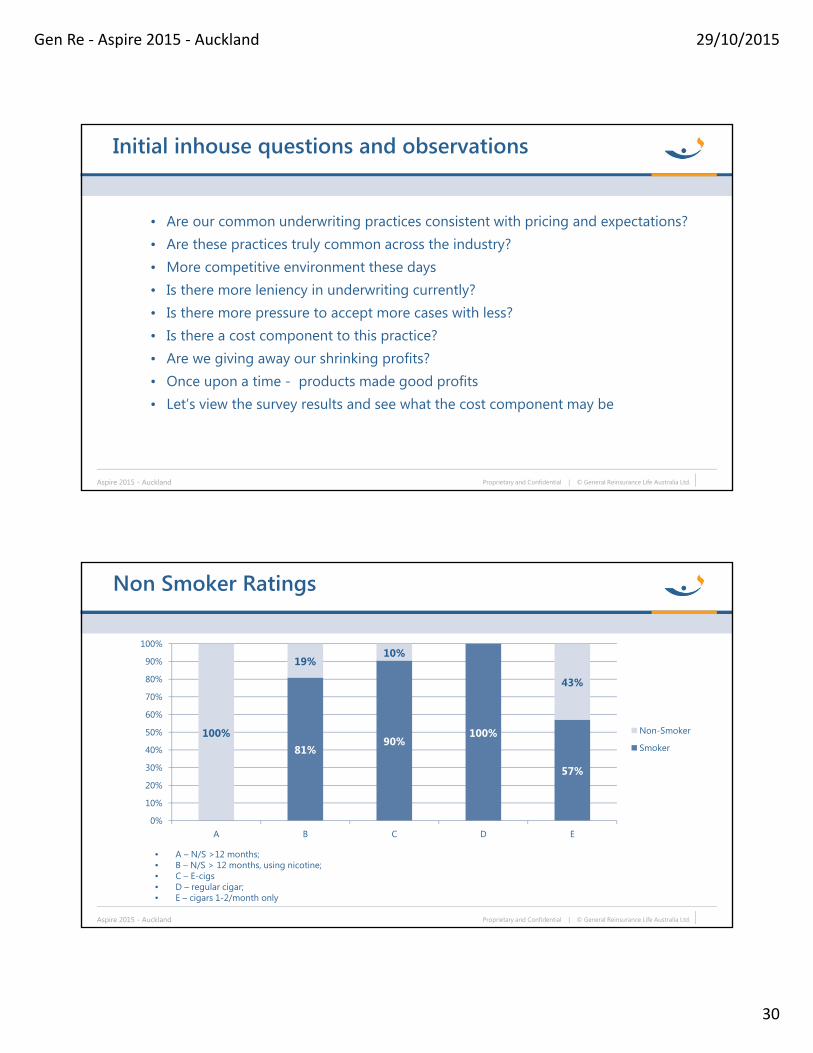

Initial inhouse questions and observations

• Are our common underwriting practices consistent with pricing and expectations?• Are these practices truly common across the industry?• More competitive environment these days• Is there more leniency in underwriting currently?• Is there more pressure to accept more cases with less?• Is there a cost component to this practice?• Are we giving away our shrinking profits?• Once upon a time - products made good profits• Let’s view the survey results and see what the cost component may be

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Non Smoker Ratings

Aspire 2015 - Auckland

81%90%

100%

57%

100%

19%10%

43%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

A B C D E

Non-Smoker

Smoker

• A – N/S >12 months; • B – N/S > 12 months, using nicotine; • C – E-cigs• D – regular cigar; • E – cigars 1-2/month only

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

31

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Smoking Abstinence Period

Aspire 2015 - Auckland

100%

81%

5%

14%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cigarettes Nicotine Replacement

0 months

3 months

12 months

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Blood test results

• Current practices for blood tests- Generally fasting blood tests required- Inconvenience to client and potential error

• However, fasting is no longer considered a necessity for:- Lipids results

• Therefore, is HbA1c a better measurement than glucose?- Glucose = fasting 8 hours prior- HbA1c = no fasting

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

32

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Blood Tests as a Limits Requirement

Aspire 2015 - Auckland

90.5%

38.1%

61.9%

9.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

MBA20 HbA1c

No

Only as a reflex test

Yes

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Blood Tests as a Limits Requirement

Aspire 2015 - Auckland

90.5%

38.1%

61.9%

9.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

MBA20 HbA1c

No

Only as a reflex test

Yes

• 100% of HbA1c auto requirements are same limits as normal blood tests

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

33

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• How does the industry treat involvement in all forms of football?

