3q’08 earnings presentation - library.corporate...

TRANSCRIPT

0

3Q’08 EARNINGS PRESENTATIONDecmber 1st, 2008

1

Forward Looking Statements

This presentation may contain projections or other forward-looking statements related to Masisa that involve risks and uncertainties. Readers are cautioned that these statements are only projections and may differ materially from actual future results or events. There is no assurance that the expected events, trends or results will effectively occur. These declarations are made on the basis of numerous assumptions and factors, including general economic and market conditions, industry conditions and operating factors. Any change to these assumptions or factors could cause the present results of Masisa and Masisa’s planned actions to differ substantially from the present expectations.

All forward-looking statements are based on information available to Masisa on the date of its posting and Masisa assumes no obligation to update such statements unless otherwise required by applicable law.

2

Contents

Performance Improvements 3Q’08 Versus 3Q’07

Results Comparison 3Q’08 Versus 3Q’07

Important Events 3Q’08

Important Events 3Q’08

Financial Overview

3

Important Events 3Q’08

Operational Results: 1.4% Ebitda increase, in spite of historical high costs, reaching a trailing twelve month

Ebitda of US$ 196.9 million. 3Q´08 Ebitda of US$ 46.8 million.

Larger market diversification, expanding in products with higher margins (melaminated wood boards and

sawn lumber). This in conjunction with a decreased dependency from the United States sales, that represented

10.9% of consolidated sales in 3Q’08, as a consequence of decreasing the exposure to the mouldings market

(MDF and Finger Joint).

October, start up of new melamine line in Coronel (Mapal), Chile. Annual installed capacity of 150,000 m3.

This is in line with the strategy of improving the product mix, focusing on higher margin products.

Focus on Core Business:

End of sale process of the OSB plant in Ponta Grossa, Brazil.

Finger-Joint Mouldings:

Shut down of the production line in Chile (Cabrero).

Production reduction in Brazil (Rio Negrinho)

Private bidding offer for sawmill and Finger-Joint moulding line in Rio Negrinho.

