a&h module: medishield life

TRANSCRIPT

1For Internal Use Only. Not for Client Presentation

A&H module: MediShield Life

11951/09/21

Confidential and Proprietary Information.2Slide

Disclaimer

This presentation is prepared by Prudential Assurance Company Singapore (Pte) Limited.

The information presented is strictly confidential and for internal use only and cannot be reproduced,

amended or circulated in whole or in part to any other person without our prior written consent.

These should not be used for sales presentation.

Information presented is not exhaustive. For exact terms, conditions and specific details applicable to the

insurance products mentioned, please refer to the relevant Product Summary and Policy Document.

This presentation is for your information only and does not have regard to the specific investment

objectives, financial situation and particular needs of any persons.

The information is accurate as at 16 September 2021 unless otherwise indicated.

Confidential and Proprietary Information.3Slide

Approval from the Company - All marketing collateral, such as advertisements, leaflets, posters, letters, brochures, websites and recruitment materials must be submitted to the Company for approval before distribution.

Basis of Recommendation - Establish link between clients’ needs and recommend products with clear and proper basis of recommendation. Always conduct proper needs-based sales analysis.

Clear, adequate and not false or misleading disclosure- Information to client and product information disclosures must be clear, adequate and not false or misleading. e.g. clearly explain risks associated with products, disclose all fees and charges.

Compliance ABC

Confidential and Proprietary Information.4Slide

What is MediShield Life?

MediShield Life Benefits

MediShield Life Premiums & Subsidies

MediShield Life & Integrated Plans (IP)

Our Solutions

Updates

Agenda

Confidential and Proprietary Information.5Slide

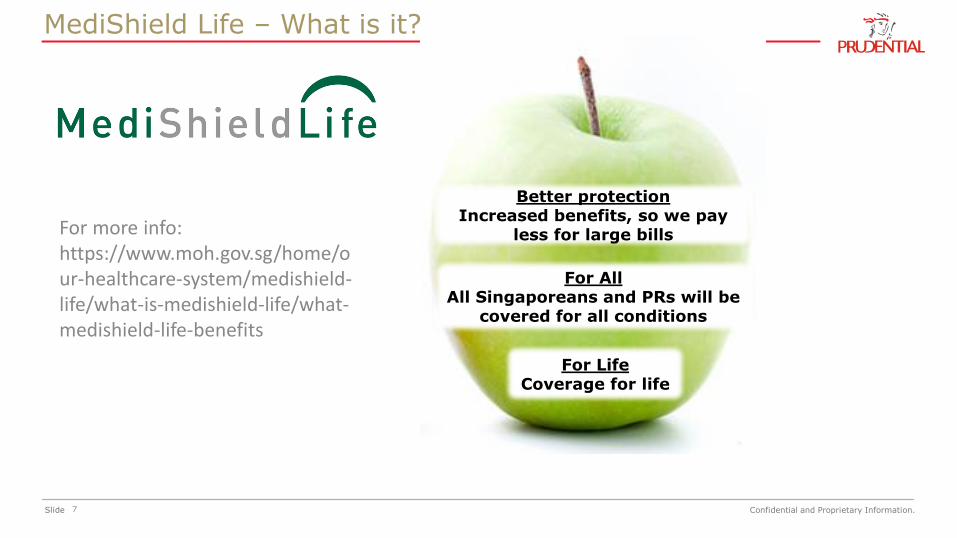

LaunchedNov 2015

MediShield Life (MSHL) is a national health insurance scheme that provides lifelong protection for all Singapore Citizens and

Permanent Residents against large hospital bills.

What is MediShield Life?

Confidential and Proprietary Information.6Slide

What is MediShield Life?

MediShield Life Benefits

MediShield Life Premiums & Subsidies

MediShield Life & Integrated Plans (IP)

Our Solutions

Updates

Agenda

Confidential and Proprietary Information.7Slide

For AllAll Singaporeans and PRs will be

covered for all conditions

For LifeCoverage for life

Better protectionIncreased benefits, so we pay

less for large bills

MediShield Life – What is it?

For more info: https://www.moh.gov.sg/home/our-healthcare-system/medishield-life/what-is-medishield-life/what-medishield-life-benefits

Confidential and Proprietary Information.8Slide

• MediShield Life will cover all Singaporeans & PRs, including those with pre-existing conditions

• Those with serious *pre-existing conditions pay a flat Additional Premium of 30% of MediShield Life premiums for 10 years.

-Meant to be symbolic to reflect higher risk

-Does not cover full cost

For All, For Life

https://www.moh.gov.sg/home/our-healthcare-system/medishield-life/what-is-medishield-life/coverage-for-pre-existing-conditions *

Confidential and Proprietary Information.9Slide

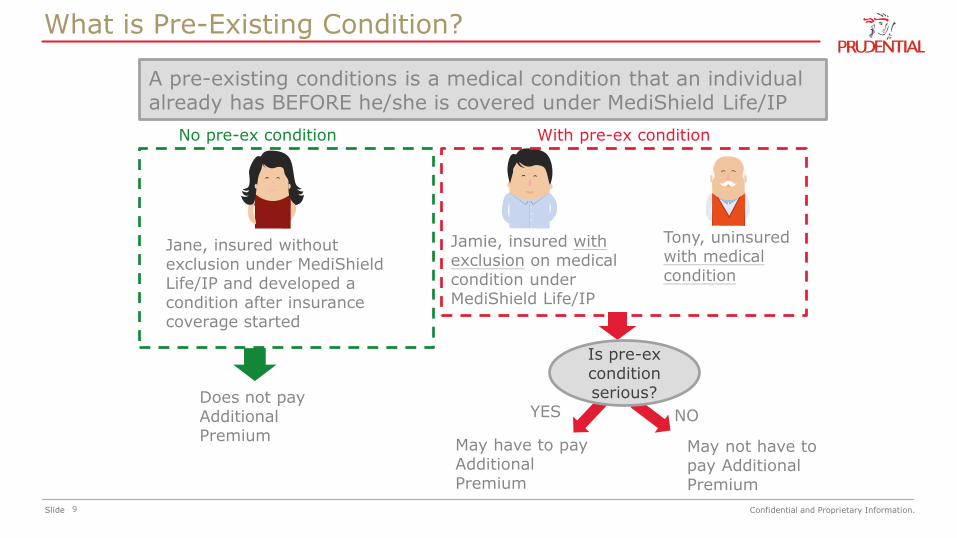

A pre-existing conditions is a medical condition that an individual already has BEFORE he/she is covered under MediShield Life/IP

Jane, insured without exclusion under MediShield Life/IP and developed a condition after insurance coverage started

Jamie, insured with exclusion on medical condition under MediShield Life/IP

Does not pay Additional Premium

May have to pay Additional Premium

YES

May not have to pay Additional Premium

Tony, uninsured with medical condition

NO

Is pre-ex condition serious?

With pre-ex conditionNo pre-ex condition

What is Pre-Existing Condition?

Confidential and Proprietary Information.10Slide

• Applicable to serious pre-ex conditions

–The Ministry has conducted an extensive review on the serious pre-existing conditions that will be subjected to Additional Premiums, with specialist advice from clinicians.Examples of serious pre-existing conditions:

• Life-threatening and may result in permanent disability

• Have high-risk of future complications or recurrence and/or may require prolonged treatment

• Stroke, cancer, kidney failure and heart diseases

Individuals will be notified individually before the start of MediShield Life if they have to pay the 30% Additional Premium

What conditions will the Additional Premiums be applied to?

Confidential and Proprietary Information.11Slide

Better Protection

• MediShield Life is targeted at Class B2/C coverage.

