1 finance school of management objective explain the concept of compounding and discounting and to...

TRANSCRIPT

1

FinanceFinance School of Management School of Management

ObjectiveExplain the concept of compounding

and discounting and to provide examples of real life

applications

Chapter 4: Time Value of MoneyChapter 4: Time Value of Money

2

FinanceFinance School of Management School of Management

Chapter 4 ContentsChapter 4 Contents

Compounding Frequency of Compounding Present Value and

Discounting Alternative Discounted

Cash Flow Decision Rules Multiple Cash Flows Annuities

Perpetual Annuities Loan Amortization Exchange Rates and Time

Value of Money Inflation and Discounted

Cash Flow Analysis Taxes and Investment

Decisions

3

FinanceFinance School of Management School of Management

Financial DecisionsFinancial Decisions

– Costs and benefits being spread out over time

– The values of sums of money at different dates

– The same amounts of money at different dates have different values.

4

FinanceFinance School of Management School of Management

Time Value of MoneyTime Value of Money

– InterestInterest

– Purchasing powerPurchasing power

– Uncertainty Uncertainty

5

FinanceFinance School of Management School of Management

Compounding Compounding

– Present value (PV)

– Future value (FV)

– Simple interest: the interest on the original principal

– Compound interest: the interest on the interest

– Future value factor

6

FinanceFinance School of Management School of Management

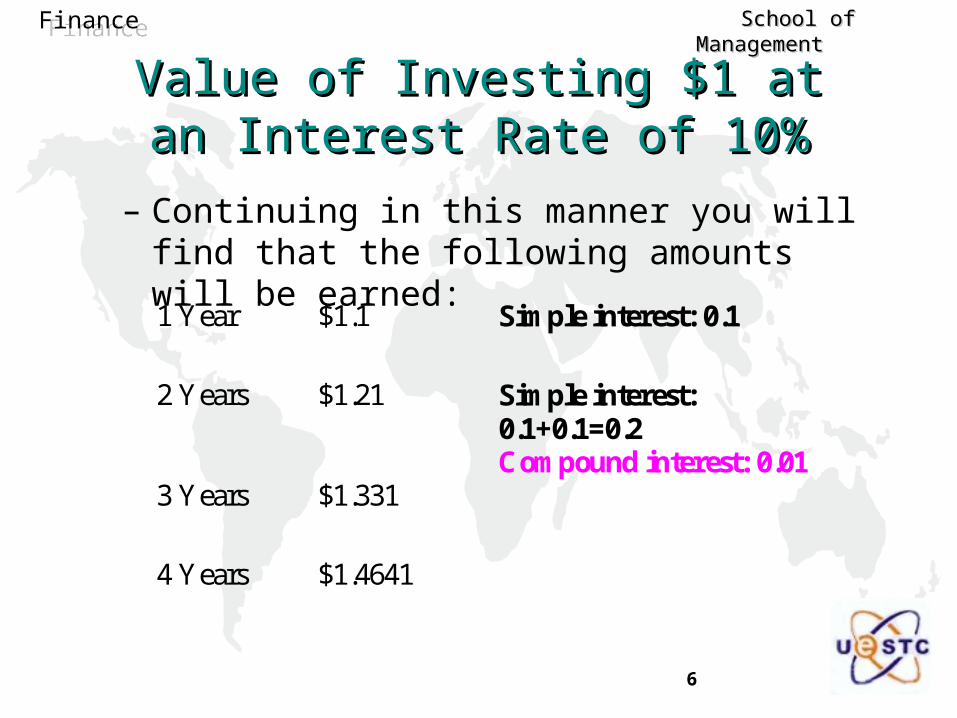

Value of Investing $1 at an Interest Value of Investing $1 at an Interest Rate of 10%Rate of 10%

– Continuing in this manner you will find that the following amounts will be earned:

1 Year $1.1 Simple interest: 0.1

2 Years $1.21 Simple interest: 0.1+0.1=0.2 Compound interest: 0.01

3 Years $1.331

4 Years $1.4641

7

FinanceFinance School of Management School of Management

Value of $5 InvestedValue of $5 Invested

– More generally, with an investment of $5 at More generally, with an investment of $5 at 10% we obtain10% we obtain

