1 knowledge as a mediator between hrm practices and innovative

TRANSCRIPT

1

KNOWLEDGE AS A MEDIATOR BETWEEN HRM PRACTICES AND

INNOVATIVE ACTIVITY

(PAPER EN PRENSA: REVISTA HUMAN RESOURCE MANAGEMENT)

Dr. Álvaro López Cabrales

Assistant Professor.

Universidad Pablo de Olavide

Departamento de Dirección de Empresas

Ctra. Utrera, Km. 1 – 41013 Sevilla

Tel. 954349180

Fax: 954348353

Dr. Ana Perez-Luño

Assistant Professor.

Universidad Pablo de Olavide

Departamento de Dirección de Empresas

Ctra. Utrera, Km. 1 – 41013 Sevilla

Tel. 954348977

Fax: 954348353

Dr. Ramón Valle Cabrera

Professor.

Universidad Pablo de Olavide

Departamento de Dirección de Empresas

Ctra. Utrera, Km. 1 – 41013 Sevilla

Tel. 954349276

Fax: 954348353

Correspondence must be sent to Dr. Alvaro Lopez- Cabrales

2

KNOWLEDGE AS A MEDIATOR BETWEEN HRM PRACTICES AND

INNOVATIVE ACTIVITY

ABSTRACT

The objective of this paper is to test how HRM practices and employees’ knowledge

influence the development of innovative capabilities, and by extension, firm’s

performance. Results confirm that HRM practices are not directly associated with

innovation unless they take into account employees’ knowledge. Specifically, our

analyses establish a mediating role for the uniqueness of knowledge between

collaborative HRM practices and innovative activity, a positive influence of knowledge-

based HRM practices on valuable knowledge and a positive contribution of innovations

to the company’s profit. Hypotheses are tested in a sample of firms from the most

innovative Spanish industries through structural equation modelling.

KEYWORDS

HRM practices, valuable and unique knowledge, innovation.

3

INTRODUCTION

In recent years, there has been a considerable increase in the literature analysing

innovation and organisational change (Anand et al., 2007). This broad body of research

has generated growing interest in identifying how companies can improve their

innovative activity and what internal and external factors have positive effects on such

behaviour (Damanpour, 1991; Galunic & Rodan, 1998; Zhou, 2006).

Based on the resource-based view (RBV), authors such as Wernerfelt (1984) and Barney

(1991) proposed that the crucial research question concerns what kinds of corporate

resources lead to sustainable competitive advantages. Following these arguments, the

types of knowledge, skills and abilities (KSA) of employees have been considered key

resources for the improvement of existing products and services or for the generation of

new ones (innovations), which by extension help to achieve competitive advantages

(Donnellon, 1996; Jackson, 1992; Nonaka & Takeuchi, 1995; Thompson, 2003). In

addition, it is argued that there must be coherence between an organisation’s human

resources management (HRM) practices and the strategies that it adopts, and this

requirement would also be applicable to an innovation strategy (Balkin et al., 2000;

Gupta & Singhal, 1993; Kang et al., 2007; Laursen 2002; López-Cabrales et al., 2006;

Schuler & Jackson, 1987). Therefore, the research question we seek to address is to what

extent the contribution of HRM practices to product innovation and performance is

conditioned by the employees’ knowledge. In order to answer this question, the purpose

of this study is to analyse, in the R&D department of innovative companies, the

mediating role of the knowledge possessed by the employees between HRM practices,

innovative activity and performance.

4

Explaining how the coherence between HRM practices and knowledge enhances

innovation and performance could extend the RBV, HRM and innovation literatures.

Specifically, this paper is expected to make three main contributions. The first

contribution is related to the relationship, on the whole, between HRM practices,

knowledge and the innovative activity in R&D departments. In this sense, our findings

improve the innovation literature providing new predictors of innovative capability. The

second contribution, which enriches the HRM literature, concerns the consequences of

HRM practices. We assume that HRM practices are directly associated with employees’

knowledge, in a similar way as proposed by Lepak and Snell (1999, 2002). Furthermore,

we add to the traditional Lepak and Snell arguments that these practices are indirectly

related to the innovative activity of organisations. The third contribution is related to the

lack of systematic empirical support received for the RBV (Newbert, 2007). For this

reason, having demonstrated that a bundle of resources (knowledge) and capabilities

(innovative activity) can be seen as good drivers of competitive advantages, this study is

an attempt to extend the empirical support for such a theoretical approach.

The structure adopted in the article, consistent with its objectives, is as follows. After

this introduction, we present a theoretical review that enables us to delimit the

relationships between knowledge, HRM practices, innovation and profits. As a result of

this analysis, several hypotheses are formulated and tested empirically, using a survey of

firms from the most innovative Spanish industries, and applying structural equation

modelling. Finally, conclusions, contributions, limitations and future lines of research

are presented.

5

THE ROLE OF EMPLOYEES’ KNOWLEDGE IN PRODUCT INNOVATION

There is a great diversity of concepts used to define the term “innovation”. Kimberly &

Evanisko (1981) explained that this term could have three different uses. Firstly, they

stated that innovation can be understood as a discrete element that includes the

development of products, programs or services. Secondly, they pointed out that

innovation can be considered a process; that is to say, they refer to different stages of the

innovation process. Finally, they mentioned that innovation can be understood as an

organisational capability (innovativeness and/or innovative capability). Conceptually

these three elements are mutually compatible. When a firm is described as innovative

(innovation as an organisational capability), it generally means that it develops or

frequently adopts products, services, programs or innovative ideas (innovation as

discrete elements) that need a series of stages (innovation as a process) in order to be

sources of competitive advantages. While these three uses of the term “innovation”

could be broadly debated, this paper will only focus on the use of innovation as an

organisational capability. The reason is that, as we have just mentioned, an innovative

company generally develops all the stages needed to give rise to new products.

Therefore, this use of the term “innovation” includes the other two. This “innovation” is

understood as a broad term that defines the ability of a firm to introduce new products or

lines (ranges) into the market (Pérez-Luño et al., 2007). That is, it is the degree to which

a company strays from existing practices in the creation of new products that are

successfully marketed (Capon et al., 1992).

It is accepted that a firm’s ability to obtain new products and other aspects of

performance are inextricably linked to the knowledge of their human resources (Foss,

6

2007; Laursen, 2002). In this sense, the most distinctive and inimitable resource

available to firms is people-embodied knowledge, which enables them to manipulate and

transform other organisational resources effectively (Argote & Ingram, 2000; Foss,

2007; Kogut & Zander, 1992). Furthermore, knowledge-based resources may be

particularly important for providing a sustainable competitive advantage (McEvily &

Chakravarthy, 2002), playing an essential role in the firm’s ability to innovate (Galunic

& Rodan, 1998), and improving performance (Wiklund & Shepherd, 2003). Therefore, it

can be inferred that competitive advantages are increasingly derived from knowledge

and technological skills, and experience in the creation of new products (Alegre et al.,

2006; Teece et al., 1997).

The previous assumptions lead us to wonder which characteristics of knowledge enable

product innovation. It is known that knowledge can be analysed from different

perspectives. Taking into account the intellectual capital literature, it distinguishes three

different aspects of knowledge: human, organisational and social capital (Subramaniam

& Youndt, 2005). Human capital is defined as the knowledge, skills, and abilities

residing with and utilised by individuals (Schultz, 1961). Organisational capital is the

institutionalised knowledge and codified experience residing within and utilised through

databases, patents, manuals, structures, systems, and processes (Youndt et al., 2004).

Finally, social capital is the knowledge embedded within, available through, and utilised

by interactions among individuals and their networks of interrelationships (Nahapiet &

Ghoshal, 1998). As Subramaniam and Youndt (2005) pointed out, each one of these

components accumulates and distributes knowledge in a different way: human capital

through individuals, organisational capital through firm structures and processes, and

7

social capital through relationships and networks. Based on these conceptual issues, we

focus on the impact of employees’ knowledge (human capital) on product innovation.

