605 north capital ave. - co.bonneville.id.us · a, form 89se section 6(b). the statute defines the...

TRANSCRIPT

RESOLUTION NO. 15-07

A Resolution by the Bonneville County Board of CommissionersConcerning Tax Exemption for FREIGHTLINER

WHEREAS, I.C. § 63-606A authorizes Bonneville County to declare that all or a portion of themarket value of a defined project with investments that meet certain tax incentive criteria may beexempted from property taxation through December 31,2020 (I.C. § 62-4403) based on thebenefit determined by the Board of County Commissioners provided to the community, and

WHEREAS, the Board of Bonneville County Commissioners, in consultation with Freightlinerhas determined to base an exemption decision upon several factors including, but not limited to:the meeting ofthe"tax incentive criteria" during the project period, the capital investmentscontributed, the amount of wages to be paid to employees, the number of qualifying new jobscreated, and whether or not the project draws new money to Bonneville County, and

WHEREAS, FREIGHTLINER has presented to Bonneville County a written plan that meets therequirements of I.C. §§ 63-606A, 63-4403, and 63-4404 for a Defined Project by showingprojected investments in plant and building facilities in Bonneville County, Idaho to provide astate-of-the-art service center for long-haul trucks and recreational vehicles with some sales oflong haul trucks more particularly described in its application attached hereto as "Exhibit A",and

WHEREAS, Bonneville County has examined the written plan, has examined the communitybenefit provided by the Defined Project, and has determined that it is in the best interest of thepublic to grant an exemption to FREIGHTLINER; and

NOW THEREFORE, the Board of Bonneville County Commissioners finds as follows:

1) Tax Exemption Findings. The Board of Bonneville County Commissioners finds asfollows:

1

a) Property Identification. The applicable parcel for this exemption is more particularlydescribed as follows: Lot 3 Block 3 Andco Subdivision Division No. 3, and Lot 12

Block 3 Andco Subdivision Division No. 3, 1St Amended Bonneville County Idaho.

b) Compliance with Prerequisites. FREIGHTLINER will construct or acquire within theapplicable timeframes approximately $11,575,000.00 of Investment in BonnevilleCounty, Idaho as defined in I.C. § 63-606A, which meets or exceeds the "tax incentivecriteria" as defined in I.C. § 63-4402,4403, and 4404.

c) Benefit. Significant economic benefits will accrue to Bonneville County as a result ofthis tax exemption and FREIGHTLINER'S investment and job creation in thiscommunity. In consideration of the foregoing, this exemption is necessary and just.

d) Determination of Proiect Period. The Board of Bonneville County Commissioners hasdetermined that the Project Period, as defined in I.C. § 63-606A, will commence January1, 2016 and continue through December 31, 2020. Accordingly the first tax year forwhich an exemption is granted is January 1, 2016.

e) Carryover. Each tax year stands on its own. There shall be no rollover or carryover oftax exemption credits or unused tax exemption valuation from year to year.

2) Grant of Tax Exemption

a) Amount of Exemption. FREIGHTLINER shall be granted a property tax exemption inthe amount ofseventy-five percent (75%) forthe taxable year January 1, 2016 throughDecember 31, 2016 up to amaximum tax credit of $83,301.00. The qualified value inthe remaining periods will be the assessed value as determined by the Bonneville CountyAssessor on or before January Ist of each year.

b) Renewal. FREIGHTLINER has requested the benefit of this exemption throughDecember 31, 2020. However, I.C. § 63-602(3) requires annual approval ofthisexemption. Nonetheless, considering I.C. § 63-606A, 63-4403, and 63-4404 anticipatean exemption being allowed over a project period extending as far as December 31, 2020and considering the amount of capital investment that must be made in anticipation ofthe commissioners granting such exemption, FREIGHTLINER, shall continue to beentitled to a 75% exemption (up to amaximum tax credit of $83,301.00) each yearthrough December 31,2018, after that a 50% exemption (up to a maximum tax credit of$55,535.00) each year through December 31, 2020, PROVIDED atimely renewalapplication is submitted to the Bonneville County Commissioners by the 15th day ofApril of each year through the year 2020. This renewal application shall includeitemized detail of FREIGHTLINER'S continued compliance with the aforementionedcode sections such that FREIGHTLINER would independently qualify for suchexemption in each successive year through December 31, 2020.

PASSED AND ADOPTED this 20th day ofJuly, 2015, during the regular meeting of the Boardof County Commissioners.

BONNIVILLE COUNTY BOARD OF COMMISSIONERS

1

Roger S f Christensen, Chairman

s<f /*

v f.£ 1 '4.-- .-,:Lee Stak@/Men* --7-*:=/7 -

David Radford, Member /

ATTEST: 6:CV.Ronald LongmoreBonneville County Clerk

2

June 19, 2015

Bonneville County Commissioners605 North Capital Ave.Idaho Falls, Idaho 83402

Application forFreightliner of Idaho LLC

Growth Incentive Exemptionunder Idaho Code § 63-606A

Re: Application for Small employer growth incentive exemption (Idaho Code § 63-606A)

Dear Commissioners:

We represent Freightliner of Idaho LLC d/b/a Freightliner of Idaho Falls (Freightliner). The companyrequests the commissioners approve this application for approval of the Small employer growth incentiveexemption under Idaho Code §63-606A (Growth Exemption). Freightliner requests a 75% tax exemptionfrom property tax on buildings, machinery, and equipment for 5 years. Freightliner further requests thetax exemption start on January 1, 2016 and run through December 31, 2020. We request a hearing as soonas possible to be heard on the above application.

