3.amol disertaion

TRANSCRIPT

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

CHAPTAR NO: 1

INTRDUCTION

1.1 Introduction of Loan:-

Loan is an amount of money advanced to a borrower, to be repaid at a

later date, usually with interest. Legally, a loan is a contract between a buyer (the

borrower) and a seller (the lender), enforceable under the Uniform Commercial

Code in most states. The terms and conditions for repayment of a loan, including

the finance charge or interest rate, are specified in a loan agreement. a loan may

be payable on demand (a Demand Loan), in equal monthly installments (an

installments loan)

It is also define as when a lender gives money or property to a borrower

and the borrower agrees to return the property or repay the borrowed money,

along with interest, at a predetermined date in the future.

Definition

An arrangement in which a lender gives money or property to a borrower,

and the borrower agrees to return the property or repay the money, usually

along with interest, at some future point(s) in time. Usually, there is a

predetermined time for repaying a loan, and generally the lender has

to bear the risk that the borrower may not repay a loan (though

loan modern capital markets have developed many ways of managing this risk).

Loan is a type of debt. Like all debt instruments, a loan entails the redistribution of

financial assets over time, between the lender and the borrower.

In a loan, the borrower initially receives or borrows an amount of money, called

the principal, from the lender, and is obligated to pay back or repay an equal

amount of money to the lender at a later time. Typically, the money is paid back in

regular installments, or partial repayments; in an annuity, each installment is the

same amount.

Page 1

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

The loan is generally provided at a cost, referred to as interest on the debt, which

provides an incentive for the lender to engage in the loan. In a legal loan, each of

these obligations and restrictions is enforced by contract, which can also place the

borrower under additional restrictions known as loan covenants. Although this

article focuses on monetary loans, in practice any material object might be lent

1.2 Secured Loan:-

A secured loan is a loan in which the borrower pledges some asset (e.g. a

car or property) as collateral.

A mortgage loan is a very common type of debt instrument, used by many

individuals to purchase housing. In this arrangement, the money is used to

purchase the property. The financial institution, however, is given security —

a lien on the title to the house — until the mortgage is paid off in full. If the

borrower defaults on the loan, the bank would have the legal right to repossess the

house and sell it, to recover sums owing to it.

In some instances, a loan taken out to purchase a new or used car may be

secured by the car; in much the same way as a mortgage is secured by housing.

The duration of the loan period is considerably shorter — often corresponding to

the useful life of the car. There are two types of auto loans, direct and indirect. A

direct auto loan is where a bank gives the loan directly to a consumer. An indirect

auto loan is where a car dealership acts as an intermediary between the bank or

financial institution and the consumer.

1.3 Unsecured Loan:-

Unsecured loans are monetary loans that are not secured against the

borrower's assets. These may be available from financial institutions under many

different guises or marketing packages:

credit card debt

personal loans

bank overdrafts

Page 2

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

credit facilities or lines of credit

corporate bonds (may be secured or unsecured)

The interest rates applicable to these different forms may vary depending on

the lender and the borrower. These may or may not be regulated by law. In the

United Kingdom, when applied to individuals, these may come under

the Consumer Credit Act 1974.

Interest rates on unsecured loans are nearly always higher than for secured

loans, because an unsecured lender's options for recourse against the borrower in

the event of default are severely limited. An unsecured lender must sue the

borrower, obtain a money judgment for breach of contract, and then pursue

execution of the judgment against the borrower's unencumbered assets (that is, the

ones not already pledged to secured lenders). In insolvency proceedings, secured

lenders traditionally have priority over unsecured lenders when a court divides up

the borrower's assets. Thus, a higher interest rate reflects the additional risk that in

the event of insolvency, the debt may be uncollectible.

Rules:-

1. A loan is not gross income to the borrower.

Since the borrower has the obligation to repay the loan, the borrower has

no accession to wealth.

2. The lender may not deduct (from own gross income) the amount of the

loan.

The rationale here is that one asset (the cash) has been converted into a

different asset (a promise of repayment) Deductions are not typically available

when an outlay serves to create a new or different asset.

3. The amount paid to satisfy the loan obligation is not deductible (from own

gross income) by the borrower.

4. Repayment of the loan is not gross income to the lender.

Page 3

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

In effect, the promise of repayment is converted back to cash, with no

accession to wealth by the lender.

5. Interest paid to the lender is included in the lender’s gross income.

Interest paid represents compensation for the use of the lender’s money or

property and thus represents profit or an accession to wealth to the lender. Interest

income can be attributed to lenders even if the lender doesn’t charge a minimum

amount of interest.

6. Interest paid to the lender may be deductible by the borrower.

In general, interest paid in connection with the borrower’s business

activity is deductible, while interest paid on personal loans are not deductible. The

major exception here is interest paid on a home mortgage

CHAPTER NO: 2

Page 4

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

BANK PROFILE

2.1 History

Bank of Baroda (BoB) (BSE: 532134) is the third largest bank in India,

after the State Bank of India and the Punjab National Bank and ahead of ICICI

Bank BoB is ranked 763 in Forbes Global 2000 list. BoB has total assets in

excess of Rs. 3.58 lakh cores, or Rs. 3,583 billion, a network of over 3,778

branches and offices, and about 1,657 ATMs. It plans to open 400 new branches

in the coming year. It offers a wide range of banking products and financial

services to corporate and retail customers through a variety of delivery channels

and through its specialized subsidiaries and affiliates in the areas of investment

banking, credit cards and asset management. Its total business was Rs. 5,452

billion as of June 30.

As of August 2010, the bank has 78 branches abroad and by the end of

FY11 this number should climb to 90. In 2010, BOB opened a branch in

Auckland, New Zealand, and its tenth branch in the United Kingdom. The bank

also plans to open five branches in Africa. Besides branches, BoB plans to open

three outlets in the Persian Gulf region that will consist of ATMs with a couple of

people.

The Maharajah of Baroda, Sir Sayajirao Gaekwad III, founded the bank on

20 July 1908 in the princely state of Baroda, in Gujarat. The bank, along with 13

other major commercial banks of India, was nationalized on 19 July 1969, by

the government of India.

2.2 Year wise History:

Page 5

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

1908-1959

1908: Maharaja Sayajirao Gaekwad III set up Bank of Baroda (BOB).

1910: BoB established its first branch in Ahmedabad.

1953: BoB established a branch in Mombasa and another in Kampala.

1954: BoB opened a branch in Nairobi.

1956: BoB opened a branch in Dar-es-Salaam.

1957: BoB established a branch in London.

1959: BoB acquired Hind Bank.

1960s

1961: BoB merged in New Citizen Bank of India. This merger helped it

increase its branch network in Maharashtra. BOB also opened a branch

in Fiji.

1962: BoB opened a branch in Mauritius.

1963: BoB acquired Surat Banking Corporation in Surat, Gujarat.

1964: BoB acquired two banks, Umbergaon People’s Bank in

southern Gujarat and Tamil Nadu Bank of Baroda in Tamil Nadu state.

1964: BoB lost its branch in Narayanjanj (East Pakistan) due to the Indo-

Pakistan war. It is unclear when BOB had opened the branch.

1965: BoB opened a branch in Guyana.

1967: The Tanzanian government nationalized BoB’s three branches there

and transferred their operations to the Tanzanian government-owned

National Banking Corporation.

1969: The Government of India nationalized 14 top banks, including BoB.

BoB incorporated its operations in Uganda as a 51% subsidiary, with the

government owning the rest.

1970s

1972: BoB acquired The Bank of India’s operations in Uganda.

1974: BoB opened a branch each in Dubai and Abu Dhabi.

1975: BoB acquired the majority shareholding and management control

of Bareilly Corporation Bank (est. 1928) and Nainital Bank (est. in 1954),

Page 6

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

both in Uttar Pradesh. Since then, Nainital Bank has expanded

to Uttarakhand State.

1976: BoB opened a branch in Oman and another in Brussels. The

Brussels branch was aimed at Indian firms from Mumbai (Bombay)

engaged in diamond cutting and jewellery having business in Antwerp, a

major center for diamond cutting.

1978: BoB opened a branch in New York and another in the Seychelles.

1979: BoB opened a branch in Nassau, the Bahamas.

1980s

BoB opened a branch in Bahrain and a representative office in Sydney, Australia.

BoB, Union Bank of India and Indian Bank established IUB International

Finance, a licensed deposit taker, in Hong Kong. Each of the three banks took an

equal share.

1985: BoB (20%), Bank of India (20%), Bank of Baroda of India (20%)

and ZIMCO (Zambian government; 40%) established Indo-Zambia

Bank (Lusaka). BoB also opened an Offshore Banking Unit (OBU) in

Bahrain.

1988: BoB acquired Traders Bank, which had a branch network in Delhi.

1990s

1990: BoB opened an OBU in Mauritius, but closed its representative

office in Sydney.

1991: BoB took over the London branches of Union Bank of

India and Punjab & Sind Bank (P&S). P&S’s branch had been established

before 1970 and Union Bank’s after 1980. The Reserve Bank of

India ordered the takeover of the two following the banks' involvement in

the Sethia fraud in 1987 and subsequent losses.

Page 7

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

1992 BoB incorporated its operations in Kenya into a local subsidiary with

a small tranche of shares quoted on the Nairobi Stock Exchange.

1993: BoB closed its OBU in Bahrain.

1996: BoB Bank entered the capital market in December with an Initial

Public Offering (IPO). The Government of India is still the largest

shareholder, owning 66% of the bank's equity.

1997: BoB opened a branch in Durban.

1998: BoB bought out its partners in IUB International Finance in Hong

Kong. Apparently this was a response to regulatory changes following

Hong Kong’s reversion to the People’s Republic of China. The now

wholly owned subsidiary became Bank of Baroda (Hong Kong), a

restricted license bank. BoB also acquired Punjab Cooperative Bank in a

rescue. BoB also incorporate wholly owned subsidiary BOB Capital

Markets Ltd.for Broking Business.

1999: BoB merged in Bareilly Corporation Bank in another rescue. At the

time, Bareilly had 64 branches, including four in Delhi. In Guyana, BoB

incorporated its branch as a subsidiary, Bank of Baroda Guyana. BoB

added a branch in Mauritius, but closed its Harrow Branch in London.

2000s

2000: BoB established Bank of Baroda (Botswana).

2002: BoB acquired Benares State Bank (BSB) at the Reserve Bank of

India’s request. BSB was established in 1946 but traced its origins back to

1871 and its function as the treasury office of the Benares state. In 1964,

BSB had acquired Bareilly Bank (est. 1934), with seven branches; it also

had taken over Lucknow Bank in 1968. The acquisition of BSB brought

BOB 105 new branches.

2002: Bank of Baroda (Uganda) was listed on the Uganda Securities

Exchange (USE).

Page 8

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

2003: BoB opened an OBU in Mumbai.

