a guide to valuing employee stock options with a reload feature

TRANSCRIPT

Journal of Applied Corporate Finance S U M M E R 1 9 9 9 V O L U M E 1 2 . 2

A Guide to Valuing Employee Stock Options with a Reload Feature by Thomas Hemmer, University of Chicago, Steve Matsunaga, University of Oregon, and Terry Shevlin, University of Washington

A GUIDE TO VALUINGEMPLOYEE STOCKOPTIONS WITH ARELOAD FEATURE

by Thomas Hemmer,University of Chicago,Steve Matsunaga,University of Oregon, andTerry Shevlin,University of Washington*

118BANK OF AMERICA JOURNAL OF APPLIED CORPORATE FINANCE

based guide to valuing a REO using the modelderived in a paper we published in 1998 (hereafterreferred to as “HMS (1998)”).2

In HMS (1998), we demonstrated that a reloadoption provides the holder with a dominant strategyof exercising an option as soon as it is in-the-money.This property of reload options enabled us to derivea “closed form” valuation model that is independentof individual risk-preferences. The risk-independentvaluation model for reload options is in stark contrastto existing valuation models for ESOs, which, asdiscussed in Statement of Financial AccountingStandards No. 123 (SFAS 123), depend upon theemployee’s exercise strategy. The exercise strategyin turn depends upon individual-specific factors,such as liquidity needs and tolerance for risk.3 Forthis reason, as we show in this paper, one advantage(largely unsuspected until now) of reload optionsover standard ESOs is that their value can beestimated with greater precision.4

We use the Kellogg Company as an example todemonstrate the application of the HMS model in apractical setting and to illustrate the value of thereload feature by comparing the reload option valueto a standard Black-Scholes value. The techniquesshown in this paper can be used by institutionalinvestors, compensation consultants, instructors,researchers, employees of firms that grant or areconsidering granting reload options, or any other

*Acknowledgements: Hemmer acknowledges financial support from theWilliam S. Fishman Research Scholarship at the University of Chicago. Shevlinacknowledges financial support from the Accounting Development Fund and theBusiness School Research Fund at the University of Washington.

1. “Nice Option If You Can Get It,” Business Week, May 4, 1998, pp. 111-114.2. T. Hemmer, S.R. Matsunaga, and T. Shevlin, “Optimal Exercise and the Value

of Employee Stock Options Granted with a Reload Provision,” Journal ofAccounting Research (1998).

3. The issue of early exercise of standard ESOs has been examined in thefollowing articles: H.A. Mozes, “An Upper bound for the Firm’s Cost of EmployeeStock Options”, Financial Management 24 (1995); S. Huddart and M. Lang,

“Employee Stock Option Exercises: An Empirical Analysis” Journal of Accountingand Economics 21 (1996); and J. Carpenter, “The Exercise and Valuation ofExecutive Stock Options”, Journal of Financial Economics (1998). The value canalso be dependent upon the likelihood that the employee will depart from the firm.For a further discussion of this issue, see C.J. Cuny and P. Jorion, “Valuing ExecutiveStock Options with Endogenous Departure”. Journal of Accounting and Econom-ics 20 (1995).

4. As shown in the following discussion, the fair value of an “unrestricted” REOcan be calculated directly. However, in practice, REOs typically include restrictionson exercise, such as time vesting. The adjustments for time-vesting described inthis paper yield value estimates as opposed to theoretically correct fair values.

if the holder of a reload option pays the strike priceby tendering previously owned shares, he receivesa new option for each share tendered in addition tothe common shares received from the exercise. Thenew reload options received have a strike priceequal to the current fair market value of the commonshares and the same maturity date as the originaloptions. According to an article in Business Weekabout a year ago,1 although the first reload optionplan was adopted only 10 years ago, reload optionswere included in 17% of all new option plans in 1997.

That same article indicated that the increase inthe use of reload options has been somewhatcontroversial. High profile cases of large gains toreload option recipients, such as Sandy Weill, whileat the Travelers Group, have left compensationconsultants, managers, and investors alike dividedover the desirability of using reload options as acompensation vehicle. Much of this controversy,however, appears to be fueled by the existinguncertainty about the magnitude of the values thatare being transferred from existing shareholders toemployees as a result of the use of reload option.The purpose of this paper is to reduce such uncer-tainty by providing the reader with a theoretically

n innovation in executive compensationthat has been gaining both in popularityand public attention is the so-calledreload option. Under a reload provision,

A

VOLUME 12 NUMBER 2 SUMMER 1999119

party interested in estimating the ex ante value of areload option grant.

The lack of a theoretically valid approach tovaluing ESOs in general and REOs in particularbecame apparent during the process that led to SFAS123, the financial accounting standard that offersguidance on the valuation of such options. From theoutset, the Financial Accounting Standards Board(FASB) argued that employee stock options shouldbe valued at the date of grant and that the valuationshould take into account all of the relevant featuresof the stock option, including the presence of areload feature. However, the FASB expressed theconcern that the addition of a reload provisioncomplicates the valuation of the stock option. Theseconcerns are expressed in paragraph 183 of SFAS123, where they state:

Because a reload feature is part of the optioninitially awarded, the Board believes that the valueadded to those options by the reload feature ideallyshould be considered in estimating the fair value ofthe award on the grant date. However, the Boardunderstands that no reasonable method currentlyexists to estimate the value added by a reload feature.

The idea that the addition of a reload featuremakes grant date valuation of the employee stockoption more difficult seems to make sense. How-ever, as mentioned above, the creation of a dominantexercise strategy serves to simplify the problem byeliminating a major problem in the valuation of em-ployee stock options, i.e., uncertain early exercise.5

In this paper, we begin by illustrating the reloadfeature with a simple numerical example and thendemonstrate the use of our valuation model tocalculate the value of the reload option. Next weproceed with a discussion of factors that complicatethe valuation of reload ESOSs, including vestingrequirements, taxes, and dividends. Finally, weapply the model to a specific company and providea comparison of the value of the reload option to thatof a standard employee stock option.6

THE RELOAD STOCK OPTION

To illustrate the mechanics of a reload provi-sion, suppose an employee had 1,000 stock optionswith a strike price of $50 per share and the stock priceappreciated by 25% to $62.50. In order to pay thestrike price of $50,000 ($50 × 1,000), he would tender800 shares ($50,000/$62,500 or 1/1.25 × 1,000). Inexchange, he would receive 1,000 common sharesand 800 options with a strike price of $62.50 pershare with the same maturity date as the originaloptions. The employee’s gain on exercise would be$12,500 (200 shares × $62.50), which is exactly equalto the “in-the-money value.”