• MediShield Life pays out a level of benefits for private hospital or Class A/B1 bills that is pegged to the equivalent Class B2/C expenses

-If you are hospitalised in a Class B1 ward, your bill will be pro-rated by 43% (SC) and 38% (PR) before the MediShield Life payout is calculated

-If you are hospitalised in a Class A ward/private hospital, your bill will be pro-rated by 35% before the MediShield Life payout is calculated

• MediShield Life will continue to pay for a small portion of higher ward stays

Confidential and Proprietary Information.12Slide

MediShield Life Benefits

Source: https://www.moh.gov.sg/home/our-healthcare-system/medishield-life/what-is-medishield-life/what-medishield-life-benefits

Note: MSHL payouts are subjected to deductible, co-insurance and respective policy & benefits limits

Confidential and Proprietary Information.13Slide

MediShield Life Benefits – Your Claim

Source: https://www.moh.gov.sg/home/our-healthcare-system/medishield-life/what-is-medishield-life/how-to-make-a-medishield-life-claim

You are responsible to pay for parts A, B & C of your claim

• (A) Maximum Claim Limit: $100,000 per policy year

• (B) Deductibles: Fixed amount you have to pay per year before any claim is payable

• (C) Co-insurance: A percentage of the claimable amount that you have to pay after deductibles. Ranges from 3% to 10% (depending on bill size).

• (D) Portion covered by MSHL

Confidential and Proprietary Information.14Slide

What is MediShield Life?

MediShield Life Benefits

MediShield Life Premiums & Subsidies

MediShield Life & Integrated Plans (IP)

Our Solutions

Updates

Agenda

Confidential and Proprietary Information.15Slide

1. MediShield Life premiums are risk-pooled to support the payouts

and benefits under MediShield Life.

2. Government provides significant support to keep premiums

affordable for Singapore Citizens and Permanent Residents

3. This includes those who need to pay Additional Premiums.

MediShield Life Premiums & Subsidies

Confidential and Proprietary Information.16Slide

Government will provide support for MediShield Life premiums, to keep them affordable

Premium Subsidies for Low to Medium Income

Transitional Subsidies

Pioneer Generation Subsidies

Additional premium

support for the needy

MediShield Life Premiums & Subsidies

Confidential and Proprietary Information.17Slide

Merdeka Generation Subsidies and MediSave top-ups

https://www.mof.gov.sg/news-publications/press-releases/pioneer-and-merdeka-generation-seniors-to-receive-278-million-in-medisave-top-ups-in-july-2021

MediShield Life Premiums & Subsidies

Confidential and Proprietary Information.18Slide

Range between 15 - 50%

+ +

You live in HDB FlatOR in Private Housing with Annual Value ≤$21,000

Your Household Monthly Income per Household member is ≤ $2,800

You do not own any property, or have only one property to your name

Premium Subsidies for Lower to Middle Income

Confidential and Proprietary Information.19Slide

Age Next BirthdaySubsidies as a percentage of premiums

(for Singapore Citizens, non Pioneer Generation)

Monthly HH income per person? $1,200 or less $1,201 to $2,000 $2,001 to $2,800

Annual value of property? < $13,000* (includes all HDB flats)

Does individual own multiple property?

No

1 – 40yo 25% 20% 15%

41 – 60yo 30% 25% 20%

61 – 75yo 35% 30% 25%

76 – 85yo 40% 35% 30%

86 – 90yo 45% 40% 35%

>90 50% 45% 40%

• If AV is higher than $13k but less than $21k, will receive 10% points less than listed subsidy rates.• PRs receive 50% subsidies to that of a similar Singaporean • https://www.moh.gov.sg/cost-financing/healthcare-schemes-subsidies/medishield-life/medishield-life-

premiums-and-subsidies/premium-subsidy-tables

Premium Subsidy Table

Confidential and Proprietary Information.20Slide

MediShield premium

MSHL premium BEFORE subsidy

MediShield Premium

MediShield premium

MediShield Life premium

Increase in Premiums

What is net premium increase?

Confidential and Proprietary Information.21Slide

MediShield Life premium payable

MediShield premium

MSHL premium BEFORE subsidy

With MSHLAFTER subsidy

MediShield Premium

Subsidy

MediShield premium

MediShield Life premium

Increase in Premiums

Net Premium Increase

What is net premium increase?

Confidential and Proprietary Information.22Slide

MediShield Life premium payable

MediShield premium

MSHL premium BEFORE subsidy

With MSHLAFTER subsidy

MediShield Premium

Subsidy

MediShield premium

MediShield Life premium

Increase in Premiums

Net Premium Increase

What is net premium increase?

Confidential and Proprietary Information.23Slide

MediShield Life premium payable

MediShield premium

With MSHLAFTER subsidy

MediShield Premium

Subsidy

What happens if subsidies are large?

Confidential and Proprietary Information.24Slide

✓ Given to all Pioneers.

✓ More generous than premium subsidies for non-pioneers.

✓ Pioneers receive special MediShield Life premium subsidies of between 40% –60%, depending on age.

✓ Pioneers will also receive $250 - $900 a year in MediSave top-ups (depending on year of birth) for life, which can be used to pay for their MediShield Life premiums

Who are they?Special generation of Singaporeans are aged 65 and older by the end of 2014.Obtained citizenship on or before 31 December 1986

Source: https://www.moh.gov.sg/medishield-life/medishield-life-premiums-and-subsidies

Pioneer Generation Subsidies and MediSave top-ups

Confidential and Proprietary Information.25Slide

• No one will drop out because of inability to afford premiums

• Meant for needy Singaporeans, who cannot afford MSHL premiums even after subsidies

• IP policyholders are not eligible for Additional Premium Support

• However, if IP policyholders fall into financial difficulty and have to drop their IP, they will retain their MSHL coverage and be eligible for Additional Premium Support if they cannot afford their MSHL premiums.

Additional Premium Support for Needy

Confidential and Proprietary Information.26Slide

✓ From 1 July 2019, Merdeka Generation seniorswill receive additional Merdeka GenerationSubsidies of 5% of their annual MediShield Lifepremiums, increasing to 10% after they turn75 years old, regardless of their householdmonthly income or the Annual Value of theirhome. This is on top of the existing PremiumSubsidies that the seniors may receive.

✓ Merdeka Generation members will also receive$200 a year in MediSave top-ups, every Julyfor five years from 2019 to 2023. These top-ups can be used to pay for their MediShieldLife premiums.

https://www.mof.gov.sg/news-publications/press-releases/pioneer-and-merdeka-generation-seniors-to-receive-278-million-in-medisave-top-ups-in-july-2021

Merdeka Generation Subsidies and MediSave top-ups

Confidential and Proprietary Information.27Slide

Source: https://www.merdekageneration.sg/

Merdeka Generation Subsidies and MediSave top-ups

Who are they?

You are eligible for the Merdeka Generation Package if you:

• Were born from 1 January 1950 to 31 December 1959; and• Became a Singapore citizen on or before 31 December 1996.