2004: BoB acquired the failed Gujarat Local Area Bank, and returned

to Tanzania by establishing a subsidiary in Dar-es-Salaam. BoB also

opened a representative office each in Kuala Lumpur,Malaysia,

and Guangdong, China.

2005: BoB built a Global Data Centre (DC) in Mumbai for running its

centralized banking solution (CBS) and other applications in more than

1,900 branches across India and 20 other counties where the bank

operates. BoB also opened a representative office in Thailand.

2006: BoB established an Offshrore Banking Unit (OBU) in Singapore.

2007: In its centenary year, BoB’s total business crossed 2.09 lakh crores,

its branches crossed 1000, and its global customer base 29 million people.

2008: BoB opened a branch in Guangzhou, China (02/08/2008) and in

Kenton, Harrow United Kingdom. BoB opened a joint venture life

insurance company with Andhra Bank and Legal and General (UK)

called IndiaFirst Life Insurance Company

2010s

2010: Malaysia awarded a commercial banking license to a locally

incorporated bank to be jointly owned by Bank of Baroda, Indian

Overseas Bank and Andhra Bank. The new bank, India BIA Bank

(Malaysia), will reside in Kuala Lumpur, which has a large population of

Indians. Andhra Bank will hold a 25% stake in the joint-venture, BoB will

own 40% and IOB the remaining 35%.

BoB opened a branch in New Zealand

2.3 BOARD OF DIRECTORS:

1. Shri. M. D. Mallya

Chairman & Managing Director

2. Shri Rajiv Kumar Bakshi

Executive Director

Page 9

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

3. Shri N S Srinath

Executive Director

4. Shri Alok Nigam

Director

5. Shri Sudarshan Sen

Director

6. Shri Ajay Mathur

Director

7. Shri Vinil Kumar Saxena

Director

8. Shri V. B. Chavan

Director

9. Dr. Masarrat Shahid

Director

10. Shri Satya Dev Tripathi

Director

11. Shri Maulin Vaishnav

Director

12. Shri Surendra Singh Bhandari

Director

Page 10

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

13. Shri Rajib Sekhar Sahoo

Director

2.3) TYPE OF PRODUCTS:

Product Profile

Followings are the main products of The Bank of Baroda. Deposits Gen-next Loans Credit Cards Debit Cards Services Lockers

(1)Deposits:

Bank of Baroda offers various deposit plans that you can choose from

depending on the term period, nature of deposit and its unique saving and

withdrawal features. A part from competitive interest rates and convenient

withdrawal options, our deposit plans offer other features such as overdraft

facility, outstation cheque collections, safe deposit lockers, ATM's etc. Fixed

deposits are categorized into deposits with a term period of less than 12 months,

more than 12 months and recurring deposits. These deposit plans offer convenient

solutions to both working individuals as well as senior citizens. Current and

saving deposits are ideal for individuals who wish to take advantage of multiple

benefits within the same plan and even be eligible to opt for overdrafts.

(2)Gen-next:

2.1: Gen-Next Junior (Saving Account)

Product Nature:

This is a Special kind of Savings Bank Deposit product for children to be

made available in Gen-Next Pune branch.

Target Group:

Page 11

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Children’s upto18 years of age.

Minimum Amount & Balance:

QAB: Rs 500/-

Charges for non-maintenance of QAB is Rs 50/ per quarter only.

Maximum Amount:

In case of joint accounts with parent and minors (with sole

account) above 14 years, there is no ceiling on the maximum

amount.

An account in the sole name of minor above 10 years and below 14

years, maximum limit is Rs 1 lakh.

Single / Joint Accounts:

In case of minor below 10 years the account shall be opened jointly

with parents / guardian.

Minors above 10 years (below 18 years) can open the account in

their sole name subject to :

Minor is able to read and write any of the recognized languages,

and

capable in the opinion of the Bank officials of understanding the

what he / she is doing and SB account rules and regulations

2.2: Gen-Next Lifestyle

Type of Facility:

Term Loan (Combo Pack) Purpose :

Purchase of Home Furnishings / Consumer Durable goods

(includes color T.V., video camera / refrigerator / washing machine

/ music system / air-conditioners / cooking system etc).

Purchase of vehicle i.e. two-wheeler / four-wheeler.

Page 12

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Purchase of Laptop / PC.

Purchase of any new electronic gadgets like Mobile, i-Pod, Handy

cam etc.

Target Group:

Working executives/ professionals.

Eligibility:

Should be an Indian National

Permanent Employees of State / Central Government, Public Sector

Undertakings, Semi government Organization, State /Central Govt.

Corporations, Urban Development Authorities, Educational

Institutions, Universities. Regular Employees of MNCs, Public Ltd

Companies with minimum two years experience out of which

minimum one year service with the present organization.

Employees of Private Limited Companies, Regional head willpermit

on case-to-case basis.

Present gross annual emoluments / income of the applicant shouldnot be less than

Rs. 2.50 lacks.

Age:

Minimum – 21 years

Maximum – 45 years

Maximum Loan Amount:

Subject to maximum of:

Furniture & Fixture / New Consumer Durables : Rs. 2 lacks

New Vehicle (Four Wheeler) : Rs. 6 lacks (Two Wheeler) : Rs. 1lac

Old Four Wheeler (Not more than 3 years old) : Rs. 4 lacks

New modern gadget/s: Rs. 1 lack

Aggregate loan amount should not be more than Rs. 8.00 lacks.

Subject to:

24 times gross Monthly income.

Page 13

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Total deductions including EMI of proposed loan should notexceed 60%

of the gross income.

Margin:

Furniture & Fixture / New Consumer Durables : 20%

New Vehicle (Two wheeler / Four wheeler) : 15%

Old Vehicle (Four wheeler only) : 40%

New Modern Gadgets (Including Laptop / PC) : 20%

2.3 Gen-Next Power (OD Facility):

Product Nature:

This is a special Savings Deposit product having an in built feature

of overdraft facility to be available at Gen-Next Pune branch. Target Group The

product is targeted to working executives and other working professionals. Our

Bank’s Staff members are not eligible to avail the product.

Minimum Amount & Balance

There is no minimum balance requirement in the account and as such no

service charges shall be levied towards this. Maximum Amount There shall be no

ceiling on the amount to be deposited and credit balance in the account.

Eligibility Criteria:

Permanent Employees of State / Central Government, Public Sector

Undertakings, Semi government Organization, State /Central Govt.

Corporations, Urban Development Authorities, Educational Institutions,

Universities. Regular Employees of MNCs, Public Ltd Companies with

minimum two years experience out of which minimum one year service

with the present organization.

Employees of Private Limited Companies, Regional head will permit on

case-to-case basis.

Page 14

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Minimum age of 21 years.

Minimum take home Salary should not be less than Rs.10,000/-.

Maintaining satisfactorily conducted salary account with theBank at least

for three months.

Special Feature:

The branch SHALL offer Overdraft facility (Clean/unsecured) to

employees who fulfill the eligibility criteria mentioned above to meetout their

regular short-term personal / family needs.

Overdraft Facility:

Maximum Age: 45 years. (This product is meant for youth)

Amount: 5 times of net take home monthly salary subject to:

Min Rs. 50,000/-

Max Rs. 2.00 lacs, subject to condition:

Risk Rating Category “A” & “B” Rs. 2.00 lack

Category “C” Rs. 1.00 lack

Category “D” NIL.

For credit rating purpose, model meant for personal loan will be taken into

consideration.

PROCESSING & DOCUMENTATION CHARGES:

0.50% of limit sanctioned / reviewed subject to minimum of Rs. 250/-+ service

tax as applicable.

Security Documents:

D.P. Note.

Letter of continuing security.

A stamped undertaking from the employee authorizing the employer to

remit the salary every month to the bank for credit of specified SB /

Current Account during the currency of the OD facility and also to deduct

Page 15

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

from the retirement / terminal benefits, the outstanding overdraft amount

with the interest in case of retirement / resignation / cessation of

employment for any reason. A copy of the undertaking duly

acknowledged by the employer has to be kept on branch.

Third party guarantees having adequate net worth. Cross guarantee may be

accepted.

Rate of Interest:

1.5% above BPLR i.e. 14% p.a. with monthly rests. A Minimum interest

of Rs. 10/- shall be charged during a month if OD is availed. Period: 12 months,

subject to annual review.

Other Conditions:

The account is to be brought into credit once in a year.

Interest Rate on Credit Balance in The A/C:

Interest shall be payable on credit balance in the account as per savings

bank account rules viz. relating to periodicity, rate andsystem of application of

interest, computation of eligible balances etc.

2.4: Gen Next Suvidha:

Product Nature:

This is a Recurring Deposit product enabling the customer to makeregular

savings on monthly basis and earns higher interest.

Customer Segment:

Individuals in their single / joint names.

Minors of age 10 years and above jointly with their parents /natural

guardians.

Minors below 10 years age through their parents.

Minimum / Maximum Amount:

Page 16

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

There is no minimum balance requirement in the account and assuch no

service charges shall be levied towards this.

Maximum Amount:

“Gen-next Suvidha” Account can be opened with monthly installments of

Rs.100/- or above & in multiples thereof with a maximum of Rs.10, 000/-

per month.

The number of installments can range from 12 to 36 months (In multiples

of 3 months).

The depositor shall, at the time of opening the account, stipulate the

amount of core monthly installment and the number of installments

payable by him which shall not subsequently alter.

The depositor is given an option to deposit higher monthly installment in

the account as and when available and the maximum amount should not

exceed Rs. 10,000/- per month. However, monthly installments paid

during the time gap of less than 24/12 months (depending upon the period

chosen) at the ending stage of the account’s tenure, shall not exceed in any

month three times the core monthly installment or Rs. 10,000/-whichever

is less.

Rate of Interest:

As decided by bank from time to time for Term Deposits of same tenure.

Loan against Deposit:

Loan can be considered against the deposit in the account in

accordance to normal guidelines for advances against Recurring

Deposit.

Interest shall be charged on such loan at the rates advised from

time to time on Loan against Bank’s Own Deposits.

Page 17

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

CHAPTER3

RESEARCH METHODOLOGY

3.1 RESEARCH METHODOLOGY:-

. Research Methodology is process of systematic gathering, recording

and analyzing of data collected by various techniques to access the respond and

accordingly prepare a report based on impact of promotional activity. It is careful

investigation or inquiry especially through search of knowledge through objective

and systematic method of finding solution of a problem. Thus in short the term

research refers to formulating a hypothesis.

Page 18

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

The present study is based on secondary data for the facts and figures

and primary data as personal interview and questionnaire. The information is

taken from the News paper, books and magazines.

Research problem is one which require a researcher to find out the best

solution for the best solution for the given problem that is to find out by which

course of action the objective can be attained optimally in context of given

environment.

3.2 OBJECTIVE OF STUDY:-

To study the different types of loans provided by Bank of Baroda and its

eligibility criteria and conditions.

To study the benefits of these loans scheme to bank.

To study the benefits of different loans to customer of bank.

