ajmal bhatty: takaful beyond the tipping point - the industry's dilemma in moving forward

DESCRIPTION

Tokio Marine Middle EastTRANSCRIPT

Takaful Beyond the Tipping PointThe industry's dilemma in moving forward

Ajmal Bhatty,

Chief Executive Officer, Takaful

1 July 2009, Takaful Summit, London

1

.... in the beginning

From perception to realization

From ridicule (of the System) to respect

2

1 July 2009, Takaful Summit, London

.... reaching the tipping pointCreating Niche, Gaining Momentum

Total number: Co’s + windows: 181

1 July 2009, Takaful Summit, London

Extraordinary level of activity since 2003

Position as at January 2008

Contribution in 2006(US$ mn)

More than 100 mn

50 mn to 100 mn

10 mn to 50 mn

Less than 10 mn

> 100 mn

50 – 100 mn

SudanMalaysiaSaudi ArabiaIran

IndonesiaQatarUAEKuwait

21 countries4

10 – 50 mn

< 10 mn

BruneiThailandBahrainJordan

MauritaniaEgyptSenegalPakistanBangladesh

Sri LankaSingaporeYemenLebanonUK

And counting…..

.... building the blocks: Spread of Takaful

.... at the tipping point

1. Resilience of Islamic Finance

2. Takaful growth outstripping conventional

3. But still there are several untapped markets

4. Huge potential in Family takaful

5. Huge possibilities in micro-takaful

6. ‘Mega Fund Flows’ .. Race to become global

Islamic financial hub … Bahrain, Kuala Lumpur,

London, Singapore, Hong Kong, Riyadh (?), Qatar

(?)

5

1 July 2009, Takaful Summit, London

This is the lower estimate for takaful premiums

$14.5bn is the higher estimate.The highest estimate is in excess of USD30bn

Potential Size of ‘Takaful Industry’

15 May 2009

http://www.islamic-banking.com/aom/takaful/ma_bhatti.php

$7.4bn estimate for 2015 was made in 2001, see below, but Industry is already at this level in 2008

6

1 July 2009, Takaful Summit, London

… challenges beyond the tipping point

1. Takaful Industry: We still have difficulty defining ourselves?

2. Takaful’s Future: Will it always remain a NICHE?

3. Business Mix: Will we ever be big ticket players?

4. Takaful Ethics: Shariah credible? SRI aligned?

5. Spreading Awareness: Correctly, Effectively

7

1 July 2009, Takaful Summit, London

Takaful, Co-operative, Islamic Insurance….. So many names? Do all these mean the same?

Takaful Industry ? Exclude Iran ?B

A

8

1 July 2009, Takaful Summit, London

Consolidated

Industry data is

hard to find?

We need

authentic and

credible industry

source to provide

vital statistics of

the industry?

difficulty defining ourselves?

Depending on our definition, we are as big as$1.4bn / $2.3bn / $6.5bn in 2007

Takaful InsurancePublication Publication

2006 2007Bahrain 34 42 Indonesia 80 104 Iran 3,685 3,505 Malaysia 545 526 Saudi 831 909 Sudan 203 232 UAE 65 83 Others 249 241 Total 5,692 5,642

Insurance Publication 2007MalaysiaConventional Insurance 8824Takaful 526Total 9350Another Report 2007 9469

Global Takaful Size, 2007 USD mInsurance Publication 1.4 Takaful excl Iran, KSA conv 2.3

Takaful Estimates incl Iran 6.5

A

B

A-B

A

9

1 July 2009, Takaful Summit, London

Do-ables (battles of mind)

Difficult (battles of heart)

To be Shariah Compliant in developing products, funds and managing operations

Setting up new takaful companies with large capital

Building state of the Art systems

Education and Training Competing for business

To be Shariah Credible in being true to its Ethics

Converting ‘conventionals’ to takaful

Using principles of Zarurah only when needed

Application of education and training to increase takaful awareness and consumer acceptability

Mass application of takaful in all OIC countries

Challenges for Takaful Industry10

THE

LETTER THE

SPIRIT

1 July 2009, Takaful Summit, London

Takaful companies in different parts of the world still reinsure conventionally or have conventional reinsurers as leaders of their reinsurance programs. Why?