1 Year $5*(1+0.10) $5.5

2 years $5.5*(1+0.10) $6.05

3 years $6.05*(1+0.10) $6.655

4 Years $6.655*(1+0.10) $7.3205

8

FinanceFinance School of Management School of Management

Value of $5 InvestedValue of $5 Invested

– If we can earn 10% interest on the principal $5, If we can earn 10% interest on the principal $5, then after 4 yearsthen after 4 years

2305.7)1.01(5 4 FV

9

FinanceFinance School of Management School of Management

Future Value of a Lump SumFuture Value of a Lump SumniPVFV )1(*

FV with growths from -6% to +6%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0 2 4 6 8 10 12 14 16 18 20

Years

Fu

ture

Va

lue

of

$1

00

0

6%

4%

2%

0%

-2%

-4%-6%

10

FinanceFinance School of Management School of Management

Example: Future Value of a Lump SumExample: Future Value of a Lump Sum

Your bank offers a CD (Certificate of Deposit) with an interest rate of 3% for a 5 year investments.

You wish to invest $1,500 for 5 years, how much will your investment be worth?

1111145.1738$

)03.01(*1500$

)1(*5

niPVFV

n 5 i 3%

PV 1,500 FV ? Result 1738.911111

11

FinanceFinance School of Management School of Management

Example: Reinvesting at a Different RateExample: Reinvesting at a Different Rate

You have $10,000 to invest for two years.

Two years CDs and one year CDs are paying 7% and 6% per year respectively.

What should you do? Reinvestment rate? You are sure the interest

rate on one-year CDs will be 8% next year.

With the two-year CD

449,11$

)07.1(000,10$ 2

FV

With the sequence of two one-year CDs

$10,000 1.06 1.08

$11,448

FV

12

FinanceFinance School of Management School of Management

Frequency of CompoundingFrequency of Compounding

– Annual percentage rate (APR)

– Effective annual rate (EFF)

Suppose you invest $1 in a CD, earning interest at a stated APR of 6% per year compounded monthly.

06168.1)12/06.01(1$ 12 FV

General formula

11

m

m

APREFF

13

FinanceFinance School of Management School of Management

Effective Annual Rates of an APR of 18%Effective Annual Rates of an APR of 18%

Annual Percentage rate

Frequency of Compounding

Annual Effective Rate

18 1 18.00

18 2 18.81 18 4 19.25 18 12 19.56 18 52 19.68 18 365 19.72

14

FinanceFinance School of Management School of Management

The Frequency of CompoundingThe Frequency of Compounding

11

APRm

me

m

APRLimEFF

Note that as the frequency of compounding increases, so does the annual effective rate.

What occurs as the frequency of compounding rises to infinity?

