1 bear stearns 18 th annual healthcare conference sept 13, 2005

TRANSCRIPT

1

Bear Stearns 18th Annual Healthcare

Conference Sept 13, 2005

2

Statements included in this presentation or in the oral comments made as part of this presentation may contain forward-looking statements, including but not limited to statements of the Company’s plans, objectives, expectations or intentions, that involve risk and uncertainties.

The Company’s actual results may differ significantly from those projected or suggested in any forward-looking statement due to a variety of factors, which are discussed in detail in the Company’s filings with the Securities and Exchange Commission.

Forward-Looking Statements

3

Our Interests are Aligned with Clients and Patients:

To make the use of prescription drugs safer and

more affordable

4

More Number of Drugs Fewer

Ben

efi

t O

pti

on

s

Impact on Client

Impact on Patient

Impact on ESI

Lower drug cost

More choice

Lower co payment

More choice

Higher Profit/Rx

More Flexibility

Alignment –Formulary Management

Therapy Class

We Provide Flexible Management of

the Supply Chain 1. Select number of drugs in therapy class 2. Determine formulary control 3. Drive towards lowest overall cost

# ofdrugs

# ofdrugs

# ofdrugs

Open

DifferentialCo-pay

ClosedLowestOverall

Cost

5

Alignment - Retail Network Management

States

Available Pharmaci

es

Most Inclusive Network

Most Restrictiv

e Network

TRICARE Access

Minimum

CA 5,644 5,071 3,881 283NY 4,444 4,224 1,829 300TX 4,236 3,821 1,827 579FL 4,020 3,670 1,966 469PA 2,970 2,825 1,687 432

Greater Management

•Higher Profit/Rx•More Flexibility

•Lower co payment•More choice

•Lower drug cost•More choice

•Impact on ESI•Impact on Patient•Impact on Client

Higher Profit/RxLower co paymentLower drug cost

Impact on ESIImpact on PatientImpact on Client

6

Impact on Client

Impact on Patient

Impact on ESI

Lower drug cost

Lower co payment

Higher Profit/Rx

Alignment – Clinical Programs

4.5

13.0

0

2

4

6

8

10

12

14

Mil

lio

ns

Q1 2003 Q4 2004

Members in Step Therapy Programs

Clients using step therapy realize on average a

2 percentage point increase in generic utilization

Plan Designs Encourage Greater Use of

Generics and Preferred Low-cost Brands

7

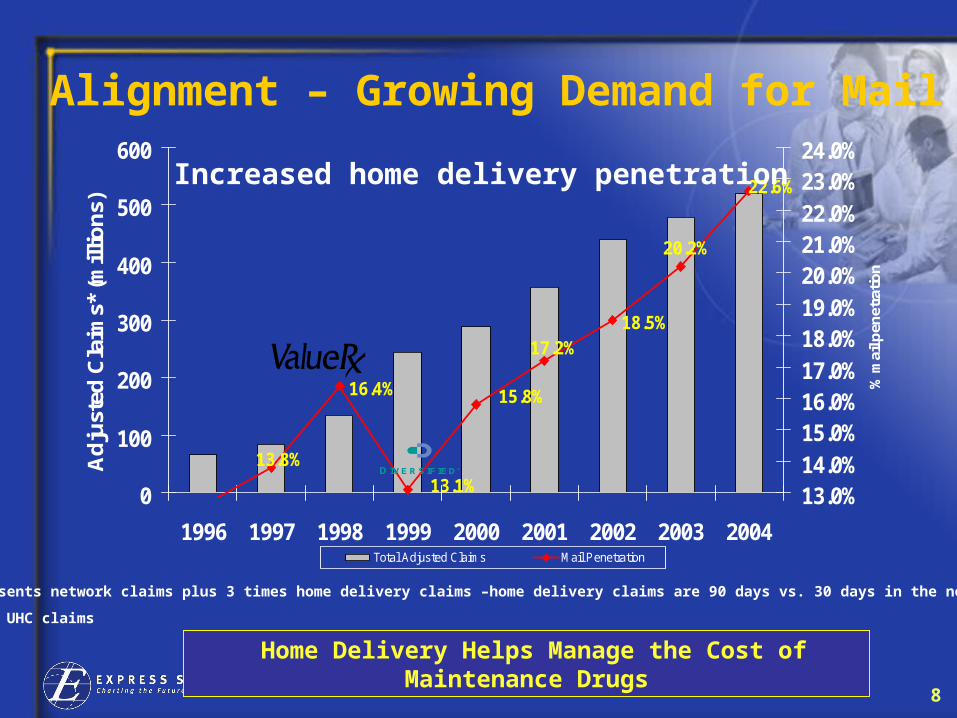

Alignment – Home Delivery

Impact on Client

Impact on Patient

Impact on ESI

Lower drug cost

Choice

Lower co paymentChoice

Higher profit/Rx

We Offer Highly Efficient, Cost-effective

Home Delivery

8

16.4%

18.5%

22.6%

20.2%

17.2%

13.8%

15.8%

13.1%0

100

200

300

400

500

600

1996 1997 1998 1999 2000 2001 2002 2003 2004

Ad

just

ed C

laim

s* (

mill

ion

