world bank document -summary of non-lending services b5 - social ... social situation in the country...

TRANSCRIPT

Document ofThe World Bank

FOR OFFICIAL USE ONLY

Report No. 22050 IRN

MEMORANDUM OF THE PRESIDENT

OF THE

INTERNATIONAL BANK OF RECONSTRUCTION AND DEVELOPMENT

TO THE

EXECUTIVE DIRECTORS

ON AN

INTERIM ASSISTANCE STRATEGY

FOR

THE ISLAMIC REPUBLIC OF IRAN

April 16, 2001

This document has a restricted distribution and may be used by recipients only in theperformance of their official duties. Its contents may not otherwise be disclosed withoutWorld Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Currency Equivalents

Currency Unit = Iranian Rial (Rls)Official Exchange Rate: US$1=Rls 1,750

Tehran Stock Exchange Rate (TSE): US$1=Rls 7,970Iranian fiscal years end March 20

Principal Abbreviations and Acronyms Used

BMJ - Bonyad Mostazafan va Janbazan (Foundation)BOP - Balance of PaymentsCAS - Country Assistance StrategyGDP - Gross Domestic ProductFDI - Foreign Direct InvestmentFSAP - Financial Sector Assessment ProgramFYDP - Five-Year Development PlanIBRD - International Bank for Reconstruction and DevelopmentIFC - International Finance CorporationIRDP - Institute of Research in Development and PlanningIRI - Islamic Republic of IranKE - Komiteh Emdad Emam Khomeini (Foundation)MDF - Mediterranean Development ForumMENA - Middle East and North AfricaMOJ - Ministry of Jihad-e-Keshavatzi (Agriculture)MPO - Management and Plan OrganizationNTB - Non-Tariffs BarriersO&M - Operation and MaintenanceOPEC - Organization of Petroleum Exporting CountriesRls - Iranian RialsSMEs - Small- and Medium-scale EnterprisesTFYDP - Third Five-Year Development PlanTSE - Tehran Stock ExchangeUNESCO - United Nations Educational, Scientific and Cultural OrganizationWBI - World Bank InstituteWHO - World Health OrganizationWTO - World Trade OrganizationWUGs - Water User Groups

Vice President: Jean-Louis SarbibDirector: Joseph P. SabaTask Team Leader: Habib Fetini

FOR OFFICIAL USE ONLY

Islamic Republic of IranInterim Assistance Strategy

TABLE OF CONTENT

I. INTRODUCTION ......................................................... 1

II. COUNTRY CONTEXT AND RECENT DEVELOPMENTS ....................................................2

Overall Context ......................................................... 2Social Context ......................................................... 4Economic Context ......................................................... 6

III. COUNTRY DEVELOPMENT PRIORITIES AND PROGRESS ........................................... 13

Economic Reform Agenda ........................................................ 13The Social Agenda ........................................................ 16Environmental and Water Resource Management Agenda ........................................................ 17Governance and Transparency Agenda ........................................................ 19

IV. INTERIM WORLD BANK GROUP SUPPORT STRATEGY: FY2002-03 ......................... 19

Past World Bank Activities ........................................................ 19Interim World Bank Group Support ........................................................ 20Supportfor Reforms and Economic Management ........................................................ 21Supportfor the Social Protection Agenda ........................................................ 22Supportfor Environment and Natural Resource Management ...................................................... 23Portfolio Performance ........................................................ 25IMF Relations ........................................................ 25

V. CREDITWORTHINESS AND RISKS ................................................................................ 27

AnnexesA2 - Iran at a GlanceB2 - Selected Indicators of Bank Portfolio Performance and ManagementB3 - Bank Group Program SummaryB4 - Summary of Non-Lending ServicesB5 - Social IndicatorsB6 - Key Economic IndicatorsB7 - Key Exposure IndicatorsB8 - Status of Bank Group Operations in Iran

MAP

This document has a restricted distribution and may be used by recipients only in theperformance of their official duties. Its contents may not be otherwise disclosed withoutWorld Bank authorization.

MEMORANDUM OF THE PRESIDENT OF THEINTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

TO THE EXECUTIVE DIRECTORS ON ANINTERIM ASSISTANCE STRATEGY

FOR THE ISLAMIC REPUBLIC OF IRAN

I. Introduction

1.1 Iran is an important country in the Middle East Region. With a population of63 million, it is the most populous country in the region, and the 16th most populous inthe world. With a GDP of US$111 billion, Iran is the second largest economy in theregion. It is also the second largest OPEC oil producer and has the world's second largestreserves of gas. Iran is progressively emerging from a long period of uncertainty andinstability, marked of by the destructive war with Iraq, internal post-revolutionary strife,international isolation, and deep economic instability. As an ancient civilization, and aninternationally important cultural pole, it exerts a great deal of influence not only in theregion but also in the world. Iran's economic prosperity, social progress, and greaterintegration into the world economy will not only bring benefits for the Iranian populationbut will also have important spill-over effects for the region.

1.2 World Bank lending to Iran resumed in May 2000 with the approval by theBoard of Executive Directors of two projects: the Second Primary Health Project(Loan 4550; $87 million) and the Tehran Sewerage Project (Loan 4551; $145 million).These loans were approved after a hiatus of seven years during which Bank activitieswere limited and focused mainly on supervision of ongoing projects and limitedeconomic work. While approving the two loans, the Executive Directors requested thatManagement prepare a strategy note reviewing the concrete progress of economic reformand developments and outlining the Bank Group's approach in Iran.

1.3 This Interim Strategy seeks to update the Executive Directors on the currentdevelopment situation in Iran, report on the progress of the process of reforms, andhighlight the development challenges and prospects faced by the country. It outlines theassistance strategy that the Bank Group will follow while preparing a Country AssistanceStrategy (CAS) for consideration by the Executive Directors within the next two years.Thus, the strategy in this note should be viewed as an interim assistance strategy. TheCAS will reflect the further deepening of the Bank's knowledge over the next two yearsof Iran's development process and priorities.

1.4 Iran is currently in the midst of a major process of econoric re-orientation, andimportant evolution of its social and institutional system. This change is taking place inthe context of a relatively open debate with wide participation. In March 2000, theParliament approved the Third Five-Year Development Plan (FYDP), which provides thebroad directions of a wide-ranging program of economic reforms and social prioritiesover the period 2000-05. The World Bank Group Interim Assistance Strategy over thenext two years would follow a two-pronged approach: (i) policy dialogue on the reformprogram through non-lending services; and (ii) targeted lending in the key social andenvironment areas consistent with the Third FYDP, and focusing on projects that have

- 2 -

the most tangible benefits and quickest impact on the population, that are least affectedby policy distortions that could constrain their effectiveness, and that are resilient toIran's risk factors (see para. 5.1-5.5).

1.5 The level of IBRD lending is envisaged to be up to US$755 million over thenext two years. This transitional lending volume is small relative to the needs of thecountry and the size of the economy. Nevertheless, the level of lending will enable theBank to play a meaningful role in assisting in some of the key priority areas of basicneeds while filling the gaps in the Bank's knowledge of the economic, sectoral, andsocial situation in the country caused by the Bank's past limited activities, and the stillearly stage of the reform process. During the next two years, the Bank will intensify itssectoral and economic work to strengthen the knowledge of the country, develop a betterunderstanding of the Government's program and priorities, and further the dialogue withthe different stakeholders to enable the Bank to develop a more informed countryassistance program.

1.6 Macroeconomic stability and sustainability, and sufficient progress in the keyareas of economic policy reform are critical to putting Iran on a sustainable growth path,notably in improved private sector environment, financial sector, and pricing systemreforms. On the international relations front, Iran's anticipated sustained progress inimproving its relationships with the rest of the world -- which constitutes a majorachievement of President's Khatami's d6tente diplomacy -- is a key factor in openingeconomic and financial opportunities for Iran and in ending its international isolation,which, among other factors, has contributed to the upheavals of its recent economichistory (see paras. 2.16-2.18). On the domestic side, continuing progress in greaterparticipation by the civil society and enforcement of transparency will enhance goodgovernance.

II. Country Context and Recent Developments

Overall Context

2.1. Since the election of President Khatami in 1997, Iran has been undergoing asignificant evolution, both internally and in its external relations. On the domestic side,Iran enters the new century with a difficult, but most animated debate about its futurebased on continuing progress in granting a greater role to civil society and the prevalenceof the rule of law. The municipal elections held in 1999, which brought electedrepresentation to the lowest levels of government, was a significant milestone. On theinternational side, Iran's foreign policy based on d6tente and President's Khatami"dialogue among civilizations" is helping Iran out of its isolation with improved relationswithin the region and with Europe, Japan, and the rest of the world. These developments,if sustained, could open significant prospects for the future economic integration of Iranwith the world economy.