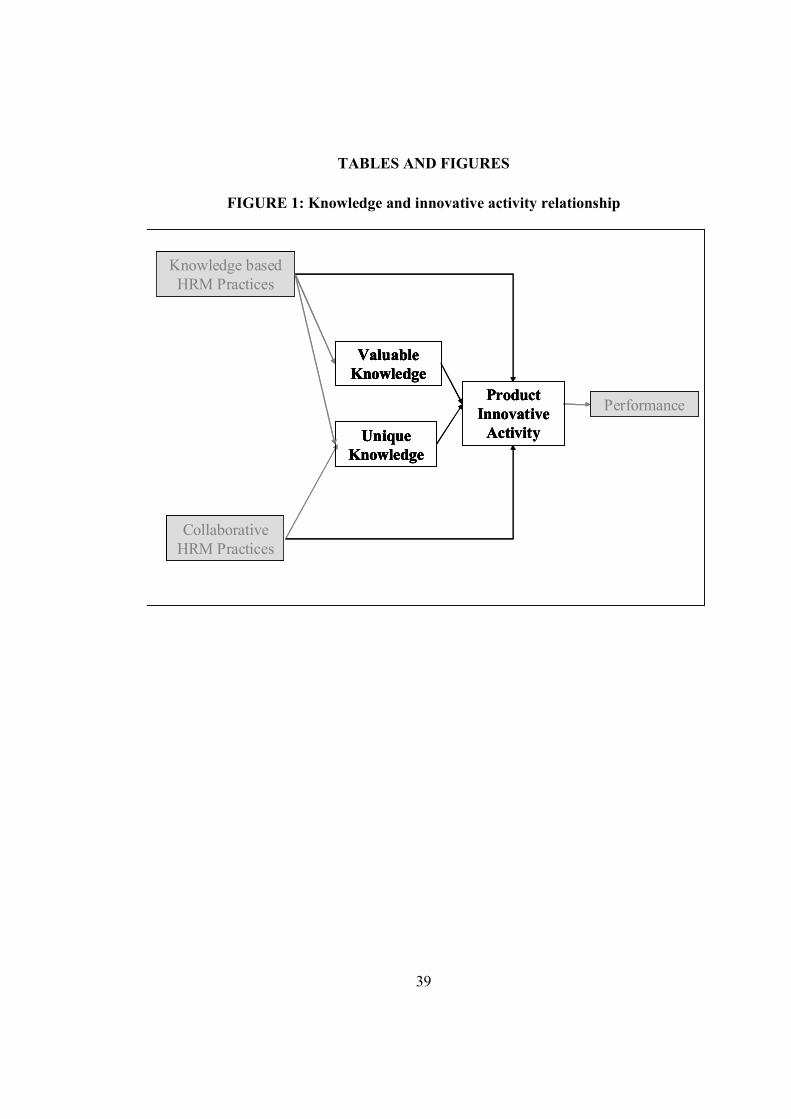

Considering the human capital approach, the value and uniqueness of employees’

knowledge are the most relevant features for product innovation, as Figure 1 explains

(Lepak & Snell, 1999; Subramaniam & Youndt, 2005).

------------------------------------------

Insert Figure 1 about here

------------------------------------------

The value of knowledge refers to its potential to improve the efficiency and effectiveness

of the firm, exploit market opportunities, and/or neutralise potential threats (Lepak and

Snell, 2002: 519). As Barney and Wright (1998) suggested, any resource creates value

through either decreasing product/service costs or differentiating product/service in a

way that allows the firm to charge a premium price, so a valuable knowledge will yield

high returns in markets increasing the ratio of benefits to customers relative to their

associated costs (Snell et al., 1999; Wernerfelt, 1984). Nevertheless, to be good at doing

something does not mean that knowledge is valuable, as Lengnick-Hall and Lengnick-

Hall (2002) pointed out. The cited authors defined value as “the degree to which the

human capital lowers costs or provides increased services or product features that matter

to customers” (2002: 50). An example is the case of Sony, which possesses valuable

knowledge in designing, manufacturing and selling miniaturised electronic technology,

and such knowledge provides it with a competitive advantage (Barney, 1995). The

second feature is the uniqueness of a person’s knowledge and skills. This means that an

8

employee must be irreplaceable and idiosyncratic with rare and firm-specific KSA

(Barney, 1991), difficult to transfer to other positions or even difficult to be duplicated

by other firms (Lepak & Snell, 1999).

Given the fact that creative people must deal with novel and ambiguous problems, they

tend to display strong, valuable and irreplaceable knowledge and skills (Mumford,

2000). Additionally, product innovation consists of successful exploitation of new ideas.

Therefore, it implies two conditions: novelty and use (Alegre et al., 2006). These

conditions can only be produced by useful or valuable knowledge. Valuable knowledge

is positively associated with product innovations because it contributes to identification

of new market opportunities, and employees with such knowledge are willing to

experiment and apply new knowledge (Costa & McCrae, 1992; Taggar, 2002).

Moreover, scholars studying innovative activity have addressed the importance of

individuals’ expertise and valuable knowledge that allows them to obtain novel ideas

and gives rise to innovations (Anand et al., 2007). Nevertheless, it must be said that

valuable knowledge is a necessary but not sufficient condition for developing product

innovations. That is, R&D departments will take advantage of the valuable knowledge

owned by their employees, but they will also need other features such as creativity,

entrepreneurship, unique knowledge, etc. to develop product innovations. Based on

these arguments, we propose our first hypothesis.

H1. Valuable knowledge is positively associated with innovation.

The second characteristic of knowledge associated with innovation is uniqueness. This

unique knowledge can create a competitive differentiation because valuable but common

(i.e. not rare) resources and capabilities are sources of competitive parity (Barney, 1995;

9

Snell et al., 1999). Furthermore, uniqueness refers to the degree of content specificity of

the knowledge and its difficulty in being transferred to other organisations (Lengnick-

Hall and Lengnick-Hall, 2002). That could be the reason why it is very difficult to be

innovative based on generic knowledge (Nonaka & Takeuchi, 1995), so people with

unique KSA are considered “rainmakers”, and their specialised knowledge contributes to

the development of new ideas or products (James, 2002). Amar (2002) suggested that

these employees possess rare KSA that are not commonly distributed in the labour

market. Therefore, their knowledge is also new to any competitor firm and is an

intangible resource for firm innovation. Based on these arguments, we propose our

second hypothesis.

H2. Unique knowledge is positively associated with innovation.

HRM PRACTICES AS FACILITATORS OF KNOWLEDGE AND PRODUCT

INNOVATION

Based on the RBV, some authors note that not only should a firm’s resources be

valuable and unique to facilitate superior performance but also the firm must have an

appropriate organisation in place to take advantage of these resources (Barney & Wright,

1998; Foss, 2007; Peltokorpi & Tsuyuki, 2006). Empirical studies have mainly focused

on the direct link between individual strands or configurations of resources and

performance, while less attention has been devoted to how management can use their

resources more effectively (Wiklund & Shepherd, 2003). Therefore, as Figure 2 shows,

HRM practices can explain, in part, the managerial processes that allow firms to obtain

valuable and unique knowledge and, by extension, how this valuable and unique

knowledge leads to innovative activity and higher performance.

10

------------------------------------------

Insert Figure 2 about here

------------------------------------------

These valuable and unique characteristics of employees’ knowledge create a “human

capital advantage” (Boxall, 1996). Nevertheless, any human capital advantage may

decrease in the long term. Therefore, organisations must define and apply appropriate

HRM practices for managing people and link them to the core capabilities of the firm

(Amit & Belcourt, 1999; Peltokorpi & Tsuyuki, 2006; Purcell, 1996). As Paauwe &

Boselie (2005: 72) indicated, “the search for the Holy Grail in HRM is the search for

those best practices or best-fit practices that ultimately result in sustained competitive

advantage for the organization.” In our case, as we focus on innovative firms, their core

capabilities and competitive advantage are related to innovations. In other words, HRM

practices can (a) increase the value and uniqueness of the knowledge through internal

development and (b) influence employee behaviour in the desired direction, in this case,

to improve firm innovation. Lepak et al. (2006) argued that HRM practices directly

influence employees’ ability to perform by affecting their knowledge, skills and abilities.

