16-1. notes payable and notes receivable section 1: accounting for notes payable chapter 16 section...

TRANSCRIPT

16-1

Notes Payable and Notes

Receivable

Notes Payable and Notes

Receivable

Section 1: Accounting for

Notes Payable

Chapter

16

Section Objectives1. Determine whether an instrument meets all the

requirements of negotiability.

2. Calculate the interest on a note.

3. Determine the maturity date of a note.

4. Record routine notes payable transactions.

5. Record discounted notes payable transactions.McGraw-Hill © 2009 The McGraw-Hill Companies, Inc. All rights reserved.

16-3

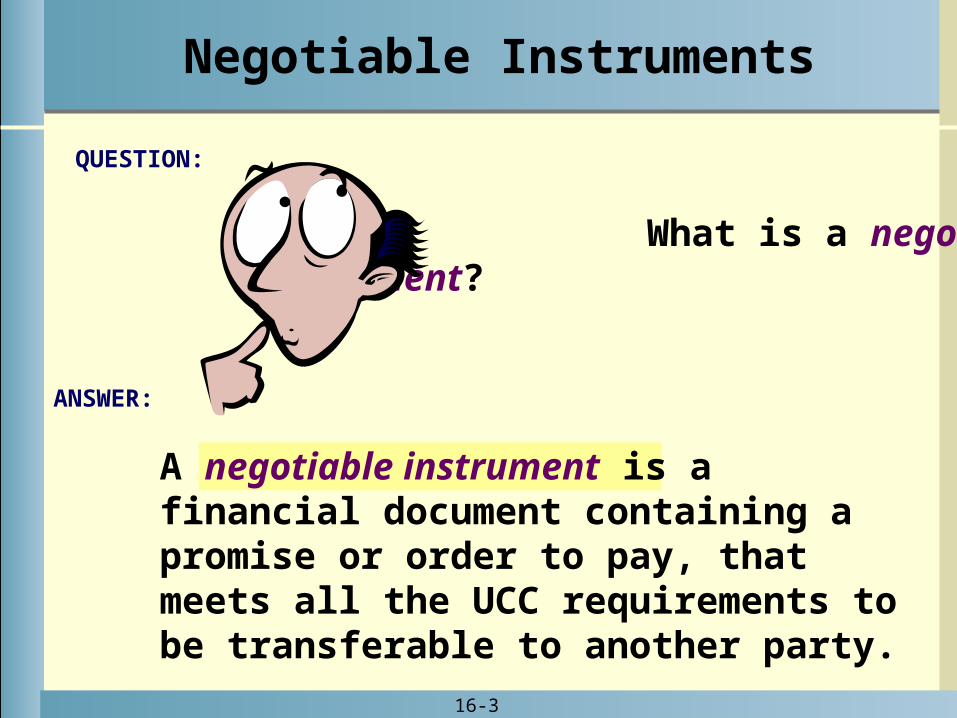

A negotiable instrument is a financial document containing a promise or order to pay, that meets all the UCC requirements to be transferable to another party.

ANSWER:

QUESTION:

What is a negotiable instrument?

Negotiable Instruments

16-4

UCC Requirements for Negotiability

Must be in writing and signed by the maker.

Must contain an unconditional promise to pay a definite amount of money.

Must be payable either on demand or at a future

time that is fixed or that can be determined.

Must be payable to the order of a specific person or to the bearer.

Must clearly name or identify the drawee if addressed to a drawee.

Determine whether an instrument meets all the requirements for negotiability

Objective 1

16-5

A note payable is a liability that represents a written promise by the debtor to pay the creditor a specified amount at a specified future date.

ANSWER:

QUESTION:

What is a note payable?

Notes Payable

16-6

Interest is the fee charged for the use of money.

ANSWER:

QUESTION:

What is interest?

