world bank document - documents &...

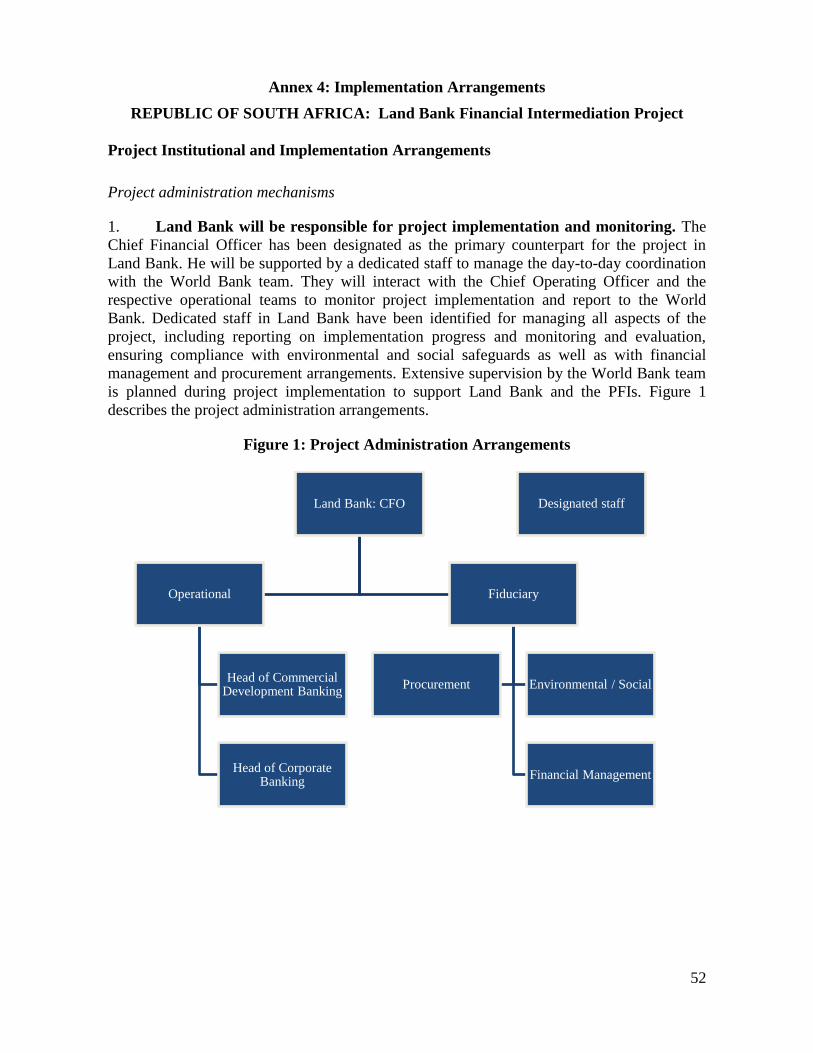

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No: PAD1122

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVLOPMENT

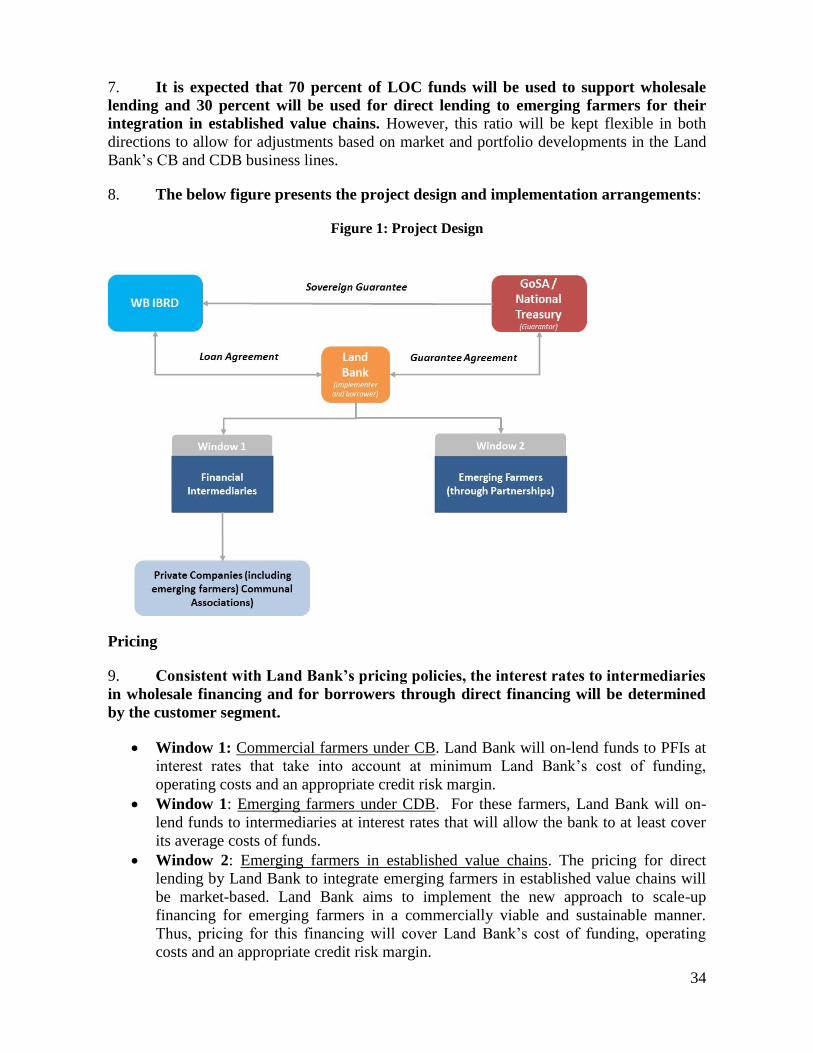

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED LOAN

IN THE AMOUNT OF US$93 MILLION

TO THE

LAND AND AGRICULTURAL DEVELOPMENT BANK OF SOUTH AFRICA

WITH THE GUARANTEE OF THE REPUBLIC OF SOUTH AFRICA

FOR A

LAND BANK FINANCIAL INTERMEDIATION LOAN

DECEMBER 29, 2016

Finance and Markets Global Practice

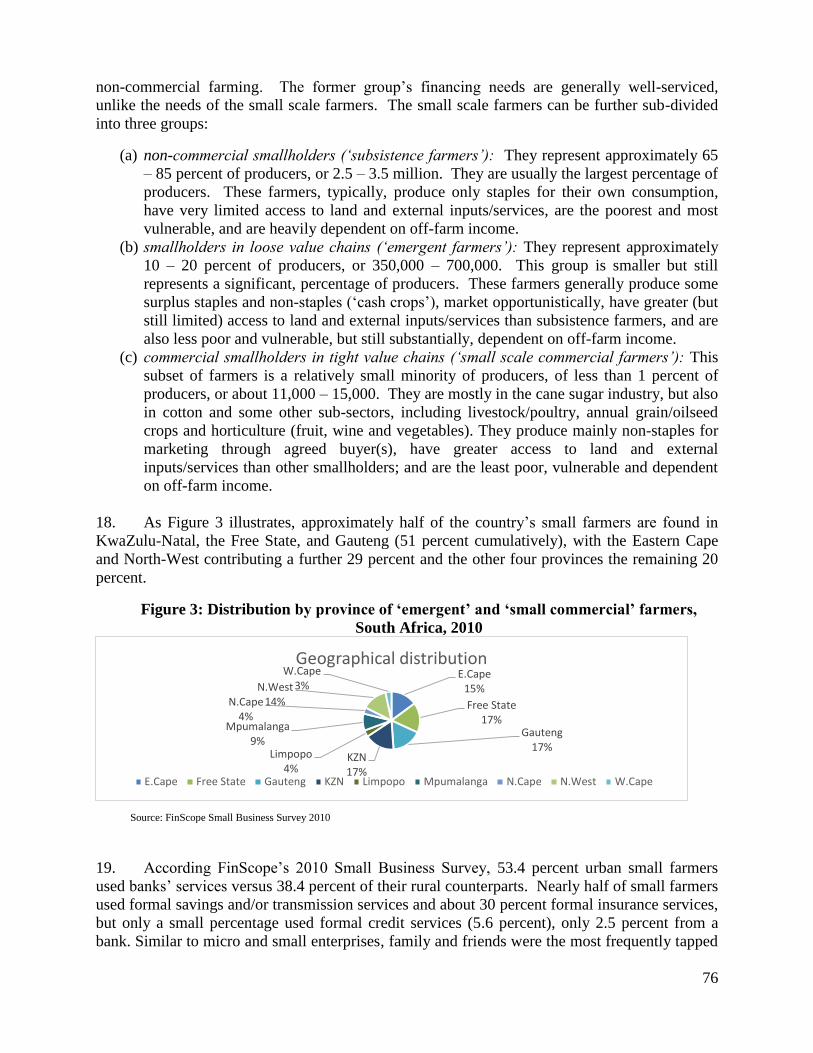

Africa Region

This document is being made publicly available prior to Board consideration. This does not

imply a presumed outcome. This document may be updated following Board consideration

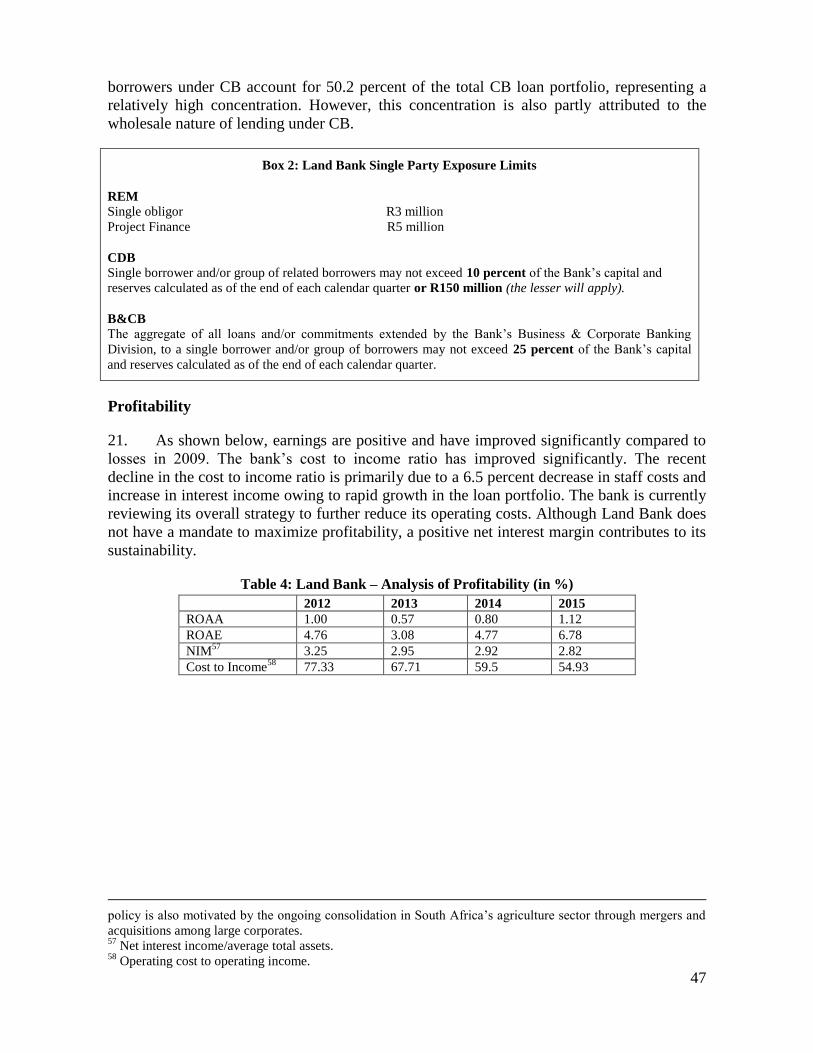

and the updated document will be made publicly available in accordance with the Bank’s