The Merdeka Generation Package is also given to seniors who:

• Were born on or before 31 December 1949; and• Became Singapore citizens on or before 31 December 1996; and• Do not receive the Pioneer Generation Package

Confidential and Proprietary Information.28Slide

Source: https://www.merdekageneration.sg/

COVID-19 Subsidies

Confidential and Proprietary Information.29Slide

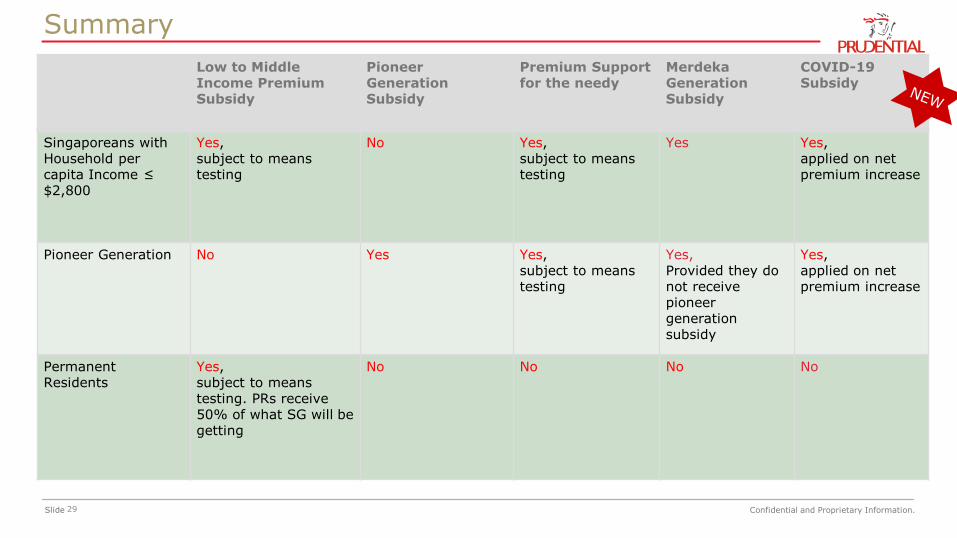

Low to Middle Income Premium Subsidy

Pioneer Generation Subsidy

Premium Support for the needy

Merdeka Generation Subsidy

COVID-19 Subsidy

Singaporeans with Household per capita Income ≤ $2,800

Yes, subject to means testing

No Yes, subject to means testing

Yes Yes, applied on net premium increase

Pioneer Generation No Yes Yes, subject to means testing

Yes, Provided they do not receive pioneer generation subsidy

Yes, applied on net premium increase

Permanent Residents

Yes, subject to means testing. PRs receive 50% of what SG will be getting

No No No No

Summary

Confidential and Proprietary Information.30Slide

Check out the Premium Calculator at https://www.moh.gov.sg/cost-financing/healthcare-schemes-subsidies/medishield-

life/medishield-life-premiums-and-subsidies/medishield-life-premium-calculator

How to get a quick premium estimation?

Confidential and Proprietary Information.31Slide

MediShield Life Premium calculator

Confidential and Proprietary Information.32Slide

What is MediShield Life?

MediShield Life Benefits

MediShield Life Premiums & Subsidies

MediShield Life & Integrated Plans (IP)

Our Solutions

Updates

Agenda

Confidential and Proprietary Information.33Slide

COMMON MISCONCEPTIONS“MediShield Life is duplicate coverage + double payment!”“We are not eligible for MediShield Life premium subsidies”

“We don’t benefit from MediShield Life!”

66% of

Singaporeans have IPs

Most Do not know how IPs and MediShield are related

Integrated Plans (IP) – Did you know?

Source: https://sbr.com.sg/healthcare/news/chart-day-two-thirds-singapores-population-covered-insurance-programme

Confidential and Proprietary Information.34Slide

About Integrated Shield Plans

Confidential and Proprietary Information.35Slide

Additional Private

Insurance Coverage

Inte

gra

ted S

hie

ld

Pla

n

• Provides basic coverage targeted at large hospital bills in Class B2/C (public hospitals)

• Administered by CPF Board

•Provides additional benefits and higher coverage in Class B1/A (public hospital) and Private Hospitals •Additional coverage administered by private insurer

MediShieldLife

Scope of Coverage Premiums

• Policyholders pay an additional premium for the additional private insurance coverage• Payable by MediSave up to a certain limit; some cash outlay may be needed

•Policyholders pay a basic MSHL premium• Fully payable by MediSave

All Integrated Shield Plan policyholders are already covered by MediShield Life.There is NO duplicate coverage, and there is NO double premium payment.

How are IPs related to MediShield/MediShield Life?

2 components

Confidential and Proprietary Information.36Slide

Premiums: first paid to IP insurer who will then pay to CPF

Claims: first paid by IP insurer who will then take from CPF

How do IP premiums and claims work?

Confidential and Proprietary Information.37Slide

With MSHL

• Jamie will be covered by MSHL for all conditions.

• The exclusion on knee-related conditions will only be applied on the addtl private insurance

Payout:

Today

Coverage: • Jamie is covered by an IP, but has an exclusion on knee-related conditions

Additional private

insurance coverage

No payout

MediShield Life

MSHL pays out

When he is hospitalised for a knee injury….

Example: Impact of MSHL on IP policyholder with an exclusion

Confidential and Proprietary Information.38Slide

• Yes, IF they meet the eligibility criteria.• The applicable subsidies will be applied on the

MediShield Life portion of their IP

Can IP policyholders receive premium subsidies?

Confidential and Proprietary Information.39Slide

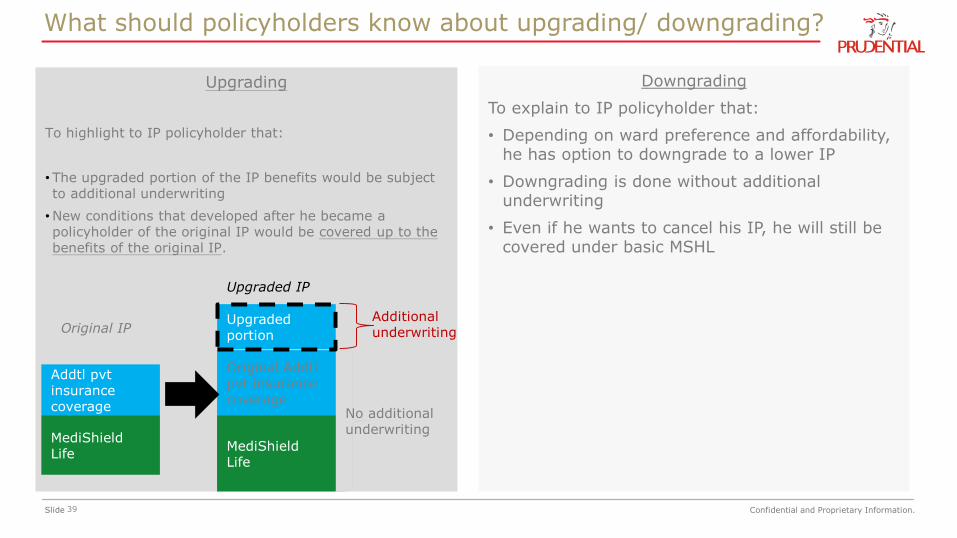

Upgrading

To highlight to IP policyholder that:

• The upgraded portion of the IP benefits would be subject to additional underwriting

•New conditions that developed after he became a policyholder of the original IP would be covered up to the benefits of the original IP.

MediShield Life

Addtl pvtinsurance coverage

MediShield Life

Original Addtlpvt insurance coverage

No additional underwriting

Upgraded portion

Additional underwritingOriginal IP

Upgraded IP

Downgrading

To explain to IP policyholder that:

• Depending on ward preference and affordability, he has option to downgrade to a lower IP

• Downgrading is done without additional underwriting

• Even if he wants to cancel his IP, he will still be covered under basic MSHL

What should policyholders know about upgrading/ downgrading?

Confidential and Proprietary Information.40Slide

MediShield Life premiums

Additional private insurance premiums

• You are able to use your MediSave account to pay for your Integrated Shield Plan’s premiums, subject to the Additional Premium Limits (AWL).

• Cash outlay may be required for premiums above the AWL.

IP

P

rem

ium

AWL

Fully payable by Medisave

LegendAWL: Additional Withdrawal Limit

What is the withdrawal limits for Integrated Shield Plan?