Calculate the interest on a noteObjective 2

16-7

Interest = Principal x Rate x Time

Amount being borrowed (also called face value)

Indicated in fractions of a year

Calculating Interest on a note

Principal x Rate x Time = Interest

$2,500 x 0.12 x (90/360) = $75

16-8

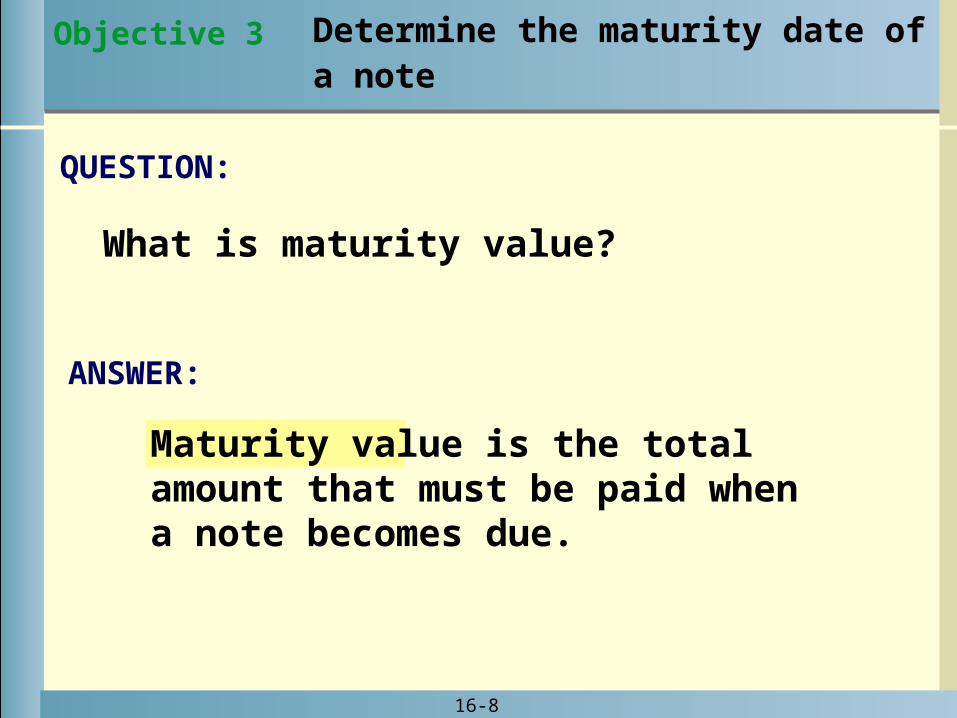

Maturity value is the total amount that must be paid when a note becomes due.

ANSWER:

QUESTION:

What is maturity value?

Determine the maturity date of a note

Objective 3

16-9

Determine the number of days remaining in the month of issue.

Determine the number of days in each full month of the note.

Determine the number of days in the last month of the note.

Add the days together to confirm that they equal the period of the note.

Calculating the Maturity Dateof a Note

Principal + Interest = Maturity Value

$2,500 + $75 = $2,575

16-10

A 90-day note is issued May 18.Number of days remaining in month of issue =

Number of days in each full month of the note =

Maturity date is August 16.

Month of May 31 days Issue Date May 18 – 18 days

Term of note 90 days Days in May – 13 days

May 13 days

77 days June – 30 days July – 31 days

August 16 days

16-11

Month Days

Period of Note 90 days

May 13

Total 90 days

June 30

July 31

Aug 16

Calculating Maturity Date

16-12

Notes Payable TransactionsNotes Payable Transactions

2010

May. 18 Store Equipment 4,000.00

Notes Payable—Trade 4,000.00

Issued note payable to

Unpainted Furniture Inc.

for purchase of store

equipment.

Record the issuance of a note payable.

Record routine notes payable transactions

Objective 4

16-13

2010

Aug 16 Notes Payable—Trade 4,000.00

Interest Expense 80.00

Cash 4,080.00

Payment of May 18

note to Unpainted Furniture Inc.

Record payment of the note payable and interest: Interest rate is 8%, term of note is 90 days.

