withstanding the resource cursecarnegieendowment.org/files/budi_hikmat_s2.pdf · budi hikmat chief...

TRANSCRIPT

Discussion Material for

Russian Economic Challenge

Moscow, 22nd March 2017

Budi Hikmat Chief Economist & Diretor for Investor Relation

PT Bahana TCW Investment Management

Withstanding The Resource Curse The Case of Indonesia: A Fund Manager’s view

Fund Manager’s Macro Map

2

Trump POTUS45 Fed hawkish Stimulus ECB, BoJ & BoE China economic stabilization

Aging society, global warming, de-leveraging, wealth inequality, multi-polar cold war

Rate still lower, disruptive innovation, currency wars, end of commodity super-cycle

External Global & Regional Dynamics

Domestic Economic

Challenges & Policy

Responses

Populist Politics & Resource Curse: The Risk of Middle-Income Trap 2030

Fiscal reforms: Subsidy system & Supply-side Revolution Prudence monetary policies

Tax amnesty: Revenue Reforms

Macro-prudential

Financial deepening

Impact, Outlook & Strategic Guideline

Current account deficit

Oil

Trade balance

Tourism, Re-industrialization

Brexit

Abated IDR exchange rate pressure encourages capital inflows

Liquidity-riven rally (LSIEV)

Equity

Bond

From stability to growth

Legal & Admin

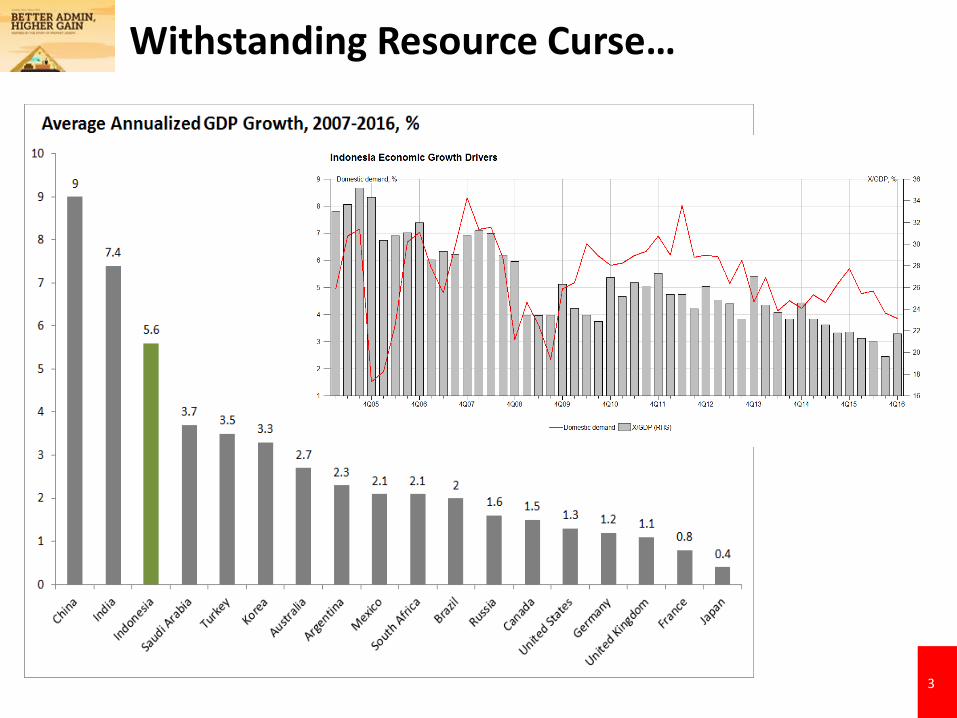

Withstanding Resource Curse…

3

Indonesia Experience With Commodity Boom Oil Bonanza 1974-1979 Asia Financial Crisis, 1998 Comdty Boom 2000-2012

Strong centralized leadership

Political Change, Reformasi

Poor macroeconomic management • Fixed exchange rate system • Weak monitoring and supervision

on banking system • Under-developed financial market • Weak tax collection & poor debt

management system --

Initial social cost to recapitalize banking system Rp400tn, weaken fiscal stimulus to achieve inclusive growth