Additional Withdrawal Limits for IP

• ANB 1 to 40: $300• ANB 41 to 70: $600• ANB 71 and above: $900

Confidential and Proprietary Information.41Slide

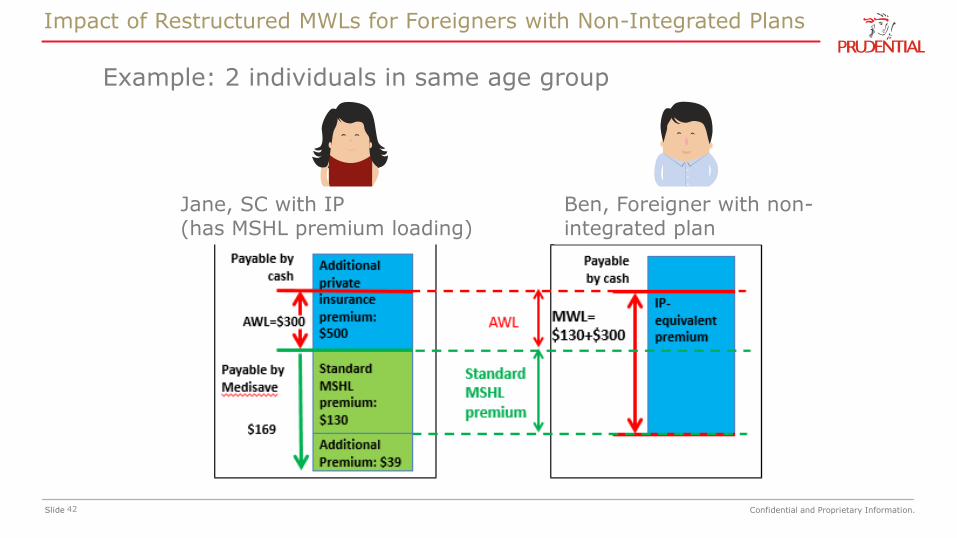

IP-equivalent plan does not have MSHL component, but premiums are payable by Medisave

MWL for full IP-equivalent premium = Standard MSHL premium +AWL

2 tier approach for IPs (ie: integrated with MSHL component)

Additional private insurance premium

Standard MSHLPremium

AWL

Payable by cash

Payable by Medisave

IP-equivalent premiumMWL

Payable by cash

Additional Premium

Standard MSHL premium

AWL

For SC/PRs For Foreigners

Approach towards Foreigners with Non-Integrated Plans

Confidential and Proprietary Information.42Slide

Example: 2 individuals in same age group

Ben, Foreigner with non-integrated plan

Jane, SC with IP (has MSHL premium loading)

Impact of Restructured MWLs for Foreigners with Non-Integrated Plans

Confidential and Proprietary Information.43Slide

The significance of 30% loading is symbolic, does not reflect actual costs of coverage. Government will cover the bulk of the costs.

Risk Loading by MediShield Life

• Period of loading: 10 years

• Affected policyholders will be notified individually.

• Conditions subject to MSHL Additional Premiums may differ from those that private insurers consider for risk-loading/exclusions

Confidential and Proprietary Information.44Slide

Standard Integrated Shield Plan

A new Standard Integrated Shield Plan (Standard IP) targeted at Class B1-level coverage has been made available from all IP-insurers from 1 May 2016. The Standard IP is a private insurance product which gives Singaporeans the option of additional coverage beyond MediShield Life, targeted at Public Hospital Class B11.

Standard IP Benefits

The benefits of the Standard IP are identical across all IP insurers. This enables Singaporeans to compare premiums across insurers easily and make an informed decision as to which plan suits their needs. Just like MediShield Life, the Standard IP will offer coverage for hospitalisation stays and selected outpatient treatments and will have co-payment features of claim limits2, deductible and co-insurance.

1. Patients hospitalised in Class B1 wards have a choice of doctor, and Class B1 wards have 4 beds, TV, and are air-conditioned.

The Government provides subsidies of 20% for Public Hospital Class B1 wards for Singapore Citizens.

2. Standard IP benefits are sized to fully cover 9 out of 10 Public Hospital Class B1 bills

Standard IP

Confidential and Proprietary Information.45Slide

MediShield Life

• https://www.moh.gov.sg/cost-financing/healthcare-schemes-subsidies/medishield-life

• https://www.cpf.gov.sg/eSvc/Web/Schemes/MedisaveCalculator/Step1

Check for MediShield/ IP Coverage

• Check at CPFB website > Login Singpass > “My Messages”- Under “Insurance”

Where to get more info?

Confidential and Proprietary Information.46Slide

What is MediShield Life?

MediShield Life Benefits

MediShield Life Premiums & Subsidies

MediShield Life & Integrated Plans (IP)

Our Solutions

Updates

Agenda

Confidential and Proprietary Information.47Slide

• PRUExtra CoPay** - Covers Deductibles and Co-insurance

**PRUExtra CoPay can only be added to PRUShield (as charged) plans^ MediShield Life is not available to Foreigners

• PRUShield Plus- Covers treatment up to Class A ward in Restructured Hospitals level

• PRUShield Premier- Covers treatment up to standard room in Private Hospitals level

• MediShield Life^

- MediShield Life is a basic health insurance plan, administered by the CPF Board that provides coverage up to Class B2/C ward level in Restructured Hospitals (limits apply)

Co-InsDeductible

Private Hospitals

Restructured Hospitals

Class C / B2

• Cash• MediSave

Main Plan

Main Plan

Optional Rider

Healthcare Financing in Singapore

• PRUShield Standard- Covers treatment up to Class B1 ward in

Restructured Hospitals level

Main Plan

Confidential and Proprietary Information.48Slide

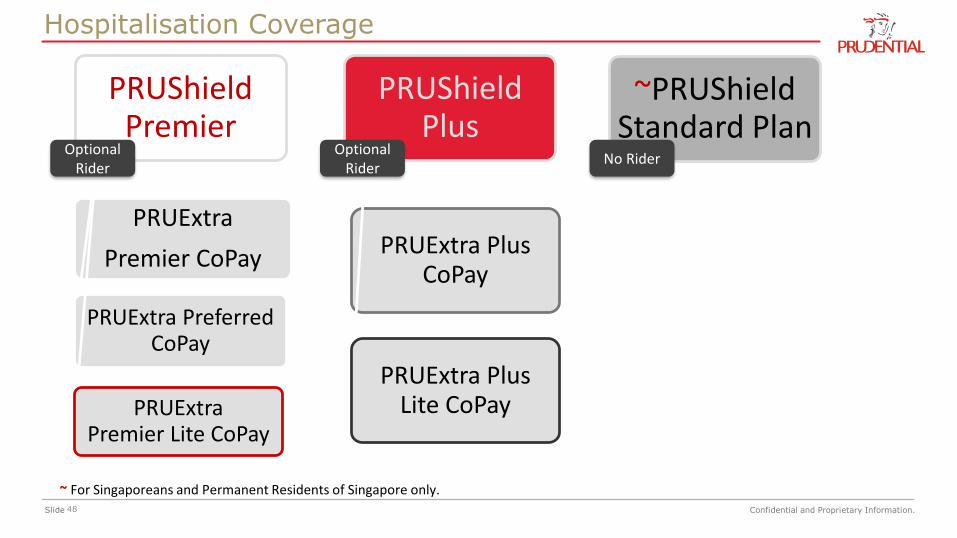

PRUShieldPremier

PRUExtra

Premier CoPay

PRUExtra Preferred CoPay

PRUExtraPremier Lite CoPay

PRUShieldPlus

PRUExtra Plus CoPay

PRUExtra Plus Lite CoPay

~PRUShieldStandard Plan

Optional Rider

Optional Rider

No Rider

Hospitalisation Coverage

~ For Singaporeans and Permanent Residents of Singapore only.