Notes Payable TransactionsNotes Payable Transactions

16-14

Discounted Notes PayableDiscounted Notes Payable

Face Amount – Discount = Proceeds

$12,000 – $140 = $11,860

Example: If a $12,000, 7% 60-day note is discounted with the bank, then the borrower would receive only $11,860.

$12,000 x 7% x 60/360 = $140 interest

Record discounted notes payable transactions

Objective 5

16-15

Recording a Discounted Note PayableRecording a Discounted Note Payable

2010

June 1 Cash 11,860.00

Interest Expense 140.00

Notes Payable—Bank 12,000.00

To record note payable

issued at a discount

Record issuance of discounted note:

Notice that Interest Expense is debited for the $140 interest paid in advance.

16-16

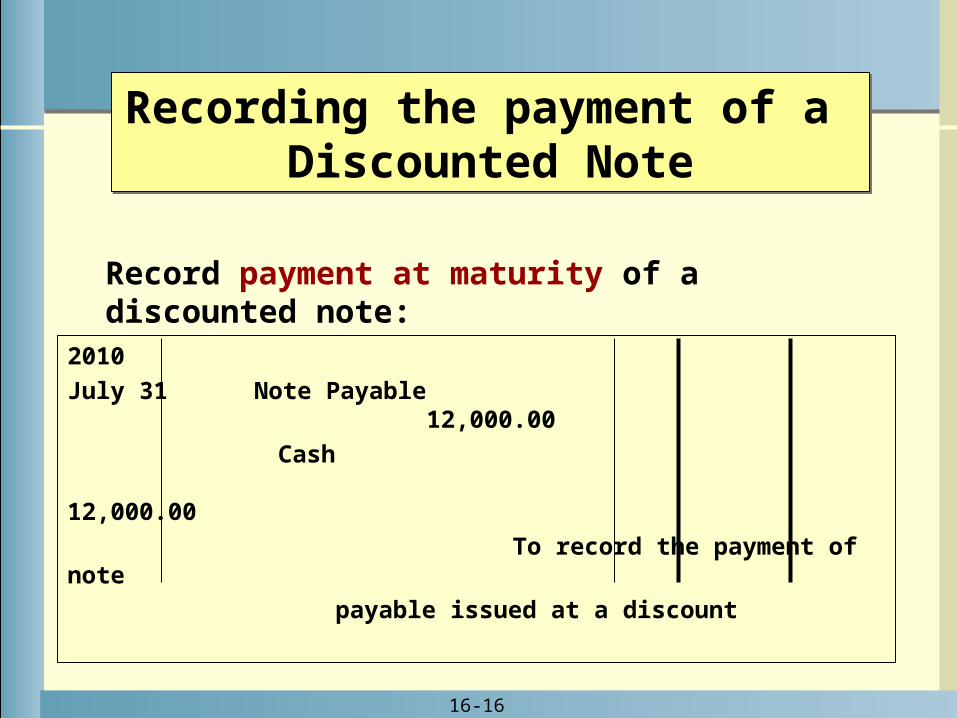

Recording the payment of a Discounted Note

Recording the payment of a Discounted Note

2010

July 31 Note Payable 12,000.00

Cash 12,000.00

To record the payment of note

payable issued at a discount

Record payment at maturity of a discounted note:

16-17

Reporting Notes Payable and Interest Expense

Notes Payable Current liabilities if due within one year.

Long-term liabilities if due in more than one year.

Interest Expense Classified as a nonoperating expense.

Listed in the Other Income and Expenses section of the income statement.

Notes Payable and Notes

Receivable

Notes Payable and Notes

Receivable Section 2: Accounting for

Notes Receivable

Chapter

16

Section Objectives

6. Record routine notes receivable transactions.

7. Compute the proceeds from a discounted note receivable, and record transactions related to discounting of notes receivable.

8. Understand how to use bank drafts and trade acceptances and how to record transactions related to those instruments.

McGraw-Hill © 2009 The McGraw-Hill Companies, Inc. All rights reserved.