As a result of the exercise, the employee haseffectively exchanged 1,000 in-the-money optionsfor 200 shares and 800 at-the-money options. Bydoing so the employee locks in the current gain of$12,500 ($12.50 × 1,000) on his initial option grantwhile still retaining the upside appreciation poten-tial of 1,000 equity securities. And, because thevalue of the new options plus gains can be largerthan, but never smaller than, the initial grant, theholder will always choose to exercise an in-the-money reload option.

This effect of encouraging early exercise isfrequently cited by issuing firms as a reason foradopting a reload provision. In most cases earlyexercise is combined with an objective of increasingmanagement share ownership. A 1992 article byLongnecker and Cross purported to identify a trendto add a “reload” feature to stock options. Accordingto the authors,

Advocates of the reload feature maintain thatit encourages executives not only to exercise optionsearly, but to hold on to shares after exercise. This isbecause (1) these shares can be used in futureexercises and reloads and (2) the reloads help pro-tect the executive in the event of a market down-turn. Given these advantages, it appears there islikely to be an increased use of them in newlyproposed plans.7

5. Note that this only holds for options with an unrestricted reload. If an optiononly allows the holder to reload once, i.e., the options received from a reload donot carry a reload provision, a dominant exercise strategy may not exist and aclosed-form value cannot be determined. For a discussion, see R. Jagannathan andJ. Saly, “Ignoring Reload Features can Substantially Understate the Value ofExecutive Stock Options,”. 1997 working paper, University of Minnesota.

6. In this paper the term “value” refers to the security’s “fair value” andcorresponds to the value required for financial reporting. According to the FASB(SFAS 123 paragraph 9) this is “the amount at which the asset could be bought or

sold in a current transaction between willing parties, that is, other than in a forcedliquidation sale”. Later, the FASB distinguishes this value from the amount of cashcompensation employees would be willing to trade for their stock options. As theFASB points out (SFAS 123 paragraph 147), “The fair values of other financialinstruments do not take into account either the source of the funds with which thebuyer might pay for the instrument or other circumstances affecting individualbuyers.”

7. B.M. Longnecker and S.L. Cross, “New Patterns in Executive Compensation,”Journal of Compensation and Benefits, September-October 1992.

120JOURNAL OF APPLIED CORPORATE FINANCE

Similar sentiments can be found in firm disclosures.For example, in its 1993 proxy statement, Alcoa states,

The continuation (reload) feature of the stockoption program was added to provide further incen-tive for increased stock ownership not only for seniormanagement but also for about 700 other optionees.This feature encourages early exercise of options andretention of Alcoa shares.

In a recent study, we provide some preliminaryevidence to support these claims.8 We find that CEOsof firms that adopt reload plans tend to have lowerlevels of share ownership before making the grants.At the same time, however, we fail to find evidenceof a relation between adoption of a reload provisionand a need for incentive realignment. In particular,we find no evidence of a relation between theadoption of a reload plan and the risk profile of thefirm or the firm’s market-to-book ratio at the time ofadoption. In addition, there is only limited evidenceof a change in the risk profile after the adoption andno evidence of a change in the market-to-book ratio.

A SIMPLE EXAMPLE

In our valuation model, we take a binomialapproach and use St to designate the share price attime t. A typical binomial model states that the pricein each period moves in accordance with the follow-ing process.

uSt–1{dSt–1 (1)

where u > 1 and d = 1/u.In keeping with common practice, we assume

that the option is originally granted with the strikeprice equal to the fair market value on the date ofgrant (S0). Assume that 1,000 American options9 witha reload feature are granted at time t = 0 with a strikeprice set equal to the current fair market value of $50.The options expire at the end of four periods. We setu = 1.25 and d = 1/u = 0.80; this means that, in eachperiod, the price can either increase by 25% ordecrease by 20%.