Feb 2021 Confidential and Proprietary Information.49Slide

PRUShield Suite of Base and Supplementary Plans

Private health insurance plan on top of MSHL to extend medical coverage up to Class B1 wards

in a Public Hospital

03

Not Applicable

PRUShieldStandard

Supplementary plan

As charged private health insurance plan on top of MSHL

to extend medical coverage for a Standard ward in a Private

Hospital

01PRUShield

Premier

Supplementary plan

PRUExtraPremierCoPay

PRUExtraPreferred

CoPay

PRUExtraPremier Lite

CoPay

All Singapore

Private Hospitals

All Singapore

Private Hospitals

SingaporePrivate

Hospitals under our Panel or

Non-panel providers

As charged private health insurance plan on top of MSHL to

extend medical coverage up to Class A wards in a Public

Hospital

02PRUShield

Plus

Supplementary plan

PRUExtraPlus CoPay

SingaporePublic Hospitals(Class A Ward)

PRUExtraPlus Lite CoPay

Confidential and Proprietary Information.50Slide

✓ Comprehensive as-charged cover for hospitalisation and medical treatments

✓ Covers up to 95% of the PRUShield deductible and half of the PRUShield co-insurance

✓ 180 days for pre- and 365 days for post-hospitalisation treatments for all conditions (longest in the market)

✓ Planned Overseas Medical Treatment Cover

✓ Future Insurance Option

What does PRUShield and PRUExtra offer today?

Confidential and Proprietary Information.51Slide

Private Hospital

Air-conditioned single, 2-bedded or 4-bedded room with attached bathroom and its luxury toiletries. Fully furnished with sofa bed, flat screen television, DVD player and free-wifi. Patients have freedom to choose the attending physicians.

Restructured 'A' Class Ward

Air-conditioned single or 2-bedded room with attached bathroom. Fully furnished with wardrobe, electronic safe, television and telephone. Patients have freedom to choose the attending physicians.

'B1' Class Ward

Air-conditioned 4-bedded ward with attached bathroom, television and telephone.Patients have freedom to choose the attending physicians.

'B2' Class Ward (for subsidisedpatients)

Fan-ventilated 6-bedded ward with shared bathroom facilities and amenities.

'C' Class Ward (for subsidisedpatients)

Fan-ventilated 8-bedded ward with shared bathroom facilities and amenities.

Source: www.nuh.com.sg and www.mountelizabeth.com.sg, 2016

PRUShield & PRUExtraPremier/ Premier Lite/Preferred CoPay

PRUShield & PRUExtraPlus CoPay / Plus Lite CoPay

PRUShieldStandard Plan

Choices of Hospitals, Wards and Doctors

Confidential and Proprietary Information.52Slide

Policy Year Limit $1,200,000 $600,000 $150,000

Living Organ Donor Transplant Benefits$60,000 per Policy Year

$40,000 per Policy Year

Not Covered

Overseas Medical Treatment As Charged As Charged

Pre- & Post-Hospitalisation Benefits As Charged As Charged

Final Expense Provision $5,000 $3,000

Pregnancy Complications benefit As Charged As Charged

Congenital Abnormalities As Charged As Charged

Future Insurance Option at Life Events$100,000 sum assured per life

$100,000 sum assured per life

PRUShieldPremier

PRUShieldPlus

PRUShieldStandard Plan

Hospital / Ward Type Private HospitalRestructured

Hospital(Class A Ward)

Restructured Hospital

(Class B1 Ward)

Hospitalisation Benefit As Charged As Charged Inner Limits

Surgical Benefits As Charged As Charged Inner Limits

Outpatient Hospital Benefits As Charged As Charged Inner Limits

PRUShield Plans – Benefit at a Glance

Confidential and Proprietary Information.53Slide

Important note on switching to PRUShield plans:

✓ Customers who switch their medical insurance plan (from another company) to PRUShield will have to go through medical underwriting

✓ DO NOT switch if there have been changes to customer’s health status since the inception of his/her medical insurance plan with the other company

▪ For customer who had previously bought his/her medical insurance plan (from another company at standard life and has since developed new medical conditions, by switching to PRUShield, he/she will have to go through medical underwriting and PRUShield policy may exclude his/her “pre-existing” medical conditions

▪ Customers need to serve a new waiting period when they switch to PRUShield

Note :

Before replacing an existing accident and health policy with a new one, you should consider whether the switch is detrimental, as there may be potential disadvantages with switching and the new policy may cost more or have fewer benefits at the same cost.

Upgrading medical coverage is subject to underwriting. Customers are advised to purchase sufficient coverage based on their needs.

PRUShield and supplementary plans do not have surrender value

PRUShield (Plus and Premier) Specific risks to customer

Confidential and Proprietary Information.54Slide

▪ Premiums are not guaranteed and may be adjusted based on future claims experience

▪ Premiums are determined based on the age next birthday of the life assured at the time of renewal

▪ For standard life customers who have made a claim, they will not be able to exercise their FIO at Life Events

▪ PRUShield and supplementary plans do not have surrender value

▪ Subject to Underwriting for upgrading of medical coverage

PRUShield (Plus and Premier) Specific risks to customer

Note: Customer are advised to purchase sufficient coverage based on their needs.

Confidential and Proprietary Information.55Slide

Benefits Limitations

Cover hospitalisation benefits

▪ Policy Year limit applies to the total claims paid out each policy year

▪ Deductible and co-insurance apply which are the amounts to be borne by the customers

▪ For PRUShield Plus: Pro-ration factor apply for medical treatments sought in ward higher than the entitled ward

▪ There are certain conditions under which no benefit is payable. These exclusions are stated in the policy document

▪ Premiums are non-guaranteed

PRUShield (Plus and Premier) Benefits & Limitations

Note:PRUShield and supplementary plans do not have surrender value

Confidential and Proprietary Information.56Slide

PRUShield (Plus and Premier) Benefits & Limitations

Benefits Limitations

Cover surgical benefits (Including day surgery)

▪ Policy Year limit applies to the total claims paid out each policy year

▪ Deductible and co-insurance apply which are the amounts to be borne by the customers

▪ For PRUShield Plus: Pro-ration factor apply for medical treatments sought in ward higher than the entitled ward

▪ There are certain conditions under which no benefit is payable. These exclusions are stated in the policy document

Note:PRUShield and supplementary plans do not have surrender value

Confidential and Proprietary Information.57Slide

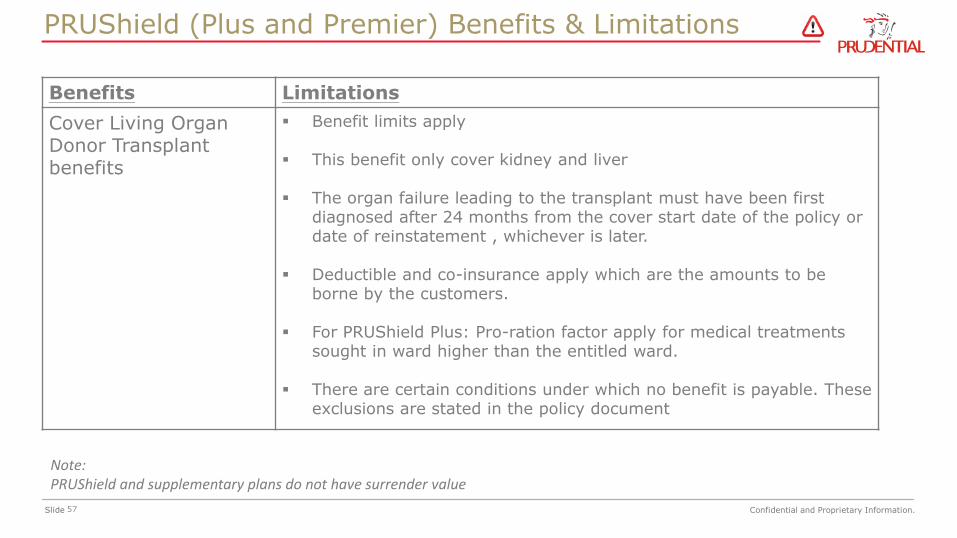

PRUShield (Plus and Premier) Benefits & Limitations

Benefits Limitations

Cover Living Organ Donor Transplant benefits

▪ Benefit limits apply

▪ This benefit only cover kidney and liver

▪ The organ failure leading to the transplant must have been first diagnosed after 24 months from the cover start date of the policy or date of reinstatement , whichever is later.

