aino communique feb 2018ainoglobal.com/magazine/aino communique - feb 18.pdf · 2018-02-23 · hike...

TRANSCRIPT

AINO Management Consultancy Pvt Ltd

AINO COMMUNIQUE – FEB 2018

Page 1 of 25

Dear Professional Colleagues, Effective Networking isn't a result of luck - it requires hard work and persistence – Lewis

Howes

Networking and Relationship Building are key point for every professionals. For our

profession it is essential to maintain cordial ties every friend, family or acquaintance. In

the course of our day-to-day professional activities we interact with governmental agencies

and key regulators on a day-to-day basis. It becomes necessity for us to have a healthy

work – life balance too!

Keeping bonds of relationship strong is of quite essential importance. A good Relationship is not when two 'Perfect people' come together; it is when two 'Imperfect people' learn to enjoy the differences. Learn the wisdom of compromise - It is better to bend a little, rather than to break a relationship forever. Thanks to the social network, the internet and whatsapp; it’s much easier to stay in touch. We are pleased to bring out our 52nd edition of AINO COMMUNIQUE which summarizes the latest significant tax and financial developments of last month. The Finance Budget, 2018 was presented by Finance Minister Shri Arun Jaitley in the Loka Sabha on 1st February, 2018. The highlights of the tax proposal introduced in the budget are given in the subsequent pages. MCA - With the rapid development in the macro level of Indian economy, the ministry of corporate affairs has come out with schemes to make easier the starting of any business, The company can be started with Zero fee, with so much simplified procedure, reduced time and without even the DIN. The MCA, in its amendment rules has also launched RUN Service (Reserve unique name) where in the procedure to reserve name has been made easier and also can be done without filing a form or use a DSC. GST – Has got ample changes like introduction of e-way bill, decrease in GST rates, many notifications etc.

We hope you find this journal is informative and of continued interest. We welcome your

feedback at [email protected]

With warm Regards,

CA. Sudheer Javali

On behalf of AINO Team!!

Determination determines your destination!

Page 2 of 25

Calendar Month Overview Page No.

Statutory Due Dates In the month of February 2018 3

Foreign Exchange Fluctuation 3

Stock Market Fluctuation 3

Commodity Market Fluctuation 3

New Notification / Circulars / Amendments

Union Budget Highlights 2018-19 4

Income Tax & TDS 6

Goods and Service Tax (GST) 6

The Companies Act, 2013 8

Director General of Foreign Trade (DGFT) 9

Monthly Articles

Article 1: Monthly Article I: Incorporation Of Companies as per

Companies Amendment Act, 2017 & Companies (incorporation)

Amendment Rules, 2018 10 Article 2: Major Amendments in Goods & Service Tax, 2017 13

Compendium

Knowledge has a beginning but no end!

Page 3 of 25

Statutory

Due Dates In the month of February 2018

Particulars Nature of payment/Return Filing Due date

TDS/TCS TDS payment 7th Feb

Issue of TDS certificate

TDS Deducted under Sec 194-IA & Sec 194 IB 14th Feb

Form 24 G (Other than salary cases) 15th Feb

TDS deducted for payments other than salaries 15th Feb

PF Monthly payment and Return filing 15th Feb

ESIC Monthly payment and return filing 15th Feb

PT Monthly payment and return filing 20th Feb

Goods & Service Tax (GST)

GSTR- 3B for the month of January-18 20th Feb

GSTR-1 for the Quarter Oct- Dec 2017 (<1.5 Cr) 15th Feb

GSTR-1 for the month of Dec 2017 (>1.5 Cr) 10th Feb

Foreign Exchange Fluctuations

Currency As on 31st Dec 2017 As on 31st Jan 2018 Change

USD 63.9273 63.6878 0.2395

GBP 86.0653 90.3539 4.2886

EURO 76.3867 79.2149 2.8282

Stock Exchange Fluctuations

Stock Exchange As on 31st Dec 2017

As on 31st Jan 2018 Change

BSE Sensex 34,056.83 35,965.02 1,908.19

Nifty 10,530.70 11,027.70 497

Commodity Market (MCX) Fluctuations Commodity As on 31st Dec 2017 As on 31st Jan 2018 Change

Gold (10 grams) 22 carat

29,156.00 28,550 606.00

Silver (1 kg ) 38,700 42,200 3,500.00

Calendar Month Overview

Page 4 of 25

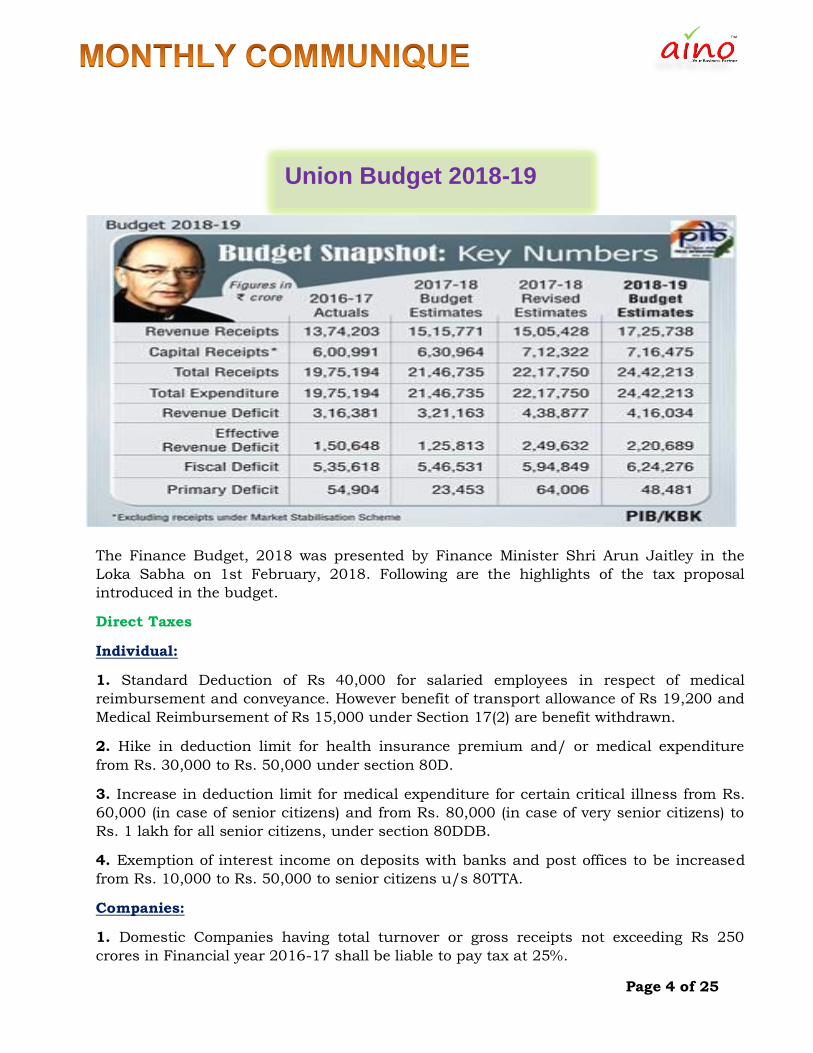

The Finance Budget, 2018 was presented by Finance Minister Shri Arun Jaitley in the

Loka Sabha on 1st February, 2018. Following are the highlights of the tax proposal

introduced in the budget.

Direct Taxes

Individual:

1. Standard Deduction of Rs 40,000 for salaried employees in respect of medical

reimbursement and conveyance. However benefit of transport allowance of Rs 19,200 and

Medical Reimbursement of Rs 15,000 under Section 17(2) are benefit withdrawn.

