asia pacific equity research 24 january 2011 top...

TRANSCRIPT

Asia Pacific Equity Research

24 January 2011

Top Stories MediaTek Inc. (OW), Taiwan Top turnaround story among large-cap tech – buy on 1Q trough (Alvin Kwock) While Mediatek is likely to see a meaningful earnings decline for FY11, multiple signs suggest 1Q will mark the trough. Notably, the new-product launch schedule has been smoother than the past, and in some cases there is even a schedule pull-in – the new management team seems to be executing quite well.

CapitaLand (OW), Singapore We reduce our PT to S$4.60, but stay Overweight (Christopher Gee, CFA) Due to an enlarged capital base, the stock has underperformed its relevant benchmark indices in the past 18 months. For this to reverse, we believe the group would need to lift its ROE above the past eight-year average of 10% and carry this positive ROE growth trajectory forwards; we estimate an FY11E ROE of 9.4%.

CapitaMalls Asia (OW), Singapore At the heel of the hockey stick – price target raised to S$2.75 (Joy Wang) While we still see near-term headwinds, with the stock trading at a 15% discount to our estimated tangible asset value and pricing in zero value for the group’s funds management business and for its platform, we see the current price as an attractive entry level. Added to our AFL, the stock is now one of our high-conviction OWs.

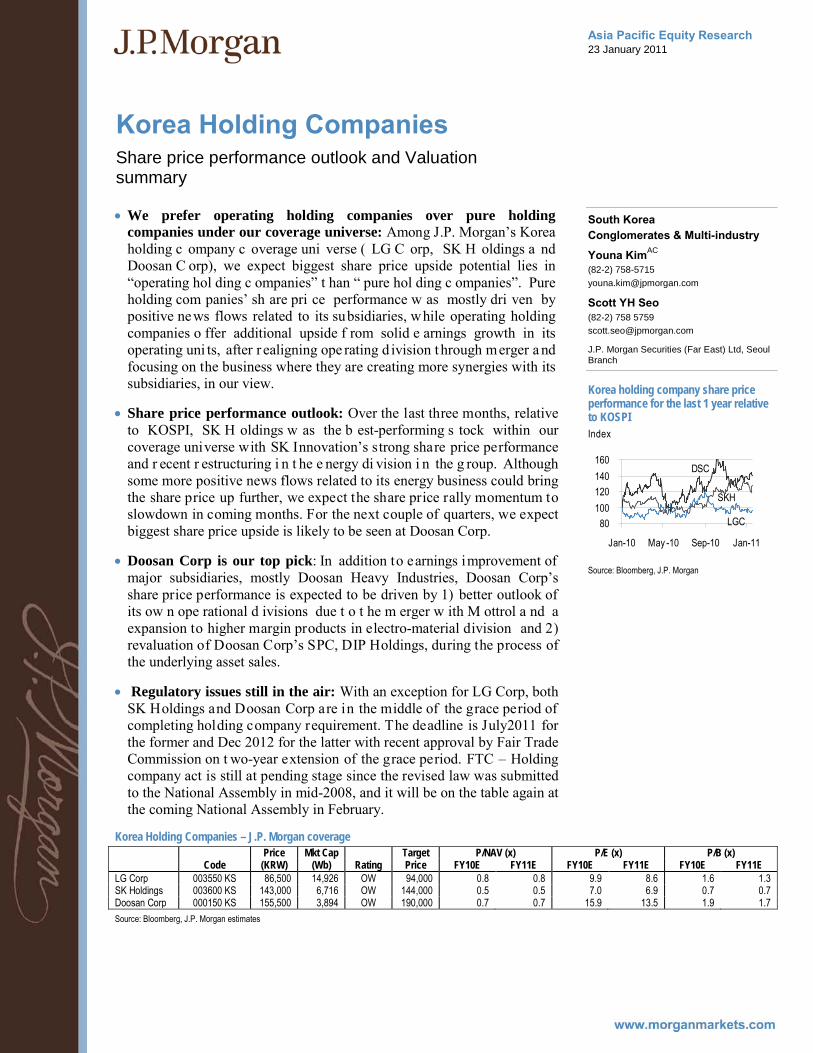

Doosan Corp (OW), South Korea New OW, with PT of W190,000 implying 22% upside (Youna Kim) We expect to see a strong revenue growth in Doosan’s own operations along with higher OPM, an upward revision in the market’s valuation of DIP Holdings, and better equity-method gains on stronger earnings visibility of its major subsidiary. It was the second best performing holding company in 2010, rallying 57% vs. KOSPI.

LG Display (OW), South Korea Cost-reduction efforts and earnings momentum to be key catalysts (JJ Park) Due to the delay in panel price recovery, LGD’s stock has underperformed YTD. Although it is likely to post another loss in 1Q11, aggressive cost reduction efforts and panel-demand recovery along with panel price stabilization from 2Q11 should drive strong earnings momentum. We reiterate our Dec-11 price target of W52,000.

Sunil Garg (852) 2800-8518 [email protected] Send me your feedback! AM perspective Adrian Mowat, Chief Equity Strategist Overheating is a risk in China

Source: Bloomberg, 20 January 2011.

A decline in China’s December CPI is a temporary reversal in trend. We advise reducing China exposure into any rally. Look for slower growth and a sustained decline in inflation to end the 17-month bear market in A-shares. But lower growth probably requires further policy tightening. We continue to view higher inflation and secular changes in China as ultimately negative for the commodity demand. If China moves from an investment-driven model, then the growth in its demand for commodities is overestimated. But structural changes are very difficult to time. Wait for policy tightening, combined with a breakdown in commodity prices, before moving significantly underweight. For more, please see Key Trades and Risks – Emerging Markets Equity Strategy, Mowat et al, 17 January 2011

Click below for the: J.P. Morgan Daily Valuations Latest Weekly AP Banks Analyzer (.xls) Daily Global Economic Briefing

Link to Other FTMs page Link to Morgan Markets page

See the end pages of each individual note for analyst certification and important disclosures, including non-US analyst disclosures. J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Recommendation and Forecast Changes CapitaLand (Overweight), Singapore (Christopher Gee,

CFA) Markers for the next decade

CapitaMalls Asia (Overweight), Singapore (Joy Wang) At the heel of the hockey stick

Doosan Corp (Overweight), South Korea (Youna Kim)

Growth with value

Hyundai Mobis (Overweight), South Korea (Wan Sun Park)

4Q10 preview: surpassing OEMs' growth. Raise PT to W370,000

JSW Energy Ltd. (Neutral), India (Shilpa Krishnan) Higher fuel costs and execution delays result in earnings cut

LG Display (Overweight), South Korea (JJ Park) Cost-reduction efforts and earnings momentum to be key catalysts

Reliance Industries Ltd (Overweight), India (Pradeep

Mirchandani, CFA) Steady 3Q, but no clarity on E&P ramp-up

Strategy Market Strategy, Global (Adrian Mowat)

Herd Instinct: Key Emerging Markets and Developed Asia Fund Flow Weekly, 13 January – 19 January 2011

Market Strategy, TIPV Markets (Sriyan Pietersz) Vietnam Strategy Update: CP Congress sets stage for post-Tet signals on policy

Economics Economy, Malaysia (Matt Hildebrandt)

Looking for a tightening signal at BNM’s meeting Thursday

Results and Company Views Bank of Ayudhya (Overweight), TIPV Markets (Anne

Jirajariyavech) Results slightly below expected on lower non-NII: loan growth & NIM above expectation

Bangkok Bank (Neutral), TIPV Markets (Anne

Jirajariyavech) NP in-line; strong loan growth in Dec10

Bank of India (Overweight), India (Adarsh Parasrampuria)

Strong improvement in asset quality

China Railway Construction Corporation Limited (Overweight), China (Karen Li, CFA) Improved protection for minority shareholder may help shift focus back to fundamentals and attractive valuation - ALERT

Dish TV (Overweight), India (Princy Singh) Strong sub additions and ARPU expansion continue

HTC Corp (Overweight), Taiwan (Laura Chen) Set to take off

Hyundai Motor Company (Overweight), South Korea (Wan Sun Park) 4Q10 preview: mix improvement and strong equity method gain

ITC Limited (Overweight), India (Latika Chopra, CFA) Q3FY11 : strong quarter; encouraging cigarette volume growth trends

Mapletree Logistics Trust (Neutral), Singapore (Joy

Wang) FY10 results review - better growth

Neowiz Games Corp. (Overweight), South Korea (Sungmin Chang, CFA) Lawsuit result is slightly positive - ALERT

Punjab National Bank (Overweight), India (Adarsh

Parasrampuria) 3Q11: NII growth strong, but asset quality disappoints

State Bank of India (Neutral), India (Seshadri K Sen,

CFA) Cheap, but high NPLs persist

Suntec REIT (Neutral), Singapore (Joy Wang) FY10 results review - carrying least office leasing risk

WCT Berhad (Overweight), Malaysia (Hoy Kit Mak) Warrant exercise price fixed at M$2.75 - ALERT

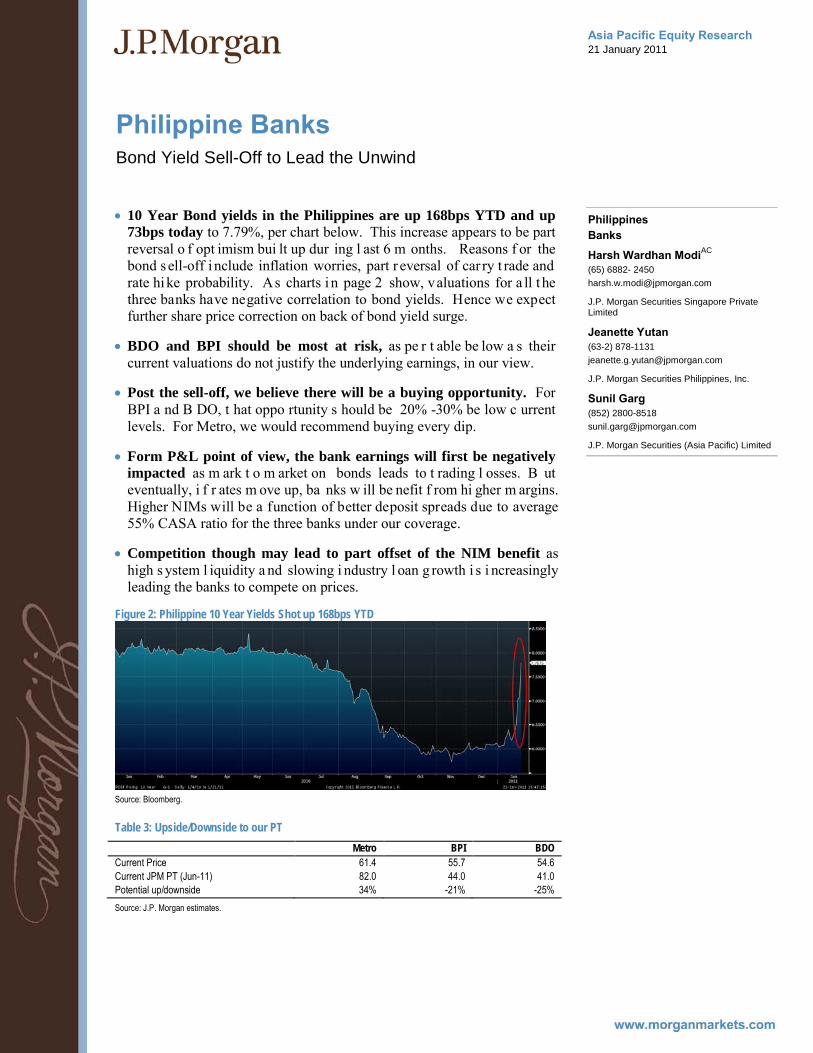

Sector Research Banks, TIPV Markets (Harsh Wardhan Modi)

Philippine Banks: Bond Yield Sell-Off to Lead the Unwind Conglomerates & Multi-industry, South Korea (Youna

Kim) Korea Holding Companies: Share price performance outlook and Valuation summary

Infrastructure, Asia Pacific (Karen Li, CFA) China tollroad sector: Limited impact from potential toll rate reform, and Class 2 government-funded highways turning toll free - ALERT

Integrated Oils, China (Brynjar Eirik Bustnes, CFA) China oil product marketing: China R&M margins strong in 4Q - Sinopec should benefit the most

Metals & Mining, India (Pinakin Parekh, CFA) The Lodestone: While scrap prices surge seems to be peaking out (for the time at least), HRC price surge continues

Mining, TIPV Markets (Stevanus Juanda) We view that export ban scare on low ranked coal is unfounded - ALERT