▪ Deductible and co-insurance apply which are the amounts to be borne by the customers.

▪ For PRUShield Plus: Pro-ration factor apply for medical treatments sought in ward higher than the entitled ward.

▪ There are certain conditions under which no benefit is payable. These exclusions are stated in the policy document

Note:PRUShield and supplementary plans do not have surrender value

Confidential and Proprietary Information.58Slide

PRUShield (Plus and Premier) Benefits & Limitations

Benefits Limitations

Cover pre- and post-hospitalisation benefits incurred 180 days before and 365 days after confinement or day surgery

▪ Policy Year limit applies to the total claims paid out each policy year

▪ Deductible and co-insurance apply which are the amounts to be borne by the customers

▪ For PRUShield Plus: Pro-ration factor apply for medical treatments sought in ward higher than the entitled ward

▪ There are certain conditions under which no benefit is payable. These exclusions are stated in the policy document

Note:PRUShield and supplementary plans do not have surrender value

Confidential and Proprietary Information.59Slide

PRUShield (Plus and Premier) Benefits & Limitations

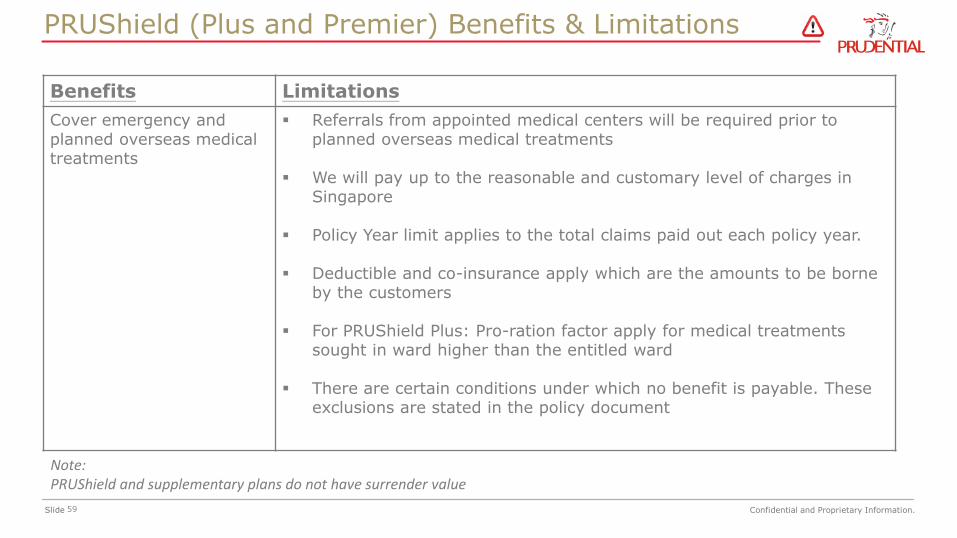

Benefits Limitations

Cover emergency and planned overseas medical treatments

▪ Referrals from appointed medical centers will be required prior to planned overseas medical treatments

▪ We will pay up to the reasonable and customary level of charges in Singapore

▪ Policy Year limit applies to the total claims paid out each policy year.

▪ Deductible and co-insurance apply which are the amounts to be borne by the customers

▪ For PRUShield Plus: Pro-ration factor apply for medical treatments sought in ward higher than the entitled ward

▪ There are certain conditions under which no benefit is payable. These exclusions are stated in the policy document

Note:PRUShield and supplementary plans do not have surrender value

Confidential and Proprietary Information.60Slide

PRUShield (Plus and Premier) Benefits & Limitations

Benefits Limitations

Cover selected outpatient treatments (cancer treatments, renal failure treatment and approved immunosuppressant drugs for organ transplant)

▪ Policy Year limit applies to the total claims paid out each policy year

▪ Co-insurance apply which are the amounts to be borne by the customers

▪ For PRUShield Plus: Pro-ration factor apply for medical treatments sought in ward higher than the entitled ward

▪ There are certain conditions under which no benefit is payable. These exclusions are stated in the policy document

Note:PRUShield and supplementary plans do not have surrender value

Confidential and Proprietary Information.61Slide

PRUShield (Plus and Premier) Benefits & Limitations

Benefits Limitations

Provide other benefits

(Final Expense Provision, Pregnancy Complications benefit, Congenital Abnormalities, Inpatient Psychiatric Treatment benefit, Short Stay Ward and Future Insurance Option at Life Events)

▪ Waiting period of 10 months apply for pregnancy complications and 24 months for congenital abnormalities benefits

▪ Benefit limits apply for some benefits

▪ Policy Year limit applies to the total claims paid out each policy year

▪ Deductible and co-insurance apply which are the amounts to be borne by the customers

▪ For PRUShield Plus: Pro-ration factor apply for medical treatments sought in ward higher than the entitled ward

▪ There are certain conditions under which no benefit is payable. These exclusions are stated in the policy document

▪ The “Future Insurance Option” at life event is capped at $100,000 sum assured in PRUShield (As Charged – Premier & Plus)

Note:PRUShield and supplementary plans do not have surrender value

Confidential and Proprietary Information.62Slide

• Customers age 1 to 75 next birthday

• Customers who are not expecting “returns” from a Non-Participating policy

• Customers who can afford to fund the premiums using MediSave (for PRUShield as charged) and/or Cash

• Customers who are looking for more comprehensive coverage than MediShield Life to cover their medical bills

• Customers who are looking for coverage up to A Ward in Restructured Hospitals

• Customers who are not expecting surrender value from their policy

PRUShield Plus Appropriate Customer Segments

Confidential and Proprietary Information.63Slide

PRUShield Plus Inappropriate Customer Segments

Customers who want returns from their policy

Customers who want level and guaranteed premiums throughout the premium payment period

Customers who want coverage up to standard room in Private Hospitals

Customers who want surrender value from their policy

Confidential and Proprietary Information.64Slide

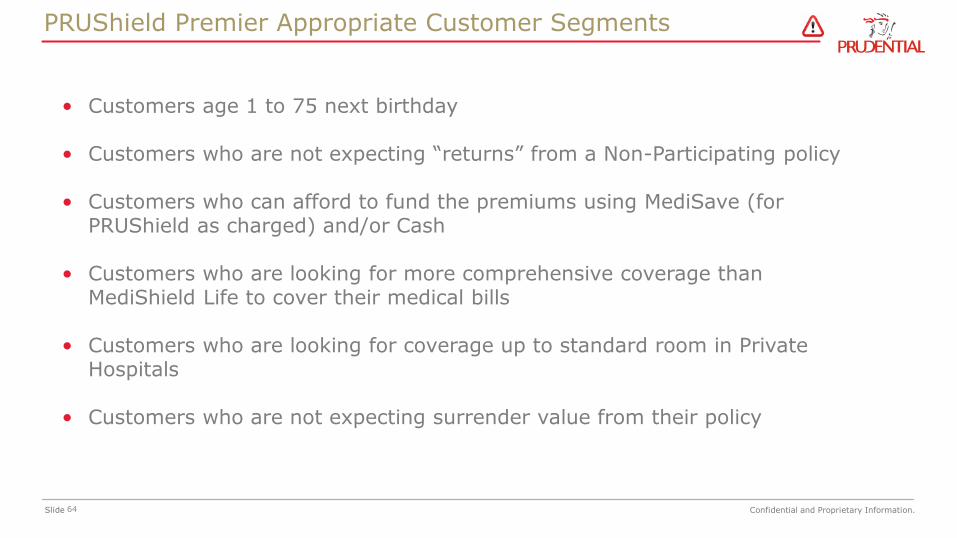

PRUShield Premier Appropriate Customer Segments

• Customers age 1 to 75 next birthday

• Customers who are not expecting “returns” from a Non-Participating policy

• Customers who can afford to fund the premiums using MediSave (for PRUShield as charged) and/or Cash