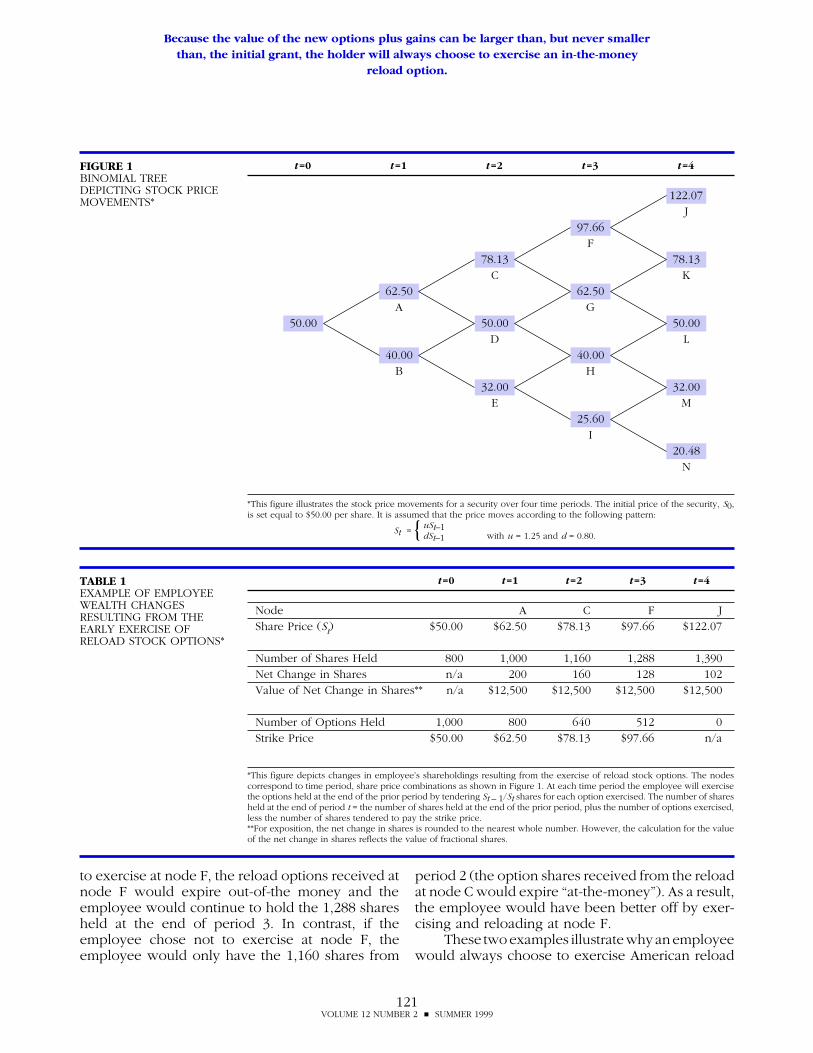

This particular sequence is depicted in Figure 1,where each node corresponds to a possible shareprice at a point in time. For simplicity, we will assumethat the employee will not exercise if the option is“at-the-money,” the employee holds onto any sharesreceived through exercise, and that initially there areno tax consequences (we address tax effects later).

We first consider the sequence in which theshare price increases each period (sequence ACFJ)and assume that the employee chooses to exerciseat each point. The first exercise, node A, correspondsto the earlier example. In order to pay the strike priceof $50,000 for the 1,000 options, the employee wouldsurrender 800 shares, with each share worth $62.50.In return, the employee receives 1,000 shares and800 options with a strike price of $62.50 that expireat the end of period 4. As a result of the transaction,the employee receives a net 200 shares, each ofwhich is worth $62.50 for a realized gain of 200 ×$62.50 = $12,500. The effects of exercise at nodes C,F and J are summarized in Table 1.

There are several items to note in Table 1.First, the gain on exercise at each point is a con-stant ($12,500).10 This is true by construction. Thereduction in the net change in shares received eachperiod is perfectly offset by the increase in thevalue of the shares. Thus, in valuing the reloadoption, we can assume a constant gain at eachexercise point. Second, the total number of claimson the firm (shares of stock plus options = 1,800claims) is constant until the end of period 4. Fi-nally, assume that instead of exercising and reload-ing the option, the employee held the options untilmaturity and exercised the options through a cash-less exercise at the end of period 4. In that case, theemployee would surrender 410 ($50,000/$122.07)shares to exercise the 1,000 options. At the end ofperiod 4 the employee would have a net increaseof 590 shares, which is exactly the amount theemployee would receive through the reload strat-egy. In other words, if prices steadily increase, theemployee is indifferent between the reload optionand the straight option.

On the other hand, assume that, in period t=3,the price is at node F, but rather than increase to nodeJ, the price drops to node K. If the employee chose

10. To reinforce this point, note that if you are at node A and the price drops,the next feasible exercise is at K and the gain is still $12,500, i.e., the share priceat node K is equal to the share price at node C.

8. T. Hemmer, S.R. Matsunaga, and T. Shevlin, “An Empirical Examination ofthe Incentives to Adopt Reload Employee Stock Option Plans,” 1998 workingpaper, University of Washington.

9. An American option is an option that the holder can exercise at any timeprior to expiration.

St =

VOLUME 12 NUMBER 2 SUMMER 1999121

to exercise at node F, the reload options received atnode F would expire out-of-the money and theemployee would continue to hold the 1,288 sharesheld at the end of period 3. In contrast, if theemployee chose not to exercise at node F, theemployee would only have the 1,160 shares from

period 2 (the option shares received from the reloadat node C would expire “at-the-money”). As a result,the employee would have been better off by exer-cising and reloading at node F.

These two examples illustrate why an employeewould always choose to exercise American reload

FIGURE 1BINOMIAL TREEDEPICTING STOCK PRICEMOVEMENTS*

TABLE 1EXAMPLE OF EMPLOYEEWEALTH CHANGESRESULTING FROM THEEARLY EXERCISE OFRELOAD STOCK OPTIONS*

t=0 t=1 t=2 t=3 t=4

Node A C F JShare Price (St) $50.00 $62.50 $78.13 $97.66 $122.07

Number of Shares Held 800 1,000 1,160 1,288 1,390Net Change in Shares n/a 200 160 128 102Value of Net Change in Shares** n/a $12,500 $12,500 $12,500 $12,500

Number of Options Held 1,000 800 640 512 0Strike Price $50.00 $62.50 $78.13 $97.66 n/a

*This figure depicts changes in employee’s shareholdings resulting from the exercise of reload stock options. The nodescorrespond to time period, share price combinations as shown in Figure 1. At each time period the employee will exercisethe options held at the end of the prior period by tendering St – 1/St shares for each option exercised. The number of sharesheld at the end of period t = the number of shares held at the end of the prior period, plus the number of options exercised,less the number of shares tendered to pay the strike price.**For exposition, the net change in shares is rounded to the nearest whole number. However, the calculation for the valueof the net change in shares reflects the value of fractional shares.

t=0 t=1 t=2 t=3 t=4

122.07J

97.66F

78.13 78.13C K

62.50 62.50A G

50.00 50.00 50.00D L

40.00 40.00B H

32.00 32.00E M

25.60I

20.48N

*This figure illustrates the stock price movements for a security over four time periods. The initial price of the security, S0,is set equal to $50.00 per share. It is assumed that the price moves according to the following pattern:

uSt–1 { dSt–1 with u = 1.25 and d = 0.80.

St =

Because the value of the new options plus gains can be larger than, but never smallerthan, the initial grant, the holder will always choose to exercise an in-the-money

reload option.

122JOURNAL OF APPLIED CORPORATE FINANCE

options that are “in-the-money.” If the employeewere certain that the price will increase, he or shewould be indifferent between holding the originaloptions or exercising and reloading. On the otherhand, if there is any probability that the price willdecrease, the employee would be strictly better offby reloading. We can then use the result thatemployees are strictly better off by exercising andreloading any “in-the-money” reload options and theresult that the gain on exercise is a constant to derivean ex-ante value for the reload option.11

Before proceeding, we contrast the valuation ofa reload option to the valuation of an employee stockoption without the reload feature. As is well known, thedecision whether to exercise an option without a re-load feature prior to maturity depends on several fac-tors, including the individual’s risk preferences. In termsof Figure 1, this means that there is uncertainty regard-ing whether exercise will take place at nodes A, C, F,etc. At each of these nodes, the individual trades off thetime value of continuing to hold the option against thepotential risk reduction (through diversification) ofexercise. Thus, the probability of exercise at each node(and hence the ex ante value) depends upon theindividual’s attitude toward risk. On the other hand, asshown in the example above (and more formally inHMS (1998)), with the reload feature, the payoffs asso-ciated with exercising at certain nodes strictly domi-nates the payoffs associated with not exercising atthose nodes, and therefore the decision to exercisedoes not depend upon individual risk preferences.