Asia Analyst Focus List Company Name Ticker Analyst Rating

Mkt. Cap (MM)

Mkt. Cap (US$ MM)

Focus List Add Date

Focus List Add Price

Close 01/20/11

Target Price

Date Target Price Set

Australia Campbell Brothers Limited (A$) CPB AU Alexander Mees, ACA OW 2697 2664 9-Sep-09 24.33 39.95 39.18 30-Nov-10 iiNet (A$) IIN AU Laurent Horrut OW 415 410 2-Aug-10 2.78 2.73 3.33 2-Aug-10 China Baoshan Iron & Steel – A (Rmb) 600019 CH Nathan M. Zibilich, CFA OW 114879 17443 12-Oct-10 7.11 6.56 10.00 12-Oct-10 China Cosco Holdings, Ltd. 1919 HK Corrine Png OW 114521 14705 11-Jan-11 8.63 9.04 11.80 29-Oct-10 China Minsheng Banking - A (Rmb) 600016 CH Samuel Chen OW 136009 20651 27-Nov-10 5.13 5.00 8.10 27-Nov-10 China Minsheng Banking - H (HK$) 1988 HK Samuel Chen OW 160825 20651 27-Nov-10 6.90 6.61 9.80 27-Nov-10 Industrial and Commercial Bank of China - A (Rmb) 601398 CH Samuel Chen OW 1538920 233665 30-Oct-09 4.95 4.22 6.70 27-Nov-10 Hong Kong AAC Acoustic (HK$) 2018 HK Charles Guo OW 24867 3193 8-Sep-09 6.91 20.25 22.00 2-Nov-10 China High Speed Transmission (HK$) 658 HK Boris Kan OW 16721 2147 6-May-10 18.42 12.16 24.30 6-May-10 China Unicom (Hong Kong) Limited (HK$) 762 HK Lucy Liu OW 290757 37335 2-Aug-10 10.22 12.34 12.90 1-Nov-10 Cosco Pacific (HK$) 1199 HK Karen Li OW 40510 5202 26-Aug-08 10.64 14.94 16.10 10-Nov-10 Geely Automobile Holdings Ltd. (HK$) 175 HK Frank Li OW 26340 3382 15-Oct-10 3.79 3.54 6.20 15-Oct-10 HSBC Holdings plc (HK$) 5 HK Sunil Garg OW 1529794 196437 24-May-10 71.65 86.40 115.00 22-Apr-10 K Wah International Holdings (HK$) 173 HK Amy Luk, CFA OW 8265 1061 13-Apr-10 2.98 3.24 3.80 25-Aug-10 Longfor Properties Co. Ltd. (HK$) 960 HK Ryan Li OW 63510 8155 18-Nov-10 9.44 12.32 13.50 18-Nov-10 Mongolian Mining Corporation (HK$) 975 HK Nathan M. Zibilich, CFA OW 38532 4948 15-Nov-10 8.68 10.40 11.45 9-Jan-11 Pacific Basin Shipping 2343 HK Corrine Png OW 9853 1265 11-Jan-11 5.01 5.10 7.00 3-Aug-10 Shenzhen Expressway H Share (HK$) 548 HK Karen Li, CFA OW 11306 1452 8-Sep-10 3.90 4.31 8.70 2-Dec-10 The United Laboratories (HK$) 3933 HK Leon Chik, CFA OW 16998 2183 5-Nov-10 15.52 13.06 24.00 7-Jan-11 Wheelock & Company Ltd (HK$) 20 HK Benjamin Lo, CFA OW 65832 8453 19-Nov-10 28.85 32.40 38.10 19-Nov-10 Zhejiang Expressway (HK$) 576 HK Karen Li, CFA OW 30966 3976 20-Apr-10 6.83 7.13 9.10 21-Nov-10 India Apollo Hospitals Enterprise Ltd. (Rs) APHS IN Princy Singh OW 59568 1306 5-Oct-10 463.15 477.65 575.00 5-Oct-10 Ballarpur Industries Ltd (Rs) BILT IN Princy Singh OW 22999 504 20-Oct-10 35.20 35.00 50.00 20-Oct-10 IndusInd Bank (Rs) IIB IN Seshadri K Sen, CFA OW 107989 2367 19-Nov-10 265.15 232.05 350.00 11-Oct-10 Sintex Industries Limited (Rs) SINT IN Princy Singh OW 42313 928 13-Jan-11 167.30 155.00 243.00 13-Jan-11 Spicejet Ltd (Rs) SJET IN Princy Singh OW 29253 641 2-Dec-10 82.15 72.25 115.00 2-Dec-10 Japan Canon (¥) 7751 JT Hisashi Moriyama OW 5415080 65372 14-Jan-11 4240.00 4060.00 5000.00 14-Jan-11 Dainippon Screen Mfg. (¥) 7735 JT Hisashi Moriyama OW 174480 2106 22-Jun-10 478.00 687.00 1000.00 17-Jan-11 FUJIFILM Holdings (¥) 4901 JT Hisashi Moriyama OW 1551597 18731 26-Jan-10 2942.00 3015.00 4500.00 28-May-10 Hitachi (¥) 6501 JT Yoshiharu Izumi OW 2006072 24218 29-Jul-09 293.00 444.00 590.00 23-Apr-10 Honda Motor (¥) 7267 JT Kohei Takahashi OW 5932428 71618 19-Jan-10 3370.00 3275.00 3600.00 22-Oct-10 Inpex Corporation (¥) 1605 JT Brynjar Eirik Bustnes OW 1818765 21957 1-Sep-10 389000.00 497500.00 630000.00 31-Aug-10 Nikon (¥) 7731 JT Hisashi Moriyama OW 736014 8885 4-Jan-11 1747.00 1836.00 2500.00 4-Jan-11 Malaysia RHB Capital (M$) RHBC MK Harsh Wardhan Modi OW 18305 5982 18-Nov-10 7.80 8.50 10.60 16-Nov-10 Philippines International Container Terminal Services, Inc. (Php) ICT PM Jeanette Yutan OW 81304 1828 8-Sep-10 35.20 42.00 49.00 20-Oct-10 Philippine Stock Exchange Inc (Php) PSE PM Harsh Wardhan Modi OW 11111 250 9-Oct-07 407.50 362.20 605.00 4-Oct-10 Singapore CapitaLand (S$) CAPL SP Christopher Gee OW 15516 12076 29-Sep-08 3.26 3.64 5.30 18-Jan-10 DBS Group (S$) DBS SP Harsh Wardhan Modi OW 34217 26632 8-Aug-08 14.36 14.82 24.00 19-Jan-11 Global Logistic Properties Ltd (S$) GLP SP Christopher Gee OW 9559 7440 18-Nov-10 2.18 2.08 2.90 18-Nov-10 Noble Group Ltd (S$) NOBL SP Ajay Mirchandani OW 13267 10326 12-Nov-09 1.83 2.20 2.50 10-Nov-10 Olam International (S$) OLAM SP Ajay Mirchandani OW 6613 5147 2-Oct-08 1.80 3.11 3.70 10-Aug-09 Singapore Airlines (S$) SIA SP Corrine Png OW 18033 14036 23-May-10 14.60 15.06 20.00 10-Nov-10 South Korea LG Chem Ltd (W) 051910 KS Samuel Lee, CFA OW 26409030 23555 14-Oct-10 327000.00 398500.00 430000.00 14-Oct-10 LG Display (W) 034220 KS JJ Park OW 13346530 11904 15-Mar-10 35900.00 37300.00 52000.00 12-Jan-11 LG Electronics (W) 066570.KS JJ Park OW 17647030 15740 15-Jan-11 114000.00 122000.00 150000.00 15-Jan-11 LG Innotek (W) 011070 KS Hyunjoon Roh OW 2576253 2298 23-Mar-10 115000.00 128000.00 240000.00 15-Jul-10 Samsung SDI (W) 006400 KS Hyunjoon Roh OW 7243776 6461 23-Jun-09 96100.00 159000.00 220000.00 28-Oct-10 SK Energy Co Ltd (W) 096770 KS Brynjar Eirik Bustnes OW 16874970 15051 5-Oct-07 147500.00 182500.00 165000.00 13-Sep-10 CJO Shopping (W) 035760 KS Jinah Lee OW 1540044 1374 11-Jan-11 250500.00 248800.00 277000.00 11-Jan-11 Taiwan First Financial Holding Co Ltd (NT$) 2892 TT Dexter Hsu OW 174551 6002 3-Sep-10 18.45 26.95 33.00 8-Jan-11 Formosa Chemicals and Fibre Corp (NT$) 1326 TT Samuel Lee, CFA OW 550838 18942 9-Dec-10 93.20 96.80 109.00 9-Dec-10 Novatek Microelectronics Corp (NT$) 3034 TT Cynthia Chou OW 56661 1948 3-Dec-10 98.50 95.10 120.00 3-Dec-10 Pegatron Corp (NT$) 4938 TT Gokul Hariharan OW 85855 2952 24-Aug-10 40.15 38.05 52.00 24-Aug-10 Powertech Technology Inc (NT$) 6239 TT Cynthia Chou OW 74756 2571 2-Aug-10 101.50 104.50 130.00 3-Aug-10 Quanta Computer Inc. (NT$) 2382 TT Alvin Kwock OW 237636 8172 13-Oct-10 48.05 62.00 68.00 29-Oct-10 TSMC (NT$) 2330 TT Rick Hsu OW 1932688 66461 19-Jan-11 78.00 74.60 88.00 7-Dec-10 Unimicron Technology Corp. (NT$) 3037 TT Christopher Ma OW 89750 3086 18-Apr-10 40.75 58.00 60.00 18-Apr-10 Thailand Banpu Public (Bt) BANPU TB Sukit Chawalitakul OW 213050 6943 15-Oct-10 724.00 784.00 906.00 15-Dec-10 PTT Public Company (Bt) PTT TB Sukit Chawalitakul OW 965825 31475 23-Mar-10 256.00 339.00 395.00 15-Sep-10 LPN Development(Bt) LPN TB Anne Jirajariyavech OW 12691 414 18-Jan-11 8.15 8.60 9.70 17-Jan-11 United States Focus Media (US$) FMCN Dick Wei OW 3393 3393 3-Jun-10 15.44 23.70 28.00 29-Sep-10

Source: Bloomberg, J.P. Morgan estimates. *Under applicable law and/or JPMorgan Chase & Co policy, all J.P. Morgan ratings and estimates for this company have been removed.

For details on the AFL methodology, please see the Asia Cash Equities page on mm.jpmorgan.com or contact your J.P. Morgan salesperson/the covering analyst. Your feedback can help us to make the FTM better. Please take a moment to tell us what you think. Click here to send comments Click here for the Blackberry version Click here to unsubscribe

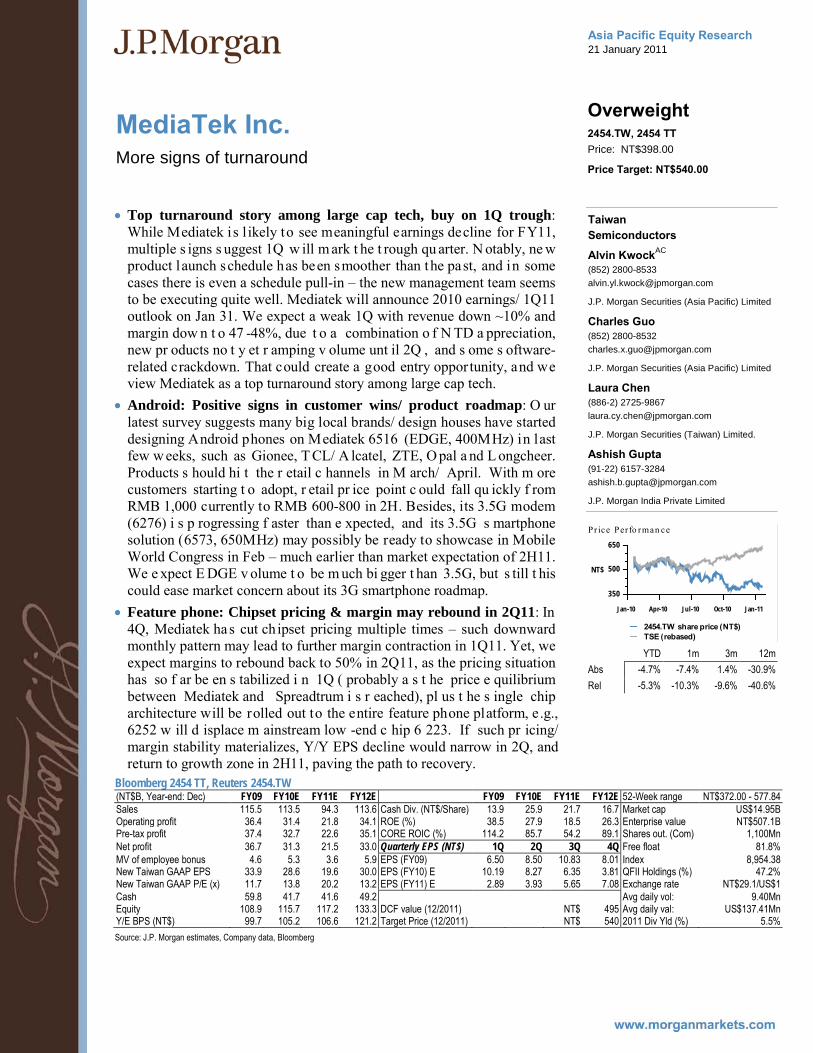

Asia Pacific Equity Research 21 January 2011

MediaTek Inc.