2.2. The Iranian institutional system is comprised of a popularly-elected Presidentand Parliament (Majlis), functioning under the guidance of spiritual leader AyatollahKhamenei. President Khatami was elected by a large majority in 1997 on a broadplatform of reforms. In his election platform, President Khatami has emphasized the need

- 3 -

for political and institutional reform based on greater involvement of civil society. Hiselection platform also emphasized the promotion of transparency and the rule of law asguiding principles for the Iranian government. A number of measures were taken toincrease personal liberties, including greater freedom of the press. From 1988 to 1998,1,222 newspapers and periodicals received licenses for publication, out of which 565licenses were issued from 1996 to 1998. At the same time, there have also been periodicreversals with the closing of newspapers, trial of journalists, and blockage of press reformcode legislation.

2.3. Within the limits of Box l. Insliiional System of thethe Islamic system established Islamic Republic of Iransince the Revolution in 1979,there is a relatively animated Val_-e-Fagib (LeAe hr Rahbar Seyed Ai Khamenei

is the s adsiiulOeo rn nkeigwt hand active political competition iie supree and spirital gide of fran. In keeping w eShiite Islamic principles of governance, the Constitfion of thein Iran through which people Islamic Republic provides for the estblishment of leadershipexpress their views, choice of by a Faqih (jurisprudent) who, based on his qaifications,society, economic aspirations, supervises and correlates govemment policies as Va1i-e-Faqihand political representation. Iran (Leader) with divine decrees. As such, Ayatollah Kbamenei ishas a universal suffrage for the leader of the Islamic Revolution, the Commander-In-Chief

hasea universal suffrage fr t of the amed forces, and the ultimate authorit in Iran.presidential and parliamentary Leow sM: Based on the constitution of 1979, which waselections. Voter participation is amed in 1989.high, reaching 83.3% during the les Majfs-e-Shuray-e Islami (National Assembly) oflast presidential elections. 2904 members. All Majlis legislation must be approved by theElectoral transparency is 12-member Counci of Guardians, six of whom are appointed

recognize by indepen by the Rahbar and six by the Majii The Expedexy Councilrecognized by independent mediate between the MajWlis and the Council of Cardians.observers as fair. Electoral system: Universal adult suffrage.

National elections: May 1997 (presidential). February and2.4. The legislative May 2000 (legisave); next elecions due by June 8, 2001elections held in February 2000 (presidential) and 2005 eslative).

Exectiveresulted in a large pro-reform Elad of state: Presiden eected by universal suffrage for aplurality in the Majlis. The local fur-year tem. Syyed Mohammed Khatami was elected inelections followed a similar May 1997, and took office in August 1997. The post of prnmetrend. The next Presidential minister was abolished in 1989. A new cabinet was approvedelection, scheduled for June by the Majlis in August 1997.2001, will be a significant Main political parties Pofitical partes do not currently form

2001, wll be a signmficant the basis of parliamentary activity. Most candidates aremnilestone in Iranian politics. independent, although idendtfiable as sympathetic to certainPresident Khatarni continues to politial lines.enjoy widespread supportamong the Iranian people, although he has yet to indicate whether he would seek re-election.

2.5. On the international side, Iran's current approach to foreign relations, based onPresident Khatami's "dialogue among civilizations," opens an era of detente and greateropenness to the outside world. Iran's relationship with its neighbors in the region, andwith the European Union countries and Japan has significantly improved recently, withfull diplomatic and commercial relations re-established. Progress in external relations hasalready benefited Iran's attempt to secure foreign investment. Over the past four years,

- 4 -

several oil and gas companies have renewed investment in Iran, and a pipeline of newinvestments is under discussion.

Social Context

2.6. Since the 1979 Revolution, Iran has given strong and special emphasis to humandevelopment, social protection, and "social justice," with significant progress to-date. Asa result of major investments in the social sectors over the last 20 years with virtuallyuniversal education and extensive health coverage, and an active Government distributivestrategy through direct transfers and indirect subsidies, the proportion of the populationliving under the poverty line has fallen significantly from 47% in 1978 to 15.5% now.Virtually all social indicators have shown improvement to the point where Iran now ranksat or near the top of comparable countries (Table 1). Of particular note is the closing ofthe gender gap in education, where enrollment rates for boys and girls show only smalldifferences, in literacy, and in political representation (see Graph 1).

Table 1. Selected Social Indicators

Population growth rate (%) 2.2 1.4 2.1 1.6Infant Mortality (per 1,000) 47 26 54 60Illiteracy Rate 36 27 34 26Female Illiteracy (% of age 15-24) 18 10 22 20

Gross Primary School Enroll. (%) 112 98.4 92 101Male 118 102* 103 n/aFemale 106 95* 89 n/a

Gross Secondary School Enroll. (%) 55 77 60 64Male 64 81 69 70Female 46 73 59 n/a

Access to Safe Water (%) 50 95 87 75Sources: Data provided by the Iranian authorities, World Development Indicators 1999,UNESCO, and World Bank staff estimates.* The drop in the rate of enrollment could be explained by the increase in private schooling.The statistics on enrollment capture only attendees of public schools.

2.7. Notwithstanding these achievements, Iran still faces three major challenges: (i)it still has a significant prevalence of poverty; (ii) it has dealt with poverty more throughhandouts and charitable transfers than through employment and empowerment; and (iii)while these explicit subsidies and transfers have the merit of reaching the poor, Iran alsomaintains, often in the name of the poor, an expensive and excessively large implicitsubsidy system that is untargeted and distortionary.

2.8. A poverty study undertaken by the Government established a strong linkagebetween poverty and unemployment: 37% of poor households in the poorest first decilehave no one working, and 45% of them have just one working person. This characteristic

- 5 -

underscores the high positive impact that growth and productive employment could haveon poverty reduction.

Graph 1. Closing Gender GapFemale and male literacy rate In rural Percentage ot Elected Women inand urban areas 1976-1996 (percent) Parliament 1981-1997

80

70

60 4

50

40 -

30 C2-

20 -10- F- -- ural w orrn -Urban w on-on 1

10 - Rural nfen .--- Urban rren

0 01976 1980 1984 1988 1992 1996 1981 1985 1989 1993 1997

Source: Plan and Budget Organization, and UNDP: Human Development Report of the IslamicRepublic of Iran, 1999.

2.9. Iran has an extensive social safety net and transfer system that reaches a largenumber of the poor. Half of the poor, about 4.5 million persons or 1.47 millionhouseholds, benefit from social coverage by government social safety net programs,charity institutions, and other non-profit organizations. These programs include directcash transfers, housing provision, education scholarships, and health and social securitycoverage. In particular, targeting and reaching the poor is made possible in Iran throughthe network of mosques, and other non-governmental institutions. The country has alsoaccumulated a rich experience of rationing during the long war with Iraq. Most of thebeneficiaries have access to bank accounts through which regular direct cash transfers aremade.

2.10. While the above cash and other direct transfer support is effective in reachingthe poor, Iran also maintains extensive implicit subsidies, including energy subsidies,exchange rate subsidies, and credit subsidies, that are excessively large (the energysubsidy alone is estimated at more than 12% of GDP), but are untargeted and ineffective.While the maintenance of these subsidies is often justified in the name of the needy, theydo not proportionately benefit the poor. In fact a large part of the subsidy system,including those directed to basic needs such as bread and medicine, are highly untargetedvis-a-vis the poor (Table 2). The total benefit from the bread, medicine, gas and kerosenesubsidies, for example, that goes to the richest decile is twice, four times, thirty twotimes, and three and a half times, respectively that going to the poorest decile, reflectingboth the extent of waste and inefficient targeting of these subsidies.

- 6 -

Table 2. Shares of Different Income Deciles in TotalSubsidies for Selected Items (1996)

Deeils Gas Ker1n Medice 0 Bread

It" decile 1.3 4.4 3.8 6.22nd decile 2.1 6.7 6.8 8.43rd decile 3.2 8.7 7.6 8.54h decile 3.9 8.6 8.9 9.95th decile 4.7 10.1 9.0 9.76t decile 6.4 11.3 10.6 10.671h decile 8.2 11.6 10.7 11.089 decile 10.3 12.1 12.8 11.39th decile 18.0 12.7 12.9 11.8IOh decile 41.8 16.1 17.5 12.5

Source: "Plan to Fight Poverty and to Raise the Income of Poor Households", Managementand Plan Organization, Social Affairs Bureau, September 2000.