4

Contents

Performance Improvements 3Q’08 Versus 3Q’07

Results Comparison 3Q’08 Versus 3Q’07

Important Events 3Q’08

Important Events 3Q’08

Financial Overview

5

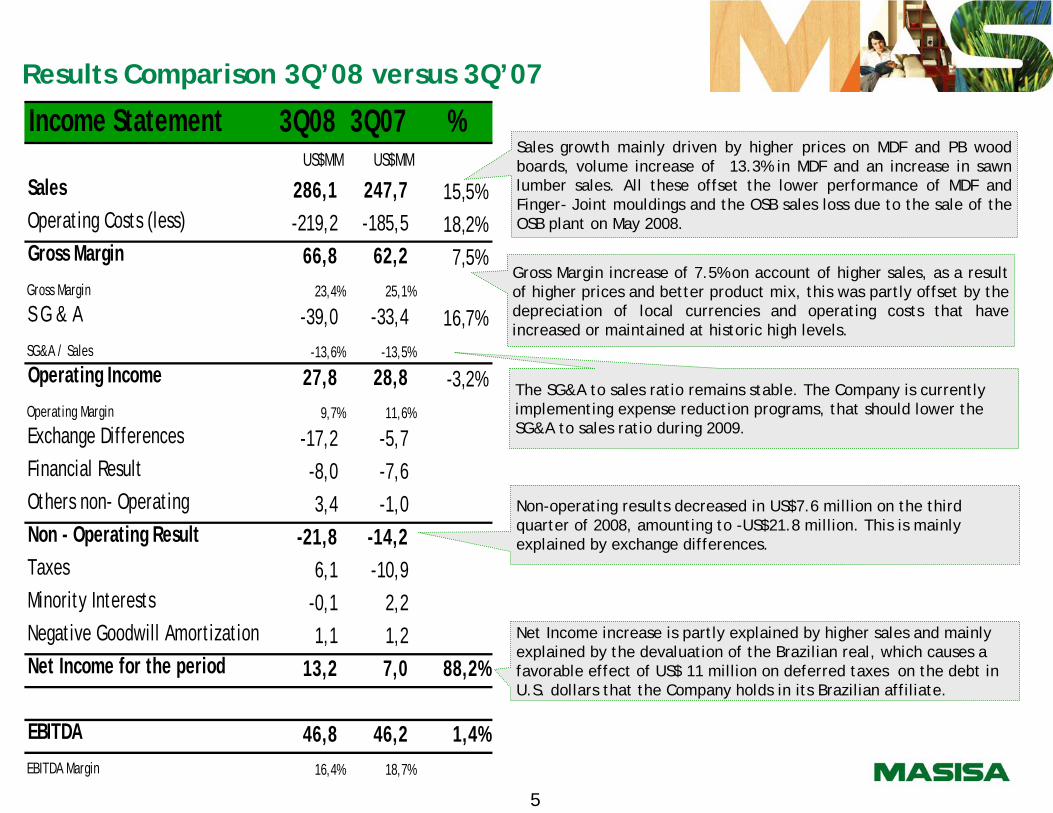

Income Statement 3Q08 3Q07 %US$MM US$MM

Sales 286,1 247,7 15,5%Operating Costs (less) -219,2 -185,5 18,2%Gross Margin 66,8 62,2 7,5%Gross Margin 23,4% 25,1%

S G & A -39,0 -33,4 16,7%SG&A / Sales -13,6% -13,5%

Operating Income 27,8 28,8 -3,2%Operating Margin 9,7% 11,6%

Exchange Differences -17,2 -5,7 Financial Result -8,0 -7,6 Others non- Operating 3,4 -1,0 Non - Operating Result -21,8 -14,2 Taxes 6,1 -10,9 Minority Interests -0,1 2,2 Negative Goodwill Amortization 1,1 1,2 Net Income for the period 13,2 7,0 88,2%

EBITDA 46,8 46,2 1,4%EBITDA Margin 16,4% 18,7%

Results Comparison 3Q’08 versus 3Q’07

Sales growth mainly driven by higher prices on MDF and PB wood boards, volume increase of 13.3% in MDF and an increase in sawnlumber sales. All these offset the lower performance of MDF and Finger- Joint mouldings and the OSB sales loss due to the sale of the OSB plant on May 2008.

Non-operating results decreased in US$7.6 million on the third quarter of 2008, amounting to -US$21.8 million. This is mainly explained by exchange differences.

The SG&A to sales ratio remains stable. The Company is currentlyimplementing expense reduction programs, that should lower the SG&A to sales ratio during 2009.

Gross Margin increase of 7.5% on account of higher sales, as a result of higher prices and better product mix, this was partly offset by the depreciation of local currencies and operating costs that have increased or maintained at historic high levels.

Net Income increase is partly explained by higher sales and mainly explained by the devaluation of the Brazilian real, which causes a favorable effect of US$ 11 million on deferred taxes on the debt in U.S. dollars that the Company holds in its Brazilian affiliate.