16-19

A note receivable is an asset representing a written promise by the debtor to pay the creditor a specified amount at a specified future date.

ANSWER:

QUESTION:

What is a note receivable?

Record routine notes receivable transactions

Objective 6

16-20

Notes Receivable TransactionsNotes Receivable Transactions

2010

Sept. 18 Notes Receivable 1,600.00

Accounts Receivable/Li Jiunn 1,600.00

To record 30-day note receivable

to replace overdue accounts

receivable.

Record the receipt of a non-interest bearing note receivable.

16-21

Notes Receivable TransactionsNotes Receivable Transactions

2010

June 11 Notes Receivable 1,200.00

Accounts Receivable/Trey Leone 1,200.00

To record 60-day note receivable

to replace an overdue account

receivable.

Record the receipt of an interest bearing note receivable.

16-22

Notes Receivable TransactionsNotes Receivable Transactions

2010

Aug 11 Cash 1,220.00

Note Receivable 1,200.00

Interest Income 20.00

Collection of Trey Leone’s note

plus

(interest= 1,200 x 10% x 60/360 days)

Record the receipt of cash from a customer in payment of their note.

16-23

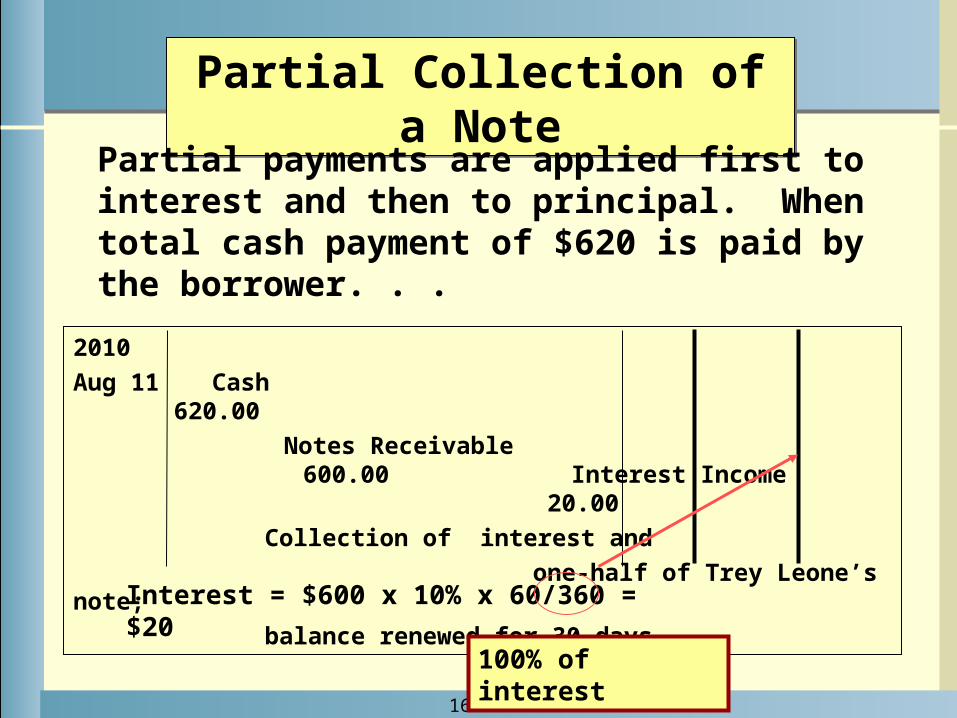

Partial Collection of a NotePartial Collection of a NotePartial payments are applied first to interest and then to principal. When total cash payment of $620 is paid by the borrower. . .