2. Hike in deduction limit for health insurance premium and/ or medical expenditure

from Rs. 30,000 to Rs. 50,000 under section 80D.

3. Increase in deduction limit for medical expenditure for certain critical illness from Rs.

60,000 (in case of senior citizens) and from Rs. 80,000 (in case of very senior citizens) to

Rs. 1 lakh for all senior citizens, under section 80DDB.

4. Exemption of interest income on deposits with banks and post offices to be increased

from Rs. 10,000 to Rs. 50,000 to senior citizens u/s 80TTA.

Companies:

1. Domestic Companies having total turnover or gross receipts not exceeding Rs 250

crores in Financial year 2016-17 shall be liable to pay tax at 25%.

Union Budget 2018-19

Page 5 of 25

2. Difference between Stamp Duty Value and Actual consideration is taxable for both

seller and buyer u/s 50C, 43CA and 56. It is now provided that if the difference is not

more that 5% of consideration the provisions shall not be attracted.

3. Section 80P provides for 100 percent deduction in respect of profit of Cooperative

Society which provide assistance to its members engaged in primary agricultural

activities. It is proposed to extend similar benefit to Farm Producer Companies (FPC),

having a total turnover upto Rs 100 Crore.

4. At present, under section 80-JJAA of the Act, a deduction of 30% is allowed in addition

to normal deduction of 100% in respect of emoluments paid to eligible new employees who

have been employed for a minimum period of 240 days during the year. However, the

minimum period of employment is relaxed to 150 days in the case of apparel industry. In

order to encourage creation of new employment, it is proposed to extend this relaxation to

footwear and leather industry.

Trust:

Provision of section 40 (ia) and 40 A(3) and 40A(3A) Cash payment exceeding Rs. 10,000/-

are being made applicable to Charitable Trust . Hence expenditure incurred without

deduction of TDS and in cash will not be eligible as application of income under section

10(23C) and section 11(1)(a).

General changes applicable to all assesses:

1. Long term Capital gain exemption under section 10(38) in respect of listed STT paid

shares being withdrawn. Tax on LTCG-STT paid will be applicable at 10% if gains

more than Rs. 1,00,000. However sale upto 31/1/2018 not covered. Further gains

accrued till 31/1/2018 not taxable if sale upto 31/7/18.

2. Education cess and Secondary Higher education of 3% gets replaced by 4% Health

and Education cess and Secondary Higher education cess.

3. Income Distribution Tax payable by Equity Oriented Mutual Funds @10%

4. E assessments will be done across the country for removing person to person

interface.

Indirect Taxes:

1. No significant indirect tax changes as gst has included most.

2. Custom duty on mobile phones increased to 20% and some mobile and tv parts to

15% to promote make in india.

Employee’s provident fund:

Women employees’ contribution limit reduced to 8% under the Employees

Provident Fund and Miscellaneous Provisions Act.

Page 6 of 25

Income Tax & TDS

Processing of income-tax returns under section 143(1) of the Income-tax Act which were filed in Forms ITR-l to 6 & applicability of section 143(1)(a)(vi)

While processing the return of income, prescribes that the total income or loss shall be computed after making adjustment for addition of income appearing in Form 26AS or Form 16A or Form 16 (the three Forms) which has not been included in computing the total income

in the return. In this regard, CBDT has issued Instruction No .(s) 9/2017 dated 11.lD. 2017 & 10/2017 dated 15.11.2017 for identification of instances in which section 143(1)(a)(vi) of the Act may be invoked by CPC-ITR, Bengaluru on the basis of information contained in the ITR

Forms 1 to 6.

http://www.incometaxindia.gov.in/communications/circular/circular1_2018.pdf

Case Study: John Baptist Lasrado vs. Income Tax Settlement Commission (T.S.

Sivagnanam J.) with respect to 234B Where duty is cast upon payer to pay tax at source, on failure, no interest can be imposed on

payee/assessee. Thus, in respect of salary income earned by assessee an employee of a multinational company outside India, employer abroad having paid interest under section 201(1A) for not deducting tax at source, assessee would not be liable for payment of interest

under section 234B

Goods & Service Tax

Effective Rate Of Tax Under Composition Scheme (Notification No. 1/2018- Central Tax dated 1st January 2018)

With the effect from 1st January, 2018 Prescribed effective rate of tax under composition scheme for manufacturers and other suppliers i.e. 0.5% CGST. Earlier

Composite tax shall be paid on entire Turnover (Exempted + Taxable + Nil) now the same shall be substituted with the words “half per cent of the turnover of taxable supplies of goods”. http://www.cbec.gov.in/resources//htdocs-cbec/gst/Notification-1-2018-central_tax-

English.pdf

Late fees for filing Form GSTR-1 (Notification No. 4/2018 – Central Tax dated 23rd January 2018) With the effect from 23rd

January, 2018, Late fees for filing GSTR-1 in case of nil return it is Rs.10 per day per tax & for rest (Payable or Carry forward ITC) it is Rs.25 per day per tax. http://www.cbec.gov.in/resources//htdocs-cbec/gst/Notification-4-2018-central_tax-

English.pdf

Late fees for filing Form GSTR-5 (Notification No. 5/2018 – Central Tax dated 23rd January 2018) With the effect from 23rd

January, 2018 Late fees for filing GSTR-5 in case of nil CGST payment it is Rs.10 per day per tax & for rest) it is Rs.25 per day per tax.

New Notification / Circulars / Amendments

Page 7 of 25

http://www.cbec.gov.in/resources//htdocs-cbec/gst/Notification-5-2018-

central_tax-English.pdf

E-way bill made compulsory from February 01, 2018 (Notification No. 74/2017-Central Tax, Dated 29-12-2017)Govt. has notified that E-way bill would be applicable from February 01, 2018 as recommended by GST Council.

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-74-central-tax-english.pdf

Late fees for filing Form GSTR-5A With the effect from 23rd January, 2018 (Notification No. 6/2018 – Central Tax dated 23rd

January 2018) Late fees for filing GSTR-5A in case of nil IGST payment it is Rs.10 per day per

tax & for rest) it is Rs.25 per day per tax.

http://www.cbec.gov.in/resources//htdocs-cbec/gst/Notification-6-2018-central_tax-

English.pdf

Late fees for filing Form GSTR-6 With the effect from 23rd January, 2018 (Notification No. 7/2018 – Central Tax dated 23rd

January 2018) Late fees for filing GSTR-6 is Rs.25 per day per tax. http://www.cbec.gov.in/resources//htdocs-cbec/gst/Notification-7-2018-central_tax-

English.pdf

Time limit for furnishing the return by an Input Service Distributor With the effect from 23rd January, 2018 (Notification No. 8/2018 – Central Tax dated 23rd

January 2018) Hereby extends the time limit for furnishing the return by an Input Service Distributor in FORM GSTR-6 for the period July 2017 to February 2018 till the 31st day of

March, 2018.

http://www.cbec.gov.in/resources//htdocs-cbec/gst/Notification-8-2018-central_tax-

English.pdf

Common Goods and Service Tax Electronic Portal for facilitating registration, payment

of tax,etc.