15

FinanceFinance School of Management School of Management

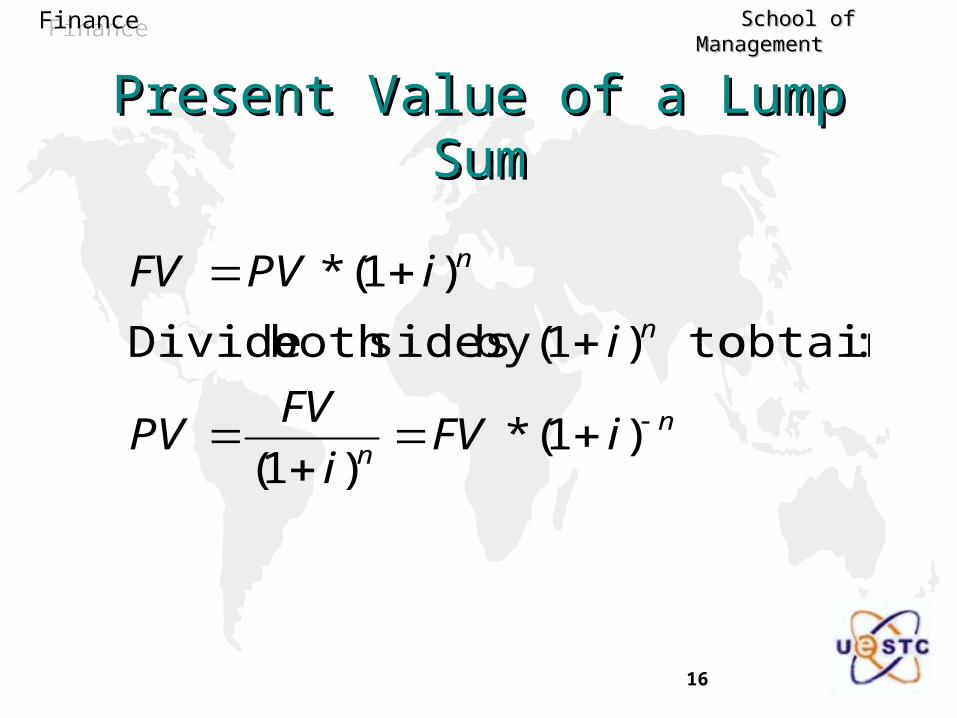

Present ValuePresent Value

– In order to reach a target amount of money at a future date, how much should we invest today?

– Discounting

– Discounted-cash-flow (DCF)

16

FinanceFinance School of Management School of Management

Present Value of a Lump SumPresent Value of a Lump Sum

nn

n

n

iFVi

FVPV

i

iPVFV

)1(*)1(

:obtain to)1(by sidesboth Divide

)1(*

17

FinanceFinance School of Management School of Management

Example: Present Value of a Lump SumExample: Present Value of a Lump Sum

You have been offered $40,000 for your printing business, payable in 2 years.

Given the risk, you require a return of 8%.

What is the present value of the offer?

today55.293,34$

55281.34293

)08.01(

000,40

)1(

2

ni

FVPV

18

FinanceFinance School of Management School of Management

Solving Lump Sum Cash Flow for Solving Lump Sum Cash Flow for Interest RateInterest Rate

1

)1(

)1(

)1(*

n

n

n

n

PVFV

i

PVFV

i

iPVFV

iPVFV

19

FinanceFinance School of Management School of Management

Example: Interest Rate on a Lump Example: Interest Rate on a Lump Sum InvestmentSum Investment

If you invest $15,000 for ten years, you receive $30,000.

What is your annual return?

point) basisnearest the(to %18.7

071773463.0

121211500030000

1

101

1010

n

PVFV

i

20

FinanceFinance School of Management School of Management

Solving Lump Sum Cash Flow for Solving Lump Sum Cash Flow for Number of PeriodsNumber of Periods

iPVFV

iPVFV

n

iniPV

FV

iPV

FV

iPVFV

n

n

n

1ln

lnln

1ln

ln

1ln*)1(lnln

)1(

)1(*

21

FinanceFinance School of Management School of Management

NPV (Net Present Value) RuleNPV (Net Present Value) Rule

– NPV

– NPV rule: Accept a project if its NPV is positive.

– Opportunity cost of capital: The rate (of return) we could earn somewhere else if we did not invest in the project under evaluation.

– Yield to maturity or Internal Rate of Return (IRR)

