1 chapter 4: time value of money copyright, 1999 prentice hall author: nick bagley objective explain...

TRANSCRIPT

1

Chapter 4: Time Value of Chapter 4: Time Value of MoneyMoney

Copyright, 1999 Prentice Hall Author: Nick Bagley

ObjectiveExplain the concept of compounding

and discounting and to provide examples of real life

applications

2

Introduction: Time Value Introduction: Time Value of Money (TVM)of Money (TVM)

$20 today is worth more than the $20 today is worth more than the expectation of $20 tomorrow expectation of $20 tomorrow because:because:– a bank would pay interest on the $20a bank would pay interest on the $20

– inflation makes tomorrows $20 less inflation makes tomorrows $20 less valuable than today’svaluable than today’s

– uncertainty of receiving tomorrow’s $20uncertainty of receiving tomorrow’s $20

3

CompoundingCompounding

• Assume that the interest rate is 10% p.a.Assume that the interest rate is 10% p.a.

• What this means is that if you invest $1 What this means is that if you invest $1 for one year, you have been promised for one year, you have been promised $1*(1+10/100) or $1.10 next year$1*(1+10/100) or $1.10 next year

• Investing $1 for yet another year Investing $1 for yet another year promises to produce 1.10 *(1+10/100) or promises to produce 1.10 *(1+10/100) or $1.21 in 2-years$1.21 in 2-years

4

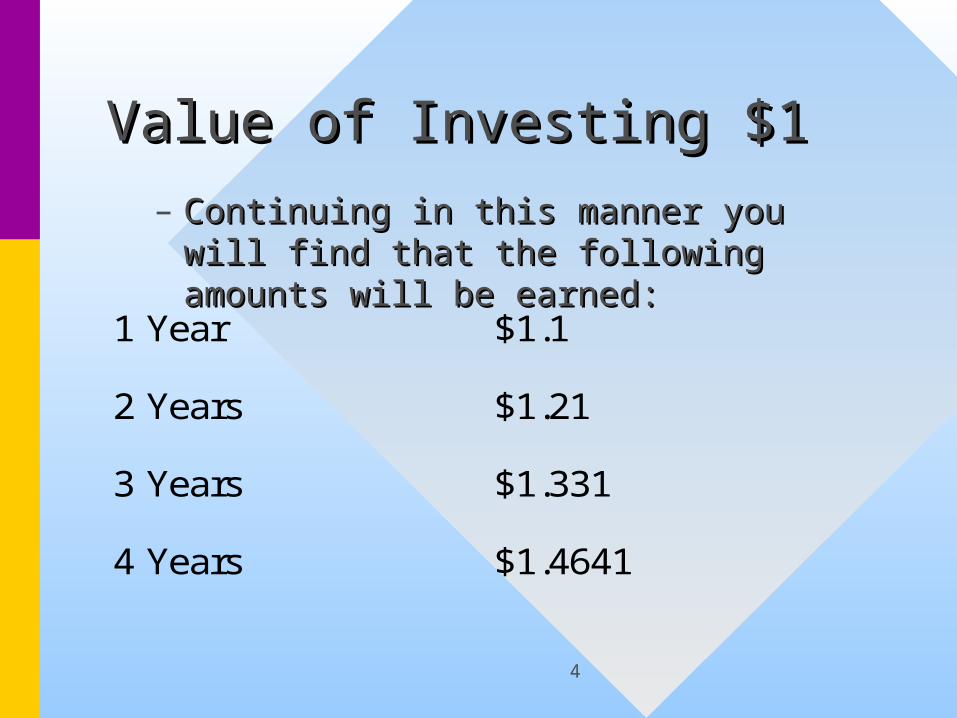

Value of Investing $1Value of Investing $1

1 Year $1.1

2 Years $1.21

3 Years $1.331

4 Years $1.4641

– Continuing in this manner you will find Continuing in this manner you will find that the following amounts will be that the following amounts will be earned:earned:

5

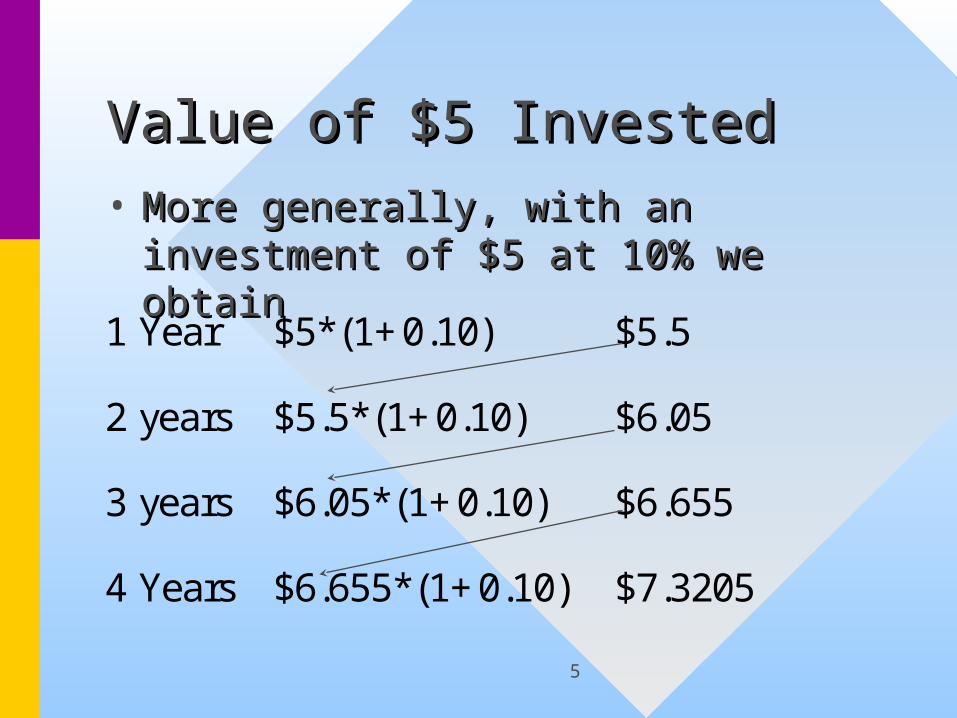

Value of $5 InvestedValue of $5 Invested

1 Year $5*(1+0.10) $5.5

2 years $5.5*(1+0.10) $6.05

3 years $6.05*(1+0.10) $6.655

4 Years $6.655*(1+0.10) $7.3205

• More generally, with an investment More generally, with an investment of $5 at 10% we obtainof $5 at 10% we obtain

6

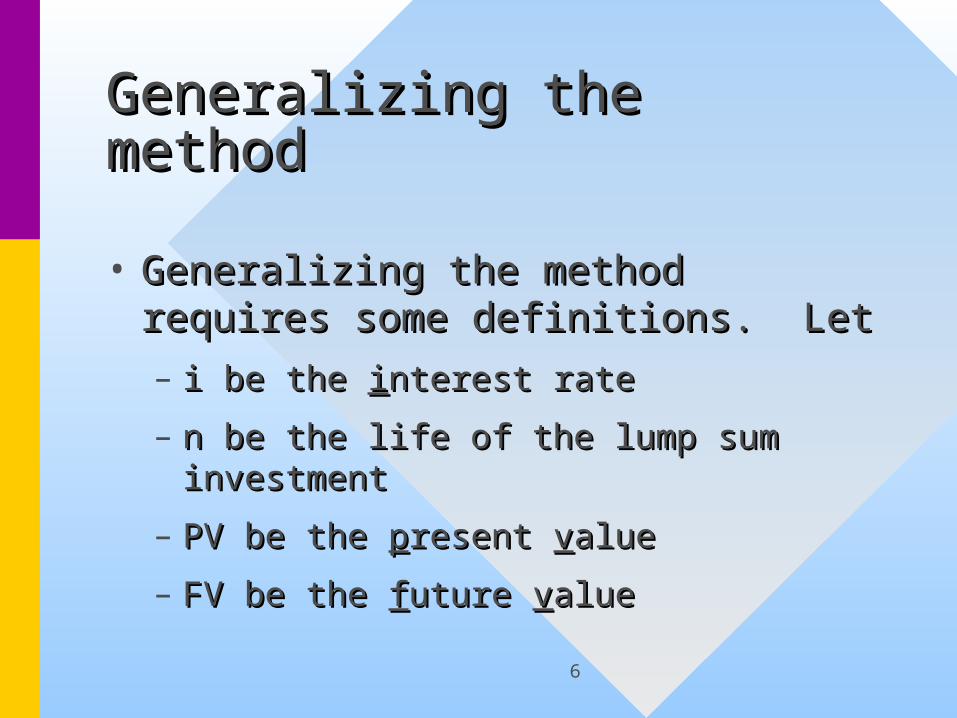

Generalizing the methodGeneralizing the method

• Generalizing the method requires Generalizing the method requires some definitions. Letsome definitions. Let– i be the i be the iinterest rate nterest rate

– n be the life of the lump sum n be the life of the lump sum investmentinvestment

– PV be the PV be the ppresent resent vvalue alue

– FV be the FV be the ffuture uture vvaluealue

7

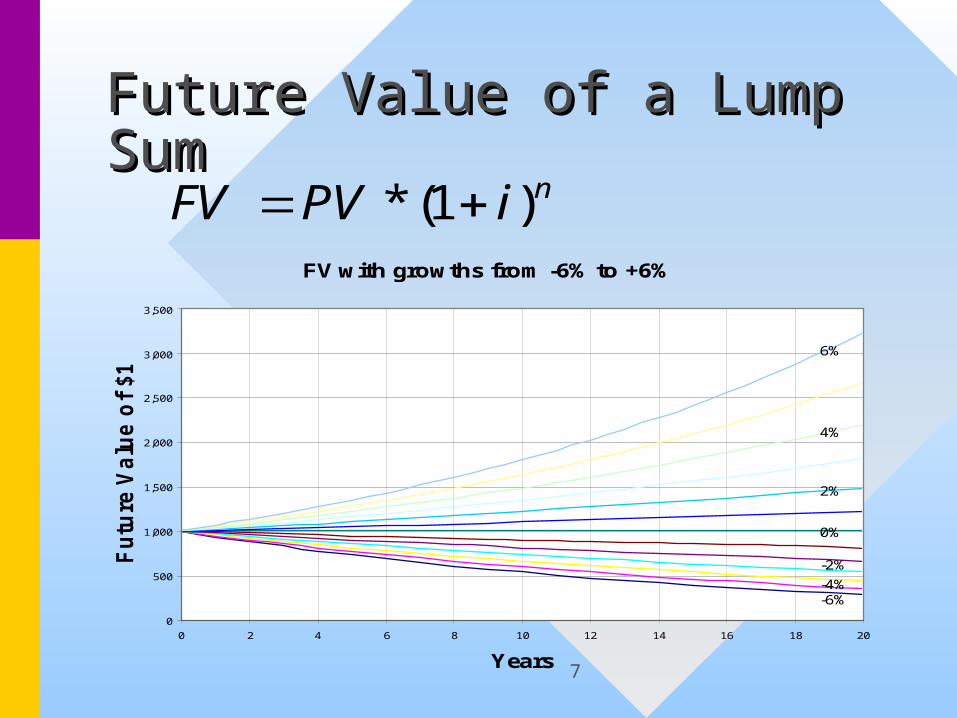

Future Value of a Lump Future Value of a Lump SumSum

niPVFV )1(* FV with growths from -6% to +6%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0 2 4 6 8 10 12 14 16 18 20

Years

Fu

ture

Va

lue

of

$1

00

0

6%

4%

2%

0%

-2%

-4%-6%

8

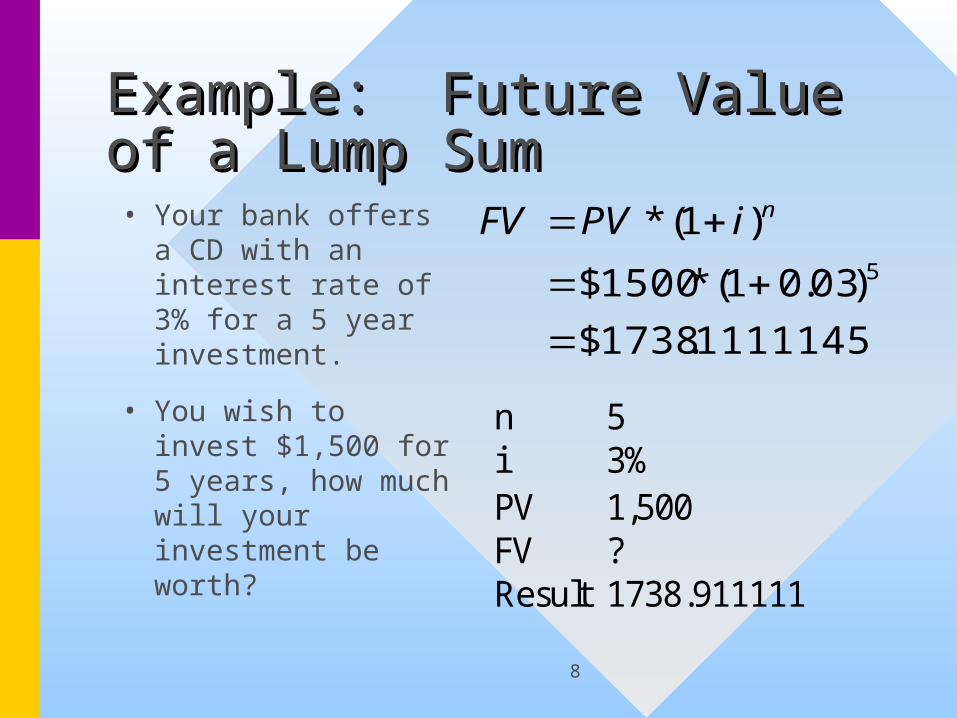

Example: Future Value of Example: Future Value of a Lump Suma Lump Sum• Your bank offers a

CD with an interest rate of 3% for a 5 year investment.