The next step is to assess the extent to which HRM practices increase the value and

uniqueness of knowledge.

One way of obtaining valuable and unique knowledge is through a system of HRM

practices called knowledge-based practices, which enable the internal development of

human resources (Lepak & Snell, 2002). This system implies a specific orientation of

selection, training, development, appraisal and compensation practices. The aim of

selection is to attract the best people to the company, in terms of their inherent potential

11

(Doorewaard & Meihuizen, 2000; Huselid, 1995). Informal contacts that favor

socialising among the workforce are encouraged (Arthur, 1994), and advantageous

conditions are offered in terms of firm-specific training and career development within

the company (Lepak & Snell, 1999). Individuals receive feedback concerning what they

do and how performance can be improved, thus promoting autonomy. It is also

convenient to make use of incentives as a form of reward (Huselid, 1995).

This model of HRM practices enables valuable and firm-specific knowledge to be

generated by means of internal development. In addition, developing HRM practices

internally helps firms to obtain the benefits of employees in terms of their value-creating

potential and firm-specific human capital (Lepak & Snell, 1999; 2002; Youndt et al.,

2004; Youndt et al., 1996). All the above are HRM practices that have been shown by

previous authors to motivate employees to develop opportunities and improve their

personal stocks of knowledge and skills (Lepak et al., 2006; Snell & Dean, 1994; Ulrich

& Lake, 1991). Thus, we try to confirm the Lepak and Snell (2002) proposition by

means of our third hypothesis.

H3a. Knowledge-based HRM practices are positively associated with the value of

knowledge.

H3b. Knowledge-based HRM practices are positively associated with the uniqueness of

knowledge.

There is another system of HRM practices, named collaborative or partnership/alliances

(Lepak & Snell, 1999; 2002), in which the HRM practices have a group orientation,

different from the orientation of the knowledge-based practices studied above. The

literature also stresses the importance of working in groups or teams to enhance the

12

uniqueness of the knowledge possessed by the members of these groups (Nonaka &

Takeuchi, 1995; Lepak & Snell, 1999; 2002). In the collaborative system, skills for

teamwork are necessary to pass any selection procedure, and such skills are the objective

of training initiatives. In addition, evaluation and remuneration processes always comply

with group criteria (Helleloid & Simonin, 1994; Lepak & Snell, 1999). Therefore, a

teamwork design is critical for disseminating specialised knowledge throughout the

organisation.

These collaborative HRM practices have been found to be an efficient means of

increasing the uniqueness of knowledge (Lepak & Snell, 1999; 2002). Communication

mechanisms, exchange programs, group-based rewards, appraisals and the like may be

established to facilitate information sharing and to equip the members of these groups

with knowledge that is very firm specific (Lepak et al., 2003). The fourth hypothesis is

as follows.

H4. Collaborative HRM practices are positively associated with the uniqueness of the

knowledge.

The above arguments suggest two critical points for this research. Firstly, HRM

practices may facilitate valuable and unique knowledge. Secondly, valuable and unique

knowledge may mediate the relationship between HRM practices and innovative

capability. Therefore, in order to close the cycle, we explore the possibility of a direct

impact of HRM practices on product innovation, independently of the characteristics of

employees’ knowledge.

As we pointed out before, Paauwe & Boselie (2005) suggested that one way that HRM

practices can generate core capabilities is by influencing employee behaviour in the

13

desired strategic direction. According to this reasoning, any firm may adopt concrete

HRM practices in the areas of job design, training, development and/or appraisal

compensation to improve the firm’s innovation.

Regarding job design, in cases where jobs are broadly defined and discretion and self-

direction are allowed, employees are able to find new solutions to problems and

opportunities that arise in the workplace (Kang et al., 2007; Lepak & Snell, 1999). It is

also claimed that empowerment practices increase the level of decentralisation, and such

an environment may better allow new solutions to be found at the shop-floor level

(Laursen, 2002). In other words, increased delegation may better facilitate the discovery

of new design and products that top levels were unable to see before (Drucker, 1999).

Firm-specific training is necessary because it improves technical abilities to solve

problems (Barton & Delbridge, 2001; Beatty & Schneier, 1997; Gupta & Singhal, 1993;

Laursen & Foss, 2003). Training activities must be reorganised by the firm in ways that

generate new understandings and new ideas. Thus, training in core skills is useful for

product innovation (Mumford, 2000).

Another practice that is strongly recommended entails employee development. It

maximises employees’ commitment to innovation and their potential to learn (Mak &

Akhar, 2003; Schuler & Jackson, 1987). Employee development includes HRM

practices such as career management, mentoring, and coaching. Employees should be

provided with guidance in establishing career paths that help them experience various

job opportunities beyond the boundaries of a single expertise in order to innovate (Kang

et al., 2007). In addition, to promote the growth of requisite skills, the organisation must

establish and manage effective mentoring relationships for new employees (Mumford,

14

2000). In addition, managers should provide coaching and feedback to overcome

performance problems (London & Smither, 1999). This is an effective way to foster

ongoing knowledge development and assessment of new solutions (Zhou, 1998).

Compensation practices must also include incentives in order to reward the search for

new solutions (Balkin & Montemayor, 2000; London & Smither, 1999; Mumford,

2000). As the behaviours required for innovating are difficult to identify a priori (Adler

& Kwon, 2002), result- or output-based incentives are more useful in managing and

rewarding joint contributions (Snell & Dean, 1994). In addition, incentives need to be

accompanied by the acquisition of knowledge or new ideas; for example, by paying for

knowledge or reputation, which may motivate employees to develop innovations

continuously.

In summary, all these HRM practices can be included in the knowledge-based system,

and they positively affect firm innovation. As a result, we may formulate the fifth

hypothesis as follows.

H5. Knowledge-based HRM practices are positively associated with innovation.

One of the organisational variables traditionally related to innovation is the use of work

teams. The basic argument is simple: innovation normally commences in the mind of a

creative individual, and that initial idea is analysed and developed collectively in a work

team (Tang, 1998). Furthermore, such groups are considered a powerful means of

creating and circulating innovative ideas (Denison et al., 1996; Griffin, 1997). Work

groups represent one of the most important recent trends in organisational design and are

considered a key element in the creation and improvement of products and services

(Donnellon, 1996; Jackson, 1992; Thompson, 2003).

15

From the list of HRM practices that could be considered with a team orientation, we

focus on selection of individuals according to their group competences, training

activities explaining how to work in teams, and team-based appraisals and compensation

practices (collaborative HRM practices). Team design requires reciprocal

interdependence among employees who work together and seek new solutions to

existing problems (Kang et al., 2007). As a consequence of designing jobs around work

groups, the organisation must value a candidate’s capacity for working in a team during

the staffing process (Lepak & Snell, 1999). Another option, also included in the

collaborative model, is training individuals with the object of developing interpersonal

skills. This type of training has a positive effect on innovation because it facilitates

interaction of the employee with colleagues and encourages the flow of new ideas and

perspectives within work groups (Lepak et al., 2003; Ulrich, 1998).

Regarding team-based appraisals and compensation practices, they are known to have a

powerful motivating role on the innovation behaviour of individuals (Eisenberger &

Armeli, 1997; Kunkel, 1997). Thus, Barczak & Wilemon (2003) demonstrated that

members of work teams have a strong interest in being remunerated as a function of the

results generated by their innovation activity. In this context, Balkin et al., (2000)

empirically demonstrated a positive relationship between long-term incentives and

innovation in companies.

In conclusion, because we consider these HRM practices to be collaborative practices

and they are related to innovations, the sixth hypothesis can be formulated as follows.

H6. Collaborative HRM practices are positively associated with innovation.

