world bank document - documents &...

TRANSCRIPT

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 4064-MLI

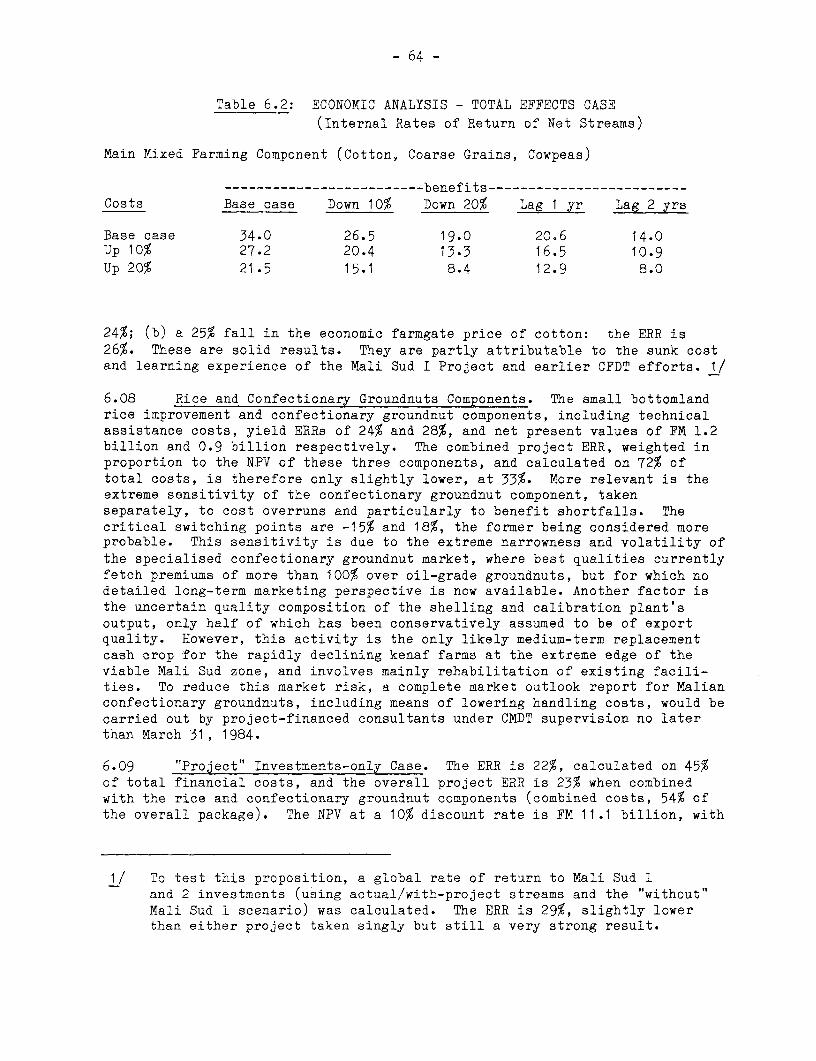

STAFF APPRAISAL REPORT

MALI

SECOND MALI SUD RURAL DEVELOPMENT PROJECT

September 13, 1983

Western Africa Projects DepartmentAgriculture C Division

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit = Malian franc (FM)US$1.00 FM 710FM 1,000 = US$1.41

WEIGHTS AND MEASURES

1 kilogram (kg) 2.20 pounds1 metric ton (t) 0.98 long tons1 hectare (ha) 2.47 acres1 kilometer (km) 0.62 miles

FISCAL YEAR

CIMDT: October 1 - September 30Government: January 1 - December 31

FOR OFFICIAL USE ONLY

ABBREVIATIONS

AV Association Villageoise(Pre-Cooperative Mutual Guarantee Village Group)

BADEA Banque Arabe pour le Développement Economique en AfriqueBCM Banque Centrale du MaliBDM Banque de Développement du MaliBNDA Banque Nationale pour le Developpement AgricoleCC Compagnie CotonnièreCCCE Caisse Centrale de Coopération Economique (France)CESAO Centre d'Etudes Sociales de l'Afrique de l'OuestCFDT Compagnie Francaise pour le Développement des Fibres Textiles

Compagnie Malienne pour le Développement des TextilesCOMATEX Compagnie Malienne des TextilesDGIS Directoraat Generaal voor Internationale Samenwerking

(Dutch Bilateral Aid)EDF (FED) European Development FundFAC Fonds d'Aide et de Coopération (France)HUICOMA Huilerie Cotonnière du MaliIER Institut d'Economie RuralIFAD International Fund for Agricultural DevelopmentIFDC International Fertilizer Development CenterIRAT Institut de Recherches Agronomiques Tropicales et des

Cultures VivrièresIRCT Institut de Recherches du Coton et des Textiles ExotiquesIRHO Institut de Recherches des Huiles et OléagineuxKIT Koninklijk Instituut voor de Tropen (Royal Netherlands

Institute for the Tropics)OACV Operation Arachide et Cultures VivrièresODIPAC Office du Développement Intégré de la Production Arachidière

et CéréalièreODR Opération de Développement RuralOSRP Office pour la Stabilisation et pour la Régularisation des PrixSB Secteur de BaseSCAER Société de Credit Agricole et d'Equipement RuralSEPAMA Société d'Exploitation des Produits Arachidiers du MaliSEPOM Société d'Exploitation des Produits Oleagineux du Mali

Société Malienne d'Etudes et de Construction de MatérielAgricole

STABEX EEC's Export Commodity Revenues Stabilization FundWAMU (UMOA) West African Monetary UnionZAER Zone d'Alphabétisation et d'Expansion RuraleZAF Zone d'Alphabétisation FonctionnelleZER Zone d'Expansion Rurale

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

MALI

SECOND MALI SUD RURAL DEVELOPMENT PROJECT

STAFF APPRAISAL REPORT

Table of Contents

Page No.

I. BACKGROUND ............................................... ... 1A. Project Background . ......................................... 1B. The Rural Sector . ........................................... 1

Agricultural Strategy in Mali ....... ...................... 3Constraints and IDA Strategy ....... ....................... 4

C. The Mali Sud Region . ......................................... 6Agricultural Development ......... ......................... 7The First Mali Sud Project ........ ........................ 10Prices and Taxation in the Mali Sud Zone ..... ............. Il

II. THE PROJECT .16A. Objectives and Summary Description .16B. Policy Reforms .............................................. 18

Cotton Imput and Output Pricing Policies .................. 18Institutional Reforms in Budgeting,Taxation and Marketing .................................. 21

External Financial Compensation Mechanisms .... ............ 23C. Project Investments ......................................... 28

Cotton and Coarse Grain Development ....................... 28Livestock Development ..................................... 29Rice Development .......................................... 31Confectionary Groundnuts .................................. 31Agricultural Inputs ....................................... 32Agricultural Credit ....................................... 33AV Development ............................................ 36Agricultural Extension .................................... 37Training .................................................. 37Applied Research .......................................... 38Cotton Tracks ............................................. 39Village Water Supply ...................................... 39Primary Health Care .40Miscellaneous Civil Works .40

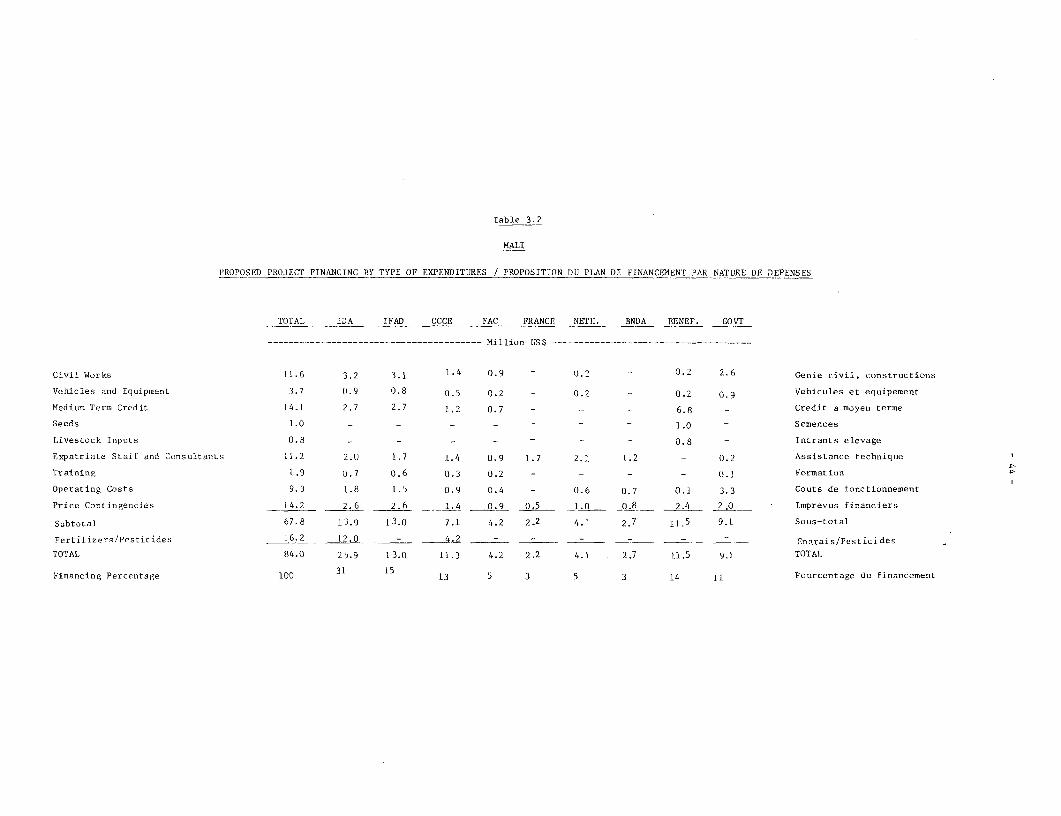

III. PROJECT COST AND FINANCING .. 41A. Cost Estimates .41B. Proposed Financing .41

This report is based on the findings of a Bank mission which visited Mali inSeptember/October 1981 comprising Messrs. J. Weijenberg, J.C. Fayd 'Herbe, Ms.N. Iwase, F. Reeb, and A. Rogerson (Bank), and J.F. Barres, L. Bourguet and J.van Dort (consultants); and two post-appraisal missions in April and September1982, comprising Messrs. J. Weijenberg and A. Rogerson (Bank).

- ii -

Table of Contents (Cont'd)

Page No.

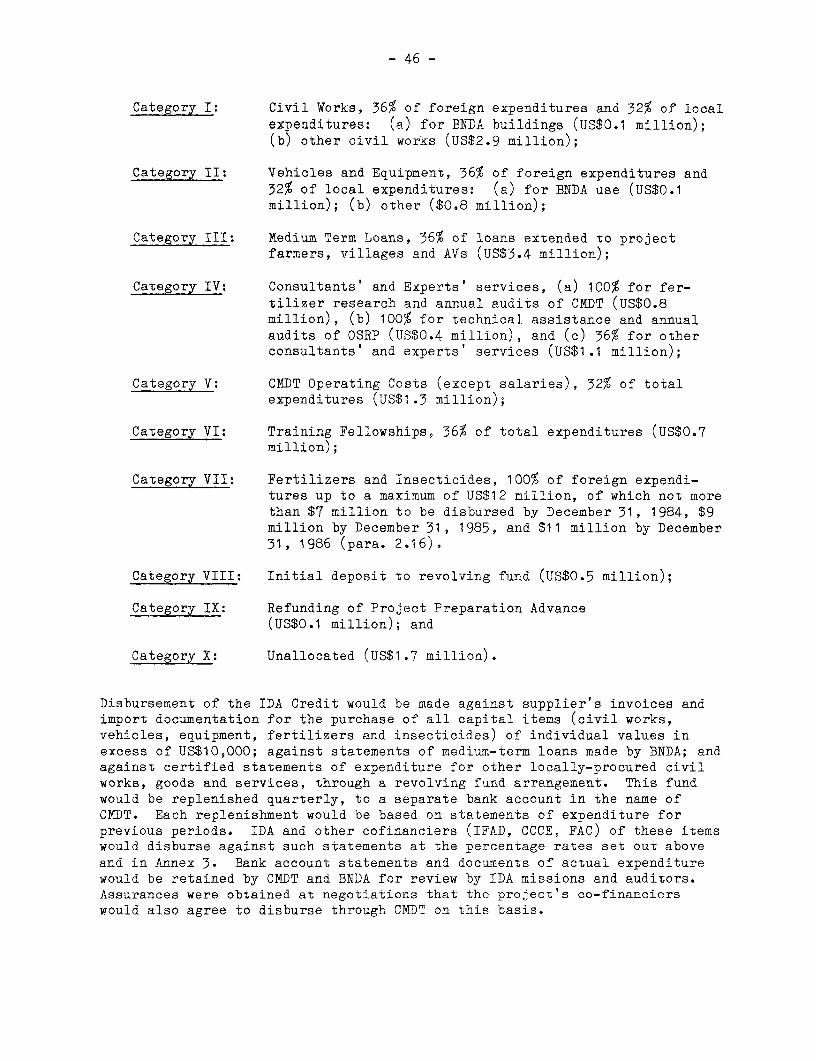

C. Procurement ................................................. 45D. Disbursements ........................... .................... 45E. Accounts and Audit ........ ................ 47

