4. lublin’s investment potential 8 - lubelska wyżyna...

TRANSCRIPT

1. Poland – key stats 4

2. Lublin in Europe 5

3. Lublin – key stats 6

4. Lublin’s investment potential 8

5. Office market in Lublin 10

6. Warehouse market in Lublin 13

7. Lublin’s major investors 16

8. Investor support – organisations and institutions 17

CONTENTS

Lublin

Wrocław

Gdańsk

Kraków

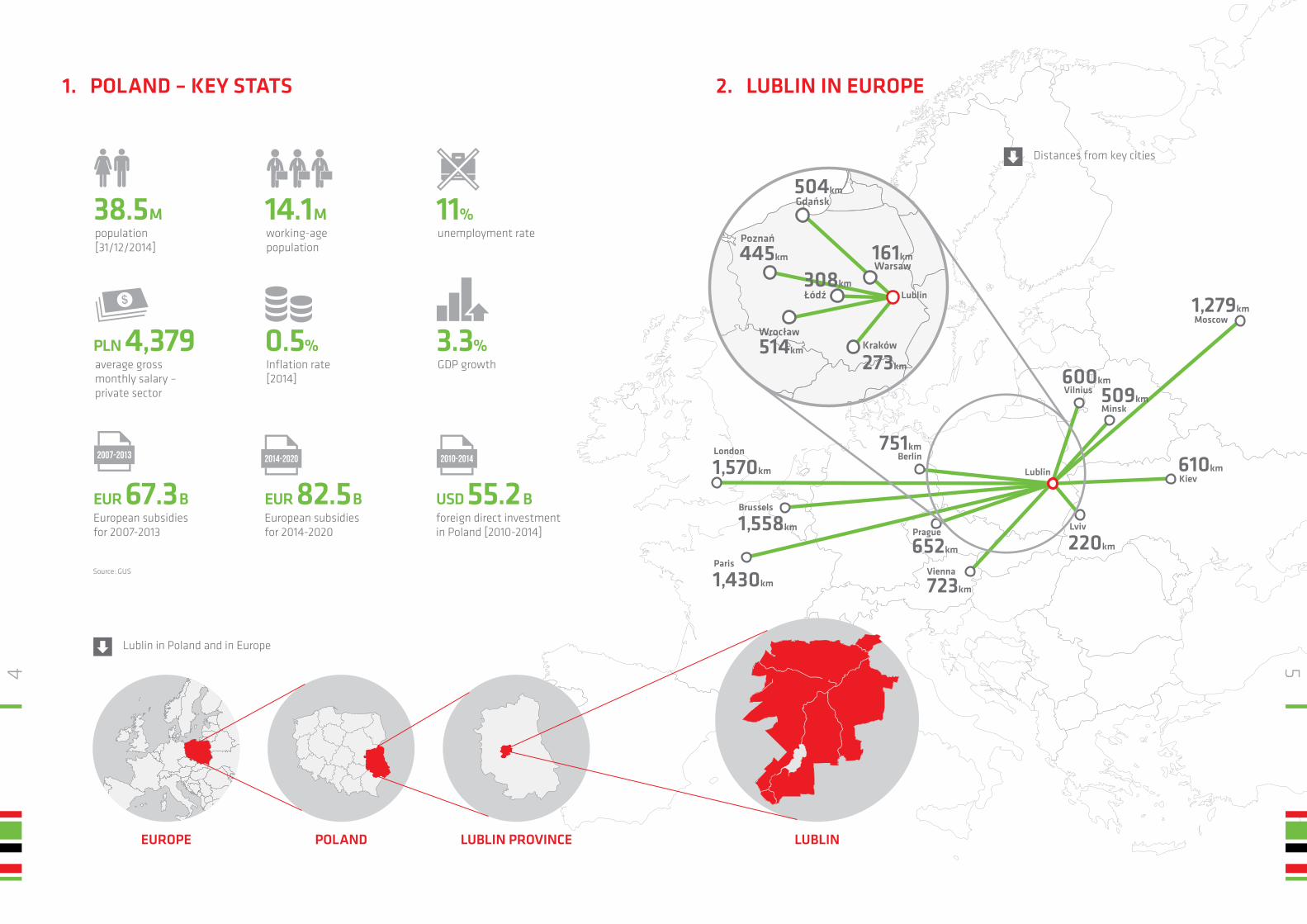

Warsaw161km

273km514km

308km

504km

Poznań

445km

Łódź 1,279km

610km

220km

723km

652km1,558km

751km

600km

509km

Lublin

Lviv

Kiev

Moscow

Vilnius

Minsk

Berlin

Prague

Vienna

Brussels

1,430km

Paris

1,570km

London

LUBLINLUBLIN PROVINCEPOLANDEUROPE

38.5 Mpopulation [31/12/2014]

14.1 M working-age population

11%unemployment rate

PLN 4,379average gross monthly salary – private sector

0.5%Inflation rate [2014]