3.3 RESEARCH DESIGN:-

A research design case the arrangement of condition for collection and

analysis of data in manner that aims to combine relevance to research purpose

with economic procedure. The most important research process is deciding on

research design.

3.4 EXPLORATORY RESEARCH:-

Exploratory research is conducted when the researcher does not know how

and why a certain phenomenon occurs. To understand this phenomenon, several

researchers have conducted focus group discussion to identify these quality

parameters.

Since the prime goal of an exploratory research is to know the unknown,

this research is unstructured. Experts and even search and even for printed or

published information are some common techniques.

3.5 DATA SOURCE:-

Page 19

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

After identifying and defining the research problem and deterring

specific information required solving the problem, the researcher’s task is to look

for the type source of data, which may yield the desired result. Research

methodology carried for this study can be two types.

1) PRIMARY DATA:-

a) Primary data collected by the researcher through interview of

bank manager and banker.

b) By structured questionnaires customer of the bank.

2) SECONDARY DATA:-

Secondary data collected by researcher through bank circular, bank

website and RBI guide lines published by RBI.

SAMLING:-

1) UNIVERS: - All person who have taken loans from bank.

2) SIZE: - 100 people who taken different loans.

3) TECHNIQUE: - No probability convenient sampling.

3.6 LIMITATIONS:-

1) The topic is based on purely academic purpose.

2) The topic is based the study of Bank of Baroda only.

3) The study is limited to Khamgaon city only.

Page 20

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

CHAPTER NO: 4

PRODUCT DETAILS

4.1 TYPE OF LAONS:

Following are the different types of loans provided by the bank.

a) Home Loan:-

o Eligibility

Existing Borrowers under Direct Housing Finance Scheme having

completed minimum 3 (three) years of repayment schedule without any

default.

Page 21

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

In case Housing loan is in Joint Name, Both the Joint borrowers should

join as borrower for the loan or consent / no objection for extending

charge of house property created out of Housing loan should be obtained.

o Quantum of loan

Maximum of Rs.10.00 lakhs.

o Margin

25% on the Present Market value of the property for aggregate loan up to

Rs.30 lakhs including the proposed limit under this scheme.35% on the

Present Market value of the property for aggregate loan above Rs.30 lakhs

including the proposed limit under this scheme.

o Security

Extension of mortgage on the House property for which Housing Loan

was sanctioned.

o Repayment

The loan has to be repaid in 120 equal monthly installments.

o Rate of Interest & Processing Charges

Rate of Interest as applicable to Bank's Existing Housing Loan Scheme in

case of renovation.The rate of interest will be 1% more than the rate of

existing housing loan in case of refurbishment, buying of furniture,

television, home theater etc.

b) Education Loan:-

The Government of India, Ministry of Human Resource Development,

Department of Higher Education has formulated an Interest Subsidy

scheme on Educational Loans for the students of economically weaker

sections (EWS) for pursuing technical/professional courses in India.

Salient features of scheme are as under:

Scheme is applicable for the loan amount availed from April 01, 2009 to

March31, 2010(Academic Year 2009-10).

Page 22

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

For Loans sanctioned earlier to 1.04.2009, only amounts disbursed during

the above period are also eligible.

Applicable to students from EWS with a annual parental/family income

limit of Rs.4.50 lakhs or less and for studies in recognized technical and

professional courses in India after Class XII from institutes recognized by

UGC/AICTE.

Interest subsidy shall be available to the eligible students only once, either

for the first undergraduate degree course or the post graduate

degrees/diplomas. Interest subsidy shall, however, be admissible for

combined undergraduate and post graduate courses.

Entire repayment holiday period interest to be provided as interest

subsidy.

In case of discontinuance of the course midstream, due to expulsion on

disciplinary or academic ground, no interest subsidy to be paid.

Moratorium period: Course duration plus one year or six months after

loaner’s employment, whichever is earlier?

After the period of moratorium is over, the interest on the outstanding loan

amount shall be paid by the student.

Proof of income is required to be certified by Tehsildar or any other

authorities to be designated by the concerned State Government.

The eligible student has to execute an Agreement with the disbursing

Branch for receiving Interest Subsidy.

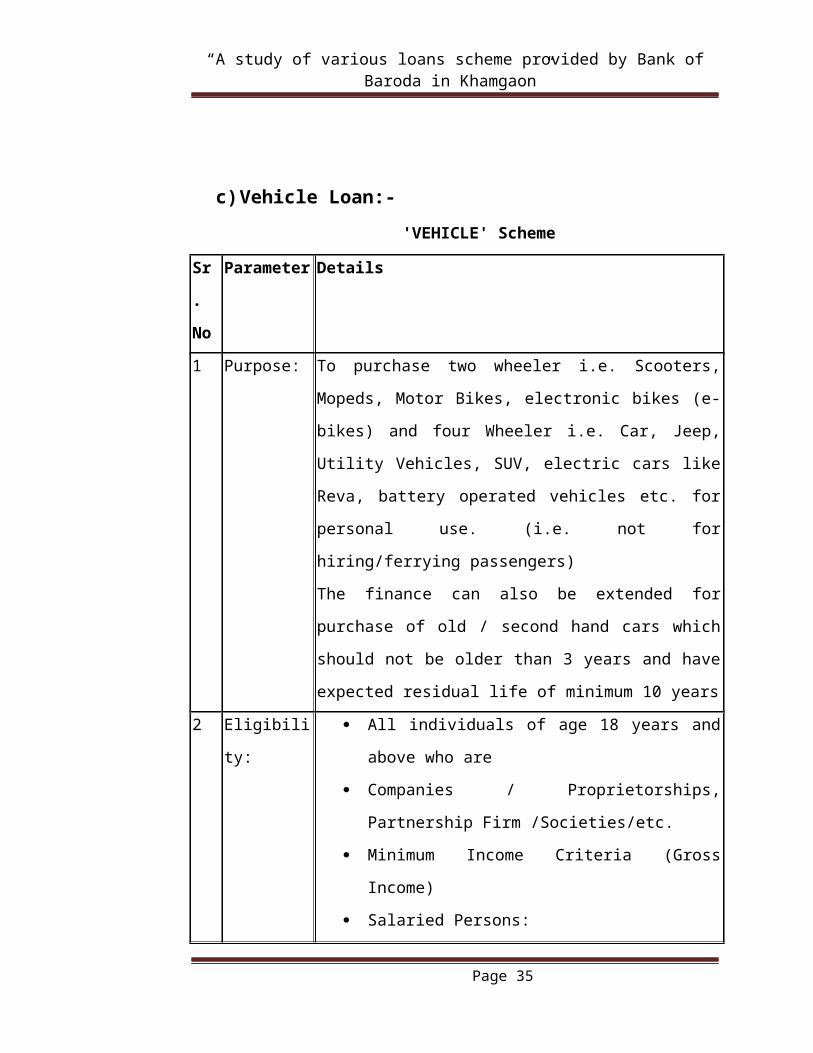

c) Vehicle Loan:-

'VEHICLE' Scheme

Sr.

No

Parameter Details

1 Purpose: To purchase two wheeler i.e. Scooters, Mopeds, Motor Bikes,

electronic bikes (e-bikes) and four Wheeler i.e. Car, Jeep,

Utility Vehicles, SUV, electric cars like Reva, battery operated

Page 23

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

vehicles etc. for personal use. (i.e. not for hiring/ferrying

passengers)

The finance can also be extended for purchase of old / second

hand cars which should not be older than 3 years and have

expected residual life of minimum 10 years

2 Eligibility: All individuals of age 18 years and above who are

Companies / Proprietorships, Partnership Firm

/Societies/etc.

Minimum Income Criteria (Gross Income)

Salaried Persons:

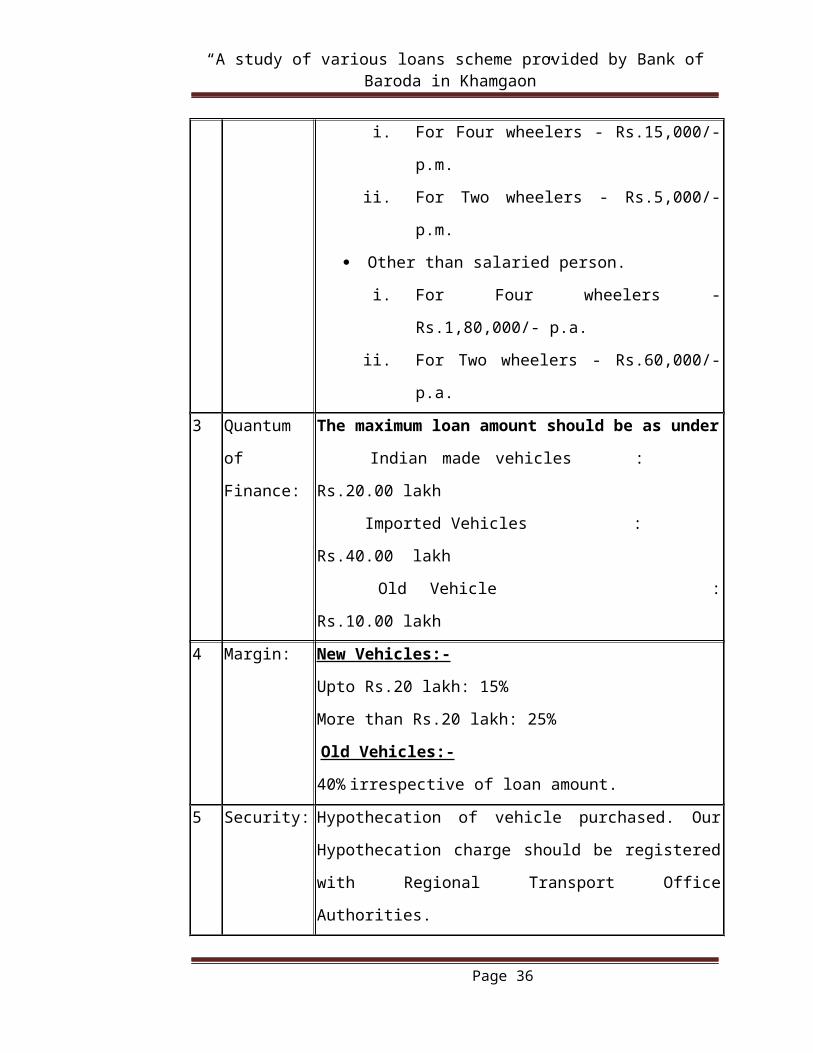

i. For Four wheelers - Rs.15,000/- p.m.

ii. For Two wheelers - Rs.5,000/- p.m.

Other than salaried person.

i. For Four wheelers - Rs.1,80,000/- p.a.

ii. For Two wheelers - Rs.60,000/- p.a.

3 Quantum of

Finance:

The maximum loan amount should be as under

Indian made vehicles : Rs.20.00 lakh

Imported Vehicles : Rs.40.00 lakh

Old Vehicle : Rs.10.00 lakh

4 Margin: New Vehicles:-

Upto Rs.20 lakh: 15%

More than Rs.20 lakh: 25%

Old Vehicles:-

40% irrespective of loan amount.