Overweight 2454.TW, 2454 TT

More signs of turnaround

Price: NT$398.00

Price Target: NT$540.00

Taiwan Semiconductors

Alvin KwockAC

(852) 2800-8533 [email protected]

J.P. Morgan Securities (Asia Pacific) Limited

Charles Guo (852) 2800-8532 [email protected]

J.P. Morgan Securities (Asia Pacific) Limited

Laura Chen (886-2) 2725-9867 [email protected]

J.P. Morgan Securities (Taiwan) Limited.

Ashish Gupta (91-22) 6157-3284 [email protected]

J.P. Morgan India Private Limited

350

500

650

NT$

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

2454.TW share price (NT$)TSE (rebased)

YTD 1m 3m 12m Abs -4.7% -7.4% 1.4% -30.9% Rel -5.3% -10.3% -9.6% -40.6%

• Top turnaround story among large cap tech, buy on 1Q trough: While Mediatek is l ikely to see meaningful earnings decline for FY11, multiple s igns s uggest 1Q w ill m ark t he t rough qu arter. N otably, ne w product launch schedule has been smoother than the past, and in some cases there is even a schedule pull-in – the new management team seems to be executing quite well. Mediatek will announce 2010 earnings/ 1Q11 outlook on Jan 31. We expect a weak 1Q with revenue down ~10% and margin dow n t o 47 -48%, due t o a combination o f N TD a ppreciation, new pr oducts no t y et r amping v olume unt il 2Q , and s ome s oftware-related crackdown. That could create a good entry opportunity, and we view Mediatek as a top turnaround story among large cap tech.

• Android: Positive signs in customer wins/ product roadmap: O ur latest survey suggests many big local brands/ design houses have started designing Android phones on Mediatek 6516 (EDGE, 400MHz) in last few w eeks, such as Gionee, T CL/ A lcatel, ZTE, O pal a nd L ongcheer. Products s hould hi t the r etail c hannels in M arch/ April. With m ore customers starting t o adopt, r etail pr ice point c ould fall qu ickly f rom RMB 1,000 currently to RMB 600-800 in 2H. Besides, its 3.5G modem (6276) i s p rogressing f aster than e xpected, and its 3.5G s martphone solution (6573, 650MHz) may possibly be ready to showcase in Mobile World Congress in Feb – much earlier than market expectation of 2H11. We e xpect E DGE v olume t o be m uch bi gger t han 3.5G, but s till t his could ease market concern about its 3G smartphone roadmap.

• Feature phone: Chipset pricing & margin may rebound in 2Q11: In 4Q, Mediatek has cut chipset pricing multiple times – such downward monthly pattern may lead to further margin contraction in 1Q11. Yet, we expect margins to rebound back to 50% in 2Q11, as the pricing situation has so f ar be en s tabilized i n 1Q ( probably a s t he price e quilibrium between Mediatek and Spreadtrum i s r eached), pl us t he s ingle chip architecture will be rolled out to the entire feature phone platform, e.g., 6252 w ill d isplace m ainstream low -end c hip 6 223. If such pr icing/ margin stability materializes, Y/Y EPS decline would narrow in 2Q, and return to growth zone in 2H11, paving the path to recovery.

Bloomberg 2454 TT, Reuters 2454.TW (NT$B, Year-end: Dec) FY09 FY10E FY11E FY12E FY09 FY10E FY11E FY12E 52-Week range NT$372.00 - 577.84 Sales 115.5 113.5 94.3 113.6 Cash Div. (NT$/Share) 13.9 25.9 21.7 16.7 Market cap US$14.95B Operating profit 36.4 31.4 21.8 34.1 ROE (%) 38.5 27.9 18.5 26.3 Enterprise value NT$507.1B Pre-tax profit 37.4 32.7 22.6 35.1 CORE ROIC (%) 114.2 85.7 54.2 89.1 Shares out. (Com) 1,100Mn Net profit 36.7 31.3 21.5 33.0 Quarterly EPS (NT$) 1Q 2Q 3Q 4Q Free float 81.8% MV of employee bonus 4.6 5.3 3.6 5.9 EPS (FY09) 6.50 8.50 10.83 8.01 Index 8,954.38 New Taiwan GAAP EPS 33.9 28.6 19.6 30.0 EPS (FY10) E 10.19 8.27 6.35 3.81 QFII Holdings (%) 47.2% New Taiwan GAAP P/E (x) 11.7 13.8 20.2 13.2 EPS (FY11) E 2.89 3.93 5.65 7.08 Exchange rate NT$29.1/US$1 Cash 59.8 41.7 41.6 49.2 Avg daily vol: 9.40Mn Equity 108.9 115.7 117.2 133.3 DCF value (12/2011) NT$ 495 Avg daily val: US$137.41Mn Y/E BPS (NT$) 99.7 105.2 106.6 121.2 Target Price (12/2011) NT$ 540 2011 Div Yld (%) 5.5% Source: J.P. Morgan estimates, Company data, Bloomberg

Asia Pacific Equity Research 21 January 2011

CapitaLand

Overweight CATL.SI, CAPL SP

Markers for the next decade ▼

Price: S$3.64

Price Target: S$4.60 Previous: S$5.30

Singapore Real Estate

Christopher Gee, CFAAC

(65) 6882-2345 [email protected]

Joy Wang (65) 6882-2312 [email protected]

J.P. Morgan Securities Singapore Private Limited

3.4

4.0

4.6S$

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

CATL.SI share price (S$)FTSTI (rebased)

YTD 1m 3m 12m Abs -3.2% -0.3% -8.5% -13.1% Rel -1.6% -1.7% -9.2% -24.8%

CapitaLand (Reuters: CATL.SI, Bloomberg: CAPL SP) S$ in mn, year-end Dec FY09A FY10E FY11E FY12E Revenue 2,957 3,490 3,839 4,223 Net Profit 1,053.0 1,233.8 1,420.0 1,360.1 EPS (S$) 0.26 0.29 0.33 0.32 DPS (S$) 0.069 0.065 0.065 0.065 EPS growth (%) -41.4% 10.8% 15.1% -4.2% ROE 8.7% 8.9% 9.4% 8.4% P/E (x) 13.9 12.5 10.9 11.4 BVPS (S$) 3.16 3.40 3.67 3.93 RNAV/Share 5.31 5.31 5.71 P/BV (x) 1.2 1.1 1.0 0.9 Dividend Yield 1.9% 1.8% 1.8% 1.8%

Shares O/S (mn) 4,263 Market cap (S$ mn) 15,516 Market cap ($ mn) 12,047 Price (S$) 3.64 Date Of Price 21 Jan 11 Free float (%) 60.0% 3-mth trading value (S$ mn) 106.9 3-mth trading value ($ mn) 83.0 3-mth trading volume (mn) 11.5 FTSTI 3,185 Exchange Rate 1.29 Fiscal Year End Dec

Source: Company data, Bloomberg, J.P. Morgan estimates.

• Conservative positioning at the end of an exceptional first ten years: Since 2000 when the group emerged from the merger of DBS Land and Pidemco Land, CapitaLand has evolved into a significant regional real estate developer differentiated by its breadth of exposure in Asia-Pacific as well as i ts real estate funds platform. However, due to an enlarged capital base the stock has underperformed its relevant benchmark indices in the past 18 months. We set out in this report what we believe are the major mi lestones for a r eversal o f t his sha re p rice p erformance t rend. We retain our Overweight rating on the stock, but remove the stock from our Asia Analyst Focus List.

• Higher base of comparison: Over 10 years the group’s managed assets have more than doubled (CAGR of 8.4%), whilst the aggregate market capitalization o f t he l isted e ntities w ithin t he g roup ha s e xpanded 4 x (15% CAGR). We estimate the group ROE will increase from the FY09 trough to above 9% in FY Dec 11E, and we have rolled over our SOTP valuation to FY 11E which is now at S$5.71/share (from S$5.35/share).

• The next moves in the next decade: Greater capital productivity at the business un it level, e specially in the m ajor s egments of r etail, commercial and serviced residences, as well as moving the capital base to t he g roup’s op timal gearing r ange of 50-70% (via acc retive investment or by way of capital reduction or both) would accelerate ROE growth. We estimate the group’s investment capacity at between S$5.1-8.8billion, 30-54% of the group’s market capitalization.

• New Dec 2011 target price of S$4.60/share, based on a historical average 19% discount to our end Dec 2011 SOTP valuation. Key risks to our target pr ice would be an i nability t o deploy the group's investment capacity into accretive investments and/or a prolonged failure to shift the group's capi tal base towards i ts optimal gearing range via active capital management.

Asia Pacific Equity Research 21 January 2011

CapitaMalls Asia

Overweight CMAL.SI, CMA SP

At the heel of the hockey stick ▲

Price: S$1.91

Price Target: S$2.75 Previous: S$2.60

Singapore Property

Joy WangAC

(65) 6882-2312 [email protected]

Christopher Gee, CFA (65) 6882-2345 [email protected]

J.P. Morgan Securities Singapore Private Limited

1.8

2.2

2.6

S$

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

CMAL.SI share price (S$)FTSTI (rebased)

YTD 1m 3m 12m Abs 0.0% 2.7% -13.2% -18.7% Rel 1.6% 1.3% -13.9% -30.4%

Unit data 52-week range S$1.83 - 2.41 Market cap (S$MM) 7,418 Market cap (US$MM) 5,777 Shares outstanding (MM) 3,884 Avg daily value (S$MM) 10.8 Avg daily value (US$MM) 8.4 Avg daily volume (shares) 5.5 STI 3,185 Exchange rate S$1.284/US$ Source: Bloomberg

• We reiterate our Overweight rating and raise our Dec-11 price target to S$2.75, based on our SOTP valuation. The stock has de-rated over the past six months, and is currently t rading at 1 .1x FY11E book and 11x FY11 r eported P /E. While we st ill see n ear-term he adwinds, w ith the stock trading at a 15% discount to our estimated tangible asset value and pricing in zero value for the group’s funds management business and for its platform, we see the current level as an attractive entry level and add CMA to our Asia Analyst Focus List.

• The earnings power of CMA's China portfolio – a ‘J’ curve: Given that the group’s China portfolio has not been contributing significantly, especially for those private funds, the market is of the view that earnings are likely to be weak for the next few years. We argue, however, based on our p roperty-by-property ana lysis, that t he group’s rental ear nings from China will more than double by 2012. This, together with the likely strong revaluation gains from China, would help the group to achieve a three-year earnings CAGR of 23%, on our estimates.

• Book value understates CMA’s underlying asset value, in our view. While the group revalues its investment assets on a semi-annual basis, the income approach adopted has resulted in a rather conservative book value, in our view. In addition, we estimate that more than S$1 billion worth of assets (on an effective stake basis) in China has yet to be carried on the group’s book, and most of the 2nd- and 3rd-tier city malls are still carried on the group’s book at cost.

• Key risks to our rating and price target: Our O verweight r ating is predicated on the v iew t hat C hina ope rations for the group will turn around i n the ne xt 12 -18 m onths. I n a ddition, t he g roup c ontinues t o carry sizable surplus capital, which could drag down the return on equity should management be unable to deploy it in time.

Reuters: CMAL.SI; Bloomberg: CMA SP S$ in millions, year-end December FY09 FY10E FY11E FY12E Sales 229 229 221 230 Reported profit 388 494 680 722 Reported EPS (S$) 0.10 0.13 0.18 0.19 Recurring EPS (S$) 0.05 0.08 0.06 0.08 DPS (S$) 0.01 0.01 0.01 0.01 ROE (%) 7 8 10 10 Recurring P/E (x) 35 23 32 25 Reported P/E (x) 19 15 11 10 BVPS (S$) 1.41 1.54 1.70 1.88 SOTP per share (S$) 2.60 2.75 2.93 P/B (x) 1.4 1.2 1.1 1.0 Div yield (%) 0.5 0.5 0.5 0.5 Source: Company data, J.P. Morgan estimates.