3.3%GDP growth

EUR 67.3 BEuropean subsidies for 2007-2013

EUR 82.5 BEuropean subsidies for 2014-2020

USD 55.2 Bforeign direct investment in Poland [2010-2014]

Source: GUS

Distances from key cities

1. POLAND – KEY STATS 2. LUBLIN IN EUROPE

Lublin in Poland and in Europe

54

Krakow Gate

Cathedral

Tribunal Dominican Church and Monastery

Grodzka Gate

Historic apartment houses

New City Hall, City O�ce

Lublin Castle

Pobrygidowski Church

Juliusz Osterwa Theatre

343,600population [31/12/2014]

25%population under the age of 25

8.6%unemployment rate

PLN 3,821average gross salary [2013]

27%higher-educated population [2011]

71,000university students

21,200university graduates

9 universities and other higher education institutions

64.3%working age population

Source: GUS

3. LUBLIN – KEY STATS

76

Lublin Chełm

Zamość

Biała Podlaska

7474

S17

S17

S17

S17

A2

S19

S19

S19

S19

S12

S12

motorways, expressways and ring roads — in use

motorways, expressways and ring roads — under construction

motorways, expressways and ring roads — bidding process

motorways, expressways and ring roads — planned

A2 S17 motorway and expressway numbers

functioning railways

Special Economic Zone [Specjalna Strefa Ekonomiczna]

SSE

SSE

Lublin Airport

Lublin is the largest and the most rapidly developing city in eastern Poland. Thanks to its strategic location, dynamically evolving infrastructure and ready access to a young and well-educated workforce, it is currently one of the most attractive destinations for those looking to invest in Poland. The city provides attractive sites for future investments and numer-ous incentives for entrepreneurs, as well as competitive busi-ness costs.

In recent years, Lublin’s growing investment potential has been acknowledged by several local and global investors, who have decided to carry out several projects such as investments in new office and warehouse space. Lublin is of special inter-est to investors due to its close proximity to foreign markets, such as Ukraine and Belarus, and also thanks to lower labour costs and ready access to its highly-qualified workforce.

Lublin was also voted one of the best cities for business in Poland in the Financial Times FDI 2015 “Polish cities of the future” ranking, where it came second in the Cost Effective-ness category for large cities.

4.1 Lublin Airport

The new Lublin Airport was completed and opened for use in 2012. It offers convenient connections with 14 cities in 10 countries in Europe and beyond. In 2014, about 190,000 pas-sengers travelled to or from this airport on over 3,000 flights. The airport is located about 10 km from the city centre, close to the S17 expressway and Świdnik Regional Industrial Park. The opening of this airport significantly boosted the econom-ic development of the Lublin region.

4.2 European funds

Thanks to financing from the European Union, over 16,000 projects were completed, with a total value of more than PLN 29B. The total value of the projects financed in the Lub-lin Voivodship exceeded PLN 19B, including PLN 1.5B for pro-jects in Lublin itself. Some major projects completed in Lublin with the help of European funds: several road infrastructure projects, infrastructure for the SEZ EURO-PARK MIELEC, in-corporating new areas into the zone, and revitalising Lublin’s Old Town.

4.3 Special Economic Zone

The Lublin Subzone forms part of the EURO-PARK MIELEC Special Economic Zone. The Subzone was created in 2009 and covers 118 hectares [with plans for expansion up to 200 hectares]. So far, around 30 industrial, logistics, and high-tech entities have invested in the Subzone, creating over 2,000 jobs. Investment volume in the Subzone exceeds PLN 500M, and is expected to increase to several billion. Companies wishing to invest in the Subzone can expect pub-lic help in the form of a company income tax exemption of up to 70% on investment expenses, and property tax exemption, as part of the regional aid program for job creating investors.