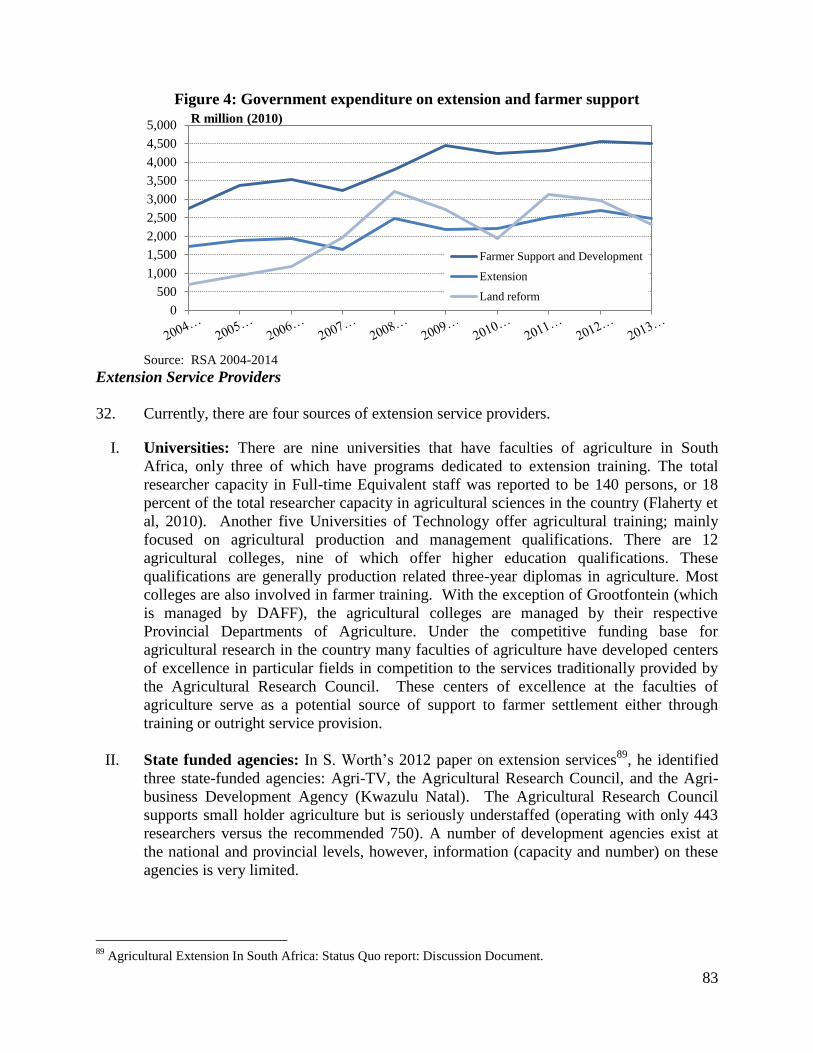

policy on Access to Information.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

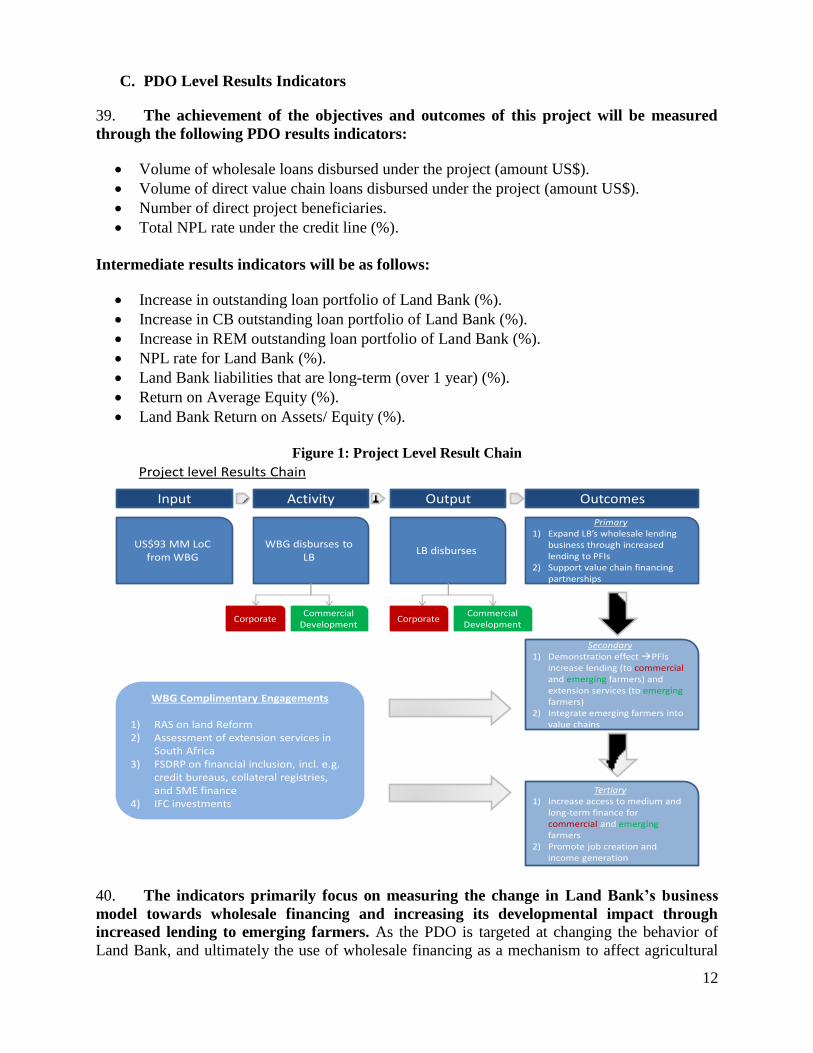

iscl

osur

e A

utho

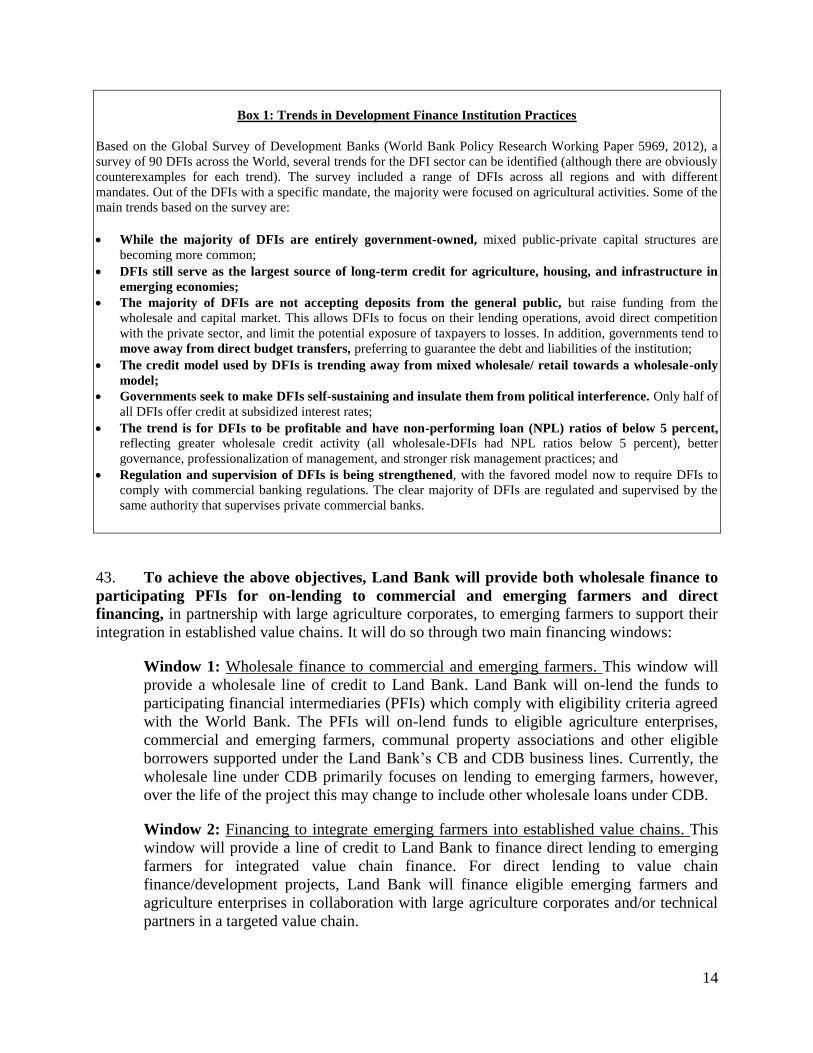

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective October, 30 2016)

Currency Unit = South African Rand

ZAR 13.47 = US$1

SDR 0.73 = US$1

FISCAL YEAR

January 1 – December 31

ABBREVIATIONS AND ACRONYMS

AES Agricultural and Environmental Services

AFC Agricultural Finance Center

AFS Annual Financial Statements

AfDB African Development Bank

AG Auditor-General of South Africa

B&CB Business and Corporate Banking

BBBEE Broad-Based Black Economic Empowerment

CASP Comprehensive Agricultural Support Program

CB Corporate Banking

CDB Commercial Development Banking

CEO Chief Executive Officer

CFO Chief Financing Officer

COO Chief Operating Officer

DAFF Department of Agriculture, Forestry and Fisheries

DBSA Development Bank of Southern Africa

DFI Development Finance Institution

DRDLR Department of Rural Development and Land Reform

EIA Environmental Impact Assessment

ERR Economic Rate of Return

ESMS Environmental and Social Management System

FIL Financial Intermediary Loan

FM Financial Management

FSDRP Financial Sector Development and Reform Program

GDP Gross Domestic Product

GRS Grievance Redress Service

IBRD International Bank for Reconstruction and Development

IDA International Development Association

IFAC International Federation of Accountants

IFRS International Financial Reporting Standards

IPF Investment Project Financing

ISP Implementation Support Plan

ISR Implementation Status and Results Report

JSE Johannesburg Stock Exchange

LOC Line of Credit

LRAD Land Redistribution for Agricultural Development

MAFISA Micro Agricultural Financial Institution of South Africa

NCR National Credit Regulator

NDP National Development Plan

NGO Non-government organization

NIM Net Interest Margin

NPF New Procurement Framework

NPL Non-Performing Loans

NPV Net Present Value

NT National Treasury

PDO Project Development Objective

PFI Participating Financial Intermediary

PLAS Proactive Land Acquisition Strategy

PS Performance Standards

RCB Retail Commercial Banking

REM Retail Emerging Markets

ROAA Return on Average Assets

ROAE Return on Average Equity

SAP Systems, Applications and Products

SARB South African Reserve Bank

SLAG Settlement/Land Acquisition Grant

SME Small and medium enterprise

S&P Standard & Poor

US$ United States Dollars

VCF Value Chain Financing

WB World Bank

WBG World Bank Group

ZAR

South African Rand

Regional Vice President: Makhtar Diop

Country Director: Ivan Velev (Acting)

Senior Global Practice Director: Gloria M. Grandolini

Practice Manager: Alejandro Alvarez de la Campa

Task Team Leaders: Gunhild Berg/Uzma Khalil

SOUTH AFRICA

Land Bank Financial Intermediation Project

TABLE OF CONTENTS

Page

I. STRATEGIC CONTEXT .................................................................................................1

A. Country Context ............................................................................................................ 1

B. Sectoral and Institutional Context ................................................................................. 4

C. Higher Level Objectives to which the Project Contributes .......................................... 9

II. PROJECT DEVELOPMENT OBJECTIVES ..............................................................11

A. PDO............................................................................................................................. 11