Short cuts apply to Shariah screening of assets as well. Why?

‘Ethical’ is the very theme of Shariah criteria, like the ethical use of money channeled into businesses that are good socially and environmentally. And yet we don’t market ourselves as Ethical besides being Islamic. Why?

Zarurah & Ethics of SRI

FAULT LINES Conventional Mind sets

Very busy Shariah Scholars

Too few Shariah Scholars

Lack of Shariah standards at Regulatory level

11

Weak Takaful Ethics

Battles of Heart

Human Rights Abused

Greenhouse gas emissions

Biodiversity challenged

Destroying flora and fauna

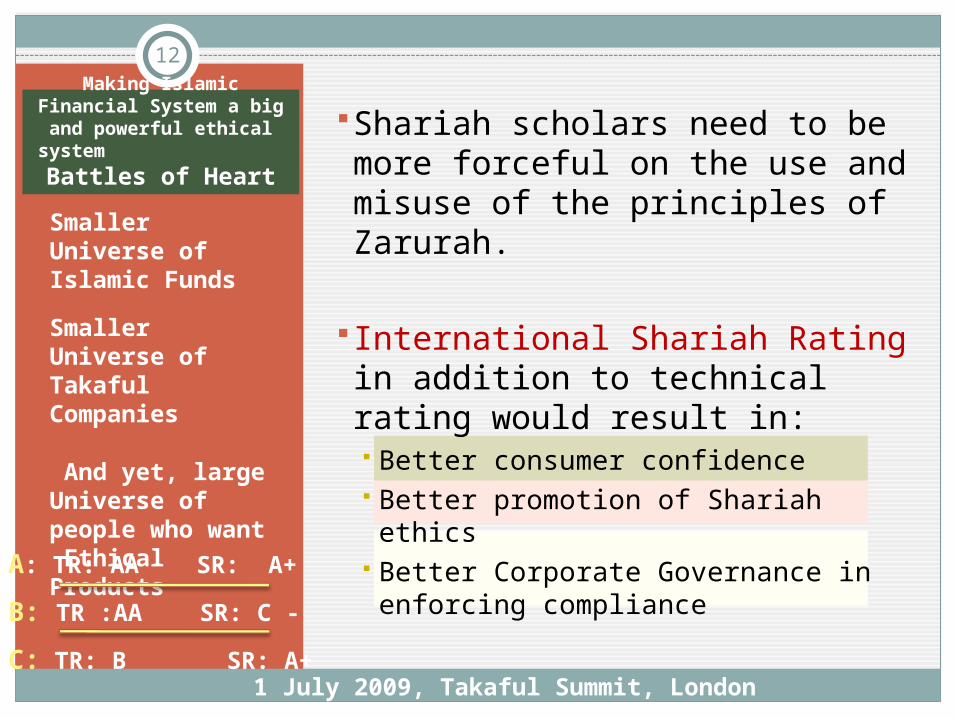

Shariah scholars need to be more forceful on the use and misuse of the principles of Zarurah.

International Shariah Rating in addition to technical rating would result in: Better consumer confidence Better promotion of Shariah ethics Better Corporate Governance in enforcing compliance

Making Islamic Financial System a big and powerful ethical

system Battles of HeartSmaller Universe of Islamic Funds

Smaller Universe of Takaful Companies

And yet, large Universe of people who want Ethical Products

12

1 July 2009, Takaful Summit, London

A: TR: AA SR: A+

B: TR :AA SR: C -

C: TR: B SR: A+

Consumer Acceptability and Takaful Ethics CEO’s of some

Takaful companies are still stating in their Annual Reports that there is Lack of Awareness about Takaful

But when you look into what they have done to alleviate this, there is not much to see

For how long will this continue?

Takaful awareness is patchy, except in Sudan, Malaysia and GCC to some extent

The word ‘takaful’ is not known to many people

Takaful is sold as ‘insurance’ and not for its ‘concept’ of ethics and fairness, for its goodness for society and environment

A dilemma for conventional Group with takaful companies is how to promote takaful as ethical in the same market where it operates conventional business, when by implication it may become unethical.