Economic Context

2.11. A stabilizing macroeconomic situation: After a long period of instability andlarge external and internal imbalances that reflected Iran's economic structural problems,its external difficulties, and its limited access to external financing, the macroeconomicsituation has recently improved significantly. During 1999-2000 the budget registered asurplus of 1% of GDP, up from a deficit of 6.7% in the previous year. A budget surplusof 12.6% of GDP is estimated for the Iranian year 2000-01 which has ended in March 20,2001. The budget surplus (equivalent to $8 billion at the TSE rate) has been allocated tothe newly created Oil Stabilization Fund. The balance of payments difficulties that havemarked most of the past decade have eased. A current account surplus of 4.3% of GDPwas registered in 1999-2000, and a surplus of about 14% of GDP is estimated for theIranian year 2000-2,001, driven by a trade surplus of $14 billion-one of the largest ever.Foreign exchange reserves are building up to more than 10 months of imports. Inflationfell to under 20%, a level it held over the past two years. Progress in reducing inflation inthe near future will, however, remain limited because of ongoing liberalization efforts,the scaling down of subsidies, and the process of unification of the exchange regime.

2.12. While the rebound in oil prices, and to a certain extent the start ofimplementation of reforms (see para. 3.6) contributed greatly to these positivedevelopments, the progress toward macroeconomic stability is being strengthenedthrough higher commitment to fiscal responsibility and by the significant fall in the debtstock and debt services. Fiscal sustainability, indeed, is being strengthened by theinstitution of the newly created Oil Stabilization Fund and the commitment of theGovernment under the FYDP to a balanced budget stance based on prudent projectionsof oil prices and revenues' over the period of the Plan. The fiscal situation is furtherstrengthened by the sharp tailing off of Iran's external debt profile. The annual total debtservice (including short term debt services) has fallen to US$6.9 billion at the end of the2000-01 Iranian year, down from an average of about US$11.5 billion during the last 4

l Projected foreign- exchange revenues from oil exports in US$ billion by the FYDP which are used as abasis for the balanced budget for the Iranian years 2000/1 to 2004/5 are: 11.09; 10.86; 11.05; 11.57; and12.08 respectively, corresponding to price levels of between US$15-17 per barrel.

- 7 -

years. It is projected to decrease to US$5 billion thereafter. The debt stock is also sharplyreduced, and has fallen to about US$8.4 billion at the end of the 2000-2001 Iranian fiscalyear, down from US$22 billion in 1995-96 (Graphs 2 and 3). The end of the debt-crisis,which has dominated much of the economic scene in the last few years, is an importantdevelopment for the Iranian economy. It opens the prospects for a more stable andsustainable macroeconomic position in the future, and provides a solid footing for thestart of the program of structural reforms envisaged in Iran's Third Five-YearDevelopment Plan (FYDP).

Graph 2. Total External Debt Stock, 1991-2000Billion of U.S. dollars

* Short term

25 | * Medium&LongTerm

20

15

10

5-

0-

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Source: World Bank Data.

Graph 3. Debt Ratio, 1991-2000(Percent)

Total Debt service/export of goods & services (excl. short-term debt)Debt outstanding/GDP (including arrears)

40

35 E=L

25 !48 g

20 ,

15

10 &V.l

01993 1994 1995 1996 1997 1998 1999 2000

Source: World Bank Data.

- 8 -

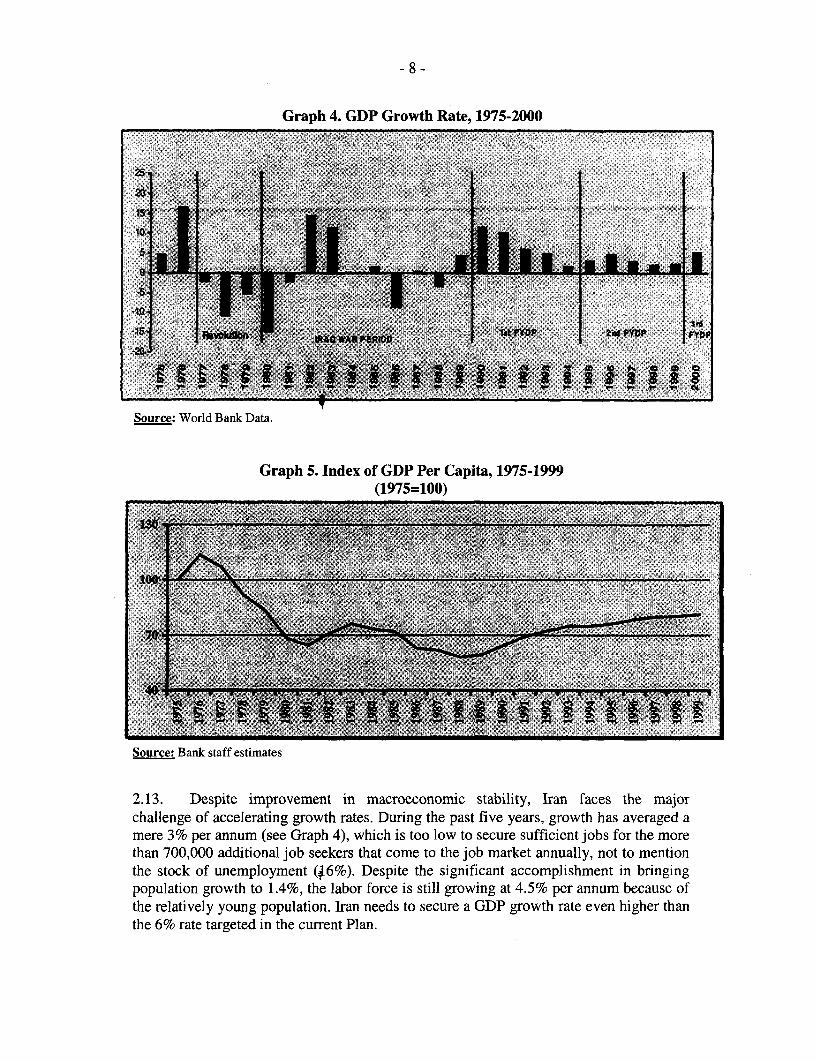

Graph 4. GDP Growth Rate, 1975-2000

Source: World Bank Data.

Graph 5. Index of GDP Per Capita, 1975-1999(1975=100)

X~~~~I IM M

4 2''t'S1E l, '. B. ,, l

Source: Bank staff estimates

2.13. Despite improvement in macroeconomic stability, Iran faces the majorchallenge of accelerating growth rates. During the past five years, growth has averaged amere 3% per annum (see Graph 4), which is too low to secure sufficient jobs for the morethan 700,000 additional job seekers that come to the job market annually, not to mentionthe stock of unemployment (Q6%). Despite the significant accomplishment in bringingpopulation growth to 1.4%, the labor force is still growing at 4.5% per annum because ofthe relatively young population. Iran needs to secure a GDP growth rate even higher thanthe 6% rate targeted in the current Plan.

- 9 -

Box 2. The "Bonyad" Foundations in Iran

Iran's post-revolution public sector includes a number of organizations in the form of semi-publicfoundafions called "Bonyad". Established in the late 1979 after the Revolution, they operate as holdings ofcompanies of the former Pahlavi Fowndation and other confiscated assets. Some of these foundations areheavily involved in a variety of economic activities and are the most important channel of carrying outIran's large social assistance programs. In addition to their own resources that they derive from theireconomic activities, they finance their social activities from the refund of their own taxes, which are held inspecial accounts at the Treasury and don't channel through the budget, and from charitable contributions.Some of them, such as Komiteh Emdad (see below) receive most of their funding directly from the budgetand are the main implementation institution of the Government social coverage program.

Our information on the size, stucture and funtioning of the Bonyads is limited, but critics of theseinstitutions in the private sector generally raise the issues of their extra-economic quWsi-monopolisticpower, and the fact they enjoy wide ranging tax and customs privileges, preferential access to credit andforeign exchange allocation, as well as regulatory protection from private sector competition. Efficiency.transparency, and good coordination between the different Bonyads in the provision of social assistancefunction are recognized also as critical to the success of the Government's new poverty reduction strategy.Within the framework of the FYDP, the Government intends to un*y the administration system of thewhole social program under the Management and Plan Organization.

Among these Bonyads, the following are of special significance due to their share in economicactivities (Baonyad Mostazafan) and the extent of their social involvement (Komiteh Inidad).