THE VALUATION OF A RELOAD OPTION

The example used in the previous illustrationprovides the insights necessary to derive a valuationmodel for a reload option. In particular, we know atwhich nodes the option will be exercised (wheneverthe price exceeds a previous high) and the gain onexercise at each node. In terms of Figure 1, exercisewill occur at nodes A,C,F,J and, potentially, at nodesG and K. Exercise will only occur at nodes G and Kif the price exceeds the previous high. Considernode G. Node G can be reached by three different

price paths (ACG, ADG, or BDG). In this example,exercise will occur only if the price path is BDGbecause options received from the exercises atnodes A and C would not be “in-the-money” at nodeG. Similarly, although four different paths will leadto node K, exercise at node K will only occur for twopaths (ADGK or BDGK).

Given that the gain at each node is a constant$12.50 per original option, in order to derive a valuefor the reload option we need to determine theprobability of a price path that will lead to exerciseat a given time and discount the gain to time t=0. Therisk-free probability of a price increase (uptick) canbe found using the following formula (from Cox andRubenstein):12

p = 1 + r – d/ u – d (2)

where r = risk-free rate. The risk-free probability ofa downtick is given as q = 1 – p.

If we use a risk-free interest rate of 5%, andcontinue to set u = 1.25 and d = 0.80, we can calculatep = 0.556. Panel A of Table 2 shows the relatedprobabilities and the computation of the value. Notethat the probability of arriving at a given nodedepends upon the number of upticks required toreach the node. For example, two upticks arenecessary to arrive at node C (giving a probability of0.556 × 0.556 = 0.309 = p2), whereas three upticks andone downtick are required to arrive at node K (witha probability of 0.556 × 0.556 × 0.556 × 0.444 = 0.076= p3q). Node K is included twice because there aretwo different paths that will result in exercise at thatnode (ADGK and BDGK).

Given the probabilities of exercise at a givennode, we next need the discounted gain on exerciseat that node. This in turn requires an appropriatediscount rate. As demonstrated in HMS (1998), theappropriate rate to use is the risk-free rate (the yieldon a security with no repayment risk with anequivalent maturity). Recall that we are estimating a“fair value” of the security, i.e., the value to a marketparticipant who can hedge the risk of holding theoption. Because the exercise decision depends

11. It can also be shown that the exercise of a reload option that is out of themoney is suboptimal. While this is a well known result for a standard option, it isless clear with a reload option. Consider the case in which the price drops to $40(node B). In this case an option with a strike price of $50 is out-of- the-money. Byexercising the 1,000 reload options, the employee would trade 1,250 shares and1,000 out of the money options for 1,250 options with the lower strike price and1,000 shares. The net effect is that the employee would give up 250 shares for 250

at-the-money options and a reduction of the strike price on the remaining 1,000options. As it turns out, such a trade is suboptimal. However, if the firm were toincrease the reload ratio, i.e., provide more than one option for each sharetendered, it is conceivable that the exercise of an out of the money option couldbecome optimal.

12. J.C. Cox and M. Rubenstein, Options Markets (Prentice-Hall, Inc. EnglewoodCliffs, NJ, 1985)

VOLUME 12 NUMBER 2 SUMMER 1999123

solely upon realized price changes, and not onindividual risk preferences, a market participant(including the granting firm) can fully hedge thereturns on the option. The value of the option is thesum of the discounted gain (using the risk-free rate)at each node for which exercise will occur multipliedby the (risk-free) probability of reaching that node.In this example, that value is $16.01.

THE MODEL

In formal terms, the value of a reload option canbe found by applying Theorem 1 from HMS (1998).That theorem states that the value, R, can becomputed as

R = ΣTt=1Pr(X,t) × Π/(1 + r)t (3)

TABLE 2COMPUTATION OF THEVALUE OF A RELOADOPTION

PANEL A: COMPUTATION OF VALUE OF A RELOAD OPTION USING FIGURE 1*

Present Value Probability ExpectedPeriod Node Path Upticks of Gain of Path Value

t = 1 A A 1 $11.90 0.5560 $6.62t = 2 C AC 2 $11.34 0.3091 $3.50t = 3 F ACF 3 $10.80 0.1719 $1.86t = 3 G BDG 2 $10.80 0.1373 $1.48t = 4 J ACFJ 4 $10.28 0.0956 $0.98t = 4 K ADGK 3 $10.28 0.0763 $0.78t = 4 K BDGK 3 $10.28 0.0763 $0.78Total $16.01

*This panel computes the value of the reload option as depicted in Figure 1 by identifying each node at which exercise willoccur, determining the probability of a stock price path that will generate exercise at that node and computing the discountedgain on exercise at that node. The discounted gain is computed as $12.50/(1.05)t and the probabilities are based on a probabilityof an uptick = 0.556 and the probability of a downtick = 0.444.

PANEL B: COMPUTATION OF VALUE OF A RELOAD OPTION USING EQUATIONS (3) - (5)**

COLUMN NUMBER

1 2 3 4 5 6 7 8

DESCRIPTION

# of Cases of tProb. of (t – Upticks and DD) Upticks Downticks That Discounted Expected

Prob. of and D Will Lead to Prob. of Gain on Gain ont D t Upticks Downticks Exercise Exercise Exercise Exercise

FORMULA

pt pt–DqDt–1CD – t–1CD–1 Pr(X,t) ΠΠΠΠΠ/(1+r)t 6×7

1 0 0.5560 0 0 0.556 $11.90 $6.622 1 0.3091 0.2469 0 0.309 $11.34 $3.503 1 0.1719 0.1372 1 0.309 $10.80 $3.344 1 0.0956 0.0763 2 0.248 $10.28 $2.554 2 .n/a 0.0609 0 0 $10.28 0

Total=$16.01

**This figure describes the calculation of the value of a reload option using the formulae shown in equations (3) - (5). Theformula computes the probability of exercise at each time period, t, and applies that probability to the discounted gain onexercise at that time t. The probability of exercise at time t, column (6), is the probability of t consecutive upticks, pt, (column3), plus the probability of exercise at other nodes at time t, (column 4 × column 5). Column 4 provides the probability of therequisite number of t – D upticks and D downticks, p(t–D)qD, and column 5 provides the number of paths leading to the nodethat generate exercise, t–1CD – t–1CD–1.