Hereby notifies www.gst.gov.in as the Common Goods and Services Tax Electronic Portal for facilitating registration, payment of tax, furnishing of returns and computation and settlement

of integrated tax and www.ewaybillgst.gov.in as the Common Goods and Services Tax

Electronic Portal for furnishing electronic way bill.

http://www.cbec.gov.in/resources//htdocs-cbec/gst/Notification-9-2018-central_tax-

English.pdf

(Notification No. 5/2018- Central Tax (Rate) dated 25th January 2018)

Seeks to exempt Central Government’s share of Profit Petroleum from Central tax.With the

effect from 25th January, 2018

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-05-2018-cgst-rate-english.pdf

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-05-2018-igst-rate-english.pdf

Page 8 of 25

(Notification No. 1/2018 – Integrated Tax dated 23rd January 2018) Amendment of notification No. 11/2017-Integrated Tax dated 13.10.2017 for cross-empowerment of State tax

officers for processing and grant of refund

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-1-2018-igst-english.pdf

(Notification No. 6/2018- Integrated Tax (Rate) dated 25th January 2018) With the effect from 25th January, 2018 Seeks to exempt royalty and license fee from Integrated tax to the extent it is paid on the consideration attributable to royalty and license fee included in transaction

value under Rule 10(1)(c) of Customs Valuation (Determination of value of imported Goods)

Rules, 2007.

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-06-2018-igst-rate-english.pdf

Clarifications regarding levy of GST on accommodation services, betting and gambling in casinos, horse racing, admission to cinema, homestays, printing, legal services etc. – Reg. Circular No. 27/01/2018-GST dated 04th January 2018) With the effect from 04th January,

2018

http://www.cbec.gov.in/resources//htdocs-cbec/gst/circularno-27-gst.pdf

Clarification on supplies made to the Indian Railways classifiable under any chapter, other

than Chapter 86 Circular No. 30/4/2018-GST dated 25th January 2018

With the effect from 25th January, 2018

Conclusion: it is hereby clarified that

• only the goods classified under Chapter 86, supplied to the railways attract 5% GST rate

with no refund of unutilised input tax credit and

• other goods [falling in any other chapter], would attract the general applicable GST rates to

such goods, under the aforesaid notifications, even if supplied to the railways.

http://www.cbec.gov.in/resources//htdocs-cbec/gst/circularno-30-cgst.pdf .

Refer to Monthly Article – 2 for details of the notification….

The Companies Act, 2013

The Companies Amendment Act, 2018

The Companies Amendment Act, 2018 has amended the rules with regard to incorporation like

RUN and Zero Incorporation Fee, etc.

http://www.mca.gov.in/Ministry/pdf/CompaniesIncorporationAmendmentRules2018_250120

18.pdf

Refer to Monthly Article – 1 for details of the rule….

Page 9 of 25

Director Identification Number for the Directors of the Companies

Individual who do not have a DIN for incorporating the Company, the same can be applied for and allotted through Spice Form during the Incorporation process and Form DIR-03 is specifically to applied by the individuals who wish to be appointed as Director in the Existing

Company. http://www.mca.gov.in/Ministry/pdf/AppointmentQualificationDirectoramendmentrules2018_25012018.pdf

Condonation of Delay Scheme

CODS which is introduced on 01.01.2018 will be in force upto 31.03.2018.E-form for CODS will be available from 20.02.2018.

http://www.mca.gov.in/Ministry/pdf/Generalcircular16_29122017.pdf

Director General of Foreign Trade

Operational Modification of IEC Registration

To make changes done in the IEC Registration which is done in offline mode, to be migrated to E-IEC- i.e.,from of offline to online.

http://dgft.gov.in/Exim/2000/PN/PN15/pn3615.pdf

Leadership is the capacity to translate VISION into REALITY!

Page 10 of 25

Introduction

The Central Government hereby makes the following rules further to amend the Companies

(Incorporation) Rules, 2014, namely, These rules may be called the Companies (Incorporation)

Amendment Rules, 2018.

Background of the Rule Prior to Companies Amendment Act, 2017, Rules in respect to Reservation of Name and Application for Incorporation Of Companies, the power was vested with Registrar, Central Registration Centre. The Name Application was to be Filed in INC-1 along with the fee as provided in the Companies (Registration offices and fees) Rules, 2014 to the Registrar, Central Registration Centre. The application submitted to the registrar will be approved and reserved for a period of 60 days. The application for incorporation of a company under this rule shall be in FORM No. INC-32 (SPICe) alongwith e-Memorandum of Association (e-MOA) in Form No. INC-33 and e-Articles of Association (e-AOA) in Form No. INC-34. Provided that in case of incorporation of a company falling under section 8 of the Act, FORM No. INC-32 (SPICe) shall be filed along with FORM No. INC-13 (Memorandum of Association) and FORM No. INC-31 (Articles of Association) as attachments. Applicability

The Companies (Incorporation) Amendment Rules, 2018 will apply for the incorporation of the

companies with effect from 26.01.2018.

Incorporation Process Under The New Rule.

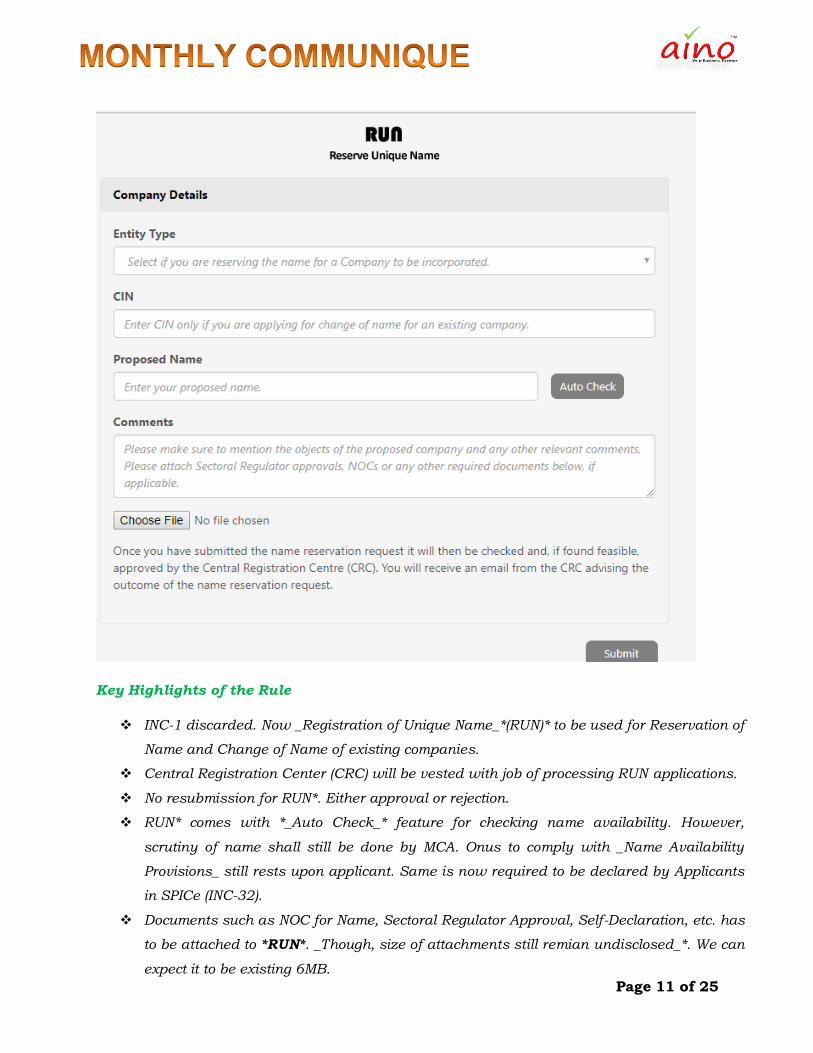

An application for reservation of name shall be made through the web service available at

www.mca.gov.in by using RUN (Reserve Unique Name) along with fee as provided in the

Companies (Registration offices and fees) Rules, 2014, which may either be approved or

rejected, as the case may be, by the Registrar, Central Registration Centre. Name approved and

reserved under RUN will be valid only 20 days.