s)

13.0%14.0%15.0%16.0%17.0%18.0%19.0%20.0%21.0%22.0%23.0%24.0%

% m

ail p

enet

ratio

n

Total Adjusted Claims Mail Penetration

* Represents network claims plus 3 times home delivery claims –home delivery claims are 90 days vs. 30 days in the network.

Excludes UHC claims

D IVERSIFIED®

Increased home delivery penetration

Home Delivery Helps Manage the Cost of Maintenance Drugs

Alignment – Growing Demand for Mail

9

Alignment – Generic Utilization

Generic Utilization Rate

38%40%42%44%46%48%50%52%54%

Q102

Q202

Q302

Q402

Q103

Q203

Q303

Q403

Q104

Q204

Q304

Q404

Q105

Q205

ESI PBM B PBM C

Impact on Client

Impact on Patient

Impact on ESI

Lowest drug cost

Lowest co payment

Highest profit/Rx

Source: From public filings

Express Scripts Leads in Generic Utilization

10

$10.3

$11.3

$10.4 $10.4

$9.8

$7

$8

$9

$10

$11

$12

$ -

bil

lio

ns

2005 2006 2007 2008 2009

U.S. Sales for Brand Products with Patent Expirations From 2005-2009

ESI Analysis

Represents

over 20%

of 2004

branded

drug sales

Our Clients and Members Will Benefit From a Growing Generic Opportunity

Alignment – Growing Generic Opportunity

11

100%$35 Total

19%3.5Other

1%0.5Growth Hormone

1%0.5Infertility

2%0.6RSV prophylaxis

4%1.5Rheumatoid arthritis

4%1.5Multiple sclerosis

4%1.5Transplant

5%1.6Hepatitis C

5%1.6Hemophilia

9%3.2Renal

10%3.4HIV/AIDS

36% $12.6Oncology

Biotech Market, $35B, 18%

Traditional Rx Market,

$155B, 82%

Alignment – Specialty Pharmacy

Specialty Market

2004

Billions

Source: ESI Analysis

Impact on Client

Impact on Patient

Impact on ESI

Lower drug cost

Lower co payment

Higher profit/Rx

Improved reporting

Improved quality of

care

Higher client

satisfaction

Clients are Seeking Solutions for High-cost

Specialty Drugs

12

2006 Upsell Pipeline is Strong

• Significant potential to continue to manage client trends in key product categories

• New products continue to be developed and rolled out

• Strong track record of success

10,000

('000

Liv

es)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Hom

e Del

iver

y

Gener

ic E

nfor

cem

ent

Nar

rowin

g Fo

rmul

arie

s

New

Clin

ical

Pro

duct

s

Spec

ialty

/Cur

aScr

ipt

Thre

e Ti

er

Sold Weighted Pipeline

13

What Are the Savings?

Availability of Proven PBM Cost Management Tools Will Produce 20%–25% Savings (CBO)

Paid byCash Customer

at Pharmacy

Retail, Clinical.Formulary

And RebateSavings 24% Mail Savings

6%

Paid byExpress ScriptsClients

Total Savings 30%

COST

Retail Pharmacy Cash Price

Express Scripts Client Savings

Express Scripts Client Costs

14

Alignment – A Win-Win-Win Proposition

Retail Non-pref. Brand

Retail Pref.