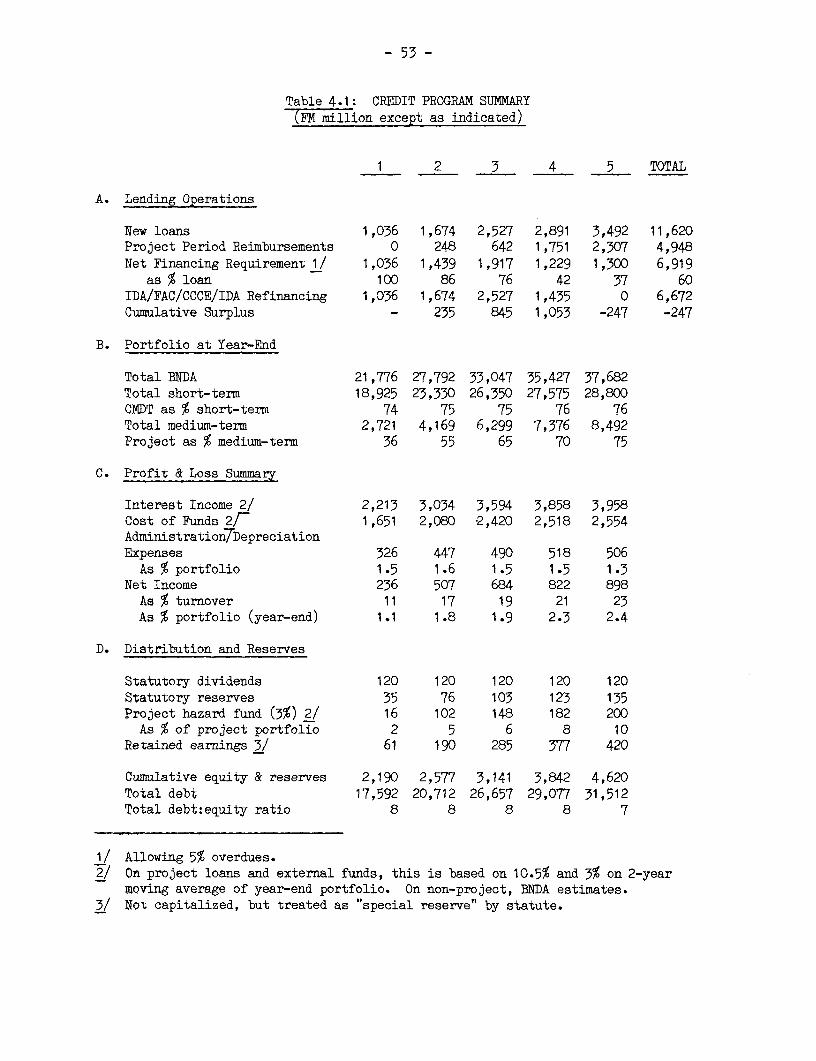

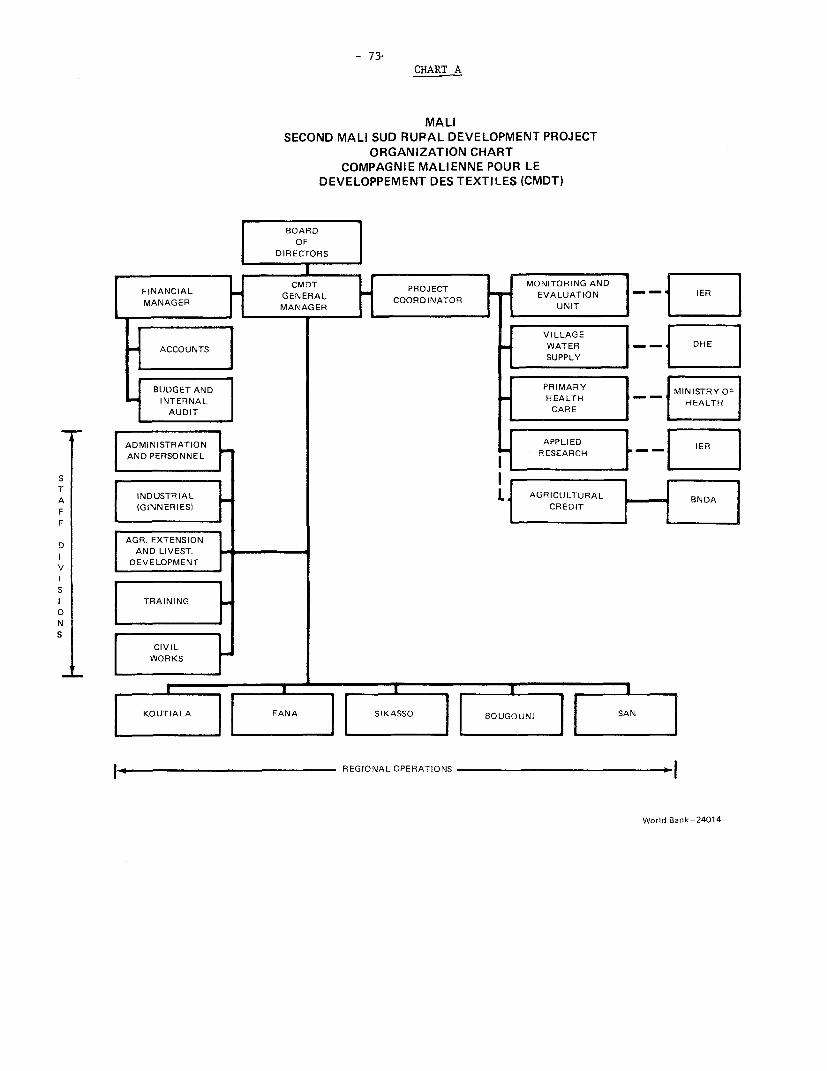

IV. PROJECT IMPLEMENTATION .......................................... 47A. Project Organization and Management (CMDT) ............... ... 47B. Agricultural Credit Services (BNDA) ..... .................... 49C. iolonitoring and Evaluation ................................... 54

V. MARKETS, PRICES, FINANCIAL ANALYSIS .. . 54A. Cereals Marketing......... 54B. Cotton Marketing.... 55C. Treasury Cash Flow .. 57D. Financial Risks ....... ..... .. 57E. Recurrent Costs and Cost Recovery . . 58F. Financial Implications for CMDT . . .58G. Farm Income and Returns per Capita (Farm Budgets) . .59

VI. JUSTIFICATION AND RISKS ... ............. ................ . 60A. Assumptions.... 60B. Results ...... 63C. Risks ..... . . .. 65

VII. AGREEMENTS REACHED WITH THE BORROWER,CONDITIONS AND RECOMMENDATIONS ................................... 66

Text Tables

1,1 Key Indicators Mali Sud Agricultural Development1971/2-1981/2.. 8

1.2 Mali Sud I Project Objectives and Results. 101.3 Comparison of Cotton Price Structure. 131.4 CMDT Financial Indicators .. 152.1 Pricing Program Summary .. 192.2 Summary of Programmatic Financing. 242.3 CMDT Debt Consolidation .. 242.4 Illustration of Cotton Account .. 262.5 Production Objectives .. 302.6 Input Requirements .. 343.1 Project Cost Suinmary .. 423.2 Proposed Project Financing by Type of Expenditure . .444.1 Credit Program Summary.. 535.1 CMDT Financial Indicators (Projected) 596.1 Key Parameters used in Economic Analysis . .626.2 Economic Analysis - Total Effects Case .. 64