4. LUBLIN’S INVESTMENT POTENTIAL

Infrastructure development

98

Sławin

Sławinek

Czechów

Choiny

Bursak

Rudnik

Ponikwoda

Hajdów

Śródmieście

Stare Miasto

Kalinowszczyzna

Bronowice

Zadębie

Majdan Tatarski

Felin

Konstantynów

Węglin

CzubyPiaski

Kośminek

Dziesiąta

Abramowice

Wrotków

Las Dąbrowa

Las Stary Gaj

2 3

10

Głębocka

Wincentego Witosa

al. Tysiąclecia

al. Solidarności

al. Warszawska

K

raśnicka

Smorawińskiego

Kunickiego

pl. U

nii L

ubel

skie

j

Nałęczowska

12

4

3

5

7

8

9

1011

13

146 12

15

1

2

Droga dojazdowa do A4

SSE

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

0

5,000

10,000

15,000

20,000

25,000

30,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

New supply per year

Cumulative supply[m2]

New supply per year[m2]

Cumulative supply (available)

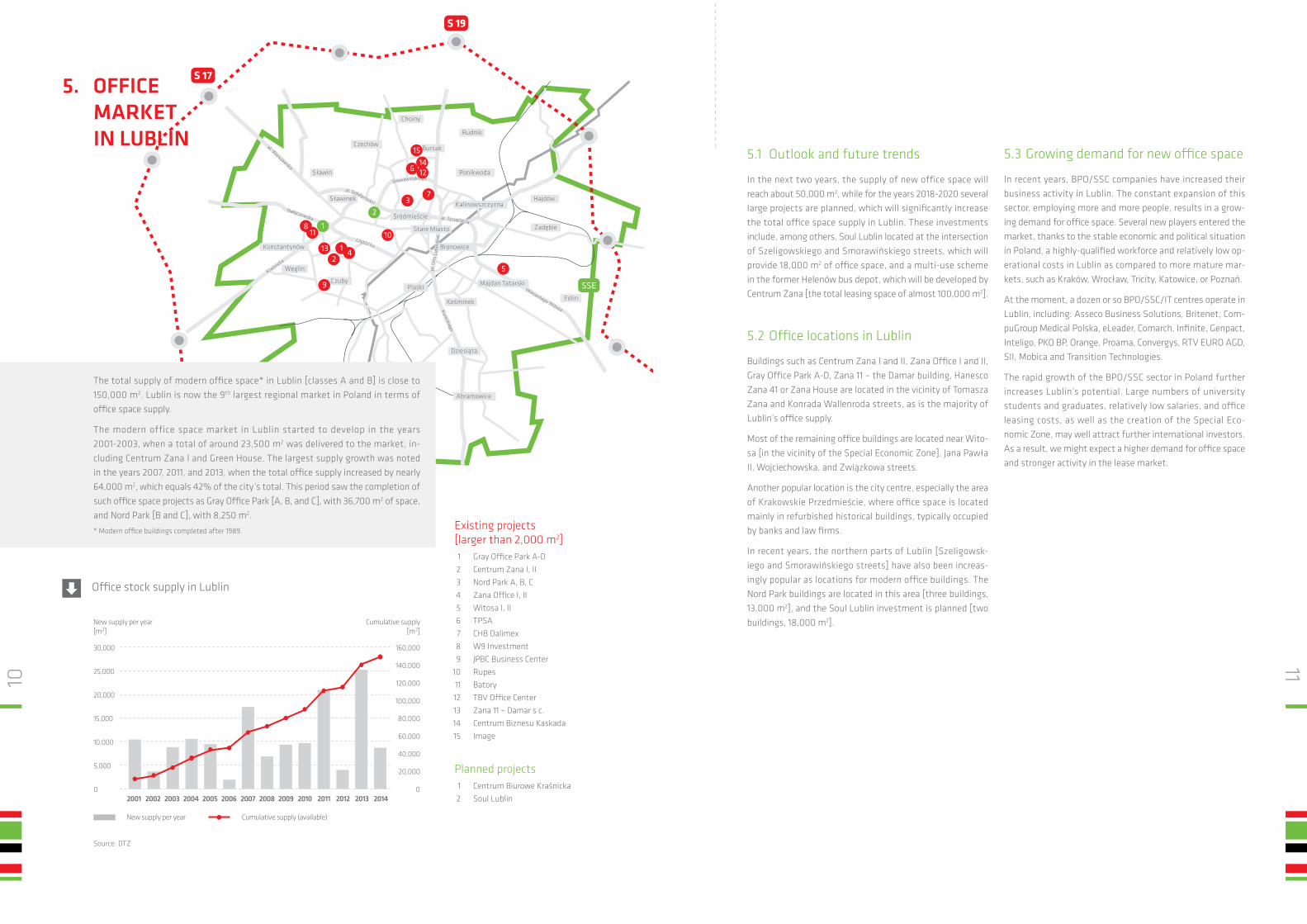

5.1 Outlook and future trends

In the next two years, the supply of new office space will reach about 50,000 m2, while for the years 2018-2020 several large projects are planned, which will significantly increase the total office space supply in Lublin. These investments include, among others, Soul Lublin located at the intersection of Szeligowskiego and Smorawińskiego streets, which will provide 18,000 m2 of office space, and a multi-use scheme in the former Helenów bus depot, which will be developed by Centrum Zana [the total leasing space of almost 100,000 m2].

5.2 Office locations in Lublin

Buildings such as Centrum Zana I and II, Zana Office I and II, Gray Office Park A-D, Zana 11 – the Damar building, Hanesco Zana 41 or Zana House are located in the vicinity of Tomasza Zana and Konrada Wallenroda streets, as is the majority of Lublin’s office supply.

Most of the remaining office buildings are located near Wito-sa [in the vicinity of the Special Economic Zone], Jana Pawła II, Wojciechowska, and Związkowa streets.

Another popular location is the city centre, especially the area of Krakowskie Przedmieście, where office space is located mainly in refurbished historical buildings, typically occupied by banks and law firms.

In recent years, the northern parts of Lublin [Szeligowsk-iego and Smorawińskiego streets] have also been increas-ingly popular as locations for modern office buildings. The Nord Park buildings are located in this area [three buildings, 13,000 m2], and the Soul Lublin investment is planned [two buildings, 18,000 m2].