Screenshot of the same is given below:

Monthly Article I: Incorporation Of Companies as per

Companies Amendment Act,2017 & Companies (incorporation)

Amendment Rules, 2018

Page 11 of 25

Key Highlights of the Rule

INC-1 discarded. Now _Registration of Unique Name_*(RUN)* to be used for Reservation of

Name and Change of Name of existing companies.

Central Registration Center (CRC) will be vested with job of processing RUN applications.

No resubmission for RUN*. Either approval or rejection.

RUN* comes with *_Auto Check_* feature for checking name availability. However,

scrutiny of name shall still be done by MCA. Onus to comply with _Name Availability

Provisions_ still rests upon applicant. Same is now required to be declared by Applicants

in SPICe (INC-32).

Documents such as NOC for Name, Sectoral Regulator Approval, Self-Declaration, etc. has

to be attached to *RUN*. _Though, size of attachments still remian undisclosed_*. We can

expect it to be existing 6MB.

Page 12 of 25

Brief of Main Objects to be entered in *RUN* in comments section.

Incorporation to be done only through SPICe Route now i.e. INC-32

SPICe (INC-32) to be now used for Incorporation of Chapter XXI (Part-I) companies i.e.

Section 366 companies.

e-MOA and e-AOA (i.e. INC-33 and INC-34) to be *not applicable* for companies having

foreign subscribers or cases where subscribers are more than 7. In both such cases

separate MOA-AOA has to be attached.

Form INC-7 discontinued for Incorporation matters.

For incorporating companies having less than or equal to Rs.10 lakh nominal capital or

companies which are without share capital and have members less than 20 - *_No

Incorporation fee._* Only Stamp Duty for registration of MOA and AOA has to be paid

as per the State Act.

As per Companies Amendment Act, 2017, the clause of submitting the Affidavits by the

Subscribers and First Directors of the Company has been scrapped off. As per the New

Incorporation Rules, only Declarations regarding the same has to be submitted by

Subscribers and First Directors of the Company. Thus, make the Process hassle free from

the requirement of procuring stamp papers for Affidavits and Notarising the same.

Thus to conclude the Companies Amendment Act, has made the Incorporation process simpler,

hassle free, economical, and time saving. This new initiative brought up by the Central Govt. is

warmly welcomed by the Professionals and Entreprenuers.

When the going gets tough, the tough get going!

Page 13 of 25

Major Changes that can be observed below which has happened as on 23rd January 2018.

With the effect from 23rd January, 2018

Point-wise analysis of major amendments in Central Goods & Service Tax, 2017 :

Any person who has been granted registration on a provisional basis under clause (b) of

sub-rule (1) of rule 24 and who opts to pay tax under section 10, shall electronically file

an intimation in FORM GST CMP-01, duly signed or verified through electronic verification

code, on the common portal, either directly or through a Facilitation Centre notified by the

Commissioner, prior to the appointed day, but not later than 180 days after the said

day (earlier 90 days).

Sl. No

Category of Composite Dealer

Rate of Tax

1. Manufacturers, other than manufacturers of such goods as may be notified by the Government

0.5% (Earlier 1%) of the turnover in the State or Union territory

2. Suppliers making supplies referred to in clause (b) of paragraph 6 of Schedule II (Restaurants)

2.5% (No change) of the turnover in the State or Union territory

3. Any other supplier eligible for composition levy under section 10 and the

provisions of this Chapter (Others)

0.5% (No Change) half per cent. of the turnover of taxable supplies of goods in the State or Union territory

Proviso to Rule. 20 has been omitted – “Provided that no application for the cancellation of

registration shall be considered in case of a taxable person, who has registered

voluntarily, before the expiry of a period of one year from the effective date of

registration”- is omitted.

Migration of persons registered under the existing law Rule 24 –

Amendment in Sub Rule 4 “Every person registered under any of the existing laws, who is not

liable to be registered under the Act may, on or before 31st March, 2018 (earlier 31st

December, 2017) at his option, submit an application electronically in FORM GST REG-29 at the

common portal for the cancellation of registration granted to him and the proper officer shall,

after conducting such enquiry as deemed fit, cancel the said registration.

Monthly Article II : Major Amendments in Goods &

Service Tax, 2017

Page 14 of 25

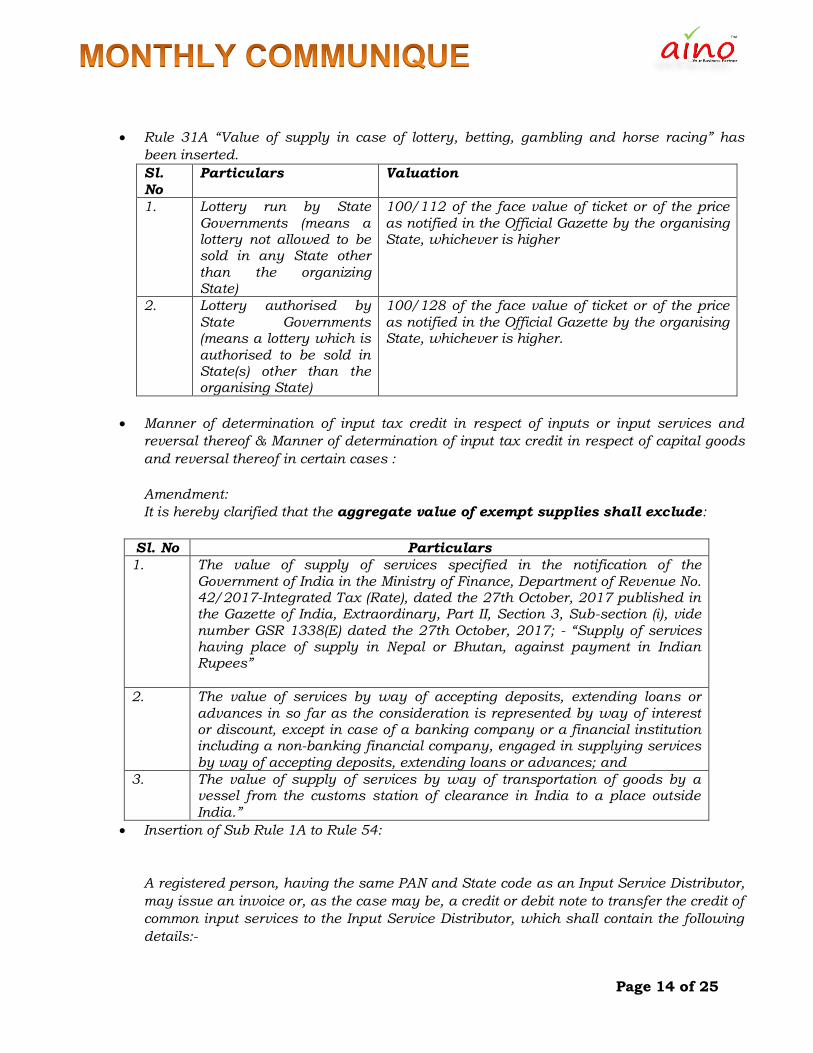

Rule 31A “Value of supply in case of lottery, betting, gambling and horse racing” has

been inserted.

Sl.

No

Particulars Valuation

1. Lottery run by State Governments (means a lottery not allowed to be sold in any State other

than the organizing State)

100/112 of the face value of ticket or of the price as notified in the Official Gazette by the organising State, whichever is higher

2. Lottery authorised by State Governments (means a lottery which is authorised to be sold in State(s) other than the organising State)

100/128 of the face value of ticket or of the price as notified in the Official Gazette by the organising State, whichever is higher.