- iii -

Annexes

1. Selected Documents and Data Available in the Project File

A. Staff Working PapersB. Sector/Project Reports

2. IDA Disbursements

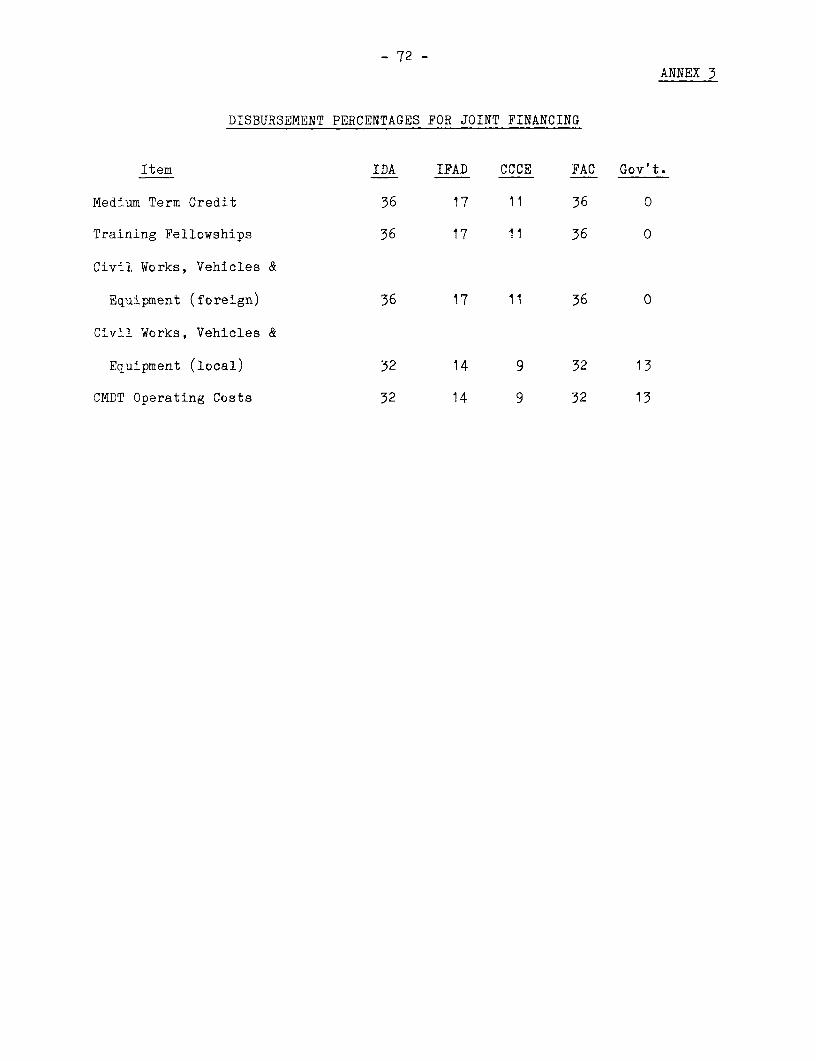

3. Disbursement Percentages by Category of Expenditure (Joint Financing)

Graphs, Charts and Maps

A. World Bank 24014 - CMDT Organisation Chart

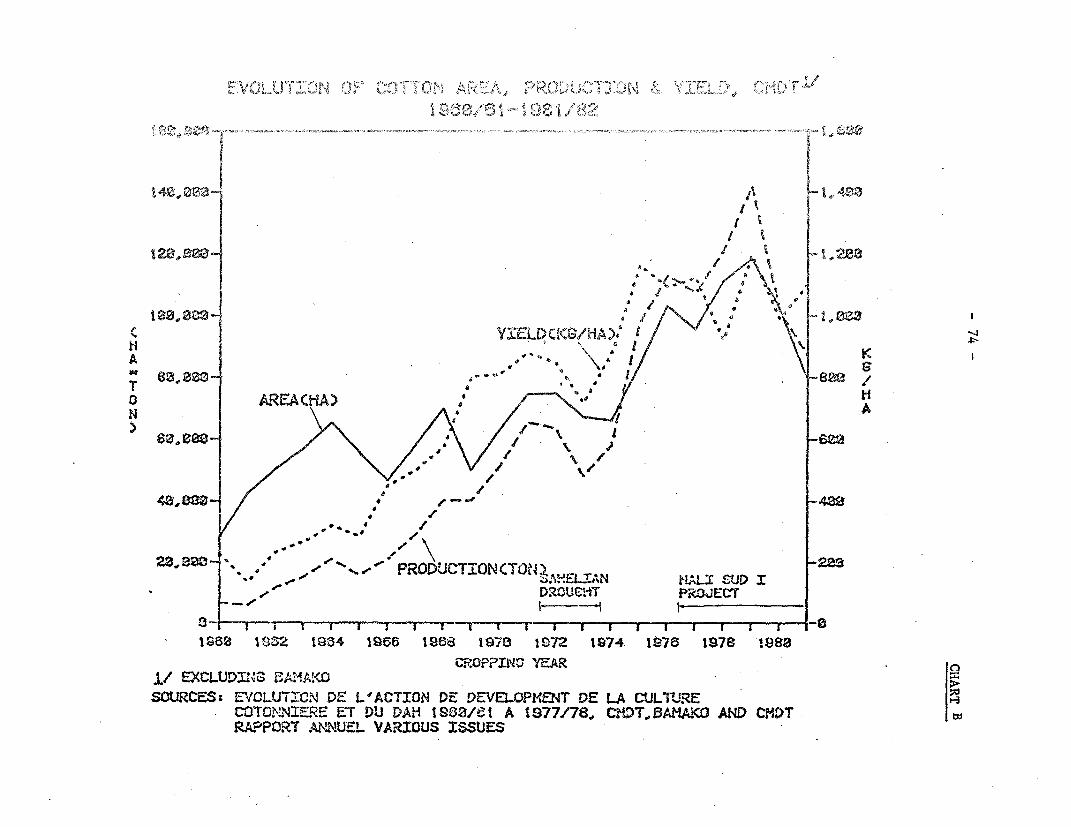

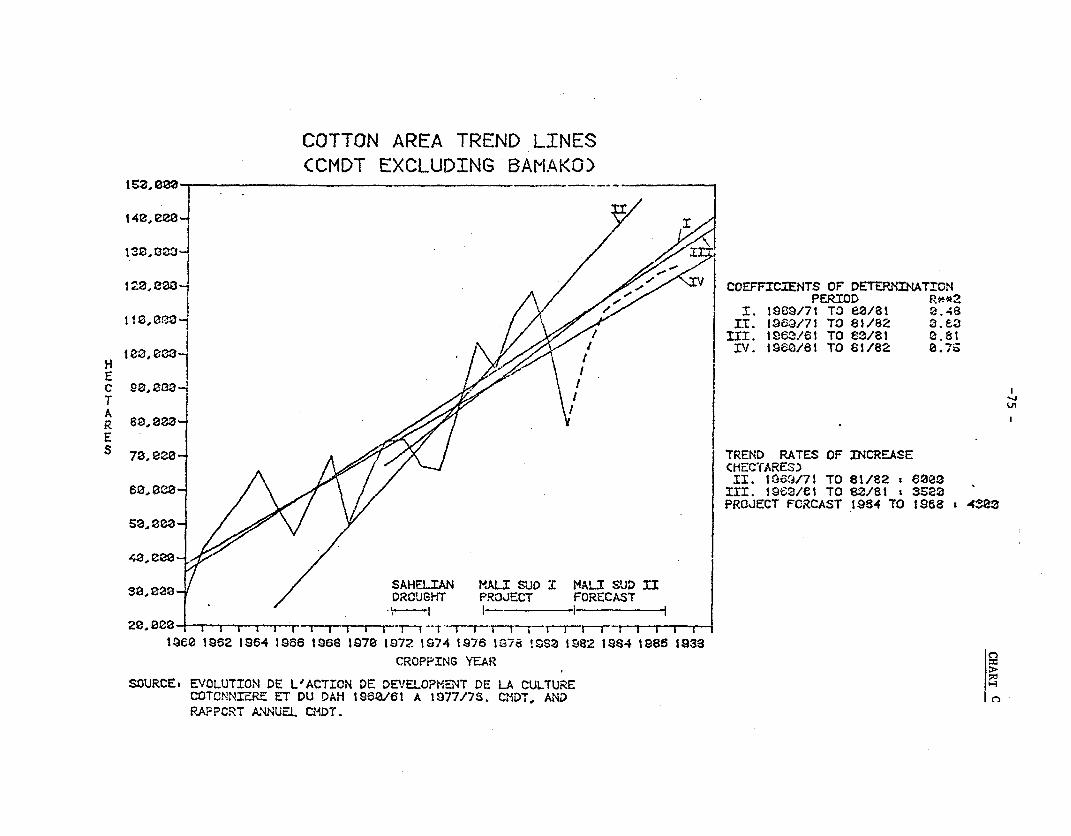

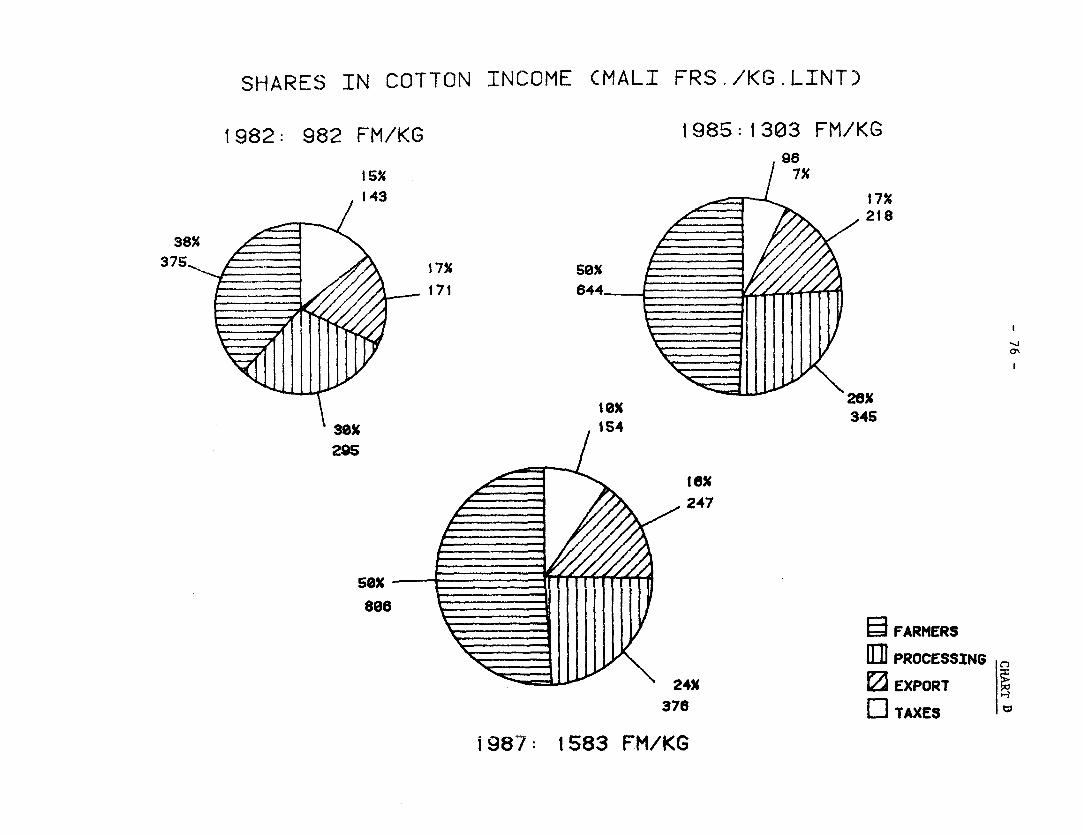

B. Evolution of Cotton Area, Production and Yields (graph)

C. Cotton Area Trend Lines (graph)

D. Shares of cotton income (pie charts)

E. IBRD 16520 - MAP

MALI

SECOND MALI SUD RURAL DEVELOPMENT PROJECT

I. BACKGROUND

A. Project Background

1.01 The project presented in this report is a follow-up to the Mali SudAgricultural Project (Cr. 669-MLI) appraised in November 1975 and for whichthe expected closing date is now December 31, 1983. The second project wasprepared by consultants in close collaboration with Compagnie Malienne pour leDeveloppement des Textiles (CMDT) and financed by Fonds d'Aide et de Coopera-tion (FAC). A post-evaluation of the first project prepared by the sameconsultants was published in January 1981. Based on its results a feasibilitystudy for the second project was available by June 1981, proposing a broad-based rural development project focussing on smallholder farmers. Anappraisal mission visited Mali in September-October 1981, followed by twopost-appraisal missions in April and September 1982. Both of the latterconcerned the design of the policy reform program of the project (ChapterII). Negotiations were held in Washington D. C. in June 1983. Whilst everyeffort has been made to take account of provisional data for 1982/83 in thisreport, most of the detailed analysis is based on the results of the agricul-tural years through 1981/82.

B. The Rural Sector

1.02 Resource Base. Less than a quarter of the country receives more than500 mm rainfall annually. However, Mali has the most favorable land endowmentof the six major Sahelian countries 1/: over a third of the total arableSahelian lands with over 800 mm rainfall, and nearly two-thirds of its irriga-tion potential. The population of 6.75 million, over 80% of which is rural,depends for its food supply on the wetter Sudano-Sahelian and Guinean zonesand the irrigated lands of the Niger delta (the northern limit of both areasbeing roughly the line between Kayes and Mopti). The vast Saharan zone of theNorth and East is almost uninhabited. Rural population density is extremelylow overall and varies directly with rainfall, except for some 200,000 ha oftraditional swamps and/or improved irrigation networks in the Segou and Moptiareas, and for parts of the South which have suffered from onchocerciasis.Long-term labor migration is an important feature of the West and North,whilst seasonal migration to the Ivory Coast is a constraint to agriculturalproduction in the South.

1/ Senegal, Mali, Niger, Mauritania, Upper Volta, Chad. Source: FAO1976. See map IBRD 16520.

1.03 Land tenure systems are still largely based on the traditional (ex-tended) family structure, with the family head deciding on priority choice ofcrops and allocation of labor and cash inputs to the main or "common" fieldsand other adults managing minor plots as time permits, often as a personalsource of revenue. Cultivation rights (usufruct) mainly accrue to those whofirst clear then continuously occupy new lands, hence ownership of animal andmachine-drawn farm implements is a major factor in land tenure. Modal "farm"size is around 4.6 ha cultivated, with other areas held fallow in the family'strust. In the Sudanian zone, several hundred holdings exceeding 20 hectaresand specialized e.g. fruit plantations bias the average rural income, which isprobably in the range $60-90 per capita, about two-thirds of rural incomes inlow-income Sub Saharan countries as a whole.

1.04 Technology and Livestock Resources. Tillage with animal traction ismore widespread in Mali than in any other Sahelian country. Farming methodsrange from quite sophisticated in the South (intensive fertilizer and pesti-cide applications in cotton/cereals rotation, 60% of farm units mechanized) toelementary hand tillage/subsistence agriculture in the marginal 300-600 mmbelt. There is significant rock phosphate production in the East, but allother inorganic fertilizers (15,000 t/annum nutrient equivalent) are imported,with the vast majority used in the Sudanian zone on cotton/cereals rotations.The country's huge livestock resources (migratory and semi-sedentarized in theDelta, sedentarized around Bamako and the South) constitute the major store ofwealth in rural areas. Mali mainly exports live animals for finishing andslaughter in coastal countries, although by-products suitable for intensivefeeding (e.g. cottonseed and cotton cake, groundnut cake) are relativelyplentiful.

1.05 Production and Consumption Patterns. Production and consumption dataare fragmentary and unreliable, which makes it difficult to draw firm conclu-sions based on historical patterns. Some two million ha are estimated to beunder cultivation of which 10% irrigated and 90% rainfed. In six recent post-drought (1976 to 1981) seasons, the two major cash crops, cotton and ground-nuts, accounted for between 80 and 120,000 hectares each, with groundnutsexperiencing a secular decline in favour of fooderops, and cotton acreage adramatie rise, peaking in 1979/80 (see below, para. 1.14). Existing varietiesof maize, improved and expanded rapidly over this period, now account for some50,000 hectares. Otherwise, apart from some pockets of rainfed rice, wheat(in the East), and tubers, the overwhelming share of the rainfed fooderop areais still sown to sorghum and millet. These account for perhaps 1.5 million haand little yield intensification or varietal improvements have so far provedpossible in the below 800 mm rainfall zone. Millet and sorghum yields are inthe 500-800 kg/ha range, giving total coarse grain production of about 1.0 to1.1 million metric tons. Overall foodgrain availability in normal rainfallyears appears to meet demand since about 1977, and is keeping pace withpopulation growth (2.6% p.a. approx.). However, Mali still imports rice toBamako at the margin whilst exporting unrecorded quantities of coarse grainsto neighboring countries and receiving substantial quantities of food aid(nearly 59,000 t in 1982). Production and yield trends in the cotton zone arediscussed below and the decline of the groundnut oil exports is extensivelydescribed in the President's report of the ODIPAC Technical Assistance Project(July 1981), particularly paras. 30 to 39 (Report P-2993-MLI).

-3-

Agricultural Strategy in Mali

1.06 The 1974-78 Plan and subsequent 1979-81 investment program gaveabsolute priority to food production investments designed to prevent a recur-rence of the shortages experienced in the 1972-73 droughts. Over 80% of Planexpenditure on foodcrops went to irrigated rice. This period also saw a majorexpansion of industrial processing capacity for cotton lint, cottonseed oil,and groundnut oil, largely based on the buoyant world commodity markets of themid 70s. Throughout the period, Government maintained a comprehensive (andpartially effective) system of quantity and price controls on trade in food-grains and other commodities, linked to the official wholesale and retailmonopoly functions of various State distributors 1/ and the legacy of cheapwage-goods policies of the early post-Independence era. Agricultural inputs,and particularly fertilizers, were subsidized until 1980/81 by as much as 45%of the cost price delivered to farmers. The 1970s also witnessed the creationand/or expansion of some 26 semiautonomous rural development agencies, "Opera-tions de Developpement Rural" (ODR), whose major sources of revenue weredetermined through commodity price and tax schedules known as "baremes". The"bareme" system became by the late 70s a major mechanism for resource alloca-tion in several subsectors, including cotton, and a key determinant ofnational monetary and fiscal policies.

1.07 Evaluation. With hindsight, each of these aspects of State inter-vention in the agricultural sector (investment planning, market regulation,institutional growth, pricing and rationing policies) has had major drawbacksin terms of sending counterproductive economic signals to producers and/orgenerating intolerable recurrent cost burdens for the State. Firstly, theinvestment bias towards irrigated rice involved the relative neglect of plen-tiful under-populated areas in the South with adequate rainfall for relativelysecure, intensive rainfed cereals cultivation at much lower investment costs,and subject to fewer management constraints. Secondly, the understandabledesire to promote local agro-based export industries entailed overconfidenceon the scope for genuine domestic value-added, given stagnating world markets,capital-intensive processes and high transport costs. The subsequent over-capacity and overstaffing has proved politically difficult to tackle eversince. Thirdly, most of the ODR were primarily conduits for providing exten-sion and social infrastructure services such as water supply, many of whichcould not be recovered directly from farmers. Behind the legal fiction offinancial autonomy, their rapid expansion and resulting accumulated losses(and/or net disinvestment through inadequate maintenance) have added to thepresent recurrent cost problems of consolidated government finances and exces-sive claims on the domestic credit market. Finally, the "bareme" process,originally intended to improve budgetary controls, has become a rigid, subjec-tive and administratively burdensome transfer price system, resulting inadditional downward pressure on producer incentives, poor cost control at allintermediary stages, and rationing and/or severe financial losses at finalpoints of sale.

1/ (OPAM, cereals; OACV, groundnuts; SOMIEX, oils, sugar).

- 4 -

1.08 New Policy Directions. The accumulated losses of major state enter-prises, particularly cereals distribution (OPAM), other consumer goods(SOMIEX), agricultural inputs (SCAER), and oil crushing (SEPOM, SEPAMA) ran upagainst increasing resistance from the fiscal and monetary authorities in thecontext of Government's growing awareness of the importance of marketforces. Major policy revisions in the scope of their operations and theextent of State subsidies were decided from late 1980. Many of these changeswere recommended in the context of IDA/Fund missions leading to the May 1982IMF Standby Agreement and some are being carried out with IDA-financed tech-nical assistance. In the agricultural sector, the major examples are: (a)the substantial 1981 liberalisation of domestic trade in coarse grains, and aparallel reduction in OPAM's responsibilities, (b) abolition of Governmentcontrol on groundnut marketing in early 1982, (c) large increases in theremaining administered producer prices for crops (e.g. rice, cotton) in1981/82, and dramatic increases - averaging 50% - for fertilizer and pesti-cides in the same year, (d) an in-depth review of the objectives, organizationand finances of the ODR, begun in April 1982 with IDA assistance, and (e) theliquidation of the OACV and SCAER monopolies.

Constraints and IDA Strategy

1.09 As the new policy directions started to work through the rural eco-nomy, three major constraints became apparent: First, the lack of an effec-tive floor price policy for coarse grains which would balance the need toreflect structural price differences through space and time with the modestfinancial and institutional resources available to carry it out. Second, theexclusion of paddy (in large official schemes) from the market liberalizationprogram, in an effort to safeguard low-priced supplies to urban target groupsand protect the turnover of State-owned rice mills. Third, a reluctance toincrease producer prices of the remaining administered crops (e.g. cotton) inline with border parities. At this critical juncture, Governnent s short-termneed to extract maximum financial surpluses from gross export revenues con-flicts with the need to optimize production of cotton by facing farmers withless distorted price signals at planting time. The first of these threeconstraints is being tackled through the Bank's continuing technical assis-tance involvement in cereals marketing reform, and the second through aproject for the rehabilitation of the Office du Niger irrigation network, nowunder preparation. The major objective of the policy reform program of thisproject is to address the third constraint so that the Government's reformprogram can be continued and reinforced in the area with the largest potentialfor rainfed agriculture in Mali, where the investment activities of theproject are also concentrated.