Direct election, fragmanted coalition, desentralization, populist

Productive & inclusive spending: Basic education, family planning, rural infrastructure, iriigation, fertilizer plant, electricity generation, transmigration, satellite communication

Consumptive & exclusive spending: Fuel subsidy, car, petro-chemical, gadget, travelling abroad. Widening inequality among regions

• Faster growth with less inequality • Current account surplus

• Slow growth with worsening inequality

• Current account deficit

4

Gini ratio

GDP growth

Overwhelming Challenge Ahead

• In the last 10 years, Indonesian economy becoming less: productive, competitive, efficient and equally distributed

• The risk of growing old before growing rich in 2030 • Solution:

– Faster & sustainable growth with better equality – Transforming from saving to investing society

5

Rich country: GDP/capita > $12K

Indonesia 2045

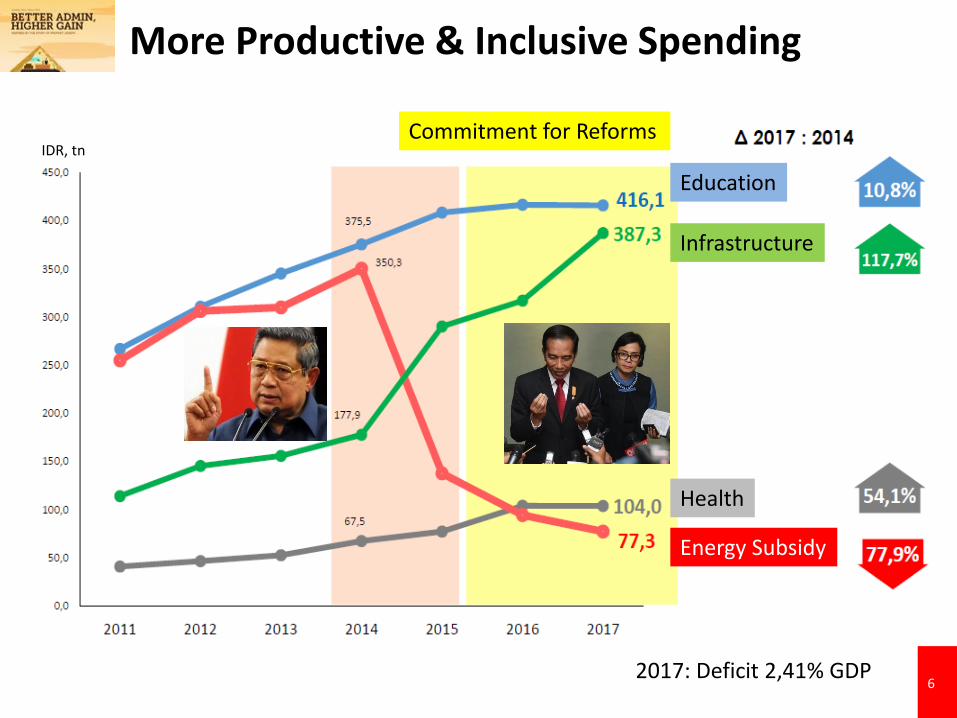

More Productive & Inclusive Spending

6

Education

Infrastructure

Health

Energy Subsidy

Commitment for Reforms IDR, tn

2017: Deficit 2,41% GDP

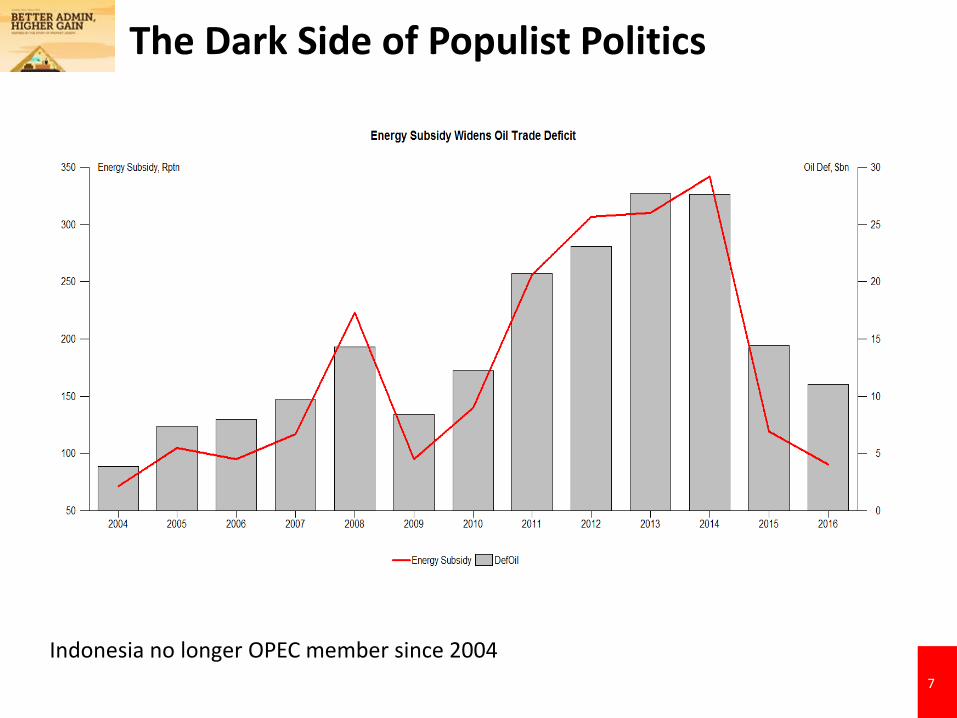

The Dark Side of Populist Politics

7

Indonesia no longer OPEC member since 2004

Tax Amnesty Program

8

Tax ratio, % GDP

Target tax collection 2017 Rp1.496tn (tax ratio 11%)

Source: IMF 2015

Entering Era of Strong Dollar

9

Index $ Global

Index Commodity

Krismon Asia

Krisis utang AS

Krisis utang Eropa

Krisis utang Negara

Berkembang

Strong DXY, Despite Excessively Created…

10

V = GDP nominal / M2

DXY

Asian Crisis

Mothers of All Disruptive Innovation

11

BoJ too aggressive

ECB Fed

BoJ

Invasion of fiat money makes rate lower for longer