2010

Aug 11 Cash 620.00

Notes Receivable 600.00 Interest Income 20.00

Collection of interest and

one-half of Trey Leone’s note;

balance renewed for 30 days

Interest = $600 x 10% x 60/360 = $20

100% of interest

16-24

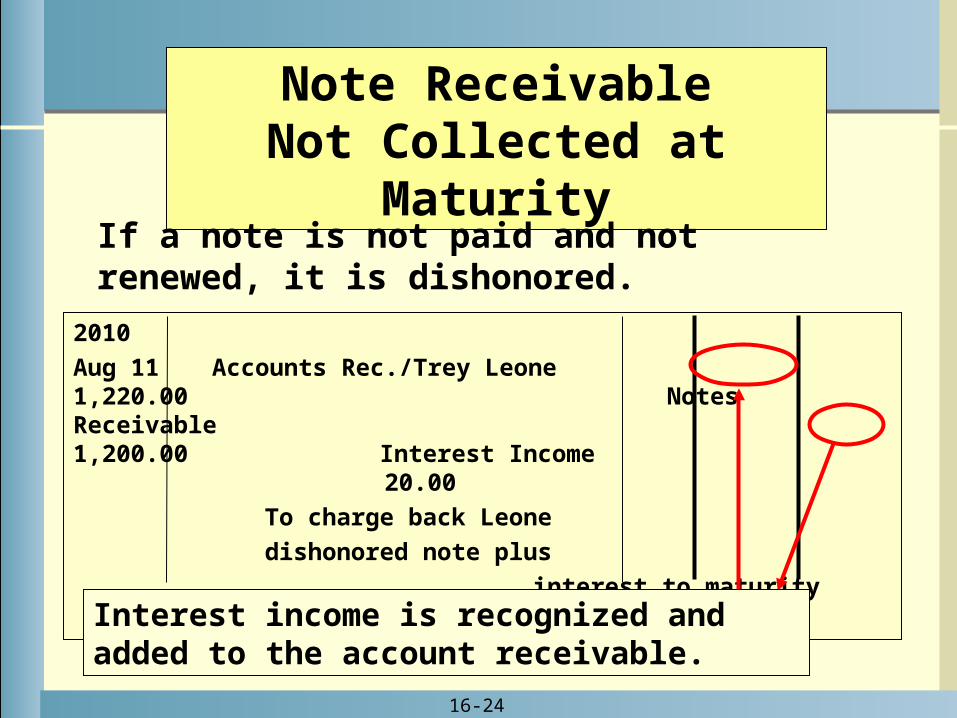

Note ReceivableNot Collected at Maturity

If a note is not paid and not renewed, it is dishonored.

2010

Aug 11 Accounts Rec./Trey Leone 1,220.00 Notes Receivable 1,200.00

Interest Income 20.00

To charge back Leone

dishonored note plus

interest to maturity

Interest income is recognized and added to the account receivable.

16-25

2010

Aug 15 Notes Receivable 1200.00

Sales 1200.00

Received 60-day, 9%

note from Sylvia Madeo

on sale of goods

Note Receivable at the Time of Sale

16-26

Discounting a Note ReceivableDiscounting a Note Receivable

If the noteholder wants cash before the maturity date, the note can be discounted (sold) at the bank.

Compute the proceeds from a discounted note receivable, and record transactions related to discounting of notes receivable

Objective 7

16-27

The bank pays the proceeds to the noteholder.

Principal + Interest – Discount

(Maturity Value)

= Proceeds

Discounting a Note Receivable

16-28

Step 1: Determine the maturity value of the note.

Step 2: Calculate the number of days in the discount period.

Step 3: Compute the discount charged by the bank.

Step 4: Calculate the proceeds.

Calculating the Discount and the Proceeds

The discount period is the period from the date the note is taken to the bank to be discounted (or sold) and continues on to the maturity date.