The fact that reload options will always be exercised simplifies their valuation byeliminating a major problem in valuing more conventional employee stock options,

i.e., uncertain early exercise.

124JOURNAL OF APPLIED CORPORATE FINANCE

where,

Pr(X,t) = pt + Σ∆D=1pt–DqD[t–1CD – t–1CD–1], (4)

S0[u – 1], if St > max [S0,....,St–1]Π = { 0, otherwise (5)

andt = time periodp = probability of an uptick, from equation (2)q = probability of a downtick = (1 – p)D = number of downticks∆ = t/2 rounded downS0 = original strike price, assumed to be $50 in our

exampleu = the magnitude of an uptick, assumed to be 1.25

in our example

mCn = number of combinations of m items taken nat a time13

T = life of original option, assumed to be 4 in ourexample

r = risk-free interest rate, assumed to be 5%Pr(X,t) = the probability of exercise in period tΠ = the payoff if exercise occurs ($12.50 per option

in our example).Starting with equation (5), S0 represents the

original strike price (in our example, $50), and urepresents the extent of an uptick (in our example,1.25). Therefore, Π represents the gain on exerciseof $50 × 0.25 = $12.50. The expression at the end ofequation (3) then is the discounted present value ofthe gain on exercise at each point in time.

Equation (4) calculates the probability of exer-cise at any time t. The first term, pt, calculates theprobability of moving along the top path in Figure1, i.e., the probability of an uptick in every period.Recall that exercise is optimal whenever the currentprice exceeds the previous high. Therefore, exerciseis optimal at every node along the top path. Thesecond term in equation (4) calculates the probabil-ity of exercise at other nodes at time t. Consider thecase in which t = 3. Referring again to Figure 1 andignoring the top path we can see that the originaloption will only be in the money if there have beentwo upticks and one downtick and that this occursat node G. Although node G can be reached through3 different paths (ACG, ADG and BDG) exercise willonly occur if the path is BDG because in the other

two cases the share price has not exceeded theprevious high, i.e., the options held by the employeeat that point in time will not be “in-the-money.” Thebinomial coefficients in equation (4) compute thenumber of combinations of two upticks and onedowntick that will lead to exercise. In equation (4),with t = 3, the sum from D = 1 to ∆, consists of D =1. If D =1 and t = 3, then t-1CD = 2C1 = 2 and t–1CD–1= 2C0 = 1. Therefore, t–1CD – t–1CD–1 = 2 – 1 = 1.

Similarly, if t=4, exercise will only occur if therehave been either four upticks or three upticks andone downtick. The probability of four upticks iscomputed by the first term in equation (4). Threeupticks and one downtick occur at node K. Node Kcan be reached by four paths (ACFK, ACGK, ADGKand BDGK) and exercise will occur for two of them(ADGK and BDGK). Using the same methodology asabove, the probability of three upticks and onedowntick is p3q1 = 0.5563 × 0.444 = 0.0763 and thenumber of possible paths that lead to exercise is

3C1 – 3C0 = 3 – 1 = 2.Substituting the value for our parameters into

the valuation equation provides the following valuefor the reload option.

R = Σ4t=1{0.556t + Σ∆

D=10.556t–D.444D[t–1CD – t–1CD–1]}× 12.50/1.05t. (6)

Panel B of Table 2 provides the details of thecalculation in equation (6). The first column corre-sponds to each of the four periods. The secondcolumn provides the maximum number of downticksthat could still result in exercise. In this column, eachnumber corresponds to a D in the summation fromD = 1 to ∆ in equation (6). Note that in applying thissummation, you must round down after computingt/2. That is, if t =3, then ∆ = 1, if t = 5 then ∆ = 2, etc.The third column shows the value of the first term inthe expression, pt for each t. The fourth columnprovides the probability of a given number of upticksand downticks for each possible t and D, i.e., p(t–D)

* qD. Column 5 shows the number of cases in whichthe given number of upticks and downticks willactually result in exercise (i.e., the share priceexceeds its previous high) and is computed by taking

t–1CD – t–1CD–1. Therefore the total probability ofexercise shown in column 6 at time t is the probabil-ity of an increase in each period (column 3) plus the

13. The term mCn is often referred to as a binomial coefficient and can becomputed as m!/[(m – n)!n!].

VOLUME 12 NUMBER 2 SUMMER 1999125

probability of t – D increases matched with Ddecreases that lead to exercise (column 4 timescolumn 5). Column 7 provides the discounted gainon exercise at each time t and in column 8 wemultiply that gain times the probability of exercise atthat time (column 6 times column 7). The sum ofcolumn 8 is the value of the option, $16.01.

EXERCISE RESTRICTIONS

The preceding discussion applies to an Ameri-can option—that is, one that allows the holder toexercise, and reload, at any time prior to maturity.However, employee stock options, including thosewith reload provisions, typically carry certain exer-cise restrictions. These restrictions take a variety offorms. Most firms impose time vesting restrictions onboth the original grant and the reload optionsreceived upon exercise, while other plans imposeperformance requirements. For example, DonaldsonCompany Inc. and Chrysler allow for reloads only ifthe market price exceeds the strike price by 25%.Some plans restrict the number of times an employeecan reload upon exercise. For example, Circuit CityStores and Donaldson allow an employee to reloadonly once and TIG Holdings limits employees to tworeloads in a given calendar year.

As discussed below, adding exercise restric-tions will strictly decrease the value of a reloadoption because the number of potential reloadpoints decreases. Therefore, the reload value ob-tained from equations (3) - (5) provides an upperbound on the value of a reload option with exerciserestrictions. In addition, because the reload feature(even with exercise restrictions) strictly increases thevalue of an option, the Black-Scholes value, using anexpected life equal to the life of the option, providesa lower bound on the reload option value.