5 Security: Hypothecation of vehicle purchased. Our Hypothecation

charge should be registered with Regional Transport Office

Authorities.

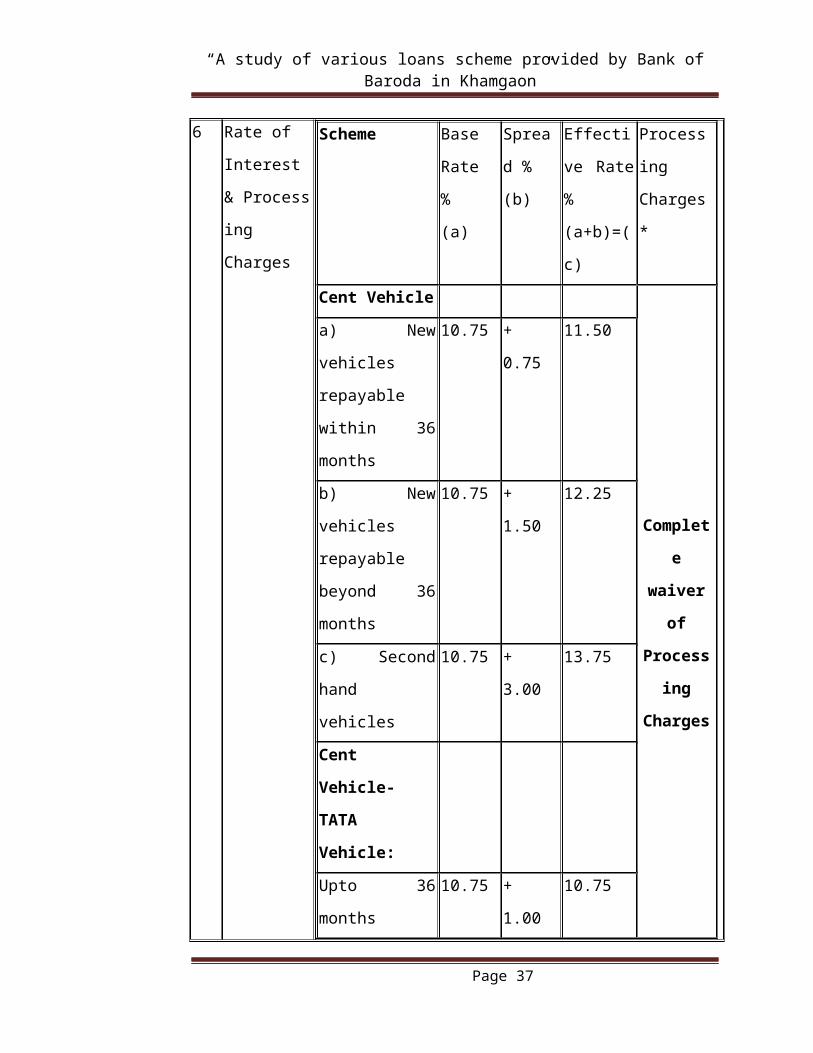

6 Rate of

Interest

& Processing

Charges

Scheme Base

Rate %

(a)

Spread

%

(b)

Effective

Rate %

(a+b)=(c)

Processing

Charges *

Cent Vehicle

Page 24

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Complete

waiver of

Processing

Charges

a) New vehicles

repayable within

36 months

10.75 + 0.75 11.50

b) New vehicles

repayable beyond

36 months

10.75 + 1.50 12.25

c) Second hand

vehicles

10.75 + 3.00 13.75

Cent Vehicle-

TATA Vehicle:

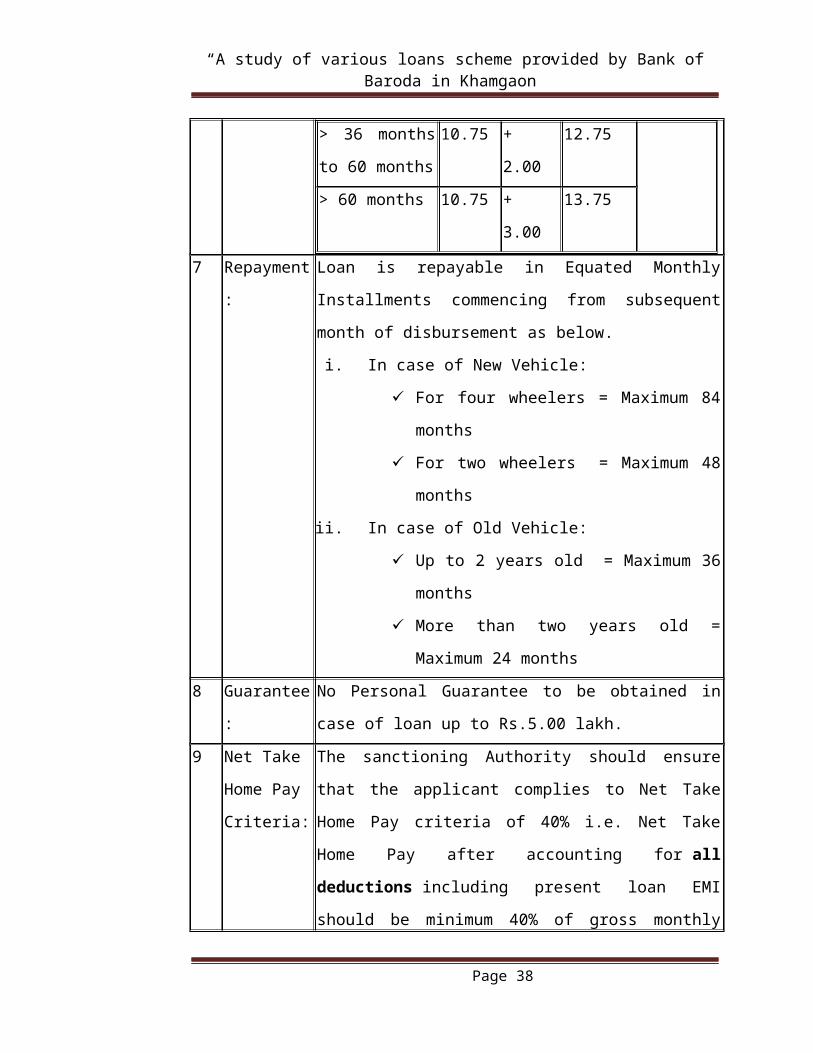

Upto 36 months 10.75 + 1.00 10.75

> 36 months to 60

months

10.75 + 2.00 12.75

> 60 months 10.75 + 3.00 13.75

7 Repayment: Loan is repayable in Equated Monthly Installments

commencing from subsequent month of disbursement as

below.

i. In case of New Vehicle:

For four wheelers = Maximum 84 months

For two wheelers = Maximum 48 months

ii. In case of Old Vehicle:

Up to 2 years old = Maximum 36 months

More than two years old = Maximum 24

months

8 Guarantee: No Personal Guarantee to be obtained in case of loan up to

Rs.5.00 lakh.

9 Net Take

Home Pay

Criteria:

The sanctioning Authority should ensure that the applicant

complies to Net Take Home Pay criteria of 40% i.e. Net Take

Home Pay after accounting for all deductions including

Page 25

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

present loan EMI should be minimum 40% of gross monthly

salary.

10 Prepayment

Charges

No prepayment penalty is levied if the loan is adjusted by the

borrower from his own sources. However, if loan is taken over

by other Banks/Financial Institutes, Prepayment Penalty is

charged @ 1.00 % on outstanding balance on the date of such

take over.

d) Personal Loan:-

Personal Loan Scheme (Non corporate)

1 Purpose Personal / Domestic

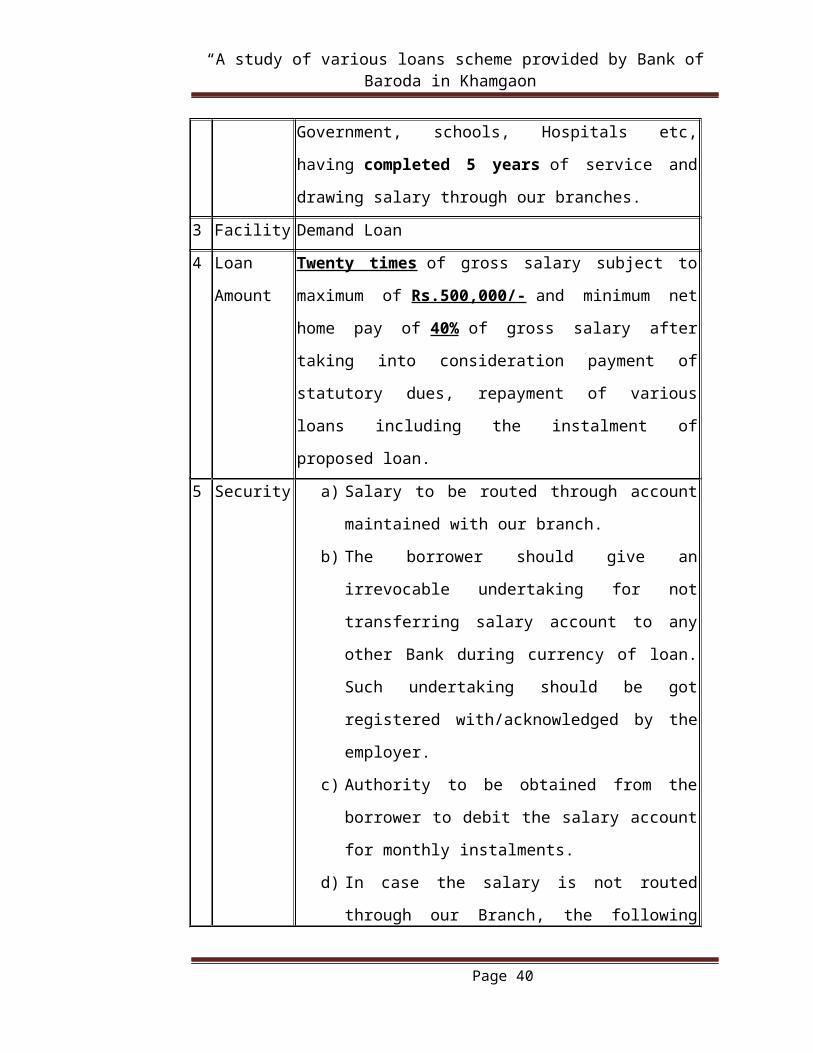

2 Eligibility Permanent Employees of Railways, Government institutions

central and State Government, schools, Hospitals etc,

having completed 5 years of service and drawing salary

through our branches.

3 Facility Demand Loan

4 Loan

Amount

Twenty times of gross salary subject to maximum

of Rs.500,000/- and minimum net home pay of 40% of gross

salary after taking into consideration payment of statutory

Page 26

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

dues, repayment of various loans including the instalment of

proposed loan.