Freightliner has recently purchased approximately 12.73 acres located near Flying J f/n/a DAD's TravelCenter south of Idaho Falls. The company plans to invest approximately 12 million dollars in buildingimprovements, machinery, and equipment. Freightliner will provide a state-of-the art service center forlong-haul trucks and recreational vehicles. It will provide sales of some long-haul trucks but the primaryemphasis will be service and maintenance.

Procedure for approval of Growth Exemption

The commissioners will sit as a board of equalization in approving the application for Growth Exemption.See I.C. §§ 63-606A(3) and 63-501.

Requirements for Growth Exemption

Freightliner must show that it will meet the following requirements under I.C. §§ 63-606A and 63-4402et. al in order to qualify for the Growth Exemption:

(1) For the project period, invest at least $500,000 in new plant and building facilities at a projectsite located in Idaho.

(2) For the project period, create at least 10 newjobs paying on average $40,000/year ($19.23/hour)plus health benefits related to the project site.

(3) For the project period, pay average wages of $32,240/year ($15.50/hour) plus health benefits toany new additional employees (above the additional 10 newjobs) during the project period relatedto the project site.

Rage'2

June 19, 2015

Requirements (1) through (3) shall be referred to as the "Tax Incentive Criteria" for purposes ofthisapplication.

(4) Certify to the Idaho State Tax Commission the taxpayer has met, or will meet, the Tax IncentiveCriteria before he can claim any ofthe incentives. IDAPA 942.02. The taxpayer shall file Form89SE with the Idaho State Tax Commission.

(5) Acquire new machinery and equipment that qualify for the Investment Tax Credit under I.C. §63-4403 (Investment Tax Credit) during the project period.

(6) Construct new plant, building facilities, or building components that qualify for the RealProperty Improvement Tax Credit under I.C. § 63-4404 (RPITC).

(7) Demonstrate to the County that investment in Freightliner's property benefits the citizens in theCounty and that granting the exemption is necessary and just.

Freightliner's application meets each ofthese sevens requirements.

(1) For the project period, Freightliner must invest at least $500,000 in new plant and buildingfacilities at a project site located in Idaho.

Under the statute, Freightliner must invest at least $500,000 in new plant and building facilities at the"Project Site" during the "Project Period."

The statute defines "Investment in new plant" as investment in new plant and building facilities that are(i) Qualified Investments; or (ii) Buildings or structural components ofbuildings. The statute makes noreference to "manufacturing" as a requirement in the new plant and building facilities. The CountyCommissioners previously approved of a tax incentive with the Cives Steel Company where theapplicable statute I.C. § 63-602NN required investment in at least 3 million ofnew plant and buildingfacilities. That statute specifically defined new plant and building facilities as "manufacturing facilities."That is not the case here. The applicable statute for the Growth Exemption does not limit the exemption tomanufacturing facilities.

Freightliner of Idaho LLC (Freightliner) sells long haul trucks, sells parts for such trucks, maintains andservices long haul trucks, and recreational vehicles. The long-haul trucking industry has a strong presencein southeast Idaho from trucking companies, long-haul truck stops, long-haul truck dealerships, and I-15which has consistent long-haul truck traffic going north or south. Freightliner has determined that a state-of-the art maintenance and service facility for the local haul trucking industry in southeast Idaho,particularly Bonneville County is needed.

In order to provide such a facility, Freightliner will construct a 65,000 square foot sales and servicefacility. Approximately 25,000 square feet will be used for service and maintenance. The remainder ofthefacility will be used for truck sales, part sales, and warehousing. s