BrandGenerics

Mail Pharma

cy

Increased Savings

Opportunities:

Client

Member

Increased

Profit

Opportunities:

Express Scripts

Moving to preferred brands, mail and generics

We make money by saving clients and members money

Moving to preferred brands, mail and generics

Moving to preferred brands, mail and generics

15

Client Satisfaction Steadily Improving

• Service and satisfaction metrics have increased consistently quarter over quarter since 2003 with an early spike in 2005

Exceed60%

65%

70%

75%

80%

85%

90%

95%

100%

ESI PerformanceExpectations

Likelihood toRecommend

Likelihood toRenew

2003

2004

1q05

16

Our Financial Results

Express Scripts has demonstrated a proven track

record

17

Financial OverviewQ2 2005 Highlights

– Adjusted EPS of $0.60*, up 30% from $0.46* last year

– Cash flow from operations of $178.3 M vs. $55.5 M last year

– Generic drugs were 54% of total prescriptions vs. 50% last year

– Gross profit of $276.7 M, up 24% • Gross profit per adjusted claim was $1.96, up

10%• EBITDA per adjusted claim was $1.19, up 4%

– Raised EPS guidance for 2005*Excludes prior period tax benefit of $0.08 in Q2 2005 and non recurring charge of $0.04for early retirement of debt in Q2 2004 – reconciliation of reported EPS to adjusted EPS is included in Table 4 of the 2Q 2005 earnings release

18

Financial Overview

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

Q1'01

Q2'01

Q3'01

Q4'01

Q1'02

Q2'02

Q3'02

Q4'02

Q1'03

Q2'03

Q3'03

Q4'03

Q1'04

Q2'04

Q3'04

Q4'04

Q1'05

Q2'05

Pe

r s

ha

re

EPS Free cash flow per share*

(1) Reflects a $70-$75 million reduction in Q2 2003 due to one-time impact of implementing a new wholesale purchase agreement

(2) Excludes a $0.04 per share charge for the early retirement of debt(3) Excludes a $0.10 charge to increase legal reserves for the cost of defense.(4) Excludes an $0.08 prior period benefit related to state tax planning strategies

Quality of Earnings

(1)(1)

(2)(2)

* Reflects a 12-month moving average of free cash flow (cash from operations less CapX)

(3)(3)(4)(4)

19

Financial Overview

$0.81

$0.88

$1.03 $1.05

$1.19

$1.12

$0.60

$0.80

$1.00

$1.20

2000 2001 2002 2003 2004** 2005***

EBITDA* per adjusted claim

* A reconciliation of EBITDA to net income and to net cash provided by operating activities can be found in the Investor Relations

section of Express Scripts’ Web site, www.express-scripts.com under Presentations.

** Excluding $25 million charge to increase legal reserves for the cost of defense and $5.5 million termination payment received.

*** 2Q ‘05

Pricing can be lowered as clients tighten formulary compliance, increase home delivery, utilize generics and restrict retail networks. These changes result in lower prices to our clients and greater profits to Express Scripts.