Bonva o_stazafan va Lanbazan (BMI) is the most important among Bonyads. According to itsown Web page (ht=to/www.ia-n 4nyad.org tnabo_ut.htm). "1 BMJ is] presently the largest economicsection in Iran, second only to the goveinment.. [BMJI and the affiliated organizations ma8ge more than400 companies andf4ctories. Within Iran, [they] are active in the most outstanding industrial and businesssectors: food and beverage, chemicals, cellulose items, metals, petrochemicals, constrwsion materals.dams, towers, civil development, farming, horticulture, animnl husbandry, tourism, transportationfi five-starhotels, commercial services, financing. joint venures, etc. Added to these, is the special legal status ofBonyad which is considered to be the most unchallenged private enterprise in Irn. "

Total assets of the BMJ are estimated at US$3.5 billion-mostly real estate-and its total turnoveris estimated at about US$1.5 billion. BMJ has a large social assistance program including financialassistance to more than 120,000 families of war veteran and families of martyrs, and covers pensions, freehealth and education services and housing to large segments of the poor. Financing of the social activities isensured by own profit and refunded taxes which are held in a special account at the Treasury.

Komiteh Emdad Emm Khomeini (KE). While its involvement in economic activities and ownassets are less important than those of Xt BMJ, KE is the most active Bonyad in social safety net provision.It provides assistance to about 4 million people, or 80% of the poor who benefit from social assistance, andprovides educational support to 600,000 students. It also provides international support and relief assistanceto other countries. The Komitch's financing resources come essentially from the Government budget andthe rest from its own resources and charitable contributions.

Other Bonyads, include: d (the Martyr Foundation) providing support for the martyrs'families as well as disabled. The foundation owns several companies in agriculture, mining, constructionand trade. &ayqd Ma (the Housing Foundation), set up in June 1979 to house the poor especially inrural areas. Financial resources come from private resources, the government developrnent budget for ruralhousing, and borrowing from the banking system.

2.14. Impediments to achieving growth: Achievement of rapid economic growth isconstrained by a multitude of distortions that have accumulated over the past two decadesof great disruptions and uncertainties, marked by the Revolution, the long and destructivewar with Iraq, and the difficult international relations situation that impeded the country'snormal access to international capital and goods. The prolonged heavy interventionist

- 10-

framework of economic management during the war and after, led to the buildup of acomplex distortionary pricing system, with multiple foreign exchange rates, quantitativetrade restrictions and distorted tariffs, and large subsidies of energy products. It also ledto the development of a large public enterprise sector, dominating up to 60% of themanufacturing sector, and large quasi-public Bonyads (see Box 2) -the latter combineproduction, commercial, and social protection functions with little transparency. TheBonyads also enjoy extra-economic power that adds to the other institutional and legalimpediments to the development of private activities. The financial sector is alsocontrolled by the state and most of the credit is administratively directed through thepublic banks (there are no private banks). The outcome has been a prolonged economicstagnation, during which time GDP per capita fell and, in spite of its slow recovery(mostly due to a steep drop in population growth), has yet to regain its pre-revolutionlevel (see Graphs 4-5).

2.15. Shifting from a "distribution-before-growth" development approach to a"distribution-with-growth" approach: To fulfill the promise of the Revolution inpromoting social justice, Iran has followed a "distribution-before-growth" developmentapproach. Indeed, while growth has stagnated and per capita GDP has declined since theRevolution, social indicators have improved significantly. This paradox of improvementin social conditions with declining growth is explained by the very active Governmentrole in important direct transfers, explicit subsidies of essential goods, and a stronghuman resources development program (universal access to education and healthcombined with successful population growth control), and also through large, butuntargeted, implicit consumption subsidies2. This transfer program, while reducingpoverty, has started reaching its limit. The shift of public resources to consumption at theexpense of production limited growth and thus job creation for the growing number ofyoung people entering the labor force. Growth was also hampered by over expansionaryfiscal spending that generated macroeconomic crisis, as was the case during the First Plan(see paras. 2.17). A major challenge of Iran's transition will be to find the appropriatemechanisms to move away from the large untargeted subsidies to more targeted subsidiesfor the genuinely poor, and to channel the resulting public savings to augment privatesavings in financing private sector investment to generate productive employment and asustainable growth with social justice. This re-orientation of the economy will also needto be accompanied by a redefinition of the role of the government to core areas, leavingproductive activities in the hands of the private sector.

2.16. Past failed attempts to reform: The Iranian authorities recognize the need forstructural reforms in the economy and have attempted to address these as early as thecountry's first FYDP (1990-95). These attempts, however, proved unsuccessful becauseof lack of resolve in the pursuit of reforms, Iran's external isolation and its limited accessto adequate foreign financing on longer terms. These factors, combined with Iran'sexternal vulnerability to oil shocks, led to major macroeconomic imbalances. During theperiod of the second FYDP, a continuously adverse external environment-including atight debt repayment schedule, low oil prices, and continued external embargo-lirnited

2 Expliciting energy subsidies, exchange rate, credit and other subsidies would add about 20% of GDP tothe reported total budget size, as measured by total expenditure, ranging about 26% of GDP.

- 11 -

Iran's ability to stabilize its economy and to pursue aggressively the economic reformagenda of the election platform of President Khatami.

2.17. First Five Year Development Plan (1990-95): The first attempt at reformstarted after the war with Iraq and within the framework of the First FYDP covering theperiod 1990-95. Iran embarked on a large infrastructure reconstruction program with totalinvestment ranging from 30 to 35% of GDP. During this period, Iran also pursued anaggressive agenda of economic policy reform, including decontrolling domestic prices,removing many trade restrictions, liberalizing the foreign exchange system, and initiatinga privatization program of public enterprises. These policies, along with thereconstruction program and an expansionary fiscal policy in support of an ambitioussocial program, resulted in an impressive 7% average annual growth during the Planperiod, and a significant improvement in social indicators, which put Iran in the forefrontof best performers of its income category, and of the MENA region. This over-expansionary fiscal stance, however, resulted in large macro imbalances. Given Iran'slimited access to longer-term external financing, the large current account deficit wasreflected in a surge in short-term debt and excessive drawing on foreign exchangereserves. In 1994, when the bunching of short-term debt coincided with lower thanexpected oil prices, an external payments crisis emerged. Large payment arrears led to aseries of reversals of the policy reforms undertaken, including the reinstitution ofmultiple exchange rates, and the halting of the privatization process as the unemploymentand social situation worsened.

2.18. Second Five Year Development Plan (1995-2000): During the Second FYDP,the economy entered into a "muddle through" phase with growth stagnating at an averageof 3% per annum, below the projected 5.1% in the Plan. In addition to the structuralimpediments, growth was mostly constrained by the excessive compression of imports(reaching up to 50% in some years) needed to make room for external debt repayments asIran's access to external financing remained restricted. Management of the unstablemacroeconomic situation left little leeway to address the structural reform issues.Macroeconomic instability was further heightened with the extension and intensificationof external economic and financial sanctions on Iran. This dampened expectations andtriggered a run on foreign exchange and consumption goods markets that induced a sharpdepreciation of about 50% of the free exchange rate to Rls 6,200 per U.S. dollar, and asurge in consumer prices by 14% during April/May 1996, bringing inflation for the yearto 49%. In yet another attempt to control the foreign exchange crisis, the authoritiesraised to 100% the export repatriation and surrender requirement, and ordered all foreignexchange transactions to go through the banking system, effectively ending the non-bankforeign exchange market. During the subsequent years of the Plan, the bunching ofrepayments of the rescheduled debt was again exacerbated by a sharp drop in oil prices in1998/99, inducing a second external payment crisis and leading to another bilateralrescheduling. The collapse in oil revenues also led to a fiscal deficit of 6.7% of GDP in1998/99 in spite of drastic cuts in capital expenditures and delays in implementation ofpublic investment projects. Table 3 summarizes the key economic indicators for the1991-2000 period.