22

FinanceFinance School of Management School of Management

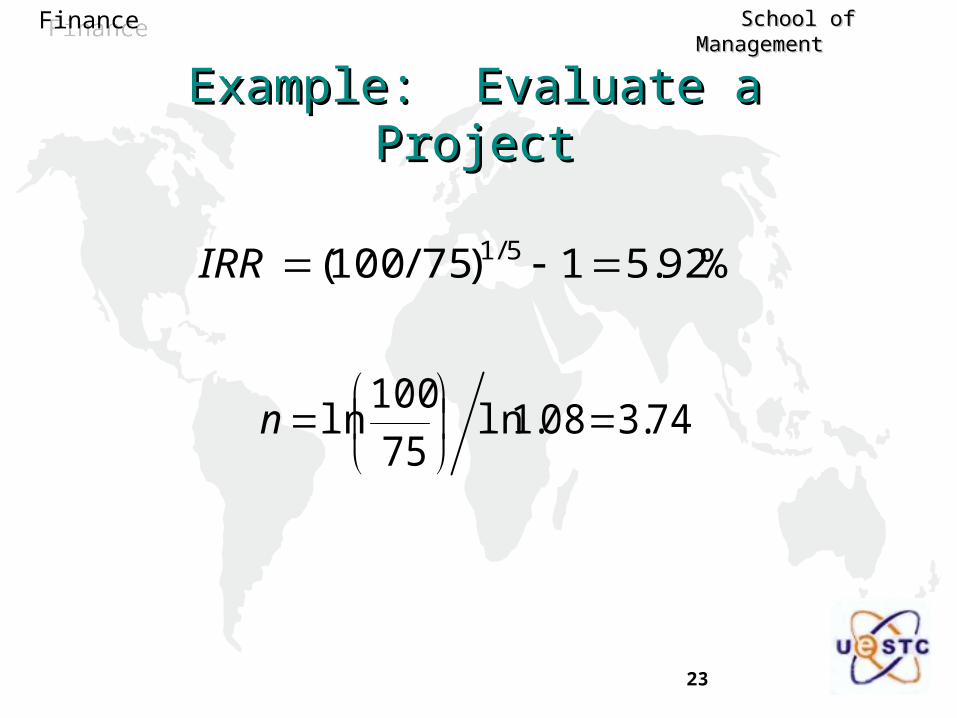

Example: Evaluate a ProjectExample: Evaluate a Project

A five-year savings bond with face value $100 is selling for a price of $75.

Your next-best alternative for investing is an 8% bank account.

Is the savings bond a good project?

94.6$

75$06.68$

75$08.1

100$5

NPV

20.110$

08.175$ 5

FV

23

FinanceFinance School of Management School of Management

Example: Evaluate a ProjectExample: Evaluate a Project

%92.51)75/100( 5/1 IRR

74.308.1ln75

100ln

n

24

FinanceFinance School of Management School of Management

Example: BorrowingExample: Borrowing You need to borrow

$5,000 to buy a car. A bank can offer you a

loan at an interest rate of 12%.

A friend says he will lend the $5,000 if you pay him $9,000 in four years.

Should you borrow from the bank or the friend?

4

$9,000$5,000

1.12$719.66

NPV

25

FinanceFinance School of Management School of Management

PV of Annuity FormulaPV of Annuity Formula

i

iPMT

i

PMT

i

PMT

i

PMTPV

n

n

)1(1

)1()1()1( 21

26

FinanceFinance School of Management School of Management

Example: Buying an AnnuityExample: Buying an Annuity

You are 65 years old and expect to live until age 80.

For a cost of $10,000, an insurance company will pay you $1,000 per year for the rest of your life.

You can earn 8% per year on your money in a bank account.

Does it pay to buy the insurance policy?