6

Contents

Performance Improvements 3Q’08 Versus 3Q’07

Results Comparison 3Q’08 Versus 3Q’07

Important Events 3Q’08

Important Events 3Q’08

Financial Overview

7

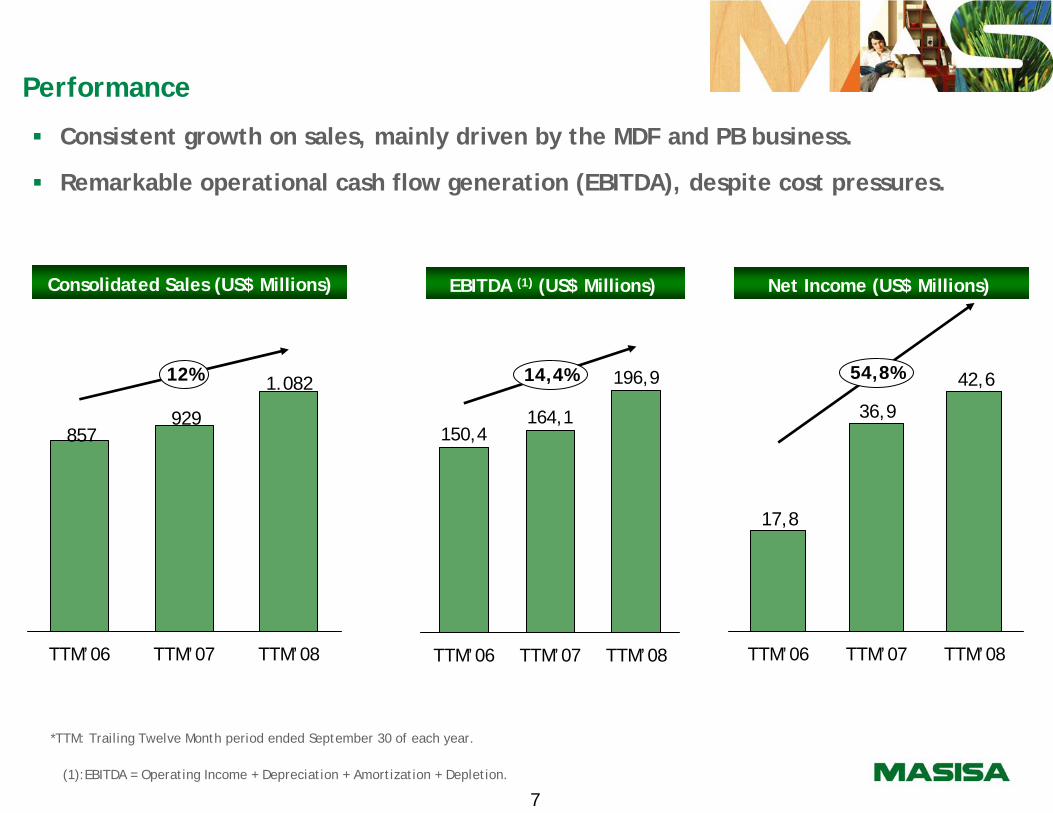

Performance

Consistent growth on sales, mainly driven by the MDF and PB business.

Remarkable operational cash flow generation (EBITDA), despite cost pressures.

*TTM: Trailing Twelve Month period ended September 30 of each year.

1.082

929857

12%

TTM’08TTM’06 TTM’07

150,4

TTM’06

164,1

TTM’07

196,914,4%

TTM’08

42,6

36,9

17,8

54,8%

TTM’06 TTM’07 TTM’08

Consolidated Sales (US$ Millions) EBITDA (1) (US$ Millions) Net Income (US$ Millions)

(1):EBITDA = Operating Income + Depreciation + Amortization + Depletion.