Manner of determination of input tax credit in respect of inputs or input services and

reversal thereof & Manner of determination of input tax credit in respect of capital goods

and reversal thereof in certain cases :

Amendment:

It is hereby clarified that the aggregate value of exempt supplies shall exclude:

Sl. No Particulars

1. The value of supply of services specified in the notification of the Government of India in the Ministry of Finance, Department of Revenue No. 42/2017-Integrated Tax (Rate), dated the 27th October, 2017 published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number GSR 1338(E) dated the 27th October, 2017; - “Supply of services having place of supply in Nepal or Bhutan, against payment in Indian Rupees”

2. The value of services by way of accepting deposits, extending loans or advances in so far as the consideration is represented by way of interest or discount, except in case of a banking company or a financial institution including a non-banking financial company, engaged in supplying services by way of accepting deposits, extending loans or advances; and

3. The value of supply of services by way of transportation of goods by a vessel from the customs station of clearance in India to a place outside India.”

Insertion of Sub Rule 1A to Rule 54:

A registered person, having the same PAN and State code as an Input Service Distributor,

may issue an invoice or, as the case may be, a credit or debit note to transfer the credit of

common input services to the Input Service Distributor, which shall contain the following

details:-

Page 15 of 25

Sl.No Particulars

1. name, address and Goods and Services Tax Identification Number of the registered person having the same PAN and same State code as the Input

Service Distributor;

2. a consecutive serial number not exceeding sixteen characters, in one or multiple series, containing alphabets or numerals or special characters - hyphen or dash and slash symbolised as “-” and “/” respectively, and any combination thereof, unique for a financial year;

3. date of its issue;

4. Goods and Services Tax Identification Number of supplier of common service and original invoice number whose credit is sought to be transferred to the Input Service Distributor;

5. name, address and Goods and Services Tax Identification Number of the Input Service Distributor;

6. taxable value, rate and amount of the credit to be transferred; and

7. signature or digital signature of the registered person or his authorised

representative

The taxable value in the invoice issued under clause (a) shall be the same as the value of

the common services.

Insertion of GST rule no.55A. Tax Invoice or bill of supply to accompany transport of

goods.- The person-in-charge of the conveyance shall carry a copy of the tax invoice or the

bill of supply issued in accordance with the provisions of rules 46, 46A or 49 in a case

where such person is not required to carry an e-way bill under these rules.”;

With effect from 23rd October, 2017, in rule 89, for sub-rule (4A) and sub-rule (4B), the

following sub-rules shall be substituted, namely:-

Sl. No

Particulars

1. In the case of supplies received on which the supplier has availed the benefit of DEEMED EXPORTS, refund of input tax credit, availed in respect of other inputs or input services used in making zero-rated supply of goods or services or both, shall be granted.

2. In the case of supplies received on which the supplier has availed the benefit of the Government of India, Ministry of Finance, notification No. 40/2017-Central Tax (Rate) dated the 23rd October, 2017 (CGST @ 0.05% on intra-State supply of taxable goods by a registered supplier to a registered recipient for export subject to specified condition ) or notification No. 41/2017-Integrated Tax (Rate) dated the 23rd October, 2017 ( Rate Changes in Schedule I goods ) or notification No. 78/2017-

Customs dated the 13th October, 2017 or notification No. 79/2017-Customs dated the 13th October, 2017 or all of them, refund of input tax credit, availed in respect of inputs received under the said notifications for export of goods and the input tax credit availed in respect of other inputs or input services to the extent used in making such export of goods, shall be granted.” (Read with Customs notification no. 78 & 79)

Page 16 of 25

Rule 138 has been inserted “Information to be furnished prior to commencement of

movement of goods and generation of e-way bill – with the effect from 1st Feb 2018”

with effect from 23rd October, 2017, in rule 96, (a) in sub-rule (1), for the words “an

exporter”, the words “an exporter of goods” shall be substituted; (b) in sub-rule (2), for the

words “relevant export invoices”, the words “relevant export invoices in respect of export

of goods” shall be substituted; (c) in sub-rule (3), for the words “the system designated by

the Customs shall process the claim for refund”, the words “the system designated by the

Customs or the proper officer of Customs, as the case may be, shall process the claim of

refund in respect of export of goods ” shall be substituted;

The application for refund of integrated tax paid on the services exported out of India

shall be filed in FORM GST RFD-01 and shall be dealt with in accordance with the

provisions of rule 89”

The persons claiming refund of integrated tax paid on exports of goods or services should

not have received following supplies on which the supplier has availed the benefit of the

Government of India, Ministry of Finance,

notification No. 48/2017- Central Tax dated the 18th October, 2017 -

notification No. 40/2017-Central Tax (Rate) 23rd October, 2017 - Central Tax rate

of 0.05% on intra-State supply of taxable goods by a registered supplier to a

registered recipient for export subject to specified conditions.

notification No. 41/2017-Integrated Tax (Rate) dated the 23rd October, 2017 –

DEEMED EXPORTS

read with notification No. 78/2017-Customs dated the 13th October, 2017 notification No.

79/2017-Customs dated the 13th October, 2017.

http://www.cbec.gov.in/resources//htdocs-cbec/gst/Notification-3-2018-central_tax-

English_New.pdf

CGST Rates Amendments:-

(Notification No. 1/2018-Central Tax (Rate) dated 25th January 2018 read with Notification No.

11/2017-Central Tax (Rate)

With the effect from 25th January, 2018

Services CGST Rate

Conditions

Composite supply of works contract as defined in clause (119) of section 2 of the Central Goods and Services Tax Act, 2017 provided by a sub-contractor to the main

6% Provided that where the services are supplied to a Government Entity, they should have been procured by the said entity in relation to a work entrusted to it by the Central Government, State Government, Union territory or local authority, as the case may be.

Page 17 of 25

contractor providing services specified in item (iii) or item (vi) to the Central Government, State Government, Union territory, a local authority, a Governmental Authority or a Government Entity.

Composite supply of works Provided that where the services are 3 contract as defined in clause (119) of section 2 of the Central Goods and Services Tax Act, 2017 provided by a sub-contractor to the main contractor providing services specified in item (vii) to the Central Government, State Government, Union territory, a local authority, a Governmental Authority

or a Government Entity.

2.5% Provided that where the services are supplied to a Government Entity, they should have been procured by the said entity in relation to a work entrusted to it by the Central Government, State Government, Union territory or local authority, as the case may be.

Services by way of housekeeping, such as plumbing, carpentering, etc. where the person supplying such service through electronic commerce operator is not liable for registration under subsection (1) of section 22 of the Central Goods and Services Tax Act, 2017

2.5% Provided that credit of input tax charged on goods and services has not been taken [Please refer to Explanation no. (iv)].

(xii) Construction services other than (i), (ii), (iii), (iv),

(v), (vi), (vii), (viii),(ix), (x)and (xi) .

9%

Time charter of vessels for transport of goods.