Asia Pacific Equity Research 21 January 2011

Doosan Corp Initiation

Overweight 000150.KS, 000150 KS

Growth with value

Price: W155,500

Price Target: W190,000

South Korea Conglomerates & Multi-industry

Youna KimAC

(82-2) 758-5715 [email protected]

Scott YH Seo (82-2) 758 5759 [email protected]

J.P. Morgan Securities (Far East) Ltd, Seoul Branch

80,000

120,000

160,000

W

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

000150.KS share price (W )KOSPI (rebased)

YTD 1m 3m 12m Abs -1.3% 0.3% 0.3% 32.3% Rel -1.3% -1.3% -10.1% 12.1%

• Initiating coverage with an OW rating and Jun-11 PT of W190,000, implying 22% ups ide potential f rom c urrent le vels. W e expe ct to see: (1) strong revenue growth in Doosan Corp’s own operations along with higher OPM; (2) an upw ard r evision in the market’s v aluation of DIP Holdings; and (3) better e quity method ga ins on s tronger e arnings v isibility of it s major subsidiary.

• Macro conditions and product mix changes support top-line growth and OPM expansion for operational divisions: Based on t he p ositive outlook for fixed i nvestment i n C hina and Korea, we forecast strong t op-line growth for Mottrol (17% of 2011 OP), as its sales are concentrated on three major dom estic c onstruction e quipment makers which ha ve large exposure to Korea a nd C hina, and di rect e xports to C hinese c onstruction equipment makers are increasing. For the electro-material di vision (23% 2011E OP) we expect increasing sales of high-end/higher operating margin CCL to support a divisional operating margin at historical highs.

• DIP Holdings is still undervalued: We estimate the value of DIP Holdings at about W 585B, or W200B higher t han Doosan C orp’s i nvested c apital when e stablishing D IP Holdings ( including W 110B of bor rowings). We think this value is underestimated by the market. If DIP Holdings and other PEFs w ere to de cide t o s ell t he unde rlying a ssets, w e t hink t he r esulting discussion on sale prices would give greater v isibility around the intrinsic value in DIP, and act as a catalyst for Doosan’s share price.

• Valuation and risks: Our pr ice t arget of W190,000 is ba sed on S OTP. Risks to our PT are: (1) softer-than-expected equity method gains from DHI; (2) lower-than-anticipated OP margins in Mottrol and Electro-material; and (3) potential concerns about DII’s and D IC’s a bility t o honor liabilities related to put-back options to FIs and balance sheet management.

Bloomberg: 000150 KS; Reuters: 000150 KS Won in billions, year-end December

FY08 FY09 FY10E FY11E FY12E Operating Profit 35 -38 310 346 457 52-week range W173,500-80,200 OP Growth (%) (61.7) (207.2) (915.2) 11.5 32.3 Market cap W4,057B Net Profit 110 232 245 289 394 Market cap US$3,618MM NP Growth (%) 215.3 111.7 5.3 18.0 36.3 Shares issued 25.MM EPS (Won) 4,428 9,386 9,802 11,530 15,721 Free float 34.4% P/E (x) 36.6 17.3 16.5 14.1 10.3 Fiscal Year End Dec BVPS (Won) 86,446 99,655 113,070 125,578 143,794 Price (W) 162,000 P/B (x) 1.9 1.6 1.4 1.3 1.1 Date of Price 20-Jan-11 DPS (Won) 1,000 2,500 2,500 2,500 2,500 Avg daily value W31.9B Dividend Yield (%) 0.6 1.5 1.5 1.5 1.5 Avg daily value US$28.4MM NAV per share (Won) 156,867 220,162 218,851 220,027 219,561 Avg daily volume 0.2MM shares P/NAV (x) 1.0 0.7 0.7 0.7 0.7 KOSPI 2,107 ROE (%) 9.7 13.7 12.6 13.2 15.9 Exchange Rate W1,121.2/US$ Source: Company reports, Bloomberg, J.P. Morgan estimates

Asia Pacific Equity Research 22 January 2011

LG Display

Overweight 034220.KS, 034220 KS

Cost-reduction efforts and earnings momentum to be key catalysts

Price: W37,300

Price Target: W52,000

South Korea Semiconductors

JJ ParkAC

(822) 758-5717 [email protected]

J.P. Morgan Securities (Far East) Ltd, Seoul Branch

Hyunjoon Roh (82-2) 758 5712 [email protected]

J.P. Morgan Securities (Far East) Ltd, Seoul Branch

Narci Chang (886-2) 2725-9899 [email protected]

J.P. Morgan Securities (Taiwan) Limited.

Justin J. Park (82-2) 758-5725 [email protected]

J.P. Morgan Securities (Far East) Ltd, Seoul Branch

30,000

40,000

50,000

W

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

034220.KS share price (W )KOSPI (rebased)

YTD 1m 3m 12m Abs -8.7% -5.1% -5.4% -11.0% Rel -8.7% -6.7% -15.8% -31.2%

• Focus on cost reduction in 2011: As we expected (see our 12 January 2011 report), LGE has announced aggressive initiatives to reduce costs from 1Q11 onw ards. C ompared w ith 2010 , when L GD e xperienced a Y/Y cost i ncrease, its cost reduction curve should return t o nor mal in 2011 due to a lower number of LED bars and falling component prices.

• Panel prices likely to hit bottom in mid-1Q11: Management expects TV panel prices to bottom out in February-March, and IT panel prices are already showing signs of stabilizing. Also, inventory across channels is at a normal level, except for LED TVs. This is in line with our view on the LCD market, although we now expect a meaningful recovery in LGD’s earnings to take place in 2Q11, rather than in 1Q11.

• Big promotion on FPR-based 3D TV: LGD sh owcased its F ilm Patterned Retarder (FPR) 3D TV during the analyst m eeting and criticized its existing Shutter Glass (SG) 3D TV, pointing at the flicker, cross-talk, bulky g lasses, and other ne gatives. W e came ba ck w ith a positive impression based on o ur own e xperience, and also positive feedback from major r etailers. LGD expects the g lobal 3D TV market sales to reach 30 million units (almost 15% of expected global total LCD TV sales) in 2011. LGD targets 70% of global 3D TV sales in 2011.

• Compelling valuation and earnings momentum: Due to the delay in panel price recovery, LGD’s stock has underperformed YTD. Although the c ompany is likely to post a nother loss i n 1Q 11, a ggressive cost reduction efforts a nd panel-demand r ecovery, along with panel p rice stabilization f rom 2Q 11, will dr ive s trong e arnings momentum, in our view. T he s tock i s currently t rading a t 1. 1x F Y11E book a nd 0.9 x FY12E book , with a double-digit R OE. H ence, w e r ecommend that investors ac cumulate the s tock. We m aintain our P /BV-based Dec-11 price target of W52,000, which is based on a mid-cycle valuation.

Reuters: 034220.KS; Bloomberg: 034220 KS W B, YE Dec. FY09 FY10 FY11E FY12E ADR Sales 20,038 25,511 26,317 27,917 52-week range W48,100-32,600 Reuters LPL.N Operating profit 1,010 1,310 1,488 2,018 Market cap W13,347B Bloomberg LPL US Net profit 1,153 1,116 1,361 1,778 Market cap US$11,873MM 52-wk range US$ 21.59~13.75 EPS (KRW) 3,222 3,119 3,804 4,968 Shares 358MM Ratio 1:2 Cash 3,362 3,271 1,062 1,697 Free Float 56% Avg daily vol. 985,754 ROE (%) 11.8 10.5 11.6 13.4 Avg daily value W103.5B Cur. premium 0.8% P/E (x) 11.6 12.0 9.8 7.5 Avg daily value US$92.MM BPS (KRW) 28,551 30,802 34,605 39,573 Avg daily vol. 2.6MM shares EV/EBITDA (x) 3.4 3.1 3.0 2.4 Index KOSPI 2,069.92 Div yield (%) 2% 2% 2% 2% Exchange rate W1,124/US$1 Quarterly EPS (KRW) 1Q 2Q 3Q 4Q Date of price 21-Jan-11 EPS (FY10) 1,813 1,429 627 -749 Price target W52,000 EPS (FY11)E -257 1,030 1,592 1,439 Consensus PT W47,000 EPS (FY12)E 1,099 1,122 1,662 1,086 Difference 11%

Source: Company reports, Bloomberg, J.P. Morgan estimates. Share price is as of 21 January, 2011.

Asia Pacific Equity Research 23 January 2011

Hyundai Mobis

Overweight 012330.KS, 012330 KS

4Q10 preview: surpassing OEMs' growth. Raise PT to W370,000 ▲

Price: W283,500

Price Target: W370,000 Previous: W350,000

South Korea Auto Parts

Wan Sun ParkAC

(82-2) 758-5722 [email protected]

Gon Suk Lee (82-2) 758 5710 [email protected]

J.P. Morgan Securities (Far East) Ltd, Seoul Branch

100,000

200,000

300,000

W

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

012330.KS share price (W )KOSPI (rebased)

YTD 1m 3m 12m Abs -3.7% -2.2% 11.8% 86.5% Rel -3.7% -3.8% 1.4% 66.3%

Bloomberg JPMA WPARK <GO>

• We expe ct strong 4Q 10 e arnings with revenue to c ome i n at W3.7T (+16% YoY; +13% QoQ), OP at W487B (+39% YoY; +12% QoQ), and NP at W695B (+46% YoY; +15% QoQ). Despite production disruption at H MC, increasing hi gh v alue a dded pa rts sales to ne w m odels o f KIA/HMC, stable A/S revenue and equity method gains will likely bring one of the strongest YoY and QoQ growths in auto/parts sector.

• We raised 2011-2012 top-line by 2~4% and NP by 4~9%, by revisiting A/S a nd m anufacturing business g rowth a nd m argins. We b elieve recently a nnounced business pl an, e specially pa rent r evenue of W14T, looks conservative, as c ompany ha s t rack r ecord of beating targeted annual business guidance. Revenue g uidance for 2010E w as W11.7T vs. JPMe of W13.7T.

• A/S revenue growth (11% CAGR in 2010E-2012E) will be quite stable, supported by strong increase in UIO of HMC and KIA globally. Also, 2011 will see addition of 3 warehouses in Italy, Russia, and US, which will be positive for expanding overseas A/S business. We assume 24% OPM for A/S business for 2011-2012.

• Module/component revenue will be growing broadly in-line, but slightly higher than HMC and KIA’s global production at 12% CAGR. Mobis started Russia module plant from Jan and will also ramp up Brazil plant in 2012E.

• We ex pect overall margin t o improve steadily on r ising C KD pa rt to HMC and KIA’s new overseas p lants and e xisting production s ites to meet capacity increase. We assume module margin of 4% and core parts margin of 6%.

• Our new Dec-11 PT of W370,000 (reflecting 2011 NP increase of 4%) is based on a PER multiple of 12x. Key r isks to our view and PT include (1) HMC/KIA production f luctuations ( +/-); ( 2) e xecution r isk of ne w manufacturing facilities (-); and (3) cash re-investment risk (-).

Hyundai Mobis (Bloomberg: 012330 KS; Reuters: 012330.KS) Won in billions, year-end December FY09A FY10E FY11E FY12E Sales (W Bn) 10,633 13,735 15,215 16,845 52-week range W318,000-140,500 Net profit (W Bn) 1,615 2,527 2,933 3,306 Market cap W27,597B EPS (W) 18,843 26,521 30,782 34,702 Market cap US$24,550MM Sales growth (%) 13.4 29.2 10.8 10.7 Shares issued 97.3MM EPS growth (%) 47.8 40.7 16.1 12.7 Price (W) 283,500 ROCE (%) 24.0 22.2 18.5 16.7 Avg daily value 40,565.00 ROE (%) 24.5 28.4 25.8 23.0 Avg daily value W84.4B P/E (x) 14.4 10.2 8.8 7.8 Avg daily volume US$75.1MM P/B (x) 3.0 2.6 2.0 1.6 KOSPI 0.3MM shares EV/EBITDA (x) 16.1 11.8 11.5 9.9 Exchange Rate 2,069.9 Source: Bloomberg, J.P. Morgan estimates. Price as of Jan 21, 2011.

Asia Pacific Equity Research 21 January 2011

JSW Energy Ltd.