• You wish to invest $1,500 for 5 years, how much will your investment be worth?

1111145.1738$

)03.01(*1500$

)1(*5

niPVFV

n 5i 3%PV 1,500FV ?Result 1738.911111

9

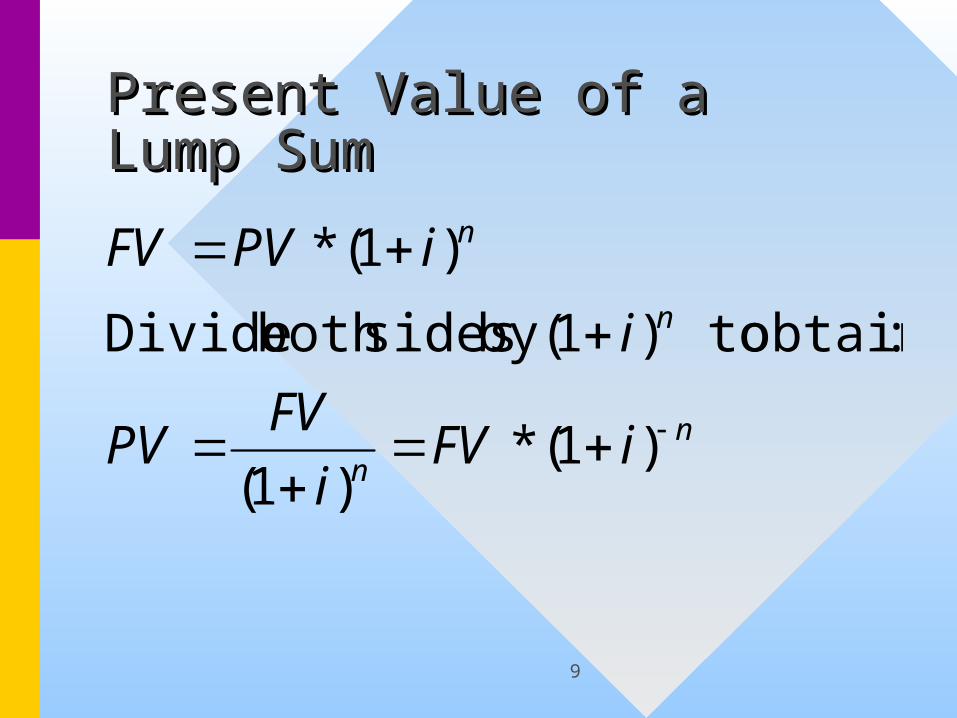

Present Value of a Lump Present Value of a Lump SumSum

nn

n

n

iFVi

FVPV

i

iPVFV

)1(*)1(

:obtain to)1(by sidesboth Divide

)1(*

10

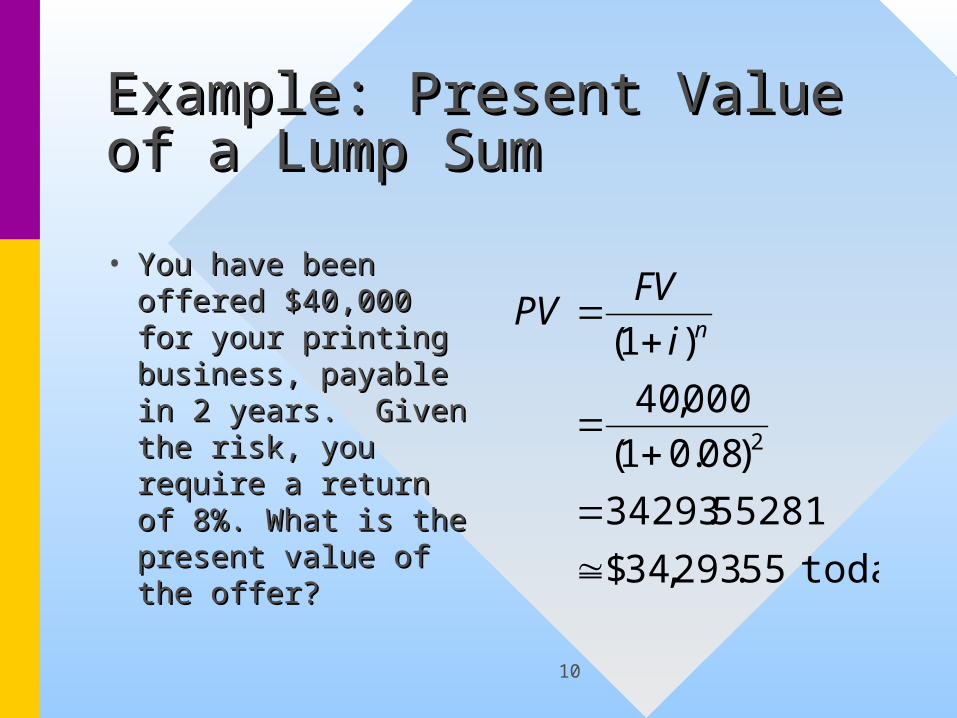

Example: Present Value of Example: Present Value of a Lump Suma Lump Sum

• You have been You have been offered $40,000 for offered $40,000 for your printing your printing business, payable business, payable in 2 years. Given in 2 years. Given the risk, you require the risk, you require a return of 8%. a return of 8%. What is the present What is the present value of the offer?value of the offer? today55.293,34$

55281.34293

)08.01(

000,40

)1(

2

ni

FVPV

11

Lump Sums FormulaeLump Sums Formulae

• You have solved a You have solved a present valuepresent value and a and a future valuefuture value of a of a lump sumlump sum. . There remains two other variables There remains two other variables that may be solved forthat may be solved for– interest, iinterest, i

– number of periods, nnumber of periods, n

12

Solving Lump Sum Cash Solving Lump Sum Cash Flow for Interest RateFlow for Interest Rate

1

)1(

)1(

)1(*

n

n

n

n

PVFV

i

PVFV

i

iPVFV

iPVFV

13

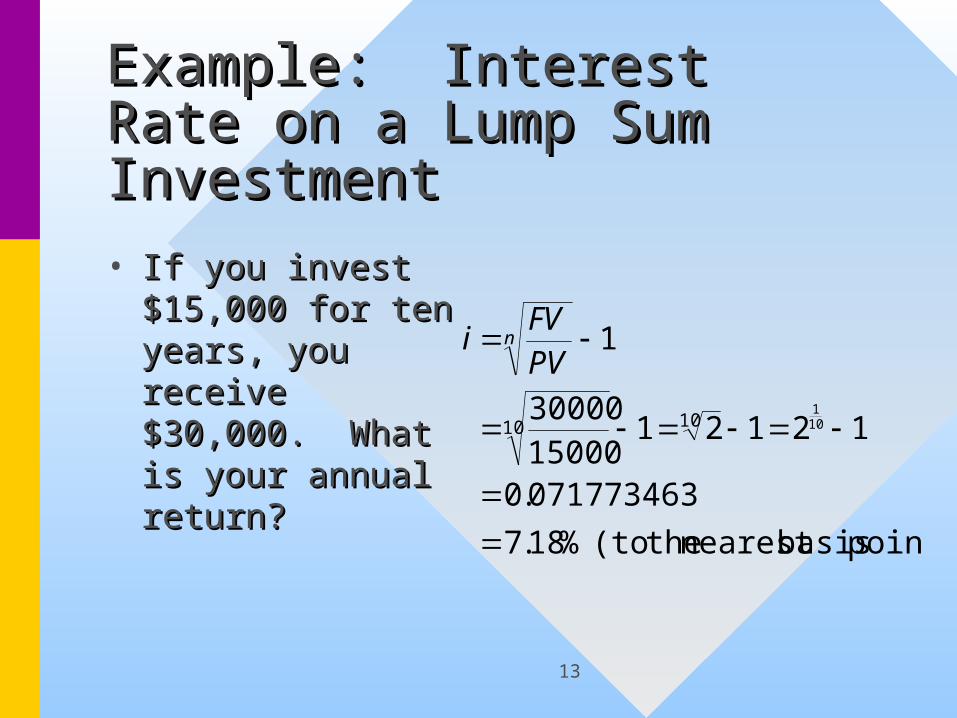

Example: Interest Rate on Example: Interest Rate on a Lump Sum Investmenta Lump Sum Investment

• If you invest If you invest $15,000 for ten $15,000 for ten years, you receive years, you receive $30,000. What is $30,000. What is your annual your annual return?return?

point) basisnearest the(to %18.7

071773463.0

121211500030000

1

101

1010

n

PVFV

i

14

Review of LogarithmsReview of Logarithms

• The next three slides are a quick The next three slides are a quick review of logarithmsreview of logarithms– I know that you probably learned this in I know that you probably learned this in

eighth grade, but those of us who do eighth grade, but those of us who do not use them frequently forget the not use them frequently forget the basic rulesbasic rules

15

– Logarithms are important in finance Logarithms are important in finance because growth is related to the the because growth is related to the the exponential, and the exponential is the exponential, and the exponential is the inverse function of the logarithminverse function of the logarithm

– Logarithms may have different bases, Logarithms may have different bases, but in finance we need only the but in finance we need only the natural natural logarithmlogarithm, that is the logarithm of base , that is the logarithm of base e.e.• The e is the irrational number that may The e is the irrational number that may

be approximated as 2.718281828. It is be approximated as 2.718281828. It is easy to remember because it starts to easy to remember because it starts to repeat, but don’t be fooled, it doesn't, repeat, but don’t be fooled, it doesn't, and it and it is irrationalirrational

16

Review of LogarithmsReview of Logarithms

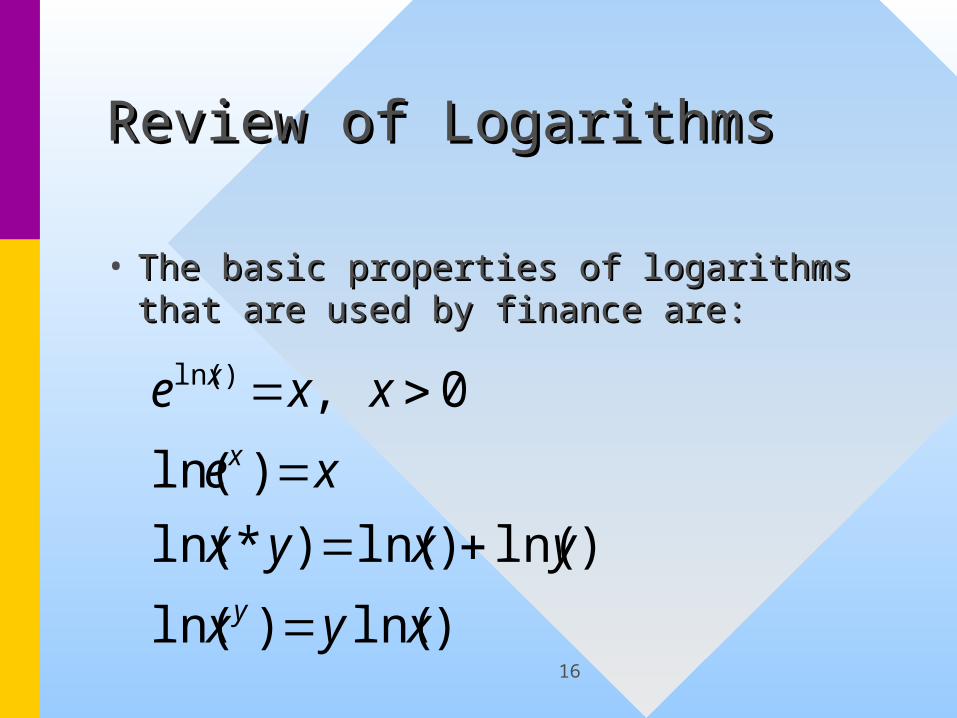

• The basic properties of logarithms that The basic properties of logarithms that are used by finance are:are used by finance are:

)ln()ln(

)ln()ln()*ln(

)ln(

0,)ln(

xyx

yxyx

xe

xxe

y

x

x

17

Review of LogarithmsReview of Logarithms

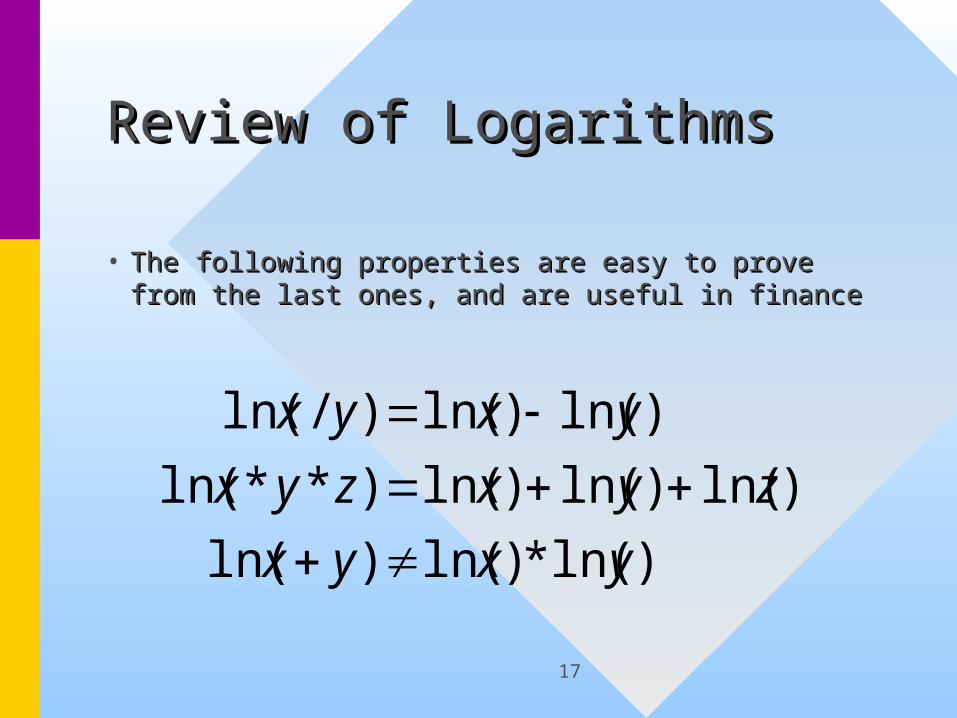

• The following properties are easy to prove The following properties are easy to prove from the last ones, and are useful in financefrom the last ones, and are useful in finance

)ln(*)ln()ln(

)ln()ln()ln()**ln(

)ln()ln()/ln(

yxyx

zyxzyx

yxyx

18

Solving Lump Sum Cash Solving Lump Sum Cash Flow for Number of Flow for Number of PeriodsPeriods

iPVFV

iPVFV

n

iniPV

FV

iPV

FV

iPVFV

n

n

n

1ln

lnln

1ln

ln

1ln*)1(lnln

)1(

)1(*

19

The Frequency of The Frequency of CompoundingCompounding

• You have a credit card that carries a You have a credit card that carries a rate of interest of 18% per year rate of interest of 18% per year compounded monthly. What is the compounded monthly. What is the interest rate compounded annually? interest rate compounded annually?