Discount Period

16-29

Recording a Discounted Note Receivable

2010

Sept. 18 Cash 1,980.00

Interest Expense 20.00

Notes Receivable–Discounted 2,000.00

To record discounting of

Jack Miller note

16-30

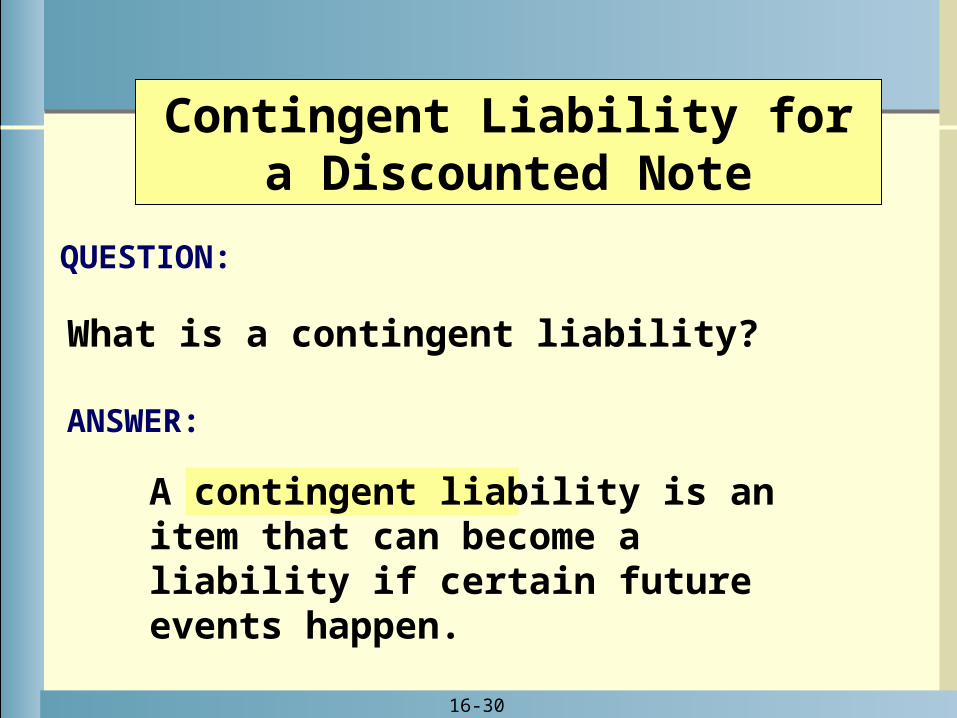

A contingent liability is an item that can become a liability if certain future events happen.

ANSWER:

QUESTION:

What is a contingent liability?

Contingent Liability for a Discounted Note

16-31

The note holder endorses the discounted note receivable.

If the maker of the note dishonors the note, the bank can obtain payment from the endorser.

The endorser has a contingent liability.

Contingent Liability for a Discounted Note

16-32

The contingent liability can appear as a separate item on the balance sheet:

Notes Receivable $ 7,400

Notes Receivable – Discounted (2,000)

Reporting Contingent LiabilitiesReporting Contingent Liabilities

Net Notes Receivable $ 5,400

Another common way to report contingent liabilities

is to present net notes receivable on the balance sheet and to include a footnote with information about the discounted notes receivable.