• Do we have consistency here?

• Is social involvement viewed as an increased risk?

Aspire 2015 - Auckland

Social/Amateur Football

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Social/Amateur Football (Union/League/AFL)

Aspire 2015 - Auckland

42.8%

28.6%

28.6%

57.2%

No

Offers loading as an alternative

Uses exclusions only

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

34

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Social/Amateur Outdoor Soccer

Aspire 2015 - Auckland

61.9%

23.8%

14.3%

38.1%

No

Offers loading as an alternative

Uses exclusions only

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Aviation results

• 21/21 thought there was additional aviation mortality risk

• 21/21 - use hours flown- Only 4 rely on hours flown on its own- everyone else uses that in conjunction with other measures

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

35

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Aviation Ratings

Aspire 2015 - Auckland

19%

43%

33%

5%

1 proxy (hours flown)

2 proxies

3 proxies

4 proxies

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Aviation

Aspire 2015 - Auckland

0.0%

100%

14.3%

76.2%

33.3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No additional mortalityrisk

Hours flown Number of takeoffs Type of licence Other - Type of craft

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

36

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Waiving of loadings

• Only 1 out of 21 companies- Never waive a +25% loading- All other companies advised that they will waive a 25% loading either:

- always (15/21)

- or sometimes (5/21)

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Waiving of +25% loadings

Aspire 2015 - Auckland

71% 67% 67% 67%

24%24% 29% 24%

5% 10% 5% 10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

For Life For TPD For Trauma For IP

Never

Rarely

Sometimes

Always

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

37

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Waiving of loadings greater than+25%

Aspire 2015 - Auckland

5%

57%52% 48%

38%

10%

10%10%

14%

29%38% 43% 48%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

For Life For TPD For Trauma For IP

Never

Rarely

Sometimes

Always

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Maximum loading waived

Aspire 2015 - Auckland

5% 10% 5% 10%

52%

62% 71%76%

38%24% 19%

14%5% 5% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

For Life For TPD For Trauma For IP

+75%

+50%

+25%

+0%

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

38

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.Aspire 2015 - Auckland

Waiving of $ per mille loadings and highest waived

• For a long time, loadings below $2 per mille were waived

• These loadings can equate to a very large loading being waived

• Survey results - significant percentage of these loadings being waived

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Waiving of loadings less than $2.00 per mille

Aspire 2015 - Auckland

29% 24% 24% 24%

10%5% 5%

24%

10% 5%5%

38%

62% 67% 71%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

For Life For TPD For Trauma For IP

Never

Rarely

Sometimes

Always

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

39

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.Aspire 2015 - Auckland

5% 5% 5% 5%

29%14% 14%

5%

67%81% 81%

90%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

For Life For TPD For Trauma For IP

Never

Rarely

Sometimes

Always

Waiving of loadings of $2.00 per mille or greater

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Maximum per mille loading waived

Aspire 2015 - Auckland

43%

62% 62% 62%

33%

24% 24% 24%10%

5% 5% 5%14% 10% 10% 10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

For Life For TPD For Trauma For IP

$2.00 per mille

$1.75 per mille

$1.00 per mille

Don’t waive.

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

40

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Pricing Implications

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Extra Mortality (Morbidity) and per mille- Extra Mortality is for risks that are proportional to the underlying curve- Per Mille is for risks that do not depend on age

• Why do we bother- We don’t have to- Concept of equity – charge each risk it correct rate- This has been diluted over time in the interest of treaty most people the same

Loadings

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

41

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Aviation• Count how many deaths per year from a group of similar Pilots

- Hours flown, etc

• How many pilots like that are there?• Say 6 deaths from 3000 pilots• 2 per mille• The trick is getting the data!