B. Project Beneficiaries ................................................................................................... 11

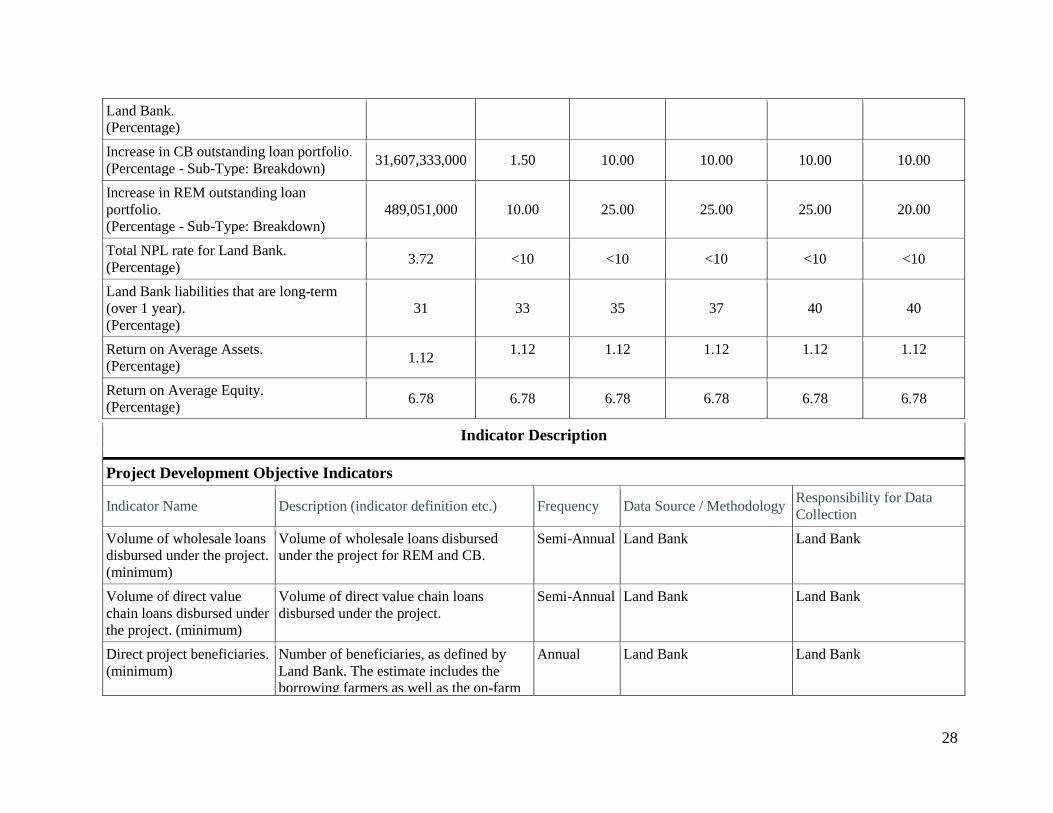

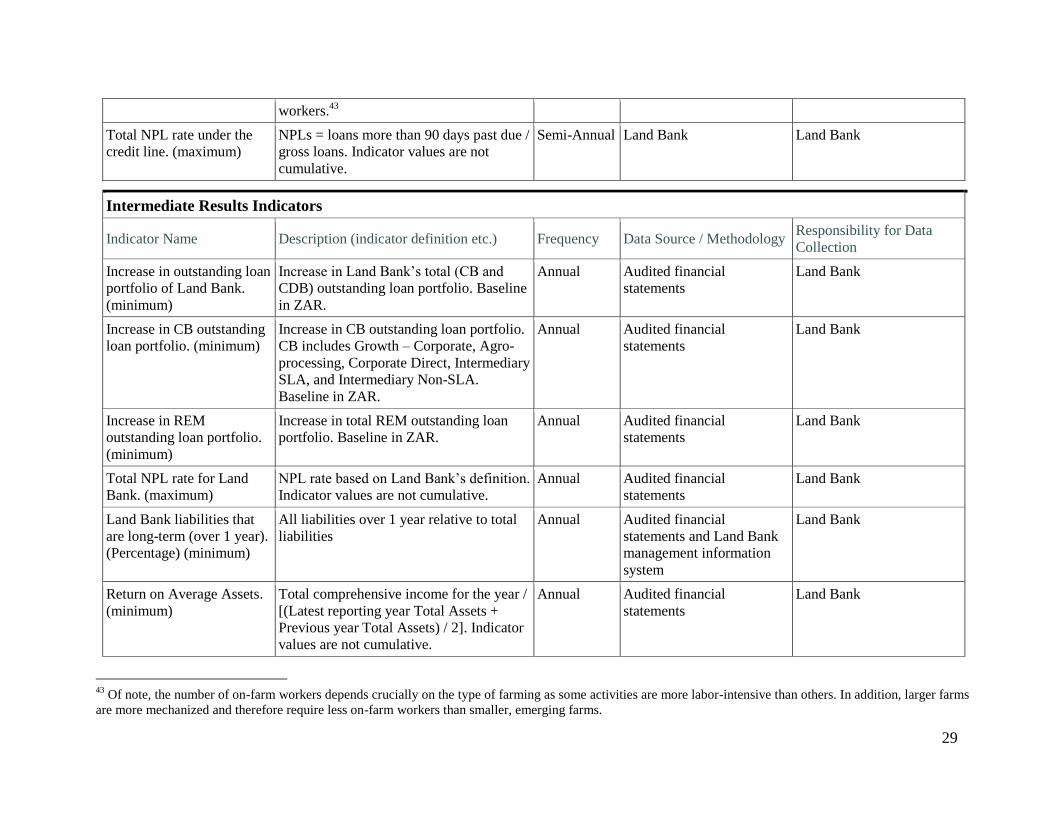

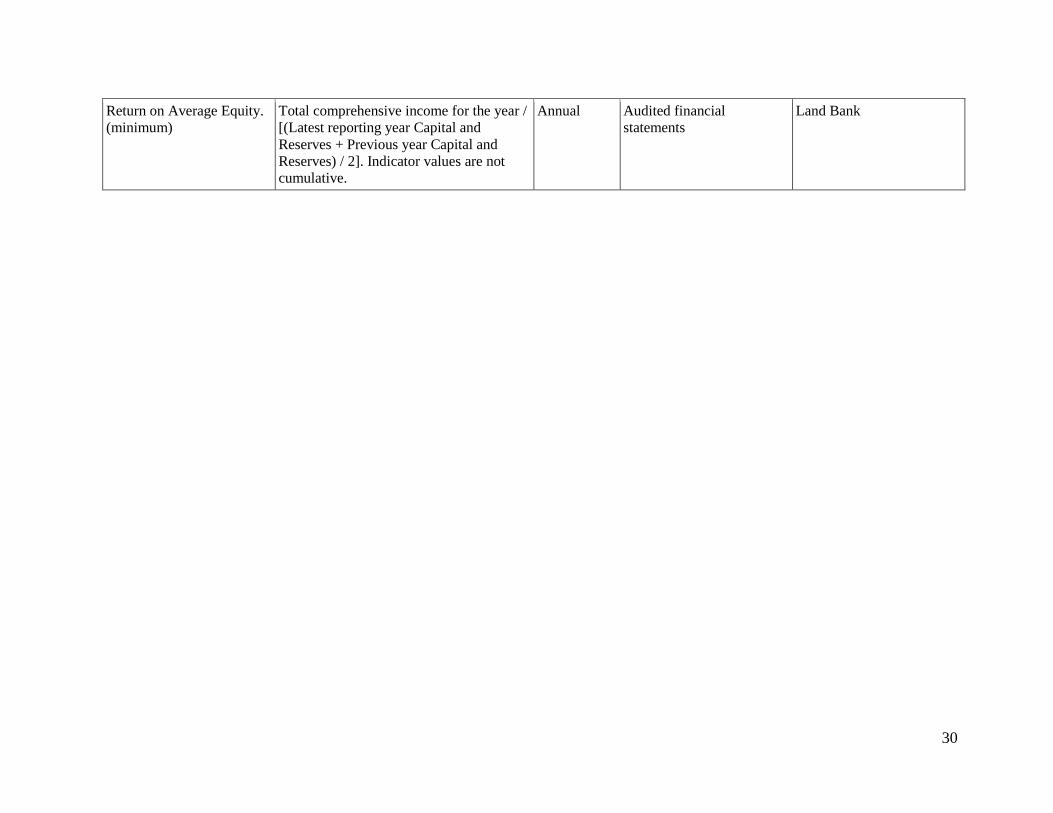

C. PDO Level Results Indicators ..................................................................................... 12

III. PROJECT DESCRIPTION ............................................................................................13

A. Project Components .................................................................................................... 13

B. Project Financing ........................................................................................................ 18

C. Project Cost and Financing ......................................................................................... 18

D. Lessons Learned and Reflected in the Project Design ................................................ 18

IV. IMPLEMENTATION .....................................................................................................20

A. Institutional and Implementation Arrangements ........................................................ 20

B. Results Monitoring and Evaluation ............................................................................ 21

C. Sustainability............................................................................................................... 21

V. KEY RISKS AND MITIGATION MEASURES ..........................................................22

A. Overall Risk Rating and Explanation of Key Risks.................................................... 22

VI. APPRAISAL SUMMARY ..............................................................................................22

A. Economic and Financial Analysis ............................................................................... 22

Financial Analysis ............................................................................................................. 22

B. Technical ..................................................................................................................... 23

C. Financial Management ................................................................................................ 23

D. Procurement ................................................................................................................ 24

E. Social and Environment (including Safeguards) ........................................................ 24

F. World Bank Grievance Redress .................................................................................. 26

Annex 1: Results Framework and Monitoring .........................................................................27

Annex 2: Detailed Project Description .......................................................................................31

Annex 3: Assessment of Land Bank ...........................................................................................41

Annex 4: Implementation Arrangements ..................................................................................52

Annex 5: Implementation Support Plan ....................................................................................62

Annex 6: Economic and Financial Analysis ..............................................................................65

Annex 7: Financial Sector, Agricultural Financing and Extension Services Overview ........71

Annex 8: PFI Due Diligence Criteria and Summary ................................................................87

i

PAD DATA SHEET

South Africa

Land Bank Financial Intermediation Project (P150008)

PROJECT APPRAISAL DOCUMENT

AFRICA

Finance and Markets Global Practice

Report No.: PAD1122

Basic Information

Project ID EA Category Team Leader(s)

P150008 F - Financial Intermediary

Assessment

Gunhild Berg, Uzma Khalil

Lending Instrument Fragile and/or Capacity Constraints [ ]

Investment Project Financing Financial Intermediaries [ X ]

Series of Projects [ ]

Project Implementation Start Date Project Implementation End Date

23-Jan-2017 1-Apr-2022

Expected Effectiveness Date Expected Closing Date

31-May-2017 31-Mar-2022

Joint IFC

No

Practice

Manager/Manager

Senior Global Practice

Director Country Director Regional Vice President

Alejandro Alvarez de

la Campa Gloria M. Grandolini Ivan Velev Makhtar Diop

Borrower: Land and Agricultural Development Bank of South Africa

Responsible Agency: Land and Agricultural Development Bank of South Africa

Contact: Bennie van Rooy Title: Chief Financial Officer

Telephone No.: 27-83380-0672 Email: [email protected]

ii

Project Financing Data(in USD Million)

[ X ] Loan [ ] IDA Grant [ ] Guarantee

[ ] Credit [ ] Grant [ ] Other

Total Project Cost: 93.00 Total Bank Financing: 93.00

Financing Gap: 0.00

Financing Source Amount

Borrower 0.00

International Bank for Reconstruction and

Development

93.00

Total 93.00

Expected Disbursements (in USD Million)