5.3 Growing demand for new office space

In recent years, BPO/SSC companies have increased their business activity in Lublin. The constant expansion of this sector, employing more and more people, results in a grow-ing demand for office space. Several new players entered the market, thanks to the stable economic and political situation in Poland, a highly-qualified workforce and relatively low op-erational costs in Lublin as compared to more mature mar-kets, such as Kraków, Wrocław, Tricity, Katowice, or Poznań.

At the moment, a dozen or so BPO/SSC/IT centres operate in Lublin, including: Asseco Business Solutions, Britenet, Com-puGroup Medical Polska, eLeader, Comarch, Infinite, Genpact, Inteligo, PKO BP, Orange, Proama, Convergys, RTV EURO AGD, SII, Mobica and Transition Technologies.

The rapid growth of the BPO/SSC sector in Poland further increases Lublin’s potential. Large numbers of university students and graduates, relatively low salaries, and office leasing costs, as well as the creation of the Special Eco-nomic Zone, may well attract further international investors. As a result, we might expect a higher demand for office space and stronger activity in the lease market.

Source: DTZ

The total supply of modern office space* in Lublin [classes A and B] is close to 150,000 m2. Lublin is now the 9th largest regional market in Poland in terms of office space supply.

The modern office space market in Lublin started to develop in the years 2001-2003, when a total of around 23,500 m2 was delivered to the market, in-cluding Centrum Zana I and Green House. The largest supply growth was noted in the years 2007, 2011, and 2013, when the total office supply increased by nearly 64,000 m2, which equals 42% of the city’s total. This period saw the completion of such office space projects as Gray Office Park [A, B, and C], with 36,700 m2 of space, and Nord Park [B and C], with 8,250 m2.

* Modern office buildings completed after 1989.

5. OFFICE MARKET IN LUBLIN

Office stock supply in Lublin

Existing projects [larger than 2,000 m2]1 Gray Office Park A-D2 Centrum Zana I, II3 Nord Park A, B, C4 Zana Office I, II5 Witosa I, II6 TPSA7 CHB Dalimex8 W9 Investment9 JPBC Business Center