Calculation of a Per Mille Load

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Remember underlying death rates for males- 0.3, 1 and 2.5 at 30,40 and 55

• So a 1 per mille load- Is +300%, 100% and 40% at each age

• Female death rates a lower- So a per mille load has a bigger effect

• About 0.3% of policies have a per mille load- Ranging from 2 per miller to 20 per mille.

• If 0.5% should have a 1 per mille load- Overall impact on death rates is about 0.5%

Per Mille Load

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

42

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Just over 5% of policies are loaded with an EM• About half of those are +50%• Let’s assume 5% would be +25%

- Cost of 1.25% to waive them

Borderline Standard

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• We do not have to treat everyone the same

• Lots of people around BMI of 29 to 34

• Can generate a significant discount if we charge them appropriately

• New rating factors- Exercise and sport- Postal code- Occupation

Preferred Life

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

43

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

What You Don’t Know You Don’t KnowAnthony Callaghan – AHC Investigations

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Claims ApplicationsCarol Smit

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

44

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Timing of investigation

• Public domain

• Not the silver bullet

• Partnership

• Brief is critical

Claims Application5 Key Considerations

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Gen Re Experience StudiesJames Louw

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

45

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Gen Re has a long history of performing actuarial experience studies in NZ

• Gen Re strongly believes in supporting the NZ Insurance Industry

• Currently planning a 2008-2014 Lump Sum study- First ever comprehensive mortality +

rider study

History

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• 30 year old Male 0.426 per mille• 45 year old male 1.087 per mille• 55 year old male 2.495 per mille

• Try remember these numbers!

NZ Mortality

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

46

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Gen Re has performed this study, for free, since 1995• Gen Re also produces Mortality and Trauma studies, eg

- Mortality was presented at the previous NZ Actuarial Seminar in 2012- Included graduated industry mortality tables- Provided to the SoA with no restrictions placed by Gen Re

• This is a preview of high level results for DI 2008-2012• Overall report will be released before year end to all participants

NZ DI

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• 11 offices participated covering 90% of the market• Disability Income business with a focus on

- Incidence- Terminations- Payout

• Mortgage DI analyzed separately for the first time• Sub-standard lives analyzed for the first time

Scope

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

47

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

A/E by Year: Longer Term

Aspire 2015 - Auckland

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Male A/E by Cnt Female A/E by Cnt

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Long duration terminations have deteriorated

• 177 Terminations Year 4+• 93 Year 6+

• So has some credibility

Terminations by duration: Previous studies

Aspire 2015 - Auckland

0%

50%

100%

150%

200%

250%

Q1 Q2 Q3 Q4 H3 H4 Y3 Y4 Y5 Y6+

2008 - 2012 A/E by Cnt2004-2008 A/E by Cnt (restated)2000-2002 A/E by Cnt

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

48

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• A more sophisticated analytics technique• Already done on NZ DI Incidence• Example Output:

GLM

Aspire 2015 - Auckland

100%

135%

170%

Men Women

Exposure

Ratio raw ix

Estimate

appr. 95%confidence interval

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Gen Re is fully committed to the NZ Market• Planning a new major study looking at more factors than usual

- For example experience of buy backs- TPD experience for first time

Summary

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

49

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Let’s get Direct – The Good, The Bad and The UglyCarol Smit

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

The Australian direct life insurance distributionSource: Plan For Life Australia Direct Life Insurance Report 2015 (statistics as at December 2014)

Aspire 2015 - Auckland

Direct, 26%

Retail Advice, 29%

Group, 45%

Sales by Business Line

Retail Advice, 50%

Direct, 11%

Group, 38%

Inforce Premium by Business Line

Telephone, 48%

Online, 30%

Mail-outs, in branch, 22%

Direct Inforce Lump Sum Risk by Channel

Term, 36%

TPD, 1%CI, 6%

IP, 7%Funeral, 12%

Mortgage, 30%

AD, 0% Other, 8%

Direct Sales by Product Line

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

50

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

NZ Retail Risk BusinessSource: FSC Statistics (June 2015)