13

Lack of takaful awareness

Battles of Heart

1 July 2009, Takaful Summit, London

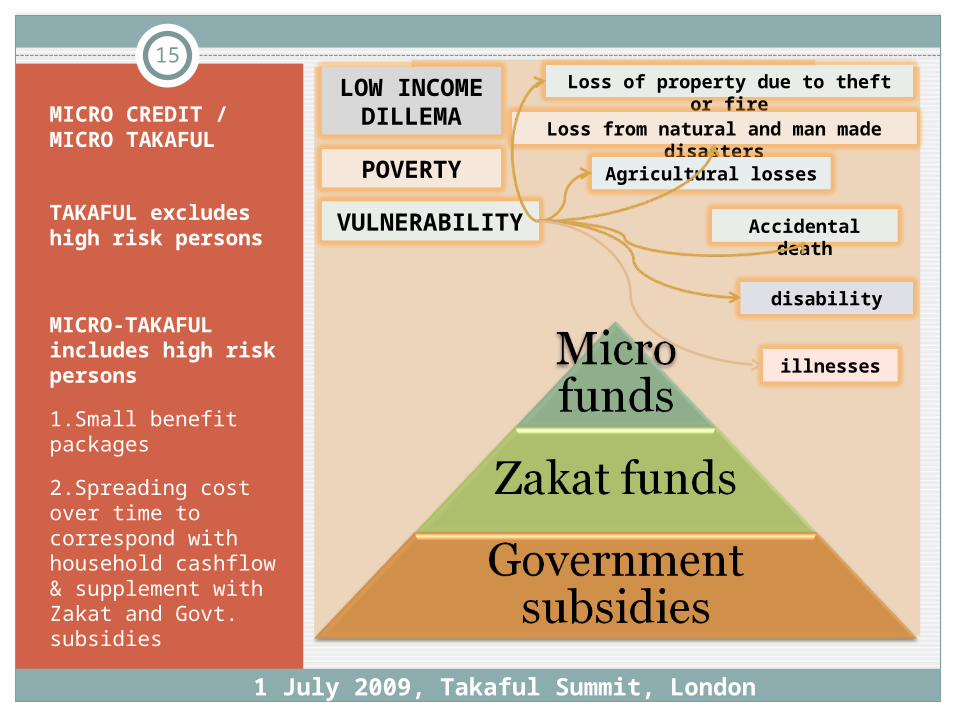

UN’s MILLENNIUM DEVELOPMENT GOALS 2000-2015

1.Halve the number of people with income <$1 per day

2.Halve number of people suffering from hunger

3.Ensure children are able to complete primary schooling

4.Ensure equal schooling for girls

5.Reduce by 2/3rd the under-5 mortality rate

Alleviating financial conditions of poor

masses in many countries

14

More than 4 bn people live on

less than $2 per day

Micro-credit and micro-takaful can be

part of the UN’s Millennium

Development Goals

MICRO CREDIT / MICRO TAKAFUL

TAKAFUL excludes high risk persons

MICRO-TAKAFUL includes high risk persons

1.Small benefit packages

2.Spreading cost over time to correspond with household cashflow & supplement with Zakat and Govt. subsidies

15LOW INCOME

DILLEMA

POVERTY

VULNERABILITY

Loss of property due to theft or fire

Loss from natural and man made disasters

Agricultural losses

Accidental death

illnesses

disability

1 July 2009, Takaful Summit, London

Takaful DilemmaRecapping

Macro Challenges Global Challenges

1.Credibility of Vital Industry Statistics

2.Shariah credibility for social goodness and avoiding dilution of principles

3.Need a paradigm shift from small is beautiful to big is powerful (and beautiful too) – enlarging the size of Islamic Financial System, facilitating micro takaful.

16

1.Concerted effort towards regulatory standardization

2.Need a) good mechanism for SRI compliance, b) redefining Zarurah principles, c) Universally acceptable Shariah Rating

3.Lobby IDB and OIC more effectively for supporting growth and expansion of takaful. It is not just their responsibility but their burden to deliver, especially in micro takaful.

1 July 2009, Takaful Summit, London

Takaful Beyond the Tipping PointThe industry's dilemma in moving forward

Ajmal Bhatty, Chief Executive Officer, Takaful

1 July 2009, Takaful Summit, London

17