10 Rupes11 Batory12 TBV Office Center13 Zana 11 – Damar s c.14 Centrum Biznesu Kaskada15 Image

Planned projects1 Centrum Biurowe Kraśnicka2 Soul Lublin

1110

Sławin

Sławinek

Czechów

Choiny

Bursak

Rudnik

Ponikwoda

Hajdów

Śródmieście

Stare Miasto

Kalinowszczyzna

Bronowice

Zadębie

Majdan Tatarski

Felin

Konstantynów

Węglin

CzubyPiaski

Kośminek

Dziesiąta

Abramowice

Wrotków

Las Dąbrowa

Las Stary Gaj

2 3

10

Głębocka

Wincentego Witosa

al. Tysiąclecia

al. Solidarności

al. Warszawska

K

raśnicka

Smorawińskiego

Kunickiego

pl. U

nii L

ubel

skie

j

Nałęczowska

14

3

2

SSE

H2 2013 H1 2014 H2 2014

17.8%

10.8%

9.3%

10 11 12 13 14 15 16

Kraków

Poznań

Wrocław

Tri-city

Szczecin

Katowice

Łódź

Lublin

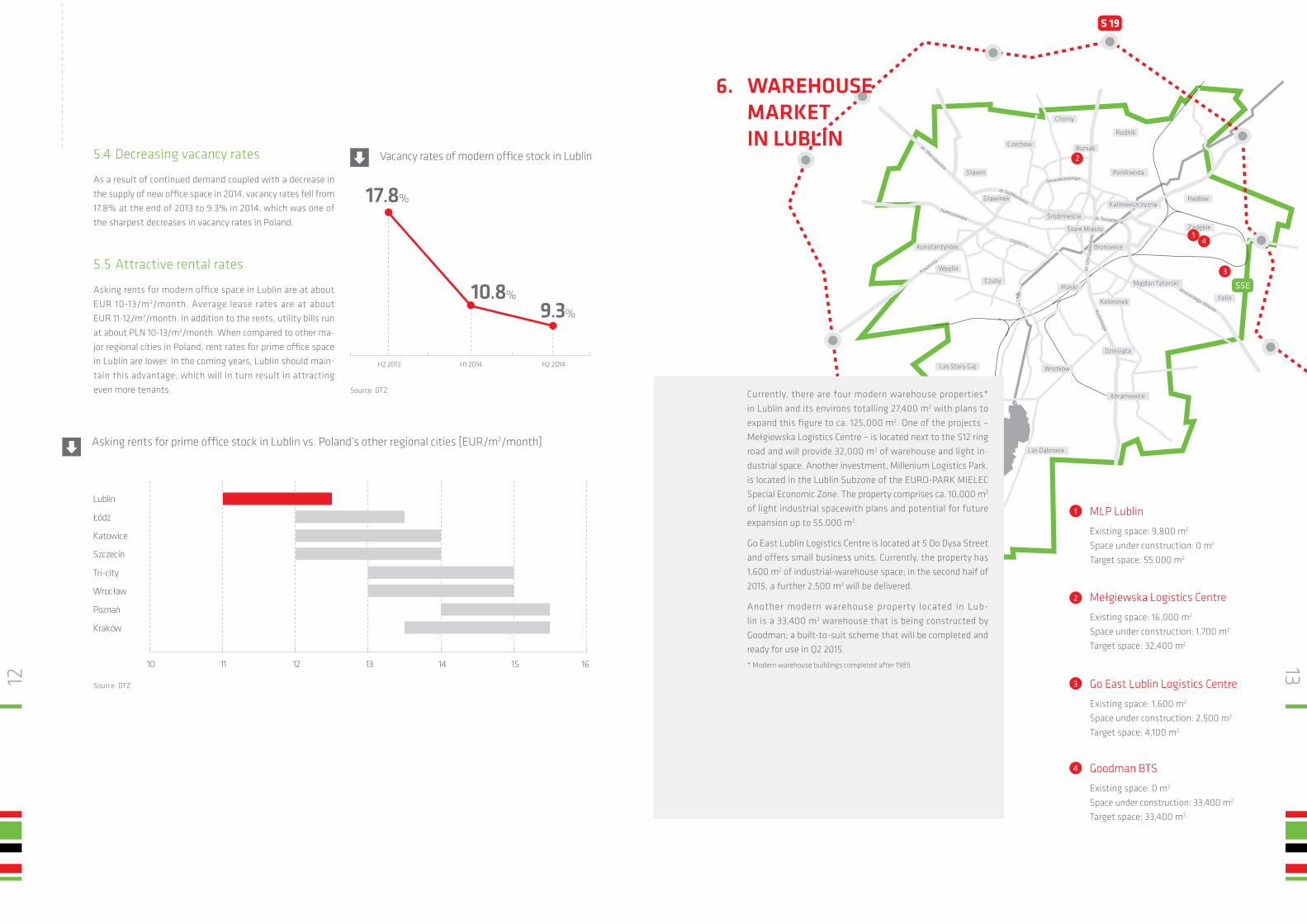

Source: DTZ Currently, there are four modern warehouse properties* in Lublin and its environs totalling 27,400 m2 with plans to expand this figure to ca. 125,000 m2. One of the projects – Mełgiewska Logistics Centre – is located next to the S12 ring road and will provide 32,000 m2 of warehouse and light in-dustrial space. Another investment, Millenium Logistics Park, is located in the Lublin Subzone of the EURO-PARK MIELEC Special Economic Zone. The property comprises ca. 10,000 m2 of light industrial spacewith plans and potential for future expansion up to 55,000 m2.

Go East Lublin Logistics Centre is located at 5 Do Dysa Street and offers small business units. Currently, the property has 1,600 m2 of industrial-warehouse space; in the second half of 2015, a further 2,500 m2 will be delivered.