Aspire 2015 - Auckland

64

64

15

Inforce Premium‐ $m

Guaranteed Acceptance

Credit Insurance

Accidental Death

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Risk Commenced: 23/04/2013 & 14/06/2013

• Event date: 27/08/2013

• Age at entry: 74

• Sum insured: $2m Accidental Death Cover

Every 40 seconds someone commits suicide in the world- WHO 29014, Preventing suicide-A global imperative

Story 1: Deadly End

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

51

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

We will not pay a claim if the accident, accidentaldeath or accidental injury arises directly orindirectly from, or is in any way related to:

• Suicide

Key Learnings: • Insurable interest• Maximum entry ages• ?Tapering beyond a certain age

Unfortunate Story

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Risk Commenced: 27/06/2012

• Event date: 27/08/2013

• Age at entry: 41

• Sum insured: $1m

Gen X (1966-1975) has the highest suicide rates…- Suicide-Australia’s Number One Cause of Premature Death: Gen Re Blog, Andres Webersinke

Story 2: No Way Out

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

52

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Business partnership

• Asphyxiation

• 2 Suicide notes

• Will

• Only cover

• Few consultations for anxiety and stress related to business pressure and prescribed anti-depressants

No Way Out cont.

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• We will not pay a claim arising directly or indirectly from:

• A pre-existing medical condition:

• A pre-existing medical condition is an injury, illness, condition or related symptom that, in the five years immediately preceding the policy commencement date and

• Suicide by a life insured within the first 13 months of the start or reinstatement of the policy.

• 5 year PEC should match suicide exclusion period

Mutual Exclusivity of Suicide and PEC Clauses

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

53

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Risk Commenced: 10/05/2011

• Event dates:- 21/05/2012- 20/11/2012= $18,000

- 09/07/2013-19/08/2013 =$580

- 14/03/2014-13/09/2014= $19,098

• Policy lapsed: 16/05/2015

Serial Claiming

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Risk Commenced: 17/08/2014

• Event date: 10/10/2014

• Sum insured: $500k

• Question:- Have you ever suffered from, been

diagnosed…any cancer- Y- Have you been discharged by your

specialist…- Y

• Risk Commenced: 21/03/2013

• Event date: 15/08/2013

• Sum insured: $750k (3 phone calls)

• But Sheila said to say “no”…

Key Learnings• Quality control of PoS• Full control of distribution channel• URE is critical

Point of SaleLet’s just say “no”… Have you ever…

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

54

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• PoS script and sales person quality control checks

• Cover increases to be handled by a different sales person

• Short form underwriting and robust rules

• Risk control checks- number of policy increases, max sum insured

• Underwriting at Claims stage

We live and we learn through hindsight

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Husband notified of her death 2 months after RCD

• MVA in Kosovo

• Claim proofs within 10 days translated into English

• We found many inconsistent information

• Non-income earning female bought several life policies over the phone- No financial underwriting- Requested electronic communication

only

• $4.5m Life Cover - Requested funeral advancements- Submitted all documents electronically

• Key Learnings:- Financial underwriting also for

simplified underwriting

Too good to be trueSales Stage Claims Stage

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

55

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Weather

• Location of the incident

• VIN decoder

• Kosovo government website

• Partnership between insurers and reinsurers

• On the ground verification

• Successful decline

Risk Management Investigation

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Sales call

• PEC Lifecover

• Claiming within 90 days of RCD

• Various red flags

• International investigation

• Key Learnings:- Financial underwriting- Protecting Claims staff

Learnings from Overseas Claims

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

56

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• 37 Claims within 60 days of RCD- 12 Fractures- 3 Cancers- Rest for illnesses

• 3 Channels- 65% claims from Channel A- 40% of claims from Building and Construction Industry for musculo-skeletal injuries

• Analyse the portfolio to monitor trends and feedback into the risk loop

Portfolio Analysis

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Summary

Aspire 2015 - Auckland

• Direct marketing offerings open a new market segment

• Opportunity for targeted marketing / white labeling

• Underwriting can be made simple but does not need to be

• Underwriting decisions and/or exclusions clauses can be designed to be “tougher”- Exclusion wordings need to be “water-proof”