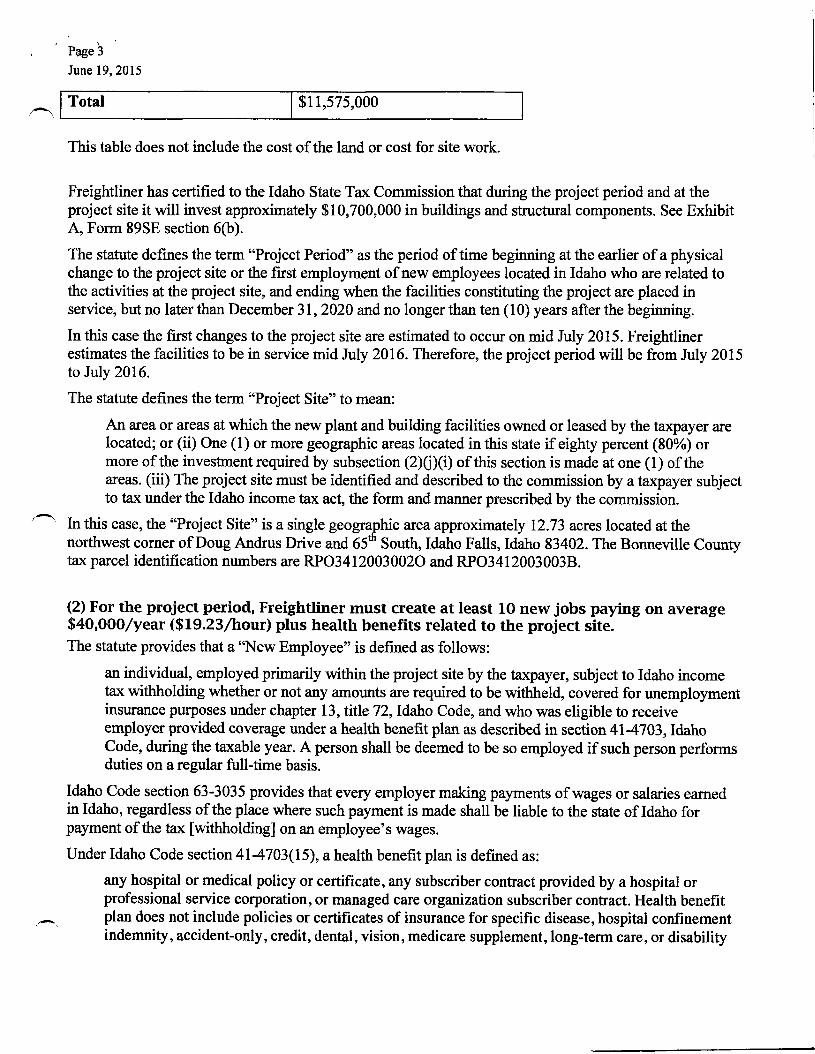

For the project period, Freightliner will invest over $11.575 million in capital investments on the projectsummarized as follows:

Item

Building and components

Equipment

Amount

$10,700,000

$875,000

Page 3

June 19,2015

Total $11,575,000

This table does not include the cost ofthe land or cost for site work.

Freightliner has certified to the Idaho State Tax Commission that during the project period and at theproject site it will invest approximately $10,700,000 in buildings and structural components. See ExhibitA, Form 89SE section 6(b).

The statute defines the term "Project Period" as the period oftime beginning at the earlier of aphysicalchange to the project site or the first employment ofnew employees located in Idaho who are related tothe activities at the project site, and ending when the facilities constituting the project are placed inservice, but no later than December 31, 2020 and no longer than ten (10) years after the beginning.

In this case the first changes to the project site are estimated to occur on mid July 2015. Freightlinerestimates the facilities to be in service mid July 2016. Therefore, the project period will be from July 2015to July 2016.

The statute defines the term "Project Site" to mean:

An area or areas at which the new plant and building facilities owned or leased by the taxpayer arelocated; or (ii) One (1) or more geographic areas located in this state if eighty percent (80%) ormore of the investment required by subsection (2)(j)(i) of this section is made at one (1) oftheareas. (iii) The project site must be identified and described to the commission by a taxpayer subjectto tax under the Idaho income tax act, the form and manner prescribed by the commission.

In this case, the "Project Site" is a single geogThic area approximately 12.73 acres located at thenorthwest corner ofDoug Andrus Drive and 65 South, Idaho Falls, Idaho 83402. The Bonneville Countytax parcel identification numbers are RPO3412003002O and RPO34120030038.

(2) For the project period, Freightliner must create at least 10 new jobs paying on average$40,000/year ($19.23/hour) plus health benefits related to the project site.The statute provides that a"New Employee" is defined as follows:

an individual, employed primarily within the project site by the taxpayer, subject to Idaho incometax withholding whether or not any amounts are required to be withheld, covered for unemploymentinsurance purposes under chapter 13, title 72, Idaho Code, and who was eligible to receiveemployer provided coverage under a health benefit plan as described in section 41-4703, IdahoCode, during the taxable year. A person shall be deemed to be so employed if such person performsduties on a regular full-time basis.

Idaho Code section 63-3035 provides that every employer making payments of wages or salaries earnedin Idaho, regardless of the place where such payment is made shall be liable to the state of Idaho forpayment ofthe tax [withholding] on an employee's wages.

Under Idaho Code section 41-4703(15), a health benefit plan is defined as:

any hospital or medical policy or certificate, any subscriber contract provided by a hospital orprofessional service corporation, or managed care organization subscriber contract. Health benefitplan does not include policies or certificates of insurance for specific disease, hospital confinementindemnity, accident-only, credit, dental, vision, medicare supplement, long-term care, or disability

Rage' 4

June 19,2015

income insurance, student health benefits only coverage issued as a supplement to liabilityinsurance, worker's compensation or similar insurance, automobile medical payment insurance ornonrenewable short4erm coverage issues for a period of twelve (12) months or less.

Freightliner has certified to the Idaho State Tax Commission that it will create over 25 jobs in Idaho in thefirst year ofthe Project Period. See exhibit A, Section 5. Freightliner will pay ten of these employees atleast $61,000 per year ($29.33/hour) plus health benefits that qualifies under a health benefit plan. SeeExhibit B, Summary of Jobs for Project Period. The employees working for Freightliner at the buildingfacilities will be subject to withholding in Idaho because the wages are earned in Idaho.

(3) For the project period, pay average wages of $32,240/year ($15.50/hour) plus healthbenefits to any new additional employees (above the additional 10 new Idaho jobs) duringthe project period related to the project site.

As stated under requirement (2) above, Freightliner has certified to the Idaho State Tax Commission thatit will pay on average $32,240/year (15.50/hour) plus health benefits to employees above and beyondthose jobs identified in requirement (2) above. The employee's wages will be subject to withholding inIdaho because the wages are earned in Idaho.

(4) Acquire new machinery and equipment that qualifies for the Investment Tax Creditunder I.C. § 63-4403 (Investment Tax Credit) during the project period.As stated above, Freightliner's investment includes $875,000 in machinery and equipment that qualifiesfor the Investment Tax Credit.