Another modern warehouse property located in Lub-lin is a 33,400 m2 warehouse that is being constructed by Goodman; a built-to-suit scheme that will be completed and ready for use in Q2 2015.

* Modern warehouse buildings completed after 1989.

5.4 Decreasing vacancy rates

As a result of continued demand coupled with a decrease in the supply of new office space in 2014, vacancy rates fell from 17.8% at the end of 2013 to 9.3% in 2014, which was one of the sharpest decreases in vacancy rates in Poland.

5.5 Attractive rental rates

Asking rents for modern office space in Lublin are at about EUR 10-13/m2/month. Average lease rates are at about EUR 11-12/m2/month. In addition to the rents, utility bills run at about PLN 10-13/m2/month. When compared to other ma-jor regional cities in Poland, rent rates for prime office space in Lublin are lower. In the coming years, Lublin should main-tain this advantage, which will in turn result in attracting even more tenants.

Source: DTZ

6. WAREHOUSE MARKET IN LUBLIN

Vacancy rates of modern office stock in Lublin

Asking rents for prime office stock in Lublin vs. Poland’s other regional cities [EUR/m2/month]

Mełgiewska Logistics Centre

Existing space: 16,000 m2

Space under construction: 1,700 m2

Target space: 32,400 m2

2

MLP Lublin

Existing space: 9,800 m2

Space under construction: 0 m2

Target space: 55,000 m2

1

Go East Lublin Logistics Centre

Existing space: 1,600 m2

Space under construction: 2,500 m2

Target space: 4,100 m2

3

Goodman BTS

Existing space: 0 m2 Space under construction: 33,400 m2 Target space: 33,400 m2

4

1312

Supply under

construction

Target amountof warehousepark supply

Supply forecast [2020]