16

FROM PRODUCT INNOVATION TO HIGHER PERFORMANCE

The final stage of our discussion is to learn whether those firms with the appropriate

stocks of knowledge and HRM practices obtain not only innovations but also the best

performance in the market. According to the literature, innovation is one of the main

sources of competitive advantages (Li & Atuahene-Gima, 2001). From an RBV

perspective, if a company develops innovations based on valuable, rare, inimitable and

non-substitutable resources such as value and unique knowledge, they will lead to higher

levels of competitive advantages (Barney, 1991). Firms that offer products that are

adapted to the needs and wants of target customers and that market them faster and more

efficiently than their competitors are in a better position to obtain higher performances

and create sustainable competitive advantages (Alegre et al., 2006; Nonaka & Takeuchi,

1995; Prahalad & Hamel, 1990). Furthermore, given that organisational capabilities such

as innovative capability can be seen as a “proxy” of competitive advantages (López-

Cabrales et al., 2006), there is a very close link between innovative activity, competitive

advantages and performance.

It has been proposed that the development of an innovation contributes to the

performance of a company (Capon et al., 1992; Damanpour, 1991; Pérez-Luño et al.,

2007). That is, innovators have the potential to create markets, shape customer

preferences, and even change the basic behaviour of consumers (Zhou, 2006), which in

summary leads to higher profits. From the above, we argue that innovative activity

represents an important capability that enhances the company’s performance. These

assumptions lead us to establish our last hypothesis.

H7. Innovation is positively associated with a higher level of performance.

17

Figure 3 summarises the main relationships and hypotheses outlined in this paper.

------------------------------------------

Insert Figure 3 about here

------------------------------------------

METHODOLOGY

RESEARCH DESIGN AND SAMPLE

In order to examine the innovative capability of R&D departments, we needed a sample

of firms that were actually involved in these activities to some extent. We therefore

started out with a sampling frame covering the most innovative companies in Spain.

There were two criteria for the selection of the population: presence in innovative

industries and a minimum number of employees. The industries with the most patents,

according to data of the Spanish Office of Patents, are the following: manufacture of

machinery, manufacture of motor vehicles, manufacture of radios, TV and

telecommunications equipment, and the chemical industry. The 2004 edition of the Duns

50,000 database was used to obtain a list of the companies in those industries with more

than 50 employees. By this procedure, a total valid population of 619 companies was

obtained. To obtain the best information about the companies’ innovative activities, we

used the R&D departments of such firms as our unit of analysis.

The methodology of contacting, then mailing the questionnaire and following up, as

proposed in the literature, was adopted (Dillman, 1991). We identified the R&D

departments of the companies in our population, and the manager responsible for this

unit was telephoned. In these phone calls, we explained the study, requested

18

collaboration, and discussed the mailing of the questionnaire. Over six months,

periodical reminders were sent to those participating companies that had not returned the

questionnaire. In total, 88 firms responded to this questionnaire, from which 86 were

considered valid. This corresponds to a response rate of 14% of the firms in our target

population. To check for non-response bias, we compared the respondents with the non-

respondents, via mean difference, based on their general features (industry membership,

number of employees, and revenue), which were available in the DUNS 50,000

database. This test showed no significant differences between the two groups

(respondents vs. non-respondents)

MEASURES

As we mentioned in the previous section, the instrument used to collect the required

information was a questionnaire with over 40 items, intended to obtain information

about the R&D department of the companies in our population. Responses for the

different items were obtained using a seven-point Likert scale except for performance,

for which we used objective data, and the size and R&D expenditures, for which we

used direct questions. To assess content validity, after a thorough review of the

literature, a panel of 12 academic experts was formed. Once their suggestions were

incorporated into the questionnaire, it was sent to the R&D manager of each company.

Dependent variables

Firm performance may be assessed in terms of how effectively the firm functions in

achieving a variety of financial benchmarks (an objective measure), or by the firm’s

position on various indicators of effectiveness and success relative to competitors’

19

ratings for these indicators (a subjective measure). In our case, we used the objective

measure to reduce the common method variance error. That is, we use the ratio of total

revenues divided by total assets as an objective measure of profits.

After conducting a full literature review of the scales used to measure the product

innovative activity of an organisation (Avlonitis et al., 2001; OECD/Eurostat, 1997), and

based on the recommendations put forward by Churchill (1979), a scale of measurement

was devised with eight items, of which the last two constitute a direct measure for

determining the convergent validity of the scale (see Table 1).

The measure of valuable and unique knowledge was adapted from the work of Lepak &

Snell (2002). Following the recommendations of our 12 academic experts and keeping

the content validity conditions, we used a scale of nine items from the 22 proposed by

the original authors. The first five items measure valuable knowledge while the

remaining four items measure unique knowledge (see Table 1).

Independent variables

The measures of HRM practices were adapted from those developed by Lepak & Snell

(2002) in their analysis of human capital architecture (1999; 2002). The items

specifically utilised were those forming their knowledge-based employment system and

their collaborative system with respect to group work. The reason for using such items is

that both models include HRM practices that have been shown in the literature to be

generators of an innovative behaviour and closely linked to the value and uniqueness of

human capital.

20

Control variables

We use size and internal and external R&D expenditures as control variables. The

reasons for choosing such variables are explained next.

Research has demonstrated that a company’s size may be linked to a greater or lesser

tendency for innovation (Bantel & Jackson, 1989). Some scholars have established that

an increase in the size of the organisation implies a higher number of resources and

higher innovative potential, while other scholars argued that small organisations can be

more innovative because they have more flexibility, a higher ability to adapt and less

difficulty in accepting and implementing changes (Damanpour, 1991). Following these

arguments, we assume that the firm’s size has an influence on the innovative activity of

organisations. The organisation size variable was measured by the number of employees

in the firm. The value of this variable ranges from 50 to 5,000 workers. Because of its

wide dispersion, a Napierian logarithm of the number of workers in the firm has been

used to estimate it, in order to avoid the scale effect.

Following several authors (Bierly & Chakrabarti, 1996; Cohen & Levinthal, 1990), we

decided to include internal and external R&D expenditures as control variables in our

study. These variables were measured by two items, in which the respondents were

asked for information on the internal and external expenditure on R&D as average

percentages of the sales turnover of the company for the previous three years.

ANALYSES AND RESULTS

The hypotheses were tested using the structural equation modelling method. We

followed the two-stage procedure recommended by Anderson & Gerbing (1988). In the

first stage, after conducting exploratory factor analysis (EFA), we estimated the

21

measurement model using confirmatory factor analysis (CFA) in order to test the

goodness of fit of the measurement scales (Anderson & Gerbing, 1988; Fornell &

Larcker, 1981). CFA has been used to test the psychometric properties of measurement

scales in a number of studies (Alegre et al., 2006; Gerbing & Anderson, 1988) and is

recommended by Montoya-Weiss & Calantone (1994) in order to assess the construct

validity and reliability of subjective measurement instruments. The purpose of CFA was

also to test the unidimensionality of multi-item constructs and to eliminate unreliable

items. Items that loaded on multiple constructs and had low item-to-construct loadings

were deleted. The individual measurement items for the study’s dependent, independent,

and control variables are listed in Table 1.

------------------------------------------

Insert Table 1 about here

------------------------------------------

The results presented in Table 1 were obtained as follows. We began by analysing the

establishment of scale dimensionality by checking the factorial structure of each of the

concepts we wanted to measure. We then tested the scale reliability. To do so, we

assessed both the individual reliability of each indicator (R² > 0.5) and the composite

reliability of each factor (CR > 0.7). Finally we analysed the scale validity by focusing

on content validity, convergent validity, and discriminant validity. As we explained

above, we reviewed previous literature in depth and used 12 experts to ensure content

validity. Convergent validity is accepted when factorial loads are higher than 0.4 and t

coefficients are significant. We also took into account the fact that the CFI, robust CFI,

22

GFI and AGFI statistics were above 0.9, the p-value for the Satorra–Bentler χ² was not

significant (p > 0.05) and the robust RMSEA was significant (RMSEA < 0.05). With

exception of the AGFI, which is sensitive to sample size and GFI, all fit indices had

optimum values. We could therefore assume that our measurement scales had

convergent validity (Hair et al., 1999) and that the goodness-of-fit of our causal

approach was acceptable (Bagozzi, 1994; Bakker et al., 2004). Following Fornell and

Larcker, we also demonstrated discriminant validity given that the average variance

extracted (AVE) of the constructs is higher than their squared multiple correlations with

the rest of the constructs (see Table 2).