In order to qualify for the Investment Tax Credit, the statute requires that the investment must be in"qualified investments." The term "qualified investments" is defined in Idaho Code § 63-3029B. Thatsection defines the term "qualified investments" by reference to sections 46(c) and 48 of the InternalRevenue Code, as such code existed prior to November 5, 1990. The Idaho Tax Commission has definedthis term as follows:

Idaho generally follows the definition of qualified property found in the Internal Revenue Code(IRC) sections 46 and 48 as in effect prior to 1986. The property musthave auseful life ofthreeyears or more and be property for which you are allowed the deduction for depreciation oramortization in lieu of depreciation.

Qualifying property includes the following property used in a trade or business:

e Tangible personal property - machinery and equipment -' Other tangible personal property - property used as an integral part of manufacturing,

production, extraction, or furnishing transportation, communications, or utility services, orresearch facilities and bulk storage facilities used in connection with those businesses

Property that does not qualify includes:

Buildings and their structural components

• The cost of property expensed under IRC Section 179

' Page 5June 19, 2015

• Property subject to a 60-month amortization• Used property not acquired by purchase• Property that is either nondepreciable or has a useful life of fewer than 3 years• The portion of property used personal use

• Vehicles under 8,000 pounds gross weight

See Exhibit C, Idaho Form 49-Idaho Investment Tax Credit, attached to this application.

Freightliner has certified to the Idaho State Tax Commission that it will spend approximately $875,000for machinery and equipment at the Project Site during the Project Period. See Exhibit B section 6(a).

A schedule is attached as Exhibit D, which shows that this amount of $875,000 qualifies under thedefinition of "Qualified Investments" provided by the Idaho State Tax Commission.

(5) Freightliner constructs new plant, building facilities, or building components that qualify for theReal Property Improvement Tax Credit under I.C. § 63-4404 (Real Property Improvement TaxCredit).

As stated above, Freightliner's investment includes buildings or structural components in the amount of$10.7 million. This investment qualifies for Real Property Improvement Tax Credit.

In order to qualify for the Real Property Improvement Tax Credit, the statute requires that the investmentmust be in "buildings and structural components of buildings related to new plant and building facilities."As mentioned above, the statute does not require that the building and facilities be a manufacturingfacility. In fact, in reviewing the legislative history for the Idaho Small Employer Incentive Act of 2005(Small Employer Incentive Act), there is no mention ofthe drafters ofthe bill or any discussions requiringthere be manufacturing facilities.

As stated above, Freightliner has certified to the Idaho State Tax Commission that it will spendapproximately $10.7 million in buildings and structural components. These investments will be made onthe project site during the project period. See Exhibit A section 6(b).

(6) Freightliner demonstrates to the County that investment in Freightliner's propertybenefits the citizens in the County and that granting the exemption is necessary and just.The last criteria for granting the Growth Exemption are found in I.C. § 63-606A(1). This section providesas follows:

The board may grant the exemption when it finds that the investments in such property benefit thecitizens within the county and taxing districts within the county in a manner and to such a degreethat to grant the exemption is necessary and just.

Freightliner provides a variety of facts below to support the fact that its plant will bring significanteconomic benefits to Bonneville County.

As stated in this application, Freightliner's project will benefit the County. The project will provide over$12 million in investments in Bonneville County and add 25 new jobs that pay from $32,000 to $60,000annually. In addition, the County and its taxing districts will receive a significant increase in tax revenue.

Page' 6

June 19, 2015

For 2014, Bonneville County assessed tax of only $100 against Freightliner's property. With the newbuildings Freightliner's assessed tax for the future will bring significant tax revenue.

Attached as Exhibit E is a table showing the estimated property taxes paid over a 20-year time period,assuming a valuation equal to the costs incurred, assuming the investment values provided, assuming nodepreciation of equipment, and assuming the current property tax levy of .009595565 over a period of 20years.

Freightliner also has letters from the following individuals that either shows data the County will benefitor support for Freightliner's project.

Letter from Christopher St Jeor. Christopher St Jeor is the Regional Economist for the IdahoDepartment ofLabor. Mr. Jeor has provided an analysis to Freightliner finding that for every jobFreightliner hires at the average wages represented, nearly one other ful14ime job may be created. Thatmeans the total change in jobs could be 46, or 22 additional jobs. He further states in the letter thatBonneville County's total employee compensation would increase by an estimated $2,244,270 per year.Mr. St Jeor will provide a letter which we will submit. Attached as Exhibit F is an e-mail statementreceived from Mr. St Jeor regarding his analysis.

Letter from Darlene E. Gerry. Darlene E. Gerry is the Executive Director for the Regional EconomicDevelopment For East Idaho (REI)I). Freightliner has worked closely with REDI in securing a site,facilitating meetings with the Department of Commerce, Idaho Department of Labor, and Idaho State TaxCommission. REDI is in support of the project and request for property tax exemption. Attached asExhibit G is a copy of Ms. Gerry's letter.

Letter from Jeffery Sayer. Jeffery Sayer is the Director ofthe Idaho Department of Commerce. His- letter is pending. We will submit the letter once we receive it.

Letter from Shelley School District 60. We reached out to Shelley School District 60 telling the Districtof our plans and request for a property tax exemption. We are waiting to receive the letter and will submitit once we receive it.

(7) Certify to the Idaho State Tax Commission the taxpayer has met, or will meet, the TaxIncentive Criteria before he can claim any of the incentives. IDAPA 942.02. The taxpayershall file Form 89SE with the Idaho State Tax Commission. Id.