Neutral JSWE.BO, JSW IN

Higher fuel costs and execution delays result in earnings cut ▼

Price: Rs88.20

Price Target: Rs93.00 Previous: Rs116.00

India Electric Utilities

Shilpa KrishnanAC

(91-22) 6157-3580 [email protected]

Sumit Kishore (91-22) 6157-3581 [email protected]

Deepika Belani (91-22) 6157-3582 [email protected]

J.P. Morgan India Private Limited

80

110

140

Rs

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

JSW E.BO share price (Rs)NIFTY (rebased)

YTD 1m 3m 12m Abs -11.6% -9.9% -27.9% -19.5% Rel -4.4% -5.9% -23.4% -28.9%

JSW Energy Ltd. (Reuters: JSWE.BO, Bloomberg: JSW IN) Rs in mn, year-end Mar FY10A FY11E FY12E FY13E Revenue 23,551 40,000 72,710 71,408 Adjusted Profit 7,455 8,329 13,716 14,252 EPS (Rs) 5.16 5.08 8.36 8.69 Revenue growth (%) 28.3% 69.8% 81.8% -1.8% Adjusted profit growth (%) (Rs) 169.4% 11.7% 64.7% 3.9% ROCE 10.7% 9.7% 14.9% 15.0% ROE 23.8% 16.3% 22.8% 20.0% P/E (x) 17.1 17.4 10.5 10.1 P/BV (x) 3.0 2.7 2.2 1.9 EV/EBITDA (x) 17.8 14.6 8.4 7.1

Shares O/S (mn) 1,640 Market cap (Rs mn) 144,653 Market cap ($ mn) 3,177 Price (Rs) 88.20 Date Of Price 20 Jan 11 Free float (%) 23.3% 3mth Avg daily volume (mn) 1.73 3M - Average daily Value (Rs mn) 182.32 Average 3m Daily Turnover ($ mn) 4.00 NIFTY 5,712 Exchange Rate 45.54 Fiscal Year End Mar

Source: Company data, Bloomberg, J.P. Morgan estimates.

• Dec-q weak, as expected. 3Q adjusted PAT of Rs1.8B (down 1% qoq) was broadly i n-line w ith our estimate (Rs1.74B) a nd 2 0% be low c onsensus. Reported PLFs were broadly in line with our estimates based on CEA data: 1) Vijaynagar (860MW) - 94% PLF up 300bps qoq; 2) Ratnagiri (300MW) - 73%, impacted by t eething issues, lower de mand; and 3) Barmer (2x135MW) - 61.5%, equipment br eakdown and fuel transportation logistics. Despite i ncrease i n operating capacity, EBITDA margins declined by ~550bps qoq: 1) ST r ealizations of Rs4.87/kwh i n 3 Q vs Rs4.65/kwh in 2Q , but be low our e stimate of R s5; 2) h igher l anded fuel cost/unit of Rs2.7/kwh (or implied ~US$140/MT for 6,100Kcal/kg coal).

• Exposure to spot coal prices erodes profitability. We de lay commissioning of Barmer (Rajasthan SEB to be averse on buying expensive power a nd on logistical is sues on coal tr ansportation) and R atnagiri (shortage of sand procurement) and assume a 3-4 month buffer in estimates. Also on a ccount of i ncreased c oal c osts, we r educe o ur FY11 and F Y12 estimates by 32% and 25%, respectively. At the analyst meet, management conceded to a 15% qoq increase in coal cost for the Mar-q. Increasing coal prices c ontinue to hur t bot tom l ine a s although captive c oal f rom S outh Africa is expected t o c ome through in F Y12, quantity i s m inimal ( 1MT). Whereas linkage coal for Barmer (on regulated returns) remains elusive and land acquisition for the J alipa ligni te mine s is a c hallenge. Management expects lignite production from Kaprudi to commence in 4QFY11.

• We reduce our Mar-12 SOTP-based price target to Rs93 from Rs116 earlier; maintain Neutral. The stock has underperformed Sensex by ~24% over the la st 3 months, and over the same pe riod, benchmark coal pr ices have increased ~15%. B ased on the nascent stage of development of the captive mine associated with the West Bengal project (Rs1,620MW) and the initial execution thrust for only 300MW, we reduce the value for the project to Rs3/share from Rs20.5/share earlier. Our SOTP valuation includes Rs80.4 for ope rational/under-construction pr ojects a nd Rs3.5/share for pi peline projects. At 8.4x FY12E EV/EBITDA, t he s tock i s a t a di scount t o ot her IPPs, which is warranted in our view due to poor pipeline visibility and fuel price risks. Higher-than-expected merchant prices or PLFs are upside risks.

Asia Pacific Equity Research 22 January 2011

Reliance Industries Ltd

Overweight RELI.BO, RIL IN

Steady 3Q, but no clarity on E&P ramp-up ▼

Price: Rs986.80

Price Target: Rs1,240.00 Previous: Rs1,260.00

India Integrated Oils

Pradeep Mirchandani, CFAAC

(91-22) 6157-3591 [email protected]

Neil Gupte (91-22) 6157 3592 [email protected]

J.P. Morgan India Private Limited

900

1,050

1,200Rs

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

RELI.BO share price (Rs)BSE30 (rebased)

YTD 1m 3m 12m Abs -6.5% -8.0% -8.8% -6.4% Rel 1.1% -2.8% -2.6% -17.9%

Reliance Industries Ltd (Reuters: RELI.BO, Bloomberg: RIL IN) Rs in mn, year-end Mar FY09A FY10A FY11E FY12E FY13E Revenue 1,512,245 2,037,400 2,561,487 2,609,727 2,682,566 Net Profit 152,492.6 158,180.0 218,872.3 244,952.9 312,046.2 EPS (Rs) 48.46 48.14 66.62 74.55 94.97 DPS (Rs) 6.03 7.00 10.00 10.00 11.00 Revenue growth (%) 13.3% 34.7% 25.7% 1.9% 2.8% EPS growth (%) -7.7% -0.6% 38.4% 11.9% 27.4% ROCE 13.3% 11.3% 13.0% 12.6% 14.3% ROE 18.9% 14.6% 17.0% 16.6% 18.2% P/E (x) 20.4 20.5 14.8 13.2 10.4 P/BV (x) 3.2 2.7 2.4 2.0 EV/EBITDA (x) 13.9 10.7 8.4 7.2 5.5 Dividend Yield 0.6% 0.7% 1.0% 1.0% 1.1%

Shares O/S (mn) 3,273 Market cap (Rs mn) 3,229,691 Market cap ($ mn) 70,928 Price (Rs) 986.80 Date Of Price 21 Jan 11 Free float (%) 50.2% 3mth Avg daily volume 5,388,555.00 3M - Average daily Value (Rs mn) 5,616.96 Average 3m Daily Turnover ($ mn) 123.35 BSE30 19,008 Exchange Rate 45.54 Fiscal Year End Mar

Source: Company data, Bloomberg, J.P. Morgan estimates.

• Steady 3Q, but no clarity on E&P ramp-up: RIL’s 3QFY11 ne t profits of Rs51.4bn came in line with our expectations. While operating performance on Refining and Petrochemicals w as v ery st rong, E&P business continues to lag, even as there is no clarity on gas ramp-up.

• Refining – strong quarter, with more to follow: RIL ha d an exceptionally strong refining quarter, with GRMs of US$9/bbl (ahead of our expectation of US$8.8/bbl). RIL continues to be positive on refining outlook w ith strong de mand g rowth east o f t he S uez and s upport f or diesel sp reads due t o ch anges i n sp ecs f or off-road diesel i n Europe. Complex refiners will continue to benefit on low OPEC compliance and a weak outlook for fuel oil, in RIL’s view.

• Petrochemicals: record quarter: P olymer spreads h ave he ld steady despite the large capacity additions in 2010 (8% cap add). With limited capacity a dditions on the hor izon, w e expect t he polymer c ycle t o bottom b y mid-2011. Polyester m argins w ere st rong acr oss t he ch ain, which benefited integrated producers l ike RIL. With high cotton prices likely to sustain, we believe, polyester outlook for FY12 is positive.

• E&P stays the dark horse: KGD6 volumes are currently averaging 52-55mmscmd. RIL did not indicate timelines for ramp-up, saying it was in talks w ith the g overnment/DGH on a g amut of i ssues r elated to i ts domestic E&P portfolio, including technical and regulatory issues. With no g uidance on E &P r amp up, w e are r educing our FY12 g as sa les estimates.

• Stock reflects E&P disappointment, not positive refining and petchem outlook: We reduce our FY11/FY12 EPS estimates by 4%/5% primarily to reflect lower gas production, and adjust our PT to Rs1240. We reiterate ou r O W on RIL. E ven bui lding i n a slower r amp-up i n E&P, three-year earnings CAGR is 25% and we think valuations a re undemanding a t 12x FY12E adj. P/E. K ey risk: Weak er economic recovery will hurt refining, petchem cycles.

Emerging Markets Equity Research 21 January 2011

Herd Instinct

Key Emerging Markets and Developed Asia Fund Flow Weekly, 13 January - 19 January 2011

Emerging Market Equity Strategy

Adrian MowatAC

(852) 2800-8599 [email protected]

J.P. Morgan Securities (Asia Pacific) Limited

Ben Laidler (1-212) 622-5252 [email protected]

J.P. Morgan Securities LLC

David Aserkoff, CFA (44-20) 7325-1775 [email protected]

J.P. Morgan Securities Ltd.

Deanne Gordon (27-21) 712-0875 [email protected]

J.P. Morgan Equities Ltd.

Rajiv Batra (91-22) 6157-3568 [email protected]

J.P. Morgan India Private Limited

Sanaya Tavaria (91-22) 6157-3312 [email protected]

J.P. Morgan India Private Limited

Faheem S Desai (91-22) 6157-3329 [email protected]

J.P. Morgan India Private Limited

During the week to 19 January, there were net inflows into all emerging market equity funds except BRIC equity. The net flows by mandate were: Total EM equity funds US$1.8billion subscription. GEMS

equity funds US$1.2billion subscription. EMEA equity funds US$715million subscription. LatAm equity funds US$172million redemption. Asia ex Japan equity funds US$75million subscription. BRIC equity funds US$82million redemption. US equity funds US$6.8billion subscription. US bond market US$3.8billion subscription. US money market US$32.8billion redemption. Net foreign buying/selling activity: Japan inflows of US$3.6billion. Outflows from all emerging markets except South Africa and Taiwan: Taiwan US$1.1billion inflows South Africa US$171million inflows Brazil US$211million outflows Thailand US$201million outflows India US$197million outflows For countries that do not publish official foreign transactions in their equity markets, we use the monthly data from EPFR Global (they cover 12,000 international, EM and US funds with total net assets greater than US$ 6 trillion). During the month of November, funds were net buyers in Australia, Singapore, China, Malaysia, Mexico, Russia, and Poland. Funds were net sellers in Hong Kong, Chile and Turkey. Please see page 13 for global portfolio weightings and household equity weights. Also see page 14 for the consensus overweight and underweight markets for November 2010.

Table 1: Market data & net foreign investment, 13 January – 19 January 2011 Index Net MTD 2011 2010 12M chg Flows YTD Agg. Avg. (%) US$M US$M US$M US$M (x).

Stock Exchange Investors' Trading Data Japan (1 wk lag) 0.3 3616 6719 6719 37974 1.9 South Africa -0.8 171 534 534 4825 0.9 Brazil** 0.6 -211 1341 1341 3600 -0.6 Taiwan 1.6 1113 2331 2331 8689 1.5 Korea 1.3 -50 736 736 18595 -0.1 India -2.7 -197 -718 -718 28711 -0.4 Thailand 2. 0 -201 -574 -574 1923 -1.1 Indonesia -1.0 -7 -425 -425 2331 -0.1 Philippines -0.1 -30 -74 -74 1231 -0.9 Monthly Tracking of Cross Border Funds (November)* # Australia -2. 0 298 - - 356 0.8 Singapore 0.4 280 - - -120 1.7 Hong Kong 1.8 -208 - - -719 -0.7 China -2.2 647 - - 2827 0.7 Malaysia -1.6 184 - - 390 1.1 Mexico 2.9 172 - - -815 1.1 Russia 1. 6 427 - - 641 1.2 Chile 0.7 -65 - - -255 -0.6 Poland -1.9 85 - - 710 0.8 Turkey -5.3 -128 - - 661 -1.3 Regional & US Mutual Fund Flows Total EM Equity**** -0.2 1764 - 6733 84112 0.8 Global EM Equity* -0.2 1229 - 3550 55045 0.9 LatAm Equity* -1.6 -172 - 904 1842 -1.0 EMEA Equity* -0.6 715 - 1434 6567 3.2 Asia ex-Japan Equity* 0.6 75 - 1267 19609 0.1 BRIC Equity* -1.0 -82 - -422 1049 -1.4 Japan Equity Funds 2.2 455 - 928 -840 2.1 Developed Europe* 2.1 961 - 595 -10256 1.3 International Equity* 1.4 1452 - 5628 6500 1.5 US Equity*** -0.3 6758 - 21635 33467 1.5 US Bond*** 3.4 3789 - 10687 149347 1.2 US Money Market*** 0.2 -32825 - -42000 -395262 -1.8

Source: Bloomberg, J.P. Morgan, I:Net, MKK, Lipper FMI, MSCI, Datastream. *EPFR Global data. **Data for Brazil is from 12 January – 18 January 2011. # 2010 Agg. figures are up to November 2010 only. ***Data from Lipper FMI. BRIC Funds separated from EM Funds from 11 May 07. The final column is designed to show the scale of net subscriptions or redemptions - the calculation is if net inflows (This weeks net subscription/(average of weeks with net subscriptions)( or if net redemptions /(This weeks net redemptions/(average of weeks with net redemptions)). ****Total EM Equity includes Global EM, LatAm, EMEA, Asia ex Japan and BRIC equity funds.