8

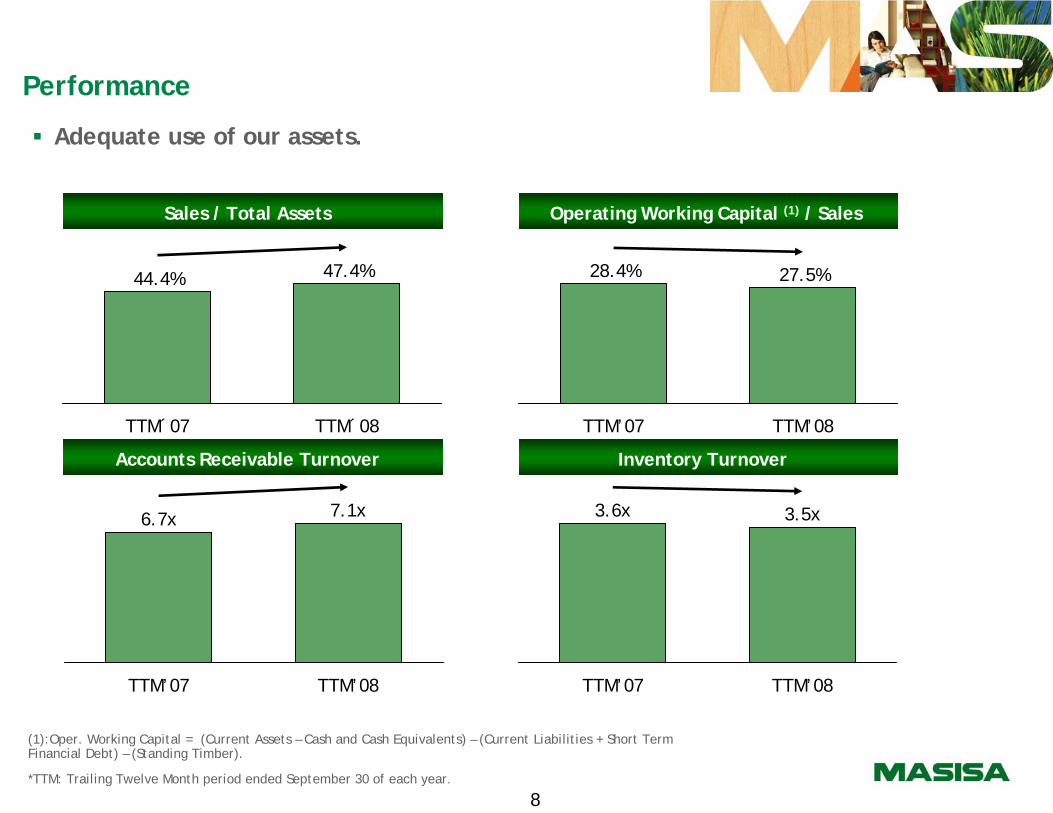

Performance

Adequate use of our assets.

Sales / Total Assets

Inventory Turnover Accounts Receivable Turnover

Operating Working Capital (1) / Sales

28.4%

TTM’07

27.5%

TTM’08

6.7x

TTM’07

7.1x

TTM’08

3.6x

TTM’07

3.5x

TTM’08

44.4%

TTM´07

47.4%

TTM´08

(1):Oper. Working Capital = (Current Assets – Cash and Cash Equivalents) – (Current Liabilities + Short Term Financial Debt) – (Standing Timber).

*TTM: Trailing Twelve Month period ended September 30 of each year.

9

Contents

Performance Improvements 3Q’08 Versus 3Q’07

Results Comparison 3Q’08 Versus 3Q’07

Important Events 3Q’08

Important Events 3Q’08

Financial Overview

10

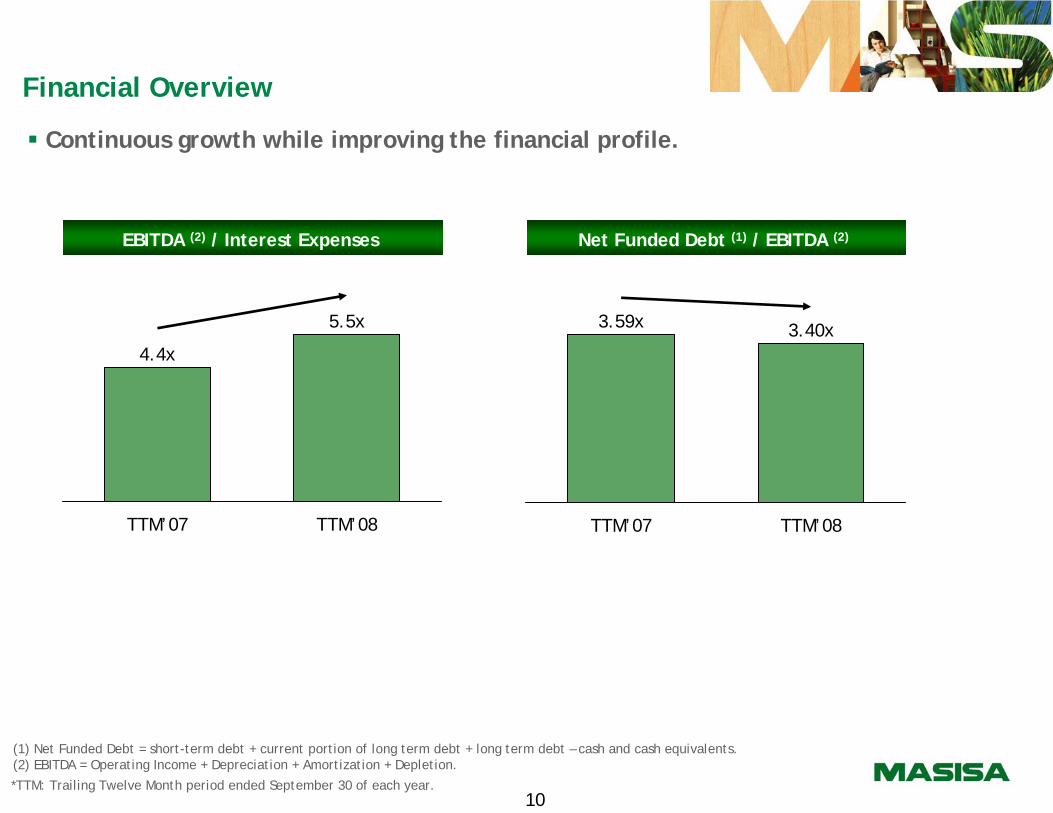

Financial Overview

Continuous growth while improving the financial profile.