As stated, Freightliner submitted Form 89SE to the Idaho State Tax Commission on April 13, 2015. SeeExhibit A.

Conclusion

To obtain the Growth Exemption, the applicant must show evidence supporting each of the sevenrequirements. Freightliner has shown that its project and investments in the project meets the statute'sseven requirements. Freightliner is legally entitled to the Growth Exemption.

The County Commissioners should grant Freightliner a 75% Growth Exemption for a period of 5 yearsstarting January 1, 2016. Freightliner's investments that qualify under the statute are $10.7 million forbuildings and structural components and $875,000 in machinery and equipment.

As shown, Freightliner's project will benefit the County. The project will provide over $12 million in- investments in Bonneville County and add 25 newjobs that pay from $32,000 to $60,000 annually. In

Page' 7

June 19,2015

addition, the County and its taxing districts will receive property tax payments that far out weigh theGrowth Tax Exemption.

We request a hearing as soon as possible to be heard on the application.

Sincerely.

36+04 vi 0, 4UMALK.,c-Jarin 0. Haminer

Beard St. Clair Gaffney

Attorneys for Freightliner ofIdaho, Inc.

189SEM EFO00044

02-13-13

CERTIFICATION FOR IDAHO'S

SMALL EMPLOYER TAX INCENTIVES

Business name

Freifikt li,tar 69 Icuto; LLCBusinass,&moo address

140 So 4 5 37 0 West0% 81518 Ond zip code

Federal employer identitication number

27-285-4476Con)801 pe,Bon and Wie

ToK Q War,ter, C 00Telephone m*or of contact person

801- 978 - 8000Wa+ VA/le CA, Ur 84/10QUALIFYING FOR THE INCENTIVES

To claim the Idaho small employer incentives, you must certify that you have met, or will meet, the following tax incentive criteria at theproject site during the project period:1. Capital investment in new plant and building fadlitles of at least $500,000,

2. Increased employment by at least 10 new employees who each earn at least $19.23 per hour worked and receive health .benefits, and

3. For new employment increases above the 10 new employees, the average wages of the additional new employees is at least$15.50 per hour worked. See the instructions for who is induded in this calculatjon.

The following information is required to certify that the proposed project will meet the small employer tax incentive criteria during theproject period. Failure to provide the requested information may result in the Tax Commission denying any tax incentives claimed underthe Idaho Small Employer Incentive Act.

1. Description of qualifying proJect

*J coUrucle£ 6€000 £9=06 ·F;ot f*e*Aftir 64*vi, 7-7uck. 5*m, /enr,1,+5 a *ct <ervic€ De*le,34,p.

2. Estimated/actual start date of project. The start date is the earlier of the date the first physical change to the project siteoccurs or the date new employees related to the project site are first employed in Idaho. The start date cannot be earlier thanJanuary 1, 2006.

TUA* 90/5

3. Estimated/actual end date of project. The project period cannot be longer than 10 years or end later than December 31, 2020.

Dece# 6· AOAD

4 Location of the proJect site(s). Identify the street address for each site. If more than one location, identify the percent of theInvestment projected at each site once the project is completed.

Not*ec Cor*tr De,o A.8,-u-s hri vt 4„(Q (>Stl,-Sovtk , 1J#60 Alls -TZ)

5. Estimated/actual number of new jobs created during the project period. For each year in the project period, enter the taxyear followed by the number of new jobs created during that year.

Yr 9,0/3 # of jobsyr 10/ 6 4 ofjobs

Yr 1017 #of jobs

Yr &01 8 # ofjobs

YC 1 0 19 + ofjobs

Total # of jobs 29

AS

0

A

0

Yr 1010 # of jobs |Yr # of jobs

Yr # of jobs

Yr # of jobs

Yr # of jobs

Warner Project

Hiring Summary

Idaho Falls, IDMarch 10, 2015

Timing

Initial

Initial

Initial

Initial

Initial

Initial

Initial

Initial

Initial

Initial

Initial

Initial

Totals

Additional (2017)

Additional (2018-2021)Tota Is

Quantity1

1

10

2

1

1

2

1

1

1

2

2

25

2

3

5

Title

General Manager

Office Clerk

service technicans

service advisors

service manager

parts manager

parts counterpersonswarehouse

delivery driver

outside salesperson

new/used truck managerssalespersons

parts advisors

parts counterpersons

$

$

$

$

$

$

$

$

$

$

$

$

Projected annual wage

1Average Wage (Initial Hires)

$

$

Average Wage (Additional Hires)

150,000

35,000

48,000

72,000

96,000

75,000

48,000

25,000

25,000

60,000

96,000

80,000

74,160

52,451

Total Payroll

$ 150,000$ 35,000

$ 480,000

$ 144,000

$ 96,000

$ 75,000

$ 96,000

$ 25,000

$ 25,000$ 60,000

$ 192,000$ 160,000

$ 1,538,000

$ 61,520

$ 148,320

$ 157,353

$ 305,673

$ 61,135

)

:49 IDAHO INVESTMENT TAX CREDIT 2014M EF000030

07-15-14

Name(s) as shown on return

PART 1 - CREDIT AVAILABLE SUBJECT TO LIMITATION

1. a. Amount of qualified investments acquired during the tax year. Include a complete list

b. Amount of investments for which you claimed the property tax exemption. Include Form 49E

c. Subtract line 1 b from line 1 a. This is the amount of qualified investments on which you mayeam the investment tax credit

2. Credit earned. Multiply line 1 c by 3%

3. Pass4hrough share of credit from a partnership, S corporation, estate, or trust:

a. Pass-through Entity Name b. Pass4hrough Entity EIN c. Pass-through Share of ITC

Total column c ............................,.