• Customers who are looking for more comprehensive coverage than MediShield Life to cover their medical bills

• Customers who are looking for coverage up to standard room in Private Hospitals

• Customers who are not expecting surrender value from their policy

Confidential and Proprietary Information.65Slide

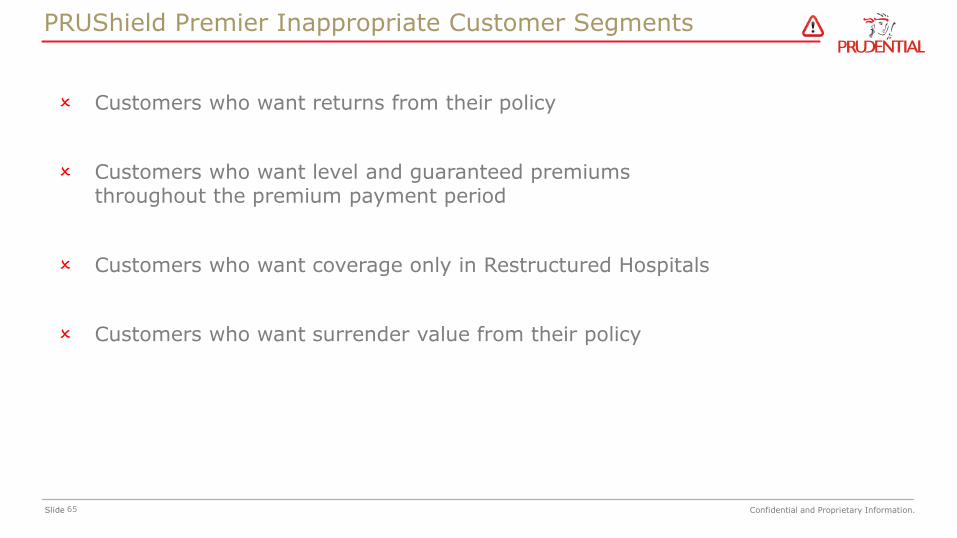

PRUShield Premier Inappropriate Customer Segments

Customers who want returns from their policy

Customers who want level and guaranteed premiums throughout the premium payment period

Customers who want coverage only in Restructured Hospitals

Customers who want surrender value from their policy

Confidential and Proprietary Information.66Slide

Benefits Risks and Limitations

Inpatient and Day Surgery Benefits ▪ Premiums are non-guaranteed and increase with age.▪ Policy Year limit applies to the total claims paid out each policy

year.▪ Deductible and co-insurance apply which are the amounts to be

borne by the customers. ▪ Pro-ration factors apply for medical treatments sought in ward

higher than the entitled ward. ▪ There are certain conditions under which no benefit is payable.

These exclusions are stated in the policy document.▪ The cover will terminate upon cessation of Singapore

Citizen/PR status

Outpatient Treatments Benefits ▪ Policy Year limit applies to the total claims paid out each policy year.

▪ Co-insurance applies which is the amount to be borne by the customers.

▪ Pro-ration factors apply for medical treatments sought in ward higher than the entitled ward.

▪ There are certain conditions under which no benefit is payable. These exclusions are stated in the policy document.

▪ The cover will terminate upon cessation of Singapore Citizen/PR status

Benefits Risks and Limitations – PRUShield Standard Plan

Note: PRUShield and supplementary plans do not have surrender value

Confidential and Proprietary Information.67Slide

Appropriate

• Customers who are looking for basic medical and hospitalisation cover that is higher than MediShield Life

• Customers who mainly need local medical cover in Singapore

Inappropriate

• Customers who are looking for medical and hospitalisation cover in higher ward class (e.g. A class ward in restructured hospitals or standard room in private hospitals)

• Customers who wish to get comprehensive medical coverage.

• Customers who need overseas medical coverage

Customer Segment – PRUShield Standard Plan

Note: PRUShield and supplementary plans do not have surrender value

Confidential and Proprietary Information.68Slide

What is MediShield Life?

MediShield Life Benefits

MediShield Life Premiums & Subsidies

MediShield Life & Integrated Plans (IP)

Our Solutions

Updates

Agenda

Nov 2020 Confidential and Proprietary Information.69Slide

Changes to MSHL: With effect from 1st March 2021

MSHL PremiumsAdjustment

MSHL Changes to Benefits

Nov 2020 Confidential and Proprietary Information.70Slide

Changes to PRUShield:

With immediate effect on

1st April 2021Benefits update

for PRUShield Plans

Nov 2020 Confidential and Proprietary Information.71Slide

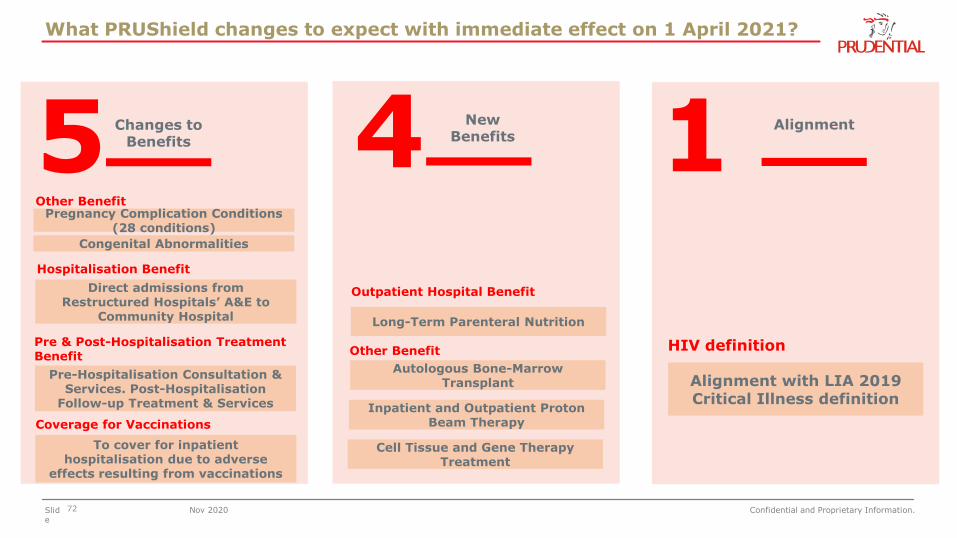

1Alignments

What PRUShield changes to expect with immediate effect on 1 April 2021?

5Changes to

Benefits

4New

Benefits

Nov 2020 Confidential and Proprietary Information.72Slide

1

What PRUShield changes to expect with immediate effect on 1 April 2021?