• Financial underwriting is essential

• Strong correlation between pricing and underwriting

• Monitoring is key

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

57

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Inside Outside Terminal Illness –understanding all perspectivesViviane Murphy

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• New Zealand Ranked Number 3 in death quality index• 15,000 people in New Zealand receive hospice care• 20 percent under age 60• 8905 deaths are due to cancer• May - $76m government boost for palliative care

Introduction

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

58

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Dr Rob Young• Michelle Dalton, Senior Product Manager, Sovereign• Robyn Prentice, Product Manager Asteron New Zealand• Andres Webersinke Managing Director Gen Re Life Australia

Panel

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

State of AdviceRobert Kerr

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

59

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• History of reviews into Commission• Current proposals• Insurers actions

Agenda

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Scope “Report on issues associated with financial products and service provider collapses that occurred in the wake of the Global Financial Crisis “

• Recommended a ban on remuneration that influences advice• Underinsurance was a significant issue• Positive benefits provided to individuals and to the broader

community • Concerns that removing direct remuneration to advisers would

- Substantially increase up-front costs of acquiring insurance- Result in considerably less insurance being sold through

advisers- Significant reduction in the number of people receiving

advice

Ripoll Inquiry - 2009

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

60

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Ban on conflicted remuneration- Not apply to retail risk insurance advice.

• A duty for financial advisers to - Act in the best interests of their clients, and - Place the best interests of their clients ahead of their own

when providing personal advice to retail clients

• Enhanced powers for ASIC

Future of Financial Advice (FoFA) reforms

http://futureofadvice.treasury.gov.au/content/Content.aspx?doc=home.htm

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Focus on advice channel only• Phase 1

- Industry roundtables- Survey of product providers

• Phase 2- Reviewed over 200 advice files - Between September 2013 and July 2014

• Report released 9 October 2014

ASIC Report 413 – Review of Retail Life Insurance

http://asic.gov.au/regulatory-resources/find-a-document/reports/rep-413-review-of-retail-life-insurance-advice/

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

61

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• 63% Compliant• 37% failed to comply with the laws relating to appropriate advice and prioritising

the needs of the client

• High upfront commission more strongly correlated with non-compliant advice

Findings of ASIC review

“The industry as a whole needs to consider how remuneration and compliance practices can better support good quality outcomes for consumers”

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• 2.6m policies inforce (June 2013)• Premium income $8.4bn (March 2014)

• Policies inforce 86 months

• Commission Levels

- 12 month clawbacks

Background to Australian Market

Initial RenewalUpfront 100-130% 10%Hybrid 70-80% 20%Level 30% 30%None /Fee /Salaried 0% 0%

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

62

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Insurers: (a) address misaligned incentives in their distribution channels(b) address lapse rates(c) review remuneration arrangements

• good-quality outcomes for consumers • manage the conflicts of interest

ASIC Recommendations

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Licensees: (a) prioritises the needs of the client (b) review business models to provide incentives for strategic

life insurance advice(c) review the training and competency(d) increase monitoring and supervision

• build ‘warning signs’ into file reviews • create incentives to reward quality, compliant advice.

ASIC Recommendations

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

63

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

9 October 2014Association of Financial Advisers (AFA) and Financial Services Council (FSC) announce they will jointly convene a working group

Brokers online responses:“So ASIC what us to pick up our game because 37% of files reviewed were not good enough. Does this then mean our industry is rotten to the core. No its not.”“A few things are blindingly obvious. ASIC went into this with a pre-conceived hatred of, firstly commissions of any sort, and up-front commission in particular.”