Asia Pacific Equity Research 21 January 2011

Vietnam Strategy Update

CP Congress sets stage for post-Tet signals on policy

Vietnam Market strategy

Sriyan PieterszAC (662) 684 2670 [email protected]

JPMorgan Securities (Thailand) Limited

Adrian Mowat (852) 2800-8599 [email protected]

J.P. Morgan Securities (Asia Pacific) Limited

Figure 1: VNINDEX Index

0200400600800

100012001400

2006 2007 2008 2009 2010

Source: Bloomberg.

• No surprises at the CPV Congress. The Party Congress which ended this week a nnounced the pol itical leadership a t the pa rty level for t he next five-year cy cle. The three k ey appointments, those of P rime Mi nister (PM), President, and Party Secretary General have been confirmed, with former National Assembly Chairman Nguyen Phu Trong being e lected party S ecretary G eneral, while P M N guyen Tan D ung ha s r eceived a second term and Truong Tan Sang was appointed President.

• The l eadership annou ncements ar e s een as positive be cause: 1) t hey clear up uncertainty over t he political succession a nd allow the government to get back to addressing the economy; and 2) Mr. Dung's re-appointment as PM is viewed as constructive (despite his association with/support f or th e S OEs), given his r eformist cr edentials and the expectation that he will provide continuity.

• First task of the new government will be macroeconomic stability. With a y oung popul ation a nd l ow s tandard of living, the g overnment understandably maintains a policy bias toward strong growth. However, this bias, at times, comes at the expense of economic stability. Given the inflation a nd B oP c oncerns, w e expect the g overnment t o tighten monetary conditions more aggressively after Tet New Year.

• Stock m arket ne eds pol icy confirmation. While t he m acro stability backdrop is u ndeniably w eak, we be lieve the m arket is focusing on macro and policy de velopments as a ( positive) inflection po int. We would look at several catalysts for entry into the stock market, including:1) A peak in inflation, which will benefit from more favorable base c omparisons in March/April 11; 2) F urther currency de valuation (most likely post-Lunar New Year); and 3) More overt policy signals on a shift toward stability (such as further interest rate hikes).

Table 1: Vietnam Market Statistics 2011YTD HOSE HASTC

Index 519.50 (+7.2%) 107.87 (-5.6%) Daily T/O (US$MM) 50.374 25.74 Market cap (US$B) 32.687 6.171 Number of stocks 279 373 2010 Market P/E 11.81 6.92 Exchange (VND/US$) 19498 O/N interbank (%) 7.2

Source: Bloomberg.

Asia Pacific Equity Research 21 January 2011

Bank of Ayudhya

Overweight BAY.BK, BAY TB

Results slightly below expected on lower non-NII: loan growth & NIM above expectation

Price: Bt25.75

Price Target: Bt30.00

Thailand Banks

Anne JirajariyavechAC (66-2) 684-2684 [email protected]

JPMorgan Securities (Thailand) Limited

Sunil Garg (852) 2800-8518 [email protected]

J.P. Morgan Securities (Asia Pacific) Limited

18

24

30

Bt

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Price Performance

BAY.BK share price (Bt)SET (rebased)

YTD 1m 3m 12mAbs 1. 0% 9.6% 4.3% 26.8%Rel 2. 9% 8.0% 0.9% -12.9%

Company data52 Wk Range 28.25-18.00Market cap (Bt mn) 162,483Market cap (USD MM) 5,334Share O/S (MM) 6,074Free Float (%) 67.1Ave. daily volume (MM) 50.1Ave. daily Value (Bt MM) 585Exchange rate 30.46Index 1, 025Year-end DecSource: Bloomberg. Price date 20 Jan 2011

• BAY’s NP came in at Bt8.8 billion for FY10 growing 32% Y/Y. This was 4% lower than our expectation due to lower-than-expected fee income and slightly higher opex. BAY’s NP for 4Q10 was Bt2.3 billion (+32% Y/Y, -3% Q/Q).

• Strong loan growth (similar to other banks), +6% Q/Q and +8% for FY10. NIM expanded 17bp Q/Q to 5.14%, driven by 17bp Q/Q reduction in funding cost.

• Non-NII dropped 5% Y/Y and -21% Q/Q, weaker than peers. We have to touch base with the bank on what drives the lower non-NII. Opex grew 35% Y/Y and 19%, partly due to more marketing and promotion expenses.

• Asset quality improved substantially with NPLs declined 20% Q/Q to Bt23 billion or 3.6% of loans (from 5.7% at YE09). Coverage ratio strengthened to 88% (from 72% at YE09). Credit cost was relatively flat at 193bp.

• We maintain our forecast and expect strong EPS growth of 28% in FY11E driven by revenue growth and credit cost reduction.

• We maintain OW rating on BAY with Dec11 PT at Bt30 based on DDM approach with 15.0% ROE, 12.0% COE, and 8.0% growth. Risks are rising competition in second hand car lending and auto cash as well as funding cost pressure in the rising interest rate environment.

Bank of Ayudhya earnings results summary (Bloomberg: BAY TB Reuters:BAY.BK) Earnings revision and valuation Bt millions (per sh. data in Bt) 4Q10 4Q09 Y/Y 3Q10 Q/Q 2011E 2012ELoan growth 6.3% 8.3% -1.2% Old EPS (Bt) 1.9 2.5 NIM 5. 14% 4.65% 49 4.96% 17 New EPS (Bt) 1.9 2.5 Credit cost 1.93% 2.08% (15) 1.96% (3) % change 0% 0%Non-NII 2, 643 2,779 -5% 3,323 -20% P/E (x) 13.9 10.6 PPOP 4, 258 4,869 -13% 5,826 -27% ROE (%) 11.5% 13.9%Net profit 2,261 1, 708 32% 2,331 -3% P/B (x) 1.5 1.4 EPS 0.4 0.3 32% 0.4 -3% Dec11 PT 30 Source: Company, J.P. Morgan estimates.

Asia Pacific Equity Research 21 January 2011

Bangkok Bank

Neutral BBLf.BK, BBL TB

NP in-line; strong loan growth in Dec10

Price: Bt164.00

Price Target: Bt165.00

Thailand Banks

Anne JirajariyavechAC (66-2) 684-2684 [email protected]

JPMorgan Securities (Thailand) Limited

Sunil Garg (852) 2800-8518 [email protected]

J.P. Morgan Securities (Asia Pacific) Limited

25,000

40,000

55,000

Rp

Jul-09 Oct-09 Jan-10 Apr-10 Jul-10

Pr ice Per fo rman ce

ASII.JK share price (Rp)JCI (rebased)

YTD 1m 3m 12m Abs 5.3% 8.1% 9.9% 233.8% Rel 4.1% 9.9% 6.8% 138.4%

Company data 52 Wk Range 169.50-105.00 Market cap (Bt mn) 311,141 Market cap (USD MM) 10,215 Share O/S (MM) 1,909 Free Float (%) 97.8 Ave. daily volume (MM) 5.1 Ave. daily Value (Bt MM) 456 Exchange rate 30.46 Index 1,025 Year-end Dec Source: Bloomberg. Price date 20 January 2011

• BBL’s NP came in at Bt24.6 billion, in-line with our expectation, +20% Y/Y. The bank’s 4Q10 NP at Bt5.6 billion dropped 5% Y/Y and 9% Q /Q. PPOP a t B t9.4 billion for 4Q 10 w as 13 % h igher Q /Q bu t dropped 4% Q/Q due to seasonality in opex (+14% Q/Q).

• Strong loan growth achieved in Dec10. BBL recorded F Y10 l oan growth of 9.9%. In 4Q10 alone loan g rowth was very s trong a t 7.7%. This w as dr iven by bot h seasonal w orking cap ital d emand as w ell a s long-waited corporate term loan demand. This was hugely above market expectation (growth consensus around 4-5% for FY10).

• Flat NIM. As l oan growth came just in Dec10, it h as yet t o generate significant i nterest i ncome. This ha s an impact on NIM w hich was a t 2.99% for the quarter, flat Q/Q. Loan yield was up 11bp due to interest rate hi ke. F unding c ost, however, w ent up by 13bp w ith r ising s hort-term borrowing cost. LDR edged higher to 90% from 84% a year ago. This remains lower than peers but BBL always prefers having low LDR.

• Non-NII growth continued to lag its peers. Total op. Non-NII g rew 7% Y/Y and Q/Q (FY10 grew 5%). Fee income a lone grew 10% Y/Y and 4% Q /Q ( +8% f or F Y10). This i s st ill c onsidered lagged performance. This is due to the bank’s lower exposure in the retail area.

• NPL declined to 3.0% (from 4.4% YE09) with coverage ratio very high at 160% (from 117% at YE09).

• Early adoption of TAS 19 (employee be nefit) resulting i n approximately Bt4 bi llion decrease in shareholders’ equity. There i s no significant P&L impact. Tier 1 capital ratio remains strong at 12.5%.

• We will revisit our forecast given the s tronger-than-expected l oan growth.

• We maintain Neutral on BBL with Dec11 PT at Bt165 which is based on D DM a pproach w ith 1 3.4% R OE, 12.0% C OE, a nd 7.0% g rowth. Risks are weaker than expected loan growth. On the upside, risk is higher than expected working capital ahead of rising interest rate.

Bangkok Bank earnings results summary (Bloomberg: BBL TB; Reuters: BBL.BK) Earnings revision and valuation Bt millions (per sh. data in Bt) 4Q10 4Q09 Y/Y 3Q10 Q/Q 2011E 2012E Loan growth 7.7% 3.9% -0.5% Old EPS (Bt) 13.0 14.7 NIM 2.99% 2.93% 6 3.00% (1) New EPS (Bt) 13.0 14.7 Credit cost 0.57% 0.56% 1 0.58% (2) % change 0% 0% Non-NII 5,774 5,374 7% 5,393 7% P/E (x) 12.5 11.1 PPOP 9,434 8,344 13% 9,827 -4% ROE (%) 11.3% 11.9% Net profit 5,649 5,917 -5% 6,174 -8% P/B (x) 1.4 1.3 EPS 3.0 3.1 -5% 3.2 -8% Dec11 PT 165 Source: Company, J.P. Morgan estimates.

Asia Pacific Equity Research 22 January 2011

Bank of India

Overweight BOI.BO, BOI IN

Strong improvement in asset quality

Price: Rs432.55

Price Target: Rs590.00

India Banks

Adarsh ParasrampuriaAC

(91-22) 6157-3576 [email protected]

J.P. Morgan India Private Limited

Seshadri K Sen, CFA (91-22) 6157-3575 [email protected]

J.P. Morgan India Private Limited

Sunil Garg (852) 2800-8518 [email protected]

J.P. Morgan Securities (Asia Pacific) Limited

300

450

600

Rs

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

BOI.BO share price (Rs)BSE30 (rebased)

YTD 1m 3m 12m Abs 2.1% 2.2% -16.3% 35.6% Rel 9.7% 7.4% -10.1% 24.1%

Bank of India (Reuters: BOI.BO, Bloomberg: BOI IN) Year-end Mar (Rs in mn) FY09A FY10A FY11E FY12E FY13E Operating Profit 47,107 41,112 55,290 63,064 75,704 Net Profit 30,073 17,411 27,323 34,478 42,029 Cash EPS (Rs) 57.14 33.11 51.95 65.56 79.92 Fully Diluted EPS (Rs) 42.96 21.82 48.15 60.80 75.16 DPS (Rs) 8.00 7.00 7.79 9.83 11.99 EPS growth (%) 49.5% (42.1%) 56.9% 26.2% 21.9% ROE 29.2% 14.2% 19.6% 20.9% 21.4% P/E 8.1 13.9 8.9 7.0 5.8 BVPS (Rs) 223.90 243.41 286.25 340.30 406.19 P/BV 2.1 1.9 1.6 1.4 1.1 Div. Yield 1.7% 1.5% 1.7% 2.1% 2.6%

52-wk range (Rs) 589.00 - 308.85 Market cap (Rs mn) 227,165 Market cap ($ mn) 4,989 Shares outstanding (mn) 525 Fiscal Year End Mar Price (Rs) 432.55 Date Of Price 20 Jan 11 Avg daily value (Rs mn) 163.1 Avg daily value ($ mn) 3.6 Avg daily vol (mn) 0.2 BSE30 19,008 Exchange Rate 45.54

Source: Company data, Bloomberg, J.P. Morgan estimates.