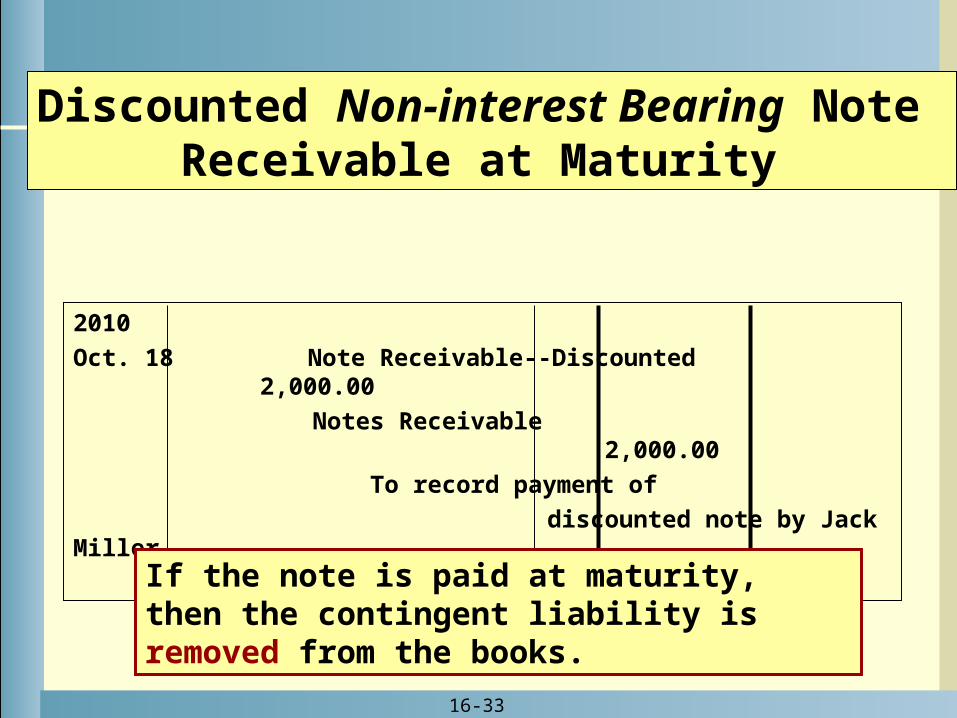

16-33

Discounted Non-interest Bearing Note Receivable at Maturity

2010

Oct. 18 Note Receivable--Discounted 2,000.00

Notes Receivable 2,000.00

To record payment of

discounted note by Jack Miller

If the note is paid at maturity, then the contingent liability is removed from the books.

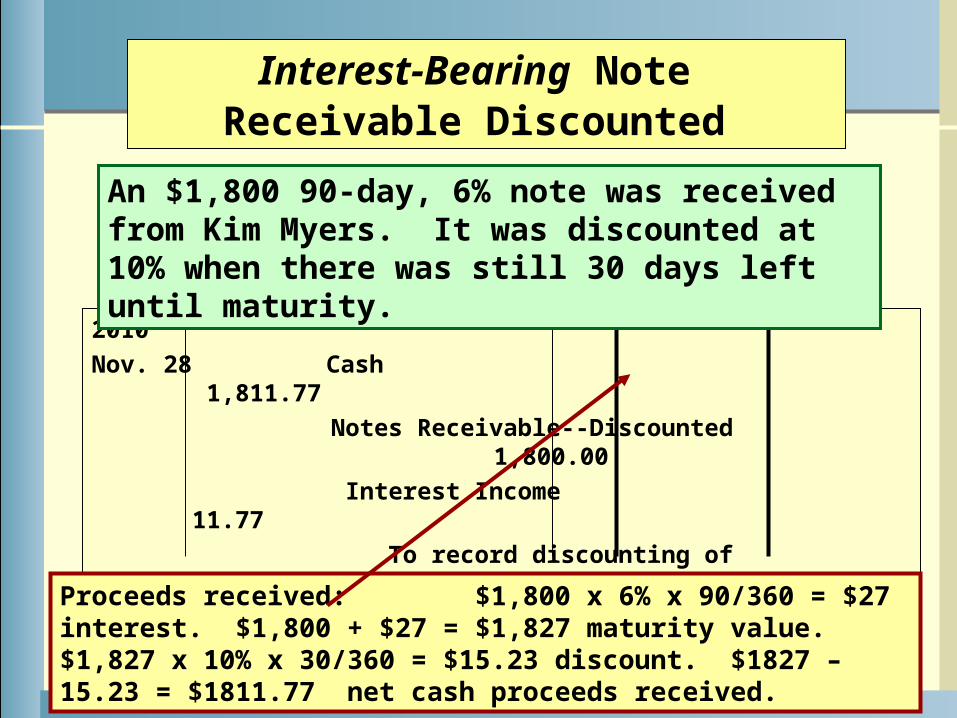

16-34

Interest-Bearing Note Receivable Discounted

2010

Nov. 28 Cash 1,811.77

Notes Receivable--Discounted 1,800.00

Interest Income 11.77

To record discounting of

Kim Myers note

An $1,800 90-day, 6% note was received from Kim Myers. It was discounted at 10% when there was still 30 days left until maturity.