• That is, if you borrowed $1 with the That is, if you borrowed $1 with the card, what would you owe at the end card, what would you owe at the end of a year?of a year?

20

The Frequency of The Frequency of CompoundingCompounding

• 18% per year compounded monthly 18% per year compounded monthly is just code for 18%/12 = 1.5% per is just code for 18%/12 = 1.5% per month month

• 18% is the APR18% is the APR

• Effective Annual rate (EAR) equals Effective Annual rate (EAR) equals 19.56% - How?19.56% - How?

21

The Frequency of The Frequency of CompoundingCompounding

• The annual percentage rate (APR) The annual percentage rate (APR) compounded monthly is code for an compounded monthly is code for an effective rate equal to one twelfth of effective rate equal to one twelfth of the stated APR per month the stated APR per month

• The annual percentage rate (APR) The annual percentage rate (APR) compounded daily is code for an compounded daily is code for an effective rate equal to one 365th of the effective rate equal to one 365th of the stated APR per day stated APR per day

22

The Frequency of The Frequency of CompoundingCompounding

• APR is a rate expressed in terms of APR is a rate expressed in terms of an annual period but compounded an annual period but compounded with a time period less than a year with a time period less than a year (e.g., a month, six months, a (e.g., a month, six months, a quarter, or a day)quarter, or a day)

• APR is different from the actual or APR is different from the actual or the effective annual rate. the effective annual rate.

23

The Frequency of The Frequency of CompoundingCompounding• Assume m compounding periods in Assume m compounding periods in

one year and an APR equal to k. one year and an APR equal to k. Then the effective rate is k/m per Then the effective rate is k/m per compounding period.compounding period.

• Invest $1 for one year to obtain Invest $1 for one year to obtain $1*(1+k/m)$1*(1+k/m)mm, producing an effective , producing an effective annual rate of ($1*(1+k/m)annual rate of ($1*(1+k/m)mm - - $1)/$1 = (1+k/m)$1)/$1 = (1+k/m)mm - 1 - 1

24

Credit CardCredit Card

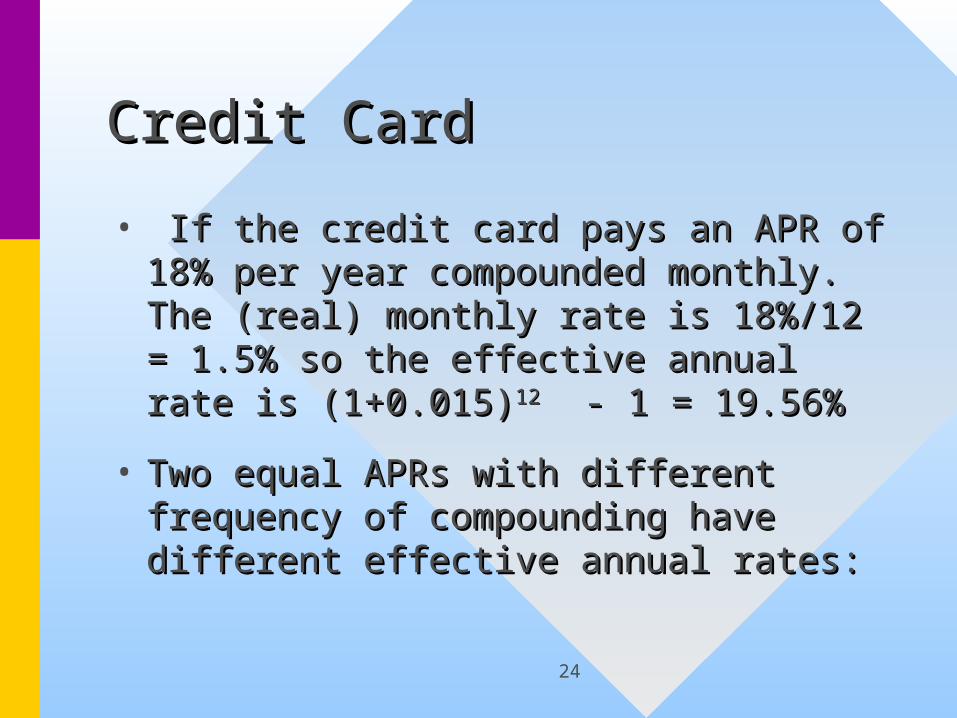

• If the credit card pays an APR of If the credit card pays an APR of 18% per year compounded monthly. 18% per year compounded monthly. The (real) monthly rate is 18%/12 = The (real) monthly rate is 18%/12 = 1.5% so the effective annual rate is 1.5% so the effective annual rate is (1+0.015)(1+0.015)1212 - 1 = 19.56% - 1 = 19.56%

• Two equal APRs with different Two equal APRs with different frequency of compounding have frequency of compounding have different effective annual rates:different effective annual rates:

25

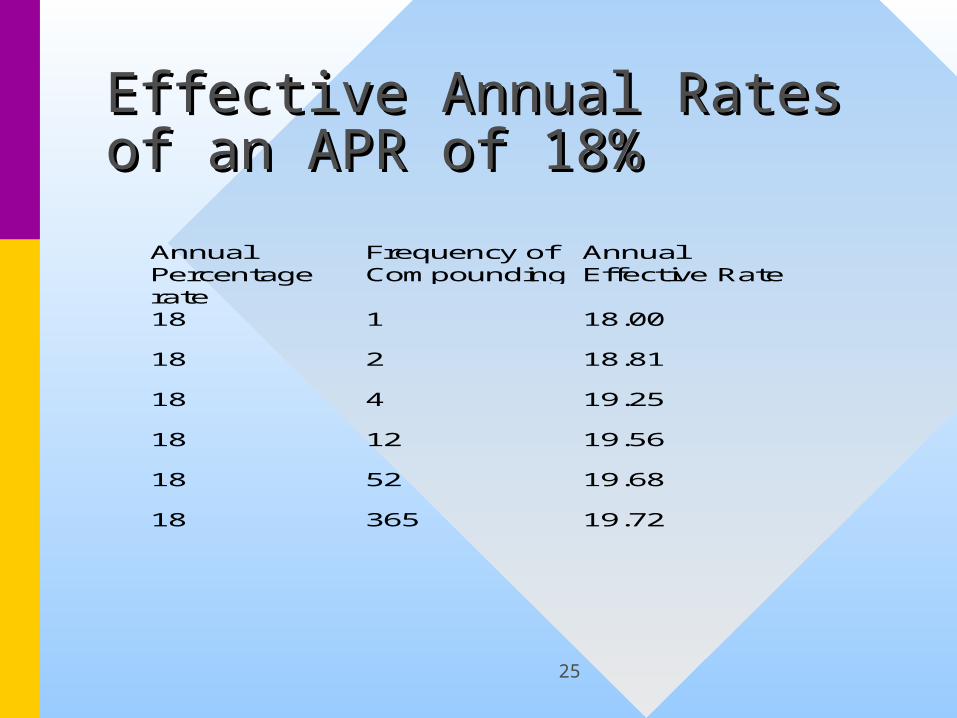

Effective Annual Rates of Effective Annual Rates of an APR of 18%an APR of 18%

AnnualPercentagerate

Frequency ofCompounding

AnnualEffective Rate

18 1 18.00

18 2 18.81

18 4 19.25

18 12 19.56

18 52 19.68

18 365 19.72

26

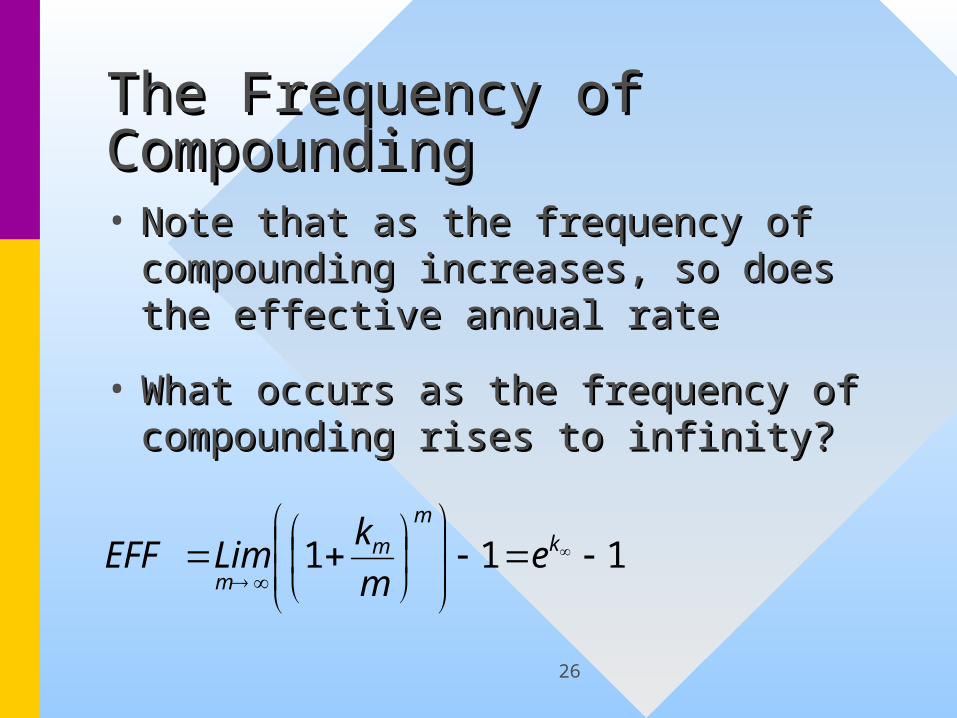

The Frequency of The Frequency of CompoundingCompounding• Note that as the frequency of Note that as the frequency of

compounding increases, so does the compounding increases, so does the effective annual rateeffective annual rate

• What occurs as the frequency of What occurs as the frequency of compounding rises to infinity?compounding rises to infinity?

111

km

m

me

m

kLimEFF

27

The Frequency of The Frequency of CompoundingCompounding

• The effective annual rate that’s The effective annual rate that’s equivalent to an annual percentage equivalent to an annual percentage rate of 18% is then e rate of 18% is then e 0.18 0.18 - 1 = - 1 = 19.72%19.72%

• More precision shows that moving More precision shows that moving from daily compounding to from daily compounding to continuous compounding gains 0.53 continuous compounding gains 0.53 of one basis pointof one basis point

28

The Frequency of The Frequency of CompoundingCompounding

• A bank determines that it needs an A bank determines that it needs an effective rate of 12% on car loans to effective rate of 12% on car loans to medium risk borrowersmedium risk borrowers

• What annual percentage rates may What annual percentage rates may it offer?it offer?