Fiscal

Year

2017 2018 2019 2020 2021 2022

Annual 18.60 27.90 18.60 18.60 9.30 0.00

Cumulati

ve

18.60 46.50 65.10 83.70 93.00 93.00

Institutional Data

Practice Area (Lead)

Finance & Markets

Contributing Practice Areas

Cross Cutting Topics

[ ] Climate Change

[ ] Fragile, Conflict & Violence

[ ] Gender

[ ] Jobs

[ ] Public Private Partnership

Sectors / Climate Change

Sector (Maximum 5 and total % must equal 100)

Major Sector Sector % Adaptation

Co-benefits %

Mitigation

Co-benefits %

Finance General finance sector 30

Agriculture, fishing, and forestry General agriculture,

fishing and forestry

sector

20

Finance SME Finance 50

iii

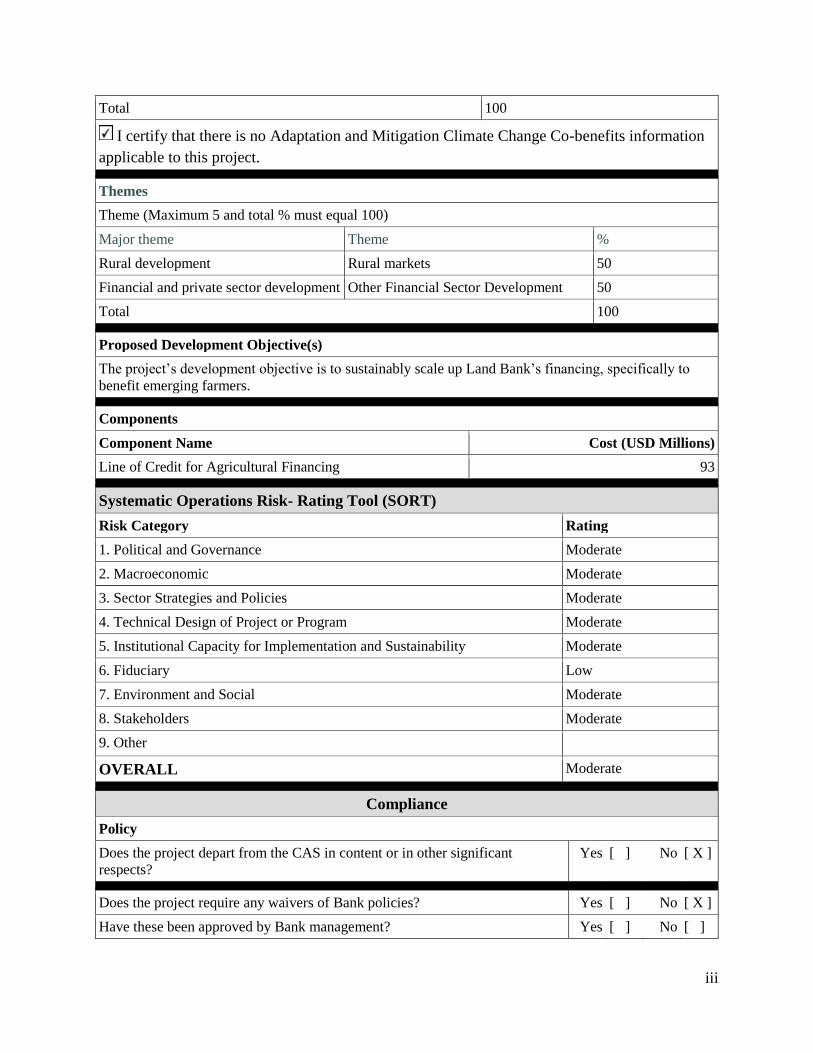

Total 100

I certify that there is no Adaptation and Mitigation Climate Change Co-benefits information

applicable to this project.

Themes

Theme (Maximum 5 and total % must equal 100)

Major theme Theme %

Rural development Rural markets 50

Financial and private sector development Other Financial Sector Development 50

Total 100

Proposed Development Objective(s)

The project’s development objective is to sustainably scale up Land Bank’s financing, specifically to

benefit emerging farmers.

Components

Component Name Cost (USD Millions)

Line of Credit for Agricultural Financing 93

Systematic Operations Risk- Rating Tool (SORT)

Risk Category Rating

1. Political and Governance Moderate

2. Macroeconomic Moderate

3. Sector Strategies and Policies Moderate

4. Technical Design of Project or Program Moderate

5. Institutional Capacity for Implementation and Sustainability Moderate

6. Fiduciary Low

7. Environment and Social Moderate

8. Stakeholders Moderate

9. Other

OVERALL Moderate

Compliance

Policy

Does the project depart from the CAS in content or in other significant

respects?

Yes [ ] No [ X ]

Does the project require any waivers of Bank policies? Yes [ ] No [ X ]

Have these been approved by Bank management? Yes [ ] No [ ]

iv

Is approval for any policy waiver sought from the Board? Yes [ ] No [ X ]

Does the project meet the Regional criteria for readiness for implementation? Yes [ X ] No [ ]

The project will have impacts that will be managed in a manner consistent with the following World

Bank Performance Standards:

Performance Standards Yes No

PS 1: Assessment and Management of Environmental and Social Risks

and Impacts

X

PS 2: Labor and Working Conditions X

PS 3: Resource Efficiency and Pollution Prevention X

PS 4: Community Health, Safety, and Security X

PS 5: Land Acquisition and Involuntary Resettlement X

PS 6: Biodiversity Conservation and Sustainable Management of Living

Natural Resources

X

PS 7: Indigenous Peoples X

PS 8: Cultural Heritage X

Legal Covenants

Name Recurrent Due Date Frequency

Description of Covenant

Conditions

Source Of Fund Name Type

IBRD Guarantee Agreement, refer Article V (5.01) of

Loan Agreement

Effectiveness

Description of Condition:

The Additional Condition of Effectiveness consists of the following, namely, that the Guarantee

Agreement has been executed and delivered and all conditions precedent to its effectiveness

(other than the effectiveness of this Agreement), have been fulfilled.

Source Of Fund Name Type

IBRD Front-end Fee, refer Schedule 2, Section III B

1 (a) of Loan Agreement

Disbursement

Description of Condition:

Notwithstanding the provisions of Part A of this Section, no withdrawal shall be made (a) from

the Loan Account until the Bank has received payment in full of the Front-end Fee.

Source Of Fund Name Type

IBRD Retroactive Financing, refer Schedule 2, Disbursement

v

Section III B 1 (b) of Loan Agreement

Description of Condition:

Notwithstanding the provisions of Part A of this Section, no withdrawal shall be made (b) prior

to the date of this Agreement, except that withdrawal up to an aggregate amount not to exceed

eighteen million six hundred thousand (US$18,600,000) may be made for payments made prior

to this date but on or after April 1, 2016 for Eligible under Category (1).

Team Composition

Bank Staff

Name Role Title Specialization Unit

Gunhild Berg Team Leader Senior Financial

Sector Specialist Financial Sector GFM01

Uzma Khalil Team Leader(ADM

Responsible)

Senior Financial

Sector Specialist Financial Sector GFM01

Chitambala John

Sikazwe

Procurement

Specialist

Senior Procurement

Specialist Procurement GGO01

Tandile Gugu Zizile

Msiwa

Financial

Management

Specialist

Financial

Management

Specialist

Financial

Management

GGO26

Ayanda Mavundla Team Member Financial Sector

Specialist Financial Sector GFM01

Christiaan Johannes

Nieuwoudt

Team Member Finance Officer Disbursement WFALA

David J. Nielson Team Member Lead Agriculture

Services Specialist Agriculture GFA05

Dorothe Singer Team Member Economist Research DECFP

Edith Ruguru Mwenda Counsel Senior Counsel Legal LEGAM

Elizabeth Chacko Team Member Consultant Financial Sector GFM01

Ioannis John Balafoutis Team Member Lead Financial

Officer/Debt

Capital Markets &

CBP

Treasury FABBK

Jemima Harlley Team Member Program Assistant Administrative AFCS1

Kisa Mfalila Safeguards

Specialist

Senior

Environmental

Specialist

Environment

Safeguards

GEN01

Lalit Raina Team Member Adviser Financial Sector GFM03

Magalie Pradel Team Member Program Assistant Administrative GFM01

Paula F. Lytle Safeguards

Specialist

Senior Social

Development

Specialist

Social Safeguards GSU07

vi

Maria Eileen Pagura Team Member Consultant Agriculture GFM01

Extended Team

Name Title Office Phone Location

Locations

Country First

Administrative

Division

Location Planned Actual Comments

South Africa

1

I. STRATEGIC CONTEXT

1. The Government of South Africa is pursuing an ambitious policy agenda to support

rural development and achieve a reduction in poverty and inequality. To attain this goal,

South Africa’s National Development Plan (NDP) focuses on agricultural development and

successful land reform as two of its top priorities. As a leading development finance institution in

the rural and agricultural sector, the Land and Agricultural Development Bank of South Africa

(henceforth Land Bank) is a key provider of agricultural financing, including to historically

disadvantaged emerging farmers. The Land Bank plays an important role in contributing to

poverty reduction and reducing income inequality. The proposed project aims to address market

failures in the provision of agricultural financing, access to finance for historically disadvantaged

emerging farmers, and limited availability of medium to long-term financing in South Africa.

The project will contribute to these broad objectives by supporting Land Bank with long-term

financing. It will help the Land Bank refocus its operations to sustainably scale up lending to

emerging farmers through wholesale channels along with extension services and through direct

lending channels to facilitate emerging farmers’ integration into established value chains. By

targeting farmers and farm workers who are considerably poorer than other income earners in

South Africa, the project will contribute to poverty reduction and income equality.

A. Country Context

2. More than twenty years after the end of apartheid, unemployment, poverty and

inequality remain important development challenges in South Africa, despite substantial

progress in overcoming the legacy of the past. While total employment increased from 9

million in 1996 to 16 million in 20151, the unemployment rate has stayed stubbornly high in the

range of 20-26 percent. In 2015 approximately 5.4 million South Africans were unemployed, of

which about 40 percent were new entrants.2 A 30 percent increase in per capita Gross Domestic

Product (GDP) since the late 1990s and a sharp expansion of the social grant coverage enabled a

significant decline in the poverty rate—from 43.5 percent of the population living below ZAR

219 (inflation-adjusted)3 a month in 2000 to 36.7 percent (or 18.3 million people) living below

ZAR 501 in 2015.4 Nevertheless, pockets of poverty remain deeply entrenched, mostly among

the historically disadvantaged population. With a relatively stagnant income Gini coefficient of

around 0.69 in 2011 (versus 0.72 in 2006 and expenditure Gini of 0.634 in 2015 (versus 0.67 in

2006), South Africa has one of the highest inequality rates in the world. Land distribution, in

particular, is one of the most unequal in the world.5 Threatening progress in poverty alleviation is

the impact of the drought on agriculture and the widening gap between those with and without

jobs.6

3. Recent developments in economic activity are not indicative of major improvements

in growth or employment. South Africa’s annual GDP is estimated to have increased by 1.3

1 Bulletin of Statistics, March 2016, Statistics of South Africa.

2 WBG South Africa Economic Update, February 2016.

3 Methodological report on rebasing of national poverty lines and development of pilot provincial poverty lines,

Statistics South Africa. Refers to population living below the National Lower Bound Poverty Line, those who can

purchase both adequate food and non-food items but must sacrifice food in order to obtain the non-food items. 2000

and 2011 data is from IES survey. 2011 data is based on rebased methodology. 4 WBG South Africa Economic Update, February 2016.