9% CAGR

20

Dom MeffePresident and CEO, CuraScript

Senior Vice President, Specialty Pharmacy

Express Scripts’ Value Proposition

Providing a Cost-EffectiveSolution for Specialty Drugs

21

Specialty Pharmacy — The Gathering Storm

Payers’ Dilemma: Looming Costs for Chronic Conditions

Biotechnology Healthcare, April 2005

Biologics’ Looming Price Tag Has Payers Retooling Pharmacy Coverage

Biotechnology Healthcare, April 2005

22

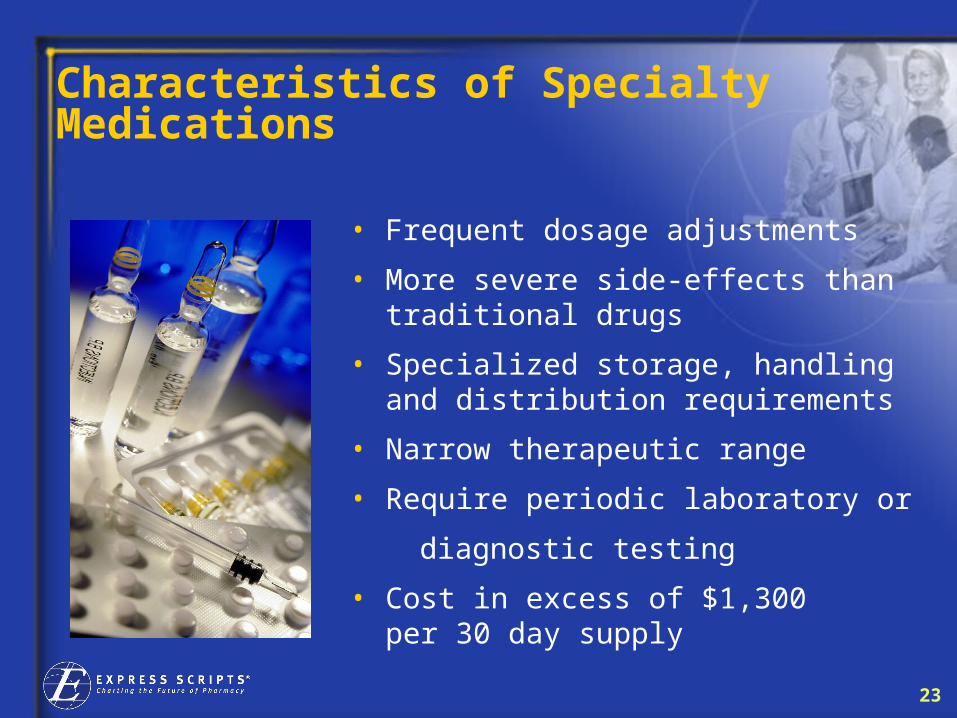

What are Specialty Medications?

• High-cost oral, injectable, infused

or inhaled medications

• Self-administered or administered

by a healthcare provider

• Outpatient or a home setting

23

Characteristics of Specialty Medications

• Frequent dosage adjustments

• More severe side-effects than traditional drugs

• Specialized storage, handling and distribution requirements

• Narrow therapeutic range

• Require periodic laboratory or

diagnostic testing

• Cost in excess of $1,300 per 30 day supply

24

Chemotherapy 32%

ChemotherapySupportive Care 15%

Multiple Sclerosis 9%

Rheumatoid Arthritis 8%

Psoriasis 12%

Hepatitis C 7%

Growth Hormone Deficiency 3%

RSV10%

IVIG 1% Hemophilia 3%

National Specialty Product Mix

$12.53 PMPM

25

Biotech - Rapid Growth

Sources:IMS Data through November 2004Wall Street Equity Research, 2004CMS National Healthcare Expenditure Projection: 2003 – 2013Data on file: CuraScript.

2004 Total Outpatient Pharmacy Spend $190 Billion

2008 Projected Outpatient Pharmacy Spend $283 Billion

Source:PhRMA, International Federation of Pharmaceutical Wholesalers & Biotech Industry Organization

26%26%18%18%

Traditional SpendTraditional Spend$210 Billion$210 Billion

Specialty SpendSpecialty Spend$73 Billion$73 Billion

Specialty SpendSpecialty Spend$35 Billion$35 Billion

Traditional SpendTraditional Spend$155 Billion$155 Billion

Biotech Drugs in DevelopmentBiotech Drugs on the Market

2005Estimated

200019951990

600

500

400

300

200

100

0

600

197

369

92

240

29100

10

Nu

mb

er

of

Dru

gs

26

Routes of Administration Specialty Drug Pipeline

• Late-stage development; Phase II or later

• Majority are injectable

Oncology

1746

26 15* 4**

Rheumatoid Arthritis

520

8 7 5

Hepatitis C

59

8 1

Crohn’s Disease

210

1 7 2

Psoriasis8

2 3 1 2

Multiple Sclerosis

77

5 2

Oral

Injectable

IV

SQ

IM

Unknown

Source: Express Scripts data

27

Current Distribution ChannelsToday’s Wild, Wild West

Typical Payer Injectable SpendTypical Payer Injectable Spend

Retail Pharmacy15%-20%

Retail Pharmacy15%-20%

Mail Order Pharmacy5%-10%

Mail Order Pharmacy5%-10%

Specialty Pharmacy5%-25%

Specialty Pharmacy5%-25%

PhysicianOffice

40%-60%

PhysicianOffice

40%-60%

OutpatientHospital15%-20%

OutpatientHospital15%-20%

Home Care& Infusion5%-10%

Home Care& Infusion5%-10%

Unmanaged injectables result in:

• Inappropriate utilization• Inconsistent clinical

management• Variable reimbursement

Unmanaged injectables result in:

• Inappropriate utilization• Inconsistent clinical

management• Variable reimbursement

• Higher cost for payer• Reduced effectiveness of

treatment• Reduced patient care• Reduced member satisfaction• Physician panel frustration

• Higher cost for payer• Reduced effectiveness of

treatment• Reduced patient care• Reduced member satisfaction• Physician panel frustration

28

Our Specialty Solution

CARE

COST SAVINGS

CONVENIENCE

The CuraScript Difference

Making specialtydrug therapy

more effective and affordable,

one patient at a time

29

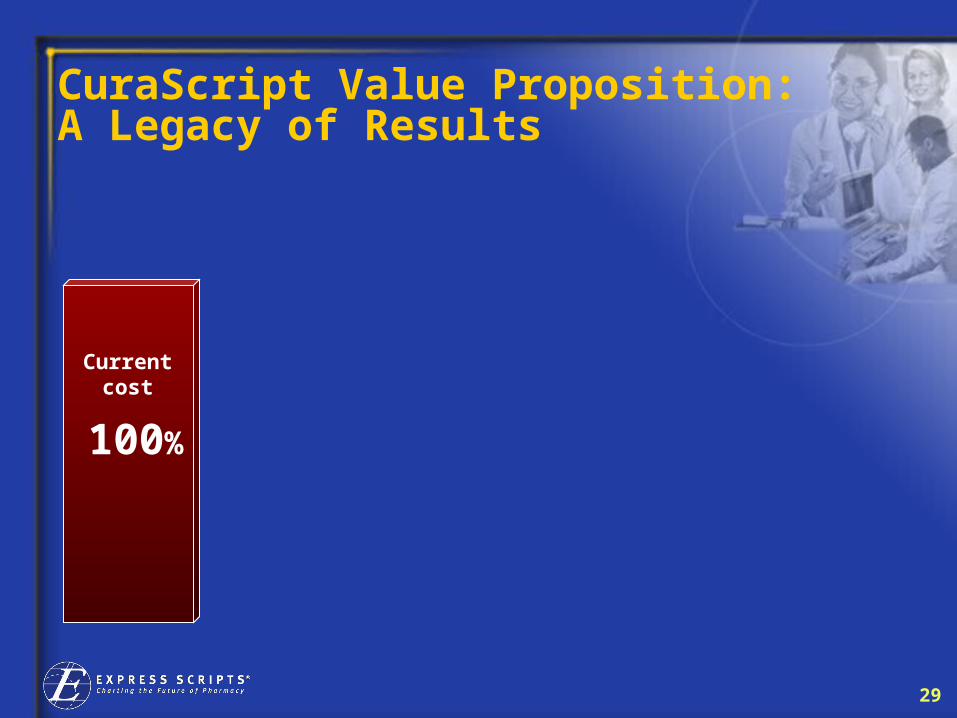

Current cost

100%

CuraScript Value Proposition: A Legacy of Results

30

Current cost

Lower unit costs

7.2% savings

100%

CuraScript Value Proposition: A Legacy of Results

31

Current cost

Lower unit costs

7.2% savings

Clinical based

utilization savings

8.2% savings

100%

CuraScript Value Proposition: A Legacy of Results

32

Current cost

Lower unit costs

7.2% savings

Clinical-based

utilization savings

8.2% savings

5.9% savings

100%

CuraScript Value Proposition: A Legacy of Results

Lower administrati

ve costs

33

Current cost

Lower unit costs

7.2% savings

Clinical based

utilization savings

8.2% savings

5.9% savings

100%

21.3%

savings

overall

CuraScript Value Proposition: A Legacy of Results

Lower administrati

ve costs

34

CARELogic™ Patient Care Management

Tools of the program include:• Patient assessment and risk stratification• Integration of diagnostic and medical data • Dedicated clinical patient support team• Critical pathway management• Intense patient education• Adherence support for medication regimen

compliance• Psychosocial assessment and counseling• Utilization and dose management• Delivery coordination of medication• Outcomes reporting