2.5% Provided that credit of input tax charged on goods (other than on ships, vessels including bulk carriers and tankers) has not been taken

Rental services of transport vehicles with or without operators, other than (i) and (ii)

9%

Services by the Central Government, State Government, Union territory or local authority

to governmental authority or government entity, by

NIL

Page 18 of 25

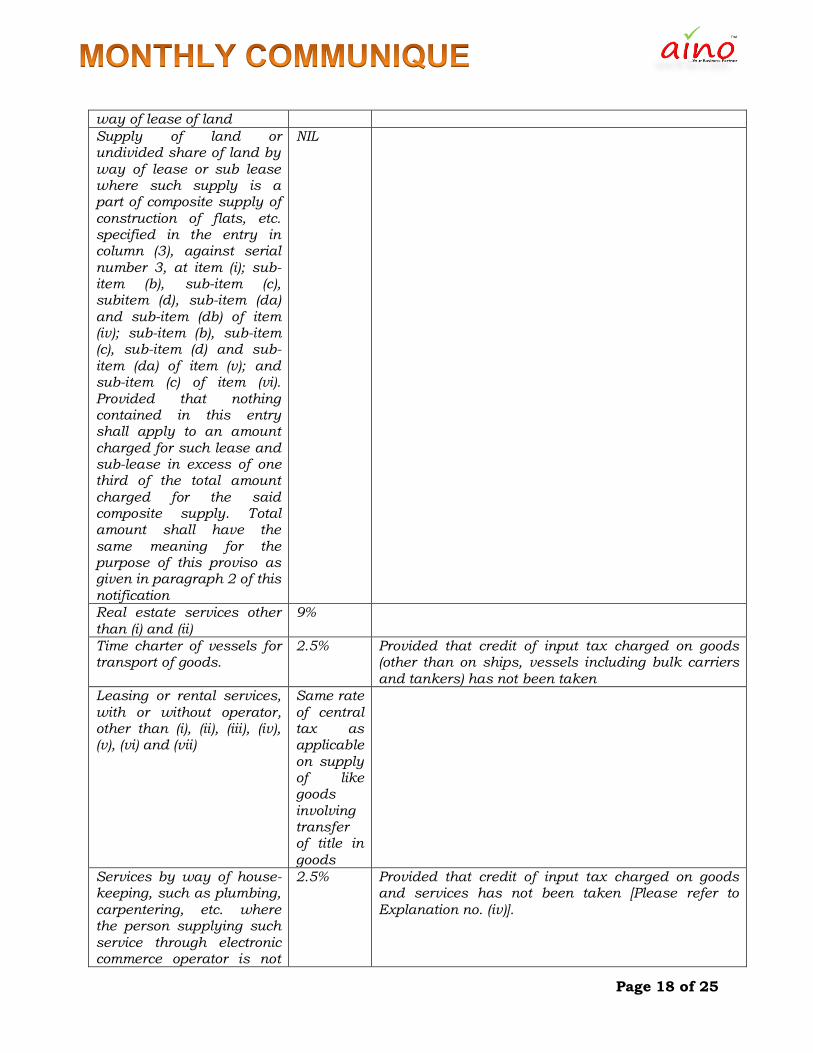

way of lease of land

Supply of land or undivided share of land by

way of lease or sub lease where such supply is a part of composite supply of construction of flats, etc. specified in the entry in column (3), against serial number 3, at item (i); sub-item (b), sub-item (c), subitem (d), sub-item (da) and sub-item (db) of item (iv); sub-item (b), sub-item (c), sub-item (d) and sub-item (da) of item (v); and sub-item (c) of item (vi). Provided that nothing contained in this entry shall apply to an amount charged for such lease and sub-lease in excess of one third of the total amount

charged for the said composite supply. Total amount shall have the same meaning for the purpose of this proviso as given in paragraph 2 of this notification

NIL

Real estate services other than (i) and (ii)

9%

Time charter of vessels for transport of goods.

2.5% Provided that credit of input tax charged on goods (other than on ships, vessels including bulk carriers and tankers) has not been taken

Leasing or rental services, with or without operator, other than (i), (ii), (iii), (iv), (v), (vi) and (vii)

Same rate of central tax as applicable on supply of like goods involving transfer of title in goods

Services by way of house-keeping, such as plumbing, carpentering, etc. where the person supplying such

service through electronic commerce operator is not

2.5% Provided that credit of input tax charged on goods and services has not been taken [Please refer to Explanation no. (iv)].

Page 19 of 25

liable for registration under sub-section (1) of section 22 of the Central Goods and Services Tax Act, 2017.

Support services other than (i) and (ii) .

9%

Service of exploration, mining or drilling of petroleum crude or natural gas or both.

6%

Support services to mining, electricity, gas and water distribution other than (ii) .

9%

Services by way of house-keeping, such as plumbing, carpentering, etc. where the person supplying such service through electronic commerce operator is not liable for registration under sub-section (1) of section 22 of the Central Goods and Services Tax Act, 2017.

2.5%

Provided that credit of input tax charged on goods and services has not been taken

Maintenance, repair and installation (except construction) services, other than (i)

9%

Tailoring services. 2.5%

Manufacturing services on physical inputs (goods)

owned by others, other than (i), (ia), (ii), (iia) and (iii)

9%

Services by way of treatment of effluents by a Common Effluent Treatment Plant.

6%

Sewage and waste collection, treatment and disposal and other environmental protection services other than (i) .

9%

Services by way of admission to amusement parks including theme parks, water parks, joy rides, merry-go rounds, go-carting and ballet.

9%

Services by way of admission to entertainment events or access to amusement facilities

14%

Page 20 of 25

including exhibition of cinematograph films, casinos, race club, any sporting event such as Indian Premier League and the like.

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-01-2018-cgst-rate-english.pdf

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-01-2018-igst-rate-english.pdf

Amendment in NIL rated supplies:

With the effect from 25th January, 2018

Notification No. 2/2018- Central Tax (Rate) 25th January 2018 read with Notification No.

12/2017-Central Tax (Rate)

Goods/Service CGST Rate Conditions

Composite supply of goods and services in which the value of supply of goods constitutes not more than 25 per cent. of the value of the said composite supply provided to the Central Government, State Government or Union territory or local authority or a Governmental authority or a Government Entity by way of any activity in relation to any function entrusted to a Panchayat under article 243G of the Constitution or in relation to any function entrusted to a Municipality under article 243W of the Constitution

Nil -

Services by way of transportation of goods by an aircraft from customs station of clearance in India to a place outside India.

Nil Nothing contained in this serial number shall apply after the 30th day of September, 2018

Services by way of transportation of goods by a vessel from customs station of clearance in India to a place outside India.

Nil Nothing contained in this serial number shall apply after the 30th day of

September, 2018

Services of life insurance provided or agreed to be provided by the Naval Group Insurance Fund to the personnel of Coast Guard under the Group Insurance Schemes of the Central Government.

Nil

Services by way of reinsurance of the insurance schemes specified in serial number 35 or 36.

Nil

Services by an intermediary of financial services located in a multi services SEZ with International Financial Services Centre (IFSC) status to a customer located outside India for international financial services in currencies other than Indian rupees (INR)

Nil

Page 21 of 25

Services by way of fumigation in a warehouse of agricultural produce.

Nil

Services by way of providing information

under the Right to Information Act, 2005 (22 of 2005).

Nil

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-02-2018-cgst-rate-english.pdf

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-02-2018-igst-rate-

english.pdf;jsessionid=BCC7319CF7D6D8CE60CDE29272CE79D1

Old Car Sale & GST Impact

With the effect from 25th January, 2018

Notification No. 8/2018 -Central Tax (Rate) dated 25th January 2018 read with Notification No.

1/2017-Central Tax (Rate) dated 28th June 2017

Sl.

No

Description of Goods CGST

Rate in %

1. Old and used, petrol Liquefied petroleum gases (LPG) or compressed natural gas (CNG) driven motor vehicles of engine capacity of 1200 cc or more and of length of 4000 mm or more. Explanation. - For the purposes of this entry, the specification of the motor vehicle shall be determined

as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under.