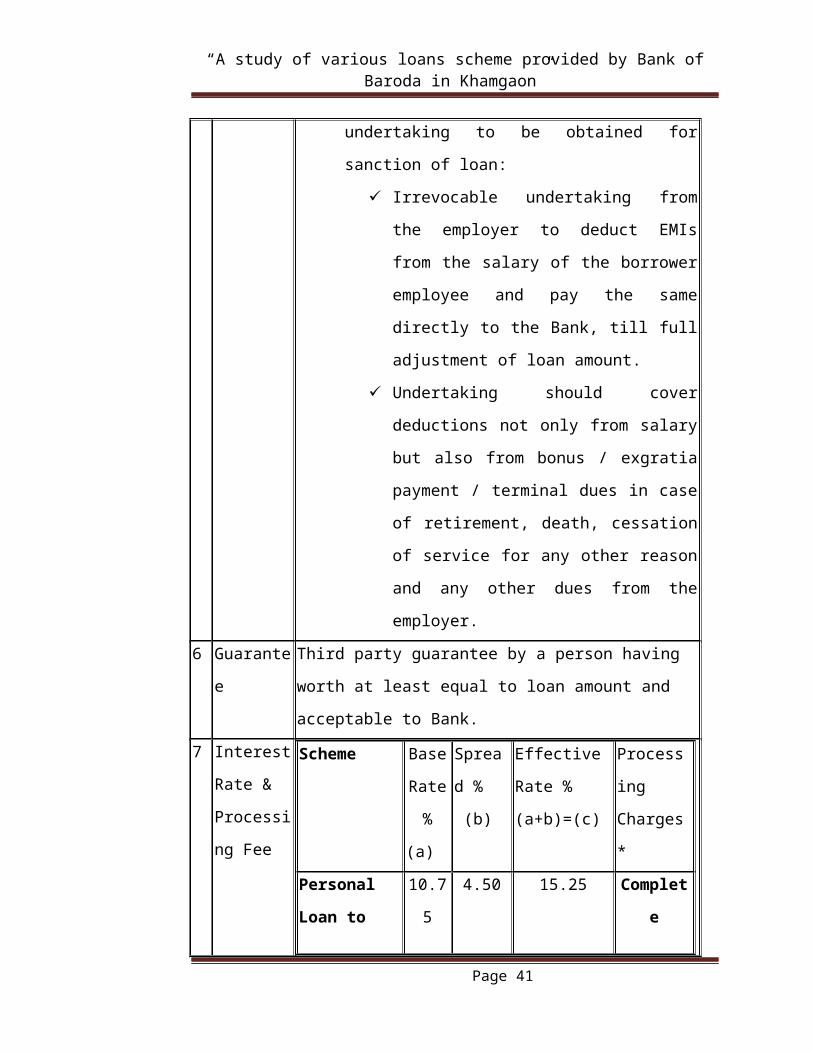

5 Security a) Salary to be routed through account maintained with

our branch.

b) The borrower should give an irrevocable undertaking

for not transferring salary account to any other Bank

during currency of loan. Such undertaking should be

got registered with/acknowledged by the employer.

c) Authority to be obtained from the borrower to debit

the salary account for monthly instalments.

d) In case the salary is not routed through our Branch, the

following undertaking to be obtained for sanction of

loan:

Irrevocable undertaking from the employer to

deduct EMIs from the salary of the borrower

employee and pay the same directly to the

Bank, till full adjustment of loan amount.

Undertaking should cover deductions not only

from salary but also from bonus / exgratia

payment / terminal dues in case of retirement,

death, cessation of service for any other reason

and any other dues from the employer.

6 Guarantee Third party guarantee by a person having worth at least equal

to loan amount and acceptable to Bank.

7 Interest

Rate &

Processing

Fee

Scheme Base

Rate

%

(a)

Spread

%

(b)

Effective Rate

%

(a+b)=(c)

Processing

Charges *

Page 27

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Personal Loan

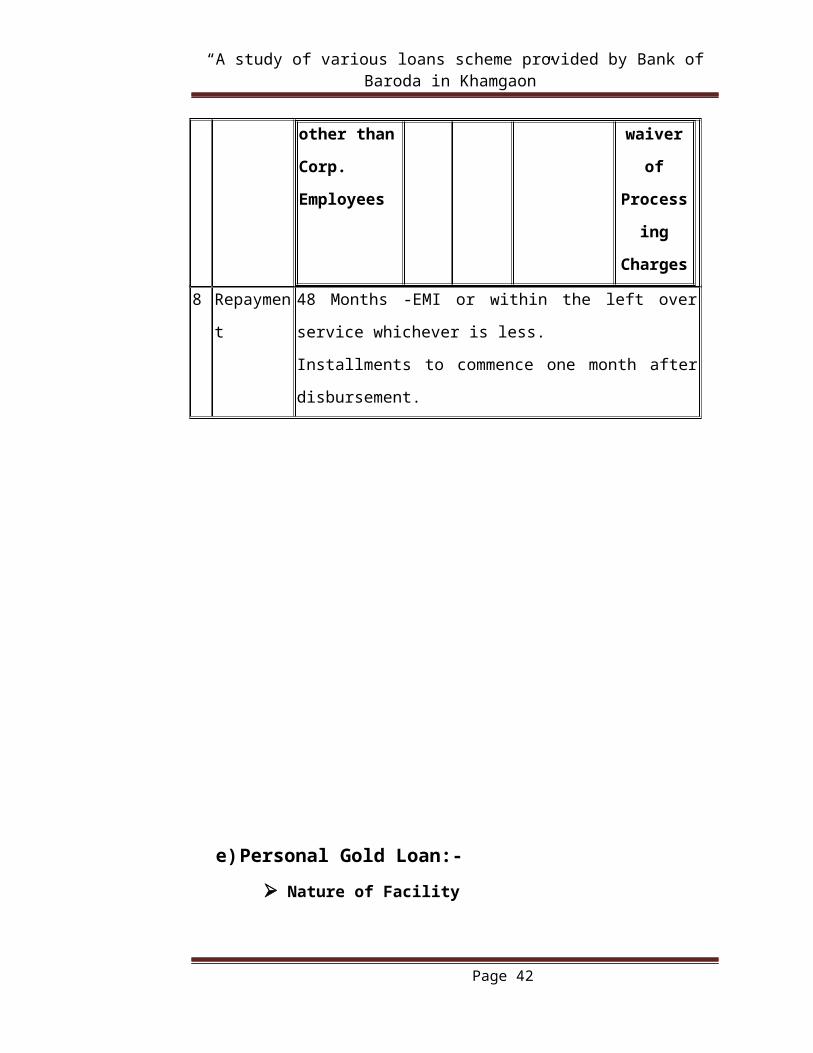

to other than

Corp.

Employees

10.75 4.50 15.25 Complete

waiver of

Processing

Charges

8 Repayment 48 Months -EMI or within the left over service whichever is

less.

Installments to commence one month after disbursement.

e) Personal Gold Loan:-

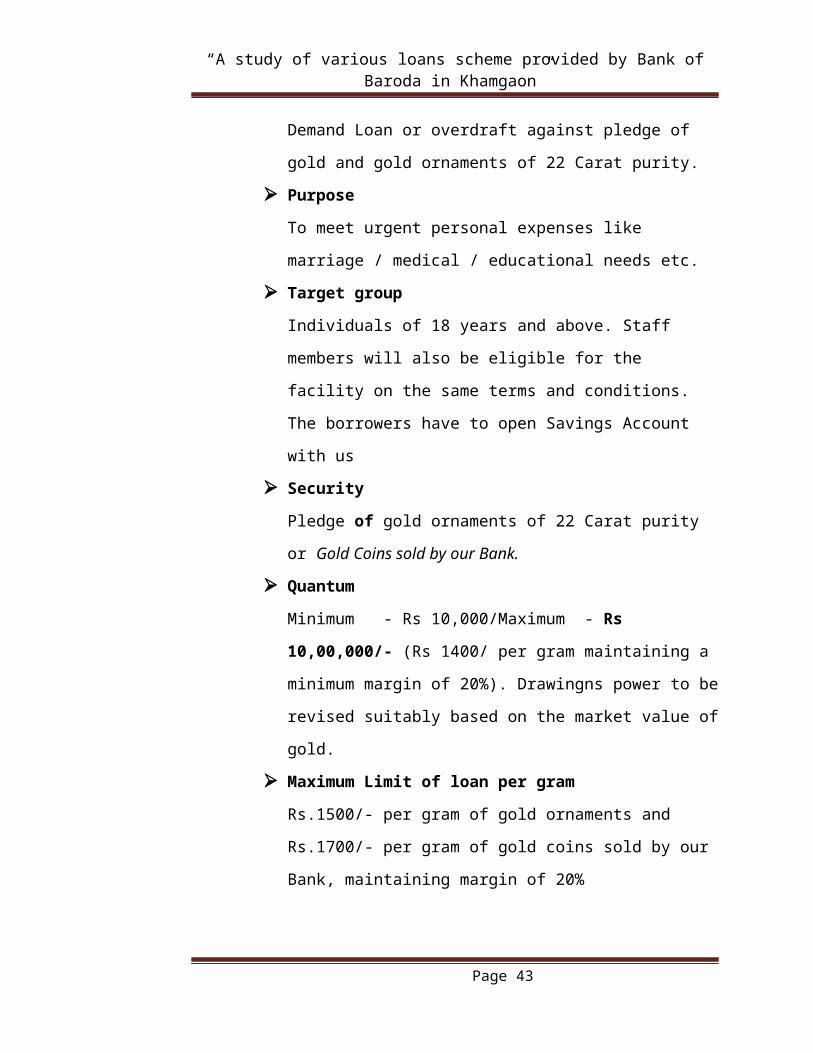

Nature of Facility

Demand Loan or overdraft against pledge of gold and gold

ornaments of 22 Carat purity.

Purpose

To meet urgent personal expenses like marriage / medical /

educational needs etc.

Target group

Page 28

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Individuals of 18 years and above. Staff members will also be

eligible for the facility on the same terms and conditions. The

borrowers have to open Savings Account with us

Security

Pledge of gold ornaments of 22 Carat purity or Gold Coins sold by

our Bank.

Quantum

Minimum - Rs 10,000/Maximum - Rs 10,00,000/- (Rs 1400/ per

gram maintaining a minimum margin of 20%). Drawingns power

to be revised suitably based on the market value of gold.

