world economic situation and prospects: key messages · lifting the vat rate in january 2019 may...

TRANSCRIPT

www.bit.ly/wespreport

www.bit.ly/wespreport

Key messages

• On the surface, global economic growth remains steady, masking underlying risks and imbalances

• Confluence of risks threaten short-term outlook: trade tensions, financial fragilities, climate risks

• Economic growth is uneven and is often failing to reach where it is most needed

• Underlying vulnerabilities endanger longer-term progress towards the implementation of the 2030 Agenda for sustainable development

www.bit.ly/wespreport

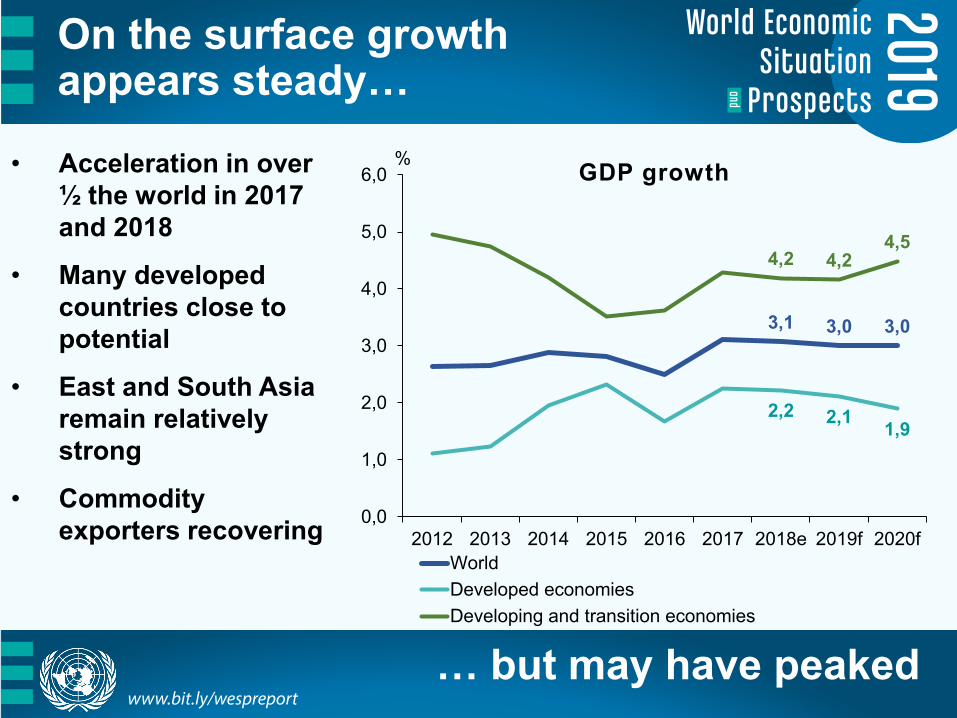

On the surface growth appears steady…

• Acceleration in over ½ the world in 2017 and 2018

• Many developed countries close to potential

• East and South Asia remain relatively strong

• Commodity exporters recovering

3,1 3,0 3,0

2,2 2,1 1,9

4,2 4,24,5

0,0

1,0

2,0

3,0

4,0

5,0

6,0

2012 2013 2014 2015 2016 2017 2018e 2019f 2020f

GDP growth

WorldDeveloped economiesDeveloping and transition economies

… but may have peaked

%

www.bit.ly/wespreport

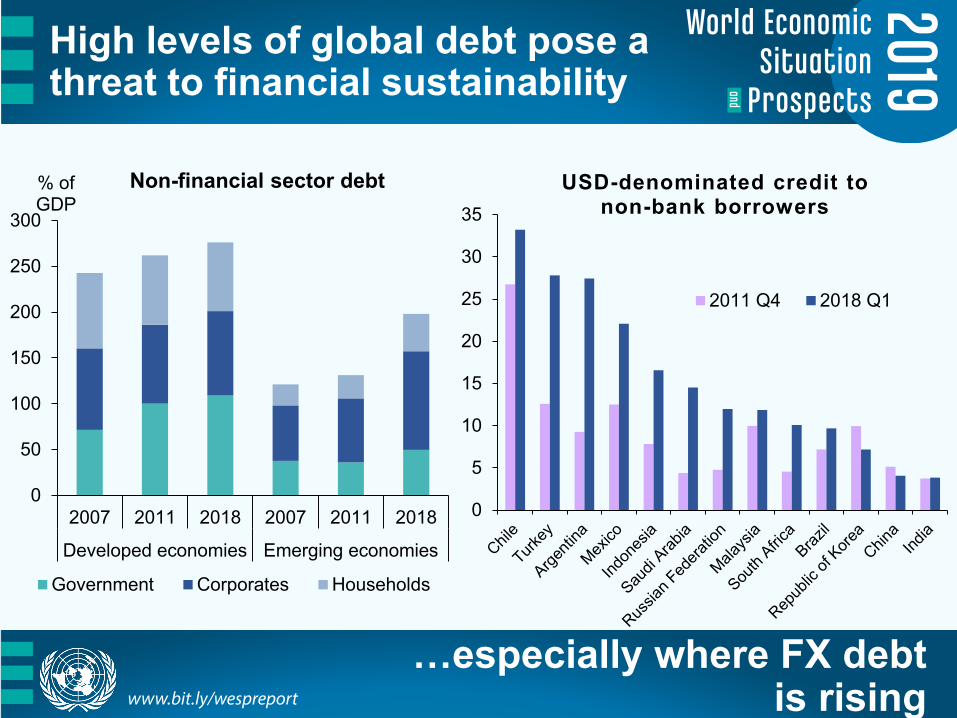