------------------------------------------

Insert Table 2 about here

------------------------------------------

The scale developed to measure innovative activity was devised with eight items.

However, after conducting CFA, we were forced to eliminate three of the items because

their standardised loadings were too low. These eliminations did not harm the content

validity of the scale. Our CFA achieved a five-item solution for the valuable knowledge

scale, as was proposed, and a three-item solution for unique knowledge. That is, we had

to eliminate one of the proposed items of the unique knowledge scale because its

standardised loadings were too low. Finally, our measurement of HRM practices

comprised two different factors, one being the HRM practices of the knowledge-based

system, corresponding to the indicators HRK1 to HRK12, and the other being the

practices of the collaborative system, indicators HRC1 to HRC9, as established by the

23

measurement proposed by Lepak and Snell (2002). However, after conducting CFA, our

results provided a five-item scale for measuring knowledge-based HRM practices. The

items remaining included internal promotions, tutoring and mentoring activities,

socialisation programs, and performance appraisals. After conducting CFA,

collaborative HRM practices were measured with a four-item scale, through selection

processes based on interpersonal abilities, training focus on team building, and

appraisals based on team performance and/or employees’ ability to work in groups. It

should be mentioned that the original study was devised with the organisation as the unit

of analysis, while our study takes as its unit of analysis the R&D department. This

difference in the unit of analysis could be a reason for the differences between Lepak

and Snell’s (2002) results and ours.

The two-stage procedure recommended by Anderson & Gerbing (1988) identified the

structural model that best fitted the data and tested the hypothesised relationships

between the constructs. As shown in Table 3, we used two structural models to test the

hypothesised relationships between the constructs. In Model 1, we presented all the

possible equations. In the adjusted Model 1, we only employed the equations that best

match the data.

------------------------------------------

Insert Table 3 about here

------------------------------------------

With respect to hypotheses 1 and 2, in which we related valuable and unique knowledge

with higher innovative activity, it has to be mentioned that only unique knowledge

24

positively and significantly influences innovative behaviour (t value, 2.181), supporting

hypothesis two. In hypothesis 3, we proposed that knowledge-based HRM practices

would positively influence valuable and unique knowledge. In this case, we only found

partial support, because such practices only influence the value of knowledge (t value,

3.531). On the other hand, we found support for hypothesis 4. That is, collaborative

HRM practices significantly and positively influence unique knowledge (t value, 1.648),

although the significance is only at p ≤ 10%. In addition, we did not find support for

hypotheses 5 and 6. That is, none of the HRM practices directly influences innovative

activity.

Lastly, as we can see in Model 1 Adjusted, innovative activity has a significant positive

influence on the company’s profits (t value, 2.638). This result supports our hypothesis

7. The only significant control variable is external R&D expenditures. Such R&D

expenditures have a negative influence on the innovative activity (t value, –8.333) and a

positive influence on the company’s performance (t value, 3.212).

CONCLUSIONS

Although innovation has attracted substantial attention in the literature, only a few

studies have analysed how employees’ knowledge and HRM practices can, on the

whole, enhance the innovative activity of organisations. Therefore, this paper contributes

to the literature by theoretically and empirically investigating such relationships.

Our analyses showed that neither of the two systems of HRM practices (knowledge-

based and collaborative) had a significant direct effect on innovative activity.

Nevertheless, when we analysed the relationships of HRM practices through employees’

knowledge, then some significant effects on innovative activity appeared. Thus,

25

although knowledge-based HRM practices contribute to the value of knowledge, this

characteristic of knowledge had no impact on innovation. On the other hand,

collaborative HRM practices increase the uniqueness of knowledge, and this firm-

specific knowledge is positive and significantly associated with innovative activity. As a

result, it can be said that the contribution of collaborative HRM practices to innovative

capability is mediated by the uniqueness of knowledge.

For scholars researching the RBV, this finding is consistent with the literature

confirming that with the appropriate management of a key resource (unique knowledge),

firms enhance their innovative capability, and by extension their competitive advantage

and performance (Barney, 1991; 1995; Lengnick-Hall and Lengnick-Hall, 2002; López-

Cabrales et al., 2006; Pérez-Luño et al., 2007). Furthermore, in a similar manner to that

proposed by Barney & Wright (1998), the firm must also have an appropriate

managerial strategy to take advantage of these resources, as collaborative HRM

practices do in our study. Our results also confirm the thesis that HRM practices are

facilitators of knowledge. Specifically, HRM practices based on knowledge are very

important for the procurement of valuable knowledge, while collaborative HRM

practices influence unique knowledge. This result is interesting because it confirms that

there is no “universalistic HRM model” for improving both the value and the uniqueness

of knowledge. Each of the two knowledge characteristics is associated with a different

and specific design of HRM practices.

With respect to the control variables, only external R&D expenditures have a significant

effect on our dependent variables. These expenditures have a double and opposite

influence. That is, they significantly and negatively affect innovative activity, and

26

significantly and positively influence performance. These findings are not surprising if

we consider that to be innovative, a company should be able to develop new products or

services by itself, departing from the internal development of new ideas (for example:

those from their R&D department, etc.). For this reason, we consider it appropriate that

these external expenditures harm such innovative behaviour because they are a way of

externalising the innovative activity. However, it is presumably expensive to develop

internal ideas. Therefore, the positive influence of external R&D expenditures on

performance can be an indication of the utility, in terms of efficiency, of outsourcing

such expenses.

Finally, it is interesting to remember that our study was focused and conducted on R&D

units. According to our results, unique knowledge from these employees is the most

outstanding resource for innovation. On the other hand, we found that certain

knowledge-based and collaborative HRM practices are not relevant in such contexts

(such as empowerment, participation in decision-making processes or job rotations), as

they were eliminated from the original HRM practice measurement scales.

These results also have practical implications. Firstly, the type of knowledge possessed

by employees in R&D departments is a key factor for product innovation. Managers

interested in developing innovations must identify and procure employees with unique

and firm-specific knowledge that is hard to copy, and determine its competitive

advantage. Secondly, managers must manage these employees by means of collaborative

HRM practices such as selection processes based on interpersonal abilities, training

activities focused on team building, and appraisals based on team performance and/or

employees’ ability to work in groups. These practices drive the skills and attitudes that

27

allow the interactions among employees and knowledge sharing that are necessary for

product innovation. Thirdly, with respect to the positive relation of external R&D

expenses with performance and the negative one with innovative activity, we propose

that companies should balance their R&D expenditures to take advantage of their effects

on performance but should not forget their damage to innovative behaviour. Finally, it is

very important to recall that we found a positive relation between innovative capability

and performance. While this finding is useful for academics analysing the role of

organisational capabilities on performance, it is even more important in its practical

implications. That is, supporting the view that investing in innovation is profitable can

motivate managers to devote resources to this activity.

Despite the above-cited contributions, this study does have certain limitations. Even

when we had enough data to conduct our research with sufficient robustness, the sample

size was not ideal to test relationships with structural equation modelling (Hair et al.,

1999) and did not allow for segmentation according to the industries considered in the

population. However, a certain homogeneity among firms exists because they were all

from innovative sectors according to the Spanish Office of Patents. Secondly, we

conducted a transactional study. In the future, it would be interesting to analyse data in a

longitudinal way to gather information about the different cycles that the innovative

activity requires. Finally, only one person in each firm, the manager responsible for the

R&D units, answered our questionnaire. Nevertheless, as we focused our research on

R&D units, the pre-test and expert panel conducted before sending the questionnaires

ensured that this manager is the person most qualified to assess the knowledge of his/her

28

employees and the HRM practices of the department. In addition, we used an objective

measure of profits to reduce common method variance error.

