1 indian sugar challenges and options sugar summit – pune - 2015

TRANSCRIPT

1

Indian Sugar challenges and optionsSugar Summit – Pune - 2015

2

Causes of the infamous Indian Sugar cycle

Increase in Sugarcane Area

Higher Sugar Production

Decline in Sugar Prices

High Cane Price Arrears

Decline in Sugarcane Area

Lower Sugar Production

Increase in Sugar Price

Improved Profitability

Sugar Production cycle is no more !

3

Why has the cycle broken?

4

2004-052005-06

2006-072007-08

2008-092009-10

2010-112011-12

2012-132013-14

0.0

5.0

10.0

15.0

20.0

25.0

30.0

60.0%

65.0%

70.0%

75.0%

80.0%

85.0%

90.0%

India Sugar production (mmt) LHS Cane price as % of Sugar Price

Mills cane price and Revenue sharing

MILLS HAD ACTUALLY PERFOMED VERY WELL!!

Rangarajan Committee suggests to pay 70:30 ratio to farmers but mills have actually paid more !!

mm

t

5

India : Long-term outlook

India to remain a flat tire but a perpetual importer

Weather to drive Ethanol to resolve surplus Cane Price rationalization Future sugar realization Refineries to be a weapon

6

Are we repeating the history?

• IN 2006/07 and 2007/08 the production was surplus over consumption and closing stocks at 11 mmt

• 2014/15 closing stocks are estimated close to 10 mmt and the prices depressed with surplus production next year and hence only export seems to resolve the problem

• Continuation of raw sugar export subsidy is very important.

7

mm

tWhere does Surplus sit in India

Nov-12

Dec-12

Jan-1

3

Feb-13

Mar-1

3

Apr-13

May-

13

Jun-1

3

Jul-1

3

Aug-13

Sep-13

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

1.3 1.63.8

6.2

8.0

8.98.2 7.1

5.94.8

3.7

Land Locked UPCoastal states for exports (MH, KNK, TN & GJ)Land locked states other than UP

Available for exports

Available for exports

Source: ED&F Man research

Currently approximate position

8

Import parity and cost vs what domestic trades

1. Import parity has been negative basis various duty regimes

2. Domestic market has always traded at export parity than trading at import parity

9

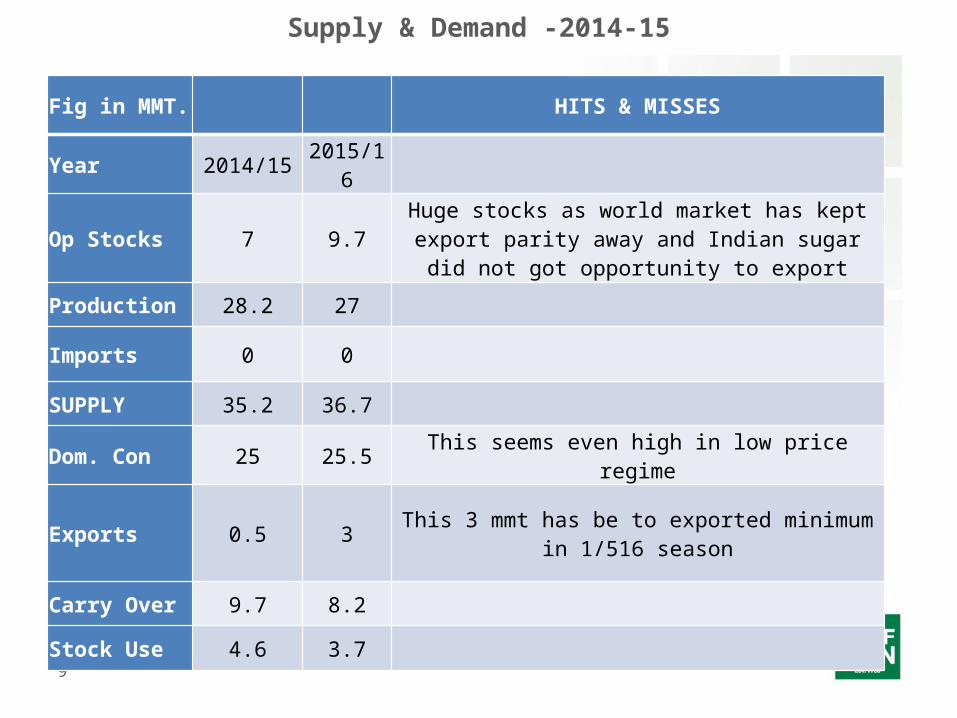

Supply & Demand -2014-15

Fig in MMT. HITS & MISSES

Year 2014/15 2015/16

Op Stocks 7 9.7Huge stocks as world market has kept export parity

away and Indian sugar did not got opportunity to export

Production 28.2 27

Imports 0 0

SUPPLY 35.2 36.7

Dom. Con 25 25.5 This seems even high in low price regime

Exports 0.5 3 This 3 mmt has be to exported minimum in 1/516 season

Carry Over 9.7 8.2

Stock Use 4.6 3.7

10

Strategy Promote exports at some discount to match export parity

Increase the realization on balance production up to import parity levels

11

Need revenue sharing model for cane pricing

Need to ensure that surplus is exported to world market at export parity

Ensure that domestic realization is better for balance production.

Support of big players from other states except Maharashtra is required

Conclusions !!!!

12

Thank You