High levels of global debt pose a threat to financial sustainability

0

5

10

15

20

25

30

35USD-denominated credit to

non-bank borrowers

2011 Q4 2018 Q1

…especially where FX debt is rising

0

50

100

150

200

250

300

2007 2011 2018 2007 2011 2018

Developed economies Emerging economies

% of GDP

Non-financial sector debt

Government Corporates Households

www.bit.ly/wespreport

Potential triggers of financial stress

• Global trade tensions• Monetary policy adjustment in developed

economies• Commodity price shocks• Policy disruption in Europe associated with

‘Brexit’• Domestic political or economic disruptions

www.bit.ly/wespreport

Economic growth is uneven…

Disclaimer: The designations employed and the presentation of material on this map do not imply the expression of any opinion whatsoever on the part of the Secretariat of the United Nations concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries.

GDP per capita growth, 2018

…and often failing to reach where it is most needed

www.bit.ly/wespreport

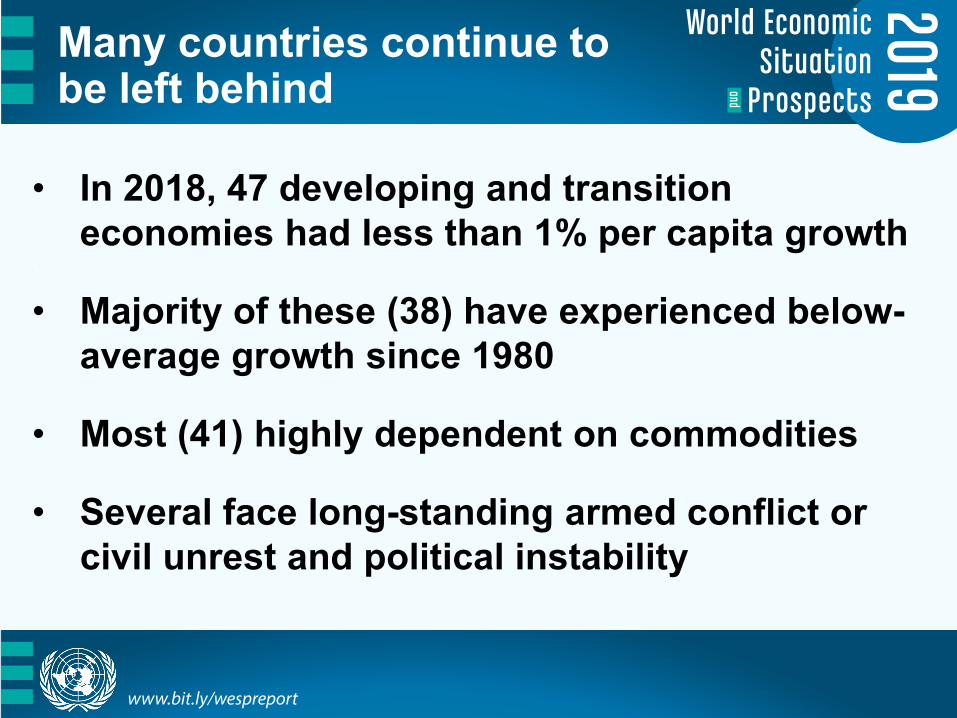

Many countries continue to be left behind

• In 2018, 47 developing and transition economies had less than 1% per capita growth