We also assumed that all hypotheses that were not supported could be considered

limitations but also future lines of research. For that reason, it could be interesting to

investigate thoroughly each of the relations that did not appear to be significant. It is also

important to analyse why valuable knowledge has no influence on innovative capability,

although such knowledge is considered relevant for sustaining human capital. Lastly,

although we focused on two groups of HRM practices, it would be interesting to

complete this analysis by including other groups of practices. It would also be

interesting to open a new line of research based on the findings about the usefulness of

investing in internal or external R&D expenditures, depending on the ultimate aim of the

companies (innovation or performance).

In conclusion, this study demonstrated the existence of two objectives that HR

management should pursue to achieve innovative capability. On the one hand,

management should incorporate HRM practices as selection processes based on

interpersonal abilities and training activities, and appraisals based on employees’ ability

to work in groups. On the other hand, organisations should bear in mind that the success

of these practices, in terms of innovation and performance, depends on the unique

knowledge of their employees.

REFERENCES

Adler, P. S. and Kwon, S. (2002). ‘Social capital: Prospects for a new concept’.

Academy of Management Review, 27: 17–40.

29

Alegre, J., Lapiedra, R. and Chiva, R. (2006). ‘A measurement scale for product

innovation performance’. European Journal of Innovation Management, 9, 333–

346.

Amar, A. D. (2002). Managing Knowledge Workers: Unleashing Innovation and

Productivity. Westport, CT: Quorum.

Amit, R., & Belcourt, M. (1999). Human resource management processes: A value

creating source of competitive advantage. European Management Journal, 17,

174–181.

Anand, N., Gardner, H. K., & Morris, T. (2007). Knowledge-based innovation:

Emergence and embedding of new practice areas in management consulting firms.

Academy of Management Journal, 50 (2), 406–428.

Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modelling in practice: A

review and recommended two-step approach. Psychological Bulletin, 103 (3),

411–423.

Argote, L., & Ingram, P. (2000). Knowledge transfer: A basis for competitive advantage

in firms. Organizational Behavior and Human Decision Processes, 82, 150–169.

Arthur, J. B. (1994). Effects of human resources systems on manufacturing performance

and turnover. Academy of Management Journal, 37 (3), 670–687.

Avlonitis, G. J., Papastathopoulou, P. G., & Gounaris, S. P. (2001). An empirically-

based typology of product innovativeness for new financial services: Success and

failure scenarios. The Journal of Product Innovation Management, 18 (5), 324–

342.

30

Bagozzi, R. P. (1994). Structural Equation Models in Marketing Research: Basic

Principles. In R.P. Bagozzi (Ed.). Principles of Marketing Research. Oxford,

England: Blackwell Publishers.

Bakker, A. B., Demerouti, E. and Verbeke, W. (2004) Using the job demands-resources

model to predict burnout and performance. Human Resource Management, 43 (1),

83–104.

Balkin, D., Markman, G. and Gomez-Mejia, L. (2000) Is CEO pay in high technology

firms related to innovation? Academy of Management Journal, 43, 1118–1129.

Balkin, D., & Montemayor, E. (2000). Explaining team-based pay: A contingency

perspective based on the organizational life cycle, team design and organizational

learning literatures. Human Resource Management Review, 10 (3), 249–269.

Bantel, K., & Jackson, S. E. (1989). Top management and innovations in banking: Does

the composition of the top team make a difference? Strategic Management Journal,

10 (Special Issue), 107–124.

Barney, J. B. (1991). Firm resources and sustained competitive advantage. Journal of

Management, 17 (1), 99–120.

Barney, J. B (1995). Looking inside for competitive advantage. Academy of

Management Executive, 9(4), 49–60.

Barney, J. B., & Wright, P. M. (1998). On becoming a strategic partner: The role of

human resources in gaining competitive advantage. Human Resource

Management, 37 (1), 31–46.

Barton, H., & Delbridge, R. (2001). Development in the learning factory: Training

human capital. Journal of European Industrial Training, 25, 465–472.

31

Barczak, G., & Wilemon, D. (2003). Team members’ experiences in new product

development, views from the trenches. R & D Management, 33, 463–479.

Beatty, R. W., & Schneier, C. E. (1997). New HR roles to impact organizational

performance: From partners to players. Human Resource Management, 36, 29–50.

Bierly, P., & Chakrabarti, A. (1996). Generic knowledge strategies in the U.S.

pharmaceutical industry. Strategic Management Journal, 17 (Winter Special

Issue), 123–135.

Boxall, P. (1996). The strategic HRM debate and the resource based view of the firm.

Human Resource Management Journal, 6 (3), 59–75.

Capon, N., Farley, J. U., Lehmann, D. R., & Hulbert, J. M. (1992). Profiles of product

innovators among large U.S. manufacturers. Management Science, 38, 157–169.

Cohen, W. M., & Levinthal, M. D. A. (1990). Absorptive capacity: A new perspective

on learning and innovation. Administrative Science Quarterly, 35 (1 Special Issue:

Technology, Organizations, and Innovation), 128–152.

Costa, P., & McCrae, R. (1992). Neo PI-R professional manual. Odessa, FL: Editorial

Psychological Assessment Resources.

Churchill, G. A. (1979). A paradigm for developing better measures of marketing

constructs. Journal of Marketing Research, 16 (1), 64–73.

Damanpour, F. (1991). Organizational innovation: A meta-analysis of effects of

determinants and moderators. Academy of Management Journal, 34 (3), 555–590.

Denison, D., Hart, S., & Kahn, J. (1996). From chimneys to cross-functional work

teams: Developing and validating a diagnostic model. Academy of Management

Journal, 39, 1005–1024.

32

Dillman, D. A. (1991). The design and administration of mail surveys. Annual Review

of Sociology, 17 (1), 225–249.

Donnellon, A. (1996) Cross-functional teams in product development: Accommodating

the structure to the process. Journal of Product Innovation Management, 10, 377–

392.

Doorewaard, H., & Meihuizen, H. (2000). Strategic performance options in professional

service organizations. Human Resource Management Journal, 10 (2), 39–57.

Drucker, P. (1999). Knowledge worker productivity, the biggest challenge. California

Management Review, 41, 79–94.

Eisenberger, R., & Armeli, S. (1997). Can salient rewards increase creative performance

without reducing intrinsic creative interest? Journal of Personality and Social

Psychology, 72, 652–663.

Fornell, C., & Larcker, D. F. (1981). Structural equation models with unobservable

variables and measurement error: Algebra and statistics. Journal of Marketing

Research, 18 (3), 7.

Foss, N. J. (2007). The emerging knowledge governance approach: Challenges and

characteristics. Organization, 14(1), 29–52.

Galunic, C., & Rodan, S. (1998). Resource recombinations in the firm: Knowledge

structures and the potential for Schumpeterian innovation. Strategic Management

Journal, 19 (12), 1193–1201.

Gerbing, D. W., & Anderson, J. C. (1988). An updated paradigm for scale development

incorporating unidimensionality and its assessment. Journal of Marketing

Research, 25 (2), 186–192.

33

Griffin, A. (1997). The effect of project and process characteristics on product

development cycle time. Journal of Marketing Research, 34, 24–35.

Gupta, A., & Singhal, A. (1993). Managing human resources for innovation and

creativity. Research Technology Management, 36 (3), 41–48.

Hair, J. F., Anderson, R. E., Tatham, R. L., & Black, W. C. (1999). Multivariate data

analysis. Englewood Cliffs: Prentice Hall.

Helleloid, D., & Simonin, B. (1994). Organizational learning and a firm’s core

competence. In G. Hamel & A. Heene (Eds.), Competence-based competition.

New York: Wiley.

Huselid, M. A. (1995). The impact of human resource management practices on

turnover, productivity and corporate financial performance. Academy of

Management Journal, 38, 635–672.

Jackson, S. (1992) Team composition in organizational settings: Issues in managing and

increasing diverse force group. In S. Worchel, W. Wood & J. Simpson (Eds.),

Group Processes and Productivity, Newbury Park: Sage.

James, W. (2002). Best HR Practices for Today’s Innovation Management. Research

Technology Management, 45 (1), 57–60.

Kang, S.-C., Morris, S. S., & Snell, S. A. (2007). Relational archetypes, organizational

learning, and value creation: Extending the human resource architecture. Academy

of Management Review, 32 (1), 236–256.