Industry Response

riskinfo.com.au/news/2014/10/09/asic-life-insurance-advice-review-unacceptable-level-of-failure/Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

17 October 2014• John Trowbridge is announced as the Independent Chair of the Life Insurance and

Advice Working Group (LIAWG)• There are six other representatives on the LIAWG, three from insurers, three from

advisers

Life Insurance and Advice Working Group formed

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

64

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Provide a unified response to the identified issues• Address the three key issues arising from the report

1. Remuneration structures2. Product design issues3. Quality of advice

• Provide specific analysis on the options and recommendations for industry change, including transitional paths

Terms of Reference

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

7 December 2014Independent Report chaired by David Murray

Examine how the financial system could be positioned to best meet Australia’s evolving needs and support Australia’s economic growth’

Wide ranging reportOver 6000 submissions and 350 pagesMade 44 recommendations

Murray Financial Systems Inquiry

http://fsi.gov.au/publications/final-report/Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

65

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Better align the interests of financial firms with those of consumers by raising industry standards, enhancing the power to ban individuals from management and ensuring remuneration structures in life insurance and stockbroking do not affect the quality of financial advice

Recommendation 24

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

17 December 2014• “Independent Recommendation” of John Trowbridge• Issues and Options paper not recommendations• Invitation for submissions

Interim Report on Life Insurance Sector

http://www.fsc.org.au/downloads/file/PublicationsFile/TrowbridgeInterimReportonRetailLifeInsuranceAdvice_2014_1217.pdfAspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

66

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Adviser Paraplanner Admin support

Initial enquiry discussion and prep for first meeting 15 mins

Conduct first meeting, understand the client,complete file notes

2 hours

Input client data to CRM software/set up client file/follow-up client for statements, etc

1 hour

Research client’s current holdings and consider appropriate recommendations

1 hour 1 hour

Obtain multiple quotes for suggested recommendations 45 mins

Document recommendations in SoA 30 mins 2-4 hours

Run new quotes on revised terms as requested by client 15 mins

Complete application forms with client 1 hour

Arrange for, and follow up, underwriting requirements until complete

45 mins 3 hours

8 hours 3 hours 5 hours

Cost per hour $299 $171 $105

Cost of Advice

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

26 March 2015Six Policy Recommendations on• Adviser Remuneration• Licensee Remuneration• Approved Product Lists• Quality of Advice• Insurer Practices

Trowbridge Report

http://www.fsc.org.au/downloads/file/MediaReleaseFile/FinalReport-ReviewofRetailLifeInsuranceAdvice-FinalCopy(CLEAN).pdfAspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

67

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Commission – Level commission (maximum 20%) plus an Initial Advice Payment (IAP)- IAP payable on inception and not more than once every 5 years- IAP set per client and not exceeding 60% of first year payment or $1,200- All payments from insurer to adviser to be fully transparent to the client

• Three year transition period - 5 year rule applied immediately- 2016, for 2 years, industry operates on hybrid commissions with a cap of $8,000.

Advisers Remuneration

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Licensees prohibited from receiving benefits from insurers that might influence recommended product choices or the advice given by the licensees’ advisers.- Volume-based payments- Free or subsidised business equipment and services- Hospitality-related benefits- Shares or other interests in a product issuer or dealer group- Marketing assistance

• Licensee Support Payment – 2% premium

Licensee Remuneration

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

68

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Approved Product List (APL) contain at least half of the authorised retail life insurance providers- Increase competition from insurers- Increase choice for advisers- Support Duty of Best Interest

• Can still exclude an insurer if issues around servicing, claims handling etc

Approved Product Lists

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Licensees, in conjunction with their advisers, re-examine their culture, behaviours and practices regarding the advice process- Raising consumer understanding of life insurance - Informed consent from clients- Reducing the administrative burden on advisers

Quality of Advice

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

69

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• A Life Insurance Code of Practice be developed and aimed at setting standards of best practice for life insurers, licensees and advisers for the delivery of effective life insurance outcomes for consumers.- Standards of practice- Product disclosure- Consumer education- Access to information- Underwriting standards- Claims Handling- Upgrade cover

Insurance Practices

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Adviser Feedback

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

70

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Josh Frydenberg – Assistant Treasurer- Supports recommendations of Trowbridge report

“The extent to which government intervention is required will depend ultimately on the industry’s own actions … it is up to the industry now to restore public confidence before time for industry leadership runs out.”