29

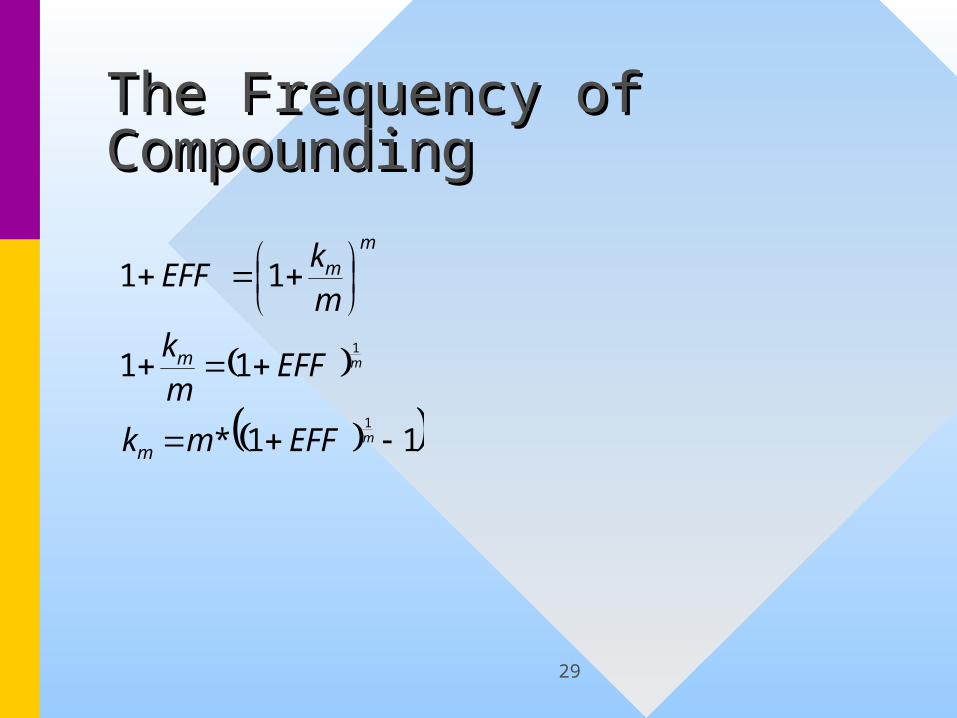

The Frequency of The Frequency of CompoundingCompounding

11*

11

11

1

1

m

m

EFFmk

EFFm

k

m

kEFF

m

m

m

m

30

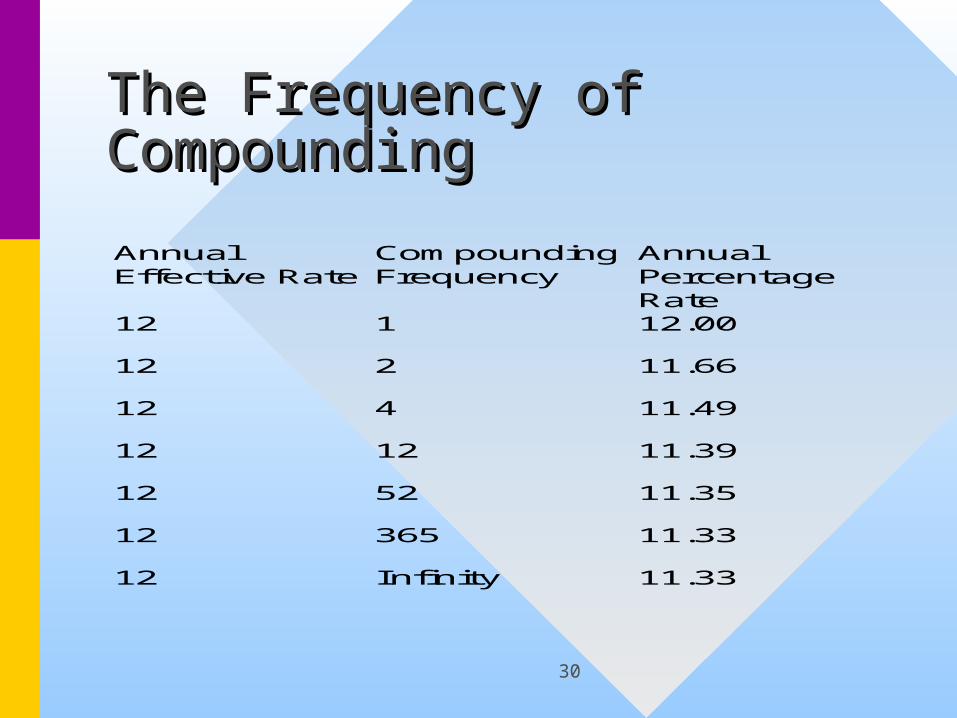

The Frequency of The Frequency of CompoundingCompounding

AnnualEffective Rate

CompoundingFrequency

AnnualPercentageRate

12 1 12.00

12 2 11.66

12 4 11.49

12 12 11.39

12 52 11.35

12 365 11.33

12 Infinity 11.33

31

AnnuitiesAnnuities

• Financial analysts use several Financial analysts use several annuities with differing assumptions annuities with differing assumptions about the first payment. We will about the first payment. We will examine just two:examine just two:– regular annuityregular annuity with its first coupon one with its first coupon one

period from now, (detail look)period from now, (detail look)

– annuity dueannuity due with its first coupon today, with its first coupon today, (cursory look)(cursory look)

32

Rationale for Annuity Rationale for Annuity FormulaFormula

– a sequence of equally spaced identical a sequence of equally spaced identical cash flows is a common occurrence, so cash flows is a common occurrence, so automation pays offautomation pays off

– a typical annuity is a mortgage which a typical annuity is a mortgage which may have 360 monthly payments, a lot may have 360 monthly payments, a lot of work for using elementary methodsof work for using elementary methods

33

Assumptions Regular Assumptions Regular Annuity Annuity

– the first cash flow will occur exactly the first cash flow will occur exactly one period form nowone period form now

– all subsequent cash flows are all subsequent cash flows are separated by exactly one periodseparated by exactly one period

– all periods are of equal lengthall periods are of equal length

– the term structure of interest is flatthe term structure of interest is flat

– all cash flows have the same (nominal) all cash flows have the same (nominal) valuevalue

34

Annuity Formula NotationAnnuity Formula Notation

• PV = the present value of the PV = the present value of the annuityannuity

• i = interest rate to be earned over i = interest rate to be earned over the life of the annuitythe life of the annuity

• n = the number of paymentsn = the number of payments

• pmt = the periodic paymentpmt = the periodic payment

35

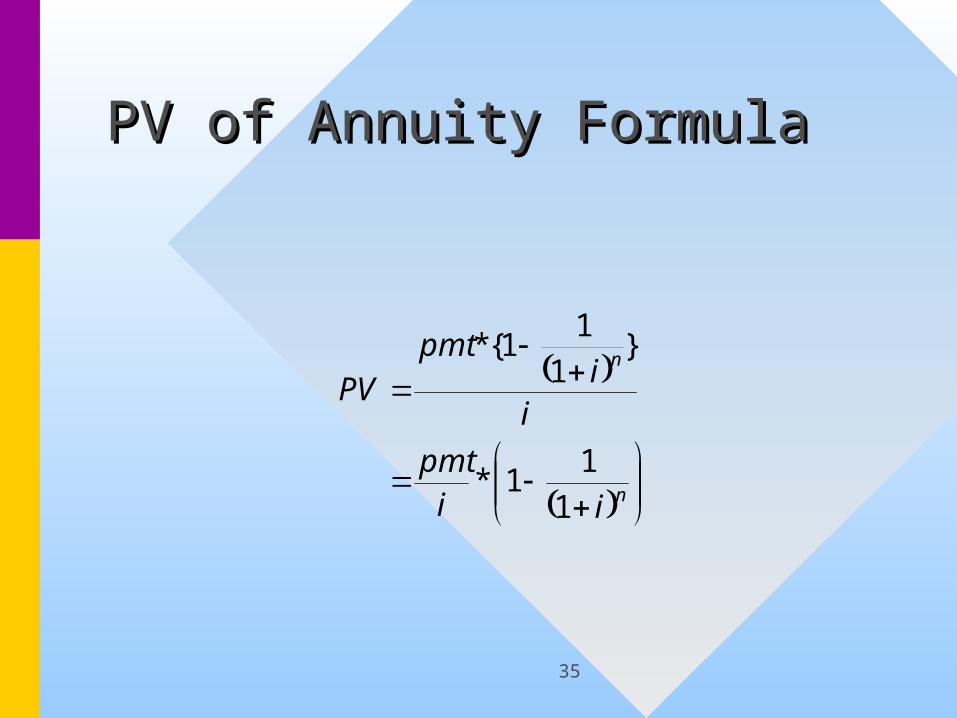

PV of Annuity FormulaPV of Annuity Formula

n

n

iipmt

ii

pmt

PV

1

11*

}1

11{*

36

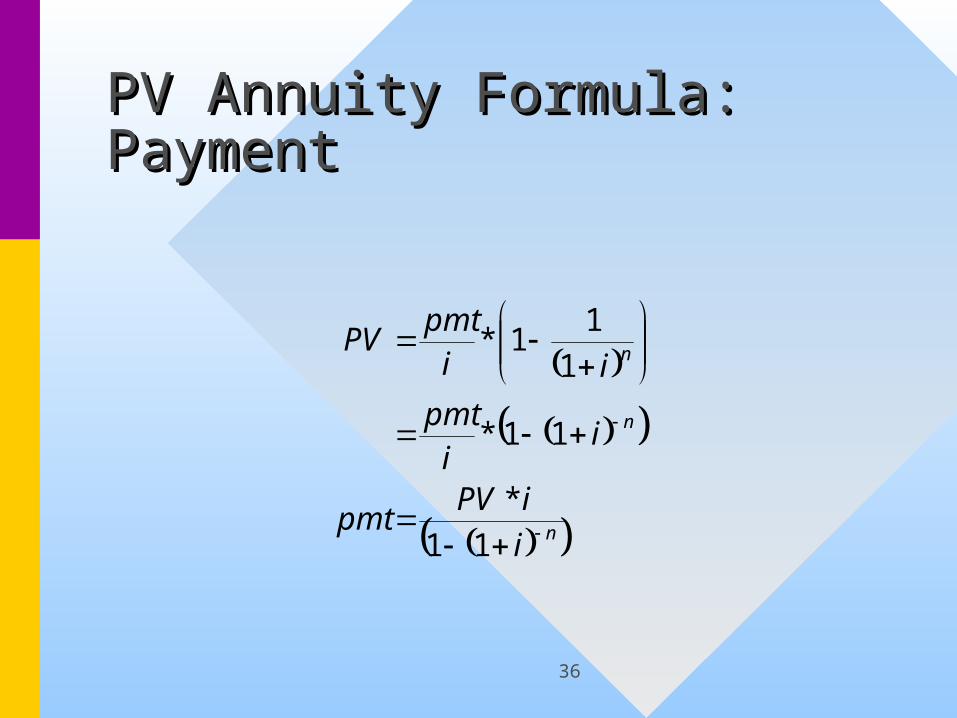

PV Annuity Formula: PV Annuity Formula: PaymentPayment

n

n

n

i

iPVpmt

iipmt

iipmt

PV

11

*

11*

1

11*

37

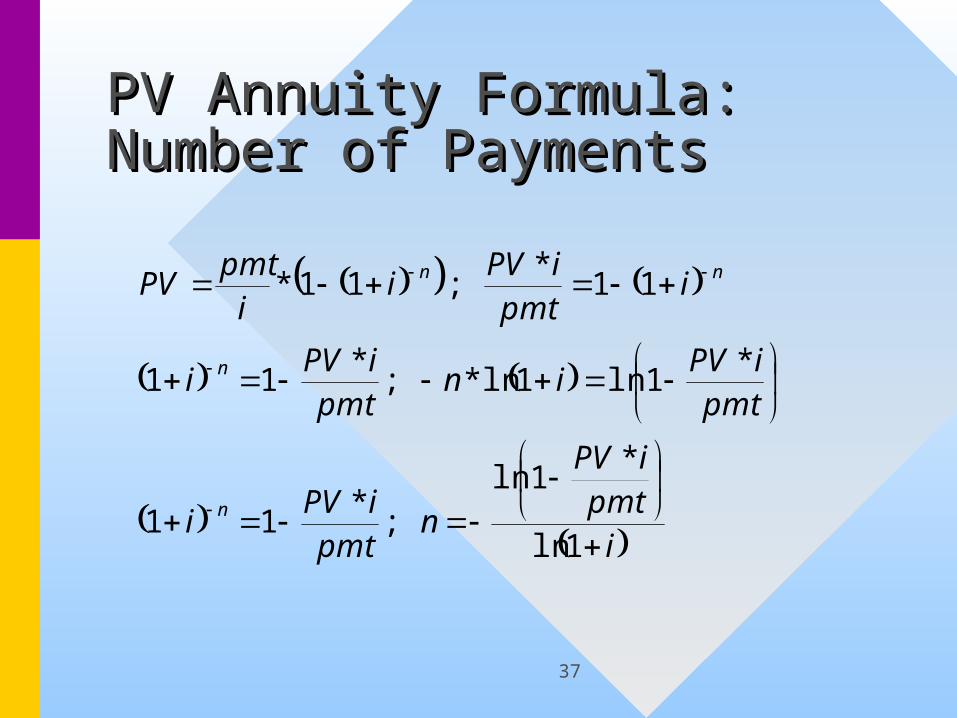

PV Annuity Formula: PV Annuity Formula: Number of PaymentsNumber of Payments

ipmt

iPV

npmt

iPVi

pmtiPV

inpmt

iPVi

ipmt

iPVi

ipmt

PV

n

n

nn

1ln

*1ln

;*

11

*1ln1ln*;

*11

11*

;11*

38

PV Annuity Formula: PV Annuity Formula: ReturnReturn

– There is no transcendental solution to There is no transcendental solution to the PV of an annuity equation in terms the PV of an annuity equation in terms of the interest rate. Students of the interest rate. Students interested in the reason why are interested in the reason why are referred to Galois Theory, 2nd. Ed I. referred to Galois Theory, 2nd. Ed I. Stewart. Stewart.