9%

2. Old and used, diesel driven motor vehicles of engine capacity of 1500 cc or more and of length of 4000 mm Explanation. - For the purposes of this entry, the specification of the motor vehicle shall be determined as per the Motor Vehicles Act, 1988 (59 of 1988) and the rules made there under.

9%

3. Old and used motor vehicles of engine capacity exceeding 1500 cc, popularly known as Sports Utility Vehicles (SUVs) including utility vehicles. Explanation. - For the purposes of this entry, SUV includes a motor vehicle of length exceeding 4000 mm and having ground clearance of 170 mm. and .

9%

4. All Old and used Vehicles other than those mentioned from S. No. 1 to S.No.3

6%

This notification shall not apply, if the supplier of such goods has availed input tax credit as

defined in clause (63) of section 2 of the Central Goods and Services Tax Act, 2017, CENVAT as

defined in CENVAT Credit Rules, 2004 or the input tax credit of Value Added Tax or any other

taxes paid, on such goods.

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-08-2018-cgst-rate-english.pdf

http://www.cbec.gov.in/resources//htdocs-cbec/gst/Notification-for-CGST-rate-Schedule.pdf

Following specific changes are with the effect from 25th January, 2018

Items taxable @ CGST 2.5%

Notification No. 6/2018-Central Tax (Rate) dated 25th January 2018 read with Notification No.

1/2017-Central Tax (Rate)

Following items are taxable @ CGST 2.5%

Page 22 of 25

i. Tamarind kernel powder

ii. Mehendi paste in cone

iii. Rice bran (other than de-oiled rice bran)

iv. Liquefied Propane and Butane mixture, Liquefied Propane, Liquefied Butane and

Liquefied Petroleum Gases (LPG) for supply to household domestic consumers”;

v. Scientific and technical instruments, apparatus, equipment, accessories, parts,

components, spares, tools, mock ups and modules, raw material and consumables required for

launch vehicles and satellites and payloads”;

Following items are taxable @ CGST 6%

i. Sugar boiled confectionery”;

ii. Drinking water packed in 20 litres bottles”;

iii. Fertilizer grade phosphoric acid”;

iv. Bio-pesticides, namely - 1 Bacillus thuringiensis var. israelensis 2 Bacillus thuringiensis

var. kurstaki 3 Bacillus thuringiensis var. galleriae 4 Bacillus sphaericus 5 Trichoderma viride 6

Trichoderma harzianum 7 Pseudomonas fluoresens 8 Beauveriabassiana 9 NPV of

Helicoverpaarmigera 10 NPV of Spodopteralitura 11 Neem based pesticides 12 Cymbopogan”;

v. Bio-diesel”;

vi. Bamboo wood building joinery

vii. Tableware and Kitchenware of wood”;

viii. Sprinklers; drip irrigation system including laterals; mechanical sprayers”;

Following items are taxable @ CGST 9%

i. derived from vegetable products[other than tamarind kernel powder]

ii. groundnut sweets, gajak and sugar boiled confectionery

matter nor flavoured ([other than Drinking water packed in 20 litres bottles)

iii. Fertilizer grade Phosphoric acid

iv. Preparations for use on the hair [except Mehendi pate in Cones]

v. shingles and shakes[other than bamboo wood building joinery]

vi. Cigarette Filter rods”;

vii. Ghamella

viii. Sanitary ware and parts thereof, of iron and steel”;

ix. Buses for use in public transport which exclusively run on Bio-fuels”;

Following items are taxable @ CGST 14%

Page 23 of 25

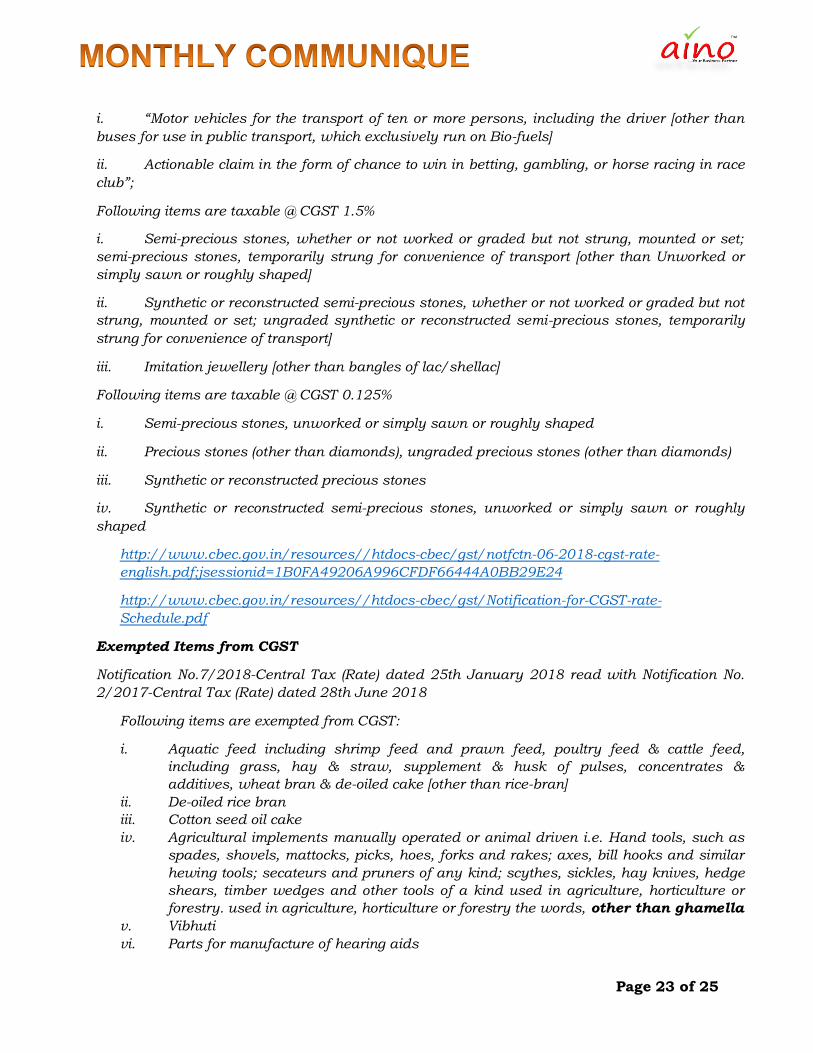

i. “Motor vehicles for the transport of ten or more persons, including the driver [other than

buses for use in public transport, which exclusively run on Bio-fuels]

ii. Actionable claim in the form of chance to win in betting, gambling, or horse racing in race

club”;

Following items are taxable @ CGST 1.5%

i. Semi-precious stones, whether or not worked or graded but not strung, mounted or set;

semi-precious stones, temporarily strung for convenience of transport [other than Unworked or

simply sawn or roughly shaped]

ii. Synthetic or reconstructed semi-precious stones, whether or not worked or graded but not

strung, mounted or set; ungraded synthetic or reconstructed semi-precious stones, temporarily

strung for convenience of transport]

iii. Imitation jewellery [other than bangles of lac/shellac]

Following items are taxable @ CGST 0.125%

i. Semi-precious stones, unworked or simply sawn or roughly shaped

ii. Precious stones (other than diamonds), ungraded precious stones (other than diamonds)

iii. Synthetic or reconstructed precious stones

iv. Synthetic or reconstructed semi-precious stones, unworked or simply sawn or roughly

shaped

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-06-2018-cgst-rate-

english.pdf;jsessionid=1B0FA49206A996CFDF66444A0BB29E24

http://www.cbec.gov.in/resources//htdocs-cbec/gst/Notification-for-CGST-rate-

Schedule.pdf

Exempted Items from CGST

Notification No.7/2018-Central Tax (Rate) dated 25th January 2018 read with Notification No.