Care management programs designed to specifically manage a disease state and the related drug therapy

35

CARELogic™ Clinical Management

Initial Clinical Assessment

Initial Clinical Assessment

Disease Specific Clinical Pathway

Initiated

Disease Specific Clinical Pathway

Initiated

Ongoing Clinical Assessment and

Interventions

Ongoing Clinical Assessment and

Interventions

Patient Care CoordinationPatient Care Coordination

Three follow-up

interventions in the first six

months

High risk Clinical assessment and on-going interventions

Patient AdmissionPatient Admission

01/11/05

36

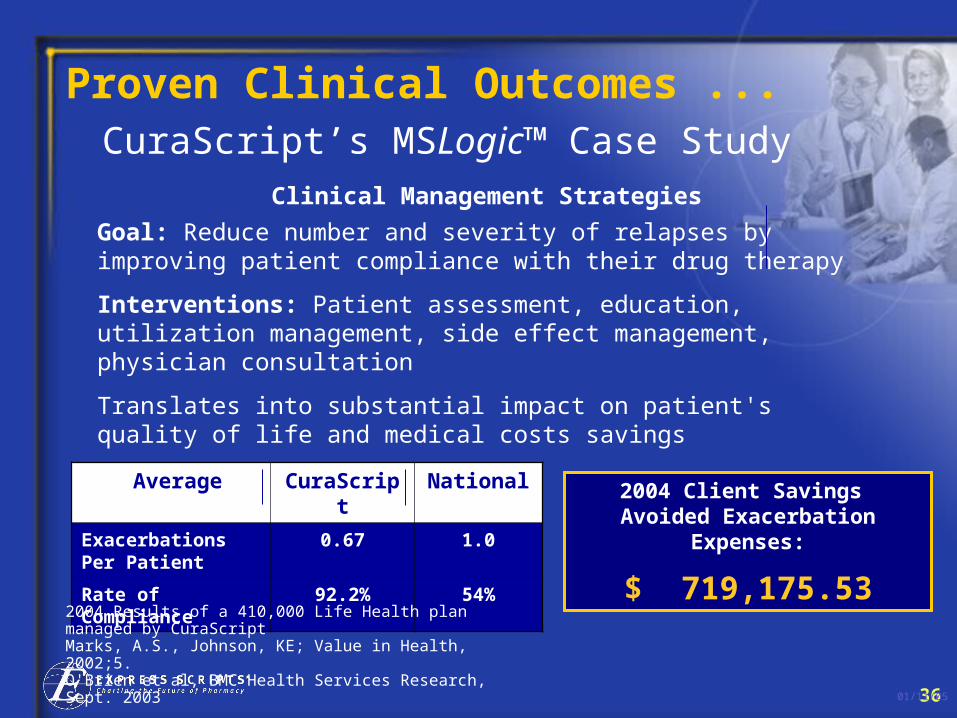

Proven Clinical Outcomes ...CuraScript’s MSLogic™ Case Study

2004 Client Savings Avoided Exacerbation

Expenses:

$ 719,175.53

01/11/05

Average CuraScript

National

Exacerbations Per Patient

0.67 1.0

Rate of Compliance

92.2% 54%2004 Results of a 410,000 Life Health plan managed by CuraScriptMarks, A.S., Johnson, KE; Value in Health, 2002;5.O'Brien et al, BMC Health Services Research, Sept. 2003

Clinical Management Strategies

Goal: Reduce number and severity of relapses by improving patient compliance with their drug therapy

Interventions: Patient assessment, education, utilization management, side effect management, physician consultation

Translates into substantial impact on patient's quality of life and medical costs savings