Proceeds received: $1,800 x 6% x 90/360 = $27 interest. $1,800 + $27 = $1,827 maturity value. $1,827 x 10% x 30/360 = $15.23 discount. $1827 – 15.23 = $1811.77 net cash proceeds received.

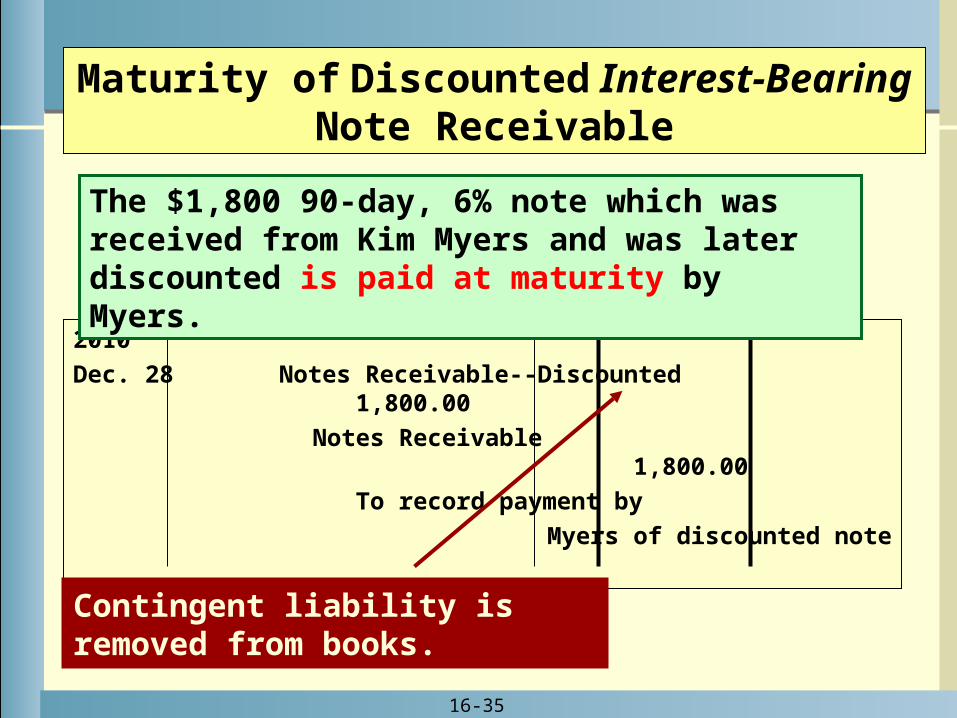

16-35

Maturity of Discounted Interest-Bearing Note Receivable

2010

Dec. 28 Notes Receivable--Discounted 1,800.00

Notes Receivable 1,800.00

To record payment by

Myers of discounted note

The $1,800 90-day, 6% note which was received from Kim Myers and was later discounted is paid at maturity by Myers.

Contingent liability is removed from books.

16-36

Notes Receivable

Current asset if due within one year.

Long-term asset if due in more than one year.

Interest Income

Classified as non-operating income.

Listed in the Other Income and Expenses section of the income statement.

Reporting Notes Receivable and Interest Income

16-37

Understand how to use bank drafts and trade acceptances and how to record transactions related to those instruments.

Objective 8

16-38

Draft: a written order that requires one party to pay a stated sum of money to another party

Check

Bank Draft A bank orders another bank to pay the stated amount to a specific party.

It is more readily accepted than a business or personal check.

Commercial Draft One party orders another party to pay a specified amount on a specified date.

It is used for special shipment and collection situations.

Drafts and Acceptances

16-39

Trade Acceptance: a draft used in recording transactions involving the sale of goods

Recorded as a sale on credit

Accounted for as a promissory note

Original transaction

Trade acceptance

16-40

Thank Youfor using

College Accounting, 12th Edition

Price • Haddock • Farina