4. Credit received through unitary sharing. Include a schedule

5. Carryover of investment tax credit from prior years. Indude Form 49C or other schedule ........................6. Credit distributed to partners, shareholders, or beneficiaries7. Credit shared with unitary affiliates

8. Total credit available subject to limitation. Add lines 2 through 5 and subtract lines 6 and 7.. .....................

PART 11 - LIMITATION

,11 1. Enter the Idaho income tax from your return

2. Credit for tax paid to other states

3. Idaho income tax after credit for tax paid to other states. Subtract line 2 from line 14. Credit for contributions to Idaho educational entities ..................................................

5. Tax available after credits. Subtract line 4 from line 3 5

6. 50% of tax after credit for tax paid to other states. Multiply line 3 by 50% ........ 67. Investment tax credit available. Enter the amount from Part 1, line 8

8. Investment tax credit allowed. Enter the smallest amount from lines 5,6, or 7 hereand on Form 44, Part 1, line 1

QUALIFYING DEPRECIABLE PROPERTY

Idaho generally follows the definition of qualified property foundin the Internal Revenue Code (IRC) Sections 46 and 48 as ineffect prior to 1986. The property must have a useful life of threeyears or more and be property for which you are allowed thededuction for depreciation or amortization in lieu of depreciation.Qualifying property includes the following property used in atrade or business:

• Tangible personal property - machinery and equipment• Other tangible property - property used as an integral part

of manufacturing, production, extraction; or furnishingtransportation, communications, or utility services; or researchfacilities and bulk storage facilities used in connection withthose businesses

• Elevators and escalators

- • Single purpose agricultural or horticultural structures• Qualified timber property• Petroleum storage facilities• Qualified broadband equipment as approved by the Idaho

Public Utilities Commission

NONQUALIFYING PROPERTY

Property that does not qualify includes:

3

4

5

6

7

8

Social Security Number or EIN

8

la

1b

1

2

3

4

1c

2

• Buildings and their structural components• Property used in lodging facilities that rent 50% or more of

their lodging units for periods of 30 days or longer, such asapartment houses or rental homes

• The cost of property expensed under IRC Section 179• Property subject to 60-month amortization• Used property not acquired by purchase• The portion of property used for personal use• Used property in excess of $150,000• Horses

• Property not used in Idaho• Vehicles under 8,000 pounds gross weight

68 VWWV.

07-1544 Insrrucrions Tor laano rorm 43

GENERAL INSTRUCTIONS

Form 49 is used to calculate the investment tax credit (ITC)earned or allowed. Each member of a unitary group of

- corporations that earns or is allowed the credit must complete aseparate Form 49.

Property Used Both In and Outside IdahoIf property is used both in and outside Idaho, compute thequalified investment for all such property using one of thefollowing methods:

1. Percentage-of-Use Method - Multiply the investment in eachasset by a fraction where Idaho use is the numerator andtotal use is the denominator. Usage can be measured bymachine hours, mileage, or any other method that accu-rately reflects the usage.

2. Property Factor Numerator Method - Use the amountcorrectly induded in the Idaho property numerator for eachasset.

The amount computed in method #2 will generally be the sameas that computed in method #1 unless your business usesthe Multistate Tax Commission special industry regulations tocompute its factors.

Carryover PeriodsCompute the ITC carryover on Form 49C.• For property acquired after 1989 but prior to tax years

beginning in 2000, the credit carryover is limited to seventax years unless the credit has not been carried over seventax years before 2000. If the credit has been carried for-ward less than seven tax years, and is eligible for carryoverto tax years beginning on or after 2000, the carryover periodis limited to 14 tax years.

• For credit earned in tax years beginning on or after January- 1,2000, the credit carryover is limited to 14 tax years.

For purposes of the carryover period, a short tax year counts asone tax year.

Election to Claim Two-Year Property Tax Exemption andForgo Investment Tax CreditIf you placed personal property in service that qualifies for theITC, you may elect to exempt this property from your propertytax. You aren't eligible for the election if your rate of chargeor rate of return is regulated or limited by federal or state law.The exemption from the property tax is for two years. After thetwo years, you must pay any applicable property tax. You can'tdaim the ITC for any property that you elect to exempt fromproperty tax.

The election is available if you had negative Idaho taxableincome in the second preceding tax year from the tax yearin which the property was placed in service. Negative Idahotaxable income must have been computed without regard toany carryover or carryback of net operating losses.

The election must be made on Form 49E and filed with theoperator's statement or personal property declaration. A copyof the election form must be included with the original incometax return(s) for the tax year(s) in which the property was placedin service.

Biofuel Infrastructure Investment Tax Credit

If you placed biofuel infrastructure in service during the tax yearand are daiming the biofuel infrastructure investment tax credit,you can't daim the ITC on the same property.

ecaptureou must compute recapture if you sell or otherwise dispose of

the property or it ceases to qualify for the ITC before it has beenin service for five full years. File Form 49ER if you daimed theproperty tax exemption. File Form 49R if you claimed the ITC.

SPECIFIC INSTRUCTIONS

Instructions are for lines not fully explained on the form.