Existing supply

27,400 37,600

124,900

200,000

Warsaw zone III

Warsaw zone II

Warsaw zone I

Central Poland

Poznań region

Lublin

Lower Silesia

Upper Silesia

Kraków region

Tri-city

2,00 2,50 3,00 3,50 4,00 4,50 5,00 5,50 6,00

6.1 Outlook and future trends

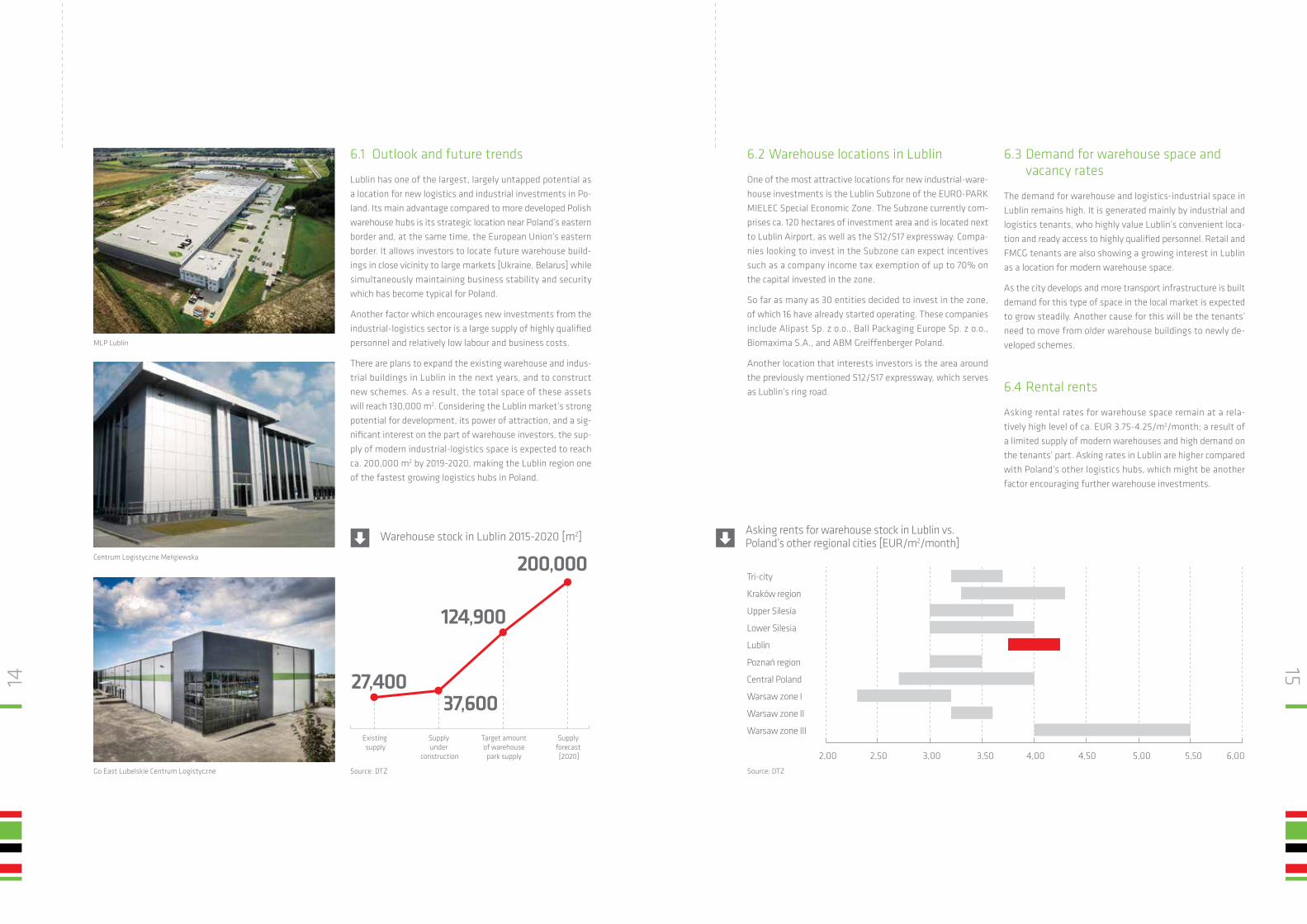

Lublin has one of the largest, largely untapped potential as a location for new logistics and industrial investments in Po-land. Its main advantage compared to more developed Polish warehouse hubs is its strategic location near Poland’s eastern border and, at the same time, the European Union’s eastern border. It allows investors to locate future warehouse build-ings in close vicinity to large markets [Ukraine, Belarus] while simultaneously maintaining business stability and security which has become typical for Poland.

Another factor which encourages new investments from the industrial-logistics sector is a large supply of highly qualified personnel and relatively low labour and business costs.

There are plans to expand the existing warehouse and indus-trial buildings in Lublin in the next years, and to construct new schemes. As a result, the total space of these assets will reach 130,000 m2. Considering the Lublin market’s strong potential for development, its power of attraction, and a sig-nificant interest on the part of warehouse investors, the sup-ply of modern industrial-logistics space is expected to reach ca. 200,000 m2 by 2019-2020, making the Lublin region one of the fastest growing logistics hubs in Poland.

Source: DTZ

6.2 Warehouse locations in Lublin

One of the most attractive locations for new industrial-ware-house investments is the Lublin Subzone of the EURO-PARK MIELEC Special Economic Zone. The Subzone currently com-prises ca. 120 hectares of investment area and is located next to Lublin Airport, as well as the S12/S17 expressway. Compa-nies looking to invest in the Subzone can expect incentives such as a company income tax exemption of up to 70% on the capital invested in the zone.

So far as many as 30 entities decided to invest in the zone, of which 16 have already started operating. These companies include Alipast Sp. z o.o., Ball Packaging Europe Sp. z o.o., Biomaxima S.A., and ABM Greiffenberger Poland.

Another location that interests investors is the area around the previously mentioned S12/S17 expressway, which serves as Lublin’s ring road.