In the case of performance vesting, the preced-ing model can be appropriately modified to reflectthe reduction in value.14 The more common time-based exercise restriction, however, creates twoproblems. The first is that the gain on the exercise isno longer constant and the second is that, under

some circumstances, the rule of exercising wheneverthe option is in-the-money may no longer be adominant strategy. The latter could occur if at certainnodes the decision to exercise and reload at onepoint in time could result in the loss of the ability toreload at a future point in time.

A simple approach to incorporating time-basedvesting, however, is to reduce the number of nodesin the binomial tree used for the calculations suchthat exercise is only feasible with time intervals equalto the imposed vesting periods. In the case of a 10-year reload option with six-month vesting periods,this amounts to using a binomial tree with 10/0.5 =20 periods as the basis for the valuation.

From a practical standpoint, the number ofnodes in the binomial tree is an arbitrary choice.However, in the case of reload options, the choicebecomes crucial because, unlike a standard option,the value of a reload is strictly increasing in thenumber of nodes at which exercise can occur.15 Byusing only 20 time periods for a 10-year reloadoption with six-month vesting, we are actuallyreducing the exercise opportunities the option holderfaces. In particular, we are restricting the holder toexercising the option on specific dates, which are sixmonths apart. Thus, this approach introduces adownward bias in the valuation. To a certain degree,this is offset by the coarseness of the binomial treeused to make the estimate, which induces an upwardbias in the gain on exercise Π. In our Kelloggexample later, we discuss this issue further andprovide a simple adjustment to address this issue.Once this adjustment is made, the resulting estimatecan be viewed as a lower bound.

TAXES

Individuals are taxed on the gain on the exer-cise of a nonqualified employee stock option in theyear of exercise at their ordinary income tax rate.16

A standard feature of reload option contracts re-quires employees to tender shares to cover thewithholding tax on the gain on exercise. Perhapssurprisingly, given an intertemporal constant tax

14. HMS (1998) provides a detailed valuation model that incorporatesperformance vesting.

15. This occurs because increasing the number of nodes increases the numberof potential reload points. See HMS (1998) for a further discussion.

16. The issuing firm also receives a deduction for the gain on exercise whenthe holder exercises a nonqualified stock option. Current tax rules also allow firmsto issue “Incentive Stock Options”. With an incentive stock option the tax on the

gain on exercise for the individual is deferred until the individual sells theunderlying stock and the gain is then taxed at the capital gains tax rate. The issuingfirm does not receive a tax deduction for an “Incentive Stock Option” unless theoption is disqualified (as discussed in S.R. Matsunaga, T. Shevlin and D. Shores,“Disqualifying Dispositions of Incentive Stock Options: Tax Benefits VersusFinancial Reporting Costs,” Journal of Accounting Research suppl. 30 (1992).

Adding exercise restrictions will strictly decrease the value of a reload optionbecause the number of potential reload points decreases.

126JOURNAL OF APPLIED CORPORATE FINANCE

rate, the presence of a positive tax rate does notaffect the employee’s exercise strategy for reloadoptions. Therefore, the before-tax value of a reloadoption is unaffected by the tax rate. In addition,because one can factor Π out of expression (4),from the employer’s standpoint, the after-tax valueof the option would be (1 – the corporate tax rate)times the before-tax value of the option.

To see that the withholding tax would not affectthe employee’s exercise strategy, look at the compu-tation shown in Table 3. The numbers in Table 3correspond to the same options considered in Table1, except that we now assume that the gain onexercise is taxed at a constant tax rate of 40%.Because the gain on exercise is constant ($12,500),the tax on the gain is also constant 40% × $12,500 =$5,000. Thus, the only difference between Tables 1and 3 is that in Table 3, the net change in shares heldby the employee is reduced by $5,000/share price.At the end of period 4, given stock price path ACFJfrom Figure 1, the employee would hold a total of1,154 shares. On the other hand, if the employeefollowed a hold to maturity and cashless exercisestrategy, the employee would tender the same 410shares as before to exercise the options, and tenderan additional [($122.07 – 50.00) *1,000*40%]/$122.07

= 236 shares to pay the withholding tax on the gain.As a result, the employee would have a net increaseof 590 – 236 = 354 shares, which is exactly theincrease shown in Table 3.

Therefore, as before, the employee is indiffer-ent between exercising and holding the option givena future uptick. Similarly, using the same analysis asbefore, one can see that the employee would bestrictly better off by exercising prior to a futuredowntick. The intuition is clear: If you know thestock price is about to drop, you are better off exer-cising the option while the stock price is still high.

DIVIDENDS

Up to this point we have ignored the possibilitythat the stock is paying dividends. Unlike a standardemployee stock option, dividends would have noeffect on the employee’s exercise strategy for areload option. As we discussed in a 1996 study, ahigh dividend rate could lead to early exercise andthereby affect the value of a standard ESO.17 How-ever, as discussed above, the optimal strategy for areload option is to exercise whenever the option is“in-the-money”, i.e., early exercise is already opti-mal. Therefore, the only adjustment required is to

TABLE 3EXAMPLE OF EMPLOYEEWEALTH CHANGESRESULTING FROM THEEARLY EXERCISE OFRELOAD STOCK OPTIONSASSUMING A 40% TAXRATE*

t=0 t=1 t=2 t=3 t=4

node A C F Jshare price $50.00 $62.50 $78.13 $97.66 $122.07

# of shares held 800 920 1,016 1,093 1,154net change in shares n/a 120 96 77 61value of net change in shares** n/a $7,500 $7,500 $7,500 $7,500

# of options held 1,000 800 640 512 0strike price $50.00 $62.50 $78.13 $97.66 n/a

*This figure corresponds to Table 1 and depicts changes in employee’s shareholdings resulting from the exercise of reloadstock options if the gain on exercise is taxed at a 40% rate. The nodes correspond to time period, share price combinationsas shown in Figure 1. At each time period the employee will exercise the options held at the end of the prior period by tenderingSt–1/St shares for each option exercised. In addition, each period the employee tenders $5,000/St shares to pay the withholdingtax on the gain, where the $5,000 represents the tax on the gain, (St – St-1) * # of options exercised * tax rate. The numberof shares held at the end of period t is equal to the number of shares held at the beginning of the period, plus the numberof options exercised, less the number of shares tendered to pay the strike price and less the shares tendered to pay thewithholding tax on the gain.**For exposition, the net change in shares is rounded to the nearest whole number. However, the calculation for the valueof the net change in shares reflects the value of fractional shares.