PART 1 - CREDIT AVAILABLE SUBJECT TO LIMITATIONLine la. Indude a list of all property you acquired and placedin service during the tax year that qualifies for the ITC. The listshould identify each item of property, your basis in the item,and the date placed in service. The basis of qualified propertyis the Idaho adjusted basis computed without regard to bonusdepreciation. Don't include any property on which you areclaiming the biofuel infrastructure investment tax credit, or anyproperty you are expensing under IRC Section 179.

Line lb. Enter the amount of qualified investments for which youclaimed the property tax exemption. This exemption is allowed inlieu of earning the ITC. Include applicable Form(s) 49E.

Line 3. Include a list of all ITC that is being passed through bypartnerships, S corporations, estates, or trusts in which you havean interest. This amount is reported on Form ID K-1, Part D,line 1. The list should identify each entity by name, EIN, and theamount of ITC that is being passed through.

Line 4. If you are a member of a unitary group, enter the amountof credit you received from another member of the unitary group.

Line 5. Enter the ITC carryover from prior years. The amountis computed on Form 49C or on a separate schedule. Include acopy of Form 49(: or the schedule. See General Instructions forthe carryover period allowed.

Line 6. If you are a partnership, S corporation, trust, or estate,enter the amount of credit that passed through to partners,shareholders, or beneficiaries.

Line 7. If you are a member of a unitary group, enter the amountof credit you earned that you elect to share with other membersof your unitary group. Before you can share your credit, you mustuse the credit up to the allowable limitation of your tax liability.

Corporations claiming ITC must provide a calculation of the creditearned and used by each member of the combined group. Theschedule must clearly identify shared credit and the computationof any credit carryovers.

PART 11 - LIMITATION

The ITC is limited to 50% of your Idaho income tax afterdeducting:• Credit for taxes paid to other states• Credit for contributions to Idaho educational entities

Line 1. Enter the amount ofyour Idaho income tax. This is thecomputed tax before adding the permanent building fund tax orany other taxes, or subtracting any credits.

Line 2. Enter the credit for tax paid to other states from Form39R or Form 39NR. This credit is available only to individuals,estates, and trusts.

Line 8. Enter the smallest amount from lines 5,6, or 7. Carrythis amount to Form 44, Part 1, line 1, and enter it in the CreditAllowed column.

-

SCHEDULE OF QUALIFIED INVESTMENTS

Item/Description

Dynamometer (EKG for heavy trucks)

(2) 7.5t bridge cranes

Lube/oil delivery equipmentDiesel particulate filter

Compressed air system

Gear press

Cleaing equipment

Forklifts/pallet jacks

Parts shelving

Compactors and bailers

Miscellaneous shop tools

IT equipment (PCs, lap tops, copiers, etc.)

Total

$

$

$

$

$

$

$

$

$

$

$

$

Estimated

Value Useful Life

200,000

330,000

85,000

25,000

100,000

15,000

85,000

50,000

100,000

75,000

110,000

100,000

$ 1,275,000

10

10

5

5

10

10

5

5

15

5

5

5

Total $

Tax Rate

Building

Equipment

$

$

0.009595565

10,700,000

875,000

Total Investment $ 11,575,000

Estimated Total Annual Tax $

Estimated Tax Paid

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

27,767

27,767

27,767

27,767

27,767

111,069

111,069

111,069

111,069

111,069

111,069

111,069

111,069

111,069

111,069

111,069

111,069

111,069

111,069

111,069

1,804,866

$

75% Exemption

111,069

Estimated Tax Exempted

$ 83,301

$ 83,301

$ 83,301

$ 83,301

$ 83,3010

0

0

0

0

0

0

0

0

0

0

0

0

0

0

416,507

BONNEVILLE COUNTY TREASURER605 N CAPITAL AVE IDAHO FALLS, ID 83402

TO WHOM IT MAY CONCERN:

DATE: 6/11/2015

ESTIMATION OF TAXES

NAME OF OWNER: FREIGHTLINER OF IDAHO LLC

PARCEL NUMBER: RPO3412003002O & RPO34120030038

FOR ESTIMATED TAXES ON PROPERTY LOCATED AT:

LEGAL DESCRIPTION:

6413 S DOUG ANDRUS DR

IDAHO FALLS ID 83402

LOT 2 AND S 270,971 SQ FT LOT 3, BLOCK 3,ANDCO # 3 SEl/4, SEC 4, T l N, R 37

RESIDENTIAL IMPROVEMENT & QUALIFIED LAND:OTHER IMPROVEMENT:

<'-'OTHER LAND:

TAXABLE AMOUNT:

PROPERTY TAXES FOR THE YEAR

WILL BE APPROXIMATLEY:

THIS INCLUDES: LANDFILL FEE: $

LIBRARY $

OTHER FEES: $

BASED ON

42.00

53.50

2014 LEVY & ESTIMATED VALUE0.009595565

2015

$

$

$ 10,700,000

10,700,000

102,768.06

THIS ESTIMATE DOES NOT INCLUDE A BUFFER TO COVER ANY INCREASE IN CURRENT YEAR LEVYOR VALUE CHANGE. THIS ESTIMATE WAS DETERMINED BY INFORMATION AVAILABLE ON THEDATE LISTED ABOVE.