5 South Africa CPS FY2014-17.

6 WBG South Africa Economic Update, February 2016.

2

percent in 20157, compared to 1.5 percent in 2014 and 2.2 percent in 2013, a result of depressed

global conditions, as well as labor unrest and electricity shortages which compounded structural

constraints.8 This weak growth is well-below the projected 5 percent growth needed to drive

down unemployment. Inflation was relatively subdued in 2015 amid lower food and fuel prices

(5.2 percent as of December 2015, up from 4.8 percent in November). However the Reserve

Bank increased the repurchase rate by a total of 125 basis points from start 2015 to end March

2016 due to a deterioration of the inflation outlook as a result of the effects from rising food

prices due to the drought, the risk of a higher pass-through from the sharp depreciation of the

rand (depreciated by more than 30 percent against the dollar in 2015 and continued to weaken in

January 2016, before showing a subsequent moderate recovery) and subdued global growth.9

4. A weaker growth environment will pose a challenge in the management of the fiscal

deficit, which in turn increases the sovereign credit risk. In an effort to mitigate sovereign

credit risk, the National Budget Speech of February 2016 announced a strong fiscal adjustment

effort, bringing the fiscal deficit from 3.9 percent of GDP for 2015/16 to 2.8 percent by 2017/18.

The original target of the 2015 budget had been 2.5 percent, however deterioration in the growth

outlook rendered the target unrealistic. In December 2015, Fitch and Standard and Poor’s (S&P)

downgraded South Africa’s creditworthiness rating to BBB-, one notch above speculative grade,

and S&P placed its rating on negative watch. The turmoil in markets experienced in December

2015 when a weakening in the government’s commitment to fiscal discipline was perceived,

hints at the potential fallout from a further ratings downgrade.10

5. A substantial reduction in poverty and inequality will be hard to achieve without a

major success in rural development. As stated by South Africa’s National Development Plan

(NDP)11

, the main challenge for rural development in South Africa is to “combat the

marginalization of the poor”. While the rural share of poverty fell from 70 percent in 1993 to

58.3 percent in 2011,12

partly due to migration of the poor to townships and informal settlements

around urban centers, rural areas remain characterized by greater poverty and inequality than

urban areas. The contraction in agricultural production at double-digit rates in the first three

quarters of 2015, as extreme weather conditions related to El Nino led to the most severe drought

in almost 20 years, pushed an estimated 50,000 South Africans into poverty.13

6. Agriculture development and successful land reform are key pillars of the strategy

laid out by the NDP for integrated and inclusive rural development. South Africa’s

agriculture sector is characterized by dualism: a modern, market-oriented capital intensive

farming sector consisting of a small number of large commercial farms (around 40,000 farming

units14

) and a large number of subsistence and small-scale or emerging farms, many in the

former homeland areas. In addition, there is growing consolidation in the industry with a number

of mergers taking place and the acquisition of smaller players.15

While improving economies of

7 National Budget Speech, February 2016.

8 WBG South Africa Economic Update 2015.

9 Statement of the Monetary Policy Committee, March 2016.

10 Ibid

11 National Development Plan, p.195.

12 Poverty Trends in South Africa, An examination of absolute poverty 2006 – 2011, Statistics South Africa.

13 WBG South Africa Economic Update, February 2016.

14 Department of Agriculture, Forestry and Fisheries (DAFF): Abstract of Agricultural Statistics, 2010.

15 Examples include the merger of AFGRI and Senwes retail businesses to become Hinterland, OCEANA’s

acquisition of Foodcorp’s fishing business, Rainbow’s acquisition of 64 percent of Foodcorp as well as a stake in

Zambia’s Zambeef, among others.

3

scale, this consolidation may also lead to lower competition in the market. Around 2006, over

80 percent of South African farmers worked on a piece of land of one hectare or smaller, and

another 11 percent on one to five hectares. Only 3 percent had access to land of larger than 20

hectares.16

It is estimated that there are 2.5 – 3.5 million households engaged in subsistence

farming, about 350,000 – 700,000 who can be classified as emerging farmers, producing part of

their output for the market, and between 11,000 – 15,000 small to medium scale farmers who are

commercially oriented.17

7. The progress of land reform has been slow and a large number of land reform

beneficiaries are not using the land productively. The government committed itself to transfer

30 percent of the 82 million hectares of agricultural land owned by whites in 1994 to historically

disadvantaged farmers by 2014, a total of 24.5 million hectares, through both land restitution and

land redistribution. According to the Twenty Year Review published by the Presidency, only 9.4

million hectares have been redistributed since 1994 through both land restitution and

redistribution.18

Achieving the objective of “productive use” of redistributed and restituted land

requires even greater efforts and innovation. Land reform in South Africa to date has involved

the transfer of relatively large commercial farms in their entirety to groups of beneficiaries. Land

reform beneficiaries are typically resource-poor, risk-averse, and inexperienced historically

disadvantaged farmers. Support provided to them after their takeover of the land, that is post-

settlement support, has been inadequate. Land reform beneficiaries have experienced numerous

problems accessing services, such as credit, training, technology extension, transport, plowing

services, veterinary services, and marketing services. The well-developed agribusiness sector

that services large-scale commercial agriculture has not been seen extending its operations to

emerging farmers who, in most cases, would be cash-strapped and incapable of paying for such

services anyway.19

As a consequence, there is limited integration of small farmers into the value

chain.

8. Support for small-scale farmers is equally crucial to job creation. Employment in the

formal agriculture sector declined from 1.1 million in 1992 to 739,000 in 201420

despite output

growth. Nevertheless, the NDP believes that with successful rural development and land reform

the agriculture sector has the potential to create 1 million new jobs21

by 2030. The NDP counts

on small-scale/ emerging farmers for over 35 percent of the job creation target, in addition to a

10 percent share from subsistence farmers, a 10 percent share expected from better use of the

land that has already been redistributed or restituted to land reform beneficiaries, and a 30

percent share from expansion of labor intensive commercial farming.

16

National Development Plan, p.199. 17

DAFF: Abstract of Agricultural Statistics, 2012; FinScope, 2010; FinMark Trust: The Status of Agricultural and

Rural Financial Services in South Africa, 2013; Center for Inclusive Banking at the University of Pretoria: The

Microfinance Review, 2013. 18

The Presidency, Twenty Year Review, p.64. 19

Edward Lahiff and Guo Li. 2012. “Land Redistribution in South Africa -- A Critical Review”, pp.14-17. 20

The Presidency, Twenty Year Review, p.65. Several factors have undermined the growth of agricultural jobs.

These include higher levels of mechanization, driven partly by a desire to compete internationally. The necessary

introduction of rights for resident farm workers, including security of tenure, has resulted in one of the most intense

migration patterns in South Africa’s history. Close to a million people were uprooted from commercial farms

between 1994 and 2003, destroying jobs and undermining household food security. See “Economic Diagnostic”

prepared for the NDP, p13. 21

National Development Plan, p.197.

4

B. Sectoral and Institutional Context

9. South Africa’s financial sector is the most developed in Sub-Saharan Africa and is

significantly larger and more diversified compared to regional and income-group peers. It

is supported by an elaborate legal and financial infrastructure and a generally effective regulatory

framework. South Africa’s financial system totaled approximately ZAR 10 trillion in assets as of

year-end 2014 (US$ equivalent of 1,026 billion). As of end 2014, the banking sector constitutes

almost 40 percent of the financial system assets, with pension funds and long-term insurers each

contributing roughly 35 and 18 percent, respectively (see Annex 7 for a more detailed

description of the financial sector).

10. The banking sector is highly concentrated, but at the same time commercially

driven and professional. The ‘big four’ banks in South Africa, two of which are foreign

owned22

, account for over 83 percent of total banking assets. This concentrated ownership

structure has led to limited competition and distorted incentives for these banks to serve the

lower end of the market, especially micro, small, and medium-sized enterprises and the low-

income population. Nevertheless, the banking system generally is highly professional and

commercially driven, and does not suffer from distortionary policies.

Provision of agricultural finance and support

11. One of the main challenges for rural and agriculture development is affordable

access to working capital for emerging farmers and medium to long-term finance for small

and medium-sized agricultural enterprises. While the financial services needs of the large

commercial farms are generally well catered for by the private sector, farmers in rural areas

experience many of the challenges faced by their peers in other African countries, ranging from

difficulties in accessing markets, poor infrastructure, and little or no physical assets that could be

used as collateral for accessing financing. With few exceptions, emerging and small-scale

farmers are unable to use the land that they farm on as collateral given that the state owns most

of the land in the former homelands. FinScope’s 2010 Small Business Survey estimates that of

the roughly 700,000 emerging and small commercial farmers, only 5.6 percent used formal credit

services and only 2.5 percent from a bank. In contrast, nearly half of those farmers used formal

savings and/ or payments services and about 30 percent formal insurance.

12. Without adequate collateral, rural farmers face challenges in accessing credit from

traditional commercial banks. While the ‘big four’ commercial banks have made efforts to

become more inclusive, their business models and cost structure do not lend themselves to

serving the agricultural sector. Some banks are funding value chain off-take agreements23

with

large processors and retailers for on-lending to smaller farmers, but such lending is small

compared to the overall loan book of commercial banks. According to the Department of

Agriculture, Forestry and Fisheries (DAFF), total farming debt amounted to ZAR 116,576

million in 2014, out of which ZAR 66,345 million was from commercial banks and ZAR 30,580

22

One is majority and the other one minority foreign-owned. 23

Off-take agreements are agreements between a producer and a buyer to purchase/sell portions of the producer's

future production.

5

million from the Land Bank.24

Compared to total commercial bank loans and advances of ZAR

2,967 billion,25

agricultural lending amounts to about 1 percent of their total loan book.

13. A wide range of programs have been implemented by the government to provide

financial support to land reform beneficiaries and small-scale farmers. In 1994 the

government introduced the Settlement/Land Acquisition Grant (SLAG) to enable individuals and

groups to finance the purchase of land from a willing seller. Until 2000, redistribution policy

centered on the provision of a grant of ZAR 16,000 to qualifying households with an income of

less than ZAR 1,500 a month. In 2001 the Land Redistribution for Agricultural Development

(LRAD) Grant was introduced to establish and promote emerging farmers. LRAD offered higher

grants, paid to individuals rather than to households, and made greater use of loan financing

through institutions such as Land Bank to supplement the grant. A few years later, the slow pace

of land reform led to the introduction of the Proactive Land Acquisition Strategy (PLAS) in

2005-06. The use of grants for land acquisition was discontinued, and the focus was shifted to

the acquisition of strategically located land through PLAS by the state. Since its inception, PLAS

has become the biggest single program area within redistribution, in terms of both budget and

land area.26

14. There are also initiatives designed to provide post-settlement support to land reform

beneficiaries. The LRAD policy for example sets out to close the post-settlement support gap

that prevailed under SLAG. In addition, the Comprehensive Farmer Support Program (CFSP)

provides two grants, one for capacity building and one for on-farm infrastructure. In order to

access on-farm infrastructure grants ranging from a minimum of ZAR 5,000 to a maximum of

ZAR 100,000, beneficiaries must make an ‘own contribution’ along a sliding scale similar to that

of the LRAD grant program. It is a once-off support package designed for LRAD beneficiaries.27

The Comprehensive Agricultural Support Program (CASP) supported by DAFF offers grants to

support short-term operating expenses and small operating needs such as machinery. These

grants are managed at the provincial level and come from funds that are transferred from the

national to the provincial level. Combined land acquisition grants, both for redistribution and

restitution, totaled ZAR 13.6 billion between 2008 and 201228

while grants for movable

equipment and fixed improvements amounted to ZAR 13.4 billion between 2004 and 2012

(DAFF). Borrowing for working capital needs to operate and expand farms has been one of the

most acute challenges for emerging and small farmers as well as land reform beneficiaries due to

the reasons mentioned above.