Fed’s excess reserve $2tn

Central Bank Commercial Banks Investment Banks/Shadow Banking

Central Bank Commercial Banks Invest Banks

Pre

Post

Strong DXY

Lower Oil Price on Bigger Supply

12

IDR: Friendly Internal Drivers

13

Bahana Fear Index

OilDef

USD

IDR

Inspiration From the Past…

14

Opportunity to Promote Lifecycle Investment

Genesis 41 and QS 12:47 Economist (Typical IMF-World Bank policy recommendation)

Fund Manager

You will cultivate consequtively for seven years Structural policy Productivity (Y) Growth Equity

Leave in the ears all you have harvested Buffer stock & Preservation Protection Gov bond

Expect the little out of which you may eat Demand management (A) Distribution Structured product

15

Invest Harvest

Aggresive Moderate Conservative

Pension Pass away Start

Labor income Non Labor income

Supply (Y+M) = Demand (C+I+G+X) Y = C + I + G + (X-M) (X-M) = (Y-A) Current account deficit = excess domestic demand 1. Demand management (A) 2. Structural policy (Y) 3. Exchange rate policy (Ex Japan) 4. External financing

Revising Overlapping Generation Model (Paul Samuelson, 1958)

Lesson To Learn

• Strong leadership to achieve national’s vision inclusively

• Fiscal policy as the anchor of policy credibility to avoid crisis – Reforms: Expenditure, revenue, future liability

– Tax reforms: Simple, equitable, regionally competitive

• Financial reforms to withstanding external transmission, including invasion of fiat money – Macro prudential, financial deepening

– Foreign debt: Monitoring and its productivity

• The role of capital market to secure good policy

• Support globalization, widening market space

• Promoting investment society to anticipate middle-income trap

16