34

Kimberly, J. R., & Evanisko, M. J. (1981). Organizational Innovation: The influence of

individual, organizational, and contextual factors on Hospital Adoption of

Technological and Administrative Innovations. Academy of Management Journal,

24 (4), 689–713.

Kogut, B., & Zander, U. (1992). Knowledge of the firm, combinative capabilities, and

the replication of technology. Organization Science, 3 (3), Focused Issue:

Management of Technology, 383–397.

Kunkel, G. (1997). Rewarding product development success. Research Technology

Management, 40, 29–31.

Laursen, K. (2002). HRM Practices for Innovation Performance. International Journal of

the Economic Business, 9 (1), 139–166.

Laursen, K and N. Foss (2003), New HRM practices, complementarities and the impact

on innovation performance, Cambridge Journal of Economics 27: 243–63.

Lengnick-Hall M, & Lengnick-Hall, C (2002). Human Resource Management in the

Knowledge Economy: new challenges, new roles, new capabilities. BK Publishers.

San Francisco.

Lepak, D. P., Takeuchi, R., & Snell, S. A. (2003). Employment flexibility and firm

performance: Examining the interaction effects of employment mode,

environmental dynamism and technological intensity. Journal of Management, 29

(5), 681–703.

Lepak, D. P., & Snell, S. A. (2002). Examining the human resource architecture: The

relationships among human capital, employment and human resource

configuration. Journal of Management, 28, 517–543.

35

Lepak, D. P., & Snell, S. A. (1999). The human resource architecture: Toward a theory

of human capital allocation and development. Academy of Management Review,

24, 31–48.

Lepak, D., Liao, H., Chung, Y., & Harden, E. (2006). A conceptual review of human

resource management systems in strategic human resource management research.

Research in Personnel and Human Resources Management, 25, 217–271.

Li, H., & Atuahene-Gima, K. (2001). Product innovation strategy and the performance

of new technology ventures in China. Academy of Management Journal, 44 (6),

1123–1134.

London, M., & Smither, J. (1999): Empowered self development and continuous

learning. Human Resource Management 38 (1): 3–15.

López-Cabrales, A., Valle, R., & Herrero, I. (2006). Contribution of core employees to

organizational capabilities and efficiency. Human Resource Management, 45 (1),

81–100.

Mak, S., & Akhar, S. (2003). HRM practices, strategy orientations and company

performance: A correlation study of publicly listed companies. The Journal of

American Academy of Business, 2 (2), 510–515.

McEvily, S. K., & Chakravarthy, B. (2002). The persistence of knowledge-based

advantage: An empirical test for product performance and technological

knowledge Strategic Management Journal, 23 (4), 285–305.

Montoya-Weiss, M. M., & Calantone, R. (1994). Determinants of new product

performance: A review and meta-analysis. The Journal of Product Innovation

Management, 11 (5), 397–417.

36

Mumford, M. (2000). Managing creative people: Strategies and tactics for innovation.

Human Resource Management Review, 10 (3), 313–351.

Nahapiet, J., & Ghoshal, S. (1998). Social capital, intellectual capital, and the

organizational advantage. Academy of Management Review, 23, 242–266.

Newbert, S. L. (2007). Empirical research on the resource-based view of the firm: An

assessment and suggestions for future research. Strategic Management Journal, 28

(2), 121–135.

Nonaka, I., & Takeuchi, H. (1995). The knowledge creating company. Oxford: Oxford

University Press.

OECD/Eurostat. (1997). Proposed Guidelines for Collecting and Interpreting

Technological Innovation Data (Synthesis Report No. 2: Country Studies). Paris:

Organisation for Economic Co-operation and Development.

Paauwe, J., & Boselie, P. (2005). HRM and performance, what next? Human Resource

Management Journal, 15 (4), 68–83.

Peltokorpi, V., & Tsuyuki, E. (2006). Knowledge governance in a Japanese project-

based organization. Knowledge Management Research & Practice, 4(1), 36–45.

Pérez-Luño, A., Valle Cabrera, R., & Wiklund, J. (2007). Innovation and imitation as

sources of sustainable competitive advantage. Management Research, 5 (2), 67–

79.

Prahalad, C. K., & Hamel, G. (1990). The core competence of the corporation. Harvard

Business Review, 68 (3), 79–91.

Purcell, J. (1996). Best practice and best fit: Chimera or cul-de-sac? Human Resource

Management Journal, 9, 26–41.

37

Schuler, R., & Jackson, S. (1987). Linking competitive advantage with human resource

management practices. Academy of Management Executive, 1, 207–219.

Schultz, T. W. (1961). Investment in human capital. American Economic Review, 51, 1–

17.

Snell, S., & Dean, J. (1994). Strategic compensation for integrated manufacturing: The

moderating effects of jobs and organizational inertia. Academy of Management

Journal, 37, 1109–1140.

Snell, S., Lepak, D., & Youndt, M. (1999). Managing the architecture of intellectual

capital: implications for Strategic Human Resource Management. Research in

Personnel and Human Resource Management. Supplement 4. 175–193

Subramaniam, M., & Youndt, M. A. (2005). The influence of intellectual capital on the

types of innovative capabilities. Academy of Management Journal, 48 (3), 450–

463.

Taggar, S. (2002). Individual creativity and group ability to utilize individual creative

resources: A multilevel model. Academy of Management Journal, 45 (2), 315–

330.

Tang, H. K. (1998). An integrative model of innovation in organizations. Technovation,

18 (5), 297–309.

Teece, D. J., Pisano, G., & Shuen, A. (1997). Dynamic capabilities and strategic

management. Strategic Management Journal, 18 (7), 509–533.

Thompson, L. (2003) Improving the creativity of organizational work groups. Academy

of Management Executive, 17, 96–111.

38

Ulrich, D. (1998). Intellectual capital = competence × commitment. Sloan Management

Review, 39 (2), 15–26.

Ulrich, D., & Lake, D. (1991). Organizational capability: Creating a competitive

advantage. Academy of Management Executive, 5, 77–92.

Wernerfelt, B. (1984). A resource-based view of the firm. Strategic Management

Journal, 5, 171–180.

Wiklund, J., & Shepherd, D. (2003). Knowledge-based resources, entrepreneurial

orientation, and the performance of small and medium-sized businesses. Strategic

Management Journal, 24 (13), 1307–1314.

Youndt, M., Snell, S., Dean, J., & Lepak, D. (1996). Human resource management,

manufacturing strategy and firm performance. Academy of Management Journal,

39 (4), 836–866.

Youndt, M. A., Subramaniam, M., & Snell, S. A. (2004). Intellectual capital profiles: An

examination of investments and returns. Journal of Management Studies, 41, 335–

362.

Zhou, J (1998): Feedback valence, feedback style, task autonomy, and achievement

orientation: Interactive effects on creative performance. Journal of Applied

Psychology, 83(2): 261–276.

Zhou, K. Z. (2006). Innovation, imitation, and new product performance: The case of

China. Industrial Marketing Management, 35, 394–402.

39

TABLES AND FIGURES

FIGURE 1: Knowledge and innovative activity relationship

Performance

Knowledge based

HRM Practices

Collaborative

HRM Practices

Product Innovative Activity

Valuable Knowledge

Unique Knowledge

Performance

Knowledge based

HRM Practices

Collaborative

HRM Practices

Knowledge based

HRM Practices

Collaborative

HRM Practices

Product Innovative Activity

Valuable Knowledge

Unique Knowledge

Product Innovative Activity

Valuable Knowledge

Unique Knowledge

Valuable Knowledge

Unique Knowledge

40

FIGURE 2: From HRM practices to innovative activity, using knowledge as a

mediator

Performance

Knowledge basedHRM Practices

Collaborative HRM Practices

Product Innovative Activity

Valuable Knowledge

Unique Knowledge

Performance

Knowledge basedHRM Practices

Collaborative HRM Practices

Knowledge basedHRM Practices

Collaborative HRM Practices

Product Innovative Activity

Valuable Knowledge

Unique Knowledge

Product Innovative Activity

Valuable Knowledge

Unique Knowledge

Valuable Knowledge

Unique Knowledge

41

FIGURE 3: Model of theoretical relationships

Performance

Knowledge based

HRM Practices

Collaborative

HRM Practices

Innovative

Activity

Valuable

Knowledge

Unique

Knowledge

H7

H3a

H4

H3b

H5

H6

H1

H2

Performance

Knowledge based

HRM Practices

Collaborative

HRM Practices

Knowledge based

HRM Practices

Collaborative

HRM Practices

Innovative

Activity

Valuable

Knowledge

Unique

Knowledge

Innovative

Activity

Valuable

Knowledge

Unique

Knowledge

Valuable

Knowledge

Unique

Knowledge

H7

H3a

H4

H3b

H5

H6

H1

H2

H5

H6

H5

H6

H1

H2

H1

H2

42

TABLE 1: Measurement model

Performance

Total sales divided by total assets

F1: Product innovative activity (CR 082.) I1. Market introduction of technologically new products developed by the company (totally or in part).