15. Value chain integration is an opportunity to address significant skills and financing

gaps of emerging farmers. In South Africa, there is a growing recognition in government and

the private sector that value chain integration may be an effective way of building up a new class

of commercial emerging farmers. Drawing on the successful experiences in the sugar, poultry,

cotton, tobacco and forestry sectors, the government and private sector are joining forces to scale

up efforts in these and other sectors. A new area opening for value chain integration is in the

supply of fresh fruits and vegetables to retail supermarkets. With new Broad Based Black

Economic Empowerment (BBBEE) procurement policies government is encouraging the private

24

DAFF: Abstract of Agricultural Statistics, 2015. 25

SARB Selected South African banking sector trends December 2014. 26

The Presidency, Twenty Year Review, pp.63-4. Edward Lahiff and Guo Li. 2012. “Land Redistribution in South

Africa -- A Critical Review”, pp.8-12. 27

Peters Jacob. 2003. “Evaluating land and agrarian reform in South Africa”. 28

National Treasury: Medium-term Budget Policy Statement, 2008-12.

6

sector to get involved. For example, Walmart-Massmart has established a supplier fund to

support emerging farmer integration into their supply chain.29

The South African Poultry

Association through the creation of the Developing Poultry Farmers Organization (DPFO)

facilitates technical and financial assistance to access contracts with egg and poultry

businesses.30

Land Bank

16. In addition to government grants, financing from Land Bank has been expected to

play a critical role in land reform and agriculture development. Land Bank was established

in 1912 and is governed by the Land and Agricultural Development Bank Act of 2002. Land

Bank was given a mandate of 11 aspects, which fall into five broader areas: (i) access of the

historically disadvantaged population to land; (ii) agriculture productivity, growth and job

creation; (iii) gender equity; (iv) environmental sustainability; and (v) food security. The NDP

published in 2011 continues to call for a key role of Land Bank in providing financial support to

land reform beneficiaries and to help them overcome difficulties in entry into commercial

farming31

(see Annex 3 for detailed assessment of Land Bank).

17. As the leading development financial institution in the rural and agriculture sector

in South Africa, Land Bank had an approximately 29 percent market share in agricultural

financing as of July 2015. The bank32

has achieved a significant turnaround during the past five

years. It is now on a sustainable trajectory with profits of ZAR 420 million in 2014/15 (up 61

percent from 2013/14), and a Return on Average Assets of 1.12 percent and a Return on Average

Equity of 6.78 percent. Total assets stood at ZAR 39.4 billion in 2014/15 with a performing loan

book of ZAR 36 billion. Non-performing loans (NPLs) under Land Bank methodology were at

3.72 percent in 2014/15 and the cost-to-income ratio was 54.9 percent. Fitch Ratings upgraded

Land Bank from AA to AA+ in January 2014. The rating was maintained at AA+ in December

2015. Moody’s Investor Services has assigned Land Bank a credit rating of Aa1.za in May 2016. The

bank does not take general deposits and funds itself mainly through the debt and capital markets,

issuing instruments such as promissory notes.

18. Land Bank is fully owned by the South African government and supervised by the

National Treasury.33

It follows prudential guidelines as issued by its Board of Directors. It is

consequently not prudentially supervised by the South African Reserve Bank (SARB). The bank

is audited by the Auditor General. Land Bank is engaged in both wholesale lending through

intermediaries as well as direct lending. Intermediaries are mainly credit providers, cooperatives,

or agri-businesses.

19. In 2015, Land Bank adopted a new strategy following the completion of its

organizational review. The review was undertaken following conditions set by NT pursuant to

29

“Smallholders and agrifood value chains in South Africa – Emerging practices, emerging challenges,” 2013.

PLAAS, Institute for Poverty, Land and Agrarian Studies, School of Government, University of the Western Cape,

pp.1-4. 30

“A Profile of the South African Egg Industry Market Value Chain,” 2014. Department of Agriculture, Forestry

and Fisheries, Republic of South Africa, pp.22-24. 31

National Development Plan, p.200. 32

Source of financial information is Land Bank’s 2014 and 2015 Annual Report. Per the report, Land Bank Group

includes REM, RCB, B&CB, LDFU, and LBLIC. Land Bank only includes REM, RCB, B&CB and Group Capital. 33

In 2008, the administrative and supervisory powers over Land Bank were transferred from the Minister of

Agriculture and Land Affairs to the Minister of Finance.

7

the issue of a government guarantee, aimed at enabling the Land Bank to raise longer term

funding. The review was completed in August 2015, and subsequently an implementation plan

was approved by the Land Bank Board. Land Bank has started implementing the new strategy

and key changes are planned to be put in place over a two-year period in line with the priorities

of Land Bank. The changes focus on: (i) a strategy to optimize the retail commercial banking

segment of Land Bank, the long-term viability of which was a concern owing to loan losses and

significant operational costs; (ii) new initiatives to potentially expand the development portfolio

of Land Bank for emerging farmers34

in a sustainable and commercially viable manner by

adopting a project finance approach in partnership with large corporates and intermediaries to

integrate the emerging farmers into established value chains; and (iii) steps to align Land Bank

financial soundness indicators, credit appraisal processes and risk management practices with

international banking standards.

20. Following the adoption of this new strategy, Land Bank has two main business lines:

Corporate Banking (CB) and Commercial Development Banking (CDB).35

The new CDB

business line is a combination of previous Retail Emerging Markets (REM) and Retail

Commercial Banking (RCB) business lines. In 2014/15, CB accounted for 83.6 percent of the

bank’s loan book and CDB accounted for 16.4 percent, of which 1.3 percent was composed of

loans provided under REM.36

21. Under CDB, the wholesale finance facility continues to focus on lending to emerging

farmers for development purposes. Farmers supported under this facility typically have no or

limited access to commercial funding and little or no collateral, but can be commercially

sustainable and viable with financing and technical support. Subsistence farmers are not

supported under CDB. Lending is based on cash-flows and non-financial support (end to end on-

farm support) is provided by Land Bank intermediaries and agricultural specialists based in Land

Bank branches.37

The wholesale lending to emerging farmers offers production financing,

installment sale finance, and medium-term loans. The total wholesale finance portfolio to

emerging farmers amounted to ZAR 489 million in 2014/15 (increase of ZAR 97 million in that

year).

22. Intensive and high-quality extensions services under the wholesale finance facility to

emerging farmers are effectively provided by Land Bank’s intermediaries. These

intermediaries have a comparative advantage in providing these services due to their close

interaction with the beneficiaries. The non-financial complementary services, especially

extension services, are critical for emerging farmers to develop (see Annex 7 for a summary of

extension services provided in South Africa). The costs for the extension services are embedded

in the overall cost structure under wholesale finance facility and are borne by the

intermediaries.38

While the provision of extension services is costly, especially for new emerging

farmers, intermediaries can generate profits from these clients over time due to the long-run and

comprehensive nature of engagement between intermediaries and their clients. The current

34

In addition to existing wholesale lending currently provided under REM. 35

The new Corporate Banking unit is the former Business and Commercial Banking unit. . 36

Information in Land Bank’s 2015 Annual Report is disaggregated by former three business lines i.e. B&CB, RCB

and REM. For the purpose of analysis in this section, the financial information for RCB and REM is consolidated

where appropriate. 37

These refer to the existing branches and Agricultural Finance Centers. 38

This means that intermediaries are shouldering the costs of providing required extension services instead of Land

Bank, partly justifying the lower-cost financing they are receiving.

8

model of providing extension services is considered to be of high quality according to the

assessment carried out during project preparation.

23. Under CDB, the RCB business line which was exclusively focused on direct retail

lending to medium scale farmers, through 27 Agriculture Finance Centers (AFCs), has

been significantly restructured to improve its long term sustainability. RCB was loss-

making due to high operating costs of the large branch network and had NPLs of 11 percent in

2014/15. RCB was losing clients to commercial banks and agricultural enterprises who started to

lend in that space and could offer a wider range of products. The competitiveness and long-term

viability of RCB was therefore questionable. The new strategy aims at consolidating the branch

network into 9 provincial offices in strategically important geographical locations which will

also result in significant staff reduction. Importantly, the consolidated branch network’s role will

specifically focus on facilitating effective partnerships in their respective regions with corporate

retailers, emerging farmers, government programs, as well as technical and financial

intermediaries to leverage on high impact and high value chain finance deals.

24. Importantly, as part of the new strategy, Land Bank aims to scale up financing

support to emerging farmers in a sustainable and commercially viable manner through

their integration in established value chains. The approach is anchored in identifying high-

potential value chain projects in a given geographic region and securing buy-in from large

agriculture corporates or technical partners to assist in supporting emerging farmers’ integration

into the chain. The agriculture corporates will provide technical support (directly or indirectly) to

the emerging farmers, building up their capacity to be sustainable suppliers to the chain. Land

Bank has identified selected potential value chain projects and agriculture corporates to partner

with in the grains, winery, horticulture and livestock sectors for this type of financing.

25. The CB business line is the corporate part of the bank and the most viable business

line. The CB business line involves both direct and wholesale lending. Lending takes place

primarily through intermediaries (cooperatives and agri-businesses). CB operates through two

offices in Pretoria and Cape Town. The total portfolio of CB amounted to ZAR 31 billion in

2014/15. While CB targets commercial farmers, the workers employed on these farms tend to be

part of the low-income population.

26. Land Bank aims at increasing its developmental focus in both CB and CDB business

lines by strengthening its wholesale business as well as its direct lending to emerging

farmers. Both business lines contain a development portfolio with “development” referring to a

focus on supporting the historically disadvantaged population in line with Broad-Based Black

Economic Empowerment (BBBEE).39

International experience with development banks suggests

that wholesale lending is more likely to be successful than retail lending. The key reason is that

wholesale lending does not require a large branch network which is costly to build and maintain

but rather leverages the networks already built by other financial service providers. Wholesale

lending is also more market enabling and does not aim at competing with the private sector.

Direct lending via value chain financing leverages the corporate partner’s ability to provide

technical support to the borrower, building up their capacity to be sustainable suppliers to the

chain. As such, emerging farmers in this scheme have the potential to increase their revenues and

thus a greater likelihood of fulfilling debt obligations to the bank. The project will therefore

focus on supporting Land Bank in scaling up its wholesale portfolio as well as expanding direct

39

http://www.economic.gov.za/about-us/programmes/economic-policy-development/b-bbee.

9

lending through LB’s new approach of integrating emerging farmers into established value

chains. Using long-term financing to fill existing funding gaps will additionally help Land Bank

meet its investment needs as well as improve its asset liability management.

27. Land Bank is making an important contribution to job creation. Land Bank

estimates that the impact of its loan disbursements on employment opportunities in South Africa

was close to 400,000 in 2013-2014.40

This estimate is comprised of over 23,000 new

employment opportunities generated and over 370,000 jobs maintained during the year. One

employment opportunity constitutes 240 days worked per year. The estimated new jobs created

are arising out of the medium and long-term loans Land Bank is providing.

C. Higher Level Objectives to which the Project Contributes

28. Through the role of Land Bank in rural and agricultural development, the project is

strongly linked to the government’s objectives of eliminating poverty, reducing inequality

and improving job creation. The goals of the NDP are fully aligned with the twin goals of the

World Bank to eradicate extreme poverty and increase shared prosperity. The operation has been

requested by National Treasury and Land Bank and carefully calibrated to their specific needs.

29. The project will contribute to poverty reduction by targeting farmers and farm

workers who are considerably poorer than other income earners. According to South

African household data (Table 1), an approximation for those working as farmers and farm

workers shows that this group is twice as poor as other workers, receives about 53 percent less

income, and lives in households with consumption per capita about 54 percent lower than other

workers. The difference holds for international as well as national poverty lines. The group is

also predominantly black. The project will support Land Bank in providing financing to those

farmers and farm workers, which will contribute to poverty reduction.