4.4x

TTM’07

5.5x

TTM’08

EBITDA (2) / Interest Expenses Net Funded Debt (1) / EBITDA (2)

3.59x

TTM’07

3.40x

TTM’08

(1) Net Funded Debt = short-term debt + current portion of long term debt + long term debt – cash and cash equivalents. (2) EBITDA = Operating Income + Depreciation + Amortization + Depletion.

*TTM: Trailing Twelve Month period ended September 30 of each year.

11

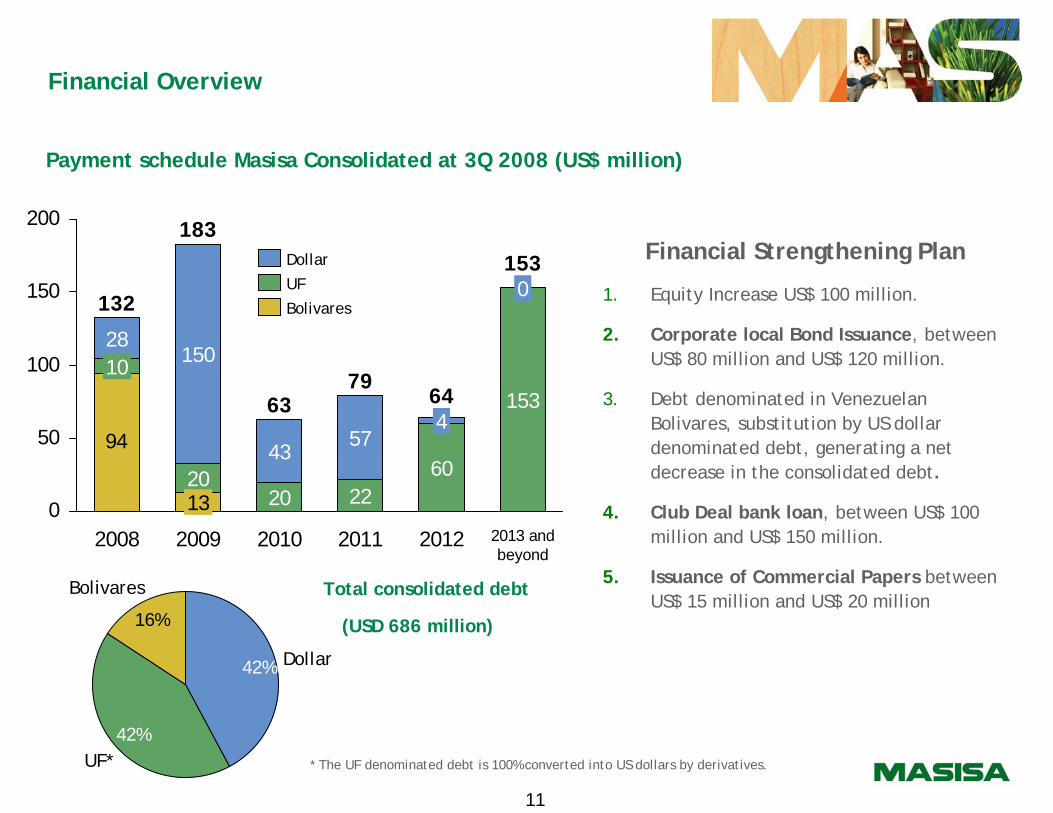

Financial Overview

Total consolidated debt

(USD 686 million)

Financial Strengthening Plan

1. Equity Increase US$ 100 million.

2. Corporate local Bond Issuance, between US$ 80 million and US$ 120 million.

3. Debt denominated in Venezuelan Bolivares, substitution by US dollar denominated debt, generating a net decrease in the consolidated debt.