Maximum Limit of loan per gram

Rs.1500/- per gram of gold ornaments and Rs.1700/- per gram of

gold coins sold by our Bank, maintaining margin of 20%

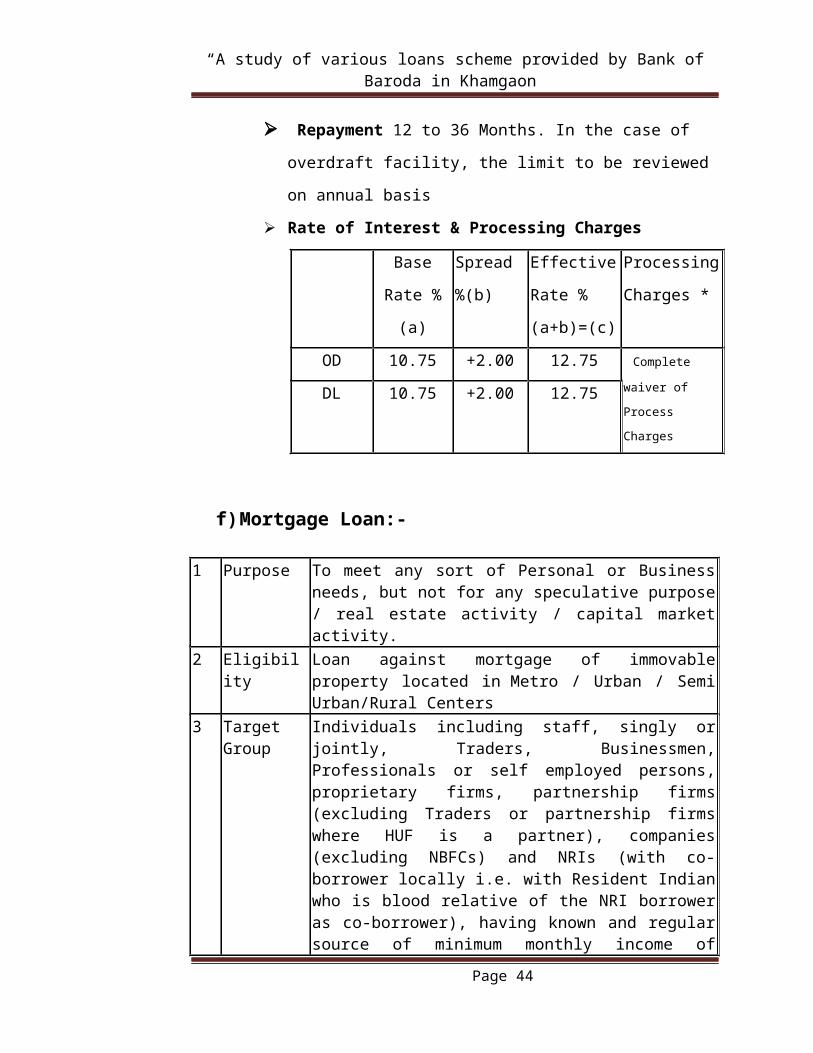

Repayment 12 to 36 Months. In the case of overdraft facility, the

limit to be reviewed on annual basis

Rate of Interest & Processing Charges

Base Rate

% (a)

Spread %

(b)

Effective

Rate %

(a+b)=(c)

Processing

Charges *

OD 10.75 +2.00 12.75 Complete waiver

of Process ChargesDL 10.75 +2.00 12.75

f) Mortgage Loan:-

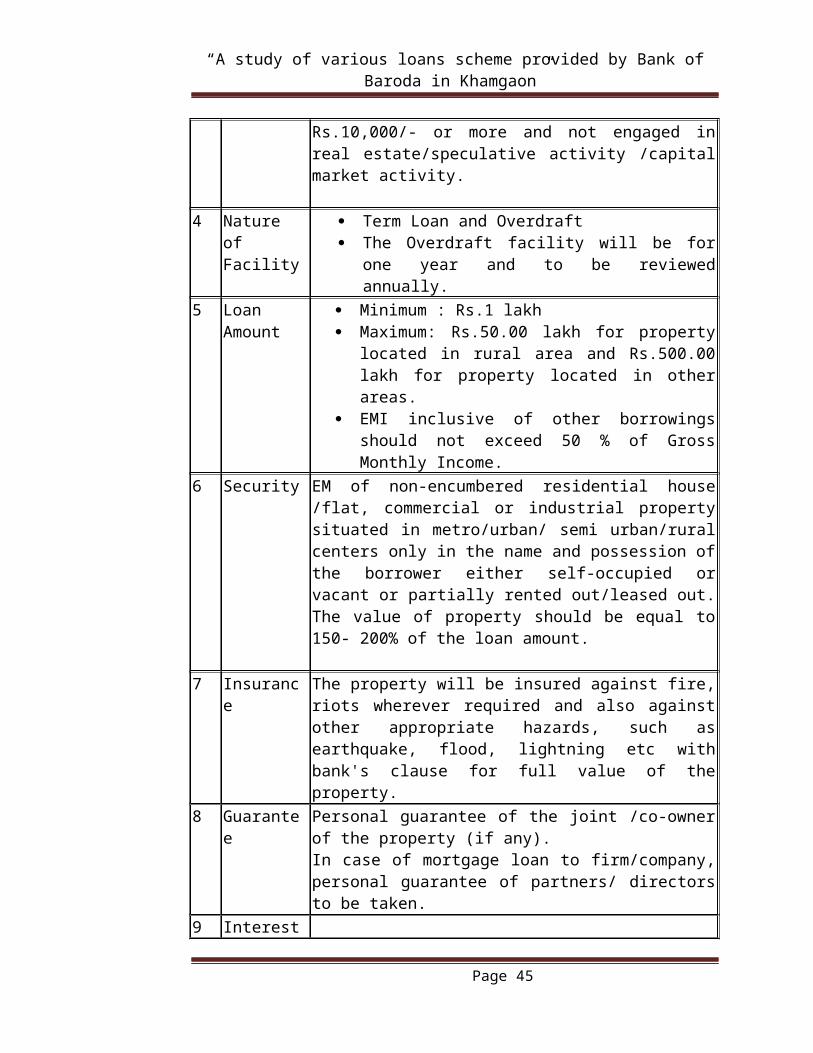

1 Purpose To meet any sort of Personal or Business needs, but not for any speculative purpose / real estate activity / capital market activity.

2 Eligibility Loan against mortgage of immovable property located in Metro / Urban / Semi Urban/Rural Centers

3 Target Group

Individuals including staff, singly or jointly, Traders, Businessmen, Professionals or self employed persons, proprietary firms, partnership firms (excluding Traders or partnership firms where HUF is a partner), companies

Page 29

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

(excluding NBFCs) and NRIs (with co-borrower locally i.e. with Resident Indian who is blood relative of the NRI borrower as co-borrower), having known and regular source of minimum monthly income of Rs.10,000/- or more and not engaged in real estate/speculative activity /capital market activity.

4 Nature of Facility

Term Loan and Overdraft The Overdraft facility will be for one year and to be

reviewed annually.5 Loan

Amount Minimum : Rs.1 lakh Maximum: Rs.50.00 lakh for property located in rural

area and Rs.500.00 lakh for property located in other areas.

EMI inclusive of other borrowings should not exceed 50 % of Gross Monthly Income.

6 Security EM of non-encumbered residential house /flat, commercial or industrial property situated in metro/urban/ semi urban/rural centers only in the name and possession of the borrower either self-occupied or vacant or partially rented out/leased out. The value of property should be equal to 150- 200% of the loan amount.

7 Insurance The property will be insured against fire, riots wherever required and also against other appropriate hazards, such as earthquake, flood, lightning etc with bank's clause for full value of the property.

8 Guarantee Personal guarantee of the joint /co-owner of the property (if any).In case of mortgage loan to firm/company, personal guarantee of partners/ directors to be taken.

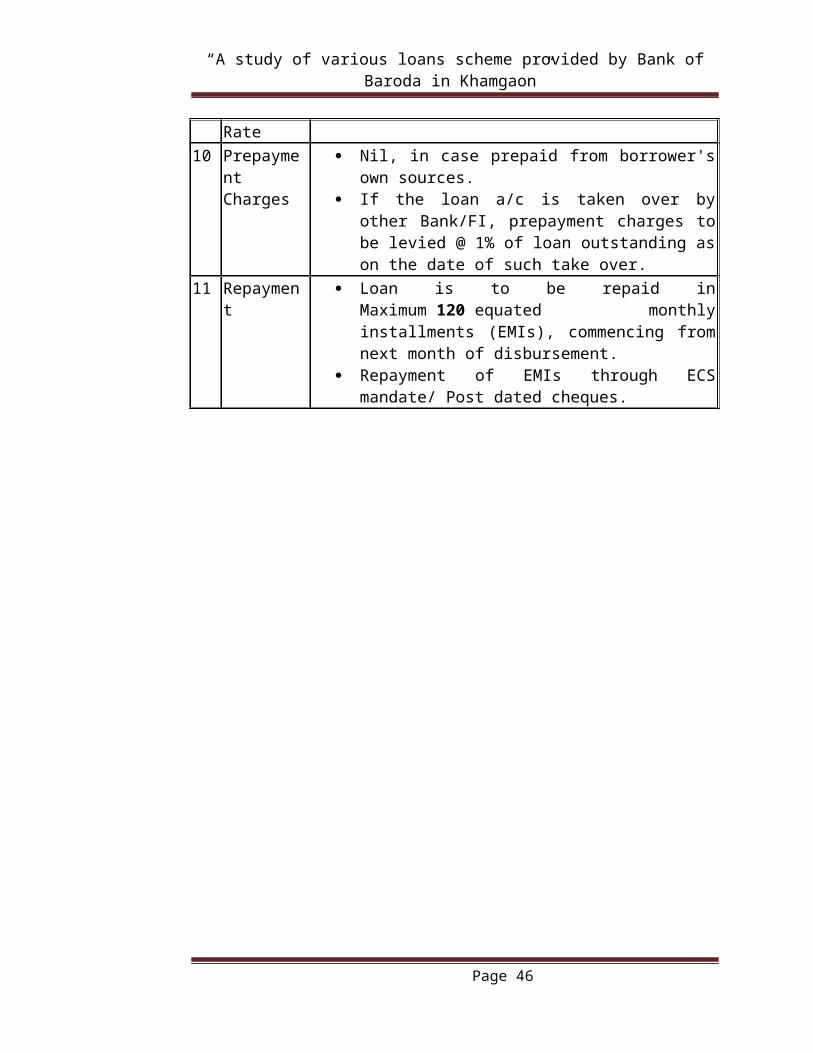

9 Interest Rate10 Prepayment

Charges Nil, in case prepaid from borrower's own sources. If the loan a/c is taken over by other Bank/FI,

prepayment charges to be levied @ 1% of loan outstanding as on the date of such take over.

11 Repayment Loan is to be repaid in Maximum 120 equated monthly installments (EMIs), commencing from next month of disbursement.

Repayment of EMIs through ECS mandate/ Post dated cheques.