39

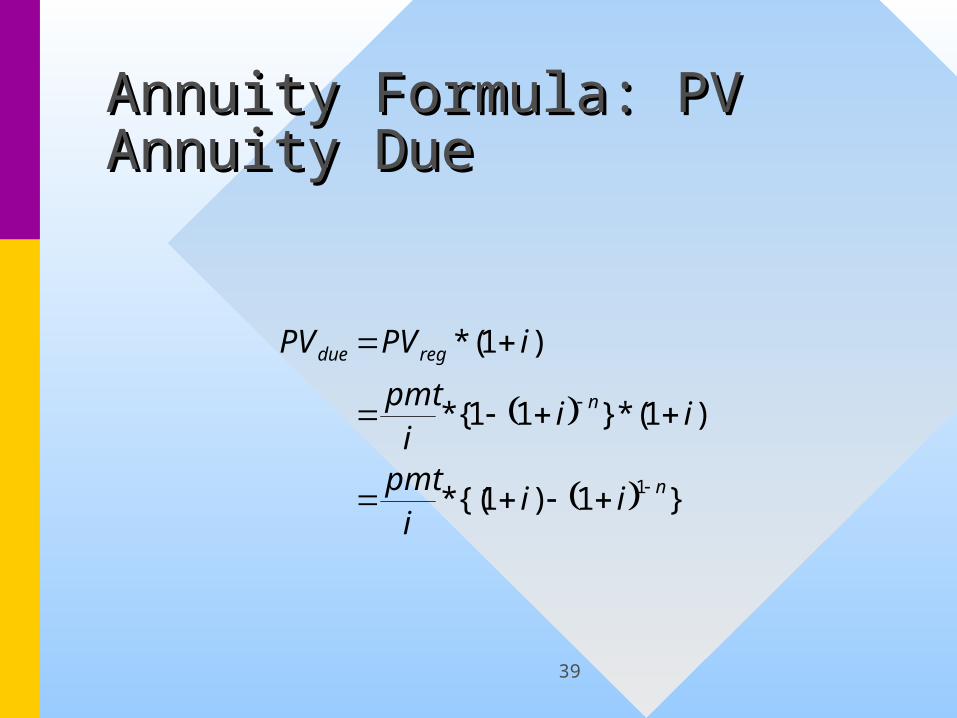

Annuity Formula: PV Annuity Formula: PV Annuity DueAnnuity Due

}1)1{(*

)1(*}11{*

)1(*

1 n

n

regdue

iiipmt

iiipmt

iPVPV

40

Derivation of FV of Derivation of FV of Annuity Formula: AlgebraAnnuity Formula: Algebra

11*

1*1

11*FV

sum) (lump 1*FV

annuity) (reg. 1

11*

n

n

n

n

n

iipmt

iii

pmt

iPV

iipmt

PV

41

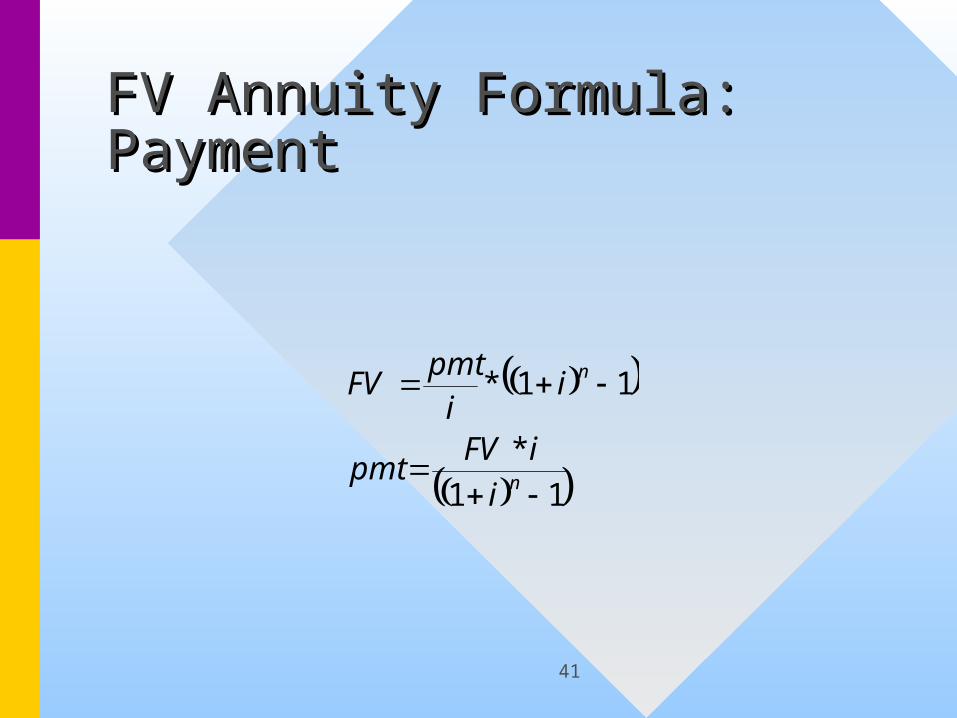

FV Annuity Formula: FV Annuity Formula: PaymentPayment

11

*

11*

n

n

i

iFVpmt

iipmt

FV

42

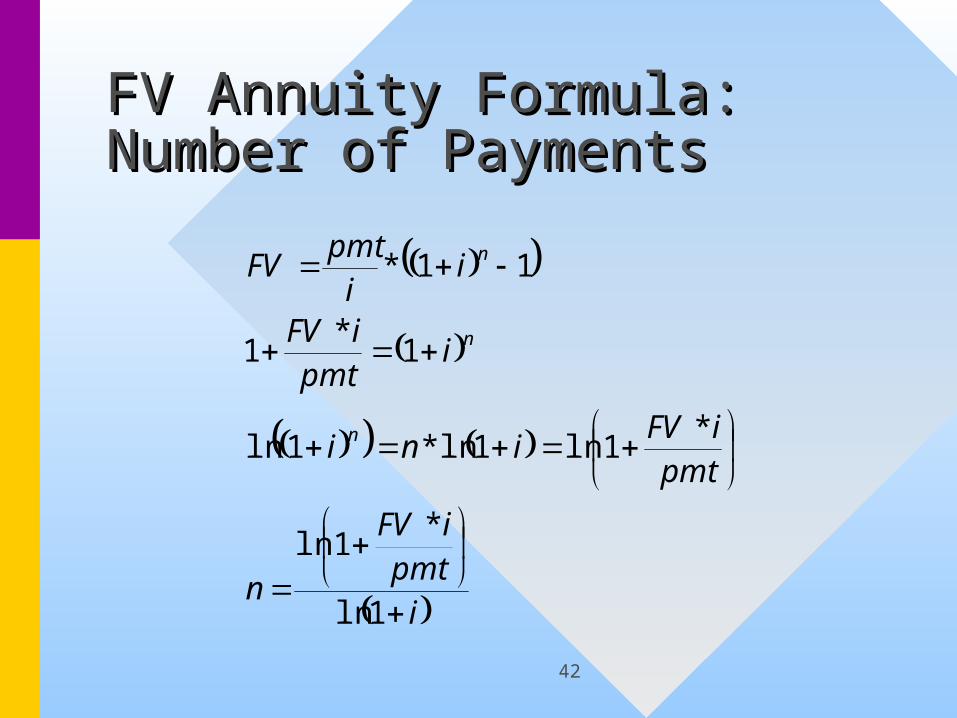

FV Annuity Formula: FV Annuity Formula: Number of PaymentsNumber of Payments

ipmt

iFV

n

pmtiFV

ini

ipmt

iFV

iipmt

FV

n

n

n

1ln

*1ln

*1ln1ln*1ln

1*

1

11*

43

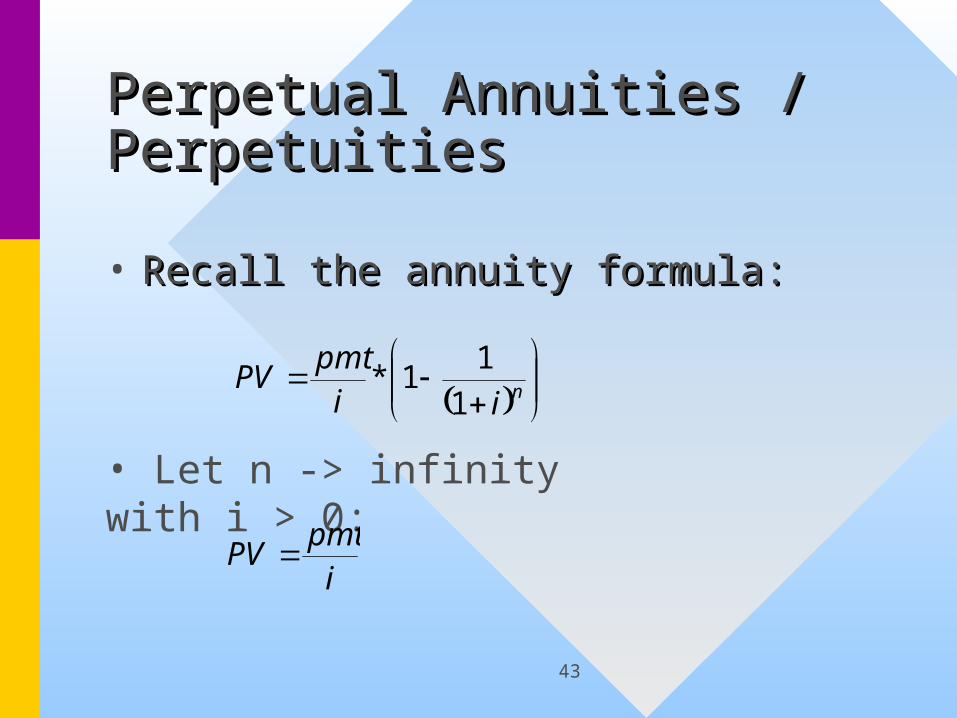

Perpetual Annuities / Perpetual Annuities / PerpetuitiesPerpetuities

• Recall the annuity formula:Recall the annuity formula:

niipmt

PV1

11*

• Let n -> infinity with i > 0:

ipmt

PV

44

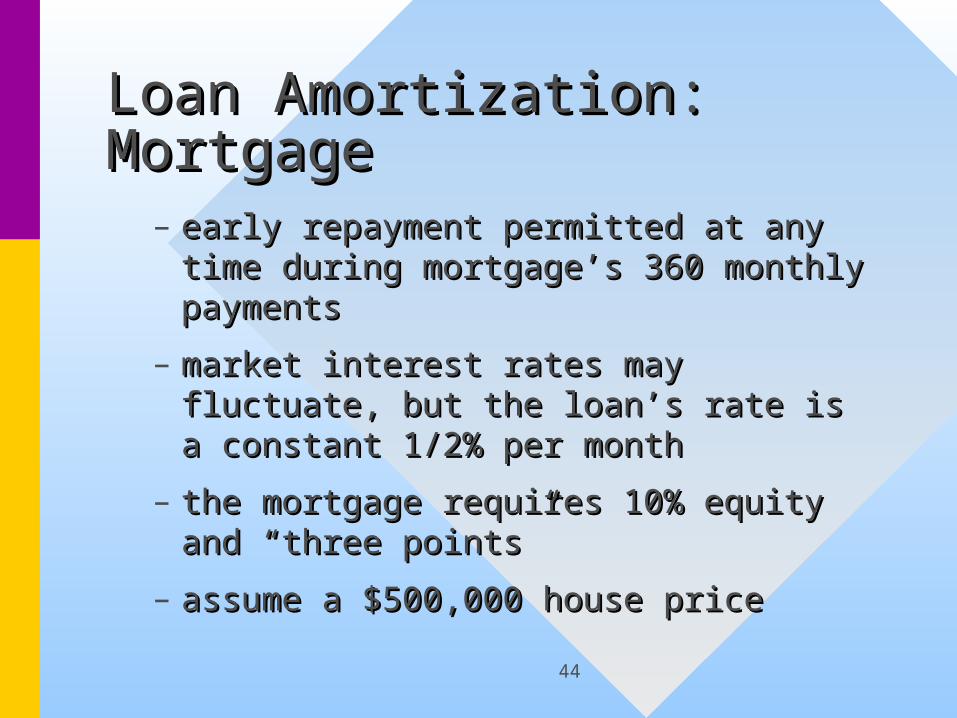

Loan Amortization: Loan Amortization: MortgageMortgage

– early repayment permitted at any time early repayment permitted at any time during mortgage’s 360 monthly during mortgage’s 360 monthly paymentspayments

– market interest rates may fluctuate, market interest rates may fluctuate, but the loan’s rate is a constant 1/2% but the loan’s rate is a constant 1/2% per monthper month

– the mortgage requires 10% equity and the mortgage requires 10% equity and “three points”“three points”

– assume a $500,000 house priceassume a $500,000 house price

45

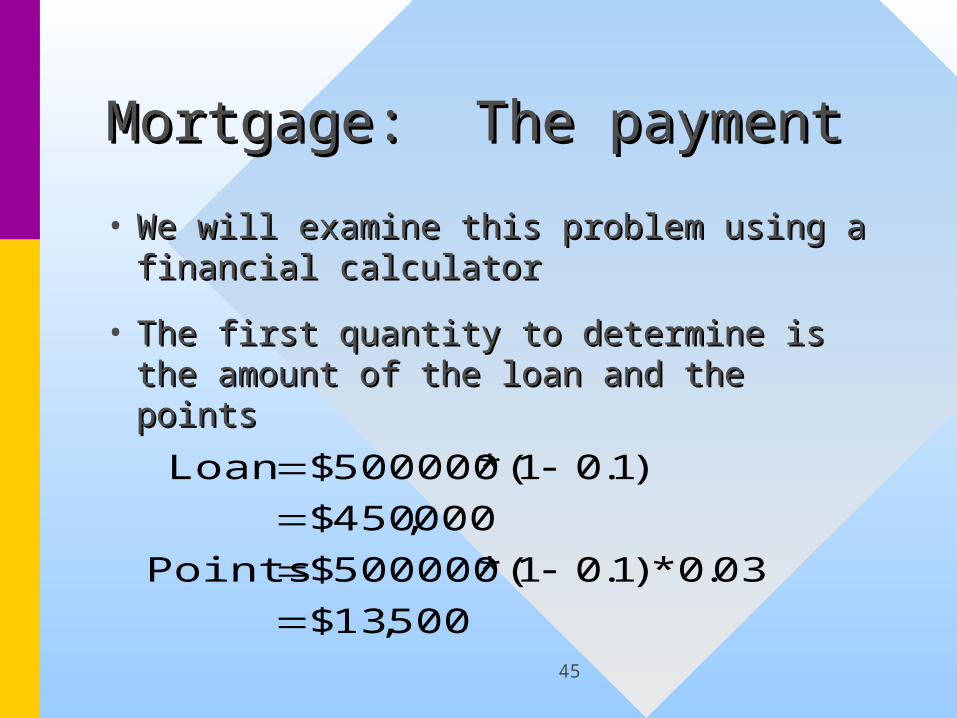

Mortgage: The paymentMortgage: The payment

• We will examine this problem using a We will examine this problem using a financial calculatorfinancial calculator

• The first quantity to determine is the The first quantity to determine is the amount of the loan and the pointsamount of the loan and the points