Table 1: Poverty Characteristics of Farmers in South Africa

Source: World Bank calculations based on Income and Expenditures of South Africa Metadata, Statistics of South Africa.

Notes: Farmers (all) is an approximation of the universe of farmers. Other wage earners includes those with gainful employment

outside of farming, and ‘other groups’ includes non-wage earners including social grant and pension recipients. The national

poverty lines are defined as ZAR335, ZAR 501 and ZAR 779 per capita per month respectively. The lowest poverty line sets a

monetary value below which an individual is not able to attain a basic minimum nutritional requirement.

30. Through supporting Land Bank’s growth and development plan, the project will

support job creation in the agricultural sector in South Africa. Based on Land Bank’s

estimates, the bank is playing an important role in job creation and job maintenance in South

Africa. Jobs are not only created for emerging farmers under the CDB business line but also for

poor farm workers who are employed on commercial farms supported under CB. Given that the

project will provide long-term funds to Land Bank, which the bank estimates to contribute most

40

Land Bank Annual Report 2013-2014.

Population $1.25 a day $2.5 a day National Low National Med National Upper

Total Economy 50,175,588 0.12 0.36 0.22 0.37 0.54 0.79 21,472

Farmers (all) 465,360 0.10 0.32 0.18 0.33 0.52 0.92 20,447

Other Wage Earners 11,524,933 0.04 0.16 0.08 0.17 0.31 0.68 34,870

Other groups (non-wage,

including social grant

beneficiaries) 38,185,295 0.14 0.42 0.26 0.43 0.61 0.83 17,441

Poverty Rates Share of

Blacks

Average

Consumption

10

to job creation and which the bank will on-lend to farmers through its intermediaries, the project

will have a direct contribution to job creation in the agricultural sector of South Africa.

31. The project will address market failures in the provision of agricultural financing

and limited access to finance for previously disadvantaged emerging farmers. Commercial

bank financing for agriculture amounts to 1 percent of commercial bank’s loan book (ZAR 2,753

billion) which is low compared to farmers reported demand. In addition, financing from

commercial banks can typically not be accessed by emerging farmers due to a lack of adequate

collateral. The CDB business Land Bank is designed to specifically provide financing to

emerging farmers, who do not have collateral as security, so that these farmers can later become

commercially viable. In addition, the CB business line also has a large developmental portfolio

in line with BBBEE and indirectly supports poor farm workers employed on the commercial

farms supported under CB. The project will support Land Bank in addressing these market gaps

by providing additional resources to specifically finance emerging farmers in a sustainable

manner.

32. Moreover, the project will support Land Bank in piloting its new approach to scale

up financing for emerging farmers by facilitating their integration into established value

chains. The emerging farmers lack financing and operate largely outside of the established

agriculture value chains. However, partnerships with corporates and technical partners operating

in the same value chain have demonstrated the potential for addressing farmers’ skills and

financing gaps by sustainably integrating emerging farmers into established value chains. This

project will support Land Bank’s initiative to finance such projects, by directly lending to

emerging farmers within a structured value chain project.

33. The project will also address the limited availability of medium to long-term

financing for Land Bank. Currently, Land Bank predominantly relies on short-term funding

sources for lending to the agricultural sector due to limited availability of medium and long-term

financing. The availability of long-term financing under the project will help Land Bank in

improving its asset-liability management and deepening its financial intermediation capacity.

34. The project will complement the active WBG engagement with the government on

achieving its rural development and financial inclusion objectives. Under the reimbursable

advisory services program agreed with the Department of Rural Development and Land Reform

(DRDLR) in 2010, the World Bank is providing knowledge advisory services to support the

development and implementation of the Comprehensive Rural Development Program that will

also help government in addressing some of the challenges faced in the implementation of the

land reform program. A US$4 million multi-donor World Bank executed Trust Fund launched in

2014, the Financial Sector Development and Reform Program (FSDRP), provides analytical and

advisory services to the South African government on a range of initiatives aimed at expanding

financial inclusion and strengthening financial stability. Among the activities in the financial

inclusion space are advice on the establishment of a credit information service for SMEs and a

movable collateral registry, a review of government support schemes aimed at expanding SME

finance, a strengthening of the retail payments landscape including agency and mobile banking,

and advice on personal insolvency and an enhanced consumer protection framework. The WBG

also delivered a diagnostic report on the possibility of public private partnerships for agricultural

insurance to the National Treasury in 2016 and is currently discussing possibilities to provide

support on this area going forward. Moreover, IFC is engaged with private financial institutions

11

to enhance private sector access to funding through short-term liquidity support and longer-term

foreign currency funding.

35. The operation is fully aligned with the Country Partnership Strategy (CPS) for

South Africa for the period of FY2014-1741

and the Twin Goals of the World Bank Group

to eradicate extreme poverty and increase shared prosperity. The project is expected to

contribute to all three pillars of the CPS. First of all, it supports the reduction of inequality by

increasing access to finance for the historically disadvantaged population, specifically to benefit

emerging farmers. Secondly, it catalyzes private investment in rural development and agriculture

through financing solutions provided by Land Bank. Thirdly, it helps strengthening institutional

capacity of Land Bank on agricultural financing as well as asset-liability management, and the

capacity of its intermediaries.

II. PROJECT DEVELOPMENT OBJECTIVES

A. PDO

36. The project’s development objective is to sustainably scale up Land Bank’s

financing, specifically to benefit emerging farmers. The PDO will be achieved by providing

long-term financing for Land Bank. This will facilitate a broader and deeper financial

intermediation by Land Bank and diversify its funding sources away from government.

B. Project Beneficiaries

37. Project beneficiaries will be the target beneficiaries under CDB and CB business

lines as detailed in the respective credit policies. The wholesale finance facility under CDB

focuses on historically disadvantaged South Africans in primary agriculture fulfilling certain

criteria, such as a maximum asset size of ZAR 3 million, access to land, farming on a full-time

basis, difficulties in accessing traditional financing due to a lack of security, and existing off-take

agreements or contracts in place. CB clients are either historically disadvantaged or other clients

engaged in primary and secondary agriculture. According to the CB credit policy, they must be

solvent, have viable business plans, and adequate security, among others. Indirectly, the project

will benefit the poor farm workers employed in the commercial farms supported by CB. Under

Land Bank’s new approach to scale up financing support to emerging farmers in a commercially

viable manner through integrated value chain finance projects (or partnerships), the target

beneficiaries are groups of historically disadvantaged emerging farmers in the form of an agri-

business, cooperative or other forms of partnerships and engaged in primary and secondary

agriculture. The beneficiaries will benefit from the financing provided by Land Bank for

investment and working capital loans. In addition, participating financial intermediaries (PFIs)

will benefit from the longer-term funding provided through the project.

38. The target beneficiaries are farmers under CDB and emerging farmers under CB

who are more likely to be poor than other income earners. As shown in Table 1 above, the

target beneficiaries are twice as poor as other workers and receive about 53 percent less income.

By supporting those farmers and emerging farmers through financing, Land Bank and the project

will contribute to poverty reduction and income equality, subject to high quality extension

services and the infrastructure required for successful farming being in place as well.

41

Country Partnership Strategy (CPS) for South Africa for period of FY2014-14, Report No. 77006-ZA, October

17, 2013.

12

C. PDO Level Results Indicators

39. The achievement of the objectives and outcomes of this project will be measured

through the following PDO results indicators:

Volume of wholesale loans disbursed under the project (amount US$).

Volume of direct value chain loans disbursed under the project (amount US$).

Number of direct project beneficiaries.

Total NPL rate under the credit line (%).

Intermediate results indicators will be as follows:

Increase in outstanding loan portfolio of Land Bank (%).

Increase in CB outstanding loan portfolio of Land Bank (%).

Increase in REM outstanding loan portfolio of Land Bank (%).

NPL rate for Land Bank (%).

Land Bank liabilities that are long-term (over 1 year) (%).

Return on Average Equity (%).

Land Bank Return on Assets/ Equity (%).

Figure 1: Project Level Result Chain

40. The indicators primarily focus on measuring the change in Land Bank’s business

model towards wholesale financing and increasing its developmental impact through

increased lending to emerging farmers. As the PDO is targeted at changing the behavior of

Land Bank, and ultimately the use of wholesale financing as a mechanism to affect agricultural

Input Activity Output Outcomes

US$93 MM LoC from WBG

WBG disburses to LB

LB disburses

Primary1) Expand LB’s wholesale lending

business through increased lending to PFIs

2) Support value chain financing partnerships

Secondary1) Demonstration effect PFIs

increase lending (to commercial and emerging farmers) and extension services (to emergingfarmers)

2) Integrate emerging farmers into value chains

Tertiary1) Increase access to medium and

long-term finance for commercial and emergingfarmers

2) Promote job creation and income generation

WBG Complimentary Engagements

1) RAS on land Reform2) Assessment of extension services in

South Africa3) FSDRP on financial inclusion, incl. e.g.

credit bureaus, collateral registries, and SME finance

4) IFC investments

Corporate Commercial

DevelopmentCorporate

Commercial Development

Project level Results Chain

13

financing in the longer-term, the indicators above measure how the project will contribute to

Land Bank’s overall portfolio and its asset-liability management framework. While it is

anticipated that the project will benefit the CDB and CB target customers, it would not be

prudent to measure beneficiary level impact in this project because the link between the project

and these beneficiaries is not direct.

III. PROJECT DESCRIPTION

A. Project Components

41. The project is a financial intermediary loan (FIL) of US$93 million to Land Bank as

the borrower and implementing agency with a guarantee of the Republic of South Africa.

The project has one component: a Line of Credit (LOC) for Agricultural Financing in the amount

of US$93 million.

Component 1: Line of Credit for Agricultural Financing (US$93 million)

42. The objectives of the LOC component are to:

Support Land Bank in refocusing its operations on wholesale lending. As explained in

section I.B., Land Bank uses both wholesale and direct lending under the Corporate

Banking (CB) and Commercial Development Banking (CDB) business lines. Given Land

Bank’s limited branch network and based on international best practices for Development

Finance Institutions (DFIs), wholesale lending is more sustainable because it helps Land

Bank leverage a network of financial intermediaries without incurring significant

operating costs. In addition, wholesale lending allows Land Bank to play a market

enabling role because it permits agricultural borrowers to build credit history with

financial intermediaries and improve their financial records for commercial loans, thus

improving their ability to gain access to credit. The LOC will help Land Bank in

expanding wholesale lending to both commercial and emerging farmers under the CB and

CDB business lines respectively. Through supporting the CB business line, the LOC will

support employment generation for poor farm workers employed on the commercial

farms supported. The CB business line also contains a large and growing developmental

portfolio in line with BBBEE, therefore making an important contribution to the NDP

and Land Bank’s development goals.

Support Land Bank’s new approach to help integrate emerging farmers into established

value chains. Based on the outcomes of its organizational review, Land Bank decided to

scale up financing support to emerging farmers in a sustainable and commercially viable

manner through partnerships with large agriculture corporates that emphasize integrating

emerging farmers in established value chains. The approach is anchored in identifying

high-potential value chain projects in a given geographic region and securing buy-in from

large agriculture corporates or technical partners to assist in supporting emerging

farmers’ integration into the chain. The agriculture corporates will provide technical

support (directly or indirectly) to the emerging farmers, building up their capacity to be

sustainable suppliers to the chain. Land Bank has identified potential value chain projects

and agriculture corporates to partner with in the grains, winery, horticulture and livestock

sectors for this type of financing. The success of these initiatives is expected to have a

demonstrative effect in the medium term helping to bring in commercial banks’ financing

for such initiatives and agriculture in general which is currently very limited.