17. T. Hemmer, S. R. Matsunaga, and T. Shevlin, “The Influence of RiskDiversification on the Early Exercise of Employee Stock Options by ExecutiveOfficers,” Journal of Accounting and Economics, (1996).

VOLUME 12 NUMBER 2 SUMMER 1999127

change the expected returns on the stock to includeonly capital gains. In other words, incorporating apositive dividend yield involves making an appro-priate adjustment to the stock price evolutions ascaptured by the binomial tree, thus changing thegain on exercise.

In keeping with common practice, we assumea constant dividend yield. If we then also assume thatdividend payments are more frequent than exer-cises, we can correctly incorporate the dividendsinto the model by calculating the gain on exercise asfollows:18

Πδ = S0[u × (1 – δ)Z/T – 1],

where Z is the number of dividend payments overthe life of the REO, δ is the dividend yield perpayment period, and T is the number of potentialexercises. In other words, if a 10-year REO has a sixmonth vesting period and the stock pays dividendsquarterly, Z/T = 40/20 = 2.19

EXAMPLE USING DATA FROM KELLOGG CO.

To illustrate the mechanics of the technique, weuse the example of Kellogg Co. The data used in theexample is taken from Kellogg’s 1994 proxy state-ment. We first calculate the unrestricted value, usingthe preceding dividend adjustment, and then add theadjustment for time-vesting. We focus on the newoptions granted on January 28, 1993 that include areload provision. The original strike price and cur-rent market value, S0 = $62.3125 and the calendartime life of the option is 10 years. Kellogg uses a risk-free rate, r = 4.86% for their new options, a constantquarterly dividend yield (δ) of 0.59% (annual yieldof 2.05%), and an annual volatility, σ = 21%.20

As discussed in detail in HMS (1998), thenumber of price changes allowed is an arbitrarychoice. In addition, although the value increaseswith the number of nodes, the value converges fairlyquickly. For our example, we allow for 1,000 stockprice changes (periods), or 100 exercise points peryear. The next step is to convert the annual rates to

period rates yielding r = (1.0486)0.01 – 1 = 0.0004757and σ = 0.21 * .01.5 = 0.021.

We can then use the following relations fromCox and Rubenstein (1985) to derive the inputs forthe valuation model.

u = eσ = e0.021 = 1.021222d = 1/u = 0.979219p = (1 + r – d)/(u – d)

= (1.0004757 – 0.979219)/(1.021222 – 0.979219)= 0.506076

The dividend-adjusted gain on exercise at eachperiod, Πδ = S0[u(1 – δ)Z/T – 1] = $62.3125[1.021222(1– .00509)40/100 – 1] = 1.309408.21 We can thendetermine the probability of exercise at each point,t, and discount the gain t periods using the risk-freediscount rate, 0.0004757. The value of the reloadwould be determined by computing the probabilityof exercise at each period, multiplying that probabil-ity by the discounted gain $1.309408/1.0004757t andsumming those values for each period. The cost toKellogg of issuing one reload option can thereby becalculated to be $35.92.

We next have to consider that Kellogg optionshave a six-month vesting period. To adjust for thetime-based vesting restriction on Kellogg reloadoptions we follow the approach discussed in section5 and use a binomial tree with 20 semi-annualperiods, thereby automatically limiting the exercisepossibilities to reflect the six-month vesting restric-tion.22 One problem with this approach is that weallow for only 20 price changes over a ten-yearperiod. The “coarseness” of this binomial tree couldcreate errors in the valuation estimate because, inessence, we are using a step function to approximatea curve. To see this, consider the last period beforeexercise. At that time, the options held in themanager’s portfolio will have six months remainingto expiration. The best estimate of the fair value ofthat option is the Black-Scholes model. Using theforegoing procedure would systematically overstatethat value. One way to address this problem wouldbe to determine the Black-Scholes value of an option

18. This approach can also be used to approximate the adjustment for caseswhere the number of exercise points exceeds the number of dividend payments.In such a case, this approach “over adjusts” for dividends. The resulting adjustedvaluation can therefore be considered to be a lower bound. The theoreticallycorrect adjustment for such cases is available from the authors.

19. Details are available from the authors upon request.20. An annual standard deviation can be converted into a monthly standard

deviation by multiplying by (1/12).5.

21. As discussed in footnote 18, since the number of exercise points (1,000)exceeds the number of dividend payments (40), this adjustment yields a lowerbound estimate of Πδ.

22. With a total of twenty periods, the valuation model can be incorporatedinto most basic spreadsheet applications. Increasing the number of nodes in thebinomial tree greatly increases the required computer power and requires moresophisticated programming.

The only adjustment for dividends required is to change the expected returns on thestock to include only capital gains.

128JOURNAL OF APPLIED CORPORATE FINANCE

with a six month life. Using that value as the fair valueof that option, we can solve for the parameters thatwould provide this value in a one-period binomialmodel. We can then use the derived parameterestimates in the reload option valuation model. Thisprocedure is illustrated below.

To derive the extent of the uptick, u, and theprobability of an uptick, p, we first equate thebinomial value of an option with one (six month)period to the Black-Scholes value of a six monthoption. We convert the volatility, 0.21, to a semi-annual volatility by multiplying by .5.5 = 0.707 to get0.1485. We use a standard Black-Scholes valuationmodel to compute the value of an option with T =1, σ = 0.1485, X = $62.3125 to get a value of $4.44.23

We then use this value as the binomial value of anoption with a life of one period and solve for theappropriate p and u. Since p is the probability of anuptick, $62.3125 × (u – 1) is the gain on exercise, and0.024 is the semi-annual risk-free interest rate, thisyields the following equation:

$4.44 = (p × 62.3125 × [u – 1])/1.024 (7)

We can then use equation two and the relation thatd = 1/u to get the following:

p = (1.024 – 1/u)/(u – 1/u) (8)

By substituting (8) into (7) we get estimates of u =1.1282 and p = 0.56912.