37

Implementation Expertise

• Program and Benefit Design Consultation• Communication Strategy

• Ongoing Account Management

Ongoing Account Management

• Patient satisfaction• Implement new programs

• Support to the client’s initiatives• Continuous communication strategies

Client satisfaction

38

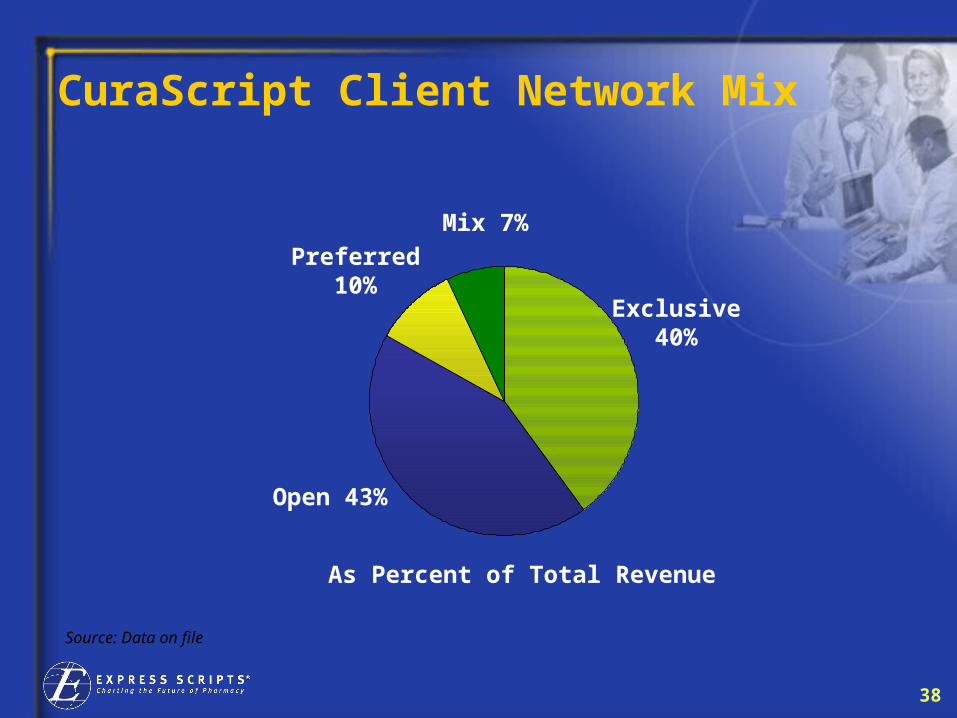

CuraScript Client Network Mix

Preferred10%

Mix 7%

Open 43%

Exclusive40%

As Percent of Total Revenue

Source: Data on file

39

Express Scripts’ specialty penetration has increased from 2% to 30%

in the first 5.5 quarters of our CuraScript acquisition.

Per

cent

age

of P

lan

Cos

ts

Source: Express Scripts Analysis.

82%

73%70% 69%

66%62%

2%

17%20%

25%30%

16%14%

8%9%11%13%13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Q1 2004 Q2 2004 Q3 2004 Q4 2004 Q1 2005 Q2 2005

RetailCuraScriptHome Delivery

CuraScript Penetration intoExpress Scripts

40

Priority Acquisition - Strategic Rationale Creates one of the largest specialty franchises in the U.S.

– $3+ billion annual specialty revenues

– One of the fastest growing sectors in healthcare

– Sector remains fragmented and market structure continues to emerge (greenfield opportunities)

Fills key therapy classes within CuraScript portfolio – “one-stop shopping for clients”

– Infertility (number one fertility franchise)

– Pulmonary Fibrosis

– Pulmonary Hypertension

– Home Infusion Offers additional capabilities

– Specialty distribution capabilities

– Supply chain services Leverages PBM core competencies (payor and manufacturer relationships, mail

order pharmacies, clinical and trend management expertise)

– Synergy potential

– Increased value proposition for clients (single vendor, integrated reporting)

41

Our Value Proposition Will Continue to Drive Growth

• Making the use of drugs safer and more affordable is more important than ever

• Plan sponsors will increasingly deploy our tools

• Express Scripts is well-positioned for sustainable growth

• Strong market fundamentals/new business opportunities • Increased use of home delivery and generic drugs• Growth in management of specialty pharmacy• Productivity and capital structure improvements

• We have taken a different approach• Alignment -- we make money by saving our clients money

• Strategic acquisitions have enhanced our value proposition

42