•

• Majority of these (38) have experienced below-average growth since 1980

• Most (41) highly dependent on commodities

• Several face long-standing armed conflict or civil unrest and political instability

www.bit.ly/wespreport

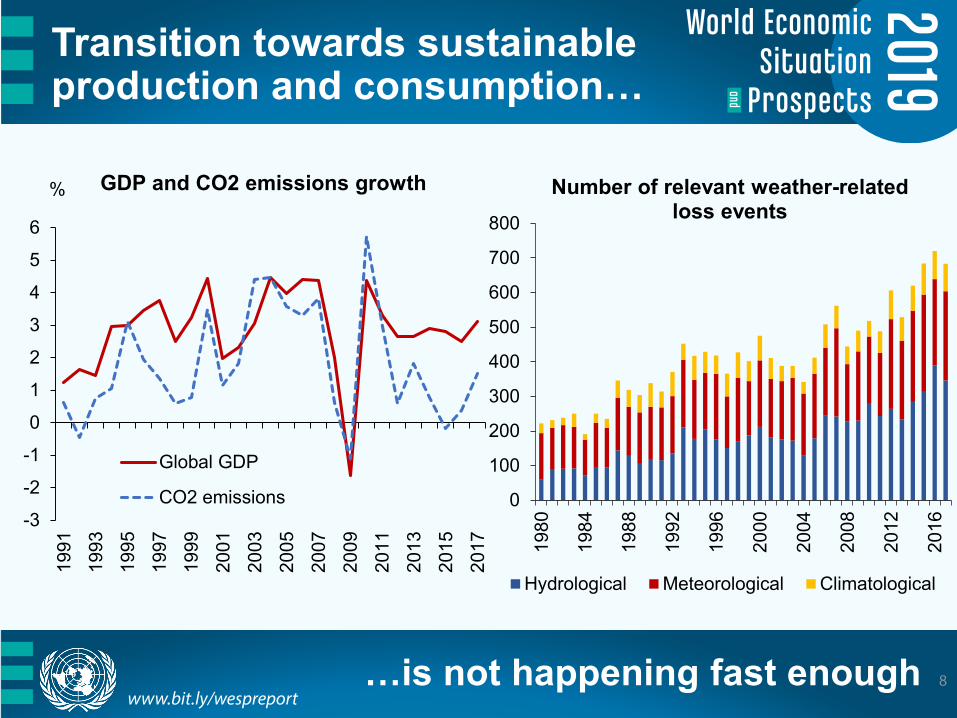

Transition towards sustainable production and consumption…

8…is not happening fast enough

-3

-2

-1

0

1

2

3

4

5

6

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

% GDP and CO2 emissions growth

Global GDP

CO2 emissions 0

100

200

300

400

500

600

700

800

1980

1984

1988

1992

1996

2000

2004

2008

2012

2016

Number of relevant weather-related loss events

Hydrological Meteorological Climatological

www.bit.ly/wespreport

Regional trends

www.bit.ly/wespreport

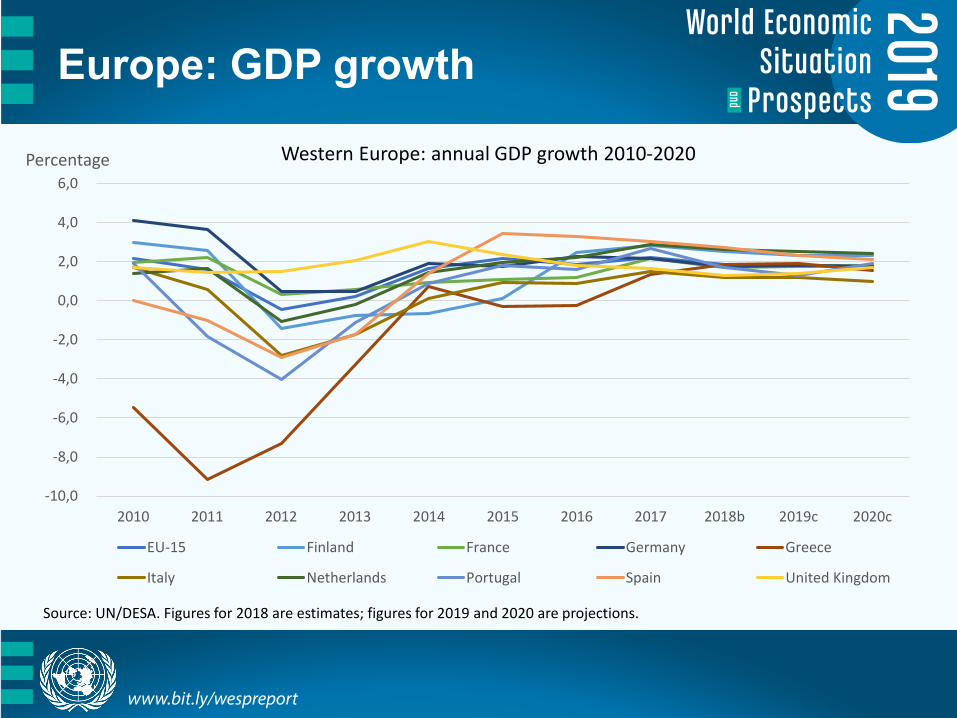

Europe: GDP growth

-10,0

-8,0

-6,0

-4,0

-2,0

0,0

2,0

4,0

6,0

2010 2011 2012 2013 2014 2015 2016 2017 2018b 2019c 2020c