1.10 Previous Bank Group Involvement. Previous Bank group lending for therural sector has amounted to US$78.3 million in the form of ten IDA credits asfollows:

(i) two projects (and one Supplementary Credit) for engineering andconstruction or improvement of polders in the Mopti Area, financed byCredits 277-MLI (US$6.9 and amendment 2.6 million, 1971 and 1975),and 753-MLI (US$15.0 million, 1977);

- 5 -

(ii) a Drought Relief project, involving mainly small-scale irrigation andlivestock schemes, through Credit 443-MLI (US$2.5 million, 1973);

(iii) an integrated rural development project in the groundnut zone,(Credit 491-MLI, US$8.0 million, 1974);

(iv) two technical assistance projects, for the Office du Niger irrigationauthority (Credit 854-MLI, US$4.5 million, 1978), and ODIPAC, thegroundnut zone area development authority (Credit 1174-MLI, 1982,US$6.5 million);

(v) a livestock development, extension, health, and water supply projectthrough Credit 538-MLI (US$13.3 million, 1975);

(vi) a forestry project, designed to establish pilot industrial rainfedplantations, through Credit 883-MLI (US$4.5 million, 1979); and

(vii) the first Mali Sud Agricultural Project (Credit 669-MLI, US$15.5million, 1977), discussed in detail below (paras. 1.18 and 1.19).

In addition, IFC approved in April 1982, an investment of US$2.6 millionequivalent to finance a sheanut 1/ butter extraction plant aimed at the exportmarket and significantly dependent on supplies collected in the Mali Sud area.

1.11 Performance Evaluation. Project performance has been patchy, withwide variations in management effectiveness and more recently a deterioratingpublic finance and credit environment which increasingly affects implementation. Project Performance Audit Reports have been issued for four projects:Mopti Rice I (Credit 277-MLI); Drought Relief Project (Credit 443-MLI); Inte-grated Rural Development Project (Credit 491-MLI); and Office du Niger Tech-nical Assistance Project (Credit 854-MLI). The most relevant lessons learnedare those which juxtapose the two major rural development projects undertakento date, in the groundnut zone (Credit 491-MLI) and Mali Sud I (Cr. 669-MLI,to be completed by December 1981 and extended to June 30, 1983). The failureof the groundnut zone project completed in 1980, provides a striking contrastto the first Mali Sud project's considerable success under comparable startingconditions. The audit report cites the following pitfalls of the groundnutzone approach which have largely been avoided by Mali Sud: (i) heavy depen-dence on outside organizations for input supply logistics, industrial proces-sing capacity, and working capital finance, (ii) limited absorption of expa-triate technical assistance in the Malian project organization, (iii) poorfinancial information and control systems, (iv) insufficient attention tocereals technical packages acceptable to farmers, (v) slow policy reactionspeed in detecting, then adjusting to changed world market conditions.

1.12 Sector Lending Strategy and Project Pipeline. The broad objectivesof IDA rural sector lending to Mali are to:

1/ Karite, an oilbearing nut producing a cocoa-butter substitute.

- 6 -

(1) facilitate transfers of resources from consumption to productivesubsectors, through price incentives and institutional reform. Thiswill invoive targeted use of project and programmatic financing(para. 2.03);

(2) concentrate rainfed agriculture support investments in the areas withmaximum potential (Mali Sud and ODIPAC);

(3) in irrigation, give priority to consolidating existing systems beforecontemplating expansion through new investments;

(4) support the spontaneous development of private trade and informalproducer groups through training and improved price incentives, so asto increase participation in farmer support services (e.g. inputsupply) and reduce public recurrent cost burdens over time; and

(5) improve the financial controls and preserve the financial indepen-dence of key agribusinesses during a difficult transitional period inthe national economic environment.

In addition to the project presented below, the only agricultural project nowin the final stages of preparation involves the consolidation of existingirrigation polders in the Interior Delta area, and integrated livestockactivities based on the Delta's pastureland resources. The presently-proposedSecond Mali Sud project is the first project in Mali which combines program-matic financing for a major policy reform program with project financing ofmore traditional project components.

C. The Mali Sud Region

1.13 General. The Mali Sud Region, covering virtually all areas of thecountry south of the Niger River and west of Mopti, with 1.5 million inha-bitants, 1/ represents approximately one quarter of the country's totalpopulation. The 100,000 farm families in the area belong to the followingtribes: Bambaras and Bobos in the North, Senoufous and Miniankas in theSouth. The climate is characterized by a distinct rainy season (from May toOctober) with average annual rainfall increasing from 800 mm in the north to1,500 mm in the extreme south. Vegetation ranges from Sudano-Sahelian in thenortheast to Guinean in the extreme southwest. Temperatures vary between 26-and 31° C. Arable lands consist of light sandy loams and loamy sands, suit-able for rainfed cotton, coarse grains, cowpeas and groundnuts. Hydromorphicclays are found on a limited scale in bottomlands making them suitable forrice cultivation. An average family of 12, including 3 to 4 adult men, cul-tivates approximately 4.6 ha, of which 1.5 ha cotton and the remainder incoarse grains and cowpeas.

1/ Of which 1.2 to 1.3 million solely dependent on agriculture.

-7

Agricultural Development

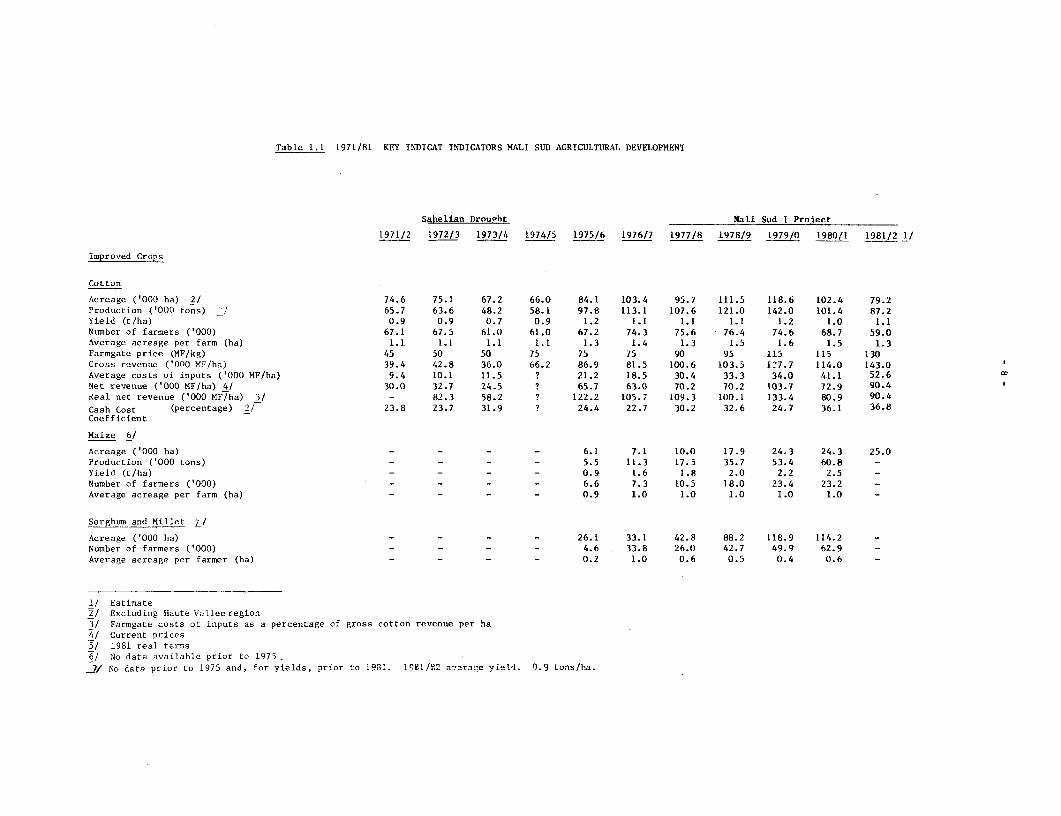

1.14 Cotton. Table 1.1 presents the development of cotton productionsince 1971-72 and improved cereals since 1975-76. A graphic presentation ofcotton production, area and yields is in graphs C and D. The area undercotton has grown steadily since the early 60s with a dip during the Saheliendrought period (1972-73). The maximum acreage planted was 119,000 ha in 1979-80. Over the last seven to eight years yields have stabilized at 1.1 tons/ha,and the average acreage per farm at 1.5 ha. The number of farmers growingcotton increased from 67,000 in 1971, to 75,000 in 1979, but has decreasedsharply over the last two years to levels comparable to 1971/72 (previous tothe major 1972/73 drought). Part of this decrease was due to low rainfall in1980 and a late start of the rains in 1981. The effect of this on yields hasbeen only marginal. At the same time, however, the partial removal of ferti-lizer subsidies without changing the farmgate price for seed cotton contri-buted to a 30% reduction of net revenue per ha in one year (1980). In thesubsequent year (1981) further removal of fertilizer subsidies was announcedto the farmers far before a 13% increase in farmgate price for seed cotton,leading to a further abandoning of cotton production by farmers. Even theaverage area grown per farm diminished and average compound fertilizer use perha fell between 1980 and 1981 by more than 15%. In one year, from 1979 to1980, the cash cost coefficient for the farmer (cash outlay/expected grossincome) increased by 45% from 24.7% to 36.1%, and his net revenue in 1981 realterms dropped to levels comparable to those attained during the Saheliandrought period in 1972. The consequences of this trend are analysed below(para. 1.23).

1.15 Rainfed Cereals. Since 1975, Compagnie Malienne pour le Developpe-ment des Textiles (CMDT), the agency responsible for agricultural extensionand cotton ginning in the project area, has promoted the growing of cereals(maize, sorghum, and millet) in rotation with cotton using the aftereffect ofcotton fertilization (in particular phosphates). There is evidence of strongcomplementarity between cotton and cereals, particularly maize, in Mali Sudfarming systems, which CMDT has deliberately and successfully exploited. Insix years (from 1975 through 1980), the area under improved cereals hasquadrupled, and maize production alone increased tenfold. 1/ Maize yields nowaverage over two tons per hectare on farms applying CMDT recommendations.

1.16 These remarkable developments (on both cotton and cereals) have beenmade possible through an efficient input distribution and extension system,building on a long process of human resource investment (absorption of moderncultivation practices) and farm capitalization (principally through rapidmechanization), and anchored on a lead cash crop with a well-developed tech-nology. Out of approximately 100,000 farms, 86% are reached by CMDT's exten-sion service. During the 1979 peak year of cotton production, 20,000 tons of

1/ Cereals grown by project farmers who apply CMDT recommendationsincluding selected seeds. Significant cereals plantings on both"traditional" and more modern techniques are not therefore reflected inCMDT statistics.

Table 1.1 1971/81 KEY INDICAT INDICATORS MALI SUD AGRICULTURAL DEVELOPMENT

Sahelian Droueht Mali Sud I Proiect

1971/2 1972/3 1973/4 1974/5 1975/6 1976/7 1977/8 1978/9 1979/0 1980/1 1981/2 1/

Improved Crops

Cotton

Acreage ('000 ha) 2/ 74.6 75.1 67.2 66.0 84.1 103.4 95.7 111.5 118.6 102.4 79.2Produiction ('000 tons) _/ 65.7 63.6 48.2 58.1 97.8 113.1 107.6 121.0 142.0 101.4 87.2Yield (t/ha) 0.9 0.9 0.7 0.9 1.2 1.1 1.1 1.1 1.2 1.0 1.1Number of farmers ('000) 67.1 67.5 61.0 61.0 67.2 74.3 75.6 76.4 74.6 68.7 59.0Average acreage per farm (ha) 1.1 1.1 1.1 1.1 1.3 1.4 1.3 1.5 1.6 1.5 1.3Farmgate price (MF/kg) 45 50 50 75 75 75 90 95 115 115 130Gross revenue ('000 MF/ha) 39.4 42.8 36.0 66.2 86.9 81.5 100.6 103.5 127.7 114.0 143.0Average costs of inputs ('000 MF/ha) 9.4 10.1 11.5 ? 21.2 18.5 30.4 33.3 34.0 41.1 52.6Net revenue ('000 MF/ha) 4/ 30.0 32.7 24.5 ? 65.7 63.0 70.2 70.2 103.7 72.9 90.4 1Real net revenue ('000 MF/ha) 5/ - 82.3 58.2 ? 122.2 105.7 109.3 100.1 133.4 80.9 90.4Cash Cost (percentage) 2/ 23.8 23.7 31.9 ? 24.4 22.7 30.2 32.6 24.7 36.1 36.8Coefficient

Maize 6/

Acreage ('000 ha) - - - - 6.1 7.1 10.0 17.9 24.3 24.3 25.0

Production ('000 tons) - - - - 5.5 11.3 17.5 35.7 53.4 60.8 -Yield (t/ha) - - - - 0.9 1.6 1.8 2.0 2.2 2.5 -

Number of farmers ('000) - - - - 6.6 7.3 10.5 18.0 23.4 23.2 -Average acreage per farm (ha) - - - - 0.9 1.0 1.0 1.0 1.0 1.0 -

Sorghum and Millet 7/

Acreage ('000 ha) - - - - 26.1 33.1 42.8 88.2 118.9 114.2 -Number of farmers ('000) - - - - 4.6 33.8 26.0 42.7 49.9 62.9 -Average acreage per farmer (ha) - - - - 0.2 1.0 0.6 0.5 0.4 0.6 -

1/ Estimate2/ Excluding Haute Valleeregion3/ Farmgate costs of inputs as a percentage of gross cotton revenue per ha4/ Current prices5/ 1981 real terms6/ No data available prior to 1975_7 No data prior to 1975 and, for yields, prior to 1981. 1U91/92 a-7crage yield. 0.9 tons/ha.