52.440,1$

%8

%)81(1000,1$

000,10$15

NPV

%56.5i

21n

27

FinanceFinance School of Management School of Management

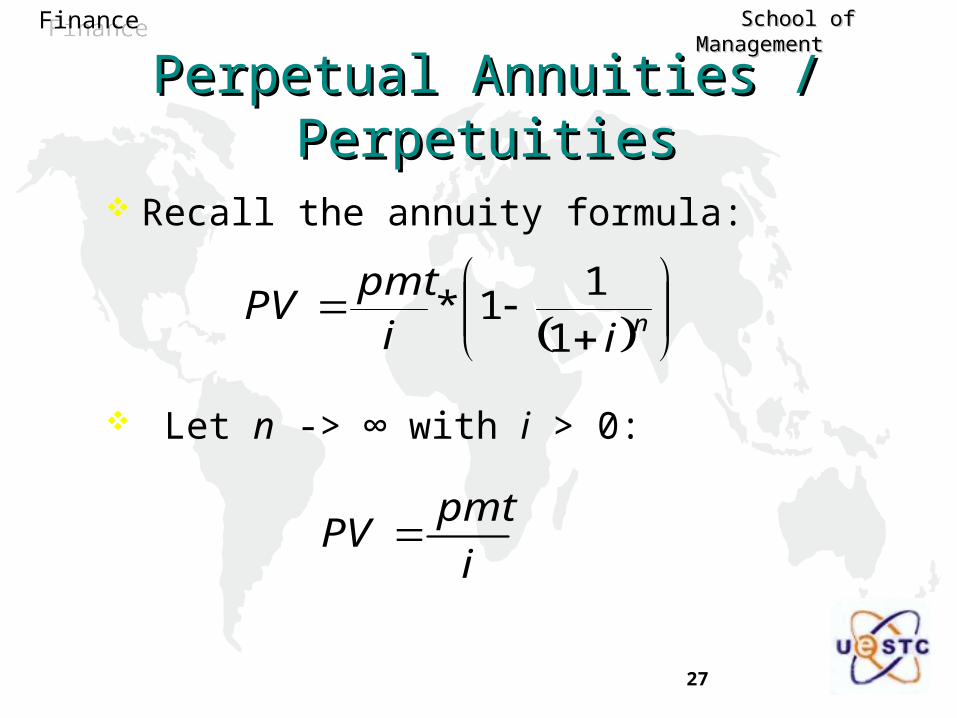

Perpetual Annuities / PerpetuitiesPerpetual Annuities / Perpetuities

Recall the annuity formula:

niipmt

PV1

11*

Let n -> ∞ with i > 0:

i

pmtPV

28

FinanceFinance School of Management School of Management

Loan AmortizationLoan Amortization

Home mortgage loans or car loans are repaid in equal periodic installments.

Part of each payment is interest on the outstanding balance of the loan.

Part is repayment of principal. The portion of the payment that goes toward the

payment of interest is lower than the previous period’s interest payment.

The portion that goes toward repayment of principal is greater than the previous period’s.

29

FinanceFinance School of Management School of Management

Calculator SolutionCalculator Solution

n i PV FV PMT Result

3 9% 100,000 0 ? -39,505.48

This is

the yearly

repayment

30

FinanceFinance School of Management School of Management

Amortization Schedule for 3-Year Amortization Schedule for 3-Year Loan at 9%Loan at 9%