4. Club Deal bank loan, between US$ 100 million and US$ 150 million.

5. Issuance of Commercial Papers between US$ 15 million and US$ 20 million

Payment schedule Masisa Consolidated at 3Q 2008 (US$ million)

94

0

50

100

150

200

2810

132

2008

150

2013

183

2009

43

20

63

2010

57

22

79

2011

4

60

64

2012

0

153

153

2013 and beyond

Dollar

UF

Bolivares

42% Dollar

42%UF*

16%

Bolivares

* The UF denominated debt is 100% converted into US dollars by derivatives.

12

Contents

Performance Improvements 3Q’08 Versus 3Q’07

Results Comparison 3Q’08 Versus 3Q’07

Important Events 3Q’08

Important Events 3Q’08

Financial Overview

13

Wood Boards Business Unit

1. Stable demand continues in most of the Latin American markets, except in the Chilean market, where there was an 8% decrease in MDF wood boards sales. On a consolidated level, MDF sales increase 38.9% and PB sales increase 16.9% when compared to 3Q´07.

2. Ability to transfer cost increases into prices continued, although the capacity has been limited on account of the strong depreciations of the local currencies. Consolidated prices increase 23% and 17% in MDF and PB, respectively.

3. Cost pressures continued, reaching historical levels. Decreases are expected early 2009 in wood, resins and transportation costs.

4. Initiatives for increasing margins continued:

Product mix sales (43% of wood boards sales are melaminated).

Sales through Placacentros represent 30% of local wood board sales.

5. New MDF plant in Cabrero, increasing supply to Latin American Pacific Coast Markets. Increase in MDF volume of 13% 3Q’08 on 3Q’07.

14

1. Continued the migration of Placacentros from brand license contracts to franchise level agreements -as scheduled.

71% of the Placacentro network has been franchised.

Total number of Placacentros as of September 30, 2008: 329.

2. Strategic relevance of new Placacentro franchise scheme:

Masisa exclusivity: sales volume increase.

Better product mix: margins increase.

Placacentro services: generates customer loyalty and enhances shopping experience – brand positioning.

3. Development of other commercial efforts – as scheduled:

Procurement Units (PU), total sales during 3Q’08: US$3.2 million versus US$0.9 million in 3Q’07.

Application of Placacentros Franchise Operating Manual. 31 Placacentros fully trained and 112 in process, as of September 30, 2008. Objective: 80% of the network trained by April 2009.

Retail Business Unit

15

Solid Wood Business Unit

1. Lower sales of MDF (-35.4%) and Finger-Joint (-36%) mouldings, due to the Company´s strategic decision of downscaling production of such products on account of the United States real estate market downturn.

2. Sawn lumber sales soared (+54.5%), on account of re-routing exports to local markets in Brazil and Venezuela and also to Middle East and Central American markets.

3. Solid wood doors, dropped slightly (-6,1%), due to specific logistic dispatch problems (bad sea weather conditions).

4. Focus on higher margin products, increasing production of sawn lumber and decreasing production of Finger-Joint mouldings. MDF mouldings production remains stable, but at lower volumes (MDF mouldingshave high sinergies with the main wood board business unit). All this has implied:

Shut down of Finger-Joint moulding productive line in Cabrero (Chile)

Production reduction of Finger-Joint mouldings at the Rio Negrinho line (Brazil).

5. Private bidding offer for the sale of a sawmill and a Finger-Joint moulding line in Rio Negrinho, Brazil:

Assets are not part of main core business (wood boards).

Assets are not synergic (too distant) to wood board plants in Brazil.

Sale with fiber supply offer or with the optino of acquiring Masisa´s forestry mass in Rio Negrinho.

16

Regional Leadership ConsolidationFinancial strengthenig plan.

New MDP Plant construction in Rio Grande do Sul, Brazil, on schedule with more than a 50% progress

and entering production on mid – 2009.

Focus on higher margin products.

Market diversification for sawn lumber.

Cost optimization programs: programs on various business lines.

Focus on main core business: wood boards.

Execution of SG&A expenses saving program during 2009, approx. annual savings of US$15 million.

17

http://www.masisa.com

For further information, please log on to our web site:

Or contact our Investor Relations team:

18