• Strong 3Q FY11: Bank of India reported net profit of Rs6.5B, up 61% y/y. Profits were marginally lower than our estimates as provisions were affected by a one -off de rivative loss of Rs2.0B. Asset quality improvement was strong, although the recent ou tperformance has reduced the valuation gap with peers.

• Good improvement in asset quality: Gross NPAs fell in 3Q given the large upg rade, bu t ov erall a sset qua lity i mproved a lso be cause o f significantly lower gross slippages at <1.0% vs 1.6% in 1H FY11. As a result, c redit c osts de creased t o ~ 70bp from ~ 1.0% in 1H FY11 a nd provision c overage i mproved by ~500bp. Management e xpects t he positive asset quality momentum to continue.

• Margin surprises: BOI’s N II i ncreased 12% q /q, with m argins improving t o 3.09% , up ~28bp q/q, given the l ow ba se i mpact a s margins in 2Q FY11 were af fected by a one-off. The ~ 30bp margin improvement w as m uch b etter t han expected, but we exp ect margin pressure over the next 2-3 quarters given the increase in funding costs.

• Some concerns: (1) The p ension liability (Rs40-45B), though not y et finalized, is higher than expected. (2)>20% growth with current tier-1 at ~8.5% could lead to dilution over the medium term. (3) Management’s increasing focus on SME/Agri/Retail to improve yields cou ld lead to asset quality risks over the medium term.

• Maintain Overweight: Our upgrade on BOI was based on a revival in asset qu ality and r elatively at tractive v aluations. Asset q uality improvement was indeed strong in 3Q, which should help profitability. With the recent ou tperformance, the valuation gap w ith P NB/BOB has narrowed to ~10%. However, our Sep-11 price target of Rs590 for BOI still implies considerable absolute upside. We maintain our Overweight rating on BOI.

Asia Pacific Equity Research 23 January 2011

China Railway Construction Corporation Limited

Overweight 1186.HK, 1186 HK

Improved protection for minority shareholder may help shift focus back to fundamentals and attractive valuation - ALERT

Price: HK$9.72

21 January 2011

Infrastructure

Karen Li, CFAAC

(852) 2800-8589 [email protected]

J.P. Morgan Securities (Asia Pacific) Limited

Other key takeaways from the call 1) Railway investments are expected to stay at high levels, with an annual capex no less than Rmb700 billion (for civil works only) in 2011-2015, based on recent remarks by key government officials; 2) CRCC is confident in achieving a 40~45% share in railway new orders; 2) CRCC’s new contracts received during 2010 exceeded the annual target set previously. 3) Management expects limited impact on margin from the rising raw material costs given most of the contracts have cost-plus formulas; in some contracts, it is customers which are responsible for procurement o raw materials. 4) CRCC and its consortium is bidding for the high speed railway project in the US, although the bid is not yet finalized.

Trading of CRCC’s A share and H- share was suspended from Jan. 20. We participated in the analyst conference call at 10 am hosted by the company on Jan. 22 (Saturday). CRCC's trading will resume on Jan. 24. Key takeaway from the call: • Transferring the Mecca Light Rail Project back to the parent,

reducing the loss to Rmb1.385 billion at most, with the difference against the provision made reflected through the balance sheet (Table 1 for details related to the loss and compensation).

1) All obligations related to the Mecca project has been transferred back to the parent, with Oct. 31 2010 as the cut off date.

2) Furthermore, CRCC will receive cash compensation in an amount of Rmb2.077 bi llion from t he pa rent to be pa id i n s everal installments with full settlements no later than mid-2014.

3) Against the write-off i t h as a lready m ade L TD i n a n a mount of Rmb4.1 bi llion ( of w hich Rmb0.294 bi llion w as boo ked i n 2009 and Rmb3.854 billion in 2010), CRCC’s loss would be reduced to a maximum of Rm1.385 billion, while a w rite-back on t he difference of R mb2.763 bi llion ( including t he cash compensation of Rmb2.077 billion to be received from the parent and a reversal on the es timated future loss o f R mb0.686 bi llion pr eviously booked) will be reflected through the balance sheet (accounted for as "capital surplus").

4) Meanwhile, C RCC i s e ntitled t o first c laim of a ny f uture compensation obtained from the Mecca project as an offset against the remaining loss of Rmb1.385 billion;

5) CRCC is also entitled to any compensation exceeding the parent’s payment of R mb2.077 bi llion and t he s ubsequent loss (if a ny), which will be reflected through the income statement as a gain.

• Minority shareholders’ interest should be better protected now through the proposed arrangement for the Mecca project, while CRCC ensures it has exercised more stringent risk control in executing its overseas contracts: Trading i s e xpected t o r esume on Jan.24. The ne ws should com e down as a pos itive in our v iew, particularly in light th at t he e ntire s ector ha s de -rated since end -Oct-2010, taking i nto account C RCC’s f allout i n S audi A rabia. More importantly, management at the analyst call ensured that it has exercised extra caution with overseas projects, with commercial interest as key consideration, which may reduce concerns that the companies are simply acting as government utility. Maintain OW on CRCC, CRG and CSR.

Asia Pacific Equity Research 21 January 2011

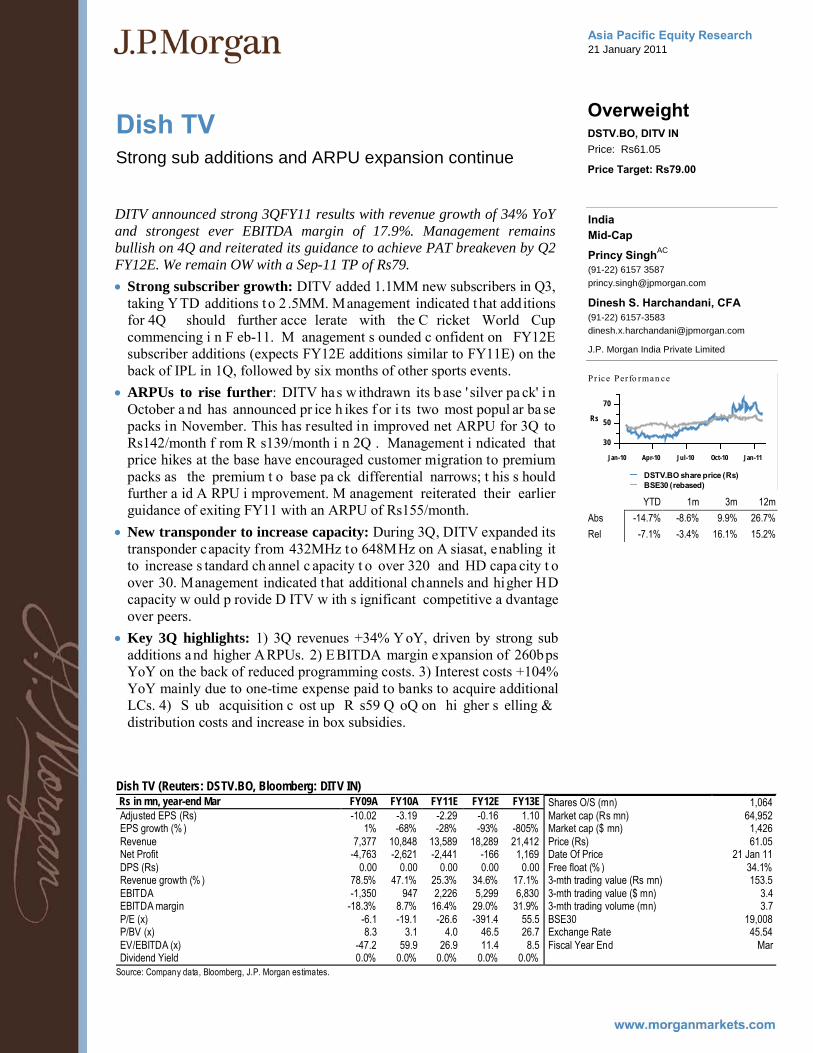

Dish TV

Overweight DSTV.BO, DITV IN

Strong sub additions and ARPU expansion continue

Price: Rs61.05

Price Target: Rs79.00

India Mid-Cap

Princy SinghAC

(91-22) 6157 3587 [email protected]

Dinesh S. Harchandani, CFA (91-22) 6157-3583 [email protected]

J.P. Morgan India Private Limited

30

50

70

Rs

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

DSTV.BO share price (Rs)BSE30 (rebased)

YTD 1m 3m 12m Abs -14.7% -8.6% 9.9% 26.7% Rel -7.1% -3.4% 16.1% 15.2%

Dish TV (Reuters: DSTV.BO, Bloomberg: DITV IN) Rs in mn, year-end Mar FY09A FY10A FY11E FY12E FY13E Adjusted EPS (Rs) -10.02 -3.19 -2.29 -0.16 1.10 EPS growth (% ) 1% -68% -28% -93% -805% Revenue 7,377 10,848 13,589 18,289 21,412 Net Profit -4,763 -2,621 -2,441 -166 1,169 DPS (Rs) 0.00 0.00 0.00 0.00 0.00 Revenue growth (% ) 78.5% 47.1% 25.3% 34.6% 17.1% EBITDA -1,350 947 2,226 5,299 6,830 EBITDA margin -18.3% 8.7% 16.4% 29.0% 31.9% P/E (x) -6.1 -19.1 -26.6 -391.4 55.5 P/BV (x) 8.3 3.1 4.0 46.5 26.7 EV/EBITDA (x) -47.2 59.9 26.9 11.4 8.5 Dividend Yield 0.0% 0.0% 0.0% 0.0% 0.0%

Shares O/S (mn) 1,064 Market cap (Rs mn) 64,952 Market cap ($ mn) 1,426 Price (Rs) 61.05 Date Of Price 21 Jan 11 Free float (% ) 34.1% 3-mth trading value (Rs mn) 153.5 3-mth trading value ($ mn) 3.4 3-mth trading volume (mn) 3.7 BSE30 19,008 Exchange Rate 45.54 Fiscal Year End Mar

Source: Company data, Bloomberg, J.P. Morgan estimates.

DITV announced strong 3QFY11 results with revenue growth of 34% YoY and strongest ever EBITDA margin of 17.9%. Management remains bullish on 4Q and reiterated its guidance to achieve PAT breakeven by Q2 FY12E. We remain OW with a Sep-11 TP of Rs79. • Strong subscriber growth: DITV added 1.1MM new subscribers in Q3,

taking YTD additions t o 2 .5MM. Management indicated t hat additions for 4Q should further acce lerate with the C ricket World Cup commencing i n F eb-11. M anagement s ounded c onfident on FY12E subscriber additions (expects FY12E additions similar to FY11E) on the back of IPL in 1Q, followed by six months of other sports events.

• ARPUs to rise further: DITV has w ithdrawn its b ase ' silver pa ck' i n October a nd has announced pr ice h ikes f or i ts two most popul ar ba se packs in November. This has resulted in improved net ARPU for 3Q to Rs142/month f rom R s139/month i n 2Q . Management i ndicated that price hikes at the base have encouraged customer migration to premium packs as the premium t o base pa ck differential narrows; t his s hould further a id A RPU i mprovement. M anagement reiterated their earlier guidance of exiting FY11 with an ARPU of Rs155/month.

• New transponder to increase capacity: During 3Q, DITV expanded its transponder capacity f rom 432MHz to 648MHz on A siasat, enabling it to increase s tandard ch annel c apacity t o over 320 and HD capa city t o over 30. Management indicated that additional channels and higher HD capacity w ould p rovide D ITV w ith s ignificant competitive a dvantage over peers.

• Key 3Q highlights: 1) 3Q revenues +34% YoY, driven by strong sub additions and higher ARPUs. 2) EBITDA margin expansion of 260bps YoY on the back of reduced programming costs. 3) Interest costs +104% YoY mainly due to one-time expense paid to banks to acquire additional LCs. 4) S ub acquisition c ost up R s59 Q oQ on hi gher s elling & distribution costs and increase in box subsidies.