EU-15 Finland France Germany Greece

Italy Netherlands Portugal Spain United Kingdom

Percentage Western Europe: annual GDP growth 2010-2020

Source: UN/DESA. Figures for 2018 are estimates; figures for 2019 and 2020 are projections.

www.bit.ly/wespreport

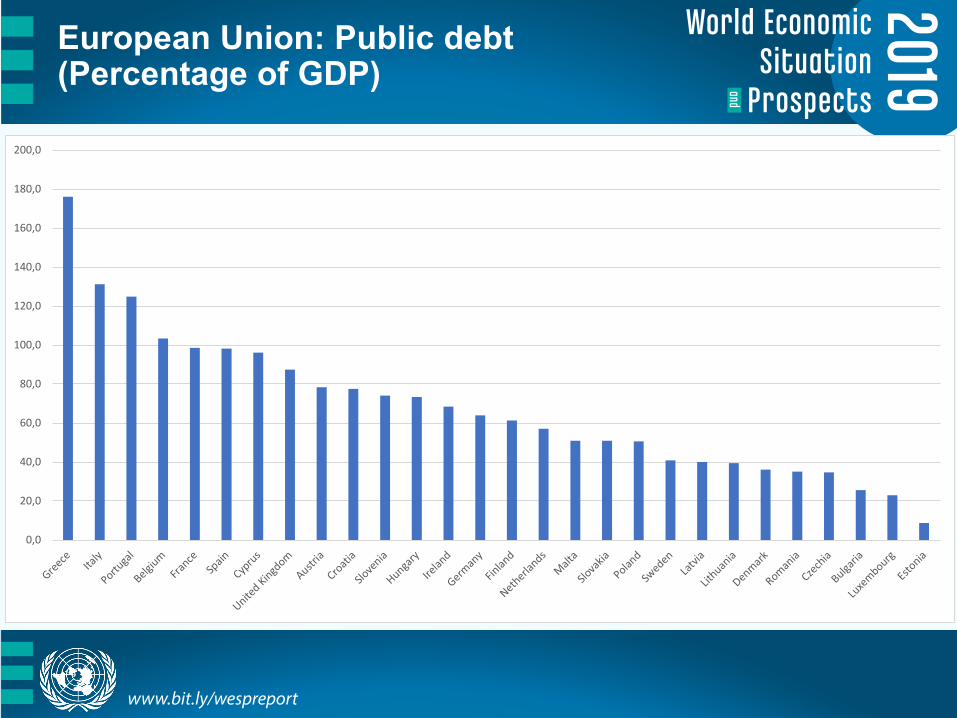

European Union: Public debt(Percentage of GDP)

0,0

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

180,0

200,0

www.bit.ly/wespreport

Economic trends in the Commonwealth of Independent States were broadly positive in 2018

Most CIS economies saw favourable economic outcomes in 2018, with accelerating growth and tapering inflation, as external conditions were generally supportive

Commodity price increases (including not only oil but also other commodities such as aluminium or cotton) and remittances sustained growth

The recovery in the Russian Federation has supported activity across the region via trade and remittance channels