• FSC Breakfast 15 April 2015“weeks not months to act”

Josh Frydenberg – Assistant TreasurerActions

http://www.fsc.org.au/media-centre/speeches/2015/the-hon-josh-frydenberg-mp-at-the-fsc-bt-political-series-breakfast-sydney-15-april-2015.aspx

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

21 April 2015• Disagreed with the remuneration reform proposals• Did not deliver on its original Terms of Reference• Some of the recommendations “unworkable”

AFA Response

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

71

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

22 April 2015• The FSC issues a response• The FSC will prepare a proposal for the Assistant Treasurer, based on the

recommendations put forward in Trowbridge Report- Proposal will be the view of the FSC alone, and not of the LIAWG

FSC response

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Hybrid (80/20) Commission only• 5 year responsibility period

AMP moves first – April 29

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

72

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

25 June 2015The Assistant Treasurer announces he has received a Life Insurance Framework, presented by the AFA, FPA and FSC, on behalf of the retail life insurance industry

Life Insurance Framework

http://jaf.ministers.treasury.gov.au/media-release/032-2015/

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Ban on other volume-based payments from 1 July 2016.

• Offer fee-for-service

Adviser and licensee remuneration

0

20

40

60

80

1 2 3 4 5

Commission

0%

50%

100%

150%

1 7 13 19 25 31 37 43

Clawback

No Tapering!

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

73

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Transitional arrangements

0

10

20

30

40

50

60

70

80

90

1 January 2016 1 July 2017 1 July 2018

Initial

Renewal

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Government to consider measures to widen Approved Product Lists by 1 July 2016

• Life Insurance Code of Conduct to be developed by the FSC by 1 July 2016

Quality of advice and insurer practices

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

74

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Ongoing reporting by life insurance companies of policy replacement data to ASIC to commence 1 January 2016

• Government to conduct a review of these measures by the end of 2018

Better enforcement and monitoring

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• ASIC to review Statements of Advice - making disclosure simpler and more effective

• Government to consider developing a mechanism to rationalise life insurance legacy products.

Industry efficiency

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

75

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Responses

Aspire 2015 - Auckland

Consumer Action Law Centre

”Proposed changes from the life insurance industry to overhaul excessive commission structures and questionable advice are a step in the right direction, but don’t go far enough.”

Advisers

“Victims for the sins of a few”“Betrayal from adviser associations (FPA and AFA)”“Clawback felt particularly unfair” “Doesn’t stop others churning my business”

Insurers

“An important step forward”“Rebuild trust”“Provide high quality to consumers”“We can now move on”

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Clarification- Level commission- Clawbacks

• FSC Working on Code of Practice for 2016

Industry steps

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

76

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Commission

0%

20%

40%

60%

80%

100%

120%

140%

Upfront

Hybrid

Level

New

0%

50%

100%

150%

200%

250%

300%

350%

Upfront

Hybrid

Level

New

Has commission increased?

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

New Prime Minister

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

77

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

New Assistant Treasurer

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Support advisers- Training

• Remove adviser costs- Support adviser marketing- Tele-underwriting- IT solutions

- Research, Statement of Advice

• Consumer Education• New Products ?• New Sales channels?

Insurers steps

Aspire 2015 - Auckland

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

78

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

• Australia has seen a history of poor advice• Believed related to high upfront commission• Moving slowly to reducing these commission• Other steps being taken• Insurers looking at their future propositions

• What are the implications for New Zealand?

Summary

Aspire 2015 - Auckland

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Aspire 2015 - AucklandThank You

Gen Re ‐ Aspire 2015 ‐ Auckland 29/10/2015

79

Proprietary and Confidential | © General Reinsurance Life Australia Ltd.

Proprietary Notice

This presentation is protected by copyright. All the information contained in it has been very carefully researched and compiled to the best of our knowledge. Nevertheless, no responsibility is accepted for its accuracy, completeness or currency. In particular, this information does not constitute legal advice and cannot serve as a substitute for such advice. It may not be duplicated or forwarded without the prior consent of the Gen Re.

Aspire 2015 - Auckland