4 New Benefits

Outpatient Hospital Benefit

Long-Term Parenteral Nutrition

Other BenefitPregnancy Complication Conditions

(28 conditions)

Congenital Abnormalities

Other Benefit

Autologous Bone-Marrow Transplant

Inpatient and Outpatient Proton Beam Therapy

Cell Tissue and Gene Therapy Treatment

Hospitalisation Benefit

Direct admissions from Restructured Hospitals’ A&E to

Community Hospital

HIV definition

Alignment with LIA 2019 Critical Illness definition

5 Changes to Benefits

Pre & Post-Hospitalisation TreatmentBenefit

Pre-Hospitalisation Consultation & Services. Post-Hospitalisation

Follow-up Treatment & Services

Coverage for Vaccinations

To cover for inpatient hospitalisation due to adverse

effects resulting from vaccinations

Alignment

Nov 2020 Confidential and Proprietary Information.73Slide

Overview of Changes to PRUShield Suite from 1 March 2021 & 1 April 2021

PRUShieldPremier

PRUShieldPlus

PRUShieldStandard,A & B Plan

1 March

2021

Premiums

Overall adjustment for SG and/or PR due to MSHL adjustment(No change in IP premiums)

• Reprice of FR (type 1 & 2) premium due to MSHL premium adjustment• FR (type 1) premiums to be aligned with SC/PR/FR (type 2) for PRUShield &

PRUExtra

NA

Age of entryExtending of maximum age of entry for foreigner from 55 ANB to 75 ANB for PRUShield & PRUExtra

1 April

2021

Changes in PRUShield

Benefits

• Pregnancy Complication Conditions• Congenital Abnormalities benefit• Direct admission from Restructured hospitals’ A&E to Community hospitals• Outpatient Telemedicine Consultation for Pre & Post-hospitalisation

Treatment benefit• Coverage for adverse effects for all vaccinations

New Benefits

• Long Term Parenteral Nutrition• Autologous Bone Marrow Transplants• Inpatient and Outpatient Proton Beam Therapy• Cell Tissue and Gene Therapy Treatment

Please note that PRUShield A & B plans had been withdrawn from new business

Nov 2020 Confidential and Proprietary Information.74Slide

TRANSITION

PLAN

PRUExtra

For policiespurchased between

8th Mar 2018 – 31st Mar 2019

Integrated Shield Plan (IP) Rider: Transition to IP With Co-Payment Feature

Nov 2020 Confidential and Proprietary Information.75Slide

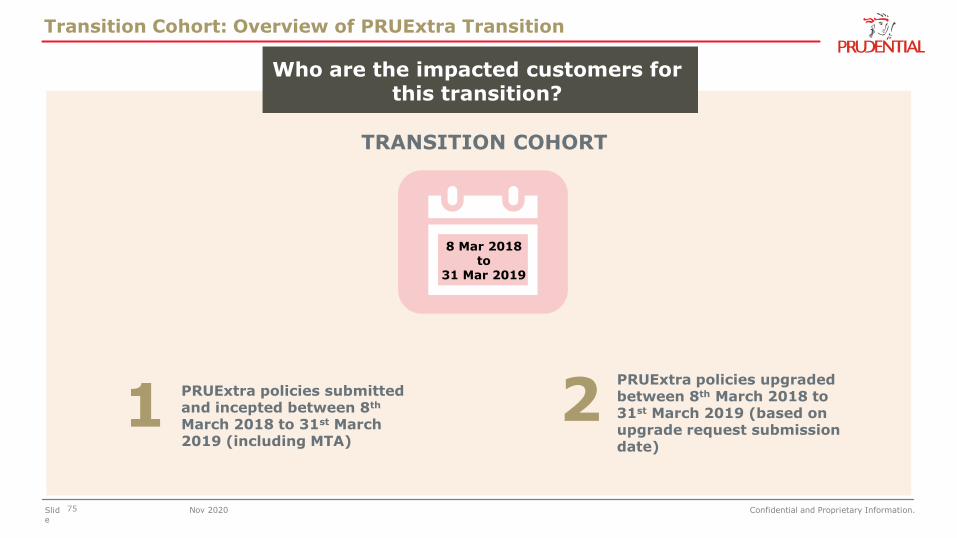

Who are the impacted customers for this transition?

8 Mar 2018to

31 Mar 2019

TRANSITION COHORT

PRUExtra policies upgraded between 8th March 2018 to 31st March 2019 (based on upgrade request submission date)

2PRUExtra policies submitted and incepted between 8th

March 2018 to 31st March 2019 (including MTA)

1

Transition Cohort: Overview of PRUExtra Transition

Nov 2020 Confidential and Proprietary Information.76Slide

Customers who purchased* (including upgrades) the IP rider between 8th

March 2018 to 31st March 2019 will be transitioning to the new IP riders with co-payment features upon their policy renewal from 1st April 2021 onwards.

Purchased between(8th Mar 2018 to 31st Mar 2019)

Transition to(From 1st Apr 2021)

PRUExtra Premier PRUExtra Premier CoPay

PRUExtra Premier Saver^ PRUExtra Premier Lite CoPay (NEW for FR)

PRUExtra Premier Lite PRUExtra Premier Lite CoPay

PRUExtra Plus PRUExtra Plus CoPay

PRUExtra Plus Lite PRUExtra Plus Lite CoPay (NEW)

*Based on proposal submission date^PRUExtra Premier Saver will be withdrawn from downgrade from 9th Feb 2021 onwards

Note: For new business, upgrade/downgrade and MTA of PRUExtra Premier Lite CoPay (FR) and PRUExtra Plus Lite CoPay (SC/PR/FR), it will only be available from 8 June 2021 onwards

Transition Cohort: Overview of PRUExtra Transition

Nov 2020 Confidential and Proprietary Information.77Slide

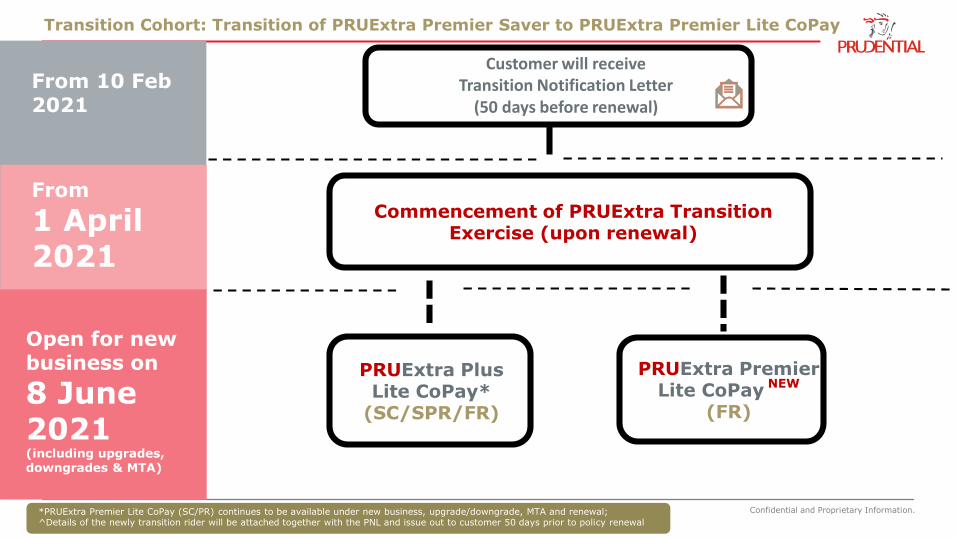

*PRUExtra Premier Lite CoPay (SC/PR) continues to be available under new business, upgrade/downgrade, MTA and renewal;^Details of the newly transition rider will be attached together with the PNL and issue out to customer 50 days prior to policy renewal

Customer will receiveTransition Notification Letter

(50 days before renewal)

Commencement of PRUExtra Transition Exercise (upon renewal)

From 10 Feb 2021

From

1 April 2021

Open for new business on

8 June 2021(including upgrades, downgrades & MTA)

PRUExtra Plus Lite CoPay*

(SC/SPR/FR)

PRUExtra PremierLite CoPay

NEW

(FR)

Transition Cohort: Transition of PRUExtra Premier Saver to PRUExtra Premier Lite CoPay

Confidential and Proprietary Information.78Slide

Keeping healthcare affordable for everyone

Health Insurance Task Force observed that full cover riders encourage:

This increases healthcare costs and insurance premiums for all Singaporeans.

78

Over-consumption by consumers

Over-servicing by some medical professionals

Over-charging by some medical professionals

As a leading insurer, healthcare accessible and insurance premiums affordable for all in the long run.