2/2017-Central Tax (Rate) dated 28th June 2018

Following items are exempted from CGST:

i. Aquatic feed including shrimp feed and prawn feed, poultry feed & cattle feed,

including grass, hay & straw, supplement & husk of pulses, concentrates &

additives, wheat bran & de-oiled cake [other than rice-bran]

ii. De-oiled rice bran

iii. Cotton seed oil cake

iv. Agricultural implements manually operated or animal driven i.e. Hand tools, such as

spades, shovels, mattocks, picks, hoes, forks and rakes; axes, bill hooks and similar

hewing tools; secateurs and pruners of any kind; scythes, sickles, hay knives, hedge

shears, timber wedges and other tools of a kind used in agriculture, horticulture or

forestry. used in agriculture, horticulture or forestry the words, other than ghamella

v. Vibhuti

vi. Parts for manufacture of hearing aids

Page 24 of 25

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-07-2018-cgst-rate-

english.pdf;jsessionid=95ED242378594E535CA04659B3EC7A01

http://www.cbec.gov.in/resources//htdocs-cbec/gst/Notification-for-CGST-

exemption.pdf

http://www.cbec.gov.in/htdocs-cbec/gst/Notification-for-CGST-rate-Schedule.pdf

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-09-2018-igst-rate-english.pdf

Notification No 9/2018-Central Tax (Rate) dated 25th January 2018 read with notification

45/2017 of Central (Rate) dated 14th November 2017

CGST needs to be charged @ 2.5% for few entities as per notification 45/2017 of Central (Rate)

dated 14th November 2017

The following entry shall be substituted in notification 45/2017, namely:

1. “Public funded research institution or a University or an Indian Institute of Technology or

Indian Institute of Science, Bangalore or a Regional Engineering College, other than a

hospital”;

2. Department of Scientific and Research”, the words “Department of Scientific and

Industrial Research”, shall be substituted.

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-09-2018-cgst-rate-english.pdf

http://www.cbec.gov.in/htdocs-cbec/gst/notfctn-45-cgst-rate-english.pdf

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-10-2018-igst-rate-english.pdf

http://gstcouncil.gov.in/sites/default/files/gst%20rates/notfctn-47-igst-rate-english.pdf

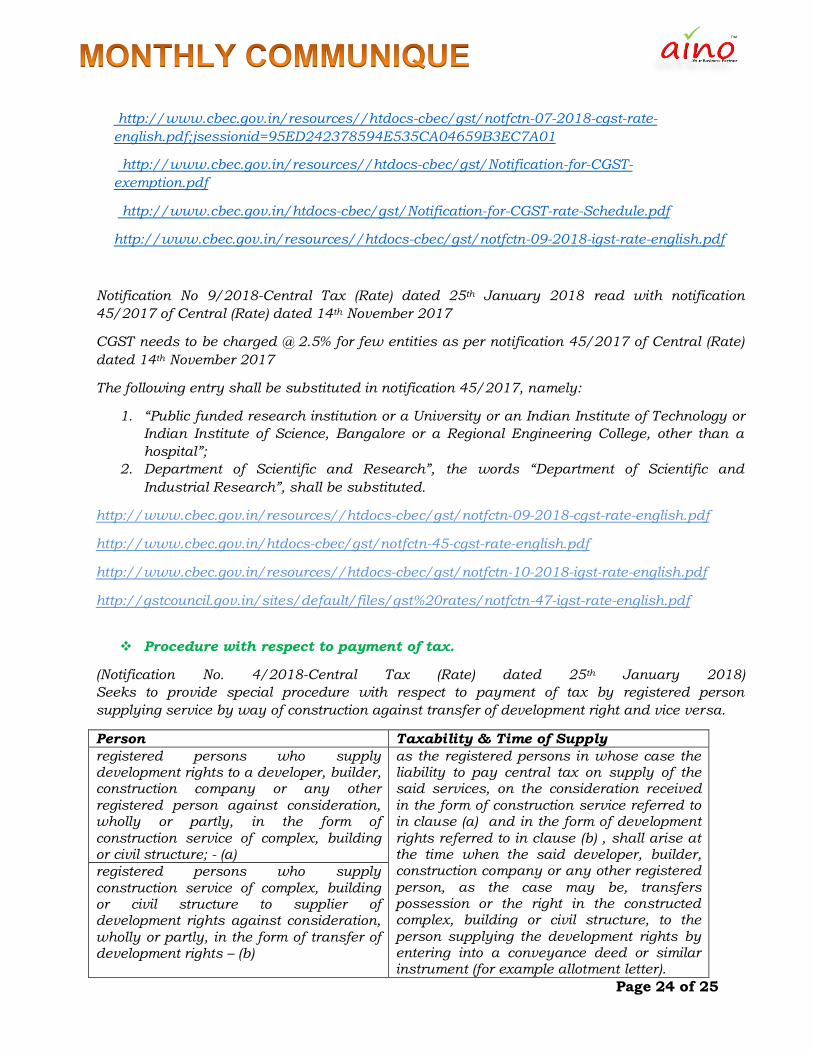

Procedure with respect to payment of tax.

(Notification No. 4/2018-Central Tax (Rate) dated 25th January 2018)

Seeks to provide special procedure with respect to payment of tax by registered person

supplying service by way of construction against transfer of development right and vice versa.

Person Taxability & Time of Supply

registered persons who supply development rights to a developer, builder, construction company or any other registered person against consideration, wholly or partly, in the form of

construction service of complex, building or civil structure; - (a)

as the registered persons in whose case the liability to pay central tax on supply of the said services, on the consideration received in the form of construction service referred to in clause (a) and in the form of development

rights referred to in clause (b) , shall arise at the time when the said developer, builder, construction company or any other registered person, as the case may be, transfers possession or the right in the constructed complex, building or civil structure, to the person supplying the development rights by entering into a conveyance deed or similar instrument (for example allotment letter).

registered persons who supply construction service of complex, building or civil structure to supplier of development rights against consideration, wholly or partly, in the form of transfer of development rights – (b)

Page 25 of 25

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-04-2018-cgst-rate-english.pdf

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-04-2018-igst-rate-english.pdf

Specification Of services supplied by the Central Govt., State Govt. Union Territory, or

Local Territory

(Notification No. 3/2018- Central Tax (Rate) dated 25th January 2018)

Seeks to amend notification No. 13/2017- Central Tax (Rate) so as to specify services supplied

by the Central Government, State Government, Union territory or local authority by way of

renting of immovable property to a registered person under CGST Act, 2017 to be taxed under

Reverse Charge Mechanism (RCM)

Service Service Provider Service Receiver who needs to pay tax under

RCM

Services supplied by the Central Government, State Government, Union territory or local authority by way of renting of immovable property to a person registered under the Central Goods and Services Tax Act, 2017 (12 of 2017).

Central Government, State Government, Union territory or local authority

Any person registered under the Central Goods and Services Tax Act, 2017.

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-03-2018-cgst-rate-english.pdf

http://www.cbec.gov.in/resources//htdocs-cbec/gst/notfctn-03-2018-igst-rate-english.pdf

We are encouraged by our readers and the complements received. In our endeavor to improve

our quality we request you to give two minutes time to give feedback.

write us at–[email protected]

Thanking You,

AINO & Team…!

This is meant for private circulation only

Aino Management Consultancy Private Ltd

No. 18/1, Jain Bhawan, First Floor, Andree Road, Shanthinagar, Bangalore – 560027 Tel . 080 22222143 | 7353444222|

E-Mail : [email protected] Web : www.ainoglobal.com

Follow Us on