- 9 -

comnpound fertilizer (14-25-14), 3,500 tons of urea and 1,100,000 liters ofinsecticides were distributed to farmers. This represents over two-thirds oftotal fertilizer and chernical use in Mali. Thanks to aggressive promotion ofanrrial-powered tillage, there are now approximately 82,000 pairs of draft oxenin the area, 53,000 ploughs, 33,000 cultivators, 10,000 planters and 25,000TJLV sprayers. Agricultural credit has so far been provided mainly throughCMDT and the reimbursement rate has never been lower than 95% for short termloans and 92% for medium term credits.

1.17 Rice. Traditional rice cultivation is concentrated in the Sikassoregion which receives an average annual rainfall of approximately 1 ,200 mm,enough to grow a rice crop on bottomland clay soils if the rains are evenlydistributed. Since 1970, the actual area cultivated has diminished from20,000 ha to 16,000 ha in 1979 with yields varying between 0.9 tons/ha in goodyears and 0.5 tons/ha in years with uneven rainfall distribution. Since theSahelian drought in 1972 and 1973, a water management improvement and exten-sion program has started, mainly financed by European Development Fund(EDF). At present, three types of improved water management schemes are inoperation:

(i) terrace developments on approximately 200 ha bottomlands in valleysehere rice is traditionally grown by women;

(ii) anproximately 1,750 ha of small perimeters 1/ irrigated from reten-tion dams; and

(îii) a 1,000 ha full water control irrigation scheme at Klela.

_he malor obstacles at present are with the small perimeters and the KlelaScheme - in some cases design deficiencies, in others bad leveling, and ingeneral insufficient training of the extension service and farmers to operatethe systems. Improved terrace developments are generally giving better re-sults, whereby only landleveling is sometimes a bottleneck. Yields on small-scale terrace developments (1,5 tons/ha) are lower than on developments (ii)and (iii), but improvement costs are much lower for the public budget sincemost of the works are executed by the farmers themselves. New full-water-control schemes are unlikely to be socially profitable, but significantimprovements can be made to the operation of existing schemes.

IThe First Mali Sud Project

1,18 The objectives of the first preject were to expand cotton productionfrom 87,000 ha to 135,000 ha, kenaf production from 2,000 to 4,600 ha,improved maize production from 6,500 ha to 14,600 ha and improved rice produc-tion from 4,100 ha to 11,600 ha, by providing project farmers with extensionservices, seed multiplication facilities, seasonal and medium-term credit and

/ Kado (140 ha), Karagouan (118 ha), Samogossoni (182 ha), Longorola(55 ha), Touroumadie (100 ha), Bamadougou (50 ha), Siecu (Loulouni - 200ha), Sinkolo (200 ha), Neguela (200 ha), Vallee du Kobi (Panga - 500 ha).

- 10 -

applied research. The project undertook to extend processing facilities for

cotton, kenaf and rice, to expand the health program in the area, and te trainCMDT staff, farmers and blacksmiths.

1.19 The results in terms of overall production are in table 1.2. Thecalculated project ERR exceeds 30% despite the recent drop in cotton pro-duction because aggregate maize production exceeded appraisal estimates andthe recent stagnation of maize acreage, and reduction in cotton production, isconsidered a temporary phenomenon largely attributable to the price policyenvironment and poor rainfall, as explained in para. 2.06. The progression of

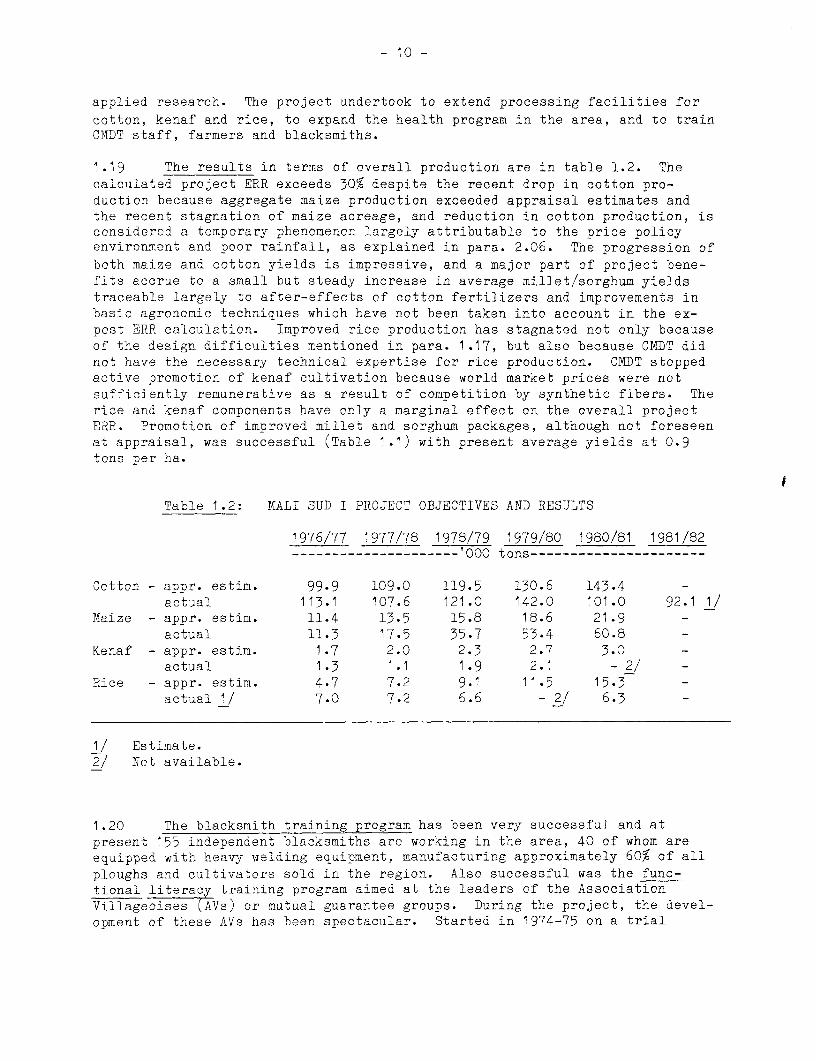

both maize and cotton yields is impressive, and a major part of project bene-fits accrue to a small but steady increase in average millet/sorghum yieldstraceable largely to after-effects of cctton fertilizers and improvements inbasic agronomic techniques which have nct been taken into account in the ex-post ERR calculation. Improved rice production has stagnated not only becauseof the design difficulties mentioned in para. 1.17, but also because CMDT didnot have the necessary technical expertise for rice production. CMDT stoppedactive promotion of kenaf cultivation because world market prices were notsufficiently remunerative as a result of competition by synthetic fibers. Therice and kenaf components have only a marginal effect on the overall projectERR. Promotion of improved millet and sorghum packages, although not foreseenat appraisal, was successful (Table 1.1) with present average yields at 0.9tons per ha.

Table 1.2: MALI SUD I PROJEOT OBJECTIVES AND RESULTS

1976/77 1977/78 1978/79 1979/80 1980/81 1981/82---------------------'000 tons----------------------

Cotton - appr. estim. 99.9 109.0 119.5 130.6 143.4 -actual 113.1 107.6 121.0 142.0 101.0 92.1 1/

Maize - appr. estim. 11.4 13.5 15.8 18.6 21.9 -actual 11.3 17.5 35.7 53.4 60.8 -

Kenaf - appr. estim. 1.7 2.0 2.3 2.7 3.0 -actual 1.3 1.1 1.9 2.1 - 2/ -

Rice - appr. estim. 4.7 7.2 9.1 11.5 15.3 -actual 1/ 7.0 7.2 6.6 - 2/ 6.3 -

1/ Estimate.2/ Net available.

1.20 The blacksmith training program has been very successful and atpresent 155 independent blacksmiths are working in the area, 40 of whom areequipped with heavy welding equipment, manufacturing approximately 60% of allploughs and cultivators sold in the region. Also successful was the func-tional literacy training program aimed at the leaders of the AssociationVillageoises (AVs) or mutual guarantee groups. During the project, the devel-opment of these AVs has been spectacular. Started in 1974-75 on a trial

- il -

basis, CMDT has promoted the creation of some 400 AVs that have graduallytaken over the collection and weighing of the cotton crop. CMDT remuneratesthe AVs for this work, and the annual average AV cotton revenue is presentlyMF 325 thousand (US$500). Many AVs also generate funds from grouped cerealssales, and levies on their members. With the income generated, the AVsfinance both economic and social investments (such as well improvements,storage facilities, village pharmacies). AV income is seldom distributed tothe participants in cash.

1.21 CMDT distributes inputs to individual farmers and AVs at the time ofcotton marketing, which means that fertilizers are available in the villagesbetween 3 to 6 months prior to the start of the agricultural season. Up tonow, credit to individual farmers has also been made available through CMDTfor both agricultural equipment and inputs. An important feature of thefinancial relationship between CMDT and farmers (individual and AV) is thatcotton marketing transactions are settled promptly and in full for cash, andinput credit (whether used on cotton or cereals) is recovered in cash later,i.e. there is no withholding at source. This creates greater confidence butmakes the risk factor for each crop more transparent to farmers. CMDT doesnot now charge interest on seasonal credit, which constitutes up to half ofthe input subsidy passed on to farmers (see proposals, para. 2.33).

1.22 The Health Component, financed by BADEA, reached a population ofabout 880,000. The component consisted of training health workers and tradi-tional midwives and providing them with means of transport. Because of ini-tial financing delays the program did not get off the ground until 1979, thusresults at the time of appraisal of this follow-up project remained belowtargets (50%). This component is executed in part of the project area(Sikasso and Segou regions) since the rest is covered by other projects. Itreaches approximately 1,100 villages, and is executed by Ministry of Healthdoctors working in the area. CMDIT only plays a role in providing finance andcoordinating these activities with AV development.

Prices and Taxation in the Mali Sud Zone

1.23 The major economic agents in the cotton subsector are: farmers, whobuy inputs and sell cotton at Government-set prices; CMDT who provides inputsand extension, and gins the seed cotton; SOMIEX, who has a monopoly on lintexports; the Treasury, who collects taxes from both CMDT and SOMIEX; and OSRP,who is supposed to compensate CMDT for shortfalls between the official ex-millprice and actual costs. Export revenues from cotton in Mali support theentire range of CMDT development activities as well as a substantial net cashflow to the Treasury and SOMIEX averaging over $10 million annually during1976-81. 1/ Given the high fixed costs of processing and transport, thesector's net surplus is extremely sensitive to world cotton price fluctuationsand to the size of the cotton harvest. Yields are relatively insensitive torainfall variations in the Sudanian zone, so the major variable is acreage

1/ Only some 10% of Central Government tax revenues, but by far thelargest sectoral source.

- 12 -

sown to cotton. This acreage is a function of the timing of rainfall and ofthe relative price of cotton, and cotton inputs, gi ven alternative opportuni-ties for using scarce family labor. The Goverument directly controls cottonoutput and input prices, but not cereals prices. Moreover, it had becomeaccustomed to the net cash flow of the Mali Sud zone as a source of budgetsupport for the State import-export monopoly, SOMIEX. It has therefore tendedto put pressure on either CMDT finances, or farmer incentives, or both, whenworld prices or the volume of production have weakened from time to time. In1982, producer prices for cotton were about 62% cf export parity equivalents,and 69% after reincorporating the effects of input subsidies affectingcotton. At the same time, effective market prices for cereals are close to100% of their border parities, reflecting the fact that Government is unable(and unwilling) te hold producer prices below their equilibrium levels, whichare also affected by export demand. Taxation is therefore being excessivelyconcentrated on a single crop which is subject to large shifts in acreage.However, Government has made considerable efforts recently to reduce theincidence of identifiable taxes on cotton: in particular, the ad valoremexport tax, was eliminated in 1981.

1.24 This chronic squeeze became critical with exceptionally bad rainfallin 1980 and 1981 (para. 1.14). As cotton volume fell and unit costs rose, sothe perceived room for increases in "bareme" cotton prices to producers, orfor maintenance of input subsidies, dwindled. All prices were then frozen forthe 1982-83 season. The medium-term option of increasing activity through afavorable shift in producer terms of trade is constrained by the need togenerate minimum levels of Treasury revenue through taxes on the sector's netprofit. If further cost increases are passed on to producers without com-pensation, their financial exposure will increase and the downward spiralcould accelerate.

1.25 Cost Structure. This vicîous circle is illustrated in table 1.3which compares the cotton cost structure in 1976-77 (the beginning of Mali Sud1, with favorable world market and climatic conditions)g 1979-80 (recordproduction year, off-peak world prices), and 1981-82 (with low output andconstant real price levels). During the Mali Sud I project period prior toappraisal of the followup project (1977 to 1981), world market pricesincreased by only 32% in nominal terms. Official input prices to producersincreased by 280%, much faster than seed cotton prices (75%) which werebroadly in line with changes in the general price index (67%). Over the sameperiod, the industry's raw materials costs increased from 26 to 40% of grossexport earnings, SOMIEX export costs increased frora 15 to 17% and CMDTprocessing and handling costs, from 21 to 29%. This reflects high overheadsand increasingly low (60% in 1981-82, over 90% in 1979-80) plant utilization,as well as increases in costs due to noncotton activities (e.g. cerealsextension) but recovered, in part from cotton revenues. The cotton sector asa whole remains - just - financially viable even under these conditions, butthe profits availàble for distribution have fallen from 22% of turnover to9%. The entire Mali Sud operation could therefore become unprofitable with afurther marginal fall in output or deterioration in terms of trade, a parti-cularly serious risk for Mali since cotton accounts for over half of the total

- 13 -

Table 1.3: COMPARISON OF COTTON PRICE STRUCTURE(Lint equivalent terms)

Actual - 1976/77 Actual - 1979/80 Est. - 1981/82

CMDT Production: 41,000 tons 53,400 tons 34,000 tons

FM/kg % FM/kg % FM/kg %

c.i.f. price (a) 755.2 100 738.5 100 930.0 100

Producer price (b) 193.5 26 296.7 40 339.6 37

Input subsidies (c) n.a. 1/ n.a. 36.8 4

CMDT (processing) (d) 2/ 156.3 21 180.2 24 267.1 29

SOMIEX (transport) (e) 112.0 15 161.7 22 161.3 17

Output taxes (f) 3/ 125.9 17 66.8 9 41.2 4

Subtotal: cif cost (g)

(b to f) 587.7 78 705.4 95 846.0 91

Gross margin (a-g) 167.5 22 33.1 5 84.0 9

Distribution:

CMDT retained earnings (h) 30.7 4 5.1 1 -15.9 4/ -2

SOMIEX surplus (i) 136.9 18 28.0 4 99.9 5/ 8

Total "Govt" (f + i) 262.8 35 94.8 13 141.1 16

(FM billion) (10.8) (5.1) (4.8)

1/ Absorbed by SCAER until 1980.2/ Excluding depreciation of ginneries.3/ Including T.O.P. (FM 15.0/kg) now refunded to CMDT.4/ Difference between actual costs before depreciation and bareme income,

including 5% commission.5/ Difference between (transfer price to CMDT plus actual SOMIEX costs), and

actual c.i.f. price.