Rachelle DePaolo

Chief Deputy Treasurer

(208) 529-1350 Ext. 1481

Christopher St Jeor I Regional Economist Communications &Research Idaho Department of Labor 1515 East Lincoln Road I IdahoFalls, ID 83401-2129 208-557-2500 ext. 3077 Cell: 760-413-7059 Fax:208-525-7268 [email protected]

The Jobs multiplier for the industry is 1.64, however, this is likely an

under representation of what the actual effect will be due to the

significantly higher than average wages that Warner Trucking will bepaying. Based on the average wage of $60,000 per job, the multiplieris more likely be around 1.92, bringing the total change in jobs to 46,

or 22 additional jobs after the initial change. This would increaseBonneville County's total employee compensation by an estimated$2,244,270 per year. - from Chris St. Jeor

1RED!\,44,--\h\\'.*%1 REGIONALECONOMIC

DEVELOPMENT

FOR EASTIDAHO

Bonneville County CommissionATTN: Roger Christensen, Chair605 North CapitalIdaho Falls, ID 83402

Dear Roger,

RE: Letter of Support for Project Warner

June 11, 2015

We have been working with this project for nearly a year, and have coordinated with the company

regarding site selection, incentives with the Idaho Department of Commerce, and utility and

transportation access. We have also referred them to the Idaho Department of Labor regarding

workforce training and funding.

This company exceeds the criteria for the "Idaho Business Advantage" (Idaho Code 63-4401 to 4409) in

terms of capital investment, new job creation for numbers ofjobs and above average wages to be paid.

They have also filed the 89SE form with the Idaho State Tax Commission.

We support their application for a property tax exemption as allowed by the statute(s), and at the

discretion and analysis of the Commission.

Thank you for your consideration.

Very truly yours,

-re--=-

C--*/ - 9% C.--I--

Darlene E. GerryInterim Executive Director

151 North Ridge Avenue Suite A., Idaho Falls, ID 83402-4002 208.522.2014

'

JUL-20-2015 09:08 FPOM: SHELLY SCHOOL DIST. M 2083575741

--

Whm I @me Rmr

July 20, 2015

TO:35299732

SHELLEY JOINT SCHOOL DISTRICT NO. 60

545 Seminary AvenueShelley, Idaho 83274

208/357-3411 208/357-5741 (fax)

Bonneville County Commissioners605 N Capital AveIdaho Falls, ID 83402

Commissioners::

Dr. Bryan D. JolleySuperintendent of Schools

Concerning the matter of the application from Freightliner for property tax exemption,the Shelley School District No. 60 does not object to this application as we encourageeconomic development in appropriate areas for the benefit of our patrons and students.

We support the Commission in its efforts to negotiate exemptions and yield to thediscrection of the Commission in its final decision.

Respectfully,

,Dr. Bryan D Jolle;Superintendent ot Schools

P:2 2

Linda,

IDAHODEPARTMENT OF LABORC.L "BuTcH" OTTER. GOVERNOR

KENNETH D. EDMUNDS, DIRECTOR

Thank you for your request regarding the potential economic impact of the Warner Trucking Project. Inorder to calculate the potential economic impact, I performed an industry input-output analysis forBonneville County. This type of statistical analysis calculates the multiplier effect of the initial injectionofjobs into the economy, as well as any trickledown, or secondary effects in the economy. In otherwords, a job multiplier greater than one is a positive indicator of additional jobs being generated as aresult ofthe initial change, and a job multiplier equal to one indicates that no additional jobs would begenerated after the initial change.

As for the Warner Trucking project, the jobs multiplier for the industry is 1.64. However, this is likelyan under representation ofwhat the actual effect will be due to the significantly higher than averagewages that Warner Trucking will be paying. Based on the average wage of $60,000 per job, the truemultiplier is more likely to be around 1.92, bringing the total change in jobs to 46, or an additional 22jobs generated after the initial input. This would increase Bonneville County's total employeecompensation by an estimated $2,244,270 per year.

I am excited to see such high quality jobs come to the region. Please let me know if you have any furtherquestions.

Thank you,

Christopher St Jeor I Regional EconomistCommunications & Research

Idaho Department of Labor1515 East Lincoln Road I Idaho Falls, ID 83401-2129208-557-2500 ext. 3077

Cell: 760-413-7059

Fax: 208-525-7268

1515 E. Lincoln Road . Idaho Falls, Idaho 83401 -3653 e Tel: 208-557-2500 0 Fax: 208-525-7268 o Web: tabor.idaho.govAn Equal Opportunity Employer and Service Provider. Reasonable accommodations are ovaitable upon request- Did 711 for TTY Idaho Relay Service.

IDAHOCOMMERCE

July 2, 2015

Linda Martin

Regional Economic Development for East Idaho151 North Ridge Ave, Suite AIdaho Falls, ID 83402

Dear Linda,

C.L. "Butch" Otter, Governor

Jeffery Sayer, Director

I would like to express my support for Project Warner's potential expansion in IdahoFalls. With projected plans for 25 new employees that will pay an average wage of$60,000 plus benefits, along with an initial capital investment of more than $11 million,this project will be a great economic boot to Idaho Falls. Additionally, the constructionof a new building will ultimately increase local property taxes and provide increasedrevenue for local schools.

As you are aware, Idaho is known for our low cost of living, reliable and low-cost power,high-quality workforce, stable tax base, and business-friendly policies, not to mentionour state's tremendous natural beauty and quality of life. We consider it to be the bestplace in America to start or expand a company.

We look forward to Project Warner starting construction on their new facility andgrowing together as their business succeeds in Idaho.

Sincerely,

Jeffery SayerDirector

700 W State Street. Boise. Idaho 83702 208.334.2470 or 800.842 5858 commerce.idaho.gov