- 12 -

Table 3. Islamic Republic of Iran: Key Economic Indicators,

1991/92-1999/00

1991192 1992/93 1993/94 1994/95 1995/96 1996/97 1997/98 1998/99 1999/00

Gross Domestic Product (in trillion of Iranian dals)GDP 50.1 66.5 93.6 128.4 178.9 235.2 275.9 327.5 415.5

(Annual percentage change)GDP 10.1 5.9 4.9 1.6 3.2 5.5 3.4 2.2 2.5

(In percent of GDP)Oil GDP 8.2 9.1 17.6 18.9 16.1 15.2 10.8 6.5 8.4Non-oil GOP 91.8 90.9 82.3 81.1 83.9 84.8 89.2 93.5 91.6

Agriculture 23.1 23.9 20.7 21.1 22.2 20.0 20.1 22.1 20.9Industry 20.1 20.1 18.7 18.6 19.7 21.0 22.3 23.3 22.8Services 48.7 46.9 43.0 41.4 42.1 43.8 46.8 48.1 47.9

Inflation (Annual percentage change)Consumer price index 20.7 24.4 22.9 35.2 49.4 23.2 17.3 20.0 20.4GDPdeflatoratfactorcost 23.6 24.9 38.4 35.8 35.5 24.6 13.4 16.1 23.7

Investmert & saving (In percent of GDP)Gross Domestic Investment 33.2 35.4 29.2 24.2 30.2 26 25.0 22.0 16.0Gross national savings 28.2 30.7 26.6 20.1 24.3 26.0 24.0 20.0 20.0

Govemrnment finance (In percent of GDP)Revenue 15.7 17.3 31.0 26.1 25.2 26.4 25.6 19.2 27.0

Oil &Gas 7.1 8.0 23.1 18.6 16.5 16.2 13.7 6.9 12.4Non-oil 9.6 9.4 7.9 7.5 8.8 10.2 11.9 12.3 14.6

Total expenditure and net lending 18.9 20.3 38.2 30.5 28.8 28.0 28.2 26.0 26Current 12.1 13.7 14.6 15.5 14.4 15.6 16.2 16.4 15Capital 5.0 4.6 7.7 7.0 7.2 7.4 7.0 5.4 7.6Earmarked expenditure 1.8 1.9 1.9 1.4 2.0 2.0 2.3 2.6 2.9Foreign exchange losses ... ... 6.0 6.7 5.2 3.0 2.6 1.6 0.4

Overall deficit(-) Isurplus -3.3 -3.0 -7.2 -4.5 -3.6 -1.6 -2.5 -6.7 1.0

External sector (In millions of U.S. dollars)Current account -10248 -7304 -4215 4957 3358 5232 2213 -2140 4728Trade balance -6529 -3406 -1207 6818 5586 7402 4258 -1168 6216

Exports, f.o.b. 18,661 19,868 18,080 19,435 18,360 22,391 18,381 13,118 19,727Imports, f.o.b. 25,190 23,274 19,287 12,617 12,774 14,989 14,123 14,286 13,511

Gross reserves (months of imports) 1.3 1.5 1.8 3.9 6.0 7.1 4.3 3.0 4.9Current account balance (% of GDP) -8.4 -5.6 -5.2 7.5 3.8 5 1.5 -1.9 4.3

External Debt (In millions of U.S. dollars)Total Debt Stock 10880 15977 23039 22693 21928 16703 11823 13999 10357

Medium & Long Term 2065 1716 5423 15986 15485 12081 9479 9496 6739Short term 8815 14261 17616 6707 6443 4622 4768 4503 3618

Debt to GDP Ratio (%) 8.9 12.2 28.7 34.5 25.0 15.9 10.2 12.4 9.3Debt to Exports Ratio (%) 58.3 80.4 127.4 117.0 119.4 60.7 60.4 61.8 42.5

Source: Management and Plan Organization, Bank Markazi Jomhouri Islami Iran, andBank Staff estimates.

- 13 -

III. Country Development Priorities and Progress

3.1 Iran's current development priorities and approach are outlined in the ThirdFYDP (2001-2005) approved by the Parliament last year. The Plan aims at a growth rateof 6% per annum during the Plan period. At the same time, the Plan continues the strongemphasis of the past on social development and equity. To achieve its objectives ofraising economic growth potential, increasing the living standards of the population, andreducing unemployment, the Plan envisages a wide range of structural reforms aiming ata balanced and gradual transition to a market economy. While greater private investmentis expected to provide the basis for more rapid growth, the Plan gives special emphasis toagricultural and rural development, and housing as the key sectors underpinning thegrowth with distribution objectives. Both of these sectors have not only potential forgrowth but also for job creation and poverty alleviation given their higher labor-intensity,in particular of unskilled and poor workers.3 The Plan also gives particular priority to theenvironment, including managing air and water pollution and the preservation of naturalresources. These aspects are discussed below.

Economic Reform Agenda

3.2 The economic reform strategy is based on a two-pronged approach aimed atdeveloping a competitive functioning of the economy by taking steps toward liberalizingthe pricing system, and shifting toward a market-based price determination as a meanstoward more efficient allocation of resources. Secondly, the strategy involves theundertaking of legal and institutional reforms to enable the development of private sectorparticipation concomitant with public enterprise sector reform and privatization, as wellas reform of the financial sector.

3.3 The reform of the pricing system includes: (i) the unification of the multipleexchange rate system and movement toward market determination of the exchange rate;(ii) trade liberalization, consisting of the narrowing of the large non-tariff barriers, andthe streamlining of tariffs; (iii) moving away from the system of administrativelydetermined credit allocation and real negative interest rates, toward competitiveallocation of credit, and positive interest rates; and (iv) addressing the issue of the largeenergy subsidies.

3.4 The other set of structural reforms in support of the development of a privatesector-based development includes: (i) strengthening the legal and institutionalframework, in particular the reform of the previously constraining legal framework offoreign direct investment, and the enactment of laws, regulations and institutionalarrangements to limit monopolistic and unfair trade practices, and the opening of alleconomic activities to the private sector; (ii) reducing the size of the public enterprisesector through privatization and public enterprise reform; (iii) starting the reform of thestate-dominated financial sector, strengthening banking regulation and supervision, andopening the way to the emergence of private banking; and (iv) strengthening ofmechanisms of social protection to limit the negative transitory effects of the reforms.

3 Our analytical knowledge of the sources of growth and the sectoral potential for growth and distributionare very limited at this stage. AAA work is planned to fill this gap.

- 14-

3.5 Iran's economic reform strategy is based on a gradualist approach given thecomplexity of the reform process and the need to avoid undue social disruption. Themagnitude and inter-locking nature of the various distortions require a careful sequencingof the reform measures. Nevertheless, the Government is committed to the full reformagenda of the Third FYDP and has already made good progress in the first year (whichbegan in March 2000) as indicated below:

3.6 Recent progress in reform implementation: Significant progress has beenrealized over the first year of the Third FYDP in several economic reforn areas:

- Foreign exchange reform: The exchange rate system was further rationalizedwith the abolition of the export exchange rate, reducing the multiple exchangerate system to two rates: the Tehran Stock Exchange (TSE) rate, currently atabout Rls8,000/US$, which approximates market rates and under which allprivate and a large part of public sector foreign exchange transactions areconducted; and an official exchange rate of Rlsl,750/US$ now used for certainlimited public sector transactions (debt payments, imports of essential goodssuch as pharmaceuticals, some capital and defense goods). Steps are now beingtaken to move to an inter-bank market of foreign exchange. Distinction between"locally" and "internationally"-sourced foreign exchange for legitimate currentaccount transactions will be abolished during 2001-2002. A commission hasbeen constituted to evaluate economic and social impacts of total unification ofthe exchai ge rate system, and to formulate a strategy to address its economicand social effects. Full unification is scheduled to happen within the currentIranian fiscal year 2001-02. Indeed, the budget law for the current yearstipulates that the next budget (March 21, 2002- March 20, 2003) shall beprepared on the basis of a unified exchange rate.

- Trade reforms: The strategy of the Government is to: (i) remove all non-tariffbarriers (NTBs) and replace them with tariffs; (ii) progressively reduce the tariffbands over the period of the Third FYDP; while (iii) progressively reducing theaverage tariff rate to a level that allows Iran to engage in WTO negotiations.Until March, 2000, out of 5,113 HS product codes, there were only 1,900products free of restrictive licensing. During the first six months of the Iranianyear 2000-01, 895 additional new products have been freed from licensing. Anadditional list of more than 2,000 new codes under import licensing to beconverted into tariffs has been presented to the Parliament. It is expected that bythe end of next Iranian year, Iran will complete the tariffication of all NTBs andmove from a positive list-based import control system to a small negative list.The authorities are also actively preparing for a WTO accession request.