I2. Market introduction of technologically improved products developed by the company (totally or in

part).

(I3) Extensions of existing product lines (that do not only entail changes to aesthetic aspects).

(I4) Changes introduced to existing products, entailing significant improvements.

I5. Development of new lines/ranges of products.

I6. Frequency of replacement of old products by others with important changes.

(I7) Proportion of technologically new or improved products in the turnover of the company.

I8. Product innovation performed by the company.

F2: Value (Lepak & Snell, 2002) (CR 0.92) V1. Employees have skills that contribute to development of new market/product/services/opportunities.

V2. Employees have skills that create customer value.

V3. Employees have skills that are instrumental in creating innovations.

V4. Employees have skills that are needed to maintain high-quality products/services.

V5. Employees have skills that enable our firm to provide exceptional customer value.

F3: Uniqueness (Lepak & Snell, 2002) (CR 0.80) U1. Employees have skills that are not available to our competitors.

(U2) Employees have skills that are developed through on-the-job experiences.

U3. Employees have skills that are difficult for our competitors to buy away from us.

U4. Employees have skills that are difficult for our competitors to imitate or duplicate.

F4: Knowledge HRMP (Lepak & Snell, 2002) (CR 0.95) (HRK1) Employees perform jobs that have a high degree of job security.

(HRK2) Employees perform jobs that empower them to make decisions.

(HRK3) Employees participate in the decision-making process.

(HRK4) Selection process focuses on selecting the best all-round candidate.

(HRK5) Selection process places priority on employee potential to learn.

(HRK6) Training activities strive to develop firm-specific skills/knowledge.

HRK7. Firm emphasises promotion from within.

HRK8. Firm emphasises tutoring and mentoring activities.

HRK9. Firm possesses a socialisation program for newcomers.

HRK10. Performance appraisals include developmental feedback.

HRK11. Performance appraisals emphasise employee learning.

(HRK12) Compensation/rewards provide incentives for new ideas.

F5: Collaborative HRMP (Lepak & Snell, 2002) (CR 0.91) (HRC1) Employees perform jobs that require them to participate in cross-functional teams and networks.

(HRC2) Employees perform jobs that involve job rotations.

(HRC3) Selection process assesses industry knowledge and experience.

HRC4. Selection process assesses the ability to collaborate and work in a team.

HRC5. Training activities focus on team building and interpersonal relations.

HRC6. Appraisals are based on team performance.

HRC7. Appraisals focus on employees’ ability to work with others.

(HRC8) Compensation/rewards place a premium on employee’s industry experience.

(HRC9) Compensation/rewards have a group-based incentive.

Internal R&D Internal expenditure on R&D as average % of the sales turnover of the company for the previous three

years

External R&D External expenditure on R&D as average % of the sales turnover of the company for the previous three

years

43

Size LN. Workers

Note: CR = Composite reliability (analogous to Cronbach’s alpha); () = Eliminated items appear in bold in

brackets

44

TABLE 2: Squared correlation matrix

F1 F2 F3 F4 F5 F1: Product innovative

activity 0.50

F2: Value 0.005 0.56

F3: Uniqueness 0.062 0.012 0.59

F4: Knowledge HRMP 0.003 0.217 0.002 0.67

F5: Collaborative HRMP 0.031 0.212 0.022 0.393 0.56 CR 0.82 0.92 0.80 0.95 0.91 Significant at p < 0.05; AVE is represented in the principal diagonal; CR is composite reliability

45

TABLE 3: Estimated coefficients and model fit indices

Latent factors

Dependent variables Independent variables Model 1

Coeff1a(t value) Model 1*

Coeff1a*(t value) Product innovative activity 0.191 (2.285) 0.173 (2.638)

Value 0.022 (0.234) –

Uniqueness –0.056 (–0.598) –

Knowledge HRM practices 0.036 (0.218) –

Collaborative HRM practices –0.055 (–0.268) –

Size –0.046 (–0.838) –

Internal R&D expenditures –0.017 (–1.016) –

Performance

External R&D expenditures 0.023 (3.810) 0.020 (3.212)

Value 0.199 (1.201) –

Uniqueness 0.385 (1.904) 0.379 (2.181)

Knowledge HRM practices –0.604 (–1.450) –

Collaborative HRM practices 0.801 (1.492) –

Size –0.185 (–1.514) –

Internal R&D expenditures 0.027 (0.817) –

Product innovative

activity

External R&D expenditures –0.060 (–1.538) –0.061 (–8.333)

Knowledge HRM practices 0.276 (1.069) 0.331 (3.531)

Collaborative HRM practices 0.148 (0.438) –

Size 0.040 (0.525) –

Internal R&D expenditures –0.001 (–0.026) –

Value

External R&D expenditures –0.007 (–1.538) –

Knowledge HRM practices –0.182 (–0.705) –

Collaborative HRM practices 0.276 (0.822) 0.183 (1.648)

Size 0.044 (0.640) –

Internal R&D expenditures 0.021 (0.818) –

Uniqueness

External R&D expenditures 0.011 (1.572) –

Overall fit index Model 1 Model 1* χ² (df) 399.632 (276) 255.055 (248)

p value 0.00000 0.36553

Satorra–Bentler χ² 368.1039 255.4539

p value 0.00017 0.35895

GFI 0.755 0.824

AGFI 0.689 0.770

CFI 0.870 0.993

Robust CFI 0.862 0.989

RMSEA (90% CI) 0.072 (0.055, 0.086) 0.018 (0.000, 0.047)

Robust RMSEA (90% CI) 0.062 (0.044, 0.078) 0.019 (0.000, 0.048)

coeff1a = Model 1 parameters; * = adjusted

If t value > 1.64 relation is significant at 10%; if t value > 1.96 relation is significant at 5%; if t value >

2.576 relation is significant at 1%

46

ALVARO LOPEZ-CABRALES, Ph.D is an Assistant Professor of Human Resource

Management in the Business Administration Department, Universidad Pablo de Olavide

(Seville, Spain), where he obtained his Ph.D in 2003. His current research focuses on

human capital, employment relationships, organizational capabilities and innovation,

working on several research projects and publishing his research in several Spanish and

international journals. He teaches human resource management courses to

undergraduate, MBA and Ph.D students

ANA PEREZ-LUÑO, Ph.D, is an Assistant Professor of Management in the Business

Administration Department, Universidad Pablo de Olavide (Seville, Spain), where she

obtained her PhD in 2007. Her current research focuses on innovation, knowledge,

competitiveness and resource based theory. She is working on several research projects,

publishing her research in several Spanish and international journals. She teaches

Organization Theory and Business Administration to undergraduate, and

Entrepreneurship and Innovation to MBA and Ph.D students.

RAMON VALLE is a Professor of Human Resource Management in the Business

Administration Department, Universidad Pablo de Olavide (Seville, Spain). He got his

Ph. D at the Universidad de Sevilla in 1983. His teaching and research interests focus on

strategic human resource management and innovation. He is heading several research

projects on innovation, organizational capital and employment relationships and is co-

author of several HRM text books and papers in international journals.