Year BeginningBanlance

Total Payment

Interest Paid

Principal Paid

Remaining Balance

1 2 3

100,000 69,495 36,244

39,505 39,505 39,505

9,000 6,255 3,262

30,505 33,252 36,244

69,495 36,244 0

31

FinanceFinance School of Management School of Management

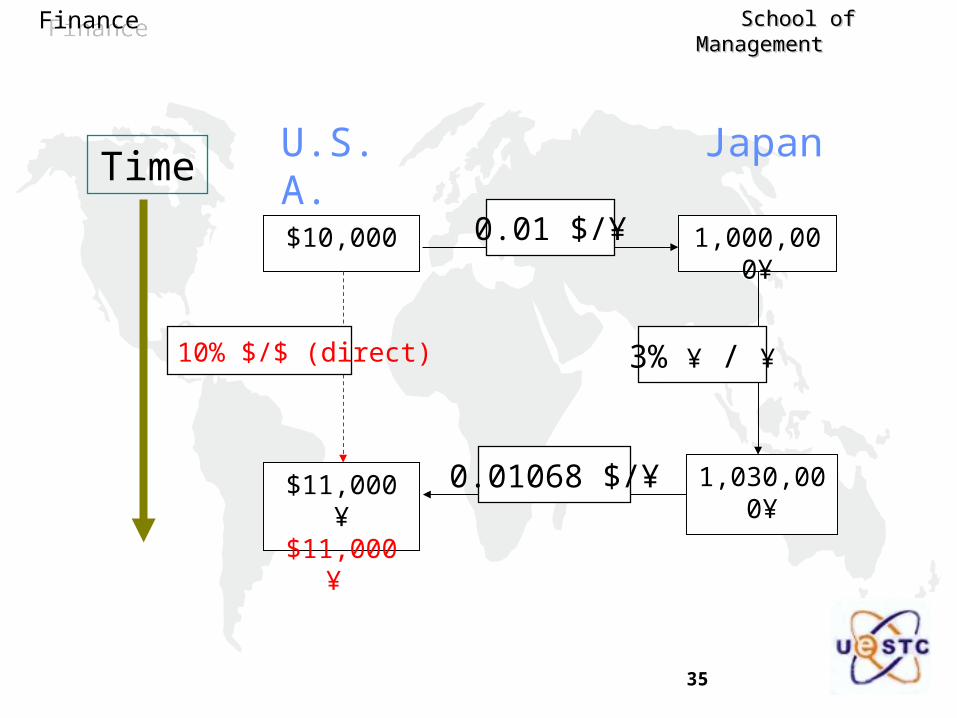

Example: Exchange RatesExample: Exchange Rates

Investing $10,000 in dollar-denominated bonds offering an interest rate of 10% per year

Investing in yen-denominated bonds offering an interest rate of 3% per year

The exchange rate for the yen is now $0.01 per yen.

Which is the better investment for the next year?

32

FinanceFinance School of Management School of Management

$10,000

$11,000 ¥

1,000,000¥

1,030,000¥

Time

10% $/$ (direct)

0.01 $/¥

3% ¥ / ¥

? $/¥

U.S.A.

Japan

33

FinanceFinance School of Management School of Management

$10,000

$11,124$11,000 ¥

1,000,000¥

1,030,000¥

Time

10% $/$ (direct)

0.01 $/¥

3% ¥/¥

0.0108 $/¥

U.S.A.

Japan

34

FinanceFinance School of Management School of Management

$10,000

$10,918 ¥$11,000 ¥

1,000,000¥

1,030,000¥

Time

10% $/$ (direct)

0.01 $/¥

3% ¥ / ¥

0.0106 $/¥

U.S.A.

Japan

35

FinanceFinance School of Management School of Management

$10,000

$11,000 ¥$11,000 ¥

1,000,000¥

1,030,000¥

Time

10% $/$ (direct)

0.01 $/¥

3% ¥ / ¥

0.01068 $/¥

U.S.A.

Japan

36

FinanceFinance School of Management School of Management

The Real Rate of InterestThe Real Rate of Interest

inflation of Rate

rate interest Nominalrate interest Real

1

11

inflation of Rate

inflation of Rate-rate interest Nominalrate interest Real

1

37

FinanceFinance School of Management School of Management

Switch to a Gas Heat ?Switch to a Gas Heat ?

You currently heat your house with oil and your annual heating bill is $2,000.

By converting to gas heat, you estimate that this year you could cut your heating bill by $500.

You think the cost differential between gas and oil is likely to remain the same for many years.

The cost of installing a gas heating system is $10,000. Your alternative use of the money is to leave it in a

bank account earning an interest rate of 8% per year. Is the conversion worthwhile?

38

FinanceFinance School of Management School of Management

Switch to a Gas Heat ?Switch to a Gas Heat ?

Assume that the $500 cost differential will remain forever. The investment in switch of heating is a perpetuity, i.e. paying

$10,000 now for getting $500 per year forever.

If the $500 cost differential will increase over time with the general rate of inflation, then the 5% rate of return is a real rate of return.

The conversion is not worthwhile unless the rate of inflation is greater than 2.875% per year.

%875.205.1/)05.008.0(

%5000,10$/500$ i

39

FinanceFinance School of Management School of Management

Taxes Taxes

rate interest tax Beforerate Tax

rate interest tax After

)1(

40

FinanceFinance School of Management School of Management

Taking Advantage of a Tax LoopholeTaking Advantage of a Tax Loophole

You are in a 40% tax bracket and currently have $100,000 invested in municipal bonds earning a tax-exempt rate of interest of 6% per year.

Now you buy a house at a cost of $100,000.

A bank offers a loan for you at an interest rate of 8% per year.

Does it pays for you to borrow?

%8.48)4.01(

%

rate interest tax After