- Energy price adjustment: Energy border prices are 4 to 5 times higher onaverage than domestic prices and subsidies are estimated at more than 12% ofGDP. Energy price adjustments, however, have proven to be highly sensitivepolitically given their high and wide-spread impact on the population, and thefears about ripple through effects in the economy. Proposals for priceadjustment were presented to the Majlis last year, but were rejected on thesegrounds. The draft budget for next year currently being discussed stipulates a

- 15-

modest increase of 15% for gasoline, kerosene, and gas prices. However, acommittee has been set up to evaluate the effects of alternative adjustmentstrategies and develop compensating strategies to cushion the effect of energyprice adjustment. Energy price adjustment will remain a critical step to thecredibility of the reforms and their feasibility, not only because it removes amajor source of resource allocation distortion in itself, but also because it wouldprovide a critical source of financing of the economic and social costs of theoverall reform process.

Privatization: Since the announcement of the privatization program in the Plan,a new privatization agency has been set up in the Ministry of Finance. TheMajlis has promulgated regulations governing privatization. The Privatizationcommittee, under the supervision of the President, has reviewed 1,039 publicsector enterprises for privatization: 217 are to remain public, 87 will beliquidated, and 735 are slated for privatization. During the first half of the year2000-01, the Government sold Rls2,040 billion (about 0.5% of GDP) equivalentof shares of public enterprises in the TSE. It has ceded to workers RlslO0 billionworth of shares. Rls1,800 billion worth of shares are being put to sale for thenext fiscal year. In the oil sector, the Oil Ministry announced that it will cede 23firms of its subsidiaries to the private sector over the FYDP. These include theNational Iranian Tanker Company and the liquefied gas distribution centers.

Financial Sector Reform: Significant policy changes are planned, or alreadyunder way, in the financial sector. This sector has been dominated by whollygovernment-owned banking entities, operating within a restrictiveadministrative regime and behind strict exchange controls. However, theGovernment envisages greater private role in the future. Already several privatecredit institutions, albeit very small, have been licensed in the last few years anda reinterpretation of the banking constitutional legislation is opening the way tothe licensing of private domestic banks (two are expected within the currentIranian fiscal year.) Also, legislation permitting the establishment of foreign-owned banks in off-shore free trade zones has been enacted. However, it willbe some time before private banking and quasi-banking operations develop intoviable alternative provider of financial services, particularly given the lack ofconsensus on the appropriate role of the state in the financial sector.Meanwhile, the state owned banks can be expected to continue to be thedominant players, and for these, greater freedom in credit allocation and pricingis envisaged, while at the same time prudential regulation and supervision isbeing strengthened. Non-bank finance is also being enhanced, and the Tehranstock exchange has re-emerged as a significant and active entity. There remainchallenging issues of adapting international regulatory practice to the all-Islamicfinancial practice of Iran and, more widely, ensuring that the financial systemcan deliver the services necessary to strengthen the productivity andinternational competitiveness of the non-oil sector. Following the recent jointBank-Fund assessment of the Iran's financial sector as part of the FSAPprogram, both institutions have been providing technical assistance in support ofwhat will need to be a sustained effort over several years for the development ofIran's financial system.

- 16-

Foreign Direct Investment: Encouraging foreign direct investment in both theoil and non-oil sectors is one of the pillars of economic revival in the ThirdFYDP. A new FDI Act is now before the Parliament and is expected to beapproved shortly. Over the past 5 years, Iran was able to attract some $10billion in private investment in the oil sector using a buy-back formula as a wayto bypass restrictions by the Constitution on ownership of natural resources byforeigners-an amount judged far below what is needed to meet Iran'sambitious plans to develop its oil and gas production. Other new options arenow being debated, including enhanced buy-backs with long-term agreementsand more incentives; joint ventures between foreign and Iranian oil and gascompanies are also being considered.

The Social Agenda

3.7 As reported above, Iran's social indicators improved substantially since theRevolution, but these achievements also present weaknesses that challenge theirsustainability. Progress in social welfare and human capital development has yet to besupported by growth and matched by productive opportunities, and the system of socialsupport remains based more on handouts and charitable transfers than on empowermentand employment. The Third FYDP correctly recognizes these weaknesses and presents atwo-pronged strategy to fight poverty based on employment creation for those who areable to work, and a more efficient and targeted social safety net to support the rest of thepoor.

3.8 Empowerment-based poverty reduction: The Plan targets an ambitiousreduction of the poverty headcount from 15% to 7% at the end of the plan period.Because of the established direct link between poverty and employment in Iran, thisshould be realized through an annual creation of 765,000 jobs, corresponding to adecrease in the rate of unemployment from 16% at its starting year to 12.5% at the end ofthe Plan. The Plan presents a sectoral approach to promoting employment and reducingpoverty. It envisages higher support to the agricultural sector through higher publicinvestment in the water management and other productivity enhancing investment, andsupport to small development activities such as fisheries, animal raising, and forestry. Inmining and industry, the strategy includes support to small and medium enterprisesthrough special incentives to investment in under-served regions. In the housing sector,tax and credit incentives are provided to promote low-income housing construction, thatwould benefit the poor directly and indirectly (through employment creation).

3.9 Improvements in education and health are envisaged in the Plan as directmechanisms for poverty alleviation through empowerment. In education, the Planemphasizes education as a means to fight poverty, as indicated by the linkages betweeneducational attainment and literacy, and poverty. It envisages upgrading the quality of theeducational system at all levels, and improving its effectiveness in terms of a betteralignment with the needs of the economy and the labor market. It also envisagesreforming education curricula, and developing appropriate programs of vocationaltraining. In health, while Iran has a well performing basic health system and good healthindicators, it still has a high rate of childhood malnutrition. The Plan emphasizes the need

- 17-

to address these deficiencies in health by developing a nation-wide nutritional educationprogram, and improving geographical coverage of basic health services. The Governmentintends also to give particular importance to improving the efficiency of the healthsystem and the quality of services at all levels, and to undertake the reform of its pensionsystem.

3.10 Improving the efficiency of the Social Safety Net: The second prong of theGovernment poverty reduction program concerns those who are disabled and those whocan not work. The plan envisages improvements in the efficiency of transfers throughbetter targeting, improving the poverty map, and enhancing the coordination between thevarious social safety net institutions, including the Bonyads, by bringing them under theadministrative control of Management and Plan Organization. A comprehensive reviewof the different institutions and the existing targeting mechanisms is underway.

3.11 Addressing the social costs of reforms: While the Plan provides importantelements of the social safety net, it does not address explicitly how these mechanisms canbe used to mitigate the adverse effects of economic reforms. Rationalization of subsidies,particularly the extensive energy subsidies, as well as privatization will requirecommensurate measures such as worker training, cash compensation, short-termemployment creation, etc. The absence of a clearly articulated social protection strategycould act as a barrier to implementation of the reforms. The Bank plans to work with theGovernment in preparing a social assessment of the reform program in terms of its impacton the different income groups, and articulating a social protection strategy which buildson the various Plan initiatives.

Table 4. Quantitative Goals of the Third FYDP to Fight PovertyTotal for the To be achievedPlan Period in

200012001Poor people to be shifted from direct assistance to employment 1,371,000 145,000(number of people over next 10 years)Housing for the poor (units over next 10 years)

Urban 667,000 66,700Rural 193,000 19,300

Health centers for rural areas (units over FYDP) 4,700 1,270Water supply (number of villages covered over FYDP) 13,000 3,250Sewerage coverage (number of villages to be covered over FYDP) 8,750 2,187Rural Roads (kilometers over FYDP) 12,000 2,400Special home care for disabled persons (persons over FYDP) 135,000 27,000

Source: "Islamic Republic of Iran: Plan to Fight Poverty." Management and Plan Organization, SocialAffairs Bureau, 2000.

Environmental and Water Resource Management Agenda

3.12 The environment agenda has been elevated as one of the highest priorities of theIranian Government. Environment affairs are handled at a vice presidential level. AnEnvironmental High Council reporting to the President includes two Vice Presidents,

- 18 -

10 cabinet Ministers and the Attorney General. Iran indeed has severe environmentalproblems-urban, rural, and coastal-that have reached critical levels.

3.13 On the urban environment side, Iran has a very underdeveloped seweragesector. Adequate waste water collection and disposal systems exist only in Isfahan,covering a population of one million, and to a limited extent in Tehran. The dominant useof absorption wells is contributing to ground and surface water pollution throughinfiltration or overflowing, and presents serious health risks. The Government recognizesthe backwardness of the sector and the Plan proposes an ambitious program to upgradethe system in all urban areas over the next 20 years. Key policy and institutionalmeasures adopted include the introduction of pricing policies of water supply andwastewater services to achieve efficient tariffs based on full recovery of O&M costs andcapital expenditures, and the promotion of private sector participation in the sector. Theincreasing volume of toxic industrial effluents also constitutes a significant urbanenvironmental concern for Iran, and figures in the action plan of the Government. TheTehran Sewerage Project approved last year represents the first major initiative consistentwith the thrust of the Plan.