6.3 Demand for warehouse space and vacancy rates

The demand for warehouse and logistics-industrial space in Lublin remains high. It is generated mainly by industrial and logistics tenants, who highly value Lublin’s convenient loca-tion and ready access to highly qualified personnel. Retail and FMCG tenants are also showing a growing interest in Lublin as a location for modern warehouse space.

As the city develops and more transport infrastructure is built demand for this type of space in the local market is expected to grow steadily. Another cause for this will be the tenants’ need to move from older warehouse buildings to newly de-veloped schemes.

6.4 Rental rents

Asking rental rates for warehouse space remain at a rela-tively high level of ca. EUR 3.75-4.25/m2/month; a result of a limited supply of modern warehouses and high demand on the tenants’ part. Asking rates in Lublin are higher compared with Poland’s other logistics hubs, which might be another factor encouraging further warehouse investments.

Source: DTZ

MLP Lublin

Centrum Logistyczne Mełgiewska

Go East Lubelskie Centrum Logistyczne

Warehouse stock in Lublin 2015-2020 [m2] Asking rents for warehouse stock in Lublin vs. Poland’s other regional cities [EUR/m2/month]

1514

Office investors

• Batory Investment • Centrum Zana• Dalimex• Damar• Max-Bud• Kamea Invest• MNS Chrzanowscy• Interbud• TBV

Warehouse investors

• CLM• ECOFUNDDESIGN• Goodman• MLP Group• Raben Group

Other major investors in Lublin

• ABM Greiffenberger Polska Sp. z o.o. • AgustaWestland PZL-Świdnik S.A. • Aliplast Sp. z o.o. • Asquini Polska • Asseco Business Solutions S.A. • Ball Packaging Europe Polska Sp. z o.o. • Baxter Manufacturing Sp. z o.o. • Biomed • Clondalkin Pharma • Comarch S.A. • Compugroup Medical Sp. z o.o. • Convergys Corporation • DAEWON EUROPE Sp. z o.o. • eLeader Sp. z o.o. • Genpact • Herbapol Lublin SA • Inergy Automotive Systems Poland Sp. z o.o. • Infinite Sp. z o.o. • LUBELLA Sp. z o.o. S.K.A. • Mobica Limited Sp. z o.o. • MW Lublin • Orange• Perła Browary Lubelskie S.A. • PKO BP • POL-SKONE Sp. z o.o. • Proama • PZ Cormay • Sii Sp. z o.o. • Solar Future Energy • Stock Polska • Trimetis • Ursus S.A.

Plac Łokietka 1, 20-950 Lublin

Tel.: +48 81 466 25 00

e-mail: [email protected]

www.lublin.eu

Mariusz Sagan

Director of DepartmentPlenipotentiary of the Major for Euro-Park Mielec Special Economic Zonetel.: +48 81 466 25 00e-mail: [email protected]

Łukasz Goś

Supervisor of the Division for Investor AssistanceProject Manager for Food Industrytel.: +48 81 466 25 06e-mail: [email protected]

Honorata Kępowicz-Olszówka

Project Manager for IT/BPOtel.: +48 781 590 025e-mail: [email protected]

Michał Grabowiecki

Project Manager for IT/BPOtel.: +48 81 466 25 11e-mail: [email protected]

Przemysław Gruba

Project Manager for Logistics and Hospitality Industrytel.: +48 81 466 25 11e-mail: [email protected]

Diana Ciszewska

Project Manager for Biotechnologiestel.: +48 81 466 25 07e-mail: [email protected]

Igor Niewiadomski

Project Manager for Automotive Industrytel.: +48 81 466 25 06 e-mail: [email protected]

7. LUBLIN’S MAJOR INVESTORS

8. CITY OF LUBLIN DEPARTMENT OF STRATEGY AND INVESTOR SERVICES

1716

DTZ is a global leader in real estate services. We provide real estate services to business, corporate occupier and investor clients, including: retail, office and industrial lease agency, integrated end-to-end service covering property and facility management, capital markets, investment consultancy, valuation, pro-ject and building consultancy.

Additionally, through the best quality market research and consultancy ser-vices, we provide our clients with global and local market knowledge. By fore-casting market trends and development, we provide best-in-class long-term solutions and support our clients.

DTZ has 28 000 employees, operating across 260 offices in 50 countries.

More information on www.dtz.com.

Publication prepared for the Department of Strategy and Investor Services for the City of Lublin by DTZ Polska sp. z o.o.