500,13$

03.0*)1.01(*500000$Points

000,450$

)1.01(*500000$Loan

46

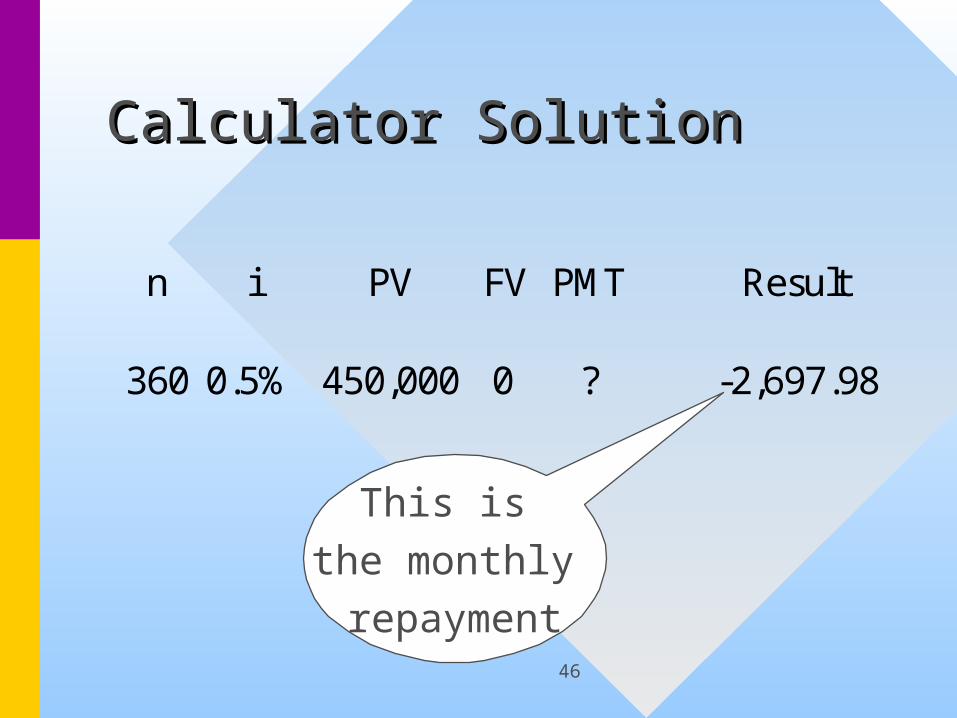

Calculator SolutionCalculator Solution

n i PV FV PMT Result

360 0.5% 450,000 0 ? -2,697.98

This is the monthly repayment

47

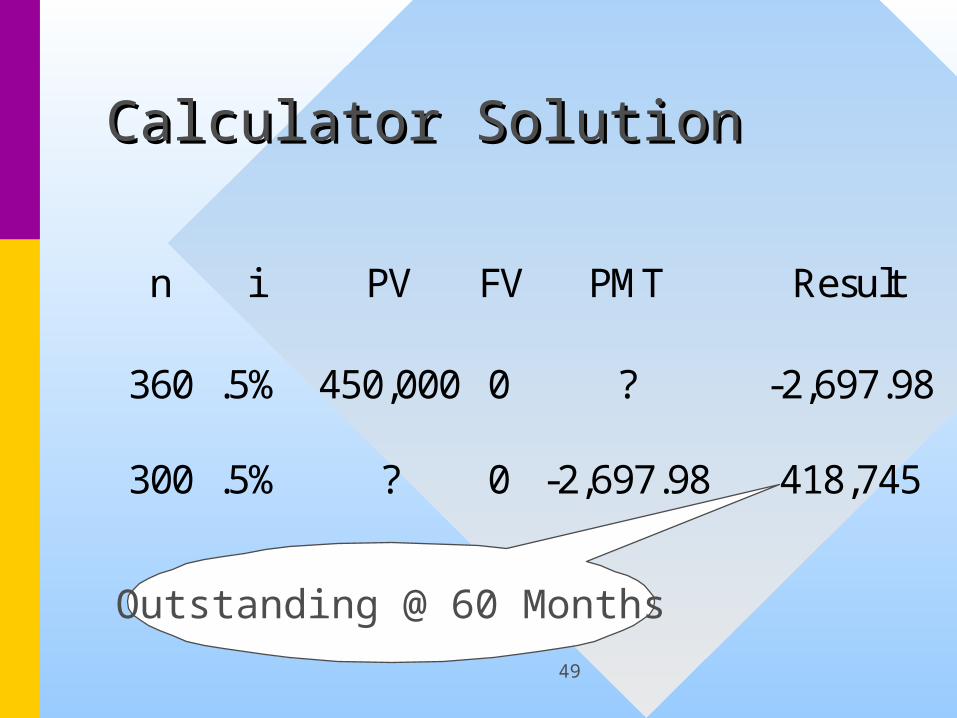

Mortgage: Early Mortgage: Early RepaymentRepayment

– Assume that the family plans to sell the Assume that the family plans to sell the house after exactly 60 payments, what house after exactly 60 payments, what will be the outstanding principle?will be the outstanding principle?

48

Mortgage Repayment: Mortgage Repayment: IssuesIssues

• The outstanding principle is the The outstanding principle is the present value (at repayment date) present value (at repayment date) of the remaining payments on the of the remaining payments on the mortgagemortgage

• There are in this case 360-60 = 300 There are in this case 360-60 = 300 remaining payments, starting with remaining payments, starting with the one 1-month from nowthe one 1-month from now

49

Calculator SolutionCalculator Solution

n i PV FV PMT Result

360 .5% 450,000 0 ? -2,697.98

300 .5% ? 0 -2,697.98 418,745

Outstanding @ 60 Months

50

Summary of PaymentsSummary of Payments

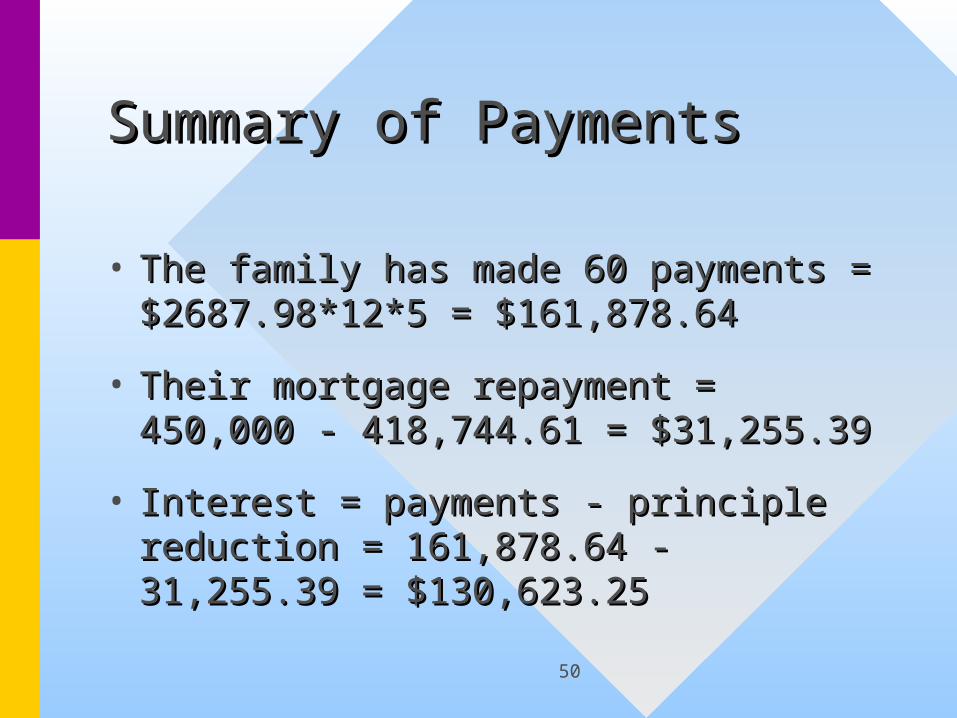

• The family has made 60 payments = The family has made 60 payments = $2687.98*12*5 = $161,878.64$2687.98*12*5 = $161,878.64

• Their mortgage repayment =Their mortgage repayment = 450,000 - 418,744.61 = $31,255.39450,000 - 418,744.61 = $31,255.39

• Interest = payments - principle Interest = payments - principle reduction = 161,878.64 - 31,255.39 = reduction = 161,878.64 - 31,255.39 = $130,623.25$130,623.25

51

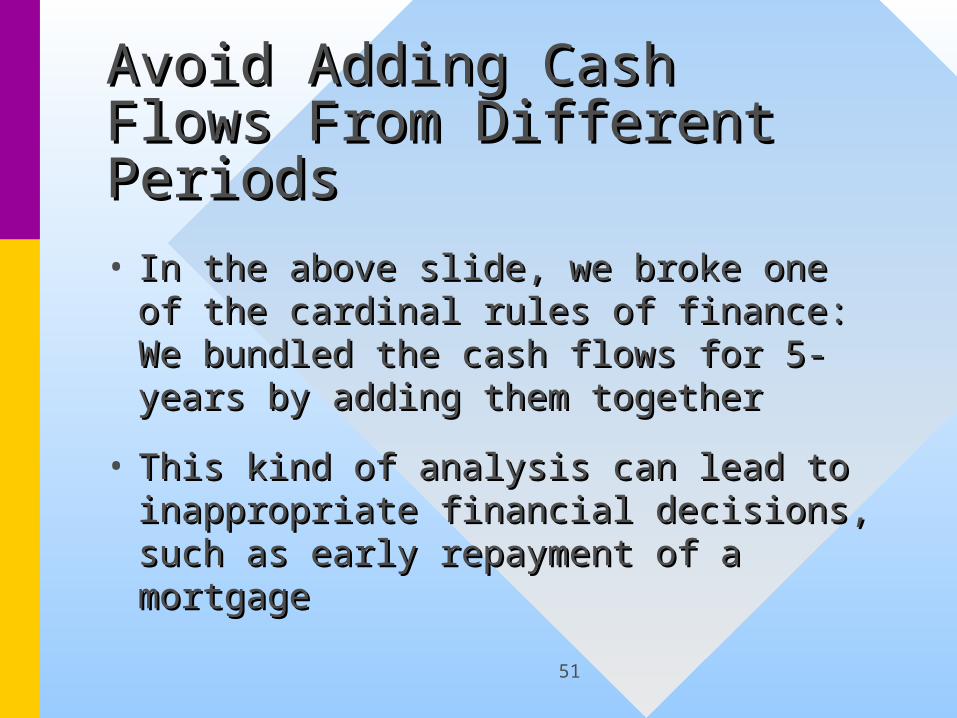

Avoid Adding Cash Flows Avoid Adding Cash Flows From Different PeriodsFrom Different Periods

• In the above slide, we broke one of In the above slide, we broke one of the cardinal rules of finance: We the cardinal rules of finance: We bundled the cash flows for 5-years by bundled the cash flows for 5-years by adding them togetheradding them together

• This kind of analysis can lead to This kind of analysis can lead to inappropriate financial decisions, such inappropriate financial decisions, such as early repayment of a mortgageas early repayment of a mortgage

52

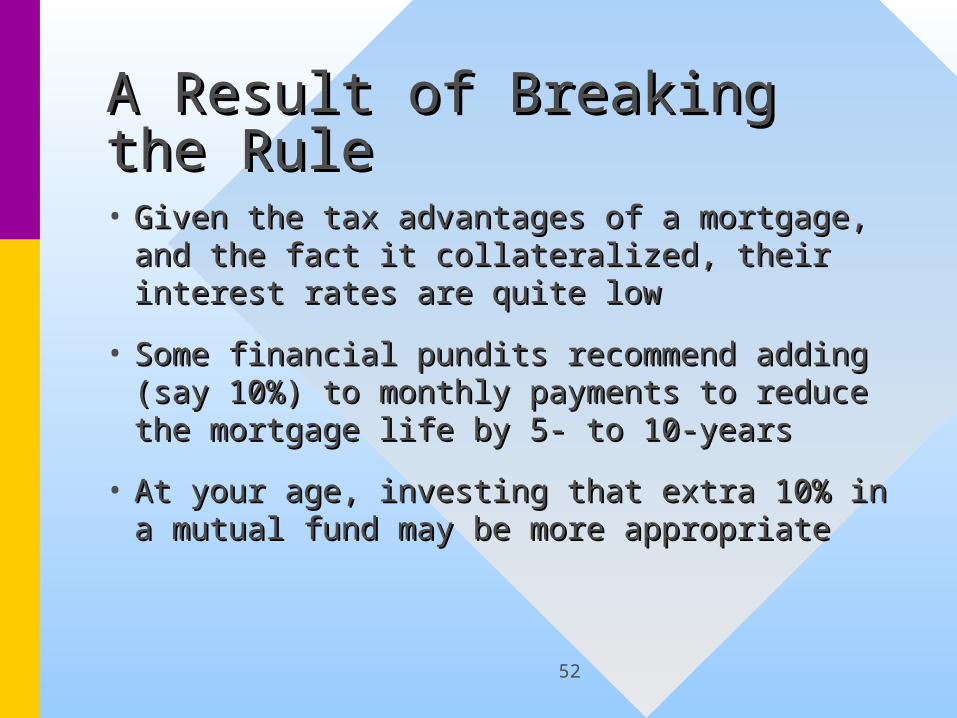

A Result of Breaking the A Result of Breaking the RuleRule• Given the tax advantages of a Given the tax advantages of a

mortgage, and the fact it collateralized, mortgage, and the fact it collateralized, their interest rates are quite lowtheir interest rates are quite low

• Some financial pundits recommend Some financial pundits recommend adding (say 10%) to monthly payments adding (say 10%) to monthly payments to reduce the mortgage life by 5- to 10-to reduce the mortgage life by 5- to 10-yearsyears

• At your age, investing that extra 10% in At your age, investing that extra 10% in a mutual fund may be more appropriatea mutual fund may be more appropriate

53

A Result of Breaking the A Result of Breaking the RuleRule• The pundits make their argument by The pundits make their argument by

adding (without discounting!) the adding (without discounting!) the difference in the cash flows between the difference in the cash flows between the scenarios. This is typically a huge sum scenarios. This is typically a huge sum of money, and this is what is “saved”of money, and this is what is “saved”

• When discounted appropriately, there When discounted appropriately, there are no significant savings. There are are no significant savings. There are huge opportunity losses for those willing huge opportunity losses for those willing to accept the risk of a stock mutual fundto accept the risk of a stock mutual fund

54

Outstanding Balance as a Outstanding Balance as a Function of TimeFunction of Time