After two years of improvements, however, the dynamics in the terms of trade are likely to be less favourable in 2019

The aggregate CIS growth is expected to decelerate modestly in the outlook, as the strong expansion recorded by some of the smaller economies in 2018 may not be sustainable, fiscal policies are growth-neutral at best and monetary tightening is on its way in several countries

Aggregate GDP of the CIS and Georgia is expected to increase by 2.0 and 2.5 per cent in 2019 and 2020

www.bit.ly/wespreport

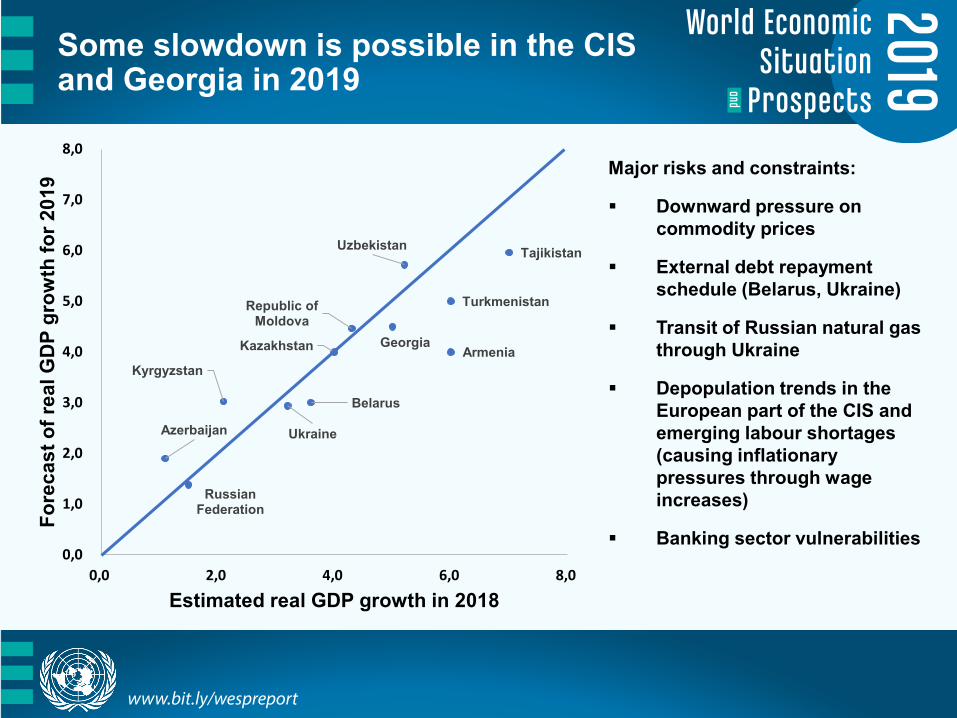

Some slowdown is possible in the CIS and Georgia in 2019

Major risks and constraints:

Downward pressure on commodity prices

External debt repayment schedule (Belarus, Ukraine)

Transit of Russian natural gas through Ukraine

Depopulation trends in the European part of the CIS and emerging labour shortages (causing inflationary pressures through wage increases)

Banking sector vulnerabilities

Armenia

Azerbaijan

Belarus

GeorgiaKazakhstan

Kyrgyzstan

Republic of Moldova

Russian Federation

Tajikistan

Turkmenistan

Ukraine

Uzbekistan

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

0,0 2,0 4,0 6,0 8,0

Fore

cast

of r

eal G

DP

grow

th fo

r 201

9

Estimated real GDP growth in 2018

www.bit.ly/wespreport

The Russian economy is expected to remain on a low-growth trajectory (1.5 -2 per cent) in 2019-2020

Constraints to growth: insufficient business lending, weak investment; banking sector vulnerabilities and moderately conservative fiscal policy

Prioritizing the build-up of protective buffers

Lifting the VAT rate in January 2019 may add to inflationary pressures in 2019, curb consumer spending, and prevent monetary relaxation

International sanctions remain a source of uncertainty, deterring investment and raising financing costs

Full implementation of the proposed sanctions may push the Russian economy into a protracted stagnation with negative regional spillovers, as the scope for import substitution is largely exhausted.