- 14 -

value of merchandise exports. The alternative of a drastic reduction incapacity (e.g. mothballing several ginneries) is not justified in view of thebuoyant long-term prospects for Malian cotton (Chapter V) and the risks of asevere processing bottleneck as and when a recovery occurs.

1.26 Distribution of Cotton Revenues. This increasing pressure on pro-ducer incentives could have been alleviated were it not for the growing burdenof taxes and cross-subsidies charged to the "bareme", to benefit various Stateinstitutions or to finance CMDT's non-cotton developmental activities forwhich full cost recovery is not practical (e.g. functional literacy). Many ofthese charges are not identified as taxes in the "bareme" but have the sameeffect, i.e. of reducing the apparent breakeven cost of raw materials andhence likely producer price for seed cotton. The major sources of consoli-dated Government revenue are (a) output taxes levied under the "bareme" onSOMIEX and CMDT (about FM 1.4 billion (see Table 1.3>), (b) accelerated amor-tization of Mali Sud 1 debt service (FM 0.4 billion), (c) import taxes oncotton inputs and taxes on seasonal interest (both borne by CMDT, over FM 0.7billion). A much more important, but less easily predicted source is the netsurplus retained by SOMIEX, the monopoly export agency. This is based on thedifference between (a) the artificial ex-mill price owed to CMDT under the"bareme" plus the real costs of export to Europe borne by SOMIEX, and (b) thegross c.i.f. revenues actually realized by SOMIEX. This "spread" should beabout 100 FM/kg in 1982, or some FM 3.4 billion, bringing consolidated Govern-ment net cash flow from a below-average year to some FM 5.9 billion (US$8.3million). SOMIEX's net cotton revenues were until recently available to coverpart of its losses on consumer goods distribution: now they are partly (atleast 50%) appropriated by the Treasury upon receipt as part of SOMIEX'soverall tax liabilities, leaving SOMIEX with substantial uncovered losses onits non-cotton operations.

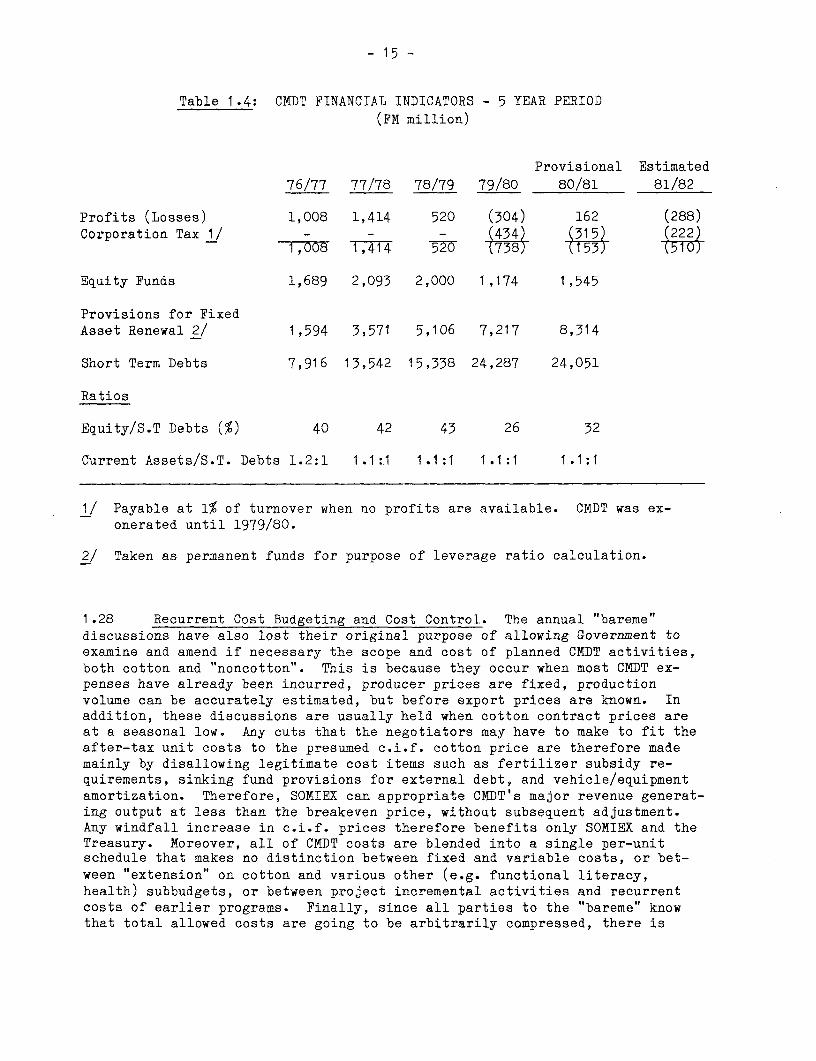

1.27 CMDT Finances. CMDT is damaged by the present financing and market-ing arrangements in two major ways. First, the injection of SOMIEX as inter-mediate buyer delays payments, increases interest charges and constantlythreatens CMDT liquidity. Second, the reduction/rejection of genuine CMDTcost items (such as input subsidies and depreciation) in the "bareme" negoti-ating process threatens CMDT solvency. This in turn prompts the bankingsystem to delay or reject CMDT's overdraft requests, creating occasional cashcrises, and eventually undermining CMDT's reputation as a reliable buyer fromfarmers. In 1981, one such crisis was resolved by Government after interven-tion by IDA. However, the financing gap resulting from underpricing of cottonto SOMIEX was transferred to farmers through one-time input price increasesaveraging over 50%, with the disincentive results described above. In 1982,total Government/SOMIEX withholdings will probably exceed the consolidatedprofits of the cotton sector. CMDT has therefore made a cash loss on cottonoperations of about FM 300 million in 1982, and will also defer part of itsrequired depreciation provisions and tax liabilities. This deterioratingtrend is analyzed in table 1.4 below. Detailed balance sheets for the past5 years (1977-81) are in the Project File, item A.9. CMDT's financialprojections are discussed in Chapter 5 below.

- 15 -

Table 1.4: CMDT FINANCIAL INDICATORS - 5 YEAR PERIOD(FM million)

Provisional Estimated

76/77 77/78 78/79 79/80 80/81 81/82

Profits (Losses) 1,008 1,414 520 (304) 162 (288)Corporation Tax l/ - - - (434) (315) (22

-,oo8 1,414 520 (738) (153)

Equity Funds 1,689 2,093 2,000 1,174 1,545

Provisions for FixedAsset Renewal 2/ 1,594 3,571 5,106 7,217 8,314

Short Term Debts 7,916 13,542 15,338 24,287 24,051

Ratios

Equity/S.T Debts (%) 40 42 43 26 32

Current Assets/S.T. Debts 1.2:1 1.1:1 1.1:1 1.1:1 1.1:1

l/ Payable at 1% of turnover when no profits are available. CMDT was ex-onerated until 1979/80.

2/ Taken as permanent funds for purpose of leverage ratio calculation.

1.28 Recurrent Cost Budgeting and Cost Control. The annual "bareme"discussions have also lost their original purpose of allowing Government toexamine and amend if necessary the scope and cost of planned CMDT activities,both cotton and "noncotton". This is because they occur when most CMDT ex-penses have already been incurred, producer prices are fixed, productionvolume can be accurately estimated, but before export prices are known. Inaddition, these discussions are usually held when cotton contract prices areat a seasonal low. Any cuts that the negotiators may have to make to fit theafter-tax unit costs to the presumed c.i.f. cotton price are therefore mademainly by disallowing legitimate cost items such as fertilizer subsidy re-quirements, sinking fund provisions for external debt, and vehicle/equipmentamortization. Therefore, SOMIEX can appropriate CMDT's major revenue generat-ing output at less than the breakeven price, without subsequent adjustment.Any windfall increase in c.i.f. prices therefore benefits only SOMIEX and theTreasury. Moreover, all of CMDT costs are blended into a single per-unitschedule that makes no distinction between fixed and variable costs, or bet-ween "extension" on cotton and various other (e.g. functional literacy,health) subbudgets, or between project incremental activities and recurrentcosts of earlier programs. Finally, since all parties to the "bareme" knowthat total allowed costs are going to be arbitrarily compressed, there is

- 16 -

every incentive to manipulate the presentation of each line item. Conversely,there îs no incentive to control costs until the apparent surplus has shrunkto zero. Farmers are not directly represented in the process, but suffer itsconsequences when the "scope" for price increases is reviewed a few monthslater, as was the case in 1981.

1.29 Stabilization Fund. Throughout the late 1970s, a substantial part ofexplicit cotton taxes on CMDT and SOMIEX were earmarked for general (multicom-modity) stabilization funds managed by the Office pour la Stabilisation et laRegularisation des Prix (OSRP). This agency, principally funded by levies onimports cf petroleum products, intervenes principally to subsidize consumerprices of e.g. rice and coarse grains by giving rebates to various ODR. Cot-ton has traditionally been a net provider of funds to other crops via OSRP.More recently, CMDT has been allowed to retain the portion of the "bareme"transfer price due to OSRP and net it out against part of the yearend short-falI of the "bareme" measured against true costs. However, OSRP itself hasnot managed to accumulate any net reserves, at a time when cotton is unlikelyto continue to generate substantial surpluses and virtually every other sub-sector, particularly oilseeds, has become a net claimant for OSRP support.The EEG's commodity export revenues stabilization fund, Stabex, reacts toshortfalls in nominal, gross revenues against a four-year moving average andis not designed to cover the net effects of deteriorating terms of trade. NoStabex transfers have yet occured for Malian cotton, and even the 1981-82 cropyear is expected to yield little in 1983.

1.30 Conclusiaon. Under the present system, there is therefore no adequateworking capital buffer to meet temporary drops in export earnings and/orincreases in unit costs. Moreover, the option of increasing real producerprices to stimulate production is constrained by the need to continue generat-ing surpluses which can yield tax revenue for the Treasury. The latter hasalready sacrificed important sources of indirect taxes levied under thebareme, and cannot readily generate additional savings to be passed on toproducers. In addition, it has to compete with SOMIEX's substantial claims oncotton surpluses which help reduce SOMIEX losses on other activities. Themajor thurst of the policy reform program described below is to help Mali overa transitional period to higher producer revenues, higher capacity utilizationand an expanded revenue base, while changing pricing and marketing arrange-ments so as to minimize the risks of excessive transfers from productiveactivities to consumption, and focus taxation on actual (verifiable) tradingsurpluses.

II. THE PROJECT

A. Objectives and Summary Description

2.01 The broad objectives of the proposed project are in accord withGovernment's policies of increasing agricultural production and farm incomesto improve the welfare and standard of living of the rural population. Themain specific objectives are:

- 17 -

(i) to stabilize and increase cotton production through an input andoutput pricing program which is consistent with world market oppor-tunities, and would achieve comparable levels of Government revenuein the medium and long term at lower tax rates, higher volumes andlower average processing costs;

(ii) to reorganize institutional arrangements for budgeting, taxation,marketing and cost recovery for cotton and related activities, in-cluding a new mechanism to protect the system from temporary priceand volume fluctuation;

(iii) to increase production of cotton, of coarse grains (maize, sorghum,millet), cowpeas, rice, and livestock, all of which depend directlyor indirectly on a healthy cotton sector, through specific inputdelivery and extension programs;

(iv) to secure future improvements of agricultural production throughapplied research;

(v) to promote independent farmer organizations (AVs) through incentivesto absorb various tasks now undertaken by Government and CMDT, andtraining; and

(vi) to meet basic needs of farmers in the area through village watersupply and primary health services whose basic operation and main-tenance will be the responsibility of farmer organizations.

2.02 In particular, the project to be implemented over five years,wouldinclude:

(a) expanding cotton production on about 16,000 ha; improving farmingpractices and input use on about 31,000 ha of maize; 35,000 ha ofmillet and sorghum, and 18,000 ha of cowpeas;

(b) partially rehabilitating and improving irrigated rice production onabout 1,750 ha of small perimeters and 1,000 in the Klela Scheme;constructing terraces and improving production on about 1,500 ha ofrainfed rice; preparing a feasibility study for an additional 1,700ha along the Klela River; and strengthening CMDT's capacity in thedesign, operation and maintenance of small irrigation schemes;

(c) supplying on medium-term credit through BNDA about 7,500 draft oxen,13,000 ploughs, 10,000 seed drills, 7,000 cultivators, 2,200 ULVsprayers, and 160 low-horsepower tractors;

(d) strengthening the BNDA network of branch offices to provide medium-term credit services in the project area;

(e) replacing imported phosphate fertilizer by about 15,000 tons oflocally produced rock phosphate;

- 18 -

(f) delivering drugs and feed supplements and improving animal husbandrypractices for beef cattle and work oxen; and installation of a smallmineral lick manufacturing unit;

(g) improving and extending agricultural research through four appliedresearch programs on cotton and coarse grains, farming systems, tech-nology transfer to small farmers, and fertilizer usage;

(h) strengthening CMDT's capacity for rehabilitation and maintenance ofabout 3,000 km of feeder roads and construction of 30 km additionaltracks;

(i) promoting 600 additional AVs and transfering all primary marketing ofcotton and credit recovery functions to the AVs;

(j) functional literacy training for AV members and training of AVleaders, blacksmiths and CMDT staff;

(k) drilling of 400 wells for village water supply and 50 wells forpastoral use, equipped with manually operated pumps; and

(1) continuing the primary health care program and training of villagelevel health workers.

