april 2011 - icici prudential life insurance · avaya global connect, ... and expansion in...

TRANSCRIPT

April 2011

Sustained leadership in life insurance

2

Agenda

2

Industry overview and outlook

ICICI Prudential: Strategic elements

Performance snapshot

3

Agenda

3

Industry overview and outlook

ICICI Prudential: Strategic elements

Performance snapshot

Evolution of industry since liberalisation

Total premium (USD bn)

Penetration (as a % to

GDP)

New business

premium1

(USD bn)

Number of players

Insurance premium per

capita (USD)

FY 2010

23

11.96

57.70

~4.3%

~42

FY 2002

13

2.37

10.22

~2.0%

~9

21% CAGR

24% CAGR

1 Retail weighted premium

Source: IRDA, Swiss Re, market estimates

Exchange rate FY 2002 $1=INR 49

FY 2010 S1=INR 464

Industry: New business premium

YOY

Growth

17% 34% 92% 31% (10%)

Source: IRDA, weighted new business premiums for individual

business

5

17% (8%)

0

50

100

150

200

250

300

IN

R in

b

illio

ns

FY 2005 FY 2006 FY 2007 FY 2008 FY 2009 FY 2010 FY 2011

LIC Private

Industry: AUM

6

Source: Life insurance council

4.23

5.49

6.99

8.48

9.34

12.90

14.67

0

5

10

15

IN

R in

trillio

ns

FY 2005 FY 2006 FY 2007 FY 2008 FY 2009 FY 2010 9m 2011

18.9%

CAGR

12.3%

CAGR

12.0%

CAGR

1Net inflow into Insurance

Household savings

Insurance1

FY

2010

28

Financial savings

Nominal GDP

Growth opportunity

FY

2015E

50

540

248

2,388

FY

2000

5

424

12.0%

CAGR

1,355

Significant opportunity at current savings rate

7

13.2%

CAGR

89

45

12.1%

CAGR

12.0%

CAGR

12.0%

CAGR

306

141

USD bn

-20%

0%

20%

40%

60%

80%

100%

1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09

Currency & Deposits Life Insurance Fund Shares/ Debentures / MFS

Provident and Pension Fund Claims on Government

Increasing life insurance fund

8

Distribution of financial savings

12.1%

20.1%

Source: UN Population division

Favourable demographics

9

Target population expected to increase by over 500 mn

by 2050

38

31

23

18

19

19

16

13

37

42

49

49

6

8

12

20

0 20 40 60 80 100

1990

2010

2030

2050

Ye

ar

Percentage

Aged 0-14 Aged 15-24 Aged 25-60 Aged 60 and above

69%

50%

Agenda

10

Industry overview and outlook

ICICI Prudential: Strategic elements

Performance snapshot

11

Sustained leadership

Highest brand recall and consideration value

amongst private players1

Brand

5,000+ - No. of distribution touch points

176,076 - No. of advisors

50+ - Corporate tie ups & bancassurance

partners

Distribution2

1. Source: Millward Brown Quarterly Brand Track ‘ Oct 2010

2. As at March 31, 2011

Sustained private market leadership

INR 47.80 bn of capital infused till March 2011

Strong parentage: ICICI Bank & Prudential PLC

Strong team of around 13,000 professionals

Organisation

12

Sustained leadership (cont..)

Servicing tie up : Over 10,000 touch points

High customer convenience: Over 60%1

service transactions through electronic modes

Rated most customer responsive company2

Service

Products catering to all life cycle needsProduct

1. For FY 2011

2. Avaya Global Connect, 2005, 2007 & 2010

13

Strategy: Way forward

Profitable growth through efficiency and productivity

Need based sales pitch

Increased focus on Bancassurance

Distribution

Sales appropriately incentivised to encourage

persistency and long term savings

Proactive segmented customer communication

Persistency

Customer centric products

Lower charges and increased protection level

Balanced

product mix

Lower distribution payouts

Rationalisation of infrastructure

Variablisation of expenses

Expense

management

Automated service delivery architecture

Upsell to existing customersService

14

Agenda

14

Industry overview and outlook

ICICI Prudential: Strategic elements

Performance snapshot

APE (INR bn)

NBP margin2

Expense ratio1

Total premium (INR bn)

Asset under management (INR bn)

Profit after tax (INR bn)

Performance snapshot

15

FY 2010

53.45

19.0%

19.5%

165.32

573.18

2.58

FY 2011

39.75

17.9%

17.3%

178.81

681.50

8.08

1Expense ratio: All expenses (incl. commission) / (Total premium

– 90% of single premium)

2Traditional embedded value basis

Renewal premium (INR bn) 101.98 100.19

New business premium (INR bn) 63.34 78.62

Policies issued since inception

16

7.05

9.56

10.83

12.74

0

2

4

6

8

10

12

14

16

No

. in

m

illio

ns

FY 2008 FY 2009 FY 2010 FY 2011

92.36

193.42

166.50

161.38

192.19

381.00

248.25

433.25

0

100

200

300

400

500

600

700

IN

R in

b

illio

ns

March

2008

March

2009

March

2010

March

2011

Debt Equi ty

327.88

285.78

573.19

681.50

1717

Robust growth in assets held

Among the largest domestic fund managers

6.0%

7.4%

5.8%

6.8%

11.5%

13.4%

20.3%

23.2%

0%

5%

10%

15%

20%

25%

Preserver Protector Balancer Maximiser

Benchmark Fund

18

Superior fund performance

Inception Dates:

Preserver Fund: May 17, 2004 Protector Fund: April 2, 2002 Balancer Fund : April 2, 2002 Maximiser

Fund: November 16, 2001

Performance since inception as on March 31, 2011

1All funds in existence for over a year

Sharp decline in expense ratio

Total Expense ratio: All expenses (incl. commission) / (Total premium – 90% of single premium)

Expense ratio: All expenses (excl. commission and front line sales cost) / (Total premium – 90% of single

premium)

19

17.3%

19.5%

23.0%

8.2%9.1%

11.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

FY 2009 FY 2010 FY 2011

Total expense ratio Expense ratio

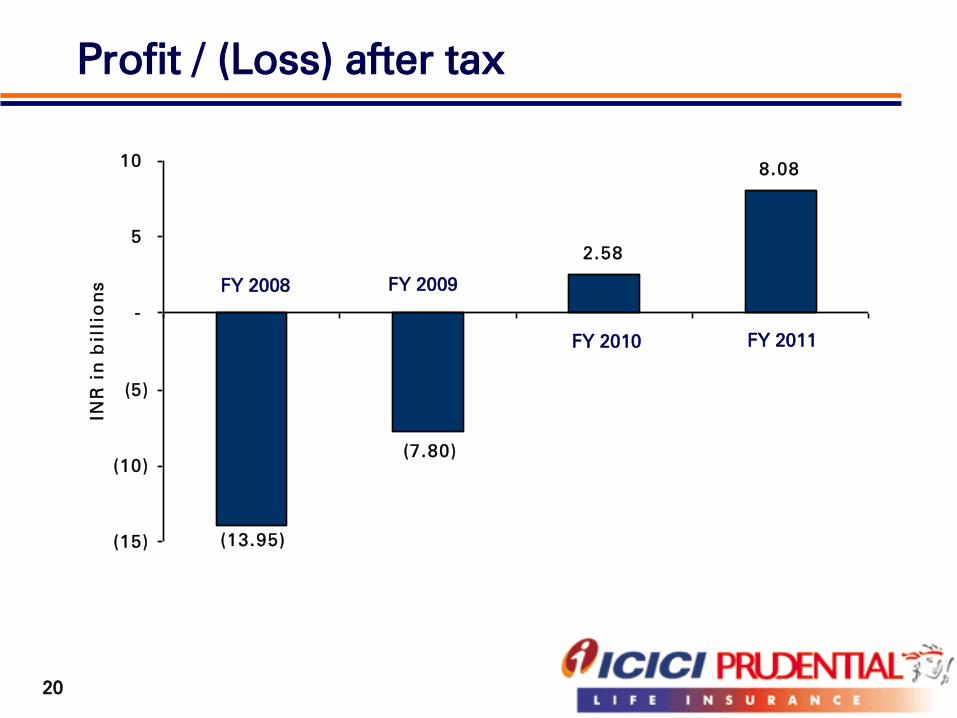

Profit / (Loss) after tax

20

FY 2008 FY 2009

FY 2010 FY 2011

(13.95)

(7.80)

2.58

8.08

(15)

(10)

(5)

-

5

10

IN

R in

b

illio

ns

2121

Summary of key achievements

Private market leader for 9 years in a row1

Asset under management2

of INR 681.50 bn

NBP margin of 17.9% in FY 2011

Over 12 million policies issued since inception

Decline in Expense ratio to 17.3% for FY 2011

APE of INR 39.75 bn in FY 2011

21

1 IRDA new business retail weighted premium basis

2AUM as on March 31, 2011

Profit after tax of INR 8.08 bn for FY 2011

Awards & Recognitions

The Most Trusted Brand

- ET Brand Equity Survey, 2008 & 2009

Runner-up Life Insurer

- Outlook Money & NDTV Profit, 2007, 2008 & 2009

Avaya Global Connect for Customer Responsiveness

- Avaya Global, 2005 & 2007

Best Business Partnership

- UK Trade & Investment India Business Awards, 2008

Excellence in Financial Reporting

- Institute of Chartered Accountants of India, 2008 & 2009

Life Insurance Company of the Year

- Asia Insurance Industry Awards, 2008

22

2323

Safe harbor

Except for the historical information contained herein, statements in this release which

contain words or phrases such as 'will', 'would', ‘indicating’, ‘expected to’ etc., and

similar expressions or variations of such expressions may constitute 'forward-looking

statements'. These forward-looking statements involve a number of risks, uncertainties

and other factors that could cause actual results to differ materially from those

suggested by the forward-looking statements. These risks and uncertainties include,

but are not limited to our ability to successfully implement our strategy, our growth

and expansion in business, the impact of any acquisitions, technological

implementation and changes, the actual growth in demand for insurance products and

services, investment income, cash flow projections, our exposure to market risks,

policies and actions of regulatory authorities; impact of competition; experience with

regard to mortality and morbidity trends, lapse rates and policy renewal rates; the

impact of changes in capital , solvency or accounting standards , tax and other

legislations and regulations in the jurisdictions as well as other risks detailed in the

reports filed by ICICI Bank Limited, our holding company, with the United States

Securities and Exchange Commission. ICICI Bank and we undertake no obligation to

update forward-looking statements to reflect events or circumstances after the date

thereof.

2424

Thank you