Page 30

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

CHAPTER NO: 5

DATA INTERPRETATION

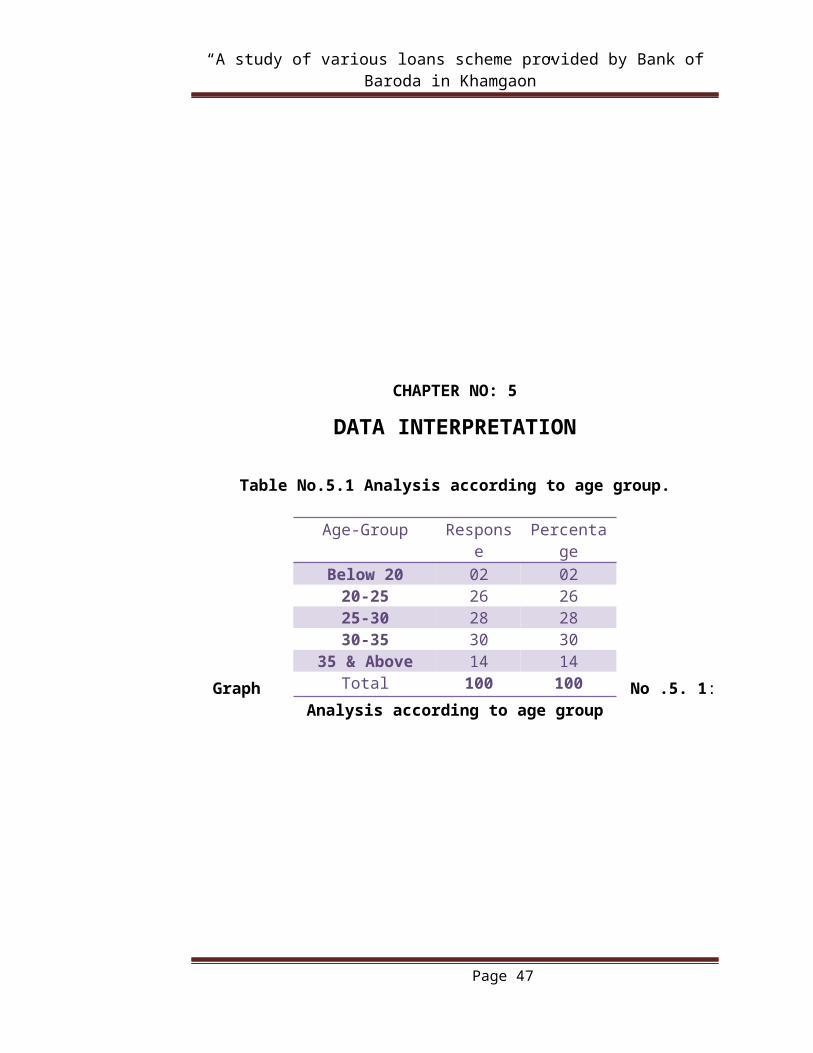

Table No.5.1 Analysis according to age group.

Page 31

Age-Group Response PercentageBelow 20 02 02

20-25 26 2625-30 28 2830-35 30 30

35 & Above 14 14Total 100 100

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Graph No .5. 1: Analysis according to age group

Below 20 20-25 25-30 30-35 35 & Above

0%

5%

10%

15%

20%

25%

30%

2%

26%28%

30%

14%

Percentage

Percentage

(Source: Primary data)

Interpretation:-

From the above data, it is clear that major group of age is 30-35 (30%), Second major group is 25-30 (28%), major group 20-25 (26%) and minor group is 35 & above (14%),below (2%), and the negligible response is from below 20 group.

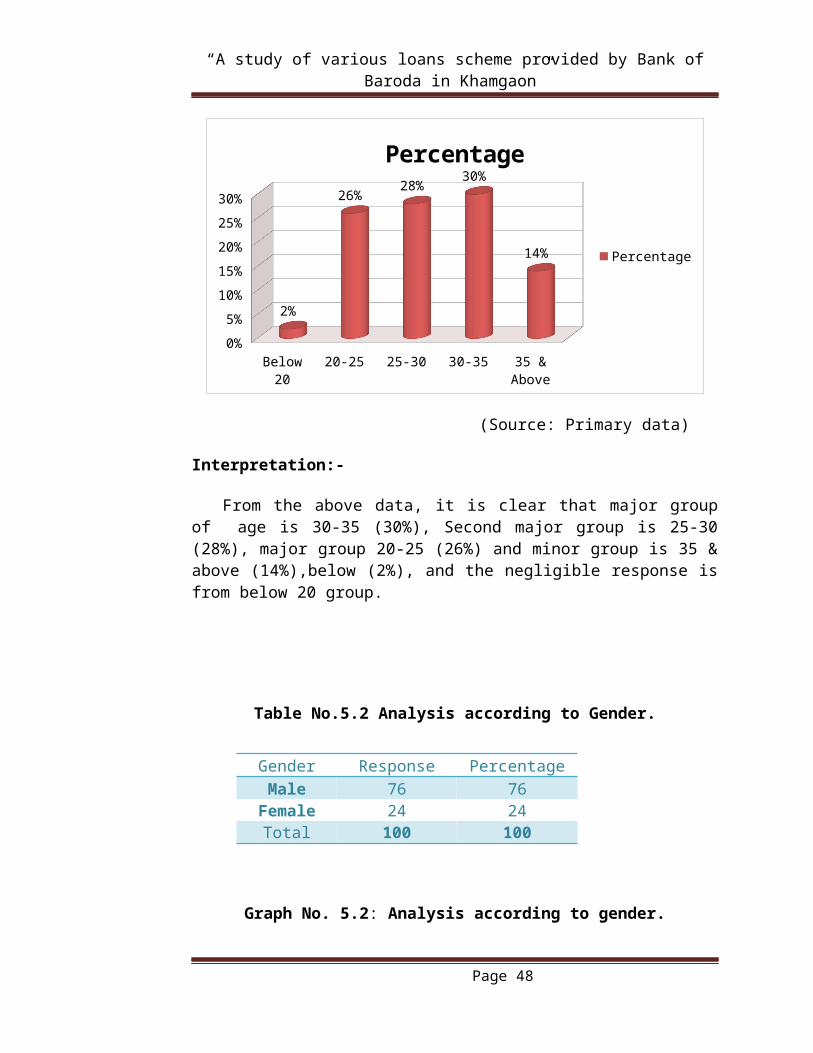

Table No.5.2 Analysis according to Gender.

Graph No. 5.2: Analysis according to gender.

Page 32

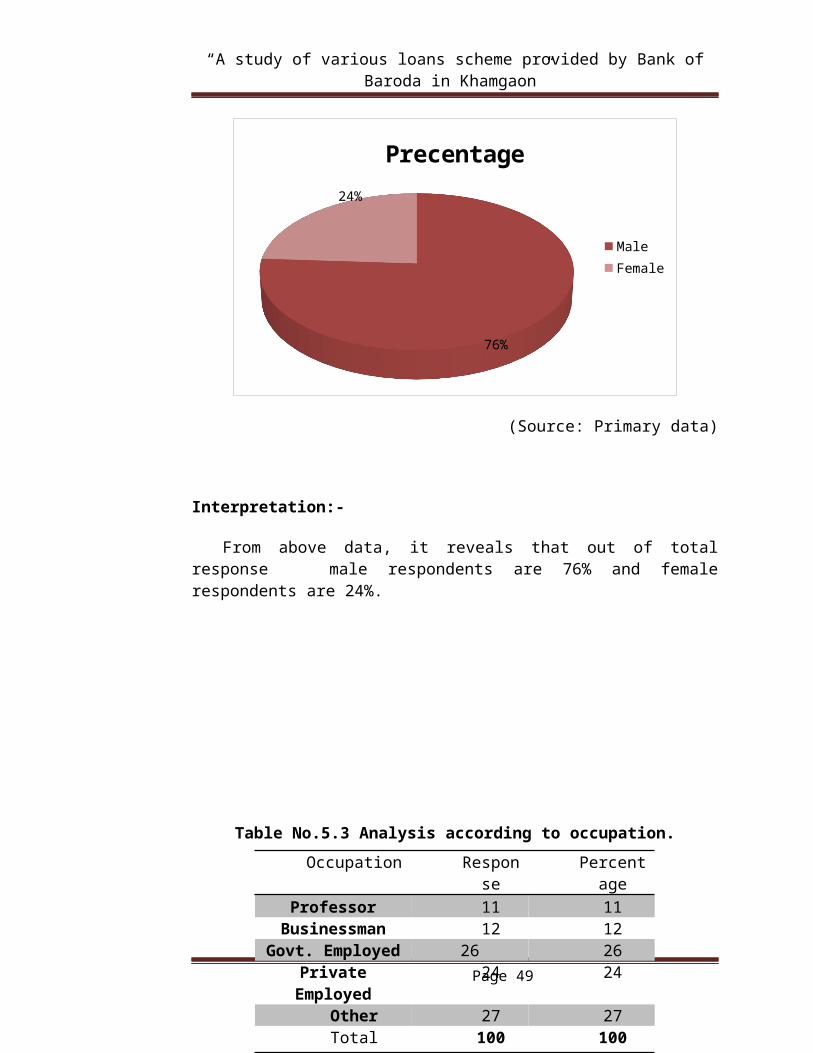

Gender Response PercentageMale 76 76

Female 24 24Total 100 100

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

76%

24%

Precentage

MaleFemale

(Source: Primary data)

Interpretation:-

From above data, it reveals that out of total response male respondents are 76% and female respondents are 24%.

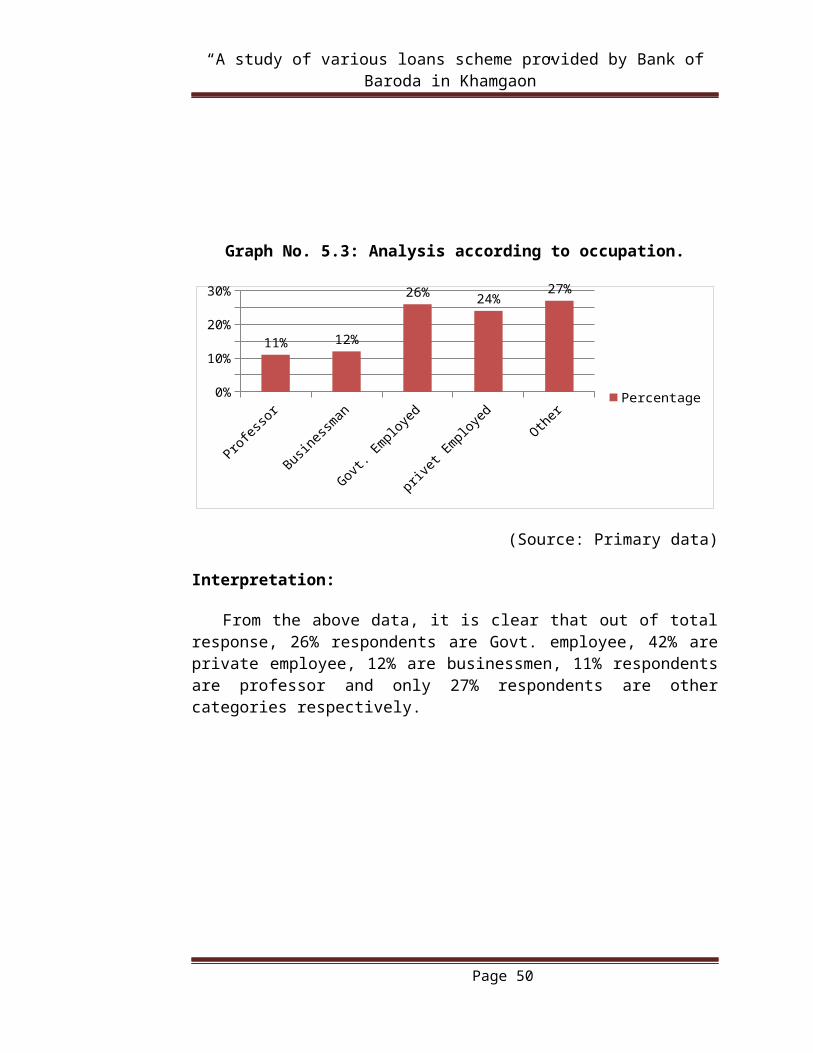

Table No.5.3 Analysis according to occupation.