Asia Pacific Equity Research 21 January 2011

HTC Corp

Overweight 2498.TW, 2498 TT

Set to take off

Price: NT$888.00

Price Target: NT$1,100.00

Taiwan Technology

Laura ChenAC

(886-2) 2725-9867 [email protected]

J.P. Morgan Securities (Taiwan) Limited.

Alvin Kwock (852) 2800-8533 [email protected]

J.P. Morgan Securities (Asia Pacific) Limited

Ashish Gupta (91-22) 6157-3284 [email protected]

J.P. Morgan India Private Limited

200

500

800NT$

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

2498.TW share price (NT$)TSE (rebased)

YTD 1m 3m 12m Abs -3.6% 1.1% 28.3% 141.0% Rel -2.8% -0.3% 18.2% 130.8%

• Guidance inline, we see upside potential. HTC hos ted i ts a nalyst meeting t oday. The management guided 8.5m uni ts s hipment i n 1Q 11 (down 7 % Q oQ) w ith s ales o f N T$9.4bn ( down 10 % Q oQ). Due t o increased higher-end product shipments, they expect gross margin to be substantial at 29-30%. OPEX ratio is guided to be 14-15%, also in line with our e stimate of 14.8 %. Due to the strong demand i n i ts existing product and new product kicking off in late 1Q, we see upside potential to its 1Q shipment/sales.

• 4G and dual core product help to sustain ASP and margin. During 4Q10, H TC s aw 6% A SP i ncrease on the ba ck of i ts s trong hi gh-end product de mand, such as Desire H D, Desire Z and Desire. Thanks t o Verizon, AT&T and Sprint’s push on 4G service, we expect 4G product (including L TE, W imax a nd H SPA+) t o c ontribute 15 -20% of H TC’s 2011 s ales. I n a ddition, t he c ompany w ill i ntroduce its f irst du al c ore product c alled “Pyramid" in e arly 2Q . T his m odel will b e w ith 4.3” touch s creen, 1080p full HD a nd HDMI s upport. We e xpect to see i ts ASP to trend up with stable margin outlook.

• Enter “the 3rd branding phase” Management is bul lish on smartphone industry growth and is set to accelerate its branding business with b etter i nventory/component m anagement, c hannel/capacity expansion and brand preference. We expect HTC will further gain share cross the region and see more upside from both Europe and Asia.

• Strong earnings growth with attractive valuation; Overweight. We stay pos itive on H TC a nd e xpect t he c ompany to r egister s trong sales/earnings growth with plenty of new product launches in late 1Q11. HTC is trading at 11x FY11 EPS with almost 70% earning growth on our estimates, we r emain Overweight w ith Dec-11 P T N T$1,100 ba sed on 14x/12x FY11E/12E earnings. Key r isks to our PT include a decline in smartphone demand, and higher margin/ASP pressure from competition.

. Table 1: 1Q11 comparison NT$ millions 1Q11 (JPM) Consensus 1Q11 Guidance Comments Net Sales 103,674 86,999 NT$94 bn, 147% YoY Gross Profit 31,362 25,740 Operating profit (EBIT) 16,065 13,392 New Taiwan GAAP Net Profit 14,255 12,881 New TW GAAP EPS 17.43 13.1 Shipments (mn units) 10.0 8.5 mn units, 157% YoY Margins (%) Gross Margin 30.25 29.59 29.5±0.5 Operating margin 15.50 15.39 Opex Ratio of 14.5±0.5 New Taiwan GAAP Net margin 13.75 14.81

Source: Company reports, Bloomberg and J.P. Morgan estimates.

Asia Pacific Equity Research 23 January 2011

Hyundai Motor Company

Overweight 005380.KS, 005380 KS

4Q10 preview: mix improvement and strong equity method gain

Price: W185,500

Price Target: W210,000

South Korea Automobile Manufacture

Wan Sun ParkAC

(82-2) 758-5722 [email protected]

Gon Suk Lee (82-2) 758 5710 [email protected]

J.P. Morgan Securities (Far East) Ltd, Seoul Branch

80,000

140,000

200,000

W

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

005380.KS share price (W )KOSPI (rebased)

YTD 1m 3m 12m Abs 4.8% 4.5% 14.2% 70.2% Rel 4.8% 2.9% 3.8% 50.0%

Bloomberg JPMA WPARK <GO>

• We expect HMC’s 4Q10 result likely to be a record high one despite production disruption in U lsan p lant. We ex pect r evenue to c ome in at W9.7T ( +0.6% YoY; + 9.7% Qo Q), OP at W877B ( +4.5% Y oY; + 16.4% Q oQ), a nd N P at W1.4T (+49.8% YoY; +4.8% QoQ). (1) Production decline to impact top-line. Production disruption in Ulsan plant will lead to 5% YoY decline in 4Q Korea plant shipment to 455,052 units (+8% QoQ). (2) Mix improvement to support profit. However, we estimate 4Q10 revenue and OP to rise slightly by 1% and 5% YoY, r espectively, du e t o i mproved mix. % of a bove m id-sized v ehicles which rose to 53% of the Korea plant shipment, an increase from 49% in 4Q09 and 50% i n 3Q 10. We noted that domestic mix d eteriorated, b ut strong SUV export (Tucson and Santa Fe) lifted the mix, leading to OP margin expansion to 9% (vs. 8.7% in 4Q09 and 8.5% in 3Q10). (3) Strong NP boosted by equity method income. We ex pect n et eq uity i ncome o f W 800B, + 54% YoY, o n contributions from KIA and China/US subsidiaries.

• Short-term share price expectations. W e ex pect January’s s easonally weak retail sales in US a nd China, inert M/S mo vement could lead t o jitters in the share price. Since Jan 14 of record high share price (W200,500 or 9.4x 2011 PER), share price has declined 8%, with valuation falling to 8.7x vs. 9.7x by global peers. We expect share price rebound towards latter half of the 1Q11 as (1) s trong new model l aunchings i n Korea will l ead to e xpansion i n domestic market share; (2) Two o ut o f top 3 volume seller o f HMC in US, i .e. Avante and Accent, will be selling from end January; (3) competitors launch schedules and earnings recovery are going to be still quiet during 1Q11.

• Concerns for 2011. However, (1) We co ntinue t o s ee H MC’s o perating leverage pe aking ou t with over 100% u tilization. ( 2) S uperiority i n Y oY earnings growth i s al so f ading co mpared t o g lobal p eers ( table 4). We n otice competitors are just beginning to enjoy operating leverage and resuming model cycles. In expectations of changing global OEM production growth dynamics in 2H11 and onwards, we reiterate our p reference for selective auto parts makers and tires. Our top picks are Mando and Hankook Tire. We maintain OW and PT of W210,000 (June-2011) for HMC, which is based on 10x 2011E EPS. Risks include US/Europe market volatilities; sharp fluctuations in F/X rates.

Hyundai Motor: (Reuters: 005380.KS; Bloomberg: 005380 KS) Won in billions, year-end December

FY09A FY10E FY11E FY12E Sales (W Bn) 31,859 36,544 39,572 42,444 52-week range W203,000-104,000 Net profit (W Bn) 2,962 5,296 5,816 6,325 Market cap W40,861B EPS (W) 10,890 19,476 21,387 23,257 Market cap US$36,350MM Sales growth (%) -1.0% 14.7% 8.3% 7.3% Shares issued 220.3MM EPS growth (%) 104.5% 78.8% 9.8% 8.7% Free float 62.9% ROE (%) 15.6% 23.3% 20.7% 18.7% Avg daily value W164.B ROCE (%) 14.6% 18.4% 15.8% 14.1% Avg daily value US$145.9MM P/E (x) 17.0 9.5 8.7 8.0 Avg daily volume 0.9MM shares P/B (x) 1.8 1.4 1.2 1.0 KOSPI 2,069.9 EV/EBITDA (x) 9.8 7.6 7.0 6.2 Exchange Rate W1,124.1/US$ Source: Bloomberg, J.P. Morgan estimates. Price as of Jan 21, 2011

Asia Pacific Equity Research 21 January 2011

ITC Limited

Overweight ITC.BO, ITC IN

Q3FY11 : strong quarter; encouraging cigarette volume growth trends

Price: Rs169.00

Price Target: Rs190.00

India Tobacco

Latika Chopra, CFAAC

(91-22) 6157-3584 [email protected]

J.P. Morgan India Private Limited

110

140

170

Rs

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

ITC.BO share price (Rs)NIFTY (rebased)

YTD 1m 3m 12m Abs -3.4% 1.0% -3.1% 38.2% Rel 3.5% 5.0% 1.4% 26.1%

• Q3FY11 earnings 5% above estimates: Net s ales, EBITDA, and P AT grew 19%, 19%, and 2 1% y /y, respectively. H igher-than-estimated cigarette, agri and other FMCG business revenues led to sales coming in 4% above our e xpectations. However, EBITDA wa s in line w ith our expectations as l ower ( than estimated) margins f or c igarette and paper business of fset margin ga ins f or a gri a nd hot el bus iness. H igher ot her income ( supported t o s ome e xtent by s ale of s ome i nvestments) l ed t o higher PAT growth.

• Cigarette vol growth trends are encouraging with revenues rising 18.4% y/y and we estimate volume growth contributing 2-3% to the same (vs. c-2% vol growth during 1HFY11). However, margins were marginally weak (-30bp y/y) during Q 3FY11. Importantly, product m ix c hanges r emain encouraging and r ecent pr ice hikes unde rtaken by the c ompany should be positive f or margins i n c oming qua rters. Lower pr ocurement c osts f or tobacco (c-10% y/y) should further support FY12 margins.

• Non-tobacco business: A mixed bag: Agri bus iness pos ted impressive performance driven by higher trading of coffee & soya and better margins for leaf tobacco. While revenue growth for Other FMCG was healthy, losses increased sequentially due to expenses on new launches (noodles, skin care) and firm input costs. Hotel division reported modest recovery with improved ARRs (+8-10% y/y) and higher occupancy levels (65-68%). Paper business performance w as s ubdued due t o one -off pi peline c orrection i n v iew of uncertainty related to change in pictorial warning for cigarette packaging.

• Tobacco and taxes: Over the next few days there will probably be a debate on the extent of excise duty hikes l ikely on c igarettes, particularly against the backdrop of a strained fiscal situation. As demand trends are healthy, we believe the industry can absorb an excise duty hike of up to 10% (implying price hi ke of 4 -6%) w ithout i mpacting de mand m eaningfully. A t c onstant prices, the current sensitivity to earnings of excise duty is 1%.

• Maintain OW: We expect ITC to deliver EPS CAGR of 18% over FY10-13E. I t i s our preferred pi ck in consumer s taples sector and in the current volatile market, should do relatively better.

Bloomberg: ITC IN; Reuters: ITC.BO Rs mn, year end Mar FY09 FY10 FY11E FY12E FY13E Net sales 156,119 181,532 212,304 248,820 289,756 52-week range (Rs) 112-185 Net profit 32,636 40,610 49,231 58,383 67,509 Market cap (Rs B) 1298 EPS (Rs) 4.3 5.3 6.4 7.6 8.8 Market cap (US$ B) 28.5 DPS (Rs) 1.9 5.0 3.0 3.5 4.5 Shrs outsting (MM) 7683 Net sales growth (%) 12% 16% 17% 17% 16% Free float (%) 68 Net profit growth (%) 5% 24% 21% 19% 16% Avg daily value (Rs MM) 1197 EPS growth (%) 5% 23% 21% 19% 16% Avg daily value (US$ MM) 26.3 ROE (%) 24% 29% 34% 33% 33% Avg dly volume (MM shs) 7.9 P/E (x) 39.1 31.8 26.3 22.1 19.2 Exchange rate (Rs/US$) 45.6 EV/EBITDA (x) 24.5 19.2 16.0 13.2 11.3 BSE sensex 19008 Dividend yield 1.1% 2.9% 1.7% 2.0% 2.6%

Source: Bloomberg, Company reports and J.P. Morgan estimates.

Asia Pacific Equity Research 23 January 2011

Mapletree Logistics Trust

Neutral MAPL.SI, MLT SP

FY10 results review - better growth

Price: S$1.00

Price Target: S$1.00

Singapore REITs

Joy WangAC

(65) 6882-2312 [email protected]

Christopher Gee, CFA (65) 6882-2345 [email protected]

J.P. Morgan Securities Singapore Private Limited

0.70

0.85S$

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11

Pr ice Per fo rman ce

MAPL.SI share price (S$)FTSTI (rebased)

YTD 1m 3m 12m Abs 3.6% 5.3% 9.9% 25.9% Rel 5.2% 3.9% 9.2% 14.2%