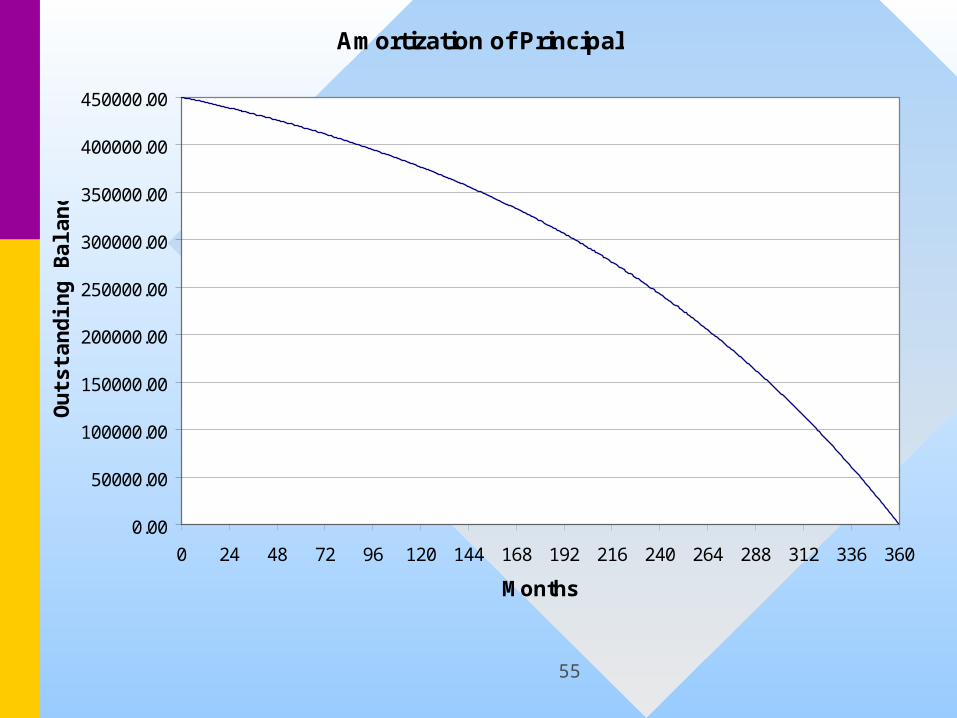

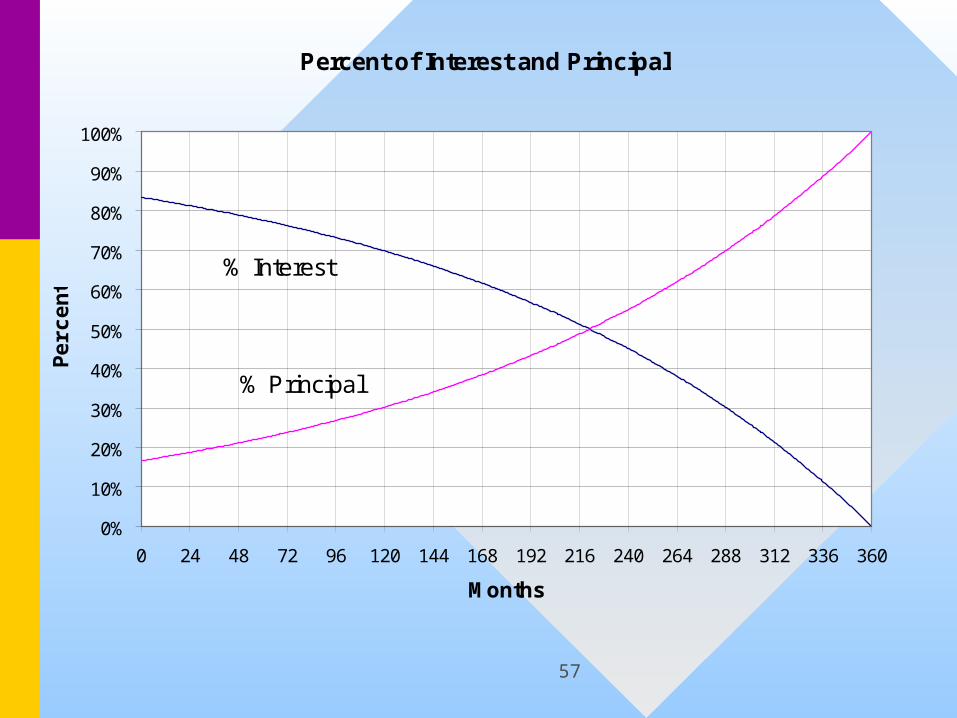

• The following graphs illustrate that The following graphs illustrate that in the early years, monthly payment in the early years, monthly payment are mostly interest. In latter years, are mostly interest. In latter years, the payments are mostly principlethe payments are mostly principle

• Recall that only the interest portion Recall that only the interest portion is tax-deductible, so the tax shelter is tax-deductible, so the tax shelter decaysdecays

55

Amortization of Principal

0.00

50000.00

100000.00

150000.00

200000.00

250000.00

300000.00

350000.00

400000.00

450000.00

0 24 48 72 96 120 144 168 192 216 240 264 288 312 336 360

Months

Ou

tsta

nd

ing

Bal

ance

56

After Tax Cash Flow

$1,500

$1,700

$1,900

$2,100

$2,300

$2,500

$2,700

$2,900

0 24 48 72 96 120 144 168 192 216 240 264 288 312 336 360

Monthly Cash Flow

Mo

nth

57

Percent of Interest and Principal

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0 24 48 72 96 120 144 168 192 216 240 264 288 312 336 360

Months

Per

cen

t

% Interest

% Principal

58

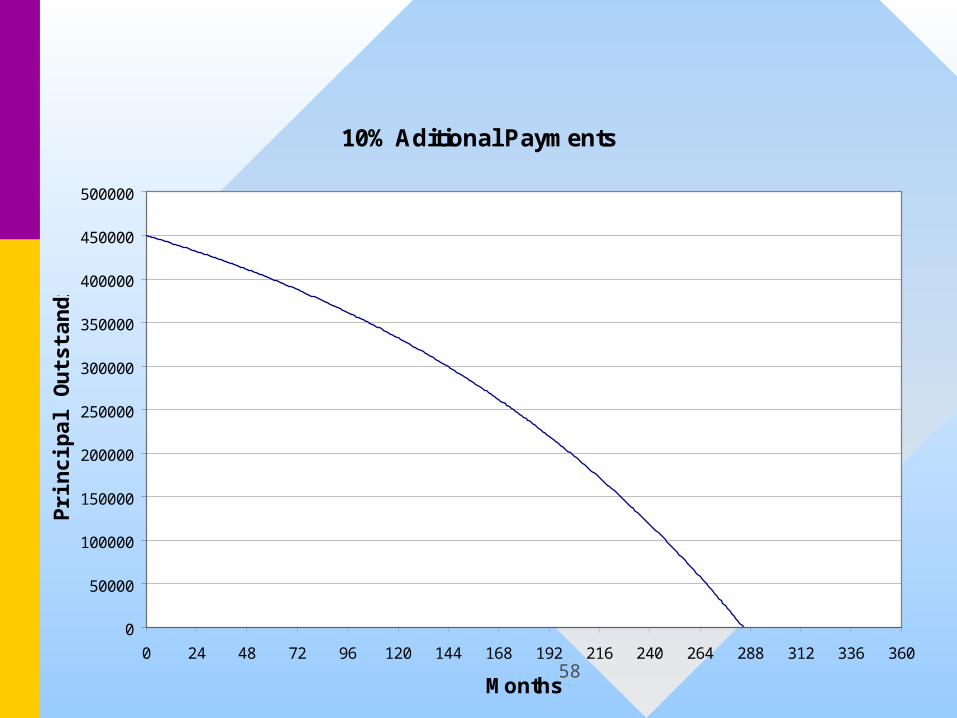

10% Aditional Payments

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

0 24 48 72 96 120 144 168 192 216 240 264 288 312 336 360

Months

Pri

nci

pal

Ou

tsta

nd

ing

59

Exchange Rates and Time Exchange Rates and Time Value of MoneyValue of Money

• You are considering the choice:You are considering the choice:– Investing $10,000 in dollar-Investing $10,000 in dollar-

denominated bonds offering 10% / yeardenominated bonds offering 10% / year

– Investing $10,000 in yen-denominated Investing $10,000 in yen-denominated bonds offering 3% / yearbonds offering 3% / year• Assume an exchange rate of 0.01Assume an exchange rate of 0.01

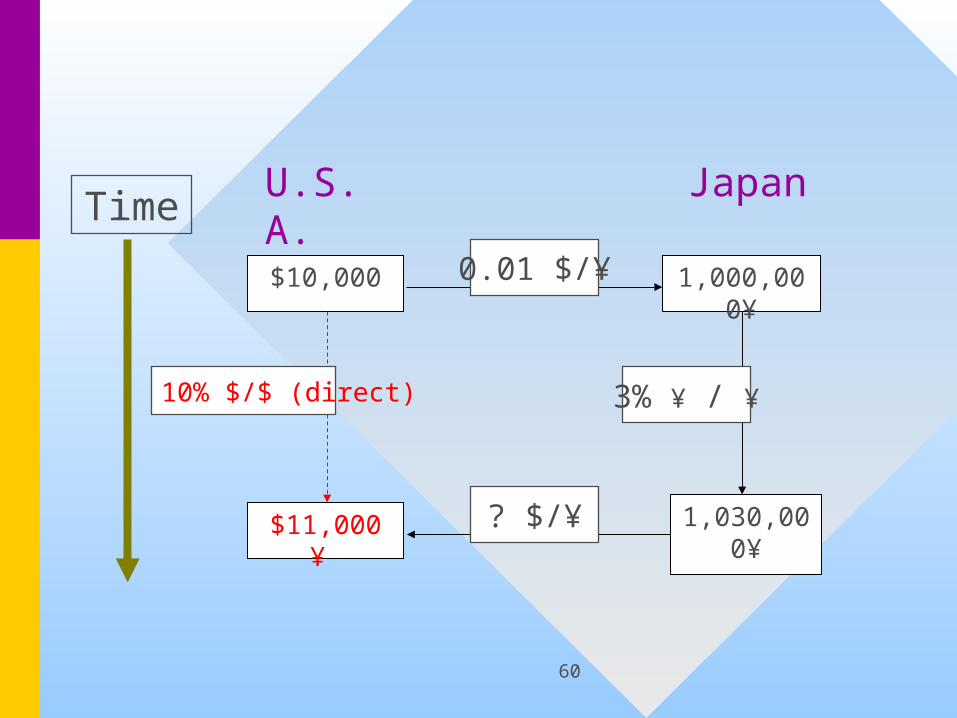

60

$10,000

$11,000 ¥

1,000,000¥

1,030,000¥

Time

10% $/$ (direct)

0.01 $/¥

3% ¥ / ¥

? $/¥

U.S.A.

Japan

61

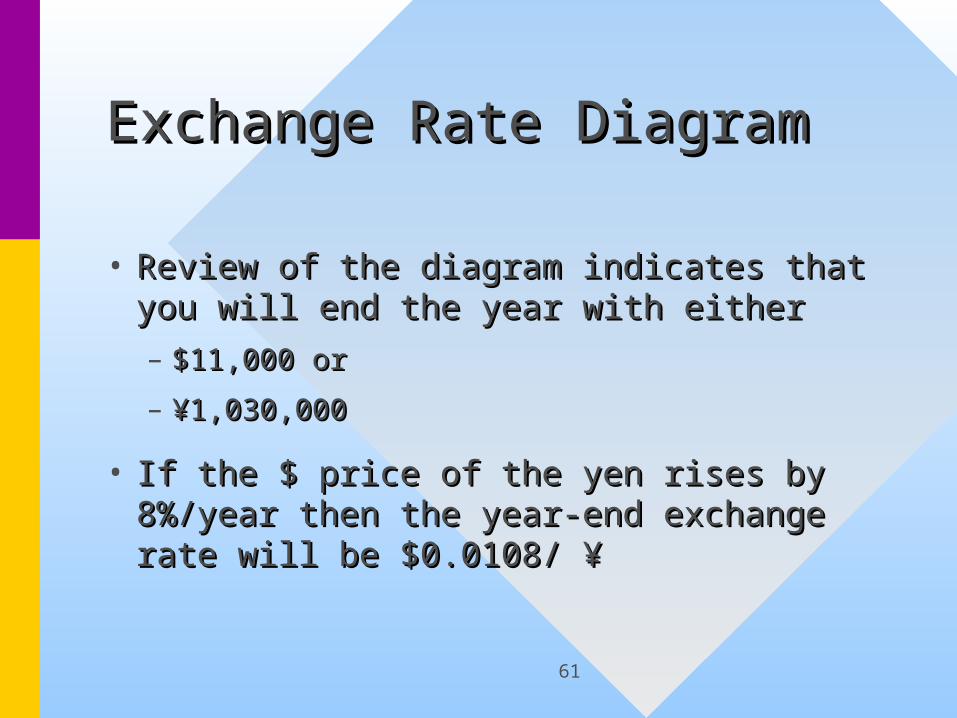

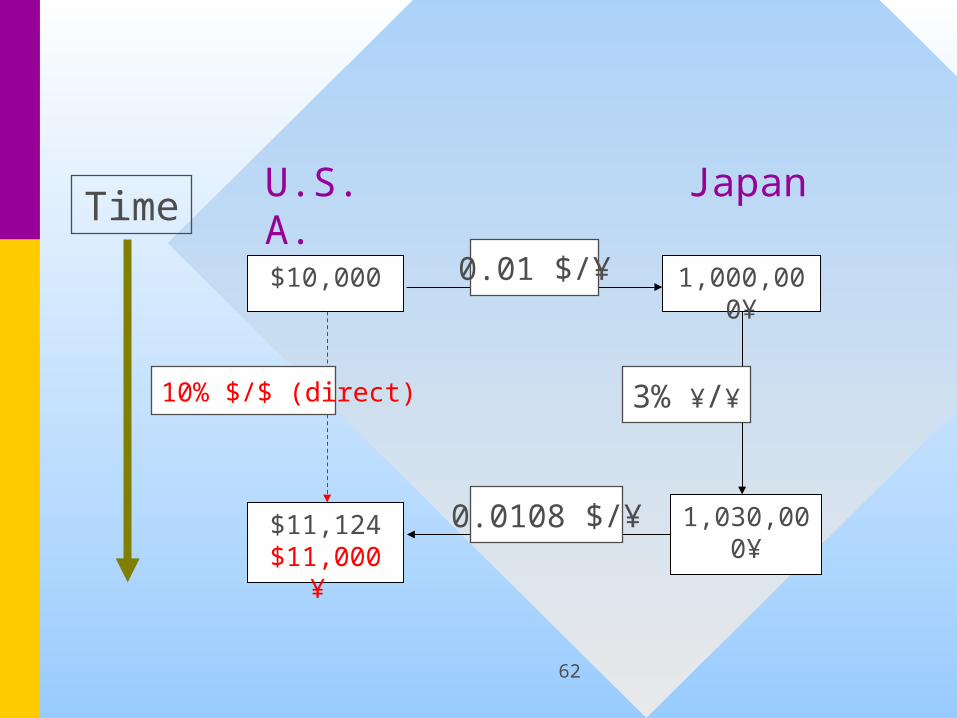

Exchange Rate DiagramExchange Rate Diagram

• Review of the diagram indicates that Review of the diagram indicates that you will end the year with eitheryou will end the year with either– $11,000 or$11,000 or

– ¥1,030,000¥1,030,000

• If the $ price of the yen rises by If the $ price of the yen rises by 8%/year then the year-end exchange 8%/year then the year-end exchange rate will be $0.0108/ ¥rate will be $0.0108/ ¥

62

$10,000

$11,124$11,000 ¥

1,000,000¥

1,030,000¥

Time

10% $/$ (direct)

0.01 $/¥

3% ¥/¥

0.0108 $/¥

U.S.A.