3.14 Air pollution also poses a major urban environmental concern. It is estimatedthat more than 5 million tons of pollutants are released per year into Iran's atmosphere,65% of which comes from motor vehicles. Heavily subsidized energy prices are widelyunderstood to be a major contributing factor. Air pollution in Tehran and other majorcities, especially from motor vehicles, exceeds by far the standards set by the WHO andposes serious health problems. There are occasions when schools are closed in Tehranbecause of the high level of air pollution. The authorities are developing a comprehensiveaction plan to deal with the aggravation of the air pollution problem, including a reviewof the energy subsidies, improving regulations of gas emissions, levying fines for non-compliance and tax-deductible expenses for industries, and encouraging the relocation ofindustrial enterprises outside cities boundaries.

3.15 Major environmental issues in the rural areas identified by the Governmentpertain to inefficient irrigation systems caused by excessive groundwater extraction thatthreatens both water quantity and quality; high conveyance and distribution losses ofsurface water due to inefficiency of the irrigation network, and low on-farm irrigationefficiency; severe soil erosion and land degradation due to lack of integrated river basinwater management, over-cultivation of marginal land, and unsustainability of highcarrying capacity of range and pasture, and deforestation.

3.16 The FYDP targets increasing water availability for agriculture by around 9%and expanding the irrigated areas by about 30%. Achieving these targets will involvedecentralization, a decline in the role of Government, and an effective involvement ofWater User Groups (WUGs) in water resource management; optimum exploitation ofborder rivers and common water resources to reduce the pressure on groundwaterextraction; and encouraging the establishment of cooperatives with expected increasesfrom 700 to 1,700.

- 19 -

Governance and Transparency Agenda

3.17 President Khatami, since assuming office in 1997, has advocated the need forpolitical and institutional reforms that increase transparency based on strengthening therule of law, and giving greater involvement of the civil society as a means to ensuringsustained pressure towards accountability of the system. Some specific measures thathave been taken in the past few years include:

- Granting much more freedom to the press, which would ultimately contribute toa more open and critical examination of government policy, fullerrepresentation of public opinion and the viewpoints of civil society. Iran todayhas a flourishing press, with different political leanings. Out of a total of 1,222newspapers and periodicals that received licenses for publication from 1988-98,565 licenses were issued from 1996 to 1998 alone.

- Reforming the budget nomenclature, process, and control mechanisms andinstitutions so as to ensure greater transparency and efficiency in publicexpenditures. A council for administrative reform headed by the President hasalso been created with the objective of fostering transparent management at alllevels of the administration.

- The Third FYDP covers also a series of measures to regulate monopolies andpromote competitive economic activities, which should enhance widertransparency and limit the opportunities for corruption.

3.18 Despite these significant measures, there is the continuing struggle betweenopposing factions with strongly differing views on the direction and speed of reforms.Periodic set-backs are, therefore, to be expected.

IV. Interim World Bank Group Support Strategy: FY2002-03

Past World Bank Activities

4.1 Iran was an active borrower of the World Bank until the oil windfall of the early1970's, when the financial assistance from the World Bank was phased out. Up untilFY76, Iran had borrowed from the World Bank a little over US$1 billion. Lendingresumed in 1991, after incomes had declined following the long war with Iraq, and theGovernment embarked on a large reconstruction program, including a program ofeconomic reforms within the First FYDP. From 1990-93, the World Bank made six loanstotaling $843 million. In May 2000 the Executive Directors approved two new loans -the Second Primary Health and Nutrition Project and the Tehran Sewerage Project.World Bank activities in the last few years in the absence of new lending focused mainlyon the supervision of the portfolio and some limited economic and sector work. The Bankalso supported capacity building through technical assistance funded from IDF grants fordebt management, banking supervision, foreign investment promotion, and theintroduction of VAT. IFC and MIGA were not active in this period, although MIGA(through FIAS) assisted the Government in implementing the IDF grant for foreigninvestment promotion.

- 20-

Interim World Bank Group Support

4.2 Iran is a large country that is emerging from a long process of internationalisolation and economic embargo that limited its normal access to long-term financingopportunities for its development needs. To achieve the plan's objectives of 6% growthand the creation of 765,000 jobs per year, an estimated 7% annual growth of investmentis required. The needs for external financing are estimated at around US$7-10 billion forthe Plan period. The lending and non-lending support from the Bank would thus beimportant and have a significant payoff for the country in this transition phase. Inaddition, the authorities see the World Bank playing an important role in supportingIran's new policy and effort to improve its relations with the international financialcommunity and to attract foreign investment. For FY 2002-03, the Bank lending programcould amount to up to $755 million.

4.3 The economic and social reform agenda of the Government as outlined in theThird FYDP, addresses the right issues to move the economy forward. The announcedsocial strategy emphasizing employment over direct assistance, improving efficiency,transparency and effectiveness of existing programs, and unifying the institutions that areresponsible for the delivery of the social program, represents a change in the rightdirection. On the economic side, the Third FYDP addresses many aspects of theprevailing structural problems of the Iranian economy, in particular the reform of someelements of the pricing system distortions and the reform of public enterprises and thefinancial sector. Implementation difficulties, however, cannot be understated because ofinstitutional, managerial and technical constraints, as well as the as yet unclear politicalconsensus. Nevertheless, the current environment is the most favorable for reforms thepolicy makers have faced in some time. Iran's substantial drop in indebtedness andimproved fiscal situation, constitute new favorable developments underpinning a morestable macroeconomic environment, providing room for maneuver that was previouslynot available. The Government can now focus more on the longer-term reforms and shiftaway from the crisis management mode that prevailed during the two previous plans. Agood start has already been made in reform implementation during the first year of thethird FYDP (see para. 3.6) which created a momentum. Bank support, through non-lending services and targeted lending for basic needs, would assist the Govemment toimplement its reform program.

4.4 In support of the Government's reform efforts, the Bank will intensify economicand sector work covering the main reform areas, and provide support for capacitybuilding in the formulation of economic and sector policies, their sequencing, andimplementation. This non-lending support will also be useful in the preparation of the fullCAS. A series of economic studies is either underway or planned over the next two yearsto provide the basis for providing fruitful policy dialogue and policy analysis and preparethe CAS. These include a study on the reform of the energy pricing system (alreadyfinalized); a Trade and Foreign Exchange System reform study (at an advanced stage); aplanned Public Expenditure Review including a Country Procurement AssessmentReport, and a Country Financial Accountability Assessment; a Country EconomicMemorandum providing analysis of the medium term framework for the economictransition and the sequencing of reforms; an evaluation of the costs of reforms and how to

- 21 -

address them; as well as other major sectoral studies, including a Water ManagementPolicy Review note, and sectoral strategy notes on housing, agriculture, air pollutioncontrol, and others (see Table. 5)

4.5 On the lending side of our assistance, given the size and needs of the country,and its creditworthiness, Bank lending volume could gradually increase to significantlevels. But with the much reduced Bank activities in the last 7 years and the resultantdeficit in economic work and sectoral knowledge, which has to be quickly made up for,the Bank Group would follow a transitional assistance strategy which can, over time, leadto a fuller involvement in 2-3 years.

4.6 Lending during this transitory short period, as specified below, will focusmainly on priority areas such identified as low income housing, sewerage, urbanupgrading, and community-based infrastructure and employment creation schemes for thepoor. These are areas that are least constrained by policy distortions being addressed, aremost resilient to potential country's economic and social risks and, at the same time, havea quick impact on improving the situation of the poor and the environment and enhanceresource management. Lending will also be directed to technical assistance in support tothe structural reform program. The Bank will continually assess the lending program onthe basis of progress in macroeconomic performance and policy outcomes and projectimplementation in the areas identified as a priority for Bank involvement. IFC and theWorld Bank Institute will combine efforts in support of this transition program. Asmentioned earlier, a full CAS will be developed within the next two years, as sufficientprogress is being achieved in our dialogue with the Government and stakeholders atlarge, and also in key areas of policy reform.

Support for Reforms and Economic Management

4.7 Bank Group support for economic reforms will include four areas: (i) analyticaland advisory work to provide an underpinning for the reforms; (ii) lending for technicalassistance; (iii) capacity building and training by WBI, and (iv) IFC support for theprivate sector.