2.03 The project will be complemented by a policy reform program linked toprogrammatic financing channelled through imports of fertilizers and pesti-cides, for a total value of FM 11,500 million (US$16.2 million). Most of thiswould indirectly compensate for the expected initial net cotton sector revenueshortfall due ta producer price increases and other reductions in Governmentcash flow due to its obligations under the program. Other amounts wouldremain with CMDT to settle its net claims on Governnent arising out of pastunderfinancing through the bareme system, and the balance would provide theinitial capitalization of a Cotton Guarantee Fund. This program would supporta series of institutional and price policy reforms. Disbursement of thisexternal assistance would be through annual tranches released followingachievement of specific pricing and subsidy goals.

B. Policy Reforms

1. Cotton Input and Output Pricing Policies

2.04 Cotton output and input prices will continue to be linked to worldmarket conditions, but Government's tax revenue constraints in the sector willbe temporarily lifted so as te break the vicious circle described in paras.1.23 to 1.30 above. The official producer price for cotton will be increasedrapidly in real terms whilst input subsidies are progressively removed. Thefollowing table illustrates the major changes involved:

- 19 -

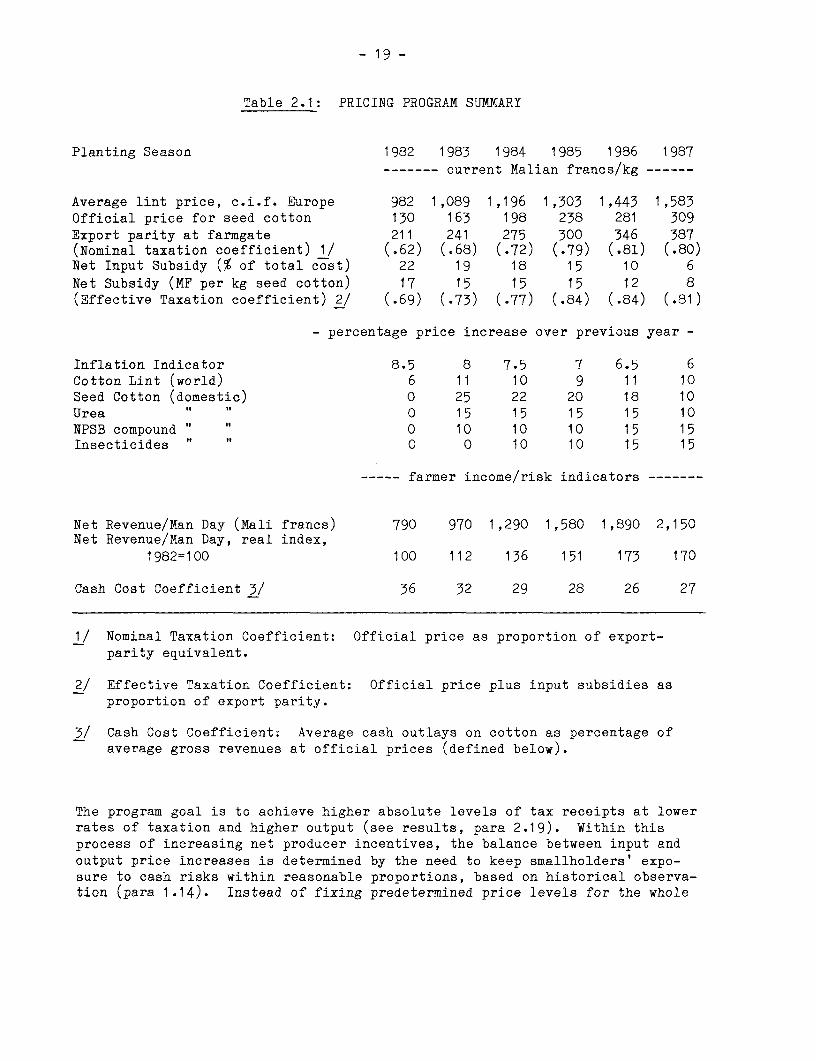

Table 2.1: PRICING PROGRAM SUMMARY

Planting Season 1982 1983 1984 1985 1986 1987- current Malian francs/kg ------

Average lint price, c.i.f. Europe 982 1,089 1,196 1,303 1,443 1,583Official price for seed cotton 130 163 198 238 281 309Export parity at farmgate 211 241 275 300 346 387(Nominal taxation coefficient) 1/ (.62) (.68) (.72) (.79) (.81) (.80)Net Input Subsidy (% of total cost) 22 19 18 15 10 6Net Subsidy (MF per kg seed cotton) 17 15 15 15 12 8(Effective Taxation coefficient) 2/ (.69) (.73) (.77) (.84) (.84) (.81)

- percentage price increase over previous year -

Inflation Indicator 8.5 8 7.5 7 6.5 6Cotton Lint (world) 6 il 10 9 il 10Seed Cotton (domestic) O 25 22 20 18 10Urea O 15 15 15 15 10NPSB compound " " O 10 10 10 15 15Insecticides I" O O 10 10 15 15

----- farmer income/risk indicators -

Net Revenue/Man Day (Mali francs) 790 970 1,290 1,580 1,890 2,150Net Revenue/Man Day, real index,

1982=100 100 112 136 151 173 170

Cash Cost Coefficient 3/ 36 32 29 28 26 27

1/ Nominal Taxation Coefficient: Official price as proportion of export-parity equivalent.

2/ Effective Taxation Coefficient: Official price plus input subsidies asproportion of export parity.

3/ Cash Cost Coefficient: Average cash outlays on cotton as percentage ofaverage gross revenues at official prices (defined below).

The program goal is to achieve higher absolute levels of tax receipts at lowerrates of taxation and higher output (see results, para 2.19). Within thisprocess of increasing net producer incentives, the balance between input andoutput price increases is determined by the need to keep smallholders' expo-sure to cash risks within reasonable proportions, based on historical observa-tion (para 1.14). Instead of fixing predetermined price levels for the whole

- 20 -

project period, which would not allow Government enough flexibility to adjust

to changed costs and/or technology, Government has agreed to achieve and main-tain a maximnlm cash cost coefficient of 30%. This is defined as total ferti-lizer and pesticide costs per hectare of cotton, at the average applicationrate, as a percentage of gross revenues per hectare of cotton at the averageyield level, This indicator is designed for ease of calculation and verifica-tion, but does not pretend to capture all the elements relevant to farmers'decision to grow cotton. Moreover, so that this improvement in farmer incen-tives îs not achieved through an increase in subsidies, Government would alsorespect a maximum subsidy, calculated on the full delivered cost includinghandling charges and taxes, of 25% in 1984, 18% in 1986 and 10% in 1987. 1/Subsidies would be fully eliminated by 1988, the year of project completion.Respect of these conditions (through official prices declared, as they usuallyare ncw, by the end of April of each year) would be a condition of disburse-ment of each annual tranche of programmatic financing. The specific per-centage increases in Table 2.1 are illustrations of pricing policies con-sistent with these rules Other combinations are possible: for example,Government has chosen to increase the producer price by 15% in June 1983, butto hcld official input prices at their present levels since import costs havefallen. This satisfies the cash cost coefficient target but implies a sharpeirincrease in input costs in 1984 to meet the subsidy target in later years.These pricing arrangements will be subject ta a joint review by IDA andGovernment no later than April 30, 1984 and annually by April 30 of eachsucceeding year, at which time the risk indicator and subsidy targets may beadjusted by mutual agreement.

2.05 The balance of priorities within the overall subsidy bill is notpredetermined. However, it is agreed that subsidies would be decreased lessrapidly on insecticides, which have a marked impact on cotton yields and haveno alternative use on cereals, Also, subsidies on imported phosphates will bedecreased faster as applications of domestic rock phosphates progress. Inaddition, Government will introduce and maintain a differential of at least15% between cash and credit sales prices for seasonal inputs (para. 2.33).This shauld help reduce handling costs for CMDT. Official prices for inputsare already close to the c.i.f. costs on imported fertilizers, but CMDT bearsadditional financial charges which account for the bulk of the subsidy.

2.06 The intention of the pricing program is to accelerate an improvementin producer terms of trade, within the limits of world market prices forinputs and for cotton lint. The review process would therefore be designed soas to avoid the risk of a protracted net subsidy to cotton, e.g. in the ex-treme case where domestic prices might otherwise be raised repeatedly in theface of an unexpected decline in world market cotton prices. The review wouldinclude (a) analysis of input costs and world market trends for cotton, (b)analysis of producer responses to earlier price signals (yield, area, andapplication rate effects) and (c) investigation of changes in CMDT's cottonproduction structure, SOMIEX transport costs, and the costs of noncattonactivities recovered out of cotton revenues. Assurances were obtained at

1/ The lower subsidy percentages shown at Table 2.1 are net of taxes onthese inputs.

- 21 -

negotiations that Government would defer producer price increases for cotton,and/or reduce the scope of CMDT or SOMIEX activities, if and when the jointreview concluded such adjustments were necessary.

2.07 Expected Effects of the Price Policy. It is difficult to isolate theimpact of cotton price increases alone on Mali Sud cotton production, sinceover the same project period, CMDT's extension and input supply efforts willsimultaneously itensify and reach a number of villages not previouslyserved. 1/ The program assumes a total incremental cotton area of 16,000hectares (15%) over 5 years, from both price effects and other interventions,as against a real increase in the seed cotton price of over 50%. This is inthe low end of the range of acreage elasticities of supply with respect toprice that have been estimated for other developing countries, namely 0.25 to0.44. 2/ This relatively modest area increase, coupled with a 10% increase inyields due both to the improvement in the cash cost coefficient and projectextension and input supply efforts, would be sufficient to restore the sectorby year 4 to nearly full use of installed capacity, which in turn signifi-cantly lowers real processing costs. Financial results for Government andfarmers are discussed below (para. 2.19).

2. Institutional Reforms in Budgeting, Taxation and Marketing

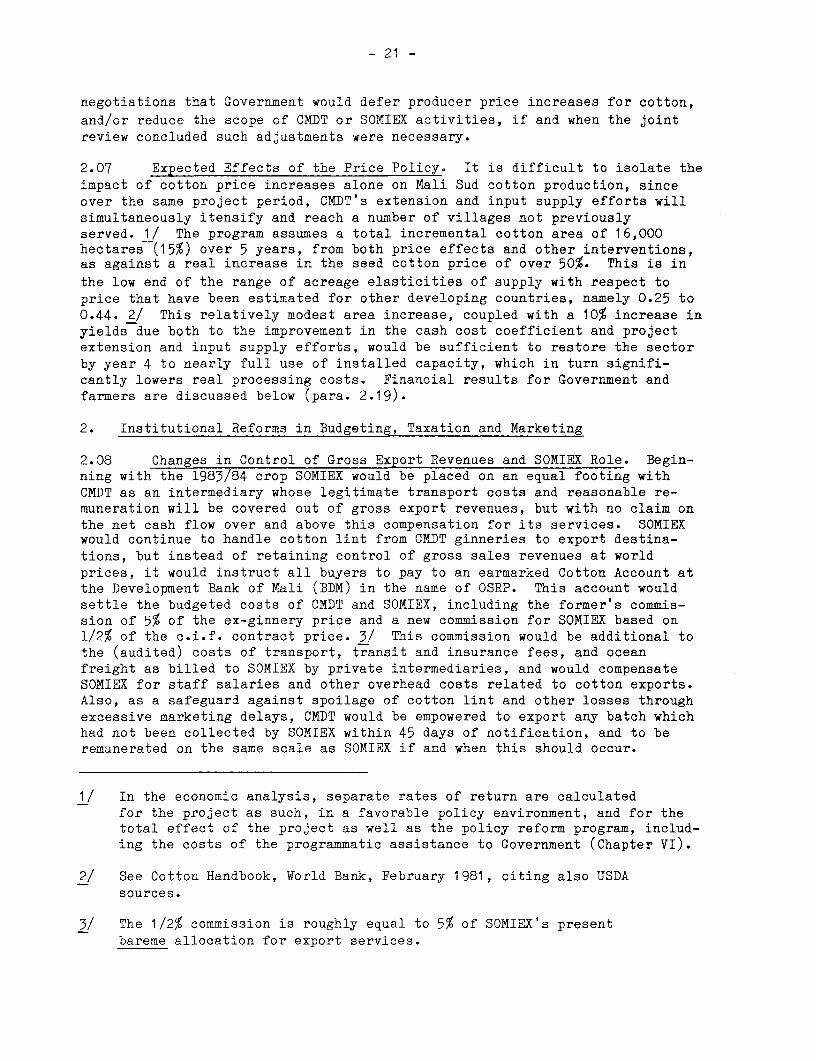

2.08 Changes in Control of Gross Export Revenues and SOMIEX Role. Begin-ning with the 1983/84 crop SOMIEX would be placed on an equal footing withCMDT as an intermediary whose legitimate transport costs and reasonable re-muneration will be covered out of gross export revenues, but with no claim onthe net cash flow over and above this compensation for its services. SOMIEXwould continue to handle cotton lint from CMDT ginneries to export destina-tions, but instead of retaining control of gross sales revenues at worldprices, it would instruct all buyers to pay to an earmarked Cotton Account atthe Development Bank of Mali (BDM) in the name of OSRP. This account wouldsettle the budgeted costs of CMDT and SOMIEX, including the former's commis-sion of 5% of the ex-ginnery price and a new commission for SOMIEX based on1/2% of the c.i.f. contract price. 3/ This commission would be additional tothe (audited) costs of transport, transit and insurance fees, and oceanfreight as billed to SOMIEX by private intermediaries, and would compensateSOMIEX for staff salaries and other overhead costs related to cotton exports.Also, as a safeguard against spoilage of cotton lint and other losses throughexcessive marketing delays, CMDT would be empowered to export any batch whichhad not been collected by SOMIEX within 45 days of notification, and to beremunerated on the same scale as SOMIEX if and when this should occur.