Japan

63

Interpretation and Interpretation and Another ScenarioAnother Scenario

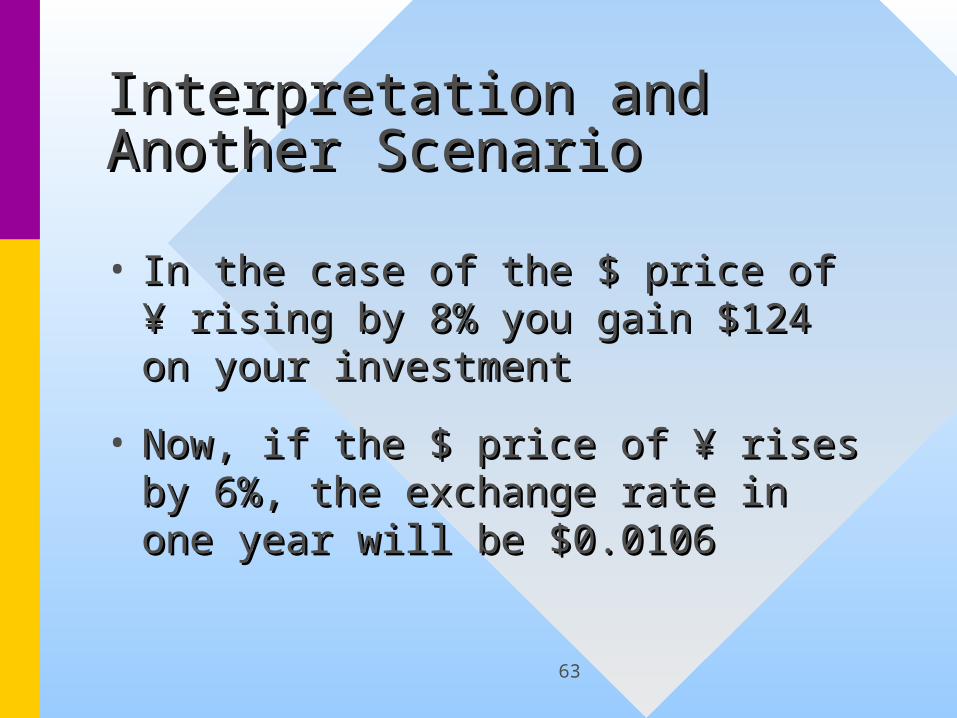

• In the case of the $ price of ¥ rising In the case of the $ price of ¥ rising by 8% you gain $124 on your by 8% you gain $124 on your investmentinvestment

• Now, if the $ price of ¥ rises by 6%, Now, if the $ price of ¥ rises by 6%, the exchange rate in one year will the exchange rate in one year will be $0.0106be $0.0106

64

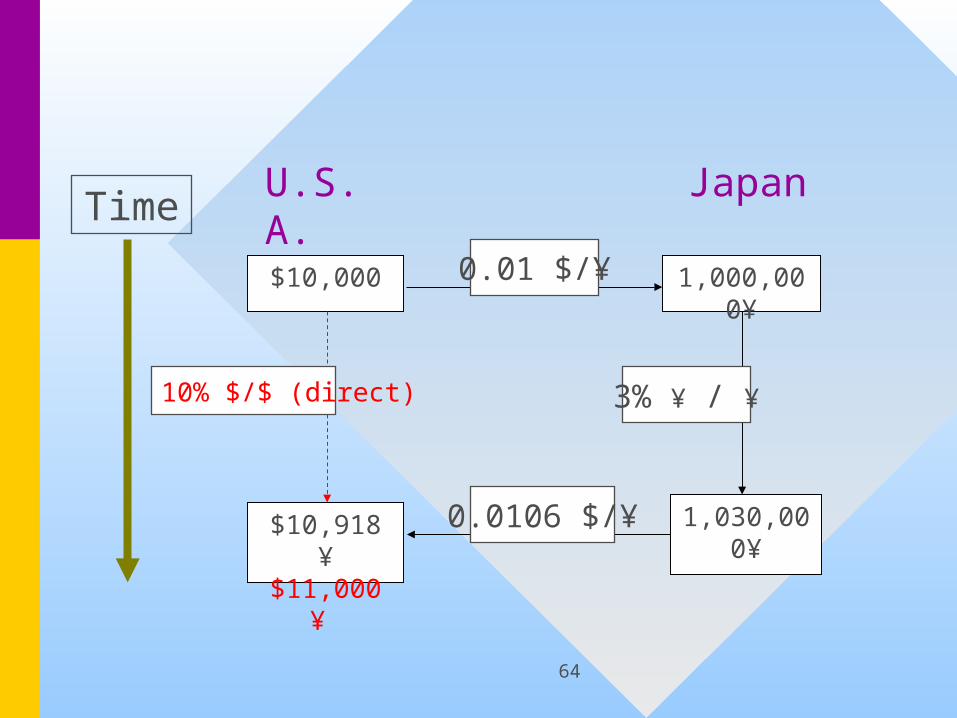

$10,000

$10,918 ¥$11,000 ¥

1,000,000¥

1,030,000¥

Time

10% $/$ (direct)

0.01 $/¥

3% ¥ / ¥

0.0106 $/¥

U.S.A.

Japan

65

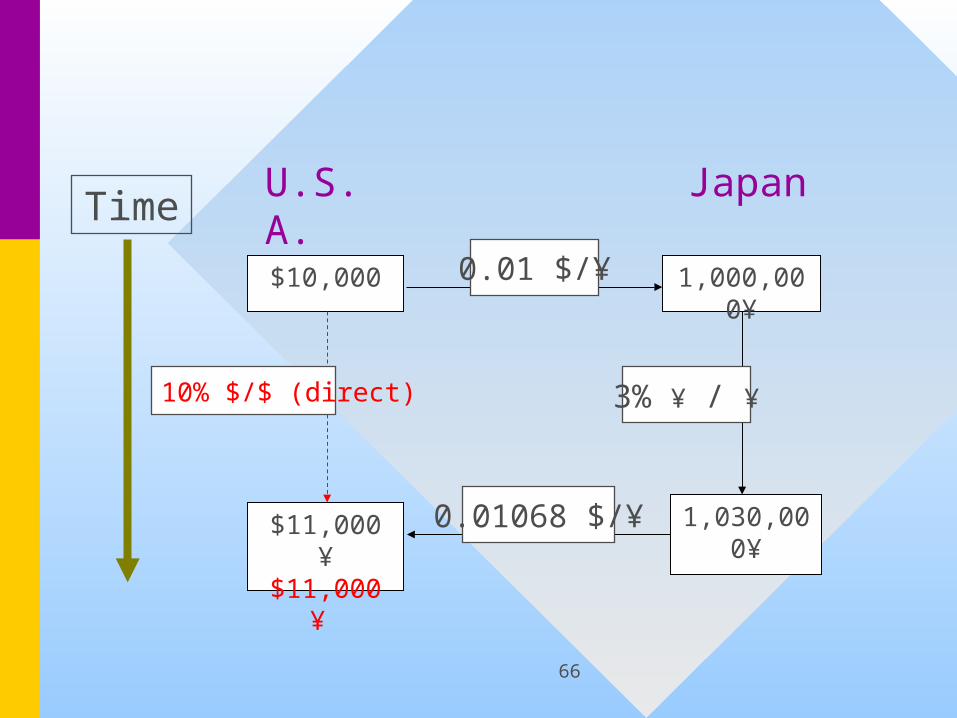

Interpretation Interpretation

• In this case, you will lose $82 by In this case, you will lose $82 by investing in the Japanese bondinvesting in the Japanese bond

• If you divide proceeds of the US If you divide proceeds of the US investment by those of the Japanese investment by those of the Japanese investment, you obtain the exchange investment, you obtain the exchange rate at which you are indifferentrate at which you are indifferent

• $11,000/¥1,030,000 = 0.1068 $/¥$11,000/¥1,030,000 = 0.1068 $/¥

66

$10,000

$11,000 ¥$11,000 ¥

1,000,000¥

1,030,000¥

Time

10% $/$ (direct)

0.01 $/¥

3% ¥ / ¥

0.01068 $/¥

U.S.A.

Japan

67

ConclusionConclusion

• If the yen price actually rises by If the yen price actually rises by more than 6.8% during the coming more than 6.8% during the coming year then the yen bond is a better year then the yen bond is a better investmentinvestment

68

4.10 Inflation and DCF 4.10 Inflation and DCF AnalysisAnalysis

• We will use the notationWe will use the notation

– IInn the rate of interest in nominal terms the rate of interest in nominal terms

– IIrr the rate of interest in real terms the rate of interest in real terms

– R the rate of inflationR the rate of inflation

• From chapter 2 we have the From chapter 2 we have the relationshiprelationship

r

rii

r

ii n

rn

r

11

11

69

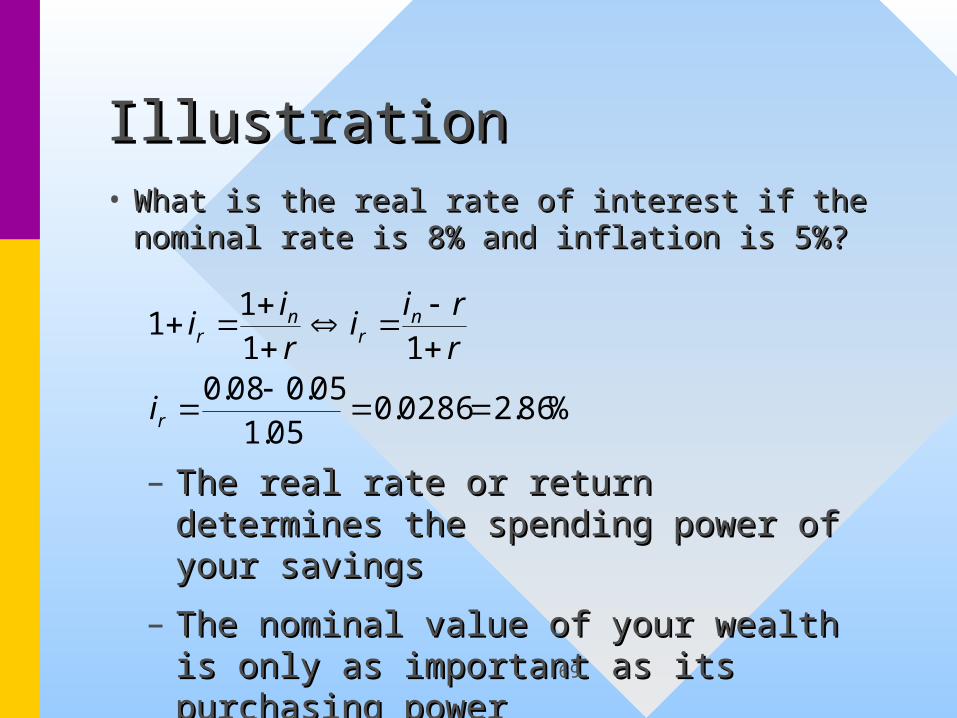

IllustrationIllustration

%86.20286.005.1

05.008.011

11

r

nr

nr

i

r

rii

r

ii

• What is the real rate of interest if the What is the real rate of interest if the nominal rate is 8% and inflation is 5%?nominal rate is 8% and inflation is 5%?

– The real rate or return determines the The real rate or return determines the spending power of your savings spending power of your savings

– The nominal value of your wealth is The nominal value of your wealth is only as important as its purchasing only as important as its purchasing powerpower

70

Investing in Inflation-Investing in Inflation-protected CD’sprotected CD’s• You have decided to invest $10,000 You have decided to invest $10,000

for the next 12-months. You are for the next 12-months. You are offered two choicesoffered two choices

• A nominal CD paying a 8% returnA nominal CD paying a 8% return

• A real CD paying 3% + inflation rateA real CD paying 3% + inflation rate

• If you anticipate the inflation beingIf you anticipate the inflation being• Below 5% invest in the nominal securityBelow 5% invest in the nominal security

• Above 5% invest in the real securityAbove 5% invest in the real security

• Equal to 5% invest in either Equal to 5% invest in either