We then follow the same procedure outlinedabove to derive the estimated value of the reload

option. In this case, there will be 20 time-periods toevaluate. Because the dividend adjusted gain oneach exercise, Π = $62.3125[1.1282(1 – 0.00509)40/20

– 1] = $7.27 here is a constant, we only need todetermine the probability of exercising and receiv-ing that gain in each time period. In the Kelloggexample, the reload value is $28.00, which is consid-erably higher than the $10.64 value reported byKellogg.24

CONCLUSION

In this paper we provide a guide for valuingoptions with a reload provision. As demonstratedhere (and more formally in HMS (1998)), the additionof a reload provision provides the employee with adominant exercise strategy—namely, to exercise theoption whenever it is “in-the-money.” The presenceof this dominant strategy allows the construction ofa valuation model that is unaffected by the employee’srisk preferences.

The model presented is relatively simple andcan easily be adapted to a spreadsheet application.The model can thus be used by those issuing orreceiving reload options to assess the value of thesecurity granted or received. In addition, the modelcan be used by educators to describe option valua-tion in general, or to illustrate how innovations tothe standard option contract affect value. Finally,the model can be used by regulators or other usersof the financial statements to obtain a better under-standing of the value of the contractual obligationsof the firm.

23. We use a dividend yield of zero for this calculation because we use theapproach detailed above to adjust the value of the reload option for dividends.Accordingly, incorporating the dividend yield in this Black-Scholes calculationwould result in double counting the effects of dividends.

24. In keeping with SFAS #123, Kellogg ignores the reload feature in its grantdate valuation. However, Kellogg does use a relatively short expected life for theoption to reflect the probable earlier exercise. Kellogg records the value of thereload options as separate option grants as they occur.

THOMAS HEMMER

is an Associate Professor of Accounting at the University ofChicago’s Graduate School of Business.

STEVE MATSUNAGA

is an Associate Professor of Accounting at the University ofOregon’s Lundquist College of Business.

TERRY SHEVLIN

is the Deloitte & Touche Professor of Accounting at theUniversity of Washington’s School of Business.

Journal of Applied Corporate Finance (ISSN 1078-1196 [print], ISSN 1745-6622 [online]) is published quarterly on behalf of Morgan Stanley by Blackwell Publishing, with offices at 350 Main Street, Malden, MA 02148, USA, and PO Box 1354, 9600 Garsington Road, Oxford OX4 2XG, UK. Call US: (800) 835-6770, UK: +44 1865 778315; fax US: (781) 388-8232, UK: +44 1865 471775, or e-mail: [email protected].

Information For Subscribers For new orders, renewals, sample copy re-quests, claims, changes of address, and all other subscription correspon-dence, please contact the Customer Service Department at your nearest Blackwell office.

Subscription Rates for Volume 17 (four issues) Institutional Premium Rate* The Americas† $330, Rest of World £201; Commercial Company Pre-mium Rate, The Americas $440, Rest of World £268; Individual Rate, The Americas $95, Rest of World £70, Ð105‡; Students**, The Americas $50, Rest of World £28, Ð42.

*Includes print plus premium online access to the current and all available backfiles. Print and online-only rates are also available (see below).

†Customers in Canada should add 7% GST or provide evidence of entitlement to exemption ‡Customers in the UK should add VAT at 5%; customers in the EU should also add VAT at 5%, or provide a VAT registration number or evidence of entitle-ment to exemption

** Students must present a copy of their student ID card to receive this rate.

For more information about Blackwell Publishing journals, including online ac-cess information, terms and conditions, and other pricing options, please visit www.blackwellpublishing.com or contact our customer service department, tel: (800) 835-6770 or +44 1865 778315 (UK office).

Back Issues Back issues are available from the publisher at the current single- issue rate.

Mailing Journal of Applied Corporate Finance is mailed Standard Rate. Mail-ing to rest of world by DHL Smart & Global Mail. Canadian mail is sent by Canadian publications mail agreement number 40573520. Postmaster Send all address changes to Journal of Applied Corporate Finance, Blackwell Publishing Inc., Journals Subscription Department, 350 Main St., Malden, MA 02148-5020.

Journal of Applied Corporate Finance is available online through Synergy, Blackwell’s online journal service which allows you to:• Browse tables of contents and abstracts from over 290 professional,

science, social science, and medical journals• Create your own Personal Homepage from which you can access your

personal subscriptions, set up e-mail table of contents alerts and run saved searches

• Perform detailed searches across our database of titles and save the search criteria for future use

• Link to and from bibliographic databases such as ISI.Sign up for free today at http://www.blackwell-synergy.com.

Disclaimer The Publisher, Morgan Stanley, its affiliates, and the Editor cannot be held responsible for errors or any consequences arising from the use of information contained in this journal. The views and opinions expressed in this journal do not necessarily represent those of the Publisher, Morgan Stanley, its affiliates, and Editor, neither does the publication of advertisements con-stitute any endorsement by the Publisher, Morgan Stanley, its affiliates, and Editor of the products advertised. No person should purchase or sell any security or asset in reliance on any information in this journal.

Morgan Stanley is a full service financial services company active in the securi-ties, investment management and credit services businesses. Morgan Stanley may have and may seek to have business relationships with any person or company named in this journal.

Copyright © 2004 Morgan Stanley. All rights reserved. No part of this publi-cation may be reproduced, stored or transmitted in whole or part in any form or by any means without the prior permission in writing from the copyright holder. Authorization to photocopy items for internal or personal use or for the internal or personal use of specific clients is granted by the copyright holder for libraries and other users of the Copyright Clearance Center (CCC), 222 Rosewood Drive, Danvers, MA 01923, USA (www.copyright.com), provided the appropriate fee is paid directly to the CCC. This consent does not extend to other kinds of copying, such as copying for general distribution for advertis-ing or promotional purposes, for creating new collective works or for resale. Institutions with a paid subscription to this journal may make photocopies for teaching purposes and academic course-packs free of charge provided such copies are not resold. For all other permissions inquiries, including requests to republish material in another work, please contact the Journals Rights and Permissions Coordinator, Blackwell Publishing, 9600 Garsington Road, Oxford OX4 2DQ. E-mail: [email protected].