14

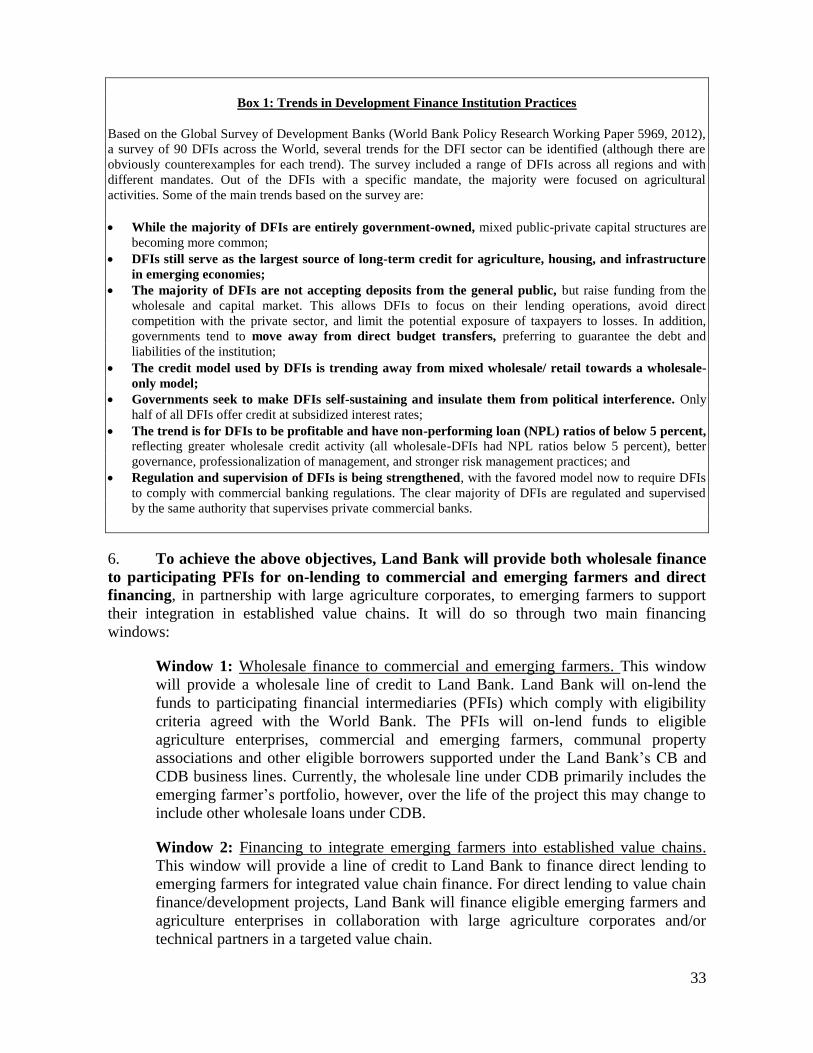

Box 1: Trends in Development Finance Institution Practices

Based on the Global Survey of Development Banks (World Bank Policy Research Working Paper 5969, 2012), a

survey of 90 DFIs across the World, several trends for the DFI sector can be identified (although there are obviously

counterexamples for each trend). The survey included a range of DFIs across all regions and with different

mandates. Out of the DFIs with a specific mandate, the majority were focused on agricultural activities. Some of the

main trends based on the survey are:

While the majority of DFIs are entirely government-owned, mixed public-private capital structures are

becoming more common;

DFIs still serve as the largest source of long-term credit for agriculture, housing, and infrastructure in

emerging economies;

The majority of DFIs are not accepting deposits from the general public, but raise funding from the

wholesale and capital market. This allows DFIs to focus on their lending operations, avoid direct competition

with the private sector, and limit the potential exposure of taxpayers to losses. In addition, governments tend to

move away from direct budget transfers, preferring to guarantee the debt and liabilities of the institution;

The credit model used by DFIs is trending away from mixed wholesale/ retail towards a wholesale-only

model;

Governments seek to make DFIs self-sustaining and insulate them from political interference. Only half of

all DFIs offer credit at subsidized interest rates;

The trend is for DFIs to be profitable and have non-performing loan (NPL) ratios of below 5 percent,

reflecting greater wholesale credit activity (all wholesale-DFIs had NPL ratios below 5 percent), better

governance, professionalization of management, and stronger risk management practices; and

Regulation and supervision of DFIs is being strengthened, with the favored model now to require DFIs to

comply with commercial banking regulations. The clear majority of DFIs are regulated and supervised by the

same authority that supervises private commercial banks.

43. To achieve the above objectives, Land Bank will provide both wholesale finance to

participating PFIs for on-lending to commercial and emerging farmers and direct

financing, in partnership with large agriculture corporates, to emerging farmers to support their

integration in established value chains. It will do so through two main financing windows:

Window 1: Wholesale finance to commercial and emerging farmers. This window will

provide a wholesale line of credit to Land Bank. Land Bank will on-lend the funds to

participating financial intermediaries (PFIs) which comply with eligibility criteria agreed

with the World Bank. The PFIs will on-lend funds to eligible agriculture enterprises,

commercial and emerging farmers, communal property associations and other eligible

borrowers supported under the Land Bank’s CB and CDB business lines. Currently, the

wholesale line under CDB primarily focuses on lending to emerging farmers, however,

over the life of the project this may change to include other wholesale loans under CDB.

Window 2: Financing to integrate emerging farmers into established value chains. This

window will provide a line of credit to Land Bank to finance direct lending to emerging

farmers for integrated value chain finance. For direct lending to value chain

finance/development projects, Land Bank will finance eligible emerging farmers and

agriculture enterprises in collaboration with large agriculture corporates and/or technical

partners in a targeted value chain.

15

44. It is expected that 70 percent of LOC funds will be used to support wholesale

lending and 30 percent will be used for direct lending to emerging farmers for their

integration in established value chains. However, this ratio will be kept flexible in both

directions to allow for adjustments based on market and portfolio developments in the bank’s CB

and CDB business lines.

45. Consistent with Land Bank’s pricing policies, the interest rates to intermediaries in

wholesale financing and for borrowers through direct financing will be determined by the

customer segment.

Window 1: Commercial farmers under CB. Land Bank will on-lend funds to PFIs at

interest rates that take into account at minimum Land Bank’s cost of funding, operating

costs and an appropriate credit risk margin.

Window 1: Emerging farmers under CDB. For these farmers, Land Bank will on-lend

funds to intermediaries at interest rates that will allow the bank to at least cover its

average costs of funds.

Window 2: Emerging farmers in established value chains. The pricing for direct lending

by Land Bank to integrate emerging farmers in established value chains will be market-

based. Land Bank aims to implement the new approach to scale-up financing for

emerging farmers in a commercially viable and sustainable manner. Thus, pricing for this

financing will cover Land Bank’s cost of funding, operating costs and an appropriate

credit risk margin.

46. The interest rates to final borrowers will be market-based to ensure sustainability

and avoid creating interest rate distortions in the market. The PFIs for both commercial and

emerging farmers will be able to freely set their interest rates, which are expected to cover at

least the cost of funding, operational costs and an appropriate credit risk premium based on the

credit assessment of the borrower.

47. The lower interest rates for emerging farmers under wholesale finance facility will

allow Land Bank and the PFIs to finance clients that would otherwise be excluded from

formal sector financing. While on-lending for emerging farmers will initially be at average cost

of funds, these farmers are expected to be able to graduate to commercial funding after a period

of five years, underlining the sustainability of the program. Moreover, Land Bank is currently

reviewing its wholesale finance facility to emerging farmers pricing policy to allow Land Bank

to at least break-even on pricing by covering at least its average cost of funds and operating

costs. In addition, interest rates for emerging farmers under CDB will be subject to continuous

review to ensure that the objectives of the program are achieved while ensuring Land Bank’s

sustainability.

48. To meet its wholesale lending objectives under CB and CDB business lines, Land

Bank is currently engaged with a broad range of intermediaries. Those include agricultural

cooperatives, large agricultural companies, and credit providers. These intermediaries have a

credit provider license and are supervised under the National Credit Act by the National Credit

Regulator. The intermediaries are primarily providing credit to their clients with whom they have

existing business relationships in the form of input supplies contracts, off-take agreements etc.

and provide technical advisory services specifically to emerging farmers. Currently, Land Bank

16

is working with ten intermediaries who are engaged under both CB and CDB. In addition,

additional intermediaries in the pipeline are expected to operate for both CB and CDB. These

intermediaries are providing financing for sugar cane, grain, citrus, fruits, vegetables and

livestock. The intermediaries are geographically spread across all provinces.

49. In addition to financing, the intermediaries provide intensive and high-quality

extension services, particularly to emerging farmers. Since Land Bank’s intermediaries have

been engaged in agricultural activities for the past several decades, they have developed a unique

comparative advantage in providing extension services to farmers specifically tailored to their

individual needs. These extension services include training, skills development and mentoring of

smallholder beneficiaries and range from hands-on advice on crop selection, plantation, inputs

needs and harvesting to training on agriculture marketing, business planning etc. For the

wholesale finance facility to emerging farmers, these extension services are embedded in the

financing, recognizing the fact that emerging farmers need financing as well as technical

assistance to succeed. A review of extension services in South Africa found that these programs

have proved successful in establishing commercially successful emerging farmers (see Annex 7

for more details).

50. While all interested PFIs of Land Bank will ultimately be appraised, Land Bank

and the World Bank initially selected six intermediaries that are operating in both the CB

and CDB business line and assessed them against the eligibility criteria. The eligibility

criteria took into consideration Land Bank’s selection criteria for intermediaries and the

recommendations on financial intermediary financing under the World Bank’s Operational

Policy OP10. The OP10 policy requires an assurance that all PFIs in a World Bank financed

LOC are viable financial institutions determined by: (a) adequate profitability, capital, and

portfolio quality as confirmed by audited financial statements; (b) acceptable level of loan

collections; (c) appropriate capacity, including staffing, for carrying out subproject appraisal

(including environmental assessment) and for supervising subproject implementation; (d)

capacity to mobilize domestic resources; (e) adequate managerial autonomy and commercially

oriented governance; and (f) appropriate prudential policies, administrative structure, and

business procedures. Annex 8 contains the detailed eligibility criteria for PFI participation in the

LOC. Land Bank will enter into Sub-Loan Agreements (SLA) with the selected PFIs, which will

specify terms and conditions on the use of the LOC as agreed between Land Bank and IBRD.

PFIs will not be obliged to draw on the available funding, and interest costs and other fees will

only be charged upon accessing the LOC.

51. Based on the assessment, two intermediaries fully meet the eligibility criteria and

three generally meet the criteria for participation in LOC. Of the six intermediaries

appraised during preparation, two intermediaries fully meet the eligibility criteria; two

intermediaries generally meet the eligibility criteria except for capital structure; and one

intermediary generally meets the eligibility criteria, however it needs to improve the quality of

its loan portfolio and cash flows going forward. One intermediary does not meet the eligibility

criteria at this moment, however it can participate as intermediary once the issues identified in

the due diligence are resolved. Annex 8 describes the eligibility criteria in more detail.

52. The available LOC funding will be used based on a drawdown mechanism. Once

PFIs are approved for funding from Land Bank, they receive a drawdown facility of the

approved amount with a fixed maturity, for example five years, which they can use to finance

projects complying with the agreed eligibility requirements. Loans to final beneficiaries will be

17

provided by PFIs from the drawdown facility up to the amount and maturity approved. Land

Bank will receive funding from the LOC based on the submission of internally approved

drawdown facilities for intermediaries in line with the eligibility criteria or the submission of

interim financial reports. There will be a limit of 25 percent of the LOC facility per intermediary