4.8 Analytical and Advisory Services are envisaged in the areas of: reform of thepricing system and its economic and social implications; trade and tariff reform strategy;privatization of public enterprises; financial sector reform and institutional development;and sequencing of the reform agenda. A study of the social safety net indicated earlierwill provide a strategy for ameliorating any adverse social implications of the reforms.

4.9 The Government expressed the need for technical assistance in several areas,including the development of financial sector institutions, and support for theprivatization program. A small Technical Assistance Loan will be provided to addressthese needs.

4.10 The World Bank Institute has provided some assistance in the past two years,in particular in the trade area, and within the framework of the MediterraneanDevelopment Forum (MDF), which has been greatly valued by the Iranian authorities.There is need for further assistance in training in several areas, in particular in trade

- 22 -

reform and WTO accession, governance, infrastructure finance, project managementskills, and macroeconomic training.

4.11 IFC Support will complement the Bank's analytical and technical assistanceactivities in support of private sector development. IFC will assist in mobilizing foreigndirect investment in specific sectors which are open to private/foreign investment as aresult of the reform process. Most sectors of the economy have been affected by morethan two decades of domestic distortions and external embargoes. While the oil, gas, andpetrochemicals sectors continued to benefit from some foreign investment, other sectorshave fallen behind. As a priority, IEFC's initial support will focus on the financial sector,particularly as it supports small and medium enterprise development as a pillar in theemployment creation strategy of the Government. As policy constraints are removed andreforms progress, support would be extended progressively to other projects which areexport-oriented, and where Iran has a comparative advantage.

4.12 Iran's private sector, while small, has limited access to financing. State-ownedbanks control the financial sector and credit allocation benefits non-competitive state-owned enterprises. Furthermore, a limited range of financial instruments is available tothe domestic private sector. As a first step, IFC proposes to support the development ofleasing institutions. Leasing, indeed, could be effective in supporting the development ofSMEs, and IFC has considerable experience worldwide. Thereafter, EFC's focus in thefinancial sector would eventually include support for formation of banks in the privatesector, trade finance, and the development of capital markets. IFC will provide, asneeded, advisory services to support any initiative in privatization of state-owned banks.

4.13 IFC's short to medium-term focus would expand to investments in companieswith strong foreign partners to promote the transfer and upgrading of technology in Iran,which is needed after years of sanctions. IFC also proposes investing in those industrieswhere Iran has a comparative advantage, or which are export-oriented. These includemanufacturing, and services, including development of business hotels with internationaloperators to develop the business travel market, which would grow as the climate forforeign investment improves.

Support for the Social Protection Agenda

4.14 Social Safety Net: The key element of the new Government approach topoverty reduction is to shift from the transfer/charity based approach to one based onemployment/empowerment. The Government is also addressing forcefully both theefficiency and targeting of its existing system of subsidies and transfers and isconsidering the reform of the institutional vehicle of its social programs. Our selectiveassistance in this area involves a series of focused operations with an expected quickimpact on the population.

4.15 A Social Fund Project would focus on micro-credit and community-basedinfrastructure and employment creation schemes. The project would be implementedthrough non-governmental organizations and focus on the poorer communities. A LowIncome Housing Project would support the Government's efforts in providingaffordable housing to low- and moderate-income families. Iran is facing serious problems

- 23 -

of housing in general and low-income housing in particular. The housing problem isaggravated by a spur in the coming of age of a large number of young Iranians, and alsourban migration. The project would provide financing for low- and moderate-incomefamilies through the National Housing Bank. A Housing Strategy Note will examine thepolicy constraints in the sector and instruments to develop market-based housing financeintermediation.

Support for Environment and Natural Resource Management

4.16 Environment: Given the severity of pollution and its impact on public health,the Bank will assist through a series of projects and advisory services that willcumulatively help in building an investment portfolio, the outcomes of which would bethe reduction of exposure to air pollution and water borne diseases and, in parallel, astrengthening of the capacity of the environment-related institutions in monitoring andenforcement. The Bank will also provide non-lending services in the field ofenvironmental risk assessment and safeguards, as well as mainstreaming environmentalconcerns into the decision-making process. Finally, as part of its regional cooperation andwith a view toward protecting the fragile marine ecosystems of the Caspian Sea, the Bankwill continue its on-going technical assistance to Iran.

4.17 Untreated sewerage as well as municipal and hazardous waste constitute one ofthe major environmental issues in Tehran and other secondary cities. Following theTehran project, a Second Sewerage Project would be developed to provide sewerageand sanitation services in one or more secondary cities. The project will include:pretreatment of industrial waters before discharging into the municipal sewers byproviding incentives to the polluting installations; appropriate treatment of municipalwaste water with proper disposal of sludge; and re-use of treated effluents foragricultural/irrigation purposes.

4.18 Iran has inadequate municipal waste disposal facilities. Iran produces about14.7 million tons a year of municipal waste, of which 2.2 million tons is generated inTehran. Iranian industries also emit a total of 100,000 tons a year of toxic substances, aswell as 15,000 tons a year of heavy metals. On the basis of a waste management sectornote which will be prepared, a Municipal Solid Waste Management Project wouldsupport the collection and safe disposal of municipal waste. The project would alsoinclude a pilot component for handling hazardous and hospital waste, as these represent agrowing problem.

4.19 Addressing the air pollution environmental problem, particularly in Tehranwhere air quality is extremely poor, will require bold actions on a variety of fronts. Onthe policy side of the problem, the Government needs to adjust significantly the level ofenergy prices. This will induce a decrease in the use of private vehicles in cities. TheGovernment needs also to expand urban public transport. Part of the savings generatedfrom energy subsidy reduction could be used to finance this shift to a public transportsystem. Conditional on significant progress in energy price reform, the World Bankwould support the Government program with an Urban Transport Project, whichwould include investments in transport infrastructure, public transportation and measuresto monitor and control air pollution. Although the project will most likely mature after

- 24 -

the transition period, preparatory work could be initiated during the period. Preliminarywork has already been done in the area of air pollution by the World Bank in 1994, andwould be updated to support such an effort.

4.20 In terms of capacity building, the Environmental Organization4 is expected toplay an important role in the formulation, implementation and enforcement ofenvironmental policies. An Environmental Management Project would assist theEnvironmental Organization in capacity building and provide it with adequate equipmentfor monitoring.

4.21 Rural Environment/Water Resource Management: The ongoing IrrigationImprovement Project (FY94) aims to improve water resource management in a number ofprovinces. This large multi-component project supported activities such as: irrigation anddrainage networks improvement, operation and maintenance (O&M), water usersorganizations, extension, research, environmental studies and institutional strengthening.Achievements under this project, as well as the privatization of the O&M activities,constitute a good basis for continued Bank involvement in rural environment and waterresource management.

4.22 Consistent with the directions in the current FYDP, a Water ResourceManagement Project would address the issues of watershed management based on ariver basin management approach. The project would include water management andagricultural development in the lower reaches of the river basin, and watershedmanagement of the upper reaches of the river basin. In the lower reaches, therehabilitation and modernization of the irrigation and drainage networks and thestrengthening of the privatization of the operation and maintenance activities should belinked to the strengthening of agricultural activities, such as extension and research. Inthe upper reaches, watershed management would be geared towards conservation of soils,rehabilitation of range land and restoration of marginal land, coupled with theimprovement of the quality and productivity of range land. The approach is intended toensure that the upstream rural inhabitants also share in the development, and participatein the management of water resources.

4.23 Environmental assessment will be an integral part of all lending operations.These will provide opportunities for the Bank to strengthen capacity for the relevantenvironmental institutions.

4.24 Urban Upgrading and Historic Sites Rehabilitation: Part of the authorities'strategy of employment creation and growth is to use its important cultural assets topromote cultural-centered tourism as an important economic sector and as a means topresent the country's civilization and image to the rest of the world. An UrbanUpgrading and Historic Sites Rehabilitation Project linked to tourism developmentwould aim at developing cultural tourism as an economically as well as anenvironmentally sustainable sector. The project would ensure regulated planning andinvestments in historic sites to reconcile the economic benefits and the environmentalrisks posed by unregulated investmnents and the expected increase of tourists. Project

4 Headed by a Vice President.

- 25 -

components would include: (i) renovation of historic sites; (ii) provision of supportivepublic infrastructure; (iii) developing incentives for the private sector participation indeveloping infrastructure and tourist facilities; and (iv) institutional/financial mechanismsto ensure that local communities realize a share of the benefits from the tourism industry.

Portfolio Performance