On the positive side: large current account surplus, low public debt and has massive foreign-exchange reserves

Social and economic development programmes for the period until 2024 should improve infrastructure and add to GDP growth, especially beyond 2019

www.bit.ly/wespreport

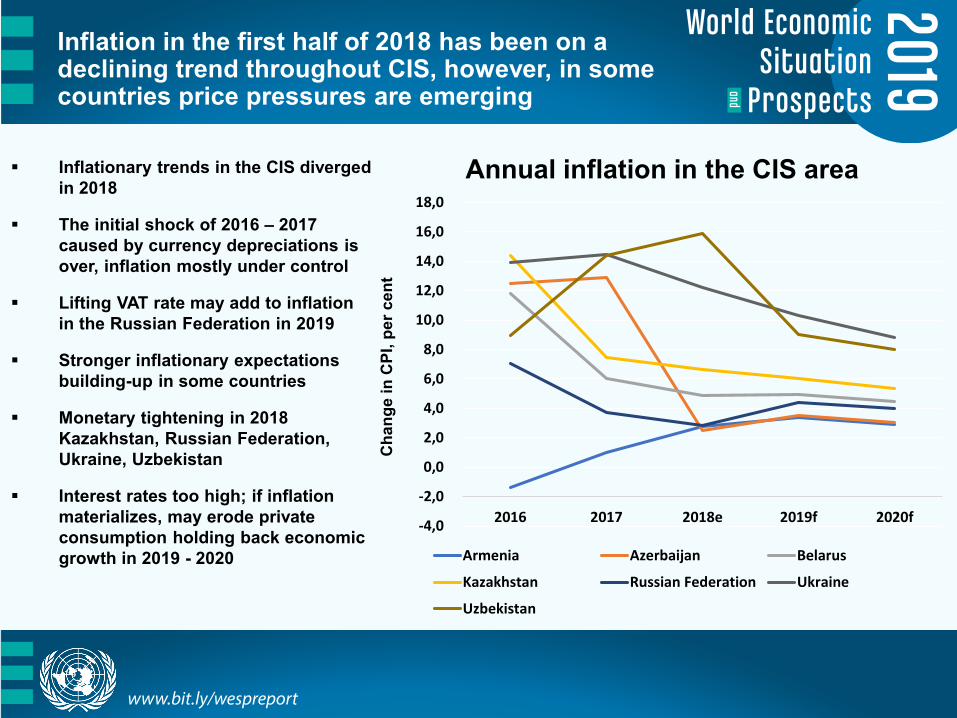

Inflation in the first half of 2018 has been on a declining trend throughout CIS, however, in some countries price pressures are emerging

Inflationary trends in the CIS diverged in 2018

The initial shock of 2016 – 2017 caused by currency depreciations is over, inflation mostly under control

Lifting VAT rate may add to inflation in the Russian Federation in 2019

Stronger inflationary expectations building-up in some countries

Monetary tightening in 2018 Kazakhstan, Russian Federation, Ukraine, Uzbekistan

Interest rates too high; if inflation materializes, may erode private consumption holding back economic growth in 2019 - 2020

-4,0

-2,0

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

2016 2017 2018e 2019f 2020f

Cha

nge

in C

PI, p

er c

ent

Annual inflation in the CIS area

Armenia Azerbaijan Belarus

Kazakhstan Russian Federation Ukraine

Uzbekistan

www.bit.ly/wespreport

South-Eastern Europe: positive economic trends set to continue

Accelerated economic growth in South-Eastern Europe in 2018 Robust domestic demand (both consumption and investment)

Favourable external environment

Serbia (the largest economy) bounced back from the past slowdown, with a double-digit growth in investment

Solid economic performance in Albania, growth in the former Yugoslav Republic of Macedonia picking up from nearly zero in 2017

The region’s aggregate GDP is expected to expand by 3.7 per cent in both 2019 and 2020

Prospect of EU accession becoming more credible

www.bit.ly/wespreport

Same challenges in SEE remain, despite the recent progress

The need for reindustrialization

Low labour force participation rate, structural unemployment constraining longer-term capacity expansion

Infrastructure development needs

Dependence on foreign financing (Brexit may impact EU funding)

Still challenging business environment

High levels of outward migration and increasing dependency ratios

A significant part of FDI stock in non-export sectors (financial services, telecommunications, real estate and retail trade)

Investment financed by loans from China has driven up external debt in some countries`

www.bit.ly/wespreport

Thank you!

Media contact: Dan ShepardUN Department of Global [email protected]

More information: http://www.bit.ly/wespreport

Global Economic Monitoring BranchEconomic Analysis and Policy DivisionDepartment of Economic and Social AffairsUnited Nations