1/ In the economic analysis, separate rates of return are calculatedfor the project as such, in a favorable policy environment, and for thetotal effect of the project as well as the policy reform program, includ-ing the costs of the programmatic assistance to Government (Chapter VI).

2/ See Cotton Handbook, World Bank, February 1981, citing also USDAsources.

3/ The 1/2% commission is roughly equal to 5% of SOMIEX's presentbareme allocation for export services.

- 22 -

2.09 Operation of the Cotton Account. Opening of the Cotton Account atBDM and the Guarantee Fund Account at the Central Bank of Mali would be acondition of effectiveness. CMDT's budget will be separated into fixed andvariable cost components calculated per ton of estimated lint exports. Sepa-rately identified budget sections will be presented by CMDT for non-cottondevelopment expenditures (such as the maize program, functional literacy androads). As export revenues are received from correspondent banks, the CottonAccount will pay SOMIEX and CMDT autematically in proportion to their budgetshares for variable costs, plus commission, and up to the ceiling of CMDT'sbudgeted fixed costs. On a given contract, shortfalls between total budgetedcosts and the realised c.i.f. price will be made good by drawing on the Gua-rantee Fund (below 2.11). Any surpluses, save for debt service paymentsdiscussed below, will be retained by the Account until the year-end, whenbudgeted and actual costs would be compared and the Cotton Account (comple-mented if necessary by drawing on the Guarantee Fund) would compensate netshortfalls, Savings (per ton) on budgeted outlays resulting from internalefficiency in CMDT and SOMIEX would be retained by the operator as taxableearnings. This would introduce some incentives for cost control, hithertoentirely lacking in the bareme process. One of the primary objectives of theinstitutional reform program is indeed to replace the present bareme mechanismxith a more efficient budgeting and profit distribution process.

2 10 Changes in Intermediate Taxes and Other Budgetary Charges. A majorobjective of these reforms is to secure the sector s net cash flow untilactual profits are determined. Therefore, clear limits must be set on variousGovernment agencies ability to tax cotton turnover upstream, at the produc-tion or export stages. Governnent has agreed to levy oely a 3% customs tax onthe border value of lint exports, plus a specific charge collected by OSRP toretire project-related external debt obligations at actual rates charged toGovernment by donors. Project-related lbans, including the proceeds of theIDA Credit, would be passed onto CMDT in grant form since OSRP would captureall net trading surpluses and ultimately redistribute them to Governmentthrough the Guarantee Fund mechanism. In any case, most of the project acti-vities financed through CMDT are not directly revenue-generating (e.g. watersupply, farmer training programs). No other direct tax on cotton output (suchas the export tax levied before 1981) may be introduced. Taxes on inputs(e.g. fuel, fertilizers) levied on CMDT and SOMIEX are not affected, but willnow be recovered out of the Cotton Account. CMDT and SOMIEX will remainliable for corporation tax (IBIC) on their net cotton earnings, but CDMT willbe exempt from the present minimum turnover tax of 1% levied even on before-tax losses. The CMDT budget would include specific amortisation provisionsfor vehicles, plant and equipment. These will be adjusted in the light of aproject-financed study on CMDT's cost structure, accounting systems, assetvaluation and depreciation, to be completed by March 31, 1984, and discussedwith IDA by June 30, 1984. Government has also agreed to specific guidelineson CIMDT capital expenditures, depreciation and then budgeting, including thetreatment of Government-owned ginning mills as part of CMDT's assets pendingformal transfer of ownership. Any CMDT activities outside the scope of theproject will require the prior mutual agreement of IDA and Government. Inparticular, CMDT may not engage in activities (such as crop marketing) which

- 23 -

require an aggregate annual subsidy exceeding FM 100 million ($150,000) unlessthis subsidy is financed by other sources on mutually acceptable terms.Governnent's full counterpart obligations to Mali Sud, including the recurrentand incremental costs of non-cotton development activities (para.. 2.17), andtaxes on project investments paid by CMDT, will be included in CMDT's budgetand recovered from the Cotton Account.

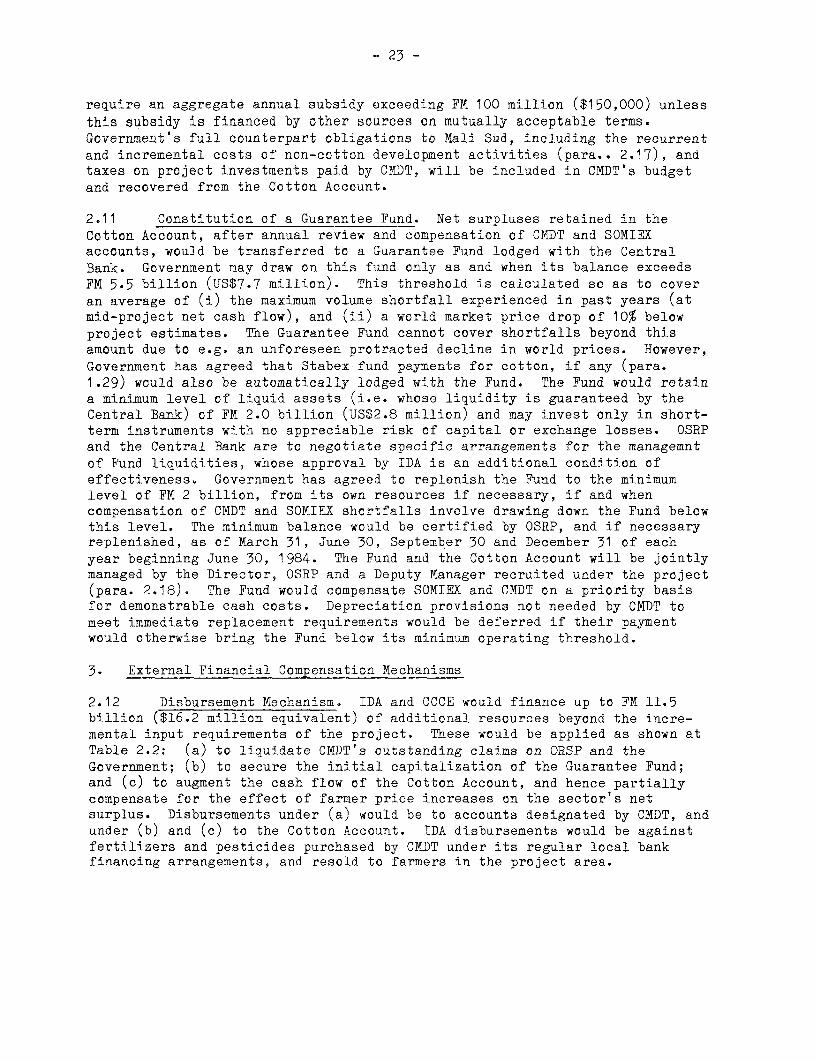

2.11 Constitution of a Guarantee Fund. Net surpluses retained in theCotton Account, after annual review and compensation of CIIDT and SOMIEXaccounts, would be transferred to a Guarantee Fund lodged with the CentralBank. Government may draw on this fund only as and when its balance exceedsFM 5.5 billion (US$7.7 million). This threshold is calculated so as to coveran average of (i) the maximum volume shortfall experienced in past years (atmid-project net cash flow), and (ii) a world market price drop of 10% belowproject estimates. The Guarantee Fund cannot cover shortfalls beyond thisamount due to e.g. an unforeseen protracted decline in world prices. However,Government has agreed that Stabex fund payments for cotton, if any (para.1.29) would also be automatically lodged with the Fund. The Fund would retaina minimum level of liquid assets (i.e. whose liquidity is guaranteed by theCentral Bank) of FM 2.0 billion (US$2.8 million) and may invest only in short-term instruments with no appreciable risk of capital or exchange losses. OSRPand the Central Bank are to negotiate specific arrangements for the managemntof Fund liquidities, whose approval by IDA is an additional condition ofeffectiveness. Government has agreed to replenish the Fund to the minimumlevel of FM 2 billion, from its own resources if necessary, if and whencompensation of CMDT and SOMIEX shortfalls involve drawing down the Fund belowthis level. The minimum balance would be certified by OSRP, and if necessaryreplenished, as of March 31, June 30, September 30 and December 31 of eachyear beginning June 30, 1984. The Fund and the Cotton Account will be jointlymanaged by the Director, OSRP and a Deputy Manager recruited under the project(para. 2.18). The Fund would compensate SOMIEX and CMDT on a priority basisfor demonstrable cash costs. Depreciation provisions not needed by CMDT tomeet immediate replacement requirements would be deferred if their paymentwould otherwise bring the Fund below its minimum operating threshold.

3. External Financial Compensation Mechanisms

2.12 Disbursement Mechanism. IDA and CCCE would finance up to FM 11.5billion ($16.2 million equivalent) of additional resources beyond the incre-mental input requirements of the project. These would be applied as shown atTable 2.2: (a) to liquidate CMDT's outstanding claims on ORSP and theGovernment; (b) to secure the initial capitalization of the Guarantee Fund;and (c) to augment the cash flow of the Cotton Account, and hence partiallycompensate for the effect of farmer price increases on the sector's netsurplus. Disbursements under (a) would be to accounts designated by CMDT, andunder (b) and (c) to the Cotton Account. IDA disbursements would be againstfertilizers and pesticides purchased by CMDT under its regular local bankfinancing arrangements, and resold to farmers in the project area.

- 24 -

Table 2.2: SUMMARY OF PROGRAMMATIC FINANCINGMillions of Mali Francs

Sources: IDA CCCE Total

Uses:

CMDT Debt Consolidation 2,000 800 2,800Guarantee Fund 1,500 500 2,000ORSP Cotton Account 5,000 1,700 6,700

8,500 3,000 11,500

2.13 CMDT Debt Consolidation. Government has historically fallen short onits obligations to CMDT by a net amount of about FM 2.8 billion ($4.0 million)as follows:

Table 2.3: CMDT DEBT CONSOLIDATION (estimates to 9/30/83)

Owed to CMDT Owed by CMDT Net due to CMDT--------------------- billion Mali Francs -----------------------

By OSRP: for undercompen-sation of baremes

2.0 2.0

By Government: for prefinan- To Government, for minimumcing of two cotton ginneries turnover tax

0.7 (0.7) 0.0

By Government: for oilmillcost overruns: 0.8 1/ 0.8

By Government: for cumulative To Government, owner ofunder provision for plant plants managed by CMDT:depreciation: 2.1 2/ (2.1) 0.0

By Government: for under pro- To Debt Service Fund,vision of Mali Sud I debt under subsidiary loanservice sinking fund: agreement:

1.0 2/ (1.0) 0.0

Total: 6.6 (3.8) 2.8

1/ Governnient is 80% shareholder in HUICOMA oil mill, and CMDT 20%. Totalcost overrun is FM 1.0 billion, advanced out of CMDT working capital.

2/ Under Mali Sud I subsidiary loan agreements, the bareme should have pro-vided these amounts for CMDT to hold as trustee until maturity.

- 25 -

This net claim of FM 2.8 billion would represent an additional tax burden of

at least 25 f/kg seed cotton if recovered on a future year's pricing schedule,penalising producer incentives. Moreover, it already strains CNDT's workingcapital and inflates interest costs on excessive overdrafts from the bankingsystem (para. 1.27). It is therefore proposed that this claim be settled atthe beginning of the project by a Government grant to CMDT, disbursed by IDAagainst fertilizers and pesticides resold by CMDT at official prices. Since

audited CMDT accounts certifying these claims are not yet available, an addi-tional condition of IDA disbursement for this part of the project would bethat audited CMDT accounts, including a special certification on the natureand amount of these debts, shall have been submitted to IDA for approval.Government and CMDT acknowledge in the proposed subsidiary agreement thatthese payments will extinguish all the liabilities involved.

2.14 Constitution of Guarantee Fund. To ensure that the Cotton Account isbacked from the beginning of the project by sufficient liquidities to meetessential processing costs and temporary shortfalls in cotton export revenues,the minimum Guarantee Fund balance of FM 2 billion (US$2.8 million) would beconstituted through a similar process of external grants-in-kind disbursed tothe Guarantee Fund Account. To enable the process ta begin immediately, CMDTexpenditures on fertilizers and pesticides up to $2.3 million (less than 10%of the IDA credit) made up to 6 months before IDA credit signature would beeligible for retroactive IDA reimbursement upon project effectiveness. Pro-curement under IDA financing will be in accordance with Bank guidelines forinternational competitive bidding. Cofinancier CCCE would make direct cashpayments for its CMDT debt consolidation and Guarantee Fund contributions.

2.15 Compensation of Cotton Account. The balance of the programmaticfinancing (FM 6.7 billion or US$9.4 million) will be disbursed in annualtranches under the same procedures. The funds so generated will complementregular export revenues received in the Cotton Account to compensate for (a)the buildup to the threshold level (FM 5.5 billion) of the Guarantee Fund,which would otherwise divert cotton surpluses from current Government taxrevenues (b) higher producer prices required under the pricing program, and(c) full recovery of developmental expenditures (recurrent and incremental)out of the cotton price structure, bath of which also lower Governnent's netcash flow from the sector for any given level of turnover. An illustration ofthe Cotton Account's operation is presented in Table 2.4, based on projectphysical assumptions, the producer price response discussed above, andprojections of CMDT fixed and variable costs over the project horizon. Netexport revenues would decline through Year 3 in both absolute and per-unitterms. They would recover by the end of the project to comparable absolutelevels, but a lower share of gross receipts. Out of these gross exportrevenues, OSRP would caver not only CMDT and SOMIEX processing costs(including commissions, amortisation and depreciation) but 100% of Mali Sud Irecurrent costs and Government's contribution to the proposed project'scosts. In the baseline projection, small net surpluses over and above thecumulative threshold of FM 5.5 billion in the Guarantee Fund would arise inYear 1, and substantial surpluses from Year 5: these would be available fordistribution to Government by OSRP. Year 2 is an illustration of a temporarywindfall arising from the attainment of the threshold level in Year 1, whichdemonstrates the need tc retain flexibility in annual tranche disbursements,

_ 26 -

Table 2.4

MALI SUD 2 PROJECT

ILLUSTRATION OF COTTON ACCOUNT - MODELE COMPTE COTON

Millions of Mali Francs/Million Francs Maliens (FM)

Item Rubrique