Page 33

Occupation Response

Percentage

Professor 11 11Businessman 12 12

Govt. Employed 26 26Private Employed 24 24

Other 27 27Total 100 100

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Graph No. 5.3: Analysis according to occupation.

Profes

sor

Business

man

Govt. Em

ployed

privet

Employe

dOther

0%

5%

10%

15%

20%

25%

30%

11% 12%

26%24%

27%

Percentage

(Source: Primary data)

Interpretation:

From the above data, it is clear that out of total response, 26% respondents are Govt. employee, 42% are private employee, 12% are businessmen, 11% respondents are professor and only 27% respondents are other categories respectively.

Table No.5.4 Analysis according to income.

Page 34

Income group Response Percentage

Below 1 lack 25 25

1 lack-2 lack 24 24

2 lack-3 lack 29 29

3 lack& above 22 22

Total 100 100

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Graph No. 5.4 Analysis according to income.

Below 1 lakh 1 lakh-2 lakh 2 lakh-3 lakh 3 lakh & above0%

5%

10%

15%

20%

25%

30%25% 24%

29%

22%

Percentage

Percentage

(Source: Primary data)

Interpretation:

From the above data, it is clear that out of the total response, 29% respondents belong to 2 lack-3 lack, 25% respondents belong to the below 1 lack, 24% respondents belong to 1 lack-2 lack, 22% respondents belong to the higher income group 3 lack & above.

Table No.5.5 Analysis according to educational qualification:-

Educational Qualification

Response Percentage

S.S.C 0 0

H.S.C 2 2

Graduate 38 38

Post graduate 48 48

Other 12 12

Page 35

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Graph No. 5.5 Analysis according to educational qualification

S.S.C H.S.C Graduate Post graduate Other0%

10%

20%

30%

40%

50%

60%

0% 2%

38%

48%

12%

Percentage

Percentage

(Source: Primary data)

Interpretation:-

From above data, it shows that out of total response, 0% respondents are passed S.S.C, 2% respondent are H.S.C, 38% respondents are graduate, 48% respondents are post graduate & 12% are other qualification.

Table No.4.6 Analysis according to loan taken.

Graph No. 5.6: Analysis according to Loan taken.

Page 36

Types of loan Response PercentageHome loan 29 29

Education loan 21 21Vehicle loan 18 18

Gold loan 9 9Personal loan 16 16Mortgage loan 7 7

Total 100 100

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

29%

21%18%

9%

16%

7%

Percentage

Home loanEducation loanVehicle loanGold loanPersonal loanMortgage loan

(Source: Primary data)

Interpretation:

From the above data, we can see that out of total response, 29% respondents have taken home loan, 21% respondents are taken education loan, 18% respondent are taken vehicle loan, 16% respondent are taken personal loan, 9% respondent are taken gold loan and 7% respondent are taken mortgage loan.

Table No.5.7 Analysis according to which year take a loan.

Graph No. 5.7: Analysis according to which year take a loan.

Page 37

year Response PercentageBefore 2000 31 31

2000-03 18 182004-07 24 242008-11 22 22

2012 & onwards 5 5Total 100 100

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

before-2000 2000-03 2004-07 2008-11 2012 &

onwards

0%5%

10%15%20%25%30%35% 31%

18%24%

22%

5%

Percentage

Percentage

(Source: Primary data)

Interpretation:

From the above data, it reveals that out of the total respondents ,31% are taken a loan before 2000, 24% are 2004-07, 22% are 2008-11, 18% are 2000-03 and 5% are 2012 & onwards.

Table No.5.8 Analysis according to marital status

Graph No. 5.8: Analysis according to marital status.

Page 38

Married & unmarried Response PercentageMarried 28 28

Unmarried 72 72Total 100 100

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

28%

72%

Percentage

MarriedUnmarried

(Source: Primary data)

Interpretation:

From the above data, it shows the analyses according to marital status 28% are married and 72% are unmarried.

Table No.5.9 Analysis according to different sources of information.

Page 39

Sources Response PercentageT.V. 5 5

News papers 20 20Bank 21 21

Friends 22 22Internet 20 20Other 12 12

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Graph No. 5.9: Analysis according to different sources of information.

T.V.

News p

aper

Bank

Frien

ds

Internet

Other

0%

5%

10%

15%

20%

25%

5%

20% 21% 22%20%

12%Percentage

(Source: Primary data)

Interpretation:

From the above data, it is revealed that out of total response, 22 respondents are select loan as friend’s advice. , 20% are from internet, 20% are from news paper, 21 are from bank, 12% are other and 5% are from T.V.

Table No.5.10 Analysis according to Factors responsible for selection of loan.

Page 40

Factors Response PercentageRate of interest 31 31

Low documentation 23 23Low service charges 16 16

Good customer service 12 12Convenient repayment 18 18

Total 100 100

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Graph No.5.10: Analysis according to factors responsible for selection of loan.

Rate of in

terest

Low docu

mentati

on

Low se

rvice

charg

es

Good custo

mer ser

vice

Convenien

t rep

aymen

t0%5%

10%15%20%25%30%35%

31%

23%

16%12%

18%

Percentage

Percentage

(Source: Primary data)

Interpretation:

From the above data, we can say that out of total respondent 31% are rate of interest, 23% are low documentation, 18% are convenient repayment, 16% are low service charges and 12% are good customer service.

Table No.5.11 Analysis according to Rate of interest.

Level of significance Response PercentageHigh significant 56 56

Significant 26 26Not significant 18 18

Total 100 100

Graph No. 5.11: Analysis according to Rate of interest.

Page 41

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

High significant Significant Not significant0%

10%

20%

30%

40%

50%

60%56%

26%

18%

Percentage

Percentage

(Source: Primary data)

Interpretation:

From the above data, Out of total respondents 56% are high significant, 26% are significant and 18% are not significant.

Table No.5.12 Analysis according to easy & fast procedure.

Level of significance

Response Percentage

High significant

59 59

Significant 31 31Not significant 10 10

Total 100 100

Page 42

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Graph No. 5.12: According to easy & fast procedure.

59%

31%

10%

Percentage

High significantsignificantNot significant

(Source: Primary data)

Interpretation:

From the above data, Out of total respondents 59% are high significant, 31% are significant and 10% are not significant.

Table No.5.13 Analysis according to Low documentation.

Page 43

Yes/no Response PercentageYes 81 81No 19 19

Total 100 100

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Graph no.5.13: According to Low documentation

Yes No0%

10%20%30%40%50%60%70%80%90%

81%

19%

Percentage

Percentage

(Source: Primary data)

Interpretation:

From the above data, we can see that out of total respondents 81% are said Yes and 19% are said No.

Table No.5.14 Analysis according to low service charges.

Yes/No Response PercentageYes 60 60No 40 40

Total 100 100

Page 44

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Graph No. 5.14: According to low service charges.

60%

40%

Percentage

Yes

No

(Source: Primary data)

Interpretation:

From the above data, we can see that out of total respondents 60% are said Yes and 40% are said No.

Table No.5.15 Analysis according to face any difficulty.

Yes/No Response PercentageYes 19 19No 81 81

Total 100 100

Table No. 5.15: According to face any difficulty.

Page 45

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

19%

81%

Percentage

Yes

No

(Source: Primary data)

Interpretation:

From the above data, we can see that out of total respondents 81% are said Yes and 19% are said No.

Table No.5.16 Analysis according to grade.

Grade Response PercentageExcellent 29 29

Good 35 35Average 21 21

Poor 15 15Total 100 100

Page 46

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Graph No. 5.16: Analysis according to grade

29%

35%

21%

15%

Percentage

Excellent

Good

Average

Poor

(Source: Primary data)

Interpretation:

From the above data, It is clear that 35% respondents are given excellent grade, 29% are given good, 21% are given average and 15% are given poor.

Table No.5.17 Analysis according to property as mortgage.

Type of property Response PercentagePlot paper 29 29

House paper 7 7Insurance paper 21 21

Other 43 43Total 100 100

Page 47

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Table No. 5.17: According to property as mortgage

29%

7%21%

43%

Percentage

Plot paper

House paper

Insurance paper

Other

(Source: Primary data)

Interpretation:

From the above data, It is clear that 29% respondents are mortgage there plot paper, 21% are given insurance paper, 7% are given house paper and 43% are given other documents as mortgage.

CHAPTER NO: 6

FINDINGS & CONCLUSIONS

6.1 FINDINGS:-

It is found that, majority of respondents were between the age group of 30-

35.

Page 48

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Majority of respondent were male.

Majority of respondents were government employees.

Majority of respondents were unmarried.

Majority of respondent were taken a loan before the year 2000.

It is found that, rate of interest, low documentation, low service charges;

good customer service and convenient payment were the most important

factor which plays an important role in decision making process of

selecting loans.

Majority of respondents were not facing any difficulty while taken a loan

from bank.

Majority of respondents have post graduate and their income is 1 lack to 3

lack and taken different types of loan and enjoy the benefits of these loans

schemes.

Majority of respondents have given good grade to bank because of their

cheapest interest rate, low documentation and low charges etc.

Majority of respondents have taken home loan from Bank of Baroda of

India because of their cheapest interest rate and these people are in age

group of 32 to 35.

Majority of respondents got information about different loan schemes of

Bank of Baroda of India from friends i.e. 22%. It means that, friends were

strongest source of information.

6.2 SUGGETIONS:

Branches of organization should arrange customers meeting to popularize

these lending schemes.

Bank of Baroda should appoint financial adviser for loans. At the apex

level a lot of publicity should be given on the advantages of bank loans.

Page 49

“A study of various loans scheme provided by Bank of Baroda in Khamgaon”

Loan application forms should be simplified.

The system of changing a reduced rate of interest based on the credit

rating of the borrowers may be introduced in personal loan schemes.

Page 50